COLLECTIVE INVESTMENT SCHEME PERFORMANCE TO DECEMBER 31, 2021

ABOUT THE LISTINGS

CounterpointSCIValue(A1)7,1713243,61623,87114,7215

36OneBCIEquity(A)7,3712830,484722,62214,0525

NinetyOneValue(R)18,24345,97521,8938,8244

MethodicalBCIEquity(B1)6,0214825,2310120,84410,55245

36OneBCISAEquity(C1)9,158333,852819,54511,5215

FairtreeEquityPrescient(A1)11,194119,3114719,51614,0034

InvestecW&IBCIDynamicEquity(A)18,08460,20119,02710,95184

KagisoEquityAlpha(A)10,675431,024318,61812,9545

SIMTopChoiceEquity(A1)6,8513728,096718,56911,66134

TrueSCIGeneralEquity(A)6,0814626,198718,401012,1495

RezcoEquity(A)2,6016121,7213318,281112,08105

CoronationEquity(A)7,2113122,1313017,791210,82195

NinetyOneEquity(R)9,437828,865717,531311,1917

SIMGeneralEquity(R)7,9111731,483917,471410,5524

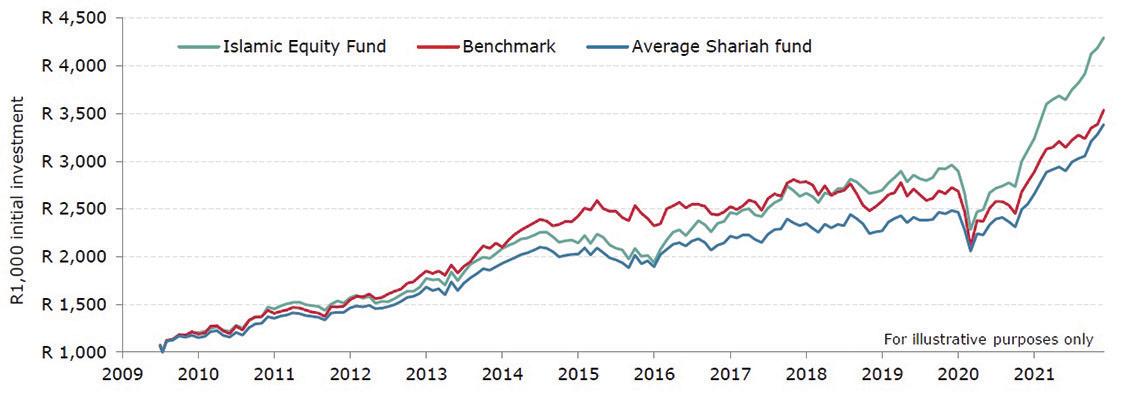

KagisoIslamicEquity(A)9,657337,871717,081512,6465

1nvestSectorNeutralMomentumInd.Tr.(A)21,31231,014416,9316

M&GEquity(A)8,549736,471816,681711,22164

CoronationSAEquity(A)8,0311029,515216,57189,08414

AylettEquityPrescient(A1)14,581547,64416,511911,89124

FairtreeSelectEquityPrescient(A1)11,972920,5014216,4720

APSCiEquity(A1)11,483522,7712216,322110,04324

M1CapitalEquityPrescient(A1)15,99727,017816,18226,77783

CoronationTop20(A)7,1313324,1010916,152310,19304

AbsaTop40Index(A)16,10528,037016,0424

DiscoveryEquity(A)13,072227,167616,04249,44374

AbsaPrimeEquity(A)7,7112327,047715,892510,53254

M&GDividendMaximiser(A)9,726935,342415,682610,42284

ElementIslamicEquitySCI(A)8,0311031,344115,632711,54145

PersonalTrustEquity(A)11,643332,853015,55289,10404

KrugerCiEquity(A)10,036424,5510515,5129

CoreSharesTop50ETF13,991930,274815,383012,0211

ObsidianSCIEquity(B3)4,9615327,527415,31318,93424

MomentumTrendingEquity(A)12,122823,8211115,2832

NinetyOneSAEquity(E)8,589528,636015,24339,55354

TrésorSCIEquity(B1)15,001229,685115,0534

SatrixAlsiIndex(A3)15,001228,596115,053410,7022

PPSEquity(A2)8,4710124,9810215,03359,2839

PortfolioMetrixBCISAEquity(B2)7,1213426,318614,83369,97344

VisioBCIShariahEquity(C)12,662432,583514,7337

DynastyCiWealthAccumulator(A2)12,522620,6513914,533810,58234

SasnBCIEquity(A)15,90821,6513414,44397,74613

StonehageFlemingSCIEquity(A1)11,443719,2514814,34407,21723

AFInvestmentsEquityFoF(A)9,896628,106614,31418,21563

StanlibM-MDiversiedEquityFoF(B1)8,509928,226514,29429,47364

ExcelsiaEquity27four(A1)6,2514239,501413,9443

FGSCIMercuryEquityFoF(A)7,9311626,168813,91448,79454

GryphonAllShareTracker(A)13,022325,3110013,874510,4926

FoundationBCIEquity(A)10,815022,0813113,7846

SanlamPrivateWealthEquity(A1)9,367930,514613,76479,32383

OldMutualRa40Index(A)11,144240,411113,744810,4527

27fourShariahActiveEquity(A1)11,024431,803813,74488,74464

IFMTechnical(A)10,944715,9415513,66494,221033

SatrixRa40Index(A1)11,124340,341213,605010,3829

SatrixDiviETF(A)14,991335,692113,595112,735

BlueAlphaBCIEquity(A)12,122828,735813,585210,73214

AbsaDividendPlusIndex(A)14,731435,382313,5753

SygniaDiviIndex(A)15,37935,572213,515412,527

PSGWealthCreatorFoF(A)7,7612227,827213,50558,3654

1nvestSectorNeutralValueInd.Tr.(A)22,99157,13213,4556

SatrixRa40ETF(A)10,715239,831313,375710,1831

•Resultsarebasedontheperformanceofa lump-sum investment overfourperiods thatendedon DECEMBER 31, 2021.Ineachoftheperiods,thereisapercentage (totwodecimalplaces)bywhichaninvestmentwouldhavegrownorshrunk,and thefund’spositionorrankrelativetootherfunds.

•Returnsforthe three- and five-year periods are annualised (thatis,the percentagerepresentstheaverageperformanceinayear).Asunittrustfundsare medium-tolong-terminvestments,themostimportantperformanceperiodsare thoseofthreeyearsorlonger.

• INITIAL COSTS havenotbeentakenintoaccountandcanhaveaneectonreturns.

• ANNUAL MANAGEMENT FEES areincludedinthereturns.

• DIVIDENDS havebeenreinvestedontheex-dividenddate(thedayaftertheyare declared)atthepriceatwhichtheunitsaresoldtoyou.

• INDICES normallysuppliedasbenchmarksreectpercentagechangesandtakeinto accountdividendsandinterest.Inthecaseofnewindices,ahistoryisnotyetavailable.

•The PLEXCROWN RATING indicateshowafundhasfaredovertimecomparedwiththe otherfundsinitssubcategoryonarisk-adjustedreturnbasis.Turnto page 57 formore informationabouttheratings.

WHAT DOES THE * INDICATE?

Theasterisk(*)beforeafund’snameindicatesthatthefundcomplieswiththeinvestment requirementsofRegulation28ofthePensionFundsAct.Fundssuitableforretirement savingsmustcomplywithRegulation28,whichlaysdownguidelinesaboutInv.indierent categoriesofassets.Toreducetheriskandvolatilityofafund,theActrestrictsexposureto equitiestoamaximumof75percentofthefundanditsexposuretopropertyto25percent.

HOW FUNDS ARE CLASSIFIED

TheAssociationforSavings&InvestmentSA’sclassicationsystemcategorisesunittrust fundsaccordingtotheirinvestmentuniverse:wheretheyinvest,whattheyinvestin andtheirmaininvestmentfocus.

ThersttieroftheclassicationsystemcategorisesfundsasSouthAfrican,global, worldwideorregional.

South African funds mustinvestatleast70percentoftheirassetsinSouthAfrican investmentmarketsatalltimes.Theymayinvestamaximumof25percentinforeign marketsandamaximumofvepercentinAfrican(excludingSouthAfrican)markets.

Global funds mustinvestaminimumof80percentoftheirassetsoutsideSA.

Worldwide funds donothaveanyrestrictionsonwheretheymayinvestbutthey typicallyallocatebetweenSouthAfricanandforeignmarketsinlinewiththemanager’s outlookforlocalversusforeignassets.

Regional funds mustinvestatleast80percentoftheirassetsinaspecic geographicregion,suchasAsiaorAfrica,excludingSouthAfrica,oracountrysuch astheUnitedStates.Regionalfundsmayinvestamaximumof20percentoftheir assetsinSouthAfrica.

Thesecondtieroftheclassicationsystemcategorisesfundsaccordingtotheasset classinwhichtheypredominantlyinvest.Atthislevel,fundsarecategorisedasequity funds,interest-bearingfunds,realestatefundsormulti-assetfunds.

Equity funds mustinvestatleast80percentofthenetassetvalueofafund.

Interest-bearing funds investinbonds,xedinterestandmoney-market instruments.

Real estate funds mustinvestatleast80percentoftheirassetsinsharesinthe realestatesectoroftheJSEorasimilarsectorofaninternationalstockexchange.Afund mayinvestamaximumof10percentinpropertysharesthatarenotclassiedinthe realestatesector.

Multi-asset funds saveyouthetroubleofdecidinghowtoallocateyourassets betweenshares,bonds,propertyorcash.Themanagersofmulti-assetfundsdecide, foryou,whichassetclassestheybelievewillproducethebestreturnsandthen,within thoseclasses,whichsecuritieswillperformthebest.Somefundshaveaxed allocationtothedierentassetclasseswhereasotherschangethemixofasset classesinlinewiththeirviewsofhowthedierentclassesorsecuritieswillperform.

DATABANK PERSONAL FINANCE | 1 ST QUARTER 2022 58

NAME 3 MONTHS 1 YEAR3 YEARS5 YEARS PLEX CROWNS % RANK % RANK % RANK % RANK SOUTH AFRICAN EQUITY GENERAL FUNDS

MONEY MARKET YIELDS

SelectManagerBCIEquity(C)11,334029,175512,92668,6149

OldMutualAlbarakaEquity(A)14,141832,623412,82677,33693

AfricanAllianceEquityPrescient(A1)10,824920,5114112,67688,69483

DenkerSCIEquity(A)7,3712830,754512,66696,22853

AbsaSelectEquity(A)9,258125,389912,64707,62663

AllWeatherBCIEquity(B2)9,238232,703312,6171

PrimeSouthAfricanEquity(A)12,622528,076912,5572

MomentumValueEquity(A)9,288036,401912,4673

OasisCrescentEquity(D)10,994527,227512,45747,65643

MomentumCoreEquity(A)8,888926,168812,3975

HollardPrimeEquity(B)10,595526,857912,27767,68633

SentioSCIHikmaShariahGeneralEquity(B1)10,585631,434012,15776,98753

BCIEquity(A)5,7715026,658412,12786,57803

OptimumBCIEquity(A)11,373826,648512,08798,86433

MomentumEquity(A)10,914831,434012,02808,08583

1nvestIndex(R)8,569626,148911,94818,2955

StanlibEquity(R)7,9711217,4115311,87828,17573

AutusPrimeEquity(A)11,024415,8815611,87828,39533

SatrixMomentumETF(A)10,465824,3410611,6483

DenkerSCISAEquity(B1)8,509932,803211,6184

SygniaEquity(A)8,3710422,7812111,58856,80773

Thethirdtieroftheclassicationsystemcategorisesfundsaccordingtotheirmain investmentfocus.

WHAT DOES THE ‘R’ OR ‘A’ MEAN?

Theseindicatetheannualmanagementfeesaunittrustcompanycanchargeanddepend partlyontheclassofunitsyoubuy.

BeforeJune1998,thefeeschargedonfundswereregulatedwithamaximumannual managementfeeofonepercentayearplusVAT.Fundslaunchedbeforethisdatehavethe letter“R”behindthefundnameandcanonlychangetheirfeesafteraballotofallunittrust holders.Manyunittrustcompanieshaveclosedtheir“R”classfundstonewinvestments andlaunchednewfundclasses.

FundsandfundclasseslaunchedafterJune1998canchargeanyfees.Typically,fees rangefrom0.25percentto2percent,excludingVAT.Fundswithunregulatedfeescanbe “A”,“B”,“C”or“D”classfunds.

Typically,“A”classfundsareoeredtoretailinvestorswhilecheaper“B”classfunds areforinstitutionalinvestorswhoinvestinbulk.Onlytheinstitutionalfundsavailable toyouthroughalinked-investmentservicesprovider(Lisp)arepublishedhere.

Thedierentclassesofasinglefundaremanagedcollectivelyandthedierence inperformancebetweenthemispurelyaresultofthedierenceinmanagementfees.

Mostrecentlywhatareknownasall-in-feeclasses(“C”or“D”classes)havebeen introduced.Thesefundschargeasinglefeecoveringthemanagementfee,thebroker feeandtheadministration(orLisp)fee.

Performance figures supplied by ProfileData

Telephone:0117285510

Email:unittrust@prole.co.za

Website:www.fundsdata.co.za

Disclaimer:Althoughallreasonableeortshavebeenmadetopublishthecorrect data,neitherProleDatanor Personal Finance canguaranteetheaccuracyofthe informationontheunittrustfundperformancepages.

SteynCapitalEquityPrescient(A1)12,332749,15311,04913,971062

CommunityGrowthEquity(A)9,128525,919210,98928,08583 MatrixSCISAEquity(A2)2,9616024,6510310,98928,47513

ClucasGrayEquityPrescient(A1)8,759141,85810,82938,61493

InvestecW&IBCIEquity(A)7,8112023,5311710,75946,43822

PrescientCoreEquity(A2)8,4110320,8213810,57957,62663

VisioBCISAEquity(B8)10,485734,562510,4896

BateleurEquityPrescient(B4)8,679328,536210,26976,56812

SygniaSwixIndex(A)7,9011820,3614310,19987,1674

M&GSAEquity(F)8,1410934,252610,16997,64653

OldMutualManagedAlphaEquity(A)8,0111125,919210,141005,16952

NedgroupInv.SAEquity(A2)7,6312724,2810710,091017,89603

AeonSmartMulti-FactorEquityPrescient(A1)8,2910520,1714410,061027,70623

MomentumCappedSwixIndex(A)7,9511425,729610,03103

SygniaItrixSwix40ETF7,7112316,7515410,01104

OldMutualEquity(A)6,5213929,81509,98105

AllanGrayEquity(A)5,8514925,69979,941066,87762

SatrixCappedSwixALSI(A1)8,4110326,01909,86107

IntegrityEquityPrescient(A1)13,112143,2579,761084,94972

VisioBCIGeneralEquity(A)9,876727,76739,751095,83872

OldMutualCappedSwixIndex(A)8,4910025,77959,63110

AnchorBCIEquity(A)7,7812123,701129,581115,70892

SentioSCIGeneralEquity(B2)8,0111127,04779,42112

AluwaniBCITop25Equity(A)8,1410917,681529,361137,30712

1nvestSectorNeutralGrwth&QlityInd.Tr.(A)10,246014,271579,33114

PrescientEquity(A2)8,859023,941109,291156,6279

FoordEquity(A)3,7315724,981029,231163,53109

AbsaSmartAlphaEquity(A)7,8311917,711519,221175,79882

DotportBCIEquity(B)8,4410223,661139,15118

OasisGeneralEquity(D)9,687131,29429,021195,63912

DATABANK PERSONAL FINANCE | 1 ST QUARTER 2022 59

FUND NAME ANNUALISED YIELD TO DECEMBER 2021 10XMoneyMarketFund3,72 27FourMoneyMarketFund4,62 AbsaPrudentialMoneyMarketFund3,92 AfenaMoneyMarketPrescientFund3,94 AllanGrayMoneyMarketFund4,57 AshburtonMoneyMarketFund4,26 BCIMoneyMarketFund3,97 BidvestPrimeMoneyMarketFund4,27 CadizBCIMoneyMarketFund4,63 CartesianBCIMoneyMarketFund4,15 CitadelSAMoneyMarketH4Fund4,08 CoronationMoneyMarketFund4,25 CounterpointSCIMoneyMarketFund4,28 DiscoveryMoneyMarketFund4,15 FairtreeMoneyMarketPrescientFund4,15 GlacierMoneyMarketFundA4,12 GranateSCIMoneyMarketFund4,23 GryphonMoneyMarketFund4,09 HollardPrimeMoneyMarketFund4,63 LegacyAfricaPrescientMoneyMarketFund3,52 M&GMoneyMarketFund4,13 MarriottMoneyMarketFund3,99 MomentumMoneyMarketFund4,40 NedgroupInvestmentsMoneyMarketFund4,04 NinetyOneMoneyMarketFund4,13 OasisMoneyMarketFund3,72 OldMutualMoneyMarketFund4,08 OldMutualM-MMoneyMarketFund4,32 PrescientCorporateMoneyMarketFund4,67 PrescientMoneyMarketFund4,67 PrimeMoneyMarketFund2,95 PSGMoneyMarketFund3,82 SatrixMoneyMarketFund3,67 SIMMoneyMarketFund4,01 SNNMoneyMarketFund4,32 StanlibMoneyMarketFund4,31 NAME 3 MONTHS 1 YEAR3 YEARS5 YEARS PLEX. % RANK % RANK % RANK % RANK SatrixDividend+Index(A1)15,181135,802013,365812,388 CitadelSAMultiFactorEquityH4(B1)13,512028,246413,365810,79204 CaleoBCIEquity(A)9,078821,2913613,20596,25843 AnalyticsCiManagedEquity(A)11,623423,6211513,18608,52503 WarwickBCIEquity(B)7,9511422,0713213,14617,43673 Mi-PlanIPBetaEquity(B2)9,697026,808113,08628,71473 ColoureldBCIEquity(B)7,6712523,5711613,0263 OldMutualM-MEquityFoF(A)8,519832,833112,97648,00593 MaestroEquityPrescient(A)11,453624,6310412,95654,52993

LynxPrimeOpportunitiesFoF(A1)8,659425,399811,08907,3468

IntegralBCIEquity(A)9,926523,3711911,53865,64902 SatrixMomentumIndex(A1)10,425924,1210811,41878,4652 StanlibEnhancedMultiStyleEquity(A1)10,685331,853711,35889,98333 BCIBestBlendSpecialistEquity(C)9,258129,375311,11897,32703

ElementEarthEquitySCI(A)9,088738,87158,861207,17732

HarvardHouseBCIEquity(A)7,3212922,371288,691211,271121

AllanGraySAEquity(A)6,8713628,70598,631226,02862

OldMutualInvestors(R)6,1614532,51368,541235,1396

BenguelaEquity27four(A1)5,7215128,28638,47124

MaziAssetManagementPrimeEquity(A)11,653234,19278,331255,30932

PerpetuaSCIEquity(A)9,597533,18298,191263,701082

MergenceEquityPrime(A1)6,2914126,83808,181274,341022

NedgroupInv.PrivateWealthEquity(A)4,3015622,471268,101282,761111

H4FocusedWealth(A1)8,0311022,571248,051295,38922

SatrixMidCapIndex(A1)3,6715827,94717,76130

PSGEquity(A)6,3214038,77167,561314,7798

NewFundsValueEquityETF6,8913540,54106,95132

AshburtonEquity(B1)7,9611318,301506,721334,431012

CounterpointSCIDividendEquity(A1)7,6912425,95916,201345,38922

IPHighConvictionEquity(A)9,158321,201376,201343,981052

NedgroupInv.Rainmaker(A)11,343923,641145,821353,801071

FNBMomentumGrowth(A)9,667219,791465,751363,291101

NorthstarSCIEquity(A)6,6513823,661135,36137

AmpersandSCIEquity(B)14,471626,74825,111384,111041

MarriottDividendGrowth(R)4,4115519,791465,111384,481001

CadizBCIEquity(A)8,1410920,551404,941395,20942

FirstAvenueSCIEquity(B1)4,7015418,511494,771401,251131

SatrixQualitySouthAfricaETF11,86319,791623,30141

SatrixQualityIndex(A1)11,91309,311632,841426,3083

FirstAvenueSCIFocusedQualityEquity(A)2,2916210,201612,32143-0,641141

NewFundsLowVolatilityEquityETF3,0215913,011592,12144

CoreSharesSADividendAristocratsETF14,58158,97164-1,66145-1,66115

CorionPrimeConcentratedEquity(A)10,964641,579

MianzoEquity27four(A1)8,2610730,1849

WealthAssociatesBCIEquity(A)10,186229,2954

DierentialNeuralEquityPrescient(A1)9,118628,8756

SatrixSmartcoreIndex(A1)8,569628,0967

PrescientCoreAllShareEquity(A2)15,191028,0868

OysterCatcherRealFinEquity(A)7,9411527,1676

PrescientCoreCappedEquity(A2)8,689226,7283

X-ChequerBCIEquity(B)6,2114326,3186

AmplifySCIEquity(A1)8,549725,8893

OldMutualESGEquity(A)9,497725,8094

VunaniBCIEquity(A)6,0314723,44118

StanlibCoreMultiStyleEquity(A)9,766823,01120

NgwediEquitySNN(R1)9,148422,63123

AeonActiveEquityPrescient(A1)10,206122,49125

CoreSharesScienticBetaMultiFactorETF5,5915222,40127

SelectBCIBlendedEquityStrategy(A)10,126322,28129

AmityBCIEquityIncome(A)1,2816421,40135

LimaMbeuSCIEquity(A1)7,6512621,20137

BacciSNNEquity(A1)7,3113019,85145

Global&LocalSNNEquity(A)8,1810813,20158

Global&LocalSNNLowVolatilityEquity(A)6,0214812,54160

SelectBCIEnhancedCoreEquity(A)16,026

SatrixGlobalInfrastructureFeederETF14,4617

SelectBCIEquity(A)10,7951

SelectBCIESGEquity(C)9,6672

*FNBMultiManagerEquity(A2)9,6074

AnchorBCISAEquity(A)9,5876

EdgeBCIEquity(A)8,2876

MomentumQualityEquity(A)6,17106

SatrixInclusionandDiversityETF1,93163

FTSE/JSEAllShareindex(J203)15,1329,2315,7111,38 INDUSTRIAL FUNDS

FTSE/JSEIndustrialindex(J257)16,0926,4515,549,27 LARGE-CAP FUNDS KagisoTop40Tracker(R)15,791027,79617,26112,341 AshburtonTop40ETF16,08528,10416,45212,192 Satrix40ETF(A)16,09428,14316,37312,133

NewFundsShari’ahTop40IndexETF17,15130,26216,30411,1710 1nvestALSI40(A)16,15327,48916,13511,864

SygniaItrixTop40ETF15,81927,67716,106

PrescientCoreTop40Equity(A1)16,47227,201216,02711,845 1nvestTop40ETF(A)16,03727,95515,85811,816

OldMutualTop40Index(A)16,06627,52815,77911,508

SatrixTop40Index(A1)16,00827,281115,701011,557

SygniaTop40Index(A)15,551127,441015,621111,449

SatrixEquallyWeightedTop40Index(A1)8,331430,86113,21127,3614

NewFundsEquityMomentumETF2,141918,281412,68138,5411 CitadelSA20/20EquityH4(B1)14,631225,531312,2114

SatrixSwixTOP40ETF(A)7,751616,65179,94157,5113

1nvestSwix40ETF(A)7,891516,98169,81167,5512

SatrixSwixTop40Index(A1)7,741716,48189,80177,3515

NewFundsS&PGIVISATop50ETF12,461317,50156,97182,6617 SaronSCILargeCap(A)3,861812,51191,94193,48161 FTSE/JSEALSI40index(J200)16,2528,4016,6512,36 MID- AND SMALL-CAP FUNDS

CoronationSmallerCompanies(R)2,16741,52316,2718,9815 SIMSmallCap(R)12,31355,53115,6224,733 NinetyOneEmergingCompanies(R)7,27548,66211,0632,676 MomentumSmallMid-Cap(A)12,90235,47510,1545,4923 OldMutualMid&Small-Cap(R)8,84441,09410,0452,517 AshburtonMidCapETF3,66627,9577,6663,584 NedgroupInv.Entrepreneur(R)13,44134,0166,2073,195 FTSE/JSEMidCapindex(J201)3,8328,888,454,33 RESOURCES FUNDS

SIMResources(A)21,63365,11143,36129,7715 NinetyOneCommodity(R)18,04633,81439,57226,613 CoronationResources(P)26,75153,08239,27329,7424 NedgroupInv.Mining&Resource(R)23,02242,84334,14425,174 SatrixResiETF(A)21,34432,18525,36521,605 MomentumResources(A)20,85528,02620,95616,6461 FTSE/JSEResi10index(J210)22,1932,3626,1822,54

FINANCIAL FUNDS

NedgroupInv.Financials(R)6,37133,4225,0815,311 MomentumFinancials(A)4,24234,4311,9524,282 SIMFinancial(A)1,88526,0041,2132,084 SatrixFiniETF(A)2,08426,7330,4943,753 CoronationFinancial(A)2,11325,4650,2351,755 FTSE/JSEFinancialindex(J580)2,5029,591,562,88 UNCLASSIFIED FUNDS

KrugerrandCustodialCerticatesETF9,2723,59215,85112,351 *CounterpointSCIPreferenceShare(A1)16,01143,97114,99211,532 SOUTH AFRICAN MULTI-ASSET

FLEXIBLE FUNDS

CentaurBCIFlexible(A)4,274128,311317,42111,6615 BateleurFlexiblePrescient(A1)7,981526,221616,98211,5225 36OneBCIFlexibleOpportunity(A)5,273720,342815,6339,6864 TrueSCIFlexible(A)3,604316,523715,22410,6144 BCIFlexibleManaged(A)5,253826,601515,2058,65114 RCIBCIFlexible(A)11,44430,95914,7466,95193 SalvoPrimeDynamicFlexible(A1)6,432826,211714,487 BlueAlphaBCIAllSeasons(A)10,51717,213514,40810,5654 *AdviceworxOldMutualIn.+5-7%FoF(B1)7,471924,202113,8499,1974 AmplifySCIFlexibleEquity(B4)11,77333,56713,81108,01143 CohesiveCapitalFlexiblePrescient(A1)7,491841,38413,58118,9093 H4Managed(B1)10,89624,102213,5811 CorionPrimeFlexible(A)7,491821,122713,33128,69104

DATABANK PERSONAL FINANCE | 1 ST QUARTER 2022 60 NAME 3 MONTHS 1 YEAR3 YEARS5 YEARS PLEX. % RANK % RANK % RANK % RANK NAME 3 MONTHS 1 YEAR3 YEARS5 YEARS PLEX. % RANK % RANK % RANK % RANK

SIMIndustrial(R)6,20314,39418,8318,732 SatrixCappedIndiETF(A)16,47126,90115,5729,531 CoronationIndustrial(P)5,42420,16213,4636,083 MomentumIndustrial(A)6,98219,23313,3245,184

OldMutualFlexible(R)5,773228,951113,17139,686

LauriumFlexiblePrescient(A1)7,002123,262312,85149,1883

VisioBCIActinio(A)8,641131,27812,80158,36133

BaobabSCIFlexible(B1)2,004837,60512,5916

CSBCIFlexibleFoF(B)5,163914,873912,53177,96153

DestinyBCIMultiAssetFoF(A)6,992223,002412,45187,21173

GryphonFlexible(B)3,79427,694812,361910,8435

AutusPrimeOpportunity(A)9,431013,034212,09207,46163

CelerityCiGrowth(B)8,311322,332511,8921

MaitlandBCIFlexibleFoF(A)6,992218,543211,60228,59124

JBLSCIFlexibleFoF(B1)6,502617,303411,5923

CinnabarSCIFlexibleFoF(A)9,81822,132611,17247,13183

GlacierAIFlexibleFoF(B)5,543412,424310,8025

FlagshipIPFlexibleValue(A1)11,12554,98110,73266,17242

4DBCIFlexible(A)6,962316,74369,25276,24232

PSGFlexible(A)5,543436,2868,76286,2822

MethodicalBCIEquityPreserver(B1)5,313611,74458,2129

ClucasGrayFutureTitansPrescient(A1)9,48943,7138,15303,74292

DotportBCIFlexibleFoF(A)7,831620,10298,12316,04252

*IPFlexibleFoF(A)6,882414,43407,43324,70281

NoblePPBCIAllWeatherFoF(A)5,933112,17447,35335,31262

CitadelSAManagedVolatilityEquityH4(B1)6,253014,32417,02346,91212

*OasisCrescentIncome(A)2,08466,60496,89356,94202

*NoblePPBCIFlexible(A)2,05475,92506,47367,21173

KornerBCIFlexible(A)4,384019,71305,2937

PrescientOptimisedIncome(B1)0,77503,09524,64385,29271

MarriottPropertyEquity(R)7,511728,36121,41392,63301

PlexusWealthBCIFlexiblePropertyIncome(A)14,02150,852-1,3940

GranateSCIFlexible(A)8,451230,5710

TRGFlexiblePrescientFoF(A1)8,021426,9814

NewFundsVol.MngdHighGrowthEquityETF6,322925,5818

*InvestecW&IBCIProgressiveYield(A)6,512524,8419

AGCapitalValueFlexibleSNN8,311324,3020

InvestecSIBCIProtectedEquity(A)11,95218,7331

MarriottEssentialIncome(C)2,384517,4833

NewFundsVol.MngdModerateEquityETF5,653314,9338

Global&LocalSNNBalancedFoF(A)6,462711,4246

NewFundsVol.MngdDefensiveEquityETF3,19449,5147

WestbrookPrimeOpportunitiesFlexible(E)1,36494,9651

AboutirPrimeWorldwideFlexible(R)7,4120

*FNBDefensiveFoF(A)5,4735

HIGH-EQUITY FUNDS

EmperorIPBalanced(A)7,259815,6217018,661

*HighStreetHighEquityPrescient(A1)9,342719,7411918,342

*LongBeachManagedPrescient(A1)4,8415915,9716518,34214,3115

FairtreeBalancedPrescient(A1)8,723616,2916218,013

*SouthernCharterBCIGrowthFoF(A)10,82628,70817,12410,8445

AylettBalancedPrescient(A1)10,93540,66116,83512,4525

*CentaurBCIBalanced(A)4,9515624,762515,51610,28115

PPSManaged(A2)5,7714521,317915,397

*SIMManagedAggressiveFoF(A1)7,508525,302115,25810,31104

DiscoveryAgg.DynmcAssetOptimiserFoF(A)10,461124,063315,1399,80185

*NedgroupInv.Managed(R)4,3316522,874715,13910,2112

KagisoIslamicBalanced(A)7,508527,071414,841010,7365

*AccornBCIBalancedFoF(C)7,289525,821714,53119,00374

AFInvestmentsAggressivePassive(A1)11,46223,574114,491210,7955

*ADBBCIFlexiblePrudentialFoF(A)7,359222,056514,47139,42274

*PrescientWealthBalancedFoF(A1)10,151623,124514,43149,65215

*SIMManagedModerateAggressiveFoF(A1)7,379123,953414,401510,07135

*NedgroupInv.Balanced(A)3,6316916,1316314,40159,51234

*CoronationBalancedPlus(A)7,309421,487714,25169,49244

*SanlamM-MAggressiveFoF(A1)8,624322,645414,18179,86174

*KagisoBalanced(A)7,279622,136313,911810,5884

ObsidianSCIBalanced(B1)4,2016722,385713,88199,01364

*NinetyOneOpportunity(R)8,703718,1214813,79209,6521

*FlagshipIPBalanced(A)5,5414817,0515813,77219,00374

*BCIPrudentialFoF(3B1)6,9810523,733813,74228,46563

CoreSharesOUTmoderateIndex(O)11,46228,421013,6923

KrugerCiBalanced(A)7,816820,1610913,5624

*BlueAlphaBCIBalanced(C)11,01429,63713,5125

*OldMutualM-MAggressiveBalancedFoF(A)7,538224,382913,47268,89414

*H4Diversied(B1)10,74822,515513,422710,3995

*StanlibM-MShar'iahBalancedFoF(B1)8,733525,621813,41289,4626

*PrescientBalanced(A2)8,634221,148213,412810,6074

*SygniaSkeletonBalanced70(A)6,8211018,6213513,39299,78195

CordatusBalancedPrescient(A1)7,329326,601513,33309,2532

*4DBCIModerateFoF(A)7,906422,335913,33308,65494

*AdviceworxOldMutualIn.+4-5%FoF(B1)7,0910322,266013,27318,99384

*SygniaCPI+6%(D)7,269720,0311313,26329,06344

*MultiAssetIPBalancedPlus(B1)7,597819,7911713,24339,54224

*StanlibM-MBalanced(B1)6,7811222,735213,23349,38294

*SBROBCIManagedFoF(A)6,6211620,3910413,18358,68483

*ChromeCiGrowth(A)9,262920,5410013,1336

*RowanCapitalBCIBalancedFoF(A)6,3312919,0413013,12379,47254

*OldMutualM-MBalancedFoF(A)7,189922,755013,08388,69473

SatrixBalancedIndex(A1)8,355225,052313,033910,0713

SanlamM-MBalancedFoF(A2)4,9715520,639613,03398,55553

DenkerSCIBalanced(A)7,419025,571912,9940

*WarwickBCIBalanced(B)6,3512817,7015112,99408,27614

NedgroupInv.CoreDiversied(B)7,627623,684012,98419,33304

*PPSBalancedFoF(A2)7,816824,283112,96429,2233

*NedgroupInv.CoreAccelerated(B)8,703727,171312,9343

FNBGrowthFoF(B1)9,771822,954612,88448,12673

*RoxburghCiBalancedPlusFoF(A)8,035820,828812,88448,76463

*CeltisBCIManagedFoF(A)6,2313518,2414612,87458,78454

*PersonalTrustManaged(A)9,352622,505612,86468,86424

*FGSCINeptuneGrowthFoF(A)6,2813219,5212212,82479,30314

*CSBCIAggressivePrudentialFoF(B)5,1415314,9017412,77488,03693

AutusPrimeDiversied(A)9,572119,7811812,7449

*WealthAssociatesBCIBalancedFoF(A)7,538221,587312,73509,87164

*NinetyOneManaged(R)2,2917215,0617212,71519,9115

*AbsaM-MPassiveGrowth(B)9,721921,836712,6352

*SanlamM-MModerateAggressiveFoF(A1)6,6311520,679312,63528,60533

*BovestBCIManagedFoF(A)7,1710019,5612012,62538,40583

*APSCiManagedGrowth(A1)10,421220,569812,61547,59813

*FALBCIBalanced(A)11,03327,921112,60557,30933

*RSABCIBalanced(A)9,153119,0013112,5956

*ImaliBCIPassiveBalanced(A)9,482320,559912,5857

*HollardPrimeStrategicAssertiveFoF(B)9,442422,824912,57588,94394

*NFBCiManaged(A)8,205420,2110712,41599,93144

*AutusPrimeBalanced(A)10,75713,5518212,33607,36903

*Point3BCIBalancedFoF(A)10,501018,3714312,25618,64503

*AssetMixCiBalanced(A)7,518420,1810812,23628,15663

*GravitonSCIBalanced(A1)7,906420,799012,22638,30603

*StanlibM-MMedium-HighEquityFoF(B1)6,7911122,096412,21648,82443

*GryphonPrudential(B)3,891687,9318712,196510,9335

*StanlibBalanced(R)6,5412015,8316812,16668,2364

NFBCiManagedGrowthFoF(A)7,846719,5312112,1367

*PersonalTrustPrudentFoF(A)7,647523,823712,09688,61523

AFInvestmentsPerformerManaged(A)6,3213020,669412,07698,63513

*MethodicalBCIBalanced(A)7,289518,2914512,05708,06683

*IPActiveBeta(A)8,434916,3216112,04718,89414

PPSBalancedIndexTracker(A2)8,425023,823712,02728,4457

*DiscoveryBalanced(A)7,896521,028512,00738,78453

*PBiBCIBalancedFoF(A)6,8510921,437811,95748,44573

*TrésorSCIBalanced(B1)9,891721,278011,94757,91733

*OldMutualBalanced(R)6,5312123,843611,84768,9240

*ClucasGrayEquilibriumPrescient(A1)6,9310728,60911,79779,70204

DATABANK PERSONAL FINANCE | 1 ST QUARTER 2022 61 NAME 3 MONTHS 1 YEAR3 YEARS5 YEARS PLEX. % RANK % RANK % RANK % RANK NAME 3 MONTHS 1 YEAR3 YEARS5 YEARS PLEX. % RANK % RANK % RANK % RANK

*IDCapitalBCIBalancedFoF(A)7,926314,5817811,7878

*M&GBalanced(A)7,478725,472011,76798,57543

*OldMutualCoreBalanced(A)8,265323,484211,68808,32593

*CelerityCiBalanced(B)7,1710020,659511,5881

*FoordBalanced(A)4,7116115,3317111,58817,39883

SageSCILongTermSolutionFoF(A2)5,9614318,0114911,56828,25633

*SimplisitiBCIManagedProtectorFoF(A)7,1110217,3315511,54837,78763

*ASForumBCIAggressiveFoF(A)7,607718,7913311,51847,64793

27fourAssetSelectFoF(A1)8,683820,639611,44857,76773

AbsaM-MCoreGrowth(C)7,478719,4312311,4386

*SasnBCIPrudential(A1)9,362515,9216611,34878,84434

*DetonPrimeManagedFoF(A)10,361420,988611,32888,26623

*RedOakBCIBalanced(A)5,4614916,0716411,31897,92723

*SanlamM-MModerateFoF(A1)6,0614217,4715311,30908,19653

*StelburgBCIBalancedFoF(A)9,093222,515511,2891

*MatrixSCIBalanced(B1)4,6816222,745111,2692

GraySwanSCIAggressiveFoF(A)9,282824,802411,2293

*PrivateClientBCIHighEquity(B)7,1610120,1511011,20947,9870

OasisCrescentBalancedHighEquityFoF(D)8,743421,806911,17957,42853

*LynxPrimeBalancedFoF(A1)6,4912322,844811,13967,4087

MomentumTarget7FoF(A)7,428922,375811,1197

*IPPrudentialEquity(A)7,518415,8716711,10987,82753

*1nvestHighEquityPassiveBalancedFoF(A)8,375124,303011,08997,13992

*SelectBCIBalanced(A)8,355215,8716711,08997,29942

*MooreCiGrowthFoF(A)8,105719,2412711,071007,25953

*OptimumBCIManagedGrowth(C)7,687420,4010311,06101

*AnchorBCIManaged(A)6,1713918,6013611,051027,061032

SentioSCIHikmaShariahBalanced(B1)7,468821,976611,011037,46843

*AbsaM-MGrowthFoF(A)8,494519,3312510,991046,961052

*PFPSCiBalancedFoF(A)9,692019,9111410,961057,97713

*InvesthouseCiBalanced(A)7,587918,3814210,94106

*CitadelBalancedH4(B1)10,60919,8711510,921077,90743

*PSGWealthModerateFoF(A)6,5312121,687110,851087,3491

*SequoiaBCIManagedGrowthFoF(A)8,654021,088410,82109

*AbsaPrudentialFoF(A)6,5911818,4913810,781107,48833

*ElementIslamicBalancedSCI(A)6,4012520,689210,761119,04354

*NorthstarSCIManaged(A1)6,0914118,3814210,751127,31923

*FALBCIBalancedFoF(A)5,2515213,8518110,741137,101002

*CSBCIPrudentialFoF(B)3,4817012,5718510,721147,63803

MomentumTarget6FoF(A)7,1110220,799010,67115

*CinnabarSCIBalancedPlusFoF(A)8,663920,0911210,671157,25952

*QuattroCiGrowthFoF(A)7,0410420,4610110,591166,721112

*AmityBCIManagedSelectFoF(A)7,498621,507510,581177,46842

*MedianBCIBalancedFoF(A)6,3912620,818910,581176,971042

*RebalanceBCIBalancedFoF(A)6,2913118,5313710,571186,871062

*27fourShariahBalancedFoF(A1)7,747119,4212410,561197,38893

*MomentumFocus7FoF(A)8,375122,715310,511206,841072

*FinancialFitnessIPBalancedFoF(A)6,1913713,3818310,501219,04354

*WealthworksPrimeManagedFoF(A)6,5711920,1511010,491227,50823

*AnalyticsCiBalancedFoF(A)9,442419,1212810,471237,13992

SentioSCIBalanced(B2)6,8710820,569810,45124

AnchorBCIDiversiedGrowth(A)7,528321,757010,431257,69783

*MomentumFocus6FoF(A)7,796921,248110,39126

*SignatureBCIBalancedFoF(A)6,1014020,4110210,331277,41863

PerspectiveBalancedPrescient(A1)4,4316433,55310,30128

*OasisBalancedUnitTrust(D)8,175522,176210,251296,791082

*PWSBCIModerateFoF(A)6,1813818,2114710,18130

*PSGBalanced(A)7,717335,32210,161317,2296

*PrescientAbsoluteBalanced(A2)7,876618,9713210,161317,82753

*CorionPrimeGrowth(A)8,454823,693910,111327,091012

*SeedBalancedPrescient(A1)8,474718,7013410,081337,18982

PerpetuaSCIBalanced(A)6,6111723,434310,011346,331162

SanlamPrivateWealthBalancedFund7,777018,3814210,011347,38892

OctagonSCIGrowthFoF(B1)5,6014717,7815010,001356,701122

*WellsFaberSCIBalancedFoF(A)6,5012214,591779,99136

*AssetbaseCPI+6%PrescientFoF(A1)9,203021,09839,981377,19972

*AllanGrayBalanced(A)5,0715420,251069,941387,40872

*SelectManagerBCIBalancedFoF(A)8,025920,141119,931396,841072

*JBLSCIManagedFoF(B1)6,2713316,741599,87140

*SIMBalanced(R)6,5012218,431409,731416,76110

*BCIBestBlendBalanced(C)6,7911120,55999,661426,451152

*AllanGrayTax-FreeBalanced(A)4,9015819,001319,631437,36902

*CapitaBCIBalanced(A)6,3612720,61979,571446,131171

*SAAssetManagementBCIManaged(A)8,644115,791699,571444,451291

*AureusNobilisBCIManaged(A)6,2013617,781509,351456,061182

PrimeShirazPrudentialAggressiveFoF(A)7,329323,94359,291465,851192

*AbsaManaged(A)4,8116024,56289,251476,681132

NewFundsMappsGrowthETF6,4012514,611769,131487,08102

*SkyblueBCICumulusModerateFoF(A)6,2513418,391419,091495,731221

*AshburtonBalanced(A)8,614417,161569,041506,611141

*ElementBalancedSCI(A)6,9410623,18448,701519,39283

AFInvestmentsRealReturnFocus(A)5,2815119,061298,551527,061032

*AfFinityCiGrowth(A)7,946216,071648,191536,781092

*CaleoBCIBalancedFoF(A)6,2013617,151577,751545,111261

*CustodianIMBCIBalanced(A)7,966116,661607,581555,251251

*CounterpointSCIBalancedPlus(A1)7,518415,021737,541566,331162

*BrenthurstBCIBalancedFoF(A)5,8014417,421547,53157

*CadizBCIBalanced(A)6,5312118,481397,411585,481231

*DotportBCIPrudentialFoF(A)6,8710817,491527,411585,811201

*RezcoValueTrend(A)0,21174-1,981906,841595,071271

*RezcoManagedPlus(A)-0,05175-2,741916,821604,931281

*NoblePPBCIWealthCreatorFoF(A)4,241669,241866,771615,281242

*MarriottBalancedFoF(A)4,9415712,631846,731625,751212

NMRQLSCIBalanced(A)4,5316314,741756,05163

*KanaanBCIBalancedFoF(A)2,891717,781885,881644,251301

*AmpersandSCICPIPlus6FoF(A)10,231519,801164,061653,131311

*PlexusWealthBCIBalanced(A)6,1713921,82683,791662,811321

*CounterpointSCIManagedP&G(A)5,3415033,5342,841671,841331

*VisioBCISABalanced(A)7,796933,415

PSGM-MGrowthFoF(D)4,9515629,666

*GranateSCIBalanced(B)7,548127,7512

*PMKManagedPrescientFoF(A3)7,906426,1616

*SelectBCIEnhancedCoreBalanced(A)10,391325,2822

CoreSharesWealthAccumulation(A)9,572124,7326

*10XHighEquityIndex(A)9,552224,6927

*InvestecW&IBCIDiversiedGrowthFoF(A)8,145624,0732

*VisioBCIBalanced(A)8,484623,6840

*WeaverBCIBalancedFoF(A)8,783322,1961

*PortfolioMetrixBCIBalancedFoF(A)7,0410421,6772

*AmplifySCIBalanced(A1)6,7811221,5274

*OysterCatcherRealFinBalanced(A)6,6411421,4976

*TRGBalancedPrescientFoF(A1)6,4312420,8887

SynergyCiGrowthFoF(A)8,634220,7191

*FairtreeInvestStrategicFactorPrescient(A1)9,352620,26105

*FisherDugmoreCiBalanced(A)7,976019,28126

*NewRoadBCIManagedFoF(A)7,269718,34144

NgwediGlobalBalancedSNN(R1)6,2813214,23179

TSBBalanced27four(A1)6,0614213,89180

*StarPrimeBalanced(C)2,271737,38189

*CelerityCiDiversied(A)13,021

*AluwaniBCIBalanced(A)7,7372

FNBCoreBalanced(A)7,5780

GradidgeMahuraCiGrowth(A)6,72113

*FNBMultiManagerBalanced(A2)5,62146

INCOME FUNDS

CoreSharesPreftraxETF17,32143,74113,66110,941

SaronSCIActiveBond(A)2,62119,02119,7129,2145

*SasnBCIFlexibleIncome(A)2,33248,68129,56310,3325

*VisioBCIUnconstrainedFixedInterest(B)2,521210,2659,3748,58105

DATABANK PERSONAL FINANCE | 1 ST QUARTER 2022 62 NAME 3 MONTHS 1 YEAR3 YEARS5 YEARS PLEX. % RANK % RANK % RANK % RANK NAME 3 MONTHS 1 YEAR3 YEARS5 YEARS PLEX. % RANK % RANK % RANK % RANK

*Mi-PlanIPEnhancedIncome(A1)2,08317,97209,2259,6135

*ThymeWealthIPMultiAssetIncome(A)1,72538,18188,896

AbsaTacticalIncome(A)2,43187,77228,847

GranateSCIMultiIncome(B)2,14277,51258,7488,8965

*AmplifySCIStrategicIncome(A1)1,91408,59138,5898,6884

*AshburtonDiversiedIncome(B)3,4849,7768,5110

*PSGDiversiedIncome(A)2,43189,6978,23117,9712

*StanlibFlexibleIncome(B1)2,45167,09338,10127,25304

*SaronSCIOpportunityIncome(A)1,34797,02357,98138,9455

BCIIncomePlus(C)1,81457,23327,97148,8574

*NorthstarSCIIncome(A1)2,41206,13647,91157,64204

MarriottCoreIncome(A)1,53674,06937,69167,97124

AbsaFlexibleIncome(A1)1,58635,58787,64177,88144

MarriottHighIncomeFoF(A)1,52683,88947,63187,83154

FairtreeFlexibleIncomePlusPrescient(A1)1,55656,93367,59198,6294

AmpersandSCIIncome(A)1,63606,84397,5620

*NedgroupInv.FlexibleIncome(A)2,24258,24157,54217,7717

TrésorSCIIncome(B1)2,63107,53247,54217,61224

*SelectManagerBCIIncomeFoF(C)1,79476,55477,32227,58233

*FNBIncomeFoF(B1)2,40217,92217,26237,15363

CustodianIMBCIIncomePlus(A)1,50705,48817,24248,12114

*SimplisitiBCIIncomePlusFoF(A)1,75506,93367,21257,44263

HarvardHouseBCIFlexibleIncome(A)2,7089,02117,20266,13493

MomentumIncomePlus(A)1,37775,76747,15277,94134

*NovareCapitalPreserverFoF(A1)1,80466,71447,14287,38283

*OptimumBCIIncome(A)1,51696,16637,1329

*BCIBestBlendFlexibleIncome(C)1,67566,53497,12307,67184

*CadizBCIAbsoluteYield(A)1,94376,78427,01317,77173

*StanlibM-MAbsoluteIncome(B1)2,21267,49266,98327,66193

*GravitonSCIFlexibleIncome(A1)2,12296,86386,92337,33293

*PrescientIncomeProvider(A2)2,36237,07346,91347,62213

*AnchorBCIFlexibleIncome(A)1,54665,53806,91347,04393

SalvoPrimeDynamicIncome(A1)1,61616,39586,8935

*CounterpointSCIEnhancedIncome(A1)2,47157,31306,84367,79163

*AutusPrimeIncomePlus(A)1,90415,03886,84367,22333

PrimeFlexibleIncome(A)1,74516,48516,8337

*MomentumDiversiedIncome(B1)1,92396,20626,80387,41273

OctagonSCIFlexibleIncomeFoF(B1)1,91406,79416,7839

*PersonalTrustIncome(A)1,77495,85726,77407,13372

*MethodicalBCIIncome(B1)1,96366,44556,7341

SelectBCIFixedIncome(A)1,56645,29826,73416,48443

*PortfolioMetrixBCIIncome(A)1,65586,82406,71427,54243

*27fourShariahIncome(A1)1,86425,27836,7142

MarriottIncome(R)1,34794,09926,71427,23322

*PrescientSAIncomeProvider(A2)2,38228,23166,63437,53253

*HollardPrimeDynamicIncome(B)1,85436,43566,61447,24313

*RowanCapitalBCIIncomeFoF(A)1,78486,45546,59457,13372

AFInvestmentsEnhancedIncome(A)0,89864,84906,59457,44263

PPSFlexibleIncome(A2)2,10306,75436,57467,2530

*CadizBCIEnhancedIncome(C)1,49715,61776,56477,17352

*NinetyOneDiversiedIncome(A)1,58636,16636,53487,3329

*CoronationStrategicIncome(A)1,91406,67456,52497,21343

*CaleoBCIActiveIncome(A)3,3857,76236,45507,21343

*CinnabarSCIIncomeFoF(A)1,60625,94696,45506,76422

*OldMutualM-MEnhancedIncomeFoF(A)1,22835,19856,34516,91412

AFInvestmentsInationLinkedBond(A)5,16315,1826,33524,23552

*FGSCIJupiterIncomeFoF(A)0,60905,68756,33526,95402

*InvestecW&IBCIActiveIncomeFoF(A)1,67565,83736,3253

*DotportBCIIncome(A)1,05844,22916,3253

*DiscoveryDiversiedIncome(A)1,53676,00676,29547,05382

AbsaM-MIncome(C)1,32815,03886,1755

MomentumInationLinkedBond(A)5,17215,0736,12564,03572

*M&GEnhancedIncome(A)2,03336,36596,06576,20482

*SIMSAActiveIncome(A1)1,36785,20846,05586,75432

*SeedIncome(A1)1,83446,54485,91596,29462

*PSGWealthIncomeFoF(A)1,69545,86715,90606,2847

IFMIncome(E)1,64596,29615,3761

*CapitaBCIRealIncome(A)1,40745,55795,35626,39452

SasnBCIOptimalIncome(A)1,43734,91895,27635,55501

InvestecSIBCIEnhancedIncome(A)0,82872,99965,0464

MomentumOptimalYield(A)1,39755,06865,02656,28471

SanlamDiversiedIncomeFoF(A3)0,99853,48954,67665,2951

SouthchesterIPOptimumIncome(A)0,72882,64984,45675,17531

*ElementSpecialistIncomeSCI(A)2,05327,37294,39685,21521

*NinetyOneAbsoluteBalanced(A)1,33805,04874,02694,0856

SanlamAlternativeIncome(A1)0,66892,68973,96704,5554

*KagisoIslamicHighYield(A)2,491310,314

*OldMutualAlbarakaIncome(A)2,48149,688

*IntellivestBCIIncome(B)2,6799,459

*PortfoliometrixBCIDynamicIncome(A)2,42199,4310

*ArgonBCIFlexibleIncome(A)3,0068,5114

*10XDefensiveIndex(A)2,7978,2316

PSGM-MMulti-AssetIncomeFoF(D)1,85438,2017

CorionPrimeIncome(A)2,13288,0519

*FinancialFitnessDiversiedIncomeIPFoF(A)1,85437,4427

*NgwediActiveIncomeSNN(R1)1,72537,4228

PrescientIncomePlus(A2)2,12297,2831

*SygniaEnhancedIncome(A)1,66576,9037

*NewRoadBCIIncomeFoF(A)1,93386,6246

LauriumIncomePrescient(A1)1,98356,5050

*RebalanceBCIRealIncome(A)1,68556,4851

*QuantumBCIIncome(C)1,68556,4752

MomentumFlexibleIncome(A)1,92396,4653

*TRGIncomePrescientFoF(A1)1,99346,4257

OakhavenSNNCoreIncome(A2)2,10306,3060

*SequoiaBCIFlexibleIncome(A)1,58636,1265

*PWSBCIFlexibleIncome(A)1,64596,0766

*PMKIncomePrescientFoF(B4)1,73525,9668

*FisherDugmoreCiDiversiedIncome(A)1,47725,9469

*Delta4BCIIncome(A)1,38765,8770

DalebrookBCIIncome(A1)1,47725,6875

*TantalumBCIStrategicIncome(A)1,68555,6376

*WealthAssociatesBCIIncome(A)1,31825,4881

*FNBMultiManagerIncome(B1)2,4417

*AluwaniBCIFlexibleIncome(A)1,9140

LOW-EQUITY FUNDS

*AbsaSmartAlphaDefensive(A)6,731217,481312,791

*SouthernCharterBCIDefensiveFoF(A)7,40419,281012,0028,41204

*AmplifySCIWealthProtector(B5)2,5212412,928812,0029,7325

*SelectBCICautious(A)5,345511,8110911,85310,0915

*StanlibBalancedCautious(B1)5,116413,038611,5947,99304

*MontroseBCICautiousFoF(A)6,302315,563911,5258,76124

*DiscoveryCons.DynmcAssetOptmsrFoF(A)6,401915,963111,4969,0395

*MultiAssetIPBalancedDefensive(B1)6,102914,825211,4379,0685

*SIMManagedCautiousFoF(A1)5,963317,971211,3088,66144

*SygniaSkeletonBalanced40(A)4,897213,357611,1599,2375

KrugerCiPrudential(A)5,604616,142711,1010

*PersonalTrustConservativeManaged(A)6,95917,341410,96118,36214

*H4Stable(B1)7,55216,092910,96119,4265

*AmplifySCIDefensiveBalanced(A1)4,459116,332210,81129,4455

*AdviceworxOldMutualIn.+2-3%FoF(B1)5,196015,464210,80138,31224

*FinancialFitnessIPStableFoF(A)5,684212,489710,73149,6035

*NedgroupInv.CoreGuarded(B)5,305716,502110,72158,67135

FNBStableFoF(B1)6,162615,124810,72158,14294

*NedgroupInv.Stable(A)3,931078,7613610,68168,2923

PPSConservativeFoF(A2)5,983215,514110,62178,8511

*StanlibM-MLowEquityFoF(B1)4,758015,534010,54188,49184

CoreSharesOUTcautiousIndex(O)7,06718,431110,5219

DATABANK PERSONAL FINANCE | 1 ST QUARTER 2022 63 NAME 3 MONTHS 1 YEAR3 YEARS5 YEARS PLEX. % RANK % RANK % RANK % RANK NAME 3 MONTHS 1 YEAR3 YEARS5 YEARS PLEX. % RANK % RANK % RANK % RANK

*NinetyOneCautiousManaged(A)5,335611,9610610,51208,5716

*OldMutualCoreConservative(A)5,534815,983010,4721

*SatrixLowEquityBalancedIndex(A1)6,003116,731810,46228,1727

*RoxburghCiConservativeFoF(A)5,873714,345910,46228,19254

AFInvestmentsConservativePassive(A1)7,40415,873210,42238,41204

*SasnBCIStable(A)6,312219,72810,38249,5245

*AutusPrimeStable(A)5,81388,6313710,31257,33513

*BCIStableFoFClass3B16,162617,251510,25267,94314

*FALBCIStableFoF(A)4,917112,838910,20277,86344

*SanlamM-MCautiousFoF(A1)4,0110613,337710,18288,31224

*27fourStableFoF(A1)6,821114,825210,17298,29234

PPSDefensive(A2)6,98819,89510,1530

*TrésorSCIStable(B1)5,923413,95699,99317,10593

*KagisoStable(A)6,132723,1329,98328,93104

*HollardPrimeStrategicDefensiveFoF(B)6,282416,13289,92338,21244

*OldMutualM-MCautiousFoF(A)4,459113,49749,92337,62413

*StanlibM-MDefensiveBalanced(B1)4,956915,29469,90347,65393

*OptimumBCIStable(C)5,395214,07669,8835

*4DBCICautiousFoF(A)5,355413,08849,88357,66383

*OasisBalancedStableFoF(D)8,56122,9239,81366,64743

*APSCiCautious(A1)7,35514,94519,78377,22553

*CeltisBCIConservativeFoF(A)3,6611411,411189,77387,72374

*LynxPrimeCautiousFoF(A1)4,857516,17259,76397,8733

*CorionPrimeStable(A)5,674315,78349,75408,18264

*FGSCIVenusCautiousFoF(A)4,518912,73929,71417,75364

*DinamikaBCIConservativeFoF(A)4,996716,59209,69426,80683

*DiscoveryCautiousBalanced(A)5,484913,16819,64438,51174

*NFBCiStable(A)5,205913,47759,61448,59154

PrescientDefensive(A2)6,431817,48139,6045

*CoronationBalancedDefensive(A)4,688312,69949,50467,61423

*SBROBCIDefensiveFoF(A)3,7811110,651279,49477,65394

*StelburgBCICautiousFoF(A)6,073015,32459,4648

*SanlamM-MDefensiveFoF(A2)3,0012011,451169,46487,64403

*GravitonSCILowEquity(A1)4,578612,46989,44497,55443

GraySwanSCICautiousFoF(A)6,132716,85179,4250

*BCIBestBlendCautious(C)4,927014,39589,36517,17563

*WealthworksPrimeCautiousFoF(A)4,797815,23479,31527,42473

OctagonSCICautiousFoF(B1)4,189912,77919,31527,29543

*BCIIncomeProvider(A)3,5211612,92889,25536,99613

*PFPSCiCautiousFoF(A)6,921014,19649,21547,75363

*WealthAssociatesBCICautiousFoF(A)4,409413,25789,19558,48194

*BovestBCIConservativeFoF(A)4,0110611,961069,14566,57763

PrimeCabernetStableFoF(A)5,534815,05509,13577,12583

*AnchorBCIDiversiedStable(A)4,867414,25619,13577,82353

*PrivateClientBCILowEquity(B)5,205913,19809,12587,5145

*SIMIn.+(A)4,668412,92889,08597,60433

*SequoiaBCIStableFoF(A)6,322115,76359,0760

*OldMutualStableGrowth(A)3,8610816,88169,01617,90323

*OasisCrescentBalancedStableFoF(D)6,521616,18249,01616,57763

*CelerityCiConservative(B)5,644412,92889,0062

*ASForumBCICautiousFoF(A)5,584714,29608,98637,17563

*SygniaCPI+2%(D)4,0410511,851088,98637,35503

*NFBCiDefensiveFoF(A)5,783913,91708,9764

*AssetMixCiConservative(A)5,764113,47758,97646,97623

*AmityBCISteadyGrowth(A)4,1010212,091048,96656,99613

*AureusNobilisBCICautious(A)4,449213,00878,94666,87653

AutusPrimeCautious(A)7,55212,211038,9167

AbsaM-MPassivePreserver(A)5,614512,271018,7868

MomentumTarget3FoF(A)4,966814,67548,7769

*PBiBCIConservativeFoF(A)4,339612,55968,76707,37493

*InvesthouseCiCautious(A)5,883613,78738,6971

*MomentumFocus3FoF(A)5,873715,72368,65726,33812

SageSCIProtectionSolutionFoF(A2)5,126314,21638,63736,73702

*CinnabarSCIStableFoF(A)5,385312,78908,63737,31533

*MooreCiStableFoF(A)5,385313,15828,62746,82672

*AssetbaseCPI+2%PrescientFoF(A1)5,076511,491158,60758,15284

*PlatinumBCIIncomeProviderFoF(A)3,8011010,721268,56767,08603

*WellsFaberSCIStableFoF(A)5,295814,19648,5577

*QuattroCiCautiousFoF(A)4,558810,961238,53786,65732

*AnalyticsCiCautiousFoF(A)6,561513,82718,47796,85662

*AbsaM-MPreserverFoF(A)4,887311,751118,44806,38802

*Mi-PlanIPIn.+3(B5)4,738110,611298,39817,31533

*MethodicalBCIStable(A)4,738111,441178,38826,93642

*Point3BCIConservativeFoF(A)6,003111,671128,33837,40483

*SelectManagerBCICautiousFoF(A)5,405114,22628,32846,48792

*M&GIn.+(A)6,401920,1848,27855,86922

DenkerSCISAStable(A)4,738111,991058,2785

*AllanGrayStable(A)3,7711215,08498,24867,40483

*RebalanceBCICautiousFoF(A)3,7311311,631138,23876,38802

LauriumStablePrescient(A1)-2,341329,741338,2387

*DynastyCiWealthPreserver(A2)7,20613,06858,20887,32523

*ABAXSAAbsolutePrescient(A1)4,349512,331008,1989

Ginsburg&SelbySCIStableFoF(A1)3,211199,051358,1590

NewFundsMappsProtectETF5,176113,22798,14916,2983

*SIMManagedConservativeFoF(A1)3,8510910,891248,13927,14573

ConstellationProtectedGrowthPrescient(A1)4,0510410,321318,0993

*1nvestLowEquityPassiveBalancedFoF(A)5,774016,15268,07944,851001

*IPDiversiedIncomeFoF(A)4,51899,871328,07946,70713

*PSGWealthPreserverFoF(A)4,817714,50578,01956,2884

*PWSBCICautiousFoF(A)3,6611411,071228,0096

*QuantumBCICapitalPlusFoF(A)4,259812,42997,96976,32822

*AfFinityCiCautious(A)5,305711,951077,96976,70712

*SignatureBCIStableFoF(A)4,1110113,11837,88986,67722

*CadizBCIStable(A)4,0810311,781107,88986,77692

*CapitaBCICautious(A)4,479014,62557,86996,23872

AbsaM-MCorePreserver(C)4,1610010,961237,8699

*AFInvestmentsStableFoF(A)4,429310,871257,831006,56772

*SanlamM-MConservativeFoF(A1)2,831228,621387,801017,45463

*EdgeBCICautiousFoF(A)4,917114,01687,791026,14892

AbsaInationBeater(A)2,001286,461447,651037,99304

*BrenthurstBCICautiousFoF(A)4,777910,631287,591046,27852

*ArgonBCIAbsoluteReturn(A)5,355412,65957,491056,17882

*PSGStable(A)4,1610019,7877,391066,5478

*SeedStablePrescient(A1)6,102913,80727,381075,17971

*SAAssetManagementBCICautious(A)5,584710,371307,301085,61942

*ElementRealIncomeSCI(A)4,708215,08497,181096,94632

*CounterpointSCICautious(A1)5,475011,631137,101106,25862

*OldMutualCapitalBuilder(A)3,541158,101396,631115,94912

*AbsaAbsolute(A)2,6012311,581146,581125,58952

*AshburtonTargetedReturn(B4)6,591415,36436,371135,05981

*OldMutualRealIncome(A)2,471268,021406,181146,60752

*DotportBCICautiousFoF(A)4,658511,341196,161155,64931

*NoblePPBCIStrategicIncomeFoF(A)2,901217,551415,921166,07902

*RezcoStable(A)-0,82131-2,721475,851175,47961

*SkyblueBCIKimberliteCautiousFoF(A)3,8610811,281205,611184,131011

*StewartBCIAbsoluteReturnBlendFoF(A)2,501256,291455,371195,01991

MFSSCICautiousFoF(B1)6,112813,22795,34120

*AmpersandSCICPIPlus2FoF(A)6,332014,16653,871213,831021

*CounterpointSCIStableP&G(A)5,684228,3313,691223,001031

*PlexusWealthBCIConservative(A)5,006615,34443,151232,991041

AllanGrayOptimal(A)-0,691306,691431,581242,811051

*OysterCatcherRealFinStable(A)5,345519,886

PSGM-MCautiousFoF(D)3,2411819,319

*SelectBCIEnhancedCoreCautious(A)6,661316,7219

*PMKStablePrescientFoF(A3)5,166216,3123

*InstitBCIManaged(A)5,205915,8633

SynergyCiConservativeFoF(A)6,481715,6537

CoreSharesStableIncome(A)7,49315,6138

*10XLowEquityIndex(A)5,534814,7753

*WeaverBCIStableFoF(A)5,913514,6156

DATABANK PERSONAL FINANCE | 1 ST QUARTER 2022 64 NAME 3 MONTHS 1 YEAR3 YEARS5 YEARS PLEX. % RANK % RANK % RANK % RANK NAME 3 MONTHS 1 YEAR3 YEARS5 YEARS PLEX. % RANK % RANK % RANK % RANK

*PortfolioMetrixBCICautiousFoF(A)4,568714,0667

MianzoCPI+3%27four(A1)4,1110113,0087

*NewRoadBCIStableFoF(A)4,837612,7093

*RSABCICautious(C)6,192512,22102

*TRGStablePrescientFoF(A1)3,5011711,25121

NgwediAbsoluteReturnSNN(R1)2,011279,30134

*StarPrimeStable(C)1,901297,18142

*SteerSNNStableClass14,28975,12146

*GradidgeMahuraCiCautious(A)4,8376

MEDIUM-EQUITY FUNDS

*SouthernCharterBCIBalancedFoF(A)8,89823,29315,63110,3715

*DiscoveryMod.DynmcAssetOptmsrFoF(A)8,691021,32814,1129,9545

*NedgroupInv.Opportunity(A)11,44131,18114,0338,25224

*MontroseBCIModerateFoF(A)8,211519,881813,4149,16105

*ADBBCIBalancedFoF(A)7,133220,771013,2158,90114

*SIMManagedModerateFoF(A1)6,814321,62713,0069,4574

*AeonBalancedPrescient(A1)6,644720,181512,9379,9835

*StanlibM-MRealReturn(B1)6,834220,251412,8489,3985

*SygniaSkeletonBalanced60(A)6,295716,846112,5799,7155

*ChromeCiModerate(A)8,141619,852012,4110

KagisoProtector(A)5,357620,621112,241110,0724

*MultiAssetIPBalanced(B1)6,844117,924312,23129,3295

CoreSharesOUTstableIndex(O)9,48323,05412,1913

FNBModerateFoF(B1)8,351319,871912,13148,34194

*SasnBCIBalanced(A)7,832316,046812,10159,4965

*RoxburghCiBalancedFoF(A)7,263018,123712,08168,71144

*SygniaCPI+4%(D)6,305617,275512,05178,60164

*StanlibM-MMediumEquityFoF(B1)5,896619,732211,99188,61154

*AdviceworxOldMutualIn.+3-4%FoF(B1)5,946517,964211,90198,49174

*FGSCISaturnModerateFundsofFunds(A)5,537417,694611,82208,15243

*HollardPrimeStrategicBalancedFoF(B)8,111720,031711,77218,88124

*FosterBCIModerateFoF(A)6,086118,153611,73228,15244

*OldMutualM-MDefensiveFoF(A)5,826817,994111,72238,28214

*APSCiModerate(A1)9,10518,513311,59247,59343

*GravitonSCIMediumEquity(A1)7,292917,595011,57257,97283

PPSModerateFoF(A2)5,946517,125811,57258,7713

*DetonPrimeBalancedFoFClassZ9,43419,442411,4926

*MelvilleDouglasStanlibMediumEqtyFoF(A)6,016317,814411,38278,40183

*PlatinumBCIBalancedFoF(A)5,647015,287711,37288,09254

*WealthAssociatesBCIModerateFoF(A)6,305618,004011,32299,4964

*AmplifySCIAbsolute(A1)4,448118,583211,2530

*MethodicalBCIAbsolute(A)6,873915,996911,2031

*CelerityCiModerate(B)7,322818,043911,1932

*PrivateClientBCIMediumEquity(B)5,986417,714511,12338,3020

*OldMutualCoreModerate(A)6,854019,462311,0534

*FoordConservative(A)3,668411,179010,95358,21233

*OasisCrescentBalancedProgressiveFoF(D)8,621122,27610,88367,2041

*DiscoveryModerateBalanced(A)6,584917,684710,86378,60163

*AbsaM-MPassiveAccumulation(B)8,041917,664810,8637

*27fourBalancedFoF(A1)8,221418,772910,85387,90293

*AssetMixCiModerate(A)6,913618,972710,77397,85303

*OldMutualAlbarakaBalanced(A)9,02621,32810,73357,51353

*CapstoneBCIBalanced(A)5,537420,061610,69416,89462

*NovareBalanced(A1)6,903717,145710,6742

*CoronationCapitalPlus(A)5,866715,977010,60437,09433

*QuattroCiModerateFoF(A)6,026214,538110,60437,28383

*ASForumBCIModerateFoF(A)6,505317,025910,55447,26393

*MooreCiBalancedFoF(A)7,412616,616410,52457,34373

*AbsaBalanced(R)5,796923,02510,50467,7233

*SBROBCIBalancedFoF(A)4,827913,678710,44477,07443

*OptimumBCIBalanced(C)7,073316,856010,3748

*SageSCIModerateSolutionFoF(A2)7,233118,353410,33497,09433

*AssetbaseCPI+4%PrescientFoF(A1)7,782418,043910,26507,99263

PPSStableGrowth(A2)5,587217,125810,1351

*PFPSCiModerateFoF(A)8,72918,06389,95527,72333

*ChromeCiDefensive(A)6,525214,81809,9453

*AnchorBCIDiversiedModerate(A)6,245818,16359,87547,73323

GraySwanSCIModerateFoF(A)7,532520,56129,8455

SIMMediumEquity(A1)5,647015,65759,8156

*CinnabarSCIBalancedFoF(A)6,903716,39669,79577,37363

*AbsaM-MAccumulationFoF(A)6,893815,94719,78586,72492

*AmityBCIPrudentFoF(A)7,063418,97279,71596,41512

*DestinyBCIPrudentialFoF(A)5,647018,64319,65607,25402

AbsaM-MCoreAccumulation(C)6,136015,41769,6560

*MergenceCPI+4%Prime(A1)4,028310,97919,65607,37363

*AnalyticsCiModerateFoF(A)8,92717,40539,58617,13422

*OldMutualModerateBalanced(A)4,368219,42259,55627,98273

IFMBalancedValueFoF(A)7,932110,97919,52633,42592

*OldMutualDynamicFloor(A)6,425518,58329,44646,83472

MomentumTarget4FoF(A)5,647017,51519,4265

MomentumTarget5FoF(A)6,016318,94289,3966

*QuantumBCIBalancedFoF(A)5,637115,85729,20676,61502

*BaroqueBCIModeratoFoF(A)5,547315,06799,16685,19572

*PrescientPositiveReturnQuantPlus(A2)9,77215,76739,07695,62551

*MomentumFocus4FoF(A)6,555117,36549,0070

*SelectManagerBCIModerateFoF(A)6,684616,46658,91716,36522

*Mi-PlanIPIn.+5(B5)6,205912,61888,75726,94452

*SAAssetManagementBCIModerate(A)7,332713,79858,71735,03581

*Mi-PlanIPIn.+7(B5)6,714513,92848,67747,81313

*MomentumFocus5FoF(A)5,527517,63498,66755,90541

*IPPrudentialFoF(A)6,724414,17838,31765,91531

*AfFinityCiModerate(A)6,604814,38828,29776,77482

*FairtreeFlexibleBalancedPrescient(A1)7,942013,78868,15786,94452

*CounterpointSCIModerate(A1)6,295711,91897,83796,41511

*MFSSCIModerateFoF(B1)8,381216,80626,5480

*NoblePPBCIBalancedFoF(A)4,46808,28926,21815,52561

*EngelbergBCIBalanced(A)5,09777,35934,3782

*AmpersandSCICPIPlus4FoF(A)8,351317,45523,57833,11601

*PMKBalancedPrescientFoF(A3)6,684624,462

*BCIMultikorModerateFoF(A)8,211521,019

*10XMediumEquityIndex(A)7,912220,5413

*WeaverBCIModerateFoF(A)8,091819,8321

*PortfolioMetrixBCIModerateFoF(A)5,946519,1226

SynergyCiModerateFoF(A)7,832318,7630

*EdgeBCIBalancedFoF(A)5,946517,1956

*FisherDugmoreCiModerate(A)6,943516,7663

*TRGModeratePrescientFoF(A1)4,987816,2567

*NewRoadBCIModerateFoF(A)6,086115,7374

*CaleoBCIModerateFoF(A)6,485415,1178

*SasnBCIHorizonM-MAccumulation(A)6,8143

FNBIslamicBalanced(B1)6,5750

*GradidgeMahuraCiModerate(A)5,9465

TARGET DATE FUNDS

DiscoveryTargetRetirement2055(A)7,90322,19110,511

*DiscoveryTargetRetirement2050(A)7,93222,18210,4527,365

*DiscoveryTargetRetirement2040(A)7,65521,45410,3737,266

DiscoveryTargetRetirement2060(A)8,09122,19110,324

*DiscoveryTargetRetirement2045(A)7,81421,47310,1957,138

*DiscoveryTargetRetirement2025(A)6,45817,69710,0467,593

*DiscoveryTargetRetirement2020(A)6,10916,3589,9977,772

*DiscoveryTargetRetirement2035(A)7,36620,2859,9687,227

*DiscoveryTargetRetirement2030(A)7,02719,1469,8497,454

*DiscoveryTargetRetirement2015(A)5,681015,0999,73107,851 ArithmeticAverage7,2019,6010,107,38

SOUTH AFRICAN INTEREST-BEARING

SHORT-TERM FUNDS

TrueSCIIncomePlus(A)1,8127,4628,0919,6915

PSGIncome(A)1,24124,88117,4827,862

*MatrixSCIStableIncome(B1)1,00314,59227,393

TerebinthSCIEnhancedIncome(B1)1,24125,8547,324

DATABANK PERSONAL FINANCE | 1 ST QUARTER 2022 65 NAME 3 MONTHS 1 YEAR3 YEARS5 YEARS PLEX. % RANK % RANK % RANK % RANK NAME 3 MONTHS 1 YEAR3 YEARS5 YEARS PLEX. % RANK % RANK % RANK % RANK

*AbsaIncomeEnhancer(R)1,4844,99107,0957,6474

CentralFundisa(B8)1,26104,80156,8867,843

NedgroupInv.Fundisa(A)1,23134,76166,8777,814

*SIMEnhancedYield(A1)1,25115,1476,8187,7855

AbsaCoreIncome(A)1,16194,29296,7797,6664

StanlibM-MEnhancedYield(B1)1,24125,0296,63107,36113

OldMutualIncome(R)1,06273,52366,57117,4894

StanlibIncome(R)1,2894,46246,53127,5283

PPSEnhancedYield(A2)1,20164,87126,48137,3512

*AshburtonStableIncome(A)1,21155,1386,40147,29134

*MomentumEnhancedYield(A)1,3084,45256,39157,20153

NinetyOneHighIncome(R)1,13214,81146,35167,3910

PrescientYieldQuantPlus(A2)1,22144,73176,33177,11193

PrimeIncomePlus(A)1,10234,63216,31187,14163

*HollardPrimeYield-Plus(B)1,3574,64206,30197,13173

StandardBankFundisa(A)1,11224,18316,26207,2214

*InstitBCIEnhancedYield(A)1,15204,33276,2521

*AFInvestmentsSuperiorYield(A)1,19174,64206,24227,04212

CitadelSAIncomeH4(B1)1,18184,72186,21237,10202

*M&GIncome(A)1,09244,68196,15247,11193

*AshburtonSAIncome(B1)1,3084,34266,05257,12183

CoronationJibarPlus(A)1,07264,33275,95266,88232

*NedgroupInv.CoreIncome(B)1,07264,32285,93276,78242

StanlibEnhancedYield(B1)1,07264,23305,9327

*StanlibExtraIncome(R)1,05284,55235,92286,89223

AbsaFundisa(A)0,85343,82345,83296,7824

*NinetyOneSTeFIPlus(A)1,08254,18315,82306,6825

*IPInterestPlus(A)1,03304,14325,66316,66261

PSGWealthEnhancedInterestFoF(A)0,97323,95335,61326,4228

OldMutualInterestPlus(A)0,90333,74355,58336,52272

GryphonDividendIncome(A)0,77353,04374,68345,47291

SasnBCIHighYield(A)1,8718,131

NgwediSNNInterestIncome(R1)1,6035,903

*VunaniBCIShortTermInterest(A)1,3865,305

AbaxSAIncomePrescient(A1)1,4055,216

AnchorBCICoreIncome(A)1,19174,8513

PSGEnhancedInterest(D)1,04292,2538

FirstGlobal1BCIEnhancedYield(A)1,0825

VARIABLE-TERM FUNDS

*AbsaBond(A)3,02197,673510,29110,0115

NedgroupInv.CoreBond(A)2,98218,71189,3729,274

CitadelSABondH4(B1)2,54377,24379,2039,342

*FairtreeAlbiPlusPrescient(A1)3,16138,49219,124

PortfoliometrixBCISABond(A)2,76278,68209,0359,2054

AnchorBCIBond(A)2,74287,95309,0069,1064

*StanlibBond(A)3,08168,39228,9379,0274

AbsaBondIndex(A)2,85248,19268,878

*AFInvestmentsPureFixedInterest(A)3,09159,73118,6998,7393

PrescientFlexibleBond(A2)4,81614,4468,68108,32203

SIMBondPlus(A)2,95228,92158,68108,67103

MomentumBond(A)2,98218,86168,65118,8083

SygniaAllBondIndex(A)2,80258,21248,61128,4914

*AllanGrayBond(A)3,09157,98298,57139,3334

NewFundsGoviETF2,70317,88318,57138,4516

*OasisBond(D)3,00208,69198,51148,7393

1nvestAlbi(Non-Tr)Ind.Tr.(A)2,73297,81328,49158,4815

*AshburtonBond(A)3,04188,75178,44168,61122

SatrixBondIndex(A1)2,72307,73348,43178,4417

AbsaM-MBond(A)2,982110,3178,35188,40183

OldMutualBond(R)2,67348,34238,19198,35192

CoronationBond(R)3,40119,95108,06208,62112

*M&GHighYieldBond(A)3,11149,43138,00218,09222

*MelvilleDouglasStanlibBond(A)2,68337,52367,93228,07231

AbsaInationLinkedIncome(A)1,54416,06397,81238,04243

PrescientFlexibleFixedInterest(A2)2,03406,84387,77248,50134

*CommunityGrowthGilt(A)2,69327,99287,66258,12212

SatrixIlbiETF(A)5,19215,1936,7826

NewFundsIlbiETF5,03315,2026,67274,3225

AshburtonInationETF4,98515,0846,66284,3126

1nvestInationLinkedBondInd.Tr.(A)5,01414,9156,42294,1727

ColoureldBCIIncome2(A)7,52119,3615,20302,16281

1nvestSABondETF2,762710,148

ArgonBCIBond(A)3,93710,029

*VunaniBCIBond(A)3,35129,7012

*OakhavenSNNBond(A2)3,8589,2514

*SygniaEnhancedAllBond(A)2,89238,3922

TerebinthSCIActiveBond(B1)2,61358,2025

SatrixSABondPortfolioETF(A)2,79268,0427

DiscoveryStrategicBond(A)2,59367,8033

*VisioBCIBond(A)3,689

*FNBMultiManagerBond(A1)3,5610

FairtreeBondPrescient(A1)3,0517

*NgwediSNNBondClassT42,7627

AmpersandSCIBond(A)2,3538

MethodicalBCIBond(B1)2,1339

SOUTH AFRICAN REAL ESTATE

GENERAL FUNDS

HarvardHouseBCIProperty(A)8,851242,4235,3412,4025

CatalystSCIFlexibleProperty(A)9,70440,6283,7823,1415

PortfolioMetrixBCISAProperty(A)7,912538,61110,723-0,9934

AbsaPropertyEquity(A)7,363638,37120,294-2,3695

CadizBCIProperty(B)7,563234,45340,045-3,13103

OldMutualSAQuotedProperty(A)9,69538,9610-0,176-1,6864 SeskileBCIProperty(A1)8,251937,9414-0,187-1,1444

PlexusWealthBCIProperty(A)12,82146,132-0,548-3,61124

HollardPrimeProperty(B)8,681337,3518-0,659-1,4853

AbsaSmartAlphaProperty(A)7,962437,4017-1,1810-4,62173 MetopePropertyPrescient(A)7,603133,4337-1,6811-3,56114 OasisPropertyEquity(D)9,92235,8725-2,2512-4,37161

MSMProperty27four(A1)8,521436,2020-2,3613

AnchorBCIProperty(A)8,202133,3938-2,4914-2,2982

DiscoveryFlexibleProperty(A)9,53841,114-2,6115-3,76133 AbsaPropertyIndex(A)8,481736,3719-3,1716 SatrixPropertyIndex(A1)8,212036,2020-3,3217-4,8120

AFInvestmentsPropertyEquity(A)7,902635,0232-3,4818-4,26143

PrescientPropertyEquity(A2)8,042235,8924-3,5019-4,82213

SygniaListedPropertyIndex(A)7,772835,9823-3,5320-4,8923 NinetyOnePropertyEquity(A)8,511540,896-3,7021-4,6718

MarriottPropertyIncome(A)9,55736,1021-3,7622-1,8173

1nvestSAPropertyETF7,972335,8126-3,7622-4,9724

MomentumRealGrowthPropertyIndex(A)7,533434,6533-3,8123

M&GEnhancedSAPropertyTracker(A)8,471837,6415-3,8324-5,35272

CatalystSCISAPropertyEquity(A)7,343738,0913-3,8425-4,3115

MomentumRealGrowthProperty(A)7,244035,6629-4,1626-4,86223

StanlibPropertyIncome(B1)7,234132,2340-4,3127-6,46291

PrimeProperty(A)7,333834,4035-4,3328-4,68192

CitadelSAPropertyH4(B1)7,832737,5316-4,5329-5,29262

AshburtonProperty(A)7,723032,8039-4,7430

SIMProperty(A)7,273936,0622-4,7831-5,8128

MomentumSARealGrowthProperty(A)7,513535,8027-4,7831

CoronationPropertyEquity(A)7,553335,4530-5,7532-5,24252 NedgroupInv.Property(A)9,89349,041-6,5433-7,94311

1nvestCappedPropertyInd.Tr.(B3)7,732935,4131-6,8034-7,6230 SatrixPropertyETF(A)8,491639,619-7,5635

CoreSharesSAPropertyIncomeETF9,61641,075

MetopePropertyIncomePrescient(A)9,70440,677

InvestecW&IBCIProperty(A)9,211035,7728

M&GProperty(A)9,46933,8836

*FNBMultiManagerProperty(A2)8,9711

FTSE/JSESAListedPropertyIndex(J253)8,3536,94-2,94-4,35

DATABANK PERSONAL FINANCE | 1 ST QUARTER 2022 66 NAME 3 MONTHS 1 YEAR3 YEARS5 YEARS PLEX. % RANK % RANK % RANK % RANK NAME 3 MONTHS 1 YEAR3 YEARS5 YEARS PLEX. % RANK % RANK % RANK % RANK

WORLDWIDE EQUITY

GENERAL FUNDS

H4WorldwideEquity(B1)12,77228,57218,44113,011

NestEggBCIWorldwideEquity(A)10,71413,381016,172

CoreSharesOUTaggressiveIndex(O)12,62332,72115,793

StewartBCIMacroEquityFoF(A)10,31720,21714,7548,412

BCIValue(B)10,34616,34814,0858,023

CorionPrimeWorldwideEquity(A1)9,20922,43611,956

PrimeWorldwideEquity(A)4,041122,4553,437

CitadelWorldwideEquityH4(B1)14,79127,273

AshburtonGlobalLeadersZAREquityFdr(A)10,38523,284

IDCapitalBCIWorldwideEquity(A)9,82816,259

ImalivestSCIWWEquity(A2)9,0510

UNCLASSIFIED FUNDS

OldMutualGold(R)32,8314,52230,30117,011

VisioBCIProperty(C)12,17239,721

WORLDWIDE MULTI-ASSET

FLEXIBLE FUNDS

NavigaBCIWorldwideFlexible(A)10,681928,42742,311

BlueQuadrantWorldwideFlexiblePrescient(A)16,351129,03133,92215,7623

RCIBCIWorldwideFlexibleGrowthClassL2,98994,709325,16314,9444

CordatusWorldwideFlexiblePrescient(A2)13,13530,10421,84415,6235

PrescientChinaBalancedFeeder(A2)9,163511,158721,73513,2773

SelectBCIWorldwideFlexible(A)12,31624,902021,71617,5415

RootstockSCIWorldwideFlexible(A)10,831725,381521,24714,2865

SimplisitiBCIFlexibleFoF(A)8,844218,106420,09811,07294

RCIBCIWorldwideFlexible(A)3,849616,327319,35912,70114

OldMutualM-MMaximumReturnFoF(A)8,534625,221819,311012,40154

NestEggBCIWorldwideFlexible(A)11,96721,673319,2611

ProvidenceBCIWorldwideDiversied(B)10,592023,922319,001212,71104

MontroseBCIFlexibleFoF(A)9,702725,921418,931312,9484

NedgroupInv.BravataWorldwideFlexible(A)13,34337,58218,711411,93194

NFBCiWorldwideFlexible(A)9,063833,46318,6215

IDCapitalBCIWorldwideFlexible(A)10,721821,083918,5016

InstitBCIWWModerateAggressiveFlexible(A)10,522119,025618,4717

PrimeWorldwideFlexible(B)6,118420,514418,361812,51134

QuattroCiWorldwideFlexibleFoF(A)9,722618,796017,811912,8994

InstitBCIWorldwideEquity(A)7,676122,223117,732011,58223

LunarBCIWorldwideFlexible(A)3,389819,375317,522111,35245

LongBeachWorldwideFlexiblePrescient(A1)1,941008,049117,302214,8153

ChromeCiMaximumReturn(A)11,141524,152217,2823

BCIWorldwideFlexibleFoFClass3B17,815819,664917,122410,52333

CohesiveCapitalWWFlexiblePrescient(A2)6,667826,311316,932512,05185

SygniaSkeletonWorldwideFlexible(A)4,049522,822716,662612,22173

CoronationGlblOptimumGrowth(ZAR)Fdr(A)5,81882,869516,662612,28163

SignatureBCIWorldwideFlexibleFoF(A)7,845719,655016,622711,49234

AFInvestmentsFlexibleFoF(A)8,494819,615116,602811,20274

BCIFlexible(A)8,325129,50516,582912,66125

ConsiliumBCIWorldwideFlexible(A)7,486316,447216,443012,47145

CeltisBCIFlexibleFoF(A)7,326520,924016,403110,80314

PPSWorldwideFlexibleFoF(A2)6,567917,536816,353211,6221

BrenthurstBCIWorldwideFlexibleFoF(A)8,954017,956616,0033

SouthernCharterBCIWWFlexibleFoF(A)11,381321,093815,713410,16353

CSBCIWorldwideFlexibleFoF(B)7,915416,087415,673511,18283

RedOakBCIWorldwideFlexibleFoF(A)7,016915,677815,3836

OldMutualMaximumReturn(A)6,548026,921115,373710,88303

AureusNobilisBCIWorldwideFlexibleFoF(A)8,614518,815915,203810,68323

BovestBCIWorldwideFlexibleFoF(A)7,875620,844115,163910,29343

PlatinumBCIWorldwideFlexible(A)9,123719,555214,944011,71204

JBLSCIWorldwideFlexibleFoF(B1)7,716015,757714,8741

CitadelWorldwideFlexibleH4(B3)13,61223,772414,8042

H4Growth(B1)11,581124,522114,714311,35243

CoronationMarketPlus(A)7,486322,083214,63449,14412

CorionPrimeWorldwideFlexible(A)7,885520,074714,634410,05363

DinamikaBCIWorldwideFlexible(A)9,143624,991914,55458,55493

FlagshipIPWorldwideFlexibleFoF(A)7,356417,026914,504611,23263

MethodicalBCIWorldwideGrowthFoF(A)8,524721,513414,46479,63383

AnchorBCIWorldwideFlexible(A)4,299410,078914,38488,94432

CinnabarSCIWorldwideFlexibleFoF(A)7,626216,477114,26498,73463

PWSBCIWorldwideFlexibleFoF(A)6,907120,074714,0450

Point3BCIModerateWWFlexibleFoF(A)11,73820,194513,74519,11423

FinancialFitnessIPFlexibleFoF(A)8,724316,777013,715211,30254

Ginsburg&SelbySCIWorldwideFlexible(A1)5,718915,837513,6353

FlagshipIPWorldwideFlexible(A)3,57974,779213,62548,74452

FNBGrowthPlusFoF(B1)11,621027,38913,61558,45502

ImalivestSCIWWFlexible(A)11,67922,692912,96568,76442

PrivateClientBCIWorldwideFlexible(B)7,995320,714312,96569,5339

FoordFlexibleFoF(A)4,479310,338812,94578,58483

CordatusWorldwideFlexiblePrescientFoF(A2)9,273422,772812,93587,96542

MarriottWorldwideFoF(A)10,092218,216312,86599,35403

AutusPrimeWorldwideFlexible(A)10,032312,068512,84608,74453

RebalanceBCIWorldwideFlexibleFoF(A)6,787619,764812,73618,55492

4DBCIAggressiveFlexibleFoF(A)9,283317,886712,67627,79562

TrésorSCIFlexible(B1)11,281421,383512,38638,39512

AnalyticsCiWorldwideFlexibleFoF(A)9,862418,975712,216410,00373

SelectManagerBCIWorldwideFlexibleFoF(A)9,812519,345412,06658,60472

BCIBestBlendWorldwideFlexible(A)7,716015,427911,80668,27522

OctagonSCIWorldwideFoF(B1)7,755915,128111,80667,75572

NinetyOneWorldwideFlexible(E)8,854119,655011,78677,0560

FairtreeWWMulti-StrategyFlex.Prescient(A1)7,306613,408411,3268

PBIBCIWorldwideFlexibleFoF(A)6,807521,123611,22697,56591

InstitBCIWorldwideFlexible(A)9,023927,231010,8970

ProsperityIPWorldwideFlexibleFoF(A)6,927015,298010,80718,17533

StonewoodBCIWorldwideFlexible(B)9,413123,30269,92726,02621

IPWorldwideFlexibleFoF(B2)9,323218,68629,81736,21611

MedianBCIWorldwideFlexibleFoF(A)6,817417,53689,78745,47631

OptimumBCIWorldwideFlexibleFoF(A)6,827311,64869,48757,93552

NovareWorldwideFlexibleFoF(A1)6,138220,82429,47767,68582

RockCapitalIPWorldwideFlexible(A)5,00918,80904,58772,57641

CounterpointSCIWorldwideFlexible(A)6,128318,96582,93782,11651

ThymeWealthIPGlobal(A)6,0685-0,73962,8279

CratosBCIWorldwideFlexible(A)11,461229,156

FussellCiWorldwideFlexible(A)9,632827,598

PMKWorldwideGrowthPrescientFoF(A3)8,005226,3312

SynergyCiGlobalFlexibleGrowthFeeder(B)13,25425,2616

PortfolioMetrixBCIUncons.AssertiveFoF(A)8,494825,2417

PortfolioMetrixBCIUncons.BalancedFoF(A)7,236723,3525

OdysseyBCIWorldwideFlexible(A)8,335022,5430

RoxburghCiWorldwideFlexibleFoF(A)8,404921,1137

FisherDugmoreCiWorldwideFlexible(A)10,911620,1746

BIPBCIModerateWorldwideFlexible(C)9,443019,1455

PortfolioMetrixBCIUncons.ModerateFoF(A)5,998618,7361

IPWorldwideActiveBeta(A)9,612917,9765

NavigaBCIWorldwideFlexibleGrowth(A)5,918717,9566

BCIWorldwideFlexibleStyle(C)7,066815,8076

RexsolomWWFlexiblePrescient(A1)8,634413,7982

HarvardHouseBCIWorldwideFlexible(A)8,335013,7683

IndependentSecuritiesBCIWWFlexible(D)5,71894,2094

PyxisBCIWorldwideFlexible(C)6,8572

InstitBCIWorldwideFlexibleFoF(A)6,7377

SanlamPrivateWealthWorldwideFlexible(A1)6,3281

AnchorBCIWorldwideOpportunities(C)5,0190

SaltLightSNNWorldwideFlexible(A2)4,8592

GLOBAL EQUITY

GENERAL FUNDS

SygniaFAANGPlusEquity(A)7,007519,896038,641

EmperorIPGlobalEquity(A)-4,1199-6,608937,11225,3514

AnchorBCIGlobalEquityFeeder(A)2,54933,378535,86322,5425

SygniaItrix4thIndustrialRev.GlobalEqtyETF3,189011,657535,434

Sygnia4thIndustrialRev.GlobalEqty(A)2,63929,897732,20522,4234

DATABANK PERSONAL FINANCE | 1 ST QUARTER 2022 67 NAME 3 MONTHS 1 YEAR3 YEARS5 YEARS PLEX. % RANK % RANK % RANK % RANK NAME 3 MONTHS 1 YEAR3 YEARS5 YEARS PLEX. % RANK % RANK % RANK % RANK

SatrixS&P500FeederETF17,66139,34229,946

CoreSharesS&P500ETF16,87240,07129,84721,134

StonehageFlemingSCIGlblBIEqtyFdr(A1)13,381630,912029,848

M1CapitalGlobalEquityPrescient(A1)13,202113,201627,70917,8010

PSGWealthGlobalCreatorFeeder(A)9,834927,443426,781018,866

BlueAlphaBCIGlobalEquity(A)13,212030,862326,601120,6355

OldMutualMSCIWorldESGIndexFeeder(A)14,011034,42525,8812

SatrixMSCIWorldEquityFeederETF14,25832,331025,8513

1nvestMSCIWorldIndexFeederETF13,212032,121325,7114

FairtreeGlobalEquityPrescient(A1)13,381631,771525,6515

1nvestMSCIWorldIndexFeeder(A)13,391532,291125,6116

SygniaItrixMSCIWorldIndexETF14,15931,871425,601718,438

AutusPrimeGlobalEquityFeeder(A)12,243020,495825,601718,0794

AshburtonGlobal1200EquityFoFETF14,33730,882124,9818

AbsaGlobalCoreEquityFeeder(A)13,221935,21424,801916,64165

SatrixMSCIWorldEquityIndexFeeder(A1)13,231831,371724,742017,3712

NinetyOneGlobalStrategicEquityFeeder(R)11,993231,181824,472116,5717

NinetyOneGlobalFranchiseFeeder(A)13,401428,922924,082218,617

StanlibM-MGlobalEquityFeeder(B1)8,576327,383524,082217,11134

ABAXGlobalEquityPrescientFeeder(A1)10,834221,625323,752317,59114

OldMutualGlobalEquity(R)12,362932,35923,592416,9414

DiscoveryGlobalEquityFeeder(A)12,892328,033223,582515,93213

CoreSharesMSCIACWIFoF(A)11,483527,743323,3426

AFInvestmentsGlobalEquityFeeder(A)9,825025,773923,112715,69233

Mi-PlanIPGlobalAIOpportunity(B2)12,392823,344522,7928

GryphonGlobalEquity(B)12,412730,872222,692915,66243

SygniaSkeletonInternationalEquityFoF(A)9,015823,854222,323016,39184

M&GGlobalEquityFeeder(A)8,106832,54822,223115,20263

PrescientGlobalEquityFeeder(A2)13,561230,592422,193213,48313

NedgroupInv.GlobalEquityFeeder(A)8,906023,764322,063316,80153

CoronationGlobalEquitySelect[ZAR]Fdr(A)6,817614,297321,673413,31322

StyloGlobalEquityPrescientFoF(A1)11,343724,594121,613516,21194

Mi-PlanIPSarasinEquisarFeeder(B5)9,635222,245121,453616,13203

CitadelGlobalEquityH4FoF(B1)12,532626,713721,243715,62253

CoronationGlobalOpp.Equity[ZAR]Feeder(A)5,918018,766521,153814,91273

PortfolioMetrixBCIGlobalEquityFoF(B2)9,884826,573820,603915,89223

DenkerSCIGlobalEquityFeeder(A)10,774330,342520,524013,20333

FoordGlobalEquityFeeder(A)8,126710,257620,454113,9529

27fourGlobalEquityFeeder(A1)10,104723,304620,204214,10283

SelectManagerBCIGlobalEquityFoF(A)7,717221,035520,0343

CoreSharesS&PGlobalDiv.AristocratsETF14,81428,563119,3444

AllanGray-OrbisGlobalEquityFeeder(A)6,077918,006619,074512,39342

GlacierGlobalStockFeeder(B)8,646128,583018,9846

BCIBestBlendGlobalEquity(A)7,837119,236218,604711,98363

SasnBCIGlobalEquityFeeder(A)10,764422,105218,4548

OldMutualFTSERaAllWorldIndexFdr(A)9,655130,142618,304912,3735

MomentumInternationalEquityFeeder(A)9,175622,525018,225013,61302

OasisCrescentInternationalFeeder(D)11,114023,854217,835111,22392

MarriottFirstWorldEquityFeeder(A)11,273920,625716,805211,80372

SanlamGlobalEquity(R)8,386516,397116,475310,3241

ElementIslamicGlobalEquitySCI(A)11,403622,854916,29549,79422

SanlamPWGlobalHighQualityFdr(A1)8,356617,986715,7455

SatrixMSCIEmergingMarketsFeederETF4,27857,547914,6456

AbsaGlobalValueFeeder(R)7,257429,452814,635710,4440

ElementGlobalEquitySCI(B)9,215515,527214,635711,40382

SanlamGlobalEmergingMarketsFeeder(A1)-0,45976,608114,28588,35461

PSGGlobalEquityFeeder(A)7,487332,67713,59599,3943

CounterpointSCIGlobalEquityFeeder(B)13,391535,72313,26609,21441

OldMutualMSCIEMsESGIndexFeeder(A)1,96953,478413,1061

DiscoveryGlobalValueEquityFeeder(A)4,288423,204812,90629,13451

SatrixMSCIWorldESGEnhancedFeederETF14,46532,946

PrescientCoreGlobalEquity(A2)13,431332,1312

BCIFundsmithEquityFeeder(A)12,922231,0719

InvestecW&IBCIGlobalLeadersEquity(A)10,114630,3425

SygniaHealthInnovationGlobalEquity(B)11,753429,9627

PPSGlobalEquityFeeder(A2)12,542527,0336

DynastyCiGlobalAccumulatorFeeder(A)13,251725,6840

BCIGuernseyGlobalGrowthFeeder(A)8,616223,3844

BenguelaGlobalEquity27fourFeeder(A1)8,066923,2247

BCICredoGlobalEquityFeeder(A)9,505421,4954

36OneBCIGlobalEquityFeeder(A)6,727721,0056

MaziAssetMngPrimeGlobalEquity(A)11,903320,4159

NedgroupInv.GlobalDiversiedEqtyFdr(A)10,254519,6161

Global&LocalSNNOshoreEquity(A)12,153119,0963

KagisoIslamicGlobalEquityFeeder(A)8,935919,0764

PrescientSigmaSelectGlblLeadersFdr(A2)6,087817,4768

LauriumGlobalEquityPrescient(A1)8,556417,1069

KagisoGlobalEquityFeeder(A)3,938616,4570

InstitBCIGlobalEquity(A)9,035713,9274

BCILindsellTrainGlobalEquityFeeder(A)3,80878,0678

AnchorBCIGlobalTechnology(A)2,05946,6980

FlagshipIPGlobalIconFeeder(A)3,26895,5782

SatrixMSCIEMESGETF3,35885,0783

AnBroBCIUnicornGlobalGrowth(A)-0,25963,1786

FairtreeGlblEmergingMarketsPrescient(A1)5,44813,1387

NedgroupInv.GlobalEMEquityFeeder(A)2,87911,3088

SatrixMSCIChinaFeederETF-0,5098-15,4490

SygniaItrixS&PGlobal1200ESGETF15,713

SygniaItrixSolactiveHealthcare150ETF14,456

10XMSCIWorldIndexFeeder(A)13,6411

CoreSharesTotalWorldStockFeederETF12,5724

BCIRootstockGlobalEquityFeeder(A)11,2938

SelectBCIEnhancedCoreGlblEqtyFoF(A)11,0741

BrenthurstBCIGlobalEquityFeeder(A)9,5853

PeregrineCapitalGlobalEqtyPrescientFdr(A)7,8570

SygniaItrixMSCIEmergingMarkets50ETF4,9982

BCISandsCapitalGlobalGrowthFeeder(A)4,8883

BCISandsCapitalEmergingMarketsFdr(A)-5,88100

InvesthouseCiGlobalFeeder(A)11,231121,191820,104 SkyblueBCISolarFlexibleFoF(A)9,972021,301619,99513,237

PSGWealthGlobalFlexibleFeeder(D)7,534117,833319,25614,435 Point3BCIGlobalFlexibleFoF(A)12,93429,14119,147 MethodicalBCIGlobalFlexibleFoF(A)9,242719,932119,108 NorthstarSCIGlobalFlexibleFeeder(A)7,064318,483018,619 NorthstarSCIGlobalFlexible(A)7,194218,532918,601015,463

MarriottInternationalGrowthFeeder(A)13,15324,24718,491112,659 NedgroupInv.GlobalFlexibleFeeder(R)6,614622,841217,901211,5510 3 SygniaInternationalFlexibleFoF(A)6,874516,533717,861313,986 4 AssetbaseGlobalFlexiblePrescientFoF(A1)9,852219,572317,691413,198 4 AmityBCIGlobalDiversiedFoF(A)9,642425,13417,341511,1112 3 CounterpointSCIGlobalManagedGrowth(A)14,27127,30315,681610,9114 3 CoronationGlobalEMsFlexible[ZAR](A)-0,1753-7,504515,631711,0613

BCIUbamMultiFundsFlex.AllocationFdr(A)6,244718,013115,5518

LynxPrimeGlobalDiversiedFoF(A1)10,051823,10915,39199,9518

WarwickBCIInternationalFoF(C)10,101720,631915,212011,4511

PSGWealthGlobalModerateFeeder(A)7,853616,583614,782110,0916

PSGGlobalFlexibleFeeder(A)6,954427,87214,12229,4719 FGSCIInternationalFlexibleFoF(A)7,963517,943213,852310,0817

KrugerCiInternationalFlexibleFeeder(A)8,493215,893813,832410,6815

APSCiGlobalFlexibleFeeder(B)9,981917,623413,82259,4221

IPForeignFlexibleFeeder(A1)10,921320,272013,65269,1622

SelectManagerBCIGlobalModerateFoF(A)8,223415,503913,31279,4520

DATABANK PERSONAL FINANCE | 1 ST QUARTER 2022 68 NAME 3 MONTHS 1 YEAR3 YEARS5 YEARS PLEX. % RANK % RANK % RANK % RANK NAME 3 MONTHS 1 YEAR3 YEARS5 YEARS PLEX. % RANK % RANK % RANK % RANK

UNCLASSIFIED FUNDS DenkerSCIGlobalFinancialFeeder(A1)7,18137,67115,08110,661 GLOBAL MULTI-ASSET FLEXIBLE FUNDS DetonPrimeGlobalFlexibleFoF(A)11,66619,042521,58114,544 5 GlobalIPOpportunity(B5)11,65723,021020,86216,882 4 Mi-PlanIPGlobalMacro(B5)11,79522,621320,84317,041 5

4

4

3

MSCIWorldindex13,7630,3223,8316,66

3

3

0

2

2

1

2

2

FoordInternationalFeeder(A)7,713811,274112,37288,9523

RezcoGlobalFlexibleFeeder(A)1,0552-2,61448,3829

EngelbergBCIGlobalFeeder(A)5,034811,51407,42303,5124 1

ChromeCiGlobalMaximumReturnFeeder(A)11,30924,355

CelerityCiInternationalGrowth(B)9,842324,266

FisherDugmoreCiGlobalGrowth(A)10,771523,438

CadizBCIGlobalFlexibleFoF(A)11,051222,9711

SanlamAIGlobalManagedRiskFeeder(A)9,472521,7814

NewRoadBCIGlobalFlexibleFoF(A)9,912121,6815

VunaniBCIGlobalMacro(A)10,651621,2017

MethodicalBCIGlobalFlexible(B1)13,42219,7222

ClucasGrayGlobalFlexiblePrescient(A1)7,624019,5324

SalvoGlobalManagedPrimeFeeder(B)9,052918,8326

PMKGlobalFlexiblePrescientFoF(A3)7,643918,6327

QuantumBCIWorldwideFlexibleFoF(A)9,402618,5428