Source GDP Growth reached 6.42% accelerating in Q2, on track to meet target of around 6%

H1 2024 GDP expanded by 6.42% y-o-y showing positive signs of recovery

FDI reached US$ 15.19 bn, up +13.1% y-o-y (*) FDI inflows includes newly licensed capital only (**) Including Hong Kong

The PMI in June indicates an improvement in the health of the manufacturing sector and overall business conditions

Exports growth accelerated, recorded 14.5% growth y-o-y

Exports rebounded, thanks to a recovery in global demand

All key export groups recorded positive growth

Similar improvement recorded in import activities during H1 2024

International arrivals significantly improved in H1 2024

• 8.8 million arrivals in H1 2024

• +58.4% y-o-y and +11.4% comparing with pre-

South Korea and China are the two largest source markets for visitors to Vietnam

• Food and Food Products (+4.0% y-o-y)

• Housing, Electricity, Water, Fuel and Construction materials (+5.5% y-o-y)

• Education (+8.6% y-o-y)

• Healthcare (+7.0% y-o-y)

The average CPI in H1 2024 increased by 4.08% y-o-y Source

The 12-month term deposit interest rate is the average interest rate of the top 25 banks in the system

USD/VND VN Index Local gold

Bank deposit rate

petrol Condo rental yield

(*) Rental yield for selected high-end and mid-end condominiums, average of Hanoi and HCMC.

Source: SBV, VNDirect, SJC, VCB, Nymex, World Bank. Calculated by CBRE Research

The credit growth of the economy reached 4.45% by the end of Q2 2024

HCMC: Pressure from 2023 strong supply affects Grade A occupancy rate

Note: The asking rents and vacancy rates in Hanoi does not include TechnoPark Tower. Asking rents are exclusive of VAT and service charge.

Source: CBRE Research, Q2 2024.

HANOI: Vacancy rates only marginally improved

Source: CBRE Research, Q2 2024.

Source: CBRE Research, Q2 2024.

Note: Asking rents are exclusive of VAT and service charge. Asking rents and vacancy rates in Hanoi do not include TechnoPark Tower.

Source CBRE Research, Q2 2024.

Hanoi: Rents are flattening out

Source: CBRE Research, Q2 2024.

Hanoi Office - Asking Rents and Rental Growth

Hanoi Office - New Supply and Vacancy Rate

Note: The asking rents and vacancy rates in Hanoi does not include TechnoPark Tower. Asking rents are exclusive of VAT and service charge.

Source: CBRE Research, Q2 2024.

Vincom 3/2

District 10, Ho Chi Minh

Reopening after renovation, June 2024

NLA: 20,000 sqm

Vincom Megamall Grand Park

District 9, Ho Chi Minh

Grand opening June 2024

NLA: 36,000 sqm

NLA: 10,581 sqm VIETNAM

The Linc Park City

District Ha Dong, Hanoi

Grand opening Q1 2024

Parc Mall

District 8, Ho Chi Minh

Expected to open in Q3 2024

NLA: 44,450 sqm

AEON Xuan Thuy

District Cau Giay, Hanoi

Expected to open in Q3 2024

NLA: 18,000 sqm

Central Premium Mall

District 8, Ho Chi Minh

Expected to open in Q3 2024

NLA: 24,000 sqm

The Diamond Residence

District Thanh Xuan, Hanoi

Expected to open in Q3 2024

NLA: 14,000 sqm

Note: Asking rent is calculated for ground floor and first floor, excluding VAT and service charge. Source: CBRE Research, Q2 2024.

There is an increased demand from Chinese retailers, in particular F&B and Lifestyle brands.

More shopping malls are undergoing renovations and revamping their tenant mix to create space for new market entrants and ensure more experiences for shoppers.

Retailers with an existing CBD presence are looking at fringe CBDs or second tier districts in HCMC and Hanoi. 04

CBRE expects 2024F rental prices to continue increasing at a favorable pace in context momentum since 2022, +8-9% in Non-CBD areas, and +17-18% in CBD areas.

in Yen Phong 2A IP

Industrial Yen Phong Expansion by Frasers Property

Source: Ministry of Planning and Investment

Biggest Factory of Suntory Pepsico in Asia in Huu Thanh IP

Pegavision Factory in Green IPark Thai Bình

First Pandora Factory in VSIPIII Binh Duong

Record high in FDI Disbursement

Foreign Direct Investment (FDI) Disbursement in the First 6 Months of the Years 2020-2024

SK Factory in Deep C Hai Phong

Image: Thanh Nien, Dau Tu Chung Khoan VnExpress

Number of km of expressway completed by period

Number of km of express way completed in the South* accounted for 69% of the total completed expressway during 2023 2025F

(*): including South Central region, Southeast region, Mekong Delta region

Source: Ministry of Planning and Investment, Vietnamplus, Vnexpress Image: Tuoi Tre

Huu Nghi Chi Lang Expressway kicks start April 21st, 2024 1,163 km 16 years (2004 2019)

Cam Lo La Son Expressway

VIETNAM INDUSTRIAL MARKET

Industrial land records mild rental growth as absorption moderates

Industrial Land Rental Rates

Ready-built factories (RBF) continued to enjoy healthy absorption, while warehouses (RBW) recorded a strong 6-month in the Southern markets

Ready-Built Factory - Supply vs Absorption

Ready-Built Warehouse - Supply vs Absorption

Source: CBRE Vietnam, Q2 2024

*RBW excludes service warehouse

North - New Supply South - New Supply North - Net Absorption South - Net Absorption

Covered markets: South includes HCMC, Dong Nai, Binh Duong and Long An; North includes Hanoi, Hai Phong, Bac Ninh, Hung Yen and Hai Duong

Ready-Built Factory Rental Rate

Ready-Built Warehouse Rental Rate

*RBW excludes service warehouse

Covered markets: South includes HCMC, Dong Nai, Binh Duong and Long An; North includes Hanoi, Hai Phong, Bac Ninh, Hung Yen and Hai Duong

Source: CBRE Vietnam, Q2 2024

Outlook: Further growth is manufacturers demonstrate increased commitment to Vietnam, prompting additional RBF sub-developers to seek entry into Vietnam

Strong historical growth

Samsung

2008: First factory in Bac Ninh

2023: Factories in 3 provinces

Acc. Registered Investment Capital (*): ~US$22.4bn x33 Vs. 2008

LG

1994: First factory in Hung Yen

2023: Factories in 2 provinces

Acc. Registered Investment Capital (*): ~US$8.0bn x617 Vs. 1995

Foxconn

2007: First two projects in Bac Giang, Bac Ninh

2023: Factories in 5 provinces

Acc. Registered Investment Capital (*): ~US$3.2bn x19 Vs. 2007

To further expand

Source: Company information, public news

Goertek

2013: First factory in Bac Ninh

2023: Factories in 2 provinces

Acc. Registered Investment Capital (*): ~US$1.4bn x35 Vs. 2013

Samsung plans to add US$1bn to Vietnam investment annually

May 9th, 2024

LG will invest an additional US$3bn in Vietnam, expected to double the capacity of its Hai Phong factory

July 3rd, 2024

Foxconn to invest US$383mn in Vietnam

circuit board plant, says state media

June 24th, 2024

Goertek to invest another US$280mn in Vietnamese consumer electronics subsidiary

Jan 16th, 2024

Demand will Benefit from Rapid Expansion of Vietnam's Logistics, but Might Face Temporary Supply Abundance

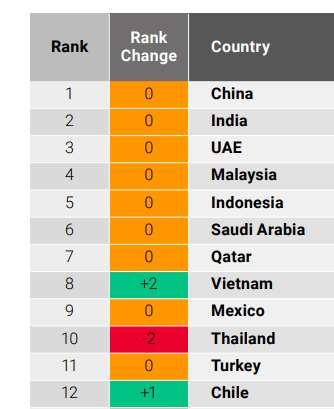

Vietnam's rank in the top Agility Emerging Markets Logistics Index 2024 continues to improve Market Size of Vietnam Freight and Logistics Industry

Market Size of Vietnam E-commerce Industry

Source: Modor Intelligence, Agility Emerging Markets Logistics Index 2024

Industrial Land, Forecasted New Supply and Rental Growth

Source: CBRE Research, Q2 2024

Tier 1: South includes HCMC, Dong Nai, Binh Duong, Long An and BR-VT; North includes Hanoi, Hai Phong, Bac Ninh, Hung Yen and Hai Duong.

Tier 2: South includes Binh Thuan, Tay Ninh, and Binh Phuoc; North includes Quang Ninh, Bac Giang, Vinh Phuc, Thai Nguyen, Ha Nam, and Thai Binh

RESIDENTIAL MARKET

HCMC: New supply in H1 2024 remained limited

accelerated in Hanoi; remained limited in HCMC in H1 2024

HANOI: Highest level of new supply in the last 5 years in H1 2024

• Affordable < 35 million VND per sq.m.

• Mid-end:35-60 million VND per sq.m.

• High-end 60-120 million VND per sq.m

• Luxuryandabove : >120 million VND per sq.m. New supply

+176% y-o-y

high-end and above units

Source: CBRE Research, Q2 2024. Note: HE

Strong buying momentum in Hanoi, with number of sold units in

Source: CBRE Research, Q2 2024

Source: CBRE Research

Nam Tu Liem district, Hanoi

Total launch: 2,200 condo units (Phase 1) LUMI HANOI | CAPITALAND

Thuy Nguyen, Hai Phong city

Total launch: >2,000 low-rise units

Nam Tu Liem district, Hanoi

Total launch: >1,100 condo units

Thu Duc City, HCMC

Total launch: >840 condo units

Nam Tu Liem district, Hanoi

Total launch: ~700 condo units

THU THIEM ZEIT RIVER | GS E&C

Thu Duc City, HCMC

Total launch: 40 condo & 10 low-rise units

VIETNAM RESIDENTIAL MARKET

PRIMARY MARKET

Prices of condominiums in Hanoi are quickly catching up with prices in HCMC in both primary and secondary markets

SECONDARY MARKET (*)

Source: CBRE Research, Q2 2024. Prices exclude VAT and maintenance fee. (*) Secondary market includes asking prices of all existing launched projects.

Landed property: After

Source: CBRE Research, Q2 2024

HANOI AND HCMC LANDED PROPERTY MARKET, AVERAGE PRICES, 2019 Q2 2024

PRIMARY MARKET

Prices of landed property in HCMC skyrocketed as new supply located in prime areas.

SECONDARY MARKET (*)

Note: Avg. apartment prices of Hanoi and HCMC are primary prices per sqm at the end of Q2 2024, including VAT and maintenance fee. Avg. apartment prices of other cities are retrieved from Numbeo in July 2024 for city center areas.

Source: Statista, Numbeo, CBRE Research, Q2 2024.

Demand: Investment purpose and the need for personal space are key reasons driving the intention of purchasing residential properties

Top 3 reasons driving properties purchase intentions in Vietnam (N=1,000)

Source:

~ 55,000 units

Lumi Hanoi (Phase 2) (Capitaland)

Nam Tu Liem

Expected launch: 2,000 units

The Matrix One (Phase 2) (MIK Group)

Nam Tu Liem

Expected launch: 1,000 units

The Metropolitan (Mitsubishi Corp.)

Gia Lam

Expected launch: >4,000 units

Vinhomes Global Gate (Vinhomes)

Dong Anh

Expected launch: 7,000 units (*)

Vinhomes Dan Phuong (Vinhomes)

Dan Phuong

Expected launch: 3,500 units (*) HCMC: ~ 35,000 units

The Global City (next phase) (Masterise Homes)

D2 (Thu Duc City)

Expected launch: 8,500 units (*)

Lotte Eco Smart City (Lotte Group)

D2 (Thu Duc City)

Expected launch: 1,000 units

Vinhomes Can Gio (Phase 1) (Vinhomes)

Can Gio district

Expected launch: 2,000 units (*)

Binh Trung Project (Phase 1)

(Khang Dien & Keppel Land)

D2 (Thu Duc City)

Expected launch: 900 units (*)

Zeitgeist (next phase) (GS E&C)

Nha Be district

Expected launch: 1,000 units (*)

Source: CBRE Research, Q2 2024.

Note: (*) Total estimated residential supply (including condominium and low-rise properties) from H2 2024 to 2026.

Forecast of new supply and sold units, Condominium, 2024-2026F

levels

In Hanoi, new supply in 2024 to double that in 2023 while primary and secondary prices expect a new peak.

In HCMC, new supply in 2024 to remain limited while primary and secondary prices continue to rise stably.

Forecast of average prices, Condominium, 2024-2026F

Average primary prices

Average secondary prices

Source: CBRE Research, Q2 2024

Forecast of new supply and sold units, Landed property, 2024-2026F

In Hanoi, new supply to improve in the second half of 2024.

In HCMC, new supply in 2024 to remain limited, while primary prices escalate by 20% y-o-y.

Forecast of average prices, Landed property, 2024-2026F

Source: CBRE Research, Q2 2024

Slowing down Bottoming out