Let the Big Dogs Eat. Join top business and community leaders at top-tier courses across the US in the #1 Charity Event In Golf.™

Make a Difference. Earn Rewards. Compete as a foursome or sponsor a local event for a chance to earn rewards, including a trip to the Applied Underwriters Invitational National Finals at Big Cedar Lodge.

Contact an Applied rep at 877-234-4450 or email invitational@auw.com to get started.

Follow us for a shot at even more rewards. Applied Underwriters Invitational® | #BigDogGolf invitational.com

Report: Building and Retaining Talent: Salaries, Benefits, Culture Matter but That’s Not Always Enough

Special Report: 2025 Agency Salary Survey: Salaries, Total Income Jump Again in 2024 But Satisfaction Continues to Decline

Report: 2024 Agents of the

Spotlight: Farmers Turn to Airbnb, Corn Mazes to Outlast Agricultural Downturn

US Chicken, Pork Plant Workers Face Higher Health Risks, USDA Studies Confirm

Reviewing Historic Predictions

Takeaways from 2024 to Build a Better 2025 and Beyond

Emerging Risks to Watch: Social Inflation, Electric Trucks, Virtual Currencies

Minding Your Business: Developing Leaders in Insurance Agencies

Marketing Connection: Insider Secrets: Creating High-Converting Sales Funnels for Insurance

Closing Quote: California Wildfire Claims Ignite IndustryWide Credibility Crisis

Opening Note

Why Soft Skills Matter

This issue reveals data and compensation insights gathered from Insurance Journal’s annual Agency Salary Survey. For the third year in a row in the survey’s 16-year history, salary averages and total compensation averages (including additional compensation such as profit sharing, bonuses, and other income) reported were higher than ever before. (See page 20 for the full report.)

This trend is good for agency employees, producers, and agency owners, but talent shortages and hiring demands have not eased for the independent agency sector. Agency owners are struggling to keep pace as the industry’s ongoing talent war continues. Competition is fierce for experienced top talent, especially in the service roles, the experts interviewed for this report say.

“Client-facing support people are really valuable,” Kevin Stipe, partner and CEO of Reagan Consulting, told Insurance Journal.

Competitive pay, job stability, and flexibility have become table stakes for companies looking to hire top-tier candidates in this sector. But those who exhibit top-level experience along with what Stipe called “soft skills” will become even more valuable in the future.

As artificial intelligence (AI) tools play a larger role in independent agencies, the technical skills that are also part of the service role job are going to become more commoditized, Stipe predicts. That’s because with these innovative tech tools agencies can equip employees with answers those technical questions much more effectively, he explained. But what AI can’t do (yet?)— is deliver to clients the service they need with “emotional IQ.” And that emotional service will become a much more valuable skill in insurance brokerage client support going forward, he said.

“We’re in a world where the soft skills are going to get more valuable,” Stipe said. “The ability to empathize with clients, display emotional IQ, that is the kind of stuff that a computer is never going to be able to do.”

It’s those soft human skills that are essential for agencies to have happy clients, he added.

“Soft skills are as important now as they will be in the future,” agreed Mary Newgard, partner and senior search consultant for Capstone Search Group, a national recruiting firm dedicated to the insurance industry.

‘We’re

in a world where the soft skills are going to get more valuable.’

“There is no technology that can replace parts of the process that require human interaction,” she added. “Some interactions can be automated, but when it comes to building relationships, working through conflict, and addressing complex needs, I don’t think AI can replace people." This rings true for many facets of an agency, from selling to and servicing clients to recruiting and retaining top talent, Newgard said.

For more, check out this issue’s special report on page 20.

Andrea Wells V.P. of Content

Chairman of the Board Mark Wells | mwells@wellsmedia.com

Marketing Administrator Alberto Vazquez | avazquez@insurancejournal.com

Marketing Director Derence Walk | dwalk@insurancejournal.com

DESIGN / WEB / VIDEO

V.P. of Design Guy Boccia | gboccia@insurancejournal.com

Web Team Lead

Josh Whitlow | jwhitlow@insurancejournal.com

Ad Ops Specialist

Jeff Cardrant | jcardrant@insurancejournal.com

Web Developer Terrance Woest | twoest@wellsmedia.com

Web Developer Jason Chipp | jchipp@wellsmedia.com

Digital Content Manager

Ashley Cochrane | acochrane@insurancejournal.com

Videographer/Editor

Ashley Waldrop | awaldrop@insurancejournal.com

ACADEMY OF INSURANCE

Director Patrick Wraight | pwraight@ijacademy.com

Online Training Coordinator George Jack | gjack@ijacademy.com

146 results for ‘bars & breweries’

News & Markets

Sica Fletcher Index: Total Agency-Broker M&A Revenue Down 26% in 2024

The 22 acquirers that make up the Sica Fletcher Index were involved in 533 agent-broker deals in 2024,

down 6% from 2023.

Members completed 146 acquisitions during the fourth quarter of 2024. This was

11% less than a year ago.

Total agency-broker revenue acquired in 2024 was $1.6 billion, a 26% decrease compared to 2023. The average agency size in revenue was about $3.1 million—about 21% lower than in 2023.

Sica Fletcher, an insurance industryfocused advisory firm, said the year’s final tally reflects “a recalibration in the market as buyers prioritize smaller, strategic acquisitions and reassess valuations amid evolving financial conditions,” as the volume of sub-$1 million deals in 2024 “continues to outweigh the volume of larger deals.”

The firm said its Agency & Broker Buyer Index captured 65% of all 2024 agent-broker deal activity, which is down from the usual 70%. The drop indicates more activity by newer market entrants.

Private equity-backed BroadStreet Partners led the SF index with 85 deals in 2024. That’s 24 more deals than last year. Hub International and Inszone Insurance were next with 62 and 48 deals, respectively.

Private equity made more than 88% of SF Index transactions in 2024. Gallagher led public companies with 45 deals in 2024.

News & Markets

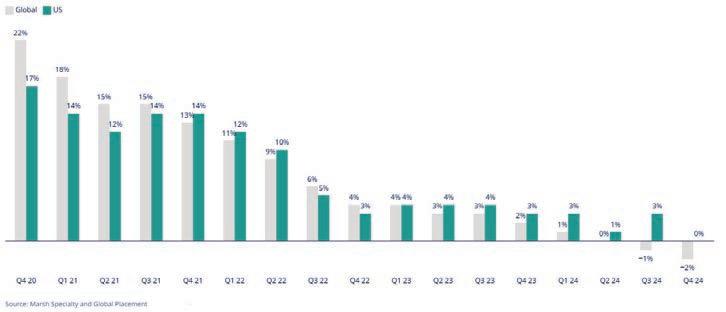

Global Commercial Insurance Rates Drop in Q4 for 2nd Consecutive Quarter: Marsh

By L.S. Howard

Global commercial insurance rates fell 2% in the fourth quarter of 2024 following a 1% decline in Q3 2024—marking the second consecutive quarterly decrease following seven years of rising rates, according to the Global Insurance Market Index published by insurance broker Marsh.

Marsh said the result continues the moderating rate trend first seen in its index in Q1 2021, which is being driven by intensified competition in commercial property insurance, a moderation of casualty rate increases, stabilizing pricing in financial lines, and accelerated rate reductions for cyber risks.

The UK and the Pacific regions again experienced the largest composite rate decreases during Q4, at 5% and 8%, respectively, while US rates were flat, following a 3% increase in Q3 2024. Asia saw 3% composite rate decreases. Europe and Canada both recorded declines of 2%, while Latin America and the Caribbean (LAC) and India, Middle East, and Africa (IMEA) experienced increases of 1%.

“The softening of rates across property, financial lines, and cyber are a positive development for clients, while the challenges in other areas of the market, particularly in US casualty, are acute,” said John Donnelly, global head of Placement, Marsh, in a statement.

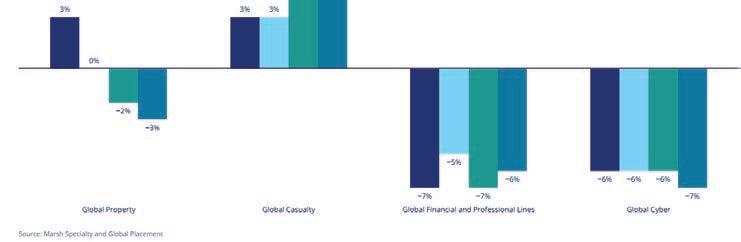

Global product line trends, Q4 2024

Property rates declined 3% globally during Q4 2024, following a 2% decline in the prior quarter. The Pacific region experienced the largest decrease, at 8%. In the US, property rates declined 4%, compared to a drop of 1% in the prior quarter. The UK rate decrease of 4% was level with Q3 2024, while Canada saw average decreases of 3%, compared with 1% in the prior quarter. Property rates were flat in Europe, continuing a moderation in the pace of increases. IMEA experienced a 3% increase in Q4, while LAC recorded a decline of

property insurance rates of 1% (versus a 3% hike in Q3 2024), marking the first decrease in 25 quarters. Asia’s property insurance rates declined 3%, level with the previous quarter.

Marsh said the global property market remains sensitive to loss events, particularly the ongoing Los Angeles wildfires, which will likely affect aggregate catastrophe losses in 2025.

Casualty insurance rates again were the only major coverage line to show an increase globally, rising 4% in Q4 2024, compared to an increase of 6% in the prior quarter. US casualty rates saw the largest increase at 7%, driven largely by excess/umbrella rates (versus an increase of 10% in Q3 2024). Latin America and the Caribbean experienced a 5% increase, while all other regions ranged from 2% declines to 1% increases.

Financial and professional rates decreased by 6% globally (versus a drop of 7% in Q3 2024). This marked the 10th consecutive quarter of FINPRO rate decreases.

Q4 rate declines were recorded in every region as a result of robust competition and available capacity.

Cyber insurance rates decreased 7% globally, following a 6% decline in the previous quarter. Every region saw rate decreases driven by strong competition among incumbent and new insurers as well as continued improvements in cybersecurity at many companies, Marsh said.

The Marsh report came out a week after USI Insurance Services reported that the commercial property insurance market in the US is showing signs of stabilizing.

USI's 2025 Commercial Property & Casualty Market Outlook noted that accounts with unfavorable loss experience will likely see rates increase by 5-15% in the first half of 2025, compared to 10-20% increases in the second half of 2024.

* Note: References to rate and rate movements in this report are averages. We have rounded percentages on rate movements to the nearest whole number.

Global and US composite insurance rate changes

Global product line trends, Q4 2024

Four cornerstones of a healthy insurance market

Mark Berven, President and COO, Nationwide Property & Casualty

hen I graduated from college, I didn’t anticipate a career in the insurance industry. Thirty years later, I couldn’t be more grateful for where my journey led me. Whether it’s helping a homeowner rebuild after a hurricane, supporting a businessowner with unique risks or helping a farmer improve grain-bin safety, I’m part of a company that makes a difference in people’s lives — and that never gets old.

Something else that’s kept me energized all these years is the belief that insurance benefits society as a whole. A healthy insurance market is an integral part of a healthy economy and healthy communities. As risks become more complex, and severe weather intensifies, we have a responsibility to protect the long-term health of the industry we love.

In my view, there are four cornerstones of a healthy insurance market for consumers: protection, affordability, resilience and partnership.

Protection

At its core, the purpose of insurance is to protect customers and help them mitigate their unique risks. Traditionally, our industry has had a “repair and replace” mentality focused on helping customers when they have a claim. This is still a critical part of what we do, but we can add more value by offering proactive tips and solutions to help customers avoid claims in the first place. For example, telematics devices can provide real-time feedback on a customer’s driving habits, and sensors can spot potentially dangerous electrical issues in their home or business. As part of this shift to a “predict and prevent” mindset, carriers partnering with distribution professionals need to develop tailored solutions that make it easier for clients to find the specialized protection that’s right for them.

Affordability

Providing specialized protection isn’t enough. The solutions we offer must fit into consumers’ budgets, which continue to be squeezed by economic factors such as inflation. To ensure that customers can manage the costs of the coverage they need, our industry must continue to invest in technology and innovations that simplify the end-to-end insurance process. We also need to make it harder for bad actors to abuse the legal system through “nuclear verdicts” that deepen the pockets of billboard attorneys and shadow investors while driving up costs for consumers.

Resilience

According to AccuWeather, the historic 2024 Atlantic hurricane season resulted in a staggering $500 billion in damages and is one of the most expensive ever recorded. As severe weather risks rise, including more frequent tornadoes and wildfires, we have a responsibility to make homes, businesses and communities more resilient. Research from leading organizations such as the Insurance Institute for Business & Home Safety (IBHS) shows that one of the most effective ways to achieve this goal is to modernize building codes across the country. It’s been encouraging to see a growing number of industry leaders, distribution professionals and policymakers join the call for stronger building codes, and I’m hopeful that our collective voices will drive positive change.

Partnership

A healthy insurance market can be achieved only through strong partnerships between carriers, distribution professionals, policymakers and customers. As risks become increasingly complex, the collaboration between carriers and distribution professionals is especially important. That’s why Nationwide has sharpened our appetite and developed the tailored offerings and risk expertise that allow our distribution partners to meet their clients’ specialized protection needs.

Nationwide founder Murray Lincoln said:

“We can accomplish more together than we can alone.”

This statement has never been truer than it is today. We look forward to working with you to support your clients and ensure a healthy insurance market for all.

$4.5 Billion

The amount 2024 pet insurance premiums are expected to total when all the numbers are crunched from last year, according to AM Best’s new market segment report, Mixed Early Pet Insurance Results but Inland Marine Remains Strong.

The number of mopeds towed, impounded, or seized last year in Boston. The city is considering permit and insurance regulations for food delivery services and other third-party drivers, including mopeds, e-bikes and scooters. The permit would require companies to have liability insurance coverage for all drivers using their platform. The ordinance is meant to address growing resident public safety complaints.

85.3%

The increase in U.S. natural disaster property and casualty claims, which hit to $217.8 billion in 2024, an 85.3% increase from 2023 according to Aon PLC.

$4.88 Million

The record-high average cost of a data breach reached in July 2024 — a 10% increase from the prior year and the highest increase since the pandemic, according to the July 2024 IBMPonemon Cost of a Data Breach study.

Declarations

Los Angeles County Fires

“We’re seeing total losses. We’re going out there and there’s really nothing to see. We’re maybe measuring the perimeter of a building trying to figure out a little bit what the structure looked like, if there’s any personal property left — that kind of thing.”

— Thomas Carstens, vice president, U.S. property/casualty for Crawford, speaking about assessing properties damaged by January’s Los Angeles County wildfires. At the end of January, preliminary data show insurance companies had already paid out more than $4 billion for losses from the biggest two of the Los Angeles-area wildfires that swept through the region and destroyed tens of thousands of homes. Insured loss estimates currently range from $8 to $20 billion.

Funding Recovery in North Carolina

“If we don’t have projects in the pipe, our contractors will leave. They’ve said it out loud. And if they leave, honestly, with eastern recovery, we will not have the ability to put it back together.”

— North Carolina Office of Recovery and Resiliency leader Pryor Gibson describing ongoing struggles with retaining a reliable base of contractors due to a lack of funds. Gibson called the situation a “double jeopardy” that could only be solved by “dependable money” rather than piecemeal funding from the legislature. The state is still struggling to recover from the devastating impact of Hurricane Helene in September 2024.

Electric Vehicle Pushback

“We’re determined not to be left behind.” — Plug Zen CEO Q Johnson in response to the new federal administration’s pushback against electric vehicles. Johnson’s Detroitbased company focuses on EV charging capabilities for companies that have fleets of cars and trucks. Johnson said he’s taking a “wait and see” approach,” but that he regularly works with people in the Michigan EV industry, and said he doesn’t expect them to dramatically change direction.

Measuring Methane

“There’s no consistency. We’re talking about an industry that’s incredibly diverse, hundreds and hundreds of companies in the U.S. alone that are engaged in oil and gas development. Each one may have a different voluntary program (to reduce methane emissions) that they’re implementing with different technologies, and so it’s really hard to have an apples-toapples comparison.”

— Jon Goldstein, vice president of energy transition at the Environmental Defense Fund in response to various reports citing lower methane levels released from certain oil and gas equipment and oil wells in 2023.

Reagan’s Challenging Airspace

“You definitely are bringing your A-game when you fly in and out of Reagan.”

— Former long-time commercial airline pilot Kathleen Bangs. Pilots who fly in and out of Washington D.C.’s Reagan Washington International Airport have long said the congested airspace can be challenging and even dangerous to maneuver. In January, the airport was the site of a collision between a commercial aircraft and military helicopter that resulted in 67 deaths.

Pollution Regulation

“If you’re allowing the polluter to determine how the cleanup and the notification is done, you’re bound to run into some problems. It is essential that the state has the authority to regulate these types of releases and these types of facilities, because we can’t expect them to hold themselves accountable.”

— Zachary Ogaz, general counsel for the New Mexico Environment Department. The state is in an ongoing battle regarding environmental clean-up of per- or polyfluoroalkyl substances (PFAS) from Cannon Air Force Base. A separate battle over Cannon’s culpability is a bellwether case in national litigation over the federal government's liability.

News & Markets

Chubb Posts Record P/C Underwriting Income for Q4 and 2024

By Chad Hemenway

Chubb posted record property/casualty underwriting income of about $1.6 billion, up 3.8% during the last quarter of 2024.

Fourth-quarter net income was down 22% to about $2.6 billion compared to the same period a year ago, but the Whitehouse Station, New Jersey-based insurer finished the fourth quarter with a combined ratio of 85.7

Chubb said the drop in Q4 net income was due to a tax benefit last year of more than $1 billion from enactment of a tax law in Bermuda.

Pretax Q4 catastrophe losses were $607 million compared to $300 million a year ago. Hurricane Milton alone caused $309 million in Q4 catastrophe losses, Chubb said. Global P/C growth in net premiums was 6.7% for Q4 2024.

CEO Evan G. Greenberg in a statement acknowledged the California wildfires as a “terrible tragedy” and added that the

insurer was on the ground, “endeavoring to assist our policyholders who have lost property, been displaced from their homes and businesses, and had their lives severely disrupted.”

He said the initial estimate of Chubb’s

catastrophe losses from the fires, to be recorded in Q1 2025, is about $1.5 billion.

P/C underwriting income for all of 2024 was also a record, according to Chubb. Underwriting income came in up 7.1% compared to last year at about $5.9 billion, and the insurer posted a combined ratio for the year of 86.6.

Chubb said net income for 2024 was also a record at about $9.3 billion, up 2.7%.

Pretax catastrophe losses were higher at about $2.4 billion compared to about $1.8

billion for 2023.

Chubb finished 2024 with global P/C net premiums written up 9.6%.

‘Overall market conditions are quite favorable, and we see really good growth opportunity for over 80% of our global P/C business, commercial and consumer, as well as our life business.’

– Evan G. Greenberg, CEO, Chubb

Greenberg in a statement said Chubb’s results for the full year were “the best in our company’s history." He added: “Overall market conditions are quite favorable, and we see really good growth opportunity for over 80% of our global P/C business, commercial and consumer, as well as our life business.”

Net Income at Selective Insurance Drops on Unfavorable Casualty Reserve Development

By Chad Hemenway

Selective Insurance Group reported a 24% drop in fourth-quarter 2024 net income as its chief executive admitted the year did “not meet expectations.”

Fourth-quarter net income was $93.2 million compared to $122.5 million a year ago. Net income for the year was down 44% to $197.8 million from $356 million for 2023.

CEO John J. Marchioni said Branchville, New Jersey-based Selective took “meaningful actions to strengthen casualty reserves in response to social inflation.”

Selective recorded $100 million in unfavorable prior year reserve development in casualty during Q4, driven by recent accident years in general liability and excess and surplus lines. Most of the unfavorable reserve development was in

commercial lines—$100 million in general liability offset by favorable development of $25 million in workers’ compensation. This added 8.5 points to the Q4 combined ratio in commercial lines, which came in at 100.2 compared to 93.1 during the same period in 2023. Net premiums written (NPW) in the standard commercial lines segment were up 9% for the last quarter of 2024 and up 11% for the year.

Selective, the holding company for 10 P/C insurers that offer standard and specialty commercial and personal insurance products via independent agents, reported an overall Q4 combined ratio of 98.5, up 4.8 points from the period a year ago.

For the year, the combined ratio was 103 compared to 96.5 in 2023.

Selective’s E&S segment, which represents 14% of total NPW, saw the Q4 combined ratio shoot up to 93.1 from 76.2 a year ago. Prior year reserve development on casualty lines of $20 million added 14.2 points compared to no adverse reserve development a year ago. New business in E&S grew 29% in Q4. Net premiums written were up 27% to $152.6 million in Q4, and were up 29% to $567.2 million for the year.

In the standard personal lines segment, net premiums written in Q4 decreased 3%. Retention was down and new business was cut in half during the period due to “deliberate profit-improvement actions,” Selective said. The combined ratio for the segment improved to 91.7 from 116.9 for Q4 and to 109.3 in 2024 from 121.7 in 2023.

Travelers Posts 28% Increase in Q4 Net Income

By Chad Hemenway

The Travelers Cos. said fourth-quarter 2024 and full-year net income increased 28% and 67%, respectively, on strong underlying underwriting results.

Travelers posted fourth-quarter net income of about $2.1 billion compared to about $1.6 billion during the last quarter of 2023. Full-year 2024 net income was nearly $5 billion compared to about $3 billion for 2023.

The New York-based insurer’s combined ratio improved 2.6 points to 83.2 for Q4 2024 and was up 4.5 points to 92.5 for the full year.

Catastrophe losses of $175 million in Q4 2024 were mostly the result of Hurricane Milton as well as an adjustment in losses from Hurricane Helene in the third quarter. Catastrophe losses were about $3.3

billion for all off 2024—about $344 million higher than the prior year—due primarily to Helene and wind and hailstorms in multiple states.

The consolidated underwriting gain at Travelers was about $1.8 billion in Q4 2024 compared to $1.4 billion in Q4 2023. Underwriting profit was up more than $2 billion to nearly $3 billion for full-year 2024.

Underwriting results for the last quarter

and full year also included favorable prior year reserve development of $262 million and $709 million, respectively.

Underwriting income in Travelers’ business insurance and personal insurance segments were nearly identical ($808 million and $807 million) for Q4 2024.

For the year, the personal lines segment reversed a 2023 loss of $817 million by recording underwriting profit of $827 million for 2024.

Travelers said Q4 2024 net written premiums in business insurance of about $5.4 billion increased 8% over Q4 2023 on strong renewal premiums and retention. In personal insurance, NPW for the last quarter were about $4.3 billion, up 7% on renewal premium changes.

Business Moves

National

Waner Pacific, Acrisure

General agency Warner Pacific, based in Westlake Village, California, acquired five general agencies from broker and fintech specialist Acrisure.

The five Acrisure General Agencies moving under Warner Pacific include Employee Benefit Risk Management, Oak Brook, Illinois; Group Benefit LTD, Urbandale, Iowa; Professional Group Marketing, Brewster, New York; National United Brokers, Westerville, Ohio; and Mature Health Services, Palatine, Illinois.

East

Renaissance, Consolidated Insurance Agents Inc.

Independent insurance agency network Renaissance acquired the agency network business of Consolidated Insurance Agents Inc. (CIA), based in Buffalo, New York. Carl Maranto is president of CIA.

Marsh McLennan Agency, Acumen Solutions Group LLC

Marsh McLennan Agency (MMA) acquired Acumen Solutions Group LLC, a Melville, New York-based insurance agency.

Acumen provides personal insurance, customized commercial insurance programs and administrative services. Acumen employees, including President Tony D’Elia, will join Marsh McLennan Agency and continue to operate out of Melville.

Union Bay Acquisition LLC, Loyalhanna Insurance Group

Union Bay Acquisition LLC, an aggregator of insurance agencies based in Lansdale, Pennsylvania, acquired Loyalhanna Insurance Group of Latrobe, Pennsylvania. Union Bay Acquisition LLC owns property/casualty insurance agent Union Bay Risk Advisors LLC.

Hub International Ltd., Byrnes Agency, Inc.

Insurance broker Hub International Ltd, headquartered in Chicago, acquired the assets of Byrnes Agency, Inc., located in Dayville and Norwich, Connecticut. The Byrnes Agency team of more than 25 associates will join Hub New England. Byrnes Agency will be referred to as Byrnes Agency, a Hub International company.

Relation Insurance Services acquired the assets of Forest Insurance Agency in Forest Park, Illinois. Dan Browne, president of Forest, will continue managing that office as a part of Relation.

WalkerHughes Insurance, headquartered in Indianapolis, Indiana, acquired Independent Brokers Agency LLC (IBA), a St. Louis, Missouri-based insurance agency. IBA represents WalkerHughes’ first acquisition outside of Indiana. Heather

Wessels, Principal of IBA, and Mike Swatske, Partner of IBA, will continue managing the St. Louis, Missouri office, assuming local leadership and continued business development roles as regional directors.

South Central

Clyde & Co, Tillman Batchelor LLP

Law firm Clyde & Co announced its merger with Dallas law firm Tillman Batchelor LLP. Mark Tillman and Colin Batchelor have joined Clyde & Co’s Dallas office as partners. Tillman Batchelor LLP served the litigation needs of domestic and international insurance carriers and their insureds, along with numerous other business entities on a direct representation basis throughout the U.S.

Southeast

ALKEME,

Professional Benefits Consultants

ALKEME, headquartered in Ladera Ranch, California, acquired Professional Benefits Consultants, based in Canton, Georgia. PBC offers a range of benefits and insurance coverage, including Medicare solutions, group health and compliance and administrative functions.

The Andrew Agency, Garriques, Lloyd & McMahon

The Andrew Agency, headquartered in Glen Allen, Virginia, acquired Garriques, Lloyd & McMahon (GLM) in Richmond, Virginia. Founded in 1963, GLM Insurance is a third-generation family-owned agency providing personal and commercial insurance throughout Virginia and North Carolina. The Andrews Agency is an independent agency serving the Mid-Atlantic region.

Ryan Specialty, Velocity Risk Underwriters

Ryan Specialty, headquartered in Chicago, plans to acquire Nashville-based Velocity Risk Underwriters, with a closing date early this year. Velocity Risk, providing coverage for catastrophe-exposed properties, is a managing general

underwriter that has been a part of Oaktree Capital Management. Velocity will become part of Ryan Specialty Underwriting Managers. As a component of this transaction, subject to regulatory approval, Velocity’s excess and surplus carrier, Velocity Specialty Insurance Company (VSIC), will be acquired by commercial property mutual insurance company FM, formerly FM Global.

Strate Insurance Group, Main Street Insurance Group

Strate Insurance Group in Morristown, Tennessee, is merging with Main Street Insurance Group, a 127-year-old agency with locations in North Carolina. The merged firm will operate as Strate Insurance Group, a Main Street Insurance Group Partner. All team members will remain with the new operation. Katherine Strate Smith will serve as partner and owner in Main Street, while Tom Strate will serve in an advisory role.

King Risk Partners, Bruce Hendry Insurance

King Risk Partners, based in Gainesville, Florida, acquired Bruce Hendry Insurance (BHI) in Immokalee, Florida. BHI has been in business for 45 years, serving much of the state, offering coverages through Nationwide, Travelers, Progressive, Mercury and other carriers.

West

Trucordia, Boulder Insurance Solutions

Trucordia, headquartered in Lindon, Utah, acquired the insurance business of Boulder Insurance Solutions in Colorado, a full-service brokerage serving small- to mid-sized companies. Trucordia was formerly PCF Insurance Services.

Heffernan Insurance Brokers, Green Financial

Heffernan Insurance Brokers, headquartered in Walnut Creek, California, acquired Green Financial in Kirkland, Washington. Fred Green, president of Green Financial, and his team have joined Heffernan Insurance Brokers’ small business division, HeffDirect.

Hub International Ltd.,

Woods Insurance Services, Inc.

Hub International Ltd., headquartered in Chicago, has acquired the assets of Woods Insurance Services Inc. in Farmington, New Mexico.

Owner and President Lyle Love and the Woods Insurance Services team will join Hub Southwest.

Woods Insurance Services will be referred to as Woods Insurance Services, a Hub International company.

Lincoln-Leavitt Insurance, headquartered in Lakeport, California, acquired Pyorre Insurance Agency. The Pyorre Insurance Agency’s Lakeport office will relocate to Lincoln-Leavitt Insurance’s location in Lakeport. Its Fort Bragg location will remain open. Leavitt Group is a privately held insurance brokerage with more than 90 agencies and 250 locations across 27 states.

Navion Insurance Associates Inc., Pegasus Capital & Insurance Services Inc.

Navion Insurance Associates Inc., headquartered in Yorba Linda, California, acquired Pegasus Capital & Insurance Services Inc., specializing in commercial insurance. Navion Insurance Associates is a retail insurance agency providing commercial and personal insurance products and services nationwide.

SageSure, headquartered in Jersey City, New Jersey, acquired GeoVera Advantage Insurance Services LLC in Fairfield, California. SageSure is a managing general agent specializing in catastrophe-exposed residential and commercial property insurance. GeoVera Nova Holdings oversees the growth and management of GeoVera Insurance Co., GeoVera Specialty Insurance Co., Coastal Select Insurance Co. and SafePort Insurance Co.

Arthur J. Gallagher & Co., Murray Gardner Insurance Agency Inc.

Arthur J. Gallagher & Co., headquartered

in Rolling Meadows, Illinois, acquired Tustin, California-based Murray Gardner Insurance Agency Inc., dba BMR Insurance. Gary Arch and his team will remain in their current location under the direction of Scott Firestone, head of Gallagher’s Southwest region retail property/casualty brokerage operations.

World Insurance Associates LLC, Business Contractors Insurance Services

World Insurance Associates LLC, headquartered in Iselin, New Jersey, acquired the business of Business Contractors Insurance Services (BCIS) in Santee, California. BCIS provides insurance services to individuals and businesses.

Hub International Ltd.,

Jackson Hole Insurance LLC

Hub International Ltd., based in Chicago, acquired the assets of Jackson Hole Insurance LLC in Wyoming. Evan Molyneaux, president, and Geoff Whitaker, senior sales executive, will join Hub Mountain. Jackson Hole Insurance will be referred to as Jackson Hole Insurance, a Hub International company.

Hub International Ltd.,

Great Basin Insurance Inc.

Hub International Ltd. also acquired the assets of Great Basin Insurance Inc. Agency Partners Dana Loreman and Bill Gilmore Jr. and their team will join Hub Northwest. Great Basin Insurance will be referred to as Great Basin Insurance, a Hub International company. Great Basin Insurance has locations in Klamath Falls and Springfield, Oregon.

International

Guy Carpenter, Carpenter Turner

Guy Carpenter, headquartered in New York City, acquired a 51.5% stake of Carpenter Turner, an Athens-based regional leader in the reinsurance broking and advisory business.

Carpenter Turner’s CEO, Alexander Turner, becomes CEO, Guy Carpenter Greece, reporting to Julian Enoizi, CEO, Guy Carpenter Europe. The agency is now operating as Guy Carpenter Greece.

People

National

AM Best, headquartered in Oldwick, New Jersey, appointed Kenneth J. Johnson as senior managing director and chief ratings officer. Stefan Holzberger became executive vice president and chief operating officer at AM Best Rating Services.

strategy, a new leadership role. Jack Jenner was promoted to a new role as managing director, international insurance.

Zurich

president of California. Sara Evans was named regional president for the Mountain West region.

Starr, headquartered in New York City, named Peter Hirs as chief financial officer, succeeding Howard I. Smith, who is retiring after more than 40 years at Starr and related entities.

The National Association of Mutual Insurance Companies (NAMIC) promoted Tony Cotto to assistant vice president and counsel for federal and political affairs.

Resilience, headquartered in New York City, named George Kotsiopoulos as president, insurance. The company named Gavin Reed as head of underwriting for North America.

Sarah Thompson is now global head of sales

Nor th America, headquartered in Schaumburg, Illinois, appointed Kristen Bessette as chief data officer. She most recently served as senior vice president and chief actuary for commercial insurance at Liberty Mutual Insurance in Boston.

Francisco Saldaña, a recent addition to Inszone, will serve as regional president for the Midwest.

Plymouth Rock Assurance, headquartered in Boston, named Ethan Tarby as president and CEO of Plymouth Rock Assurance Corporation. Tarby served as interim president and CEO since June 2024. He will lead Plymouth Rock’s Independent Agency Group.

East

Mark J. McDonnell as CEO. McDonnell replaces outgoing CEO and current board chair, Daniel C. Bridge. Brody N. Gilbert was named executive vice president and chief operating officer (COO).

NFP, an Aon company headquartered in New York City, named Patrick O’Neill as head of its Financial Institutions Group. He succeeds Lauren Kim, who was named the company’s regional managing director for P&C in the Northeast.

Inszone Insurance Services, headquartered in Sacramento, appointed Chris Tracy as regional

The governing committee of the Automobile Insurers Bureau of Massachusetts (AIB) appointed William H. Scully as president. Scully served as interim president, succeeding Kim A. Barber, who retired in April 2024. Scully served as vice president and chief actuary since 2020.

DeCotis Specialty Insurance, headquartered in Providence, Rhode Island, hired Chris-Michael Carangelo as a commercial lines broker.

Vermont Mutual, headquartered in Montpelier, Vermont, named company president

The MEMIC Group, headquartered in Portland, Maine, promoted Kaila McCracken to vice president of business intelligence and analysis. McCracken previously served as director of financial planning.

Harford Mutual Insurance Group, headquartered in Bel Air, Maryland, hired Shane Crockett as vice president and chief underwriting officer. Bryan Yekstat was named assistant vice president, claims. Matthew Summerell was promoted to assistant vice president, business development. Craig White joined Harford Mutual as director of information security.

Vermont Governor Phil Scott named Sandy Bigglestone as acting commissioner of the state’s Department of Financial Regulation.

Protecdiv, headquartered in Philadelphia, appointed Steve

Stefan Holzberger

Peter Hirs

George Kotsiopoulos

Sarah Thompson

Gavin Reed

Jack Jenner

Kristen Bessette

Patrick O'Neill

Lauren Kim

Sara Evans

Chris Tracy

Francisco Saldaña

William Scully

Chris Carangelo

Mark McDonnell

Kaila McCracken

Sandy Bigglestone

Skowronski as executive vice president and chief financial officer.

XS Brokers, headquartered in Quincy, Massachusetts, hired Annie Dawson as senior vice president to head national carrier relations and strategy. XS Brokers also named Scott Burns as senior vice president of its newly created product division for cyber liability.

The MEMIC Group, headquartered in Portland, Maine, promoted Matt Holbrook to vice president of data and analytics.

Holbrook most recently served as senior director of data, analytics and technology.

West

Front Row

Insurance Brokers LLC, headquartered in Vancouver, British Columbia, hired film insurance broker Tony “Anthony” Baratta to its Los Angeles office. Baratta joins Front Row after a 16-year career at Gallagher Entertainment, where he served as area senior vice president.

Washington State Insurance Commissioner Patty Kuderer hired members for her executive team at the Office of the Insurance Commissioner, including Andrew Davis, deputy commissioner for consumer protection; Tanya Lavoy, deputy commissioner for public affairs; Larry Robinette, tribal liaison; Tom Zuvela, chief financial officer; Sam Gutierrez, external communications manager and Alissa Julius, executive assistant to the commissioner.

The California Insurance Wholesalers Association (CIWA), promoted Yana Connors of CK Specialty to president from her previous role as vice president. Other promotions include Garett Kaneko of Amwins as vice president, Sarah Sloan of Paragon Insurance Holdings steps to the treasurer, and Aimee Bernadicou of Wholesure as secretary. John Donahue, also of Wholesure, transitions to the role of immediate past president. David Klayman of Seneca and Jack Else of Nationwide were named new board members.

Paige Maisonet to chief people officer. Maisonet oversees talent acquisition, people operations and employee experience.

Aspire, headquartered in Rancho Cucamonga, California, named Isaac Adams the vice president of product. Adams most recently served as Aspire’s chief marketing officer.

The Pacific Association of Domestic Insurance Companies (PADIC), headquartered in Auburn, California, elected Anisha Basi, general counsel for Pacific Specialty Insurance Company, to serve as PADIC president.

Midwest

Grange Insurance Company, headquartered in Columbus, Ohio, promoted Mike Hickman to vice president, national underwriting and business operations, a role serving on the company’s commercial lines leadership team.

Southeast

Justin Davis joined Alliant Insurance Services, headquartered in Irvine, California, as a producer within its employee benefits group.

Boston Mutual Life Insurance Company, headquartered in Canton, Massachusetts, appointed Bill Neely as regional sales director for North Florida in its distribution and business development department.

Brooks Insurance, a wholly owned subsidiary of Venbrook Group LLC headquartered in Los Angeles, hired Tiffani Ann Garabedian as senior vice president of underwriting.

Newfront, based in San Francisco, promoted

Grange Insurance Company, headquartered in Columbus, Ohio, promoted Mike Hickman to vice president, national underwriting and business operations.

Canopius, headquartered in Chicago, appointed Laura Burke as U.S. head of cyber and technology. Burke assumes the role after serving as executive vice president, cyber and technology, since joining the company in 2020.

Bradley Cassidy, based in Fort Myers, Florida, joined Alliant Insurance Services as vice president within its Alliant Americas division. Alliant is based in Irvine, California.

South Central

BenefitMall, headquartered in Dallas, appointed Tim Kealamakia to its team

as the new benefits sales executive for the Mountain West region.

Tokio Marine HCC, based in Houston, Texas, appointed Brendan Gaine to the new role of head of North American distribution. TMHCC also appointed Stuart Heath as head of distribution – international. Heath previously served as TMHCC’s head of delegated property

Steve Skowronski

Annie Dawson

Scott Burns

Matt Holbrook

Tony Baratta

Tiffani Garabedian

Paige Maisonet

Isaac Adams

Mike Hickman

Laura Burke

Tim Kealamakia

Special Report: Agency Salary Survey

Building and Retaining Talent: Salaries, Benefits, Culture Matter but That’s Not Always Enough

By Andrea Wells

Independent agency owners, producers, and support staff continue to report higher pay, according to Insurance Journal’s national online Agency Salary Survey results. But for the second year in a row, survey respondents report a decline in satisfaction when thinking about their compensation.

“When I hear from insurance professionals that they aren’t

happy with compensation, typically that is a symptom of something else,” said Mary Newgard, partner and senior search consultant for Capstone Search Group, a national recruiting firm dedicated to the insurance industry.

Newgard, also the author of Insurance Journal’s Ask the Insurance Recruiter monthly column, said when employees think about leaving, their dissatisfaction may be coming from other things built around compensation—not just money.

“Is the employee challenged in their role? Are there career advancement opportunities? Are they happy with the people

that they work with?”

Newgard said employees also may decide to leave out of concern for the future of the agency. Is the agency stable? Do the agency owners make good decisions? Does the employee enjoy the agency’s culture?

In today’s fast-paced, hard-market conditions, employees may feel overworked. “‘Do they just keep dumping on me more without recognizing where I'm at?’ These are the same kinds of secondary factors that are tied to compensation that employees consider important outside of compensation,” she said. Newgard said that years

ago these soft benefits were “wellness programs, gym memberships, increased benefits, and volunteer time off.”

“These things get bubble wrapped around compensation to make somebody a very happy employee and a retained employee,” she said.

Today, employees value a flexible work schedule, opportunities for career advancement, and culture. So, while compensation alone will make a few insurance professionals make a job change, more often employees leave when they feel an imbalance between comp, career opportunities, and agency culture, Newgard said.

“That’s when agencies see a lot of turnover, too,” she noted. “It might be easy for some agencies to change comp, but just changing comp alone is not usually good enough to correct retention issues.”

Finding balance between those key issues is important to retaining and maybe even attracting new talent, Newgard added.

Service Roles in High Demand

The hard insurance market—and the need to remarket accounts as a result—is pushing the demand for service roles even more than last year, according to Art Betancourt, founder and CEO of AEBetancourt, a national professional placement and executive recruiting firm for the industry.

Betancourt told Insurance Journal that in 2023, his firm saw recruiting efforts focused about 50/50 on service staff and producers. In 2024, his firm spent about 60% of its recruiting on service positions alone.

“We’re seeing a lot of agencies, especially with the hard market, with a huge need for service,” he said. He expects that need to continue to increase in 2025. “Even though we’ve seen an increase in employees in the sector, it is still nowhere close to enough to meet the demand, especially with all the retirements that continue to happen as the industry ages. Service is definitely a huge need.”

Newgard always tells her clients that the biggest role—and most frequent position to hire for—will always be the client service professional or account manager. Agencies compete with other firms, maybe even just across the street, for experienced talent.

“The job descriptions for account managers at those agencies is basically the same,” she said. It’s mostly a lateral move. “So, you have to ask the question: ‘What is it that’s going to attract somebody at my competitor’s office to come do that same role and that same function for me?’”

It’s a stronger compensation plan that builds in “different variables,” she said. Compensation “plus the other things wrapped around it will create the trifecta that every agency should be striving for,” she added. “Because if they strive for that trifecta of career advancement within the position itself, a very strong culture—however you choose to define that—and a strong, multifaceted compensation plan, then that helps you not only attract that talent but retain it.”

Some good news, according to Betancourt, is while service role salaries in independent continued on page 22

How Agencies Base Compensation Incentive Plans

Average Agency Salaries by Experience

Average CSR Salaries by Region

Average CSR Salaries by Region

Special Report: Agency Salary Survey

Average CSR Salaries

What Strategies Agencies Implemented

What Strategies Agencies Plan to Implement in 2025

What Benefits Agencies Offer

Changes to Health Insurance Plan

continued from page 21

agencies are not trending down, the upward pressure is not as aggressive as two years ago.

“Comp is still growing—we still see it trending up—but we’re not seeing as much of the crazy ‘we’ll pay anything’ type numbers, especially from the large national brokers,” he said. “We’re not seeing big comp packages as the reason people leave as much as we have in the past.” But he agrees that more movement is happening in service positions because of undesirable agency culture or when employees feel overworked. “People are willing to buckle down and get work done with limited resources, but they have to know that leadership is working to solve it.”

Skills Matter

Client-facing support people are extremely valuable in today’s hard market as agencies have seen increased workloads over the past several years.

Technical skills and insurance coverage knowledge will always be valued skillsets for customer support, but softer skills such as the ability to interact with clients—in a human way—could make account managers and CSRs even more valuable in the future, according to Kevin Stipe, partner and CEO of Reagan Consulting.

The price to hire a high-quality account manager or CSR has gone up nationwide as agencies compete for the best talent in a remote working world, he said.

“California and New York agencies were going into the heartland and offering people the opportunity to work remotely, and that bid up the compensation levels,” he said.

“But I think the thing that’s most interesting to me right

now is how AI is going to play into this.”

Artificial intelligence (AI) technologies are making big leaps in agency productivity on many fronts, Stipe said, but clients will always want a human. “So, the soft skills of client-facing support [people] are going to get more valuable as the technical skills that are also part of that job become more commoditized,” he predicted. “You can equip people with AI to be able to answer questions more effectively than before,” he said. But a computer is never going to be able to do what a human can do, Stipe said. “You want to trust a human being. You want empathy from a human being. You want a human being that can read the tone of your voice and respond,” he said.

“Customer service reps in our industry—really good ones—fuse together that empathy, emotional IQ, with technical knowledge and the ability to answer questions and adapt to situations and make sure things get done,” Stipe said. “I think what we’re going to see with AI is some of those technical skills, AI can handle, but AI can’t handle the emotional IQ stuff.” And those “soft human skills are so essential to have happy clients,” he said.

Newgard added that soft skills are as important now as they will be in the future.

“Agencies have thought about efficiency for a long time,” she told Insurance Journal. “It’s one of the reasons we see so many outsource policy administration to third-party companies.”

But as AI forces agencies to think about division of duties in different ways, it’s important to understand that technology will never be a solution for everything, she added.

“There is no technology that can replace parts of the process that require human interaction,” she said. There are elements within insurance that are transactional. “Some interactions can be automated, but when it comes to building relationships, working through conflict, and addressing complex needs, I don’t think AI can replace people.” This applies to many facets of an agency, from selling to and servicing clients to recruiting and retaining top talent, Newgard said.

Average CSR Salaries by Gender

Special Report: Agency Salary Survey

Survey Reveals How Work From Home Changed

Salaries, Total Income Jump Again in 2024 But Satisfaction Continues to Decline

By Andrea Wells

Insurance agency owners, producers, and support staff on average made more money in 2024, but for two years in a row, satisfaction with their compensation declined, according to the latest Agency Salary Survey, published annually by Insurance Journal. Changes in overall salary and total income rose again in all categories in 2024. Management/agency owners/ principals and producers/ sales both saw large increases in total income change from 2023 to 2024, while the support staff/CSR/account executives category revealed a slight increase in total income change compared to the previous year. (See chart on page 21.)

Surprisingly, satisfaction with compensation declined for the second year even though salaries and total income rose on average in all three categories.

Satisfaction with compensation fell in this year’s survey to an average of 3.27 (2024) from 3.36 (2023) last year. This is a

steady decline in the average satisfaction index scores of 2022 (3.61) and 2021 (3.41) Note: The Agency Compensation Satisfaction Index is based on a scale of 1-to-5 where “5” equals “most satisfied.” (See Agency Compensation Satisfaction Index chart, page 21.)

• Management/agency owners/agency principals reported a compensation satisfaction score of 3.76 in 2024, down slightly from 3.76 in 2023.

• Producers/sales reported satisfaction of 2.96 in 2024, down from 3.12 in 2023.

• Support staff/CSR/account executives reported a satisfaction score of 3.08 in 2024, down from 3.16 in 2023.

The score for overall satisfaction was higher when agencies offered employee benefits—both hard benefits (such as group health, life/ disability, dental, profit sharing, 401(k) plans, ESOPs, IRAs, and flexible savings accounts) and soft benefits (such as child care/day care, education reimbursement, pet insurance, and paid family leave). (See

Employee Benefit Satisfaction Index, page 24.)

Employee benefit satisfaction ranked highest when agencies offered added benefits such as child care/ day care (3.8), education reimbursement (3.76), profit sharing (3.76), stock options (3.62), and paid family leave (3.59). The survey found that in nearly all employee benefit categories queried, employees showed more satisfaction with overall compensation when those benefits were offered. The one exception this year was a slight decline in satisfaction when offered pension plans, perhaps due to limited

options of this benefit.

As noted, the survey revealed an upward trend in total compensation for all agency positions this year.

Producers/sales positions saw the highest increases in total compensation, according to this year’s survey.

The 2025 Agency Salary Survey, based on more than 500 responses nationwide, revealed that total income changes, which includes salary plus additional compensation such as profit sharing, bonuses, and other income, were:

• Agency owners, principals, and management total income increased 17.9% for 2024,

compared to a 16.1% increase in total income in 2023.

• Producers/sales total income increased the most in 2024 to 20.8%, compared to a 12.6% increase in 2023.

• Agency support staff total income showed a 11.3% increase for 2024, compared to a 9.6% increase for 2023.

Salaries only (excluding bonus and incentive income), also rose again in 2024, and at a higher rate than the previous year, according to this year’s survey results:

• Salaries for agency owners, principals, and management rose 15.8% in 2024, compared to 13.8% in 2023.

• Producers/sales reported average increases in salary of 17.9% in 2024, compared to 11.9% in 2023.

• Salaries for agency support staff rose 11.0% in 2024, compared to 8.0% in 2023.

Insurance Journal’s Agency Salary Survey collected about 500 responses from agency owners and employees nationwide via an online survey in January 2025. Paul Osbourne, senior analyst at Demotech Inc., assisted with analysis of this year’s survey results. For more information, contact Andrea Wells at: awells@insurance journal.com.

continued on page 26

Special Report: Agency Salary Survey

continued from page 25

News & Markets

Viewpoint: How Will the California FAIR Plan Fare? What’s Next for Independent Agents?

If there is a single bright spot to be found in the aftermath of the costliest wildfire in California’s history, it is that both the property/casualty insurance industry and the independent agents who serve as its personal point of contact with insureds now have a golden opportunity to remind consumers just how effective they can be when disasters occur.

By Rene Swan

Call to Action

Independent agents face an enormous call to service at a time when the state’s insurance market faces great uncertainty. The latest wildfires could not have come at a worse time for California, which has been beset by an insurance availability crisis as multiple carriers with considerable market share in the state have exited—in large part due to their inability to achieve rate adequacy through the state’s department of insurance.

2025, the department has already issued nonrenewal bans on more than 100 ZIP codes. The California Department of Insurance is also urging consumers to begin the claims process by contacting their insurer or agent to try and settle claims before contacting a public adjuster or an attorney.

In the weeks and months to come, claims adjusters will be tasked with assessing insured losses among more than 18,000 structures destroyed or damaged in the Eaton and Palisades fires. Each case requires the same degree of professionalism and care.

While it’s often tempting to paint a catastrophe of such magnitude in broader strokes (for example, insured losses likely ranging between $20 and $45 billion, the destruction spanning acreage three times the size of Manhattan), our focus must remain on serving those who put their trust in our hands.

Insureds need our industry to respond quickly and efficiently, and independent agents must once again rise to the challenge.

Now, however, is neither the time for semantics nor for pointing fingers. Rather, it is a time for solutions—and a new way forward.

Most recently, California Insurance Commissioner Ricardo Lara issued an emergency declaration allowing unlicensed claims adjusters to work— overseen by a qualified licensed adjuster, qualified manager, or insurer—to share the load in expediting the claims process. Carriers will still use their own adjusters or even contract with independent adjusters in handling the deluge of claims.

In the aftermath of any wildfire declaration of emergency by the governor, the commissioner is permitted to impose a one-year moratorium on non-renewals and cancellations in affected areas. For

The need for patience and empathy among independent agencies and their customer-service reps must be kept top of mind as the claims process mounts. Sincere empathy is the hallmark of any successful agency, but it must be consistently maintained—and members of those agencies, from the principal to the CSRs, must be cognizant of their own emotional well-being under tense conditions as the claims count grows, and agency staff have multiple conversations with insureds on one of the worst days of their lives.

Agency owners would do well to discuss this challenge with team members and keep an open dialogue with their agency-owner contemporaries to share best practices in claims handling.

Fate of the FAIR Plan

A large percentage of the insured losses from the Palisades and Eaton fires will

continued on page W4

STRENGTHENING OUR EXPERTISE

Congratulations, Kevin Chuc!

At the Surplus Line Association of California, we prioritize continuous learning and industry expertise to better serve our members. We’re proud to announce that Kevin Chuc, a key member of our Data Analysis team, has earned his California P&C insurance license, joining colleagues Yusuf Mayet and Paul Cruz in achieving this distinction. Their accomplishments play a key role in reinforcing trust and confidence in the surplus lines marketplace.

Congratulations, Kevin, on this milestone in your career!

VP, Legal Compliance

Kevin Chuc AVP, Data Analysis

Paul Cruz Insurance Analyst Manager

Yusuf Mayet

News & Markets

continued from page W2

be in homeowners. It’s estimated that roughly 22% and 12% of the structures destroyed in the Palisades and Eaton fires respectively are covered under the FAIR Plan.

‘Insureds need our industry to respond quickly and efficiently, and independent agents must once again rise to the challenge.’

Bear in mind that because FAIR Plan policies are limited to $3 million in coverage for dwellings, some homeowners will discover how much they might end up paying out of pocket when increased demand causes rebuilding costs for labor and materials to skyrocket. What’s more, the FAIR plan’s standard policy language limits coverage to actual cash value—basically, the depreciated value of the home.

Delays in rebuilding will also cause payouts to rise for displaced residents forced into long-term housing arrangements. Increased demand for such housing is already causing rental prices to swell, which will lead to higher additional living-expense claims for carriers—some of which may be limited by policy contractual language.

Yet, the larger question remains: What happens if the insured losses exceed the FAIR Plan’s resources?

It’s worth noting that the FAIR Plan was never intended to be a state-sponsored insurance fund. Firas Saleh, director of product management at Moody’s, noted in a blog the plan’s exposure in L.A. County was $112.2 billion with year-overyear growth of 53%, and that L.A. County exposure represents about 23% of the plan’s portfolio.

FAIR Plan President Victoria Roach recently reported that the plan has a surplus of nearly $377 million available for claims and expenses not yet incurred. Its total cash on hand is $1.4 billion, with the approximate $1 billion difference reserved for current outstanding liabilities such as loss reserves and expenses, commissions payable, and other incurred expenses. The plan does have reinsurance treaties in place, with payouts tied to losses exceeding the first $900 million.

Should the FAIR Plan prove unable to meet its compensatory obligations, California insurers are required to help pay those losses through assessments proportionate to their prior market shares, going back two years.

For the first $1 billion in personal lines and $1 billion in commercial lines assessments, insurers could seek to recoup half their share of the assessments through fees billed to policyholders. At the moment, it remains uncertain just what the plan’s total financial responsibility will be. While the plan has nearly $6 billion in exposure to potential loss from the Palisades Fire, for example, the plan recently estimated that its total losses might be closer to $3.75 billion—not a small number, but within its current ability pay, Roach has stated.

Balancing Act

Speculation also continues as to whether the insured losses incurred from the wildfires will put more pressure on an insurance market with coverage-availability issues. Without substantial regulatory actions, insurers will require incentives to write more property in the state. In 2023 and early 2024, major homeowners insurers including State Farm Mutual Insurance Co., Allstate, and Farmers either pulled back on or limited new business in California, raising questions about insurance availability for property—particularly in areas at high risk for wildfire, such as the wildland urban interface.

As 2024 ended, Lara announced a catastrophe modeling and ratemaking regulation to enable insurers to employ the models in their rate formulations. In return, carriers must increase their number of policies in wildfire-exposed areas equivalent to no less than 85% of their statewide market share.

If insurers can both utilize catastrophe models and pass along the cost of reinsurance, in theory it will make it easier for them to write more business in riskprone areas. Plus, if insurers can recoup

some or all of the cost of purchasing reinsurance, they could then buy more of it, enabling them to assume more wildfire exposures. Which, admittedly, is a lot of “if”s.

Time will tell if insurer appetite and legislative or regulatory action can be brought into balance over the next several years. If they cannot, it will prove increasingly difficult—and expensive—to obtain coverage in California.

Sparking Subrogation

While the causes of the fires have not yet been determined, those answers will help insurers determine whether they can subrogate claims.

Southern California Edison, which was found at fault for both the 2017 Thomas fire and Woolsey fire in 2018, is under scrutiny for its possible involvement in sparking the Eaton fire. Reports show residents saw flames at the base of a tower perched above Eaton Canyon, visible in photos and videos shared online. If the utility’s equipment is found to have caused the blaze, California law requires that the utility pay for the wildfire damages and recover its costs through a regulatory process.

On the Front Lines

In the meantime, California’s independent agents will continue to serve as the human face and friendly ear of our industry to those who have lost so much. Agencies that are members of a network have a competitive advantage in this area, as they have more opportunities to communicate across ZIP codes and learn what’s working for their fellow members in serving clients affected by this unfolding tragedy.

All agents with insureds affected by the devastation, however, have one thing in common: in the months to come, they have the opportunity to show just how compassionate and effective they can be in helping families navigate the slow road to resuming a life of relative normalcy.

And that is no small thing.

Swan is regional executive vice president/West for Renaissance, a network of independent insurance agencies.

My New Markets

Restaurants

Market Detail: Pacific Excess Insurance

Marketing is a wholesaler/ general agent with a specialty in restaurants and access to many standard, surplus lines and workers’ compensation markets. Highlights of Pacific Excess’s offerings include higher commissions; fast quotes; no premium volume requirements; markets for unique risks. Has pen; appointment required. Available Limits: Not disclosed

available), direct bill and flexible payment options; risk management tools; generous commissions. Available Limits: Umbrella limits up to $10 million (additional layers available).

Carrier: Admitted, rated A by AM Best States: Available in all states plus the District of Columbia.

Contact: Christa Van Zant; christa. vanzant@minico.com; 800-447-8383.

Defend the Shield Law

Enforcement

Liability Insurance

Market Detail: Offered by Waters Insurance Network and created specifically for law enforcement officers, Defend the Shield Law Enforcement Liability Insurance offers liability coverage and defense costs, as well as paycheck protection and Death in the Line of Duty coverage. Personal and portable. $1,500 maximum premium; $500 minimum premium; has pen.

Available Limits: Not disclosed.

Carrier: Various, both admitted and non-admitted.

States: Available in Arizona, Arkansas, California, Colorado, Connecticut, Florida, Georgia, Idaho, Illinois, Iowa, Kansas, Kentucky, Louisiana, Maine, Michigan, Missouri, Nebraska, Nevada, New Hampshire, New Jersey, New Mexico, New York, North Carolina, North Dakota, Ohio, Oklahoma, Oregon, South Carolina, South Dakota, Tennessee, Texas, Utah, Virginia, Washington, Wisconsin.

Contact: Barry Colburn; submissions@ pacificexcess.com; 800-222-5582.

Nonprofit Social Services Insurance

Market Detail: MiniCo Insurance, a leading source for insurance solutions and nonprofit intelligence for brokers and advisors, offers insurance coverage for nonprofits social services. We understand that nonprofits do not live in a vacuum; they follow their mission and rely heavily on the expertise and support of their insurance advisor. MiniCo has been a value provider in creating tailored insurance programs for nonprofits for over 30 years. It’s our mission to keep the needs of our brokers, advisors and their nonprofit clients satisfied, therefore providing peace of mind and security for many years.

Program features: Over 300 eligible classes; exclusive A.M. Best “A” rated admitted paper; separate limits for abuse and molestation; wide array of coverages tailored for nonprofits and social services; includes primary coverage for employed medical doctors; very competitive pricing; dedicated and flexible underwriting; umbrella limits up to $10 million (additional layers

Family Entertainment Centers

Market Detail: Bolton Street Programs’ Family Entertainment Center Safety Association (FECSA) Insurance Program has been providing comprehensive insurance products and solutions to the entertainment and leisure industry for over 25 years. This program provides robust insurance protection to many different types of family entertainment and related attractions, including motorized, movement, games and sport centers. The focus of this program is small to medium size location-based family entertainment centers, indoor and virtual golf, axe throwing, bowling alleys, ice skating rinks, roller skating rinks, miniature golf, batting cages, go-kart facilities, outdoor driving ranges, movie theaters, ride simulators, escape rooms, indoor laser tag, and arcades for building, personal property, and business income. All mobile equipment can be included under our inland marine coverage, such as inflatable rides, concessions, bumper cars, and go-karts. Coverage highlights: Property business income; general liability — $1 million per occurrence / $2 million products, completed operations; excess liability; $1 million employee benefits liability; workers’ compensation; minimum premium $3,500.

Available Limits: General liability — $1 million per occurrence / $2 million products, completed operations; $1 million employee benefits liability.

Carrier: Not disclosed.

States: Available in all states plus the District of Columbia.

Contact: Robert Sperber; rsperber@ sterlingrisk.com; 516-417-5107.

Carrier: SOPAC; non-admitted; not rated. States: Available in all states plus the District of Columbia.

Solutions offers transportation workers’ compensation coverage. Specialty Comp is a national workers’ compensation facility specializing in underwriting for middle market, hard-to-place, high hazard risks in various industries. Its team of skilled and experienced underwriters have access to a broad appetite and underwriting authority, providing leverage in accounts with more difficult underwriting conditions and environments. Underwriters are matched with industry leading safety, loss control and claim service professionals, as well as licensed in-house claim advisors and premium audit experts. Has pen; appointment required.

Available Limits: Not disclosed.

Carrier: Admitted; rated A by AM Best. States: Available in all states plus the District of Columbia.

Contact: Steven Math; steve.math@ specialtycompins.com; 214-453-2964.

Idea Exchange: The Competitive Advantage

Reviewing Historic Predictions

Back around 2013 (the copy I have is not dated, so I might be off a year), McKinsey & Company published a study that caused some angst within the industry. The study, “Agents of the Future: The Evolution of Property and Casualty Insurance Distribution,” posited that agents had long been local, and by inference, small.

By Chris Burand

Then they became controversial in the opening paragraph by noting how carriers and consumers no longer value, at least to the same extent, the historic benefits of the local agent who knew their customers well and generally provided good advice. Knowing customers well had served carriers and consumers well for 100 years.

From a carrier’s perspective, the upfront underwriting these agents provided was literally invaluable when done well. From a customer’s perspective, quality advice

and placing them with the right carrier was also invaluable although less visible.

McKinsey states on the first page this local knowledge had diminishing value because carriers were developing predictive modeling, an early form of AI in many ways, so they didn’t need the upfront underwriting and, therefore, didn’t need to pay for it. And consumers were effectively conditioned that insurance, particularly auto insurance, which is the largest line, was nothing more than a commodity.

The report suggested changes should have already happened, but the authors were seeing signs the changes were accelerating. They stated the following:

“Within five to 10 years:

• Most personal lines and small commercial customers will interact with their agents and carriers across the full range of channels: in-person, through mobile devices, and by phone, Internet and Video conference.

• Carriers will continue to use technology to increase their direct interaction with

the primary customer, delivering more consistent service at a lower cost.

• Agents will be compensated only for the unique value they deliver to the customer and the carrier.

• Carrier agent management models in both the IA and Exclusive channels will focus resources on those agents that deliver profitable business.

• Winning agents will deliver tailored and relevant expertise and excel at multichannel marketing, while increasing their scale and operational efficiency.”

If the authors were surprised these changes haven’t already occurred, they should be floored because the last three outcomes haven’t come close to happening in the 10-year window they forecast!

I don’t possess any true facts showing most personal lines and small commercial customers interact across the full range of channels. It seems to me most people like two channels, not three and not one, and preferences vary materially. I don’t have

any facts to prove I’m right, just anecdotal evidence in working with agents every day. Because preferences vary materially, agents need to be able to work across all modes, but any given customer doesn’t communicate using all modes.

Use of Technology

Carriers are definitely using more technology. Whether the use of such technology is delivering more consistent service at a lower cost is highly debatable. Similarly, whether carrier predictive modeling systems work is also debatable.

To prove the former point, per AM Best’s Aggregates & Averages for the year 2012, the P&C industry’s underwriting expense ratio excluding commission expense was 18.0%. The commission expense was 10.2%. Rent/Equipment was 1.8%, and All Other expense was 4.8%. (I don’t know whether predictive modeling costs are in Equipment or All Other.)

The same report for 2023 (published in 2024) states that underwriting expense excluding commission expense was 14.2%. This is a huge decrease. Commission expense increased to 10.8%. Rent/ Equipment expense decreased to 1.6%, and All Other expense decreased to 3.4%.

Carriers have become, other than commission expense, much more efficient. But has predictive modeling improved loss ratios? Per the McKinsey report, much of the focus on predictive modeling would be personal auto. The five-year private passenger auto liability loss ratio was 68.2% in the year ending 2023. The five-year average ending in 2012 was 65.2%! It’s a good thing carriers saved so much money so they could afford the higher loss ratio.

Predictive Predictions

Two key points McKinsey made have not come to fruition. Predictive modeling is not making the industry’s largest line more profitable from a loss ratio perspective. This is likely due to multiple factors including how the industry rarely manages to make an underwriting profit because of price competition. What may have occurred is that predictive modeling has worked to minimize rate increases. More likely what has happened—and

the evidence is strong for this—is that a handful of carriers have built predictive modeling software that works so well they don’t really need underwriters or agents. But most carriers have failed to do the same. The results I analyze in detail, carrier by carrier, show the ones who have the systems are eating the others’ lunches.

Second, carriers still believe in paying all agents the same regardless of the agent’s true financial contribution. In fact, it is obvious they are paying some distributors even more now, and yet many of those distributors’ value proposition has deteriorated. They’re just large enough to demand more money, and the carriers may pay because they haven’t developed quality systems which otherwise would have met McKinsey’s forecast.

Slow Mo

Another aspect is just how slowly this industry moves. The world may be moving faster and faster, but not this industry. Part of the reason might be how carrier boards of directors are designed and chosen, especially at the mutual carriers. The pace of change may be accelerating now because so many mutuals got caught with their pants down when interest rates increased almost simultaneously with the realization that they should never have been offering property reinsurance—much less property reinsurance with little geographic diversification. But maybe this acceleration is best described as we are now simply moving at a faster turtle’s pace.

And while 10 years later, McKinsey’s fifth bullet point hasn’t really been fully realized, undoubtedly, the winning strategy for traditional agents and brokers is still to be a professional who knows their customers and provides solid, educated advice. I do recommend changing the compensation model so the client pays you rather than the carrier. Note though: if the distributor is a roll-up acquirer, the traditional model is too expensive, which creates an even more lucrative opportunity for the traditional agent with patience.

Burand is the founder and owner of Burand & Associates LLC based in Pueblo, Colo. Phone: 719-4853868. E-mail: chris@burand-associates.com.

2024 AGENTS of the Year