Exploring the MedSpa M&A Market

Trends, drivers and 2025 outlook for this emerging industry

Medical spas, or MedSpas, are hybrid establishments combining the luxury of a traditional spa with medical-grade aesthetic procedures. As an intersection of health, beauty and medicine, MedSpas have seen a surge in popularity in recent years. As wellness and aesthetic care continue to gain prominence in the daily lives of millions, the medical spa sector has become a focal point for M&A, reflecting a robust market landscape poised for further growth.

The MedSpa sector's prominence was evident at various healthcare conferences attended by the LevinPro HC team in 2024. During McGuireWoods ’ 17th Annual Healthcare Finance and Growth Conference in September 2024, Eugene Goldenberg of Edgemont Partners commented:

Similarly, Craig Castelli of Caber Hill Advisors also noted during the

Continued on page 2

Physician Group M&A Slows

Economic and election uncertainty hits on 2024 activity

The Physician Medical Group (PMG) sector experienced a decline in deal volume throughout the year. In 2024, 473 PMG deals were announced, a 12% decline from the 537 PMG deals announced in 2023 and a 24% decrease from the 622 deals reported in 2022. In the fourth quarter of 2024, there were 101 PMG deals, which is the slowest quarter for the year.

Visit us Online: levinassociates.com

Some advisors that the LevinPro HC team has spoken to throughout the year have noted several significant factors contributing to the decline in PMG deal volume. Common themes that advisors cited were uncertainty surrounding the election, an unstable economy, higher interest rates and even heightened scrutiny surrounding private equity investments in the healthcare industry.

Continued on page 12

McGuireWoods conference:

"Med Spa was a surprise a year or two ago, but at this point, it’s no longer a secret."

Although the MedSpa market is typically an area we do not cover at LevinPro HC, due to its focus on nonmedical, aesthetic services rather than traditional healthcare, we have decided to dive a little deeper into this sector to understand what exactly is driving activity in the sector.

The primary driver behind MedSpa M&A activity is the escalating demand for non-invasive cosmetic procedures, fueled by a focus on personal appearance and health consciousness. Consumers are increasingly willing to invest in aesthetic enhancements like laser hair removal, Botox injections and body contouring, especially with rising disposable incomes supporting these luxury treatments. Technological advancements

further propel this growth, as MedSpas adopt innovative treatments that enhance both efficacy and safety, attracting more clients and making these establishments lucrative for investors interested in new tech integration.

Additionally, the market's fragmentation, with more than 66% of MedSpas being under single ownership as of 2024 according to the 2024 Medical Spa State of the Industry Report by the American Med Spa Association, offers substantial opportunities for consolidation. This allows investors to merge or acquire smaller practices, streamline operations and expand market share. Demographic trends also play a pivotal role; an aging population seeking anti-aging solutions alongside a growing demographic, both male and female, interested in aesthetic services broadens the consumer base, diversifying service offerings and boosting M&A appeal.

ISSN#: 2375-7612

Published monthly by: Irving Levin Associates LLC

P.O. Box 1117, New Canaan, CT 06840

Phone: 800-248-1668 Fax: 203-846-8300 info@levinassociates.com

www.levinassociates.com

Editor: Dylan Sammut

Analyst: Kate Humphrey

Analyst: Avery Swett

Advertising: Cristina Blazek-Hearty

The full, annual subscription includes 51 weekly e-newsletters, 12 monthly issues, four quarterly reports

©2025 Irving Levin Associates, LLC All rights reserved. Reproduction or quotation in whole or part without permission is forbidden.

This publication is not a complete analysis of every material fact regarding any company, industry or security. Opinions expressed are subject to change without notice. Statements of fact have been obtained from sources considered reliable but no representation is made as to their completeness or accuracy.

Navigating the complex regulatory environment presents both challenges and opportunities, requiring strategic deal structuring to comply with varying state laws on medical practice ownership. A key factor is the Corporate Practice of Medicine doctrine, which differs by state but generally restricts non-physician ownership of medical practices. To work within these constraints, investors often employ strategies like management service organizations or physician partnerships, allowing for compliant acquisitions while enabling growth.

Additionally, the surge in wellness tourism has positioned MedSpas as key attractions for travelers, encouraging strategic investments in new markets to capitalize on this global interest. In the United States, cities such as Miami, with its luxury spa culture and accessibility, Los Angeles, where Hollywood drives aesthetic trends, and New York City, a global hub for fashion and beauty, have emerged as hotspots for MedSpa medical tourism. According to American Med Spa Association’s 2024 report, the U.S. medical spa industry saw an increase from 1,600 facilities in 2010 to a projected 11,553 by 2025, reflecting a significant growth in demand for these services. These destinations blend aesthetic medical treatments with

May 15-16, 2025

Encore Boston Harbor | Boston, MA

www.may25.nhcfosummit.com

www.may25.nhcxosummit.com

vacation experiences, attracting clients looking for both rejuvenation and a taste of local culture, highlighting a trend where medical procedures are increasingly part of a broader travel itinerary.

According to market research, the global MedSpa market was forecasted to reach $22.2 billion by the end of 2024 and grow to $83.9 billion in 2033, with a compound annual growth rate of 15.7%, indicating not just a burgeoning interest but a sustained growth trajectory. Among the most active players in the MedSpa M&A market in 2024, Princeton Medspa Partners led with three acquisitions (Ridha Plastic Surgery & Medspa, Pure Skin Aesthetic & Laser and Mirabile Beauty, Health & Wellness), demonstrating a clear strategy for growth through consolidation.

The 2025 Outlook: Trends and Advice from Industry Experts

As Alex Veach, Director of Transaction Services at Austin, Texas-based Agenda Health, shared in a recent

interview, MedSpa M&A activity is expected to intensify through 2025.

“Our firm had the opportunity to advise on several MedSpa transactions in 2024, and we expect to see that trend grow even stronger in 2025,” said Veach. “The space has seen several healthcare investors acquire aesthetics platforms in 2023 and 2024 - we think these buyers will aggressively pursue acquisition opportunities to grow their platforms over the course of 2025. This will create a great exit environment for owners looking to exit.”

Regarding what sets MedSpa transactions apart from other healthcare deals, Veach highlighted the unique value placed on ownership and provider reputation in the space:

“Every sector of healthcare services is different and requires deep experience to facilitate successful exits. There are a myriad of examples for this in the MedSpa space, but one key factor in our MedSpa transactions

Esteemed Media Partner

that differentiates it from others we work in is the emphasis aesthetic businesses place on their owners and providers. Buyers in this space place a high value premium on practices with owners and providers that have a great reputation in their communities, and in our transactions, will look to make sure they can construct partnerships with owners in a way that aligns incentives and empowers them with resources to expand their reputation and brand into new markets.”

Veach also offered advice for prospective buyers looking at the MedSpa space:

“In our experience, being willing to pay a premium for the right brand can make all the difference for buyers looking to build a platform in the space. Since this space is so reputation-centric, buyers who are willing to pay up for the right brand with great owners attached will set themselves up for success as they build their platform.”

Looking ahead to 2025 and beyond, the MedSpa sector will continue its rapid expansion, driven by strong consumer demand and advancements in aesthetic technology. Private equity firms and strategic buyers remain highly engaged, drawn to the sector’s highmargin services and recurring revenue potential. As competition intensifies, investors will likely focus on consolidation and scaling operations to strengthen their market positioning.

Regulatory complexities, particularly state-specific laws governing medical practice ownership, will continue to influence deal structuring and acquisition strategies. Additionally, the growing influence of medical tourism and continued innovation in non-invasive treatments could further shape the market. With sustained consumer interest and financial backing, the MedSpa industry is poised to remain a profitable segment within the broader healthcare and wellness landscape.

Top Stories of January 2025

Zimmer Biomet Buys Paragon 28 For Approximately $1.1 Billion

Zimmer Biomet Holdings, Inc. announced that it

entered into a definitive agreement to acquire all outstanding shares of common stock of Paragon 28, Inc. for an upfront payment of $13 per share in cash. This corresponds to an equity value of approximately $1.1 billion and an enterprise value of approximately $1.2 billion.

Based in Englewood, Colorado, Paragon 28 is a medical device company exclusively focused on the foot and ankle orthopedic segment and is dedicated to improving patient lives. The company was established in 2010 to address unmet and under-served needs of the foot and ankle community. Paragon 28 provides orthopedic solutions, procedural approaches and instrumentation that cover a wide range of foot and ankle ailments including fracture fixation, forefoot, ankle, progressive collapsing foot deformity or flatfoot, Charcot foot and orthobiologics.

Zimmer Biomet makes and markets musculoskeletal products that help treat patients suffering from disorders of or injuries to bones, joints, or supporting soft tissues. The company has operations in 25 countries and sells in more than 100 countries. According to its financial results report, it generated $7.39 billion in revenue for the full year of 2023.

The proposed transaction is expected to immediately accelerate Zimmer Biomet's revenue growth. Zimmer Biomet plans to fund the proposed transaction through a combination of cash on the balance sheet and other available debt financing sources. The transaction is anticipated to close in the first half of 2025.

Goldman Sachs is serving as exclusive financial advisor to Zimmer Biomet and Hogan Lovells is serving as legal advisor. Piper Sandler is serving as exclusive financial advisor to Paragon 28 and Cravath, Swaine & Moore LLP is serving as legal advisor.

New Mountain Capital Makes Growth Investment in Access Healthcare

Dallas, Texas-based Access Healthcare has announced a strategic investment from affiliates of the private equity firm New Mountain Capital. This investment

will support Access Healthcare's next phase of growth, focusing on advancing its capabilities in artificial intelligence, workflow automation, product development and expanding into new markets.

Access Healthcare is a technology-enabled revenue cycle management platform that helps healthcare providers and stakeholders reduce costs by improving operations across the front-end, mid-cycle and backend of the revenue cycle. The company was founded in 2011.

New Mountain Capital is a growth-oriented investment firm with more than $55 billion in assets under management. It is based in New York City.

The Access Healthcare leadership team will continue to guide the organization through its next phase of growth and development. Financial terms of the deal were not disclosed.

In Motion Physical Therapy Joins PE-Backed Ivy Rehab

Private equity-backed Ivy Rehab announced in January 2025 that it has partnered with In Motion Physical Therapy in Downingtown, Pennsylvania. Financial terms of the deal were not disclosed.

In Motion Physical Therapy is a provider of outpatient physical therapy in Pennsylvania. The company is led by a team of therapists specializing in orthopedics, spine rehabilitation and manual therapy.

Founded in 2003, Ivy Rehab, a portfolio company of middle-market private equity firm Waud Capital Partners , is a network of outpatient physical, occupational and speech therapy and applied behavior analysis clinics throughout the United States.

"We are thrilled to welcome In Motion to Ivy Rehab," said Jonathan Jean-Pierre, Chief Operating Officer of Ivy Rehab. "Their commitment to providing personalized,

high-quality care aligns perfectly with our mission to deliver exceptional rehabilitation services. By joining forces, we can expand access to top-tier physical therapy and continue to positively impact the Downingtown community."

"This partnership with Ivy Rehab allows us to bring even greater resources and expertise to our patients, enhancing their care and supporting our mission of helping individuals achieve their highest level of function and well-being," said Brock Harper, Owner of In Motion Physical Therapy.

Concentra Announces Agreement to Acquire Nova Medical Centers for $265 Million

Concentra Group Holdings Parent, Inc. announced that it has signed an agreement to acquire U.S. Occmed Holdings, doing business as Nova Medical Centers The transaction values Nova Medical Centers at $265 million and is expected to close in the first quarter of 2025.

Nova Medical Centers is an occupational health services company based in Houston, Texas. The company operates 67 centers in Texas, Georgia, Tennessee, Indiana and Wisconsin providing workers’ compensation injury care services, physical therapy, drug and alcohol screening and pre-employment physicals as part of its full suite of occupational health services.

Concentra is a leading healthcare company focused on improving the health of America's workforce. Through its managed practice groups and affiliated clinicians, the company currently provides occupational medicine, urgent care, physical therapy and wellness services from 520 medical centers nationwide. Concentra was created through a joint venture between Select Medical Corporation, a wholly owned subsidiary of Select Medical, Welsh, Carson, Anderson & Stowe and other minority equity holders including Cressey & Company.

The transaction was announced alongside Concentra's preliminary 2024 financial results on January 22, 2025. Concentra currently expects to finance the

announced transaction using a combination of cash on hand, available borrowing capacity under its existing revolving credit facility and new debt financing.

Johnson & Johnson Buys Intra-Cellular Therapies For $14.6 Billion

Johnson & Johnson (J&J) announced on January 13 that it will acquire all outstanding shares of Intra-Cellular Therapies for $132.00 per share in cash for a total equity value of approximately $14.6 billion.

Intra-Cellular Therapies is a biopharmaceutical company focused on the development and commercialization of therapeutics for central nervous system disorders. According to its most recent annual report, Intra-Cellular Therapies had revenues of $462 million during fiscal year (FY) 2023, and EBITDA was reported as a loss of nearly $158.9 million during FY 2023.

Intra-Cellular has developed CAPLYTA® (lumateperone), a once-daily oral therapy approved to treat adults with schizophrenia, as well as depressive episodes associated with bipolar I or II disorder (bipolar depression), as a monotherapy and adjunctive therapy with lithium or valproate. The company has also developed ITI-1284, a Phase 2 compound being studied in generalized anxiety disorder and Alzheimer’s disease-related psychosis and agitation, as well as a clinical-stage platform.

J&J is one of the largest global healthcare and pharmaceutical companies with more than 130,000 employees worldwide. Its business lines include pharmaceuticals, medical devices and consumer healthcare products. According to its most recent financial report, J&J's revenue for the full year 2023 was $85.2 billion, and EBITDA was approximately $24.6 billion.

With this agreement, J&J adds Intra-Cellular Therapies’ CAPLYTA®, ITI-1284 and its clinical-stage pipeline to its portfolio. The closing of the transaction is expected to occur later in 2025.

Citi is serving as financial advisor to J&J, and Cravath,

Swaine & Moore is serving as its legal advisor. Centerview Partners LLC and Jefferies are serving as financial advisors to Intra-Cellular Therapies, and Davis Polk & Wardwell LLP is serving as its legal advisor.

This deal also represents J&J’s sixth-largest healthcare transaction to date, surpassing its $13.1 billion acquisition of Shockwave Medical earlier in 2024. J&J’s largest healthcare transaction to date remains its $30 billion acquisition of Actelion Ltd., announced in January 2017.

InTandem Capital Completes Strategic Investment in Healthfuse

InTandem Capital Partners, LLC, a healthcare servicesfocused private equity firm, announced that it has completed a strategic equity investment in Milwaukee, Wisconsin-based Healthfuse.

Founded in 2011, Healthfuse combines proprietary technology, analytics and research to help hospitals build, operate and optimize their revenue cycle vendor management office and guarantees bottomline improvement. Healthfuse has delivered more than $1.5 billion in bottom-line improvements for its clients, which includes a network of more than 350 hospitals nationwide.

New York-based InTandem Capital Partners invests in and helps accelerate the growth of small to mid-sized companies in select healthcare services sectors.

Goodwin Procter served as legal counsel to InTandem Capital, and TripleTree served as the firm’s exclusive financial advisor. Cantor Fitzgerald & Co. served as Healthfuse’s exclusive sell-side financial advisor and Bass, Berry & Sims served as its legal counsel. Financial terms of the deal were not disclosed.

Optima Health Expands Occupational Health Services With BHSF Occupational Health Deal

Optima Health announced on January 16 that it has acquired BHSF Occupational Health for £1.4 million (approximately $1.7 million USD). The acquisition will expand Optima’s customer base

and add 60 occupational health clinicians to its team.

BHSF Occupational Health is a United Kingdom-based company specializing in preventing work-related illnesses and injuries, safeguarding workers from occupational hazards and promoting overall workplace health and safety. According to the original deal press release from January 16, the business generated £8.3 million (approximately $10.1 million USD) in revenue, £3 million (nearly $3.7 million USD) in gross profit and a pretax loss of £400,000 (approximately $488,000 USD).

Optima Health is a United Kingdom-based provider of corporate health and wellbeing solutions that help organizations and their people by managing their health.

“The decision to sell the business to Optima Health plc comes after careful consideration, and we believe Optima will be a great home, as they share very similar values and their commitment to excellence aligns with BHSF,” said Stuart Hayhurst, Chief Executive Officer of BHSF Group. “We are confident that the business will continue to thrive under the new leadership.”

Optima Health sees potential to grow the business and is actively seeking additional bolt-on acquisitions to enhance its portfolio.

PwC’s Behind the Numbers of Medical Costs

PwC’s Health Research Institute published an article in early January 2025 that projects commercial healthcare spending growth will hit a 13-year high in 2025, with an 8% increase in the Group market and 7.5% in the Individual market. This is driven by inflation, the rising cost of prescription drugs and increased behavioral health utilization. Updated 2023 and 2024 trends reveal higher-than-expected costs due to increased use of GLP-1 drugs and deferred pandemic care.

While cost-saving measures like biosimilars offer some relief, they do not counter the increasing expenses. The report highlights the need for healthcare organizations to develop strategies that balance cost management with affordability. This is necessary to address the

broader challenge of healthcare accessibility.

The article continues to say, “Organizations should reshape strategies; reengineer financial, workforce and business models and capitalize on each transformational opportunity — from investments in innovation and technology to deals — to overcome the inflationary chokehold and forge a path to a drastically different cost and business model.”

Healthcare inflation is driven by rising hospital service costs, which grew 6.3% year over year in Q4:23, and ongoing wage inflation. Despite improved hospital margins in 2024 compared to 2022, providers face operational challenges and higher expenses. Increased consolidation among hospitals and physicians is a key cost inflator impacting contract negotiations.

Read the full article here

Featured Interview Series

Behind the Deal: PGP Advises on Women’s Health Transaction with Webster Backed Nova Women’s Health

Physician Growth Partners (PGP), a sell-side healthcare investment banking firm dedicated to representing independent physician practices in transactions with private equity, announced it advised on a new Women’s Health platform transaction.

Webster Equity Partners recently formed Nova Women's Health Partners through its simultaneous acquisition and merger of WomanCare and Women’s HealthFirst alongside Georgia-based Midtown OB/ GYN

Women’s HealthFirst is an OB/GYN practice with five locations in Illinois. There are 10 physicians on staff. WomanCare is a 17-physician OB/GYN practice that is based in four locations in Illinois.

Founded in 2003, Webster Equity Partners is a private

equity firm that invests in the branded consumer and healthcare services industries and provides equity financing, expertise and a broad contact network for management buyouts and growth capital.

We spoke with Ezra Simons, Co-Founder & Partner at PGP, who was able to provide additional information regarding the deal.

Q: How did PGP get involved in this transaction? How long has this transaction been in the works for?

A: We had been working on it for about 18 months. It was more complicated bringing two groups together and finding the right partner who understood the why / what / how aspects of the partnership. Like most of our transactions, we were referred by a former client.

Q: Since Webster is merging the two companies to start a new platform, what made them stand out as a potential merger?

A: Webster’s women’s health group, Nova, got started in October with a group in the southeast. Our groups in Chicago were founding groups alongside the southeast group. Webster has a strong track record working with doctors to build platforms that provide value to the communities, payors, providers and patients. That was attractive to our clients in Chicago who feel like they can deliver a stronger value proposition to the market, together. At the same time, Webster understood the importance of aligning with the junior providers in both groups as well as the administrative teams which was very important to make sure they were considered in the partnership.

Q: How did this transaction align with Webster’s acquisition strategy?

A: Webster is focused on partnering with great groups of physicians across the career spectrum. They were also focused on partnering with groups that have strong clinical models, excellent reputations and great leadership. The shareholders and physicians in both Chicago practices checked a lot of those boxes.

Q: Were there any specific challenges that arose

• Print/Publication Ads

• Digital Banner Ad Campaigns

• Thought-Leadership Sponsorships

• Lead Generation Options

Download our Media Kit - Book Your Campaign Today!

during the acquisition process? And how were they resolved?

A: The biggest aspect was making sure that the non-shareholders were excited about this and were considered strongly in connection with this opportunity. That took considerable work to ensure they were treated equitably. Several became partners at closing.

Q: According to our data, there were 17 OB/GYN deals announced in 2024 and 26 in 2023. Do you anticipate high or low deal volume in 2025? Why?

A: We expect 2025 to be a strong year. Many private equity-backed businesses (within healthcare and beyond) were finding their footing during 2023/2024 and focusing on driving growth internally, given some of the broader credit hurdles. Most folks expect things to open during 2025. We’re excited to potentially see some of the larger players transact amongst sponsors, across verticals, providing further runway within PPM.

Q: How does this merger fit into trends that you’ve seen in the fertility and OB/GYN M&A markets?

A: We continue to see strong interest in women’s health verticals, as well as a continued interest in fertility as access continues to open there from the payor side. Obviously, there are some question marks about how the incoming administration’s policy might shape some of that, but IVF / fertility seems to be outside of the intended purview to a degree. Webster’s entrance into women’s health will add another relevant option for OB/GYN groups nationally considering whether a partnership makes sense for them. At the end of the day, we want independent groups to have lots of options, whether that means pursuing a partnership or remaining independent. OB is very tough to do well, for a long time, without scale (think of having five people splitting a call pool over 15 years), so we’re excited for more options for those groups to get a level of support.

Q: What range are you currently seeing for valuations and how does that compare to the start of 2024?

A: There is a click down in average valuation

2023-current vs 2023. And there is no question that we are seeing investors being much more selective, structured and conservative when it comes to what fits their “buy box.” However, we still are seeing strong, multiple bids, processes for strong assets.

Behind the Deal: Agenda Health Advises on Clear Path Home Care Sale to Avenues Home Care

Healthcare-focused M&A advisory firm Agenda Health announced that it has facilitated the sale of Clear Path Home Care to Avenues Home Care, a portfolio company of Capital Alignment Partners.

The transaction was announced at the end of 2024. It marks a strategic expansion for Avenues, adding six new locations in Texas and broadening its reach to 14 locations across Texas, Tennessee and Georgia. The LevinPro HC team spoke with Alex Veach, Director of Transaction Services at Agenda Health, about the firm’s role in the deal and the broader trends shaping the home care M&A landscape.

Based in Denton, Texas, Clear Path Home Care is a family owned company dedicated to providing non-medical senior home care services in North Texas. The company was founded in 2013 and specializes in 24-hour care, Alzheimer’s and dementia care, stroke care, companion care, veterans’ care and homemaker services to help with meals, laundry and everyday activities.

Avenues Home Care provides personalized homecare services for adults, seniors and veterans. The company has 14 locations across Texas, Tennessee and Georgia. Avenues Home Care was acquired by Nashville, Tennessee-based private equity firm Capital Alignment Partners in March 2024.

Austin, Texas-based Agenda Health served as the sellside advisor for Clear Path Home Care in the transaction. As part of the engagement, Agenda conducted a competitive market process that generated multiple offers. According to Veach, Capital Alignment Partners emerged as the buyer after presenting an offer that aligned with both the financial and cultural priorities of

the seller.

Veach noted that the acquisition process was smooth, with no significant challenges during the due diligence phase, and that the strong cultural fit between buyer and seller played a key role in ensuring the transaction’s success.

“One thing we feel made this transaction so smooth was the strong culture fit between buyer and seller,” Veach explained. “While value is very important in these transactions, our experience has been that partnering with a buyer that aligns culturally with the seller’s values can be just as important, which is why we run our processes in a way that optimizes for finding owners not just the highest offer, but also the right offer.”

“This transaction represents one of our strongest processes in 2024, both in terms of offer volume and offer strength,” Veach continued. “We see this as yet another indicator of a very strong home care M&A market going into 2025. There is not a better time for home care agency owners to consider an exit.”

The sale of Clear Path Home Care highlights ongoing trends in the non-medical home care sector. Strong buyer interest, driven by demographic shifts and increasing demand for home-based care, continues to propel M&A activity in this space.

The transaction also reflects the growing involvement of private equity in the home care market. Capital Alignment Partners, through its portfolio company Avenues Home Care, exemplifies how private equity firms are leveraging strategic acquisitions to build regional and national platforms.

Private equity activity has been a consistent driver of M&A in the home health and hospice (HH&H) sector. According to data captured in the LevinPro HC database, private equity firms and their portfolio companies accounted for 43% of the 93 total HH&H deals announced in 2024. This marks a slight increase from 2023, when private equity was involved in 39% of the 99 transactions. However, overall deal volume has steadily declined since the record-breaking 159

transactions in 2021, when nearly half of all deals (48%) involved private equity buyers. Despite the slowdown, private equity remains a powerful force in the market, focusing on opportunities to consolidate operators and expand services in response to rising demand for home-based care.

The non-medical home care space, in particular, has emerged as a key area of interest for private equity, thanks to its recurring revenue model, low capital requirements and growing need driven by an aging population.

“Agenda has been very active this year representing owners in transacting both to private equity investors as well as strategic buyers,” Veach said. “All of the owners that we work with have different goals in their transaction process, and we look at different types of buyers as an opportunity for us to present our clients with offers from several different perspectives, which gives them the opportunity to select the partner they feel aligns best with what they’re looking to accomplish.”

For Avenues Home Care, the acquisition is a significant step in its mission to provide veteran-centric home care services. With Clear Path Home Care’s presence in Texas, the acquisition enhances Avenues’ ability to serve seniors, veterans and families across the state. The deal also ensures continuity of care, with Clear Path’s staff remaining in place under the Avenues umbrella.

"Adding Clear Path Home Care's multiple North Texas locations to Avenues is a tremendous step in our mission to support families and veterans seeking reliable, quality care in their communities," said Doug Markham, CEO of Avenues Home Care, in the company’s original deal announcement.

2024 Physician Group Activity...cont. from page 1

The most active buyer was MB2 Dental Solutions, which had 50 transactions. This is a slight decline from 2023 when MB2 Dental Solutions reported 59 acquisitions. In 2024, the company expanded its practice across 22 states and more than 80 physicians.

MB2 Dental Solutions partners with dentists and specialists to provide general dentistry services, orthodontics, cosmetic dentistry and oral surgery services. In November 2024, Warburg Pincus invested $525 million in the company.

The second most active buyer was Heartland Dental, a portfolio company of KKR & Co. Inc. since 2018, with 19 transactions. This is a significant increase from 2023 and 2022 when Heartland Dental announced three and two transactions, respectively.

Dental was the most active subsector, with 243 deals announced throughout 2024, representing a nearly 29% increase from 2023 when 180 dental deals were reported. Additionally, this represents the greatest increase of deal volume amongst the PMG specialties from 2023 to 2024. In addition to MB2 Dental Solutions and Heartland Dental, active buyers in the dental space include Imagen Dental Partners (18 deals), Specialized Dental Partners (16 deals) and Dental365 (12 deals).

Internal medicine was the second most active specialty, with 39 transactions. This represents a 15% decline from 2023, when 46 internal medicine deals were announced. The decrease in deal volume for internal medicine represents the largest drop in reported deals, per specialty, for the PMG space. However, it is on par with activity in 2022, when there were 41 internal medicine transactions.

Complete Health, a portfolio company of the private equity group Pharos Capital Group, was the most active buyer in the internal medicine space, with three transactions. Complete Health expanded its presence in Alabama, Florida and Virginia and by more than 15 physicians.

Other active sectors include eye care (32 deals), oncology practices (23 deals), orthopaedic (20 deals), dermatology (19 deals) and OB/GYN (19 deals).

Private equity investment declined in 2024, but firms nonetheless remained dominant in the PMG market. In total, 59% of PMG transactions were completed by a private equity (including portfolio companies) buyer. This marks a notable decrease from 2023, when private equity represented 63% of the acquirers. Independent physician medical groups account for 150 PMG buyers, virtually on par with the 156 reported in 2023.

Health systems accounted for 7% of PMG acquirers throughout 2024, a 40% increase from 2023. In October, University of Iowa Health Care, an 811-bed public teaching hospital and level 1 trauma center affiliated with the University of Iowa, announced the acquisition of Mission Cancer + Blood, a physicianowned oncology practice. The purchase price was $280 million. This transaction is the largest, by purchase price, announced by a health system in 2024. No other buyer types made a notable contribution to PMG transactions.

Disclosed spending in 2024 in the PMG field totaled $12.8 billion across nine deals. This is a notable increase from disclosed spending in 2023, totaling more than $2.2 billion across seven transactions. The transaction with the largest price tag in 2024 was Cencora, Inc.’s acquisition of Retina Consultants of America (RCA) for $4.6 billion.

Cencora was formerly known as AmerisourceBergen. RCA is a specialty platform created by the merger of Retina Consultants of Houston, Retina Group of Florida, Long Island Vitreoretinal Consultants and Retinal Consultants (Northern California).

While 2024 presented economic uncertainty leading to an M&A decline, it is not all doom and gloom for 2025. Between potential changes that the Trump Administration may bring to healthcare M&A, such as a more “pro-business” agenda and fewer restrictions on private equity investments, the PMG market could see a rebound in activity.

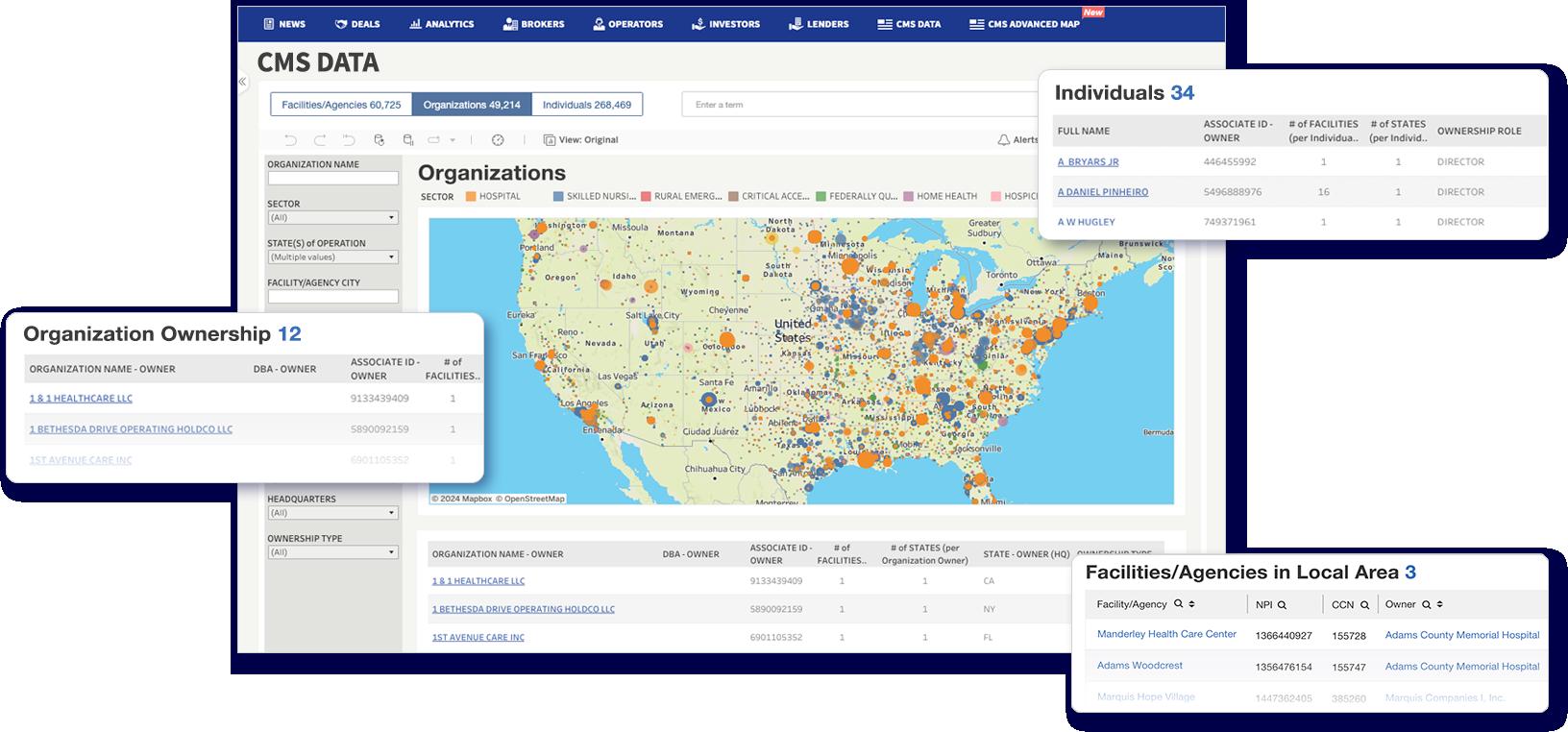

Prospecting, market studies, due diligence and deal comps all in one tool

The most comprehensive seniors care and healthcare M&A database now bolstered by the most up-to-date facility and ownership-level data in the industry.

Improve your deal prospecting by identifying thousands of active organizations and individuals

Get granular deal, facility and ownership data on tens of thousands of healthcare sites nationwide

Find fragmented markets with little corporate penetration and highlight who is selling

See who is growing their Medicare/Medicaid market share in your sector or local market

Gain insights into healthcare sectors and learn which markets are getting the most investor attention

Care and Healthcare M&A Intelligence

Seniors

Top Deals January 2025

ResCare Community Living N/A

Sevita

Behavioral Health Care

1/20/2025

$835,000,000 N/A Boston, MA

In Brief: The acquired assets include BrightSpring Health's community living business, namely ResCare Community Living. The community living business is expected to generate approximately $1.2 billion in revenue and approximately $128 million of Adjusted EBITDA in 2024, according to the original deal press release from January 21, 2025.

Top Deals January 2025

Biotechnology & Pharmaceuticals

Intra-Cellular Therapies NASDAQ: Johnson & Johnson NYSE: JNJ 1/13/2025

$14,600,000,000 Bedminster, NJ ITCI New Brunswick, NJ

In Brief: Intra-Cellular Therapies is a biopharmaceutical company focused on the development and commercialization of therapeutics for central nervous system disorders. According to its most recent annual report, Intra-Cellular Therapies had revenues of $462 million during fiscal year (FY) 2023, and EBITDA was reported as a loss of nearly $158.9 million during FY 2023.

IDRx Private GSK Plc NYSE: GSK 1/13/2025

Cambridge, MA Brentford, United Kingdom

In Brief: Headquartered in Cambridge, Massachusetts, IDRx is a clinical-stage biopharmaceutical company dedicated to transforming cancer care with precision therapies. Founded in 2021, IDRx's leadership team has collectively been involved in the discovery, development and commercialization of more than 10 approved drugs.

Top Deals January 2025

Transcarent

Seattle, WA ACCD Denver, CO

In Brief: Accolade provides personalized healthcare services, including virtual primary care, mental health support, expert medical opinions and care navigation. It partners with employers, health plans and consumers to offer solutions aimed at improving healthcare outcomes, reducing costs and simplifying access to care.

Top Deals January 2025

Hospitals

In Brief: Regional Medical Center is a 258-bed facility with a Level II trauma center. It holds a Joint Commission advanced certification as a Comprehensive Stroke Center. Regional also hosts inpatient and outpatient services, including advanced orthopedics, cardiovascular care and neurosciences.

Top Deals January 2025 Other Services

McKinney, TX New York, NY

In Brief: Soleo Health is a McKinney, Texas-based provider of specialty pharmacy services and infusion therapy administered in the home or at alternate sites of care. Soleo operates more than 40 infusion centers across the United States, with 514 employees. The buyers are CourtSquare Capital Partners and WindRose Health Investors, LLC.

Deal

Volume, January 2025 vs. December 2024 and January 2024

Announced Deal Value,

January 2025 vs.

Source: LevinPro HC, February 2025