READ THE WASHINGTON INFORMER YOUR WAY:

n In Print – feel the ink between your fingers of our Award Winning Print Edition

n On the Web – www.washingtoninformer.com updated throughout the day, every day

n On your tablet

n On your smartphone

n Facebook

n Twitter

n Weekly Email Blast – sign up at www.washingtoninformer.com

202-561-4100

For advertising contact Ron Burke at rburke@washingtoninformer.com ...Informing you everyday in every way

In Memoriam

Dr. Calvin W. Rolark, Sr. Wilhelmina J. Rolark

PUBLISHER

Denise Rolark Barnes

THE WASHINGTON INFORMER NEWSPAPER (ISSN#0741-9414) is published weekly on each Thursday. Periodicals postage paid at Washington, D.C. and additional mailing offices. News and advertising deadline is Monday prior to publication. Announcements must be received two weeks prior to event. Copyright 2016 by The Washington Informer. All rights reserved. POSTMASTER: Send change of addresses to The Washington Informer, 3117 Martin Luther King, Jr. Ave., S.E. Washington, D.C. 20032. No part of this publication may be reproduced without written permission from the publisher. The Informer Newspaper cannot guarantee the return of photographs. Subscription rates are $55 per year, two years $70. Papers will be received not more than a week after publication. Make checks payable to:

THE WASHINGTON INFORMER 3117 Martin Luther King, Jr. Ave., S.E Washington, D.C. 20032

Phone: 202 561-4100

Fax: 202 574-3785

news@washingtoninformer.com www.washingtoninformer.com

STAFF

Micha Green, Managing Editor

Ron Burke, Advertising/Marketing Director

Shevry Lassiter, WIN-TV Producer

Ra-Jah Kelly, Digital Asset Manager

Lafayette Barnes, IV, Editor, WI Bridge DC

Desmond Barnes, WIN Daily Editor

Anthony Tilghman, Social Media Strategist ZebraDesigns.net, Graphic Design

Mable Neville, Bookkeeper

Angie Johnson, Office/Circulation Manager

REPORTERS

Stacy Brown, National Reporter

Sam P.K. Collins, Political/Education Reporter

Zerline Hughes, Housing Reporter

Brenda Siler, Lifestyle Reporter

Lindiwe Vilakazi, Health Reporter

Ed Hill, Sports Reporter

Jada Ingleton, WI Comcast Fellow, WIN Daily

Newsletter Editor

Eden Harris, Reporter

PHOTOGRAPHERS

Shevry Lassiter, Photo Editor

Ja Mon Jackson, Asst. Photo Editor

Roy Lewis, Jr.

Robert R. Roberts

Anthony Tilghman

Abdullah Konte

Cleveland Nelson

By Kevin Reen CEO of Home Lending at Wells Fargo

The hardest part of any journey is the first step. It’s true in life and it’s particularly true when it comes to purchasing a home. The lack of funds for a down payment remains one of the largest barriers to homeownership most people face. That’s especially true for traditionally underserved minority homebuyers.

And yet, consider how important that first step is. Homeownership is one of the most effective ways families can build intergenerational wealth. Typically, homeowners build equity over time and are able to take advantage of tax deductions. In addition to these financial benefits, homeownership brings substantial societal benefits for families and the communities they live in. However, we know that traditionally underserved communities continue to face significant challenges when it comes to purchasing a home.

Wells Fargo is focused on strengthening underserved communities and advancing racial equity in homeownership. While we continue to pursue multiple efforts to address a broader variety of factors driving the homeownership gap, we’ve found that providing down payment assistance can make a significant difference for many potential homebuyers. As such, in 2023 Wells Fargo launched our Homebuyer Access grant, a program that provides $10,000 toward the down payment for eligible homebuyers who currently live in or are purchasing homes in certain underserved communities.

The Homebuyer Access Grant program is currently available in select communities in eight Metropolitan Statistical Areas (MSAs) and additional areas in New Jersey. Eligible homebuyers can also combine the grant with other programs for which they may qualify, allowing them to maximize the support available to them. This flexibility ensures that we are providing comprehensive assistance to help first-time homebuyers succeed.

Potential homebuyers looking to purchase a home in any of the eligible areas and those who currently live in those areas can find out more about the program, including how to contact a local Wells Fargo Home Lending office in their area, at https://wellsfargo.com/homegrant I have seen firsthand the impact that this program can have. It is heartening to hear stories from individuals who, with the help of the Homebuyer Access Grant, have been able to achieve their dream of owning a home. Sometimes all you need is a little help with that first step.

Kevin Reen is the head of Wells Fargo Home Lending. g

Submitted by Wells Fargo

A life of hard work and sacrifice offers the opportunity to leave a legacy that that lifts up not only your family, but your community. There are important considerations as you approach financial planning to transfer wealth to future generations.

Creating an estate plan is a foundational step. While it can seem intimidating, a team of trusted professionals, including a financial advisor, estate planning attorney, and accountant, can ask the right questions and help you avoid potential pitfalls.

“Developing an estate plan is about taking control. You are directing how the assets you have accumulated over your lifetime are passed on to the people and organizations that you care about,” says John Ripoll, Senior Vice President for Wells Fargo Advisors.

Your situation’s complexity will determine which documents your plan requires; however, these five are often included in an estate plan:

A will provides instructions for distributing your assets to your beneficiaries when you die. In it, you name a personal representative (executor) to pay final expenses and taxes and distribute your remaining assets.

A durable power of attorney lets you give a trusted individual management power over your assets if you can’t manage them yourself. This document is effective only while you’re alive.

A health care power of attorney lets you choose someone to make medical decisions for you if you are unable to communicate your wishes, or don’t have legal capacity to make treatment decisions for yourself.

A living will expresses your intentions regarding the use of life-sustaining measures if you are terminally ill. It doesn’t give anyone the authority to speak for you.

By transferring assets to a revocable living trust, you can provide for continued management of your assets during your lifetime and after

your death — possibly for generations to come.

Establishing a plan is only the beginning. Significant life events are likely to call for changes to your plan.

Ripoll explains, “It’s important to regularly review your plan to ensure it continues to meet your needs. You want to consider whether your estate planning documents, asset titling, and beneficiary designations have been coordinated to allow your assets to be distributed according to your wishes. A regular review of who you have named as agent, executor, guardian for minor children, and trustee is important to ensure those named are still willing and able to serve when needed.”

Investment and Insurance Products are:

• Not Insured by the FDIC or Any Federal Government Agency

• Not a Deposit or Other Obligation of, or guaranteed by, the Bank or Any Bank Affiliate

• Subject to Investment Risks, Including Possible Loss of the Principal Amount Invested

Wells Fargo Advisors is a trade name used by Wells Fargo Clearing Services, LLC, Member SIPC, a registered broker-dealer and non-bank affiliate of Wells Fargo & Company.

©2019-2023 Wells Fargo Clearing Services, LLC. All rights reserved. g

When Black homeownership rates increase, more Black households gain access to a proven way to build personal and intergenerational wealth.

Markets change but that does not mean buying a home is out of reach. At Wells Fargo, we can help you navigate the home buying journey during all types of economic cycles.

Our mor tgage affordability calculator1 at wellsfargo com helps you determine which mor tgage options best align with your financial goals.

When you are ready to talk, our Home Mor tgage Consultants are here to help you create a plan to optimize the benefits of homeownership now and over time

The Black homeownership rate rose throughout 2022 even in the face of rising mor tgage rates, hitting 45 2% in the third quar ter - up from 42 7% in 2019 This is the largest point increase of any racial or ethnic group 2

Submitted by Wells

Fargo

Women-owned businesses continue to fuel the economy, representing 39.1% of all businesses –over 14 million – employing 12.2 million workers, and generating $2.7 trillion in revenue. According to the 2024 Wells Fargo Impact of Women-Owned Business Report, in partnership with Ventureneer, CoreWoman, and Women Impacting Public Policy (WIPP), the number of women-owned businesses between 2019 and 2023 increased at nearly double the rate of those owned by men; and from 2022 to 2023, the rate of growth increased to 4.5 times. Whether it was during COVID-19 lockdowns in 2020 or supply chain disruptions throughout the pandemic, women business owners are driving economic growth:

• During the onset of the pandemic in 2020, despite business closures, women launched more businesses than they closed, while the number of men-owned businesses declined. Women-owned businesses also grew their workforces and increased their revenue while men’s numbers shrank.

• From 2019 to 2023, women-owned businesses’ growth rate outpaced the rate of men’s 94.3% for number of firms, 252.8% for employment, and 82.0% for revenue.

• During the pandemic, women-owned businesses added 1.4 million jobs and $579.6 billion in revenue to the economy.

• Nearly half a million wom-

en-owned businesses with revenues between $250,000 and $999,999 grew their aggregate revenues by about 30%, illustrating their ambition, grit, and readiness to cross the $1 million revenue threshold.

“The impact that women-owned businesses make on the economy is undeniable. Even more impressive is that growth in women entrepreneurship – whether it was their workforce or revenue – grew during an extremely difficult time,” said Wells Fargo Women’s Segment Lead for Small Business, Val Jones. “From the trillions in revenue they contribute to the economy to the millions in jobs, women-owned businesses are coming out of the pandemic stronger than they went into the pandemic and many are thriving. It’s a testament to their resiliency and the breadth and depth of support they’ve received from government entities, banks, corporations, and philanthropic organizations that must be sustained.”

Also, during the COVID-19 pandemic and the transition to the post-pandemic period, Black/African American and Hispanic/Latino women-owned businesses increased at a much higher rate than all women-owned businesses. Between 2019 and 2023, Black/African American women-owned businesses saw average revenues increase 32.7% and Hispanic/Latino women-owned businesses 17.1% compared to all women-owned businesses' 12.1% rise.

Further, women-owned businesses with 50 or more employees account for nearly half of women-owned businesses’ employment and revenues.

Currently, women-owned businesses with 50 or more employees average $31.8 million in revenue generating $1.3 trillion in aggregate revenue. If they achieved the average revenue of men-owned businesses with 50 or more employees, they would add $1.2 trillion in revenue to the U.S. economy.

“The surge in growth rates of women-owned firms with more than 50 employees proves their strength and adaptability during and post the pandemic era,” said Wells Fargo Women's Segment Lead for Commercial Banking, Judith Goldkrand. “To sustain the growth and close the gaps, it’s important that we continue to create opportunities that help these businesses flourish, including removing barriers to capital, providing technical assistance, and offering support with business certification.”

“The surge in growth rates of women-owned firms with more than 50 employees proves their strength and adaptability during and post the pandemic era.”

Judith Goldkrand Wells Fargo Women's Segment Lead for Commercial Banking

More than a decade ago, women-owned businesses were concentrated in just three industries. Now, half of all women-owned businesses (50%) are concentrated in these four industries:

• Other services (hair and nail salons, pet care, laundries, and dry cleaners): In 2023, women owned 2,267,000 other services companies, accounting for 16.2% of all women-owned businesses.

• Professional, scientific, and technical services (legal, bookkeeping, and consulting businesses): In 2023, women owned 2,017,000 businesses in this category, accounting for 14.4% of all women-owned businesses.

• Administrative, support and waste management, and remediation services (office administration, staffing agencies, and security and surveillance services): In 2023, women owned 1,671,000 businesses of this type, accounting for 11.9% of all women-owned businesses.

• Healthcare and social assistance (child day care and homecare providers, mental health practitioners, and physicians): In 2023, women owned 1,588,000 healthcare and social assistance companies, accounting for 11.3% of all women-owned businesses.

While these industries have the most women-owned businesses, between 2019 and 2023, the sectors that saw the most significant growth (50%) were in finance, insurance firms, real estate, transportation, and the warehouse industry.

While women business owners represent 39.1% of U.S. firms, they only account for 9.2% of the workforce and 5.8% of revenue. Closing the gap in average revenues for those ethnically or racially diverse has the potential to generate $667 billion in additional revenue, while closing the gap in average revenues between women- and men-owned businesses has the potential of generating $7.9 trillion in additional revenue to the nation’s economy. g

AtWellsFargo,webelievethatstrongcommunitiesstart withstablehomes.That’swhywe’vepledgedoursupportto helpgrowhomeownershipindiversecommunitiesacross thecountry.

Throughourinvestmentsinaffordablehousinginitiatives andfinancialeducationprograms,we’reworkingtomake homeownershipaccessibletoeveryone.

Joinusinbuildingabrighterfutureforourcommunities, onehomeatatime.

Readytobeapartofsomethingbigger?Learnmoreabout WellsFargo’scommitmenttohomeownershipandhowyou cangetinvolvedinbuildingstrongercommunities.

Scantolearnmoreat wellsfargo.com/mortgage/buying-a-house

Buildyourhomeownershipfuturesooner withaDream.Plan.Home.SM mortgage

Yourfamily’sfuturemaycontinueintheneighborhoodyou andyourfamilyhavecalledhomeforgenerations.

Orexpandtoadifferentcityorstatetopursuenew opportunities.

Eitherwayifyouwanttocontinuethislegacy,WellsFargocan helpsimplifyyourhomebuyingjourney.

TheWellsFargoDream.Plan.Home.SM Mortgageisawayto purchaseyourhomewithaslittleas3%downonafixed-rate loan.Withalowdown-payment,mortgageinsurancewillbe required,whichincreasesthecostoftheloanandwill increaseyourmonthlypayment.Talkwithahomemortgage

consultantaboutloanamount,typeofloan,propertytype, income,first-timehomebuyer,andhomebuyereducation requirementstoensureeligibility.

Dream.Plan.Home.offersflexibleunderwritingand streamlinestheapprovalprocessifyouhavelittletono credithistory,establishedcreditwithstrongcreditscores,or less-than-perfectcredit1

WellsFargoisheretohelpyouplanandbuildyour homeownershipfuture.

Call1-866-383-5345tostartyourhomebuyingjourney withWellsFargo.

1.TheDream.Plan.Home.℠mortgageisdesignedforconsumerswithincomeatorbelow80percentoftheareamedianincome(AMI)wherethepropertyislocated.

Submitted by Wells Fargo

Game Plan – the comprehensive intuitive mobile-first learning management system built by student-athletes for student-athletes – announced an expanded sponsorship with Wells Fargo – its exclusive provider of financial education curriculum since 2015. Through this expanded sponsorship, Game Plan will be offering free financial education to all 1,200 collegiate athletic departments – including those at 107 HBCUs, courtesy of Wells Fargo.

This announcement came ahead of August 2024, when the NCAA board of directors began requiring all Division 1 colleges to provide student-athletes with life skills development, including financial education, and ensures that collegiate athletic departments can help student-athletes navigate the Name, Image and Likeness (NIL) era. As a part of this expansion, Wells Fargo is investing in updating its current financial education program available on the Game Plan app with engaging courses on budgeting & saving, credit management, planning for the future, and more, along with offering oneon-one advice and planning sessions with bankers to empower collegiate student-athletes to capitalize on their NIL earning potential.

“The financial expertise that Wells Fargo has brought to university athletic departments and student-athletes through our platform for more than eight years now has been invaluable,” said Mike Banville, CEO at Game Plan. “With the NCAA life skills mandate implemented in August and at a time when student-athletes stand to gain more than ever through NIL, this is the perfect time to offer this enhanced financial education program.”

Gigi Dixon, head of External Engagement for Diverse Segments, Representation, and Inclusion at Wells Fargo, added, “Empowering financial success is core to who we are at Wells Fargo as The Bank of Doing. Student-athletes are expected to juggle classes, games, practices,

meetings, and other commitments. The greatest advantage Game Plan provides is housing all of the content critical to their life skills development in one easy-to-access efficient digital platform. We’re looking forward to updating our financial education curriculum and meeting university athletic departments and student-athletes where they are to ensure that higher education institutions meet guidelines and individuals can navigate this increasingly complex landscape to its maximum benefit.”

Harry Stinson III, MS-SA, Interim Vice President of Institutional Advancement & Executive Director of the Lincoln University Foundation, Director of Athletic & Recreational Services at Lincoln University, offered, “Wells Fargo has provided our students with financial education workshops that have elevated their ability to manage their finances in a new way. The workshops are short, yet detailed, and provide insight into the complexity of managing finances and prepares our students for their future success. From learning about taxes, owning your own business, renting versus buying, and understanding credit, our students are in position to think critically and strategically regarding their future and this program within the Game Plan platform is a game changer for us.” To-date, more than 875 athletic organizations have placed their trust in Game Plan, and within the duration of the Wells Fargo sponsorship, student-athletes on the Game Plan platform have successfully finished over 48,000 Wells Fargo Financial Education courses. g

By Micha Green WI Managing Editor

Fighting racial economic inequities is important in achieving overall racial equity for African Americans.

The wealth gap between white and Black Americans is wide and contributes to not only economic inequities, but also to housing, environmental, and health disparities as well.

In the January 2024 Brookings report “Black wealth is increasing, but so is the racial wealth gap,” by Andre Perry, Hannah Stephens and Manann Donoghoe, the authors break down various research that reveals economic trends and disparities.

The report's authors, drawing data from the Federal Reserve’s between 2019 and 2022, share that total wealth increased for all racial

and ethnic groups, with Black wealth growing from $27,970 to $44,890. Nonetheless, African Americans overwhelmingly lagged behind other racial and ethnic groups, with Latino households making $62,000, white households earning $285,000 and Asian American households $536,000.

According to Brookings: “The growing disparity means that in 2022, for every $100 in wealth held by white households, Black households held only $15.”

The racial wealth gap is wide, but there’s hope. Spreading the good news of financial literacy.

The National Education Association’s (NEA) reports in NEA Today that while closing the racial wealth gap will take time, financial literacy is critical in combating the problem.

Nonetheless, the article notes, access to financial literacy is key and often the challenge.

“Having a basic understanding of our financial system, the effects of debt, and how to build wealth, would benefit all students, but especially students of color. However, only 27 states require schools to offer a course in personal finance, and only 18 require that all students take it to earn a diploma,” according to the June 2023 piece.

However, Maryland does require financial literacy standards to be implemented by district, Virginia requires a standalone one-credit course, and on March 20, the D.C. State Board of Education voted to adopt financial literacy standards.

In order to combat racial economic inequities it’s important to spread the importance of financial literacy beyond the classroom.

Parents must teach their children about financial literacy at an early age; college students must learn about financial opportunities, benefits, managing money, and saving and invest-

ing for the future; and adults of all ages should continue to be versed in ways of handling finances, increasing their earnings and building generational wealth.

This special edition shares tips for parents teaching children about money, emphasizes the importance of credit, discusses the benefits of side hustles, highlights programming for financial opportunities and generational wealth, and unveils the ins and outs about financial literacy in schools.

While reading this edition, consider ways you might be able to implement these tools and use these resources in your life, and then spread the good news!

As the saying goes, “knowledge is power.” Share this information with your friends, family and community.

The more people begin to talk about financial literacy, the more folks will learn, and, for the Black community in particular, having that knowledge will be powerful in combating economic injustice.

g

5

By D.R. Barnes WI Staff Writer

Gone are the days when simply saying, "Money doesn't grow on trees," was enough to teach children about finances. Economic trends prove it’s crucial for children to begin learning about money at an early age, with parents serving as their first teachers. Early financial literacy lessons are particularly important in the Black community, where multiple research reveals there are major economic barriers and disparities.

Research shows that African Americans often lag behind in financial awareness. According to the National Urban League, financial literacy includes understanding eight key areas of personal finance covered by the TIAA’s Personal Finance Index (PFIN): earning, consuming, saving, investing, borrowing, managing debt, insuring, comprehending risk and uncertainty, and knowing go-to information sources.

The Federal Deposit Insurance

Corporation (FDIC) also emphasizes that "teaching kids about money early on will help them become more financially independent as they grow older."

Financial education has been linked to lower debt levels, higher savings, and higher credit scores as children mature.

Financial literacy lessons can start at ages 4 to 6, or even earlier, to help build a strong foundation for future financial well-being.

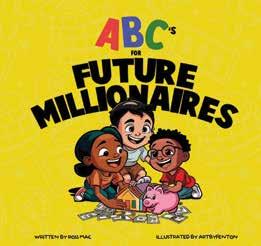

Ross Mac, renowned entrepreneur and financial expert, whose brand Maconomics has been featured on Yahoo Finance, BET, and Bloomberg, recently released an innovative children's book to introduce young readers to essential financial concepts and empower them to build a prosperous future.

The book, "ABC for Future Millionaires," combines vibrant illustrations with engaging narratives to teach children the basics of financial literacy, such as saving, investing and budgeting.

This hardcover board book uses each page to highlight child-appro priate money management language terms. The book introduces financial terms such as asset, bank, credit card, deposit, and economy from A to Z.

“Each letter of the alphabet is paired with a fundamental financial term, making learning both fun and educational,” Mac, a father of three, told The Washington Informer. “The book is designed for children aged 1 to 12, making complex financial concepts accessible and enjoyable.”

"By 2053," Mac added, "the median net worth of Black Amer icans is expected to fall to ZERO. My mission has always been to prevent this by educating our community about financial literacy. With 'ABC for Future Millionaires,' I’m starting that

Starting the conversation about money with children is key, but how does one begin teaching the lessons? Below are some simple and effective tips:

Use Everyday Moments as Lessons: Children learn best through experiences they can relate to. When you’re at the store, for example, show them the value of money by letting them help make decisions.

Ask questions like, "Which item costs less?" or "How much change will we get back?" Use these real-world opportunities to demonstrate budgeting and spending.

Introduce a Savings Jar or Piggy Bank: Instead of just giving your child a piggy bank, introduce the concept of savings goals. Set up three jars labeled "Spend," "Save," and "Share."

Encourage your child to divide any money they receive among the jars. The "Spend" jar is for small, immediate purchases, the "Save" jar is for larger goals, and the "Share" jar is for charitable giving. This approach can help them understand different aspects of money management.

Pay Them for Extra Chores: Rather than paying an allowance for nothing, tie it to extra chores. This helps children understand the concept of earning money through work. It also gives them the satisfaction of contributing to the household and the reward of spending or saving what they’ve earned.

Be sure to discuss how much they earned and whether they’d like to save part of it.

Set Savings Goals Together: Sit down with your child and help them set a savings goal, like buying a new toy. This teaches them patience, goal-setting, and the importance

education early, giving our children the tools they need to succeed financially from a young age." g

of delayed gratification.

early age. (Courtesy

Create a chart so they can track their progress. Seeing the savings grow can be highly motivating for young children.

Encourage Smart Spending Decisions: It’s essential to help children learn to make wise spending choices.

If your child wants a new toy or gadget, encourage them to wait a few days before purchasing. This waiting period helps them distinguish between impulse buys and things they genuinely value. It's a good time to discuss whether the item is worth the cost and whether saving might be a better option.

Use Books and Stories to Teach Financial Concepts: Books like "ABC for Future Millionaires" can be great tools for introducing financial concepts to children in a fun and engaging way. Young readers can learn terms like asset, bank, credit card, and more through relatable illustrations and simple definitions. Reading such books together can spark discussions and make children comfortable with financial terms at an early age.

Lead by Example: Children often model what they see their parents do. Let your child see you budgeting, paying bills, saving, and making financial decisions. Explain what you are doing and why.

By seeing you practice good financial habits, they will understand the importance of being financially responsible.

With consistent lessons and age-appropriate activities, you can give your child a headstart on becoming financially savvy. Introducing concepts such as saving, investing, and budgeting early on can lay the foundation for a lifetime of financial stability.

"ABC for Future Millionaires" is available for pre-order now and will be officially released on [Release Date]. For more information on the book and upcoming events, please visit maconomics.com.

AI was used to generate tips to teach children about money and saving.

By James Wright WI Staff Writer

Ward 8 resident Jacque Patterson

has a full-time position as the chief community engagement and impact officer for KIPP DC Schools, a charter school system, while also serving as an at-large member of the D.C. State Board of Education, a part-time post. With all of those responsibilities, he will be the first to admit a little extra money doesn’t hurt.

Thus, Patterson works a side hustle as a community consultant, helping nonprofits who want to set up operations in his ward and neighboring Ward 7.

“Nonprofits approach me on strategies to meet with leaders who reside east of the river and the best way to build relationships with them,” said Patterson, 59. “The word of mouth is ‘If you want to come east of the river, talk to Jacque.’”

A side hustle or gig is defined by Merriam-Webster as “work performed for income supplementary to one's primary job.”

Patterson told The Informer he charges a small fee for his work, usually through a contract, amd said he likes his side hustle “because it is making a positive impact in the community.”

Patterson is one of more than 57 million Americans (36% of workers) that have a side hustle or gig work arrangement either as their primary or secondary job. This includes a quarter of all full-time workers and half of all part-timers, according to “Gig Economy Statistics: Demographics and Trends in 2024” posted on the Team Stage blog.

The “Gig Economy Statistics” reports that the side hustle economy is expanding three times faster than the total U.S. workforce. Over 50% of the U.S. workforce is likely to participate in the gig economy by 2027.

The report said people aged 1824 are more likely to work within the gig economy. Further, 76% of gig workers say they are satisfied with their choice of having a side hustle.

Angela Heath is the president of District-based TKC Incorporated, a consulting business, and an expert on the gig economy. She is the author of the book, “Do the Hustle without the Hassle” and has hosted gig topic forums such as The Gig Worker Summit and The Boom Conference.

In “Making the Gig Economy Work for You” by Daniel DiGriz, published by The Clark Hulings Foundation for Visual Artists, Heath offers tips for people working a side hustle.

“I have a process where I do my planning at the beginning of the year,” said Heath. “I have a yearly calendar, I put all of my family commitments on it that I know about, like vacations. When I set up my quarterly goals, I decide exactly what I need to meet them.”

Heath said, “you start to get an idea about what’s realistic to make in a month, with the amount of time you want to dedicate to it.”

“Then you have to think through whatever family obligations you have, and financial commitments you have, how you fill that gap, and then go for those opportunities,” she said.

Heath said the gig economy is not new “we’ve had contractors and freelancers since way back” but noted “what is new is the technology that enables us to find opportunities quickly, cheaply.”

Ward 8 resident Ivan Jose Cloyd is the founding principal of Quad-

rant Partners, a company that specializes in real estate development and media.

Cloyd’s side hustle is working as a television consultant. He advises politicians, entrepreneurs and entertainers how to get on television to sell their products, campaigns or talents.

He also coaches people how to pitch television show ideas to cable networks.

Cloyd, 34, said his side hustle comes from his many years as an actor and working behind the scenes in the television industry. He said the side hustle maintains his lifestyle while he works on Quadrant.

“The side hustle is an immediate payout,” he said. “It is my way of making sure that the bills get paid as I work on real estate development.”

Cloyd’s advice to those considering a side hustle is to “look at your skill sets and don’t go outside what you already know.” However, he said side hustles must not replace the primary job.

“That would be a mistake,” he said. “Don’t be consumed by

your side hustle.”

Patterson emphasizes finding a side hustle that is so gratifying, it doesn’t feel like work.

“I would encourage anyone looking at a side hustle to do what they are passionate about,” Patterson said. “If they do what they are passionate about, it doesn’t seem like work. You must enjoy your hustle.”

g @JamesWrightJr10

By Jacqueline McSears Boles, SVP, Director of Retail Banking, Industrial Bank

The COVID-19 pandemic taught us many things, the importance of spending time with family, the impact of positive community support, the value in self-care, and the importance of having a solid budgeting and savings plan.

The pandemic also illuminated the need for greater financial literacy in many communities. Low financial literacy threatens the well-being of individuals and families, especially in underserved and low-income communities.

According to the Fed’s 2022 Economic Well-Being of U.S. Households survey 37% of Americans lack enough money to cover a $400 emergency expense.

Evident is the need to mandate the inclusion of financial literacy and empowerment into the educational curriculum beginning at the elementary school level. When young people lack the financial knowledge, they need to

make informed decisions, they are more likely to become trapped in cycles of poverty and debt. Children must learn the value of saving. Differentiating needs versus wants, as it relates to budgeting, is also essential to solid money management. Learning to maintain healthy finances should begin with their grade school allowances.

Every child should be required, or at least encouraged, to open a savings account and then taught the fundamentals of saving and budgeting during their primary years. As they approach middle school, children should study strategic investment practices and begin to position their funds for future growth. The high school focus could then shift to understanding the importance of managing credit, thus avoiding the devastation

that occurs when credit cards are sent to their college dorms, despite their lack of income.

A 2021 survey done by collegefinance.com found that college students averaged more than $3,280 in credit card debt another survey showed that only 20% of college students reported having excellent money management skills.

Many of our children will earn the degrees and other highly regarded credentials but be labeled unemployable because of failing credit scores. It is imperative that we focus on financial education and empowerment beginning with our youth. All school systems must incorporate a comprehensive financial literacy program into the standard curriculum. Subjects must include Banking, Saving and Investing, Budgeting, Credit, Fu-

ture Planning, Identity Theft, and Homeownership.

We must ensure that when faced with future economic stresses, our children will be unaffected by the conditions that are rampant today, assured that their core values will generate better financial decisions. By instilling a solid understanding of financial management, a large population of our youth will realize homeownership and investment rewards at much earlier ages than their parents. They will possess the knowledge and skills to manage their household finances, despite external economic conditions. Knowledge is power. Now is the time to empower our children with the information required to sustain a bright and secure tomorrow. g

https://industrial-bank com

beyondbanking@industrial-bank com

Industrial Bank offers a unique “Community Banking” relationship designed for the justice exposed.

Committed to serving as a recidivism interrupter. Industrial Bank started its work with the justice system in 2016 when 2 bank employees were volunteers with a local non-profit servicing currently and formerly incarcerated individuals. The organization provided an eight-week program that included financial literacy to young men between the ages of 14 and 17 who were housed in the Baltimore City jail charged as adults. In January 2018, the Bank partnered with the DC Department of Corrections providing financial empowerment sessions to over 80 incarcerated men and women. The first session began with groups in both medium and maximum-security levels and later included men ages 18 – 25 in a specialized group called Young Men Emerging (YME). Our financial empowerment program was not only well received by the residents of DC Jail and the YME group, but the surrounding community of non-profits dedicated to supporting returning citizens has also been extremely supportive of the Bank’s efforts.

I m p a c t

Former DC Jail residents that completed the program in 2018

Have since been released and established their first ever banking relationship with Industrial Bank.

Industrial Bank has participated in supporting the returning citizens as they encounter freedom, in most cases for the first time in over 2 decades.

O v e r v i e w : T o L e a r n M

V i r t u a l l y

Since 2021, Industrial Bank has partnered with the South Carolina Department of Corrections to bring the same experience to incarcerated men virtually. We currently serve Lee Correctional Facility in Bishopville, SC and Tuberville Correctional Facility in Tuberville, SC.

150

Justice exposed men and women have completed our financial literacy series

https://industrial-bank com beyondbanking@industrial-bank com

Session 1 : Bank Overview, Program Structure and Banking Basics

Session 2 : The Importance of Saving and Budgeting

Session 3 : Understanding and Managing Credit

Session 4 : Effective Communication

Session 5 : Understanding Insurance and Investments

Session 6: Entrepreneurship, Homeownership or Power of Attorney

Session 7 : Graduation Ceremony/Presentation of Certificates by Bank President/CEO

By Theodore R. Daniels SFEPD Founder & President

Each of us has a unique financial path. One must acquire financial knowledge and skills to ensure a successful financial path for financial stability, resilience, and wealth building. Some surveys and data indicate individuals and families who have strong financial paths are financially literate and have these commonalities:

• Delayed gratification or long view of life

• Increased savings and investments

• Limited consumer debt

• Diversified investments (real estate and financial assets)

• Sound mortgage and auto loan decisions

• Accumulation of retirement savings

• Higher wealth accumulation

On the other hand, surveys and data show that those individuals and families who lack financial stability, resilience, and wealth are likely to have these commonalities:

• Impatience, e.g., current gratification, “present-biased”

• Limited savings

• Limited or no investments

• Casual spending

• High debt loads

• Low retirement savings

• Poor loans (use predatory loans)

• Limited wealth

It is important to increase Americans' financial literacy because this knowledge offers individuals and families the opportunity to enhance or maintain their long-term financial well-being and economic security. In fact, raising Americans'

financial literacy allows everyone to participate in a broader spectrum of the American economy and creates a more stable, fairer, and robust marketplace. Moreover, increasing one’s financial literacy can yield economic security, which can eliminate the financial stress that leads to socio-economic problems that have a negative impact on society.

Each day, we make financial decisions-consciously or unconsciously, and how we approach those decisions has a tremendous impact on our ability to maintain economic security, which is the endgame. Therefore, it is imperative that we acquire the financial knowledge and skills needed to make informed financial decisions regarding the use of our financial resources.

Our quarterly “Financial Success” newsletter (https://sfepd. org/newsletters/) offers excellent financial knowledge, up-to-date financial information, and strategies to help you develop your financial path. g

By Theodore R. Daniels SFEPD Founder & President

Financial literacy can be a friend and support system to help you navigate financial choices and transactions. Moreover, financial knowledge is a powerful tool that allows you to analyze and filter information and enables you to understand the nature of financial transactions.

Being financially literate helps us make sound decisions regarding using credit, establishing financial goals and budgeting, saving, and investing wisely. It also teaches us about risk management (insurance), taxes, and estate planning. Learning to identify fixed, variable, and discretionary expenses enables us to develop budgets to control living expenses, leading to greater savings and wealth.

Knowing how to acquire, use, and manage credit can save you a lot of money and deplete household financial resources. The difference between a low credit score and a high credit score can be very costly.

Have a plan to manage your available financial resources. Create shortterm, mid-term, and long-term financial goals that will drive each component of personal money management and produce greater lifetime financial well-being.

Have a family conversation about your and your family's values to choose how the family's financial resources will be used to ensure financial sustainability, resilience, and wealth.

Everyone should know that financial literacy is empowering. It equips you with the skills to take control of your life and maximize your financial resources. Through financial literacy training, every person, even those with limited means, can learn how to manage finances better and improve their financial and economic status. Learn all there is to know about personal money management concepts and their applications. Additional information can be found at www.sfepd.org. g

Sponsored by JPMorganChase

Getting in the habit of saving money is important, as it helps lead to creating a financial cushion to cover future expenses. Saving is not easy, especially when everyday products are at an all-time high given recent years' rising inflation and simply suggesting cutting back on small indulgences can be irritating. Thankfully, there are options to help saving money become more of a habit to better equip you for life’s unexpected needs. Before determining how much to start saving, first understand money coming in and money coming out – like cost of rent, food, car or public transportation, utilities, and other direct payment expenses, such as subscriptions to various streaming services. Apps can help track these recurring expenses, making it a good time to reconsider or renegotiate them.

Once you’ve understood your monthly budget, check what’s remaining to determine a doable amount to start setting aside each month. When it comes to saving, there are various strategies, from keeping a certain amount in your bank account each week, to automating transferring money from your checking to your savings account each month. You can also save for something specific, like a vacation, home project, or a splurge

you’ve had your eye on for a while. Here are a few saving account options to consider:

Standard Saving Accounts are the most common, easy to access and typically open. Savings accounts can often be accessed and managed online or through the bank’s mobile app, which can make things easier. Before choosing an account that best suits your needs, ask if there is a monthly service fee and potential ways to waive the fee.

Money Market Accounts are similar to savings accounts, but the customer receives more interest on their money, something that varies with banks. They usually require a minimum balance.

High Yield Savings Accounts are increasingly popular, often coming with higher interest rates, making them suitable for short-term savings goals. They work a lot like the typical savings account, allowing for deposits and withdrawals, but there may be transaction limits and minimum balance requirements. They are also protected up to $250,000 at FDIC insured banks.

Certificates of Deposit (CDs) are highly sought after when interest rates are favorable, but you must commit to leaving the money deposited in the CD untouched for the agreed upon term, which is usually months or years. There may be minimum deposit requirements, but they offer returns so are useful for short-term goals, such as

the down payment on a house or car.

Long-Term Accounts provide an opportunity to accumulate returns over years, depending on how the markets fluctuate. These accounts are designed for a specific financial goal and have tax advantages. Consult your financial institution for long-term savings account options, some of which may include:

• 529 Plans: Saving over the years to pay for the education of a child, grandchild, or niece/nephew. Savings are tax-deferred and can only be used for the beneficiary's education, whether for college or another educational institution.

• 401(k): Retirement savings accounts your employer offers. Contributions are usually made monthly (a percentage of the salary) via direct deposit. There are limits to how much you can contribute.

• IRA: There are various types of individual retirement Accounts (IRAs), offering another personal retirement savings option. Contri-

butions are limited, not necessarily offered by an employer, and like the 401(k), they are only used after retirement.

Be sure to ask your bank or financial advisor whether the account you plan to open has a monthly deposit or balance minimum, or any additional requirements or fees. For more budgeting and savings tips, visit chase.com/ financialgoals.

For informational/educational purposes only: Views and strategies

described may not be appropriate for everyone and are not intended as specific advice/recommendation for any individual. Information has been obtained from sources believed to be reliable, but JPMorgan Chase & Co. or its affiliates and/or subsidiaries do not warrant its completeness or accuracy.

Deposit products provided JPMorgan Chase Bank, N.A. Member FDIC © 2024 JPMorgan Chase & Co.

Submitted by United Bank

We all know that life can be unpredictable — and when it comes to finances that it’s best to be prepared for the worst. Enter the emergency fund — money we put away for unexpected emergencies that’s often referred to as a “rainy day fund.” It’s best kept in a savings account, and if we’re wise about it, we contribute to it as often as possible and touch it only when we have to.

But what’s the best way to build one? There are several effective tactics for accruing emergency savings, and the best approach for your own situation will likely depend on your personal preferences, your financial realities, and your level of monetary self-discipline.

No matter what our situations, most of us can take baby steps toward building and growing an emergency fund. If you’re looking for ways to bulk up your own emergency fund, consider these six

creative tactics for putting money away for a rainy day:

This tactic is a great way to get into the habit of saving, and over time the “missing” money will become less and less noticeable. The idea is to set aside a certain amount of money from each paycheck — choosing a set amount that you can comfortably spare — and put it straight into savings on or around payday.

While this tactic may not build a big emergency fund quickly, it’ll definitely add up over time — and as they say, slow and steady often wins the race. When you get spare change after making a cash purchase, or even $1 and $5 bills after breaking a larger bill, drop it into an empty jelly jar or coffee can at

home. When the jar or can fills up, take the funds to your bank and deposit them into your savings account.

We all come across unexpected or otherwise extra money on occasion, whether it’s thousands of dollars in a tax return or $20 in a birthday card. While it might be tempting to hit the town, do some splurge spending, or take a vacation with the windfall, try putting a sizable portion — or even all — of the money away in your emergency fund.

When you have extra money left in your checking account at the end of a pay period, consider putting the surplus into your emergency fund. After all, you’ll have the benefit of a full paycheck’s

worth of new funds in your checking account, so you will be able to spare some money for savings.

Most of us can find room for cutbacks in our budgets, whether it means dining out a little less often, going without that second or third video-streaming service, carpooling to work, or even brewing our own coffee instead of buying a daily cup at the coffeehouse.

6. Let your money work for you

When you put your emergency funds into a high-yield savings account or a money market account, it will begin to grow on its own, even without you making additional deposits. And, of course, as

more and more time passes (and interest accrues), you’ll begin to see compound interest — meaning you’ll be earning “interest on the interest” from your savings. This article is for general informational purposes only. It is not intended to provide specific financial, investment, tax, legal, accounting, other advice or to imply that a particular United Bank product or service is available or appropriate for you. For specific advice you should contact a professional advisor. A professional advisor will recommend action based on your personal circumstances and the most recent information available.

Member FDIC. g

Personal checking and savings account options from United Bank are crafted to perform for you today and throughout your financial future. Our flexible options give you the features and benefits you need and expect, supported by outstanding customer service that meets you wherever you are.

Personal Banking

Checking | Savings | Credit Cards | Lending

By Jada Ingleton WI Digital Equity Fellow

a teen debating how much money to spend on the latest trends and gadgets, to helping an aspiring homeowner decide what house to buy. As schools emphasize mathematics, science, history and language arts as learning fundamentals, studies have shown that a strong foundation in economic values also has long-term benefits.

As organizations and education systems continue to advocate for financial literacy, the District is moving toward economic educational empowerment. In March, the D.C. State Board of Education voted to adopt financial literacy standards, which were then developed by the Office of State Superintendent of Education (OSSE) to be utilized as an elective course for high school students.

“Financial literacy skills are critical for D.C. students to be fully prepared to pursue and succeed on the life path of their choosing,” said then D.C. State Superintendent Dr. Christina Grant in a March statement. “These Financial Literacy Standards ensure that all our high school students have access to the knowledge and skills needed to make strategic and well-advised financial decisions as they consider their future, such as pursuing higher education or entering the workforce. We are proud of the work that went into the development of these standards and grateful for the partnership and collaboration of the State Board of Education to formally adopt these standards.”

D.C. Public Schools (DCPS) have adopted these new financial literacy standards to ensure economic prosperity for the next generation of leaders, entrepreneurs and homeowners emerging from the District.

As of the 2024-25 academic year, District high schoolers have the opportunity to take a standalone, elective course where they’ll obtain knowledge and skills across five content sections: Earning Income, Saving and Investing, Spending, Credit and Managing Risk.

According to OSSE’s official report, in addition to educating students on individual financial circumstances and the influence of personal and systemic factors, the standards cover various survival tools, and will leave students with the necessary skill set to:

• Identify opportunities in Washington, D.C. for financial support in higher education and career growth.

• Investigate ethical dimensions of different types of investments and consider environmental factors for large purchases, such as vehicles.

• Analyze the influence of generational wealth and inherited assets on personal savings and investing.

• Understand the various forms and functions of taxation and requirements for paying taxes.

• Create a budget based on different and changing individual inputs, constraints and goals.

• Analyze factors which impact individual housing decisions, including individual preferences, discriminatory practices, costs, tax credits, budgets and housing availability.

• Compare and consider the impact of different types of insurance.

Unlike Virginia high schools and across some districts in Maryland, a financial literacy course is not required to graduate in D.C.; however, the newfound curriculum reflects a growing demand to expand financial education nationwide.

“There's been a real move to focus on financial literacy, particularly post-pandemic. Given the way that the economy is changing so fast, the idea of being able to adapt, pivot and sort of see new opportunities around corners is really an important perspective in every area of life now, and certainly in the kind of economy that, as you know, has been developing globally,” said Jackie Kraemer, director of Policy Analysis and Development at the National Center on Education and the Economy (NCEE).

Kraemer noted the benefits of teaching financial literacy early.

5 D.C. Public Schools have adopted new financial literacy standards and as of this school year, District high schoolers can take a standalone, elective course where they’ll obtain knowledge and skills related to economics, saving, credit and more. (WI File Photo/Robert R. Roberts)

“[Financial literacy] empowers [students] to be better decision-makers… [and] think about how to plan for [the future], which are the kind of capacities that we really want to develop in our students so that they're prepared to navigate all the changes in the world and the changes in their own lives,” she said.

OF A ‘BETTER, MORE EQUITABLE

NCEE researches worldwide academic institutions to provide district and school leaders across the country with skills, information, and resources to establish high-performing learning systems, crafting transformative policy reform that has helped shape new perspectives on education.

According to Kraemer, the organization's findings, internationally and within the U.S., have emphasized the importance of realigning educational goals to build a better, more equitable public education system.

“The E in our name (NCEE) is

really about looking at…how the education system is designed to be aligned with economic and societal goals, really thinking about how to ensure that students are given a path to economic mobility through education,” she explained.

“We are honing in on what the learning systems look like, and I think the focus on financial literacy and economic education that you see as a real area of interest in the United States recently, is reflecting some of the discussions about expanding the purpose of education.”

Similarly, the Council of Economic Education (CEE) recognizes the role of school curriculums in building a strong ecosystem, prioritizing advocacy and professional development training to help bridge the divide in financial literacy.

While CEE research shows an unprecedented growth of a 12-state increase to pass personal finance requirements since 2022 (36 states have personal finance requirements, with a little more than half for economics), there is still a noticeable 14-point gap concerning financial education for students in states who don’t require the course to graduate.

But, financial education is not just subject to the educators – the tutelage starts at home, preferably “as little as you can get them,” said CEE's president, Nan J. Morrison.

“When you're little, you start to see things happening, you start to interpret them, you store them away, and then when you get into high school, you're ready to think about broader things – budgeting, investing…the power of compound interest, so you're in a better position to understand other kinds of things…for an adult point in time.”

Morrison told The Informer, financial literacy decisions are about “the bigger picture” and

can impact people’s livelihoods down the line, vocationally and personally.

Research from a Finance and Economics Discussion Series – published through the Federal Reserve – shows that high school graduates who received instruction in personal finance had lower loan-default rates and higher credit scores than those from neighboring states without such classes. Additionally, financially literate students who pursue higher education make up a greater percentage of scholarship recipients and hold better rates on loan financing deals.

“Every time you have this knowledge, it applies to a whole bunch of things that you might decide to do. All of those things go into developing your own human capital, but also helping you to make better decisions in your business life. Understanding where the economy is going, understanding what's happening in the world, that can help you to understand the world better, and make those decisions more effectively for yourself, your community and your country,” Morrison said.

In cities like the nation’s capital, where economic development thrives on entrepreneurship, having access to remunerative tools and resources is particularly imperative. Small businesses, often deemed the “backbone” of the country, brings revitalization to communities and generational wealth to families, both elements that can lead to economic equity. Morrison commends entrepreneur-driven cities for advancing capital growth, and reaffirms the power of investing in education to forge a better path for future generations.

“I think that when you marry up financial and economic education, it's just what you're thinking about in terms of your life goals,” she said. “You can usually make that work – not always, not for everyone – but you have a much better shot at having the life you want to live if you have this information.”

g

By James Wright WI Staff Writer

Bernice Waller works as the administrative assistant at Our Lady of Perpetual Help Roman Catholic Church in Ward 8. She was tasked with opening the doors of the church for Lafayette Barnes, the facilitator for a generational wealth building workshop and brunch sponsored by Allen Chapel AME Church’s Men’s Ministry on Sept. 28.

While it was her job to open the facility, Waller also wanted to participate in the event and made a point to sit at the front table with friends and acquaintances.

“I attended this because I wanted to learn more about death benefits and how to plan for my children’s future,” Waller, 74 said. “Many family members are afraid to have this conversation. They say ‘I don’t want to talk about that’ but we need to because this is happening. We need to make sure that all papers are in place.”

Waller was joined by 60 people in the church’s Panorama Room that listened to speakers talk about the importance of good financial management. The event took place as statistics reveal

that the District is a racially biased jurisdiction when it comes to the distribution and possession of wealth.

A post on the DC Fiscal Policy Institute’s website in October 2022 reported that in the District, 87% of the city’s wealth is held by white families, even though they consist of 39.6% of the population. In the District, white households have 81 times the wealth of Black households and 22 times the wealth of Latino households.

The median household income for white residents, at $149,734, is over three times higher than the median income of Black residents, which is $49,652. White households have higher median incomes than all other races in the District, but the disparity between white and Black households is the most disproportionate, according to data from the District government’s Council on Racial Equity.

Barnes said the time has come for Af-

rican Americans to change their mindset about money.

“We as a people are not realizing the importance of debt management,” he said. “It is important to pay your taxes. It is important to pass those assets. You should leave something for other people and your children to have.”

Martin Booker is the AARP Foundation’s director of Financial Health. Booker said the AARP Foundation aids members in being financially solvent.

“The AARP Foundation has published articles on money that members can access,” he said. “We also have interactive tools such as videos that are helpful.”

Booker mentioned an article “99 Great Ways to Save” on the AARP website that informs members on the various methods to conserve money. He also told the attendees to analyze the subscriptions they receive and get rid of those that are not needed and to ask creditors to lower their interest rates on their credit cards.

“It doesn't hurt to ask,” Booker said.

Billie Jean Wright is the CEO of Momentum Title Escrow. Wright advised the attendees to get in the habit of saving some of their money and investigate ways of investing.

“When I got some money, I used to go out and buy Louis Vuitton [products] but now I invest in stocks and other investments,” Wright said. “I am proud of how much money I save.”

Wright stressed the importance of regularly checking credit reports for accuracy and eliminating credit card debt as much as possible. To those who think they are too old to become wealthy, she said “it is never too late to build wealth.”

Tax attorney Ruthven R. Phillips agreed with Wright on paying off credit card debt and advised them to use only one card for holiday shopping.

“It doesn’t help when you have charged up gifts on different cards,” he said. “It is easier to keep track if you are using one card.”

He also emphasized the importance of budgeting.

“Budgeting is not a bad word,” Phillips said. “Your budget should be dynamic and able to change over time as circumstances change.”

In a nod to the young people in the audience, Phillips gave out a book “Motley Fool: An Investment Guide for Teens” by David and Tom Gardner. When he announced the book, Jalen Carter, from Austell, Georgia instantly hopped up and went to the front to get the copy.

“I am happy to get this book,” Jalen, 15, said. “It will help me learn more about money and how to spend it.”

Jalen said he was happy he attended the event along with his family.

“I learned a lot about money here today,” he said.

g @JamesWrightJr10

those 55 and up, that’s our promise to you. All of our checking options provide the convenience of mobile and online banking, access to 55,000 surcharge-free ATMs, Zelle®, bill pay, and mobile deposits. Life is full of financial destinations. We’re with you all the way.

Submitted by Marshall Heights Community Development Organization Inc.

Marshall Heights Community Development Organization Inc. (MHCDO) is a HUD-approved housing counseling agency. MHCDO has a rich history of serving the residents of the District of Columbia, particularly Ward 7.

Babatunde Oloyede, President and CEO, is pleased to showcase housing counseling services supporting generational wealth. Financial Literacy is a critical component of our services. We can meet you where you are: beginner, intermediate, or advanced levels.

HUD recently approved MHCDO to add Emergency Preparedness to its services. MHCDO celebrated National Preparedness Month by launching our inaugural "The Readiness Conference." The conference, held on September 13, 2024, highlighted all emergency preparedness entities and roles.

MHCDO is responsible for the critical area of "Financial Preparedness." Financial preparedness, an essential dimension of disaster preparedness, contributes to effective responses to disasters and recovery. It is also critical for reducing the risks of economic hardship and falling into poverty linked with disaster.

The Readiness Conference was a pivotal event designed to equip residents of the District of Columbia with critical information and resources to prepare for climate-related emergencies effectively.

Expert Speakers included the Federal Emergency Management Agency (FEMA), the D.C. Emergency Management Agency (HSEMA), the National Oceanic and Atmospheric Agency (NOAA), Fire/Emergency Management Services, and others.

The goal was to empower residents with knowledge and tools to safeguard themselves, their families, and their communities against unexpected emergencies and severe weather.

MHCDO launched the conference in Ward 7 as it is reported that vulnerable communities were less prepared for

disaster; those vulnerable communities typically were characterized by higher residential mobility, people living alone, single- parent households, households living under the poverty line, public housing, higher income inequality, and lower rates of homeownership.

One of MHCDO's core values is to "Support Ward 7 First." MHCDO believes deeply in and makes every effort to live, work, hire from, and recreate in Ward 7 first, the District of Columbia second, and the Washington, DC region third.

In the past few years, many American households have been affected by some of the costliest disasters of our generation.

The impact can be catastrophic if the clients we serve in our community are not financially prepared for a disaster.

Strategies to promote emergency savings should include help from financial educators and counselors at MHCDO to create a more significant financial capacity. Multiple studies and media stories have highlighted the lack of preparedness of most households to cope with financial emergencies such as costly car repairs or loss of income from work.

A lack of money for emergencies is problematic because financial shocks will happen. The coronavirus pandemic threatened the livelihoods of many workers who lacked paid leave and/or could not work from home, throwing the need for emergency funds into focus.

Difficulty coping with financial shocks puts households at risk for hardship and more harmful outcomes—difficulty meeting basic needs such as housing and food - following financial shocks like job loss.

MHCDO offers a comprehensive set of workshops and one- on-one counseling. Workshops include:

• Savings Plan: Involve high-yield accounts to grow your emergency fund faster.

• Credit Scoring: Your score is a crucial factor in financial success. It determines how much you will pay for basic quality-of-life concerns like housing, credit cards, and insurance.

• Estate Planning: Protect and

provide for your family; it is a vehicle to transfer generational wealth.

• Cloud-based Financial Record Keeping: Climate change conditions require placing our essential documents in the cloud. Too often, disaster victims are left without documents critical to securing housing and other assistance after a disaster.

• Borrowing Essentials: Helps you to make informed decisions when borrowing. One wrong decision can impact your life for years.

• Predatory Lending: Learn warning signs of a predatory and the attributes of a suitable lender.

The Survey of Consumer Finances showed that only about half of households had adequate emergency savings. The National Household Survey (NHS) reported that only 67% of American households set aside some money for an emergency, and half had no more than $500.

Another study found that having no money to pay for gas, hotels, food,

or rental cars presented substantial barriers to residents' evacuation during Hurricane Katrina.

Other counseling services available at MHCDO are the Home Equity Conversions Mortgage (HECM) as a way to inform homeowners about the pros and cons of the reverse mortgage, Foreclosure Prevention to build strate-

gies to prevent default or delinquency, Emergency Preparedness counseling to shore up homeowners and residents financially before a disaster as well as assist residents in developing an emergency plan. These programs expand MHCDO's influence beyond Ward 7, the District of Columbia, and into neighboring States. g

By Stacy Brown and Demarco Rush WI Senior Writer and WI Contributing Writer

As the nation prepares for Election Day on Nov. 5, the top issue of concern for Americans throughout all polls is no doubt the economy.

In her quest for the White House, Vice President Kamala Harris, the Democratic presidential nominee, has made several proposals aimed to build up America’s middle class.

She has proposed introducing more generous tax benefits for families, in turn hiking the corporate tax rate to help offset spending from bigger tax credits.

Harris also wants to permanently restore the Expanded Child Tax Credit to Up to $3,600. Currently the mark for the 2023 tax year is $2,000 per child. For middle-class working families, the expanded Child Tax Credit lowered taxes or helped them pay their rent or mortgage, along with buying food, and essentials for their children.

Her plan also includes a Child Tax Credit of $6,000 for middle-income and low-income families for the first year of their child's life. This would lower taxes or aid with the costs of formula, diapers, car seats and other costs.

The vice president’s proposal to expand the Child Tax Credit is projected to raise $4.1 trillion in taxes from 2025 to 2034. After accounting for tax cuts and credits, the net revenue would be around $1.7 trillion. However, factoring in slower economic growth, the increase in revenue would drop to $642 billion. The plan is also expected to reduce long-term GDP by 2%, lower capital investments by 3%, decrease wages by 1.2%, and result in 786,000 fewer full-time jobs, according to a report from the Northwest, D.C.-based Tax Foundation. Meanwhile, Republican Senator JD Vance has suggested increasing the Child Tax Credit to $5,000 per child, though he admitted its “viability” would depend on Congress. Marc Goldwein, senior policy director for the Committee for a Responsible Federal Budget, said he estimates Vance’s plan could cost between $2 trillion and $3 trillion

over the same period, but the estimates may change as more details are released.

“The tax credits and other carve outs would complicate the tax code, run more spending through the IRS, and, together with various price controls, fail to improve affordability challenges in housing and other sectors,” Tax Foundation officials concluded.

For lower earning Americans without children, Harris is proposing an expansion of the Earned Income Tax Credit to help individuals who earn less than $63,398 (married filing jointly) or $56,838 (individual) in earned income with a $1,500 tax credit, almost tripling the current number.

The tax credits Harris is proposing could lift millions of children out of poverty and help with the cost of raising kids, but it could come with a price to pay. According to the nonpartisan Tax Foundation,

tax changes in Harris’s tax proposals could reduce long-run GDP by 2%, wages by 1.2%, and employment by about 786,000 full-time jobs.

To combat inflation that Americans saw peak at 9.1% in June 2022, the highest rate since 1981, Harris plans to call on Congress to pass the first-ever federal ban on price gouging.

The bill will set rules for big corporations to make sure they can’t unfairly increase prices on essential goods like groceries during times of crisis.

“Corporations should not be able to exploit times of crisis to excessively and indefensibly increase their profit margins at the expense of American families,” said Harris in her 82 page economic policy breakdown.

Harris also proposes to erase medical debt from the credit reports of Americans.

To provide access to more jobs to Americans that didn’t attend college,

tax relief for developers who build homes that are sold to working families that wouldn’t make their money back originally.

Along with that goal, Harris intends to call on Congress to pass the Preventing the Algorithmic Facilitation of Rental Housing Cartels Act, which aims to crack down on algorithmic systems used by landlords that contribute to surging rent prices by making those practices illegal under antitrust laws.

Harris is also calling on Congress to pass the Stop Predatory Investing Act, which would remove key tax benefits for major investors that acquire large numbers of single-family rental homes.

This would discourage millionaires and beyond from having monopoly-like control on the housing market in certain low-income areas.

The main talking point by Harris in rallies and interviews in regard to housing has been promising to provide working families who have paid their rent on time for two years and are buying their first home, up to $25,000 in down-payment assistance.

Harris is also proposing to eliminate four-year degree requirements for half a million federal jobs.

Keep in mind though, many of these acts would need to be agreed upon and voted through by the United States House and Senate before it can be put into action.

Access to housing is a key component of Harris’s campaign; she wants to expand homeownership by increasing the supply of housing thus making it easier to obtain homeownership.

To achieve this goal she intends to push for the Neighborhood Homes Tax Credit, which would support the new construction or rehabilitation of over 400,000 owner-occupied homes in lower income communities.

This would provide significant

This is where Harris’ plan to increase housing is key, if there is more supply along with demand, prices of homes will decrease thus making the down-payment assistance even more impactful.

Harris's tax plan relies on higher taxes on businesses and the wealthy through unrealized capital gains to raise new revenue.

According to the Wharton Budget Model, the Harris campaign’s proposed expansions of the CTC, EITC, and ACA premium tax credits would cost more than $2.1 trillion over the next 10 years.

“Down payment assistance for first-time homebuyers would add another $140 billion in costs, which we estimate to assist 1.4 million homebuyers annually,” Wharton

HARRIS Page FL-19

researchers concluded. “Raising the corporate tax rate to 28% would raise about $1.1 trillion in new revenue, offsetting slightly less than half of the cost of the other provisions.”

Harris said she intends to increase the corporate income tax rate from 21% to 28% as opposed to former President Donald Trump who advocates for it to be 15%.

This shows the contrast in the two candidates' strategies. Harris is looking for money through taxing the wealthy and corporations, while Trump wants to lower taxes for all but potentially increase prices by putting tariffs on certain imported goods. Time will tell which candidate gets to enact their policies and if they’ll work.

A Harris Poll conducted for The Guardian Newspaper this week shows that Harris' economic proposals are more popular than Trump’s. In a blind test of 12 policy ideas—six from each candidate—four of the top five most popular were from Harris’s campaign.

The most favored proposal was

Harris’ federal ban on price gouging for food and groceries, with 44% of respondents supporting it. Other top Harris policies included expanding the Child Tax Credit and tax breaks for new small businesses, both supported by 43% of respondents.

Trump’s only top five policy was his plan to eliminate taxes on Social Security benefits, which garnered 42% support. While Trump’s policies remain popular with Republicans, Harris’ platform resonated more with independents and younger voters, particularly millennials and Gen Z.

“Though Harris has received criticism for being ‘light on policy,’ a majority of all voters in the poll suggested they understand her policies just fine,” researchers wrote. “More than 60% of voters said they understood Harris’ policies on the economy.”

Don’t know if you’re registered to vote? Not sure what your voting center is? Want to request an absentee ballot? Use The Washington Informer’s Voter Resource Guide to ensure you’re ready for Election Day! g

By AARP Staff

The AARP Foundation’s TaxAide program began in 1968 and as the nation’s largest free tax preparation service has helped 1.5 million taxpayers receive more than $1 billion in refunds just last year.

Less well known to the public is Tax-Aide’s sister program, Property Tax-Aide, which helps older adults with lower income get money back.

More than 9 million Americans likely qualify for property tax relief, but only about 8 percent of them apply for it, according to AARP Property Tax-Aide research. Now in its fifth year, the program wants to see more people get the tax relief available to them.

Jim Mayerle of Grand Rapids, Minnesota, has been a volunteer with the Property Tax-Aide program for two years. “The majority of the

afford the cost of a commercial tax preparation service,” he says. “We simplify the process for them, and they are delighted by our service.”