RAISING DOWN PAYMENTS

Why MLOs should teach clients the Amish approach

ORIGINATORS VS. REAL ESTATE AGENTS

It’s time to teach them how GSE loans really work

AVOID FATAL CAREER MISTAKES

Don’t be branded for life from these errors

TAKE THE PLUNGE

Stand out among a sea of applicants when job hunting

BROKERS ON THE PROWL

Try these proven tactics to snare more business FRIEND OR FOE?

The trust issues with artificial intelligence

Vol. 15, Issue 10 $20.00 OCTOBER 2023

A PUBLICATION OF AMERICAN BUSINESS MEDIA

Leverages in High Places Leverages in High Places And a Process as Smooth as Tennessee Whiskey And a Process as Smooth as Tennessee Whiskey Rates that Won’t Achy Break Your Heart (or Wallet) Rates that Won’t Achy Break Your Heart (or Wallet) INFO@RCNCAPITAL.COM RCNCAPITAL.COM 860.432.5858 ©RCN Capital, LLC. 2023 All Rights Reserved. NMLS #1045656. RCN Capital, LLC is licensed in AZ (License #: 0932325), CA (Loans made or arranged by RCN Capital, LLC pursuant to a California Finance Lenders Law license # 60DBO-46258), MN (MN-MO-1045656), and OR (ML-5571). This is not an offer to lend. All offers of credit are subject to due diligence, underwriting and approval. Not all borrowers will qualify and not all borrowers that qualify will receive the lowest rate or best terms. Actual rates and terms depend on a variety of factors and are subject to change without notice. MOSEY ON DOWN WITH YOUR DEAL, NOW LENDING NATIONWIDE! MOSEY ON DOWN WITH YOUR DEAL, NOW LENDING NATIONWIDE!

RAISING DOWN PAYMENTS

Why MLOs should teach clients the Amish approach

ORIGINATORS VS. REAL ESTATE AGENTS

It’s time to teach them how GSE loans really work

AVOID FATAL CAREER MISTAKES

Don’t be branded for life from these errors

TAKE THE PLUNGE

Stand out among a sea of applicants when job hunting

BROKERS ON THE PROWL

Try these proven tactics to snare more business FRIEND OR FOE?

The trust issues with artificial intelligence

Vol. 15, Issue 10 $20.00 OCTOBER 2023

A PUBLICATION OF AMERICAN BUSINESS MEDIA

Join Now 800.400.5451 fnba.com/wholesale Providing Certainty in an Uncertain Market

P&L in the Industry

out of 10 Approved

App to CTC in 22 Business Days

Guidelines

Easiest

9

Average

Simple

Lending in All 50 States

4 Act Like An Olympian Champions overcome tough times to be winners. 6 Look Beyond Lack Of Experience But do due diligence before hiring new MLOs. 8 Be An Outstanding Panelist Stand out when you’re one voice among many. 10 Make Your Clients Unsinkable Mortgage seekers need to know the complete cost of homeownership. 14 Non-QM Resource Guide AMC Resource Guide 15 People on the Move See who the movers and shakers are in the mortgage industry. 16 Build-A-Broker: Avoid Fatal Errors Your career could die from pretty basic mistakes. 20 Your First Million Dollars: Make Yourself Heard Have trouble getting points across? Seek unbiased assitance. 22 Benchmarks & Best Practices: Helping Others Helps You Once you become a financial literacy mentor, your business will flourish. 24 Wholesale Lender Resource Guide 26 Friend Or Foe? Learn where ChatGBT falls in the mortgage origination universe. 30 Defining Your Career When job hunting, make it known you’re more than just your numbers. 34 Don’t Settle For Second Brokers are fighting to be the first choice of consumers. 38 Data Bank 40 Listen Up Real Estate Agents How to get the message across that FHA mortgages are good choices. 56 Non-QM Lender Directory 57 Wholesale Lender Directory Originator Tech Directory AMC Directory 58 Facebook Thoughts: The Chair’s A Marvel. Nick? Not So Much. nationalmortgageprofessional.com OCTOBER 2023 Volume 15 Issue 10 CONTENTS nationalmortgageprofessional.com COVER STORY PAGE 46 Funds For Downpayments Barn raising works for the Amish. Now there’s a mortgage equivalent. SPECIAL ADVERTISING SECTION PAGE 13 Originator Tech Showcase NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | OCTOBER 2023 | 3

Achieving The Gold Standard

Jackie Joyner-Kersee, the Olympian who was named Female Athlete of the 20th Century by Sports Illustrated, would talk about her upbringing in East St. Louis. This is not the nicest place to live, to work, to survive. But where others saw blight and despair, she simply closed her eyes to the bad and concentrated on the good. She focused on herself, on making herself exceed. She trained incessantly, she focused her efforts on what she did best — and she became the fastest woman alive.

It’s a story that echoes one told by Amanda Beard. At just 14, Beard went to the Olympics in Atlanta and improbably won gold in swimming. She was the star of the day, a product of instant fame. But then puberty started changing her body, and the curves of a developed woman changed her speed in the water. Her critics said she was washed up. She barely qualified for the next Olympics and was failing in every heat — until the very end, when she shook off her fears and found her self-esteem, and in a sudden burst of motivation following many rounds of tears, she managed to earn a bronze medal. She has since gone on to win more gold and silver — all told, she’s won seven Olympic medals — but she stresses that no medal was more important to her than that bronze one. It’s the one where she finally found herself.

Loan originators these days may be feeling a lot like these Olympians. So much is stacked against them, the probability of success so small, that it would be easy to give up. Giving in to self-pity is easy. So is blaming the economy, the lack of housing inventory, high rates. Of course, all of those are factors that make success now harder than it was. But purchase loans are still being made, refinances still occurring, fix-and-flip still turning over. Someone out there is medaling in loan origination.

If it’s not you, then please give this issue a thorough read. It is full of techniques and strategies to get you on the winners’ dais. We’re showing you how ChatGPT can win over borrowers for you. We help you understand your worth as you consider working for a different company. What do rookies need to get going? — we’ve got that, too. And maybe more business will come your way if you incorporate being a trusted financial advisor into your profile.

This is, too, NMLS license renewal season. Take it seriously, as this is where you get critical hands-on information on how to properly make a loan that’s good for everyone: originator, lender, buyer, and borrower.

Olympians, after all, don’t give up. They adapt. It’s the only way to win.But these LOs won’t give up. And we’ll be with them for the journey, writing their stories.

STAFF

Vincent M. Valvo

CEO, PUBLISHER, EDITOR-IN-CHIEF

Beverly Bolnick

ASSOCIATE PUBLISHER

Christine Stuart

NEWS DIRECTOR

Keith Griffin

SENIOR EDITOR

Mary Quinn

MULTIMEDIA PRODUCER

Erica Drzewiecki, Katie Jensen, Ryan Kingsley, Sarah Wolak

STAFF WRITERS

Rob Chrisman, Dave Hershman, Erica LaCentra, Harvey Mackay, Lew Sichelman, Mary Kay Scully

CONTRIBUTING WRITERS

Regina Morgan

ADVERTISING SALES EXECUTIVE

Nicole Coughlin

ADVERTISING ASSOCIATE

Alison Valvo

DIRECTOR OF STRATEGIC GROWTH

Julie Carmichael

PROJECT MANAGER

Meghan Hogan

DESIGN MANAGER

Stacy Murray, Christopher Wallace

GRAPHIC DESIGN MANAGERS

Navindra Persaud

DIRECTOR OF EVENTS

William Valvo

UX DESIGN DIRECTOR

Andrew Berman

HEAD OF CUSTOMER OUTREACH AND ENGAGEMENT

Matthew Mullins

MULTIMEDIA SPECIALIST

Melissa Pianin

MARKETING & EVENTS ASSOCIATE

Kristie Woods-Lindig

ONLINE ENGAGEMENT SPECIALIST

Joel Berman

FOUNDING PUBLISHER

Submit your news to editors@ambizmedia.com

If you would like additional copies of National Mortgage Professional Call (860) 719-1991 or email subscriptions@ambizmedia.com www.ambizmedia.com

VINCENT M. VALVO Publisher, Editor-in-Chief

© 2023 American Business Media LLC. All rights reserved. National Mortgage Professional magazine is a trademark of American Business Media LLC. No part of this publication may be reproduced in any form or by any means, electronic or mechanical, including photocopying, recording, or by any information storage and retrieval system, without written permission from the publisher. Advertising, editorial and production inquiries should be directed to: American Business Media LLC 88 Hopmeadow St. Simsbury, CT 06089 Phone: (860) 719-1991

info@ambizmedia.com

OCTOBER 2023

Volume 15, Issue 10 LETTER FROM THE PUBLISHER

4 | NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | OCTOBER 2023

Helping mortgage professionals achieve their clients’ purchase and investment goals, Acra Lending was formed to specialize in alternative income products, such as bank statements, asset depletion and verification of employment programs. Our programs have been developed over years to include fixed and adjustable rate mortgages (ARMs) for residential properties on both an owner-occupied and non-owned occupied basis.

Check out some of our programs listed and partner with the industry’s leading private mortgage lender.

Acra Lending is a registered dba name of Citadel Servicing Corporation, 3 Ada Parkway, Ste 200A, Irvine, CA 92618; (888)-800-7661 (“CSC”) NMLS ID# 144549, Licensed under Arizona Mortgage Bankers License # 1034431, California Department of Financial Protection and Innovation under the California Residential Mortgage Lending Act license # 41DBO-74196, Finance Lenders License # 60DB0-94450, CA-DRE #01799059, Florida Mortgage Lender Servicer License # MLD523, Georgia Mortgage Lender License/Registration # 23462, Minnesota Residential Mortgage Originator License Other Trade Name #1 MN-MO-144549.1, Nevada Mortgage Company License # 4449, North Carolina Mortgage Lender License # L-160722, Oregon Mortgage Lending License # ML-5599, Tennessee Mortgage License # 125315, Utah-DRE Mortgage Entity License - Other Trade Name #1 12074249, Virginia Lender License # MC-5845. For mortgage professionals only. This is for informational purposes only. For legal and professional advice on applicable state and local licensing requirements that apply to you, please contact an attorney. Acra Lending is an equal opportunity lender. Rates, terms, and programs subject to change without notice. O er of credit subject to credit approval per applicable underwriting and program guidelines, applicant eligibility, and market conditions. Not all applicants may qualify. Not valid in the following states: AK, ND, and SD.

CONTACT US TODAY TO GET STARTED THE INDUSTRY’S LEADING PRIVATE MORTGAGE LENDER CALL US TODAY (888) 800-7661 SALES@ACRALENDING.COM | WWW.ACRALENDING.COM OR VISIT OUR SITE! ACRALENDING.COM INVESTOR CASH FLOW/DSCR Qualify based on the cash flow of the desired property. Available on Single Family Residences, 2-4 Units, Condos, Condotels, Townhomes, and Non-Warrantable Condos Qualify with 100% on personal account deposits and 50% on business account deposits (12 consecutive months) 12 MONTH BANK STATEMENT Letter of good standing with current financial institution or international credit report FOREIGN NATIONAL Qualify with enough liquid assets to cover the loan balance ATR-IN-FULL More great programs from the industry’s leading private mortgage lender available at www.acralending.com LEADING BUILT FOR SELF-EMPLOYED, INVESTOR, AND FOREIGN NATIONAL BORROWERS

Determining The Quality Of Rookies

Simple use of due diligence increases chances of success

BY DAVE HERSHMAN, CONTRIBUTOR, NATIONAL MORTGAGE PROFESSIONAL MAGAZINE

BY DAVE HERSHMAN, CONTRIBUTOR, NATIONAL MORTGAGE PROFESSIONAL MAGAZINE

In the last issue, we discussed the topic of rookies coming into this industry. To managers that are hiring — we were all rookies at one point, and someone gave us a shot. There is no way of determining which rookies will fail and which ones will succeed. But we can increase the chances on our end in a few ways:

• Making sure the rookies we hire are quality rookies.

• Making sure the rookies we hire have the right experience.

Making sure that the rookies we hire have the training and mentoring they will need.

This month I would like to focus on the quality aspect. How do we ensure that the person we hire is a quality person? Most of the time, people come into this

industry by accident. Again, going back to my own story, I played racquetball with people in this industry. They thought my aggressiveness on the court would translate into top production. They were right, by the way, but not for that reason.

The point is — just because you have a connection with the person does not mean they are the right fit for the company and the industry. There is an important idiom in business: Success is not an accident.

Let me add one more:

Failure is not an accident.

SIMPLE SOLUTION

You will increase your chances of success and decrease your chances of failure by accomplishing a decent amount of due diligence. Where should this work be focused?

• On-line. Look at their social media. Are there postings that contain red flags? Drunken parties might be one. Offcolor postings might be another. Controversial postings might be another. We are not looking to see if we agree

DAVE HERSHMAN 6 | NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | OCTOBER 2023 RECRUITING, TRAINING, AND MENTORING CORNER

with their opinions and philosophies. But remember, if they are going into sales, they must be someone who can relate to everyone. I personally have strong opinions about many things, but you won’t find them posted on social media.

• References. Speak to those they have worked before in the past. Even if they are coming out of college, they should have had summer jobs and teachers you can speak to. Are they reliable? Do they pick up concepts well? Are they social? Do they relate well with people? Are they leaders? You should even speak to someone who

referred them. Describe the job — would they really fit in this position?

Of course, these concepts apply to experienced hires as well. How many times have you hired an experienced loan officer and then found out it was a mistake? A mistake you could have avoided if you had done your due diligence up-front? Again, success is not an accident. If the experienced producer has a mediocre track record, there is usually a reason for that — though 90% of them will tell you it was the fault of the previous company(s). That is a red flag right there.

With a rookie — it is a bit harder to extrapolate from their experience to success in this industry. But many of the traits are relatable. And many of the traits which would prevent success are relatable as well.

Note I have talked several times about the experience of rookies. Rookies have experience and this experience is just as crucial as the experience of present producers. More on that topic in the next column. n

Dave Hershman is the top author in this industry with seven books published as well as the founder of the OriginationPro Marketing System and the OriginationPro’s on-line comprehensive mortgage school. Dave is also Director of Branch Support for McLean Mortgage. His site is www. OriginationPro.com and he can be reached at dave@hershmangroup.com

NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | OCTOBER 2023 | 7

Rookies have experience and this experience is just as crucial as the experience of present producers.

Preparing For A Panel

BY ERICA LACENTRA, CONTRIBUTOR, NATIONAL MORTGAGE PROFESSIONAL MAGAZINE

With event season in full swing, mortgage professionals should be thinking about what opportunities exist at trade shows and conferences that allow them and their company to gain greater visibility with the event audience. Having the ability to speak at an event can be a tremendous opportunity to position yourself and your company as an authority in the industry and share your expertise in a more actionable way than just giving an elevator pitch at your booth. While giving a solo presentation to a large audience can be daunting or it can be difficult to snag a coveted keynote spot, participating in a panel discussion can be a great way to start your foray into the world of professional speaking. However, while you may think that being a panelist is going to be a breeze

compared to being the one and only speaker during a solo session, there are certain steps that folks should take to better prepare for participation and ensure that they are providing a more informative experience for the audience.

So, if you’re a first-time panelist, what should you do to prepare?

CONNECT WITH FELLOW PANELISTS

The best piece of advice for any person participating in an industry panel is to take time to connect with the panel moderator and your fellow panelists long before you hit the stage. Unlike an individual speaking session where you are monologuing information usually with an accompanying presentation, the best and most entertaining panels are when participants have a meaningful and lively conversation based on the presented topic. Great panel sessions flow seamlessly from topic to topic and create actual discussions among the panelists so that certain concepts can be expanded so that each participant

NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | OCTOBER 2023 THE XX FACTOR ERICA LACENTRA

A panelist differs from being a solo speaker — prepare accordingly

Panelists at Originator Connect in Las Vegas, 2023.

can provide a unique viewpoint.

To ensure there is no shortage of topics that panelists can add their insights to, it is critical that the moderator and panelists connect ahead of time to create an outline of the flow of the panel. Panelists should craft questions with the moderator to ensure they have a chance to touch on all the most critical information to provide value for the audience to guarantee a better flow to the discussion. Panelists

figures, it certainly doesn’t hurt to come prepared with key takeaways that you can provide to the audience. You should be thinking about how you are going to be able to add the most value for the audience on this topic and preparing actionable advice or insight that you can add as the panel discussion progresses. It could be anecdotal, it could be stats you have researched, or it could be a mix of both, but regardless, you should be going into a panel discussion knowing what

self-promotion to get their money’s worth rather than providing insight on the topic at hand. Panelists who often monopolize the conversation aren’t really adding value to the discussion. Audience members are usually turned off by this behavior and tune out this speaker. In order to avoid being tuned out, remember that contributing value to a panel discussion is the best promotion you could do for yourself and your company. Rather than making your

should be thinking about what topics you, as a group, want to cover and how they could logically flow from one discussion point to the next.

Also, you should be thinking about how each panelist’s area of experience can be best highlighted so that each participant has an equal amount of time to show off their expertise. When done properly, a moderator can pitch a single question to one panelist and it should either cycle through all panelists so that each participant can provide a unique key piece of information or build off a previous piece of information. Done right, if panelists don't have anything specific to contribute to one question, they can at least use the information gleaned as a stepping stone for the next topic so that everything connects and flows properly.

PREPARE YOUR TALKING POINTS

After you’ve had a chance to connect with the panel moderator and your fellow panelists and you know the general format and topics being covered, it’s time to prepare your own talking points. While panels should be more conversational and not just regurgitating facts and

key points you want to present that the audience will be walking away from the session with.

You can create general notes that you can bring with you to make sure you are addressing your talking points while also making the discussion more fluid. Especially during your first panel, it can be easy to get distracted or off track as the conversation progresses. Preparing your talking points ahead of time and having them on hand will make sure you hit everything you had hoped to discuss and also ensures you look like you are on top of your game throughout the panel.

REMEMBER IT’S NOT JUST ABOUT YOU

Audiences like panel sessions because they can learn from numerous industry experts in one sitting. A good panel should be the equivalent of multiple solo speaking session highlights condensed into one discussion.

One of the biggest mistakes that panelists often make is thinking they don’t have the same opportunity for company and self-promotion to the extent that they would during a solo speaking session. Often speakers will overcompensate by doing too much

talking points all about you, add industry insight and position yourself as a thought leader. Present real life examples and be relatable, honest, and vulnerable, and listen and add to other panelists’ commentary. This will ultimately show the value you and your company can provide to audience members.

DON’T BE PERFECT, JUST PREPARED

At the end of the day, getting ready for your first or hundredth panel all comes down to preparation. Panels can be an extremely valuable tool to gain additional reach and recognition at events. Just remember it’s all about the actionable advice you can provide that audience members can ultimately take away at the end of the session, not blatant self-promotion. Panels should be seen as an opportunity to connect with your fellow panelists as well as the audience and as long as you are providing your unique perspective and knowledge, you’ll be in a good spot to make the most of your participation. n

Erica LaCentra is chief marketing officer for RCN Capital.

NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | OCTOBER 2023 | 9

The best piece of advice for any person participating in an industry panel is to take time to connect with the panel moderator and your fellow panelists long before you hit the stage.

‘Hidden’ Costs Sink Too Many Ships

First-time homebuyers have to leave renters’ mentality behind when it comes to costs

BY LEW SICHELMAN, CONTRIBUTOR, NATIONAL MORTGAGE PROFESSIONAL MAGAZINE

Are we sending too many marginal buyers into the homeownership abyss? Research suggests we are. Not because they can’t afford their mortgage payments, which they often barely can. Rather, because the actual cost of owning and caring for a house can sometimes be overwhelming, if not downright devastating.

Never mind that more

young home buyers can name the latest Taylor Swift tune than their lawmakers in Washington. More importantly, at least in the mortgage business, nearly two-thirds of them cannot ID the four elements of a mortgage payment, according to a study by Clever Real Estate. Spoiler alert: It’s principal, interest, taxes and insurance, or PITI for short.

Another survey, this one from insurance group Hippo, found that roughly half of recent home buyers

10 | NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | OCTOBER 2023 THE MORTGAGE SCENE LEW SICHELMAN

said owning a house is more expensive than they anticipated; there’s just too much maintenance and upkeep. A Zillow study found that three out of four buyers have regrets; chief among them, the home needs more work or maintenance than expected.

EXTRA $1K A MONTH?

But maintenance is only one of the recurring expenses ownership entails. There are a host of other costs that should

be considered — but often are not. Some call them “hidden.” Others say they’re “ignored.” And still others say they’re simply “forgotten.” But by whatever name you choose, they’re no roses.

Taken together, these costs add $1,180 a month on top of the typical house (principal and interest) payment, according to Zillow and Thumbtack, a site that links homeowners to local contractors. Hit by these expenses — expenses they did not expect or at least consider — it’s no wonder a good many buyers not only regret their decisions but also fall into default and maybe even lose their places to foreclosure.

In other words, home buyers who focus solely on the cost of mortgage interest and principal are doing themselves a disservice. And so are the lenders who allow them to do so. Might not it be better to at least warn would-be borrowers of the land (no pun intended) mines that lay ahead?

Two costs often ignored by buyers are insurance and property taxes, likely because they are usually included as part of their monthly payments. But unlike the P and I portions of a fixed rate mortgage, the total of which does not change over the loan’s term, the T and I shares change, mostly up and often annually.

Take property taxes, which are the

— and in a hurray, says David Logan, an economist with the National Association of Home Builders (NAHB).

Property taxes are inescapable if you don’t want a lien placed on your place. And unless you want to go commando, you’ll need homeowners insurance for protection against fire, theft, and major disasters. What’s more, if you have a mortgage, insurance will be required.

The decisions by major insurers to leave California and Florida has opened the door for companies in those states and elsewhere to up the ante. One Miami owner reports his premiums are more than double his property taxes because of the cost of windstorm coverage.

The Insurance Information Institute tells me the average home insurance premium has increased 11% year-over-year in 2022 to $1,700 annually. Florida owners have experienced the highest one-year average increase: 42% to $6,000 a year.

BEWARE THE OMNIPOTENT HOA

Homeowners association dues are often forgotten until the first bill arrives. This cost is unavoidable as well. You have to pay whether or not you use the pool, play golf, or hang out in the clubhouse, And because their costs are

principal means by which state and local jurisdictions pay for the services they provide their citizens, accounting for more than a third of their total receipts. Some $174 billion in taxes were paid by property owners in the first quarter, nearly twice the 15-year average, the Census Bureau reports.

Over the previous four quarters, moreover, tax growth has accelerated substantially in each quarter, quadrupling since the first quarter of 2022. Property tax revenue is catching up to home values

rising, just like everybody else’s, they are continually marching upwards.

Almost a third of all housing is in properties governed by homeowners or community associations, and more than three-quarters of all new construction is under the auspices of associations, the Foundation for Community Association Research reports.

While there’s no specific data on dues, about a third pay between $100 and $300 a month. And as with everything else, dues are increasing. Two-thirds

NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | OCTOBER 2023 | 11

One Miami owner reports insurance premiums are more than double his property taxes because of the cost of windstorm coverage.

of associations report increasing their assessments in 2022, and 84 percent expect to increase assessments in 2024 to keep up with rising costs.

If dues don’t keep up, the property could go downhill. Dues in my small neighborhood have never, ever been raised. And now we can’t afford to repair the community basketball court or fix and powerwash the entryway fencing. A big jump in dues is in the offing.

Then there’s the cost of utilities, which varies depending on your location, age, and size of the property and the number of occupants. According to figures developed by the NAHB from Census Bureau data, fuel runs about $2,500 a year while water and trash costs $845. And that was in 2021.

Move.org, a site that matches people to household moving outfits, has far more detailed and up-to-date monthly numbers: $117 a month for electricity, $45 for water, $62 for natural gas, $66 for sewer, $60 for the Internet, $48 for streaming services, $114 for mobile phone service and anywhere from $25 to $100 for trash. That is a total of at least

$537 for everything on the list. Improvements are a discretionary decision, but maintenance is necessary to keep your place in good working order. Maintenance costs vary widely, depending on your location. But more than half of the first-time buyers polled by U.S. News and World Report said they encountered

unexpected repairs after moving in.

Based on what Thumbtack considers 17 “essential” maintenance projects, the average cost nationally is $6.413. But they range from a low of $3,467 in Las Vegas to a high of $8,639 in Los Angeles That’s more than a $5,000 difference!

“What I find frustrating is how fast things like appliances fall apart and head for the dump,” warns a Tennessee homeowner. “If someone tells you the washing machine will last 10 years, don’t believe them.”

No doubt that owning a place is more costly than renting. But some buyers/ borrowers, especially those doing so for the very first time, come into it with a renter mentality. At the very least, they need to be forewarned of what lies ahead. n

Lew Sichelman is a contributing writer to National Mortgage Professional magazine. He has been covering the housing and mortgage sectors for 52 years. His syndicated column appears in major newspapers throughout the country.

THE MORTGAGE SCENE

12 | NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | OCTOBER 2023

Two costs often ignored by buyers are insurance and property taxes, likely because they are usually included as part of their monthly payments.

wemlo

Boca Raton, FL

Area of Focus: Loan Processing

Third-party processing service, wemlo, empowers mortgage professionals through transparent, flexible, and efficient loan processing. To better serve our customers and their borrowers, wemlo proudly offers processing support in 47 states (plus Washington DC) for more than a dozen loan products including Conventional, FHA, Jumbo, VA, and Non-QM.

wemlo.io

(866) 523-3876

info@wemlo.io

LICENSED IN: AL, AK, AZ, AR, CA, CO, CT, DC, DE, FL, GA, ID, IL, IN, IA, KS, KY, LA, ME, MD, MA, MI, MN, MS, MO, MT, NE, NV, NH, NJ, NM, NC, ND, OH, OK, OR, PA, RI, SC, SD, TN, TX, VT, VA, WA, WV, WI, WY

Zero 1 Solution LLC Stockton, CA

Area of Focus: Software

1Solution Mortgage allows you to Originate, price a loan scenario with proposal, CRM, Marketing and more …

• Scenario

• Communication CRM

• LOS

• Essentials

• Marketing

• HR 1smtg.com

(888) 458-0650

info@1smtg.com

LICENSED IN: All U.S. States, U.S. Virgin Islands

SPECIAL ADVERTISING SECTION ORIGINATOR TECH

SHOWCASE

NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | OCTOBER 2023 | 13

Acra Lending Lake Forest, CA

Acra Lending is the leader in NonQM Wholesale and Correspondent lending programs. Offering a range of programs and services geared toward helping mortgage professionals and borrowers achieve their purchase and investment goals. We are committed to providing simplicity, consistency and an optimal customer experience.

acralending.com

(888) 800-7661

sales@acralending.com

LICENSED IN: AL, AZ, AR, CA, CO, CT, DC, DE, FL, GA, ID, IL, IN, KS, KY, LA, ME, MD, MI, MN, MT, NE, NV, NH, NJ, NC, OK, OR, PA, SC, TN, TX, UT, VA, VT, WA, WI, WY

Champions Funding

Gilbert, AZ

Mission Driven Non-QM + CDFI Wholesale Lender

At Champions Funding, we Non-QM all day, every day! It’s our core business, and we live to serve underserved borrowers through our valued broker partners. We put diversity and inclusion into mortgage lending by empowering the mortgage broker community to provide solutions for non-traditional credit profiles and those who cannot get approved with standard financing. Through our highly coveted CDFI certification backed by the U.S. Department of the Treasury, we can offer our flagship neighborhood products and tap into a $1 Trillion market of historically underserved communities in the country.

Focused on speed to closing (in days, not weeks), smooth processes, and user-friendly access to our underwriting and support teams, we offer modern, flexible, and responsible non-traditional lending solutions.

champstpo.com

(949) 763-9494

Wholesale@ChampsTPO.com

LICENSED IN: AZ, CA, CO, CT, DC, FL, GA, HI, IL, IA, MD, MI, NJ, NC, OR, PA, SC, TN, TX, UT, VA, WA

Newfi Wholesale

Emeryville TX

DSCR, Bank Statement, 1099, Asset Depletion, Buydowns, Full Doc Non-QM

No one knows Non-QM like us. Newfi Wholesale is an exception-based Non-QM lender dedicated to helping brokers find success. We offer a full Non-QM product suite including: Full-Doc, Bank Statement, 1099, Asset Depletion, Interest Only, Non-QM ITIN, Non-QM Buydown, DSCR 1-4 & 5-8 Units, DSCR Condotels, Graduated Payment Mortgages, and more. At Newfi about 1/3 of our funded deals have exceptions that we make in-house!

newfiwholesale.com

(888) 415-1620

support@newfi.com

LICENSED IN: AL, AK, AZ, AR, CA, CO, CT, DC, DE, FL, GA, HI, ID, IL, IN, IA, KS, KY, LA, ME, MD, MI, MN, MS, MO, MT, NE, NV, NH, NJ, NM, NC, ND, OH, OK, OR, PA, RI, SC, SD, TN, TX, UT, WA, WV, WI, WY

PCV Murcor Pomona, CA

pcvmurcor.com

sales@pcvmurcor.com

(855) 819-2828

AREA OF FOCUS: Nationwide Real Estate Valuations Management — Appraisal Management Company

DESCRIPTION OF PRODUCTS OR SERVICES: Licensed in all 50 states, plus D.C., PCV Murcor provides nationwide appraisal management and valuation advisory for residential and commercial

real estate. An industry leader with over 40 years of experience managing valuation needs for mortgage lending, financial institutions, estate and litigation, real estate investors, and mortgage servicers.

NON-QM LENDER RESOURCE GUIDE

Find the full list of Non-QM Lenders on page 56 Find the full AMC list on page 57

14 | NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | OCTOBER 2023

AMC RESOURCE GUIDE

NMP’S MONTHLY SECTION OF HANDS-ON PRACTICAL ADVICE

BUILD A BROKER

Don’t Kill Your Career

YOUR FIRST MILLION DOLLARS

Smooth Communications

BENCHMARKS & BEST PRACTICES

Be A Money Mentor

CAREER TICKER

People On The Move

PEOPLE ON THE MOVE //

> Cenlar FSB, a New Jersey-based mortgage loan subservicer, announced that Gabe Rinaldi has joined the company as vice president of enterprise portfolio management.

> Dovenmuehle Mortgage Inc., an Illinois-based mortgage subservicing company, has hired Patricia McCarthy as its new vice president of insurance administration.

> Chicago-based Key Mortgage Services Inc. announced hiring Jason Brown as vice president, area sales manager, and the promotion of LaToya Spann-Martin as area sales manager and leader of the company’s new community impact and lending division.

HOWSPONSORED BY NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | OCTOBER 2023 | 15

BUILD-A-BROKER

Dumb Ways To Die

PEOPLE

BUILD-A-BROKER: HANDS ON PRACTICAL ADVICE

> Californiabased loanDepot announced that Melanie Graper has been named chief human resources officer.

> Home Orbit Lending announced that Matthew Valentine, a long-time resident of Raleigh, joined the team to help build the company’s brand in North Carolina.

> Black Knight Inc. announced that real estate industry veteran Lucie Fortier has been named executive vice president of the company’s MLS Solutions group.

> Jeremy Potter has been named to the new position of president at titleLook. Potter had previously been working as a strategic advisor.

ON THE MOVE //

16 | NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | OCTOBER 2023

One slip can ruin your career, so follow the right protocols

BY SARAH WOLAK, STAFF WRITER, NATIONAL MORTGAGE PROFESSIONAL MAGAZINE

BY SARAH WOLAK, STAFF WRITER, NATIONAL MORTGAGE PROFESSIONAL MAGAZINE

One of the world’s most popular — and probably catchiest — public service announcements is a singalong tune called “Dumb Ways to Die.” Originally created as a PSA by Metro Trains Melbourne in 2012 to promote rail safety, the song highlights various foolish ways one could meet their demise, such as sticking a fork in a toaster or standing too close to a train platform.

Funny enough, mortgage loan officers can learn from this jingle, too. Although the dumb ways to die may not directly apply to a typical mortgage loan officer, they themselves face a number of dumb missteps that could jeopardize their careers.

In certain areas, the saying “rules were meant to be broken” might hold some truth. However, this sentiment is far from applicable in the realm of mortgage loan officers. Some LOs think now that they’ve graduated from high school or college, skipping school is no longer an issue, but it’s just one dumb way for a career to die. And still, some LOs fail to comprehend that their future livelihoods depend on upholding regulations and avoiding those potential pitfalls that could stain their permanent records.

That’s of course why regulatory agencies and acts such as the Consumer Financial Protection Bureau’s (CFPB) regulations and the Real Estate Settlement Procedures Act (RESPA) — which prevents behaviors like undisclosed loan costs and kickbacks — are put in place. After all, loan officers are expected to exercise due diligence in their work — in and out of the office.

COMPLIANCE IS CRUCIAL

A surefire way to nip your career in the bud is to skip school. LaDonna Lockard, executive vice president for Utah-based Mortgage Educators & Compliance — a mortgage training, education and regulatory compliance provider — says that the start of 2023 kicked off with a huge compliance issue. “We’re still dealing with the repercussions of the REES (Real Estate Educational Services) Settlement,” Lockard said. “We saw a huge lawsuit where hundreds of MLOs all lied about their NMLS education. Basically, someone was checking off that these loan officers completed their education but they really didn’t take the annual courses.”

Lockard says that this sets off bells and whistles in the LO community, especially if the LOs who cheated attempt to re-establish their careers.

SPONSORED BY

> First Mortgage announced that Erich Cosio, a long-time Fort Worth resident, rejoined the company.

> Cenlar FSB, a New Jersey-based mortgage loan subservicer, has appointed Allison Batts as vice president of executive client management.

> Toorak Capital Partners, a capital provider to private lenders, announced that Scott Goldman has joined the company as head of asset management.

> KFS Mortgage Company has announced the hiring of Sabrina Johnson to its team as the new director of mortgage production.

NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | OCTOBER 2023 | 17

“Anyone willing to risk their licenses and livelihoods over eight hours of education … well, y’all probably shouldn’t be doing this anyways,” she said. “There were heavy repercussions, too. Anyone involved in it can no longer take online education between one and three years, depending on each state’s ruling. And several lost their licenses or got put on probation.”

It’s not the first time that the NMLS has cracked down on regulations, Lockard says. “They now have something called BioSig-ID, which is a biometric ID system that NMLS had to put into online courses because they found out that LOs were having others fill out their paperwork,” she explained. “A lot of reputations have been ruined [and] employers will be mindful of those enforcement actions, like what else are

you willing to cheat on or do?”

Anthony Johnson, partner and recently-appointed CEO at Mortgage Educators & Compliance, says that he is “constantly amazed” at the lengths LOs will go to in order to cheat on their education. “It’s in the law that they need eight hours of education, and people will try to send others in their place to complete that,” he said.

Lockard said that when it comes to being compliant, sharing is caring and no information is too much to provide your state NMLS. Lockard says that the concern she usually gets from clients is they feel they’re raising a red flag on themselves. But she tells them that it’s better to disclose than to be sorry. “I had one person who called [us] because they had filed for bankruptcy and kept their

license as an LO and claimed that they didn’t know to file [bankruptcy] with the state. And when it came time to renew their license, the state said no. I think the biggest thing that we’re going to see coming up is bankruptcies, foreclosures, and tax liens start to affect people’s licenses in that way. You should always keep the state up to date on any financial changes.”

>

HAVE A NEW HIRE OR PROMOTION TO SHARE? Submit the information to Keith Griffin at kgriffin@ambizmedia.com for possible publication. Announcements should include a headshot.

BUILD-A-BROKER: HANDS ON PRACTICAL ADVICE

BUILD-A-BROKER > Mortgage Capital Trading Inc., a mortgage capital markets technology company, announced the appointment of Steve Pawlowski as managing director, head of technology solutions. > Gateway Mortgage, a division of Gateway First Bank, announced the promotion of Mark Revard to division executive vice president/ national production manager.

CMG Home Loans, the retail division of CMG Financial, a privately held mortgage banking firm, has welcomed Area Sales Manager Michael Wise

PEOPLE ON THE MOVE //

“I don’t think an enforcement action is a scarlet letter forever. You can recover, but like any public mistake, you’re always going to have to explain it.”

18 | NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | OCTOBER 2023

> LaDonna Lockard, executive vice president, Mortgage Educators & Compliance

REPUTATION PRECEDES

Getting slapped with a formal discriminatory action will stay on an NMLS profile forever, Lockard says. “Your customers can see this information, whether you have an enforcement action or a cease and desist … it’s all on the NMLS Consumer Access page,” she said. “And even if the state pulls a license, [that person will] always have to disclose if they’ve ever had a professional license revoked if they apply for another professional license.”

Lockard says she’s also seen mortgage loan officers get their licenses pulled for issues that don’t have to do with the NMLS or RESPA. “I know an MLO who got their license taken for having two DUIs,” she

between their two separate roles, they can get slapped for that.”

MARKETING AND MONEY MISHAPS

Even though most LOs are eager to advertise their services, marketing and creating relationships are two areas where regulatory mistakes can occur, says Ari Karen, a litigation attorney. He has seen LOs attempt to bend rules to give their referral partners kickbacks. “A lot of people try to ‘get cute’ by skating around RESPA kickback rules,” Karen, a partner and head of litigation for labor and employment law firm Mitchell Sandler, based in Washington, D.C., explained. “It might work with your employer but it

into your personal sites, anything you say can affect you from a regulatory or professional standpoint and affect your relationship with your realtors or customers,” Karen explained. “You may alienate a whole group of borrowers.”

Karen says that another thing that LOs need to consider is how they leave their employers. “A lot of people can violate regulations when leaving their company for another. For example, if they start working for someone else while still holding a job with their initial employer,” Karen said. “They can’t download any borrower or loan information, and they can’t solicit employees.”

Karen says that careless LO practices tend to snowball into larger issues. Another job-related mistake Karen

said. “I don’t think an enforcement action is a scarlet letter forever. You can recover, but like any public mistake, you’re always going to have to explain it.”

Johnson says that having a regulatory action on your record is something that LOs will have to explain for the rest of their careers. “It’s going to stay with you. There’s not a time frame or process after [an action[ has been implemented where it will be removed,” Johnson said. “You have to face it … And it doesn’t look good if you have multiple marks on your license.”

Considering others’ reputations also has a role, especially when entering into partnerships or co-advertising opportunities, Lockard advised. “If you’re looking into partnerships, do your due diligence and investigate their reputation and how they follow the rules,” she said. “Advertising is another area that people get into a lot of trouble with. If an LO is co-advertising with someone who is a Realtor and there isn’t a firm delineation

isn’t going to fly with the CFPB. There’s also the idea of if other people do it, they can do it, too. Candidly, that will work for a lot of people … if everyone does it, everyone honestly won’t get caught. But what if you’re the ones who do?”

In August, the CFPB fined Freedom Mortgage $1.75 Million for illegal kickbacks. The CFPB said Freedom provided real estate agents and brokers with numerous incentives — including cash payments, paid subscription services, and catered parties — with the understanding they would refer prospective homebuyers to Freedom for mortgage loans.

Social media is another area where LOs can fudge up the boundaries of their contracts. Karen recommends separating business from pleasure, meaning that LOs should consider keeping their business content out of their personal content, and vice versa. “When you’re inviting business people intentionally

sees is LOs who quickly sign on with a company they really know nothing about. “Another [issue] is not carefully reading agreements. I see situations where an MLO will sign with a sign-on bonus of, say, $100,000 but the contract says if they leave even one day before the bonus is owed, they owe back that money. And of course, they don’t want to pay it, which creates more issues,” he said.

Another mistake? Chasing those big sign-on bonuses without checking the company’s culture or reputation. “They didn’t look at the pricing or beyond the bonus,” Karen said. “The same goes for when a lead-based LO goes to a retail space where it’s more relationship-based. Or if they’re working for companies that have issues with compliance. They’re usually not longterm players … they do really well for a bit and then go away. Having a longterm career view is important so it’s important to be cognizant of that.” n

SPONSORED BY

“There’s also the idea of if other people do it, they can do it, too. Candidly, that will work for a lot of people … if everyone does it, everyone honestly won’t get caught. But what if you’re the ones who do?”

NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | OCTOBER 2023 | 19

> Ari Karen, litigation attorney

Good Communication Is Never An Accident

BY HARVEY MACKAY, CONTRIBUTOR, NATIONAL MORTGAGE PROFESSIONAL MAGAZINE

Adoctor decided to put his overweight patient on an unconventional diet. He advised him, “Eat your regular meals for two days, then ‘skip’ a day. Do this for two weeks and come back to see me. I would expect you to lose at

Two weeks later, the patient returned for his appointment and surprised the doctor by losing

“You lost all that weight by following my instructions?” the doctor asked.

The man responded, “Yes, but I thought I was going to drop dead on the third day.”

“From hunger?” asked the doctor.

“No,” said the man.

“From skipping.”

Do you think the doctor rephrased the instructions for the next patient?

Avoiding misunderstandings is fundamental to a successful workplace, not to mention life in general. Getting along is largely dependent on your communication skills. If doing your job is important, you need to let people know what you’re doing, and you need to understand what they want from you.

USE YOUR EARS, NOT YOUR MOUTH

Curious though it may seem, effective communication starts with listening, not talking. Expressing yourself is vital, but understanding what others are telling you allows you to make your arguments more persuasive.

Warren Buffett, one of the world’s richest persons, famously said: “If you improve your

HARVEY MACKAY BUILD-A-BROKER: HANDS ON PRACTICAL ADVICE YOUR FIRST MILLION DOLLARS

20 | NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | OCTOBER 2023

If you are frequently misunderstood, run your remarks by an unbiased person

communication skills, I will guarantee you that you’ll earn 10% to 50% more money over your lifetime.”

It’s been said that a message sent is only as good as the receiver’s perception of it. Verbal communications tend to create confusion and misunderstanding for a

remarkably simple reason: the 500 most commonly used words in the English language have more than 14,000 definitions.

To make communication really work, we need to make sure the people we’re communicating with understand what we are saying as well as we do. Communication requires both effective sending and receiving. To avoid a breakdown in communication, break down your message so that everyone can understand it.

As tempting as it may be to use big words, or too many words, try to keep your messages as simple and direct as possible. Too much fancy language tends to confuse the listener/reader and dilute the message.

One of the best examples I can offer is Abraham Lincoln’s Gettysburg Address. At just 271 words, it is considered to be one of the greatest and most influential statements on the American national purpose. That speech wasn’t the main event of the day — it followed a two-hour, 13,000-word speech by Edward Everett. That speech was well received, but how many of us have read and remember Everett’s speech?

Include everyone in the same message rather than relying on another to share and interpret your intentions. Keeping everyone on the same page prevents misunderstandings and hurt feelings. If someone has questions or doesn’t understand what you are trying to accomplish, share that information too (without calling out the questioner.) Others may have the same concerns, so listen to the feedback and respond accordingly.

SHOW YOU CARE

Craft your message to fit the

occasion. Bullet points, timelines, committee assignments, goals — whatever makes the most sense to convey the information. Reread your communications before you send them. That extra step can help you find any confusing or unclear statements.

If you are frequently misunderstood, run your remarks by an unbiased person. If they have trouble comprehending your message, clear it up before you circulate it. Saving time and confusion works to everyone’s advantage.

In short, showing that you care about communication demonstrates respect for your co-workers who are serious about the project at hand. That’s what leaders do.

The Chinese sage Confucius was once asked about his views on the importance of good communication in getting things done.

“What,” asked his questioner, “is the first thing to be done if good work is to be accomplished?”

Confucius replied, “Getting the definitions right, using the right words.” Asked to elaborate, Confucius explained in effect that “when words are improperly applied, issues are misunderstood. When issues are misunderstood, the wrong plans are devised. When the wrong plans are devised, wrong commands are given. When wrong commands are given, the wrong work is performed. When the wrong work is performed, organizations fail. When organizations fail, people suffer.”

Mackay’s Moral: I know you believe you understand what you think I said, but I am not sure you realize that what you heard is not what I meant. n

SPONSORED BY

Harvey Mackay is a seven-time New York Times best-selling author with 15 books.

The 500 most commonly used words in the English language have more than 14,000 definitions.

NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | OCTOBER 2023 | 21

As tempting as it may be to use big words or too many words, try to keep your messages as simple and direct as possible.

Add A New Role To Your Job Description: Financial Literacy Mentor

Educating borrowers has potential to pay dividends down the road

We are living in the most connected era of human history. Nearly everyone has access to all the information they could ever want or need on the internet via smart phones or laptops. Despite this, there is still a significant need for greater financial literacy among today’s adults.

BENCHMARKS & BEST PRACTICES MARY KAY SCULLY BUILD-A-BROKER: HANDS ON PRACTICAL ADVICE

MARY KAY SCULLY, CONTRIBUTOR, NATIONAL MORTGAGE PROFESSIONAL MAGAZINE

22 | NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | OCTOBER 2023

Look at the P-Fin Index, for example. An annual barometer of financial literacy among U.S. adults, the index includes 28 questions that examine eight functional areas of financial knowledge, including borrowing and saving. The 2023 survey found that, on average, U.S. adults correctly answered only 48% of the study’s index questions and that Gen Z, followed by Gen Y (often referred to as millennials) performed worst, answering only 38% and 45% of questions correctly respectively.

With the average age of a first-time homebuyer falling squarely in the millennial age range, according to the National Association of REALTORS (NAR), loan officers have to be prepared to fill the gaps in their first-time home buyers’ financial knowledge.

WHY IT MATTERS

Greater financial literacy is, understandably, linked to greater financial well-being. In the 2023 P-Fin study, respondents with a very high level of financial literacy consistently had better financial well-being than respondents with a very low level of financial literacy. In fact, those with a very low level of financial literacy were found to be more than four times as likely to have difficulty making ends meet, nearly three times as likely to be debt constrained, and more than four times as likely to lack emergency savings sufficient to cover one month of living expenses. With greater financial literacy and greater financial well-being, homebuyers are better positioned for sustainable homeownership.

THE NEED FOR SMES

Buying a home is often the largest

financial decision of someone’s lifetime. First-time homebuyers, especially, need someone who is educated and confident and can support them through the homebuying journey. Some younger first-time buyers may lean on their parents or another trusted source, while others do not have that luxury.

borrowers, as well. Every borrower needs someone that can answer their questions and talk through decisions with them.

Spending so much money is daunting and borrowers want to be sure they are making the best financial decision. It’s important that no one assumes their borrowers are entering the mortgage process with all the knowledge they need. Even if they’ve bought a home before, they may still have gaps in their understanding of the mortgage process. It’s a critical skill to be able to assess the borrower’s financial knowledge and help to fill any gaps to ensure their homebuyers are fully educated about the process and the financial commitment they are making.

WHAT LOAN OFFICERS CAN — AND SHOULD — DO

Loan officers (LOs) can, and should, be the expert that buyers need. The loan origination process is more than just taking an application, it’s being a guide and a resource throughout the homebuying journey. LOs need to be able to educate buyers about all aspects of the mortgage process, including the different loan products available, expectations for down payments and closing costs, earnest money and escrow, credit scores and their impact, mortgage insurance, and the list could go on.

Homebuyer education courses and resources are a critical tool, but loan officers should be prepared to assist their

The time that LOs take to educate borrowers has potential to pay dividends down the road. By serving as a subject matter expert and trusted resource, LOs are not only helping the buyer make an informed financial decision, but they are building a relationship. If the buyer sees their LO as a valuable resource and financial mentor, they can be more likely to come back when they need additional loans or when it is time to buy another home. Additionally, borrowers that have a trusting relationship have greater potential to refer their friends or family who also need some additional education during the homebuying process.

LOs serve a critical role not just in getting borrowers into homes, but helping them make well-informed financial decisions during the process. Serving as a subject matter expert and trusted advisor can assist borrowers of all ages and financial backgrounds. According to Vince Shorb, the CEO of National Financial Educators Council (NFEC), “Most college graduates spend close to 16 years developing skills that will allow them to get a high-paying salary. However, these people typically spend little to no time learning how to save and invest their money.”

Financial comprehension is key for loan officers who want to succeed and see their borrowers do the same. And it’s a critical component of helping your homebuyers attain sustainable homeownership. n

SPONSORED BY

Mary Kay Scully is the Director of Customer Education at Enact, leading the development of the company’s customer education curriculum.

NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | OCTOBER 2023 | 23

Every borrower needs someone that can answer their questions and talk through decisions with them.

KNOW IT ALL. Way more than a magazine.

Stronger Stories

We discuss the issues in the industry others may be too wary to touch, and we never let advertise relationships affect our stories.

Hands-On Advice

Find actionable advice from professionals across the industry with tips to further your career, grow your business, and more.

Industry Insights

Don’t just read the news — understand it. Find insightful articles from leading industry voices to help digest all the changes in the

ACC Mortgage Rockville, MD

ACC Mortgage is the oldest NonQM lender that has never stopped lending in 22 years. We specialize in Bank Statement, ITIN, P&L, Foreign National and DSCR lending. Price, Product and Process are what make for Non-QM success.

ACCMortgage.com

LICENSED IN: AZ, AR, CA, CO, CT, DE, DC, FL, GA, ID, IL, IN, KS, MD, MI, NV, NJ, NC, OK, OR, PA, SC, TN, TX, UT, VA, WA

Newfi Wholesale Emeryville TX

DSCR, Bank Statement, 1099, Asset Depletion, Buydowns, Full Doc Non-QM

No one knows Non-QM like us. Newfi Wholesale is an exception-based Non-QM lender dedicated to helping brokers find success. We offer a full Non-QM product suite including: Full-Doc, Bank Statement, 1099, Asset Depletion, Interest Only, NonQM ITIN, Non-QM Buydown, DSCR 1-4 & 5-8 Units, DSCR Condotels, Graduated Payment Mortgages, and more. At Newfi about 1/3 of our funded deals have exceptions that we make in-house!

newfiwholesale.com

(888) 415-1620

support@newfi.com

LICENSED IN: AL, AK, AZ, AR, CA, CO, CT, DC, DE, FL, GA, HI, ID, IL, IN, IA, KS, KY, LA, ME, MD, MI, MN, MS, MO, MT, NE, NV, NH, NJ, NM, NC, ND, OH, OK, OR, PA, RI, SC, SD, TN, TX, UT, WA, WV, WI, WY

WHOLESALE LENDER RESOURCE GUIDE

nmplink.com/subscribe Find the full Wholesale Lenders list on page 57

Discover Where Your Competitors Stand In The Mortgage Market

Adapting to today’s dynamic mortgage market has changed the way we analyze trends and track competitors. Luckily, we have the tools you need to determine your competitors’ market share and see how individual loan originators are performing in their market.

Mortgage MarketShare Module

Our Mortgage MarketShare Module provides real-time market insights on all lenders, helping you easily benchmark your company’s market share, identify new and emerging markets, and measure your sales performance against your competition.

Loan Originator Module

Our Loan Originator Module provides you with access to the largest and most comprehensive loan originator database in the country. Take advantage of this access to identify top-producing loan officers, verify production, and monitor competitors.

GET A FREE MORTGAGE COMPETITOR ANALYSIS

To show you just how powerful our modules are, we’re offering a free customized mortgage competitor analysis. Simply visit www.thewarrengroup.com/competitor-analysis and provide us with a few details. You’ll receive an updated 2021 vs. 2022 Quarterly Mortgage MarketShare Report at the company level paired with a Loan Originator Report highlighting top LOs and individual performance.

Visit www.thewarrengroup.com to learn more today!

Questions? Call 617.896.5331 or email datasolutions@thewarrengroup.com.

BENEFITS

• Monitor Residential and Commercial Lending

• Measure Sales Performance and Market Activity

• Identify High-Performing Competitors

• Uncover Emerging Markets and New Opportunities

• Pinpoint Top Loan Officers for Recruitment

• Identify and Verify Loan Originator Performance

• Measure Loan Activity Against Competition

• Highlight Success for Market Positioning

NEED MORE DATA?

Inquire about our NMLS Data Licensing and LO Contact Database options.

Robots Can’t Relate Robots Can’t Relate

26 |

MAGAZINE | OCTOBER 2023

NATIONAL MORTGAGE PROFESSIONAL

Incorporating

BY SARAH WOLAK, STAFF WRITER, NATIONAL MORTGAGE PROFESSIONAL MAGAZINE

For some industry veterans, there’s nothing to worry about. “We’ll always need in-person mortgages,” says David Lykken, founder at Transformational Mortgage Solutions. For Lykken, ChatGPT is but an asset to the industry.

So it makes sense that companies like Big Purple Dot (BPD), a real estate CRM platform provider based out of Irvine, Calif., are integrating ChatGPT into its CRM ecosystem. The company is calling the collaboration “BPD AI assistant” and using it for conversational purposes between lenders and clients. According to the company’s CEO Roxana Davidoff, the integration features include natural language processing, accurate responses and queries, sales objections handling, and sales management to boot. Davidoff claims that this is the first phase in a series of updates to BPD’s CRM model.

“The way we’ve integrated [ChatGPT] is that we’ve allowed our clients — LOs and real estate agents — to use a conversational AI solution to leverage natural language processing to interact with their clients,” Davidoff asserts. “We’ve integrated [the AI] so that agents or loan officers can respond to the consumers’ inquiries in realtime. And what I mean by that is, anytime someone has a question or wants to reach out to a potential loan officer, our BPD AI will instantly respond back. It’s a quicker way to streamline communication.”

Davidoff says that right now is a golden era in artificial intelligence technology. “It’s pretty limitless as to what we can do with Open AI,” she said. “When you think about technology and where we are, I think

that it’s going to happen in a much quicker way and in a direction where things will be streamlined better and quicker that these manual tasks will go away. It all comes down to speed and efficiency.”

But others aren’t convinced, and even tech’s biggest moguls are finally agreeing that AI needs to slow down. At the tail end of March, over 1,000 tech bigwigs including Elon Musk and Steve Wozniak signed an open letter calling for a six-month pause on training AI systems more powerful than GPT-4 — also known as ChatGPT. Perhaps it’s pride or insecurity that’s prompting tech talking heads to take caution, but nevertheless, ChatGPT is a sense of contention in not only the tech world.

SKEPTICISM

SKEPTICISM

Steve Richman, a mortgage consultant, is a naysayer of the new wave of artificial intelligence infiltrating the industry, especially as ChatGPT has been tested to suggest loan products and attempt to write mortgages. “I still believe in face-to-face mortgages,” he said “I’m a big believer that you need to talk to people. And someone who is taking out a halfa-million-dollar loan isn’t looking to essentially push button and get a loan.”

Richman says that he’s seen demonstrations where borrowers can plug their parameters into ChatGPT and the bot will come out with loan products suitable for that consumer. “So that’s where people are concerned about getting jobs.

ChatGPT into mortgages is a friend or a foe has some originators concerned if artificial intelligence

To replace or not to replace, that is the question. At least that’s when it comes to whether Open AI’s ChatGPT is taking over the job market — particularly in the mortgage industry.

NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | OCTOBER 2023 | 27

And it probably won’t get rid of all jobs, but it will take away some,” he said. “It’s not there yet. We had automated underwriting and people thought it would get rid of underwriters, and though we didn’t lose all, we lost some [jobs].”

For Richman, his main concern is determining intellectual property. “When I write a blog post, I specifically write at the bottom that it was written by Steve Richman, not ChatGPT,” he said. “I also encourage LOs to constantly say that they don’t use ChatGPT to post or write [their] stuff. ChatGPT is great at helping people with the easy, generic stuff. But when it comes down to technicalities, it’s hard to trust it.”

It’s not to say that Richman is telling LOs to avoid the platform altogether — he just advises them to not risk being replaced by the intelligence application. “It’s great for marketing,” he said. “It’s amazing to ask it prompts such as the top 10 questions first-time homebuyers have. But make that prompt your own, provide your own answers instead of relying on ChatGPT.”

Richman also says ChatGPT’s red flag is that it puts people into boxes rather than distinctly remembering individual users. “For example, if you ask the bot to write a poem about your name, it’s going to give everyone with that same name the same response,” he explained. “It’s lacking personalization, which is why it’s on the individual LO to maybe revamp ChatGPT’s responses and gear them towards customers’ needs.”

Richman’s other worry is that the platform is untrustworthy. “When I plugged in a prompt as to how to attract first-time homebuyers, one of ChatGPT’s suggestions was to produce a blog featuring neighborhood statistics such as crime rates, schools, and income levels,” he said. “Well, those three things are illegal for a real estate agent to talk about. So be sure if you’re an LO who uses ChatGPT, don’t just hand over its responses to the public without fact-checking and putting your own spin on it. Not only do the responses sound not like

PRO-INNOVATION

PRO-INNOVATION

Richman’s concerns are formed by the news and popular media that he’s seen about AI. For instance, Richman said that his viewing of the recent film “M3GAN,” which depicts an artificially intelligent doll who develops self-awareness and becomes hostile, made him even more wary about society’s adoption of artificial intelligence. But for others, it’s simply a new way of life.

Lykken is one of the more positive industry vets when it comes to embracing ChatGPT’s innovation. “It will be a mistake if people do not embrace it and learn how to use it,” he affirmed. “It’s a decided advantage when working with Realtors, builders, and other industry folks. The amount of data ChatGPT provides can be a catalyst for other ideas.”

Lykken also says that in order for LOs to get the most value out of ChatGPT, they need to learn to ask the application the right questions to elicit the most fruitful responses.

“Learning to ask the right questions from ChatGPT is crucial. The data set that you can get back needs to be validated and verified and current,” he said. “Avoid using data from earlier years if you know that data has changed. I, for one, am using it constantly. The amount of data i can bring to clients is extraordinary.”

Although Lykken describes himself as proinnovation, especially when it comes to artificial intelligence, he also acknowledges that LOs shouldn’t be worried about being replaced in the near future. “The relational component between borrowers and LOs is something ChatGPT can’t take away, especially when it comes to a conversation and reading someone’s emotions,” Lykken said. “Robots can’t relate. [ChatGPT] can help you lay out the exact need of your consumer and help you reveal blind spots in an application … but it can’t replace communication.” n

you at all, but they could get you in trouble.”

and help you reveal blind spots in an application … but it can’t replace communication.’ ”

> David Lykken, Transformational Mortgage Solutions

the exact need of your consumer

28 | NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | OCTOBER 2023

“ChatGPT ‘can help you lay out

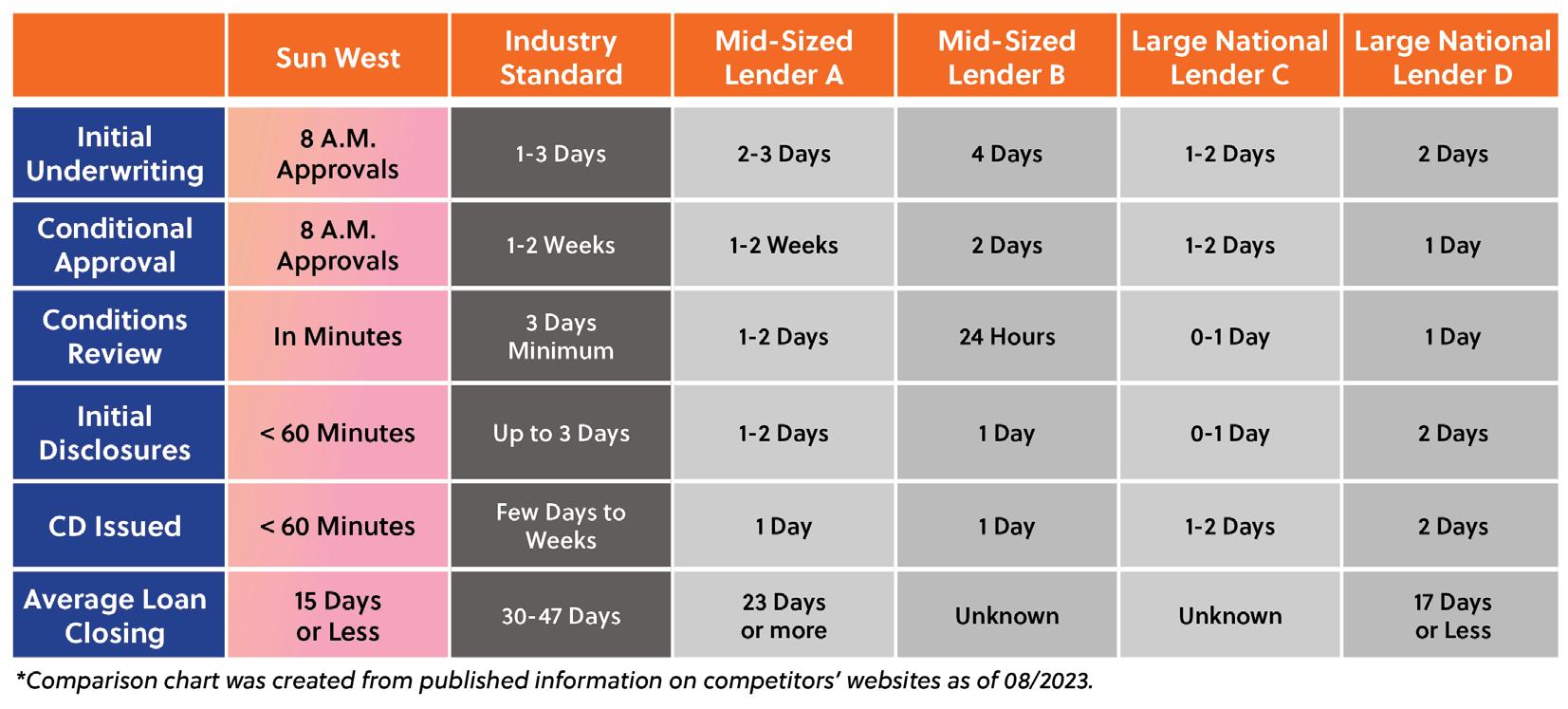

Speed, Reliability, 100% Trusted* No Overlays High Quality Delivered to Customers and Freddie/Fannie (GSEs) No Repurchase Fear and Love Your GSE

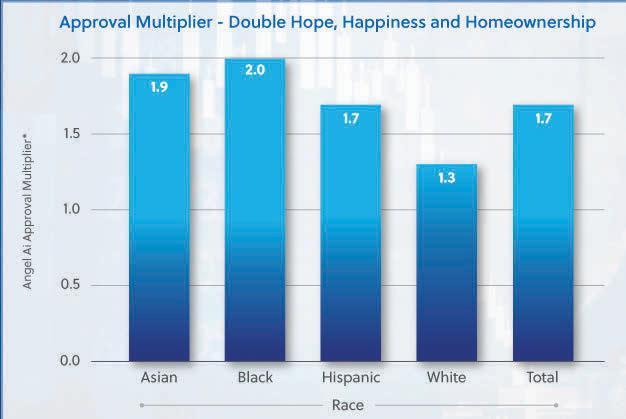

Angel Ai is the engine under the hood of Sun West Mortgage. Our matchless Ai speed and quality is why we are loved by the GSEs and our customers. We are so far ahead of the industry, just look at this side-by-side comparison with other popular lenders.

Swift. Accurate. Brilliant: Discover the Angel Ai Advantage

• 2x Approval Multiplier1 for the Black community and 1.7 times Approval Multiplier across all loans

• FICOS as low as 500; Yes to No Credit Score/ Alt Credit

• Manual Underwriting Allowed

• NO Overlays

• Approvals in Hours. No later than 8 A.M. Next Morning

• Conditions Reviewed in Minutes

• Free Ai Loan Processing completed in under an hour

• Touchless Ai Closings in 15 Days or less. Just deliver the last condition and the CD is auto-balanced and the docs are out.

• Free 100% Trusted* TRU Approvals in hours. Make no loan contingency offers!

• Angel Ai answers your most complex scenarios in minutes and Sun West stands behind Angel Ai 100%.*

• No need to buy scenario questions and TRU Approvals with points.

Competition? What Competition?

Sun West is light years ahead of these other lenders.

1Approval Multiplier

(Sun West decline rates) *When the loan application is submitted to Sun West, Sun West will honor the guidance and decisions that Angel Ai gives during the loan origination process, provided that the information provided is complete, accurate, and the terms of the transaction and the borrower’s financial and credit profile does not change from what was provided. Certain conditions apply, contact us for more information. For licensed mortgage professionals only; not for consumers. For licensing information, go to: www.nmlsconsumeraccess.org (NMLS 3277). Sun West Mortgage Company, Inc. (NMLS ID 3277) in California holds a Financing Law License (#6030119) [Loans made or arranged pursuant to a California Financing Law license], licensed by the California Department of Financial Protection and Innovation, Phone: (866) ASK-CORP, has a DRE Real Estate Corporation License Endorsement (#00793885), licensed by the California Department of Real Estate, Phone: (877) 373-4542. Georgia Residential Mortgage Licensee. Massachusetts Lender License # ML3277. Approval Multiplier is the ratio of national decline rates according to the Urban Institute to Sun West decline rates. Scan the QR Code Now to See More Comparisons! Plus, guess who the other lenders are and win a gift box. Visit swmc.com/comp Nothing Is Beyond ReachTM AngelAi.com

is the ratio of (national decline rates according to the Urban Institute) to

You’re More Than Your Production

Practical advice for LOs looking to change employers — even in a down market

30 | NATIONAL

PROFESSIONAL MAGAZINE | OCTOBER 2023

MORTGAGE

BY SARAH WOLAK, STAFF WRITER, NATIONAL MORTGAGE PROFESSIONAL MAGAZINE

Standing out in a sea of applicants can be a daunting task, but with the right approach and mindset, it’s possible to make yourself an attractive candidate to any job hiring manager. Especially on the cusp of a new job opportunity, it can be intimidating for loan officers — whether they’re industry veterans or newcomers — to make themselves stand out beyond their production numbers. And in a time where production is down overall and job applications are a survival of the fittest feat, loan officers need to market themselves beyond their production.

Companies always look at production first. It’s a given, tangible piece of information that immediately tells the job recruiter or hiring manager what the loan officer has done and what monetary value they can bring to the job. “Numbers don’t lie,” said Jordan Bernbaum, a senior loan officer and recruiter for Arizona-based NEXA Mortgage. “But LOs have to think of job recruitment like doing a college entry application. If production is your GPA, then we look at how you communicate, or anything extra you bring to the table.”

Bernbaum says that like a college application, there are many ways to make yourself stand out that don’t necessarily have to do with production. “[There are] LOs [at NEXA] like Renato Rodic who brought the MLO box suite of programs that runs some of our internal systems, and Josh Pitts who runs Shred Media. If you’re not doing anything like them, then don’t worry. I’m the digital nomad LO traveling the world. Others are great at support or are Non-QM gurus. There are so many ways to stand out,”

Bernbaum said.

And Bernbaum reiterated that standing out is crucial in a sluggish market. And it can involve LOs taking themselves out of their comfort zones. “Branching out in a down market is key. I’ve seen LOs learn new loan products that more closely align with their focus areas, such as DSCR. Some LOs have gone into the insurance game on the side,” he said. “[And even] upping their social media presence. There are so many ways to go when the market is down, and you find yourself with more idle time to accomplish that.”

SELLING YOURSELF

Since Bernbaum is both a loan officer and recruiter, he understands what recruiters are looking for and just how loan officers can execute that vision. “If I can add anything to what I’ve already said, it would be [for LOs] to keep at it and treat this business with care and professionalism. I think any recruiter’s biggest fear is that the person they bring on is someone who isn’t going to reflect well on them,” he said. “You don’t want to see the person you brought on board alienate half the company’s target market on their Facebook profile, while [your company’s] logo is prominently displayed.”

For others who have been in the business for decades, it’s a no-brainer as to how to market themselves. For Jonny Fowler, he’s taken his knowledge of knowing what makes an LO marketable and applied it to his own coaching company, Jonny Fowler Media. Fowler has worked as a corporate development manager for NRL Mortgage and as a senior vice president for Hancock

“An LO has the responsibility to determine what they want to do and what being a loan officer means to them.”

NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | OCTOBER 2023 | 31

> Jonny Fowler, founder, Jonny Fowler Media

Mortgage Partners in the past, among several other positions in his 29 years in the mortgage industry. He’s even done recruiting. So Fowler understands that at the end of the day, production is important — but it’s certainly not the end-all of being a loan officer.

“People who have an understanding of markets recognize that after 2022, your production had little to do with you and more about the market,” Fowler said. “LOs come and go, but the ones that come in when refinances are good and purchases are good don’t know how to pivot when the market changes. People who don’t let the down market get to them will always succeed.”

Fowler says that as a coach, the biggest issue that he deals with is getting clients out of their own heads and having a negative mindset. “I can’t handle when a client is constantly negative about the marketplace,” he said. “To those clients, I challenge them to figure out what they like, what they don’t like, and their attributes. Turnover and attrition are horrible for any business, and an LO has the responsibility to determine what they want to do and what being a loan

is in an inverse relationship with the company, too. Fowler says that companies are often irresponsible when it comes to taking care of their loan officers. “Many clients of mine experience the island effect where it feels like they were stranded to learn everything on their own,” Fowler explained. “In my 29 years, I know that if you make it easy on a LO to bring in business, they have the ability and potential to bring in as much business as you can handle. If you make it difficult, they will only bring in as much business as they can bear the pain. And in order to make it easy, it’s a collaborative effort. LOAs and

someone truly wants to help themselves they will make time,” he said.

BEING VALUABLE

Michael Hammond, president and founder of NexLevel Advisors, is a fellow coach and marketer in the industry. Hammond, like Fowler, is active in coaching LOs who want to market themselves as more than a number. “The number one mistake that a lot of LOs make as the market is shifting, whether they’re new or old [to the business], is focusing too much on their reviews and being all about themselves,” Hammond said. “They need to focus on what value they can bring to borrowers. And how they can do that is by telling anecdotes about how they helped people and showing that they’re relatable.”

officer means to them.”