FROM BOARDROOM TO BATTLEGROUND Kevin DeLory’s Unyielding Fight Against Cancer And Corporate Challenges A PUBLICATION OF AMERICAN BUSINESS MEDIA Vol. 16, Issue 6 $20.00 JUNE 2024 INSIDE: 2024 PRISM AWARDS FROM CHEESE TO KEYS Trip Topken III’s Unlikely Origin Story RATES DROP, RISKS RISE Mortgage Industry Braces For EPO Dilemma > Kevin DeLory, partner and chief TPO lending officer, Equity Prime Mortgage (EPM) MORTGAGE MAVERICKS MAKE REALITY TV MAGIC Inside Fairway’s Docuseries That Blends Family, Finance, And Film

FROM BOARDROOM TO BATTLEGROUND Kevin DeLory’s Unyielding Fight Against Cancer And Corporate Challenges A PUBLICATION OF AMERICAN BUSINESS MEDIA Vol. 16, Issue 6 $20.00 JUNE 2024 INSIDE: 2024 PRISM AWARDS FROM CHEESE TO KEYS Trip Topken III’s Unlikely Origin Story RATES DROP, RISKS RISE Mortgage Industry Braces For EPO Dilemma > Kevin DeLory, partner and chief TPO lending officer, Equity Prime Mortgage (EPM) MORTGAGE MAVERICKS MAKE REALITY TV MAGIC Inside Fairway’s Docuseries That Blends Family, Finance, And Film

Easiest P&L in the Industry

9 out of 10 Approved

Average App to CTC in 22 Business Days

Simple Guidelines

Lending in All 50 States

Join Now 800.400.5451 fnba.com/wholesale Providing Certainty in an Uncertain Market

> Despite battling two cancer diagnoses, Kevin DeLory refuses to step back from his leadership role at Equity Prime Mortgage, stating that work is his energy source and what heals him. CONTENTS

STORY PAGE 64

CANCER CAN’T STOP KEVIN

Overcoming two cancer diagnoses and a lifetime of challenges, DeLory drives Equity Prime Mortgage’s wholesale division to new heights with unmatched determination and resilience.

COVER

NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024 | 3

mortgage lenders for diversity, inclusion, and addressing the unique challenges faced by the LGBTQ+ community in

2024 PRISM AWARDS

Refi-Ready or Not, Here Comes the Cash Wave

Uncovering the surprising career paths that lead to the mortgage industry.

Defense Against Rejection Inside the glass house, loan officers need resilience as they navigate rejection in real estate dynamics.

Breakers Dealing with co-workers who toe the line.

As mortgage rates flirt with the 5.875% mark, industry leaders gear up for a potential $4 trillion refi surge.

on the

who the movers and shakers are in the mortgage industry.

the fascinating origins of sliced bread and other revolutionary inventions that remind us of the power of perseverance.

Benchmarks and Best Practices: Find Your Purpose, Fuel Your Passion Discover how reflecting on your purpose can reignite your passion and elevate your impact in the mortgage industry.

My Best Deal: From Co-op Woe To Two-Family Glow Transformed from co-op rejection to two-family joy, clients find $340K dream home solution.

As mortgage rates fluctuate, brokers face escalating conflicts over Early Pay Off (EPO) penalties, sparking debates and backroom deals.

6

And Now for Something Completely Mortgage

8

10 Boundary

14

Playing

19 People

20

To Smartphones

23 Originator Tech Resource Guide Wholesale

Resource Guide 24

Move See

Your First Million Dollars: From Sliced Bread

Discover

Lender

26 Non-QM Resource Guide AMC Resource Guide

28

30 Mortgage Meteorolgy

32

Report

Mortgage Market Maelstrom

nationalmortgageprofessional.com

CONTENTS

4 | NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024

40 Behind The Mortgage Lens

Behind the scenes of L.O.

Confidential: A Season on the Street, where mortgage mavens take the spotlight in a groundbreaking series.

50 Title Trouble: Government Proposals Risk Mortgage Market Stability

Navigating uncharted waters with title waivers and alternative insurance products.

56 A Cheesy Journey To Mortgage Mastery

Peter ‘Trip’ Topken III’s path from cheese mishap to NEXA mortgage success.

STAFF

Vincent M. Valvo CEO, PUBLISHER, EDITOR-IN-CHIEF

Beverly Bolnick ASSOCIATE PUBLISHER

Erica Drzewiecki, Katie Jensen, Ryan Kingsley, Sarah Wolak STAFF WRITERS

Dave Hershman, Erica LaCentra, Harvey Mackay, Lew Sichelman, Mary Kay Scully CONTRIBUTING WRITERS

Nicole Coughlin ADVERTISING ASSOCIATE

Alison Valvo

DIRECTOR OF STRATEGIC GROWTH

Julie Carmichael PROJECT MANAGER

Meghan Hogan DESIGN MANAGER

Stacy Murray, Christopher Wallace GRAPHIC DESIGN MANAGERS

Navindra Persaud DIRECTOR OF EVENTS

William Valvo UX DESIGN DIRECTOR

Andrew Berman

HEAD OF CUSTOMER OUTREACH AND ENGAGEMENT

Krystina Coffey, Matthew Mullins MULTIMEDIA SPECIALIST

Alan Nero MEDIA SPECIALIST

Melissa Pianin

MARKETING & EVENTS ASSOCIATE

Kristie Woods-Lindig ONLINE ENGAGEMENT SPECIALIST

Joel Berman FOUNDING PUBLISHER

Lydia Griffin MARKETING INTERN

82 Non-QM Lender Directory 83 Wholesale Lender Directory Originator Tech Directory AMC Directory 84 Facebook

Puns, Paradoxes, And Pandemonium!

Thoughts:

JUNE 2024 Volume 16 Issue 6 NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024 | 5

And Now For Something Completely Different …

For those with a penchant towards quirky British humor, the headline of this piece should be very familiar. It was a signature line in Monty Python’s Flying Circus when the show wanted to cut from one particular sketch into another that was, well, completely different. You might be watching a sketch about someone trying to return a dead parrot, and suddenly find yourself watching grown men strutting ludicrously as part of the Ministry of Silly Walks.

The fans of the show have made the phrase something of a meme, even long before “memes” were a thing. In life, it’s a turn of phrase that literally means suddenly having to cope with something unexpected (not unlike how “No One Expect The Spanish Inquisition!”) or, of course, completely different.

Our writers keep finding stories like these. This is an industry that is all but built on the notion. Who, after all, grows up thinking, “I want to work in mortgages!” except perhaps the children of successful brokers. No, more often it’s someone

who was on a much different path, who stepped into this industry as a side gig, or by accident, or just to fill in between other jobs. And then, they stayed and found a place to build a career. So, for the next few issues, you’ll see some of these stories — the music producer who was lured by the industry’s siren song, the youth pastor who found the calling to teach mortgage pros how to better serve clients, the son of Indian immigrants who followed his parents into mortgage finance but augmented it with his own love of technology. In these stories, we find empathy, education and enlightenment about what drives the best in the business, so that it can drive us, too.

Of course, not all surprises are centered on the job itself. In this issue, we talk to Kevin DeLory, an executive at Equity Prime Mortgage, whose brush with cancer forced his priorities to pivot and which gave him a tighter perspective on what’s important in leadership. It’s also the story of how having colleagues and friends who are there for you can make all the difference. Just like, say, the folks who were the creative team of Monty Python’s Flying Circus.

And now for something completely different …

VINCENT M. VALVO Publisher, Editor-in-Chief

Submit your news to: editors@ambizmedia.com

If you would like additional copies of National Mortgage Professional, call (860) 719-1991 or email subscriptions@ambizmedia.com www.ambizmedia.com

© 2024 American Business Media LLC. All rights reserved. National Mortgage Professional magazine is a trademark of American Business Media LLC. No part of this publication may be reproduced in any form or by any means, electronic or mechanical, including photocopying, recording, or by any information storage and retrieval system, without written permission from the publisher. Advertising, editorial and production inquiries should be directed to: American Business Media LLC, 88 Hopmeadow St., Simsbury, CT 06089, Phone: (860) 719-1991, info@ambizmedia.com

LETTER FROM THE PUBLISHER 6 | NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024

Taking It Personal Dealing with rejection

is tough. You have to be, too.

BY DAVE HERSHMAN, CONTRIBUTING WRITER, NATIONAL MORTGAGE PROFESSIONAL MAGAZINE

There is no doubt that being inside a real estate office will put a loan officer in touch with a plethora of opportunities. However, these opportunities come with many costs. One of the most significant costs is the personalization of rejection.

A salesperson’s ability to recover from rejection is one of the most salient traits of success. There are many ways an originator might experience rejection — including unreturned phone calls, refusal of meeting requests, and, of course, losing a loan because of myriad reasons. When a milliondollar refinance walks two days before settlement, the typical loan officer suffers from an awful feeling in the pit of their stomach.

When you are a “street” loan officer, rejection from real estate agents is not unusual. Many already have relationships and they will use just about any statement to ward off inquiries. My personal favorite is: “I am a listing agent, so you don’t need to call on me.”

What is laughable about this statement is that listing agents tend to be top producers. Which means that they transact more sales than the average agent. When

they sell a listing for someone who is going to purchase another house, do you think they tell them to go find another agent? They might assign that task to a member of their team, but it is still their client. However, it is an easy way to get rid of most loan officers. And the loan officer’s research should have told them that they were a listing agent before they ever approached the agent. This is why I advise loan officers to reply to this question with this statement: “That is why I am interested in working with you. I specialize in helping listing agents find more listings, sell them more quickly and turn them into lead machines.”

A SLAP IN THE FACE

Now back to serving a real estate office from the inside. What is so different about rejection in this situation? It is more up close and personal. Imagine

DAVE HERSHMAN 8 | NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024 RECRUITING, TRAINING, AND MENTORING CORNER

A salesperson’s ability to recover from rejection is one of the most salient traits of success.

working in the office and a top agent arrives with a sales contract in hand and their favorite loan officer is financing the deal. What’s more, the deal is closing in two days and thus the loan officer can’t even offer a second opinion.

Obviously, the loan officer never heard about the sale until now. One hour later, they are in an office lunch or sales meeting with that agent — exchanging pleasantries. Sure, the loan officer would like to stand up and say something like, “What’s the deal?” (that is the clean version).

But they can’t. Taking an antagonistic approach is not going to help them develop a relationship with the agent and a confrontation in front of the office would be devastating. But you can see how more “up-front and personal” this rejection is than what might be experienced by a street, remote, or bank loan officer.

Instead, they must suck it up and congratulate

the agent. Going a step further, they should also offer their help if any is needed, and they should not forget to ask if the agent has any other prospects they are working with. Asking for a referral when the agent is feeling a bit guilty is not a bad approach.

The bottom line is that the more opportunities an officer presents, the greater the opportunity for rejection. Any loan officer who does not ask for the business does not witness as much rejection. But in the case of being inside the glass house, you can’t have a glass ego. n

Dave Hershman is the top author in this industry with six books published as well as the founder of the OriginationPro Marketing System and the OriginationPro’s on-line comprehensive mortgage school. His site is www.OriginationPro.com and he can be reached at dave@hershmangroup.com

NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024 | 9

ERICA LACENTRA

Mind Your Toes

Tips for handling coworkers who overstep their boundaries

BY ERICA LACENTRA, CONTRIBUTING WRITER, NATIONAL MORTGAGE PROFESSIONAL MAGAZINE

When it comes to having a well-functioning workplace, it is critical that team members and co-workers have a certain level of trust and respect for one another. However, it’s likely that at some point in your career, you will encounter a co-worker who seems to constantly overstep their boundaries. They may try to oversee tasks that fall outside their wheelhouse, take over projects in an attempt to get the credit and glory, or give you or other colleagues orders even if they don’t manage you directly.

While it can be an unfortunate annoyance if it’s happening on a one-off basis, it can be downright disruptive and counter-productive for you and your business if it is a frequent occurrence. When you identify a co-worker who is pushing the boundaries of their role, it can be important to address it headon before it becomes a bigger problem. So, if you have a colleague who is really starting to step on your toes, what can you do to stop this behavior in its tracks?

ASSESS THE SITUATION

In a case like this when a coworker is crossing your boundaries or undermining your contributions, you will likely want to react immediately

to nip this behavior in the bud, however, it is important to take a step back and assess the situation as a whole before determining your next step.

First, you want to make sure you are approaching the situation rationally. Can it be extremely frustrating when your colleague oversteps or makes you look bad? Absolutely, but take a step back to settle your emotions and look at the scenario more pragmatically. Are you potentially misconstruing their behavior? Is this a one-off situation or has the coworker continuously displayed this behavior towards you? If it is the first time this has happened, you may likely be dealing with an over-eager colleague who didn’t realize what they were doing and did not mean any ill will towards you. In this scenario, a polite straightforward one-on-one conversation is best. Explain what actions they took or what behavior they displayed towards you that you felt crossed the line and give your colleague a bit of grace to be able to correct their actions.

Next, if you have identified that this is a recurring problem, you will want to look at each situation individually to determine if there are any common threads as to why this could be happening. Is this only happening with certain projects? Maybe your colleague is not pleased with the work you’ve been contributing and took things into their own hands, or maybe tight deadlines put extra pressure on your coworker where they felt the only solution was to take on more to get things done.

If you find your colleague is overstepping in most situations, it could also be a case where they are looking for more recognition, trying to establish more authority, or maybe they don’t feel like their ideas are being heard. Identifying when this

NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024 THE XX FACTOR

When you identify a co-worker who is pushing the boundaries of their role, it can be important to address it head-on before it becomes a bigger problem.

NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024 | 11

behavior is being displayed can be key to the strategy you want to take when speaking with your co-worker. You should always stick to the facts of the situation rather than tossing in assumptions to an already tricky conversation.

APPROACH WITH PROFESSIONALISM

You’ve analyzed the situation, you’ve gotten your facts together, and now comes the hard part, having a potentially difficult or uncomfortable conversation with your co-worker. It is important to approach this conversation with professionalism and tact so that things don’t wind up even worse. You want to go in with the mindset that you are working toward a solution that will make both of your working relationships in the future more positive.

than dictating an appropriate resolution(,?) will also make your colleague feel heard and they will be more likely to build towards a good path forward.

Once you have had that conversation with your colleague, you will likely want to clue your boss in on what’s happening. Your boss needs to be aware of any issues that are occurring between you and a colleague in case they pop up again and it will be good for them to know what the plan is for you both to have a positive working relationship going forward.

REINFORCE YOUR POINT AS NEEDED

Hopefully, the steps you have taken will remedy the situation and you will have a much more productive relationship with that colleague going forward. However, not every situation will be resolved after a single conversation. Be cognizant of how things are going post-conversation and leave the lines of communication open with that co-worker. Check-in in a friendly manner and if things start falling off or they start falling back into their old habits, don’t be afraid to speak up and remind your colleague of what you had previously talked about.

You should always stick to the facts of the situation rather than tossing in assumptions to an already tricky conversation.

You need to be ready to also hear your colleague’s perspective and take their feedback as well. Again, make sure your conversation sticks to the facts rather than your assumptions about the situation, state your thoughts, take in their input, and work towards a solution forward. Working together, rather

It’s okay to stand your ground and respectfully reinforce your point to avoid future issues. Having a colleague who repeatedly steps on your toes can be challenging to navigate, but with the right approach and willingness to work with that individual, you should be able to create a more harmonious professional relationship. n

Erica LaCentra is chief marketing officer for RCN Capital.

12 | NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024

*Complimentary registration available to NMLS-licensed active LOs and their support staff. Show producers reserve the right to determine final eligibility. NMLS Renewal class open to conference attendees only. Exclusive events and networking party are open to registered attendees only. The Mortgage Star Conference for Women returns to the beautiful historic Hotel Monteleone in the heart of the French Quarter of New Orleans. This event brings together the stars of mortgage, for meaningful discussions, insightful presentations, and to celebrate one another. Then, stay for the Ultimate Mortgage Expo, free for Mortgage Star attendees. Star Mortgage CONFERENCE FOR WOMEN — LIVE IN NEW ORLEANS — The most impactful event for mortgage women. Register for free with code NMPFREE mortgage-star.net JULY 10

Ready, Set, Refi?

Lenders prep for possible refi bonanza

BY LEW SICHELMAN, CONTRIBUTING WRITER, NATIONAL MORTGAGE PROFESSIONAL MAGAZINE

Alikely refinance boom is on the horizon. If rates drop much below, say, 6%, something like $4 trillion worth of mortgages will be refiable. The question is, will you be ready for the onslaught?

Mat Ishbia certainly intends to be. The chairman of United Wholesale Mortgage thinks a “monstrosity” of an opportunity is building, and he’s going to be ready, he said during a recent earnings call.

There’s already been a mini-boom of sorts. In February, Fannie Mae, Freddie Mac, and Ginnie Mae securitized more than $12.5 billion in refinanced loans. That’s up nearly 42.5% from January when rate-term refi volume increased 22% from December. And for the first week of March, the Mortgage Bankers Association reported that its refi index increased 12% from the week before and was 4% higher than a year ago.

But Ishbia believes a larger wave, perhaps even a tsunami, may soon be at hand. He doesn’t know how long the burst will last, maybe three months or maybe three years. “But I’m going to be ready, and we’re going to be ready at when nobody else is,” Ishibia said on the call. And when it does come, he said, “it’s going to be pretty big.”

The UWM chairman doesn’t know exactly at what rate the floodgates will open, either.

But he suggested that 5.875% could be the point at which the boom begins.

WHAT’S UP

Joe Garrett, one-half of the banking and mortgage consulting firm of Garrett, McAuley & Co., picked up on Ishbia’s remarks in a recent company newsletter and asked his readers, “Are you, or will you be, ready?” So I decided to ask around to see if folks are doing anything to be ready, and if so, what exactly are they doing to prepare?

“If a refi tide comes in, we’ll find out very quickly who is exposed.”

>Joe D’Urso, CEO, TitleEase

Plaza Home Mortgage co-President Jeff Leinan is not pinning his hopes on a surge in refis. Instead, the privatelyowned San Diego-based wholesale and correspondent lender is looking for “significant growth” in the purchase money sector, which Leinan calls the company’s “strong suit” given its broad array of loan options and its strong relationships with brokers.

“If rates drop to the mid-5s or lower, our industry will see a significantly larger purchase boom because affordability will improve and unlock lots of golden handcuffs that have been keeping sellers and

THE MORTGAGE SCENE LEW SICHELMAN 14 | NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024

and we’re going to be ready at UWM, when nobody else is.”

> Mat Ishbia, chairman, United Wholesale Mortgage on the potential refi ‘tsunami’ approaching.

NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024 | 15

inventory out of the market,” Leinan says. “There’s a lot of pent-up demand out there,” he adds, citing a recent study that found 89% of owners would consider a move within the next 12 months if rates dipped below 6%.

Not that Plaza is turning its nose up at refis. Far from it. But Leinan doesn’t believe the pool of anxious borrowers who are ready to jettison their higher-rate loans is as large as some prognosticators think. Only half of the 2023-vintage mortgages would be eligible to refi if rates dipped below 6%, he says.

By the MBA’s projections, that’s roughly $650 billion worth of loans that might be in the money. At 6% or lower, then, as many as 3.8 million borrowers would be eligible to refi. That’s a powerful lot of business. But the Plaza executive says he’s not confident they all will pull the trigger.

“About half that number were eligible in the past and didn’t refi. The question is why?” Leinan says. “Maybe their economic circumstances are an issue, or they have small balances and are close to paying off their loans. About a third of that number have had their loans over 15 years. But if they haven’t done it by now, what is the likelihood they will in the future?”

SERVICE AT THE READY

“We are ready,” says Toby Wells, president of Denver, Colorado-based Cornerstone Servicing, which

administers 60,000 or so mortgages.

As a division of Cornerstone Capital Bank and a third-party subservicer, the company always tries to keep its loan officers in front of its customers. And with the new data-based systems that are available today, it’s much easier to identify those seeking lower rates.

“It’s a lot different from the old days,” Wells told me. Cornerstone is still pushing leads to its loan officers, but now it’s in “a much better position” to evaluate those customers who would truly benefit. “We’re not just making annoying outbound calls to all our customers just because mortgage rates are lower,” he explains. “Rather, based on known credit information, income, and other data, we’re contacting customers who are likely to refinance.”

There are “numerous” new tools to help companies like Cornerstone evaluate their portfolios, says its president, and it is making use of a number of them.

With this obvious caveat — it all depends on how low mortgage rates decline — Ryan Hardiman, president of Middletown, R.I.-based Embrace Home Loans, believes the entire industry “should prepare” now to refi borrowers who purchased their homes between late 2022 and all of 2023.

Toward that end, Embrace, one of the largest full-service lenders in the country and licensed in all 50 states plus the District of Columbia, has developed a separate “manufacturing process” for fulfillment to

Insurance-Free Refis?

At this writing, details of Fannie Mae and Freddie Mac’s pilot programs to purchase “certain” refinance loans that do not come without title insurance are sketchy. But by now the experiment is well underway despite the loud protestations of the title business.

The “small scale, limited

duration” pilot is expected to cut closing costs by an average of $750 — but up to $1,500 — on loans where “there is confidence” there are no prior liens or encumbrances on the underlying properties. Only mortgages with 80% of lower loan-to-value ratios in “select” geographical areas need to apply. Of course, the GSEs will charge a

fee — an amount unknown at this time — to cover their risk.

The Federal Housing Finance Board has promised robust oversight. And well it should, says the American Land Title Association. Already at odds with attorney opinion letters, which Fannie Mae and Freddie Mac began accepting in lieu of title coverage

THE MORTGAGE SCENE

16 | NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024

support refinances. And Hardiman says he has “options to create capacity” without the need for hiring internally. That’s “something we believe will allow us to scale effectively when capacity needs to be expanded,” he says.

When rates do improve the Embrace leader is expecting borrowers with heavy debt loads to seek out cash-out refis. “With consumer debt at record highs and the cost of living putting an extra strain on finances,” he says, “we should see cash-out refinance opportunities for consumers to help alleviate these burdens.”

Currently, home equity lines of credit are a “very popular choice” among those with low-rate first mortgages who want to access their homes’ equity. As prime rates have risen, HELOCs have been less attractive, Hardiman says. “But they continue to be a good option for some homeowners looking for interest-only payments” and consumers should be more drawn to them as rates improve.

NO FLOOD WARNING

Still, Embrace doesn’t see a flood of refis on the horizon — or even a huge jump in purchase lending — largely because most owners are all but locked into lower rate loans, the so-called “lock-in” effect. Pointing to a recent Redfin report, Hardiman notes that 88.5 % of all homeowners have loans with rates less than 6 %, and 78.7 % of them have rates below 5 %. Consequently, he says, they’re not likely to

refi or sell and move up (or down).

Any rate below 6% will “seriously energize” borrowers who have loans with rates just 50 basis points higher, offers Larry Goldstone, president of capital markets and lending at BFI Financial Services. They’ll be drawn not just to rate-and-term refi, though. Lower rates, he says, should also “trigger a wave” of folks who have been waiting to take cash out of their appreciated houses or get out from under high-rate second mortgages.

Moreover, Goldstone doesn’t buy into the premise that borrowers with 3% mortgages will never give up their low-rate loans, prepay, or even sell and move to another joint. “Feeling ‘loan locked’ is a psychological problem that borrowers will get over if they wish to change where they live,” he told me. “I’ve seen this before. Most Americans are, by nature, on the move. If they take a new job in another state or simply want to move across town, they’ll trade down or trade up to do so.”

BSI, which originates and services and sub-services mortgages and sells mortgage loans to permanent investors. is “absolutely” preparing for when the market breaks loose from the doldrums. “We are planning to recruit loan officers and back-office support staff,” says Goldstone.

“We are already carrying excess staff capacity in anticipation of an increase in first mortgage lending. Our strategy includes focusing on self-service by providing a seamless experience for borrowers who submit

in 2022, ALTA argues that the test expands the government-sponsored enterprises’ authority beyond their mission and charters. It also puts the agencies in harm’s way.

“If title concerns arise under the pilot, mortgage companies would expect the GSEs to settle the issue, exposing lenders and taxpayers to greater risk,” says ALTA President

Diane Tomb. “The last time the GSEs engaged in significant risk-taking, they imploded the housing finance system and [the] American economy.”

Tomb also warns that if the pilot becomes standard operating procedure, it could decimate the title business, 90% of which is made up of small, local companies.

This winter, Fannie announced

the full-scale availability of a onestep validation process under its Desktop Underwriter program for borrower assets, income, and employment with a single report. The process began as a pilot originally launched in 2017. Just thought I’d mention that.

~ Lew Sichelman

NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024 | 17

applications online, which allows us to scale without adding staff. We also are sharpening our call center capabilities to allow us to quickly identify borrowers who are eligible to refinance to be routed to a loan officer for a conversation.”

The Irvine, Texas, company also is investing in technology and data analytics to allow it to produce more loans per employee. Internally, BFI’s data warehouse allows the company to segment borrowers into categories so it can present them with relevant offers for specific loan types. And it can stratify the data by the borrower’s rate, location, credit score, original LTV and estimates of current LTV. Externally, meanwhile, it employs software to identify the location of mortgage notes, recorded deeds of trust, and other key documents that help qualify borrowers “as seamlessly as possible.”

“If rates drop to the mid-5s or lower, our industry will see a significantly larger purchase boom because affordability will improve and unlock lots of golden handcuffs that have been keeping sellers and inventory out of the market.”

> Jeff Leinan, Co-President, Plaza Home Mortgage

“All of this information helps us better understand and serve our customers,” Goldstone told me.

Joe D’Urso is another who isn’t convinced a new refi wave is on the way, “At least not in regard to timing,” says the president and CEO of TitleEase, the Providence, R.I.-based national title services firm. But if it comes, he’s pretty sure the mortgage business can handle it.

TECH INITIATIVE

“While some players will probably not be ready,” D’Urso says, “the industry as a whole has done an excellent job of staffing up in prior years to meet extreme volumes and I believe it can do so again.”

How well individual players respond remains to be seen. But the TitleEase leader believes technology will be a key factor. And on that front, there’s a “long way to go,” he told me.

When loan volumes were soaring several years ago, most lenders and service providers were too busy

to make deep investments in process improvements and technology enhancements,” he says. “Even though there is generally less free cash to make those investments when volumes diminish, technology needs to be embraced now more than ever.”

As D’Urso sees it, if there is another wave, there will be the usual haves and have-nots. “The companies that have embraced technology to make their processes more efficient — as well as those that have broadened their offerings with ancillary business lines — will be the winners, while the others will be behind the eight ball and struggling just to tread water.”

On that score, he is reminded of the famous Warren Buffet quote about the insurance marke: “You only find out who is swimming naked when the tide goes out,” Buffet said. To which D’Urso adds, “If a refi tide comes in, we’ll find out very quickly who is exposed.” n

Lew Sichelman is a contributing writer to National Mortgage Professional magazine. He has been covering the housing and mortgage sectors for 52 years. His syndicated column appears in major newspapers throughout the country.

THE MORTGAGE SCENE 18 | NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024

HOW

> Xactus appointed Danielle Walker as senior vice president of business development. Previously, Walker served as the vice president of product development.

> Erin Dee took on a new position as Chief Operating Officer at InterLinc Mortgage.

> AnnieMac Home Mortgage welcomed Ian Aubourg as the newest addition to its leadership team, serving as Senior Vice President of Retail Sales.

> Equifax recently announced that Barbara Larson, former Chief Financial Officer for Workday, has been elected to its board of directors.

PEOPLE

MOVE //

ON THE

NMP’S MONTHLY SECTION OF HANDS-ON PRACTICAL ADVICE

FIRST MILLION DOLLARS

World

BEST PRACTICES

Industry

SPONSORED BY NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024 | 19

YOUR

How Persistence Shaped Our

BENCHMARKS &

Fueling Passion And Purpose In The Mortgage

CAREER TICKER People On The Move

PEOPLE ON THE MOVE // YOUR FIRST MILLION DOLLARS

Persistence … It’s Never Too Late

How to be the best thing since sliced bread

BY HARVEY MACKAY, SPECIAL TO NATIONAL MORTGAGE PROFESSIONAL MAGAZINE

We’ve all heard the expression “the greatest thing since sliced bread.” But how did sliced bread originate?

The Anecdote International website provides the story. In 1912, the son of a German immigrant had an idea: People might want to buy bread that was already sliced instead of having to cut it themselves. Otto Rohwedder was 32 when he had his brainstorm, and he spent five years developing the first commercial-grade machine for slicing bread. Instant success, right? Not exactly. Even

> Carrington Mortgage Services welcomed Steven Winokur as the vice president of marketing, third-party originations.

> Planet Home Lending has hired Paul Walker to be its Chief Financial Officer.

though his family and friends were sure it would be a big hit, it took Rohwedder 10 years to sell his first bread slicer.

The struggling Chillicothe Baking Company was the first company to purchase one. However, after using Rohwedder’s invention, sales rose 2,000 percent in a matter of months.

And once other companies saw how useful the bread slicing machine was, it began selling at a brisk pace. Soon every bakery wanted one. Sandwiches have never been the same.

DETERMINED TO WIN

Persistence and determination are what keep us hammering away. I don’t know any entrepreneurs who have achieved any level of success without those two traits. When you have a dream that you can’t let go of,

> Todd Lautzenheiser joined Newfi Lending as SVP, Correspondent Sales. Lautzenheiser will lead several account executives who have also joined Newfi Correspondent.

> Oklahomabased Gateway First Bank has appointed Jonathan Wallace as Chief Financial Officer.

HARVEY MACKAY

BUILD-A-BROKER: HANDS ON PRACTICAL ADVICE

20 | NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024

When you have a dream that you can’t let go of, trust your instincts and pursue it.

> Floridabased A&D Mortgage announced its appointment of Andrey Gunin as its new Chief Financial Officer.

> Rocket Companies announced Shawn Malhotra as its first-ever group Chief Technology Officer (CTO) and will oversee the development of technology across the entire Rocket Companies’ ecosystem. > City National Bank has hired Rick Bechtel as Executive Vice President of Mortgage & Residential Lending.

HAVE A NEW HIRE OR PROMOTION TO SHARE? Submit the information to editors@ambizmedia.com for possible publication. Announcements should include a headshot.

SPONSORED BY

NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024 | 21

trust your instincts and pursue it.

Author Malcolm Gladwell explained that it takes 10,000 hours of practice to become an expert in something. Ten thousand hours is roughly 5 years of full-time work at 2,000 hours per year. If you do it as a hobby for 10 hours a week, it will take you 20 years to get to expert level.

We won’t all become experts, but we can all keep hammering away until we can make it work.

Look at some of the great inventions of our time, such as the telephone. Alexander Graham Bell approached American communications company Western Union and offered them the rights to his patent for $100,000, but company bigwigs balked at the proposal citing the “obvious limitations of his device, which is hardly more than a toy.” Undeterred, Bell established the Bell Telephone Company in 1877 and less than a decade later, more than 150,000 people were the proud owners of telephones in the U.S.A.

What do you suppose Bell would say about the phone in your pocket now?

Television is another invention that took a long time to get going. In 1926, American radio pioneer Lee De Forest said television was a commercial and financial impossibility. Twenty years later, people were still not convinced. In 1946, film producer Darryl Zanuck said, “People will soon get tired of staring at a plywood box every night.”

According to estimates, there were 123.8 million TV homes in the United States for the 2022-2023 TV season. And the number of TV households continues to grow.

Personal computers were much the same. In 1949, one year after the world’s first stored program computer made its debut, a mathematician declared: “We have reached the limit of what is possible to achieve with computer technology.”

Even as the capabilities and functions of computers grew, there were naysayers like Ken Olson, founder of the computer company Digital Equipment Corp. who said in 1977 “there is no reason anyone would want a computer in their home.” Nearly 80 percent of all American households now own a computer.

As a business owner I am grateful that their

persistence paid off. I clearly remember the old-school methods of ordering, production, delivery, and followup. I’ll take our office computers any day.

We won’t all become experts, but we can all keep hammering away until we can make it work.

Cell phones also took a long time to catch on. My first cell phone from the 1980s was the size of a brick with a short-life battery. Even Motorola, who pioneered the cell phone, failed to see its potential in 1981. Now we are lost without our cell phones. Believe it or not, online shopping didn’t catch on for a long time either. In 1966, “Time Magazine” ran an article that claimed: “Remote shopping, while entirely feasible, will flop because women like to get out of the house, like to handle merchandise, like to be able to change their minds.”

Approximately 76 percent of U.S. adults now shop online, and annual retail e-commerce sales hit $5 trillion worldwide. Imagine surviving the pandemic without the convenience and selection available from the gazillion websites that we browse daily.

All because someone saw the value in reaching a broader audience and didn’t stop until they figured out how to do it.

As comedian Steve Martin said, “Thankfully, persistence is a great substitute for talent.”

Mackay’s Moral: Good things come to those who persist. n

Harvey Mackay is a seven-time New York Times best-selling author with 15 books.

YOUR FIRST MILLION DOLLARS BUILD-A-BROKER: HANDS ON PRACTICAL ADVICE

22 | NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024

ORIGINATOR TECH RESOURCE GUIDE

wemlo

Boca Raton, FL

Area of Focus: Loan Processing

Third-party processing service, wemlo, empowers mortgage professionals through transparent, flexible, and efficient loan processing. To better serve our customers and their borrowers, wemlo proudly offers processing support in 47 states (plus Washington DC) for more than a dozen loan products including Conventional, FHA, Jumbo, VA, and Non-QM.

wemlo.io (866) 523-3876 info@wemlo.io

Licensed In: AL, AK, AZ, AR, CA, CO, CT, DC, DE, FL, GA, ID, IL, IN, IA, KS, KY, LA, ME, MD, MA, MI, MN, MS, MO, MT, NE, NV, NH, NJ, NM, NC, ND, OH, OK, OR, PA, RI, SC, SD, TN, TX, VT, VA, WA, WV, WI, WY

Zero 1 Solution LLC

Stockton, CA

Area of Focus: Software

1Solution Mortgage allows you to Originate, price a loan scenario with proposal, CRM, Marketing and more …

• Scenario

• Communication

• CRM

• LOS

• Essentials

• Marketing

• HR

1smtg.com (888) 458-0650 info@1smtg.com

Licensed In: All U.S. States, U.S. Virgin Islands Find the full Originator Tech list on page 83

WHOLESALE LENDER RESOURCE GUIDE

ACC Mortgage Rockville, MD

ACC Mortgage is the oldest NonQM lender that has never stopped lending in 22 years. We specialize in Bank Statement, ITIN, P&L, Foreign National and DSCR lending. Price, Product and Process are what make for Non-QM success.

ACCMortgage.com

LICENSED IN: AZ, AR, CA, CO, CT, DE, DC, FL, GA, ID, IL, IN, KS, MD, MI, NV, NJ, NC, OK, OR, PA, SC, TN, TX, UT, VA, WA

Newfi Wholesale Emeryville CA

DSCR, Bank Statement, 1099, Asset Depletion, Buydowns, Full Doc Non-QM

No one knows Non-QM like us. Newfi Wholesale is an exception-based Non-QM lender dedicated to helping brokers find success. We offer a full Non-QM product suite including: Full-Doc, Bank Statement, 1099, Asset Depletion, Interest Only, Non-QM ITIN, Non-QM Buydown, DSCR 1-4 & 5-8 Units, DSCR Condotels, Graduated Payment Mortgages, and more. At Newfi about 1/3 of our funded deals have exceptions that we make in-house!

newfiwholesale.com (888) 415-1620 support@newfi.com

LICENSED IN: AL, AK, AZ, AR, CA, CO, CT, DC, DE, FL, GA, HI, ID, IL, IN, IA, KS, KY, LA, ME, MD, MI, MN, MS, MO, MT, NE, NV, NH, NJ, NM, NC, ND, OH, OK, OR, PA, RI, SC, SD, TN, TX, UT, WA, WV, WI, WY

KNOW IT ALL. Way more than a magazine.

Stronger Stories

We discuss the issues in the industry others may be too wary to touch, and we never let advertise relationships affect our stories.

Hands-On Advice

Find actionable advice from professionals across the industry with tips to further your career, grow your business, and more.

Industry Insights

Don’t just read the news — understand it. Find insightful articles from leading industry voices to help digest all the changes in the industry.

Find

on page

nmplink.com/newsletters NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024 | 23

the full Wholesale Lenders list

83

Find Your Purpose, Ignite Your Passion

Overcome the ‘passion gap’ to stand out

BY MARY KAY SCULLY, CONTRIBUTING WRITER, NATIONAL MORTGAGE PROFESSIONAL MAGAZINE

BY MARY KAY SCULLY, CONTRIBUTING WRITER, NATIONAL MORTGAGE PROFESSIONAL MAGAZINE

“P

urpose is the reason you journey. Passion is the fire that lights the way.” ~ Anonymous

I have loved this quote recently because it really makes me think. What am I doing and, most importantly, why am I doing it?

BEST PRACTICES MARY KAY SCULLY BUILD-A-BROKER: HANDS ON PRACTICAL ADVICE 24 | NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024

BENCHMARKS &

In this business, you may feel like a mere order taker for a 30-year fixed-rate mortgage. But while that may get you by, it’s not going to feel very fulfilling. It’s hard to wake up every morning excited for the work that lies ahead of you, but taking the time to reflect on your purpose in this industry — and the passion that got you here in the first place — not only helps you make progress professionally, but helps you better serve your borrowers.

PASSION AND PURPOSE

According to Deloitte, America’s workforce has a “passion gap.” Less than 12.3 percent of America’s workforce possesses the attributes of worker passion: questing, connecting, and commitment. Deloitte’s study states, “each of these attributes leads to behaviors that drive sustained performance improvement and help people integrate knowledge from professional networks and lessons from difficult challenges into a disciplined commitment toward making an increasing longer-term impact.” The more passionate workers are, the more they realize their own potential and contribute to the success of their company.

In the mortgage industry especially, with its cyclical nature, it can be challenging to feel passionate about your work despite all the ups and downs. However, I am here to remind you of why you should be passionate about the work you do.

WHAT YOU DO MATTERS

Simply put, this job matters. In the mortgage industry, we are part of the biggest financial decision most people will make in their lives. It’s more than just selling a product — you are playing a part in what often alters the course of a household’s financial future.

Homeownership is a key way to build generational wealth. And the difference it makes is significant. NAR reported that homeowners’ wealth is 40 times higher than that of renters. Especially now, as buyers are spending more of their income on homes than ever, we play a critical role in getting them into the right home on the right terms.

In the mortgage industry especially, with its cyclical nature, it can be challenging to feel passionate about your work despite all the ups and downs.

It’s no surprise America’s workforce is feeling this gap in passion. Some workers have been in the same position for a long time and are feeling tired or bored, while others are still struggling to keep up with rapid post-pandemic change. Because of this, Forbes has reported that many workers feel their burnout is even worse than during the pandemic.

If you’ve found yourself losing your passion, take the opportunity to remember the part you can play in the trajectory of someone’s financial future. Your purpose as a mortgage professional is to help borrowers achieve the dream of homeownership, and the difference you help make in your borrowers’ lives is worthy of your passion.

HOW TO TRULY HELP

Because your job has a significant impact on borrowers’ financial situations, it’s important to do everything you can to set them up for success.

SPONSORED BY

NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024 | 25

Less than 12.3 percent of America’s workforce possesses the attributes of worker passion: questing, connecting, and commitment.

Your purpose is more than taking an application and pushing borrowers along to close.

There are many opportunities during the homebuying process where you can help empower borrowers to be better homeowners. Invest in borrower education to help them make the best financial decisions for their situation. To go above and beyond, provide them with homeowner resources to help them understand how to take care of their purchase, build equity and get the most out of their investment.

Newfi Wholesale Emeryville, CA

newfiwholesale.com (888) 415-1620 support@newfi.com

Your purpose is important — and your passion leads the way. Passion fuels enthusiasm and, as Henry Banks said, “a salesman minus enthusiasm is just another clerk.” Remember the impact of your work, and you’ll be positioned to help borrowers and be the best resource you can be. n

Mary Kay Scully is the Director of Customer Education at Enact, leading the development of the company’s customer education curriculum.

DSCR, Bank Statement, 1099, Asset Depletion, Buydowns, Full Doc Non-QM

No one knows Non-QM like us. Newfi Wholesale is an exception-based Non-QM lender dedicated to helping brokers find success. We offer a full Non-QM product suite including: Full-Doc, Bank Statement, 1099, Asset Depletion, Interest Only, NonQM ITIN, Non-QM Buydown, DSCR 1-4 & 5-8

PCV Murcor Pomona, CA

pcvmurcor.com sales@pcvmurcor.com (855) 819-2828

AREA OF FOCUS: Nationwide Real Estate Valuations Management — An Appraisal Management Company

DESCRIPTION OF PRODUCTS OR SERVICES: Licensed in all 50 states, plus D.C., PCV Murcor provides nationwide appraisal management and valuation advisory for residential and commercial real estate. With a foundation built on 43 years

Units, DSCR Condotels, Graduated Payment Mortgages, and more. At Newfi about 1/3 of our funded deals have exceptions that we make in-house!

LICENSED IN: AL, AK, AZ, AR, CA, CO, CT, DC, DE, FL, GA, HI, ID, IL, IN, IA, KS, KY, LA, ME, MD, MI, MN, MS, MO, MT, NE, NV, NH, NJ, NM, NC, ND, OH, OK, OR, PA, RI, SC, SD, TN, TX, UT, WA, WV, WI, WY

of experience, PCV Murcor brings a deep understanding of our clients’ goals that complements appraisal modernization. Our use of state-of-the-art AI technology ensures precision and efficiency in every aspect of our service. Experience innovation-powered recision and timetested excellence with unparalleled service and cutting-edge products.

BUILD-A-BROKER: HANDS ON PRACTICAL ADVICE

BENCHMARKS & BEST PRACTICES

Find the full AMC list on page 82

Find the full AMC list on page 83

AMC RESOURCE GUIDE

26 | NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024

NON-QM LENDER RESOURCE GUIDE

YOUR CAREER IN HIGH GEAR

The face you know at the school you don’t.

Introducing Maximum Acceleration, your new, premier provider of continuing education.

We’re not just bringing you a lecture. We’re bringing you the fuel to spark your competitive fire, the plan to win the game on the merits, the confidence to know the rules and master them.

We’re Maximum Acceleration, and we’re where loan originators go to put their career in high gear.

— LaDonna Lockard, CEO

MAXCLASS.COM

Complimentary registration available to NMLS-licensed active LOs and their support staff. Show producers reserve the right to determine final eligibility. www.greatnorthwestexpo.com PRODUCED BY PORTLAND, OR Holiday Inn Portland South Wilsonville, OR Register for FREE with promo code NMPFREE JUN 18 Oregon’s largest gathering of mortgage pros. Innovate. Educate. Motivate.

From Co-Op Conundrum To Double Delight

Name: Irene Amato

How much was your best deal worth?

$340,000.

What made it your best deal?

This client approached us to purchase a two-bedroom co-op with her son. However, the co-op did not meet the qualification criteria due to a pro-rata share. Additionally, the cooperative development had taken out a second mortgage, resulting in a mortgage balance that exceeded the guidelines set by Fannie Mae and Freddie Mac. It was the co-op that got declined, not the client. I explained to the clients that this decision was for their protection, as the co-op was not financially sound with the additional debt. Throughout my entire career, I have never had a client, knock on wood, who lost a house and did not find a better situation.

I suggested to the mother, “Your son

Job Title: Owner Business: ASAP Mortgage

is handy. Why aren’t you considering a two-family house? You can find one with two three-bedroom apartments to rent out, which will help you cover expenses. Plus, you’ll have a yard.” Initially, the mother didn’t think they would qualify for such a property, as nobody had ever suggested it to her before. However, two months later, they successfully closed on a twofamily property.

What else was interesting about the deal?

Three months later, they expressed to me that they believed they would not have lasted in a co-op. With their new twofamily property, they enjoyed having a yard, the ability to have a dog, and the

convenience of a garage, eliminating the need to park outside. Overall, it was a significantly improved situation for them. n

Have a great story about your best deal? We’re not talking about your biggest deal. We want to hear about your best deal - the one that resonates with you personally, the one that became the story you’ve told again about why you’re in this business. Head over to https:// nmplink.com/bestdeal and tell us the details. You could win a $100 Amazon gift card if your story is selected for publication. WIN a $100 Amazon gift card!

NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024 | 29

Welcome to The Greatest Mortgage Conference In The Known Universe.

The Originator Connect Conference is the nation’s largest gathering of mortgage professionals, and it returns to Planet Hollywood in Las Vegas this August 15-18 for another fantastic, session-packed event.

Originators attend for FREE using code NMPFREE.

TITLE SPONSOR

BROKER BUSINESS IS BUILT ORIGINATORCONNECT.COM AUG 15 AUG 18 HERE.

PRODUCED BY THE ORIGINATOR CONNECT NETWORK 30 | NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024

FRIDAY NIGHT RECEPTION

FEATURING THESE EXCLUSIVE EVENTS:

& A CAN’T-MISS NETWORKING PARTY

*Complimentary registration available to NMLS-licensed active LOs and their support staff. Show producers reserve the right to determine final eligibility. NMLS Renewal class open to conference attendees only. Exclusive events and networking party are open to registered attendees only. +FREE NMLS RENEWAL CLASS

Is It A Deal Or Chicanery?

Negotiating EPOs with lenders

BY KATIE JENSEN, STAFF WRITER, NATIONAL MORTGAGE PROFESSIONAL MAGAZINE

The mortgage industry has seen a glimmer of hope as industry experts forecast declining rates in 2024.

The Mortgage Bankers Association (MBA), Lawrence Yun of the National Association of Realtors (NAR), Rob Chrisman, and other well-trusted sources have pooled their bets, with predictions on interest rates ranging from 7% to 5% for the end of the year.

Even though many industry experts were wrong in forecasting a rate decline last year, many originators are preparing for a potential resurgence in refinances this year. Whether those originators are right or just desperate for sales activity to pick up, the anticipation has sparked debate and conflict over early pay off (EPO) penalties. An EPO occurs when a borrower sells or refinances their home too early, which is defined in the lender’s contract and is typically four to six months after the loan is funded.

This can create a major dilemma for the originating broker. Doing an early refinance or sale may be in the client’s best interest, but investors in the secondary market count on making money off of interest revenue from the original loan. When an EPO occurs, the investor charges a penalty to the wholesale lender, and the lender charges a penalty to the originating broker — sometimes even if the borrower refinanced with a different lender — which can mean returning their

commission or paying 1% of the loan amount, depending on different lenders’ contracts.

But, no one was overly concerned over an EPO frenzy during the last refinance boom in 2021, so why raise the alarm now?

According to Redfin, nearly 80% of homeowners have mortgages with rates below 5%, having refinanced during the pandemic. The only borrowers expected to refinance or sell if rates decline in 2024 are those who purchased homes in the past 18 months, which increases the threat of EPO penalties for originators.

Generally, brokers cannot escape EPO penalties once the broker signs a lender’s contract, except by ending their partnership. Some brokers claim negotiation is possible if they generate enough business for the lender. But, those deals are shrouded in mystery, and according to some sources, not to be trusted.

EQUAL RISK

It may seem as if EPOs are solely a broker problem, but they can come back to bite wholesale lenders as well if their policy frustrates enough of their partners.

A cautionary tale for lenders comes from Christopher Foote, chief growth officer for Milestone Mortgage, who decided not to renew his company’s contract with PRMG Mortgage because of their buyback policy, which includes EPOs.

“Sometimes it can be to your own

32 | NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024

Generally, brokers cannot escape EPO penalties once the broker signs a lender’s contract … Some brokers claim negotiation is possible … But, those deals are shrouded in mystery, and according to some sources, not to be trusted.

NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024 | 33

detriment,” Foote said about refinancing borrowers early. “But you also have to do what’s right for the client. And at the end of the day people need to save money in this economy.”

He said PRMG’s contract states they can force a broker to buy back a loan at any time and for any reason the lender deems necessary. Foote attempted to negotiate, saying that Milestone was PRMG’s top broker partner in Massachusetts, but they still refused to alter the contract. If brokers, like Foote, use their business as leverage to negotiate, it means reducing the amount of loans sent to that lender or canceling the partnership altogether.

“We loved working with them, but not under unreasonable terms,” Foote said. “Because, ultimately, they [EPOs] could bankrupt you.”

PRMG Mortgage did not respond to a request for comment.

Losing one broker partner is not detrimental to a wholesale lender’s business. But, if more top-performing partners decide to leave because they don’t want to be punished for going after refinances, it can negatively impact a lender’s market share.

It may not be feasible for most lenders to simply eat the penalty cost instead of having their brokers pay it, especially if they’re already struggling to maintain profitability in this market. That is why Jonathan Fowler, vice president of business development for American Financial Network Mortgage Inc., said it’s worthwhile for both wholesale and retail lenders to negotiate their EPO policy for top broker partners or top originators.

“If somebody’s sending me a hundred million dollars a month of business, and I lose a hundred thousand dollars one month on EPOs, can I raise their pricing by two basis points and recoup my money without ever causing a problem between the wholesaler and my customer, which

is the broker shop? Yeah. It’s probably a better business decision to change it by two basis points than it is to potentially ruin a relationship,” Fowler said.

Years ago, as a top producing originator for Allied Mortgage Capital Corporation’s Texas-based branch, one of Fowler’s investors would waive his EPO penalties, unbeknownst to Fowler.

“I asked the question, ‘I know that this sounds crazy, but why do I never get any buybacks from you?’ And they quite simply put it, ‘You’re sending me a billion dollars a month, why would I ever push a $30,000 buyback on you?’ ” Fowler said, recounting conversations with this investor.

Rocket Pro TPO cuts a deal with their top 20 broker and correspondent partners through its Pinnacle Program, where they don’t have to pay any fees if another originating company pays off the new loan early.

“An EPO is just to protect some of the losses from a lender standpoint,” said Rocket Pro TPO Executive Vice President Mike Fawaz. “The only time our broker is liable within our Pinnacle Program to pay an EPO is when they actively refinanced the loan … as long as you are not the one generating that loan, or the one proactively working that loan, you’re not liable for it.”

Fawaz said more top brokers are now showing interest in Pinnacle’s EPO fee waiver compared to when it initially launched during the previous refinance boom in 2021. He suggested that’s likely because the brokers anticipate the new refinances will be for borrowers who bought their homes more recently, after rates went up, increasing the risk of an EPO.

However, what makes Pinnacle especially unique is that it explicitly states Rocket Pro TPO selectively enforces its EPO penalties, unlike some lenders which have more of a secretive or unspoken agreement with their originator or broker partner, as in

34 | NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024

the case of Fowler.

Fawaz recognizes that being explicit about the agreement is what protects brokers and makes the deal legitimate. Knowing the Pinnacle program has publicly established guidelines, Fawaz said brokers can trust Rocket to not renege on their promise, unlike what other lenders have allegedly done.

“A key differentiator between Rocket Pro TPO and our competition today is that our Pinnacle program protects the broker community when it comes to EPOs versus, ‘Hey, we’re gonna waive an EPO, but the moment you decide you’re not gonna do business with us, we’re gonna send you these crazy bills’,” said Fawaz. “And that’s not how we do business.”

“That being said, even if such a policy is not in written form, I would not be the least bit surprised that such was happening on a more de facto basis.”

He said it’s highly unlikely a lender would agree to contracting the deal even if the broker pushed for it.

“I doubt any companies would be brazen enough to have written policies about such selective enforcement, which

Section 8(a) of RESPA prohibits a person from giving or accepting any fee, kickback, or “thing of value” in exchange for a referral related to a real estate settlement service involving a federally related mortgage loan.

could be used as evidence of RESPA violations,” Brody said.

BACKROOM DEALS

If a lender agrees to negotiate its EPO policy with a broker, it is most likely going to happen without a contract as a kind of backroom deal. That’s not to keep jealousy from stirring between broker partners, though. According to James Brody, compliance expert and senior partner with Garris Horn LLC, lenders won’t put EPO policy negotiations in a contract because it could be seen as a RESPA violation.

“While there has been and always will be an element of special treatment for those companies who can generate a greater volume of good loans, I have only heard unconfirmed rumors with regard to such selective EPO enforcement,” Brody said.

Section 8(a) of RESPA prohibits a person from giving or accepting any fee, kickback, or “thing of value” in exchange for a referral related to a real estate settlement service involving a federally related mortgage loan. Under RESPA, a “thing of value” may include a payment, advance, loan, service, or other consideration.

“The thing of value (i.e., the agreement not to enforce EPO Penalties) would be given in exchange for the referral of loans to be closed,” Brody said.

Brokers may enter into backroom deals at their own risk, though, and Fowler believes a deal can be done in a way that protects the broker. He recommends ensuring such an agreement is in writing, preferably in a binding contract that lays out all the terms and conditions.

He also strongly recommends clarifying

NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024 | 35

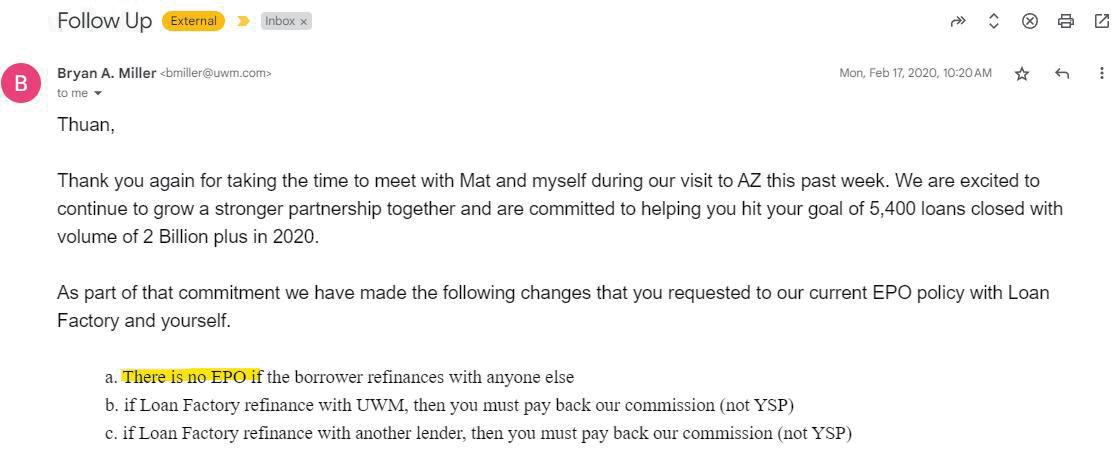

> A screenshot (below) of an email sent from UWM Account Executive Bryan Miller to Loan Factory CEO Thuan Nguyen confirming the changes they made to their EPO policy specifically for Loan Factory.

when the agreement goes into effect and when it expires, otherwise a lender could easily retroactively charge the broker EPO Penalties.

“Just because I don’t enforce or push back that EPO today doesn’t mean I can’t push it back a year from now,” Fowler said.

That is how Loan Factory CEO Thuan Nguyen got into an altercation with United Wholesale Mortgage (UWM) in 2021. After receiving UWM’s ultimatum, stating brokers must either choose to work with Rocket Pro TPO and Fairway Independent Mortgage or UWM, but cannot continue doing business with both, Nguyen’s deal with UWM regarding EPO penalties was reneged upon, even though it was documented through an email exchange.

“They [United Wholesale Mortgage] assured me in writing there would be no EPO,” Nguyen said. “The promise was upheld for 1 year until the Ultimatum. Upon facing the Ultimatum, I realized that they are not a good partner for me. I chose Rocket. Consequently, they sent me an invoice totaling $594,175.50.”

Nguyen showed NMP a screenshot of an email sent from UWM Account Executive Bryan Miller confirming the changes they made to their EPO policy specifically for Loan Factory. The promise Nguyen refers to was that he would not have to return his commission if a borrower refinances early

with a different broker.

“Once they see that you are stepping away from them, they will go after you,” Nguyen said. “Even if I show them that I have their written email confirming the agreement that they won’t charge EPO, they still walk past their promise.”

“I tried to sue UWM but I did not,” because UWM dropped its claims, Nguyen said. “After I paid them about $70K, they said it is all settled and I don’t owe them anything.”

UWM did not respond to multiple requests for comment.

Fowler explained why some lenders may get away with charging EPO penalties retroactively, even when the broker received a written promise that they would not get charged.

“So, if I decide today not to push these back and you decide six months from now not to do business with me anymore, it doesn’t mean that I lost my time to push back,” Fowler said. “It can still be done.”

‘BROKERS NEED REPRESENTATION’

“Brokers need representation,” said Client Direct Mortgage CEO Ramon Walker, after UWM hit him with more than $124,000 in EPO penalties on 12 different transactions,

36 | NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024

dating back to 2020. He was given seven days to pay the full sum.

UWM notified Walker of the EPO Penalties in a cease and desist letter sent in December 2023. Walker said this was the first time he’d been notified. In the letter, UWM also took issue with a Facebook group Walker created, UWM Vs. Rocket Pro TPO. Walker said the group allows brokers to freely debate the pros and cons of working with either lender. However, UWM attorneys accuse Walker of “improper use of UWM’s intellectual property” and allowing “defamatory statements” to be made by members in the group.

Walker said his working theory is that UWM knew about those EPOs for years and are only demanding payment now because he created the group.

individual that’s writing us the contract,” Walker said.

Fowler agreed, saying that brokers are too vulnerable to fight back. If any broker wants to challenge a lender’s demand for repayment or negotiate their contract in advance, hiring an attorney is possible, but not always feasible.

“Brokers don’t have attorneys on speed dial because they cost so much money,” Fowler said. “Even most independent mortgage bankers have weak attorneys for in-house counsel … ”

After receiving a demand notice, Fowler said attorneys for independent mortgage

“Unfortunately, there are many brokers that are doing business with other lenders, and they are in a bad position because they don’t know what’s gonna happen. They’re always on edge. And that is not a world that anybody should live in.”

“Their [UWM’s] gain on sale in 2020 was 300 basis points,” Walker said. “They made $1.5 million off of me that year. In their mind, they’re probably like, ‘Oh, don’t worry about these couple of EPOs. We’ll get him next year.’”

> Mike Fawaz, Executive Vice President, Rocket Pro TPO

UWM did not respond to multiple requests for comment.

Although Walker expressed that he isn’t afraid of a fight and would “love to get in discovery with UWM,” he believes the broader broker community is too vulnerable against lenders.

“We need an organization that actually protects us, and is not complicit with the

bankers only look to confirm that the banker did the loan and double check the amount the lender is asking for, but rarely do they dispute whether or not the originator should be charged.

“We’re stuck in a David versus Goliath kind of thing,” Fowler said.

“Unfortunately, there are many brokers that are doing business with other lenders, and they are in a bad position because they don’t know what’s gonna happen. They’re always on edge,” Fawaz said. “And that is not a world that anybody should live in.” n

NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024 | 37

PASADENA | NOV. 7, 2023

MORTGAGE ROUNDUP

HOUSTON | NOV. 14, 2023

TEXAS

UNCASVILLE, CT | JAN. 11, 2024

Events for mortgage brokers & originators

Connecting you to the story of your success.

Don't miss out! These recent events were huge successes — providing great educational and networking opportunities. Make plans to attend the next one nearest you!

We want every broker and originator to feel empowered, informed, and connected to the resources needed to develop your career. The Originator Connect Network, the nation's largest producer of mortgage events, is about fostering a community founded on professionalism, collaboration, and personal and professional growth.

To find the next event nearest you, visit:

ORIGINATORCONNECTNETWORK.COM

ARIZONA CALIFORNIA COLORADO FLORIDA GEORGIA ILLINOIS LOUISIANA MICHIGAN NEVADA NEW ENGLAND NORTH CAROLINA OREGON TENNESSEE TEXAS UTAH WASHINGTON

NEW ENGLAND THE MORTGAGE

Closing On Camera

Docuseries follows LOs in tough market

BY ERICA DRZEWIECKI, STAFF WRITER, NATIONAL MORTGAGE PROFESSIONAL MAGAZINE

Amoving montage, a catchy song, and an intense title sequence give the appearance of prime time television, but this reality show is definitely more relatable to mortgage mavens than teenage drama queens.

A touch of fate reconnected Emmy-award winning director and producer Kirby Bradley with his childhood classmate, Fairway Independent Mortgage CEO Steve Jacobson. What the two were able to create using their expertise along with that of videographer and editor Mike Hechanova is the only one of its kind, with the potential to change how the world looks at mortgage finance.

L.O. Confidential: A Season on the Street is a threepart series released to YouTube on Nov. 28, 2023. It follows three Fairway teams in Indiana, Arizona, and Texas as they navigate life and work during one of the toughest mortgage markets.

“I think that anyone watching this, even if they don’t care about mortgages, will really draw inspiration from how all these folks have figured out how to live their lives,” Bradley says. “You’re going to learn something about mortgages, which a lot of people don’t know … but all of us understand family.”

THE PREMISE

Bradley and Jacobson grew up together in smalltown Wisconsin. They reconnected a few years back when a mutual friend passed away.

40 | NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024

NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024 | 41

“Randy Cross was pivotal in Fairway’s origin story in that he was the one who came up with the name Fairway,” Bradley says. “His death brought us back together in the sense that we just bonded sharing our feelings about Randy, then it gradually developed into a working relationship.”

With many years producing and directing television shows and documentaries for HBO, CNN, and ESPN, Bradley and his work have been recognized with 33 Emmy Awards, three Peabodys, and two duPonts. He did a few promotional videos for Fairway, then came on board full time in January 2021 to start a video production department at the company.

“I traveled all over the country, met a lot of loan originators, and was really impressed by how dedicated they were to their jobs. I thought it was great material and really outside of the box.”

So Bradley and Hechanova pitched the idea for the series to Jacobson, who helped them locate three Fairway branches that would be ideal for the job. “I wasn’t really sure they would be willing to do it,” Bradley says, “but

they showed a lot of faith and gave us the green light.”

AN INVESTMENT

Based in Madison, Wisconsin, Fairway is the #2 overall retail lender in the U.S., with more than 650 branches and $42 billion in loan volume in 2022.

Filming a docuseries mostly in-house was not a huge financial commitment, though it did take Bradley, Fairway’s chief content officer, and Hechanova about six months to do. Company officials did not disclose the project’s budget in interviews. The first episode had close to 4,000 views by Jan. 24.

“When Kirby Bradley pitched us the idea for L.O. Confidential, he stressed that, even though the project was large in scope, he would be able to tap into his decades of experience creating award-winning TV programming and would be able to keep the budget very manageable,” Jacobson says, adding, “We have been extremely happy with the impact the series has had across the industry.”

Discovering the series could motivate other mortgage companies to use this medium as a tool of engagement with potential clients and workers.

“If any other company is willing to invest in high quality video production like this, how far are they willing to go for their employees and customers?” says Fairway Sales Manager Austin Smith, whose team in Greenwood, Indiana was one of those featured. “I think that speaks to their character and vision.”

Company officials’ main goal for the project was to share Fairway’s mission and potentially recruit new LOs to its team. Sales Manager of Fairway’s Heritage Group in Garland, Texas Craig Brown put together an action plan to promote the series and let other mortgage companies and even real estate agents know it exists. As to how they are measuring its success, the best is yet to come.

“We’ll let you know in six months,” Brown says. “Obviously, you can measure based on views on YouTube, but there’s more to an impact than that. We have several different avenues and strategies that Fairway will be taking and our branch alone will be taking. As we get the word out through more of a strategic placement distribution, then I think we’ll see a lot more attractions start taking place. In terms of

42 | NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024

> Kirby Bradley, Director, L.O. Confidential and Chief Content Officer, Fairway Mortgage

> Craig Brown, Branch Sales Manager, Fairway Mortgage

> Craig Brown, Branch Sales Manager, Fairway Mortgage

NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024 | 43

> Linda Davidson, Branch Manager and Senior Loan Officer, Fairway Area Leader

> Linda Davidson, Branch Manager and Senior Loan Officer, Fairway Area Leader

recruitment, it’s going to be hard to really track whether that is organic or through the video. We’re looking at the click through rate, conversion rate, form fields that they’re able to acquire from these videos.”

It was important for Fairway to showcase its nonprofit arms in the docuseries — the American Warrior Initiative, (AWI) and Fairway Cares. AWI helps wounded military heroes, providing service dogs, business grants, home upgrades, and mortgage-free housing.

“Steve, the CEO of our company, cares about the KPIs (Key Performance Indicators) but he cares more about the impact this is making,” Brown says. “We don’t necessarily want to raise this flag and say, hey, we’re the biggest, best mortgage company out there. Being the most philanthropic, that’s what we want to be known for.”

THE TEAMS

Brown’s mother Linda Davidson happens to be the Heritage Group’s senior LO and branch manager. While stronger than ever, family and

office harmony took time to bolster — a recurring theme in the show.

“If you had told me when he was 16 that we could even stay in the same room for more than an hour but most of all, work together, I would have said not just no, but heck no. We’re both very headstrong, opinionated, and stubborn,” says Davidson, who brought her son onto the team 12 years ago only to discover their strengths balance each other.

“He brings a technical, business development and marketing side, and I bring the mentorship of just loving to lead and help others grow,” Davidson says.

“Linda definitely brings the heart of the branch where I bring a lot of the head,” Brown adds.

The Martinez sisters — Ericka, Jessica, and Jazel — head up the 3M Group in Phoenix, AZ. The cameras follow them from the gym where they begin their day to the office, where they do their best to drive success while keeping their own family dynamics under control.

The sisters were flattered that Fairway’s corporate team chose their branch to feature in the docuseries, and it actually strengthened their individual relationships with each other.

“The reality is that we’re sisters but it’s not perfect — we fight like sisters,” Senior LO Ericka Martinez Hirons says. “Going through that process and seeing it from a different lens gave Jessica and I an understanding that the things we were upset about didn’t really matter. At the end of the day, the most important thing is family.”

Prior to the project even being announced, the pair had been seeing a therapist to work out their personal and professional grievances. Post filming, they have overcome those divisions.

The third branch featured is headed up by Smith, a husband and father of three.

“How often does somebody say hey, let’s film a documentary on you. Naturally I was curious,” Smith says. “I talked about it with my wife and our team and everybody was supportive.”

Filming and seeing the series back was “a humbling experience” for Smith, who has a son with autism. “As my wife and I watched it back it made us reevaluate some things in our life. I hope any LO that watches this realizes they also need an opportunity to reevaluate things for themselves. I hope it gives them a chance to

44 | NATIONAL MORTGAGE PROFESSIONAL MAGAZINE | JUNE 2024

“We don’t necessarily want to raise this flag and say, hey, we’re the biggest, best mortgage company out there. Being the most philanthropic, that’s what we want to be known for.”

> Brown

look at things from a different microscope.”

GETTING PERSONAL