THE MAGAZINE OF THE harassment | cryptocurrencies | tax reform | blockchain | work-life balance

EXPLORING THE ISSUES THAT SHAPE TODAY’S BUSINESS WORLD SPRING 2018

F O R M E R LY T H E M I DW E S T AC C O U N T I N G & F I N A N C E S H OWCA S E THE SHOW is changing. New name. New experience. Newlevel of awesome! Tu e s d a y-We d n e s d a y Augus t 28-29, 20 18 D o n a l d E . S t e p h e n s C o n v e n t i o n C e n t e r R o s e m o n t , I l l i n o i s Preparing you for the future! Tax Reform l Artificial Intelligence Cybersecurity l Blockchain Healthcare l A&A l Data Analytics

Developed for CPA firms

CPACharge is a professional, affordable online payment solution that lets you give clients the options they want Unlike other payment solutions, CPACharge deposits 100 percent of payments, with fees debited the following month, for easy, accurate reconciliation We provide PCI Level 1 compliance and security, and expert in-house support Get the solution that’s trusted by more than 50,000 professionals as the best way to get paid CPACharge

MEMBER DISCOUNT PROGRAM CPACharge is a registered ISO of C tizens Bank N A MORE

$1,000 Pay CPA Card Number CVV Exp. **** **** **** 9998 001 NOV 2021 Payment Detail Submit to Smith Johnson, CPA cpacharge.com/icpas 855-612-1016

OPTIONS, FASTER PAYMENTS

2 INSIGHT | www icpas org/insight SPRING 2018 www icpas org/insight IGNITING YOUR INFLUENCE 2 42 7 2 83 1 3 23 5 THE RISKS AND REWARDS OF CRYPTOCURRENCIES HOPPING ON THE TAX REFORM TRAIN spotlights 8 Seen & Heard How Winning Companies Keep Winning 10 Tech Pulse Business Interest in Blockchain Booms 50 Gen Next Brewing Your Own Business By Joshua Lance, CPA , CGMA 52 IN Play Q&A with Kim Szalkus, CPA By Sarah Herrmann trends 12 Professional Issues Hurt of Harassment By Clare Fitzgerald 14 Employee Benefits Remote Possibilities By Kristine Blenkhorn Rodriguez 16 Personal Finance Cashing in With Tax Reform By Mark Gilbert, CPA , PFS 18 Practice Management Turning Tax-Time Clients Into All-Time Clients By Jeff Stimpson insights 4 Today ’s CPA Is Anyone Listening? By Todd Shapiro 6 Leader ’s Letter Committed to Success By Rosaria Cammarata, CPA , CGMA 40 Capitol Report High Times Ahead in Illinois? By Marty Green, Esq 42 Corporate Minded A Growing Career, A Growing Family By Amanda L Gavin, CPA , MBA 44 Partner Perspectives Lessons to Learn From Today ’ s Young CPAs By Marc Rosenberg, CPA 46 Ethics Engaged The Golden Rules of Ethics By Elizabeth Pittelkow Kittner CPA, CGMA, CITP , DTM 48 Tax Decoded Federal Tax Reform’s Implications on Illinois By Keith Staats, JD

ILLINOIS CPA SOCIET Y

550 W Jackson Boulevard, Suite 900, Chicago, IL 60661 www.icpas.org

Publisher/President & CEO

Todd Shapiro Editor Derrick Lilly

Creative Director

Gene Levitan

Women’s Committee

Women to Watch Awards

We are looking for outstanding women who have made significant contributions to the accounting profession, their organizations, and to the development of women as leaders. Awards will be given in two categories and will consider the following:

experienced leaders

• Mentoring other professionals

• Major or unique contributions to the profession

• Leadership in workplace improvements

• Authorship of professional articles/ speaking engagements

• Involvement in community service and/or professional organizations

emerging leaders

• Demonstration of leadership

• Contributions to the profession

• Creation and implementation of unique workplace initiatives

• Involvement in community service and/or professional organizations

• Involvement with her alma mater

To nominate a candiate today, visit www.icpas.org/womentowatch

Deadline for nominations is 6.1.18

Deadline for application materials is 6.15.18

Candidates must be members of the Illinois CPA Society (ICPAS) and the American Institute of Certified Public Accountants (AICPA).

NOT A MEMBER?

Visit www.icpas.org and/or www.aicpa.org.

Photography Jay Rubinic + Derrick Lilly

Circulation

John McQuillan

ICPAS OFFICERS

Chairperson

Rosaria Cammarata, CPA, CGMA | Mattersight Corporation

Vice Chairperson

Geoffrey J Harlow, CPA | Wipfli LLP

Secretar y

Dorri C McWhorter, CPA, CGMA, CITP | YWCA Metropolitan Chicago

Treasurer

Kevin V Wydra, CPA | Crowe Horwath LLP

Immediate Past Chairperson

Lisa Hartkopf, CPA | Ernst & Young LLP

ICPAS BOARD OF DIRECTORS

Christopher F Beaulieu, CPA, MST | FSB&W LLC

John C Bird, CPA | RSM US LLP

Brian J Blaha, CPA | Wipfli LLP

Jon S Davis, CPA | University of Illinois

Stephen R Ferrara, CPA | BDO USA LLP

Jonathan W Hauser, CPA | KPMG LLP

Scott E Hurwitz, CPA | Deloitte & Touche LLP

Anne M Kohler, CPA, CGMA | The Mpower Group

Thomas B Murtagh, CPA, JD | BKD LLP

Elizabeth S Pittelkow Kittner, CPA, CGMA, CITP | Litera Microsystems

Maria de J Prado, CPA | Prado & Renteria CPAs

Seun Salami, CPA | Jones Lang LaSalle Inc

Stella Marie Santos, CPA | Adelfia LLC

Andrea K Urban, CPA | ThoughtWorks Inc

BACK ISSUES + REPRINTS

Back issues may be available Articles may be reproduced with permission

Please send requests to lillyd@icpas org

ADVERTISING

Want to reach 25,000 accounting and finance professionals? Advertising in INSIGHT and with the Illinois CPA Society gives you access to Illinois’ largest financial community Contact Mike Walker at mike@rwwcompany com

INSIGHT is the magazine of the Illinois CPA Society Statements or articles of opinion appearing in INSIGHT are not necessarily the views of the Illinois CPA Society The materials and information contained within INSIGHT are offered as information only and not as practice, financial, accounting, legal or other professional advice Readers are strongly encouraged to consult with an appropriate professional advisor before acting on the information contained in this publication It is INSIGHT’s policy not to knowingly accept advertising that discriminates on the basis of race, religion, sex, age or origin The Illinois CPA Society reserves the right to reject paid advertising that does not meet INSIGHT’s qualifications or that may detract from its professional and ethical standards The Illinois CPA Society does not necessarily endorse the non-Society resources, services or products that may appear or be referenced within INSIGHT, and makes no representation or warranties about the products or services they may provide or their accuracy or claims The Illinois CPA Society does not guarantee delivery dates for INSIGHT The Society disclaims all warranties, express or implied, and assumes no responsibility whatsoever for damages incurred as a result of delays in delivering INSIGHT INSIGHT (ISSN-1053-8542) is published four times a year, in Spring, Summer, Fall, and Winter, by the Illinois CPA Society, 550 W Jackson, Suite 900, Chicago, IL 60661, USA, 312 993 0407 Copyright © 2017 No part of the contents may be reproduced by any means without the written consent of INSIGHT Send requests to the address above Periodicals postage paid at Chicago, IL and at additional mailing offices POSTMASTER: Send address changes to: INSIGHT, Illinois CPA Society, 550 W Jackson, Suite 900, Chicago, IL 60661, USA

2018

Call for Nominations 2

today’sCPA

INSIGHTS FROM TODD SHAPIRO, ICPAS PRESIDENT & CEO

{Follow Todd on Twitter @Todd ICPAS}

{Watch Todd’s CEO Video Series on YouTube}

Is Anyone Listening?

If you think gaining influence and making decisions in your organization is hard, you ’ re not alone.

Ilearned early on in my career just how challenging, and sometimes frustrating, the decision-making process can be. Seemingly ages ago, as a manager at Quaker Oats, I attended an influence m a n a g e m e n t s e m i n a r p u t o n b y m y e m p l o y e r a t t h e t i m e . T h r o u g h o u t t h e s e m i n a r t h e i n s t r u c t o r s c o a c h e d u s o n v a r i o u s ways to influence others. Shortly after, I was in a meeting with my division president discussing which way to go on a business issue, which seemed like a good time to test my new influencing skills. I was utilizing all the methods taught to me during the seminar w h e n m y b o s s s t o p p e d m e a n d s a i d , “ We ’ r e d o i n g i t m y w a y, because I’m on this side of the desk, and you’re on that side of the desk ” That experience has stayed with me to this day

Making decisions “because I said so” or “because I’m the boss” not only risks making poor choices, it risks losing the support of t h o s e i m p l e m e n t i n g o r i m p a c t i n g t h e o u t c o m e F r o m f i r s t h a n d experience, I can tell you nothing breaks the spirit of staff more than being faced with those words Likewise, nothing encourages and empowers staff more than feeling like an influential part of the decision-making process

Every day, in every organization, countless decisions are made S o m e a r e s m a l l , a n d s o m e a r e c r i t i c a l t o t h e l i f e b l o o d o f t h e organization, literally setting the direction of the culture and future of the business I often tell my staff that it’s not necessarily most important who makes the final decisions but whether you had a seat at the table to influence the outcomes

So, how does one become an influencer? Just as I stress that in most situations there’s no single “right” answer, there’s no single m e t h o d t o g a i n i n g i n f l u e n c e R a t h e r, i n f l u e n c e g r o w s a n d becomes most powerful when backed by knowledge, experience, and command of compelling data and information (I’m a strong believer in data-based decision-making).

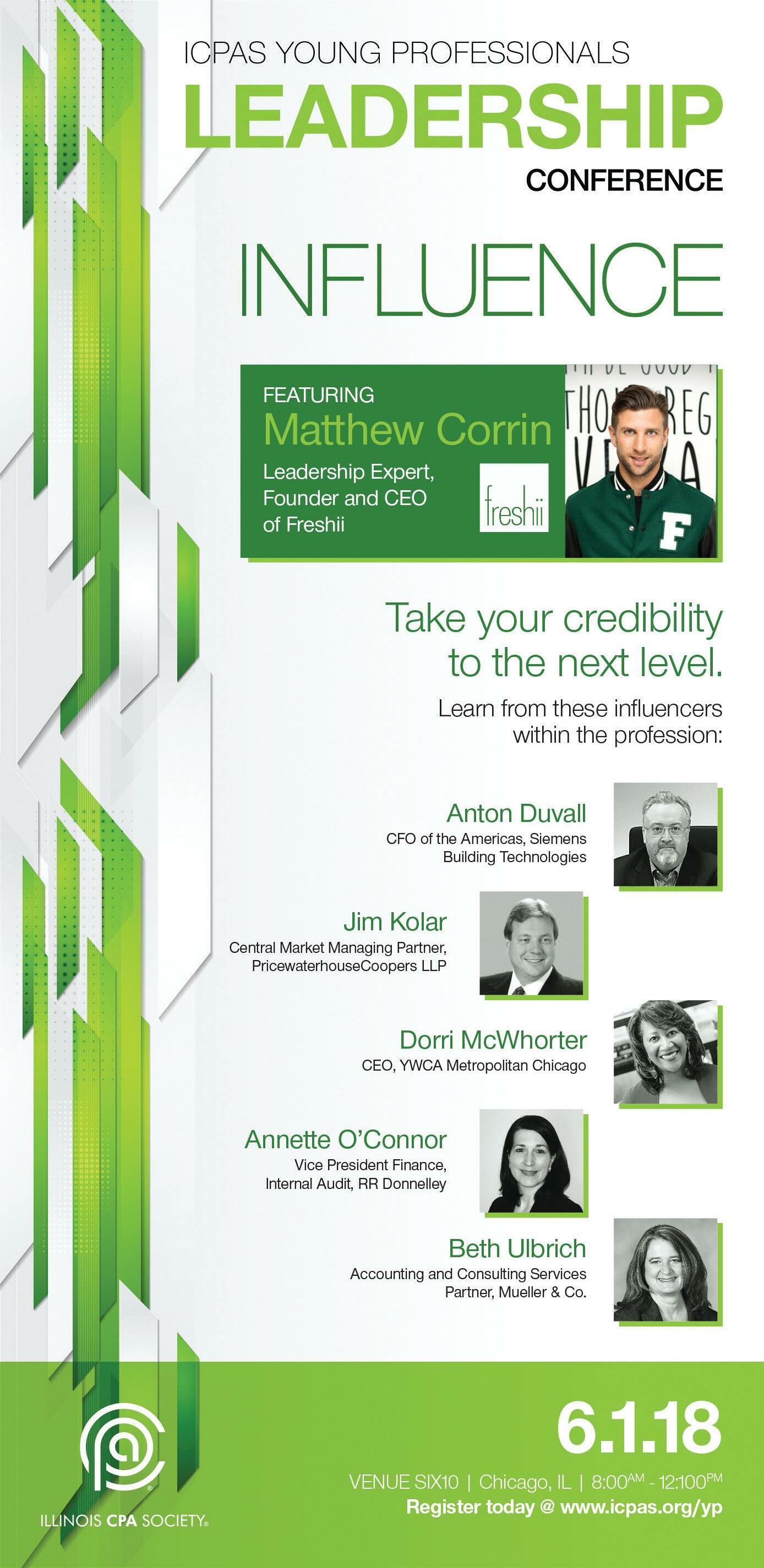

We must stop mistakenly thinking of influencers only as the people already “in charge ” Being influential and influencing decisions is not just the purview of experienced, long-term staff, or the partners, CEOs, CFOs, and other executives; the reality is, we all have a responsibility and desire to be influencers Young professionals, especially, need to embrace the mindset of becoming influential and decision-makers in organizations (this will be the theme of this year ’s Young Professional Leadership Conference)

Stop and look at the world around us At the end of the day, I want you to ask yourself if you’re going to be an influencer or stay on t h e s i d e l i n e s B e i n g a n i n f l u e n c e r a n d , u l t i m a t e l y, a d e c i s i o nmaker, comes with great responsibility I encourage you to step up and take it We need more positive and innovative influencers and decision-makers in our profession

4 INSIGHT | www icpas org/insight

You probably already have life insurance. But do you have enough?

Over the years, your living expenses may have increased. Could your current life insurance benefits:

• Help your family maintain their lifestyle?

• Pay for your kids’ college education?

• Allow your spouse to retire comfortably?

It ’s always a struggle to lose someone you love But your family’s emotional struggles don’t need to be compounded by financial problems

That’s why the Group 10-Year Level Term Life Insurance Plan is made available to ICPAS members * This valuable insurance program offers:

• Your choice of benefit amounts up to $250,000.

• Rates that are locked in for 10 full years.

Four Learn more today! Visit www.plansforICPASmembers.com or call 1-800-842-4272 for more information

households without any life insurance would have immediate trouble paying living expenses

loss

*Underwritten by Hartford Life and Accident Insurance Company, Hartford, CT 06155 Life Form Series includes GBD-1000, GBD-1100, or state equivalent All benefits are subject to the terms and conditions of the policy Policies underwritten by Hartford Life and Accident Insurance Company detail exclusions, limitations, and terms under which the policies may be continued in force or discontinued Program Administered by Mercer Health & Benefits Administration LLC AR Insurance License #100102691 CA Insurance License #0G39709 In CA d/b/a Mercer Health & Benefits Insurance Services LLC 82328 (3/18) Copyright 2018 Mercer LLC All rights reserved

Help protect your loved ones when they may need it the most with economical life insurance

PEAC E O F M I N D

in 10 U.S.

from the

of the

• Benefit amounts remain steady for the 10-year coverage period. There are no age reductions. 1 Insurance Barometer Study, LIMRA, 2017 See how affordable additional peace of mind can be for you and your family (including eligibility, benefits, premium rates, exclusions, limitations and termination provisions) *

primary wage earner.1

’sletter

Committed to Success

It’s an honor to be able to write this letter. It’s tradition for the new Illinois CPA Society Board Chair to share their story of how they got here, but I can’t share mine without sharing my parents’ story I’m a born and bred Chicagoan, and like many, I’m the child of immigrants My parents each traveled their own journey to the U . S . a s y o u n g a d u l t s b e f o r e m e e t i n g , m a r r y i n g , a n d w o r k i n g together to support a growing family My mom worked six days a week as a seamstress for decades until the day she finally owned that business My dad worked factory and other labor jobs while taking computer and engineering classes at night, graduating with his bachelor ’s degree several years after I did. We sometimes struggled financially, but because of their determination and ingenuity, we never wanted for anything important

My dad instilled in me a love of numbers, process, and technology My mom taught me to be resourceful in solving problems, and to consider the details and the bigger picture in any situation They both taught me the importance of planning and commitment, while our circumstances gave me an early appreciation for the importance of financial literacy and stability. Given that, it’s not a surprise that I declared my major as accounting in a fifth-grade essay about what I wanted to be when I grew up

Except for five years in public accounting, I’ve spent my entire career in corporate finance My CPA credential has served as an invaluable foundation for a broad range of responsibilities I’ve

experiences in financial reporting, operations, systems, and process engineering, eventually taking on a leadership role that let me do all those things at once. I never could turn down a challenge.

Challenge has always invigorated me, and I hope it invigorates you, because these are exciting times for our profession We’re in the midst of a technological revolution that is reinventing the way we work, the skills we need, and the risks we manage Working for a technology company, I see this transformation gaining speed and scope every day We’re also experiencing a rapidly changing workforce as a large generation of experienced professionals retires.

These disruptive forces are creating opportunities we couldn’t have imagined a decade ago To capitalize on these opportunities, our profession needs to continue to attract and retain new and diverse talent We need to encourage innovation and embrace new ideas about how we work and what we do We also need to continue to enhance the competencies that define us as CPAs and the CPA credential to include technology-based skills, like data analytics, so we can respond to new demands in our business world

As I learned early on, success requires commitment I believe in, and am committed to, the continued success of our profession As your chair, I’m committed to the continued success of you

6 INSIGHT | www icpas org/insight

b e e n a b l e t o l e v e r a g e m y C PA b a c k g r o u n d t o g a i n r o l e s a n d

Rosaria Cammarata, CPA , CGMA is Vice President & Controller for Mattersight Corporation

A MESSAGE FROM 2018 ICPAS CHAIR ROSARIA CAMMARATA, CPA, CGMA

leader

Study accounting

the language of business

Nor thwestern’s online post-baccalaureate cer tificates provide working professionals with the precise education they need for career advancement , CPA exam preparation or graduate school application. Three cer tificates — Fundamentals of Accounting, Advanced Accounting, and CPA Preparation are available online.

Apply today — applications are accepted every quarter. sps.nor thwestern.edu/accounting • 312-503-2579

P O S T-BA C C A L A U R E A T E P R O G R A M S

—

How Winning Companies Keep Winning

A long-term bull market has made it easy to enhance shareholder value, but The Boston Consulting Group (BCG) warns that real winning doesn’t always come so easy BCG’s recent repor t, “The Transformations That Work and Why,” reveals at any time, nearly one-third of large U S companies endure severe, two-year declines in their ability to create shareholder value and about a third fail to recover within the following five years

Citing flat R&D investments and capital expenditures as recent red flags, BCG fears many companies aren’t doing enough to keep up and could slip into decline So how do winners keep winning, and losers star t winning?

BCG says companies must “fundamentall y transform themselves in ways that dramatically and sustainably improve per formance ” The kicker? They must do this at least once ever y five years The payof f? A 14-percentage point increase in long-term shareholder returns

So, whether you’re leading a company or advising one, here’s what BCG’s evidence-based repor t says leads to winning transformations and increasing long-term company values:

Spending on Revenue Creators: “In the long term, revenue growth is the biggest factor in transformation success,” BCG says “A company can’t cut and trim its way to top-quar tile per formance ” Instead, it should aim to grow by spending on R&D and innovation with a clear link to sales growth

Taking a Formal Transformation Approach: “CEOs and leaders need to show compelling plans, take immediate

action, and lay the groundwork for leading with a clear vision and solid objectives,” BCG states Bold and clear communication establishes credibility with investors and other stakeholders

Appointing Action-Oriented, Disruptive Leader s: “To transform a company, the CEO and senior leaders must be willing to change the business dramatically,” BCG suggests And if they’re not? Well, they may have to go The disruption necessar y for real transformations cannot be underestimated

Taking R apid Action: “Instead of tr ying to reinvent the company all at once, leaders should work to immediately kick of f rapid moves that are easy to implement in the first 1 00 days and can generate results in 3-to-12 months,” BCG says, which can boost CEO credibility

Applying Directive & Inclusive Leadership: “Transformation takes more than traditional, directive leadership; it also calls for inclusive leadership, such as fostering collaboration, soliciting feedback, and empowering teams,” BCG explains, meaning CEOs and HR teams must be mindful of how transformations af fect people throughout the company

Building a Diver se Leader ship Team: Companies must also focus on acquiring talent and leadership that will sustain the changes into the future. As BCG notes: “It’s impor tant to strike the right balance between external hires, with new ideas and capabilities, and internal talent, with deep knowledge of the business and organization ”

8 INSIGHT | www icpas org/insight

To sp e a k w i t h one of our e xecut i ve recrui t ers , c all 312.582.180 0 t oday! w ww.brilliantfs .com Follow @ BrilliantFS. Our t e a m is compris e d o f f o rmer a ccounting a n d f inance p r o fessionals wh o k now t h e industry. We c a n h elp. Searc h i n g f or you r n ex t acc o u n t i n g o r nance role? Let B r illiant g uide you thr oug h t h e p rocess.

Business Interest in Blockchain Booms

Bitcoin may have brought blockchain into the limelight, but the technology behind cr yptocurrency record-keeping is increasingly spreading into the mainstream business world

“Companies that move products and people through complex supply chains see promise in the inherent security and ease of use of blockchain,” says David Schatsky, an emerging technologies anal yst and managing director at Deloitte LLP, in an inter view with Kim S Nash for the Wall Street Journal

A blockchain digital ledger allows users to add blocks of information to the chain af ter each par ty runs algorithms to mutually evaluate and validate a proposed transaction Once approved, the transaction or data is time-stamped and added to the chain, which is inherently encr ypted, unchangeable, and always up-to-date on all users’ systems

Nash repor ts British Air ways is testing blockchain for maintaining consistent real-time flight data across airpor t gates and monitors, airline websites, and in customer apps Walmar t is also betting big on the technology, developing blockchain solutions with IBM to manage its suppl y -chain data for dozens of products

As Nash learned, Walmar t’s blockchain allows the company to precisely track the produce and products it carries For instance, the retailer has been testing the technology for

several months in its mango supply chain between the U S , Mexico, and some South American countries

“Af ter a mango is picked from a tree, it makes many stops before getting to a store shelf. Farmers, packing-house workers, and others along the way use a mobile app from Walmar t to send details such as har vest dates, locations, and images of their fruit to the retailer’s blockchain,” Nash writes Walmar t’s head of food safety, Frank Yiannas, tells Nash that the process is simpler and more secure than the array of barcodes, scanners, paper forms, and individual databases typically used In fact, in a simulated recall, Yiannas says his team traced the origin of a bag of sliced mangoes in just 2.2 seconds in the blockchain versus the nearly seven days it took using Walmar t’s other systems

Y iannas explains that blockchain’s speed and accuracy allows the retailer to save sales, and prevent fur ther illness and possibl y death, as stores will know exactl y which mangoes to pull of f shelves in case of crisis

With corporate spending on blockchain sof tware expected to reach $2 1 billion in 20 1 8, up from $9 45 million in 20 1 7, according to researcher International Data Corp , blockchain is quickly becoming a technology accounting and finance professionals will need to know and embrace

10 INSIGHT | www icpas org/insight

Hurt of Harassment

When workplace harassment goes overlooked, victims and organizations suffer the consequences

BY CLARE FITZGERALD

Sexual harassment cases in the entertainment, media, and political spheres have dominated headlines recently, but workplace harassment has long been pervasive across industries, especially in traditionally male-dominated fields. And accounting and finance hasn’t been an exception

As the #MeToo and Time’s Up movements bring renewed attention to sexual harassment and gender inequality, organizations across America are working to root out the attitudes and mentalities that drive hostile and inappropriate behavior. But they’ll need to do more than update anti-harassment policies to do that Creating safe environments for employees also requires understanding the psychology of harassers, addressing power disparities that commonly drive workplace harassment, and fostering cultures of trust and respect

INTIMIDATION GAME

The U.S. Equal Employment Opportunity Commission defines sexual harassment as unwelcome sexual advances, requests for sexual favors, and other verbal or physical conduct of a sexual nature that explicitly or implicitly affects an individual's

employment, unreasonably interferes with an individual's work performance, or creates an intimidating, hostile or offensive work environment According to Eugene Hollander, a Chicagobased attorney with experience in sexual harassment cases, behavior that constitutes sexual harassment can range from seemingly harmless sexual jokes or comments to aggressive groping, touching, or displaying pornographic images in the workplace and everything in between

Harassment can occur anywhere, by anyone, in any organization. What many employers also mistakenly overlook is that they can be held liable for harassment experienced by employees from someone outside of their organization, such as vendors or clients

But in most workplaces, harassment is driven by and revolves around an imbalance of power, according to Dr Jessica Lippman, a Chicago-based clinical psychologist “The perpetrator holds the key to moving up, so the victim’s choices are either to submit and be exploited to advance, or resist and risk not advancing or facing retaliation,” she explains, noting that women are the victims in most harassment cases. “It’s a lose-lose situation.”

12 INSIGHT | www icpas org/insight

P R O F E S S I O N A L I S S U E S

Often, harassment starts in a non-threatening manner but escalates quickly into aggressive behavior “The perpetrator sees the victim as being vulnerable He might start by complimenting her work and offering to help with her career. Perpetrators make their victims feel special It’s all part of the seduction They often are very charming, and they use that charm to manipulate,” Lippman says

In addition to having manipulative personalities, Lippman says narcissism is a common trait among sexual harassers. “They have an inflated view of themselves and their talents, and they can’t understand why anyone wouldn’t welcome their advances,” she says. “They have an enormous sense of entitlement, but also a deep need for approval It’s the narcissist’s secret that they need to defend against not being special at all costs ”

Because they see themselves as special, sexual predators often have a Machiavellian attitude; the means justify the ends, which allows them to disengage morally and find ways to justify their behavior, Lippman explains Another common trait is a lack of empathy “They are dismissive of other people’s feelings and careless toward their victims,” she says

But power is their ultimate weapon, and they are driven by a desire to dominate and control Knowing that they hold power, Lippman says harassers won’t hesitate to disparage anyone who calls them out as inappropriate And in the past, perpetrators in positions of power knew that they wouldn’t get called out “People are obedient to authority,” Lippman stresses. “They may not like what’s going on, but in many cases, they won’t do anything to stop it ”

BAD BUSINESS

Harassment can be a festering problem, and the effects on employee morale and productivity can be devastating to business Toxic environments increase workplace stress, and often lead to increased absenteeism and turnover. Despite increasing pleas for action, many victims would still rather leave than report being harassed. “Victims don’t want to be labeled, ignored, or not believed So, they suck it up and it affects their performance, or they leave, because they know they can’t work in such a hostile environment,” Lippman explains.

In addition to the human costs, reputational and financial risks to organizations can be steep. According to Hollander, a variety of damage claims can be brought in a sexual harassment case against an employer, such as pain and suffering, mental anguish, and compensatory damages, which can quickly add up to costly payouts And although compensatory and punitive damage awards in federal sexual harassment claims are capped, state claims are not If a victim brings a negligent supervision claim, for example, and the facts suggest that an employer knew about the harassment and swept it under the rug or did nothing to stop it, a company could face a federal sexual harassment claim and a state claim “A jury could award hundreds of thousands of dollars in such cases, and that can be crippling for many businesses,” Hollander warns

ZERO TOLERANCE

Employers are responsible for maintaining a safe environment and protecting employees from any behavior that could cause physical or psychological harm Plante Moran, a Midwest-based accounting, tax, and consulting firm, refers to that responsibility as creating a “jerk-free culture,” according to Diana Verdun, director of human resources “We want to create an environment that shouldn’t and doesn’t have problems with workplace harassment,” she says,

noting for Plante Moran, achieving that goal starts with hiring people who fit in with the firm’s culture and values

Strong anti-harassment policies, clear reporting mechanisms, and comprehensive training also are key to ensuring that employees understand what constitutes harassment, how to report it, and the consequences of any inappropriate behavior. Plante Moran includes workplace harassment training as part of its onboarding process and incorporates more advanced training as people move into managerial and supervisory roles. “We educate our people on this topic throughout their careers, so they know how to manage through any issues and how to handle any concerns,” Verdun explains

Maintaining an atmosphere where people feel comfortable talking about sensitive topics also is important “We always try to acknowledge that the whole person comes to work, and that people have things on their minds that they should feel comfortable talking about We don’t want people to think they have to check their concerns at the door,” Verdun says. “Building an environment of trust gives people confidence that any concerns they have will be taken seriously and investigated ”

Although organizations need to have clear codes of conduct, rules will always be broken As Hollander notes, “The world is made up of all sorts of humans, and people are still going to do what they’re going to do.”

That’s why employers need to be prepared to take immediate action if an issue does arise “Anti-harassment policies are important, but they need to have teeth,” Lippman says “Companies can host town hall meetings and talk about values, but people have to see what they’re saying isn’t just rhetoric. Women have to feel that they will be heard, that their claims will be investigated, and that there will be consequences if someone crosses the line Companies need to show that harassment won’t be tolerated, and they need to be clear about what will happen if they find out that an employee is being harassed And it can’t just be a slap on the wrist ”

Plante Moran adds weight to its zero-tolerance policies with support from the top “If evidence shows that someone at our firm is doing something that falls into ‘jerk’ behavior, then that person simply will not be with the firm anymore, regardless of his or her position Public accounting firms have many owners, and it’s important that they all agree with that philosophy ”

Ultimately, though, policies and education can only go so far Eliminating hostile attitudes and power imbalances in corporate America will mean promoting more women into the executive ranks. The accounting and finance industry continues to struggle on that front, leaving it vulnerable to reputational harm if change isn’t made Plante Moran and many other notable firms have instituted women leadership programs and have increased their numbers of female partners Many are also working to highlight the benefits of a diverse workforce, but there’s still progress to be made in this profession

“We need to understand the value of the differences that people bring,” Verdun says. “While we work really hard at getting this right, we’re always learning from our staff and others in the marketplace to ensure we’re continuing to improve in these areas It all comes down to respecting each other as humans and creating environments in which everyone can excel.”

www icpas org/insight | SPRING 2018 13

Remote Possibilities

With more workers wanting to telecommute, it ’ s time to address the ins and outs of managing remote employees

BY KRISTINE BLENKHORN RODRIGUEZ

What does the typical telecommuter look like to you? You m o s t l i k e l y e n v i s i o n e d s o m e o n e q u i t e y o u n g , h e a d p h o n e s o n , Starbucks at hand, dressed for lounging instead of business, right?

While you might be right sometimes, you’re also oh-so-wrong The typical telecommuter is 50-plus years of age a salaried, college-educated, non-union employee, according to Global Workforce Analytics (GWA)

Surprised? Don’t be; already roughly one-in-four workers telecommute, and half of the U.S. workforce holds jobs that are at least partially compatible with remote work arrangements.

In 2016, 1 5 million Illinois residents worked at home at least half of the time, not including the self-employed And GWA says regular work-at-home arrangements among the non-self-employed p o p u l a t i o n h a v e g r o

nearly 10 times faster than the rest of the workforce

It’s not just worker preference or work-life balance trends fueling the rush towards remote work; business benefits include happier employees, employee savings of $2,000 to $7,000 annually, and

, according to GWA.

While remote work promises big benefits, it also brings new business challenges, changing the way teams interact and deliver results.

COMMON CHALLENGES

Moving from the traditional face-to-face work environment to a remote model has its nuances, but handled skillfully, the benefits far outweigh the challenges below

Management styles. Many seasoned leaders will have to rethink and change their management styles to be successful in remote working environments “They’re used to managing face time and now they must instead manage productivity without it,” says Janice Aull, owner of performance improvement facilitation firm Aull About U “In remote working environments, the emphasis is less on relationships and more on outcomes ”

Trust is a major predictor of managerial success in remote work environments “Some leaders are naturally trusting; others are distrusting. It’s a continuum. But we’ve found trust, more than anything else, predicts distributed leadership success,” says Dr Laura Hambley of Work EvOHlution, an industrial psychology firm that develops assessments and profiles for distributed work situations.

14 INSIGHT | www icpas org/insight E M P L O Y E E B E N E F I T S

w n n a t i o n a l l y b y 11 5 p e rc e n t s i n c e 2 0 0 5

,

a n n u a l s a v i n g s o f $ 11 , 0 0 0 p e r p e r s o n f o r a t y p i c a l b u s i n e s s

employees are slacking off, the opposite is often the problem Because home has become “the office,” many managers, and even their employees, take advantage of that fact

Sending weekend or late-night emails with expectations of immediate responses is inappropriate, Aull says, unless that has always been part of the job “Management needs to set expectations for hours of work availability Otherwise, it’s far too easy for work to bleed into personal time, which makes most employees less productive instead of more productive ”

Technology troubles. Even if a company provides each employee with a basic at-home technology package to ensure consistency, usability is not guaranteed “As an employee, you have to create self-directed learning for the technology that will make it easier for you to do your job from home or wherever you may be,” Aull says Continuous learning and a continuous growth mindset are key to success, and sometimes so is a contingency plan

“Having a Plan B is essential for day-to-day success,” Hambley adds “Technology can be iffy What if connectivity breaks at the start of a conference call? Where does everyone reconvene virtually? These are the kinds of issues many team leads still don’t plan for and they can reduce productivity ”

Communication conflicts. “In a remote environment, if you don’t have the right tools and policies, people can become really good at getting their stuff done but not very good at collaboration Team effort still matters,” says Kevin Eikenberry, owner of The Kevin Eikenberry Group, a leadership and learning consulting company that provides training, consulting and coaching services to organizations He emphasizes it’s not just a matter of choosing the right collaboration technology tools but also encouraging communication amongst team members.

The ability to choose the right communication medium at the right time is a skill worth teaching employees, according to Hambley “Remote working promotes an over-reliance on email But, there are times when picking up the phone is better. Or, when a video call to see body language and facial cues trumps just audio,” she explains. “The better teams get at discerning what works for different types of situations or personalities, the better the team dynamic.”

FRONTLINE FINDINGS

While expert observations are helpful, nothing beats hearing from those in the field trying to make remote work, well, work.

National Equity Fund. Gaylene Domer, VP of Facilities Management, notices less stress amongst employees during her company’s usually very hectic March through November deal-making timeframe. Employees say it’s because they can now work from home a couple of days per week: they save time commuting and are better able to keep work-life balance despite the frenzied pace of business.

“Turnover has gone from 8 percent to 4 3 percent in four years, a n d w e ’ r e a t t r a c t i n g n e w e m p l o y e e s a t a b e t t e r r a t e , ” D o m e r explains. “People admit that they’ve been offered more money e l s e w h e r e b u t t o o k t h i s j o b b e c a u s e o f t h e f l e x i b i l i t y r e m o t e work offers them.”

What’s more, with 93 of 176 employees now participating in the work-from-home program, Domer says National Equity Fund was able to save $2.5 million over the course of its office lease.

Domer admits that winning over senior managers was crucial to making the program successful. “I urged our senior managers to

take their work-from-home days because otherwise team members wouldn’t. It wasn’t so hard once our CEO started to do it. He has been a champion from day one.”

N o d e S o u rc e . J o e M c C a n n , f o u n d e r a n d C E O , s a y s h e h a d a n epiphany about remote working arrangements while sitting in an A m s t e r d a m c a f é “ I w a s w o r k i n g f o r a l a rg e s o f t w a r e f i r m a s a developer on a contract basis I was in a great café in Amsterdam, enjoying life and work, and I thought, ‘This is the way it should be.’ Something had to give. People are fed up with long commutes, lack of time with their kids, inflexible schedules. I went from Wall Street and corporate America to a life that included work but was not all work, all the time ”

M c C a n n t u r n e d h i s e p i p h a n y i n t o N o d e S o u rc e , a c o m p l e t e l y remote company from inception: “We are distributed by design I f y o u s t a r t d e c e n t r a l i z e d , y o u r D N A i s t h e r e Yo u d o n ’t h a v e a l l t h e i s s u e s o f t r a n s f o r m i n g l a rg e c e n t r a l i z e d s y s t e m s i n t o workable, agile systems.”

“A nine-to-five workday is irrational and archaic,” McCann continues “Some of my software developers do their best work at 2 a m I am most productive at 5 a m I hire people who deliver in part because they do their yoga midday, have brunch with their uncle every Wednesday, whatever They get to design their day as long as they continue to deliver ”

B r o a d Pa t h H e a l t h c a r e S o l u t i o n s . A w h o p p i n g 9 6 p e rc e n t o f C E O D a r o n R o b e r t s o n ’s r o u g h l y 1 , 4 0 0 e m p l o y e e s w o r k f r o m home Robertson says BroadPath went “all-in” on a remote model not only to help employees, but because it allows the company to better serve clients

The company uses Beehive, a self-developed remote management and collaboration technology that allows employees to see and interact with each other. “A big problem with hybrid deployments is that remote workers feel left out,” Robertson explains.

Beehive also is used to also facilitate the workplace fun remote workers would normally miss “For example, we are launching a r e m o t e i n s t r u c t o r- l e d f i t n e s s p r o g r a m w i t h y o g a c l a s s e s f o r employees Think fitness challenge for at-home workers, but they do it together in real-time Lots of brick-and-mortar companies h a v e t h e s e o n s i t e , b u t f e w s e e m t o o f f e r t h e m t o h o m e - b a s e d workers,” Robertson says.

Pizza day where pizzas are delivered at the same time to workers on a team allows workers to still have face time together during lunch, joking and laughing despite being miles away from each other Crazy hat day is another employee favorite, according to Robertson “It’s about developing connection, in the end And it helps my leaders better manage their teams,” he says.

Broadpath’s results so far? Attracting higher caliber employees, producing higher quality work, lower attrition, and lower costs

CALLING IT

Te

p l o y m e n t g r o w t h f o r telecommuters has outpaced non-telecommuters year-over-year for more than a decade. Remote working arrangements are not a fad, but rather a way for companies to maintain productivity and profitability in an era where workers simply don’t want to be tied to a traditional office environment

e m p l o y e e s t o focus on accomplishment, not activity,” Eikenberry says. But the millions of dollars saved in office space and higher retention rates don’t hurt either.

www icpas org/insight | SPRING 2018 15 “ D i s t r u s t f u l t y p e s m i c r o - m a n a g e , w h i c h w r e a k s h a v o c i n a n y working environment but particularly in a remote one ” Wo r k - l i f e i m b a l a n c e s . W h i l e d i s t r u s t f u l m a n a g e r s w o r r y t h e i r out-of-sight

i n

h

e n t h i s

o r y i s a n y

A t i t s b e s t , t e l e c o m m u t i n g f o rc e s “ l e a d e r s

l e c o m m u t

g ’s g r o w t

i s u n l i k e l y t o s l o w, l e t a l o n e s t o p , i f r e c

t

i n d i c a t i o n e m

a n d

Cashing in With Tax Reform

Tax law changes make early saving for education expenses all the more enticing.

BY MARK GILBERT, CPA, PFS

BY MARK GILBERT, CPA, PFS

Among the many savings and investment vehicles students and parents can use to finance education expenses think Coverdell Education Savings Accounts, Roth IRAs, and U S savings bonds the most popular plans just got a shot in the arm thanks to tax reform

Around since 1996, 529 plans, or “qualified tuition plans,” are taxadvantaged savings plans sponsored by states, state agencies, or educational institutions, and authorized by Section 529 of the Internal Revenue Code, to encourage education saving.

The Tax Cuts and Jobs Act of 2017 introduced some important changes to 529 plans that should only further their popularity Here are the highlights and some practical ideas for implementation and use

EXPANDED USE

529 plans come in two types: (1) prepaid college tuition savings plans, and (2) defined contribution-type account balance plans, which are funded with “after-tax” contributions. 529 plan contributions grow on a tax-free basis, much like in a Roth IRA, and withdrawals remain tax-free if used for qualified education expenses.

Previously, “qualified education expenses” meant only certain college-related expenses Now, the law permits up to $10,000 per year of tax-free withdrawals from 529 account balance plans to cover tuition and fees of public and private elementary and secondary schools.

This is a dramatic expansion, which allows 529 account balance plans to essentially replicate or replace Coverdell Education Savings Accounts (ESAs) While annual contributions to Coverdell ESAs are limited to $2,000 per child, annual 529 plan contributions max out at the gift exclusion amount of $15,000 per donor per child, or $75,000 if “front loading” five years’ worth of contributions, a prudent estate planning strategy often used by grandparents.

It’s my hope that the expanded use of 529 account balance plans will encourage families to start saving earlier in a child’s life. With education costs continuing to rise, the more time allowed for contributions to grow prior to withdrawal, the better

I generally recommend funding 529 plans for college to cover about 66 percent of the anticipated total expense, with the remaining 33 percent coming from other savings, investments,

16 INSIGHT | www icpas org/insight P E R S O N A L F I N A N C E

current cash flow, and scholarships or financial aid. For families wishing to send children to private elementary or secondary schools, I believe funding a 529 plan account to cover 100 percent of the qualified costs is best because the availability of scholarships and financial aid is more limited Additionally, any unused 529 plan funds can be used for college or another child’s education. How should 529 plan funds be invested? As you would with your retirement savings, you must consider risk tolerance and time until funds will be withdrawn to form a reasonable investment strategy. While each family’s situation is unique, I often recommend an agebased methodology: the youngest child’s account is invested heavily in equities while the oldest child’s account is invested more in bonds and cash. When investing for elementary and secondary school, the same philosophy holds the shorter time frame until need means these accounts should be in fewer equities and more in stable income vehicles I also recommend setting up separate accounts for each child’s college, elementary, or secondary education expenses to better manage the funding goals

COVERDELL ESAs ELIMINATED

Thanks to the new tax law’s 529 plan expansion, Coverdell ESAs are essentially obsolete In fact, lawmakers have ruled 529 plans to be the superior education savings vehicle and have eliminated the option of new Coverdell ESAs Why would they do this? First, as noted earlier, 529 plans benefit from having higher contribution limits Second, there’s no age limit on disbursing 529 plan funds, whereas Coverdell ESA funds must be disbursed by the time the child or beneficiary reaches age 30 The only downside of this

move is that 529 plans generally have limited investment options whereas Coverdell ESA funds could have been invested in nearly any publicly traded security

So, what now? I recommend existing Coverdell ESAs be rolled over to 529 plans to obtain the more generous benefits

ABLE OPTIONS

ABLE, aka Achieving a Better Life Experience, accounts were created by 2014 legislation designed to assist individuals with disabilities These accounts are similar to 529 plan accounts in that they can receive a maximum after-tax contribution of $15,000 per year and grow on a tax-deferred basis that becomes tax-free if used for “qualified disability expenses ” These qualified expenses include education, housing, transportation, health care, and financial management to improve the quality of the disabled beneficiary’s life The primary benefit of the ABLE account is that a wide range of expenditures can be made, and assets accumulated, without disqualifying the disabled beneficiary from various public service benefits like Social Security, Medicaid, and SNAP (“food stamps”). Thanks to tax reform legislation, 529 plan accounts can now be rolled over to ABLE accounts This is a great benefit for families who have funded 529 plan accounts for children who later became disabled and are unable to attend college.

The new tax law has set forth several changes that surely will increase the popularity and usability of 529 plans. Whether for your family’s own benefit, or for your clients’, I encourage you to further familiarize yourself with the nuts and bolts of these savings plans that can drastically improve future finances

www icpas org/insight | SPRING 2018 17

Turning Tax-Time Clients Into All-Time Clients

It ’ s prime time for CPAs to turn their seasonal clients into year-round revenue generators.

BY JEFF STIMPSON

CPAs certainly hear a lot from their clients during tax season, but how can they transform this seasonal flood of tense traffic into a steady stream of year-round revenue? It’s quite simple, really The best way to turn seasonal clients into year-round clients is to sell them on added services by consistently communicating your value and benefits

Naperville, Ill -based accounting, tax, audit, and advisory firm Sikich, for instance, makes it a point to hold specific in-person client meetings at the end of each year. “These meetings serve several purposes,” says Illinois CPA Society member Louis Sands, CPA, JD, a managing director in Sikich’s accounting, audit, and tax practice. “First, they allow us to build stronger relationships with clients and get to know them on a more personal level Second, meeting at the end of the year allows us to uncover information that can help us better plan for the upcoming tax season, make any necessary end-of-year changes, and talk about longer-term plans and strategies ”

In fact, a renewed focus on tax strategies and financial planning, thanks to the Tax Cuts and Jobs Act of 2017 (TCJA), is likely to be a boon for CPAs and other advisors hoping to build better connections with clients in the year ahead.

“Since the passing of tax reform, we’ve had an unprecedented surge in client conversations,” says Charles “Chuck” McCabe, president and CEO of Richmond, Va -based Peoples Income Tax and The Income Tax School in Glen Allen, Va “Everybody is interested in learning how the new tax law will impact them.”

CHANGE IS OPPORTUNITY

“The key with something as omnipresent as the new tax law is to be proactive and understand how it applies to your clients before they call you,” Sands says “Reform is being talked about all over, and people are hearing different, sometimes contradictory, advice. Your clients are relying on you ”

This presents a unique opportunity for CPAs to showcase their expertise by providing clients with much-needed information and tips, McCabe suggests, which could ultimately spur them to seek you out for other services, like payroll, financial services, or taxpayer representation

Many Sikich clients, for example, are closely held businesses “The top things we’re discussing with these clients are the 20 percent potential deduction for pass-through entities, the prepayment of taxes, and suspension of many applicable deductions,” Sands explains.

18 INSIGHT | www icpas org/insight P R A C T I C E M A N A G E M E N T

“One of the biggest changes brought by the TCJA involves the calculation of qualified business income,” adds Illinois CPA Society member Mark Heroux, JD, principal in the tax services group at Baker Tilly in Chicago. “Many of our clients are passthrough entities, and the TCJA provides a new scheme for taxing these. The rules are complex, have uncertainty, and pose risks and opportunities ”

TCJA changes affecting repatriation of offshore income is another topic raising a lot of questions and confusion “Don’t be hasty with your conclusions there are different options available to taxpayers who might want to repatriate income, and modeling these options is a must before making decisions,” Heroux says, suggesting this is another area CPAs can use to drive value-added services and discussion

The point is to show that you’re an expert, that your services are scalable, and, most importantly, that you want to serve clients beyond what they’re already coming to you for

COMMUNICATION IS CRUCIAL

Whether your forte is offering tax reform insight to corporations or maximizing an individual’s income tax savings, one of the best ways to determine additional services you can offer to benefit your clients is to, quite frankly, ask them “Surveys and Q-and-As are easy, inexpensive ways to secure useful client feedback and information,” Sands says.

That said, McCabe recommends limiting surveys to about 10 questions and offering appealing incentives to complete the survey if it’s not directly related to a service just provided And don’t neglect post-engagement feedback, which is crucial for client service and business development

Following client engagements, Baker Tilly’s dedicated client services director conducts satisfaction assessments through a mix of direct telephone calls, client visits, and web-based surveys, according to Thomas Walker, CPA, JD, the firm’s Chicago-based regional managing partner.

“We verify that we’re delivering on the commitments we made, and that clients’ needs and expectations are being met,” he says, explaining that all documented client feedback is shared with the engagement team and partner

“Additionally, we utilize Huddle, a cloud collaboration software,” Thomas says “Huddle allows for secure collaboration anywhere, anytime, and on any device, making it easy for our internal teams and clients to come together, share and edit files, assign tasks, and track activity in a secure environment This investment in technology supports real-time communication both internally at Baker Tilly and with clients and provides a seamless trail from initial planning through the final financial statement issuance.”

TIMING IS EVERYTHING

When going beyond service and engagement communications, it’s important to consider how, and how often, to communicate with clients In his book, “Guide to Start and Grow Your Successful Tax Business,” McCabe urges writing to every client at least once a year, and clients with complex tax situations and small business owners should receive formal communications at least two or three times a year The letters should act as reminders that you’re available to serve first and foremost, but they also should summarize any changes in your practice that could potentially benefit your clients and any economic or regulatory developments that could affect them

Email newsletters, website or blog posts, and social media posts also are effective communication tools you can use more frequently

to drive awareness of your services, news and information of interest to clients, speaking engagements, important filing dates, referral offers, and much more These informal communications should be easy for clients and potential clients to understand and share After all, “A referral from a current customer is the number one way to secure new clients,” Sands notes

Baker Tilly, for instance, promotes its complimentary educational content, including seminars, roundtables, live and on-demand webinars, and targeted industry newsletters and alerts, through these channels “Both clients and prospective clients have access to these through our website and by signing up for our mailing list,” Walker says. “Education allows our firm and our professionals to stay in front of our client base on a regular basis while providing them with timely information ”

THE PAYOFF

“Take the long view on every client and strive to build relationships as opposed to transactions,” Walker encourages “ROI is not the only metric of success. Rather than weighing potential fees against hours required, we constantly ask ourselves how we can better understand our clients’ businesses and therefore identify additional areas where we can add value.”

Converting seasonal clients into year-round clients is a process

It takes effort. It might even take getting new certifications or learning new practice areas But diversifying and cross-selling year-round services that complement your core offering, and effectively communicating about them to current and prospective clients, will undoubtedly open new business development and retention opportunities

www icpas org/insight | SPRING 2018 19 E xperiencing: • Stress? • L ack of Sleep? • IRS induced Nausea? We have helped thousands sell... and WE CAN HELP YOU! Ta x Se as on Cessation Pro gram Trent Holmes 800-397-0249 Trent@APS.net www.APS.net D e l i v e r i n g R e s u lt sO n e P r a c t i c e At a t i m e

April 1, 2017 - March 31, 2018

$105,000

Jovencio & Violeta Mangahas

$65,000

Dempsey J Travis Foundation

$15,000

Deloitte LLP

$10,000

Abbott Laboratories

Crowe Hor wath LLP

Illinois CPA Society

nois CPA So Washin r tuni

Mega “My d with A natura bit. Th helpe maste my CP gratef

$ 00 awarded 60 scholar ships ,000 donor s

$500 - $999

Jason Parish

Amanda Pictor

President ’s Paver s

Bill Graf

Sheldon Holzman

Kenneth & Jacqueline Hull

ICPAS O'Hare Chapter

ICPAS Women's Executive Committee

Stacy Janiak

John E & Jeanne T Hughes

Charitable Foundation

Kenton Klaus

Dave & Darlene Landsittel

Scott Lehman

Sara Mikuta

Elizabeth Murphy

Morris Oldham

Belverd Needles, Jr & Marian Powers

$5,000

Edilber to & Carmelita Or tiz

$1,000 - $4,999

Anonymous

Alverin M Cornell Foundation

Maria Fides Balita

BKD Foundation

Howard Blumstein

Mar trice Caldwell

Rose Cammarata

Cameron Clark

CNA Foundation

Joseph D'Amico

Lindy Ellis

Ar thur Farber

Follett Corporation

William Gif ford, Jr

Mark Glochowsky

Lee Gould

Beth Pagnotta

Floyd Perkins

Melody Ragan

Kim Rice

Deborah Rood

Stella Marie Santos

J Bradley Sargent

Todd Shapiro

Elizabeth Sloan

Scott Stef fens

Duane Suits

Myra Swick

Catherine Villinski

Kimberley Waite

Connie Watkins

Jef fer y & Julie Watson

Mar y Ann Webb

Cher yl Wilson

Wipfli Foundation Inc

Lawrence & Nancy Wojcik

Donna Zarcone

Anonymous (3)

Brent Baccus

Peter & Natasha Granholm

Sharon Gregor

Lisa Hanlon

Geof frey & Virginia Harlow

Lisa Har tkopf

Margaret Hickey

ICPAS Central Chapter

ICPAS Young Professionals Group

Illinois Tool Works Foundation

Donald Kieso

Anne Kohler

Thomas Mur tagh

Stephen Nor th

Annette & Tom O'Connor

Jennifer Roan

JoAnna Simek

Richard Thompson

$250 - $499

Anonymous

Bolanle Babatunde

Terr y Bishop

Genevieve Burns

Rebekuh Eley

Stephen Ferrara

Mar y Fuller

Rober t Giblichman

Lawrence Gill

Marla Gordon

Gar y Har t

Trudie Kanter

Wendy Kelly

Jef frey Krol

Richard & Donna Loraine

Dave Luzi

L James Margner

Rita McConville

Miller Verchota Inc

Kenneth Posner

Prado & Renteria CPAs

Dan Rahill

Deborah Ringer

Joan Rockey

John Rogers

Elizabeth Roghair

Katherine Scherer

Michael Singer

Gerard Swick

Marites Sy

Meredith Vogel

Adriane Wong

Kevin & Karen Wydra

$100 - $249

Anonymous (8)

Sheldon Abrams

Annabelle Abueg

Michael Amoroso

John Baily

JoAnn & Bob Benzer

Joseph Bigane, III

Brian Blaha

Roslind Blasingame-Buford

Bruce Breitweiser

James Brennan

Elizabeth Buf fardi

M David Cain, Sr

Margaret Car tier

Vilma Chan

Bridget Coleman

Har vey & Arlene Coustan

Joseph Cvinar

Michael & Beverlee Dallmann

Jon Davis & Heather Pesch

Jim Dickey

James Dolinar

Melody Driver

Amy Dybowski

Kimi Ellen

Jonathan Hauser

Melinda Henbest

Julie Her witt

Angela Hickey

Kathy Hor ton

Eileen Iles

James Johnston

John Kaiser, Jr

David Kalet

Deanna Kanosky

Jason Klein

Kristina Kor win

Beth- Anne Lang & Lillie Miller

Paul Lau

Cher yl LeeVan

Sara Leone

Dianne Lystlund

William Malsch

Ted Mandigo

Randy Markowitz

Kenneth & Kathleen Naatz

Rebecca Newton

William O'Neill

Charles Phillips

R Bruce Pickens

Elizabeth Pittelkow

Michael & Noreen Potempa

Ernest Potter

James Quaid

Roy Raemer

Elliott Robbins

John Saladino

Jennifer Schultz

Richard Shapiro

Edward Slack

Christine Smith

Laurence Sophian

Michael Tadla

William Taylor

Huber t Thomas

John Tolar

Andrea Urban

Jay Wilensky

Carl Woodard

Doyoung Yong

Kenneth Yu

Anthony Zordan

UP TO $99

Anonymous (6)

John Abernethy

Sandra Adam

Angela Agnew

Keshav Agrawal

Rao Akella

Jude Alagna

Omar Alaskari

Andrew Alexander

Alonzo Allen

Alan Allphin

Paul Alpern

Daniel Ammentorp

Jennifer Anderson

Susan Anderson

Steven Andes

Wayne Barcheski

Ar thur Barrett

William Bar ta

Richard Bar tell

Jens Bauml

Mr & Mrs Gerald Bayer

Charles Baygood

Dennis Beard

Chris Beaulieu

Kylie Bechtold Bashir Bello

Benchmark Aspen & Associates Ltd

Cur tis Bennett

Donald Bennett

Peter Bensen

John Berg, Jr

Jordan Berger

Dana Berglind

Denise Berkin

Howard Bernstein

Kenneth Ber trand

Jeannine Cohn Best

Rona Bezman

Chester Biel

Lydia Bilyeu

John Blackburn

Michael Blakeman

Carla Blanchard

William Bledsoe

David Blum

Mark Blumenthal

Sarah Ann Bohnsack

John Bone

Basil Booton

Rober t Boscacci, III

Gar y Bowen

Mar y Bowman

Rober t Brackett

Thomas Brandt

Jennifer Braswell

Thomas Breecher

Thomas Brescia

Mar y Bresson

Steven Brewer

Thomas Broderick

Marcia Brown

Michael Brown

Scott Brown

Terrence Brown

William Bruno

Joseph Br yk

Alber t Buabeng

Kymberly Buchanan

Kenneth Bunce

Teresa Burczak

John Burghout

Timothy Buzard

Carrie Byers

Nicholas Caccamo

Joseph Callahan, Jr

Paolo Camoletto

Paul Caponigri

Dariusz Caputa

Karen Carlos

Mur thy Cherala

Scott Cheshareck

Rober t Chicoine

Christopher Childs

Rajeev Chopra

Chiu-Yeung Chow

Ronald Cierny

Eleanor Clanahan

William Clark

Marsha Clesceri

D Close

Susan Coats

Brian Coderre

Herber t Cohen

Janice Coker

Jay Colber t

Joan Comfor t

Kevin Conarchy

Christopher Conneely

Carolyn Coonce

Joseph Cordell

Alan Cornue

Michelle Cozzini

Marcia Craig

Diane Cranmer

Anne Cummings

James Cunningham, Jr

Kevin Currid

Edwin Czopek

Czeslaw Czubik

Brian Dahly

John Dai

James Dale

Angie Dallam

John Daly

Christopher D'Andrea

Donald Danner

Antonio Davila, Jr

Mark Davis

George De Heer

Paul DeFiore

Deborah DeHaas

Alan DeMar

James Dempsey

Jennifer Denil

Carla Denison-Bickett

Jenny DeNosaquo- Wilson

Esha Desai

Antonio DeSensi

Thomas DeSimone

Donald Dickinson

Bernard Dickneite

Diane Dillon

Maria Diokno

Toni Diprizio

Melchor Domantay, Jr

Paul Donnell

Angela Dowell

Joel Downie

Patricia Doyle

Mar tin Draths, III

Andrew Dreyfuss

Jeremy Dubow

Richard Duf fy

Gregor y Dunham

Susan Eby

Daniel Ecker t

Susan Edelman

Rolf Eilhauer

Glenn Eisenhuth

Ruth Elbaum

Joe Elber ts

Christopher Elder

William Elliott

Dallie Ellis-Stetson

Rober t Engstrom

Eric Ephraim

Michael Ericksen

Susan Esa

Pablo Espiritu

Paul Estrem

Margie Fabro

Maurice Farbstein

Michael Fehlen

Rober t Feldgreber

Charles Feller

Emily Ferdina

Sarah Ference

Carlos Ferreira

John Ferrentino, Jr

Ralph Fishman

Shari Fitzgerald

Steven Flack

Ronald Flinn

Patrick Flynn

Vincent Forgione, Jr

Kevin Foster

Michael Frank

Thomas Frank

Rober t Fraser, Jr

Thomas Frawley

Mar tin Freeman

Jessica Freiburg

Deborah Froelich

Richard Fugiel

Annette Fulcher

Richard Galloway

Vishal Gandhi

Manish Garg

Daniel Gar tland

James Gavin

Christine Gavlin

Debra Gay

John Gaynor

Ronald Geib

Stanley Ger tzman

Tracey Gibbons

Sheldon Ginsburg

William Gladden

Thomas Glavin

Edward Glazar

Gene Goldberg

Stuar t Goldsand

Mar vin Gollob

Evan Goran-Dr y

Dianne Goren Radtke

Ryan Goulding

Peggy Graf

David Gransee

Alan Gray

Rober t Grecco

Stan Green

Brad Greenberg

Tom Greenway

Steven Greim

William Griswold

David Groeber, Jr

Anne Gromer

Donald Grossman

Jonathan Grossman

Mar y Grossman

Gregor y Grosvenor

Raymond Grothaus

Rober t Grottke

Nancy Grunde

Katherine Gudgel

James Guerra

William Guska, Jr

Mark Guziec

Donald Hacke

Brett Hale

Harold Hale

Terr y Hall

Timothy Hall

Ethel Hall-Langwor thy

M Dean Hamilton

Farid Hanna

Georgann Hanna

Glenn Hardesty

Eric Harkness

Norris Harstad

Patrick Har t

Sharon Har vey

James Haugh

Dennis Hawkins

Rober t Hedrick

Harlan Heller

John Hellner

Steven Henrickson

Marianne Her f f

Rober t Navarro

“Being

re

in this leadership role really forced me to overcome my shyness and helped me have a better college experience. This great oppor tunity helped me discover how much fun it can be to get involved.”

g an ke ar y a a

Joel Her ter

Stanton Herzog

Michael Hickey

Bernard Hicks, Jr

James Hill, Jr

Man Kit Ho

James Hogan

Alpachino Hogue

Russell Holmgren

Jana Holt

David Hooker

John Hopkins

Ilir Hormova

Michael Horst

Murray Hor witz

David Hutchison

Elaine Igelman

Brian Ippensen

Douglas Ir win

Alysa Isaacson

Anthony Isher wood

Kenneth Iwanicki

Joseph Izen

Andrea Izykowski

Jesse Izzo

Jerrold Jacks

Kenyetta Jackson

Michael Jacobson

Ryan Jaeger

John Janas

Ronald Jar vis

Frank Jasek

Michael Jefver t

Mark Jewell

Joseph Jimenez

Charlaina Johnson

Joseph Joyce

Paul Julien

David Jurcenko

Amy Justice

Richard Kaczor

Peter Kaminsky

Vera Kapka

Bur ton Kaplan

Howard Kaplan

Sharad Kapur

Edward Karasek, Jr

Mar ylou Karkow

Barr y Katz

John Kavalunas

Karl Keane

Katrine Keller

John Kent

John Kintner

David Kipp

Hal Kirby

Diane Klocke

Mark Knapczyk

Kathleen Knolhof f

William Knopf

Alfred Koermer

Alicja Kolendo

Br iana Willia

Rober t Kolman

Michael Kolokotronis

Alan Kolosh

Masahiko Kon

Mar vin Kopulsky

Stephen Kosin

James Kostrewa

John Kovatch

Terence Kozicki

Harr y Kramer

Brian Kregor

Steven Kroll

Maria Krull

Treva Kruse

Wayne Krusen

Thomas Kuchta

Michael Kudia

John Kulczewski

Leynette Kuniej

John Kustes

Lawrence Ladner

Howard Lamper t

Ronda Landr y

Tina Langston- Andersen

Edward Lannon

Thomas Larocca

Cher yl Laska

Jef frey Lasky

Stephen Latreille

James Laubinger

Babatunde Lawal

Rober t Lay

Valentina Lazarova

Thomas Lechowicz

Daphne Lee

Shelly Lee

Terr y Leipsig

John LeMay

William Lemna

Debra Lessin

John Levy

Steven Levy

Maurice Lewis

Fan Li

Sicong Li

Peter Liao

Christopher Lilek

David Lilek

Jui-Yuan Lin

Lin Lin

Jonathan Lindh

Paul Lipka

Joel Litman

Mar y Little

Zara Lo

Thomas Lockowitz

Raymond Lombardi

Augustus Lonardi

Larr y Lonis

Lori Lorgeree

Tracey Lowenthal

Richelle Therese Lu

John Lubke

Gregor y Luczak

Donna Lund-Magnus

Lisa Lutz

Mai Luu

Daniel Lyons

Rober t Maas

Thomas Macciaro

Rose Marie Mack

William MacLean

Michael Madden

Dominic Maduri

Louis Mago

Kevin Mahoney

Janet Malone

Daniel Maloney

Lawrence Manelis

Vasliki Manis

Herman Marino

Jennifer Mark

Mark Marosi

Patricia Marzullo

Joanna Maslan

Anthony Massaro

Alan Maty

JoAnn May

Michael Mayo

Melvin Mayster

Joan Mazurek

Andrew McCormick

Margaret McCoy

Jef frey McCutcheon

James McDermott

James McEnerney, Jr

Kyle McGinnis

William McGrane, Jr

James McMahon

Joseph McNeely

James McPhedran

Karen Meades

Nicholas Mechales

Charles Meeder

Neal Mehlman

Antony Meister

John Meister

Richard Meltzer

Gregor y Messing

Terr y Michaels

Anne Mieleszuk

Leonard Miller

Randall Miller

Patrick Miner

Gar y Mingle

Dan Mirjanich

Paul Miscinski

Alber t Mitchell, Jr

James Mitchell

Linda Mitchell

Matthew Mitzen

Lawrence Mocadlo

Ilaria Mocciaro

Megan Mocogni

David Moes

Kevin Mof fitt

Brian Mohr

Cynthia Moody

L Joe Moravy

Karla Morgan

Richard Morris, Jr

Michael Morse

Ernest Mrozek

Carmen Mugnolo

Thomas Mula

John Mulkerin

David Murphy

Emmett Murphy

James Murphy

Vani Sreenivas Mur thy

Craig Myers

Edward Nadler

Jef frey Narcisi

Christine Nardini

Kari Natale

Lawrence Neal

Leonardus Neggers

GJ Neumayer

James Ngai

Vesna Nikolic

James O'Brien

Rober t O'Brien

Amanda Ochsendor f

David O'Connor

Edward Odmark

Michael O'Hara

Joseph Olsen

Ben O'Malley

William O'Malley

Akin Omotosho

James O'Neill

Kevin Ooms

Kirk Openchowski

Karen O'Reilly

Thomas Ottenhof f

Vicki Paavilainen

Rober t Palasz

Heather Paquette

Tai Park

Wayne Parsons

Ruth Patterson

Amy Patton

Whitey Patton

Frederick Paulman

David Pavela

Frank Pavlica

Joseph Pedota

James Peers

William Peluchiwski

Cinda Pembroke

Clair Penner

Rober t Pernini

Linda Perri

Elaine Pesavento

Mark Pesavento

Pamela Peters

Carla Peterson

Kur t Peterson

Ryan Petrey

Marianne Phelan

Dana Phillips

Brent Piechowiak

Samuel Pincich, Jr

Terr y Pitcher

Krista Piwonka

Anthony Polinski

Peter Ponzio

David Post

Paula Pouliot

Walter Powers

Kathr yn Preston

James Pribel

Jay Price, Jr

Clyde Proctor

Todd Prof fitt

Patricia Purpura

Kyle Putnam

Richard Putz

Gavin Quan

Michael Quane

Judith Quedenfeld

Patricia Quinlan

Aran Quinn

Anny Quon

Joel Radakovitz

Randi Ragins

Roy Ramer

George Ranstead

Terrence Raterman

Richard Raupp

William Razzino

Jean Regan

Michael Regan

Stephanie Reicher t

Arnold Reingold

Christopher Reiser

Howard Renner

Eugene Retzer

Gloria Rex

Catherine Riddick

Rochelle Rif fer

Natalie Rinard

Terr y Robbins

Eileen Rober ts

Dennis Robin

Howard Rosell

Lynn Rosen

Nancy Ross

Linda Rossi

Sharmistha Roy

William Rudolphsen

Camille Rudy

Maurice Sabath

Ahsan Sadiq

Kana Sakaide

Jason Samikkannu

Alan Sanchez

Dan Sanchez

Catherine Santoro

Everett Sather

Mar vin Schaar

Elizabeth Schaefer

Margaret Schaefer

Phillip Schaefer

David Schafer

Michelle Schef fki

Rober t Scheuermann

William Schirmang

David Schmeltzer

Laurie Schmidgall

Michael Schneider

William Schneider

Rober t Schoen

Rober t Schroeder

Richard Schultz

John Schur ter

Florian Seidel

Howard Serlin

Michelle Serna

David Shade

Gar y Shadid

Lawrence Shane

Audra Shindo-Chan

Cecilia Siciliano

Barbara Siegel

June Silder

Rober t Silverman

John Simon

John Simpson

Peter Siu

Stephen Slaber

James Slamp

John Sluzynski

David Smith

“Thank you fo helping me o Your suppor t and motivatio impossible, p

William Stahler

John Stanfield

Daniel Stanovich

Linda Stawicki

James Stefo

John Steger

Maurice Steiner

Rober t Stencel

John Stephens, III

Christina Stevens

Lee Stiles, Jr

Howard Stone

Janet Storey

Joni Strand

Michael Szymanski

James Taibleson

Ramya Tallarovic

Angeles Tapia

Miles Taub

Shirley Taylor

Kenneth Thomalla

Jef frey Thomas

John Timmer

Gregor y Tissier

Frank Tlusty

Kathleen Tollaksen

Michele Tomczak

David Towne

Timothy Voncina

Raymond Voros

Gail Vos

James L Vour voulias & Associates LTD

Julie Vuotto

Brandon Wade

Genevieve Waldron

April Walker

Richard Walker

Sherr y Walters

Bradley Walton

Frederick Walz

Monika Warnecka

STUDENTS STILL NEED YOUR HELP

Each year, we have more qualified candidates than awards to give You could help us close that gap Get involved and suppor t our programs to ensure oppor tunities are possible for hundreds of future CPAs.

Prog

rams to Suppor t

These programs inspire and reward deser ving future CPAs:

• Tuition & Textbook Scholarships

• CPA Exam Awards

• S tudent Ambassador Program

• Mar y T Washington W ylie Internship Preparation Program

How to Get Involved

• Encourage people you know to apply for the programs

• Volunteer your time and exper tise

• Donate and help fund more prog rams

Matthew Warren

David War tner

Jef frey Waters

James Watson

Carolyn Webber

Susan Weber

Sheila Weinberg

Ar vin Weindruch

Harriet Weinstein

Michael Weisberg

Constance Weissman

Matthew Welch

John Wellhausen

John Wentwor th

Darnell Wenzel

James Werner

Glen Wher fel

Barbara White

William White

Richard Whyte

Laura Wilhelm

Richard Wilkens

Kelly Willett

Jennifer Williams

Charlotte Wilson

Michael Wojcik

Agnieszka Wojtowicz

Charles Wolf

David Wolfe

Fred Wolter

Lorna Wolter

William Woolf

Thomas Woulfe

Leiyang Xin

Steven Yang

Rober t Yarbrough

James Yerbic

Frank Young

Carl Yudell

Raul Zarco

Jia Zeng

William Zink

Donors with a multi-year pledge are recognized for the full amount of their pledge in the first year and for their pledge installment amount paid in the remaining years of the pledge Ever y attempt was made to acknowledge all donors who have given during this period If you see a discrepancy, please call 3 12 517 7656

kloot o Jr r

Help make a dif ference: www.icpas.org/annualfund

24 INSIGHT | www icpas org/insight

BY CAROLYN KMET

I n fl u e n c e i s a n i n ta n g i b l e , yet i nva l u a b l e , p e rs o n a l a s s et . I t ’ s a fo rc e s h a p e d by th e i n t ri n s i c va l u e s o f th o s e w h o h o l d i t . W h e n w i e l d e d w i th h e a r t a n d p a s s i o n , i n fl u e n c e can inspire masses. When applied with force o r m a n i p u l a t i o n , i n fl u e n c e c a n d e st roy a n d d i s h e a r te n I n fl u e n c e , i n a l l i t s fo rm s , i s th e ability to convince others to follow you, even when they aren’t required to

“ I n fl u e n c e i s p e rs u a d i n g oth e rs to d o something for you that gives them no direct benefit but is essential to the greater strategy. Influence is convincing someone to see your perspective and act upon it,” explains Illinois CPA Society member Annette O’Connor, vice p re s i d e n t o f fi n a n c e a n d h e a d o f i n te rn a l audit at RRD in Chicago

www icpas org/insight | SPRING 2018 25

Influence isn’t necessarily defined by the scale of an a u d i e n c e . Ra th e r, a t th e h e a r t o f i n fl u e n c e i s th e

ability to have your words inspire action.

INSPIRING INFLUENCE

To see the power of influence in action, we can turn to Canadian fast casual restaurant franchise Freshii Since its founding in 2005, Freshii has opened hundreds of restaurants across 20 different countries “ We want to provide meals and snacks that help you live your best life,” the company says That sounds welcoming and all, but key to Freshii’s success isn’t a simple slogan, it’s the positive influence CEO Matthew Corrin has on Freshii’s stakeholders

“ There are two ways to build influence,” Corrin explains “One way is to manipulate someone; the other way is to inspire someone ”

Inspiring ever yone in the company to be the best version of themselves and to maximize their own potential is at the hear t of Corrin’s influence, and it resonates through Freshii’s corporate culture For example, Freshii’s leadership team makes a concer ted ef for t to ensure that ever yone in the organization understands how their work ties into the broader company objective

“ We spend a lot of time thinking about the ‘why’ factor,” explains Freshii’s Chief People Of ficer Ashley Dalziel “ We want people to know they have ownership over what they do, and that their work makes a dif ference That, I think , is how Corrin’s inspiration and influence come to life ”