How will the commercial property market develop in 2025? Comprehensive market survey among real estate stakeholders

International Poul Erik Bech

For 10 consecutive years, EDC Poul Erik Bech has conducted a large and comprehensive market survey on expectations for the commercial property market in the year ahead. The survey is the largest in the industry and is based on input from nearly 1,800 respondents regarding their outlook for 2025.

What is the outlook for the commercial property market in 2025?

The outlook for the commercial property market in 2025 appears more optimistic compared to last year’s survey. Overall, there is a renewed investment appetite among the nearly 1,800 respondents, largely driven by expectations of further interest rate cuts in 2025. At the same time, sustainability is once again a growing focus, while uncertainty remains about the future path of inflation in 2025. These are just some of the key findings from EDC Poul Erik Bech’s expectations survey, now in its 10th consecutive year and recognized as the largest and most comprehensive survey in the commercial property industry.

For the 10th consecutive year, we at EDC Poul Erik Bech have conducted our large, comprehensive market survey, attempting to gain insights into the future of the commercial property market. This year, nearly 1,800 industry players from the real estate sector have responded to the survey, which covers everything from expectations for various property types, interest rates, sustainability, and the new public valuations.

Joseph Alberti, Head of Research at EDC Poul Erik Bech, says: ”This year, we are setting a new participation record, with nearly 1,800 respondents taking part in our expectations survey. Overall, there is a much greater sense of optimism among the participants. Compared to last year, when darker clouds loomed over the commercial property market, there is now a much stronger confidence in the market for 2025.”

”One of the major differences from last year is the interest rate. This year, 87% expect falling interest rates in 2025, while 10% anticipate stable rates. Despite the majority expecting a rate decrease, 68% still consider interest rates to be the primary challenge for the commercial property market in the year ahead, confirming that interest rates remain the key issue in the industry. In addition, loan conditions and opportunities are also a significant concern, with 67% emphasizing their importance.”

Uncertainty about inflation

Expectations regarding the inflation outlook for 2025 are one of the most divisive issues among respondents. 38% expect inflation to decrease, 51% expect it to remain unchanged, while only 11% predict an increase in inflation in the coming year, which surprises Joseph Alberti:

”The survey was conducted in September and October 2024, when inflation was at 1.3%, which is relatively low. Given that the ECB aims for inflation to hover around 2% in the medium term, it is somewhat surprising that 38% of respondents expect inflation to decrease further in 2025. Our expectation is that inflation will stabilize and likely increase slightly, bringing it closer to the 2% target by the end of 2025.”

Sustainability regains focus

For the past four years, sustainability has been a key topic in our expectations survey, and this year is no exception. The responses indicate that sustainability is once again

a major focus for the respondents. According to Joseph Alberti, this shift may be due to the market facing greater challenges last year:

”Last year, sustainability stagnated in our expectations survey, which was somewhat surprising. However, we must consider that the year was characterized by widespread challenges in the industry, including high interest rates, inflation, and rising construction costs, which likely pushed sustainability down the agenda for many property stakeholders. This year, however, we can clearly see that sustainability has once again become a central focus. We also believe that sustainability will play an increasingly significant role in the property market as regulations tighten and more companies are required to report on their sustainability efforts.”

Joseph Alberti, Head of Research

EDC Poul Erik Bech

Facts about the respondents

In the 10th edition of the Expectations Survey, 1,795 respondents participated, marking the highest number in the 10 years we have conducted the survey. 62% of the respondents report that they invest in properties not intended for their own use. This is in line with previous years, with 59% in 2024 and 63% in 2023.

The geographic distribution of respondents is spread across the entire country. 26% are from Copenhagen/Frederiksberg or the Greater Copenhagen area. 11% of respondents are based in Aarhus, and the same percentage applies to Southern Jutland. Next is North Zealand with 10%, followed by South/West Zealand and East Jutland, both with 9%. 1% of respondents are based abroad.

Nearly half of the respondents represent companies with 2-25 employees, and 35% are from sole proprietorships. 10% come from companies with 26-100 employees. Together, these account for 90% of all respondents, which is not surprising, considering that small and medium-sized enterprises make up the vast majority of all Danish companies. 10% of respondents come from companies with more than 100 employees.

The distribution of respondents, both geographically and in terms of number of employees, helps provide a nuanced picture of property stakeholders’ expectations for the year ahead.

Do you invest in properties that are not for own use?

Where is your company currently located? If you have offices in multiple locations across the country, please refer to the office where you are located.

Investment profile

Where are you currently investing?

What

profile of properties do you invest in? (Choose as many as apply)

There has been no significant change in expectations regarding the types of properties respondents are investing in this year compared to next year. However, it is notable that all three property profiles have seen a significant increase compared to the 2023 survey. This suggests that investment interest has grown over the past few years, both in low-risk properties with stable cash flow and in opportunistic properties, where the risk is higher.

How large is your company’s total investment capacity?

What type of property/space do you currently use for your business?

Market prices

What are your expectations for the development of market prices in the coming year for …

Residential rental properties

The most significant change compared to last year is in residential rental properties, where 43% expected falling prices last year, compared to just 9% this year. This is a decrease of 34 percentage points. In contrast, the expectation for rising market prices has increased from 16% last year to 55%, marking the first time since 2019 that more than half of respondents expect market prices to rise.

Office properties

The trend for office properties is similar, though not to the same extent. There has been a decrease of 31 percentage points, while 21 percentage points more expect stable prices, and 10 percentage points more expect rising prices. However, the majority still expect stable market prices, which reflects the trend seen before the downturn in the real estate market.

Warehouse and logistics properties also experience a decline, with 35% in 2024 expecting falling market prices, compared to just 18% this year. Nearly half expect stable market prices, while 33% anticipate rising prices for warehouse and logistics properties.

The outlook is least positive for retail properties, with 60% expecting falling market prices, compared to 71% last year. There has been a small increase of 3 percentage points in the share expecting rising market prices for retail properties.

Market prices on commercial lands

Market rent

What are your expectations for the development of market rents in the coming year for ...

In general, respondents are slightly more positive about market rents compared to their expectations for this year. In three out of the four property segments, the proportion expecting rising market rents has increased, with residential rental properties seeing the most significant rise.

A total of 96% expect either rising or stable prices, the highest level we have seen in the past four years. Compared to the last two years, the proportion expecting falling prices has significantly decreased, from 15% in 2023 to 12% in 2024. Overall, respondents have had expectations of either rising prices or stable market rent over the years, but this year, 57% expect market rents to increase, which is 17 percentage points higher than the expectations for 2024.

Regarding market rents for office properties, respondents do not expect significant changes. 62% expect market rents to remain unchanged. It is worth noting that there are 11 percentage points fewer respondents expecting falling rents, while those anticipating rising rents have increased from 16% to 18%. Therefore, the number of respondents expecting either falling or rising market rents for office properties is nearly equal, with over half expecting little change.

Office properties

Residential rental properties

There has been little change in market rents for warehouse and logistics properties compared to last year’s survey. Just over half of the respondents expect rents to remain stable, while nearly a third anticipate an increase in market rents.

Market rents for retail properties stand out when compared to other property segments. Only 8% expect an increase in market rents, while half of the respondents anticipate a decline. The remaining respondents expect stable rents, which clearly indicates that retail properties are expected to face the most difficulties in 2025. A trend observed over the past few years.

Vacancy

What are your expectations for the development of vacancy rates in the coming year for ...

In general, there are no significant expectations for vacancy rates to change in either direction throughout 2025. It is only within retail properties that the majority of respondents expect vacancy rates to increase. For the other property types, the expectation is for the status quo, at least according to the responses from the majority of respondents.

Residential rental properties

There has been an interesting development in expectations regarding vacancy rates for residential rental properties. The percentage of respondents expecting a decrease in vacancy rates has increased by 12 percentage points, while the percentage expecting an increase in vacancy rates has decreased by 17 percentage points. This suggests that there is greater interest in residential rental properties compared to the past few years. This could be due to the fact that, in many areas, there has been limited new construction relative to the high demand, meaning supply has only slightly increased while demand remains higher.

Office properties

There has been only a slight shift in expectations regarding vacancy rates for office properties. As in the previous year, only 12% expect a decrease in vacancy rates, while 33% anticipate an increase. However, this represents a 10 percentage point decrease from last year, when 43% expected a rise in vacancy rates. More than half of the respondents, however, do not expect significant changes in vacancy levels.

Warehouse and logistics properties are the most stable property segment compared to expectations for vacancy rates in the previous survey. Similar to last year’s survey, 56% expect vacancy rates to remain unchanged. There has been a slight increase of 1 percentage point in the share expecting a decrease in vacancy rates, and a corresponding 1 percentage point decrease in those expecting an increase.

Retail is the only property type where a majority of respondents expect an increase in vacancy rates. This is not surprising, as it has been the most challenged sector in recent years, particularly due to e-commerce. However, it is worth noting that the proportion of respondents expecting higher vacancy rates has decreased from 66% in 2023 to 51% in 2025, while the share expecting stable vacancy rates has risen. This could suggest that the retail sector is moving towards a gradual stabilization.

Economic development

What are your expectations for the development of inflation in the coming year?

Following last year’s survey, where more than half of the respondents expected inflation to decrease, the majority now anticipate that inflation will remain unchanged in 2025. Furthermore, 38% expect inflation to decline further, while 11% expect an increase in inflation during 2025.

This is a surprising development, considering that the survey was conducted in the fall of 2024, when inflation stood at 1.3%. The ECB aims for inflation to reach around 2% in the medium term. Therefore, it is somewhat unexpected that more respondents do not anticipate inflation to rise in 2025. Our expectation is that inflation will remain relatively stable, with a slight increase over the course of 2025, bringing it closer to the 2% target.

What are your expectations for the development of interest rates in the coming year?

Interest rates have been a major topic in the commercial property market over the past couple of years, and for good reason. We’ve seen significant increases in rates over the last two years, but it now seems that the interest rate level has peaked and are beginning to decline. There is a strong expectation that rates will fall throughout 2025 – in fact, 87% of respondents anticipate a decrease in interest rates, while 10% expect rates to remain unchanged.

Over a 10-year period, expectations for interest rates have seen significant fluctuations. In our first Expectations Survey conducted in 2016, only 2% expected interest rates to decrease. This was largely due to the fact that in early 2015, the central bank had reduced rates to as low as minus 0.75%. At that time, 77% expected the interest rate level to remain unchanged, and this was the general expectation during the first 3-4 years of the Expectations Survey between 2016-2019. During this period, only a few expected rates to decrease further, while more and more anticipated rate increases, which peaked in 2019 when 41% expected rising interest rates.

In the outlook for 2020 and 2021, it was once again anticipated that the interest rate would remain unchanged. However, this outlook shifted in the expectations for 2022 and 2023, where over 60% expected rates to rise. This prediction proved accurate, likely due to the fact that long-term interest rates began rising in 2021, after having generally declined with only minor fluctuations since the 2008 financial crisis.

After a few years of rising interest rates, it became more difficult to predict the direction of rates in the expectations for 2024, which was reflected in last year’s survey. In that survey, 30% expected rates to decrease, 28% believed rates would rise, while the remaining 42% anticipated no change. The interest rate in 2024 has largely remained unchanged, although several rate cuts occurred in the autumn, which most likely influences respondents’ expectations for 2025, where more than 97% expect either falling or unchanged interest rates.

Investment

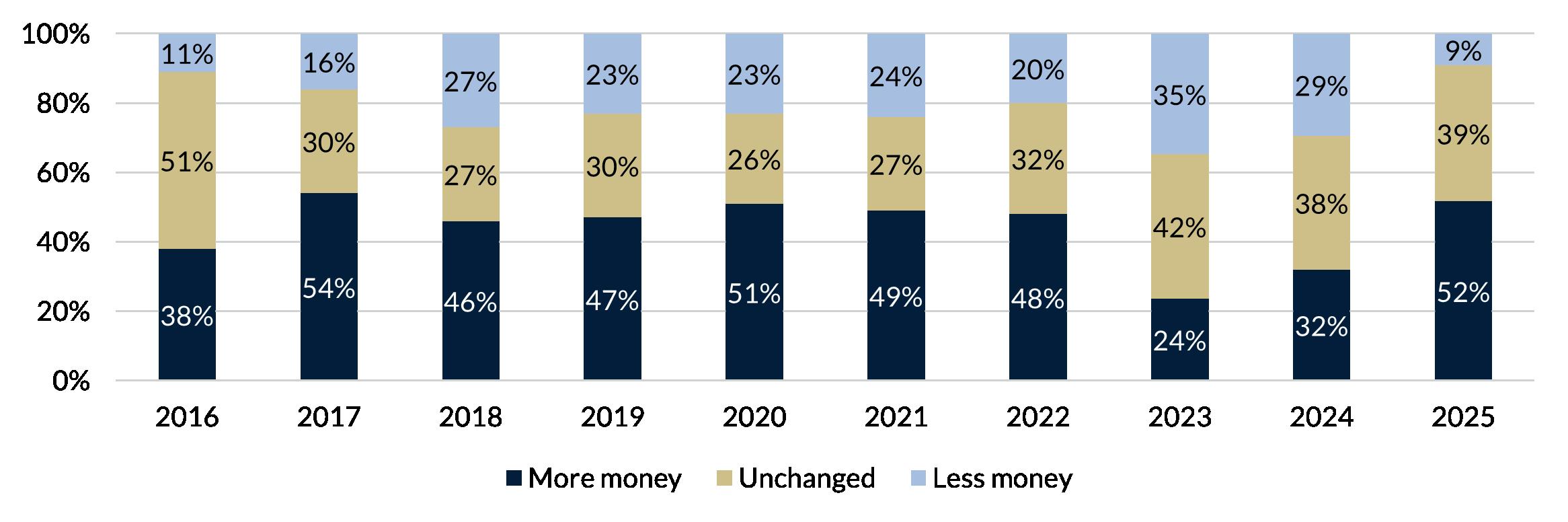

Do you plan to spend more/less money on real estate investments in the coming year?

Overall, the sentiment in the commercial property market has shifted, with more respondents than in the past 8 years expecting to spend more on property investments in the coming year. At the same time, only 9% expect to spend less, the lowest level in the 10 years we’ve conducted our Expectations Survey. This reflects a notable optimism in the commercial property market, particularly compared to expectations for 2023, when more respondents anticipated spending less. Additionally, when compared to expectations for 2024, the distribution across the three categories was much more evenly spread.

What types of properties are potential investments for you in the coming year?

(Choose as many as apply)

There have not been significant changes regarding which property types are considered potential investments. Residential rental properties remain the most popular property type by far. Overall, housing plays a dominant role, as four of the five most popular property types are related to residential real estate.

What areas do you expect to invest in the coming year? (Choose as many as apply)

Aalborg

Odense

Aarhus

Copenhagen/ Frederiksberg

Financing

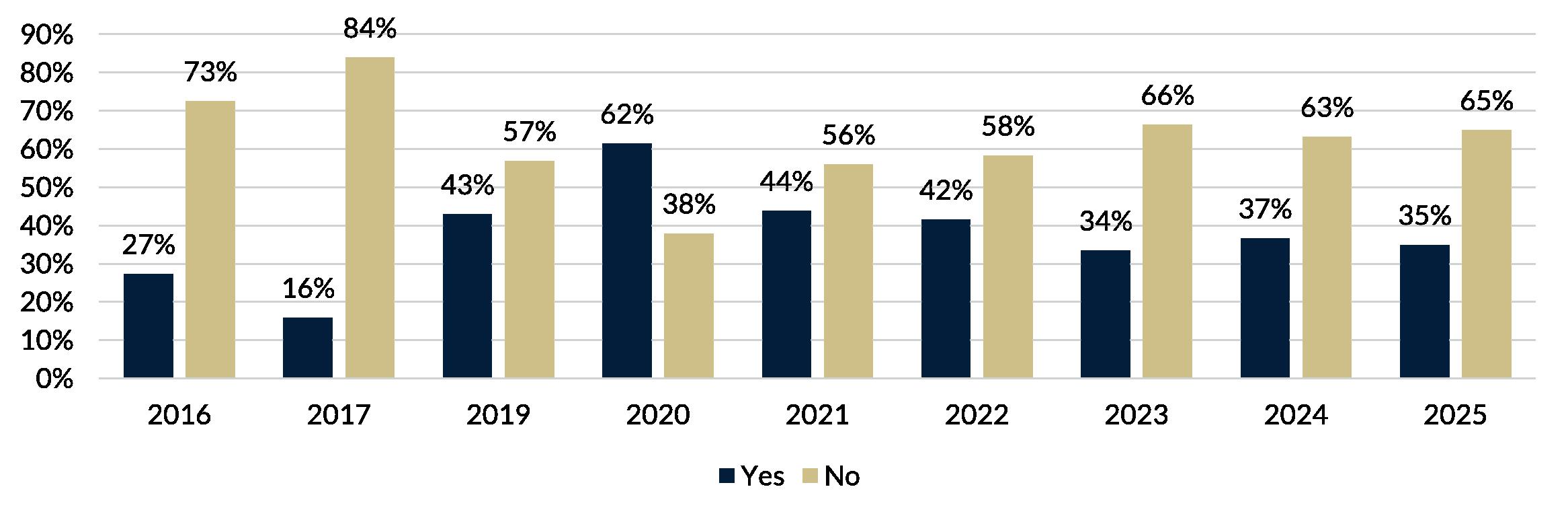

How do you perceive the opportunities to obtain financing for real estate investments in the coming year?

Over a 10-year period, the majority of respondents have consistently indicated that obtaining financing has become progressively more difficult compared to the previous year. Between 2016 and 2022, 60-72% of respondents expected that financing opportunities for property investments would remain the same as when the survey was conducted. However, in the expectations for 2023, there was a significant increase in the percentage of respondents anticipating that securing financing would become more challenging.

In the 2023 expectations, 78% of respondents anticipated that obtaining financing would become more difficult. However, this outlook has improved significantly since then. This year, 23% believe that financing opportunities for property investments in 2025 will be more challenging than they are today, while 20% expect them to improve. The remaining 56% predict that the conditions will remain unchanged in 2025.

We appear to be returning to the period before the property sector’s challenging times, when approximately 60% of respondents anticipated that financing opportunities would remain consistent with the conditions at the time of the survey.

The sharp shift in 2023 can likely be attributed to the elevated interest rates during that period.

To own or rent

Do you own or rent the primary premises you use?

Would you consider selling your premises to rent something instead?

Would you consider buying something instead of renting?

Premises requirements

Do you expect to spend more/less money on commercial premises?

Do you expect changes in your needs of premises?

(E.g. relocating, expanding to new premises, or downsizing to smaller premises)

What are the reasons for changes in premises requirements? (Choose as many as apply)

What is most important to you when choosing premises? (Choose as many as apply)

Sustainability

In general, there is an expectation that sustainability will be more prominent in 2025 than previously anticipated for 2024. This is reflected in the share of respondents who have a policy that sustainability should play a role in the selection of premises, their willingness to pay more for sustainable premises, and the number of respondents who have considered optimizing their properties for sustainability.

It was somewhat surprising that sustainability figures stagnated in last year’s Expectations Survey, but many in the commercial property sector were likely focused on the broader challenges, such as high interest rates, inflation, construction costs, building materials, etc. As a result, sustainability was deprioritized. However, this year’s figures indicate a continued increase in the focus on sustainability. With EU taxonomy, legislation, and other regulations on the horizon, large companies, in particular, will need to increasingly focus on sustainability and implement clear policies in this area.

Does you or your company have a policy that sustainability should play a role in the selection of premises?

In last year’s surveys, over 80% of respondents did not have a policy in place regarding sustainability’s role in the selection of premises, and the development had stagnated around that point. This year, however, there has been a significant increase of 11 percentage points, with 30% of respondents now stating that they have a policy where sustainability is incorporated.

It is worth noting that it is particularly office, educational, and clinic properties where 40% of respondents state that sustainability is part of the policy when selecting premises. In contrast, 25% report having a policy in place requiring sustainability to play a role in the selection of their warehouse, production, or industrial properties. However, 41% indicate that they have considered it, which suggests that sustainability is an area that has expanded to all property types or is at least in the process of doing so.

Does sustainability play a role for you in relation to your current investment strategy?

After decreasing from 59% in the 2023 expectations to 53% in the 2024 expectations regarding the proportion of respondents for whom sustainability plays a role in their current investment strategy, the share of respondents has increased again in the 2025 expectations, with 63% answering yes. This is the highest proportion in the four years we have asked about sustainability.

Have you/your company considered optimizing your property/properties in terms of sustainability? E.g. energy renovation

Sustainability

Are you willing to pay more for a sustainable property, assuming the location, condition, and cash flow are the same?

To what extent do you believe that tenants are willing to pay more for sustainable rental properties in ... (Compared to rental properties with the same location, size, and condition)

To what extent do you believe that future property tax or other property-related fees will be influenced by the property’s sustainability, including, for example, the type of energy label?

To what extent are you or your company willing to pay more for sustainable rental properties in ... (Compared to rental properties with the same location, size, and condition)

To what extent do you believe that properties will become less marketable due to low ESG ratings?

New public valuations

This year, we have asked respondents about their views on the new public valuations, which have been a significant topic in the property market over the past year. Not surprisingly, there is an expectation that these new valuations will influence the pricing of commercial properties in 2025. There is not much difference between residential rental, office, industrial and logistics, or retail properties in this regard.

To what extent do you believe that the new public valuations will impact the pricing of commercial and investment properties?

Generally, around 20% of respondents across different property types do not believe that the new public valuations will impact the pricing of commercial properties. This means that nearly 80% expect the new public valuations to influence pricing in 2025, with residential rental properties being the highest (80%).

Residential rental properties

Office properties

Warehouse-/logistics properties

Retail properties

In cases where the new valuations result in significant increases in property tax, for example in the largest cities, to what extent can the increase be passed on to tenants?

If the new public valuations lead to significant increases in property taxes, approximately 60% of respondents across various property types believe that the increase can, to some extent, be passed on to tenants. At the same time, it is worth noting that retail properties have the fewest respondents who believe the increase can be passed on to tenants, with 25% of respondents stating that they do not believe the increase can be attributed to tenants in the case of retail properties.

To what extent have the new public valuations affected your investment strategy?

Significant challenges

What do you consider to be the most significant challenges for the real estate market in the coming year? (Choose as many as apply)

Despite broad consensus that interest rates will decline in 2025, 68% of respondents identify interest rate developments as a significant challenge for the commercial property market in the year ahead.

Meanwhile, 67% highlight lending conditions and opportunities as a concern, and 47% expect construction costs to present a major challenge for the sector.

Furthermore, 39% and 28% point to increased regulation and the new public valuations, respectively, as critical challenges for the commercial property market.

ESG and sustainability are seen as obstacles by 22%, while 19% consider geopolitical uncertainties among the most pressing challenges in the coming year. Climate change is flagged as a significant issue by 16% of respondents.

Finally, 3% identify other factors as the primary challenges, citing examples such as rising vacancy rates.

Background of the survey

For 10 consecutive years, EDC Poul Erik Bech has conducted a large and comprehensive market survey on expectations for the commercial property market in the coming year. The survey is the largest in the industry and is based on the expectations of nearly 1,800 respondents for 2025.

EDC Poul Erik Bech’s Expectations Survey is celebrating its 10th anniversary this year. Over the past decade, the majority of the questions have remained the same, providing a solid overview and enabling comparisons with the results of previous years’ surveys. Our Expectations Survey offers a historical perspective on how industry professionals foresee the development of the commercial property market. As a result, large parts of the survey are based on findings from previous years’ surveys.

For the fifth consecutive year, sustainability and ESG have been included in the survey framework. Given that sustainability is a key focus in the real estate industry, it remains relevant to continue exploring how respondents expect sustainability to evolve year after year.

This year, 1,795 respondents participated in our survey, which was primarily distributed through EDC’s comprehensive database of Danish businesses, property investors, and tenants. In addition, data collection was carried out through networks and social media campaigns targeted at professionals in the industry with an interest in property investment. The responses were gathered between September 20 and October 16, 2024.

The respondents include professionals from investment firms, law firms, banks, logistics companies, retail businesses, and more. An investor is defined as someone who invests in properties with the aim of generating a return, rather than for personal use.

The survey reflects the respondents’ expectations for the market, and EDC Poul Erik Bech’s own views are not included in the survey. However, to some extent, we do comment on the survey results, and our views will be expressed during the final seminar on Expectations for 2025.

Not all results in the survey add up to 100%, as some questions allow for multiple answers.

Are you curious about how the commercial property market is developing locally, or are you looking for concrete data on vacancy rates, rent levels, yield requirements, or demographic conditions in relation to a construction project or your next real estate investment?

CityFact collects all relevant market data into one analysis product distributed across 20 geographical areas. Choose the areas that interest you, and we will keep you informed about the developments in the area.

Research & Analysis

EDC Poul Erik Bech’s Research & Analysis department provides customized analyses for both large institutional investors and private investors. We have carried out projects for clients including PFA, PensionDanmark, PenSam, Coop, COPI Group, and Salling Group, offering services such as due diligence on the buyer’s assessment of the seller’s properties before finalizing a transaction. Our tasks include, among others:

• Commerciel Due Diligence

• All relevant aspects of project development, as well as the purchase and management of investment and owneroccupied properties

• Analyses for, for example, lawyers requiring data for residential property litigation

• Analyses of rent levels and realized transaction prices

• Analyses of the supply and demand dynamics in major cities as well as smaller provincial towns

• Analyses of housing stock trends based on ownership types in specific, defined geographic areas

Joseph Alberti Head of Research

joal@edc.dk +45 5858 7467

Niclas Holm Research Manager

niho@edc.dk +45 5858 8784

CONTACT

EDC Poul Erik Bech

Zealand/Funen

Copenhagen +45 5858 8378

Herlev +45 5858 8376

Taastrup +45 5858 8472

Hillerød +45 5858 8377

Roskilde +45 5858 8395

Køge +45 5858 8379

Næstved +45 5858 8380

Slagelse +45 5858 8396

Odense +45 5858 8397

Jutland

Kolding +45 5858 8399

Aabenraa +45 5858 8425

Sønderborg +45 5858 8422

Esbjerg +45 5858 8398

Vejle +45 5858 8423

Aarhus +45 5858 8670

Silkeborg +45 5858 8427

Herning +45 5858 8567

Viborg +45 5858 8424

Aalborg +45 5858 8449

Vendsyssel +45 5858 8487

International +45 5858 8563

Research +45 5858 8564

Agriculture East +45 5858 8574

Agriculture West +45 5858 8683

Project +45 5858 8487

Capital Markets +45 5858 8572

Be the first to know when new properties come up for sale

We have Denmark’s largest buyer/tenant register. If you haven’t found the right property yet, let us help you!

Create your personal wish in our nationwide buyer/tenant register, and be the first to know when new properties come up for sale. We screen all properties for you and only show you the properties that match your wishes.