INVESTORS ARE FALLING IN LOVE WITH FIGURE’S HUMAN-FREE UNDERWRITING

HIGHER RATES complicate rate-reduction strategies

GINNIE MAE ISSUERS FACE NEW REPORTING REQUIREMENTS for cyber incidents

ANGEL AI CUTS COSTS WITHOUT CUTTING CORNERS

INFRASTRUCTURE UPGRADE

Save your servicing with cloud-based systems

YIELD CURVE PLAYING BY ITS OWN RULES?

INNOVATION DATABANK MARKETS Pavan Agarwal CEO of Sun West Mortgage Company Innovate Automate Dominate

Jackie Frommer head of lending at Figure Lending

Pioneers, Leaders, Innovators.

If these words come to mind when considering your ideal candidate for our list of Powerful Women of Mortgage Banking, then show your support for today’s female leaders in the mortgage profession and submit your nomination.

Nomination Deadline: July 5, 2024

nmplink.com/MBMWomen Mortgage Banker Magazine’s October issue will feature a special section celebrating 2024’s Powerful Women of Mortgage Banking.

Visit

MAGAZINE

MortgageBanker

REGULATORY CORNER

GINNIE MAE IMPLEMENTS RAPID CYBER INCIDENT REPORTING REQUIREMENTS

Effective March 4, 2024, issuers of Ginnie Mae mortgage-backed securities must notify Ginnie Mae of any cybersecurity incident within 48 hours of its detection.

Ginnie Mae remains dedicated to the security and integrity of all operational systems and critical technology infrastructure related to the issuance and servicing of Ginnie Mae Mortgage-Backed Securities (MBS). In support of these objectives, Ginnie Mae will be implementing Cybersecurity Incident reporting requirements. Effective [March 4, 2024,] Issuers, including those who subservice for others will be required to notify Ginnie Mae of a Significant Cybersecurity Incident, as described below.

A Significant Cybersecurity Incident (Cyber Incident), is an event that actually or potentially jeopardizes, without lawful authority, the confidentiality, integrity, or availability of information or an information system; or constitutes a violation or imminent threat of violation of security policies, security procedures, or acceptable use policies and has the potential to directly or indirectly impact the Issuer’s ability to meet its obligations under the terms of the Guaranty Agreement. The requirement to notify Ginnie Mae applies to all Issuers. Issuers who subservice for others must also notify Ginnie Mae when a Cyber Incident affects one or more of their subservicing clients.

Issuers must notify Ginnie Mae within 48 hours of detection that a Cyber Incident may have occurred. The notification must be sent to Ginnie Mae via email to: Ginnie_Mae_Cybersecurity_Incident@hud.gov and contain the following information:

• Date/time of Cyber Incident,

• A summary of the incident based on what is known at the time of notification,

• Designated point(s) of contact who will be responsible for coordinating any follow-up activities on behalf of the notifying party.

Once the notification is received, representatives from Ginnie Mae will contact the designated point of contact to obtain additional information and establish the appropriate level of engagement needed depending on the scope and nature of the incident. Ginnie Mae is reviewing its information security requirements with the intent of further refining its information security, business continuity and reporting requirements.

Ginnie Mae has revised Chapter 03, Part 18 of the Mortgage-Backed Securities Guide, 5500.3, REV-1 (MBS Guide), by adding Section C to reflect this new requirement. Additionally, the term Cybersecurity Incident has been added to the MBS Guide Glossary.

Any questions about the policy can be addressed to clients’ Account Executives directly.

Ryan Kingsley

Katie Jensen, Sarah Wolak, Erica Drzewiecki

Alan

Melissa

Submit your news to editors@ambizmedia.com www.ambizmedia.com © 2024 American Business Media LLC. All rights reserved. Mortgage Banker Magazine is a trademark of American Business Media LLC. No part of this publication may be reproduced in any form or by any means, electronic or mechanical, including photocopying, recording, or by any information storage and retrieval system, without written permission from the publisher. Advertising, editorial and production inquiries should be directed to: American Business Media LLC 88 Hopmeadow St. Simsbury, CT 06089 Phone: (860) 719-1991 info@ambizmedia.com STAFF Vincent M. Valvo CEO, PUBLISHER, EDITOR-IN-CHIEF

Bolnick ASSOCIATE

Beverly

PUBLISHER

EDITOR

STAFF WRITERS Alison Valvo DIRECTOR OF STRATEGIC GROWTH Julie Carmichael PROJECT MANAGER Meghan Hogan DESIGN MANAGER

Wallace, Stacy Murray GRAPHIC DESIGN MANAGERS Navindra Persaud DIRECTOR OF EVENTS William Valvo UX DESIGN DIRECTOR Andrew Berman HEAD OF CUSTOMER OUTREACH AND ENGAGEMENT

Mullins, Krystina Coffey

SPECIALIST

Christopher

Matthew

MULTIMEDIA

Nero MEDIA SPECIALIST

Pianin

& EVENTS ASSOCIATE

Woods-Lindig ONLINE ENGAGEMENT SPECIALIST

MARKETING

Kristie

ADVERTISING ASSOCIATE

Griffin MARKETING INTERN

you would like additional copies of Mortgage Banker Magazine call (860)719-1991 or email info@ambizmedia.com

Nicole Coughlin

Lydia

If

Yield Curve, Schmield Curve?

THE YIELD CURVE IS A HARBINGER, NOT THE BE-ALL, END-ALL FOR LENDERS.

BY ROB CHRISMAN , CONTRIBUTOR, MORTGAGE BANKER MAGAZINE

The “experts” talk about how the U.S. Treasury Curve is currently “inverted.”

What does that mean, and should it matter to lenders?

The fact is, the yield curve (a graphical representation of yields, usually of U.S. Treasury or governmentbacked securities, stretching from overnight to 30 years) has been inverted for some years now as we move through the spring of 2024, and doesn’t show a lot of movement away from that situation. The sun continues to rise in the east, geese head north for the summer, and the economy has

not ground to a standstill. But, what is the “yield curve,” what exactly does an inverted yield curve mean, and what are the implications for lenders?

Let’s start with the basics. Traditionally, shorter-term securities have lower rates and longer-term securities have higher rates because obviously someone wants to be paid more if they are going to tie up their money for longer. Loan officers know that adjustable-rate mortgage rates are usually lower than 15-year mortgage rates. This is important to lenders because bond traders and investors base their decision making (what to buy or sell, and at what price) on mortgage securities based on a spread

to Treasury securities.

Being inverted means that shortterm treasury yields (the one-year, two-year, and three-year) have higher rates of return (aka “yield”) than, say, the 10-year or 30-year do. This is counterintuitive, since the longer you give someone your money for, the higher the rate of return you would expect. And this is what normally happens, unless you’re entering a period of economic uncertainty. In periods of economic uncertainty, it makes sense to have an “inversion” of the yield curve: short-maturity interest rates exceed long-maturity rates typically associated with a recession in the near future.

MARKETS

4 MORTGAGE BANKER MAGAZINE | MAY 2024

Put another way, in “normal market conditions,” as compensation for higher risk, thousands of investors expect higher rates of interest for money they lend over a longer time horizon. This is traditionally reflected in an upward sloping treasury curve. Inversion shows investors are more apprehensive about the long term than they are about the short term. They believe a recession is imminent. Short-dated deposits, bills, and notes offer higher yields than those on longerdated bonds. But, lenders should know that when the economy slows down, rates go down.

Yield curves are upward sloping to compensate investors for the added risk of tying up their money for longer periods. Longer-term bonds carry greater risk of various potential losses, ranging from inflation to default. Investors, therefore, normally require an additional return, in the form of higher yields, to offset the risks of venturing out along the yield curve. A yield-curve inversion does not cause a recession. Instead, the slope reflects changing expectations about the economy, and these expectations are useful predictors of economic downturns.

Spring of 2022 and again at certain times during 2023: no one wanted to pay above par.

ROB CHRISMAN

If investors expect a downturn, they likely also anticipate that the Federal Open Market Committee (FOMC) will cut the future policy rate to provide monetary policy accommodation. The expectation of lower future rates reduces longer-term rates, and this could result in an inverted yield curve. Any aggressive monetary policy tightening by the FOMC, which would push up current rates relative to future ones, heightens the odds of a future decline in economic activity leading to overall lower rates, including mortgage rates.

“In periods of economic uncertainty, it makes sense to have an “inversion” of the yield curve: shortmaturity interest rates exceed longmaturity rates typically associated with a recession in the near future.”

In recent months investors have bought or sold treasuries and mortgage-backed securities depending on what they think is going to happen to inflation. It is generally assumed that prices will increasingly rise in the years ahead, and investors need to be compensated for bearing that risk, since higher inflation will erode their future purchasing power. For this reason, bond yields contain an inflation premium, normally an increasingly higher premium for bonds with longer maturity dates.

> Rob Chrisman

Lenders and originators should also know that the yield curve is influenced by more than monetary policy expectations. The shape and slope of the yield curve also reflect market attitudes toward various risks, and these too are influenced by economic outcomes. Interest rates on longterm securities reflect expectations of what might happen during the life of the bond, or mortgage. In other words, investors shy away from paying a premium price above 100 (par) for mortgages with high rates, assuming that at some point the borrower will refinance because rates have dropped. Why pay 103 for something that will return 100 in six months? We saw this phenomenon on rate sheets in the

Keep in mind that no one owns a crystal ball with a clear view of the future, and that the slope of the yield curve is not the only indicator of potential future economic activity. Stock prices, and their dividend streams, are often mentioned. The Commerce Department’s (now the Conference Board’s) index of leading economic indicators appears to have an established performance record in predicting real economic activity.

Yield curve inversion is not a lasting feature of the capital markets landscape. Know that whenever the yield curve is inverted, investors have already begun to anticipate its “normalization” which typically takes place in the context of falling interest rates, what Wall Street terms a “bull steepening.” In those instances, both short- and long-term interest rates fall, with the front end (shorter-dated maturities) rallying more than the long end. A bull steepening is bullish for fixed income markets, including mortgage rates.

Lenders and originators should keep in mind that yield curve normalization will only take place once the economy softens. Lenders know that a soft economy, however, can impact the percentage of borrowers that qualify. But a soft economy might be far in the future given the very tight labor market: unemployment is not going down. For now, 30-year fixed rates are clustered around seven percent, and this may be the norm for quite some time. And business cycles will continue on.

MORTGAGE BANKER MAGAZINE | MAY 2024 5

Welcome to The Greatest Mortgage Conference In The Known Universe.

The Originator Connect Conference is the nation’s largest gathering of mortgage professionals, and it returns to Planet Hollywood in Las Vegas this August 15-18 for another fantastic, session-packed event.

Originators attend for FREE using code MBMFREE.

6 MORTGAGE BANKER MAGAZINE | MAY 2024 BROKER

IS BUILT

HERE.

BUSINESS

ORIGINATORCONNECT.COM AU G 15 AU G 18

TITLE SPONSOR PRODUCED BY THE ORIGINATOR CONNECT NETWORK

& A CAN’T-MISS NETWORKING PARTY

FRIDAY NIGHT RECEPTION

FEATURING THESE EXCLUSIVE EVENTS:

*Complimentary registration available to NMLS-licensed active LOs and their support staff. Show producers reserve the right to determine final eligibility. NMLS Renewal class open to conference attendees only. Exclusive events and networking party are open to registered attendees only.

MORTGAGE BANKER MAGAZINE | MAY 2024 7

NMLS RENEWAL CLASS

+FREE

Building A Digital Bridge Between Separate Revenue Streams

MENU CLOUD-BASED TECHNOLOGY CAPITALIZES ON THE ENTIRE BORROWING CYCLE

BY DAVID AACH, SPECIAL TO MORTGAGE BANKER MAGAZINE

While mortgage lenders have faced rough seas before, today’s housing waters have rarely been so choppy. High mortgage rates, low inventory, and fierce competition are not only diminishing profits, but they are creating stern headwinds that make forward progress feel impossible.

It’s particularly true for lenders that both originate and service their own loans. While such a strategy can help insulate organizations from the impact of market shifts, rarely are companies able

to navigate both sides of the business with any real cohesion. Yet, amidst these stormy seas, the beacon of innovation shines brightly, offering smooth passage and the opportunity to turn operational challenges into avenues for growth.

As an analog industry evolves for the digital age, mortgage bankers must build cloud-based bridges between their origination and servicing channels. For larger lenders, efficiencies and costsavings await. For smaller lenders, besides an upgrade, it may just mean survival.

REGULATORY

8 MORTGAGE BANKER MAGAZINE | MAY 2024

ADAPTATION: THE CONSTANT STRUGGLE

One only needs to look back two years to see how quickly and dramatically the lending environment can change. Rates went from all-time lows during the height of the COVID-19 pandemic to the highest level in more than three decades during 2022 and 2023. Coupled with near-historically low inventory, the stunning transformation placed enormous pressure on lenders who found themselves having to trim headcounts while still finding a way to compete for an ever-smaller pool of borrowers.

At any point, the market could shift again. Most market observers, including the Mortgage Bankers Association (MBA), forecast a sizable drop in rates this year. Such a reduction in borrowing costs could find lenders once again struggling with staffing and capacity issues.

However, servicers face their own set of challenges, including a small but steady increase in delinquency rates. Should rates fall, they’re likely to face early payoffs. Sadly, legacy mortgage technologies play only a passive role when it comes to navigating these shifts.

Numerous reasons account for this passivity, perhaps the most significant being that lenders who service their own originations typically use separate technologies for each business. More often than not, the platforms they use for each channel are difficult or impossible to integrate since most of those programs were developed decades ago before the cloud-computing era.

Try as they might, most tech vendors have also struggled to transition their premise-based loan operating system (LOS) and servicing software to the cloud. Now cloud native solutions are available, though, lenders can chart a smoother course through the tidal rate environment of the mortgage market.

THE ROLE OF A DIGITAL BRIDGE

By deploying modern, cloud-based digital lending technology, mortgage bankers can start transforming their loan origination workflows from the point of sale all the way through closing with very little investment. Automating dozens

or even hundreds of routine tasks eliminates the routine, manual tasks once required of their loan officers, processors and underwriters.

The journey doesn’t have to end once a loan closes, though. Lenders who leverage digital servicing technology in the same cloud infrastructure as their LOS can connect and coordinate their origination and servicing operations. Creating this digital bridge allows lenders to immediately onboard newly originated loans, creating a single, seamless, digital strategy that encompasses the entire borrowing cycle.

For lenders who retain their servicing, this unleashes numerous benefits. Cloud-delivered systems facilitate growth and digital adaptation without major investments in resources or staff. Whether their focus is retail, wholesale, or correspondent lending, cloud-based automation is highly customizable and flexible. Lenders can leverage the technology to stay lean, improve efficiency, and close more loans, while also gaining the agility to quickly expand or shrink their mortgage offerings in response to evolving market and customer demands.

Building a digital bridge that allows data to channel seamlessly between the origination and servicing side of a lender’s business enhances that lender’s ability to study the relationship between these sets of data. Advanced analytics that generate strategic insights lead to more informed decision-making and accelerated growth.

A SEA CHANGE AWAITS

Mortgage bankers in today’s market face a rising tide of costs for originating and servicing loans. The MBA reported that in the third quarter of 2023 independent mortgage banks (IMBs) and mortgage subsidiaries of chartered banks lost approximately $1,015 per loan they originated (pre-tax), nearly double their per loan losses in the second quarter. Servicing income, buoyed by the recent spike in rates, began to ebb as interest rates receded, slightly.

With cloud-native origination and servicing technology, all point-of-sale, underwriting, and servicing software is completely browser-based and infinitely scalable. Automation enables lenders to adapt quickly to any rate environment without having to go through the painful – and painfully expensive – process of hiring, firing,

MORTGAGE BANKER MAGAZINE | MAY 2024 9

“Automation enables lenders to adapt quickly to any rate environment without having to go through the painful – and painfully expensive – process of hiring, firing, and rehiring staff.”

> David Aach, Chief Operating Officer Blue Sage

and rehiring staff. At the same time, digital, cloud-based technology is extraordinarily fast to deploy.

While, typically, only large financial institutions both originate and service loans, cloud-based servicing technology opens the gates for smaller originators to adopt servicing capacity – again, without major investments in resources or staff.

By efficiently and costeffectively holding their originations and servicing in the same cloud ecosystem, these smaller lenders gain a competitive advantage by being able to maintain relationships with borrowers throughout the mortgage borrowing cycle, not only creating deeper levels of trust, but opening up opportunities to cross-sell other financial products and services.

THE BOTTOM LINE

In tumultuous times, digital mortgage origination and servicing technology offer a sense of stability, similar to how fins and rotors stabilize

a ship in turbulent waters. More than simply tools, the automations and application programming interfaces (APIs) behind new cloudbased platforms create lifelines that help lenders steer both sides of their business in tandem, more efficiently, and more costeffectively.

As the digital evolution of the mortgage business accelerates, adopting cloudbased technologies may mean survival for some mortgage lenders.

Lenders are no more capable of controlling the housing market than they are controlling the weather, or the timing of interest rate cuts. However, lenders can control how they evolve with the market. Building a digital bridge between origination and servicing is not only building a bridge between revenue channels, staff, and customer databases. It’s building a bridge between the past and the future of a lender’s profitability in the mortgage business.

10 MORTGAGE BANKER MAGAZINE | MAY 2024

Join us for the third annual Suncoast Mortgage Expo in sunny Florida that will motivate originators, drive your business forward with new tools, and energize and educate on ways to propel volume to new heights.

What better place to take a break from the daily grind? Take a day to recharge in a beautiful location and head back to the office with a fresh perspective, new tools and new connections made at Suncoast Mortgage Expo! This valuable, one-day conference is dedicated to helping originators grow and succeed. Interesting sessions, interactive discussions and networking opportunities and an exciting show floor filled with service providers who want to help you – it’s all at Suncoast Mortgage Expo!

Complimentary registration available to NMLS-licensed active LOs and their support staff. Show producers reserve the right to determine final eligibility.

pros. MAY

TAMPA,

Embassy

Florida’s top gathering for mortgage

30

FL

Suites Tampa 3705 Spectrum Blvd, Tampa Scan here to register for FREE (promo code MBMFREE) or go to WWW.SUNCOASTMORTGAGEEXPO.COM

Brokers & Beignets

Build your business in the Big Easy

Picture this: You arrive at the historic French Quarter of New Orleans, the scent of beignets and freshly brewed coffee mingles with the soulful melodies of jazz drifting from nearby clubs. Your excitement grows as you approach your destination, the iconic Hotel Monteleone.

Nestled in the heart of the French Quarter, the Hotel Monteleone stands as a timeless symbol of elegance and Southern hospitality. Its grand facade, adorned with wrought-iron balconies and lush greenery, exudes old-world charm and allure. As you

pull up to the entrance, you are greeted by the sight of uniformed bellmen bustling about, ready to assist with luggage and offer warm smiles of welcome.

Stepping into the lobby, you’re enveloped in a sense of luxury and history. The opulent decor, with its marble floors, crystal chandeliers, and rich mahogany furnishings, harkens back to a bygone era of glamour and sophistication. Yet, amidst the grandeur, there is an unmistakable sense of warmth and intimacy, as if each guest is being welcomed into the embrace of a dear friend.

12 MORTGAGE BANKER MAGAZINE | MAY 2024

As you ascend the grand staircase, you are struck by the buzz of energy that permeates the air. The sound of lively conversation and the clinking of glasses fills the hallway, mingling with the faint strains of jazz music drifting up from the lobby below. Arriving at the conference area, you are greeted by the sight of attendees from all corners of the mortgage industry, engaged in animated discussions and networking opportunities.

The expo hall itself is a bustling hive of activity, with rows of booths showcasing the latest innovations and services in the mortgage industry. From technology solutions to compliance resources, the array of offerings is vast and impressive. The traveler eagerly immerses themselves in the exhibits, eager to glean insights and make valuable connections with fellow professionals.

JULY 10 — 11, 2024

Throughout the day, you attend informative workshops and panel discussions, gaining valuable knowledge and industry insights from leading experts in the field. You take diligent notes, exchanging ideas with colleagues and forging new connections that will prove invaluable in your professional endeavors.

As the day draws to a close, you reflect on the wealth of information you have acquired and the connections you have made. With a sense of fulfillment and anticipation for the days ahead, you make your way back to your room at the Hotel Monteleone, grateful for the opportunity to participate in such a dynamic and enriching event in the vibrant city of New Orleans.

The Ultimate Mortgage Expo is a two-day event for the Gulf Coast Region’s mortgage professionals. Since 2013, the Ultimate Mortgage Expo has been providing unique opportunities for brokers, originators, and support staff to build their businesses. This year, we’ve expanded the event, with even more sessions on Wednesday, July 10, plus another incredible networking party. The cherry on top is that all of this is free for attendees, thanks to supporters of the show, who you can meet in the exhibit hall on both Wednesday and Thursday. Just use our code OCNFREE on your registration.

MORTGAGE BANKER MAGAZINE | MAY 2024 13

UltimateMortgageExpo.com

NEW ORLEANS

MORTGAGE EXPO

*Complimentary registration available to NMLS-licensed active LOs and their support staff. Show producers reserve the right to determine final eligibility. NMLS Renewal class open to conference attendees only. Exclusive events and networking party are open to registered attendees only. ULTIMATE

Raising An Ai Brainchild In The Mortgage Industry

BY SARAH WOLAK , STAFF WRITER , MORTGAGE BANKER

14 MORTGAGE BANKER MAGAZINE | MAY 2024 C0-COVER STORY

MAGAZINE

Angel Ai takes on the next five years with a new ‘do and functions to boot.

Pavan Agarwal likes saving money. When he looks around his office and sees only 11 underwriters at work, he smiles to himself. That smile is powered by Angel Ai. Let’s do some math:

Last year, Sun West Mortgage Company’s artificial intelligence platform, Angel Ai, processed 75% of all borrower-submitted documents. The remaining 25% – flagged for exceptions –had to be scoured by underwriters who manually submitted the data to Angel Ai.

This year, roughly 6.5% of borrowersubmitted documents were flagged. In real numbers, 1,517 loans were decided by Angel Ai, and 107 loans were sent for a second signature.

There’s no carrot and no stick, but because Angel Ai learned, she was promoted, and Sun West CEO Pavan Agarwal was able to trim his underwriting team by 70% –saving money.

Sun West’s Chief Operating Officer Jennifer Vallinayagam said they employed 40 underwriters at the peak in 2020. The 11 underwriters still on staff she calls “data scientists,” and they handle Angel Ai’s back-end functions. From loan approvals to restructuring options to reviews, they feed the problems they solve back into Angel Ai, which learns and improves as an AI-underwriting engine from these corrections being made.

But, building revolutionary technology does not come without these challenges. That’s what learning – and thus machine learning – is all about, improving over time. The power and opportunity of artificial intelligence is its ability to learn and adapt as the market continuously changes.

Though Angel Ai’s intelligence gaps must be overseen by the C-suite, Agarwal and Vallinayagram themselves, rapid change and rapid improvement define

the artificial intelligence program. Agarwal’s ambitions for Angel Ai break beyond the mortgage business, all with the intention of driving engagement on the platform – and saving people money, be they bankers or babysitters.

Admittedly, the financial services industry has been slow to adopt customer service AI tools. But, adoption is expected to accelerate in the next 12 to 18 months, according to a new report published by Syntellis Performance Solutions.

“The future is that the app is opening up and becoming everyone’s personal assistant. A lot of things we do today for realtors and loan officers can also be done for everyone else.”

> Pavan Agarwal, CEO of Sun West Mortgage Company

“Financial institutions across the country continue to face numerous economic and market pressures in 2024, including interest rate shifts, evolving customer demands, and rising competition from neobanks and other digital-only providers,” said Eric Wheeler, senior director of product management at Syntellis Performance Solutions (now part of Strata Decision Technology). “Our survey shows that banks, credit unions, and other financial institutions are boosting investments in data and analytics, AI, and other technologies to enhance customer service, increase efficiencies, and streamline processes as they work to navigate these challenges.”

The survey offers a glimpse into the likely future for artificial intelligence in the financial services realm. As mortgage companies’ costs rise, AI solutions across the loan process, in customer service or underwriting, will save companies money and time by lowering headcounts and streamlining processes. Agarwal has been planning for this future for years, developing Angel Ai so that the program is ready when the market is ready.

But, Rome wasn’t built in a day, and neither was Agarwal’s easy smile.

OVERCOMING GROWING PAINS

Agarwal has been dutifully raising his brainchild, Angel Ai, since 2018, when the program was launched as an internal tool adopted from Sun West’s tech-oriented sister company, Celligence.

From mid-2018 to the third quarter of 2020, Angel Ai closed 40,000 to 50,000 loans. Through the end of 2023, that number moved north of 180,000 loans.

The program’s growth has accelerated since September 2022 when Angel Ai was launched beyond Sun West’s borders, meaning every licensed mortgage professional could submit loans to the platform even if they didn’t work with Sun West. From October to November 2022, six Angel Ai accounts were created. From October to November 2023, more than 5,000 accounts were created.

In total, more than 138,000 messages (inquiries about loans) have been submitted through the platform, with almost 23,000 unique conversations occurring in the last few months, says Vallinayagam.

The platform attracts brokers like Greg Tanner of Carolina Home Loans.

Tanner became an independent broker in 2022. While looking for loan

MORTGAGE BANKER MAGAZINE | MAY 2024 15

investors to partner with, Tanner found Sun West and Angel Ai. “Now Sun West gets a large chunk of my business, and I’ve easily closed 20 to 25 loans using Angel Ai,” Tanner said. “I’ve been in the mortgage space for about 20 years, and the tool has especially helped me with income calculation, which is sometimes difficult, and it helps if you have a second set of eyes on it.”

He also appreciates Sun West’s “100% Assurance” policy. “Sun West stands by Angel Ai’s findings – even if it makes a mistake – and will still write the loan,” Tanner explains.

This sentiment shows that Angel Ai is still a work in progress despite its improving success rate.

While Sun West’s promise to stand by Angel Ai’s outputs builds users’ confidence, it also means that the platform has to be spoon-fed data, babysat by its creators. But, underwriting and loan processing is only a sliver of the potential Agarwal sees for Angel Ai.

BIG PLANS AND BLOCKCHAIN

Although Sun West and Celligence have ambitious plans for Angel Ai, Agarwal only has a rough idea of how he wants to roll out all these changes as he continues to smooth out back-end functions.

“The first and most important is a full, chat-based loan application for the consumer so they can apply for a mortgage using just a chat,” the CEO affirmed. “We also want to implement a robust set of training data for consumers to ask any questions about financial services. Really, anything they’d go to Google for.”

The idea, Agarwal says, is that users can initially engage with Angel Ai by asking a general question, and then go deeper. This initiative would capitalize on a trend toward increasing consumers’ financial literacy in the mortgage industry. As a direct-to-consumer origination strategy, it also shows the potential for Angel Ai to disrupt other mortgage lenders’ businesses.

Agarwal, a proponent of increased adoption of blockchain in the mortgage

industry, says adding NFT functionality ties these initiatives together. The Sun West team piloted the NFT function at a Diwali party hosted by Agarwal at his home in Puerto Rico.

“When [you] click on that NFT, [you] can go and see it, see all the information,” said Agarwal. “An NFT is nothing more than a ticket. It’s a token … that is now with a record that the owner owns it. And the blockchain gives that ownership, immutability, and permanency.”

Agarwal further explained how this works: “If and when [borrowers] give us enough data about themselves, we can say, ‘You qualify for $1 million. It says today, based on the information I have, you can close today on $1 million, so here’s a token.” With that token, which represents a pre-qualification for $1,000,000, the borrower can purchase a house.

It’s a hefty promise that, once on the blockchain, can’t be taken back, which could lead to the borrower’s dream home – or a million-dollar mistake on Angel Ai’s behalf. But, that’s the bet Agarwal is willing to take.

“It’s a commitment to get the loan, right? There’s a handful of conditions on that, like the property you purchase needs to be eligible, the title has to be clear, and your financial position doesn’t change from the time we issue the token to the time we close the deal,” he said.

Given the blockchain learning curve and the confusion average consumers face in understanding the technology, Agarwal may face headwinds. Nevertheless, he’s trying to plan for a mortgage future where these technologies, he thinks, will be increasingly ubiquitous.

DIFFERENTIATION BRINGS CONSUMERS BACK

Agarwal says the brand message for Angel Ai is ever-expanding, which is part-and-parcel

16 MORTGAGE BANKER MAGAZINE | MAY 2024

“Angel Ai [won’t] do your homework or generate your essay. But [it will] do other really interesting things that you may want and need.”

MORTGAGE BANKER MAGAZINE | MAY 2024 17 > Pavan Agarwal

of Agarwal’s user engagement strategy. The growth of the platform is tied to the roll-out of other features on Angel Ai’s drawing board – features that Agarwal banks on for expanding the brand’s audience inside and outside the housing industry.

“The future is that the app is opening up and becoming everyone’s personal assistant,” Agarwal said. “A lot of things we do today for [real estate agents] and loan officers can also be done for everyone else.” He knows it’s ambitious to try integrating every consumer outside of the financial services industry.

It’s even more ambitious to hope they will use Angel Ai regularly. “I want to get it out in front of consumers so they can start using it … we already did the hardest financial service possible, which is mortgages.” He cites event management, landing page creation, and online invitations as non-mortgage use cases for Angel Ai.

“Whether you’re a loan officer hosting a first-time buyer seminar or a mom having a birthday party, you still have to do the same things,” Agarwal believes.

Agarwal knows that Angel Ai is likened to ChatGPT. Thus, staking out the differences between these programs is a messaging and branding issue for Sun West to solve.

“We don’t want if a consumer has to ask why they should use Angel Ai, because then we messed up … we didn’t brand and communicate correctly,” Agarwal explained. “The question should be, ‘When do I use Angel Ai?’ not ‘Why should I?’.” He continues, “Angel Ai’s not going to do your homework … or generate your essay. But [it will] do other really interesting things that you may want and need.”

Some of those features do already exist. For example, the company created and patented “Ai-Sign,” which allowed them to do away with using DocuSign and replace it with an in-house product.

According to Angel Ai’s website, AiSign “provides the ability to slide through pages and view content before signing. At the end of each page, Angel Ai prompts users to add their signature by clicking on the designated option below.” Users can

sign documents using their fingers, as well as save their signatures for future use on the same document.

Because Agarwal’s goal is to keep users on the platform as long as possible, the team is also working on a credit repair function. This is “the biggest thing on Angel Ai’s horizon” because half of all consumers need some form of credit repair, Agarwal says.

“The idea is to give consumers a reason to stay on the platform and to be on the platform. And that’s why credit repair is so important; it gets them on the platform, gets us involved with them, and starts building trust so that when Angel Ai says, ‘Hey, have you thought about a mortgage?’ Or when they go to Angel Ai and say, ‘Hey, I need to think about a mortgage,’ we know their credit situation and can point out their best options.”

While differentiating from other AI programs remains a focus, Agarwal believes that he’s already beaten much of the competition in the mortgage space. Armed with its first-mover advantage, Angel Ai is backed by humans who know the program, and market, inside and out.

Tanner of Carolina Home Loans stands by this. “Human interaction is almost immediate if Angel Ai has an issue,” he said. “It’s helped me have confidence in my work, especially as a new broker.”

CHALLENGING THE STATUS QUO

Agarwal is confident that the next five years in Sun West’s growth in the artificial intelligence world will prove to stick with all ages – as he sees it, the next generation of homebuyers. He

cites name recognition, brand swag, and being deemed cool as reasons why Angel Ai resonates with younger mortgage folks, and younger folks in general.

Take, for example, the “12-year-old girl test” that Agarwal swears by. Sun West’s marketing director Anthony Toro tells Agarwal that his daughter is the most popular girl at school because she has access to Angel Ai merchandise. This tells Agarwal that the brand will succeed with the general consumer market eventually.

Angel Ai’s former alias, Morgan, failed this test. The rebranding of Morgan (to Angel Ai) during the middle of 2023 was intended to change people’s perception of the product. Now, people know that Angel Ai is an artificial intelligence system, unlike when “Morgan” was just seen as a woman’s name.

But, what does a 12-year-old know –or care – about an artificial intelligence platform akin to ChatGPT? Agarwal says it doesn’t matter; what matters is brand stickiness. It’s a big risk to do a rebrand after five years of existence under one banner. According to Agarwal, Morgan was a hybrid of the phrases “Mortgage Can” and “Mortgage Magician.”

It didn’t work.

“It’s got to go viral with children because they grow up to be young adults who will use your product. I’ve hit a home run with the brand as far as consumers appreciating and accepting the brand, people,” the CEO says. “Another good sign is [young people] love the merchandise … and they keep trying to get more. So I think we’ve hit a home run on the branding, and we’ve hit a home run in the messaging.”

Even though preteens have a long way to go until getting a mortgage, Agarwal says brand recognition should impact all ages. He drew parallels between successful brands like Nike, Apple, and Red Bull, highlighting the importance of a compelling message beyond product features. “Everyone knows Red Bull gives you wings,” Agarwal quips.

What he knows, if all else fails, 12-yearold girls are keen on Angel Ai.

18 MORTGAGE BANKER MAGAZINE | MAY 2024

TALKING

IS IN POOR TASTE.” Learn how to save for your retirement at WeSaySaveIt.org. National Institute on Retirement Security, 2016.

“

ABOUT MONEY

20 MORTGAGE BANKER MAGAZINE | MAY 2024 Automation Attracts Investors Who Love Homogenous Loan Pools

Human-free underwriting promises to expand primary and secondary, non-agency markets

BY RYAN KINGSLEY , EDITOR , MORTGAGE BANKER MAGAZINE

Ask Jackie Frommer if she runs a finance company or a tech company and she says both.

“I work for a tech company that is driving financial innovation,” says the head of lending at Figure Lending, the sandbox and subsidiary of Figure Technology Solutions, a fintech company pushing the envelope on automated underwriting in the mortgage industry. “We’re a lender to be a lender and demonstrate that our tech works.”

At the vanguard of innovation, that is what is required. Have a grand idea? Sweet! Prove it.

“You can maybe afford to have an inefficient product process with a mortgage because it’s so big,” Frommer explains. “It’s much harder to have an inefficient process with a HELOC where you can originate it in an economic way as a lender and still have it make sense for the customer and for the investor.”

Having held executive roles in consumer lending, wealth management, and securitization business at Lehman Brothers, Barclays, JP Morgan Chase, and Bank of America, Frommer now finds herself the cowcatcher on a train that is quickly gathering speed – but, a train with no conductor, only the

train tracks and switcher to guide it.

“We don’t have any underwriters,” she says. “We don’t have anyone that’s making an underwriting decision.”

Figure was founded in 2018 with a singularly ambitious goal: use technology to change the way that loans are originated and traded –automate underwriting to securitize homogenous loan pools, eliminating inefficiencies and origination risks to increase liquidity in the privatelabel secondary. If 2018 was the year that Figure pitched its premise, 2023 was the year that Figure proved it – investors have fallen in love with Figure’s loans.

Last April, the company closed its first rated HELOC securitization ever – a $236.7 million loan pool of Class A and B notes, rated AAA and A by the rating agency, DBRS Morningstar. By December of 2023, Figure had closed its fourth rated securitization of the year.

The latest transaction was backed by more than 2,600 fixed-rate open HELOCs with an aggregate principal balance of over $195 million and collective credit limits of over $204 million, with 75% of the loans having a 30-year term. The loans had a weighted average FICO score of 744, a combined loan-to-value (CLTV) ratio of 65%, and a debt-to-income (DTI) ratio of 38%. The notes were rated

AAA, AA, A-, and BBB- by Kroll Bond Rating Agency (KBRA) – a first for KBRA.

More notably, the deal included 20 unique class A-D investors, including alternative asset managers, insurance companies, private equity funds, and hedge funds, 15 of whom were new to the Figure shelf of securities. To that end, it was the largest order book of any Figure deal and significantly oversubscribed: Class A was 5.25x oversubscribed; Class B was 2.95x oversubscribed; Class C was 4x oversubscribed; and Class D was 4.25x oversubscribed.

These numbers demonstrate the increasing number of price points for investors to buy into Figure’s loan pools and that there is more investor demand than supply of loans at each price point. As a result, the investor spread has tightened. AAA notes priced at 240 basis points and A- notes priced at 330 basis points are the tightest for any Figure transactions to date.

With the home equity puzzle seemingly solved and an initial public offering (IPO) rumored for 2024, programmers at Figure have been playing in a new sandbox. “We’re going to start to focus on using this exact same technology for jumbos and Non-QM,” says Frommer. “We’re actually talking to someone about

MORTGAGE BANKER MAGAZINE | MAY 2024 21

“We’re not going to change anything in our system to allow you to somehow contort yourself to fit into the process.

There’s

not anyone you can call here to a discretionary decision about the loan for you. The process is process on any given day.”

> Jackie Frommer, head of lending at Figure Lending

22 MORTGAGE BANKER MAGAZINE | MAY 2024

potentially a DSCR product as well.”

Without the guarantees of the government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac, non-conforming mortgage borrowers – those with too much bread for the government’s spread – find themselves with costlier financing and fewer loan options. Similar issues plaguing home equity lending also plague Non-QM lending – high costs of origination, cumbersome underwriting, and worst of all, illiquidity.

“The ultimate goal is to use our technology to drive more liquidity for everybody in the capital markets and be able to have more people offer non-traditional, non-agency products,” Frommer explains. In non-agency markets, lenders need more certainty that investors will buy the loans they fund; investors need more certainty the loans they buy will perform.

Figure can make that happen, at least on a pilot basis, by the end of 2024, says Frommer. And yet, the company’s long-term plans are even grander.

“We’re hoping,” she says, “long run, and we’re using HELOC as a use case, that really we can create a market that is very much like a TBA [to be announced] market where the homogeneity of the product that’s originated on the tech enables a lot more efficient purchase and ultimate trading of the loan because it’s 100% understood by everybody who is in the process.”

However, Frommer adds, “it’s a very, very difficult task.”

AUTOMATE TO UNDERWRITE HOMOGENEITY

With manual underwriting, humans assessing loan files make subjective judgments based on a set of rules.

“What we are doing,” Frommer

“We’re creating a loan that is very easy for any investor to understand as long as it’s been originated with our tech because it looks like every other loan. Similar to what exists in the TBA market with Fannie and Freddie, people can really get comfortable, hopefully, in the long run, buying a loan before it’s even originated.”

>Jackie Frommer

explains, “is we’re taking rules that we’ve predefined over the six years we’ve been originating HELOCs –how we’ve been able to understand how certain characteristics drive performance of our loans.”

Those rules are tweaked over time in accordance with data analyses –not artificial intelligence (AI) – that assess the performance of different cohorts of loans. When performance

deteriorates or improves, the rules are refined, “but the rules at any given point are all exactly the same,” says Frommer. Though the underwriting rules are written by humans, all subjectivity has been removed from the decision-making process of qualification, inherently eliminating human error.

The only time humans have their hands on the machine is when certain pieces of borrower information cannot be verified digitally. For example, if Plaid, a data transfer network used for cross-checking applicants’ financial data, can not verify an applicant’s income, the applicant can upload tax returns to be fed through Figure’s rules engine.

Fully automated underwriting lowers barriers to entry for both borrowers and originators by reducing the costs and complications of origination. But, Figure also employs automation outside of underwriting to trim other inefficiencies and costs in the loan process. Automated valuation models (AVMs) replace appraisals, lien searches replace full title and insurance, customer service agents replace loan assistants for contacting borrowers when information can not be gleaned from digital sources.

That being said, if an applicant does not fit Figure’s underwriting rules, “we’re not going to change anything in our system to allow you to somehow contort yourself to fit into the process,” Frommer continues. “There’s not anyone you can call here to make a discretionary decision about doing the loan for you. The process is the process on any given day.”

Figure implemented that “no exceptions” policy so as to differentiate themselves from other lenders – and differentiate their rules engine from other automated underwriting programs – all in service to investors’ preferences. Fully automated, noexceptions underwriting produces homogenization in securitized loan

MORTGAGE BANKER MAGAZINE | MAY 2024 23 system contort There’s to make doing is the day.”

pools, which reduces uncertainty for investors – and investors hate uncertainty.

“There are other lenders who will allow more of an exception process, and we’re fine with that because the benefit of using our technology ultimately is to create this marketplace that can trade very efficiently because of the nature of the fact that the loans have been originated in a consistent way,” Frommer says. While she acknowledges that Figure cannot serve every borrower seeking a home equity loan, refining the rules on the back end is a way to serve more.

“In my mind,” Frommer shrugs, “I’m not sure why any investor wouldn’t like that process better because you know exactly what you’re getting.”

OVERCOMING FEARS OF THE UNFAMILIAR

Frommer says that many originators and lenders fail to grasp that they can make more money – and build their borrower base – by originating Figure’s HELOCs instead of purchase mortgages.

The abundance of use cases for Figure’s five-days-to-close HELOCs greatly expands the potential borrower base. The potential borrower base expands in a higher interest rate, higher home price environment where people cannot afford to move. Not only does Figure’s HELOC stand in for the cash-out refinance product, but also replaces the “huge” personal loan market.

The speed, ease, and lower costs making HELOCs an attractive alternative to personal loans for borrowers are precisely what make HELOCs a compelling alternative for originators.

Though loan balances are smaller – the minimum at Figure is $15,000, though their average is $90,000 – Frommer says originators can do “20 times as many, 30 times as many” HELOCs in the same amount of time it takes to complete one purchase mortgage.

One purchase mortgage carries the hope of one refinance, maybe a few referrals, maybe a home equity loan, somewhere down the line. Originating 20 or 30 times more HELOCs in the time it takes to originate one purchase

mortgages means working with 20 or 30 times more borrowers, multiplying the future business to be gleaned from those relationships.

“The smart lending officers, they get that,” Frommer shrugs. “They get the fact that this is just really fast and requires little work on their end . . . We definitely let all of our partners know, and all the lending officers know, that it is as simple as sending a link. It is very low-touch for them.”

Educating partners and originators about the HELOC opportunity remains a challenge, the narrative that HELOCs are time-intensive, costly, and cumbersome to underwrite still difficult to quash. Originators need to understand the effort and time tradeoff, Frommer says. It is a brand-new way of originating loans and people fear what they do not understand.

“I think that scares some of them,” Frommer levels, “because it’s so fast and we give them transparency into where the loan is. But, it’s not that same manual process that they may have with a loan that’s underwritten by a guy in their shop that they can call and try to push through the platform.”

Investors, seeing the opportunity,

24 MORTGAGE BANKER MAGAZINE | MAY 2024

have quickly overcome the fear of the unfamiliar.

Besides being homogeneously underwritten and originated, Figure can amortize the draw period over 30 years, lowering the monthly payments for borrowers. Though Figure offers various terms, the 30-year is most popular because of the lower payments. The longer, lower payment schedule makes Figure’s loan pools that much more attractive to investors.

HOMOGENEITY LOWERS ORIGINATION RISK

Frommer attributes the growing attractiveness of Figure’s loan pools to investors’ growing familiarity with the broader asset class of home equity loans – which have not been originated at scale since the Great Financial Crisis – and Figure’s fully automated rules engine.

“People have gotten comfortable that the process actually, in a lot of ways, is better than a process with any sort of human intervention,” Frommer says. The strong performance of Figure’s securitized loan pools proves the potential for automated underwriting to eliminate origination risk Figure’s hands-free approach also carries over to partners – the loans they originate with Figure’s tech “look exactly like” the loans Figure originates.

White-labeled loans are originated under partners’ names – like Movement Mortgage, the Loan Store, CMG Financial, or Guaranteed Rate –who white-label Figure’s technology and take the funding risk for those loans. “We tell them how much they need to fund,” Frommer explains, “then they put the loan up for sale to us and we’ll purchase it. If for whatever reason they want to sell it to somebody else, there’s an agreement where we potentially allow them to do that.”

Figure has a much broader base of partners through their wholesale

“It’s not that same manual process that they may have with a loan that’s underwritten by a guy in their shop that they can call and try to push through the platform.”

>Jackie Frommer

platform, Frommer says, which was launched in June 2023. Brokered loans close in Figure’s name. Brokers need to walk borrowers through some of the attributes of the loans “so that they can be doing the work that they need to do to truly be a broker,” Frommer explains, but then it is as easy as sending a link.

“If you get a loan with us, you have met those rules,” Frommer continues, “and there’s nothing that someone can do in terms of human intervention that can change those rules. We don’t allow for exceptions, so you have to have met those rules.”

Homogeneity means it does not matter who originates the loan; to investors, it all looks the same. An

investor who buys Movement’s loans or Guaranteed Rate’s loans does not need to understand new underwriting teams or processes because their loans are underwritten in the exact same way – through Figure’s rules engine.

What does change from partner to partner, Frommer explains, is average FICO credit scores, combined loanto-value ratios (CLTVs), or debt-toincome ratios (DTIs), on account of their customer base. These differences blend into different loan pools for securitizations.

A NEW SANDBOX, THE SAME TOYS

Frommer says that attracting more investors to the secondary market and reducing the cost to originate home equity loans has helped expand access to second-lien financing for borrowers across the mortgage industry.

But, the company is not angling for home equity lending dominance. “We actually saw a huge gap in the market,” she explains, “and nobody actually offering those loans in a way that worked for the customer and, quite frankly, worked for the originator, either.” Unlike the agency space, “originators aren’t necessarily comfortable originating loans if they don’t know the takeout’s going to be there,” explains Frommer.

Despite traditional underwriting for Non-QM loans being slightly more complex than for home equity, including more regulation due to their closed-end nature, Frommer says Figure has already developed many of the rules necessary for exporting their HELOC rules-engine to other nonagency spaces.

“There’s got to be some sort of market,” Frommer continues, “that develops where people have confidence in how these loans are underwritten.” Bringing the certainty of homogeneity to Non-QM originations will lower costs and risks, helping to attract more investors to Non-QM’s private-label secondary,

MORTGAGE BANKER MAGAZINE | MAY 2024 25

improving the cost and access to financing for borrowers.

“We’re going to focus on using our technology in the closed-end first lien space to originate sort of in the exact same way with our tech, in a homogenous way, where we can get investors comfortable that the loans all perform in the same way,” Frommer explains, the goal being, “no matter who originates them, the tech and the automation will drive the underwriting process and create that same homogeneity in the non-agency space.”

The fact that banks have pulled even further away from originating non-conforming loans only amplifies the opportunity for Figure to bring its tech to bear on Non-QM lending, originating and securitizing homogeneity in order to build liquidity into the market. Because Figure’s partners already use Figure’s technology for HELOCs, the comfort

with Figure’s process is already there.

“They allowed us to put new technology right into their organizations, and so they now have access to our technology, which can be easily modified to do a Non-QM loan,” Frommer says.

Here, too, the performance of Figure’s loans will serve as the basis for building investors’ confidence in non-agency loans originated with fully automated underwriting. With some fine-tuning over the next couple of months, Frommer expects to roll out a Non-QM product with fully automated underwriting “in the back half of the year, at least on a pilot basis.”

COMPETING IN AN AUTOMATED FUTURE

Differentiation can be difficult in the technology industry. It can be even more difficult in the lending industry. Everyone wants

something cheaper. But, cheaper usually comes at someone else’s expense, be it the borrower, originator, or lender.

Never does cheaper come at the cost to investors. A lack of liquidity in the secondary market only drives up costs in the primary market. Frommer says the long-term benefit of Figure’s efforts lies in making the non-agency market work more like the agency market.

“We’re creating a loan that is very easy for any investor to understand as long as it’s been originated with our tech because it looks like every other loan,” Frommer explains. “Similar to what exists in the TBA market with Fannie and Freddie, people can really get comfortable, hopefully, in the long run, buying a loan before it’s even originated.”

The strong emphasis on process now allows Figure to replicate that process in other markets, like Non-

26 MORTGAGE BANKER MAGAZINE | MAY 2024

QM and DSCR. Knowing what the loan will look like and how it will perform reduces many of the due diligence factors for investors and rating agencies. The impact of lowering these barriers is even greater in non-agency markets given the lack of government guarantees.

“We have a multi-stage process that we’re working on to create the TBA,” says Frommer. “The first one is getting a group of buyers comfortable buying all of our loans regardless of who our originators are and our common loan purchase agreement. We’ll probably have that done pretty soon. Then, ultimately, we’re going to introduce a guarantor structure and create something that looks much more like a traditional TBA that exists in the agency space.”

Where increasingly more companies are leveraging automation, few are leveraging blockchain. Even fewer are leveraging both, but Figure is one of them. The launch of Figure Markets – independent of Figure Technology Solutions – in mid-March came with the announcement of a new decentralized custody crypto exchange and blockchain-native security marketplace for trading in various digital assets.

Not only do investors trust Figure’s technology independent of the originator, “the fact that it was put on blockchain in an immutable fashion,” Frommer explains, “you can track all of the transactions and understand what has changed and what hasn’t changed” for individual loans and loan pools.

Storing loan transactions on the blockchain gives investors full transparency into loan performance, enhancing the ability to efficiently monitor and trade these assets in the secondary market. Frommer calls this “a big benefit” given Figures’ ongoing goal of creating a permanent capital structure for non-agency securitizations.

“It’s not something that’s going to happen overnight,” Frommer admits, “but the steps to it, I think, will happen relatively quickly.”

MORTGAGE BANKER MAGAZINE | MAY 2024 27

Utah’s top gathering for mortgage pros. Innovate. Educate. Motivate.

28 MORTGAGE BANKER MAGAZINE | MAY 2024

Do you have what it takes to reach the top?

Each year, the Utah Mortgage Show stages an extraordinary expo celebrating, advancing and supporting the men and women who finance residential and commercial real property. It is Utah’s largest and most comprehensive mortgage event. With top speakers, great hands-on sessions and a wealth of opportunities from exhibitors and sponsors, it’s a can’t-miss day for hundreds of Utah’s Amazing Mortgage Professionals.

MAY 8

SALT LAKE CITY, UT

Sheraton Park City Hotel Register for FREE with promo code MBMFREE

www.utahmortgageshow.com

Complimentary registration available to NMLS-licensed active LOs and their support staff. Show producers reserve the right to determine final eligibility.

PRODUCED BY

MORTGAGE BANKER MAGAZINE | MAY 2024 29

Secondary Strategies: Buydowns vs. Float Downs

Higher rates for longer complicate rate-reduction strategies

BY PREETAM PUROHIT, SPECIAL TO MORTGAGE BANKER MAGAZINE

When the Federal Reserve reduced the Fed funds rate to zero during the COVID-19 pandemic, an unintended consequence was the mass refinancing of mortgage borrowers to record-low mortgage rates.

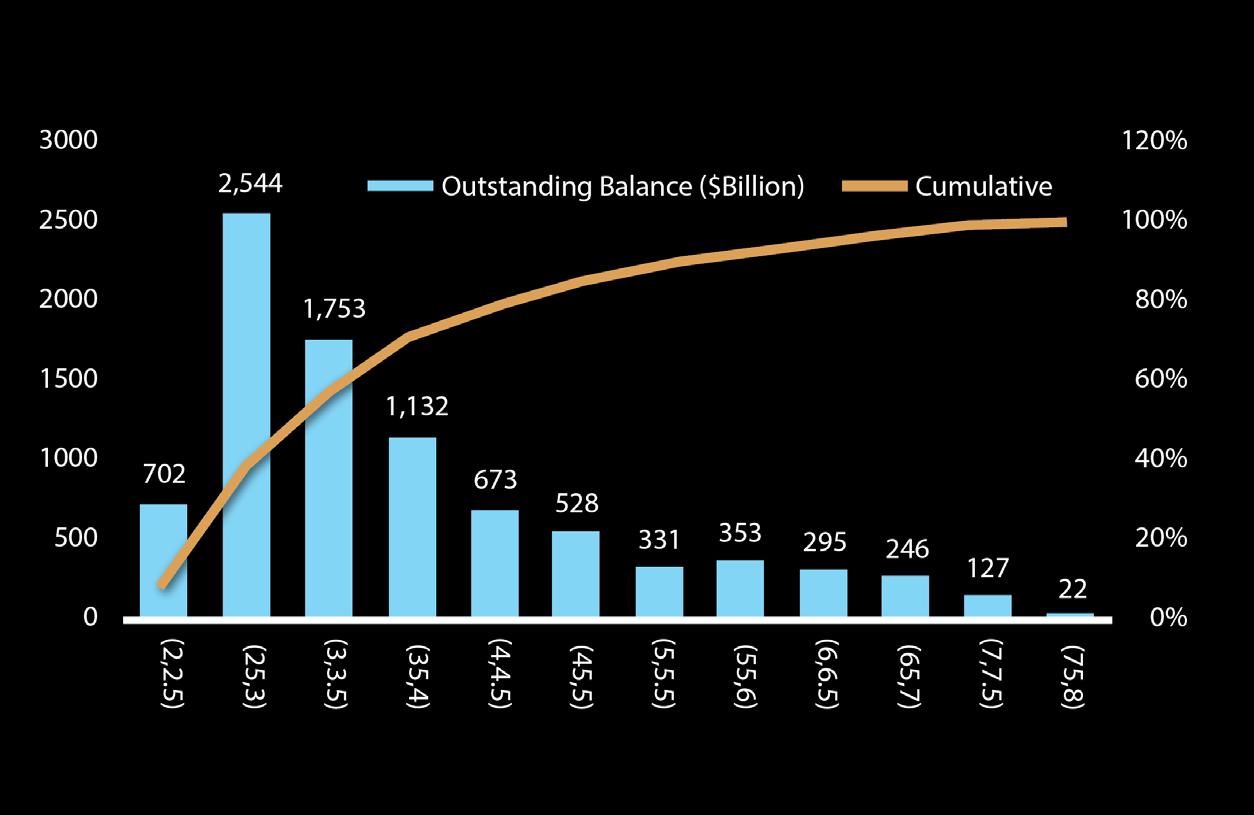

As seen in the distribution of weighted average coupons (WAC) in Chart 1, 70% of existing mortgages with outstanding balances have an interest rate less than 4%. This lock-in effect disincentives existing mortgage holders to sell their homes, exacerbating the shortage of homes for sale. The lock-in effect’s constraints on supply has contributed to the steady increase in home prices despite interest rates nearly doubling over the past two years.

This simultaneous increase in home prices and mortgage rates has led to the deterioration in borrower

affordability even in light of a strong economy and related wage increases.

According to the Mortgage Bankers Association’s (MBA) Purchase Application Payment Index, as of January, the national median monthly

mortgage payment had jumped to $2,134, an increase from December’s $2,055. As seen in Chart 2, the National Association of Realtors’ (NAR) Home Affordability Index is sitting at its lowest levels since

30 MORTGAGE BANKER MAGAZINE | MAY 2024

THE LOCK DESK

tracking began in the 1980s.

Though interest rate cuts would improve near-term and long-term affordability for borrowers by lowering costs for lenders and borrowers and likely increasing inventory, the Federal Reserve has signaled that interest rates will stay higher for longer, meaning affordability will remain lower for longer. In an elevated rate environment, mortgage rate reduction tools like buydown mortgages and rate lock float downs can help borrowers overcome near-term affordability barriers.

However, the use-case for these strategies are distinct. Considerations by investors in the secondary market limit the flexibility for lenders who want to offer these options, but first lenders must understand how the interest rate environment influences these rate-reduction strategies.

BUYDOWN MORTGAGES

To address the affordability crisis, lenders have introduced temporary buydowns to restore purchasing power to borrowers. A buydown mortgage provides borrowers with lower mortgage rates for a period of one to three years, depending on the product, which lowers borrowers’ monthly payments for that duration. By way of example, a 2-1 buydown

means the mortgage rate is reduced by 2% in the first year of the mortgage and 1% in the second year, before returning to the regular mortgage rate in the third year. The same logic applies to a 3-2-1 buydown, or a 1-0 buydown.

The mechanics of this rate reduction tool are simple: funds made available by the lender, builder, or seller are deposited into an escrow account to replace the reduced payments by the borrower. Lender- and builder-paid buydowns are more popular with borrowers because sellers usually negotiate concessions in the sale price of the property.

rate. So, a lender may lower a borrower’ mortgage rate from 7% to 6.25% for the first year, after which the borrower will pay 7.25%. In effect, the borrower is selling discount points instead of buying discount points (which entails paying the lost interest up front).

“With the temporary buydowns, I am able to provide the borrower with reduced interest and a reduced payment depending on the purchase price,” explains Brian Woltman, a branch manager with Embrace Home Loans. “The conversation is around refinancing the house in 2-3 years because there is optimism in the market that rates will eventually come down.”

An attractive feature associated with this loan is that any unused escrow funds can be used towards principal pay down by the borrower when refinancing the loan. “We have to be cognizant of circling back with borrowers in a year to hopefully get their payment to a steadier pace,” says Woltman.

RATE LOCK FLOAT DOWNS

Whereas buydown products enter the market to help affordability when rates aren’t expected to drop in the near future, rate lock float downs are

Borrowers purchase the float down option like a mortgage rate insurance policy –they are buying the option to “float down” their locked rate if mortgage rates do decline during the locking period.

> Preetam Purohit

Once the buydown period expires, the borrower is responsible for the full mortgage payment. The lender recoups the interest income lost by lowering the borrower’s initial rate by bumping up the post-buydown period

a better tool when rates may drop in 60-90 days, or when borrowers want peace of mind in the case of an interestrate rally during the lock period.

Signaling from the Federal Reserve about higher rates for longer complicates the conversation

MORTGAGE BANKER MAGAZINE | MAY 2024 31

with borrowers about float downs. However, because the market generally anticipates rate cuts to happen sometime this summer, float downs may be an effective strategy for locking-in borrowers who would otherwise hold out for mortgage rates to officially drop.

Borrowers purchase the float down option like a mortgage rate insurance policy – they are buying the option to “float down” their locked rate if mortgage rates do decline during the locking period. For this reason, float downs are most effective in conjunction with longer locking periods.

Like buydowns, the mechanism for offering rate lock float downs is simple: lenders charge an upfront fee that is typically 0.25%-1% of the loan amount. So, buying the float down option for a $400,000 loan would cost the borrower $1,000-$4,000. Depending on the lender, the option “activates” if mortgage rates drop by a set percentage (typically 0.125%-0.25%) during the locking period.

HEDGING RATE-REDUCED LOANS

Over the past few months, the share of buydowns issued by the governmentsponsored enterprises (GSEs), Fannie Mae and Freddie Mac, has been increasing, reaching roughly 6%-7% of all issued pools in January. It is a similar

story for government-insured issuance (FHA, VA, and USDA), with the share of buydowns increasing to 7.5% in January.

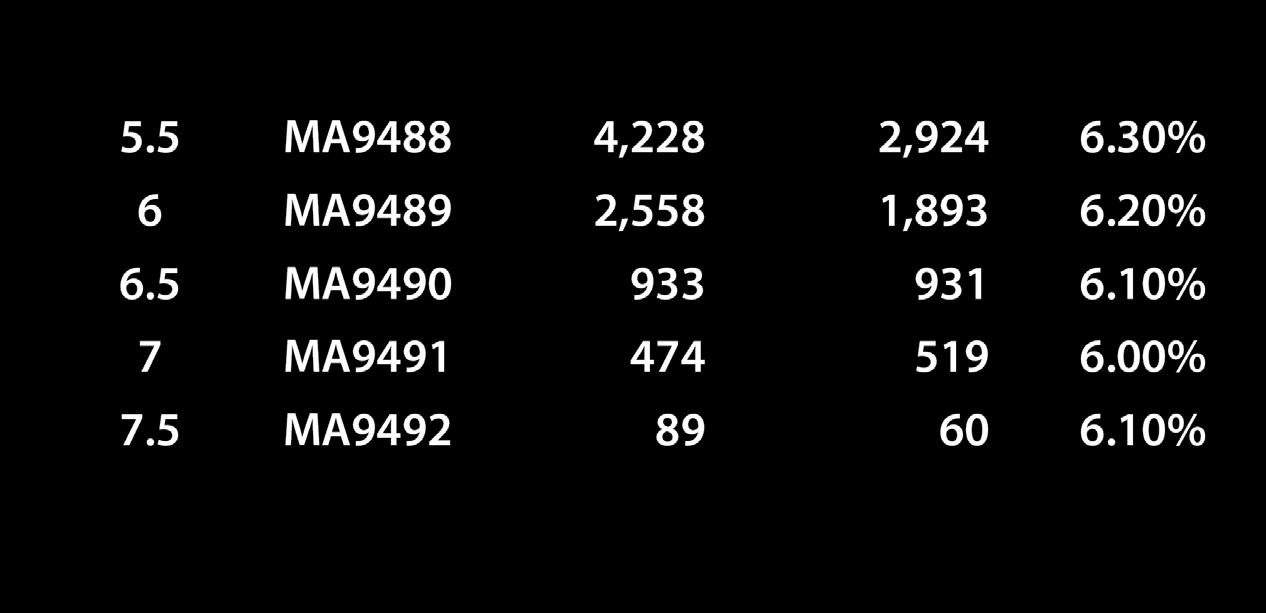

Chart 3 shows some of the liquid coupons from the latest issuance in Feb 2024.

However, not all loans can be bought down, and those restrictions on buydown mortgages are intended to limit investor risk. Because of these restrictions, not all lenders find it worthwhile to offer buydown options, given the rate environment and lenders’ core borrower base.

For example, all buydown mortgages have to be underwritten to the regular mortgage rate – the rate the borrower will pay at the end of the buydown period. Within the conventional universe, investor loans and cash-out refinance are not eligible for buydowns. Similarly, FHA buydowns are only available for fixed-rate purchase loans.

Seller buydowns come with their own risks for both the borrower and investors. If mortgage rates remain elevated, or even increase, the borrower will not be able to refinance the loan and their payment will increase at the end of the buydown period. Because many borrowers purchase buydowns with the intention of refinancing after the buydown period ends, investors should understand that prepayment risk is minimal during the buydown period, yet increases substantially after the

buydown period ends.

Although the share of buydown loans has risen recently, analysts do not see systemic risks arising from increased issuance so long as the share of new issuance does not exceed 10%.

Complexities associated with hedging float-down loans is a primary reason not every lender offers float down options to borrowers. Typically, float downs require the use of options on U.S. Treasury bonds (Treasuries) or mortgage-backed securities (MBS) to hedge – both of which have their own pros and cons as hedging tools.

While MBS options perfectly negate the interest-rate risk associated with float-down loans, they are an over-thecounter (OTC) product that requires dealer relationships and substantial minimum trading amounts. Treasury options, on the other hand, allow small trading amounts, but fail to completely offset the interest-rate risk, meaning lenders are still on the hook for the Treasury-Mortgage basis risk – which can be significant in highly volatile environments.

Preetam Purohit, CFA, CQF, FRM, is currently the head of hedging and analytics at Embrace Home Loans. He has more than 12 years of experience in fixed-income trading, hedging, analytics, risk management, and capital markets, with a focus on analytics, derivatives, and mortgage-backed securities. He previously worked at Hartford Investment Management Company (HIMCO) and the Federal Home Loan Bank of Des Moines (FHLB) and was one of NMP Magazine’s “40 Under 40” in 2023.

32 MORTGAGE BANKER MAGAZINE | MAY 2024

The Mortgage Star Conference for Women returns to the beautiful historic Hotel Monteleone in the heart of the French Quarter of New Orleans. This event brings together the stars of mortgage, for meaningful discussions, insightful presentations, and to celebrate one another. Then, stay for the Ultimate Mortgage Expo, free for Mortgage Star attendees.

MORTGAGE BANKER MAGAZINE | MAY 2024 33 *Complimentary registration available to NMLS-licensed active LOs and their support staff. Show producers reserve the right to determine final eligibility. NMLS Renewal class open to conference attendees only. Exclusive events and networking party are open to registered attendees only.

Star

— LIVE IN NEW ORLEANS —

Register for

Mortgage CONFERENCE FOR WOMEN

The most impactful event for mortgage women.

free with code NMPFREE mortgage-star.net

MBMFREE

JULY 10

10

Build your business in the Big Easy!

The Gulf Coast’s premier mortgage event, the Ultimate Mortgage Expo, returns to the stunning Hotel Monteleone in New Orleans. This year, enjoy 2x the exhibit hall, 2x the education sessions, and one incredible networking party.

Originators attend for FREE using code MBMFREE

The Ultimate Mortgage Expo happens in conjunction with the Mortgage Star Conference for Women

ULTIMATEMORTGAGEEXPO.COM Mortgage

*Complimentary registration available to NMLS-licensed active LOs and their support staff. Show producers reserve the right to determine final eligibility. NMLS Renewal class open to conference attendees only. Exclusive events and networking party are open to registered attendees only.

JUL

JUL

ULTIMATE MORTGAGE EXPO

11

VALVO VS BERMAN NEW EPISODES WEEKLY WHERE IDEAS GO HEAD TO HEAD EXCLUSIVELY ON WATCH NOW @WatchNMP