www.wscpa.org • memberservices@wscpa.org

Tel 425.644.4800

170 120th Ave NE Ste E101 Bellevue, WA 98005

BOARD OF DIRECTORS

Sarah Funk Chair

Joel Williams Vice Chair

Ed Ramos Treasurer

Richard Burger Mackey Secretary

Andrew Brajcich Immediate Past Chair

Kimberly D. Scott President & CEO

Jerrilyn Bogart

Jamie Hueners

Writu Kakshapati

Michaela Kay

Kelly Nelson

Ursula Perkins Liz Redmond Jillian Robison

Scott Rodgers

David Togami

CHAPTER BOARD CHAIRS

Marcie McAllister Everett Area

TBD Seattle/Bellevue Area

Nick Fuller Spokane Area

Nick Braun-Lopez Tacoma Area

TBD Tri-Cities Area

Canada Segura Yakima Area

Wade Helms Yakima Area

MAGAZINE PRODUCTION

Jeanette Kebede Editor

Jennifer Johnson Art Direction

The Washington CPA is published by the Washington Society of Certified Public Accountants for its members. Views and opinions appearing in this publication are not necessarily endorsed by the Washington Society of CPAs.

The products and services advertised in The Washington CPA have not been reviewed or endorsed by the Washington Society of Certified Public Accountants, its board of directors, or staff.

The Washington CPA is published quarterly by the Washington Society of Certified Public Accountants, 170 120th Ave NE Ste E101, Bellevue, WA 98005.

$12 of members’ annual dues goes toward a subscription to The Washington CPA

Periodicals postage paid at Bellevue, Washington and additional mailing offices.

Cover and Contents Graphics: © iStock/treety, © iStock/ Rawpixel

POSTMASTER:

Send address changes to The Washington CPA, c/o WSCPA, 170 120th Ave NE Ste E101, Bellevue, WA 98005.

June 12 | Save the Date

Plan to join us on June 12 for the 3rd Annual WSCPA Membership Summit! This exclusive FREE event is an opportunity to connect with fellow accounting professionals, exchange ideas, and gain valuable insight into the latest happenings affecting the profession. Throughout this event, you will have the opportunity to engage with your peers, participate in interactive educational sessions while earning CPE.

Don’t miss out on this chance to network with like-minded peers and celebrate the accounting profession. Registration will open soon! Learn more about the 2024 Summit on our blog at wscap.org/summit-recap

The effective date for designing and implementing a quality management (QM) system that complies with the AICPA’s new standards is Dec. 15, 2025. Progressing toward your new QM system is essential, and the AICPA has developed a free practice aid to help. Visit wscpa.org/qm25 for tools and resources to help you get started.

• Our 2nd Annual Membership Summit offered up to 8 hours of complimentary CPE. More than 400 in-person and 230 online attendees fostered an inspiring community of professional growth through education and networking. Save the date: the 2025 Membership Summit is June 12!

• Member volunteers continue to help develop relevant and engaging conferences, resulting in a higher 4.5/5 overall rating and growing attendance.

• More than 1,550 members connected with their peers at the WSCPA’s 52 in-person events, including 8 professional forums across the state.

• Membership in our Peak Firm program continues to grow and so do the benefits: Peak Firms can now take advantage of in-house CPE training with a focus on leadership development at little or no cost.

• More than 255 students benefited from 20+ resume review sessions, employer meet and greets, and CPA exam review resource events.

• CPA members volunteered to speak in community schools around the state, introducing students to the profession and sharing the benefits of an accounting career.

• Our committee and staff vigilantly monitored and responded to over 60 bills during the 2024 session.

• HB 1920 was developed and passed to update the Washington Accountancy Act, allowing the Washington State Board of Accountancy to be responsive to the profession in modernizing rules and regulations.

• Continued to work together with national organizations, other state societies and state boards, along with firms and businesses, to address pipeline challenges.

• Invested in future CPAs by awarding 101 scholarships to Washington accounting students totaling $585,000, with nearly 100 volunteer members serving on the scholarship review committee.

• Granted $32,000 to organizations working to address the accounting pipeline by fostering greater inclusion and diversity within the profession.

We can't wait to see what 2025 brings!

"To lead with intention, to innovate with vision, and to build a profession that thrives amid change."

Sarah Funk, CPA, CGMA

As Chair of the WSCPA Board of Directors, I am honored to lead during a transformative period for our profession. Halfway through my term, I reflect on our journey—a path marked by collaboration, innovation, and a steadfast commitment to excellence thanks to the high bar set by those who have come before me and the remarkable WSCPA staff.

Our profession continues to navigate an era of rapid, disruptive change. Pipeline challenges, technological advancements, evolving regulations, and shifting client expectations are reshaping the landscape at an unprecedented pace. In this environment, success requires more than adaptation—it demands the courage to lead with confidence. Challenges will arise, but we must face them with clarity and determination, acknowledging obstacles without allowing them to dictate our trajectory.

At our recent WSCPA board meeting, we engaged in a pivotal planning session alongside the Washington CPA Foundation Board and the WSCPA Diversity, Equity, and Inclusion (DEI) Council. These discussions underscored the importance of strategic vision and collaborative leadership. We focused on strengthening member engagement, exploring innovative solutions to enhance the value the WSCPA provides, and prioritizing initiatives that will shape the future of the profession.

This work is critical as we address the talent pipeline challenges facing our profession. The challenges go beyond attracting talent and must extend to include how to create an ecosystem where diverse perspectives thrive and contribute to our collective success. As a profession, we must bridge experience with ambition and ensure that knowledge is passed down to those poised to lead in the years to come.

A defining theme of our profession’s evolution is the role of technology, particularly generative artificial intelligence (AI). In a Puget Sound Business Journal article entitled, “AI is Here. Now, How Do You Use It?” Nick Pasion observed, “Employers are clear: Artificial intelligence tools are the next essential technology in the workplace. Like computers or email, it will become as indispensable as water or air.” It’s definitely hard to overstate the transformative impact of tools like ChatGPT, introduced just over two years ago. These advancements will continue to fundamentally impact how we work, offering us the ability to execute tasks with unparalleled speed and precision.

What will the specific impact be on accountants though? To borrow the words of Barry Melancon, recently retired AICPA President and CEO, “AI will not replace accountants; however, accountants who use AI will replace those who do not.” This statement serves as a call to action for our profession. The integration of AI into our workflows isn’t optional—it’s essential.

AI enables us to automate routine tasks, analyze complex data, and deliver deeper insights to clients and organizations. But the true opportunity lies in how we harness this technology to elevate the strategic value we provide. As leaders, we must embrace AI not just as a tool for efficiency but as a catalyst for innovation.

At WSCPA, we are committed to preparing our members for this technological shift. Attendees at WSCPA’s fall conferences learned about AI tools for accountants and how AI, through the introduction of deep fakes, is affecting cybersecurity. Through education, resources, and a focus on ethical implementation, we aim to ensure that every CPA is equipped to lead in this new era.

The World Economic Forum’s “The Future of Jobs Report 2023” indicates that, on average, workers are expected to dedicate approximately 44 hours per year to learning and training to stay current over the next five years. This equates to about 0.8 hours per week, or roughly 11 minutes per day. This investment in continuous learning is crucial for adapting to the rapidly evolving job market and technological advancements, including AI.

The accounting profession is currently facing a significant talent pipeline challenge. The number of accounting graduates and CPA candidates has been declining, and this trend raises concerns about ensuring an adequate future supply of qualified professionals.

In response, leaders within the profession and the WSCPA are advocating for reforms to make the path to becoming a CPA more attainable, aiming to increase accessibility while maintaining the profession’s rigorous standards.

These initiatives reflect a concerted effort to strengthen the CPA pipeline and ensure the profession remains robust and capable of meeting future demands. Be sure to read your Present Value newsletter for the latest updates on alternative pathway proposals and other news related to the pipeline.

As I look ahead to the remainder of my term, I am struck by the energy and optimism within our community. Events like the Emerging Leaders Workshop showcase the potential of our profession to inspire and drive meaningful change. These moments remind us of our purpose: to lead with intention, to innovate with vision, and to build a profession that thrives amid change.

Our path forward requires bold leadership. It requires a commitment to results-driven action, a focus on fostering inclusion, and a willingness to adopt new tools and technologies. But more than that, it requires us to work together, leveraging the strength of our collective expertise and passion. If you are looking for a way to share or grow your expertise, you can begin by joining a WSCPA resource group or committee.

The second half of this WSCPA year holds tremendous promise. With so many talented professionals in our community, I am confident that we will continue to achieve remarkable things.

Approaching the future with confidence, courage, and a clear vision. Together, we can shape a results-driven future for our profession—one that not only meets the moment but redefines what’s possible to future proof our profession.

Here’s to an exceptional year ahead. Let’s build the future we want to see.

Mike Nelson

The Washington State Board of Accountancy (WBOA) has made a change to which firms are subject to peer review by amending WAC 4-30-130.

At their meeting on October 18, 2024, the WBOA adopted a rule change which adds an exclusion to the peer review requirement for firms that perform compilation services.

By making this change the WBOA will require only CPA firms providing attest services to complete peer review at their license renewal. It is important to note that any firm that is a member of the AICPA will still be required to complete peer review for compilation work through their membership obligation with the AICPA.

Small firms in Washington who do not perform attest work but have been completing compilations, however, will no longer be required to complete peer review. The motivation for WBOA’s passage of this change is to increase the number of firms that are willing to offer compilation services.

Mike Nelson

At their meeting on October 18, 2024, the Washington State Board of Accountancy (WBOA) opened the rulemaking process to address mobility for CPAs licensed in other states to practice in Washington.

HB 1920, which the WSCPA Government Affairs team helped support during the 2024 legislative session, gave the WBOA the rulemaking authority to adopt changes to regulations for CPAs who are licensed outside of our state to practice in Washington.

As part of the national discussion around licensure, the mobility for a CPA licensee has come to the forefront of issues with mobility and practice privileges for CPAs with clients in multiple states.

Licensees who have been practicing for many decades will remember that mobility was established in the early 2000s when states adopted substantial equivalency and 150 education hours, one year of experience, and passage of the CPA exam as the requirements for licensure. Before mobility, CPAs who practiced in multiple states had to obtain a license in each of those states. As states have been looking to change the initial licensure requirements, the breaking of mobility has been presented as a major roadblock to CPAs and the public.

To head off this issue and in recognition that mobility has become crucial to CPAs in border communities, firms with cross-state clients, and in industry, many states are looking to separate the mobility discussion from the ongoing discussion around licensure requirements.

Four states, Nevada, Nebraska, Alabama, and North Carolina, have had what is being called “automatic mobility” for up to nearly two decades. These policies essentially allow a CPA in good standing from any state to practice in those states regardless of the requirements they met to obtain initial licensure in their home state. This is simple for both CPAs who know they do not need to worry about their licensure requirements before doing work for clients in those states and for those boards of accountancy which do not need to review licensing requirements from other states for individual licensees.

The WSCPA supports the WBOA adopting a form of automatic mobility in Washington. While this does not directly help Washington licensees as it covers CPAs licensed in other states, the coalition and cooperation between states moving to automatic mobility would benefit Washington CPA licensees as other states adopt similar policies.

Alaska, Oregon, and California are working on legislation and rulemaking to address licensing and mobility. They are all looking at adopting automatic mobility. Washington joining them on automatic mobility would help build regional support. Idaho

is also watching closely as Washington and other neighboring states discuss this topic. The WSCPA would like to see all or the majority of states adopt automatic mobility as this would be the simplest way for Washington CPAs and businesses to continue practicing as they have been across state lines.

The WBOA will post draft language in the coming months to https://acb.wa.gov. The first public hearing on this proposal will be held at the next WBOA meeting, Friday, January 31, 2025. If you have comments and would like to make your voice heard, you can email the WBOA ahead of time or attend the meeting virtually or in person in SeaTac. There will be another public hearing at a future meeting in March or July of 2025 as well before any proposal is adopted.

Mike Nelson is WSCPA Manager of Government Affairs. Contact Mike at mnelson@wscpa.org.

illustrations: © iStock/debela, © iStock/Hanna Plonsak, © iStock/filo photo: © iStock/cosmonaut

• For the latest news on mobility and licensing, be sure to read the Present Value newsletter.

• Stay up-to-date on the latest advocacy news and highlights by following our blog, All Things Advocacy. Visit wscpa. org/advocacy25

WSCPA Executive Director 1996-2005

Marcia Holland-Risch, former Executive Director of the WSCPA, passed away on November 21, 2024.

Marcia was a remarkable leader whose legacy continues to resonate within her professional community. As Executive Director of the WSCPA from 1996 to 2005, Marcia brought exceptional experience and strategic vision to the organization. Her expertise in advocacy was pivotal in aligning Washington State under the Uniform Accountancy Act (UAA) to achieve mobility for the CPA license.

"Known for her innate ability to engage members and ensure their voices were heard, Marcia strengthened the WSCPA's commitment to serving the accounting community with dedication and integrity," said WSCPA President & CEO Kimberly Scott.

A Certified Association Executive, she served as the executive director of several other professional organizations, leaving a remarkable footprint in each role. Her legacy continues through the many lives she touched, inspiring those who were privileged to know her.

to our members, guest speakers, sponsors, students and leaders for attending our in-person conferences and events in 2024. We look forward to seeing you again in 2025.

Monette Anderson, CAE

The buzz is real: in-person events are making a bold comeback, and WSCPA members are leading the charge! Attendance at our fall conferences skyrocketed by 30%, and it’s easy to see why. These events don’t just deliver valuable content; they also reinforce WSCPA’s position as the pre-eminent community for CPAs. The electric atmosphere and engaging activities—from pet photo contests to Oscar-style networking—reminded us all of the unmatched value of face-to-face connections. Below are some highlights from fall conferences in case you missed the fun.

Thanks to members who take time to fill out survey content. We read every comment, and your feedback really helps us make sure we continue to bring the content, speakers and engagement you’re looking for. A few highlights from fall conferences:

“It was an awesome and relevant day.” - Pacific Tax Institute

“I loved the pet picture posting—fun idea!” - Pacific Tax Institute

“Thank you. I am so grateful to attend today. The speakers were wonderful and I felt very engaged with the people, the content and the profession.” - Emerging Leaders Workshop

“Loved seeing so many people in person. Also encouraged by how many people stayed for the networking event.” - Not-forProfit Conference

“I was in person yesterday and online today. Both days were incredibly well done! Every aspect was top notch.” - Not-forProfit Conference

“It was a great event with great speakers, timely topics, and an engaged audience. Great work to the WSCPA team!” - Fraud Conference

One of the standout events this year was the WSCPA Fraud Conference, which rolled out the red carpet—literally! Clark Nuber returned to the stage with their 3rd Annual Fraudie Awards, showcasing the top fraud schemes of the year. We leaned into the trend with Oscar-style photo ops, red carpet interviews, and a popcorn machine networking break that brought learning and fun together seamlessly.

WSCPA added a playful twist to our events, creating opportunities for attendees to connect and have fun. A pet photo contest stole the spotlight, with dozens of adorable submissions lighting up our social wall. With the help of our sponsors, the top five nominees were chosen, and audience members cast their votes for their favorite CPA companion.

Our sponsors are joining in on the fun, too. New WSCPA sponsor Praece introduced an interactive challenge with a tech-savvy twist—guessing the number of “computer keys” in a jar. The winner, armed with a little help from ChatGPT, submitted the closest guess and walked away with a shiny new iPad. During the artificial intelligence (AI)-focused session that same day, presenter Lauren Renninger from Armanino had stated, “Don’t worry that you’ll be replaced by AI, worry you’ll be replaced by someone who knows how to use AI better than you do.” It was a comment that was as insightful as it was timely, further reinforcing the value of staying ahead of the curve.

While we’re thrilled to see in-person attendance on the rise, we also deeply value our virtual audience. For many, virtual attendance is the only option due to busy schedules, travel limitations, or personal preference. That’s why we’re committed to ensuring our online attendees stay at the heart of the action. Joining the social wall, competing in trivia games, or contributing to the live virtual chat are just a few ways we’re making sure virtual participants feel engaged and connected. These interactive features are designed to ensure every attendee is a valued part of the WSCPA community, regardless of location.

Thank you for continuing to show up, share your insights, and inspire your peers. Your contributions demonstrate the value of a diverse, inclusive WSCPA audience, and we’re excited to continue innovating for you.

The true magic of in-person events lies in the moments between sessions—the hallway conversations, shared laughs over coffee, and those unexpected career connections that can only happen face-to-face. To amplify these opportunities, our post-conference networking receptions are now open to all members, inviting them to reconnect and build meaningful relationships.

Looking ahead, WSCPA is doubling down on creativity and connection. Expect more engaging themes, interactive activities, and opportunities to collaborate with peers, mentors, and industry leaders. These events not only provide immense value but also reinforce WSCPA’s role as the pre-eminent community for CPAs and top-notch professional development.

If you’ve been waiting for the right time to return to in-person events, this is your moment. The energy is back, the connections are stronger than ever, and we can’t wait to welcome you. Be sure to join us for spring conferences!

Dr. Gabriel Saucedo, PhD, and Shruti Moolani, Chartered Accountant

The workpaper review process remains fundamental to both maintaining audit quality and guiding early-career auditors. Traditionally, audit review has relied on in-person discussions, allowing preparers and reviewers to clarify issues and exchange feedback in real-time. Yet, the rise of remote work, especially post-COVID-19, has introduced a new dependency on digital communication tools like email, Zoom, and firm-specific platforms. While these tools provide flexibility and convenience, they can also present challenges, sometimes resulting in misunderstandings or lacking the immediacy of face-to-face conversations that foster constructive feedback. This evolution has reshaped feedback dynamics within audit teams, offering both new opportunities and unique challenges. Recognizing the essential role of the review process in safeguarding audit quality, this article uncovers fresh insights and practical strategies for firms aiming to refine their approach. By blending the benefits of advanced technology with the unique advantages of in-person interactions, audit teams can enhance their review process, foster auditor development, and ultimately drive higher-quality outcomes.

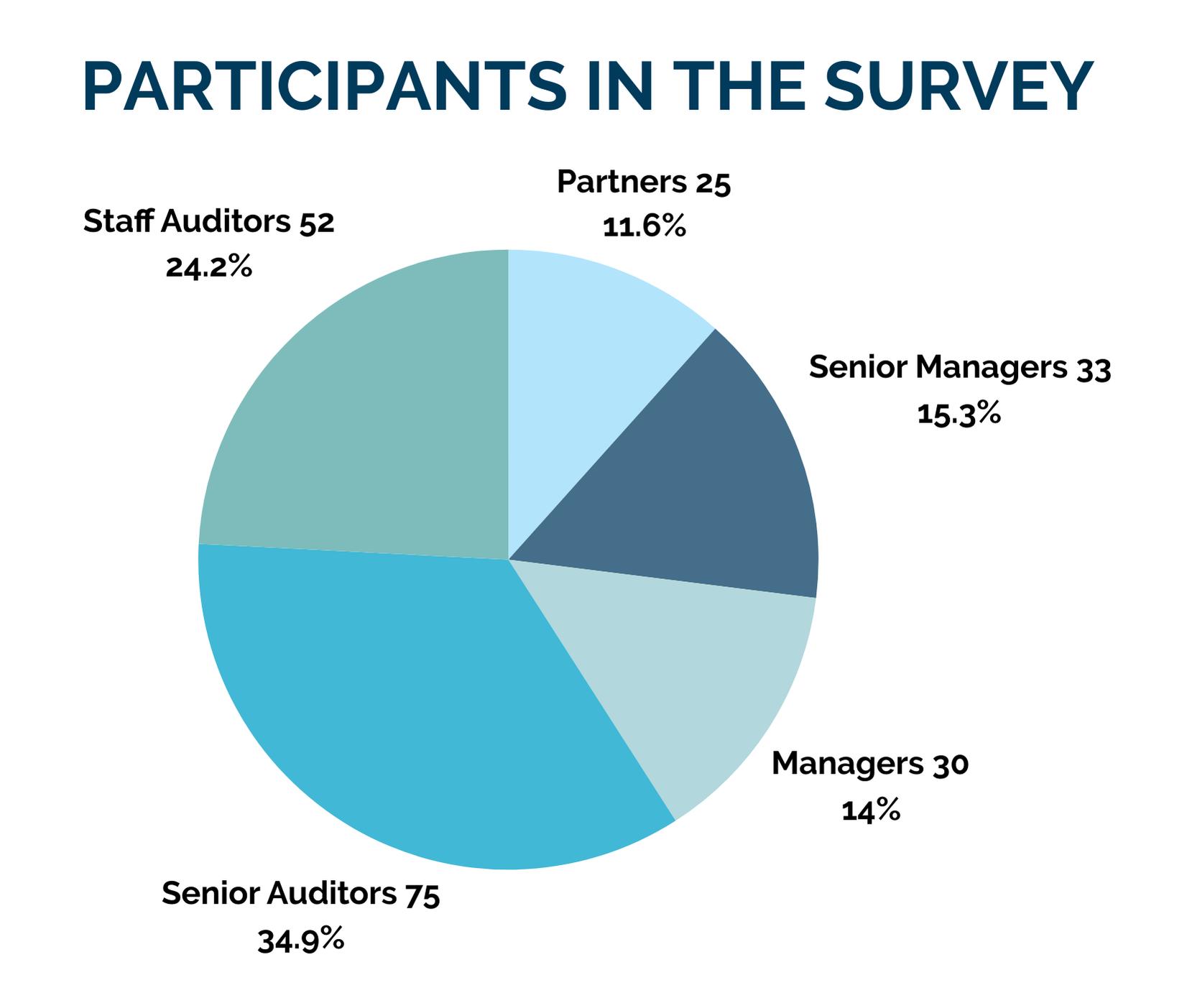

For this article, we build upon previously published academic works titled “Audit Roles and the Review Process: Workpaper Preparers’ and Reviewers’ Differing Perspectives”1 and “Shifting Styles: Do Auditor Performance Levels Influence the Review Process?,”2 both of which explore how distinct preparer and reviewer roles shape the review process. These studies use data surveyed from professionals across Big 4 and other prominent firms, examining how they are navigating changes in the review process. Survey responses from 215 participants (see table below) provide a balanced view, capturing experiences from professionals primarily working with public clients (65%) and others in non-public, governmental, and not-for-profit sectors.

Two parallel surveys were administered to collect data, one for preparers and another for reviewers. Partners and managers completed the reviewer survey, while audit staff participated in the preparer version, presenting a comprehensive look at how the review process is perceived from both vantage points. The data reflects a range of experience levels: reviewers, with an average of 11.3 years, bringing seasoned perspectives, while preparers, averaging 4 years, sharing task-focused insights.

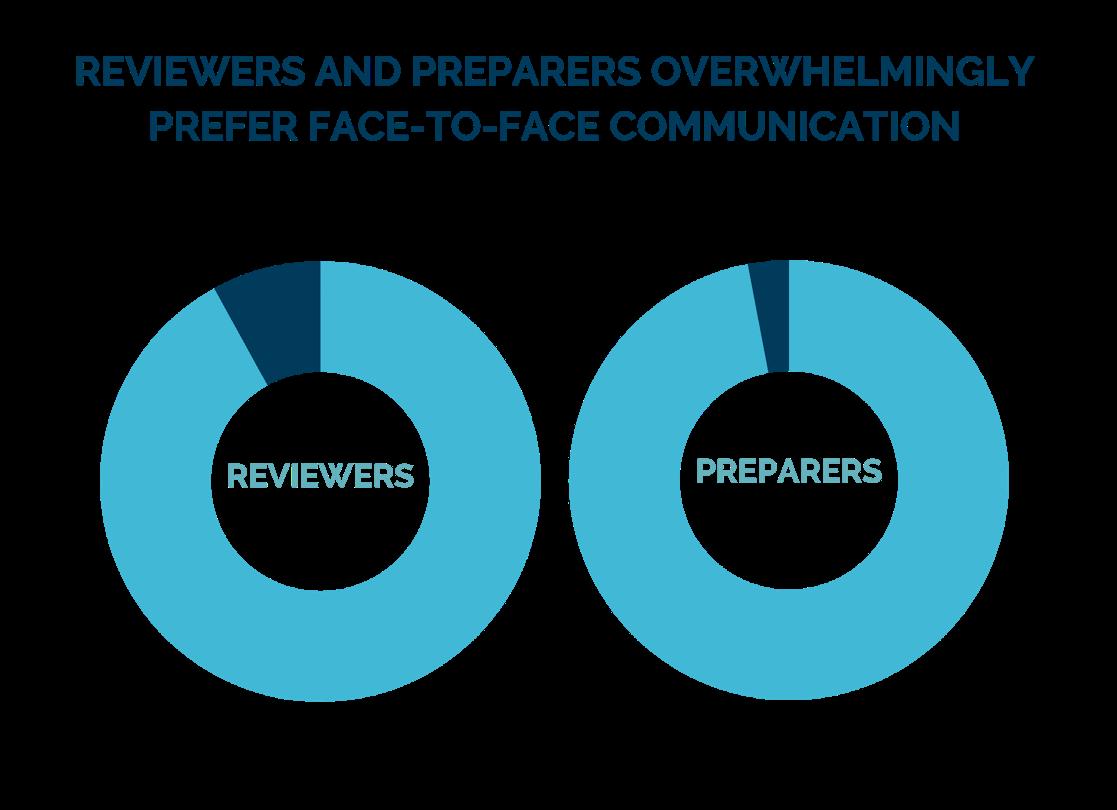

The referenced studies indicate that experienced auditors typically approach the review process by considering various factors, such as the preparer’s competency, audit complexity, and client-specific risks. Preparers, on the other hand, tend to focus on task-specific goals and often have a narrower view of the overall engagement. This divergence is expected, given that reviewers are responsible for the quality of the audit, while preparers concentrate on executing their tasks efficiently. Notably, both reviewers and preparers overwhelmingly preferred face-to-face communication for discussing review notes (92% of reviewers and 97% of preparers indicated this as their preferred method over telephone, e-mail, firm developed software, virtual [video conferencing] or other options). This may not be overly surprising, as in-person communication fosters clarity and prevents misunderstandings, which helps ensure feedback is conveyed accurately.

However, the increasing use of remote work has made faceto-face communication less frequent. Electronic tools, such as email, Zoom, and firm-developed platforms, are now more common. While convenient, many audit professionals worry that these tools can lead to misinterpretations and a lack of full understanding or comprehension, as they lack the immediacy of in-person discussions.

Another element of the aforementioned studies uncovers that auditors’ performance levels also significantly influence the review process. Higher-performing auditors tend to receive more empowering, strategic feedback, while lower-performing auditors receive more directive guidance. This reflects Situational Leadership Theory, where reviewers tailor their feedback

based on the readiness and performance levels of preparers. Reviewers often provide broader, risk-focused feedback to senior preparers, while less-experienced auditors receive more specific procedural instructions.

Prioritizing In-Person Communication

With remote or hybrid work here to stay, there is unlikely a complete reversion to face-to-face work for all teams. However, wherever feasible, audit firms should prioritize face-to-face discussions for critical review notes, as these interactions allow for a more interactive exchange of ideas. Early career auditors, in particular, benefit from observing how review comments relate to broader audit risks. Firms could adopt a mixed approach, combining the flexibility of remote work with scheduled in-person interactions, such as periodic team meetings or client site visits. This not only enhances communication but also helps rebuild relationships within audit teams, which can be strained by remote work.

While face-to-face communication remains essential, audit firms must also adapt to the realities of remote work. Firms should invest in improving the usability of electronic review tools, ensuring that these platforms facilitate clearer, more interactive feedback. Current tools often lack the ability to engage reviewers and preparers in real-time discussions, leading to potential miscommunication. Collaboration platforms that integrate features like video conferencing or threaded discussions within workpapers could help simulate in-person interactions, allowing both parties to ask questions and clarify feedback in context. A two-tiered review process could also be beneficial, where initial review comments are provided electronically, followed by a video or in-person discussion to ensure the preparer understands the feedback.

Remote work has provided preparers with new opportunities to observe client meetings and interactions between senior auditors and clients, allowing them to gain insights into the decision-making process. This visibility can aid in preparers’ professional development, offering learning experiences that were previously limited by travel budgets or office constraints. Firms should capitalize on this aspect of remote work by providing preparers with greater access to client discussions. This can help bridge the gap in professional development caused by reduced in-person interactions.

As remote work becomes the norm, effective digital communication is critical for maintaining audit quality. Custom training programs can help auditors develop skills for delivering clear and constructive feedback using electronic tools. A firm

might implement a training module where auditors practice giving feedback in a simulated remote environment, using tools like Zoom and Teams, to ensure that their points are clear and actionable. This helps avoid common issues such as misinterpretation of feedback or delays in resolving review comments.

An early career auditor could be invited to virtually "shadow" a senior auditor during a critical client presentation or audit planning session, giving them real-time exposure to highlevel discussions and decisions that enhance their learning experience. Even in a remote work environment, mentorship can be maintained through regular virtual check-ins and observation of key meetings.

Integrating Artificial Intelligence and Automation in Reviews

AI and automation tools can assist in the review process by flagging common errors, suggesting improvements, and reducing the workload for human reviewers. These tools can handle routine checks, allowing auditors to focus on more complex judgment-based tasks. For instance, A firm uses an AI-based tool to review financial documents, which automatically flags inconsistencies, freeing up auditors to focus on assessing overall audit risks and providing strategic feedback instead of spending time on manual checks.

A feedback portfolio is a compilation of all the review comments and suggestions an auditor receives over time, which can serve as a personalized development tool. For example, an early career auditor maintains a digital portfolio of feedback received over different audits. When preparing for a new audit, they review this portfolio to see recurring themes, such as the need to improve documentation, helping them proactively address weaknesses before the review process begins.

Overall, research highlights the critical role of effective communication in the audit review process, particularly the strong preference for face-to-face interactions among both reviewers and preparers. However, the increasing reliance on electronic communication tools, driven by technological advancements and remote work trends, poses challenges that must be addressed to maintain audit quality. To bridge the gap between traditional and modern communication methods, firms must enhance the effectiveness of electronic tools and provide training to ensure that review comments are clearly understood. By doing so, they can ensure that the benefits of technology do not overshadow the importance of personal interaction in the audit process.

Shruti Moolani holds a Chartered Accountant designation and is currently pursuing her Master’s in Accounting and Analytics (MSAA) at Seattle University. She previously worked at Wellness Forever Medicare Limited, BDO, and KPMG, all in India. smoolani@seattleu.edu

Shruti Moolani: Throughout my career in audit and risk advisory, I have found the review process to be a critical component of my development as an auditor. Early on, face-to-face feedback was invaluable as it allowed me to quickly clarify issues and understand the bigger picture of audit risks, which sharpened my skills. As remote work became more prevalent, I noticed that while digital tools like email and Zoom offer flexibility, they sometimes lack the immediacy and depth of in-person discussions and a chance to connect more with my seniors and team. However, I’ve also seen the benefits of remote work, especially for early career auditors who can now observe senior auditors in client meetings, gaining insights they might not have had access to in traditional office settings.

Dr. Gabriel Saucedo is an Associate Professor and Chair of the Accounting Department at Seattle University. Prior to completing his PhD at Virginia Tech, Gabriel earned his undergraduate business administration degree from Gonzaga University and worked at KPMG-Seattle in the audit practice. saucedog@seattleu.edu

Dr. Gabriel Saucedo: As I instruct my audit students each quarter (just as I did when I was a mentor and manager at KPMG), I emphatically communicate that review notes are arguably the best form of on-the-job training. Furthermore, students should be ready that firm leadership doesn’t hand out gold stars for every small task that is done correctly. However, review notes should not be viewed seen negatively. New accountants should view these review notes as areas for significant learning, growth, and improvement (although too many review notes may signal poor work performance).

1. Ater, Brandon, et al. "Audit roles and the review process: workpaper preparers’ and reviewers’ differing perspectives." Managerial Auditing Journal 34.4 (2019): 438-461.

2. Gimbar, C., Jenkins, J. G., Saucedo, G., & Wright, N. S. (2018). Shifting styles: Do auditor performance levels influence the review process? International Journal of Auditing, 22(3), 554-567.

applicants. The job was posted again, and the team finally landed a great candidate, but Mallory Penn, CPA, senior director of accounting for the White Sox, admits she was getting nervous. “I was a little surprised that we weren’t batting people away,” she says. “We’re a professional sports team—I thought we’d get hundreds of resumes!” So, if a professional sports team is struggling to attract accounting talent, what does that mean

released its “Accounting Talent Strategy Report” in July 2024, detailing six strategies to help address the accounting talent shortage. Among the strategies is telling a more compelling story about accounting careers.

CPAs in particular can help lead the way in this charge to better attract and engage talent and support the pipeline.

Recently, Mark Wolfgram, CPA, MST, tax director at Bel Brands USA Inc., started to notice something: The first thing CPAs do when they get together is discuss how hard they’re working. “We always lead with that, and it’s not something that endears the profession to the young people we’re trying to keep,” he notes. Jonathan Hauser, CPA, a partner in KPMG’s business tax services practice, noticed the same trend. “It’s our default as humans,” he says. “We focus on the hard things because it’s viewed as a badge of honor, but we don’t talk equally about the tremendous opportunities in this profession. Accounting professionals work hard, but the long hours are tempered with flexibility, interesting work, and many different career paths. So, rather than telling our war stories, we need to tell our glory stories.”

For Hauser, his glory story centers around the flexibility he’s incorporated into his own life over the course of his career. He emphasizes that flexibility isn’t only available to partners. “I was a senior-level staff member when my first son was born,” he says. “My hours were flexible and allowed me to do what I needed to do on a personal level and get my work finished to meet deadlines.”

Wolfgram says reframing the narrative in everyday conversations can go a long way. For example, when someone asks how he’s doing, instead of responding with how busy he is, he describes the good work he’s actually doing. His most recent response: “I traveled to Paris, New York, and Washington, D.C. and worked with people in two different languages to file an application between the United States and French governments to determine how much profit each government gets to share. It was incredibly interesting, and I was able to enjoy spending time in each of those cities. This project has helped me grow as a professional, learn new things, and get better every day.”

Hauser says another part of the profession’s story must include how technology and artificial intelligence are being used to improve employees’ career trajectories: “These tools allow individuals to feel like they didn’t spend four years in school just to calculate depreciation. Now, people can leverage their leadership training and technical skills to work with clients and build their toolboxes through experience. Technology is providing new opportunities—let’s tell people about that.”

Another important story to share is how CPAs’ unique skill sets allow them to give back to their communities in countless ways. Wolfgram says it’s a key issue for today’s young professionals, one that he often underestimates. “It can give a more meaningful experience to your life to know what you do makes a difference, and it’s probably the profession’s most underrated thing.”

Perhaps another underrated or underestimated highlight of the CPA profession is the ability to align your personal interests with your career.

While Penn admits she could be doing accounting and finance functions for any organization, working for one of the nation’s oldest professional baseball teams—the Chicago White Sox—is a childhood dream.

As a lifelong White Sox fan, Penn shares that working for the organization brings unique and fun everyday interactions and experiences, including walking through the tunnel leading to the players’ clubhouse and crossing paths with team members, working with members of the player development department who are often former professional baseball players themselves, conducting a financial analysis of a new sponsorship deal, training scouts to use a new expense reporting tool, or helping the groundskeeper with his budget.

“I love interacting with all of these people from different backgrounds,” Penn says. “Our accounting team does everything from budgeting to tax reporting to financial accounting to analysis, and I participate in things I wouldn’t get to do in a segmented corporate environment.”

What’s more, while the team’s baseball department handles the actual salary negotiations, Penn and her department are deeply involved from a budgeting and forecasting perspective. “We look at the organization’s bottom line to provide guidance to ownership and baseball leadership so they know what our financial position looks like,” she says.

Specifically, Penn recalls one notable off season where salary negotiations involved several big-name players (i.e., big salaries): “We had to forecast what it would look like to sign someone with a really big salary. We analyzed whether we could make that money back through better attendance or ticket sales. Everything we do is for the team on the field.”

But it’s on White Sox game days when the reality of working for a historic sports team really hits her: “There’s a Major League Baseball game going on just outside my office walls, and I can go watch a couple of innings at lunch!”

Martrice Caldwell, CPA, says earning her CPA credential opened many doors for her career: from the outset of her career in public accounting to spending more than 15 years in the nonprofit sector to now serving as controller for the Chicago Fire Football Club.

While Caldwell hadn’t necessarily pictured herself in the sports world at any point in her career, someone in her professional network forwarded her the controller position description, and it turned out Caldwell knew the chief financial officer. “Yes, I was in the right place at the right time, but I also had the experience,” Caldwell says. “I had been growing my network, and I thought, ‘Why not me?’”

When Caldwell joined the Chicago Fire two years ago, she says there was definitely a learning curve. She knew how to write up the five-step process of revenue recognition, but now she needed to apply it to ticket sales, player transfer fees, sponsorships, and merchandise sales. She quickly learned how and why things are done the way they are for a professional sports team.

Like Penn, working for a professional sports team allows for interesting, unique work that most don’t get a chance to see up close. While Caldwell isn’t part of the salary negotiations themselves, her team helps those who are doing the negotiating understand the financial implications of roster decisions to ensure compliance with Major League Soccer (MLS) roster rules. MLS players are employed by the league rather than being paid by the team itself, creating complexities that must be carefully accounted for.

“We develop our rosters based on these rules, and it occasionally involves players who’ve been transferred from other leagues or clubs,” she says. “There can be transfer fees associated with player movement. The intricacies around those transactions and how they follow accounting principles are so interesting. We determine how to account for revenue and expenses in these different scenarios, and then we explain our processes to auditors.”

Although sharing the everyday good stories, like those of Penn and Caldwell, are a must for the profession, burying some of the profession’s problems isn’t going to help either. Experts warn that behind every good story there also needs to be the genuine truth.

“Young people are savvy,” Wolfgram cautions. “If we’re only producing social media posts and content that positively depict the profession, but then a student attends a Beta Alpha Psi meeting and hears from young professionals whose real-life stories don’t align, they’ll see right through it. There’s a difference between telling a good story and living it.”

Parikh says Topel Forman’s policy is to be very upfront with its staff about the hours and time commitments required of them, but they’ll work with their staff to balance their lives: “Our partners are dedicated to helping staff find their balance. Life happens. People get married. They get sick. The marketplace has shifted, and candidates are looking for that flexibility. I think public accounting firms have come a long way.”

For Wolfgram, he’s making sure to walk the talk with his own corporate finance team: “I’m trying to give them the opportunities to have the flexibility I enjoy—not just by saying I believe in it, but by letting them do it. That means if someone has a family event, I’m not going to call them about a tax return. These are the types of things that I can do personally without waiting for things to change on a bigger scale.”

Overall, Hauser calls potential solutions to the pipeline challenge a three-way street that involves: 1) employers doing a better job of helping employees avoid burnout, 2) employees owning their schedules and setting boundaries, and 3) managing client expectations—what needs to be completed today versus tomorrow.

“It’s tough to get the balance right, but we need to be focused on all three of these things,” he stresses. “Let’s take a step back, figure out how to help people live their lives, and share the good story.”

As he listens to conversations about the pipeline challenges, Wolfgram says his main takeaway is there’s no silver bullet that one person, firm, or organization can do to solve the problem: “But that doesn’t mean we give in. We’re problem solvers. We need to continue to do the best we can to solve this, and everyone can do it by tweaking their mindset.”

Caldwell adds: “Yes, accounting is demanding, and programs can be challenging, but you get to chart your own path. I don’t know anywhere else you can do that. Those are the kinds of messages we need to share.”

illustrations: © iStock/treety, © iStock/Rawpixel

Reprinted courtesy of Insight, the magazine of the Illinois CPA Society.

"Rather than telling our war stories, we need to tell our glory stories.”

Affinity Group CPAs & Consultants

Alegria & Company PS

Baker Tilly LLC

Brantley Janson Yost & Ellison

The WSCPA Peak Firm program recognizes and awards special benefits to firms that sign up 100% of their eligible staff for WSCPA membership. Being a Peak Firm establishes you as a leader in the profession and provides an array of discounts and benefits.

Learn more and enroll your firm at wscpa.org/peak-enroll

Exclusive Benefits Include:

• Membership Dues Stay With Your Firm – Traditionally, WSCPA memberships remain with an individual, even if they leave your firm. When a member leaves a Peak Firm, we’ll honor your previous investment by providing FREE membership for the remainder of the membership year to your new hire.

• Easy Billing – Don’t get lost in paperwork—we’ll provide you with a single membership renewal invoice for all your employees.

• FREE In-House Training - Get 2.5 hours of personalized in-house training (valued up to $2,000), customized to meet the specific needs of your organization.

• FREE WSCPA Room Rental – One room per year, up to $1,200 value, subject to availability.

• FREE Job Listings – Up to two free listings on the WSCPA Job Board per year, additional listings at discounted member rate. Up to $200 value.

• FREE Passport Corporate Cards – All staff, members, and support staff/nonmembers; up to 30% of paid membership.

• Recognition – Your firm will be listed as a Peak Firm on the WSCPA website and social media, as well as in our quarterly magazine, The Washington CPA

• Receive a Peak Firm Logo – Display on your website to recruit staff and clients.

All benefits are for the membership year, June 1 - May 31.

Clark & Associates CPA PS

Cook CPAs and Consultants, PLLC

Cordell Neher & Company PLLC

Dwyer Pemberton & Coulson PC

Eide Bailly LLP

Falco Sult & Co

FBCPA Group PS Inc

Finney Neill & Co PS

Gonzaga University Accounting

Greenwood Ohlund PS

Hellam Varon & Co Inc PS

Hunt Jackson PLLC

Hutchinson & Walter PLLC

Jacobson Jarvis & Co PLLC

James Russell PLLC

Johnson & Shute PS

Johnson Stone & Pagano PS

Kovarik & Kim PLLC

Larson Gross PLLC

Lodder CPA PLLC

Martin Bircher Thompson PC

McDevitt & Duffy CPAs

Moss Adams LLP

Newman Town PLLC

Nicholas Knapton PS

Norris Lutkewitte PLLC

Northwest CPA Group PLLC

Opsahl Dawson PS

Rekdal Hopkins Howard PS

Ryan Jorgenson & Limoli PS

Shannon & Associates LLP

Smith & DeKay PS

Starr & Leaf CPA Group PLLC

StraderHallett PS

Sweeney Conrad PS

The Doty Group PS

The Myers Associates PC

Vine Dahlen PLLC

Werner O'Meara & Co PLLC

Willet Zevenbergen & Bennett LLP

Your Financial Solutions LLC

Matthew F. Hersch, CFP®, CEPA

As technology continues to advance, professional service industries, including accounting, are seeing traditional, repetitive tasks increasingly handled by automation. For CPA firms, this shift offers an invaluable opportunity to reimagine the value they bring to clients. Instead of merely providing routine services, firms can deliver a deeper, more strategic level of engagement tailored to complex, evolving client needs. Here's how CPA firms can go beyond the basics and cultivate a richer, more impactful client relationship.

The first step in this transformation is identifying and prioritizing the clients who stand to benefit most from high-touch services. Segmenting clients based on factors like revenue and complexity will allow you to focus on those with the most intricate needs and highest potential for growth. For a more detailed review of this, please see my article in the October 2024 issue of the WSCPA’s Washington CPA magazine. By focusing on these "best clients," firms can allocate resources more effectively, fostering stronger partnerships and providing customized solutions for those with multi-dimensional financial and business challenges.

To deliver a comprehensive experience, CPA firms should adopt a three-step process including the following aspects: Approach, Discover, and Implement.

• Approach: Establish a meaningful, trust-based connection with each client, setting the stage for a more in-depth relationship based on open communication and long-term collaboration.

• Discover: Dive into every corner of the client's financial landscape, including personal, business, and financial plans, to fully understand their unique needs and ambitions.

• Implement: Develop an actionable plan that includes an integrated team of professionals dedicated to advancing the client's goals, ensuring alignment and focused execution.

A high-performing network of professionals is critical to delivering elevated services. Establishing this team requires careful planning and strategic selection.

Start by identifying a core team, typically including you, an estate attorney, wealth manager, and property and casualty specialist. From there, consider the needs specific to your best clients and add professionals with niche expertise. If you work with many business owners, you may want to consider commercial bankers, investment bankers, mergers and acquisitions (M&A) attorneys, valuation experts, succession specialists, etc. Define your ideal partner profile, considering factors like career stage, specialties, growth aspirations, and entrepreneurial mindset. Use your existing network to find candidates, identify industry groups to join, and events to attend to expand your circle.

Once you've identified potential partners, begin reaching out. Leverage your current network, and don't hesitate to ask your best clients for introductions to the professionals they value. Join relevant groups, attend targeted events, and set networking goals for each engagement. As you connect with potential partners, dig deeper to assess alignment in values, client service philosophy, and willingness to collaborate.

With your network and client segmentation in place, it's time to engage your best clients in a new way. Present your enhanced process - built on the Approach, Discover, and Implement framework - explaining how this shift will provide a more holistic, proactive service experience.

For this model to be successful and sustainable, there must be a "universal gain" for everyone involved. Clients should see an immediate benefit from having a coordinated, strategic team guiding their decisions and addressing challenges early. You, the CPA, benefit by creating more meaningful impact, driving

referrals, and securing project-based billing opportunities outside of the busy season. Your professional partners also gain by collaborating on cases that may ultimately benefit their practices, even if not every engagement results in immediate revenue.

Rather than sending clients out to independently meet with various professionals, bring the entire team together to work closely with you and the client. By facilitating these interactions, you can help guide the discussions, identify synergies, and ensure that the client's comprehensive plan aligns with their goals.

Finally, remember that the search for potential partners should never end. Continuously explore new connections and maintain strong relationships with existing ones. This ongoing commitment to growth and collaboration will empower your firm to provide the kind of value clients can't find elsewhere.

By moving beyond the basics, CPA firms can redefine their role in their clients' lives, evolving from service providers to trusted advisors capable of navigating the complexities of modern finance and business. In a world where technology is handling the basics, it's time to focus on the unique human insights that only you can bring.

Disclosure: Matthew Hersch is a Financial Advisor with the Global Wealth Management Division of Morgan Stanley in Seattle, Washington. The information contained in this

is not a solicitation to purchase or sell investments. Any information presented is general in nature and not intended to provide individually tailored investment advice. The strategies and/or investments referenced may not be appropriate for all investors as the appropriateness of a particular investment or strategy will depend on an investor's individual circumstances and objectives. Investing involves risks and there is always the potential of losing money when you invest. The views expressed herein are those of the author and may not necessarily reflect the views of Morgan Stanley Smith Barney LLC, Member SIPC, or its affiliates. Information contained herein has been obtained from sources considered to be reliable, but we do not guarantee their accuracy or completeness. CRC# 4044501 11/2024

We appreciate your support!

Applications are open to rising first- and second-year college students interested in the accounting profession. You could receive a $2,000 accounting scholarship! APPLY BY APRIL 15, 2025

BECOME A SCHOLARSHIP REVIEWER

Help us give away over $550,000 in accounting scholarships! Contact Benjamin Warren for details at bwarren@wscpa.org

a $5,000

The Washington CPA Foundation is excited to be able to offer over $550,000 in scholarships for students in Washington State. If you will be a third-year college student or higher in the fall, have a minimum 2.5 GPA (or equivalent), attend an accredited college in Washington state, and want to be a CPA—please apply!

APPLY BY FEBRUARY 10, 2025 WSCPA.ORG/PATHWAY

RYLANDERLAW: Your Partner in Protecting Businesses

Expertise | Efficiency | Excellence

At Rylander & Associates, PC, we understand the crucial role CPAs play in guiding business decisions. Specializi ng in business law and intellectual property, we provide comprehensive legal strategies to protect your clients’ innovations and corporate interests. Our team, licensed across Washington and other states, ensures meticulous management of IP assets and robust legal support through experienced litigation of business di sputes and intellectual property infringement.

Expand Your Advisory Reach

Leverage our expertise to enhance your client services. Partner with us to safeguard the innovations and business ventures that drive growth.

Rylander & Associates, PC (360) 750-9931 www.RylanderLaw.com

by Aaron Johnson, Brett Durbin, and Scott Edwards, Ballard Spahr LLP

On October 24, 2024, in a 7-2 decision, the Washington Supreme Court upheld the Department of Revenue’s reversal of its long-standing interpretation of the Business and Occupation (B&O) tax investment deduction in Antio LLC v. Department of Revenue, Wash., No. 102223-9.

Since the legislature amended the statute in 2002, the Department had allowed the deduction for any investment income, so long as the taxpayer was not a banking, lending, or security business as statutorily defined. This decision greatly narrows the deduction.

The majority’s ruling accepts the Department’s strained claim that a little-known and largely ignored two-page decision in 1976, O’Leary v. Department of Revenue, adopted an unusual and circular interpretation of the undefined term “investment.” The ruling then alleges that the Washington Legislature “did not abrogate” O’Leary’s purported definition of “investment” when it revised the statute in 2002 to expressly define the types of businesses ineligible for the investment income deduction. Consequently, even though the 16 investment funds involved in the case were the type of entities eligible for the deduction, the Court nevertheless held that the funds were ineligible to deduct their investment income because only “incidental investments of surplus funds” met the purported O’Leary definition of “investment.”

For decades, nearly all taxpayers that are not one of the explicitly excluded banking, lending, or security businesses have relied on the B&O tax deduction found in Revised Code of Washington (RCW) 82.04.4281, to deduct investment income. This was consistent with the Department’s website which had long confirmed that “most mutual funds, private investment funds, family trusts, and other collective investment vehicles… are allowed the B&O tax deduction for amounts derived from investments.” As a result, the taxpayer community is in for quite a shock, as this new interpretation of the deduction greatly increases the B&O tax liabilities of a wide variety of taxpayers and creates significant uncertainty regarding the scope of the deduction.

To try to understand this decision, we have to go back in time to an earlier version of the deduction and two cases at the core of the majority’s ruling.

Before 2002, the statute provided a B&O tax deduction for “amounts derived by persons, other than those engaging in banking, loan, security, or other financial businesses, from investments or the use of money as such.”1 This deduction was first considered by the Court in 1976 in Sellen v. Department of Revenue. The case consolidated the claims of several businesses, including a general contractor, a brewer, two medical nonprofits, and a cemetery trust fund. There, the taxpayers challenged the Department’s denial of the investment income deductions they reported on their tax returns.

• The contractor and the brewer “invested a small percentage of [their] revenues in short term investments.”

• The medical nonprofits maintained a reserve fund which invested in “savings deposits, commercial paper, stocks, bonds, and real estate notes and mortgages.”

• The cemetery trust had the power to invest in stocks, bonds, and bank deposits.2

In Sellen, the Court began its analysis by noting:

“The investment incomes clearly are ‘(a)mounts derived by persons…from investments or the use of money as such.’ Thus, respondents’ incomes are deductible unless respondents are ‘engaging in banking, loan, security, or other financial businesses.’”3

After noting that undefined terms should be accorded their ordinary meaning, the Sellen Court said “The words ‘financial businesses’ are not defined in the statute, and the common meaning of the phrase contemplates a business whose primary purpose and objective is to earn income through the utilization of significant cash outlays.” Since that was not the primary purpose or objective of any of the plaintiffs, the Court held that none of them were “financial businesses,” and they therefore qualified for the deduction. In short, the only question addressed by Sellen was the interpretation of the term “financial business,” not the meaning of the term investment.

Ten years later, the Court was presented with a second case involving the same statutory language, O’Leary v. Department of Revenue. That case involved a partnership that bought and sold apartment buildings. There the taxpayer claimed the investment deduction for interest income that it earned from installment sales contracts where the buyer paid over time with interest. The two-and-a-half-page opinion sloppily based its decision on the Sellen case, inaccurately citing it for the proposition that “an interpretation of ‘investment’ should be limited to the plain and ordinary meaning of the word.”4 The problem is that Sellen only addressed the term “financial business,” but it did not analyze the plain and ordinary meaning of the term “investment.”

Thus, when the O’Leary Court explicitly adopted the Sellen Court’s limitation of the statute’s application to “incidental investments of surplus funds,” it was actually adopting the Sellen Court’s interpretation of the term “financial business,” despite claiming not to consider whether O’Leary was engaged in a financial business.

The limitation of O’Leary was highlighted in 2000 in Simpson Investment Co. v. Department of Revenue. There, the Washington Supreme Court held that holding companies receiving dividends and other investment income from subsidiaries could not take the deduction because they were ineligible “financial businesses” noting that the term “financial business” encompassed more than “banking, loan, and security businesses.”5 Unsurprisingly, the analysis used by the Court in Simpson to determine whether the holding company was a “financial business” focused on whether the investment activities were incidental to the activities of the business.6

In response to the Simpson decision, the Washington Legislature expressly rewrote the statute to allow the deduction to any company that was not one of the statutorily defined banking, lending, or securities businesses. In doing so, the Legislature found that the Simpson decision “could lead to a restrictive, narrow interpretation of the deductibility of investment income for [B&O] tax purposes.”7 The Legislature did not stop there, but went on to state: “The legislature intends, by adopting this recommended revision of the statute [the current version of RCW 82.04.4281], to provide a positive environment for capital investment in this state, while continuing to treat similarly situated taxpayers fairly.”8 Again, since this revision passed, most—if not all—taxpayers that qualified for the deduction used it, without objection from the Department.

Since 2002, the statute has provided a deduction for “amounts derived from investments,” and has only excluded those entities ineligible to claim the deduction, specifically the “banking,” “lending,” and “security” businesses, explicitly defined by statute.

In ruling for the Department, the Antio majority looked to O’Leary and determined that the term “investment” in RCW 82.04.4281

means “incidental investment of surplus funds.” To get to this conclusion, the Court added words the Legislature never used and interpreted the term “investment” contrary to its plain and ordinary meaning, despite O’Leary’s acknowledgement that the interpretation of an “investment” should be limited to the plain and ordinary meaning of the word.9 While O’Leary’s sloppy mischaracterization of Sellen’s interpretation of “financial business” as an interpretation of “investment” reached the same result as Sellen (because O’Leary was an ineligible financial business under the prior version of the statute), it creates significant problems under the current statutory framework.

Here, the Court did not elaborate on the scope of its definition; rather, it held that the Antio entities’ investments in distressed debt instruments did not qualify as “investments” because the entities’ investment activities were more than an “incidental investment of surplus funds.” Suffice it to say, to qualify for the investment deduction after Antio, taxpayers will need to ensure any amount of “investment” income is an “incidental investment of surplus funds.” Taxpayers and the Department will now be forced away from the clear and predictable approach that has been used since the 1970s and move towards a facts-andcircumstances test that does not yet exist.

Notably, in reaching its decision, the Court did not give any weight to the fact that the Department’s website provided “most mutual funds, private investment funds, family trusts, and other collective investment vehicles…are allowed the B&O tax deduction for amounts derived from investments.” This is an important reminder for taxpayers that they cannot rely on what the Department says on its website.

Ironically, the taxpayers most at risk of assessments are those that the Department’s own website said could take the deduction: mutual funds, private investment funds, family trusts, and other collective investment vehicles. From there, related and adjacent taxpayers should pay heed to this new decision and adjust their businesses and affairs, accordingly.

As with all taxes, there are a number of steps taxpayers can take to reduce or eliminate their potential liabilities going forward and we highly recommend that taxpayers take steps to analyze their potential exposure as soon as possible.

One of the biggest issues that needs resolution is the issue of apportionment; namely, what investment income is attributable to Washington for purposes of imposing the B&O tax. The existing apportionment statutes and rules do not cleanly address the attribution of investment income for taxpayers that are not financial institutions. As a result, it is vital to stay tuned in on apportionment developments down the road.

With respect to the application of law in this case, the Court’s decision likely represents the final word, although the taxpayers timely filed a request for reconsideration. After the taxpayers filed their Motion for Reconsideration, the Seattle Chamber of Commerce filed an amicus (or friend of the court) brief. In an unusual turn of events, the Supreme Court called for a response to the amicus brief, but not to the taxpayers. As a result, both the taxpayers (in support of the Chamber’s amicus brief) and the Department (in opposition) submitted a response.

So what happens now? We wait for the Supreme Court to decide whether they will reconsider their decision.

For questions, solutions, and next steps, please contact any member of Ballard Spahr’s State and Local Tax Team.

This article published with permission of Ballard Spahr LLP. View the original article here. https://www.ballardspahr.com/insights/alerts-and-articles/2024/lp/antiowashington-supreme-court-upholds-department-of-revenues-efforts

Aaron Johnson, Brett Durbin, and Scott Edwards are SALT partners at Ballard Spahr. Contact them at https://www.ballardspahr.com/services/ practices/tax/state-and-local-tax

1. RCW 82.04.4281(1980) (formerly RCW 82.04.430(1)).

2. 87 Wn.2d at 879-80.

3. 87 Wn.2d at 882.

4. O’Leary, 105 Wn.2d at 682 (citing Sellen 87 Wn.2d at 883). As noted above, the Sellen Court’s invocation of the axiom that undefined statutory terms are accorded their ordinary meaning was actually presented on p. 882, not p. 883, and was made with respect to the interpretation of the phrase “financial business” not “investment” since the Court noted that the “investment incomes” at issue “clearly are amounts derived from…investments.”

5. Simpson Inv. Co. v. Dep’t of Revenue, 141 Wn.2d 139, 162, 3 P.3d 741 (2000)

6. Id.

7. Antio, LLC et al. v. Dep’t of Revenue, Wash. No. 102223-9, p. 1 (2004) (Gordon McCloud, J. dissenting) (citing LAWS OF 2002, ch. 150, § 1).

8. Id. at 1-2.

9. O’Leary, 105 Wn.2d at 682.

Are you interested in using your CPA skills to make an impact in your local community, or do you know of a nonprofit organization needing help from a CPA? Find or submit an opportunity at wscpa.org/volunteer-opportunities

• NAMI Washington - new

• Community Carrot – new

• Washington DECA – new

• Adoptee Mentoring Society – new

• Roosevelt Alumni for Racial Equity (RARE) – new

• Equal Origins Pierce County Community Development Corporation (PCCDC)

IBA Sells Privately Held Companies: Do you represent a client who is ready to retire or has taken a company as far as they want to or can? IBA is the Pacific Northwest’s oldest business brokerage (M&A) firm. We are professional negotiators with over 4,300 completed transactions. Please contact us if we can be of assistance at 425.454.3052, 509.907.9406, or www.ibainc.com.

Established Renton CPA Firm for Sale Fullservice CPA firm, established in 1975, looking to sell. Gross in excess of $800k. Experienced staff. Owner available to assist with transition. Contact Robert McCorkle, bob@mccorklecpa. com or 425.228.6133.

Generalist CPA Seeking Practice to Buy. CPA would like to buy into an existing firm either as a partner or acquire a business from a CPA. Experience with multistate clients and licensed in CA, MT and WA with businesses from $1mm to $300M. Generalist with experience in many industries and entity types. Experience with HNW individuals. Interested in sensible transition period and seller financing / earn-out. Respond to wacpa@proton.me.

Northern Olympic Peninsula Firm for Sale!

With over 19 years of experience, Accounting Biz Brokers specializes in the sale of accounting firms and tax practices. Selling your accounting firm is complex. Let us make it simple. Northern Olympic Peninsula, WA Gross $390k. Contact Kathy Brents, Accounting Biz Brokers, admin@ accountingbizbrokers.com or 501.499.4357.

Are you looking to retire or sell your accounting and tax practice? Eastside CPA firm is looking to acquire Seattle or Eastside CPA practice. We will work with you to make sure that the terms are mutually acceptable and practice transition goes smoothly. We are a full-service CPA firm. Our focus is small businesses and their owners, HNW individuals. Our services include tax, consulting, accounting and bookkeeping, as well as full payroll service. Please contact us at cpafirm. seattle@gmail.com.

Are you ready to sell your practice for top dollar?

Private Practice Transitions specializes in guiding owners through every step of the process—from valuation to closing. Our expert brokers ensure a smooth, profitable sale with a 100% success rate. Services include confidential marketing, buyer vetting, and deal structuring to maximize value. Not yet ready to sell but curious about the value of your practice? At PPT, we offer a Broker’s Opinion of Value service. Our Opinion of Value (OOV) provides a comprehensive and unbiased assessment of your practice’s market value, ensuring you have the knowledge you need to make confident, strategic decisions. Contact us today at (253) 509-9224 or visit privatepracticetransitions.com to get started!

CPA in Downtown Spokane. I am a CPA in downtown Spokane who is looking for an accountant to share office space with me or a JV arrangement on tax clients/general accounting services. Ideal situation would be an accountant who has some existing clients and wants to grow his or her business by adding more accounts and assisting with the workload on my current existing accounts. This in primarily an income tax practice with some accounting support work. Contact Terry at 509.462.0315 or email terrenced@spk-acct.com.

Check out this free benefit for WSCPA members!

Verifyle and the WSCPA have partnered to offer all members access to Verifyle Pro™️, Verifyle’s premium, ultra-secure online file sharing and messaging service (a $108 value) at no cost to WSCPA members

Sign up at verifyle.com/wscpa using the email on your WSCPA member account.