19 minute read

E: sigvard.orts-jun@orts-gmbh.de W: www.orts-grabs.de T: +49 451 – 39885

source of synthetic graphite in battery production.

A little over 30% of the petcoke that is produced is sold into these higher valueadded markets for higher quality petcoke; the remaining production is used as a fuel source. The carbon-source-market share has been growing recently as demand in these markets has been growing faster than overall petcoke production.

Fuel-grade petcoke is used in a variety of industries — primarily as a substitute for coal, but sometimes for fuel oil. Petcoke has higher calorific value (i.e. kcal/kg) and much lower ash content than coal. However, it is more difficult to burn, has higher sulphur content, and is more difficult to pulverize6, so it typically sells at a discount to coal. The cement industry is the largest consumer of fuel-grade petcoke because cement kilns are particularly well suited to burn petcoke, and inherently capture approximately 90% of the sulphur oxides (SOx) emissions resulting from burning petcoke.

The next largest demand segment for fuel-grade petcoke is the ‘other industry’ category, which includes lime7, brick, calcium carbide, and glass production, as well as gasification of petroleum coke to produce chemicals (e.g., ammonia, urea ammonium nitrate, etc.). The remaining categories in declining market size are power generation, long-term storage, and iron & steel production. The ‘long-term storage’ category refers to petcoke produced as a by-product of upgrading bitumen (primarily Western Canadian oil sands) where the petcoke is placed underground as part of the reclamation process associated with the open cast (open pit) mining of bitumen.

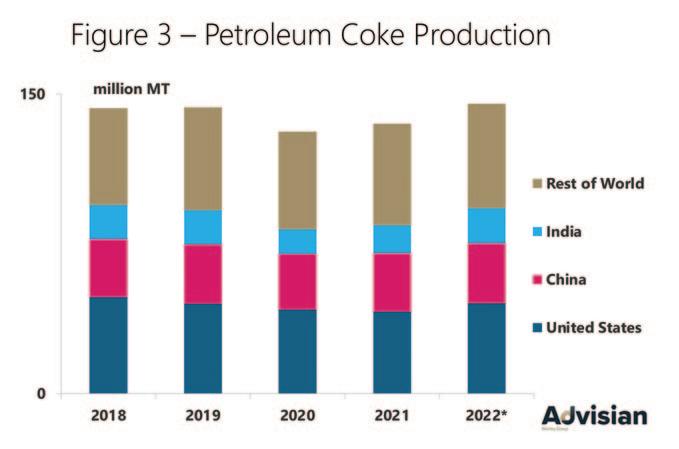

PETCOKE PRODUCTION TRENDS Global petcoke production is dominated by three countries — China, India, and the United States (see Figure 3 – Petroleum Coke Production). Production trends for these countries has been markedly different over the last five years. In 2019, global petcoke production was essentially the same as 2018 because increased production outside of the three top producing countries (Rest of World –ROW) was offset by reduced production by the US (–6%), while production in China and India was essentially unchanged. Because the crude slate for US coking got lighter due to increased tight light oil (i.e., shale oil) production, US petcoke production decreased. US tight light oil (TLO) has very few bottoms and produces very low quantities of petcoke per barrel crude oil.

Going into 2020, the refining industry was expecting that bunker demand for the consumption of high-sulphur residual fuel oil (HS RFO) would plummet to comply with MARPOL 20208. The maritime industry consumed 3.2‒4.0 million barrels per day (180‒230 million tonne/year) of high-sulphur residual fuel oil (HS RFO) in 2018 and 2019, and this market was important to many refineries as an outlet for their HS RFO. It was expected this reduced HS RFO demand would cause a glut of HS RFO, and the price discount of HS RFO, in contrast to crude oil prices, would increase significantly.

Since coking economics tends to improve when the discount of HS RFO to crude oil increases, it was expected that coking economics would be very favourable and petcoke production would be robust. This briefly turned out to be the case as US Gulf Coast (USGC) petcoke production rose significantly during the fourth quarter of 2019 and in January and February of 2020.

Then governments around the world began implementing shelter in place orders (i.e., lockdowns) to control the Covid-19 pandemic. This caused refined product demand to decrease significantly, though, at first it was not entirely clear just how much demand was going to drop overall. As commercial passenger air travel plummeted, automobile use fell (especially for commuting), industrial production slowed, and freight traffic declined, demand for refined products rapidly fell. Consequently, refinery utilization rates (a.k.a. run rates) were reduced to match refined product production with reduced demand, and globally petcoke production fell by 8.5%.

However, not every region of the world

[6] Coal (and petcoke) is typically pulverized to approximately the consistency of talcum powder to facilitate the pulverized (suspension) fuel combustion process used in the power, cement, lime, and many other industries. [7] Lime kilns are very similar to cement kilns and have the same inherent capabilities to successfully burn petcoke like cement kilns. [8] MARPOL 2020 refers to the International Maritime Organizations’ MARPOL (International Convention for the Prevention of Pollution from Ships) Annex VI, Regulation 14 rule limiting sulphur oxide (SOx) emissions globally from seaborne vessels that went into effect 1 January 2020.

was impacted equally in 2020. Production decreases varied regionally as lockdown strategies were significantly different from country to country. Petcoke production decreases ranged from 5% (ROW) to 28% (India) depending on the extent of lockdowns and start-up of new cokers in ROW.

Global petcoke production rebounded (+3.0%) in 2021 as Covid-19 lockdowns eased but remained below 2018 and 2019 levels. India was key to the global rebound as its petcoke production increased by 14%. China and ROW production increased each increased 5% while US production decreased 4%. Much of the US production decrease was caused by weather events including Arctic Storm Uri in Texas and Hurricane Ida in the Louisiana Gulf Coast.

OPEC+ PRODUCTION CUTS — SURPRISINGLY IMPORTANT TO PETCOKE In April of 2020, OPEC+ members struck a historic deal to cut their combined crude oil production by 9.7 million bbl/day during May and June of 2020. They also agreed to reduce their production cuts to 7.7 million bbl/day (i.e., increase production by 2.0 million bbl/day) from July 2020 through December 2020. In January 2021 OPEC+ increased production by 0.5 million bbl/day, then continued with uneven monthly production increases until by July 2021 when production was 1.9 million bbl/day higher than in December 2020 (monthly production cut reduced to 5.8 million bbl/day).

These crude oil production cuts were especially important to the petcoke market because OPEC producers tend to preferentially cut heavy oil (which trades at a discount to lighter crude oils) production to maximize revenue from reduced oil production. As we noted previously (see Petcoke Background), migration to lighter crude oil also means less petcoke will be produced from each barrel of crude. It took some time for the impact of OPEC+’s production cuts to work its way through the crude oil market before the OPEC+ production cuts impacted refinery crude slates as huge inventories were built in March 2020. However, in time, crude slates became lighter, and less petcoke was produced. For example, USGC refinery utilization in March 2020 was 90.2%. Following Arctic Storm Uri, USGC refinery utilization had recovered to 87.5% by April 2021 but petcoke production was 10% less than in March 2020.

From August 2021 through June 2022 OPEC+ members continued increasing production evenly by ~0.4 million bbl/day monthly, then by ~0.65 million bbl/day in July and August 2022 leaving no more production cuts still in place. OPEC members claim to have slim spare capacity, and we do not expect significant changes in the global crude slate gravity (i.e., weight) due to OPEC production increases going forward.

Global petcoke production is forecast to increase 9% in 2022, driven by very strong growth in India and strong growth in the US. India’s production increase is driven by sharply increased refinery utilization rates and migration to heavier crude slates due to OPEC+ production cuts being phased out. The US production increase is driven by increased refinery utilization rates, migration to heavier crude slates, and assumption that there will be no unusual weather-related production outages in 2022 like there were in 2021.

IMPACT OF RUSSIA/UKRAINE CONFLICT With the onset of Russia’s invasion into Ukraine, a coalition of countries (EU, Canada, US, Japan, Australia, and Singapore) imposed numerous sanctions on Russia, including a ban on importing Russian oil (crude and products). Russian crude oil exports to these countries declined quickly, though the timing of when a full ban will go into effect varies. In the case of the EU, a complete ban goes into effect at the end of 2022 or early 2023, depending upon the category of imports. US President Biden issued an Executive Order on 8 March, banning the import of Russian oil, liquefied natural gas, and coal into the United States. The ban has had little impact on US petcoke production other than causing the sulphur content of petcoke produced at a few refineries to increase.

Initially, the sanctions of Russian oil supplies were expected to severely dent global crude oil supply, but this has not materialized. Increased exports of Russian oil to China and India have negated lower exports to countries imposing sanctions. India and China are taking advantage of highly discounted Russian oil due to sanctions. The US EIA in its latest report expects Russian oil production to average 10.85 million bbl/day in 2022, compared to an average of ~10.8 million bbl/day in 2021, which implies sanctions have had virtually no impact on Russian crude oil production. OPEC in its latest monthly report also shows a similar story by predicting Russian oil supplies to average 10.88 million bbl/day in 2022. Using the US experience as a guide, we expect that the ban on Russian crude oil will have minimal impact on petcoke production other than some shifts (down as well as up) in petcoke sulphur content.

COAL AND PETCOKE PRICES The coal market is important to the petcoke market because fuel-grade petcoke typically is a substitute for thermal (steam) coal. The seaborne thermal coal market is approximately 25 times larger than the seaborne fuel-grade petcoke market, so the petcoke market cannot meaningfully impact seaborne thermal coal prices. On the other hand, thermal coal prices act as cap on petcoke prices as buyers will switch from petcoke to coal if petcoke is not economically attractive vis-à-vis coal ($/MMBtu delivered basis).

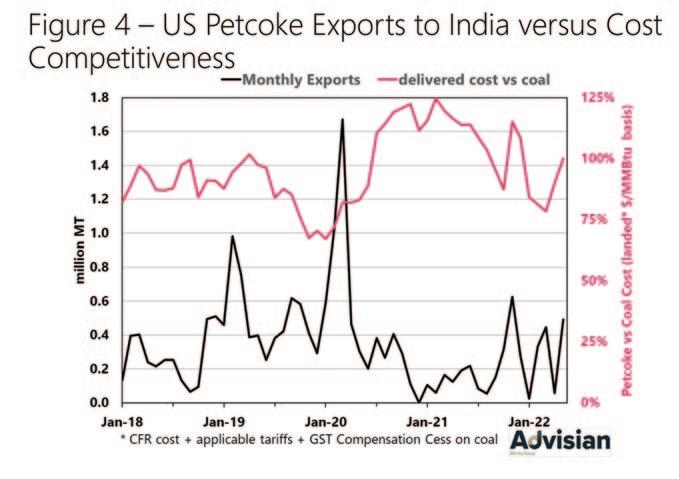

The primary market for imported fuelgrade petcoke in India is the cement industry which will quickly switch between thermal (steam) coal and petcoke, depending on relative economics (see Figure 4 – US Petcoke Exports to India versus Cost Competitiveness). For example, USGC petcoke was at a significant discount to coal ($/MMBtu landed9 basis) from October 2019 through January 2020, and exports to India increased dramatically in February and March of 2020. Conversely, from July 2020 through September 2021 petcoke was more costly than thermal coal, and export volumes were very low.

As USGC petcoke production has recovered to more typical levels it has become necessary for some USGC petcoke to be sold into India.

COAL MARKET- REMARKABLY DISJOINTED Prices for traditional ‘marker’ thermal coal prices (e.g., Northwest API2, South African AP4/RB1, Australian Newcastle) have soared to historical highs. The primary driver appears to be anticipation of a supply shortage due to sanctions on Russian coal imports into the EU. On 8 April 2022, the EU announced its fifth package of sanctions against Russia in response to its invasion of Ukraine, under which all deals for Russian coal had to be finalized by April 9 and all Russian coal imports had to be completed by August 10, 2022. The ban was applicable to all coal and solid fuels originating from Russia. In 2021, Russia accounted for 43% of EU coal imports. The market appears to be expecting the continent will fall short of coal once the coal ban is in full force.

Further, the natural gas crisis in Europe has also impacted the coal market by encouraging additional thermal coal demand to cover for the shortfall in natural gas supplies. Responding to sanctions, Russia demanded payment for natural gas in rubles. Some countries objected and Russia stopped natural gas supplies to Poland, Bulgaria, the Netherlands, and Denmark, plus severely curtailed supplies to Germany through the Nord Stream 1 (NS1) pipeline. In response, some European nations restarted mothballed coal-fired power generation. Consequently, several international agencies expect European thermal coal demand in 2022 to increase 5–10% Y/Y.

While European coal demand is poised to rise in 2022, India coal imports could easily exceed Europe’s increased seaborne thermal coal demand. While India’s total coal imports of all-types during the first seven months of 2022 are only up by ~8 million MT (+6%), the Indian government is planning to import an additional ~76 million MT of thermal coal during Indian Fiscal Year 2022-2023 (1 April 2022 –31 March 2023). These planned coal imports will be over and above the normal imports.

However, coal imports by China, which imported 324 million MT of coal in 2021, have slowed in 2022. During the first seven months of 2022, China’s total coal imports fell by 18% Y/Y (~30 million MT). China has ramped up its domestic coal production significantly and is on pace to produce ~7–9% (+285-365 million MT) more coal in 2022 than in 2021.

Discounts for 5,500kcal/kg vs. 6,000kcal/kg ‘marker’ Australian and South African coal prices are at unprecedentedly high levels. Historically, increasing discounts have been an indication of weaker underlying demand. Another sign that suggests benchmark thermal coal

prices are inflated is the fact thermal coal prices are significantly higher than coking coal prices, which is unprecedented and surprising since coking coal is higher quality than thermal coal. Meanwhile, discounts for Russian Baltic and Black Sea coals vs. Northwest European thermal coal (i.e., API 2) are within the range of 60–70%.

Like the ban on importing Russian oil, the ban on importing Russian coal has had more impact on where Russian coal is exported than on the volume of Russian coal being exported. Russian coal has been exported at heavily discounted prices to many countries including China, India, and Turkey.

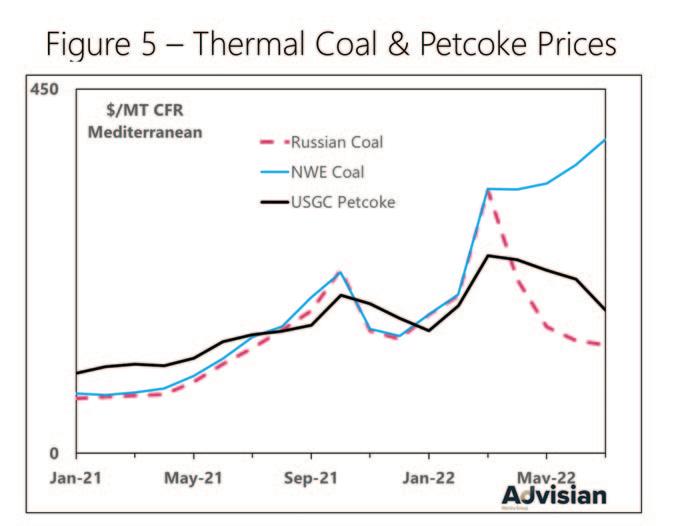

IMPACT ON PETCOKE MARKET Recently USGC petcoke prices have appeared to be very attractive compared to traditional ‘marker’ coal prices. However, in key Mediterranean markets such as Turkey, USGC petcoke also has to compete against heavily discounted Russian coal (see Figure 5 – Thermal Coal & Petcoke Prices). It is this competition that has constrained upward movement of USGC petcoke prices. Additionally, petcoke has lost market share to Russian coal in the Mediterranean market, leaving additional volumes of USGC petcoke to be sold into Asia (principally India).

LONGER TERM OUTLOOK – PETCOKE MEGATRENDS Developments in specific industries as well as the evolution of the energy transition are expected to significantly shape the petcoke industry going forward. We refer to these developments as petcoke megatrends and are summarized as follows: v Pace of the energy transition from oilbased transportation fuels to renewable fuels and electric vehicles. v Repurposing of petroleum refining assets to renewable fuel. v Increased demand for battery production to support increased use of electric vehicles and renewable power generation. v Growth in aluminium production (primary and recycled). v Inert anode (also known as ‘carbon free’) aluminium smelting technology (eliminates current need for calcined petcoke in consumable anodes).

Each of these trends will have a different impact on petcoke production or consumption and the net effect will determine the future course of petcoke. These megatrends will be discussed in more detail at our upcoming 21st Annual Petcoke Conference.

Ben Ziesmer (Senior Adviser)

Ben is a widely recognized authority in global petroleum coke consulting. He successfully led Advisian’s Fuel Grade Petcoke practice for many years and now acts as a senior advisor to the team. Ben continues to be a key contributor to Advisian's Pace Petroleum Coke Quarterly, as well as providing support to single client consulting projects, the annual Advisian Petcoke Conference and other Advisian petcoke related publications.

About the authors

Pedro Mackay (Principal Consultant)

Pedro has 29 years of experience working in various energy-related fields such as oil exploration, solid fuel purchasing and trading including petroleum coke and coal, ocean freight chartering, consulting in the petroleum coke industry, and raw materials purchasing in the coke calcining industry. Through his career, Pedro has held responsibilities focused on purchasing and supply chain aspects related to solid fuels for cement plants and raw materials for calciners, solid fuel trading, ocean shipping, and consulting. He holds a bachelor’s degree in Mechanical Engineering from the University of Texas at Austin and a Master’s in International Management from Thunderbird.

Rituraj Jha (Consultant)

Rituraj is Mumbai-based consultant for Houston Market Services team (Advisian) and is a contributing author for Advisian’s Pace Petroleum Coke Quarterly© (PCQ) and Calcined Petroleum Coke Report© (CPC). He is also involved in numerous petroleum coke market studies and is the team’s regional expert on Indian petroleum coke market. Background-wise, Rituraj is a chemical engineer from one of India’s top engineering colleges, with a specialization in petroleum refining.

Advisian (formerly Jacobs Consultancy, Inc. and previously The Pace Consultants, Inc) has published the Pace Petroleum Coke Quarterly© since 1983. The report has been published monthly since January 1985 and is considered the global authoritative source of petcoke market information.

Hudig & Veder can safely be described as a one-stop-shop for logistics solutions. The company specializes in the worldwide transport and storage of various types of cargoes such as (dry) bulk, breakbulk and project logistics.

Knowledge and experience are crucial pillars of Hudig & Veder’s services, and are a big part of the success of the company. However, developments in the IT field also play a big part. Examples of this include setting up processes as efficiently as possible, and realizing data links with customers.

Hudig & Veder was founded in 1795, since which time it has grown into the logistics giant it now is. Every day, about 100 people are hard at work at different divisions: Chartering; Bulk; Forwarding; and Agencies. With its head office centrally located near the Port of Rotterdam, but supported by global partners and through joint ventures in the Middle East and Europe, Hudig & Veder can offer services on a global scale. Customers can trust that their business is taken care of through perseverance and creativity. Customers know that they can rely on Hudig & Veder to provide them with fitting solutions for all their logistical challenges. ABC-CONCEPT The Hudig & Veder ABC-concept consists of optimal co-operation and short communication lines between the divisions: Agencies, Chartering and (Break) Bulk. Therefore, at the drop of a hat, complete and full services can be offered and custom-made logistical plans can be provided. One of those services is warehousing. Hudig & Veder has its own warehouse in the Laurens harbour in Rotterdam. In various other collaborations with partners, terminal and storage

services for incoming and outgoing cargo flows for break-bulk and project cargo can also be offered. These include: v customs formalities and transfer via all modes of transport; v loading and unloading of barges and seagoing vessels; v transshipment; and v loading of containers and special equipment. CREATIVITY IS MUST Creativity is an important requirement for ‘At Hudig & Veder we prefer the teams at Hudig & Veder. It is used effectively to provide the best logistical a personal approach’ answers to the customer’s needs. Furthermore in the maritime business, flexibility is key. A good team and an international network are both important in such circumstances. Fortunately, all the Hudig & Veder teams have the knowledge and experience to deal with all circumstances in the right way. This is why the high quality of service that Hudig & Veder’s customers are used to, and have grown to expect, can be guaranteed.

OUR ABC-CONCEPT

As Hudig & Veder Group, we are keen on creating an ultimate logistical plan for our customers by combining different departments and disciplines within our ABC-concept.

Our ABC-concept can therefore be best described as an existing supply chain under control of Hudig & Veder. Agencies, Chartering, Forwarding, Bulk & Projects, we offer the optimal collaboration between our business departments.

Fairplay Towage Group, a major European tugboat operator with over 100 tugs in operation, has placed an order with Damen Shipyards Group for two Damen RSD tugs 2513. The vessels will be delivered in January 2023.

The twin-fin Reverse Stern Drive (RSD) Tug 2513 is one of Damen’s most capable and innovative harbour tugs with excellent seakeeping behaviour, superb manoeuvra bility and outstanding towing character istics, with a maximum of 80 tonnes bollard pull. As one of Damen’s Next Generation Tugs Series, the RSD tug 2513 also has a focus on offering increased safety, sustainability, reliability and efficiency.

Fairplay’s new tugs will be equipped with powerful render recovery winches with auto tensioning systems, as well as FiFi1-rated fire-fighting systems. Fairplay has also voluntarily opted for immediate IMO Tier 3 compliance by specifying Damen’s Marine NOX reduction system with its advanced active emissions control system using SCR (selective catalytic reduction).

The vessels were already in production at Damen’s specialist tug building facility, Damen Song Cam Shipyard, Vietnam, when the order was placed, ensuring the rapid delivery. Other factors in Fairplay’s decision to source its latest vessels from Damen included their design and quality and the Damen Triton digital platform for the optimization of operational efficiency. Joschka Böddeling, Damen Sales Manager, said: “We are very pleased to be supplying Fairplay with these state-of-the-art tugs. Fairplay has operated Damen-built vessels for many years and we were delighted when last year they purchased a Shoalbuster 2711 for general operations in the North and Baltic seas. This latest contract further reinforces the co-operation between our two companies.”

Arkadiusz Ryz, Fairplay Towage Polska, said: “We are delighted with this order which is connected to our last year purchase in Damen. Thanks to strong connection with our clients, we actively respond to the growing market needs with highest quality and efficiency available. Those two highly manoeuvrable and highperformance new modern tugs will strengthen our fleet and co-operation with Damen.”

DAMEN SHIPYARDS GROUP — OCEANS OF POSSIBILITIES Damen Shipyards Group has been in operation for over 90 years and offers maritime solutions worldwide, through design, construction, conversion and repair of ships and ship components. By integrating systems, Damen creates innovative, high-quality platforms, which provide customers with maximum added value. Damen’s core values are fellowship, craftsmanship, entrepreneurship and stewardship. Its goal is to become the world’s most sustainable shipbuilder, via digitalization, standardization and serial construction of its vessels.

Damen operates 35 shipyards and 20 other companies in 20 countries, supported by a worldwide sales and service network. Damen Shipyards Group offers direct employment to more than 12,000 people.

IS YOUR CARGO COVERED?

Cygnus Hatch Sure Ultrasonic Hatch Cover Tester • Reliable Solution For Hatch Cover Weathertightness Tests • Accepted By P&I Clubs And ABS Type Approved • Powerful And Robust Transmitter SAVE 10%