OFFICERS AND EXECUTIVE COMMITTEE MEMBERS

Anthony Nestler Chair Hickory Point Bank & Trust

Anthony Nestler Chair Hickory Point Bank & Trust

REGION 1

Miguel Gomez CIBC Bank USA

Maria Tabrizi First Women’s Bank

REGION 2

Peter Brummel Grundy Bank

T. J. Burge Chair-Elect Community Partners Savings Bank

Courtney Olson First Bank Chicago

REGION 3

Lawrence Horvath Heartland Bank and Trust Company

Kathy Williamson Bank of Farmington

Megan Collins Vice Chair Bank of America

Frank Pettaway Treasurer The Northern Trust Company Courtney Olson At-Large Category First Bank Chicago

Amy Randolph At-Large Category Busey Bank

Thomas Chamberlain Immediate Past Chair

Iroquois Federal Savings & Loan Association

Randy Hultgren Secretary Illinois Bankers Association

REGION 4

Scott Bland First Neighbor Bank, N.A.

Brett Tiemann INB, National Association

REGION 5

Ted Macon

Farmers State Bank of Hoffman

Bethany Shaw Peoples National Bank, N.A.

ALLIANCE

Ryan Martz Solutions Bank

MEMBERS-ATLARGE

Gustavus Bahr PNC Bank, N.A.

Dave Conterio Hometown National Bank

David Doedtman Washington Savings Bank

Brian Hannon

Cornerstone National Bank & Trust Company

Quint Harmon Resource Bank, N.A.

Tom Hough Carrollton Bank

Robert Kelly Old National Bank

Karlie Krehbiel Lisle Savings Bank

Alan Kwasneski Marquette Bank

Amy Randolph Busey Bank

Dalila Rouri BMO Bank, N.A.

Timothy Smigiel Liberty Bank for Savings

Daniel Wujek State Bank of Cherry

Two Offices to Serve You! Springfield Office: 800-783-2265 • Chicago Office: 800-878-2265

To connect with our staff, use this email format: firstinitiallastname@illinois.bank

Executive Administration

Randy Hultgren, President & CEO

Erich Bloxdorf, Management Consultant

Mindy Manci, Executive Assistant & HR Manager

Pam Macha, Springfield Office Coordinator

Finance and Administration

Mark Bennett, CPA, Executive Vice President and CFO

Matthew Keeling, Director

Marie South, Financial Assistant

Law Department

Carolyn Settanni, Executive Vice President & General Counsel

Carly Berard, Associate General Counsel

Andrés Sánchez, Staff Attorney

Jeavon Greenwood, Administrative Assistant

Government Relations

Ben Jackson, Executive Vice President

Aimee Smith, Assistant Vice President

Matt Imburgia, Director

Member Relations

Julie Winterbauer, Senior Vice President

Tim Robinson, Director, Bank Relations

Illinois Bankers Business & Education Services, Inc.

Callan Stapleton, CAE, EVP & President of Business and Education Services

Adam Walsh, Vice President, Insurance Services

Lyndee Fein, Director, Education & Conferences

Jocelyn Holzmacher, Director of Marketing

Robin Lane, Director, Associate Membership

Rachel Selvaggio, Director, Business and Education Services

Denise Perez, Director, Education & Training

Amy Sale, Education Assistant

Illinois Bankers Group Insurance Trust

Erich Bloxdorf, Plan Administrator

Mike Mahorney, Senior Trust Advisor

Hillary Meyers, Trust Manager

Banker is strictly prohibited without written permission of the publisher.

Dear fellow IBA members,

Since 1891, our Association has brought together bankers from around Illinois to do together what we cannot do on our own. That, by its nature, is the power of a successful association.

This value was displayed at our Women in Banking conference held in Springfield on October 17 and 18. Over 180 attendees from around the state assembled to learn, share experiences, and deepen business connections, with a program uniquely tailored to the professional development of female bankers. We are fortunate to have the IBA arrange such special experiences for our colleagues, which in turn, help our individual banks prosper.

When we attend IBA events, get involved, and serve on boards and committees, we make connections that can have significant positive effects on our careers and our businesses. Whether it is getting different perspectives on business matters or

collaborating on a loan participation, our members enjoy tangible benefits by spending time with industry peers. I have made great friendships, learned much, and developed business opportunities by getting to know other bankers at events, seminars, and board meetings.

The Illinois Bankers Association is much more than education, conferences, and networking. Together, the Association creates a unified (and amplified) voice for Illinois banks. The voice of the IBA, representing the interests of 246 member banks, carries a weight and credibility unmatched by any singular voice of a member. Our IBA team harnesses this strength in its proactive advocacy efforts. Today, this “voice of the IBA” is roaring loudly, as the Association takes a leading role in combatting the Interchange Fee Prohibition Act on behalf of all Illinois banks, our communities, our economy, and Illinois’ future.

Thank you for your commitment to the Illinois Bankers Association and its mission. Best wishes for continued success.

It is impossible to put a price tag on friendships, opportunities, powerful advocates, and the preparation of future leaders. Engagement with the Illinois Bankers Association brings all these benefits and so much more. Banking is all about helping people pursue their dreams and building communities. This is a noble profession, and yet the daily threats to banking through regulation, legislation, and economic uncertainty make this a very challenging industry that requires a team to fight for you. The Illinois Bankers Association is the team fighting for strong banks in every community now and for decades to come.

The value of your Association has never been clearer than in the past months in our combat against the unlawful and illconceived money grab by the biggest box stores with the assistance of the legislature through the Interchange Fee Prohibition Act. The IBA is in the unique position of strength to bring every sector of banking together to prepare and file litigation to stop its implementation. Also, through the efforts of your Association, entities such as the Office of the Comptroller of the Currency decided to file a brief that exactly supports our position against this law that harms consumers. Whether it is fighting for all bankers with elected officials, providing gold-standard training, offering powerful solutions, or building lifelong friendships, the value of your Association has never been clearer or greater.

The IBA Law Department

We are looking into making e-sign available to our customers. We would like to know what is allowed or considered a best practice with respect to e-signatures. Are there certain documents that still require “wet” signatures in Illinois, such as signature cards, loan documents, and compliance disclosures?

Electronic signatures generally are accepted in Illinois. However, we do not recommend accepting electronic signatures on certain loan documents, such as promissory notes that are negotiable instruments, unless they meet the criteria set forth in the Illinois Uniform Electronic Transactions Act (Illinois UETA).

The general rule under Illinois law is that electronic signatures have “the same force and effect under the laws of this State” as wet signatures. Like the federal ESIGN Act, the Illinois UETA provides that an electronic signature may not be denied legal effect or enforceability solely because it is in electronic form. Accordingly, we believe that signature cards, compliance disclosures, and many loan documents may be signed electronically without impacting their enforceability.

However, the Illinois UETA generally does not apply to transactions governed by Article 3 of the Uniform Commercial Code, including promissory notes that are negotiable instruments — unless the electronic document meets the Illinois UETA’s enhanced criteria to be considered a “transferable record” (included in the resources below). The UETA’s “transferable record” requirement ensures that a single, authoritative copy of an electronic promissory note can be enforced by its holder — similar to a paper promissory note.

In other words, the UETA guarantees the enforceability of electronic signatures on promissory notes that are negotiable instruments only if the promissory note qualifies as a “transferable record.” Consequently, if your bank does not have access to the electronic storage capabilities that would allow you to meet the enhanced criteria for maintaining transferable records, we recommend obtaining wet signatures on tangible promissory notes.

We received a nonwage garnishment order for a customer who has a joint account. We garnished the account, and the joint owner who was not the subject of the garnishment has asked to see the order. Are we allowed to show the garnishment order to the joint owner who is not named in the order?

ANSWER

Yes, we believe you are allowed to — and should — send a joint account holder a copy of the garnishment order that resulted in their funds being garnished.

The Illinois Banking Act provides that a bank “shall disclose financial records . . . under a lawful . . . court order only after the bank sends a copy of the . . . court order to the person establishing the relationship with the bank.” In the case of a joint account, we believe both joint owners are persons who have established a relationship with your bank. Consequently, we believe you must send a copy of the garnishment order to both joint owners, including the joint owner who was not named in the garnishment order, since you are

disclosing their financial records to a third party. Such disclosures would not violate the privacy rights of either joint accountholder, since the Illinois Banking Act’s privacy requirements authorize banks to disclose customers’ records in response to a lawful court order.

Also, we believe a joint account holder is entitled to a copy of a garnishment order, even if they are not named in the order, since they may be able to claim an exemption protecting their interest in the account funds or raise other defenses to the judgment creditor’s attachment of the funds. For example, the joint owner who was not named in the garnishment order still could be entitled to claim a $4,000 personal property exemption in the account funds.

For customers who receive e-statements, if we receive a message that the statement was undeliverable due to their email address no longer existing, is it our responsibility to reach out to the customer to correct the error? This has occurred when an individual customer has elected to receive statements at their work email and then changes jobs, or a business customer’s statements are sent to the email of an employee who no longer works for the business. Are we in violation of any law or regulation if a customer doesn’t receive an e-statement due to their email address being disabled?

We are not aware of any law or regulation that would require you to contact a customer after receiving notice that an e-statement was not delivered. However, from a customer service standpoint, it may be prudent to contact your customer by phone or physical mail to determine whether they would like to designate a new email address for receiving e-statements.

Both Illinois and federal law require you to obtain a consumer’s affirmative consent to receive statements electronically. When obtaining this consent, you also must provide a consumer with a clear and conspicuous statement informing of them of their right to withdraw their consent to receive statements in an electronic format and describing the procedures they must use to

withdraw consent “and to update information needed to contact the consumer electronically.” At the time of providing affirmative consent, the consumer must consent “in a manner that reasonably demonstrates that the consumer can access information in the electronic form that will be used to provide the information that is the subject of the consent.”

Assuming your bank followed these procedures, your customer initially demonstrated their ability to access e-statements through their email, and the customer has not since updated their contact information, we do not believe you are in violation of any law or regulation if an e-statement is returned due to an email address being disabled.

Our IBA Law Department provides many resources to help our bank members meet their compliance challenges, including a toll-free Compliance Hotline (1-800-GO-TO-IBA) and a dedicated compliance website (www.GoToIBA.com). We also publish a free weekly e-newsletter highlighting the latest regulatory developments, select recent Q&As, and other useful information –let us know if you want to subscribe!

Note: This information does not constitute legal advice. You should consult bank counsel for legal advice, even if the facts are similar to those discussed above.

By Rob Nichols, President and CEO, American Bankers Association

Football season is in full swing, and here in the nation’s capital, the home of the Washington Commanders has a new name: Northwest Stadium, the moniker of Virginia-based Northwest Federal Credit Union, which recently inked a multi-year, multi-milliondollar stadium naming deal.

If you’re wondering how a credit union—a nonprofit, tax-exempt entity—can afford such a hefty marketing spend, you’d be asking the right question. When Congress passed the Federal Credit Union Act authorizing the creation of federal credit unions, its intention was for these institutions to serve people of modest means within clearly defined communities united by a common bond.

But times have changed. Today, many credit unions—in pursuit of endless growth—have dramatically expanded their fields of membership. Northwest—whose marketing budget ballooned by 88% from 2022 to 2023—was founded in 1947 to serve CIA employees. It now offers membership through multiple federal agencies, as well as “hundreds of businesses and community organizations.”

Northwest isn’t the only credit union spending top-dollar on marketing to grow membership far beyond its original scope. In fact, several of the largest credit unions now purport their potential membership base to be upwards of 330 million Americans—effectively the entire population of the United States.

If you’re wondering how a credit union—a nonprofit, tax-exempt entity—can afford such a hefty marketing spend, you’d be asking the right question.

If credit unions are now empowered to cast a net this wide and compete aggressively for market share with taxpaying institutions, it’s time for policymakers to stop punting the ball on ensuring that these institutions are accountable and transparent in their operations.

ABA expressed this view in a recent letter to NCUA Chairman Todd Harper—who has himself questioned whether credit unions should be spending so much on stadium naming deals, when those funds could be better spent supporting members. In addition, there have been several positive policy developments in recent days that suggest a growing appetite in Washington for greater accountability and transparency for the $2.3 trillion credit union industry.

One example: In a recent policy statement, the FDIC signaled that it will begin requiring credit unions to provide additional information when applying to acquire an FDIC-insured bank. Credit unions have targeted a total of more than $9 billion in bank assets so far this year, with 18 deals announced in 2024 alone. ABA remains deeply concerned about the increasing number of these types of transactions and the potential tax losses and effects on local

communities that accompany them. Regulators should rightfully scrutinize these deals, given that credit unions are not subject to any federal Community Reinvestment Act requirements.

Greater accountability is also expected through an upcoming rulemaking on executive compensation transparency from the National Credit Union Administration that would require the disclosure of certain financial information by federal credit unions. Given that credit unions are democratically controlled financial cooperatives, it is essential that their member-owners have greater visibility into how top executives are incentivized relative to these transactions.

Regulators are not the only ones taking note—in fact, in just the past year, a total of 80 members of Congress have publicly questioned credit union activities.

Taking all these developments into consideration, it seems the time is right to move the chains on credit union accountability. You can count on ABA to continue playing offense on these issues in the months ahead.

E-mail Rob Nichols at rnichols@ aba.com.

By BOK Financial Capital Markets

After four years of hiking rates and then keeping them high, the Federal Reserve has now started lowering rates, hitting the ground running with a large cut of 50 basis points (0.50%) in September. As rates continue to fall, it’s important for management teams to understand how lower rates will impact their institutions’ income statements and to take steps to better position themselves for the even lower-rate environment likely to come.

First, let’s consider where we are now and how we’ve gotten here. Over the past few years, federal and consumer spending have been driving economic growth, despite higher interest rates. However, with many consumers now having used up all their excess savings from COVID— and then some—and also having record credit card debt, it’s questionable whether consumer spending can last at these levels. Meanwhile, unemployment has risen, which has raised concerns about weakening in the job market, even though unemployment is still relatively low on a historical basis. Given all these factors, the market is now forecasting a large number of Fed rate cuts, and some investors are wondering if the Fed can still pull off a soft landing or if a recession is in the making.

Against this backdrop, each decision your management team makes in the last quarter of 2024 will be impactful for 2025. For instance, one important question to consider is when to begin cutting deposit rates. As financial institutions assess their ability and willingness to do so, margin and liquidity position will be important considerations. The news cycle also may aid decision-making this time around, as the Fed cuts likely will be well covered by the media. Consider reviewing rates against wholesale funding rates regularly and be prepared to adjust deposit rates frequently. Conversely, intermediate Treasury and wholesale funding rates have already fallen. To the fullest extent possible, attempt to hold loan rates higher for longer until the cost of funds begins to recede. Frequently, we see a race to the bottom on loan rates, so be prepared to fight for every basis point! This strategy may allow your institution to manage net interest margin from both sides of the balance sheet.

With a significant inversion in the yield curve between Fed Funds and intermediate Treasuries, a non-parallel yield curve shift may be a more likely outcome. This may be led by the front end coming down more significantly than any changes in term Treasury rates that have already accounted for expected future rate cuts. If your institution has substantial risk around falling rates, you may be wondering if it is too late to manage your position given the inversion in the curve. What if you will benefit at some point from a steeper lower yield curve? Can you wait it out? With these questions in mind, you may want to take some proactive steps to hedge the risk of the market being wrong.

The current yield curve challenges investors to diversify risks. Although keeping large amounts of cash or short securities can generate the highest yield today, doing so could result in significant yield erosion if or when the short end comes down. Equally, the decision to lock into investments further out on the curve may give up immediate earnings for possible future benefit.

Instead, a balanced investment strategy could allow your institution to add a mix of securities that average a yield close to the Fed Funds rate with an allocation to call-protected assets. We urge management teams to consider the trade-off of investing in only the highest yield options compared to the potential benefits of adding assets with call protection that could result in an unrealized gain when the Fed lowers rates further.

Finally, it’s important to keep in mind that repeating the past is unlikely, but it’s still essential to learn from it. Understanding the choices that your institution made and then making informed decisions for the future is how your institution can and will put its best foot forward.

Kent Musbach is a senior vice president and Marc Gall is a senior vice president and asset/liability strategist for BOK Financial Capital Markets.

Contact BOK Financial Capital Markets at 866-440-6514 to discuss the latest economic outlook and timely considerations. We can help guide a unique, well-conceived strategy that considers many variables and potential outcomes.

By Julie Winterbauer, Senior Vice President, Member Relations

Membership in a group means different things to everyone. For decades, we have been passionate about bringing the collective soul together for one purpose, one mission. That purpose varies within our membership and as we reflect on the year, we are reminded of the value the IBA brings to our members and honestly to all banks in Illinois. But the story begins with the foundation.

Banking is more than a business; it’s a vital service to our communities, customers, owners, and shareholders. The foundation of every successful bank is its dedicated staff. You cannot build a great bank without an exceptional team of bankers. In these times of navigating the best practices to recruit and retain your staff, the IBA is here to support you! Investing in your people shows that you value their contributions and empowers them to drive your bank’s success. Whether you enroll your team members in our extensive educational programs, encourage them to pursue advanced leadership and banking certificates, or elevate their exposure (therefore, the bank’s exposure) by involving them in one of our 19 boards or committees, you are demonstrating a commitment to their growth. The IBA does not take our position lightly. We are

dedicated to providing you with the resources and support needed to elevate your team, helping them become the best bankers.

A strong foundation of dedicated employees is essential for strengthening, protecting, and growing your bank. Protection is a key element for the bank, its team, and its customers. Regulations may be crafted with the best intentions to protect our industry, consumers, and businesses. However, they often add to the already heavy burden banks face, creating a widely recognized, unfair burden and unintended consequences on our industry. That’s why we have an exceptional advocacy team fighting for and protecting you! We are the only trade association representing banks at the federal, state, and city levels and we aren’t afraid to fight the big fights! And remember since we are inclusive to all banks, we recognize the big picture when stopping, supporting, or crafting legislation – when you give an inch, sometimes they take a mile. Together, we stand united in our efforts to protect your bank, giving you peace of mind and reinforcing the solid foundation upon which you can build your future.

Not surprisingly, the IBA steps up BIG TIME with another critical tool in the toolbelt for crafting a strong foundation. We offer a dedicated team of attorneys

and our exclusive members-only online resource — Compliance Connection®. This unique resource is designed for compliance officers at all levels. The platform provides information on both state and federal laws along with important accompanying information (regulator guidance, recent FAQs, articles, sample forms and policies, and much more) presented in a user-friendly format. And, what about compliance education? The IBA provides an exclusive curriculum of 100 courses through Regulatory University which satisfies much of the compliance education for your team – from front line to directors. Best of all, the compliance suite of products is FREE for our members!

While we have your attention, let’s share more! We alluded to protecting our members and crafting a strong foundation. As you work to make your bank a stable stronghold in the communities you serve, you must ensure that you are shoring up your protections so you will not fail those you are serving. Our insurance offerings were established years ago to provide coverage to our members that could not be found elsewhere. We encourage you to explore our comprehensive

range of financial institutions’ coverages ranging from cybersecurity to medical; we have solutions for you. Our team of insurance agents can review your coverage and often find significant savings, holes in coverages, new lines that are needed, or offer our unique Group Trust program for medical and ancillary coverage.

What do you need to fully armor your bank and position it at the forefront of protecting and serving your customers? A plethora of carefully vetted, top–tier preferred vendors to give you the finest arrows in your quiver – you want to know that you can pull from that bag, ensuring that you have the most effective and trusted solutions for your bank.

The IBA is honored to serve banks in Illinois. For the past 133 years, we have humbly referred to ourselves as the rock of this remarkable industry by providing real, tangible value and we look forward to continuing our mission of “Advocacy. Education. Industry Resource…for all Illinois bankers.” As always, we are dedicated craftsmen committed to the ambitious goal to continue building and growing banking in Illinois.

By Christy Thomas, Audit Manager, SBS CyberSecurity

Cyberattacks no longer only impact the targeted organization but also have a ripple effect that harms partners, service providers, customers, and others. In an era where digital interconnectedness is the norm, the consequences of cyber incidents extend far beyond the initial breach, affecting a wide network of stakeholders.

As data breaches continue to trend up, organizations are spending more money and resources to ensure they have the appropriate solutions in place to prevent attacks without disrupting normal business. This escalating threat landscape underscores the critical role of the ISO in adopting proactive security measures.

Consider the following topics as part of an information security program review:

One of the most crucial risks to organizations in today’s environment is ransomware. The CSBS updated the Ransomware Self-Assessment Tool (R-SAT) to version 2.0 due to evolutions in the ransomware threat environment, bad actor tactics, and changes in environments and controls.

Inadequate mitigation measures or lack thereof may intensify vulnerabilities and increase the risk of ransomware attacks if not promptly addressed. The R-SAT provides significant advantages by raising awareness about ransomware risks, identifying security gaps, and giving executive management and the board of directors the information they need to make informed decisions and allocate resources appropriately. It also assists auditors, consultants, and examiners in evaluating security practices and incorporates

lessons learned from organizations that have experienced ransomware attacks.

An organization's board of directors is ultimately responsible for its overall security. Without a solid grasp of cybersecurity, the board may make decisions that inadvertently weaken the organization's security posture and lead to insufficient budget allocation for cybersecurity initiatives. Additionally, a lack of understanding can result in security strategies not aligning with overall business objectives, as well as underestimation of cybersecurity risks leading to inadequate risk management and crisis response plans.

Approximately 60-75% of our customers utilize an outsourced vendor for firewall management; while it is a trusted relationship, the organization has the ultimate oversight responsibility. The organization should, at a minimum, understand its network baseline to determine the right questions to ask and key risk indicators for its environment.

When a vendor manages your firewall, it introduces both risks and opportunities. Relying on a third party means your organization is dependent on their expertise, responsiveness, and reliability. However, misconfigured firewalls can lead to vulnerabilities and become exposed to threats. Also, having limited visibility into the vendor’s operations can hinder your ability to monitor and assess security effectively and ensure proper data protection measures to prevent unauthorized access or leaks.

To mitigate the risks of vendor firewall management, it is important to implement appropriate controls, including defining roles, responsibilities, and expectations in written contracts to eliminate any questions as to who is doing what. Periodic security audits of the vendor’s practices should be conducted as part of your vendor management program.

Administrative access to the firewall should be limited to authorized personnel only, and require strong authentication mechanisms, such as MFA and individual authentication (no shared accounts). Oversight should include receipt and review of comprehensive logs or read-only access, at a minimum, to monitor these logs for suspicious activities or policy violations.

Remember that collaboration and transparency are essential – and these controls play a crucial role in ensuring the security and proper functioning of firewalls. By implementing them diligently, organizations can enhance their oversight and response capabilities regarding firewall activity.

Implementing MFA is a key defense strategy, adding an essential layer of security by requiring two or more verification factors. Enhancing network security with MFA solutions helps increase datacenter security, boosts cloud security for a safer remote working environment, and minimizes cybersecurity threats.

Additional controls surrounding administrative access to directory services, network backup environments, network infrastructure, organization’s endpoints/ servers, remote access (employees and vendors), and firewall management are recommended. Many cybersecurity insurance vendors now require organizations to complete a self-attestation to renew policies. Included within the attestation is the verification of multi-factor authentication for remote access users and administrative users.

The vendor management program continues to evolve and requires diligent monitoring and research, especially for those vendors deemed critical to operations. Adhering to FFIEC Guidance and Interagency Guidance ensures comprehensive risk evaluation in vendor relationships, comprised of due diligence procedures, acquisition procedures, defined vendor risk classifications, annual risk assessments, presentation of critical vendors to an authorized committee, and adequate contract review procedures.

Effective vendor management optimizes costs, grants access to vendor expertise, enhances agility, minimizes potential disruptions, and provides a seamless customer experience. However, poor vendor management practices can lead to operational disruptions, security breaches, and non-compliance with regulatory requirements.

Organizations should adopt a comprehensive vendor management program to address vendor risks and ensure adherence to legal and regulatory standards.

An independent assessment is crucial for identifying and mitigating potential cyber threats within the Microsoft 365 environment. The independent assessment should evaluate the environment and ensure the organization has implemented appropriate controls to mitigate risks, including malware, third-party app access, data loss prevention, external sharing, advanced threat protection, and permissions.

Common security gaps within the Microsoft 365 environment include overly privileged administrator roles, incorrectly implemented multi-factor authentication, inadequate admin center settings, audit log and activity log neglect, and authorization misconfiguration.

Implementing various disaster recovery measures to prevent and mitigate ransomware attacks is important, including keeping multiple backups on and off-site, replicating critical data, encrypting data, and air-gapped backups. Regular testing of backup procedures is essential for ensuring data recoverability in the event of an attack. An air-gapped backup is not connected to a network, so it cannot be reached by hackers, as many ransomware variants attempt to find and delete any accessible backups. Maintaining offline, current backups is critical because there is no need to pay a ransom for data that is readily accessible to your organization.

An additional step to mitigate ransomware, which may be an option depending on budgeting, is immutable backups. An immutable backup is a backup file that cannot be altered in any way. It should be unchangeable and able to deploy to production servers immediately in case of ransomware attacks or other data loss. Keeping an archive of immutable backups can guarantee recovery from a ransomware attack by finding and recovering the last clean backup you have on record.

As part of risk mitigation, organizations should create, maintain, and exercise a basic cyber incident response plan and associated communications plan for a ransomware incident. If a vendor or MSP is responsible for maintaining and securing backups, ensure they follow the applicable best practices. Formalizing security requirements through contract language is a best practice that safeguards your data integrity.

Regularly testing and validating backup processes can give an organization confidence in its ability to restore data in the event of an emergency. This includes restoration testing, functional failover testing - spinning up critical backup servers, and other emergency preparedness testing (tabletop exercises, simulations, etc.).

The shift towards remote audits and examinations has spotlighted the Bank Protection Act of 1968, ensuring institutions manage and monitor physical security effectively in line with regulatory expectations and risk levels. The move to remote audits poses challenges for physical security verification, often relying on videos or photographs for assessment.

To bolster physical security measures, it is recommended to appoint a dedicated security officer to oversee the comprehensive implementation of the security program and deliver an annual security report to the board of directors.

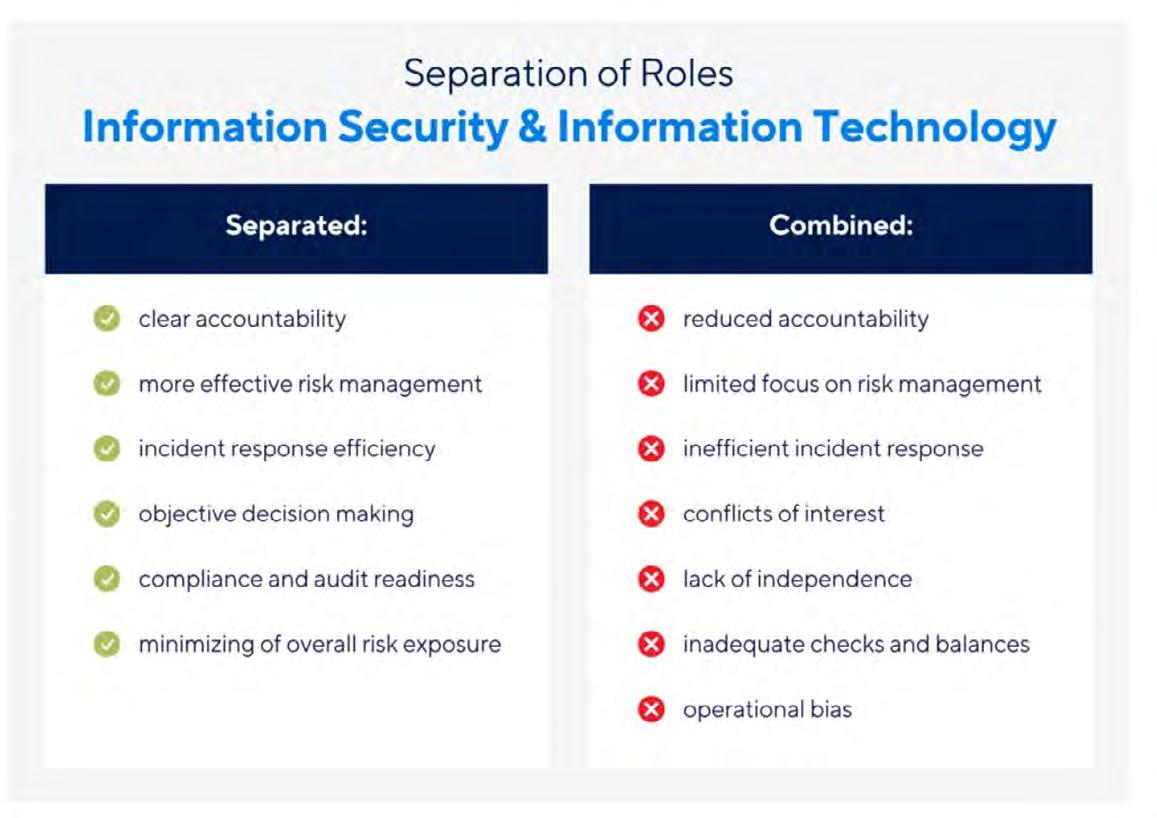

Once a financial institution reaches $750 million in assets, the regulatory and external audit scrutiny will increase surrounding the segregation of roles associated with information security and information technology. The information security officer should be independent of IT operations staff and should not report to IT operations management.

The following policies should be documented within an information security program, and some have become formal recommendations by examiners and regulators within the last 12 months.

• End-of-Life (EOL) Policy

• Imaging Policy

• ATM/Debit Card Management Policy

• Instant Issue Policy

• Internet Banking Policy

These enhancements aim to bolster the institution's security posture, ensuring comprehensive coverage of physical and digital security aspects in alignment with evolving regulatory standards and cyber threat landscape.

S h a p i n g T o m o r r o w ' s

Transform talented employees, new or seasoned, by cultivating the next generation of bank leaders through the dynamic Future Leaders Alliance Program (FLA). This unique program builds employee confidence, creates a positive environment, and strengthens the organization’s performance. The FLA leadership framework contains an emphasis on personal and professional development, community service, and networking

C

By Connor Heaton, SRM

The rapid advancement of artificial intelligence, particularly generative AI tools like ChatGPT, is ushering in a new era of financial fraud. Malicious actors are leveraging these technologies to craft more convincing and sophisticated scams, putting consumers and institutions at greater risk than ever.

ChatGPT and WormGPT have enabled fraudsters to craft more convincing and sophisticated phishing messages, overcome language barriers, and increase personalized attacks. One security group recorded a 135% increase in novel social engineering attacks with earmarks of AI tools in the first two months of 2023. Another report estimates a 3000% increase in deepfake-based fraud between 2022 and 2023. Numerous indicators suggest that AI enables threat actors to craft sophisticated and targeted attacks at speed and scale.

But it's not just phishing. Fraudsters are exploiting AI across multiple fronts:

Deepfakes and Identity Fraud: In February 2024, a finance worker was tricked into transferring $25 million to scammers using a deepfake of the company's CFO in a video call. On at least 20 other occasions, AI-generated deep fakes were used to fool facial recognition systems with fake identity cards. There are even examples predating the advent of generative AI.

Website and App Spoofing: AI tools can tremendously aid website development, fueling a rise in fraud. Attackers are using AI to rapidly create spoofed banking websites and mobile apps nearly indistinguishable from the real

thing. 50% of phishing links now lead to these fake dataharvesting sites. Consumers continue to be targeted at a slightly higher rate than corporations, underscoring the importance of educating users and helping them protect themselves.

Corporate Fraud – False Vendor Invoicing: Corporate bank accounts have also become attractive targets for a new breed of sophisticated social engineering scams. Fraudsters are exploiting the complex structures and communication gaps within large organizations. The attack pattern is straightforward but effective: fraudsters spoof an email or website to impersonate a trusted supplier and request payment to a fraudulent account.

Even when banks flag these transactions and call clients to confirm, they often do so because they believe the request is legitimate. Employees frequently won't realize until the legitimate vendor inquires about the missed payment.

FakeGPT and Data Theft: Even AI tools themselves aren't safe – a wave of nearly 1,000 fake ChatGPT websites created to collect user data have been identified and blocked by Meta from being shared on its platforms.

Financial institutions aren't sitting idle. Over the past year, incumbents like MasterCard, Jack Henry, FIS, PSCU, and more made considerable investments in AI and partnered with or acquired startups to bolster their defenses.

Large players like JPMorgan Chase are tuning custom generative AI models to analyze unstructured data like emails and wire instructions for fraud signals. Their models train on the bank's data to learn to flag suspicious activity.

These models are additive, integrating into existing fraud prevention frameworks. AI is woven in at various points in the payment lifecycle –validating account details upfront, flagging anomalies in-flight, and scoring transactions for fraud risk after the fact. Layering cutting-edge AI on top of proven rule-based engines and other controls creates a formidable, end-to-end defense.

Payment leaders like Visa, Mastercard, Verafin, and others are taking the same approach, incorporating the new AI capabilities into their fraud offerings, and as a result, most FIs benefit from AI-enhanced fraud protection without needing to undertake custom AI fraud projects themselves.

The Biometric Authentication Arms Race Biometrics vendors broadly agree that in the current arms race between voice synthesis and synthetic voice detection, biometrics alone are inadequate authentication for something as high-risk as an ACH transaction.

Additional layers of probabilistic scoring, such as factoring in behavioral data like time of call, phone number, and device/connection information are vital to selecting the appropriate level of challenge (e.g., password, MFA, out-of-wallet questions).

No biometric solution will ever be perfect – accuracy in identifying synthetic audio can vary substantially, from below 80% to over 98%, depending on how the antispoofing model has been trained relative to the live audio.

It will be up to individual institutions to determine their risk appetite and set requirements for accuracy and specificity. As is the case with automation broadly, the performance target for adoption often isn't perfectionit's just better than humans.

Digital identity proofing, authentication, and Know Your Customer (KYC) checks are getting more difficult due to the democratization of advanced AI image and video generation and editing capabilities.

Generative AI hobbyists online are pioneering prompts, finetuned models, and sophisticated combinations of open- and closed-source technologies to produce highly plausible KYC-style verification photos and videos.

Moreover, this is possible with part-time enthusiasts and consumer-attainable technical setups; we should expect companies, hacker groups, organized criminals, and state actors with far deeper pockets to fool KYC checks much more quickly and reliably.

There's already plenty of evidence of this sort of synthetic fraud – "on at least 20 occasions, AI deepfakes had been used to trick facial recognition programs by imitating the people pictured on [stolen] identity cards."

Currently, having any significant number of photos and videos of your face publicly available on the internet, as most of us do, is an increasingly serious liability. Consumers, so far, show no signs of changing their behavior, putting the onus on businesses to effectively identify and block increasingly sophisticated identity theft.

The challenges of reliably verifying digital identities online are here to stay until a comprehensive, nationwide solution emerges – an effort likely to span a decade or more. In the meantime, we find ourselves firmly in an era of questioning the humanity and intentions behind every digital interaction. While effective, current AI-proof identity verification methods are highly onerous for users and businesses. As fraudsters ramp up their use of generative AI, this friction will only intensify, fueling demand for more streamlined and holistic identity solutions.

Proposed remedies like Worldcoin may or may not ultimately prove adequate. Worldcoin is a startup co-founded by OpenAI's Sam Altman that aims to become the global choice for a zero-knowledgeproof biometric authentication solution. Regardless, one thing is clear: governments and businesses must unite around a practical framework well before 2035 to avert a full-blown crisis of trust in online identity.

Until then, financial institutions must double down on maximizing the efficiency of their fraud operations and educating clients at every high-risk point of contact on the fraud modalities they may encounter. Continuous monitoring and improvement are necessary for FIs to stay one step ahead in the escalating battle against AI-powered fraud.

Connor Heaton is the Director of Artificial Intelligence at SRM, an advisory firm serving financial institutions in North America and across the globe. He leads client engagements focused on artificial intelligence and helps organizations understand and adopt disruptive technologies.

... The Illinois Bankers Insurance Services proposal surpassed our expectations with extraordinary savings and better insurance coverage. The time to receive a quote was minimal, and the cost savings more than covered our annual dues ...

The annual Fall Golf Outing was held at the beautiful Bloomington Country Club on September 30th.

Almost 60 attendees enjoyed the perfect fall weather day, filled with comradery, strategic networking and opportunities to immerse with like-minded industry peers. Thanks to our sponsors and everyone who participated!

Mark your calendars for the 2025 Fall Golf Outing to be held at the Bloomington Country Club on September 22, 2025!

Central Bank Illinois

The 2024 Women in Banking Conference, held on October 17-18 at the Crowne Plaza Springfield, was a resounding success with record-breaking attendance of nearly 200 participants. The event featured a diverse array of sessions focused on professional development, networking, and empowerment for women in the banking industry.

Highlights included presentations on building networks, supporting women in banking, and finding one's voice in the workplace. The conference also offered unique experiences such as yoga sessions and Dutch Treat Dine-Arounds for networking opportunities.

A standout moment was the Women in Banking Award Ceremony, which recognized outstanding achievements in the industry. Denise Ward from Central Bank Illinois was honored as Woman of the Year, while Ashley Speed from Grundy Bank received the Woman on the Rise award. These accolades celebrate their significant contributions and leadership in banking.

The event wrapped up with an inspiring session led by Natalie Bartholomew, known as The Girl Banker, who motivated attendees to champion women's roles in banking and cultivate the future generation of women in banking.

Save the date for next year’s conference OCTOBER 2 - 3, 2025

The recent BankTech Conference brought together industry leaders and innovators to explore technologies and strategies shaping the future of banking. With a focus on artificial intelligence, cybersecurity, and digital transformation, insights were on display for bankers looking to stay ahead in an increasingly competitive landscape.

Kicking things off, Ben Udell, SVP of Digital Innovation at Lake Ridge Bank, demystified generative AI applications for everyday banking operations. He highlighted the transformative potential of generative AI, addressing common concerns such as bias and privacy while providing actionable strategies for banks to pilot AI initiatives effectively.

The risks and benefits of AI in financial institutions took center stage during Scott Stevens' presentation. As Chief Information Security Officer at Integrity Technology Solutions, Stevens provided executivelevel guidance on AI implementation, covering compliance requirements and best practices for protecting sensitive information.

Beardstown Savings, s.b. received accolades for their partnership with Worldwide Tech Connections, offering digital translation services in over 50 languages to enhance inclusivity and serve underbanked communities.

Byline Bank was honored for their AI-powered approach to commercial loan origination, significantly improving efficiency and data quality through innovative integrations.

Cybersecurity was the focus of an engaging role-play session led by Mishaal Khan and Matt Cox from Mindsight. Their "Attackers vs Defenders" demonstration illustrated various attack methods and defensive strategies, providing attendees with practical insights into prioritizing and managing security risks.

The emergence of non-traditional competitors was addressed by Larry Pruss of Strategic Resource Management. Pruss explored how neobanks, fintech platforms, and insurtech companies are reshaping the industry, urging established banks to embrace digital transformation to remain competitive.

Closing out the event, Peter Tapling of PTap Advisory discussed the latest developments in payments, including the FedNow Service and upcoming CFPB rulemaking. Tapling emphasized the strategic importance of navigating changes in payment speed, visibility, and options.

As bankers left the summit, they were armed with fresh perspectives on leveraging technology to enhance operations, improve customer experiences, and stay ahead in an evolving financial landscape.

Mark your calendar for next year’s conference, October 23, 2025, in Oak Brook.

Meetings were held with key legislative leaders and regulators to discuss the pressing needs facing small and large institutions from around the state of Illinois” with “The highlights of this visit were meet ings with regulators, including with new FDIC Director Jonathan McKernan, the CFPB, the Federal Reserve, and top officials from the OCC.

The key message delivered was that the Illinois banks are doing well, even though they must deal with unprecedented levels of regulatory and legislative challenges. We updated our Members of Congress from Illinois on our litigation to stop implementation of the Interchange

Fee Prohibition Act. We also updated them on the Access to Credit in Rural Economies (ACRE) Act that allows banks to offer the same tax treatment on rural loans that Farm Credit does.

We focused on important legislative topics including our support for ACRE, which would level the taxation playing field between banks and Farm Credit. We also discussed tax parity for credit unions, urged support for cannabis banking reform, and strongly opposed Durbin’s Credit Card Competition Act, another power grab by Durbin on payment cards on behalf of mega-retailers.

Together, the IBA and Illinois grassroots bankers are continuing to foster important banker-legislator connections that are critical to our industry’s success as we continue to battle legislation and regulation.

By Faruk Daudbasic, Senior Vice President - Group Head, Director of

Community Development Financial Institution (CDFI) Banks, like First Eagle Bank, are proud to be at the forefront of driving community development and economic empowerment. With a long-standing "Outstanding" rating for the Community Reinvestment Act (CRA), our designation underscores a commitment to serving underserved communities, advancing financial inclusion, and fostering economic resilience. We invite other financial institutions to join us in this mission by partnering with CDFI’s in Illinois.

Here are the key benefits for banks when collaborating:

Partnering with CDFIs allows financial institutions to support community development initiatives while earning CRA credit. The FDIC financial institution letter (FIL64-2017), along with the OCC policy statement and documentation, confirm regulatory support for CRA credit related to such partnerships. Both current and

upcoming CRA guidelines emphasize the importance of CDFI partnerships, with these activities qualifying for CRA consideration. Additionally, partnering with CDFIs will also earn credit under the newly implemented Illinois Community Reinvestment Act (IDFPR, Section 345.200 Assessment Factors e), further reinforcing the value of these partnerships. Our approach ensures investments align with regulatory requirements, enabling banks to fulfill their CRA obligations while making a positive impact in underserved communities.

Most CDFIs, including First Eagle Bank, offer fully FDIC-insured deposits through the IntraFi Network's Certificate of Deposit Account Registry Service (CDARS). By investing in CDs through CDARS, partner banks can safely place funds while remaining within FDIC insurance limits. This arrangement provides a

secure avenue for supporting community development with peace of mind.

Collaborating allows institutions to participate in financing projects that uplift communities. Our CDFI status reflects a strong commitment to funding local businesses, affordable housing projects, and community facilities in underserved neighborhoods. Partner banks contribute to meaningful economic development, helping create jobs, support small businesses, and promote sustainable growth.

Partnering with a CDFI enhances your institution's commitment to diversity, equity, and inclusion. As a CDFI, we are dedicated to addressing the financial needs of historically underserved populations. By investing with us, your bank demonstrates a commitment to social equity and economic empowerment, reinforcing your DEI initiatives.

Partnerships provide an opportunity for banks to be recognized for their commitment to community development. We work closely with our partners to share the outcomes of our initiatives, showcasing the collective impact on local communities. This not only enhances the visibility of partner banks but also builds goodwill and trust with clients, stakeholders, and regulators.

Prioritizing financial literacy and education as essential components of community development. Our programs aim to improve financial capabilities, providing the tools and resources for individuals and businesses to thrive. By partnering with CDFIs, banks can participate in these initiatives, helping to bridge financial education gaps in the community.

Joining forces with CDFIs opens doors to collaborative opportunities in a network of CDFIs and mission-driven financial institutions. We actively seek partners who share

our vision for a more inclusive and equitable financial system. Together, we can unlock new potential and make a lasting impact through co-financing projects, shared resources, and combined expertise.

We encourage banks looking to enhance their CRA performance, support economic development, and commit to social equity to consider partnering today. Together, we can drive meaningful change and unlock the potential of communities that need it the most.

About the author: Faruk Daudbasic is Senior Vice President - Group Head, Director of Community Development for First Eagle Bank

For more information about partnership opportunities with First Eagle Bank, please contact us at 312-8509232 or fdaudbasic@febank.com to explore how we can collaborate on your community development goals. First Eagle Bank – Chicago, IL www.febank.com.

Below is a list of other IBA member CDFIs that may offer similar solutions. Please contact them directly to learn more about their specific offerings. For potential partnerships with other CDFIs, visit their respective websites provided below for additional details and information.

• International Bank of Chicago, Chicago, IL www.inbk.com

• Pan American Bank & Trust, Melrose Park, IL www.panamerbank.com

• Pulaski Savings Bank, Chicago, IL www.pulaskisavings.com

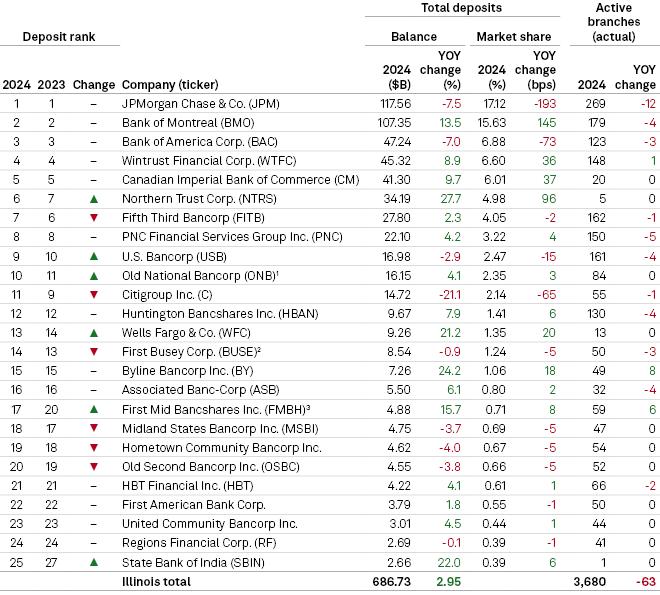

By Rica Dela Cruz and Hussain Shah, Market Intelligence

Banks in Illinois booked a nearly 3% growth in deposits year over year, pushing the state's share of total US deposits higher.

Deposits in Illinois accounted for 3.95% of the nation's deposits as of June 30, compared with 3.86% a year ago, according to the annual Summary of Deposits data from the Federal Deposit Insurance Corp. In the year ended June 30, Illinois deposits grew at a higher rate relative to the entire US banking industry.

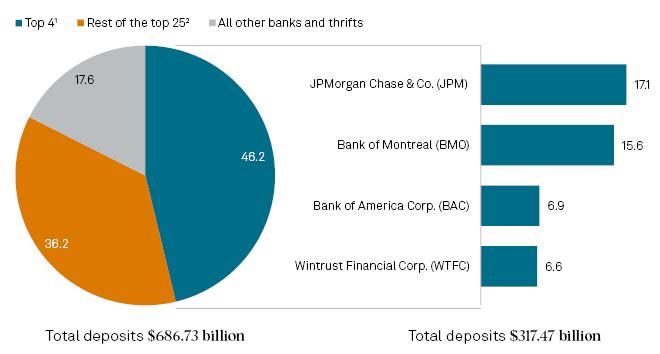

As of June 30, deposits in Illinois totaled $686.73 billion, up 2.95% year over year even as the number of bank branches in the state fell by 63 to 3,680. The US banking industry's deposits increased 0.8% to $17.406 trillion after dropping for the first time on record a year earlier, when three large banks collapsed.

US deposits returned to growth despite an elevated competition for deposits in a high-interest-rate environment. The first Federal Reserve rate cut in years is already in the rearview mirror, with more rate cuts potentially ahead.

"Lower rates could be a catalyst to drive loan and deposit levels higher," Wedbush Securities analyst David Chiaverini wrote in a Sept. 25 note.

The top four banks by deposits in Illinois were unchanged from a year earlier. JPMorgan Chase & Co. and Bank of America Corp. — two of the Big Four US banks — continued to rank first and third, respectively, even though their Illinois deposits dropped 7.5% to $117.56 billion and 7.0% to $47.24 billion, respectively, on a year-over-year basis.

JPMorgan booked a 193-basis-point decline in its market share to 17.12% and shed 12 of its Illinois branches, putting the total number of its branches in the state to 269. BofA logged a 73-basis-point decline in its market share to 6.88%.

At No. 2, Bank of Montreal, the parent company of Chicago-based BMO Bank NA, recorded a 145-basispoint jump in its Illinois market share as its deposits in the state climbed 13.5% to $107.35 billion.

Rosemont, Ill.-based Wintrust Financial Corp. nabbed the fourth spot with $45.32 billion in Illinois deposits,

up 8.9%. The competition for deposits in Chicago is "more or less stable," Wintrust President and CEO Timothy Crane said.

"We've been seeing six months to 13-, 14-month type rates at around 5%. The only surprise that I would have personally is that some people have longer terms out there than others," Crane said during a July 18 earnings call. "We're thinking that those rates should be 5% and down here going forward.

Among the top 25 banks by deposits in Illinois, Chicagobased Northern Trust Corp. logged the largest year-overyear increase in state deposits at 27.7% to $34.19 billion, followed by Chicago-based Byline Bancorp Inc. with a 24.2% jump to $7.26 billion. Citigroup Inc. booked the biggest decline at 21.1% to $14.72 billion.

Effingham, Ill.-based Midland States Bancorp Inc. was one of the banks that posted a year-over-year decrease in Illinois deposits. Its deposits were $4.75 billion, down 3.7%.

In a July 25 news release, Midland States Bancorp President and CEO Jeffrey Ludwig said the company hired a market president for Northern Illinois and a chief deposit officer who will "positively impact our treasury management services and our ability to add new commercial deposit relationships."

Aurora, Ill.-based Old Second Bancorp Inc. reported $4.55 billion in Illinois deposits, down 3.8% year over year, and Bloomington, Ill.-based HBT Financial Inc.'s Illinois deposits amounted to $4.22 billion, up 4.1%.

D.A. Davidson analyst Jeff Rulis downgraded his call on the stocks of Old Second and HBT to "neutral" from "buy," respectively, on Sept. 25. Among other things, the analyst believes the companies' credit and deposit strengths could "be overlooked or minimized should the market's attention turn to 'risk-on' credit names and/or banks with a greater ability to lower deposit costs" given the Fed's rate cut path.

All Covered, IT Services from Konica Minolta

100 Williams Dr Ramsey, NJ 07446-2907

Website: allcovered.com/

Primary Contact: Michael Postorino, mpostorino@allcovered.com

Facebook: facebook.com/ AllCoveredIT

Twitter: x.com/allcovered

LinkedIn: linkedin.com/company/ all-covered

All Covered is a trusted IT services provider for financial institutions, offering advanced solutions to enhance customer relationships from acquisition through retention and growth. Their certified security and compliance experts leverage extensive experience in banking and IT security to ensure regulatory compliance and implement robust protections against cyber threats. They partner with financial institutions of all sizes, blending global digital transformation expertise with local market knowledge. By addressing the unique needs of each organization, they help fortify defenses, safeguard data, and drive digital maturity, ensuring your business stays secure and competitive.

Bosch Security Systems LLC

4954 Bay Cir

Orange Beach, AL 36561-3913

Website: boschsecurity.com

Primary Contact: Tracie Bales tracie.bales@us.bosch.com

Facebook: facebook.com/ BoschSecurity

Twitter: x.com/BoschSecurityUS

LinkedIn: linkedin.com/company/ bosch-security-systems

Bosch Security Solutions is a leading global supplier of security, safety and communications products and systems. Their product portfolio includes intrusion detection, access control, video, fire detection and public address systems. Bosch provides specific solutions for the financial industry to protect lives, buildings and assets. In addition, they have solutions to your common security challenges such as vagrancy, ATM vandalism (hook and chain, skimming, etc.), night-drop fishing, access control, and so much more.

CHAMP Titles

2019 Center St Ste 202 Cleveland, OH 44113-2358

Website: champtitles.com

Primary Contact: Chris Keller chris.keller@champtitles.com Facebook: facebook.com/champtitles Twitter: x.com/champtitles LinkedIn: linkedin.com/company/ champtitles

CHAMP Titles is a leading provider of digital vehicle title, registration, and lien systems of record in the United States. In 2024, the company launched its Electronic Lien and Title Service (ELT) in Illinois. ELT is a software solution for the electronic submission of liens that is set to transform the vehicle titling process, reducing costs, improving efficiency, reducing fraud risk, and decreasing environmental impact. Illinois is the fourth state to adopt CHAMP’s solution.

Country Banker Systems, LLC

PO Box 99

Clyde, KS 66938-0099

Website: countrybanker.com

Primary Contact: William Ohlde will@countrybanker.com

LinkedIn: linkedin.com/company/ countrybanker

Country Banker is a financial analysis software system emphasizing a doublecolumn balance sheet and offers accrual adjusted or cash basis options. Customizable cash flow templates and loan presentations pair with balance sheet spreads; sensitivity testing; ratio and trend analysis; credit quality risk rating; and income statement analysis.

Darling Consulting Group 260 Merrimac St

Newburyport, MA 01950-2192

Website: darlingconsulting.com

Primary Contact: Kelly Coletti kcoletti@darlingconsulting.com

LinkedIn: linkedin.com/company/ darling-consulting-group

For over 40 years, DCG’s only business has been to help banks manage balance sheets effectively. DCG provides independent risk management consulting and strategic advisory services including asset/ liability management, model risk management/validation, capital planning, and data-driven solutions.

Duane Morris, LLP

190 S La Salle St Ste 3700 Chicago, IL 60603-3433

Website: duanemorris.com

Primary Contact: Joseph Silvia JSilvia@duanemorris.com

Facebook: facebook.com/ DuaneMorrisLLP

Twitter: x.com/DuaneMorrisLLP

LinkedIn: linkedin.com/company/ duane-morris-llp

With continued competition for deposits and market volatility, banks are looking for ways to better analyze branch footprints and untapped markets. In addition to the most recent release of Summary of Deposit data by the FDIC, our tools allow for a quick, yet comprehensive analysis of vital competitor data. Our data can help you with M&A, networking planning, regulations, competitive analysis and more.

– Analyze deposit market share on a national and regional level

– Visualize footprints with powerful mapping tools

Leverage Pre-built Excel Templates for streamlined market assessment

Elevate your intelligence with U.S. Bank Branch data feeds

Duane Morris LLP, a law firm with more than 900 attorneys in offices across the United States and internationally, is asked by a broad array of clients to provide innovative solutions to today's legal and business challenges.

The NBS Group, LLC

1331 Silas Deane Hwy Ste 205 Wethersfield, CT 06109-4300

Website: thenbsgroup.com

Primary Contact: Thomas Grottke tgrottke@thenbsgroup.com

Facebook: facebook.com/people/TheNBS-Group/61559096219194

LinkedIn: linkedin.com/company/ the-nbs-group

At The NBS Group, they specialize in navigating the intersection of the business of banking and technology, providing tailored consulting services to propel banks efficiently into the future. With a deep understanding of the challenges and opportunities throughout all aspects of the financial sector (commercial, retail, mortgage, and wealth), they empower community and small regional banks to remain competitive, relevant, and stay ahead in an ever-evolving industry and technological landscape.

As seasoned consultants in the banking and technology space, they bring a wealth of experience to guide institutions through the intricacies of digital transformation and technology modernization. Their expertise spans a range of critical areas:

Strategic and Technology Planning: They craft customized strategies and technology operations roadmaps that align business objectives with innovative technology solutions. They work closely with leadership to design comprehensive strategies that ensure long-term success.

Core Banking System Modernization: They are familiar with both new and legacy core solutions, digital and LOS platforms, and efficiently guide management teams through vendor and solution evaluations, contracting, and deploying new platforms or selected applications. By modernizing technology environments, they position organizations for enhanced agility, scalability, and performance.

We congratulate you on completing the rigorous 25-month program and joining the more than 23,000 alumni who have gone on to leadership positions in their organizations, associations and the financial services industry. Best wishes for continued success!

Luke Alberson

The Iuka State Bank Salem

John Avendt Old Second National Bank Chicago

Susan Baldwin MidAmerica National Bank Canton

Chelsea Ballou The First National Bank and Trust Company Roscoe

Robert Chadwick Holcomb Bank Rochelle

Trent Cox CBI Bank & Trust Galesburg

Michelle Dawson Blackhawk Bank & Trust Milan

Kristin Dinderman Exchange State Bank Lanark

JoAnna Engels State Bank of Cherry Cherry

Maria Godina Security Savings Bank Monmouth

James Hinks

First Mid Bank & Trust, National Association Mattoon

Aaron Holt First Mid Bank & Trust, National Association Mattoon

Marcie Hoskins

The First National Bank of Carmi Carmi

Benjamin Johnson Alliance Community Bank Mason City

Andrew LaPour Foresight Financial Group, Inc. Rockford

Theodore Macon Farmers State Bank of Hoffman Hoffman

Michelle Matthys CBI Bank & Trust Roscoe

Bo Mays

Sterling Federal Bank, F.S.B. Sterling

Reid Oberle Central Bank Illinois Geneseo

Kacie Rankin

Peoples Bank & Trust Charleston

Meredith Robb The Iuka State Bank Salem

Corey Tedford OSB Community Bank Ottawa

Brent Winch

Sunrise Banks, National Association Chicago

Sponsored by:

Merchants Bank recently announced the hiring of Marc Kramer as a Senior Mortgage Loan Originator for Merchants Mortgage, a division of Merchants Bank. Kramer, who is based in northeastern Illinois, will operate out of the company’s Chicago offices.

With an insightful background in the real estate and lending markets within the greater Chicago area, Kramer brings a wealth of experience to the team. In this new role, he will support current and prospective clients through the entirety of the borrowing process, providing a variety of mortgage loan products to meet their specific home buying needs.

Prior to joining Merchants Bank, Kramer most recently served as a loan officer at PrimeLending and operated as a private mortgage banker at Wells Fargo Home Mortgage. In these capacities, he held multiple responsibilities in the fulfillment of complex loan needs for high-net-worth borrowers and supporting self-employed individuals and first-time home buyers

Blackhawk Bank & Trust announced the appointment of Christopher J. Lemon as the new President of the bank, effective October 11, 2024. Lemon succeeds Jim Huiskamp, who is pursuing new endeavors after a successful tenure and 20 years of dedicated service. Huiskamp’s leadership has been instrumental in solidifying the bank’s reputation for excellence and community commitment.

Lemon transitions into the role from his position as Senior Vice President and Loan Officer, bringing over 44 years of experience with Blackhawk Bank & Trust. Throughout his tenure, he has demonstrated a proven ability to drive innovation, foster strong customer relationships, and support the bank’s growth and development.

His extensive understanding of bank operations began in 1981 when he joined the bank’s management program, first starting in the Bookkeeping Department. By 1982, Lemon had gained experience as a teller, Assistant Branch Manager, and Loan Officer.

“Chris Lemon is equipped to help lead Blackhawk Bank & Trust into its next chapter,” said Chairman of the Board Gerry Huiskamp. “We are confident in his vision and commitment to our customers and our community. And we are confident in this new era that this institution will remain Not for Sale.”

on their home ownership journey.

“Marc Kramer is an outstanding addition to the Merchants Mortgage team with an extensive understanding of Chicagoans’ lending interests and needs,” said Mike Axelrood, Regional Manager of Mortgage Sales. “He exemplifies the commitment and enthusiasm that our team is constructing as we continue to navigate further into this market.”

Kramer is a graduate of the University of Illinois Urbana-Champaign, where he earned a bachelor’s degree in economics. He later attended law school at the University of Illinois, receiving a juris doctor degree.

As President, Lemon will prioritize maintaining Blackhawk Bank & Trust’s commitment to delivering personalized, community-centered financial solutions while ensuring that customers continue to receive the exceptional service they expect and deserve.

Lemon expressed his enthusiasm for the new role, saying, “I am honored to serve Blackhawk Bank & Trust in this capacity. I look forward to driving meaningful growth and continuing to build on the strong foundation set by Jim’s many years of leadership. I’m confident with this dedicated team, our customers will continue to experience trusted and personal service they’ve come to know.”

In addition to his distinguished career at Blackhawk Bank & Trust, Lemon has been actively involved in many civic organizations as well as a long-standing coaching career with the Alleman High School baseball program. He resides in Coal Valley, IL with wife, Theresa.

The Illinois Bankers Association recognized John W. Conrad, of The Frederick Community Bank, as an inductee into the IBA’s 50-Year Club. The 50-Year Club recognizes and celebrates bankers who have achieved 50-plus years in the industry!

A 50-Year Club nomination is a capstone event for a banker filled with rewarding experiences and achievements. Conrad started his career with The Cissna Park State Bank on October 1, 1974. His first position was filing checks and progressed to teller and then bookkeeping. Early in his career, the Illinois Bankers Association offered a banking school at Southern Illinois University. It was a two-year program

Randy Hultgren, President and CEO of the Illinois Bankers Association, made the trip to Madison, Wisconsin to attend the graduation of the recent class of the Graduate School of Banking. Randy is pictured with a recent graduate, JoAnna Engels, Vice President, State Bank of Cherry.

Ms. Engels was a recipient of the IBA Scholarship to the Graduate School of Banking. She noted, “Thank you IBA for the scholarship and being a part of my education to

with a two-week intensive classroom experience each of the two years. During that time, John became an Assistant Cashier. He was gradually introduced to the lending side, became Vice President and eventually President. John served the Board of Directors as Secretary for many years. In January 2014, John retired from his position as President of The Cissna Park State Bank but continued as a Director. In 2018, The Cissna Park State Bank and The First National Bank of Paxton merged to form The Frederick Community Bank and John still serves as a Director. Congratulations John on your career milestone!

expand my knowledge in banking. I would encourage anyone thinking about it to take the plunge! It's takes hard work, many hours and dedication but it is so worth it.”

Congratulations JoAnna!

After a 50-year career in banking, Rick Catt, President and Chief Executive Officer of First Robinson Savings Bank, N.A. and First Robinson Financial Corporation has announced his retirement.

Mr. Catt began his career at the First National Bank of Oblong in Oblong, Illinois in 1974. In 1977, he was promoted to Assistant Cashier. Continuing his upward path in banking, he was named Assistant Vice President & Auditor in 1979 and promoted to Vice President

in January 1981. In 1984, he was appointed to Assistant Secretary to the Board of Directors of the First National Bank of Oblong.

On August 1, 1989, he was named President and Chief Executive Officer of First Robinson Savings Bank, National Association in Robinson, Illinois. In addition to those responsibilities, he was named President and Chief Executive Officer of First Robinson Financial Corporation in March 1997.

A graduate of Oblong High School in 1970, Mr. Catt graduated with honors from Eastern Illinois University with a Bachelor of Science Degree in Education, majoring in Mathematics with minors in Physical Education, Health, and Drivers Education.

In 1980, he graduated with honors from the Illinois Bankers Association Banking School at Southern Illinois University and the Illinois Bankers Graduate School of Banking in 1985 at the University of Illinois.

Congratulations Rick on a great banking career and well-deserved retirement!

Peoples Bank & Trust proudly recognized Terry Schafer for an extraordinary milestone—

45 years of dedicated service. This anniversary not only marks Terry’s remarkable tenure with the bank but also highlights her unwavering commitment, exceptional work ethic, and invaluable contributions to customers and our wonderful communities.

Terry joined Peoples Bank & Trust in 1979, starting as teller and gradually rising through the ranks to her current position as Assistant Vice President of Human Resources. Over the years, Terry has been a pillar of reliability and a source of inspiration for colleagues and clients alike. Her in-depth knowledge of the banking industry, combined with genuine care for customers, has set a standard of excellence that embodies the core values of Peoples Bank & Trust.

Throughout her 45-year journey, Terry has witnessed and adapted to significant changes in the banking sector. From the introduction of digital banking to evolving regulatory environments, Terry’s ability to navigate and embrace these changes has been instrumental in maintaining the bank’s reputation for innovation and customer-centric service. She exemplifies the “We Put People First” tagline of the bank.

“Terry’s dedication and loyalty are truly commendable,” said John Gardner, President and CEO of Peoples Bank & Trust. “Her contributions over the past four and a half decades have been invaluable. We are fortunate to have someone of her caliber on our team, and we look forward to many more years of her expertise and leadership.”

Terry’s 45 years with Peoples Bank & Trust is a testament to her dedication and passion for her work, customers, co-workers, board of directors, local organizations and the communities she has engaged with during her career.

Gardner concluded, “As we celebrate this significant milestone, we extend our heartfelt gratitude to Terry for her many years of service and look forward to her continued contributions.”

The Petersburg Chamber of Commerce announced that Neil Gurnsey was selected to receive the 2024 Petersburg First Citizen Award, which was presented on Saturday, September 21 during the Petersburg Harvest Fest celebration.

Neil lives at Lake Petersburg with his wife, Janelle, and their three children, Willa, Gwyn, and Haze. He is vice president and loan officer at Petefish Skiles and Company Bank in Petersburg. He is a graduate of PORTA High School and received his bachelor’s degree in communications from Bradley University in Peoria and is currently in the Graduate School of Banking through the University of Colorado.

Neil has served as president of the PORTA Foundation for more than a decade and plans an annual fundraiser to generate funds to buy specific items for PORTA classrooms that they could not otherwise receive. He announces multiple sports at PORTA High School, including football with his eldest daughter, and boys and girls basketball and was instrumental in establishing online streaming of boys basketball games. He coaches both the high school and junior high boys golf teams, and he established fundraising that helped purchase a

new sign at Shambolee Golf Course. He also worked tirelessly to get new equipment for the players.

He is a long-time coach of girls soccer, often two teams at a time, he established basketball skills camps for local youth and continues to do so, and he re-established and runs a youth golf camp at Shambolee. He is also a member of the PORTA Hall of Fame selection committee.

He is a founding member of the Menard County Men’s Club, a former member of the Lincoln League, and served as both President and Vice President of the Chamber of Commerce for several years. He was instrumental in establishing popular events like Drinkin’ with Lincoln and to ensure that Harvest Fest continues. He served as the leader of the Lake Petersburg Fireworks.

Neil is a local banker, but he also provides community service in this role. He makes home visits in the evenings and on weekends to help customers with their banking needs. He does this especially for the elderly who have a difficult time leaving their homes.

“Neil Gurnsey is very deserving of being the 2024 Petersburg First Citizen,” said a nominator. “He has been serving our community in a variety of ways since he was in his late 20s. He does so with energy, a smile, and a love of service. We all need to be as community and service driven as he is. He has done the majority of his community and public service while being a husband and father of three young children. His willingness to continually put others first is very admirable. However, his humbleness is even more inspiring.” Congratulations Neil!

By Nicholas McFadden, President & CEO