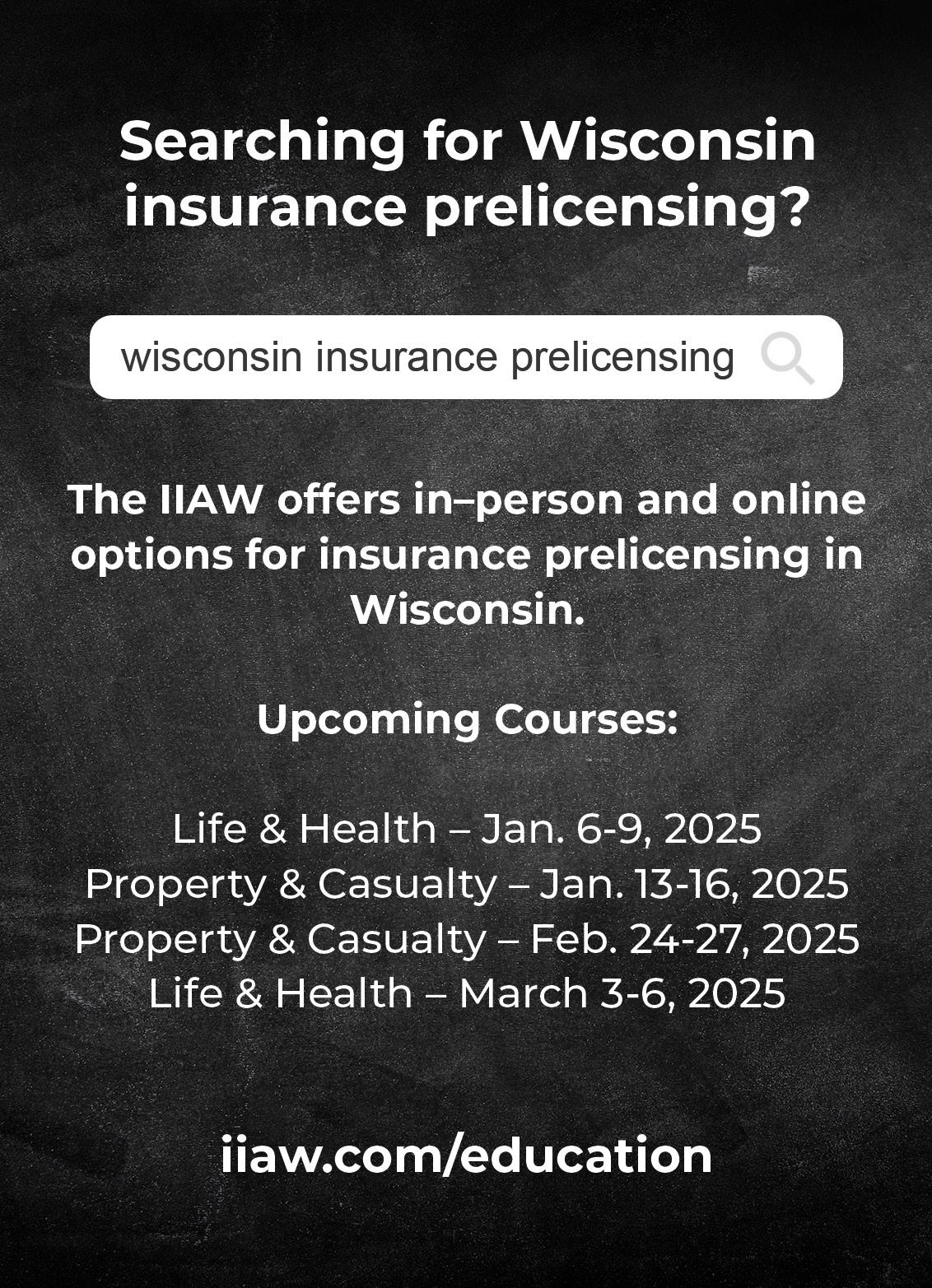

INDEPENDENT INSURANCE AGENTS OF WISCONSIN

725 John Nolen Drive

Madison, Wisconsin 53713

Phone: (608) 256-4429 Fax: (608) 256-0170 www.iiaw.com

2024-2025 EXECUTIVE COMMITTEE

Interim President: Dan Lau | Robertson Ryan Insurance

Secretary-Treasurer: Mike Harrison | R&R Insurance Services Inc.

Chairman of the Board:

Mike Ansay | Ansay & Associates

State National Director: Nick Arnoldy | Marshfield Insurance Agency, Inc.

2024-2025 BOARD OF DIRECTORS

Janel Bazan | Avid Risk Solutions/Assured Partners

Adam Coole | The Insurance Center

Alex Kihslinger | Emerging Leader Chair Liaison | Robertson Ryan Insurance

Beth DeLaForest | Aspire Insurance Group, Inc.

Sean Fitzgerald | SF Insurance Group

Jason Knockel | Kunkel & Associates, Inc.

Andrea Nelson | Unisource Insurance Associates, LLC

Brad Reitzner | M3 Insurance Solutions

IIAW Staff

Matt Banaszynski | Chief Executive Officer

608.256.4429 • matt@iiaw.com

Mallory Cornell | Vice President 608.210.2975 • mallory@iiaw.com

Kim Kramp | Accounting Supervisor 608.210.2976 • kim@iiaw.com

Trisha Ours | Director of Insurance Services 608.210.2973 • trisha@iiaw.com

Evan Leitch | Agency Solutions Advisor 608.210.2971 • evan@iiaw.com

Kim Fiene | Marketing & Communications Director 608.210.2977 • kimf@iiaw.com

Andrea Michelz | Education & Membership Engagement Coordinator 608.210.2972 • andrea@iiaw.com

Diana Banaszynski | Events Coordinator and HR Business Partner 608.256.4429 • diana@iiaw.com

Ali Smeester | Accounting Specialist 608.256.4429 • ali@iiaw.com

Wisconsin Independent Agent is the official magazine of the Independent Insurance Agents of Wisconsin (IIAW) and is published monthly by IIAW 725 John Nolen Drive, Madison WI 53713. Phone: 608.256.4429. IIAW does not necessarily endorse any of the companies advertising in publication or the views of the writers. IIAW reserves the right, in its sole discretion, to reject advertising that does not meet IIAW qualifications or which may detract from its business, professional or ethical standards. © 2024

For information on advertising, contact Kim Fiene, 608.210.2977 or kimf@iiaw.com.

With a long history of supporting independent agents, an "A" rating from A.M. Best, and a customizable lineup of home, auto and business insurance, Integrity Insurance combines the stability of a large carrier with the personalized service of a small business. Integrity fosters productive, long-term relationships with its agents, providing tools and resources to help them succeed in today’s marketplace. Integrity is proud to be a committed, connected partner for independent agents.

Integrity's partnership with Grange Insurance is more than two decades strong. The relationship gives Integrity access to modern insurance products and services that create a better experience for customers and agents.

Integrity offers our agents a crystal-clear appetite that covers many classes and a wide variety of commercial products including Commercial Package, Worker’s Comp, Commercial Umbrella and Commercial Auto. Integrity also provides coverages such as Cyber and Employment Practices and Liability Insurance and Equipment Breakdown

Coverage that’s crucial for your clients in today’s workplace. Our commitment to providing the best to our agent partners includes services and policies that are true differentiators. Our 36-Month Package Policy offers rate stability for your clients. Integrity’s Commercial Service Center takes care of the little things so you can grow your business. Our Risk Management Consulting team gives businesses of any size a partner to help identify issues and develop solutions.

Integrity Personal Lines offers a full suite of customizable Home and Auto products that can help agents meet the needs of any client. Additional coverages such as ID Theft, Cyber, Umbrella and Underground Service Line give your clients the peace of mind and protection they expect from their insurance.

Integrity policyholders and agents have access to the latest developments in technology. Policyholders can access their billing and policy documents from any desktop or mobile device with our Integrity Insurance app or a MyIntegrity online account. Policyholders can also pay their bills via EFT (Electronic Funds Transfer)

and receive claims payments via electronic claims payment. Integrity also has self-service options for policyholders such as our DIY Home Inspection tool and our Easy Snap for minor auto claims.

For more information about Integrity, visit integrityinsurance.com.

Contact: Cathy Colón

Regional Sales Manager (920) 968-9326 ccolon@imico.com

Integrity Insurance was established in 1933 and offers auto, home and business insurance protection through a network of independent agents throughout Iowa, Minnesota and Wisconsin. With partner Grange Insurance based in Columbus, Ohio — the 13-state Grange Enterprise has $3.2 billion in assets and $1.5 billion in annual revenue and holds an A.M. Best rating of "A" (Excellent). Learn more by visiting integrityinsurance.com.

The Independent Insurance Agents of Wisconsin are thrilled to invite you to our 2025 convention May 7 & 8 at American Family Field, home of the Milwaukee Brewers!

Get ready for a grand-slam experience alongside Wisconsin’s top independent insurance agents in a truly unique setting. The IIAW has lined up a one-of-a-kind experience that knocks it out of the park! registrAtion is now open!

InsurCon2025 • May 7-8, 2025

WEDNESDay, May 7TH

8:30AM-10:30AM

Sheraton Milwaukee Brookfield Hotel 375 S Moorland Rd, Brookfield

9:30AM-10:30AM

10:45AM

12:10PM

American Family Field X-Golf Suite (PNC Club Level)

3:10PM

4:00PM-8:00PM Broken Bat Brewery 135 E Pittsburgh Ave, Milwaukee

8:00 PM

THUrSDay, May 8TH

8:00AM-9:00AM

American Family Field - Third Base Ward

8:00AM-11:00AM

PNC Club Level & SKYY Lounge

10:00AM-11:00AM

Northwestern Mutual Legends Club (PNC Club Level)

9:00AM-10:00AM Yount & Aaron Rooms (PNC Club Level)

10:00AM-11:00AM Yount & Aaron Rooms (PNC Club Level)

11:30AM-2:00PM PNC Club Level & SKYY Lounge

2:45PM-3:45PM

Third Baseline Visitor’s Dugout

4:00PM-4:45PM

Third Baseline Visitor’s Dugout

5:00PM-6:30PM

Third Base Ward

Registration & Brewers Game Ticket Pickup

Tickets must be picked up at the Sheraton Milwaukee Brookfield Hotel by 10:30AM

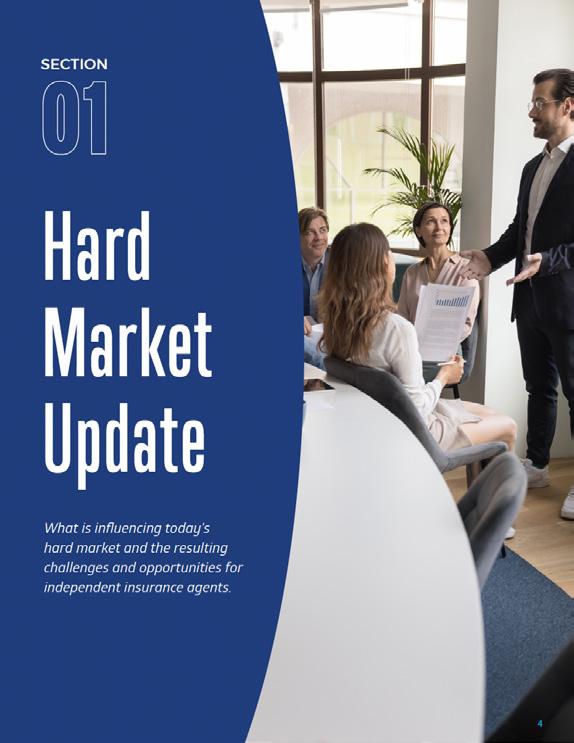

Industry Update - Presented by IIAW CEO Matt Banaszynski. Filed for 1 WI CE credit

Bus Departs Sheraton Milwaukee Brookfield Hotel for American Family Field

Brewers Game vs. Astros & X-Golf *Optional Add-On During Registration*Experience the excitement with seven state-of-the-art indoor golf simulator bays spread across two floors, including three bays offering spectacular views of the ball park. Lunch & beverages provided. Tickets are limited and offered on a first-come, first-serve-basis. Purchase your game day ticket for $50 within your attendee registration.

Bus Departs American Family Field for Broken Bat Brewery

Wiffle Ball Tournament, Trivia, Dinner & Awards - After the Brewers game, we’ll head over to Broken Bat Brewery for trivia, dinner, an awards presentation and networking. Wiffle Ball Tournament spots are available on a first-come, first-served basis.

Bus Departs Broken Bat Brewery for Sheraton Milwaukee Brookfield Hotel

Registration

Exhibitor Setup

Generational Selling Workshop Presented by Chubb - This seminar will explore generational selling techniques that will allow you to tailor your approach to different age groups. Learn how to improve and enhance client relationships with people from multiple generations.

Turning Science into Solutions to Mitigate Property Risk with the Insurance Institute for Business and Home Safety (IBHS) - Jennifer Gardner, IBHS Senior Director for Member and Industry Engagement, will provide a background on IBHS research, perils studied, and solutions developed to bend down the loss curve and mitigate avoidable damage from severe weather events.

The Insurance Industry’s Climate Crunch (Willis Towers Watson) - Scott St. George, WTW’s Head of Weather & Climate Research, will spell out how climate change has already redrawn the risk landscape for major physical perils, and provide a look ahead to help insurers prepare for a more perilous future.

Exhibitor Showcase & Lunch - Network & connect while you visit the exhibitor booths. Agency attendees can win big prizes from Super Door Prizes and by playing Blackout Bingo. Meet & greet with Bernie the Brewer and the Famous Racing Sausages!

CEO Panel - Gain valuable insights from top CEOs as they share their perspectives on where the industry is headed, what challenges lie ahead, and how agents can position themselves for success. TBA - Stay tuned for the announcement!

Keynote Speaker - TBA - Stay tuned for the announcement!

Food & Cocktail Reception - Meet & greet with our keynote speaker and a former Milwaukee Brewers Player - TBA

The Independent Insurance Agents of Wisconsin hosted its first IA Tech Summit on November 14, 2024, bringing industry professionals together for a day of insightful discussions and hands-on learning.

The Summit began with personalized support sessions from Applied Epic, Vertafore, and HawkSoft, where participants explored the latest tips and tricks for leveraging their AMS platforms.

The Agency Panel—Beth DeLaForest (Aspire Insurance Group), Matt Schulz (Ansay & Associates), and Amber Seitz (M3 Insurance)— delivered valuable insights, while sessions with Nick Oliver from Redbird Security LLC

and Casey Nelson from Catalyit offered fresh strategies for cybersecurity and tech adoption.

The Carrier Panel, led by Jeremiah Johnson (Integrity Insurance), Farres Moidu (Central Insurance), and David Williams (Acuity Insurance), provided engaging perspectives on industry trends.

The event concluded with a presentation from the IIAW's Matt Banaszynski and Evan Leitch on new tech platforms to save time and money, followed by a networking cocktail hour.

A huge thank you to all the speakers and attendees for making the summit a success!

The Independent Insurance Agents of Wisconsin (IIAW) market share and line-of-business reports are invaluable tools for insurance agents. They offer critical insights into market dynamics, helping agents strengthen their relationships with insurers, refine their strategies, and better serve their customers. Here’s how agents can effectively use these reports to enhance their operations.

The IIAW’s reports provide detailed data on:

• Market share of insurance companies by state and line of business.

• Growth trends in direct written premiums.

• Profitability metrics like combined ratios.

• Insights into niche and dominant players in various lines, such as workers’ compensation, commercial auto, and liability insurance.

These insights are essential for making informed decisions in a competitive insurance landscape.

1. Enhance Relationships with Insurance Carriers Agents can use IIAW’s reports to foster stronger partnerships with the insurance companies they represent:

• Highlighting Opportunities: Agents can identify carriers with strong performance in specific lines of business and align their agency focus accordingly. For instance, a carrier with a growing market share in commercial auto might be an ideal partner for agents looking to expand in that line.

• Negotiating Support: By understanding a carrier’s market performance and profitability in Wisconsin, agents can negotiate better terms, marketing support, or resources to target specific markets.

• Carrier Benchmarks: Agents can benchmark the carriers they represent against competitors, providing data-driven feedback on product offerings, rates, or claims handling efficiency.

2. Strategic Planning for the Agency - The reports offer a foundation for data-driven strategy development:

• Market Positioning: Agents can identify underserved markets or lines of business with growth potential. For example, if the workers’ compensation line shows regional growth, agents can adjust their marketing focus to capture this opportunity.

• Competitive Analysis: Understanding which companies dominate specific lines allows agents to position themselves effectively by targeting niche markets or leveraging their carrier relationships.

• Operational Focus: Identifying lines with low combined ratios can help agents prioritize policies that contribute to carrier profitability, fostering long-term partnerships.

3. Better Serve Customers - Agents can use the insights to improve client relationships and product offerings:

• Tailored Recommendations: By understanding the market leaders and their strengths in specific lines, agents can guide customers toward carriers that offer the best coverage, rates, or service.

• Educational Value: Sharing market trends with customers—such as the rise in premiums or profitability issues in specific lines—positions the agent as a knowledgeable advisor, building trust and credibility.

• Proactive Risk Management: Insights into loss trends in lines like commercial auto or liability insurance can help agents advise clients on risk management practices, reducing claims and improving client satisfaction.

1. Regularly Review Reports: Schedule time to analyze the reports and extract insights relevant to your agency’s focus.

2. Collaborate with Carriers: Share findings with your carrier representatives to discuss market opportunities and align efforts.

3. Educate Your Team: Train staff on how to use the reports for customer interactions, marketing strategies, and operational improvements.

4. Communicate with Clients: Incorporate insights into newsletters, client meetings, or social media content to demonstrate expertise.

The IIAW market share and line-of-business reports are more than data compilations—they are strategic tools that empower agents to grow their business, deepen relationships with insurers, and deliver exceptional value to customers. By leveraging these insights, agents can position their agencies as market leaders in an everchanging insurance landscape. The following is an analysis on Commercial Auto, Other liability (occurrence) and Worker’s Compensation lines of business in Wisconsin you can put to use in your agency.

The Wisconsin insurance market for "Other Liability (Occurrence)" in 2023 reveals a dynamic sector driven by active players and notable premium shifts. This analysis synthesizes data from The Independent Insurance Agents of Wisconsin report, focusing on trends, key performers, and insights into the other liability insurance ecosystem.

1. Premium Growth: The market observed significant increases in direct written premiums for many insurers. For instance:

• West Bend Insurance Group led the market with $84.4 million in premiums, reflecting a 7.9% year-over-year growth.

• The Travelers Group followed, with premiums growing by 12% to reach $58.8 million.

• Remarkable growth rates were seen in smaller insurers, such as Upland Specialty Insurance Company (+215.7%) and Ascot Insurance US Group (+56%).

2. Profitability Challenges:

• Combined ratios, a profitability metric, showcased varied performance. Ratios below 100% typically indicate profitable underwriting, while higher figures reflect losses.

• West Bend Insurance Group achieved a strong 2023 combined ratio of 78.8%, showcasing efficient operations.

• Conversely, AXIS US Operations reported a challenging combined ratio of 182.6%, underscoring underwriting losses.

The market structure highlighted a mix of dominant insurers and growing niche players:

Dominant Groups:

• West Bend Insurance Group accounted for 25.3% of the state's market.

• Travelers Group contributed 12% of the total premiums, offering a diversified portfolio.

Growth Leaders:

• Hartford Insurance Group experienced the highest premium growth rate (+33.3%), reaching $24.4 million.

• Smaller groups like Concert Insurance Group demonstrated an astonishing 3,370% increase, reflecting strategic expansion.

Geographic and Industry Influence

Wisconsin's market contributed varying percentages to national figures:

• Premium Distribution: Insurers like SECURA Insurance Companies allocated over 20% of their national premiums within Wisconsin, highlighting their local focus.

• National Presence: Larger entities like Chubb INA Group maintained a broader geographic spread, with Wisconsin accounting for just 1% of their U.S. premiums.

1. Challenges:

• High Combined Ratios: Many insurers, including Zurich Insurance US PC Group (110.3%) and State Farm Group (131.7%), faced operational challenges in maintaining profitability.

• Volatility: Groups such as Swiss Reinsurance Group reported a staggering 1,000% combined ratio in specific cases, signaling risk assessment and claims management difficulties.

2. Opportunities:

• Emerging Players: New entrants like Triangle Insurance Company, Inc., with a 177.4% growth, indicate untapped potential.

• Technology Adoption: Leveraging data analytics for better underwriting and risk modeling can transform the sector's profitability dynamics.

The Wisconsin "Other Liability (Occurrence)" insurance market in 2023 is marked by robust growth among dominant players, emerging competition, and profitability challenges. While larger firms consolidate their positions, niche and regional players continue to capitalize on specific market segments.

The 2023 Workers' Compensation market in Wisconsin reveals intriguing dynamics, including premium shifts, profitability insights, and a competitive landscape dominated by key players. The report from The Independent Insurance Agents of Wisconsin highlights the financial performance and strategic positioning of various insurers operating in the state.

1. Overall Performance: The market saw a slight contraction in total direct written premiums, amounting to

$1.96 billion, representing a 0.5% decrease from 2022.

2. Growth Leaders:

• Travelers Group led with $158.6 million in premiums, marking a 5.3% increase and maintaining a dominant 4.1% share of the U.S. workers' compensation market.

• Old Republic Insurance Group experienced significant growth (+24.2%), reaching $72.6 million in premiums, indicating robust regional performance.

3. Decliners:

• American International Group (AIG) experienced the most dramatic decline, with premiums falling by 63.9% to $27.6 million.

• Smaller groups, such as Nationwide Property & Casualty Group, saw declines exceeding 50%.

1. Combined Ratios:

• The combined ratio is a critical measure of underwriting profitability, with ratios below 100% signifying profitability.

• West Bend Insurance Group reported an impressive combined ratio of 71.5%, showcasing its efficient operations.

• In contrast, Cities and Villages Mutual Insurance Co. faced challenges with a 146.3% combined ratio, highlighting underwriting losses.

2. Multi-Year Trends: The five-year weighted average combined ratio for Wisconsin stood at 86.4%, slightly above the U.S. average of 80.1%, reflecting consistent regional performance.

1. Dominant Players:

• Travelers Group and West Bend Insurance Group together account for over 15% of the market, emphasizing their dominance in Wisconsin.

• Sentry Insurance Group closely followed with $135.3 million in premiums, marking a 15.3% increase.

2. Regional Specialists:

• Rural Mutual Insurance Company allocated 100% of its workers' compensation business to Wisconsin, demonstrating a focused local strategy with a combined ratio of 65.2%, one of the best in the state.

1. Growth in Small and Niche Players:

• ICW Group (+42.4%) and SUNZ Insurance Company (+98.8%) emerged as growth leaders, capturing market opportunities with innovative underwriting strategies.

• Groups like Tokio Marine US PC Group expanded

aggressively, posting a 68.4% increase.

2. Underwriting Challenges:

• Several insurers, including Erie Insurance Group, reported combined ratios exceeding 190%, reflecting significant challenges in claims and risk management.

1. Profitability Pressure: The variance in combined ratios underscores the importance of robust risk assessment and claims management practices to mitigate underwriting losses.

2. Technology and Innovation: Insurers leveraging technology for better data analytics and underwriting precision could gain a competitive edge.

3. Regulatory and Economic Environment: Economic shifts and labor market trends in Wisconsin will play a crucial role in shaping premium growth and profitability in the coming years.

Wisconsin's 2023 Workers' Compensation insurance market presents a mixed picture of growth opportunities and profitability challenges. The strong performance of established players like Travelers and West Bend, coupled with the rise of niche insurers, highlights a competitive and evolving landscape. Moving forward, strategic innovations and efficient claims management will be key to sustaining growth and navigating market complexities in an environment of decreasing rates.

The 2023 Wisconsin Commercial Auto Insurance market reflects significant growth, dynamic competition, and evolving profitability challenges. Based on the Independent Insurance Agents of Wisconsin's comprehensive report, this article highlights the industry's performance, key players, and emerging trends.

The Wisconsin Commercial Auto Insurance sector achieved a remarkable 15.2% increase in direct written premiums, totaling $1.01 billion in 2023. This robust growth demonstrates a healthy demand for commercial auto coverage, driven by economic activities and the transportation industry's expansion.

• Acuity Insurance leads the market with premiums of $77.8 million, reflecting a 1.6% growth and a 96.7% combined ratio, indicating near-profitable underwriting.

• West Bend Insurance Group follows closely, with

$71.1 million in premiums and an 8.3% increase, showcasing strong regional focus.

2. Significant Growth Rates:

• Fortegra P&C Group recorded a staggering 11,321.7% increase, reaching $26.8 million, highlighting its aggressive entry and rapid market expansion.

• AmTrust Group grew by 296.2%, achieving $13.3 million, a testament to its strategic positioning.

Profitability Challenges

The industry's overall combined ratio of 91.2% demonstrates a profitable but competitive landscape. However, profitability varies widely among insurers:

1. High Performers:

• Chubb INA Group achieved the lowest combined ratio of 59.2%, reflecting superior underwriting efficiency.

• Zurich Insurance Group maintained strong profitability with a 67.2% combined ratio.

2. Struggling Insurers:

• CNA Insurance Companies reported a 166.3% combined ratio, indicating substantial underwriting losses.

• Hartford Insurance Group faced challenges with a 153.6% combined ratio.

Market Leaders and Strategies

The Wisconsin market showcases a mix of dominant players and emerging competitors:

1. Regional Dominance:

• Acuity and West Bend Insurance Group collectively control a significant portion of the market, leveraging their local expertise and strong agent networks.

• Rural Mutual Insurance Company focuses exclusively on Wisconsin, allocating 100% of its premiums to the state, achieving a competitive combined ratio of 92.6%.

2. National Giants:

• Progressive Insurance Group, despite a 5.7% decline in premiums, remains a key player with $68.5 million in premiums and a competitive 91.1% combined ratio.

Emerging Trends

1. Growth in Specialty Insurers: Groups like Accelerant US Holdings Group (+508.8%) and Fairfax Financial (USA) (+84.5%) are aggressively targeting niche segments within the commercial auto space.

2. Improving Profitability through Innovation: Insurers leveraging data analytics, telematics, and improved risk assessment tools are achieving better combined ratios, such as Auto-Owners Insurance Group with an 87.8% ratio.

3. Economic Impact on Loss Ratios: The rising cost of claims and vehicle repairs, coupled with supply chain disruptions, has pressured loss ratios for many insurers, requiring enhanced operational efficiencies.

Conclusion

Wisconsin's 2023 Commercial Auto Insurance market demonstrates a vibrant, growing industry with opportunities for innovation and efficiency. While dominant players continue to solidify their positions, emerging competitors and niche insurers are reshaping the competitive landscape. For stakeholders, focusing on risk management, operational efficiency, and customer engagement will be essential to navigating this evolving market.

Ingredients

• 6 large eggs

• 3 Tbsp. room-temperature unsalted butter

• 3/4 c. confectioners’ sugar

• 1/2 tsp. ground cinnamon

• 1/4 tsp. ground nutmeg

• 1/8 tsp. ground cloves

• Pinch ground all-spice

• 2 1/2 c. whole milk

• 1/2 c. dark rum

• 1/2 c. brandy

Directions

1. Separate eggs. Whisk together egg yolks and butter in a large bowl until yolks are pale. Whisk in confectioners’ sugar and spices.

2. Beat egg whites until stiff peaks form. Fold whites into yolk mixture.

3. Heat milk just until warm. Remove from heat, and stir in rum and brandy. Transfer milk mixture to a bowl, and gently fold in egg mixture. Transfer to a punch bowl, and garnish with nutmeg.

It truly is the most wonderful time of the year, and many of us have a treasured collection of holiday items that we’ve dusted off and put on display for all of our guests to enjoy.

As much as I would like to talk about my Hallmark snowman collection, I’m also interested in discussing what your agency collects! Do you have an assortment of credit card numbers, perhaps? Some lovely motor vehicle records (MVRs) on hand for display? Or maybe your focus is on gathering signed Acord applications?

When it comes to client information that must be kept in the agency file, a few documents can be critical to defending an E&O allegation or claim. As a rule of thumb, any time you can verify a customer’s request, decision or acknowledgment, this information should be kept in the file.

• Signed Applications: Always get applications signed and save them in the client file.

• Exposure Checklists or Intake Forms: These types of internal documents typically contain a lot of detail provided by the client. If there is verification of the information or a signature, that is even better.

• Change Requests: This may be a formal request, a follow-up email after a phone call, or an email from the client.

• Email Correspondence: Organize and save all email communication between the agency and the client.

• Carrier Correspondence: Much like you need

to save client emails, carrier emails are also important. Especially if they contain verifications or underwriting information.

• Policy Information: Maybe I should’ve started with this one, but always keep up-to-date policy information in the client file.

• Motor Vehicle Record (MVR): An MVR is considered a consumer report protected under the Fair Credit Reporting Act. As an insurance agent, it should only be used to determine if the driver is an insurable risk. It should NEVER be shared with anyone outside of the agency, even the driver.

• Credit Card/Banking Information: This one likely does not need much explanation, but is a good reminder during our busy workdays.

• Social Security Numbers: Again, I probably do not need to point this out, but I have found some personal information in client files that the agency likely would not like to have breached.

Whether you are admiring your holiday collections or your best-in-class client file storage, we wish you all a safe and happy end to 2024. Cheers to all of your hard work!

> Mallory Cornell, Vice President, IIAW

This season and all year long, the IIAW is grateful for the support of our members. Your commitment strengthens the independent insurance channel, and we are proud to have you as part of the IIAW family.

Thank you for your continued support!

The role of insurance brokers and agents has changed significantly in the last decade. In times of hurricanes and floods, agents have moved from risk-reduction professionals to life-changing providers of resources that help and reassure clients.

Hurricanes Helene and Milton made it clear that hurricanes, storms and floods can happen anywhere and anytime and are not limited to the coast. So, what can we do to be better prepared for and respond to these events?

Typically, there are two forms of personal lines insurance related to hurricanes or severe storms: a standard homeowners property & casualty policy that includes storm and windstorm coverage and a separate policy for flood or stormwater coverage.

Notably, most standard homeowners policies include wind coverage. However, depending on the location, risk and carrier, the policy may also feature a “named storm endorsement" that decreases wind coverage and increases deductibles, inspiring some homeowners to add a second policy to cover any gaps. It's important to check clients' policies for named storm endorsements because some carriers will exclude wind.

Flood or stormwater coverage may or may not be included in routine homeowners policies. For example, water that is meant to stay outside the property—such as water from nearby

bodies of water or storm surge—is typically not covered. Water that is supposed to stay inside the property—like water from a burst pipe—will usually be covered.

If homeowners want flood coverage, they must purchase a flood policy through a private insurer or through the National Flood Insurance Program (NFIP) sponsored by the Federal Emergency Management Association (FEMA).

While the NFIP may seem like a lifesaver, the truth is that agents and brokers must now act like financial planners and review the overall financial budget required to weather a storm.

For example, FEMA's flood program and policies do not include additional living expenses if a client needs to relocate during post-storm repairs. It's one thing to ask a client to decide between an expensive flood policy that provides additional living expenses versus a FEMA flood policy that does not. But explaining the real costs of renting a three-bedroom home at $3,000 or more per month while still paying their original mortgage is a scenario that should be explained.

Agents should help clients form a disaster plan. Having a disaster plan in place may seem trivial or an afterthought for your insureds, but it's something they should prioritize. Agents also need to take preparedness seriously and follow through for the sake of your clients, their loved ones and your business.

When a storm is approaching, people will run to the grocery store for bread and milk. But this is also the time to make sure you have other resources in place. Who is their plumber? Electrician? Tree guy? They should have this information at hand.

What about mortgage forbearance and pricegouging post-storm? Monitoring the National Weather Service, Mike's Weather Page and the National Hurricane Center for storm updates can help manage the anxiety of information overload and manage expectations.

After a storm hits, the first thing to do is check on you and yours. Make sure you're okay before helping others. Beyond that, you need to quickly assess the damage. Injuries and property damage should be triaged and the worst cases will be handled first.

It's also critical to remind insureds to document the damages after a storm. Encourage them to

take pictures with their phones, especially of emergency purchases—adjusters will need that documentation. Clients should also take photos and videos of their personal assets as part of their disaster plan and save the images in the cloud.

Also, disaster plans are living documents. As needs change, your clients' coverage should also be reviewed regularly and evolve with their circumstances.

Clayton Matthews leads the claims department at Oakbridge Insurance, a Lloyd's syndicate for coastal property with a business specialty in working with homebuilders through its nearly 50-year-old national Webber Homebuilders Program.

This article was originally featured on iamagazine.com in November 2024.

The traditional coverage your customers need. The customized options your customers desire.

The affordable price your customers deserve

We’ve been successfully protecting small businesses since 1983.

Hurricane Helene materialized within a few days and was ranked as the deadliest storm in U.S. history since Hurricane Katrina before landing in Florida and causing widespread devastation across the Southeastern U.S. A week later, Hurricane Milton hit Florida and caused further destruction in some of the areas that had just been hit by Helene.

What can we learn from these storms? The biggest lesson is that we need to start taking storm risks more seriously and focus on preparedness. Another weather disaster will happen.

Independent agents can help their homebuilder and construction clients avoid or better manage the impacts of catastrophic weather through various approaches. To help businesses minimize risk and avoid the costs of future claims, here are five components to a preparedness plan that agents can help their construction clients implement:

1) Comprehensive risk assessment. Business leaders should perform comprehensive risk assessments and ensure all documentation is in order. Qualitative and quantitative risk assessments should include potential risks following a hurricane and flooding, including human, strategic, financial, operational, legal and

criminal risks.

2) Commercial insurance basics. Commercial policies address hurricanes and severe storms differently. It is extremely important to review the myriad of possible interrelated policies and their clauses, such as rental reimbursement and business interruption. There are also additional policies available that can make a huge difference based on the industry beyond general liability, umbrella and business continuity.

3) Communication. Homebuilders and construction companies should establish communications protocols, such as text groups, call trees and hidden websites, and acquire equipment, including generators, satellite phones and more. They should also clarify who makes what decisions and who reaches out to whom on behalf of various audiences.

4) Regular inventories and updates. It's essential for companies to regularly take a full inventory, prepare a video archive of their assets and regularly update policies to reflect purchases or property updates. Frequent construction status updates are also essential for documentation.

5) Site preparations. When a hurricane is closing in, construction clients should have a site assessment and preparation checklist that

addresses these questions:

• Can the company board up or otherwise close a site?

• What potential projectiles are present, both incoming and outgoing?

• What can be tied down or removed?

• Should signage be removed?

• Can supplies be moved to a secure location?

• Can power be disconnected to prevent fires?

• What water run-off issues exist?

Having a disaster plan in place may seem trivial or like an afterthought for a business, but organizations need to take preparedness seriously and follow through for the sake of loved ones, the team and the health of the business.

After ensuring the team is safe from harm, the importance of quick triage and prioritization can make a world of difference in a homebuilder or construction client's recovery.

One of the best ways to evaluate damage or losses is to have an established chain of command. Even before a storm hits, a business should establish the person or persons who will access work sites and provide real-time updates.

Whoever is leading the chain of command should have a detailed plan to restart operations. This can involve connecting with employees, determining if road conditions are safe, securing the site, determining whether buildings have functioning utilities, assessing if it is safe to re-enter and determining if there are enough supplies to return to work. It's essential to be realistic about the situation and keep employee safety top of mind.

As the stormwater recedes and planning begins for the next steps, businesses should consider the following questions:

• How has the team been affected and how does that impact returning to work?

• For those who cannot return, how can the company help?

• What travel assistance can the business provide for those who can return to work but face transportation challenges?

• Must the company legally—or can it graciously—pay those who are unable to return immediately?

• What additional steps should the company take to secure its work sites?

• What supplies does the company have that it can donate to those in need as it reassesses its own timeline?

After severe weather strikes, it is critical to document the damage. Clients should take photos and videos of their business assets as part of their pre-storm management and safety practices. Store the footage somewhere safe and keep a backup copy elsewhere. Insureds often leave money on the table because they can't remember every piece of business equipment they owned before storm damage. However, if they have everything in photos and videos, they can present that to an adjuster, making the entire claims process much easier.

Clayton Matthews leads the claims department at Oakbridge Insurance, a Lloyd's syndicate for coastal property with a business specialty in working with homebuilders through its nearly 50-year-old national Webber Homebuilders Program.

This article was originally featured on iamagazine.com in November 2024.

Now that the election is over, it is time to analyze how the results will likely impact the independent agency system, specifically insurance agency values.

Since 2016, agency values have steadily risen over the past 8 years, regardless of who occupied the White House or controlled Congress. This time period largely paralleled the hard market, which has naturally created increases in premiums and revenue, thereby giving agency values an automatic increase in growth, one of the key factors in valuation. As a result, IA Valuations’ data shows agency values have appreciated by over 40% since 2016.

In this article, we will break down the 3 key questions post-election that could impact agency values. Similar to past elections, the agenda for the major parties is starkly different, particularly for how they could impact agency owners.

First, the primary area of difference is related to tax rates: individual, business, and capital gains rates. Both parties agreed on enhancing the childcare tax credit to help working families manage the costs of child care, but that is where the similarities in the major parties’ tax plans ended.

Trump and the GOP campaigned vigorously on cutting taxes to stimulate economic growth, whereas Harris and Democrats campaigned on middle-class tax cuts and implementing a variety of tax increases on business and higher-income earners. This issue, more than any others, would’ve had the greatest impact on agency values, specifically what an agency owner would’ve taken home after a sale based on tax rates.

With Republicans winning the Presidency and the US Senate, we will see an aggressive effort to extend the 2017 20% corporate and pass-through entity tax cuts. In addition, we will not likely see Trump and the GOP

take any steps towards implementing an increase in capital gains taxes or other tax increases. This will be a priority agenda item for the Republicans as they enter the new Congressional session.

Knowing that, the second issue we will look at is what impact the election outcome will have on M&A activity. Given the results, we will not see the same agent and broker M&A run-up that we experienced in Q4 2020 and 2021 when Biden won the presidency, and Democrats controlled the House and Senate. Looking back, the IA system experienced a record level of M&A activity (20%+ increase in any previously recorded or activity since) during those time periods due to the uncertainty of capital gains and individual tax rates. With the threat of a significant increase in capital gains taxes, many M&A advisors, CPAs, and financial planners urged their agency owner clients to rush to close their sales in 2020 and 2021 before Democrats were able to enact tax increases.

As we know now, the tax increases were never adopted because the Democrats could not get all the members of their party onboard with increasing taxes.

For agents considering when to sell, tax increases hinging on the election outcome are no longer a factor. Agency owners can control the timing of their decisions without fear of the federal government changing tax rates and having an impact on their value or take home from the sale. This should result in a decrease in M&A activity and therefore could create a larger supply of agencies.

The other issue related to this is what happens with interest rates. With inflation being tamed over the past year, interest rates will not likely go back up, and therefore it should free up cheaper capital for PEbacked brokers to continue their hunt for acquisition targets, thereby keeping the demand for agencies high. We do not expect the election outcome to have a significant impact on the Federal Reserve’s

positioning on interest rates.

The third and final issue is the only uncertainty in the insurance industry resulting from this election. It is the future funding and extensions of federal government subsidized insurance programs, namely flood and crop insurance. The future funding of the flood and crop insurance programs will be under greater scrutiny as budget hawks will put pressure on GOP leaders to reduce spending. With the growing national debt, it will be difficult to fund every federal initiative and deliver tax cuts.

This will create a challenge in messaging for independent agents as we advocate for the preservation of tax cuts while asking for greater funding for the flood and crop insurance program. If your agency has a large federal flood or crop book of business, pay close attention to how these programs are treated during the first time federal funding runs out under GOP rule as it will provide some insight into how the majority policymakers plan to treat the funding of these programs.

In conclusion, like elections in the past, we do not anticipate the results to have much of an impact on agency values. We expect values to continue to trend up and the outcome of the election should buy agency owners more time to make their decision on

when and how to transition ownership or sell due to the stability in tax rates expected over the next few years.

If the election outcome or your personal situation has you contemplating the next steps with your agency, please contact Jeff Smith, CEO of IA Valuations, at jeff@iavaluations.com to explore your options.

IA Valuations and Agency Link – Founded in 2017, the IA Valuations team has performed over 300 valuations to independent insurance agencies across the U.S. Our advisors have 25+ years of experience guiding agency owners on maximizing their agency value, planning, and legal needs for ownership transition. In addition, IA Valuations has provided perpetuation planning, financial modeling and business planning for independent insurance agencies. Finally, IA Valuations has advised dozens of agency owners on selling their agencies through our Agency Link process. Agency Link is a platform that connects buyers and sellers together to further the growth and strength of the IA system. To learn more about IA Valuations, please visit IAValuations.com or contact@iavaluations.com.

In a world dominated by digital marketing, here's a tried-and-true method that has made a strong comeback in the advertising arena: direct mail.

Yes, you read that right. Good old-fashioned paper mail can support your independent agency in connecting with your audience. And that includes both personal and commercial lines customers and prospects.

So don't say farewell to your postal carrier just yet. Delve into the world of direct mail. This 150-year-old marketing channel can be a real game-changer for your firm.

Remember the thrill of receiving a personal letter in your mailbox? That nostalgic feeling holds the key to effective direct mail. In a cluttered digital landscape, direct mail stands out, demanding attention and fostering a genuine connection.

Receiving physical mail is becoming a novelty today. A survey from the United States Postal Service shows that 57% of baby boomers, 45% of Generation X, 41% of millennials, and 37% of Gen Z would be disappointed if they stopped getting physical mail.

Further, 71% of boomers and Gen Xers say that mail feels more personal than digital communications, the USPS survey found. While younger demographics are less likely to want to

receive marketing mail, 93% of millennials read mail from local brands. And 38% of Gen Z have gone to a company's website after receiving a relevant direct mailing.

Direct mail isn't just about sealing an envelope. It requires a strategy that depends on effectively timing a key offer. Here are two scenarios where the timing of your mail can yield optimal results:

Seasonal sending. Want to make a bold statement and introduce your independent insurance agency to a wide audience? Opt for a mass mailing with a well-timed theme. A seasonal campaign or a special offer can keep it impactful and fresh.

For instance, sending personalized insurance quotes during tax season is a value to potential clients. Matching up with real estate sales, spring and early summer are great times for home insurance-related communications. Or try a trip protection insurance reminder right before the busy holiday travel season. If your agency does more than property & casualty, highlight life insurance from September through October.

Welcome to the neighborhood. A warm and informative welcome package for new homeowners establishes a personalized connection. It can position your agency as a

neighbor and go-to resource for coverages in which you specialize.

Don't send all your direct mail in one shot. Consider “waves" of mailings. In advertising parlance, it's called “flighting" over a stretch of several months. Flighting not only is more effective because you can adjust messaging as you go, but it's also easier on your staff. For example, you could send 200 pieces every other week over the span of 12 weeks. Test different imagery and calls to action.

A flighting strategy could also include three similar direct mail offers to the same customers or prospects over the course of six or 10 weeks.

Designing a powerful mail piece is an art. Keep these five tips in mind to create your agency's compelling masterpiece:

1) Eye-catching imagery. A picture is worth a thousand words, and in the realm of direct mail, it can also be worth a thousand conversions. Choose images that resonate with your target audience—whether it's a family enjoying a peaceful moment at home or a young professional confidently embarking on a new journey.

Going beyond stock art, smart agencies will proudly show their associates' smiling faces helping customers on the phone, serving at a community event, or inviting the recipient to send them a text or email. Make that personal connection with good photography.

2) Clear and concise messaging. People have short attention spans, so your message should be brief and crystal clear. Use concise, benefit-driven language that highlights how your insurance services can make their lives or businesses more secure.

3) Action needed. Be sure to include a strong call to action to encourage engagement, including inviting the recipient to stop by your booth at the local farmer's market or other event

and to follow you on social media. Educate the community in your mail piece about the importance of all the relevant coverages you offer. Remember you are working to protect them. You could ask specific customers to call or email your agency to get a free umbrella insurance quote, for example.

4) Personalize. Skip the generic “Dear Sir/ Madam" greetings. Personalize your mail with the recipient's name. If possible, include details that make them feel seen and understood.

5) Postcards work, too! Try sending some oversized, colorful postcards to business owners or families. Recipients don't have to open an envelope, and your branding and messaging can be showcased in some beautiful imagery for all to see. Postcards can be cheaper to print and mail than something that requires folding, collating, inserting and sealing into envelopes.

After sending out your direct mail pieces, it's time to gauge their impact. Tracking the success of your campaign is crucial to refining your strategy and ensuring a healthy return on investment. Here are some tips:

Include a unique URL or landing page URL in your direct mail to track the number of visitors who come from your campaign. This allows you to measure the online engagement generated by your mail. The landing page can serve as an effective lead capture tool, so be sure to include a downloadable asset or contact form to obtain the visitor's contact information.

In a world where digital fatigue is real and personal connections are appreciated more than ever, direct mail emerges as a beacon of marketing brilliance. Its tactile appeal combined with strategic timing, captivating design and measurable results can transform your agency's advertising game.

This article was originally featured on iamagazine.com in October 2024.

Filling open positions in the insurance industry is becoming increasingly challenging. With 400,000 positions expected to open due to retirements alone, and rising turnover rates, it’s more critical than ever to adopt a smarter hiring strategy.

74% of Employers report hiring the wrong person for a job.

50% or More of an Employee’s Salary is often spent replacing a bad hire.

85% of Applicants exaggerate on their resumes.

Unconscious Bias: Even with good intentions, unconscious bias can lead to biased decision-making during the recruitment process.

“The process of working with WAHVE has been phenomenal. Everyone we have worked with has been efficient and very knowledgeable, and their innovative platform and processes have resulted in the best and most qualified staff additions we have ever made!”

Alexander Giraldo, VP RMS Insurance Brokerage

WAHVE’s TAO simplifies the hiring process by eliminating the need to sift through countless resumes. Our direct hire talent solution attracts and screens candidates for the best fit with your needs and company culture, using a unique seven-step process that minimizes bias.

Job Request: The system guides you through the selection of hard and soft skills necessary to define the position.

Job Ad: An automated job post creation includes a unique URL, bringing applicants directly to our platform.

Applications: Candidates complete an intuitive application, detailing their skills, experience, and credentials.

Matching: A proprietary machine learning algorithm matches applicants’ skills and experience to your job requirements.

References: An automated system customizes reference checks based on the professional relationship with the reference.

Interviews: Industry experts conduct blind interviews to further assess the applicants’ fit.

Hire: A bias-free short list of top scored candidates is provided for your selection.

WAHVE’s TAO ensures a seamless and efficient hiring process tailored to your company’s specific needs. Our approach helps you minimize hiring risks, reduce costs, and secure talent that aligns perfectly with your organizational culture.

“WAHVE made the hiring process a lot easier. The fact that they qualify all the applicants is a huge relief from the drudgery of sorting through resumes. It’s as close to plug and play as you’ll get.”

Andrew

Allen, Executive Vice

President

| Steck-Cooper & Co

“It’s hard to find good people in this job market … The candidate we hired through WAHVE has great phone presence. She’s bubbly, a breath of fresh air. She knows her stuff and fits our culture. If we have a hiring need in the future, we would definitely work with WAHVE again.”

Jeff Nosenzo, Vice President | Brown Insurance

For over a decade, using our proprietary software and qualifying process, we’ve screened over 100,000 applicants for thousands of jobs across all sectors of the industry in the U.S. and Canada. Tap into our extensive experience and insights to help you reduce the cost and time to find, hire and retain the most qualified talent to fill your needs.

Let us help you qualify and hire the right talent.

Embrace a smarter hiring strategy with WAHVE and secure the experienced talent your business needs to thrive in a competitive landscape. sales@wahve com www wahve com |

Wisconsin reaffirmed its battleground status by becoming the first state in the 'blue wall' to flip for Trump Tuesday night. This effectively secured his path to becoming the 47th President of the United States. Despite polls showing a tight race, Trump led Harris by about 30,000 votes, or less than 1% (49.6% to 48.8%), marking a wider margin than his 2016 win in the state. Although Harris had a financial edge and strong field operations, voter concerns about the economy and Harris's underperforming with minority and young voters ultimately helped Trump, who garnered more total votes than he did in 2016.

In a similarly close contest, incumbent Democrat U.S. Senator Tammy Baldwin narrowly defeated Eric Hovde by just over 27,000 votes, securing her seat for another six years. Wisconsin voters split their choices for the first time since 1968, electing a U.S. Senator from a different party than their presidential pick. Despite Baldwin's win, Republicans gained control of the U.S. Senate, unseating several Democratic incumbents. All U.S. House of Representative incumbents in Wisconsin's delegation won their re-elects. At the same time, Republican candidate Tony Wied easily defeated Democrat Kristen Lyerly to win the open 8th District in northeast Wisconsin. Control of the U.S. House of Representatives remains in the air, with Republicans holding a slight lead in maintaining control and giving the 47th Presidentelect a Republican Congress.

Following Wisconsin's first election under newly drawn legislative maps, the State Assembly will remain in Republican control with a 54 to 45 seat majority. These new maps, which were redrawn based on the 2020 census data, played a significant role in the election outcomes. This is a net gain of 10 seats for Assembly Democrats, primarily due to the new district maps. Assembly Speaker Robin Vos can

still claim a favorable result, as Republicans retained some critical seats in Democratic-leaning areas, giving the party flexibility in the upcoming session. Democrats will return with a significantly larger and newer caucus, setting them up to influence future legislation and budget negotiations and having broader committee representation.

In the State Senate, Democrats clinched all four of the competitive swing seats, reducing the Republican majority from 22-11 to 18-15. This narrower margin significantly limits the maneuvering room for Senate Republicans, potentially necessitating Democratic support for key legislation and major budget issues. Looking ahead to 2026, Democrats will only need to flip two of four competitive seats to regain the majority, a prospect that will shape legislative strategy on both sides. Republicans will likely face a strong headwind, with the midterm elections historically favoring the party not in the White House.

The state Legislature will start the 2025-26 session with 37 freshman lawmakers - more than a quarter of the legislative branch. Six new Senate Democrats, eight new Assembly Republicans, and 23 new Assembly Democrats will be sworn in for the next two years. More than half of the Assembly Democratic caucus (45 members) will comprise entirely new members.

Wisconsin's political landscape remains active as the state gears up for another crucial race - a State Supreme Court election in April 2025. This election is expected to be fiercely competitive and costly, with the potential to significantly influence the balance of power in the high court, making it a race of major importance.

>

Penn National Insurance sells property-casualty insurance in 12 states by partnering with more than 1,200 independent agency operations.

In 2012, we affiliated with Wisconsin-based, Partners Mutual Insurance Company. As one company, we bring the personal attention and local focus of a regional carrier, along with the quality of products and services of national carriers.

Penn National Insurance has an A.M. Best Rating of A (Excellent). This rating is assigned by A.M. Best to companies that have an excellent ability to meet their ongoing insurance obligations.

Penn National Insurance has achieved a “Superior Rating” for Personal Lines Claims Customer Experience for five consecutive years.

We offer an array of comprehensive commercial insurance solutions to fit the needs of your business, including Businessowners, Commercial Auto, Property, General Liability and Workers’ Compensation.

In addition, we offer personal auto and homeowners insurance.

We are looking for select commercial lines agencies in Wisconsin. Vicki Lentz 262-432-3420 vlentz@pnat.com

Clay Zogata 715-383-5454 czogata@pnat.com

Waukesha, WI

On Friday, November 15, 2024, the U.S. District Court for the Eastern District of Texas held that the Department of Labor’s (DOL) final rule (2024 Rule) raising the salary-level for exempt Executive, Administrative, and Professional (EAP) employees, as well as Highly Compensated Employees (HCE), was unlawful. The court vacated the 2024 Rule in its entirety for all employers, which means that it is no longer in effect nationwide.

By way of background, to be considered an exempt EAP or HCE, the employee must make a certain salary (salary level), be paid on a salary basis, and perform specific job duties. The DOL’s 2024 Rule impacted the EAP salary level in multiple stages:

• On July 1, 2024, the salary level increased from $684 per week ($35,586 annually) to $844 per week ($43,888 annually);

• On January 1, 2025, the salary level was scheduled to increase again to $1,128 per week ($58,656 annually);

• On July 1, 2027, the salary level was scheduled to increase to an undetermined amount; and

• Every 3 years thereafter, the salary level was set to automatically increase.

The 2024 Rule increased the HCE salary level in similar graduated fashion.

In Texas v. Department of Labor, the plaintiffs challenged the 2024 Rule, arguing that DOL's changes to the rule were in excess of the agency’s authority. The court agreed.

The court noted that although the EAP exemption does not refer to a salary level test, Congress delegated to the DOL the power to “define and delimit” the exemption. As part of its duty to “define” what it means to work in an exempt capacity, the DOL may set a minimum salary level for the purpose of screening out obviously non-exempt employees. The court stressed that because the focus of the EAP exemption should be on the exempt employee’s duties, the DOL’s ability to set a salary level is not unlimited. In other words, the DOL must not set a salary level that has the effect of supplanting the required evaluation of the employee’s role to determine whether the employee engages in exempt or non-exempt duties (duties test).

The court found that each aspect of the 2024 Rule did just that. In holding the July 1, 2024 increase unlawful, the court noted that this increase comes only 5 years after the salary-level was increased in 2019 and that, unlike past increases, it does not account for an increase to the federal

minimum wage, which has stayed the same. Similarly, the January 1, 2025 salary-level jump is estimated to render non-exempt at least 2 of every 5 employees that otherwise satisfy an EAP exemption’s duties test. Had it gone into effect, the January 1, 2025 increase would have caused approximately 3 million exempt employees to be classified as non-exempt as of that date, even though their duties would not have changed. As a result, the court found that the July and January salary levels impermissibly superseded the respective duties tests for each EAP exemption.

The court also held that the 2024 Rule’s automatic increase provision was unlawful because in having the salary level increase without notice-andcomment rulemaking, the DOL was eschewing its duty to “define and delimit” the EAP exemptions. The court noted that while Congress has given agencies the ability to promulgate rules with automatic indexing functions in other contexts, it did not grant the DOL such authority here.

Because the court vacated the 2024 Rule nationwide, this means that the July 1, 2024 increase is no longer in effect, and, as of now, the January 1, 2025 increase will not occur.

The DOL has the right to appeal the ruling. However, an appeal is not likely to change the end result, as the incoming Trump administration is expected to change course and either abandon the rule or substantially pare back any changes to the 2019 salary level of $694 per week, which was set by the DOL during Trump’s first term.

Employers who have already raised their EAP or HCE employees’ salaries to comply with the new rule, whether to comply with the July 1, 2024 or January 1, 2025 increase, may be wondering if they can revert employees’ salaries to their previous amounts. While employers technically can do so, rolling back employees’ salaries may be premature before the outcome of the DOL’s likely appeal. Rolling back salaries is also likely to create morale issues, especially in a labor market that remains tight. If an employer is going

to revert its exempt employees’ salaries to their pre-July 1, 2024 amount, the employer should provide plenty of advance notice, as well as check to see if additional notice is required by state law.

While employers do not need to increase their salaries again in advance of January 1, 2025, some employers may have already communicated upcoming salary increases to employees. If an employer no longer intends to go through with the increase, they should again provide ample notice to their affected employees, as well as check state law notice requirements. Employers planning to make downward adjustments or who are not going through with a scheduled increase in light of the Texas decision should also be cognizant of how they conveyed the increase to employees. If the employer made a definitive promise to the employee, there may be a looming breach of contract issue.

Due to the 2024 Rule and the legal challenges thereto, exemptions under federal and state minimum wage and overtime laws are getting a lot of attention. Although the Texas decision provides clarity as to the salary level increases, it is still a good time to make sure that exempt employees satisfy the applicable duties test and make any necessary classification changes. After all, the Texas decision made clear that the EAP exemption is about “duties, not dollars.”

If you have any questions about this ruling or compliance with federal and state wage and hour laws, please contact a member of Godfrey & Kahn’s Labor & Employment team.

This article was originally featured on GKLaw.com in November 2024.

WEST BEND, WI (November 18, 2024) – West Bend Insurance Company is proud to announce the addition of two new officers to its leadership team. Dee Brown joins as senior vice president and chief human resources officer, while Bob Cataldo has been named vice president and chief investment officer. Both will play key roles in advancing West Bend’s corporate strategy.

Dee Brown brings more than 25 years of human resources expertise to her new role. Previously, she served as chief human resources officer at Covenant Living Communities & Services, one of the nation’s largest not-for-profit retirement living organizations. Dee holds a bachelor’s degree in Organizational Leadership and a master’s degree in Organizational Development, both from Roosevelt University. She is also SHRM-SCP® certified. Passionate about community service, Dee serves on the board of directors for Ronald McDonald House Charities of Chicagoland & Northwest Indiana.

Bob Cataldo has more than 30 years of investment management experience, including most recently, 11 years with UFG Insurance (United Fire). Bob has a bachelor’s degree in Economics from the University of Notre Dame and an MBA from Drake University. He’s also earned the Chartered Financial Analyst (CFA®) designation. He’s active in his Iowa community,

serving on the boards of trustees for Mercy Medical Center and Brucemore, a historic mansion and estate, and volunteering at school activities.

Rob Jacques, president and CEO, stated, “We’re excited to welcome Dee and Bob to the leadership team. Their outstanding experience aligns perfectly with our strategic direction and will help us foster stronger relationships with our agents, associates, and policyholders. I’m confident their leadership will drive our continued growth and strengthen our foundation for the future.”

For more than 130 years, West Bend Insurance Company has been a trusted provider of comprehensive insurance solutions for businesses, homeowners, and auto owners. With a wide portfolio of property, casualty, umbrella, and workers’ compensation coverage across 14 states, as well as surety coverage nationwide, West Bend remains dedicated to delivering exceptional service and protection.

Agreement Includes Seven Lines of Business in 22 states; Allows Each Company to Grow Their Respective Core Business

Boston, MA – Safeco Insurance, a Liberty Mutual company and a leading provider of personal lines insurance solutions, has entered into a book transfer agreement with Main Street America Insurance, a well-established property and casualty carrier currently offering commercial and farm and ranch products as well as fidelity and surety bonds nationwide.

The eligible renewal book represents auto, home, renters, condo, umbrella, landlord, motorcycle, RV, and watercraft policies. The deal enables

Safeco to grow its personal lines presence in 22 states as Main Street America Insurance shifts to focusing exclusively on commercial lines, a move the carrier announced in late August.

“This represents one of the largest book transfer opportunities for Safeco and our agents and reinforces our position as a leading personal lines carrier for independent agents,” said Luke Bills, president of Independent Agent Distribution, US Retail Markets, Liberty Mutual Insurance. “This partnership will amplify our growth potential in several states and pave the way to expand our network of agency relationships.”

“At Main Street America, our Agents First, Agents Only pledge is more than a tag line. This partnership with Safeco is a concrete example of putting those words into action to offer a thoughtful solution as we make this strategic shift to focus solely on commercial lines,” said Richard Vaughn, head of sales at Main Street America. “This agreement offers another option for our agents to continue to provide high quality service and protection for their personal lines clients.”

While many of Main Street America’s nearly 4,000 independent agents are already appointed with Safeco, those not yet affiliated with the company are eligible to seek an appointment, further ensuring a smooth transition of eligible policies. Safeco’s advanced capabilities and experience with book transfers were a strong point of consideration in the deal with both companies focused on keeping the agent and customer experience at the center of the process.

The transition will begin in the second quarter of 2025, subject to regulatory requirements in relevant jurisdictions.

Acuity Insurance announced plans to hire more

than 200 employees in 2025, with most hires coming from new openings and positions. Job openings will span nearly every area of the company.

“As Acuity continues to grow, we are proud to add to our family of employees to meet the needs of the individuals, families, and businesses that depend on us to protect what matters most,” said Acuity President Melissa Winter.

Acuity’s revenue grew by 17% in 2023 and is on pace to eclipse that mark in 2024, surpassing $3 billion for the first time in the insurer’s nearly 100year history.

“Our ongoing expansion and continued strength and stability allow us to create new jobs and expand opportunities for current team members,” said Acuity CEO Ben Salzmann.

“We are excited to offer rewarding career opportunities to people across experience levels to fuel our progress. Acuity seeks candidates who have relevant skills while emphasizing an alignment with our core values and culture. We also remain committed to offering flexible work arrangements, including onsite at our corporate headquarters, remote, or hybrid, to support the diverse needs of our employees while maintaining a collaborative team environment,” said Joan Ravanelli Miller, Acuity General Counsel and Vice President - Human Resources.

Acuity’s employee-focused corporate culture, exceptional facilities, and rich benefits have led to continued recognition as a great workplace. For more information, visit www.acuity.com/ careers.

Acuity Insurance is a leading provider of insurance solutions, delivering exceptional coverage and customer service to individuals and businesses in 32 states. With over $3 billion in annual written premium, the insurer manages assets exceeding $7 billion and is rated A+ by AM Best and S&P. Headquartered in Sheboygan, Wisconsin, Acuity employs over 1,700 people.

IIAW agency members have unlimited access to on-demand courses and live webinars through CEU!