Let the Big Dogs Eat. Join top business and community leaders at top-tier courses across the US in the #1 Charity Event In Golf.™

Make a Difference. Earn Rewards. Compete as a foursome or sponsor a local event for a chance to earn rewards, including a trip to the Applied Underwriters Invitational National Finals at Big Cedar Lodge.

Contact an Applied rep at 877-234-4450 or email invitational@auw.com to get started.

Follow us for a shot at even more rewards. Applied Underwriters Invitational® | #BigDogGolf invitational.com

A Look at Rate Trends

Premium renewal rates were up again in fourth-quarter 2024 but continue to trend lower for most commercial lines products.

Premiums increased year over year for all major commercial lines, except workers’ compensation, according to the January 2025 results of the Ivans Index.

Month over month, commercial auto, business owners policy (BOP), and commercial property experienced decreases in premium renewal rate change, while general liability, umbrella, and workers’ comp saw an increase, the Index revealed. Ivans reported that premium renewal rate changes by line of business include:

• Commercial Auto: 9.4%, down from nearly 10% in December, but up from January 2024, which was 7.4%.

• BOP: 9%, down from 9.6% at the end of December. This is a slight decrease from last year’s 9.3% in January.

• General Liability: 4.2%, up slightly from December, which was 4.16%, and decreasing from January 2024, which was 5.4%.

• Commercial Property: 9.74%, down significantly from 11.1% in December, as well as from 10.3% in January 2024.

• Umbrella: 9.5%, up from 9.1% in December 2024 and 6.35% in January 2024.

• Workers’ Compensation: -1.44%, up slightly from -1.45% in December, but down from -0.67% in January 2024.

The Ivans Index analyzes more than 120 million data transactions, measuring the premium difference year over year.

‘Month over month, commercial auto, BOP, and commercial property experienced decreases in premium renewal rate change, while general liability, umbrella and workers’ comp saw an increase.’

In another recent survey, The Council of Insurance Agents & Brokers (CIAB) reported slightly lower increases for commercial property/casualty premiums across all account sizes, noting overall premiums rose by 5.4% in Q4 2024—about the same as the third quarter’s 5.1% and the second quarter’s 5.2%. CIAB said the last quarter of 2024 was the 29th consecutive quarter of premium increases across all account sizes.

According to CIAB, while commercial property remained a challenge in Q4, premiums increased by an average of 6% compared to nearly 8% in Q3 and almost 12% in Q4 2023. Premiums for D&O, workers’ compensation, employment practices, and cyber fell in Q4, with cyber seeing the largest decrease out of all lines of 1.8%.

Commercial auto and umbrella rates each went up in Q4, the survey found. Marking the 54th straight quarter of increases, commercial auto had the highest average increase in premiums out of all lines, at 8.9%. Umbrella had an average premium increase of 8.7% in Q4. “Claims for [commercial auto] seemed to have risen, with 50% of respondents reporting an increase in claims in Q4 2024.”

| jcarlson@insurancejournal.com

ADMINISTRATION / CIRCULATION

Chief Financial Officer Terry Freeburg | tfreeburg@wellsmedia.com

Circulation Manager Elizabeth Duffy | eduffy@wellsmedia.com

Staff Accountant

Sarah Kersbergen | skersbergen@wellsmedia.com

EDITORIAL

V.P. of Content Andrea Wells | awells@insurancejournal.com

Executive Editor Emeritus Andrew Simpson | asimpson@wellsmedia.com

National Editor Chad Hemenway | chemenway@insurancejournal.com

Southeast Editor

William Rabb | wrabb@insurancejournal.com

South Central Editor/Midwest Editor Ezra Amacher | eamacher@insurancejournal.com

West Editor Don Jergler | djergler@insurancejournal.com

International Editor L.S. Howard | lhoward@insurancejournal.com

Content Editor Allen Laman | alaman@wellsmedia.com

Assistant Editors

Jahna Jacobson | jjacobson@insurancejournal.com

Kimberly Tallon | ktallon@carriermanagement.com

Columnists & Contributors

Contributors: David Lawhorn, Vincent Loh, Rajeev Gupta

Columnists: Chris Burand, Mary Newgard

SALES / MARKETING

Chief Marketing Officer

Julie Tinney | jtinney@insurancejournal.com

West Sales

Dena Kaplan | dkaplan@insurancejournal.com

Romeo Valdez | rvaldez@insurancejournal.com

Kelly DeLaMora | kdelamora@wellsmedia.com

South Central Sales

Mindy Trammell | mtrammell@insurancejournal.com

Southeast and East Sales (except for NY, PA, CT) Howard Simkin | hsimkin@insurancejournal.com

Midwest Sales

Lisa Whalen | (800) 897-9965 x180

East Sales (NY, PA and CT only)

Dave Molchan | (800) 897-9965 x145

Advertising Coordinator

Erin Burns | eburns@insurancejournal.com

Insurance Markets Manager

Kristine Honey | khoney@insurancejournal.com

Sr. Sales & Marketing Coordinator

Laura Roy | lroy@insurancejournal.com

Marketing Administrator Alberto Vazquez | avazquez@insurancejournal.com

Marketing Director Derence Walk | dwalk@insurancejournal.com

DESIGN / WEB / VIDEO

V.P. of Design Guy Boccia | gboccia@insurancejournal.com

Web Team Lead

Josh Whitlow | jwhitlow@insurancejournal.com

Ad Ops Specialist

Jeff Cardrant | jcardrant@insurancejournal.com

Web Developer Terrance Woest | twoest@wellsmedia.com

Online Training Coordinator George Jack | gjack@ijacademy.com

Help Protect Your Customers from the Financial Impact of Unexpected Legal Issues

LawGuard is a new offering that can help differentiate your company from the competition.

Turnkey product

LawGuard is fully functional and ready to implement saving you the high costs and lengthy timelines associated with traditional product development.

New revenue growth & diversification

Partnering with LawGuard provides an easy and efficient way to diversify your revenue by creating a new recurring revenue stream for you and your shareholders with minimal risk.

Expertise and support

LawGuard's development team has combined experience of 80+ years in legal expense insurance, and we've created an e-commerce website to help market and execute enrollment.

WHITE LABEL OPPORTUNITY

Your company can easily market LawGuard as a white label offering or in its current branded format. It's entirely up to your organization and the approach that best fits your strategy and market position.

FINANCIAL SECURITY

LawGuard is underwritten on "A" rated insurance carrier's paper*. This means the company has an excellent ability to meet its financial obligations.

FOR MORE INFORMATION

To learn more about partnering with LawGuard, visit Partner.LawGuard.com.

To learn more about LawGuard, visit LawGuard.com

News & Markets

US P/C Industry Improves Despite 2024 Underwriting Loss Changes in Personal Lines Segment Driver of Expected Improvement

By Chad Hemenway

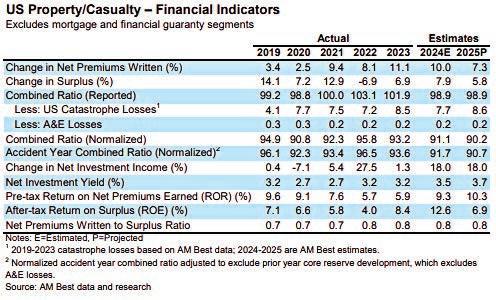

The U.S. property/casualty industry took another underwriting loss in 2024, but results improved thanks to rate increases and changes in risk selection, most notably in the personal lines sector.

A report from industry rating agency AM Best late last month said U.S. P/C insurers posted an underwriting loss of $2.6 billion in 2024—a large improvement over the underwriting loss of $24.6 billion recorded in 2023. The estimated combined ratio for 2024 was 98.9 compared to 101.9 for 2023.

AM Best said it expects the industry in 2025 to “build on its solid rebound” with improved underwriting and operating results—even in the face of more losses from secondary perils and continued adverse litigation trends such as social inflation and third-party litigation funding.

The personal lines segment will be a driver of expected improvement, AM Best said. In 2024, personal lines posted a net underwriting loss of $11.9 billion compared to a loss of $36.7 billion in 2023. Rate increases in auto and home insurance helped drive improvements in personal lines;

the combined ratio for auto was 98.7 (from 104.9 in 2023) and homeowners was 105.7 (from 110.9 in 2023).

AM Best said personal lines premium increased 12.9% in 2024 and is projecting to increase 9% this year.

“Insurers are focusing on achieving the rate increases necessary to address their calculated rate needs, particularly for lines of coverage such as private passenger auto and homeowners multiperil,” the agency said, adding that insurers are “prepared to withdraw from a given state entirely if needed increases are not approved.”

The homeowners segment is still expected to record a slight underwriting loss in 2025, according to AM Best, but the achievements in 2024 in personal auto—after three years of underwriting

losses—should continue as the line has made strides to achieve rate adequacy while effectively using technology and data analysis.

“Because this line [personal auto] accounts for a third of all the P/C industry’s annual direct premium and more than half of personal lines premium, its results—whether positive or negative—have a material impact on the P/C industry’s overall results,” AM Best said, predicting a further reduction in combined ratio in 2025 for private passenger auto to 97.5 from 98.7 in 2024.

Though commercial lines outperformed personal lines with a 2024 combined ratio of 97, it was no thanks to commercial auto, which turned in a combined ratio of 108.5. AM Best said it has a negative outlook for commercial auto, general liability, and D&O.

“AM Best estimates that commercial lines net premiums were up 6.1% in 2024, from 8.1% in 2023, reflecting continued price declines in workers’ compensation as well as certain specialty casualty lines,” the agency reported. For 2025, AM Best said it expects growth to weaken to about 4% but the combined ratio should remain steady at 97.

News & Markets

Small, Medium-Sized Firms Lacking in ‘Continuity’ Planning: Survey

Mid- and small-market businesses (SMBs) face a lot of the same big-picture challenges, but how they prioritize risk, spending, and solutions varies widely.

According to Nationwide’s latest risk management survey, mid-market business owners are most concerned about economic and financial risks, regulatory changes, and technological and supply chain disruptions over the next two years.

Meanwhile, small-market business owners also list economic and financial risks as a top concern, but their worries about technological disruptions are eclipsed by concerns about market conditions, natural disasters, inflation, and labor. Despite implementing various risk management strategies, only 54% of business owners feel highly protected against these threats.

Budgeting for Risk Management

Small business owners dedicate more of their budget (18%) to risk management and safety than mid-market business owners (6%). Eight in 10 (83%) middle-market businesses have a dedicated safety budget. High-risk industries like construction and manufacturing allocate even more to safety at 19% and 13% of their annual budget, respectively.

Mid-market business owners report top areas of investment for risk mitigation include technology/security (40%), followed by security/cybersecurity enhancement (24%), labor/staffing (19%), supply chain/supplier stability (17%), and training programs (11%), according to the survey.

Over the same period, small-market businesses plan to invest in technology/ security (24%), offerings/growth (21%), costs/revenue (20%), recruitment/employee retention (17%), and supply chain/ supplier stability (14%).

Impacts of Evolving Regulations and Standards

Middle-market business owners overwhelmingly agree that evolving regulatory and safety standards hinder operations.

Three-quarters (78%) say changes had an impact on their risk management needs, and 20% feel their business is unprepared to respond to new regulations.

Mid-market business owners are more likely to act in areas such as additional training, utilizing technology (72% vs. 62% of small business owners), and implementing KPIs (69% vs. 58% of small business owners). Technology provides crucial risk management or regulatory support for 76% of mid-market businesses, with 11% reporting it is central to all their risk management activities and 65% using it in specific areas but not comprehensively.

Small business owners are split, with 51% saying regulatory changes impact their risk management practices and 48% reporting little impact.

Where Are the Gaps?

While businesses scramble to implement plans and evolve with technology, there are still gaps. For example, 55% of mid-market business owners report having a disaster preparedness plan, and 60% of small- and mid-market business owners currently have a fall protection program in place. Two-thirds of mid-market businesses report that compliance is integrated into overall risk management framework, but only about one-third of small businesses (34%) make the same claim. While half of mid-market businesses (52%) use technol-

ogy for real-time monitoring of compliance issues, only 29% of small businesses have invested in that tech.

Many owners struggle to recognize the value and impact of their efforts: only 51% currently view risk management initiatives as effective. Their top challenges with safety and risk management include:

• Cost of safety measures (38%).

• Maintenance of safety equipment (31%).

• Resources required for conducting regular safety assessments (30%).

Some 21% of businesses report not having a business continuity plan, leaving them vulnerable to operational disruptions.

“Despite nearly 90% of businesses having formal risk management policies that are regularly reviewed, a critical vulnerability remains: 1 in 5 businesses lack a business continuity plan,” said Mark McGhiey, Nationwide’s leader of commercial lines risk management.

“This gap leaves them exposed to potential disruptions that could severely impact their operations,” he said. “Agents can help identify and fill these gaps with commercial clients, partnering with them and carrier-provided risk management experts to develop and implement a comprehensive business continuity plan. These efforts can significantly enhance clients’ resilience and ensure they’re prepared to navigate unexpected challenges.”

$200 Billion

The amount of insured catastrophic losses predicted for 2025. American International Group CEO Peter Zaffino used the insurer's fourth-quarter earnings call to talk about reinsurance attachment points, throwing in the possibility that 2025 could be the year for $200 billion in insured catastrophe losses. “This could recalibrate the entire industry,” he told analysts on the call.

63%

The number of lawyers who say they used AI for work last year. Twelve percent said they use it regularly. AI can produce false information, known as “hallucinations.”

A federal judge in Wyoming recently threatened to sanction two lawyers who included fictitious case citations in a lawsuit against Walmart. Attorney ethics rules require lawyers to vet and stand by their court filings or risk being disciplined. The American Bar Association has told its 400,000 members that those obligations extend to “even an unintentional misstatement” produced through AI.

63.7%

The increase in national residential reconstruction costs, including materials and retail labor, over the past 10 years. Over the past decade, there’s been a dramatic increase in reconstruction costs, according to 360Value at Verisk. The 10-year analysis examined residential and commercial reconstruction costs between October 2014 and October 2024.

$2 Billion

The Federal Emergency Management Agency said it needs to borrow $2 billion from the U.S. Treasury to cover claims from National Flood Insurance Program policyholders. FEMA, administrator of NFIP, said it expects to pay out more than $10 billion in flood claims related to hurricanes Helene and Milton in 2024 and claims for other flooding events last year.

Declarations

Uninsurable Future?

“We’re marching steadily towards an uninsurable future in the United States because we’re not doing enough fast enough to address the underlying cause, which is climate change.”

— Dave Jones, California’s insurance commissioner from 2011 to 2018. Citing rising fire risks and other problems, seven of the top 12 insurance companies either paused or restricted new business in California in 2023. State regulations give insurers more latitude to raise premiums in exchange for issuing policies in high-risk areas, including consideration of climate change in premiums and passing the costs of reinsurance to consumers.

Vape-Flavored Violations

“The vaping industry is taking a page out of Big Tobacco’s playbook: they’re making nicotine seem cool, getting kids hooked, and creating a massive public health crisis in the process.”

— Letitia James, New York state attorney general, who is seeking hundreds of millions of dollars in civil fines and damages from 16 corporate and individual defendants for gross negligence and creating a public nuisance by selling fruit- and candy-flavored vapor products to impressionable children. A 2020 state law bans sales of flavored vapor products and requires vape purchasers to be at least 21. E-cigarettes have been the most used tobacco product among U.S.children since 2014.

AI: Revolution or Doomsday?

“The context of 2024 is of continued trends of severe storms and hail, heat waves and drought, a weakened but continuing respiratory infection pandemic, and geopolitical concerns within and between countries. AI is trumpeted to revolutionize business unless the technology facilitates a doomsday scenario.”

— The 18th Annual Emerging Risk Survey, a joint survey from the Casualty Actuarial Society and the Society of Actuaries.

Accountability for Hate Groups

“If we have less people involved, that is a win.”

— Rachel Carroll Rivas, interim director at the Southern Poverty Law Center’s Intelligence Project. Two North Dakota nonprofits, North Dakota Human Rights Coalition, the Immigrant Development Center, have settled their lawsuit against Patriot Front, a white nationalist hate group. The group allegedly intimidated immigrant business owners. The lawsuit could impact the group’s recruitment because of the accountability it brings, Carroll Rivas said.

FEMA Frustration

“If this is the way they are, (Trump) ought to do away with (FEMA).…Their attitude was, you know, this happened to you, but it’s up to you to fix it. And I ain’t the one who caused it.”

— Danny Bailey, a 61-year-old Buncombe County, North Carolina retiree, said he struggled with his FEMA application process after Hurricane Helene. He eventually received $42,500 after losing the trailer he lived in, his sister’s double-wide mobile home and a barn to flooding. His family had moved to the property in 1968.

Mall Sweet Home

“It’s a simple matter of looking at the housing stock that’s available and looking at the growing demand and looking at every option to expand those opportunities. The Lord’s not making new land.”

— Texas Sen. Bryan Hughes, a Mineola Republican, arguing for new legislation that would effectively allow owners of struggling office properties in the state’s largest cities to convert that space into residences. The bill would forbid cities and counties from requiring owners of flagging office buildings and commercial properties like shopping malls and strip centers to go through a rezoning process if they want to add apartments or condominiums.

People

National

Westchester, Chubb’s Excess and Surplus Lines Division, headquartered in Alpharetta, Georgia, named Matt Booker, head of brokerage property and inland marine, as property practice leader. Tom McLaughlin, head of brokerage casualty, has been appointed casualty practice leader. Andrea Larkin, recently appointed head of financial lines, will become the financial lines practice leader. Dave Roberts, executive vice president, Westchester digital and middle market, will take on operations, programs and IT.

Ignite Specialty Risk, headquartered in London, appointed Ankit Patel led the contingent legal risk insurance team for the Americas at Liberty Mutual Corporation.

Alliant Insurance Services, headquartered in Irvine, California, hired professional employer organization (PEO) specialist Crystal Calvo as vice president within its employee benefits group. Calvo most recently served as a senior broker relationship manager within the PEO division at ADP.

QBE North America, headquartered in New York City, appointed Lauren Finnis as senior vice president of distribution. Finnis joins QBE from Willis Towers Watson, where she served as head of commercial lines in their insurance consulting and technology practice.

AXA XL in the Americas, headquartered in Hamilton, Bermuda, hired Peter Bakker

as head of environmental package solutions for middle market in the Americas. Based in New York, Bakker joins AXA XL after 13 years with Aspen Insurance.

director and senior lawyer in Aon’s litigation risk group.

Tokio Marine HCC (TMHCC), based in Houston, Texas, appointed Brendan Gaine as head of North American distribution, a newly created role. Gaine joins TMHCC from Brightway Insurance, where he was head of national franchise sales. TMHCC also appointed Stuart Heath as head of distribution – international. Heath previously served as TMHCC’s head of delegated property.

Kirstie Settas-Jones joined Alliant Insurance Services as vice president within its employee benefits group. Based in Florida, Settas-Jones serves a nationwide client base. Alliant is based in Irvine, California. Prior to joining Alliant, Settas-Jones was senior vice president, consultant relations with Progyny, Inc.

January 2023 as executive vice president. She previously served as chief client officer, U.S. casualty and executive vice president at Aon.

East

Hiscox, headquartered in Atlanta, appointed Karen Baldwin as vice president, media practice leader. Baldwin leads Hiscox USA’s media liability practice. Baldwin most recently served as AXIS Capital’s vice president, media, film & entertainment product leader.

Willis, a WTW business headquartered in London, named Stephen Kyriacou as head of litigation and contingent risk solutions, and senior director of transactional solutions for North America. Kyriacou most recently served as managing

Tokio Marine HCC (TMHCC), based in Houston, Texas, appointed Greg Hamlin as president of its newly launched U.S. healthcare professional liability business. Based in New York City, Hamlin joins TMHCC from Berkshire Hathaway Specialty Insurance, where he served as senior vice president for institutional accounts.

RP Hallenbeck joined Amwins, headquartered in Charlotte, North Carolina, in the newly created role of healthcare practice leader. Hallenbeck most recently he served as the national business development leader for MedPro Specialty.

(HUB), headquartered in Chicago, appointed Carol Murphy as North American casualty practice leader. Murphy joined HUB in

Chesapeake Employers’ Insurance Company, headquartered in Towson, Maryland, named Jodi M. Swartz as the company’s senior vice president and chief growth officer. Swartz most recently served as senior vice president, marketing and communications for PayScale.

Lawley, headquartered in Buffalo, New York, appointed four new partners, Michael Jantzi II; Michael Knott, leader of Lawley’s healthcare practice group; Kevin Ross, leader Lawley’s construction and real estate segments; and Michael Ross, property and casualty insurance advisor.

Rosenberg & Parker, headquartered in Wayne, Pennsylvania, promoted Jack Rosenberg to president. Elizabeth Cervini was promoted to executive vice president development; John Wescott was promoted to executive vice president strategy and firm architecture; and James DiSciullo was promoted to director of advisory and production.

XS Brokers, headquartered in Quincy, Massachusetts, hired Annie Dawson as senior vice president to head national carrier relations

continued on page 16

Peter Bakker

Karen Baldwin

Stephen Kyriacou

Greg Hamlin

Carol Murphy

Jodi Swartz

continued from page 14

and strategy. Dawson most recently served as a director for national binding authority at RT Specialty.

Plymouth Rock Assurance, headquartered in Woodbridge, New Jersey, named Greg Kalinsky as president and CEO of the Plymouth Rock Management Company of New Jersey. Kalinsky comes to Plymouth Rock after a 37-year career at GEICO, where he held multiple leadership roles.

Southeast

Adrienne Johnson joined Alliant Insurance Services, headquartered in Irvine, California, as vice president within its employee benefits group. Johnson is based in Nashville.

Hiscox, headquartered in Atlanta, appointed Alexandra Furth as head of claims in the U.S.

Before AIG, Furth held deputy general and corporate counsel roles with Liberty Mutual, the University of Massachusetts and Resolute Management.

Orion180, headquartered in Melbourne, Florida, hired former The Hartford executive Chris DiMartino as chief under-

writing officer. Prior to joining Orion180, he served as senior vice president of insurance services at AAA Northeast. Orion180 Chief Operations Officer (COO)

Ryan Jesenik has been promoted to president, insurance.

Jesenik will retain his responsibilities as COO while also leading growth strategy.

Midwest

DOXA, headquartered in Fort Wayne, Indiana, hired five new executive leadership team members.

Matt Bishop joined the team from AGIA Affinity as head of operating entities and business verticals. He came to DOXA from Farmers. Cindy Bush joined as senior vice president, people and culture. Doron Hai joined as chief operating officer. Ammon Smartt joined as general counsel and secretary. Amy Watts was named senior vice president of marketing.

JM Wilson, headquartered in Portage, Michigan, promoted Lesley Boles to senior personal lines underwriter. She joined JM Wilson in January 2023 as a personal lines underwriter.

Encova Insurance, headquartered in Columbus, Ohio, appointed Dawn Colavecchi as commercial lines regional vice president, and Todd Becker as vice president, commercial underwriting office, workers’ compensation. Colavecchi

most recently served Encova as a senior production underwriter in Michigan. Becker previously served as vice president and business director for the Standard South workers’ compensation small business team.

South Central

previously served as executive vice president, risk practices at Lockton Companies.

The Workers’ Compensation Insurance Rating Bureau of California (WCIRB) named Andrea Coleman as president and CEO. Coleman joined the WCIRB in May 2022 as executive vice president and chief operating officer. Coleman succeeds Bill Mudge, who transitioned to CEO emeritus until his retirement on April 1.

CoVerica, headquartered in Dallas, appointed Mark Holland as president and CEO. Holland previously served as the co-founder, partner, and CEO of BenCom and recently launched BenefitHelp. BenefitHelp and its team will integrate into CoVerica, expanding its service offerings.

One General Agency (OGA), headquartered in Oklahoma City, promoted Taylor Matthews to vice president of operations. Matthews joined OGA during an acquisition in 2024. Russ Iden is OGA’s newest marketing specialist. Kraig Rosenow was promoted to OGA’s director of underwriting. Jana Anderson has rejoined OGA as a senior advisor.

West

ICW Group Insurance Companies, headquartered in San Diego, appointed Mark Moitoso as president. He succeeds Kevin Prior, who will remain CEO. Moitoso

IMA Financial Group, headquartered in Salt Lake City, named Kendall Empey as president, Salt Lake City and market leader for Utah. Empey most recently served as chief operating officer at Lockton.

Media Guarantors, a CAC Group Company headquartered in Los Angeles, appointed Angus Sutherland as senior vice president of business development and client relationships.

The Oregon Department of Consumer and Business Services appointed Matt West as administrator of the Workers’ Compensation Division. West began with the Workers’ Compensation Division in 2003 as a benefit consultant and served as the division’s deputy administrator for two years before becoming the interim administrator in January 2024.

Alexandra Furth

Dawn Colavecchi

Mark Holland

Mark Moitoso

Kendall Empey

Angus Sutherland

Todd Becker

Adrienne Johnson

Chris DiMartino

Ryan Jesenik

Business Moves

East

Insurance Services of New England, ACORN Insurance Alliance Agencies

Regional independent agency network Insurance Services of New England (ISNE) expanded into Connecticut with eight additional agencies. The Connecticut agencies include Ahrens, Fuller, St. John & Vincent Insurance, Enfield; Allied Insurance Center, Bristol; Anderson-Meyer Insurance Inc., Glastonbury; Robert J. Evaristo & Associates Inc., Ellington; Lindquist Insurance Associates Inc., Farmington; Rose Insurance, Oxford; Sundel & Milford Inc., Waterbury; and Thomas Fahy Insurance Agency Inc., West Hartford. Before joining ISNE, the eight agencies were members of the former ACORN Insurance Alliance, which closed in January.

World Associates LLC, Grandview Brokerage LLC

World Insurance Associates LLC acquired the business of Grandview Brokerage LLC of Brooklyn, New York. Grandview provides commercial and personal insurance with specialties in healthcare, real estate and the jewel industry.

Segal, J.A. Mariano Agency

Segal, a leading benefits and human resources consulting firm, acquired a book of business from the J.A. Mariano Agency, a commercial insurance brokerage. This transaction augments Segal’s established insurance brokerage practice’s capabilities

as a retail insurance broker dedicated to addressing risks related to workplace, unions and benefit plans. Robert J. Eberle, Jr., joined Segal as an insurance consultant, and Robert J. Eberle, III, joined as an associate consultant.

Arthur J Gallagher & Co., Agilis Partners LLC, Dominick Falcone Agency, Inc., and Falcone Associates, Inc.

Global insurance broker Arthur J. Gallagher & Co. acquired Waltham, Massachusetts-based Agilis Partners LLC. Agilis is an investment and retirement plan consulting firm with offices in greater Boston, New York and Denver. Tom Cassara and his team will remain in their current locations under the direction of Jeff Leonard, Gallagher’s Global Financial & Retirement Services Business leader. The Agilis acquisition follows Gallagher’s acquisition of Syracuse, New York-based Dominick Falcone Agency, Inc., and Falcone Associates, Inc.

Southeast

King Risk Partners, Kerr Agency Inc.

Florida-based insurance broker King Risk Partners acquired the Kerr Agency Inc., an independent insurance agency in Simsbury, Connecticut. The acquisition furthers King Risk Partners’ expansion across the Northeast. Kerr is King’s fifth agency in Connecticut.

Trucordia, CADA Insurance Services

Trucordia acquired the insurance business of CADA Insurance Services,

which has multiple offices in Louisiana, including Baton Rouge, Chalmette, Gretna and Kenner. CADA Insurance offers auto, home, commercial, general liability and workers’ compensation solutions.

Ryan Specialty, Velocity Risk Underwriters LLC

Specialty insurance provider Ryan Specialty acquired Velocity Risk Underwriters, LLC from funds managed by Oaktree Capital Management, L.P. Based in Nashville, Velocity is a managing general underwriter (MGU) providing first-party insurance coverage for catastrophe-exposed properties. Velocity will become a part of the Ryan Specialty Underwriting Managers division of Ryan Specialty.

Midwest

HUB International Limited, Yavitz Insurance Group

HUB International Limited acquired the assets of Yavitz Insurance Group. Located in St. Louis, Missouri, Yavitz Insurance is a privately owned insurance agency providing comprehensive commercial and personal insurance solutions for individuals and businesses. Ken Yavitz, owner, and the Yavitz Insurance team will join HUB Kansas and Missouri. Yavitz Insurance will be referred to as Yavitz Insurance Group, a Hub International company.

HUB International Limited, Mayfield Insurance Inc.

HUB International acquired the assets of Mayfield Insurance Inc., based in Mooresville, Indiana. Dean Mayfield, President, and the Mayfield Insurance team will join Hub Midwest East. Mayfield Insurance will be referred to as Mayfield Insurance, a Hub International company.

King Risk Partners, Barker, Beck, Collins & Kronauge Agency

King Risk Partners acquired Barker, Beck, Collins & Kronauge Agency (BBC&K), an independent insurance firm in Dayton, Ohio. BBC&K was founded in founded in 1923. Malcolm King, CEO of King Risk Partners, said the acquisition reinforces the broker’s ability to provide top-tier service in the Midwest region.

Risk Strategies acquired Comprehensive Benefits Inc. and Gabrielson Insurance & Financial Services, located in Greater Detroit. The joint acquisition preserves an established working relationship between the two partner companies. Based in Southfield, Michigan, Comprehensive Benefits offers employee benefits services for fully insured and self-funded programs for organizations. Gabrielson Insurance & Financial Services has a complementary focus, offering services in its employee benefits work similar in scope to Comprehensive Benefits.

South Central

Crest Insurance, Horizon Insurance Services

Crest Insurance acquired Horizon Insurance Services, a full-service insurance agency based in Houston. The Horizon Trucking team, led by Ramon Canlas, is known for its expertise in commercial insurance and trucking and transportation services.

Inszone Insurance Services, Texas Classic Insurance Agency, Inc.

Inszone Insurance Services acquired Texas Classic Insurance Agency, Inc.

Founded in 1991, Texas Classic Insurance Agency serves clients across the Dallas/ Fort Worth area from Granbury and Liberty Hill locations. The Texas Classic Insurance team will continue to serve customers from their existing offices.

West

Trucordia, Boater’s Insurance Agency

Trucordia acquired the insurance business of Boater’s Insurance Agency in the San Francisco Bay Area. Boater’s Insurance Agency specializes in providing insurance services within the marine industry. The firm is licensed in 50 states.

Trucordia, formerly PCF Insurance Services, is the group name for an insurance brokerage headquartered in Lindon, Utah.

World Insurance Associates LLC, Stern Insurance Group

World Insurance Associates LLC has acquired the business of Stern Insurance Group (SIG) in Scottsdale, Arizona. SIG was founded in 1987 by Daryl Stern and specializes in counseling corporations in

employee benefits and risk management services. World Insurance Associates is headquartered in Iselin, New Jersey, and provides individuals and businesses with personal and commercial insurance, financial planning services and human capital management services.

Special Report: High-Value Homeowners

Insuring ‘Red Zone’ High-Value Homes: A

Look at California’s Wildfires and the Luxury Home Insurance Market

By Allen Laman

When the calendar flipped to 2025, Lacey Garrison Strom was optimistic.

As the executive vice president of private client services at California-based Heffernan Insurance Brokers, Garrison Strom secures insurance coverage for affluent clients across the Golden State. Her renewals were flat—some even went down.

“I was so excited,” she reflected in a February interview. “This is going to be our year, rates are finally normalizing, we have

some good news for our California clients.”

Not even a week into January, however, a devastating series of wildfires ravaged Southern California, burning tens of thousands of acres of land and destroying thousands of homes and structures.

Claims Journal reported in late January that insured loss estimates range from $8 billion for the two largest fires to $40 billion for all five. AccuWeather estimated damages and economic losses will total between $250 billion and $275 billion.

As the flames were extinguished in Southern California, insurance brokers

who specialize in securing coverage for high-value and luxury homes helped their clients pick up the pieces of their lives. In interviews with Insurance Journal, they also looked ahead to how the fires could impact insurance for this segment in the area moving forward.

“The scale of this fire is so vast,” Garrison Strom said. “We’ve experienced nothing like it.”

Fires Impact on Home Insurance

Jim Tolliver, private client group practice leader at Woodruff Sawyer, explained

‘The scale of this fire is so vast. … We’ve experienced nothing like it.’

that the catalyst for change in the overall California home insurance market can be traced back to 2017. During that year, the California Department of Forestry and Fire Protection (Cal Fire) reported that 9,270 fires burned nearly 1.6 million acres and destroyed approximately 11,000 structures across the state.

Total acreage burned by wildfires in California surpassed 1 million acres in four of the following seven years, with 2018 being “the deadliest and most destructive wildfire season on record in California,” per Cal Fire.

A record-breaking 4.3 million acres burned in 2020 alone.

In the last five years, major insurers have pulled back from the California home insurance market. This goes for both the standard market and the high-value home market.

“So, the consumer today has been left with an option that looks like, ‘Hey, I have to pay a lot more for less coverage if I can find it,’” Woodruff Sawyer’s Tolliver explained. “‘And if I can’t find it, I’m forced to go to a state-funded insurer of last resort.”

High-Value Home Insurance

In Woodruff Sawyer’s affluent market—homes with more than a $3 million replacement cost value—state-funded coverage from the California FAIR Plan is inadequate because it tops out at a $3 million replacement cost value. Woodruff Sawyer has a niche focus in the affluent and ultra-affluent markets, and its insureds are accustomed to paying hundreds of thousands, if not millions, in premiums for personal insurance.

For those in the high-value arena, continued on page 22

Special Report: High-Value Homeowners

continued from page 21

properly valuing and adjusting losses is key, Tolliver said.

When it comes to upgraded fixtures and custom home alterations, “a middle-market carrier is not meant to respond to that type of thing,” Tolliver said. High-value carriers make sure homes are rebuilt with all the same bells and whistles, he explained, and handholding throughout the claims process is a bigger priority.

Tolliver estimated that Woodruff Sawyer has more than 500 clients in California. He explained that one resident may be able to get coverage for their property, but a neighbor across the street may not. This could be due to the quality of a home, the type of building, where it sits on a street in relation to surrounding vegetation, or the home’s replacement cost valuation.

If, for example, it would cost $25 million to repair a home, carrier options dwindle significantly, and of those who can insure high-value homes, an insurer may have too much aggregation on a specific street to take on a neighboring property.

“The other part is that they may not have the capacity,” Tolliver said. “Some of the homes that we insure can be well over $50 million, sometimes double that. And the underwriting capacity might not be in the marketplace to do that at the very given time they need insurance.”

Niche brokers like Woodruff Sawyer find ways to leverage coverage through non-standard markets that exclude certain types of perils alongside options like the FAIR Plan.

In a July 2024 story published by Insurance Journal, both Tolliver and Garrison Strom reported encountering potential home buyers who can’t get insurance or people who want to sell their home but cannot because buyers are unable to get insurance to secure a loan. The carriers that independent brokers work with have largely shifted to non-admitted products in the California high-value home insurance market, Tolliver said.

David Clausen, CEO of Coastal Insurance Solutions, explained that even before the recent Southern California fires began to burn, it was virtually impossible to get a carrier to write an admitted market policy

for homeowners who have a $25 million home in a very high-risk area.

“I think that as the underwriting guidelines got stricter, it often meant higher deductibles and additional documentation, mitigation measures, and certainly [for] the more expensive homes, the more closely they’re going to get looked at on an individual risk basis,” Clausen said.

Garrison Strom shared that luxury homeowner clients still had carriers that were offering some coverage in California— typically through non-admitted products —including PURE, Cincinnati Insurance, AIG, and other options.

“They weren’t cheap,” she said, “but they’re clients that could afford to pay. Some clients chose not to. We did have luxury homeowners that chose to go with the California FAIR Plan or a direct writer and underinsure their homes, if that’s what they wanted to do. Or, even with a non-admitted carrier, [they] chose to buy less coverage because it was less money.”

She said the insurance appetite specifically for luxury homes can be attributed to insurers working with clients who are remodeling homes, buying newly built homes, or undergoing ground-up construction where the insurer can require building elements such as ember-resistant vents, gutter guards, and other forms of fire-resistant hardening.

“Their homes are built differently,” Strom added. “They can wrap their arms around that risk, and also, often, that type of client comes with a portfolio. So, it’s not just one home and maybe a car and maybe an umbrella policy. Usually, there’s more coming with it, so the economics of it make sense for the carrier to take on that exposure.”

Creativity is infused in the process of securing coverage, but brokers are “very limited in the options we can provide for a home that’s … in the highest red zone you can find. In some cases, we just can’t solve that situation,” Tolliver said.

He added that some insureds pay a 50% wildfire deductible on their dwelling coverage. Tolliver often gets calls from folks in California being dropped by their carriers or being subjected to significant rate increases, exclusions, or endorsements

Brokers are ‘very limited in the options we can provide for a home that’s … in the highest red zone you can find.’

that “reduce coverage incredibly.”

“Everybody’s cherry-picking,” Tolliver said of carriers. “And they’re going to be careful about sticking their neck out on anything they think that’s going to have a total loss.”

Fire Impacts on Luxury Carriers

It would be naïve to think the recent wildfires won’t have impacts on the high-value home insurance market in the area, Tolliver said. He believes the degree of impact will vary by carrier. Chubb, AIG, PURE, and Cincinnati Insurance have positioned themselves well over the last three to four years, he said.

“They’ve gotten their underwriting where, I think, [they] may not have the rate they want, but I think they have the risks that they want,” he said. “So, they’ve been ahead of that curve.” Tolliver said he thinks these companies are in as strong of positions as they can be, “and time will tell, really, what that means.”

Chubb has said the wildfires will cost the insurer $1.5 billion pre-tax in the first quarter. AIG estimated in February that, though it was still too early to determine the full impact of the fires, its net loss would be approximately $500 million, before reinstatement premiums.

In an earnings call, Steve Spray, president and CEO of Cincinnati Financial,

shared that estimated first-quarter 2025 pre-tax catastrophe losses totaled approximately $450 million to $525 million net of reinsurance recoveries. He added that, had the wildfire effect occurred in 2024, “we believe we would still have earned a modest underwriting profit.”

Garrison Strom said that most of the luxury markets saw this coming. While direct writers with lots of volume got hit the hardest, the luxury home insurers have healthy portfolios, she said. They have healthy reinsurance treaties and are doing the best they can for their clients.

Fire Impacts on Policyholders

On Jan. 27, Tolliver said that Woodruff Sawyer did have insureds in the area of the recent wildfires. He was certain that some of the policyholders had claims, but to his knowledge, none were total losses at the time.

Clausen said on Jan. 28 that Coastal Insurance Solutions did have a few policyholders hit by the fires.

Garrison Strom said her affected clients felt powerless. Those who still had homes standing were desperate to know when they’d be back in them, she explained, but brokers couldn’t tell them because the timeline remains largely unknown.

The road to rebuilding in the Palisades and Pasadena areas will likely be a long

one. Massive debris cleanup must be completed before remediation can even begin, Garrison Strom said. Some luxury homeowners have other properties they can live in during this process, but for others, cost-of-living expenses in temporary housing for an extended period will add up.

“There’s not a lot we can compare it to,” Garrison Strom said. “You’re looking into these clients’ eyes, and they’re just so desperate for information. All we can do is just keep answering their calls and trying to find as much information as we can and do the best that we can.”

Clausen also pointed to the difficulties with finding comparable homes to live in as the rebuilding process begins. Additional living expenses coverage presents a challenge, he said, noting that it could take at least a year or even two to rebuild homes destroyed by the recent fires.

“There’s less luxury homes available than there are, we’ll call [them] everyday homes,” Clausen said. “As the supply of those homes goes down, the price to rent them goes up and certainly becomes a game of what’s fair for additional living expenses.”

Most people are planning to rebuild, Clausen said. “I just hope that the market can become competitive again,” he said, adding that regulators and insurers need to find a way to work together so that companies remain willing to do business in California while collecting premiums that accurately reflect the level of risk.

“Right now, insurers are pulling out, capacity is shrinking, premiums are rising, and the market is facing significant challenges,” he continued. “No matter where you live, there’s risk. It would be a shame to see some of the most beautiful landscapes in the U.S. become uninhabitable or unaffordable simply because insurers can’t find a sustainable, long-term path to profitability.”

Clausen explained that he hopes those in a position to make a difference recognize “the urgent need for systemic reforms—ones that create a more resilient and equitable insurance landscape for California’s residents, business owners and insurers alike.”

What They’re Watching

Tolliver is interested to see what the disaster means for the California FAIR Plan. Based on his experience in submitting new locations for FAIR Plan coverage, Tolliver said, “they seem ill-equipped to administratively handle the volume of requests. I am concerned based on the number [of] recent wildfire claims in California that they will also struggle to process the volume [and] adjust claims in an accurate and timely fashion.”

As of press time, the FAIR Plan reported it had paid more than $914 million to policyholders, including advance payments, to cover claims related to the Palisades and Eaton fires. In February, California Insurance Commissioner Ricardo Lara approved a California FAIR Plan request for a $1 billion assessment on admitted market insurers to cover claims from the Los Angeles wildfires.

Tolliver sees the need for more insurance resources with greater limits for Californians with high-value homes because “there’s going to be people that did not have enough coverage,” he said. He also sees a need for more codes and protections to help make housing more fire-resistant, and he believes that consumers need to take more responsibility in the places they choose to live.

When asked how she thinks the fires will affect insurance for luxury homes in the region, Garrison Strom said it depends on what the state department of insurance does. She believes the department needs to give carriers rate—and not a low number—or more flexibility in forms and contracts.

“So that they’re not so stuck in giving these broad coverages,” Garrison Strom explained. “Because until that happens, there’s no reason for these carriers to do business here.”

Clausen echoed these comments in his interview. “I would keep an eye on how this market is going to shake out,” Clausen said. “I think it’s unclear on the direction of capacity. I just think the market is unstable at this moment. And I’m not sure that capacity is going to come back roaring in for quite a while, from an admitted standpoint, anyway.”

Special Report: Risk Management

Preventing Workplace Violence Is Not a One-Size-Fits-All Exercise: Risk Management Experts

By L.S. Howard

Businesses are now required to implement robust workplace violence prevention plans in California—under a new law that became effective in July 2024. But risk management experts warn that compliance needs to be more than a check-the-box exercise if lives are to be saved. It’s a lesson that should be understood by businesses across all 50 states, they say.

Paul Hatcher, chief executive officer and founder of Merrill Herzog, the crisis management specialist, warns that prevention of workplace violence is not a one-size-fitsall exercise. “There are law firms that know nothing about prevention of active shooter risks, which have been selling a ‘compliant’ template online for $150 to businesses in California.”

He said a plan needs to be an actionable, living docu-

ment—and not one that sits on the shelf.

Hatcher was discussing how businesses can remain compliant with California’s workplace violence prevention law (SB 553), which has been in effect since July 1, 2024. But businesses across the country can also benefit by implementing their own plans, similar to what is required by the law to help prevent workplace violence. (See related article on page 28.)

Wyoming-headquartered Merrill Herzog often works closely with Gabriel, an Israelbased security technology company, to develop risk prevention protocols. Further, they often partner with specialty insurers, such as Chaucer, and Samphire Risk, the managing general agent, which include loss prevention and risk mitigation services as part of their active assailant insurance policies.

“Preparation, planning, and

prevention for these horrific events can ultimately save lives, and insurance is leading the way as a forcing function to help organizations do just that,” said Hatcher. “The harsh reality is most attacks could have been prevented had the early warning signs simply been identified, communicated, and dealt with properly. The earlier you can identify a potential or actual threat, the higher the probability that you can stop it.”

Lives can be saved through simple awareness, he added.

It’s important that businesses ensure they have the proper procedures and policies in place and that these plans are actionable, rather than creating a document of 300 pages, which just sits on a shelf gathering dust like many organizations have, Hatcher said.

“We work with those organizations to help them create actionable policies that will both protect them in

the immediate situation and then also post-incident when everybody gets sued—because everybody will get sued.”

And then there’s the training, which Hatcher said includes everything from the tactical side of training—such as run, hide, and fight—to emergency medical training. Also included are tabletop exercises and full-scale exercises with local law enforcement integration.

“We have an acute focus on not looking at what everybody else has done, per se, to check the box, but work to actually build a product that helps protect people and save lives. That has been our goal. And so every time we step into a new organization, we look at it and go, ‘Is this fit for purpose? Does it work?’ Because the policies and procedures are not one size fits all,” Hatcher said.

For active assailant, he said, Merrill Herzog’s main role is to prevent attacks via security audits and technology integratio—which involves working with an organization like Gabriel and its founder and CEO Yoni Sherizen.

Gabriel provides the technology while Merrill Herzog helps identify where the organization needs panic buttons and cameras.

“And then we integrate our services together to create a comprehensive active shooter or active assailant mitigation program, if that’s what the clients want,” Hatcher explained.

“Couple that with insurance, and you’ve mitigated, transferred risk like no other program out there,” he said.

Sherizen described the work of Merrill Herzog and Gabriel with the re/insurer Chaucer as taking an historic step in preventing mass shootings and other active assailant threats because the product incentivizes preventative measures, rather than simply paying for the consequences of these deadly events.

Insureds that buy active assailant cover from Chaucer have the benefit of the risk management services offered by Merrill Herzog and Gabriel. “Those insureds get real-time crisis management support through Gabriel’s automated alerting platform that loops in with the Merrill Herzog response team,” Sherizen said.

Early Detection

“Merrill Herzog doesn’t do gates, guards, and guns. We’re not a security firm, and we don’t do technology or installation of cameras. We are advisers on risk,” Hatcher said. “We come in from a ground truth perspective of how can a business deter, detect, and delay an attacker coming.”

Having cameras on a prem-

ises isn’t enough. They record an incident and don’t stop an attack—and mass shooters don’t care if they’re on camera, both risk executives affirmed.

Gabriel goes far beyond cameras by creating a backend integration of various systems, which, using artificial intelligence, includes early detection of an active shooter. Gabriel also provides panic buttons, which include shot detectors, and video cameras, which provide emergency monitoring once the panic button is hit.

Gabriel’s hub leverages AI, smart automation as well as human intelligence. “There are two sides to the coin, but we often say we’re ‘trigger agnostic,’” according to Sherizen at Gabriel.

For example, the Gabriel platform kicks in if the camera spots a weapon, if an access control system identifies someone trying to get into the building, or if a former employee is trying to use key cards to gain access, he said, noting that the platform continued on page 26

‘Most of us grew up with fire alarms and fire drills, or depending where in the world you live, tornado drills. We learned [that] when you have the alert, you do X, everything will be okay. Unfortunately, [for] our children and in today’s workplaces, the threats have become very dynamic and change from second to second.’

– Yoni Sherizen, CEO and founder of Gabriel

‘Preparation,

planning, and prevention for these horrific events can ultimately save lives, and insurance is leading the way as a forcing function to help organizations do just that.’

- Paul Hatcher, CEO and founder of Merrill Herzog

Special Report: Risk Management

continued from page 25

automates all the critical things that have to happen at the same time.

When a threat has been detected, the Gabriel system automatically alerts key stakeholders. “Once a threat has been verified, then law enforcement is immediately contacted,” Sherizen said.

Gabriel’s system doesn’t just provide camera monitoring—it provides a virtual command, based on what a first responder would want to have: a floor map for the entire building that shows where the assailant is in real time. In addition, the dashboard provides a breakdown of emergency action plans, who to contact

110 results for ‘agriculture’

with all needed emergency and medical numbers. Everything the crisis team needs is in the palm of their hands, Sherizen said.

And last but not least, Gabriel provides real-time communications chat within the application, so the crisis team can communicate with staff and the victims.

During an emergency, the crisis team in charge has the ability to send responding law enforcement via text or email a web-based link to the real-time situation, Hatcher said, explaining that it’s a single time share link which goes away after the incident to provide privacy along with an immediate response.

Everything happens in parallel, rather than sequentially as has been tradition. Under the normal processes for such attacks, someone will see something, phone security, and security will pull up the camera system and finally go to their access control system and lock the doors, Sherizen said. That sequence of events leads to critical lost time, chaos, and people at greater risk of being harmed in a best-case scenario, he added. “In the worst-case scenario, there will be actual damage to people, property, and the business.”

Sherizen said Gabriel aims to leverage technology in an unobtrusive way “to get ahead of these threats by picking up on suspicious behavior, suspicious activity, objects, etc., and then automating the workflow from there,” without creating a prison-like environment for businesses.

“Most of us grew up with fire alarms and fire drills, or depending where in the world you live, tornado drills. We learned [that] when you have the alert, you do X, everything will be okay. Unfortunately, [for] our children and in today’s workplaces, the threats have become very dynamic and change from second to second,” Sherizen said.

“So, we need new technological tools in order to be able to manage that and have the situational awareness and the ability to communicate in real time, to get people away from danger, and as danger evolves, to continue to update information and alerts to keep people safe.”

News & Markets

Washington Bill Would Provide Restitution for Policyholders Harmed by Insurers

Abill to allow the Washington’s insurance commissioner to order restitution for policyholders

harmed by insurance companies moved out of the state Senate Business, Financial Services, and Trade Committee.

Senate Bill 5331 gives the commissioner authority to require insurers to compensate insureds who have been wronged in the insurance process, addressing a current gap in the law that limits enforcement to fines without restitution. Fines collected by the OIC go to the state’s general fund.

The bill, sponsored by Senator Adrian Cortes, D-Battle Ground, also authorizes the commissioner to fine property/ casualty insurers companies up to $10,000 per violation, rather than issue a total fine of $10,000. For health insurers, the limit is already $10,000 per violation or offense. SB 5331 would align the two.

Insurance Commissioner Patty Kuderer said the bill will enable the state to provide more direct aid to victims.

The bill now moves to the full Senate for further consideration.

AM Best Revises Outlooks to Negative for Mercury and Subsidiaries Over LA Wildfires

AM Best revised the outlooks to negative from stable and affirmed the Financial Strength Rating of A (Excellent) and the Long-Term Issuer Credit Ratings (Long-Term ICR) of “a” (Excellent) for the members of Mercury Casualty Group.

Concurrently, AM Best revised the outlook to negative from stable and affirmed the Long-Term ICR of “bbb” (Good) of the organization’s publicly traded ultimate parent, Mercury General Corporation based in Los Angeles. AM Best also revised the outlook to negative from stable and affirmed the Long-Term Issue Credit Rating of “bbb” (Good) of MGC’s $375 million, 4.4% senior unsecured notes, due 2027.

and costs stemming from the recent Los Angeles wildfires in January.

Mercury has exposure to the Palisades and Eaton fires, with gross catastrophe losses estimated at $1.6 billion to $2.0 billion before reinsurance, subrogation, FAIR Plan assessments and recoupment of FAIR Plan assessments. Mercury’s reinsurance program provides for catastrophe reinsurance limits of $1.29 billion on a per occurrence with a retention of $150 million and reinstatement premium of $101 million.

The ratings reflect Mercury’s balance sheet strength, which AM Best assesses as very strong, as well as its adequate operating performance, neutral business profile and appropriate enterprise risk management.

The outlooks were revised to negative due to uncertainty of Mercury’s net ultimate losses as well as uncertainty surrounding future reinsurance structure

Fitch Ratings said in an outlook revision in late January that it expects MCG’s credit profile will withstand the impact of the Eaton and Palisades fires near Los Angeles, but the agency also gave a negative outlook that reflects “the potential for credit deterioration and financial pressure from a third large catastrophe event or an aggregation of smaller weather-related claims.”

AM Best said its rating affirmations reflect its expectation that Mercury’s capital position will withstand the impact of the wildfires after the company makes the full determination of its ultimate losses.

“The outlooks are expected to remain negative until such time that AM Best can with certainty establish the impact of the ultimate net losses from the California wildfires on Mercury’s capital, profitability, and future reinsurance costs,” AM Best stated.

The FSR of A (Excellent) and the LongTerm ICRs of “a” (Excellent) were affirmed by AM Best with the outlooks revised to negative from stable for the following members of MCG:

• Mercury Casualty Company

• Mercury Insurance Company

• California Automobile Insurance Company

• California General Underwriters Insurance Company, Inc.

• Mercury Indemnity Company of Georgia

• Mercury Insurance Company of Georgia

• Mercury Insurance Company of Illinois

• Mercury Indemnity Company of America

• Orion Indemnity Company

• American Mercury Insurance Company

• American Mercury Lloyds Insurance Company

• Mercury County Mutual Insurance Company

News & Markets

FEMA to Borrow $2 Billion to Pay Flood Claims After Hurricanes Helene and Milton

By Chad Hemenway

The Federal Emergency Management Agency said in February that it needs to borrow $2 billion from the U.S. Treasury to cover claims from National Flood Insurance Program policyholders.

FEMA, administrator of NFIP, said it expects to pay out more than $10 billion in flood claims related to hurricanes Helene and Milton in 2024, as well as claims for other flooding events last year.

“The NFIP is not designed to pay for multiple catastrophic events in a single year without additional financial assistance,”

FEMA said. “The combined losses from 2024 have depleted the NFIP’s funds generated from premiums to pay claims.”

More than 57,400 flood claims related to Hurricane Helene have been handled by the program, which has paid out more than $4.5 billion as of Feb. 6. It expects to pay losses from Helene of between $6.4 billion and $7.4 billion.

February on over 21,100 claims. The range of final losses from Milton is estimated to be $1.2 billion to $2.9 billion, FEMA said. Milton struck Florida on Oct. 9, 2024. For the private insurance industry, Milton will go down as the costliest hurricane of the historic 2024 season, and the storm will likely be one of the costliest of all time. But Milton was more of a wind event than Helene, which made landfall in Florida as a Category 4 in late-September before dumping record rainfall in Southeast states including Georgia, North Carolina, and South Carolina.

For Milton, the NFIP so far has paid out over $740 million as of the first week in

FEMA’s debt is now about $22.5 billion. It has the authority to borrow up to about $30.4 billion and already had borrowed $20.5 billion following hurricanes Katrina, Sandy, and Harvey, FEMA said. Elizabeth Asche, senior executive of the NFIP, said it is “strategically utilizing short-term borrowings in 60-day increments, demonstrating our careful and responsible management of the borrowing authority.” She added: “The widespread, devastating flooding following hurricanes Helene and Milton re-emphasizes the financial effects

flooding can have not just to survivors but also the National Flood Insurance Program.”

According to the Congressional Research Service, the NFIP—funded by the premiums it collects for flood insurance policies—had $615 million on hand as of Jan. 25 to pay claims.

CRS, a nonpartisan shared staff to congressional committees and members of Congress, said NFIP owes the debt it takes and pays for accruing interest through premiums. Since 2005, the NFIP has made six principal repayments totaling about $2.8 billion and interest of about $6.2 billion. CRS said the program pays about $619 million in interest annually, accruing $1.7 million in interest daily.

The program did not need to borrow between November 2017 and February 2025. According to CRS, NFIP in October 2017 had $16 billion of debt cancelled of a total of about $30.4 billion at the time. This was to pay claims for hurricanes Harvey, Irma, and Maria. But in November 2017, NFIP borrowed $6.1 billion to pay claims for losses incurred from this trio of hurricanes, increasing total debt to about $20.5 billion—where it stood until now.

NFIP has been reauthorized 32 times since 2017. Its current reauthorization is set to expire on March 14.

Sedgwick: U.S. Product Recalls Reached High Level Again Last Year

The number of U.S. product recalls remained high in 2024 with more than 3,200 events recorded for the second consecutive year, a new report shows.

Sedgwick brand protection’s 2025 U.S. State of the Nation Recall Index, which analyzes recall data from the automotive, consumer product, food and drink, pharmaceutical, and medical device industries, shows 3,232 recalls across five industries, marking the second-highest annual total in the past six years. According to the authors of the report, 2023 and 2024 are the only consecutive years in the past decade in

which U.S. recall events have exceeded 3,200.

However, the 680.9 million defective products recalled last year was the lowest level since 2015, a drop from the nearly 1.5 billion units recalled just two years earlier in 2022. The report shows multiple industries hit recall milestones in 2024. The consumer products sector experienced its second-highest recall total in the past eight years, while the medical device sector recorded a four-year high for

recall events. The food and drink industry recorded the second-lowest annual total in the last decade in 2024, despite a six-year high in terms of units impacted. The pharmaceutical sector hit an 11-year annual low for the number of defective units recalled. Despite the relatively low number of units recalled, the food and drink industry faced several major recalls in 2024, driven by safety risks such as lead-contaminated cinnamon and Listeria contamination in

Idea Exchange: Workers’ Compensation

A Review of California’s Workplace Violence Prevention Law

Workers’ compensation insurers and California employers alike have faced new responsibilities for employee safety from July 1, 2024, when legislation aimed at reducing workplace violence took effect. Now that the law has been in effect for six months, perhaps it is a good time to review its essential aspects.

By David Lawhorn

The Workplace Violence Prevention Bill (SB 553) marks the first time a state has attempted to address the pressing issue of attacks on employees across general industry. It has been several years in the making and, after a COVID-related delay, gained new impetus following the fatal 2021 shooting by a co-worker of nine staff working at a San Jose railyard.

The rules are far-reaching and center on the creation and implementation of written Workplace Violence Prevention Plans (WVPPs). They apply to all companies in the state with only a few exemptions. Healthcare is one of these since stringent requirements for that sector already apply. At first sight, the legislation may look daunting. It defines “workplace violence” broadly, to include any act of violence or threat of violence that occurs in a place of employment. It also hands workers’ comp insurers responsibility for auditing the WVPPs or enlisting a certified professional to do so. Some commentary has focused on potential liability issues for carriers associated with this oversight role. However, the legislation provides a good opportunity for the insurance industry to demonstrate the value of its services.

Despite the July 1 effective date, many companies are still working to completely

fulfill their obligations under the law. The biggest implication for insurers are the resources and training that have been needed to be put in place to help clients comply.

To do so, employers have been establishing, implementing, and maintaining effective written WVPPs including:

• Allocation of responsibility for implementing the plan.

• Employee involvement.

• Communication and training.

• Identification and correction of hazards.

• Incident response.

• Procedures for reporting and investigating incidents.

• Plan reviews.

In addition, employers must keep records of workplace violence hazard assessment, incident logs, and investigations for a minimum of five years, and

training records for at least a year.

SB 533 isn’t California’s final response to the workplace violence issue. It is intended as an interim framework while the California Division of Occupational Safety and Health devises new standards and regulations. It must do so by Dec. 31, 2025, for adoption no later than Dec. 31, 2026.

It is up to insurers to help clients keep abreast of any changes to last year’s requirements as the new regulations are enacted.

When pondering the impact on insurers’ costs and on rates, it is important to keep sight of the fact that the legislation is designed to reduce the likelihood of injury or death in the workplace, rather than to make things harder for companies and their workers’ comp carriers.

Current data isn’t available, but in 2022, the Department of Justice reported a worrying increase in fatal and non-fatal workplace violence in the five years to 2019. In total, 17,865 people were killed at work from 1992 to 2019 across the country.

A total of 454 homicides took place in 2019, which marked a 58% decrease from a peak of 1,080 homicides recorded in 1994. From 2014 to 2019, workplace homicides increased by 11%, according to the DOJ’s Bureau of Justice Statistics.

The US Bureau of Labor Statistics in 2022 published data recording 392 workplace homicides in 2020 and another 37,060 non-fatal injuries from workplace violence.

Sales and related occupational groups accounted for almost a quarter of all workplace homicides. The second most affected sector was transportation and material moving.

This legislation should help businesses identify their unique exposures and put specific controls in place as protection for these exposures.

The California bill is expected to be emulated by other states, many of which are already contemplating legislation to combat workplace violence, according to legal intelligence company

LexisNexis. The Californian requirements and any other legislation they inspire are likely to encourage critical thinking when it comes to addressing workplace violence.

In terms of the industry’s new oversight role, many workers’ comp carriers are rising to the occasion. Audits are already part of normal business practices, and insurers are required to conduct or verify safety consultations or carry out claims analyses in states including New York, Pennsylvania, Texas, and Arkansas.

Some of these are much more resource-hungry than the pending California rules. In New York, for example, Code Rule 59 stipulates safety and loss prevention consultations and evaluations for workplaces with payrolls of over $800,000 and an experience modification rate of more than 1.2. (EMRs are used to quantify risk for the purpose of workers’ comp insurance, with the average being 1.0.) Employers that do not follow the law have to pay a 5% surcharge on the manual portion of their workers’ comp premium, with that surcharge rising another 5% for each year of non-compliance.

As for fears that this could spark a wave of lawsuits against insurers if insureds’ WVPPs prove ineffective, or encourage claims on general liability policies, it’s unwise to make blanket predictions. The industry similarly spent a lot of time hypothesizing about possible liability exposures during COVID, but the reality is these situations are complex and nuanced, with their own unique circumstances.

Fortunately, there haven’t been significant additional costs from the resources insurers have deployed to help clients meet their new obligations and to execute our own oversight responsibilities.

‘This legislation should help businesses identify their unique exposures and put specific controls in place as protection for these exposures.’

Insurers are expert at adapting to evolving risk and changing regulatory requirements, and will continue to do so.

In terms of workers’ comp rates and carrier appetite for the line of business, there is the theoretical possibility that this legislation significantly reduces workplace violence. If that does, in fact, happen, it could influence lines of business that tend to have higher workplace violence claims, such as school systems.

Time will tell how effective requiring businesses to have a written WVPP that includes employee involvement and job hazard analysis will be.

However, the new law represents a real chance for carriers to burnish their credentials as risk advisory partners rather than merely recipients of premiums and payers of claims.

We all want to end workplace violence, and those insurers that can offer appropriate resources and assist with compliance have a great opportunity to make their mark.

Lawhorn is director of loss control at AmTrust Financial Services Inc. He is a seasoned risk management leader with nearly 30 years of experience in loss control and underwriting support. As director of Loss Control at AmTrust Financial Services, he oversees risk control for excess and surplus lines, the QC Department, and RC Technical Services. Lawhorn previously led the National Field Risk Control Team and then Large Account Services. He has held leadership roles at FHM Insurance Co., Falls Lake Insurance, and Builders Mutual, specializing in workers’ compensation and multi-line risk control. His expertise spans construction, manufacturing, hospitality, and largescale risk management.

Hospitality Risks

Directory

Searching for the right market for a hard-to-place hospitality risk? Look no further than Insurance Journal’s Hospitality Risks Directory — a comprehensive listing of excess and surplus lines intermediaries and carriers offering hospitality risks coverage nationwide.

The information listed in this directory has been compiled to serve as a resource guide for independent agents and brokers looking for superior markets for everything from nightclubs to special events, hotels to motels, spas, resorts and restaurants too.

All markets profiled in this directory have been updated with the most current information available provided directly by the intermediaries and carriers writing the coverage. IJ has made every attempt to ensure the accuracy of all information listed in this directory.

To submit a listing for future Hospitality Risks directories, e-mail Kristine Honey at: khoney@insurancejournal.com. We hope you find IJ’s 2025 Hospitality Risks Directory to be a useful tool when searching for quality markets.

To comment on this directory, or any other Insurance Journal resource, please e-mail: editorial@insurancejournal.com.

Banquet Halls

Banquet Halls coverage category sponsored by:

Nautilus Insurance Co. & Great Divide Ins. Co. - for more info, check out our ad on page 19 (National).

Banquet Halls

Eastern

Executive

First

(Liq. Liab

Gorst & Compass Insurance

Hospitality

Insurance Program Mgrs Group (Work Comp)

James River Insurance Company All States

Jimcor Agencies

JM Wilson

Joseph Krar & Associates

Nautilus Insurance Co. & Great Divide Ins. Co. All States

NeitClem Wholesale Insurance Brokerage, Inc. AZ CA NV

New Age Underwriters Agency, Inc. Most States

New England Excess Exchange

Number One Insurance Agency, Inc. MA

Osprey Underwriters All States

Pacific Excess Insurance Marketing Most States

Patriot National Underwriters, Inc. AR KS

Professional Liability Ins. Svcs, Inc. - Underwriting Facilities All States

Quirk & Company

River Valley Underwriters

Roush Insurance Services, Inc. IA IL

RT Specialty

Southern Insurance Underwriters (SIU)

Specialty Insurance

TAPCO Underwriters, Inc. Most States

W.A. Schickedanz Agency, Inc. AR IL MO

Walter General Agency (WGA) AR

Western Surplus Lines Agency, Inc. LA

Wilson Smith Group AZ

XPT Specialty