Let the Big Dogs Eat. Join top business and community leaders at top-tier courses across the US in the #1 Charity Event In Golf.™

Make a Difference. Earn Rewards. Compete as a foursome or sponsor a local event for a chance to earn rewards, including a trip to the Applied Underwriters Invitational National Finals at Big Cedar Lodge.

Contact an Applied rep at 877-234-4450 or email invitational@auw.com to get started.

Follow us for a shot at even more rewards. Applied Underwriters Invitational® | #BigDogGolf invitational.com

Open more doors with Foremost ®

Stress and Opportunity

The first quarter of 2025 has been a whirlwind. New presidential administration. Historic wildfires. Financial market volatility. Trade war and tariff talks. A looming recession. Higher costs at the grocery store. Higher car repair bills. Higher cost of wood products including paper (this is a big one for Insurance Journal) Oh my. And yet through it all the insurance industry seems to be doing remarkably well. Many of the largest property and casualty insurers have set record incomes for 2024. But overall, I think it’s safe to say that stress is part of the picture for the industry and the clients it insures.

According to a recently released study by Sentry Insurance, more than two-thirds of polled executives reported feeling more stressed at the beginning of 2025 than they did at the start of 2024.

The survey, conducted by Wakefield Research on behalf of Sentry, found stress levels elevated in 67% of participants. At the same time, 74% of executives said they were not completely confident that their company’s current insurance coverage is adequate.

“Our research highlighted a recurring theme: managing risk is a big part of managing stress,” said David Dickinson, customer research director at Sentry. “Executives are experiencing worsening external challenges and putting strategies in place to protect the future of their businesses. This year, many are increasing safety measures, reassessing their insurance, and making adjustments to navigate external pressures.”

Wakefield Research polled 1,000 owners and C-suite leaders of U.S. companies for Sentry’s 2025 C-Suite Stress Index.

Nearly half (47%) of business leaders reported optimism that their companies will thrive this year. Of those optimists, 63% described the stress they face heading into 2025 as higher compared to this time last year.

Economic uncertainty (47%), supply chain challenges (44%), the cost of employee health care (41%), labor shortages (38%), and inflation (36%) ranked as the top five concerns among the survey participants.

In addition to economic and labor factors, 72% of surveyed execs expressed concerns about rising litigation and multi-million-dollar verdicts in their industry. Ninety percent said their business has been affected by severe weather in the past five years, with nearly two-thirds (63%) experiencing outages that left company, customer, or vendor systems temporarily inoperable.

‘Executives are experiencing worsening external challenges and putting strategies in place to protect the future of their businesses.’

Specifically on the insurance front, Sentry found that nearly all executives (97%) plan to re-evaluate their insurance policies this year.

Could this be an opportunity for agents and brokers to shine?

Yes, said Sentry, as some 43% of the respondents indicated they will re-evaluate their policies with an eye to adding insurance coverage to lower risks. Some 38% are looking to shore up areas where they are not currently covered but know they should be. What are you doing to respond to your clients’ worries and stress today? What more could you do?

Andrea Wells V.P. of Content

Chairman of the Board Mark Wells | mwells@wellsmedia.com

Marketing Administrator Alberto Vazquez | avazquez@insurancejournal.com

Marketing Director Derence Walk | dwalk@insurancejournal.com

DESIGN / WEB / VIDEO

V.P. of Design Guy Boccia | gboccia@insurancejournal.com

Web Team Lead

Josh Whitlow | jwhitlow@insurancejournal.com

Ad Ops Specialist Jeff Cardrant | jcardrant@insurancejournal.com

Web Developer Terrance Woest | twoest@wellsmedia.com

Web Developer Jason Chipp | jchipp@wellsmedia.com

Digital Content Manager

Ashley Cochrane | acochrane@insurancejournal.com

Videographer/Editor

Ashley Waldrop | awaldrop@insurancejournal.com

ACADEMY OF INSURANCE

Director Patrick Wraight | pwraight@ijacademy.com

Online Training Coordinator George Jack | gjack@ijacademy.com

The Secret Sauce: 3 Key Ingredients to Crafting Your Client’s Story of Risk

By Rami Levine, Director of Underwriting, AIU

As we approach the second quarter of 2025, the commercial property insurance market shows signs of softening — but not to the extent we have seen in previous cycles. Tighter market conditions are now a longterm reality across most property types including hospitality and frame habitational.

Last year, favorable underwriting results added stability and increased competition, especially in non-catastrophe-prone areas. However, insurance carriers continue to reassess their capacity and risk tolerance. While some insurers have already withdrawn from high-risk areas in California and Florida, those that remain are introducing new, more restrictive programs. Not every insurer or program will fit your client’s risk profile. That’s where your expertise as an agent becomes invaluable. Your ability to match the right programs to the right businesses requires an understanding of how to tell your client’s story of risk.

Effectively Position Your Client’s Risk in 3 Steps

1. Prepare all the ingredients you need. Sharing comprehensive details from the start makes it quicker for underwriting teams to review your submission and to determine if it’s a good fit. When preparing your submission, double-check you are including the following details:

• A cover note providing a quick and precise synopsis of risk

• Complete loss history inclusive of detailed claims information

• Clear target premium and deductible expectations

With these components laid out, underwriters can quickly provide indications and follow up with quotes soon after. For example, instead of simply stating that a property is being non-renewed, illustrate the full story: “This account is being non-renewed by Carrier X due to changing guidelines but has a clean five-year loss history and a target premium of $X.” This level of detail helps underwriters quickly determine competitiveness and leads to a streamlined process.

2. Get to know our appetite.

Understanding your insurer’s appetite for risk

— or the specific risks they prefer to write — saves everyone time and increases your chances of successfully placing business. When you take the time to learn which risks a particular program will cover, you dramatically increase your chances of binding coverage.

At AIU, our appetite is well-defined and focused on the three “H” industries: habitational, hospitality and healthcare. Within these sectors, specific guidelines correspond to location, loss history, and property maintenance standards. When agents familiarize themselves with these parameters, it significantly boosts the likelihood of success.

Stay in touch with insurers to better understand their appetite. Don’t be afraid to send a quick email asking, “I have a healthcare facility in this location—is that something you would consider?” or “Would this coastal property be an issue for your program?”

• Loss history, including past claims and steps taken to mitigate future risk

• Daily management practices, especially for seasonal or high-turnover properties

• Maintenance schedules and completed improvements

• Vacancy rates and tenant profiles, such as Section 8 or student housing

• Any previous non-renewals and the reasons behind them

The AIU team prides itself on quick responses and clear guidance. If you’re unsure whether a risk fits our appetite, just ask. If it doesn’t match, we’ll let you know quickly so you can explore other options. The key is keeping those communication channels open and active.

3. No mystery ingredients necessary.

Is there something in your client’s risk profile you are hesitant to disclose? Chances are your underwriter will find it anyway. Underwriters today have numerous tools to verify information, ranging from online search engines and artificial intelligence to property inspections and public records.

Omitting essential details about a property’s loss history, management practices, or tenant profile won’t remain hidden for long, but will erode trust and rapport.

Instead, be forthcoming and transparent about:

When you share the complete story upfront, you establish credibility and set the table for a more productive underwriting process — and a much stronger long-term partnership.

The recipe for a successful partnership

The renewal process is always another hurdle for agents and insureds, but with AIU, renewals are remarkably simple. AIU internally vets all program locations pre-renewal. Once a location is deemed eligible to renew, AIU does not require a full submission. Simplicity is a significant goal for us and those we partner with.

In today’s challenging market, finding the right partner for each client’s risk requires skill and knowledge. By providing complete information, understanding insurer appetites and maintaining transparency, you can position yourself as a valuable partner — both to your clients and the carriers you work with — in 2025

News & Markets

Liberty Mutual to Sunset Safeco Brand in 2026

By Chad Hemenway

Safeco Insurance will stop being a brand name in 2026, and Liberty Mutual Insurance will sell all of its personal lines products under the Liberty Mutual name.

Safeco has been Liberty Mutual’s brand for the independent agent channel to sell home, auto, and specialty business since Safeco was acquired by the Boston-based insurer in 2008.

“The Safeco legacy is one of strength, partnership, and an unwavering commitment to independent agents,” said Luke Bills, president of independent agent distribution, in a statement. “We will carry that legacy forward and will bring our agents even greater value with this brand change.”

But come 2026, the Safeco logo in agency offices—the same one that once adorned a Major League Baseball ballpark—will be replaced with Limu Emu and Doug. Novelties commemorating Safeco’s 100year anniversary in 2023 (born in Seattle by Hawthorne K. Dent as General Insurance Company of America) will be stored away.

Liberty Mutual, the sixth-largest writer of personal lines in the U.S., said the policies of Safeco customers will not be impacted and customers will keep their agent relationship. Liberty Mutual also uses direct distribution and licensed sales reps.

Transitioning away from the Safeco name will “fully harness the Liberty Mutual brand value for all of our customers, agents, and partners, across all distribution channels,” added Tyler Asher, Liberty Mutual chief distribution and marketing officer, US Retail Markets. Liberty Mutual said direct and independent agent channels will remain differentiated.

The Safeco brand will be retired in 2026.

“Importantly, this will significantly simplify our business, allow us to dedicate our considerable marketing power behind a single brand, and enable us to leverage and scale our technology to deliver unified but differentiated products and experiences across channels,” Asher added.

Since it was bought by Liberty Mutual, Safeco’s 22,000 or so independent agencies helped grow the business to $13 billion in annual premium, as the company sometimes stepped in to assume books of business from other insurers. It did so late last year, taking on the personal lines book of Main Street America. In September 2024, Safeco said it entered into a personal auto and umbrella lines book transfer agreement with Columbia Insurance Group.

Resilience: Third-Party Risk Involved in 31% of Cyber Claims

More merger-and-acquisition activity and technology consolidation have given cyber hackers plenty of entry points to exploit, making third-party cyber risk a dominant driver of claims for Resilience in 2024.

New research from the San Franciscobased cyber solutions company found 31% of claims it handled in 2024 dealt with third-party risk, including ransomware and outages affecting vendors.

“Third-party risk isn’t only making headlines—it’s driving unprecedented losses. While this risk is often invisible until it’s too late, it’s now clear that the industry has reached a tipping point,” said Vishaal “V8” Hariprasad, co-founder and CEO of Resilience.

“Businesses can no longer afford to consider their partners’ vulnerabilities as siloed from their own,” he said. “By understanding this new reality of shared risk, enterprises can make smarter

business decisions and meaningfully mitigate material loss.”

Third-party risk led to claims with incurred losses for the first time ever. Resilience said these claims made up 23% of incurred claims in 2024, compared to none in 2023.

Recent incidents such as Change Healthcare, CDK, and PowerSchool have highlighted how cyber hackers exploit single points of failure.

Ransomware kept its position as the top cause of loss in 2024. More than 60% of Resilience claims were related to ransomware.

The cyber insurer also flagged transfer fraud as rising in popularity. Claims involved transfer fraud made up 18% of incurred claims in 2024.

News & Markets

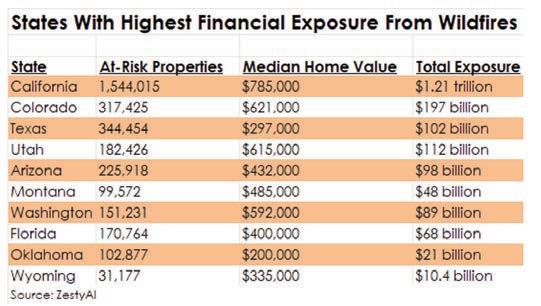

ZestyAI: More Than $2 Trillion in US Homes at High Risk of Wildfires

While Western wildfires have dominated disaster news for decades, new analysis using artificial intelligence shows millions of homes across the country—even in the swampy Southeast—are at risk for wildfires.

ZestyAI found that $2.15 trillion worth of U.S. residential property is at high risk of wildfire damage. The study assessed 126 million properties nationwide and revealed that 4.3 million individual homes face heightened wildfire risk.

“Wildfires are threatening more properties than ever before, with billions of dollars in exposure even in areas many people don’t associate with fire risk,” said Attila Toth, founder and CEO of ZestyAI.

The study used AI models trained on over 2,000 past wildfires and mapped exposure at the property level, integrating satellite and aerial imagery, topography, and structure-spe-

cific characteristics. The report found growing development abutting wildlands and intensifying climate conditions are driving higher wildfire risk in states like North Carolina (4.6% of homes at high risk), Kentucky (2.9%), Tennessee (2.3%), and even South Dakota (11.0%).

Unsurprisingly, California has the highest total exposure for wildfire damage, with over 1.54 million homes at risk and $1.21 trillion in total exposure. California was followed by Colorado, Texas, Utah,

and Arizona.

Because many areas are not historically prone to wildfires, homeowners may be unaware of risks and underinsured, Toth said. One in eight U.S. homeowners already lacks adequate insurance coverage.

On the other hand, Toth said, “Insurers have traditionally relied on broad, regional models that don’t account for individual property characteristics. That means some homeowners are denied coverage even when their true risk is much lower than their neighbors.”

Toth said that AI-driven risk analytics can mean more accurate and efficient assessments of wildfire exposure. Granular, property-specific insights can help insurers make smarter underwriting decisions—keeping coverage available in high-risk areas while ensuring that homeowners who take mitigation steps are recognized.

US Commercial Lines Prices Up 5.6% With Signs of Moderation: WTW Pricing Survey Reveals

U.S. commercial insurance rates showed a continued upward trend, with signs of moderation in the fourth quarter of 2024, according to the latest findings from WTW’s Commercial Lines Insurance Pricing Survey (CLIPS).

Carriers reported an aggregate price increase of 5.6% in the fourth quarter— down from the 6.1% rate recorded in the third quarter of 2024. WTW said in a

press release that specific coverage lines experienced “significant changes.”

“The fourth-quarter data shows a continued upward trend in overall pricing, with signs of moderation compared to prior quarters,” said Yi Jing, senior director of insurance consulting and technology at WTW. “Lines such as commercial auto and excess/umbrella liability continue to see notable price increases, while the commercial property market experienced a significant slowdown in pricing adjustments. These trends underscore key shifts within the commercial insurance landscape.”

Forty-one insurers representing approximately 20% of the U.S. commercial insurance market (excluding state workers compensation funds) participated in the survey.

Excess and umbrella liability recorded its highest price increase in the past three

years, while commercial auto recorded its highest price increase in CLIPS history and continued to rise in double digits.

The press release said that commercial property experienced “the most notable shift this quarter” with a moderate price increase that was significantly lower than the prior quarter.

Rate increases for mid-market accounts continued to moderate; this extended the trend from the previous quarter. WTW reported that small accounts also saw lower price increases compared to the prior quarter. Price increases for large accounts remained virtually unchanged.

CLIPS data is based on new and renewal business figures obtained directly from carriers underwriting the business. CLIPS participants represent a cross-section of U.S. P&C insurers that includes many of the top 10 commercial lines companies and the top 25 insurance groups in the U.S.

40%

The number of mid-market business owners who report their top area of investment for risk mitigation is technology/security, followed by security/cybersecurity enhancement (24%), labor/ staffing (19%), supply chain/supplier stability (17%), and training programs (11%), according to Nationwide's Risk Management Survey 2024 Insights Report. Small-market businesses plan to invest in technology/security (24%), followed by offerings/growth (21%), costs/revenue (20%), recruitment/employee retention (17%) and supply chain/supplier stability (14%).

21,500

4%

The amount the Congressional Budget Office (CBO) projects the GDP will drop by 2100, projecting future temperature increases versus if temperatures remain unchanged after 2024. The CBO gives a 5% chance that GDP in 2100 will be at least 21% lower than it would have been in the absence of additional changes in temperature.

The number of insurance industry job vacancies each year over the next decade, according to the Bureau of Labor Statistics. If current trends continue, the rate of new hires will not keep pace with retirements and other departures. Among Gen Z workers, 77% prioritize work-life balance, while 92% emphasize the importance of mental health in the workplace. These shifting attitudes will call for new ways of approaching the talent shortage.

$2.15

Trillion

The value of U.S. residential property at high risk for wildfire damage. Data analysis from ZestyAI assessed 126 million properties nationwide and found that 4.3 million individual homes face heightened wildfire risk. Growing development abutting wild lands and intensifying climate conditions are driving higher risk in states like North Carolina (4.6% of homes at high risk), Kentucky (2.9%), Tennessee (2.3%) and South Dakota (11.0%).

Declarations

D&O Dampening

“Despite recently favorable statutory underwriting results, the softer pricing of the past couple of years could ultimately dampen the financial performance of D&O insurers because the premium base to support future claims activity has diminished, even as risks are emerging and expanding.”

— AM Best commentary warning that recent softer pricing for directors and officers coverage could begin to affect insurers’ underwriting results. Renewal premiums for monoline D&O liability continued to fall during the first three months of 2025, particularly for companies involved in initial public offerings, special purpose acquisition companies, and de-SPAC companies.

Affordable Ag Insurance

“This type of crop insurance program is unique in that it was a bipartisan effort that originated in Delaware to help protect Delaware producers and our agriculture industry. This program is based upon a farmer’s choices in their risk management strategy and helping them select the right insurance plan for protecting their revenue.”

— Delaware Secretary of Agriculture Don Clifton explaining the state’s new insurance program, which promises to reduce premiums for 2025 crop insurance plans for producers who had an eligible plan in 2024.

Rx Regulations

“The notion that big government is going to be in anybody’s medicine box is not something that I think is reflective of where most Americans are at.”

— Joe Shields, managing director of Transparency-Rx, in response to Florida insurance regulators asking companies to hand over extensive amounts of data on people’s pharmacy claims, including personal information and prescription drug usage. The unusual move is raising privacy concerns.

Cyber Con Lawsuit

“Con artists are evil and will stop at nothing to steal everything you have… We already know that they target older Iowans, but now it seems that they even hunt through obituaries to target widows. They convince these older women that they need help and then send their victims to crypto ATMs. And the crypto ATM companies take a cut of the profits. It’s not just wrong, it’s illegal. I’m fighting to get Iowans their money back and force the crypto ATM companies to make big changes.”

— Iowa Attorney General Brenna Bird commenting on recent lawsuits the state filed against Bitcoin Depot and CoinFlip, Iowa’s two largest cryptocurrency ATM operators.

Dying Bees, Higher Prices

“The beekeeping industry has been warning for almost 20 years that we’re going to pass a point of no return at some point… Bees are the backbone of agriculture. All things that make food delicious and nutritious come from honeybees.”

— Blake Shook, a Texas beekeeper who co-founded a business that supports others in the bee business, noting the impact of the high number of bee deaths over the past year. Shook said the decrease in bees could impact the price of fruits, vegetables and other foods that rely on bee pollination for growth. Texas is one of the nation’s top beekeeping states.

California Fire Fund

“We have confidence in the fund.” — Edison International CEO Pedro Pizarro speaking on the California Wildfire Fund, which allows the state’s utilities to recover some wildfire-related claims payments. The $21 billion fund has been largely untapped by investor-owned utilities like Southern California Edison and may shield Edison International’s balance sheet if equipment owned by the company’s electric utility is found to have caused a deadly Los Angeles fire in January.

Business Moves

National

Arthur J. Gallagher & Co., Woodruff Sawyer Insurance brokerage

Arthur J. Gallagher & Co. has signed a definitive agreement to acquire Woodruff Sawyer for $1.2 billion.

Andy Barrengos, chairman and CEO of San Francisco-based Woodruff Sawyer, will operate under the direction of Peter Doyle, head of Gallagher’s U.S. retail property/ casualty brokerage operations.

The deal, expected to close in the second quarter of 2025, follows Gallagher’s much larger late 2024 agreement to acquire AssuredPartners for $13.45 billion for its middle-market reach.

Woodruff Sawyer is another middle-market play, but also has larger clients. The brokage offers commercial property/ casualty products, employee benefits solutions, and risk management services from 14 U.S. offices and one U.K. office.

In 2018, Woodruff Sawyer firm celebrated 100 years in business. The firm started out in life insurance as E.L. Woodruff & Sons in 1918.

Employee-owned Woodruff Sawyer ranked 24th in Insurance Journal’s 2024 Top 100 Independent Property/Casualty Agencies, with P/C revenue of about $214.7 million. AssuredPartners ranked fifth on Insurance Journal's list.

Gallagher said Woodruff Sawyer’s reported pro forma revenues and EBITDAC (Earnings Before Interest, Taxes, Depreciation, Amortization, and Coronavirus), with expected synergies, for the trailing 12 months ended December 31,

2024 were $268 million and $88 million respectively.

Rolling Meadows, Illinois-based Gallagher said integration costs and expected non-cash management retention costs are expected to total $150 million over the next three years.

East

Alera Group, Kaplansky Insurance Agency

Needham, Massachusetts-based Kaplansky Insurance Agency has been acquired by the national financial services firm Alera Group.

This new partnership brings more than 100 agents to add to Alera Group’s property/casualty offerings in the Northeast.

The independent agency was founded in 1974 in Brookline by Ely Kaplansky at the age of 22. The agency has grown into one of the largest privately held insurance agencies in the Northeast. Over the last 50 years, Kaplansky has completed 53 acquisitions and welcomed more than 50,000 clients.

The agency has 18 locations in Massachusetts and Rhode Island. Last month, Kaplansky disclosed it recently bought two central Massachusetts insurance agencies and a third in the western part of the state.

The Alera announcement said that Kaplansky Agency employees will continue serving clients in their existing roles.

Terms of the transaction were not disclosed. MarshBerry Capital acted as financial advisor to Kaplansky in the Alera

transaction.

Illinois-headquartered Alera Group is a privately-held independent financial services firm with $1.5 billion in gross revenue and 4,500 colleagues. Alera Group was formed in 2017 by the merger of 24 independent insurance firm and backing from Genstar Capital. In 2020 Alera received $150 million from The Carlyle Group to fund acquisitions.

Selectsys, Expert Insured

Tennessee-based Selectsys, an insurtech specializing in business process outsourcing, acquired Expert Insured, an artificial intelligence-led insurance management system for wholesalers, carriers and managing general agents.

Headquartered in Boston, Expert Insured has a new CEO, Spencer McDonald, previously with McKinsey & Co.

Expert said it utilizes AI-enhanced workflows and management tools to automate processes and improve efficiency for insurance companies.

Selectsys, with offices in Knoxville, Tennessee, has been around for more than 20 years, providing business processing and tech for MGAs and wholesalers, the company said.

NSM, New Mountain Capital

New Mountain Capital, an investment firm, has agreed to buy the commercial insurance division of Pennsylvania-based NSM Insurance Group.

The firms said in a news release that the deal is expected to close in the next 45 days. Terms were not disclosed.

Based in Conshohocken, outside of Philadelphia, NSM holds a portfolio of some 15 niche insurance programs as well as a retail brokerage. It has been supported by capital from Carlyle, a global investment firm.

Geof McKernan is CEO of NSM. He and Bill McKernan, president, will join the board of directors, but Aaron Miller, chief commercial lines officer at NSM, will be CEO of the division that will be part of New Capital. Miller has more than 20 years of experience in property-casualty commercial lines.

The new NSM commercial division will continue to be marketed as NSM until a new brand name is established, the companies said.

NSM was founded in 1990 and now has some $2 billion in premium.

New Capital, based in New York, said it has about $55 million in assets under management. The firm focuses on business growth and long-term capital appreciation.

Midwest

HUB International Limited, John L. Kiley Agency, dba DAR The Rocchio Agency

HUB International Limited, headquartered in Chicago, acquired the assets of John L. Kiley Agency, Inc. dba DAR The Rocchio Agency.

Headquartered in Carmel, Indiana, The Rocchio Agency is an independent insurance agency providing commercial and personal insurance and employee benefits services. Their expertise in the residential construction, including custom home building, and real estate development industries support Hub’s Specialty practices.

David Rocchio, sole owner, and The Rocchio Agency team will join Hub Midwest East. The Rocchio Agency will be referred to as The Rocchio Agency, a Hub International company.

HUB International Limited, Lindenwood Agency, Inc.

HUB International Limited, headquartered in Chicago, acquired the assets of Lindenwood Agency Inc.

Located in St. Charles, Missouri, Lindenwood Agency is one of the largest independent insurance agencies in St. Charles and has been in business for over 50 years.

The agency provides commercial and personal insurance to businesses and individuals in the local communities of Missouri and Illinois.

Melodie Smith, president, Ryan Mica, vice president, and the Lindenwood Agency team will join HUB Kansas and Missouri.

Lindenwood Agency will be referred to as Lindenwood Agency, a Hub

International company.

Arthur J. Gallagher & Co., Dyste Williams

Arthur J. Gallagher & Co., headquartered in Rolling Meadows, Illinois, acquired Dyste Williams, a Minneapolis-based retail insurance agency specializing in commercial lines, employee benefits and personal lines services in the Upper Midwest region.

Ted Dyste, Nels Dyste, and their team will maintain their current location, operating under the Gallagher Agency Alliance division. They will report to Jen Tadin, who heads Gallagher Select, the company’s U.S. property/casualty operations for small businesses and personal insurance.

The acquisition, announced on March 3, 2025, aims to strengthen Gallagher’s small business capabilities.

Gallagher Agency Alliance specifically focuses on merging with agencies specializing in small business property/casualty insurance and employee benefits.

Financial terms of the transaction were not disclosed.

Inzone Insurance Services, Kouri & Assosicates Inc.

Inszone Insurance Services, headquartered in Rancho Cordova, California, acquired Kouri & Associates Inc., based in Sioux Falls, South Dakota.

Kouri & Associates was established in 1970 when the Kouri family entered the insurance business. By 1977, they became an independent agency, focusing on personal lines and select commercial offerings for small businesses.

Bryan Kouri led the agency since 1990. Over the decades, Kouri & Associates has evolved to serve a broad range of policies, including homeowners, auto, life, and commercial coverages.

Under the Inszone Insurance umbrella, Bryan Kouri, partner Sheldon Koski and the Kouri & Associates team will continue to serve clients from their Sioux Falls office.

South Central

Artemis Insurance,

Ozark Insurance Agency

Artemis Insurance, a full-service

insurance agency and the new parent brand of Texan Insurance, announced its partnership with Louisiana-based Ozark Insurance Agency, a provider of personal and commercial insurance solutions for six decades.

Ozark Insurance Agency was founded by Robert “Bob” Mitchell in 1971. Originally started as a real estate agency, it branched into the insurance industry later that year. Bob’s son, Gary Mitchell, joined the agency in 1978 – he and his wife Elke bought it from his father in 1999.

In May 2019, Gary and Elke made the decision to retire and sold the business to their daughter and son-in-law – Kristi and Kyle Watson.

Kyle, Kristi, and their staff continue to serve the insurance needs of South Louisiana.

The Ozark Insurance Agency team will remain in place.

Higginbotham, EZ CERT

Higginbotham, headquartered in Fort Worth, Texas, forged an association with Program Insurance Group of Georgetown, Texas — also known as the home of EZ CERT, a nationally deployed insurance certificate tracking service.

Through the association, Higginbotham will acquire EZ CERT.

EZ CERT streamlines compliance, seeking to make the process seamless for franchisees; and to ensure that franchisors stay protected.

Program Insurance Group is an independent insurance agency that offers business, nonprofit and personal insurance to a range of clients in Texas, and specialized franchise insurance to entrepreneurs across the countrye.

Southeast

FM, Velocity Specialty Insurance Co.

Velocity’s excess and surplus (E&S) carrier, Velocity Specialty Insurance Co. (VSIC), will be acquired by Rhode Island-based global commercial property insurance company FM, subject to regulatory approval.

The deal will allow FM to expand into E&S property insurance.

National

Allianz Commercial, headquartered in New York City, appointed Jenna Contreras to the North American distribution team in the newly created role of portfolio solutions leader for wholesale and managing general agents (MGA) programs. Based in Chicago, Contreras leads the wholesale and MGA/programs’ key strategic broker trading relationships across the U.S. and Canada.

Ryan Specialty, headquartered in Chicago, promoted Dawn D’Onofrio to executive vice president and global chief underwriting officer of its specialty underwriting segment, Ryan Specialty Underwriting Managers. She most recently served as CEO of WKFC Underwriting Managers/ AgRisk/Ryan National Programs. Ravi Singhvi, president of WKFC Underwriting Managers, will continue to lead WKFC and AgRisk as the attritional property specialty of the merged entity.

Swiss Re’s commercial insurance arm, with U.S. headquarters in Armonk, New York, appointed Katie McGrath as chief underwriting officer. She assumes the role on June 1. McGrath, based in New York City, is currently CEO, North America. She succeeds Kera McDonald, who will serve as Swiss Re’s group chief underwriting officer.

president within its employee benefits group. Based in Atlanta, Georgia, Norris will work with a national client base. Alliant is based in Irvine, California.

East

Sadler Norris joined Alliant Insurance Services as vice

Midwest

Risk Strategies, headquartered in Boston, hired Craig D. Simon as managing director in its national private equity practice. Based in New York City, Simon has over 25 years of experience, previously serving as a team leader for U.S. energy and power at Marsh. Risk Strategies also named Melissa Lewis as chief operating officer, commercial lines. She succeeds Drew Carnase, who is retiring after over 30 years in the industry. Based in Overland Park, Kansas, Lewis joined Risk Strategies in 2023 and most recently served as senior director of business operations.

tered in Dallas, appointed Robert Conyers Jr. as energy practice leader. Conyers joined Brown & Riding in 2017 and became a principal in 2023.

Georgia, appointed Alex Faynberg as executive vice president and head of pet insurer Health Paws. Faynberg is currently division president of Chubb Workplace Benefits.

West

Novatae Risk Group, headquartered in Dallas, named Nick Greggains as president. Greggains has over 35 years of insurance industry experience, most recently serving as president and CEO of Ethos Specialty Insurance Services.

Price Forbes Re (PF Re), headquartered in London, appointed Sherman Power to the newly created role of executive vice president, alternative risk and capital solutions. Based in Dallas, Sherman joins from Aon Re, where he served as global head of innovation and capital advisory.

Southeast

Jami Long joined Robertson Ryan Insurance, headquartered in Milwaukee, Wisconsin, as chief financial officer (CFO). Long most recently served as CFO at WHR Global.

South Central

Brown & Riding, headquar-

Smart Choice, headquartered in Greensboro, North Carolina, promoted Jef Morgan to senior vice president of InsurTech. Morgan joined Smart Choice in 2011 and most recently served as vice president of recruiting.

Westchester, Chubb’s excess and surplus lines company headquartered in Alpharetta,

The Liberty Company, headquartered in Gainesville, Florida, appointed Derrick Martine as vice president, producer, employee benefits in its Irvine, California, office. Martine most recently served as an employee benefits advisor at Morris & Garritano Insurance Services.

LP Insurance Services LLC, headquartered in Reno, Nevada, named Cathy Santoni as director of commercial lines. Santoni has over 30 years of experience, most recently serving as vice president of risk services at Sequoia.

Ashley Powers and Trent Vance joined Alliant Insurance Services, based in Irvine, California, as senior vice presidents within its employee benefits group. Powers most recently served as vice president of client services at OneDigital. Vance served as an area vice president, health and welfare, at Gallagher.

Katie McGrath

Craig Simon Jami Long

Robert Conyers

Nick Greggains

Melissa Lewis

Derrick Martine

Cathy Santoni

Ashley Powers

Jef Morgan

Dear Reader:

Every business has a unique narrative, often intertwined with the personal experiences of its founders. Insurance Journal has had the privilege of encountering and appreciating countless captivating stories within the industry. Over time, we have observed the growth and transformation of the companies belonging to our readers and advertisers.

As a leading provider of industry news and information, we acknowledge that we cannot showcase every corporation that we come across. Our role as journalists also adds a layer of complexity to the process. Therefore, we have created this exclusive supplement to allow our clients and their associates to share their stories, in their own words.

We hope that you find this supplement both intriguing and educational. The team at Insurance Journal sends our best regards.

Data Driven Results

• $16.7 Billion total in-force premium

• $2.5 Billion / 17.6% premium growth

• 453 Independent Member Agencies signed

• 517

Average of new members annually

• 40+

National Strategic Partner Companies

SIAA advocates for data utilization in independent insurance agency operations. Why? You could say our results speak volumes, but we know sustained success happens by focusing on people.

To learn about our balanced approach to success and/or move your agency forward, contact us today. siaa.com info@siaa.com

THE POWER OF PARTNERSHIP

American Heritage Insurance Brokers owner Tatsiana Tarasava and Smart Choice-Colorado State Director Olga Ivchenko, CIC.

For this independent insurance agent and Team USA Aquathon athlete, partnering with Smart Choice was a winning strategy. After a role as a dedicated agent, she needed more coverage options for her clients and wanted to join a network that had clout with carriers. With over 10,000 partnered agencies, Smart Choice gave her just that along with higher commissions and greater profit sharing. WWW.SMARTCHOICEAGENTS.COM | 888.264.3388

“In a very challenging personal lines market, my state director helped me diversify into commercial lines with their Smart Start program where they provide all the expertise I need.”

THE POWER OF PARTNERSHIP

For this independent insurance agent, former competitive gymnast and winner of the Miss American Queen Pageant, partnering with Smart Choice helped her achieve the balance of full ownership while securing much needed market access. After a series of leadership positions at an A-rated carrier, she wanted to join a network that would help her rise to the top.

With over 10,000 partnered agencies, Smart Choice gave her just that along with higher commissions and profit sharing.

Here to help you reach for the stars.

“I met with several networks and Smart Choice won hands down. I had my list of non-negotiables, and they were able to meet and exceed every single one of them, and then some.”

The Castle Insurance Agency owner Jackie Morgan and Smart Choice Virginia State Director Roger Gill

Special Report: Agribusiness

Hard Market, High Tech: Ag Insurance Adapts

By Ezra Amacher

Faced with heightened climate risks and political uncertainties, insurers writing agribusiness and farm and ranch are deploying data analytics and technology as they grapple with a hard market and the need for greater transparency with their agricultural clients.

Insurers are turning to a variety of models for risk assessment and using the data to determine how to accurately assess and price risks in this asset-heavy industry, according to insurance professionals who specialize in agriculture.

“With wildfires obviously being all over the news and certainly being very prominent, a lot of insurance carriers are utilizing wildfire mapping and wildfire scoring systems to determine how likely or how probable [it is that] a certain location would be prone to wildfires,” said Chris Moore, president, EPIC Farm & Ranch.

While wildfires are most prevalent out West, mapping technologies indicate that Texas and Florida are also at risk for wildfires, making it a challenge to place coverage in those states, Moore said.

Carriers have become more cautious about insuring agribusiness in Midwest states heavily prone to severe winds and large windstorms.

“I think that derecho that took place in Iowa several years back made a lot of insurance companies take pause and reanalyze certain wind areas and how they need to map out potential wind severity,” Moore said.

As insurers tackle wildfires and extreme weather events, they’re also keeping a close eye on the uncertainty coming out of Washington, D.C.

“A change in administration can bring out exposures for our members,” said Jeff Gullickson, president, Western Growers Insurance Services. “Potential tariffs could impact their business; we’ve already seen a change in some markets as a result. There’s always a shortage of labor in specialty ag, and any sort of issues around that can impact the availability of that workforce.”

Gullickson said that a tariff in Canada, for example, could drive up the price of fertilizer in the U.S., creating an economic impact on the agriculture industry.

‘If this data could be accessible to the ag producers, it could give them better insight on climate risk and help them to make better decisions to reduce their exposure to the risk.’

“If oil goes up, diesel goes up; tractors and trucks and transportation is all dependent on diesel,” Gullickson added. “So, for the business issues around agriculture, the political landscape can change those week to week.”

A new administration also brings fresh concerns

over funding of the U.S. Department of Agriculture and crop insurance programs. The USDA plays a critical role in funding the ag industry, particularly after natural disasters.

The USDA dispersed $161 billion in financial assistance to agricultural producers from 2019 through 2023, according to a recent U.S. Government Accountability Office report.

The Trump administration has already shown a willingness to cut spending in the department.

“The impact of uncertainty can delay farm expansion and

crop decisions,” said Scott Tuxbury, EVP of Mountain States, XPT Specialty.

In contrast to the prior presidential administration, the White House will likely be less strict in enforcing environmental regulations, Tuxbury added. This could translate to less regulatory concern in the farming and ranching community.

Embracing technology

Insurance companies operating in the agriculture sector have turned to remote sensing, AI, and data analytics to improve risk assessment and claims processing.

“Insurers were early adapters of AI, and it is used extensively

in the underwriting and pricing of farm accounts,” Tuxbury said. “Imagery plays a significant role in individual account underwriting and allows for a more specific risk assessment of properties and locations. The fact that the data is readily available will also be important for the claim processing.”

While such data exists, more can be done to share information with customers about what goes into individual pricing models. Insurers would create more trust with customers by being transparent with how they use data, he said.

“As an industry, I don’t think we do a very good job of explaining pricing or risk assessment to customers,” Tuxbury said. “It is important to help them understand the benefits from AI and remote

sensing, in that they can have a direct impact on their pricing.”

Another way insurers can work with consumers is by sharing climate data they’ve accumulated over the years, according to Tuxbury. Insurers have been reluctant to share this data, which is primarily used for risk assessment, pricing, and risk concentration. Ag producers don’t generally have access to the data.

“If this data could be accessible to the ag producers, it could give them better insight on climate risk and help them to make better decisions to reduce their exposure to the risk,” Tuxbury said.

Other technologies have made their way to the agriculture industry in recent years, such as drones, telematics, and worker sensors.

In many cases the new technologies won’t impact the liability of the customer, Tuxbury said, but in certain cases they will. He pointed to the use of drones for more active activities, such as weed control (spraying) and fertilization, as an area where customers need to exercise discernment.

“This has presented significant liability exposure to those farmers and ranchers,” he said.

As for telematics, there can be a bit of hesitation to implement them in an auto fleet, but there’s direct evidence of the positive impact of telematics on fleet loss records and their claims, according to Gullickson.

‘Insurers were early adapters of AI, and it is used extensively in the underwriting and pricing of farm accounts.’

Whenever data is being collected and shared, it’s vital the broker understands where that information is going, he said, noting the importance of “making sure that you understand as a broker the technology the client is using and the application and how they’re applying that, and are you looking at available coverages to help them with that.”

Hard Market Persists

Insurance brokers specializing in farm and ranch make it clear that market conditions are harder today than in recent years.

“We were in a risk-on environment and we were able to get insurance companies to attach to risk pretty easily,”

Moore said. “Really over the past two years it’s been significantly more difficult to place property insurance. And I would say that statement is true across the entire country.”

Moore said reinsurance requirements are limiting how much risk insurance companies are able to take and pass on. Now if there’s too much risk at any one location or across the portfolio for an insurance company, there are more constraints around capacity, he said.

California, the largest food producer in the U.S., has fewer carriers who want to write agriculture in the state, said Gullickson, whose clients focus on specialty crops. There had been indication of softening in the California property market heading into the year, he said, but that was before the Los Angeles area wildfires.

“Obviously every broker out there is trying to put together property towers using multiple carriers to get coverage in place,” Gullickson said. “We’ve seen alternative funding options such as captives and parametrics. There’s some wildfire parametric coverage available.”

While parametric insurance has been a useful tool to address limitations of the current property insurance market, there’s a need for additional excess and surplus lines capacity, Moore said.

“If an account isn’t getting any offers from the standard market, I would say that there’s very few very excess of surplus line carriers that we can go to and that we can talk about the risk,” Moore said. “I understand that a lot of these companies avoid entering in this market space because it is a very niche area.”

News & Markets

Most Ransomware Claims Begin With Compromised Perimeter Security: Coalition

More than half of ransomware claims in 2024 started with threat actors compromising perimeter security appliances, according to a new report from Coalition.

In its Cyber Threat Index 2025, the insurance provider reported that 58% of claims began with such compromises.

UK-based IT services company

Netcentrix defines perimeter security as “a set of security measures designed to stop external threats from entering your network.” These include firewalls, intrusion protection and detection systems, and virtual private networks (VPNs).

Coalition found that VPNs and firewalls were the first and fourth most exploited technologies used for initial access last year.

The most commonly compromised products fall under a more general category of perimeter security appliances, Coalition said in the report, explaining that these devices “are often built into an organization’s physical networking infrastructure, typically offering both VPN and firewall functionality.” Vendors such as Fortinet, Cisco, SonicWall, Palo Alto Networks, and Microsoft build these products.

Remote desktop software was the second most exploited technology for

ransomware attacks, and email ranked third.

In addition to analyzing what technology was accessed in ransomware claims, Coalition also studied how that technology was compromised. This was defined in the report as a ransomware attack vector.

The threat index reported that compromised credentials were the most common attack vector, representing 47% of known initial access vectors (IAVs) in ransomware incidents. Such attacks typically targeted remote desktop protocol and VPNs, Coalition found, “which provide threat actors with privileged access to internal systems and networks,” the report said.

Coalition reported that software exploits were the second most common known IAV. These exploits typically take advantage of a vulnerable system, the report said. They can range from simple commands that exploit a single vulnerability to advanced espionage software that chains together multiple vulnerabilities, Coalition reported.

“While ransomware is a serious concern for all businesses, these insights demonstrate that threat actors’ ransomware playbook hasn’t evolved all that much—they’re still going after the same tried-and-true technologies with many of the same methods,” said Alok Ojha,

Coalition’s head of products, security.

“This means that businesses can have a reliable playbook, too, and should focus on mitigating the riskiest security issues first to reduce the likelihood of ransomware or another cyber attack,” Ojha said. “Continuous attack surface monitoring to detect these technologies and mitigate possible vulnerabilities could mean the difference between a threat and an incident.”

Coalition forecasted that the total number of published software vulnerabilities will increase to over 45,000 in 2025—a rate of nearly 4,000 per month and a 15% jump over the first 10 months of 2024.

“SMBs lack both the resources to patch a high number of vulnerabilities— requiring dedicated IT staff and testing infrastructure—as well as the experience to focus on the most pressing vulnerabilities,” the report said.

Coalition said its security recommendations are calibrated using data from its 360-degree perspective on cyber risk. Sources include digital forensics investigations, data collected from an internet-wide view by scanning every IPv4 address, proprietary AI models to analyze vulnerabilities and exposed login panels, and actuarial evidence from cyber insurance claims.

My New Markets

General and Professional Liability for Temp Staffing Companies

Market Detail: INVO Underwriting LLC offers general and professional liability for temp staffing companies across the entire U.S. From healthcare staffing to industrial and clerical positions, INVO Underwriting accepts a wide range of staffing operations. Through INVO Underwriting insurers can access StaffShield, a specialized team providing tailored insurance solutions for temporary staffing companies. INVO offers coverage for staffing services: general liability, staffing services professional liability and temporary staffing, or healthcare staffing. Whether a client needs general liability & professional liability as well as other ancillary lines, INVO can cover it. Program highlights include nationwide coverage, fast and easy submissions, ancillary lines, admitted and non-admitted options and competitive commissions. All classes welcome.

Available Limits: Not disclosed. Carrier: Not disclosed.

States: Available in all states and the District of Columbia.

Market Detail: QuoteWell, a tech-driven wholesale broker, offers markets targeting risks with <30% liquor sales (higher percentages considered), noting crime score and loss history will drive assault & battery coverage. Changes such as stricter liquor regulations and evolving consumer preferences can significantly impact risk assessments for dining establishments. Applicants with less than three years of restaurant management experience may be excluded. Ansul systems required over cooking surfaces and maintenance service frequency will be considered. BBQ restaurants need a smoker distance from the building of 10 feet or more. Submission requirements include but may not be limited to loss history, supplemental applications, website/Facebook/Instagram pages and ACORD applications. Minimum Premiums: General Liability: $750; Excess

Liability: $750-$5,000; Liquor Liability (<30% Liquor Sales): $750; and Commercial Property: $3,500-$5,000. Has pen.

Available Limits: Not disclosed. Carrier: Not disclosed States: Available in most states and the District of Columbia. Not available in Alaska, Florida and New York.

Market Detail: EliteMGA, LLC - Home Inspector E&O Insurance offers the essential coverage required to protect home inspectors from potential claims that could cost a lot. Error and omissions insurance offers clients peace of mind and businesses full coverage. EliteMGA’s home inspector insurance is uniquely positioned to offer tailored coverage at competitive rates through their own insurance captive, EliteRE. EliteRE is the first and only insurance carrier 100% dedicated to the home inspection industry and designed with home inspectors in mind. EliteMGA’s staff can customize a plan based on individual business needs to ensure they are fully protected when on the job. EliteMGA partners with HomeGauge and InterNACHI to offer benefits to members. Available Limits: Not disclosed Carrier: Not disclosed States: Available in all states and the District of Columbia.

carrier. Has pen.

Available Limits: $1,000,000 CSL Limit Carrier: Not disclosed.

States: Available in all states and the District of Columbia.

Market Detail: Insurance Allies is a boutique insurance brokerage and part of Specialty Program Group (HUB International), one of the largest sports and entertainment insurance teams in the country. Insurance Allies specializes in niche sectors of the entertainment industry. With a portfolio that includes over 1,000+ entertainment venues across the United States, their team is dedicated to providing tailored insurance solutions for high-adrenaline environments like axe throwing, escape rooms, go-kart facilities, smash rooms and more. Insurance Allies understands that price matters, but their mission prioritizes educating clients and ensuring coverages are comprehensive and aligned with the unique risks they face. Insurance Allies knows that each business is unique, and they take the time to understand what matters most to a business. As an independent brokerage, they have the flexibility to source the best policies from any provider, giving clients access to the most competitive and appropriate options.

Available Limits: Not disclosed.

Contact: Victor D’Angelo; wm@elitemga. com; 800-355-1185.

Unladen Liability

Market Detail: Innovative Risk has developed a mono-line Unladen Liability program for a broad range of customers who have both small and large transportation fleets. Includes available non-trucking liability, trucking liability, heavy trucks, commercial auto liability, short haul trucking and long-haul trucking. In the Unladen Liability program, Innovative Risk can provide underwriting solutions on an admitted basis for high-risk classes of business. Underwriter is A-rated, non-admitted

Carrier: Not disclosed.

States: Available in all states and the District of Columbia.

ASouthern California restaurant has been fined more than $1.1 million over wage theft and sick leave violations.

The California Labor Commissioner’s Office took the action against Food Source LLC, a Buena Park restaurant, issuing penalties for wage theft and failure to comply with paid sick leave laws that impacted at least 90 workers, with 73 employees owed more than $532,000 in unpaid wages, overtime, liquidated damages and incomplete wage statements.

to document sick leave availability on pay stubs and not providing supplemental paid sick leave during the COVID-19 pandemic.

Contractor Fined $430K for California Labor Violations

Aconstruction company was fined more than $430,000 for California labor violations that resulted in unpaid wages, overtime and other violations.

The state’s Labor Commissioner’s Office secured the settlement to return unpaid wages and damages to 86 carpenters employed by the Howood Company Inc. on construction projects in San Diego and San Bernardino counties.

The LCO also filed a lawsuit seeking nearly $576,000 in unpaid wages, damages and penalties related to the employer’s failure to provide sick leave. The suit also addresses violations such as denying workers access to paid sick leave, failing

Under California’s Healthy Workplace, Healthy Families Act of 2014, employees who work at least 30 days in a year are entitled to accrue paid sick leave, which can be used for personal or family health needs. The law requires employers to inform workers of their sick leave rights, document accrued balance and ensure access to leave when needed.

Justice Department Launches Hostile Workplace Probe into University of California

The Justice Department opened an investigation into the University of California to determine if the UC system has allowed an Antisemitic hostile work environment to exist on its campuses.

The investigation, being conducted under Title VII of the Civil Rights Act of 1964, will assess whether UC has engaged in a pattern or practice of discrimination based on race, religion and national origin

against its professors, staff and other employees.

According to an announcement by the Federal Task Force to Combat Anti-Semitism, the investigation aims to determine if the UC system allowed an Antisemitic hostile work environment to exist on its campuses.

According to Leo Terrell, a task force member and senior counsel to the Assistant Attorney General for Civil Rights, following the October 7, 2023, Hamas terror attacks in Israel, there has been an outbreak of antisemitic incidents at higher education institutions.

“The impact upon UC’s students has been the subject of considerable media attention and multiple federal investigations,” Terrell stated. “But these campuses are also workplaces, and the Jewish faculty and staff employed there deserve a working environment free of antisemitic hostility and hate.”

The fines were given to Howood Company, the general contractor, and two other employers, Wermers Multi-Family Corp. and JPI California Construction LLC, for multiple labor violations.

The L CO started an investigation when a complaint was received from the Carpenters/Contractors Cooperation Committee Inc. It was reported that several workers had not received their owed wages, while other complaints of wage theft were made on two additional construction projects involving Howood.

After the investigations, citations were issued for labor violations at all three projects. Howood reportedly did not pay its workers for several weeks on the following projects:

• 1600 Orange Ave, Redlands

• 4354-4364 Twain Ave, San Diego

• 1509-1521 Broadway, San Diego, CA 92101

The L CO is part of the Department of Industrial Relations.

News & Markets

Washington Senate Passes Restitution, Credit Scoring Study Bills

The Washington state Senate passed three bills with insurance implications in mid-March, including a bill giving the insurance commissioner the authority to order restitution to harmed policyholders and a bill studying the impacts of insurance rating factors like credit scores.

Senate Bill 5331 gives the commissioner the authority to order restitution for harmed policyholders. The commissioner can fine insurance entities that violate the law but can’t order them to pay restitution to the people they’ve victimized.

The bill, sponsored by Senator Adrian Cortes (D-Battle Ground), also authorizes

the commissioner to fine property/casualty insurance companies up to $10,000 per violation, rather than issue a total fine of $10,000.

Senate Bill 5589 was introduced by Insurance Commissioner Patty Kuderer and sponsored by state Sen. Bob Hasegawa, D-Seattle.

The bill would enable the commissioner’s office to analyze how insurance companies use credit history and credit-based insurance scores to understand premiums for lines of insurance like homeowners and auto.

Kuderer has raised concern about the reliance on algorithms and data determining premiums. The study would also look at factors that bill proponents believe could create unfair discriminatory barriers for specific groups of residents.

The effort appears to pick up where Washington Insurance Commissioner Mike Kreidler left off. He created a controversial rule banning credit scoring in insurance underwriting, which was challenged in court.

The bill calls for a preliminary report to be submitted to the Legislature by Dec. 31.

The Senate also passed a technical cleanup bill on Monday and passed a bill modifying the authority for fire loss insurance data on Friday.

The bills now move through the House of Representatives and must pass out of that chamber by April 16.

Fertilizer Manufacturer Fined $400K for Washington Worker Death from Toxic Gas

Afertilizer manufacturer has been fined $394,200 for the death of a worker killed by toxic gasses at a work site.

The Washington State Department of Labor & Industries fined Two Rivers Terminal LLC for safety violations following the death of Viktor Voloshin, 56, at its Pasco facility.

On June 7, 2024, surveillance footage showed Voloshin entering a tanker truck to clean it, where toxic hydrogen sulfide gas from fertilizer residue killed him.

Voloshin, who worked for the company for 11 years, was also a father of 12.

L&I cited the company for multiple willful and repeat serious violations, including failing to provide air monitoring, ventilation or protective equipment.

Two Rivers Terminal, which has a reported history of safety infractions, is still appealing pervious fines totaling $672,320.

The company is appealing the latest

penalties. Fines go toward the workers’ compensation supplemental pension fund.

Special Report: Restaurants & Bars

Restaurants and Their Insurance Agents Strive for Stability as Costs Continue to Rise

By Andrea Wells

This year restaurants and bars continue to grapple with many of the same challenges they faced in 2024. The rising cost of labor and food, along with the ongoing struggle to recruit and retain employees, remain among the top concerns for restaurant operators nationwide.

The good news: the restaurant industry is expected to reach new sales heights again in 2025, according to the National Restaurant Association’s 2025 State of the Market report, which projects $1.5 trillion in sales and employment growth of more than 200,000 new jobs.

The positive news doesn’t come without challenges, restaurant insurance specialists told Insurance Journal. Rising expenses again will tighten profits for restaurant and bar operators, which makes the role of their insurance agents and brokers even more critical, they say.

Tighter profit margins in restaurants today are one reason an operator might seek the help of a new insurance partner, John Parkhurst, hospitality practice leader, Trucordia, told Insurance Journal. Today’s market makes it a great time for new growth and opportunity for committed hospitality insurance specialists, he added.

Challenges Restaurants Face

The most pressing issue that restaurants face today is the rising cost of labor. For the average restaurant, in the past four years labor costs have risen 31%, according to the National Restaurant Association (NRA).

“There’s just a lack of people who want to work in the restaurant industry, so that alone drives up your labor costs,” Parkhurst said. “They’re paying dishwashers in the city of Chicago and the suburbs $18 to $20 an hour,” he said. When payroll goes up, so does workers’ compensation costs, he added.

Jon Siglar, executive vice president, carrier relations manager, at ALKEME, which writes mostly high-end chains and national chains in the fast-food, fast-casual, and fine-dining space in California, said it’s a mixed bag for his clientele. Siglar, who grew up in the family restaurant business working almost every position, said some of his clients are doing “amazingly well” today with “sales off the charts,” while others are struggling.

“Where my operators are struggling is in the franchise, fast-food space—those that are now paying $20 minimum wage,” he added. As of April 2024, all “fast food restaurant employees” in California must be paid at least $20 per hour. That wage increase is estimated to have led to 9,600 job losses from September 2023 to September 2024, according to a report by Edgeworth Economics in late November 2024.

The second biggest challenge for restaurants is the rising cost of food, which rose an average of 29% in the past four years, the NRA reported in February. And it’s not just the rising cost of eggs. “Chicken went from $40 a case to $140 a case for chicken wings alone,” Parkhurst noted.

Other expenses for running a restaurant—the building, supplies, credit card processing fees, and insurance—are also going up quickly, the NRA said. Yet, despite the sector’s cost concerns, the market overall is still healthy and growing.

“There’s still more restaurants opening up,” said Dan Beck, vice president at Snapp & Associates, an ALKEME company, which writes restaurants and bars ranging from a single operator taco shop to large fine-dining establishments, primarily in San Diego County, California. “We’re not seeing many closures; it’s just margins are tighter for the operators I speak to.”

“Overall, I think the marketplace has found some stability,” said Kimberly Gore, national hospitality practice leader and chief marketing officer at HUB International.

“If you’re doing what you should and you’re a good risk, then you’re going to see that this year,” she said. “If

you’ve had some issues around claims or different things, then working with a strong broker on some of those proactive things that help an underwriter see what’s going to happen is helpful,” she said.

This is where hospitality specialists can help the most, she said. “That’s the reason that you really have to understand what the restaurant’s doing,” she added. “We’re absolutely going to talk about pricing, we’re absolutely going to talk about markets, but what we really try to do is understand what they’re doing.” What’s their one-year, three-year, five-year plan? she asked. “How do we build something out that’s a little more stable than just being in and out of a market rate kind of environment?” And that starts with risk management and training, she added.

Siglar agrees with that approach. “A big part of what Dan and I do at ALKEME is work closely with our insureds to impact their insurance costs—not only just by trying to find the cheapest quote that has the best coverage but also being proactive” in helping to manage the operator’s risk exposure.

For Siglar and Beck, California’s property market and employer’s liability market—specifically wage-and-hour coverage—can be extremely tough. “Wage-and-hour coverage is getting harder to get for our clients,” Siglar said. In general, restaurants are facing increased litigation, he added.

“We’re dealing with increased litigation from attorneys in California on workers’ comp,” he said. “I just had another one of my continued on page 30

Special Report: Restaurants & Bars

continued from page 29

clients call me yesterday—they rarely have an injury but had to terminate a chef for cause,

Exclusions:

and within five days they were notified of a cumulative trauma claim, so now they have to deal with that.”

Active Assailant Coverage - Oh My!

This market has opened the door for new business opportunities for specialists in hospitality. As restaurant owners search for ways to save money they are more willing to “shop” their insurance.

“It helps to get your foot in the door,” John Parkhurst, Hospitality Practice Leader, Trucordia, said. Start by offering to take a look at their insurance portfolio especially when you know a carrier increased rates 15%, he said. “It wouldn’t hurt to take a look,” he said. “I’ve actually been able to offset some of those increases by just quoting their work comp … getting the work comp down can offset an increase on the BOP side.”

Another way he gets in the door as a specialist is by understanding their business and their coverage and possible gaps. Parkhurst says he often advises prospects on their current coverages and has found that many may not fully understand their policies.

Another area he reviews closely is policy exclusions. “You’re starting to see carriers doing firearms exclusions on their policies and unfortunately that kind of risk can happen anywhere,” he said. He suggests a standalone active assailant policy to those who are missing this critical coverage.

Another coverage gap he has found when reviewing a prospect’s portfolio is exclusions for assault and battery coverage. “I just picked up a couple of nightclubs in Nashville that had no idea that they had assault and battery exclusions on their policy,” he said. “I said, ‘Hey, just so you’re aware, you’re on a general liability policy. You’re insured for a slip and fall and that’s about it. Anybody gets into a fight, you have no coverage.’ And they didn’t understand that coverage was missing,” he said.

Educating clients and prospects on their coverage options brings in new business, he says, even in today’s hard market.

“I think the clients that I deal with appreciate the explanation of all the coverage,” he said. It’s also just good due diligence and best practice to make sure clients are fully covered, he added. “My philosophy has always been to sell coverage first, price second. If somebody doesn’t want an assault and battery just to save a few dollars, I’ll typically walk away from a risk like that.”

Parkhurst says most restaurants today are fighting to keep a very thin profit margin since the pandemic. If their insurance partner can help them reduce their risk and save a bit of money, they will be rewarded with a great client.

Nuclear verdicts in the United States are breaking records, with 27 court cases each awarding compensation of more than US$100 million during 2023, according to Swiss Re executives. Social inflation in the U.S. rose to 7% in 2023—a 20-year high—a situation that is being driven by litigation costs from mega-jury awards, said Dr. Jérôme Jean Haegeli, group chief economist for Swiss Re, who spoke during a press briefing at last year’s reinsurance Rendez-Vous de Septembre in Monaco.

The U.S. Chamber of Commerce has also reported that the number of verdicts above $100 million reached a record in 2023, up nearly 400% from 2013.

‘There’s still more restaurants opening up … We’re not seeing many closures; it’s just margins are tighter for the operators I speak to.’

For the restaurant and bar space, nuclear verdicts can occur from a dispute in a restaurant parking lot to a food safety issue as well as exist outside the restaurant industry, a spokesperson for Society Insurance, a mutual insurance company that specializes in the restaurant sector, told Insurance Journal.

Society Insurance warned that certain states are more prone to “outsized” jury verdicts. “Between 2013 and 2022, California, Georgia, Florida, Illinois, New York, and Texas accounted for 61% of such verdicts in the country,” the insurer said.

Liquor Liability

Liquor liability exposures are generating “nuclear verdict” concerns in some states.

Liquor liability insurance provides protection from litigation involving alcohol incidents. “Laws regarding the selling and consumption of alcohol are not established by the federal government, so agents should know their local liquor laws intimately,” Society Insurance advised.

Local authorities establish and enforce these laws, which means the specific guidelines as to who can sell, purchase, and consume alcohol and under what conditions—as well as the punishments for violation—vary widely across jurisdictions.

“Although all 50 states have a minimum drinking age of 21 and maximum limit for blood alcohol content allowable to operate a vehicle, that’s where the similarities end and differences begin,” Society explained.

“Right now, 42 states and Washington, D.C. have dram laws. The DRAM Shop Act allows third parties or others to recover damages caused by alleged over-service of alcohol.” That means even if a business is not liable in these complicated situations, legal defense costs can add up quickly.

This is a large concern for some restaurants, said David DeLorenzo, CEO and owner of Ambassador Group Insurance and Bar and Restaurant Insurance, based in Phoenix. Casualty lines, specifically liquor liability, have been a pain point for years for restaurant operators in Arizona, he said.

“Property is going to be property; we can always predict,” he said. “But what you cannot

predict is the liability, and what could happen and why, and when you will get sued,” added DeLorenzo, who himself has owned and operated more than 13 restaurants throughout his career. “And that, to me, I think is a problem in every market now in Arizona, specifically with liquor liability,” he said.

“You can get sued for serving one drink to somebody that gets in an accident later that night,” DeLorenzo said. “That

driver may not have been over the legal limit of intoxication, but the fact that you should have known that they were intoxicated when being served could get you dragged into the lawsuit.”

Carriers have said, “We’re not going to write these sorts of establishments anymore,” he said. “Now they may not write establishments that are open past 10 p.m., or that have a band, or have video games,

or are not so heavy in food.” It becomes hard for these type of “fun” establishments to get any “let’s just say affordable coverage” to cover everything that they need, DeLorenzo said. “And if they do get coverage, they need to look out for new exclusions.”

For example, DeLorenzo discussed a client he’s insured for 20 years that is located near a college. “They’ve had a couple of million-dollar [claims] over the past three to four years,” he said. “I’ll be able to find them something, but something is not necessarily good enough anymore, he added. “The best quote I have is a sublimit of $100,000.” The carriers are not going to take a chance on another million-dollar claim, he said, “even though they’ve stated that they’ve done more training, and they’ve put all these things in place to mitigate that [exposure].”

It’s stressful to explain the market every few days to his long-term clients, and now friends, he said.

Liquor is always a critical discussion with underwriters, HUB’s Gore said. That’s why it’s important to have more detailed conversations with restaurants on their exposures to fully understand the risk.

“Maybe the underwriting guideline says that alcohol receipts have to be less than 40% of their food. Well, if you’re in a very high-end finedining restaurant, your alcoholic beverage could be more than an appetizer. It could be more than some of the small end meals,” she said. “So, when you look at a percentage basis, then you also have to look at what is the cost of an average meal.” And be able to explain that to the underwriter.

The same is true for the low-alcohol drinks or no-alcohol cocktails, which are growing in popularity, she said. Those beverages present a lower exposure, so knowing how all that runs through the point-of-sale system is important, she added.

“Everything is about data, and that is going to help a client when they’re in the insurance market,” Gore said.

Why Knowing the Business Really Matters

Parkhurst said his background in hospitality has helped him with clients many times over the years.

“I know when to call them, when not to call them. I know their pain points and pay attention when things change—like the minimum wage goes up, or when food prices go up, that sort of thing,” he said.

“Understanding something as simple as their hoods and ducts and safety things in the restaurant makes it easier to talk their language,” he said.

Parkhurst is not alone in that regard. Many specialty brokers have been working in this sector for decades, both inside brick-and-mortar restaurants and in the restaurant insurance industry. Experience and market knowledge matter more today than ever as restaurants struggle with rising costs of operating their business.