Rachel Jordan frames life’s best stories with just a lens and a little magic.

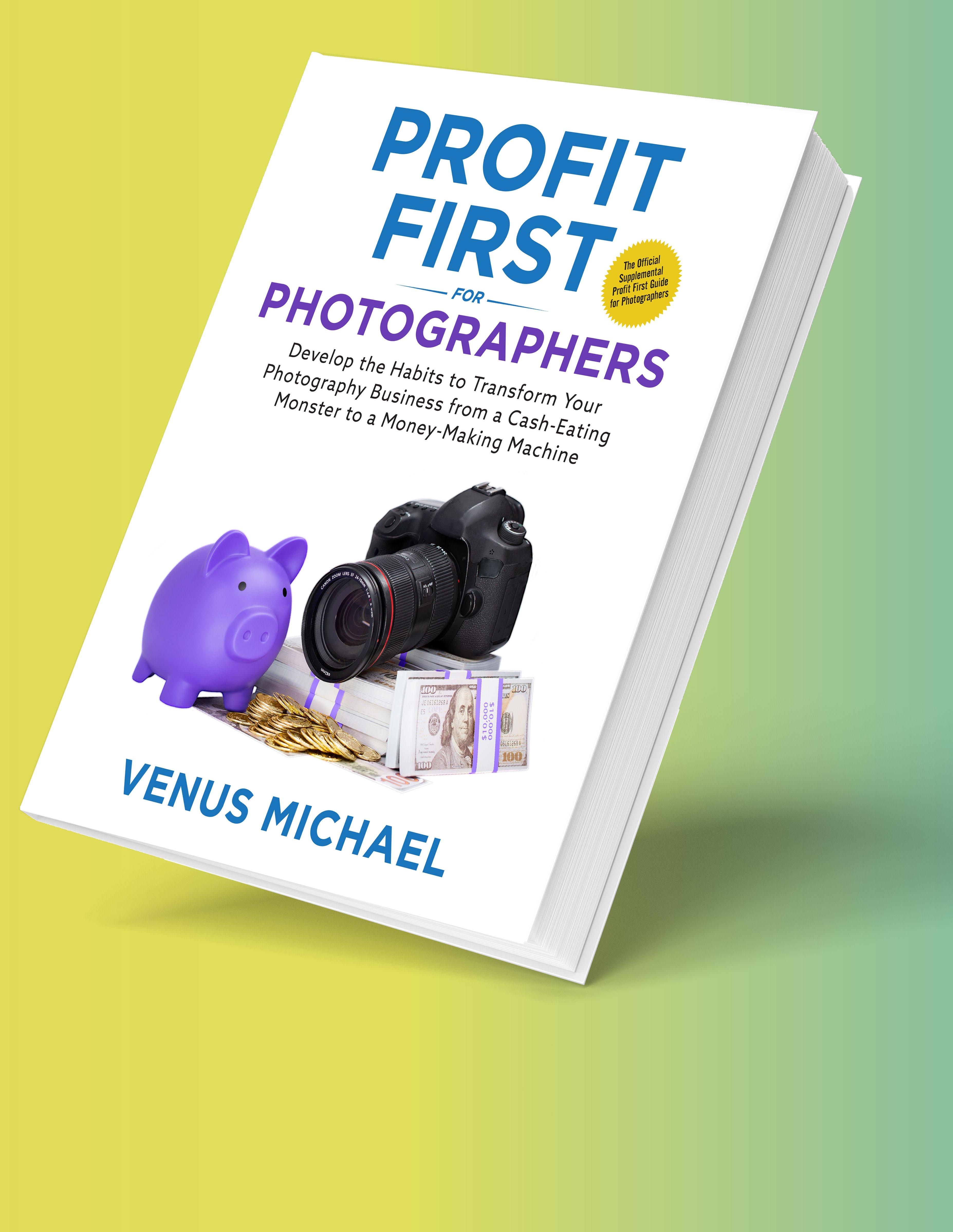

The Wait is Over. Now Available

16

FAMILY MATTERS

Compassion, fun, and family—the lens through which Rachel Jordan thrives.

10 ABILITY

So you want to write a book 10 insider tips on navigating the process.

Trends

Cash flowCrisis, Senior Scams and The Dog Days of Summer.

PERSON ABILITY

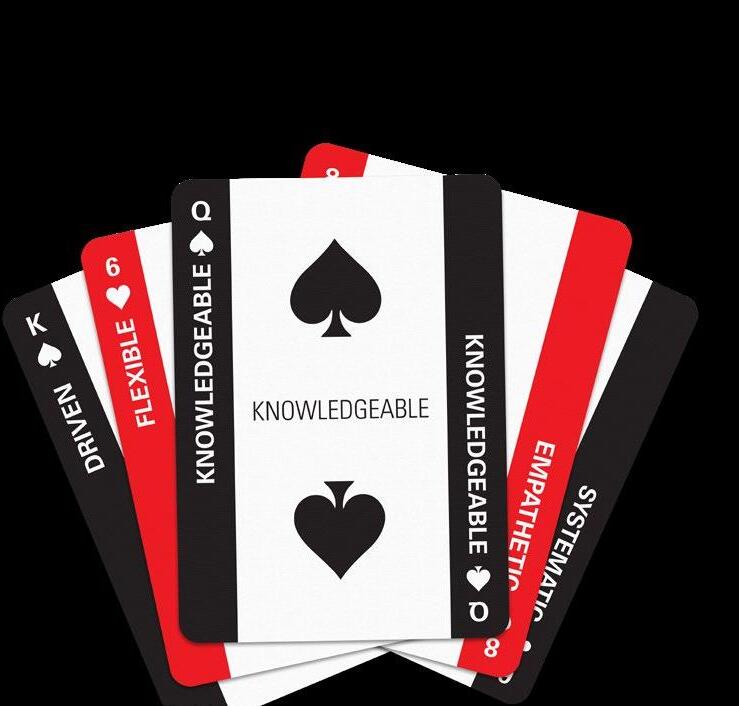

Stephen Shapiro Personality Poker yields a winning hand.

Ask Venus Answers to real bookkeeping questions from real clients.

PROFITABILITY

The Big Picture

This exclusive book excerpt helps unlock the CEO mindset.

Unlocking Growth

How to use AI to grow your photography business. 24

TRADITIONAL FORMULA

In this model, your business’s profits are whatever money will be left over. It’s simple in theory, but it is more likely to leave you with less profit—if you have any at all.

Why? Because you’re human, and humans aren’t good at keeping leftovers. If you have food to eat, you eat it. If you have money to spend, you spend it.

PROFIT FIRST FORMULA

What you need is a formula that prioritizes your profit, so that you know at the beginning of the year how much money you want left. By deciding up front how much you want to have at the end of the year, you force yourself to find ways to get the same things done for less money.

THIRD QUARTER 2024 VOLUME 2 NUMBER

Venus Michael Owner, Small Business Development Expert

I didn’t get to seclude myself in a private cottage in an exotic locale to churn out words like it was my job. No. I actually had a job. This full-time hustle I call One21 Account-Ability. And writing the book was supposed to increase the profitability of my business. It would be a lead magnet like none other. It would set me apart from the rest. It would open doors.

That was 20 months ago now. Nearly two years. And let me tell you, most days it was like stepping into a boxing ring—a fierce, messy, and deeply bruising personal battle. I walked into it with a sense of purpose, thinking I was ready to take on the world. But almost immediately, I was met with resistance—the kind that comes from within, where every doubt and insecurity you’ve ever had rises up to meet you.

I’d sit down to write, and the inner critic would start shouting, “Who do you think you are? What makes you think you have something worth saying?” The blank page became a battlefield where I fought to silence that voice, to push through the fear that I wasn’t enough. It was brutal. There were days I wanted to walk away, to believe that maybe this wasn’t my fight.

And honestly, I did step away for a while. The book languished for a few months while I nursed my battered ego and insecurities.

But then, I remembered why I started. I wasn’t writing to be perfect; I was writing to be real. To tell the truth, my truth, in all its raw, unpolished glory. So, with a whole lot of encouragement from my friends, my mentors and the editor of this little magazine, I decided to show up, even on the days when I felt like a fraud. I let the words spill out, messy and imperfect, because that’s what it means to be human. That’s what it means to live fully.

Finishing that book was a victory, one that I celebrated on July 9th when Profit First for Photographers was officially born into the world. At least according to Amazon. It isn’t a best-seller, at least not yet, but the copies that have sold are influencing lives and businesses just as I imagined it would. And it was my personal victory. I had faced myself, fought my way through the doubt and fear, and come out on the other side with something real, something true. And that, to me, was everything.

“But then, I remembered why I started. I wasn’t writing to be perfect; I was writing to be real. To tell the truth, my truth, in all its raw, unpolished glory.”

REMARK ABILITY

So you want to write a book

Venus’s top 10 tips on navigating the process

signed up for a rollercoaster of caffeine-fueled nights, blank page standoffs, and sudden bursts of inspiration at the most inconvenient times—like in the shower or at 3 am. Your plot will twist, your characters might rebel, and at some point, you’ll question all your life choices. Just kidding. Kind of.

From my experience, writing a book isn’t just about stringing words together; it’s about wrestling with ideas, confronting your doubts, and somehow creating something beautiful out of the chaos. It’s hard, it’s messy, and some days it might feel impossible, but when you finally

hold that finished manuscript in your hands, you’ll know it was all worth it. So, grab that pen, and let the adventure begin!

Decide to Begin: Writing a book isn’t just something you do—it’s a commitment to yourself. Decide that your voice matters, that your story deserves to be told, and that you’re going to show up for it, even when it’s hard.

Set a Routine: Writing is like training for a marathon—you need to show up regularly to build strength. Set aside specific times to write, even if it’s just 30 minutes a day. Honor that time as sacred.

Embrace the Mess: Writing isn’t about perfection; it’s about

truth. Allow yourself to write badly. Let the words spill out without judgment. The mess is where the magic happens, so lean into it.

Hire a Writing Coach: Sometimes, you need someone in your corner who can see your potential even when you can’t. (I used AJ Harper, and and I don’t regret it!) A writing coach can help guide you through the tough spots, keep you accountable, and provide the encouragement you need to keep going. They’re there to help you shape your voice, refine your story, and remind you that you’re capable of writing the book you’ve dreamed of.

Silence the Inner Critic: Your inner critic will try to convince you that you’re not good enough, that you don’t have anything worth saying. Recognize that voice, and then tell it to sit down and shut up. You’re in charge here, not your fear.

Write for Yourself First: Don’t worry about who will read your book or what they’ll think. Write for yourself. Write the book that you need to read, the one that comes from deep inside you. Let it be your truth, your story.

Take Breaks, But Don’t Quit: There will be days when you feel stuck, when the words don’t come. It’s okay to step away, to take a break, but don’t let that turn into quitting. Return to the page, even if it feels impossible.

Edit with Love: When it’s time to revise, approach your work with love and compassion. Don’t tear it apart—nurture it. Ask yourself, “How can I make this stronger, clearer, more true?” But always remember that your words, even in their rawest form, are worthy.

Hire a Good Editor: When you’ve poured your heart into your manuscript, the next crucial step is finding a good editor. A skilled editor will not only catch the small errors but will help you shape your story into its best possible form. They’ll challenge you to dig deeper, clarify your message, and ensure that your voice shines through. Trusting someone with your words is scary, but it’s essential to making your book the strongest it can be.

Finish the Damn Thing: The hardest part of writing a book is finishing it. You’ll be tempted to stop, to leave it unfinished because you’re scared of what comes next. Don’t. Push through the fear and finish it. You owe it to yourself to see this through.

BY THE NUMBERS

82% of business failures in the United States are caused by cash flow problems.

31% of business owners have said they missed big payments this year. These include owner’s salary, supplier bills and even rent.

22% report late payments.

24% report seasonal fluctuations.

33% increased labor costs.

71% report that cash flow issues have affected them personally.

Dog Days

You instinctively know it’s the “dog days of summer” (the back sweat gives it away), but do you know why it’s called the dog days of summer?

According to the Farmers’ Almanac, the phrase originated in Ancient Rome. The Romans noticed that the star they called Sirius, the Dog Star, was in conjunction with the sun in late July. They believed the Dog Star’s brightness made things hotter on Earth during the late summer months. So, they named this period diēs caniculārēs, or “days of the dog star,” which was later shortened to “dog days.”

SUMMER SLANG

IT’S AUTOMATIC

Profit First teaches business owners to pay yourself first, but you can actually apply that to every area of your life! By automating your savings, investments, and even routine payments, you’re setting yourself up for effortless financial success. Where to start? We always say choose one and then build from there. Many banks offer auto-save options that round up your purchases to the nearest dollar and transfer the difference to your savings. That’s a no-brainer. As for investments, paycheck employees can often choose to send a fixed amount or percent to their investment accounts each pay period. Solopreneurs or small business owners might consider opening a separate savings account for a routine allocation of income. Kind of like Profit First, but for investment savings. Either way, with automation, you’re consistently building your wealth and preparing for the future, all while focusing on living your best life today.

FRAUD ALERT

Senior Scam

It’s been a big summer for financial fraud, and the outlook isn’t promising—especially for seniors.

Scams targeting individuals aged 60 and older, often called elder fraud, caused over $3.4 billion in losses in 2023, marking an 11% increase from the previous year. What’s particularly alarming is that these scams aren’t just about quick cash. Increasingly, fraudsters are playing the long game, cultivating “friendships” and convincing their targets that they’re genuinely in need of help.

This summer, I’ve received several calls from people seeking advice on potential scams. One such case involved Debbie and Glenn, a recently retired couple who tragically fell victim to senior wire fraud. They lost over $100,000—nearly a third of their carefully built retirement savings— through coercion tactics and criminals impersonating bank security officials. The scammers didn’t stop at the theft; they moved the couple’s funds into

cryptocurrency, making recovery impossible.

Debbie and Glenn had planned to use that money for their retirement and healthcare costs, but now their financial future is uncertain. And the harsh reality is because the money was moved to cryptocurrency, they will never see their hardearned savings again. This story is a stark reminder that fraud isn’t just about numbers—it’s about real people whose lives are turned upside down by these heartless schemes.

As we navigate this growing threat, it’s crucial to remain vigilant and educate our loved ones about the dangers lurking behind seemingly innocent interactions. Fraudsters are becoming more sophisticated, but awareness and caution can be powerful tools in fighting back.

And that’s true for businesses as well. 43% of all cyberattacks target small businesses. And 60% of small businesses that become victims of cyber-attacks are forced to go out of business because of loss of revenue and security.

PRO TIP

SURVEY SAYS

CASH FLOW CRISIS!

A RECENT SURVEY BY CASH FLOW COMPASS OF 750 SMALL AND MEDIUM-SIZED BUSINESSES REVEALS A STARTLING TREND: ON AVERAGE, THESE BUSINESSES OVERESTIMATE THEIR CASH FLOW BY A STAGGERING 42%.

What does this mean in practical terms? It’s a wake-up call for many business owners who believe they have their financial situation under control, only to find themselves grappling with unexpected cash flow shortages that can jeopardize their business stability and mental well-being. The disconnect between perception and reality often results in missed payments, stalled projects, and a detrimental cycle of short-term crisis management.

Serial entrepreneur and author Mike Michalowicz, known for his book Profit First,

highlights the peril of cash flow overconfidence. He explains that this overestimation traps business owners in a reactive mindset, where decisions are made in the heat of the moment rather than with long-term stability in mind. As businesses expand, it becomes crucial for owners to escape this cycle and focus on creating operationally efficient and resilient enterprises.

This insight underscores the importance of not only understanding one’s financial reality but also implementing strategies that support sustainable growth. As businesses navigate these financial challenges, a shift towards a more strategic approach to cash flow management could be the key to long-term success.

P.S.

At One21, we help businesses take control of their cash flow, and put your finances on the right track.

PERSON

ONE -ON-ONE WITH

Stephen Shapiro

Stephen Shapiro’s crowd-pleaser Personality Poker yields a winning hand for business teamwork.

Within the first few minutes of conversation, one can see Stephen Shapiro as most would describe him—as creative, quirky, fun, and a little counter-cultural. Whatever it is that resonates with so many is clearly working. His most popular book-turned-seminar Personality Poker has open doors around the globe, including Fortune 500 companies including 3M, Marriott, NASA, P&G, and USAA.

The concept is simple. Each suit in a deck of Poker cards represents a different personality type. Diamonds are creative, Hearts are empathetic, Clubs are organized, and Spades are analytical. Each type is needed to play with a full deck, meaning a complete team with each team member doing the job they are best meant to do. Personality Poker is designed to assess what type of person you are and then meet with other types needed to complete the deck.

Good in theory, more challening in application. Which is why Stephen is so often called to faciliate the Personality Poker experience. A role

STORY JOHN SOTOMAYOR

he relishes for various reason. Turns out this seemingly extro verted personality actually sees himself as painfully shy and extremely introverted. And his success with Personality Poker rose after a devastating budgetary disaster.

High Roller

In 1995, Stephen ran a big practice at Accenture and was given a $30 million budget. “In Personality Poker, I am what is known as a Diamond, which means I am the creative, spontaneous type. Not very good at being organized,” Stephen explains. “I am also a bit of a Heart because I love to connect with people.”

With a $30 million budget, Stephen decided he needed a co-leader who could take the blame in case anything went wrong.

“I brought in John. He was a larger-than-life, happy Diamond-Heart, as it turned out,” Stephen says. “John and I got along great. We were both the same.”

He learned three things about that project. First, they

“In Personality Poker, I am what is known as a Diamond, which means I am the creative, spontaneous type. Not very good at being organized,”

developed more new novel ideas in that project than any other project in the entire history of the company. That was the Diamond characteristic; they wanted to be the best. Second, everyone at the project had a blast—that was the heart, they wanted everyone to enjoy themselves.

Third, “It was the biggest waste

of $30 million you’ve seen in your life,” Stephen says with chagrin.

They got so focused on being fun and innovative, that they never thought about the “Clubs,” which was the implementation.

“That was our blind spot,” Stephen says. “The Clubs are the ones who plan the work

and work the plan. They make sure we understand what it is we need to deliver.”

That project ended as a big failure. For the next project, they cut his budget from $30 million to $6 million. He also did not get to choose his co-leader. “They gave me Ray,” Stephen says wryly. “Ray was a self-proclaimed anal-retentive program

“Personality Poker allows you to bring in different groups needed for a full deck.”

manager, who was annoying as hell and in my face,” he shares.

“’We are over budget,’ he’d say. ‘I need the deliverable. I need it now!’”

They were going at it for over a month, and Stephen was miserable. “Going to work felt so restricted and so limited,” he says. “I finally pulled Ray aside to have lunch off-site and said, ‘Ray, I have to tell you, I don’t like you.’ He laughed and said, ‘I don’t like you either.’”

But one thing was clear: even though Stephen and Ray didn’t like each other, they knew they needed each other. They personalities actually worked to make a full deck. So they

decided to figure out a way to make it work.

“And we did,” Shapiro said. “What we created was magical.”

They had more success with a $6 million budget because they learned how to work together, and more importantly, they learned how to appreciate one another.

“That to me is one of the most powerful stories on why we need something like Personality Poker,” Stephen says.

How It Works

There are four general principles behind Personality Poker:

First, each person on your team needs to play in their strong suit. They need to know

PERSON ABILITY

what they do better than anyone else, and that is the work they need to be doing as their center of gravity.

Second, you need to make sure you are playing with a full deck, which means you need to have all the different styles but what happens is, we believe ‘opposites attract’ but the reality is opposites detract. People want to be with people who are similar so when we hire people, we hire those that fit the mold.

“When we hire people that fit the mold, the organization grows mold because you have all that sameness, that chronic similarity,” Stephen explains.

Personality Poker allows you to bring in different groups needed for a full deck.

Third, everyone does their part, so they divide and conquer.

Fourth, the last part is to shuffle the deck. In certain types of situations, you want collaboration among all the different suits.

Pivot

As with all things in life and business, there comes a time when we reach a pivotal moment—a crossroads where change is not just an option, but a necessity. This realization led to the perfect name for Stephen’s new book: Pivotal. The title beautifully encapsulates the essence of these critical turning points and ties seamlessly into the journey that Personality Poker represents.

“During the pandemic, the word ‘pivot’ was the word everyone used,” Shapiro explains. The problem was everyone was spinning in circles. They were chasing problems, rather than planting their feet.

“I have done some fun work with the Orlando Magic,” Shapiro shares, leading into his example. “When we think about the pivot in basketball, it seems the foot is moving around in circles. Yet the most important foot is not the one that is moving, it is the one that is not. Once you move that planted foot, it is no longer pivoting, it is traveling,”

Shapiro says. The player gets hit with a penalty.

“The same thing is true in business,” Shapiro said. “It is OK to change and to be adaptable, but first, we need to focus on stability.”

The essence of Pivotal is knowing what we shouldn’t change so we can build a solid platform so that when we do need to change, it is built on a solid foundation.

“It is focused on what is now, rather than on what is next,” Shapiro said. “We are so enamored with the future that we are not paying attention to what we need to do right now.”

Venus Michael answers your cash management questions

I’m confused about when certain purchases count as a cost of goods sold and when they don’t. Can you break that down?

Absolutely! This is one of the most common pain points for photographers.

At its surface, cost of goods sold (COGS) seems easy to calculate—it’s simply the amount you spent to create and deliver your goods or services over a given time period. But when you really start digging, it can sometimes be hard to distinguish between COGS and a normal business expense.

Think of COGS as expenses you wouldn’t otherwise have if you hadn’t performed the service or produced the product. This includes direct costs (like raw materials, merchandise for resale, and packaging) and indirect costs (like the labor required to create the product and costs to store the products).

Conversely, if it’s something you would purchase whether you have one or 100 clients (like office space or a software subscription), it doesn’t count as COGS. Marketing costs also don’t fit into this category since those are less about individual products and more about customer acquisition.

Here is a real-world example: Sophie runs a photo studio. For an upcoming project, she needs new dresses for the models. Since she only needs them for the one photo shoot, she rents them from Rent the Runway. In this case, the expense counts as COGS; she would not have otherwise bought the dresses if it weren’t for that photo shoot. (However, if Sophie chose to purchase the dresses instead of renting, they’d become part of inventory and supplies, and are no longer COGS.)

Why does it matter? Knowing your COGS can help you determine the absolute lowest price to sell a product to break even; if you aren’t tracking your COGS, you aren’t tracking your profit.

I have used Profit First for about 3 years. I have always had a separate COGS account, but your book doesn’t account for that type of account. What’s the correct way to handle this?

When managing COGS with Profit First, having a separate account is generally a good practice. So your instincts are right! However, about half of

the businesses I work with choose to keep COGS within their main operating account, which streamlines their bookkeeping and makes it easier to manage cash flow. Ultimately, whether or not to use a separate COGS account depends on your specific business needs and preferences. If separating COGS provides you with clearer insights and better control, go for it.

If I set aside my profits, how will I grow?

This is one of the most common questions we get about Profit First. What I’ve found is that the fastest, healthiest growth comes from practices that prioritize profit. And it is not because they plow money back into their business. Rather, when you take your profit first, your practice will tell you immediately whether you can afford the expenses you are incurring; it will tell you whether you are streamlined enough; it will tell you whether you have the right margins. If you can’t pay your bills after taking your profit first, you must first address those pain points, readjust, and make the fixes.

FAMILY MATTERS

Don’t let her compassionate outlook and warm laugh fool you. Rachel Jordan is serious—about her photography, her family, and her business.

STORY SARA HAYNES

It’s jitters and glam, joy and intimacy—getting your picture taken can stir up tremendous emotions. The bliss of a wedding day or the anticipation in a senior portrait captures a moment, keeping the memory alive, not just for the people in the images, but for generations to come

The person taking that image must be able to capture all the emotion in that memory. This is when Rachel Jordan of Rachel Jordan Photography gets down to business.

“I spent time really boiling down the most important thing my business does,” Rachel says. “Pictures are the souvenir for the event and the memory of the time spent together. I want my clients to feel confident, understood, and excited to share the results. Once you do that, you can’t help but take beautiful images. That’s the essence of what I do—getting to the core of what the client wants and serving them first.”

Rachel takes this kind of care in everything she does. While she pushes herself to try new things, she isn’t reckless or impulsive. She takes the time to educate herself and plan.

“I like to take big swings,” says Rachel, when describing how she approaches new challenges. She’s also thoughtful about preparing ahead of time.

Rachel’s main reason for staying on top of things is because she wants more quality

time with her family—husband Max, a videographer, and their six-year-old daughter, Emily. With both she and Max being self-employed, she understands that proper money management leaves her more time to focus on what’s important to her.

Rachel started contemplating photography while working at weddings as a makeup artist.

“I started taking pictures of my clients and my closeup retouching for my makeup portfolio, and I loved it so much that I decided to go for it.”

In 2020, she put down the makeup brush and picked up the camera. She focused on engagements and weddings, booking two years’ worth of weddings in her first year.

“I was honest with the couples about the transition in my life. That helped me connect with them.”

That authentic transparency with clients distinguishes Rachel Jordan Photography from others. She spends more time before the shoot getting to know and understand her clients, talking through the plan, and make sure each image is personal to them. She takes time to learn more about them, what places and objects are meaningful to them, what they want and don’t want from the shoot.

“If a client is worried about how her arms are going to look in the pictures, she won’t be comfortable during the shoot. I tell her if she doesn’t like how

“Pictures are the souvenir for the event and the memory of the time spent together.”

The person taking that image must be able to capture all the emotion in that memory.

her arms look, we’ll retouch them. She relaxes and we get better pictures.”

Rachel likes connecting with her clients, and the time it takes is essential to her career enjoyment, but she also needed financial stability for her family.

“Sometimes we have bad months. One of the concerns I have is how to navigate the slow months, take care of myself and my family, and control my family budget.

That’s where Venus Michael, of One21 Account-Ability, comes in.

Rachel had read Profit First before she even started her photography business and knew that’s how she wanted to manage her money. That

meant she needed a bookkeeper who could help her.

“I was so excited when I found Venus because she not only knew Profit First but specialized in photography. She advised me to not jump in right away but to take time to make sure this was right for my business. A couple of months later, I started working with her and never looked back.”

Venus helped Rachel stabilize her income with drip accounts, a Profit First cash flow management method that helps maintain a steady income even in leaner months.

“Sometimes I’d have a full month of bookings but no actual income because of the upfront output for the shoots,” says Rachel, noting that

photographers often need to account for fronting expenses for equipment and materials.

Rachel and Venus worked together to figure out and fine tune what worked best for Rachel’s business. Now, Rachel and her husband have more control over when they book their revenue, have a seasonal savings account, and more income security.

Venus also advised Rachel on expanding her business in ways that were personal to Rachel, giving her the confidence to raise her fees and get compensated appropriately for all her extra prep time.

Rachel has spent the past year growing her portrait clientele instead of focusing on weddings. Venus made

“I started taking pictures of my clients and my closeup retouching for my makeup portfolio, and I loved it so much that I decided to go for it.”

sure that Rachel could do this without losing income. She is now charging the same for portraits as she did for weddings, but since portraits take less time than weddings, she has more free time. Next year, she plans on using the portrait service price for weddings, getting paid more for the additional effort.

“I have to have data [to plan my growth] and Venus helps me with that—talking me through being responsible with my business income,” says Rachel, who loves spreadsheets. In fact, Venus and Rachel worked together on a Profit First-focused spreadsheet for photographers that originated with one Rachel created for her own business.

Venus’ influence even reached Rachel’s daughter. Af ter she sent Emily the book My Money Bunnies: Fun Money Management for Kids, Emily set up money bunny jars for spending, saving, and tithing. Emily also keeps all the copies of In the Zone magazine by her bed. “I like looking at all the photos and seeing Ms. Venus’ picture,” Emily says.

It’s clear that Venus is more than just a business consultant and bookkeeper to Rachel—she’s becoming part of the family.

“Venus is a great source of ideas, encouragement, and accountability. I know I can always talk to her.”

“Sometimes we have bad months. One of the concerns I have is how to navigate the slow months, take care of myself and my family, and control my family budget.”

PROFIT ABILITY

The Big Picture

This excerpt from Profit First for Photographers unlocks the CEO mindset, transforming your business into a profitable venture while preserving your creative spark.

Have you seen that internet meme of Captain Jack Sparrow yelling, “Stop blowing holes in my ship”? I think of that meme every time someone asks me, “Where can I find the money?”

Picture this: Your business is a ship on the ocean. You’re surrounded on all sides by expenses, all armed with cannons. Their goal is to sink your ship, and your goal as Captain is to defend it. But they’re going to hit you with everything—not just vendors and bills, but also sleek new equipment, or that sparkly dress you simply must have for your props closet.

SEE FOR YOURSELF

Contact One21 today to discover how Profit First could work for your business.

A lot of photographers struggle when it comes to learning how to navigate this aspect of business. There is a wealth of courses, mentors, and trainers to teach you how to take a photo, adjust lighting, pose subjects, and even price services, but no one is talking about what to do in the back office. To keep your business in ship shape, you must up your game and pay attention to the stuff outside of the view of your camera. Let’s talk about that stuff.

Plugging the holes

Look over that expense by vendor report we pulled in Chapter 5 again (see sidebar). Inspect it for payments and vendors that are Iwannas blowing holes in your bank account. Remember Parkinson’s Law? When you were first starting out, you didn’t have all these expenses, but you still got the job done. Which ones aren’t helping you get the job done now? Can you cut some of those even temporarily? Look at the difference between your CAPs (Current Allocation Percentage) and your TAPs (Target Allocation Percentage) to decide what needs to go first.

Inspecting the Hull

If you wait until your tax return is due to review your numbers, you have waited too long. It’s important to review and understand the financial health of your business at any given time. That can be a massive undertaking if you don’t have

a bookkeeper who sits down faithfully every month and reviews your financial statements with you, while making sure you as a creative truly understand the story that the numbers on the page are telling. Even if you do have that person, you may not have the time or desire to devote to that meeting. That’s exactly why Profit First is the perfect tool to use. The system you just learned about is the way your business communicates with you in real time, showing you things that might need your attention. Looking at the financial statements once a month is also important to give you a bird’s eye view of the entire big picture.

Hiring the Right Crew

When you think about hiring someone, an admin, an associate photographer, an on-staff editor etc., there are a few things to think about. First, do not hire for the sake of hiring. Think about the purpose of the new position. What are they going to do for you? What are they going to take off your plate? How much time are you going to get back to work on other things? How much will your real revenue increase by having them as a resource on your team? Do you want them there full-time or part-time? Once you have gathered all your answers, it is time to sit down and consider what you’re going to pay for this position. And if it will benefit you, move forward with the hire.

Bank Access for Users.

Imagine you’ve hired an assistant to help you handle the parts of your business that you don’t have time or desire to do yourself. One of those things is banking. So, you give your assistant your bank login because you’re just too busy to deal with it. Why pay the fee for multiple users?

First of all, you should never be too busy to deal with your money. Second, it’s not fair to put an employee in that position. They may not feel comfortable taking on that liability, or worry about being blamed if something happens to the account. Third, compare it to giving out your debit card and PIN number, and then trying to claim fraud when your account is drained. If you willingly give your user ID and login to anyone else, that person has full and legal access to do all kinds of transactions, not just the ones you want them to do.

Let’s say your assistant decides one day that you don’t pay her enough. So she begins to Zelle herself an extra $50 a week. Six months and $1,300 go by before you finally notice. Can you go back to your bank and say, “Oh my gosh, fraud?” No, not really. You literally gave them the keys to the castle. You could file a police report, but there’s no guarantee that anything will be done about transactions that weren’t actually fraudulent.

If you give your employee their own user login, you get

CROP THOSE EXPENSES

Zoom in on your business finances and see where you can make cuts. Start by collecting a list of all your expenses for the last 12 months and sort by “one offs” and “recurring.” If you have a bookkeeper, they can help you. If you use accounting software, you can pull an expense by vendor report.

Total the list and then multiply by 10% (0.1). That 10% is what you must work on cutting this week. I know we’re trying to do a few percentages each quarter, but it takes a while for billing cycles to reflect cancellations.

Now look through your list carefully, at all the people and businesses you make payments to. For each one, ask yourself: “Is this an Ineeda (I need it) or an Iwanna (I want it)?” The Ineedas are the essentials you must have in order to run your business, such as your camera, editing software, studio space (if you have one). The Iwannas are things like the lease for that luxury car, the cool software you only use once or twice a year, the membership for an association you’re not active in; they’re nice to have, but you can do just fine without them.

A few of the most common Iwannas for photographers are:

Software. What good is spending $10 a month on a program you “might use someday” if that day never comes?

Dresses and props. Many photographers suffer from what I call Sparkly Dress Syndrome. Maybe you love shopping for clothing and props “for your sessions,” but clients never end up using them. Are you buying them for your sessions, or because you love to shop for them?

Equipment. Don’t get stuck in the thought process that some shiny new equipment equals a magic transformation in the work you can produce. You as the photographer are the magic; and you as the business owner must protect the profitability of the business.

With recurring expenses that are Ineedas, you might be able to find other options or renegotiate terms with the vendor. If it’s an Iwanna, let it go.

Raising your revenue will also affect the percentages so you don’t feel like you’re cropping out too much. However, raising the revenue is a slower game and can take longer to see the rewards. Do not depend on this when doing your initial crop.

When Poppy looked at her list, she quickly found three subscriptions for software she didn’t even use and canceled them. In all, she cut more than $700 per month ($8,400 per year) in Iwannas, lowering her operating expenses by 5% and instantly exceeding her goal of 3% for the first quarter of implementation. Win!

to pick what they have access to. You also have the ability to revoke access as you end relationships with people. If your assistant has their own login and then you part ways, you just go into your online banking and delete that profile. You don’t have to worry about whether they know your password.

The Lookout: Hiring a Bookkeeper

As with anything involving your money, there are a lot of emotions tied to hiring a bookkeeper. The most common emotions I hear about are vulnerability, embarrassment, and fear of judgment. Opening up

your pocketbook to a stranger can sometimes feel just like that nightmare people have of showing up to high school without your pants.

Remember that accounting is an analytical task, and you as a creative person may struggle with that task. I’m the total opposite of that; I have a fancy DSLR camera and three lenses I enjoy playing with, but there’s no way I could take photos like you do. To be totally honest with you, I use auto mode. In the same way, you might have a subscription to an accounting software, but I wouldn’t be surprised to hear that you don’t understand how to harness the power of it.

How To Use AI To Grow Your Photography Business

As a photographer, you’re likely juggling multiple roles—visionary, content creator, salesperson, customer support, and more. What if you could offload some of these tasks and focus more on what you love?

Let’s explore how AI tools like ChatGPT can help you grow your photography business faster and with less work.

The 3 Pillars of Business Growth

Before we dive into AI applications, it’s crucial to understand the three pillars that drive business growth in photography:

• Marketing: Capture the attention of your ideal clients

• Messaging: Optimize your sales process

• Monetization: Enhance client experience and diversify income

I call this the “Brand Builder Trifecta” because it forms the foundation of every successful business.

Let’s break down each pillar and see how AI can streamline your efforts.

1. Marketing

Marketing is all about visibility. It’s how you get your work in front of the right eyes. But it’s not just about posting pretty pictures—it’s about strategic, consistent outreach that

resonates with your ideal clients. AI can help you:

• Generate social media content ideas

• Write newsletters and blog posts

• Assist with video/podcast scripting

• Optimize local SEO and Google listings

• Create outreach messages for partnerships

AI helps you share consistent, impactful content across all platforms.

2. Messaging

Your messaging is how you communicate your value to potential clients. It’s not just what you say, but how you say it —your unique voice that sets you apart in a crowded market. AI can help you:

• Articulate your Unique Selling Proposition

• Improve your website content and sales funnel

• Write case studies from your best client experiences

• Explain your unique process or approach to photography

• Create lead magnets like checklists or ‘how to prepare’ guides to build your email list AI helps you find the right words to express your unique value and move people into action.

3. Monetization

Monetization isn’t just about making sales—it’s about creating such an exceptional experience that clients are happy to invest in your services and refer you to others. It’s also about finding innovative ways to generate income beyond traditional photoshoots. AI can help you:

• Draft client proposals, contracts, and agreements

• Generate follow-ups emails and meeting summaries

• Brainstorm creative shoot ideas and pose suggestions

• Develop new package offerings

• Ideate on additional products/ services

AI helps you to provide premium client experiences while exploring new revenue opportunities.

How to Get Premium Results from AI

Now that you understand how AI can assist in each area of the Brand Builder Trifecta, let’s talk about how to get the best results. The key lies in a three-layer approach:

• Brand Context: Educate the AI about your business basics, including your offerings, ideal client avatar, brand story, voice, and tone. This forms the foundation for all

AI-generated content.

• Task Context: Clearly define what needs to be done and how. Be specific about the desired outcome and any particular requirements or preferences.

• Specific Variables: Provide any relevant details needed to complete the task, such as client names, event specifics, or current promotions.

Here’s an example of what to tell ChatGPT:

Brand Context: I’m a wedding photographer specializing in candid, photojournalistic style images for adventurous couples. My brand voice is warm, friendly, and slightly humorous.

Task Context: Write an email to follow up with a potential client after our initial consultation. The email should recap our discussion, address any

concerns they mentioned, and gently encourage them to book. Specific Task Variables:

• Client Names: Sarah and Mike

• Wedding Date: June 15, 2024

• Venue: Sunset Cliffs, San Diego

• Their main concerns: Family groupings and scenic images

• Transcript of our meeting: With this approach, you’ll see better quality and more accurate results with your AI tools.

Grow Faster & Have More Fun

By integrating AI into your marketing, messaging, and monetization strategies, you’ll:

• Maintain consistent, quality content across channels

• Communicate your unique value more effectively

• Enhance client experiences and diversify your income The result? Happier clients, less stress, and more time for creativity.

AI helps you find the right words to express your unique value and move people into action.

Your Path to Profitable Online Courses Starts Here

If you enjoyed this article, then visit DesignHacker.com for more training and resources to grow your business faster.

Stefi and Andrew, the team behind Course Builder Pros

The Allure & Reality of Growth

Melissa Darveau explores the highlights of growth and the hidden challenges that can arise if you’re not fully prepared.

Growth is a thrilling phase for any business owner. When asked about their business goals, most owners will mention growth. It’s exciting because it signifies that your startup is gaining traction. Brand recognition increases, sales climb, you begin hiring staff, and your initial vision starts to feel tangible. This excitement often leads to ambitious thoughts like, “If we double our sales this year, then…”.

However, it’s crucial to approach growth cautiously. Rapid, unplanned growth can quickly turn from an asset into a liability. We often call this “growing yourself out of business.” It happens more frequently than you might think. This is exactly why, understanding the cost of growth is vital. Think of it as a fourlegged stool.

Leg 1: Increased Costs

The first leg involves the obvious increase in the cost of goods sold (COGS) and overhead. As you produce more products or offer more services, the costs associated with these sales will naturally rise. This includes purchasing more materials and dealing with higher merchant service fees due to increased card sales.

Leg 2: More Time on the Business

The second leg is spending more time managing the business rather than working directly in it. You might wonder, “How do I do that when there’s only one of me?” The answer is hiring employees. Even a parttime admin can significantly help manage your workload. This stage is also an excellent time to reassess the professionals you’ve surrounded yourself with. As your business grows, you need a team that offers consulting, not just transactional services. This team should help you understand how your growth decisions will impact

cash flow, taxes, and financing. Many business owners stick with the same CPA, bookkeeper, or banker long after outgrowing their services. If these professionals aren’t helping you navigate the complexities of growth, it’s time to find ones who will. Having a solid understanding of how growth impacts your finances is crucial.

Leg 3: Increased Risk

The third leg is increased risk. Hiring staff, expanding into new spaces, and purchasing equipment all come with inherent risks. It’s important to understand these risks and ensure you’re properly secured. Business insurance costs will rise, and it’s wise to consult with your business attorney to review and

Understanding the cost of growth is vital. Think of it as a four-legged stool.

tighten contracts with partners, customers, and vendors.

Another aspect of risk is planning for unforeseen events that might affect you personally. If you fall ill, have an accident, or even pass away, the absence will significantly impact your business and family. Although it’s uncomfortable to think about, securing life insurance, a will, and powers of attorney will make navigating such situations easier for your family and business partners.

Leg 4: Increased Need for Credit and Banking Services

The fourth leg is the increased need for credit and banking services. Growth requires capital, which can come from various sources, including private equity, cash reserves, and financing. Discuss with your

banker the best credit options for expansion. For long-term investments like property or equipment, a term loan is suitable. For short-term needs (less than a year), a line of credit is optimal.

The business credit you established as a startup will support your creditworthiness for more complex lending. Remember, you’ll still be personally guaranteeing your business debt. Most lenders won’t consider non-recourse lending unless you’re a nonprofit or a for-profit company with over $500 million in annual sales.

As your business grows, it’s also essential to review and enhance fraud prevention measures. Increased transactions with clients and vendors mean a higher risk of fraud. Fraud can happen to any business, and it’s usually ACH or check fraud,

which can take much longer to resolve than credit or debit card fraud. Protecting your business from fraud is crucial, as getting your money back can take 90120 days. Banks offer various fraud prevention services, such as positive pay for checks and ACH, dual control wires, and phantom accounts. Although these services might increase bank fees, the security they provide is invaluable. Think of it as insurance; you hope never to use it, but you’ll be glad you have it if needed.

While this overview covers many aspects of business growth, it only scratches the surface. Reach out to your team of professionals to discuss these topics in depth. Stay informed and proactive throughout your growth stage to protect and enhance what you’re building.

Melissa Darveau

is a 23-year banking veteran. A native Austinite and graduate of Texas State University, Melissa is a Commercial Banker in the Austin area for Truist Bank. She has extensive finance experience and is wellversed in financial reporting. She has a strong understanding of the story a company’s

financials are telling. She applies a consultative approach to coaching business owners on how best to: 1. Begin, 2. Stabilize, 3. Grow or 4. Transition

In her free time, she enjoys gardening, traveling and taking motorcycle rides through the hill country. She currently lives in the Central Texas Hill Country with her husband, Dale, as well as their 5 dogs and 5 cats.