Published by Levin Associates 29th Edition | 2024 The Senior Care Acquisition Report ABSTRACTMISSING50+Pages HTTPS://LEVINASSOCIATES.COM/SENIORCARE-ACQUISITION-REPORT-2024

Irving Levin Associates Publications and Services

Newsletters

The SeniorCare Investor

Dealmaker’s Forum

HealthCareMandA.com

Health Care Deal News

Annuals

Health Care Services Acquisition Report

The Senior Care Acquisition Report

Quarterlies

The Health Care M&A Report

Online Database of M&A Transaction and Contact Details

LevinPro LTC

LevinPro HC (Access free with certain paid subscriptions.)

The Senior Care Acquisition Report

29th Edition, 2024

ISSN 1089-1412

ISBN 978-1-970078-45-9

Published by:

Irving Levin Associates, LLC 51 Locust Ave. Suite 202 New Canaan, CT 06840 Phone 203-846-6800/Fax 203-846-8300 www.levinassociates.com

ABSTRACTMISSING50+Pages

Managing Editor: Benjamin Swett

Editor-at-Large: Stephen M. Monroe

Research Analyst: Stephanie Mallozzi

Advertising: Cristina Blazek-Hearty

HTTPS://LEVINASSOCIATES.COM/SENIORCARE-ACQUISITION-REPORT-2024

© 2024 Irving Levin Associates, LLC Allrightsreserved.Reproductionorquotationinwholeorpartwithout permissionisforbidden.

FirstClassPostageispaidatNorwalk,CT

This publication is not a complete analysis of every material fact regarding any company, industry or security. Opinions expressed are subject to change without notice. Statements of fact have been obtained from sources considered reliable, but no representation is made as to their completeness or accuracy. POSTMASTER: Send address changes to The Senior Care Acquisition Report, 51 Locust Ave. Suite 202 New Canaan, CT 06840.

Table of Contents Preface v Introduction 1 Overview of the Acquisition Market 1 Publicly Announced Seniors Housing & Care Transactions (2003 – 2023) 1 Dollar Value of Publicly Announced Seniors Housing & Care Transactions (2003 – 2023) 2 Average Price per Unit for AL/IL Communities (2003 – 2023) 3 Average Price per Bed for Skilled Nursing Facilities (2003 – 2023) 4 The Skilled Nursing M&A Market 5 Average and Median Price per Bed: Skilled Nursing Facilities (2013 – 2023) 5 Price per Bed by Quartile (2022 – 2023) 6 Ranges in Price per Bed (SNF) (2019 – 2023) 6 Distribution of Skilled Nursing Facility Prices (2022 – 2023) 7 Average Price per Bed: Stabilized vs Non-Stabilized SNFs (2021 – 2023) 8 Average Price per Bed by Age of Skilled Nursing Facility (2021 – 2023) 9 Average Price per Bed by Region (2022 – 2023) 9 Statistics on Skilled Nursing Facilities Sold 10 Average Size of Nursing Facilities Sold (2013 – 2023) 10 Average Price Paid per Bed by Size of Facilities (2022 – 2023) 10 Average and Median Price per Square Foot (SNF) (2015 – 2023) 11 Skilled Nursing Valuation Statistics 12 Trend in Skilled Nursing Facility Cap Rates (2003 – 2023) 12 Weighted Average Cap Rate by Beds (2003 – 2023) 13 SNF Cap Rate Compared with the 10-Year Treasury Rate (2008 – 2023) 14 Average and Median Gross Income Multiples (SNF) (2013 – 2023) 15 Operating Statistics on Skilled Nursing Facilities Sold 15 Average Occupancy (SNF) (2011 – 2023) 16 Average and Median Operating Margins (SNF) (2013 – 2023) 17 Average Operating Margin by Age of Skilled Nursing Facility (2020 – 2023) 17 Relationship between Average Price per Bed and Operating Margin (2022 – 2023) 18 Average and Median NOI per Bed (SNF) (2019 – 2023) 19 State by State Pricing Statistics (2019 – 2023) 20 The Seniors Housing M&A Market 21 Average and Median Price per Unit AL/IL Combined (2013 – 2023) 21 Price per Unit by Quartile: AL/IL Combined (2022 – 2023) 22 Ranges in Price per Unit (2013 – 2023) 22 Average and Median Price per Unit: Assisted Living Properties (2013 – 2023) 23 Price per Unit by Quartile: Assisted Living (2022 – 2023) 24 Average Price per Unit: Stabilized versus Non-Stabilized AL Communities (2019 – 2023) 25 Average Price per Unit: AL Single Facility Sales vs AL Portfolios (2022 – 2023) 26 Average Price per Unit: AL versus AL/MC (2019 – 2023) 27 Average Price per Unit: “A” vs “B” vs “C” Assisted Living Communities Sold (2021 – 2023) 28 Operating/Valuation Statistics: “A” vs “B” vs “C” AL Properties Sold (2023) 28 Average and Median Price per Unit: Independent Living (2013 – 2023) 29 Price per Unit by Quartile: Independent Living (2022– 2023) 30 Average Price per Unit: “A” vs “B” and “C” Independent Living Properties (2022 – 2023) 31 Average Price per Unit: AL vs IL (2019 – 2023) 32 Statistics on Seniors Housing Communities Sold 32 Average Price per Unit by Property Age (AL/IL) (2022 – 2023) 33 Average Size of Properties Sold (2013 – 2023) 33 Average Price Paid per Unit by Size of Property (2022 – 2023) 34 The Senior Care Acquisition Report, 29th Edition, 2024 iii

HTTPS://LEVINASSOCIATES.COM/SENIORCARE-ACQUISITION-REPORT-2024

ABSTRACTMISSING50+Pages

Average and Median Price per Square Foot (AL/IL) (2013 – 2023) 34 Average Price per Unit by Region (2022 – 2023) 35 Seniors Housing Valuation Statistics 36 Trend in AL/IL Cap Rates (2003 – 2023) 36 Trend in AL/IL Unit-Weighted Cap Rates (2003 – 2023) 37 Distribution of Seniors Housing Cap Rates (2022 – 2023) 38 Relationship between Average Price per Unit and Cap Rate (AL/IL) (2022 – 2023) 38 Average Cap Rate by Size of Community (AL/IL) (2019 – 2023) 39 Average Cap Rate by Age of Community (AL/IL) (2019 – 2023) 39 Trend in Cap Rates: AL (2013 – 2023) 39 Trend in Cap Rates: IL (2013 – 2023) 40 AL/IL Cap Rate Compared with the 10-Year Treasury Rate (2008 – 2023) 41 Average GIMs: IL vs AL (2019 – 2023) 41 Operating Statistics on Seniors Housing Communities Sold 42 Average and Median Operating Margins (AL/IL) (2013 – 2023) 42 Average Operating Margins: AL vs IL (2013 – 2023) 43 Average and Median Operating Margin by Age of Community (2019 – 2023) 43 Relationship between Average Price per Unit and Operating Margin (2023) 44 Average and Median NOI per Unit (AL/IL) (2013 – 2023) 45 Average NOI/Unit by Age of Community (2019 – 2023) 45 Average NOI per Unit: AL vs IL (2005 – 2023) 46 Average and Median Occupancy (AL/IL) (2013 – 2023) 46 State by State Pricing Statistics (2019 – 2023) 47 The CCRC Market 48 Average Price per Unit: CCRCs (2006 – 2023) 49 Average Cap Rate: CCRCs (2006 – 2023) 50 Average Operating Margin: CCRCs (2006 – 2023) 51 Average NOI Per Unit: CCRCs (2006 – 2023) 51 Map of Regions 53 Definitions 54 Appendix 56 The Senior Care Acquisition Report, 29th Edition, 2024 iv

MISSING50+Pages HTTPS://LEVINASSOCIATES.COM/SENIORCARE-ACQUISITION-REPORT-2024

ABSTRACT

Preface

For 29 years, Irving Levin Associates has been publishing the results of our annual study of trends in the skilled nursing and seniors housing acquisition markets. Our analysis of trends for key statistics such as price per bed or unit, cap rates, income multiples and other valuation metrics goes back to the early 2000s.

The Report reviews the skilled nursing and seniors housing acquisition markets with more than 60 graphs and charts detailing the acquisition market over the past several years, but with a specific focus on 2023. Any charts without data labels in this Report have their full data reported in the Appendix section.

There were 81 primarily skilled nursing transactions and 270 primarily seniors housing transactions in 2023 used to calculate the various statistics in this Report. It should be noted that all the transactions used in the statistical part of this Report include the purchase of the real estate and the operations of the facility (see Definitions). There are always a certain number of the publicly announced senior care transactions that are not used in the statistical compilations in the Report for a variety of reasons. These would include lack of a disclosed price, the presence of leases or management contracts, sale/leaseback financings with the same operator or other transactions that were not considered to be arm’s length. However, for some of the publicly announced transactions without financial data, we have been able to obtain the confidential financial data to be used just for the statistics. In addition, every year there are a certain number of transactions used in compiling the statistics for this Report that are from “private” or confidential deals gathered from industry contacts.

ABSTRACTMISSING50+Pages

In this Report, the 2023 statistics are based on the sale of more than 207 skilled nursing facilities with approximately 22,360 beds with a total value of $2.2 billion, and more than 477 seniors housing communities with approximately 41,200 units at a total value of $6.2 billion. In the aggregate, this Report includes statistics on the sale of more than 1,515 skilled nursing facilities with 175,900 beds and a value of $14.2 billion, and more than 2,400 seniors housing communities, 221,150 units and a value of $37.8 billion in the five-year period 2019 to 2023.

We would like to thank all our colleagues in the industry for their help in making this Report the most comprehensive study available on the skilled nursing and seniors housing acquisition market.

Benjamin Swett

Stephen M. Monroe Managing Editor Editor-at-Large

CARE-ACQUISITION-REPORT-2024

The Senior Care Acquisition Report, 29th Edition, 2024 v

HTTPS://LEVINASSOCIATES.COM/SENIOR-

INTRODUCTION Overview of the Acquisition Market

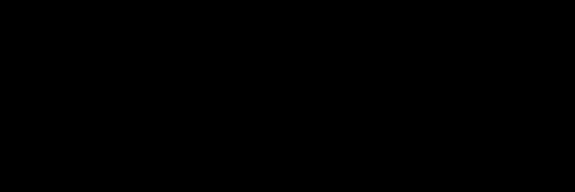

The seniors housing and care industry has suffered a long and uneven operational recovery from the pandemic, with occupancy gains usually overshadowed by soaring expenses and uneven profits. These issues, combined with the financial havoc that fast-rising interest rates wreaked on the economy and the debt markets, could have led to a collapse in the M&A market for senior care properties. Yet, dealmaking reached its second-highest annual total ever in 2023, with 501 publicly announced transactions. That is 10% lower than 2022’s volume of 556 deals but still stands well above previous active dealmaking years like 2021 (456 transactions) and 2019 (459). The comparison with pre-pandemic 2019 is starker, as the debt markets were far more open at the time and the operating environment, although weakened by years of overdevelopment, was in a farstronger position than post-pandemic. So, what were the market dynamics that led to the secondhighest total of transactions ever recorded?

Front and center were interest rates and the ensuing ripple effects through the economy and financial institutions. The lending environment seemed to fundamentally shift in the third quarter of 2022 when interest rates were rising at such a pace that buyers and lenders started to renegotiate or terminate deals. Banks were already pulling back on lending before the twin collapses of Silicon Valley Bank and Signature Bank in early 2023 spurred regulatory changes that dried up liquidity and helped raise the cost of borrowing in general. Buyers that still could obtain debt but could not support the debt payments, on the purchase prices previously appraised, demanded discounts. Thus, it was a buyer’s market in 2023 and values plummeted.

Depressed values kept many potential sellers on the sidelines, especially for those with stable properties, positive cash flow and, of course, the ability to wait. There were also owners hoping for another year of resident rate increases to appear in the trailing financials and boost their property’s chances of sale, and purchase price. After all, why sell now at a lower price when you do not have to? On the other hand, those with funds reaching their investment horizons, debt that had come due with no extension options, or who had had enough of owning and operating after three incredibly difficult years, made for some highly motivated sellers and helped further depress values for the properties that actually sold in 2023. However, enough sellers (and buyers) helped spur M&A activity to near-record levels.

Source: The Senior Care Acquisition Report, 2024 103 85 128 146 127 96 89 117 172 189 229 308 372 346 308 436 459 363 456 556 501 0 100 200 300 400 500 600 Publicly Announced Seniors Housing & Care Acquisitions (2003 - 2023) The Senior Care Acquisition Report, 29th Edition, 2024 1 ABSTRACTMISSING50+Pages HTTPS://LEVINASSOCIATES.COM/SENIORCARE-ACQUISITION-REPORT-2024

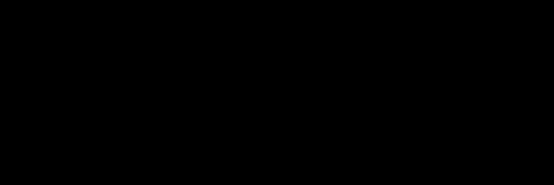

But buyers were also not interested in making large portfolio purchases, in general, because of the difficulty in financing the acquisitions and in integrating so many properties (usually with operational difficulties) into their management portfolios. Due to that lack of demand, few portfolios were marketed, and the vast majority of senior care transactions featured one or two properties each. Smaller deals and lower values combined for the lowest dollar volume spent on seniors housing and care deals since 2009, during the depths of the Great Financial Crisis This is based on publicly disclosed prices, but there were few behind-the-scenes portfolio deals that would have substantially raised the 2023 total. In the end, dollar volume dropped to $7.6 billion, or by 47% year over year, showing the real impact of higher capital costs on the M&A market.

Historically, dollar volume has not been the most accurate indicator of market health or activity, as one or two multi-billion-dollar acquisitions can heavily skew this figure. However, it can be a more accurate sign of an unhealthy market, as was the case in 2020 and in 2023, but for different reasons.

Looking closer at the 2023 deals, three of the top-four deals by purchase price were foreign, including one in Japan (Nippon Life Insurance Co.’s $1.41 billion acquisition of Nichii Holdings, including its significant nursing home assets) and two in Canada, all accounting for 31% of the sector’s total 2023 spend. By comparison, foreign deals took two of the top-five spots in 2022, by price, but those two only represented 8% of the year’s total dollar volume. So, extracting those three foreign deals shows a steeper decline in dollar volume between 2022 and 2023.

Dollar Value of Publicly Announced Seniors Housing & Care Transactions (2003 - 2023)

ABSTRACTMISSING50+Pages HTTPS://LEVINASSOCIATES.COM/SENIORCARE-ACQUISITION-REPORT-2024

The largest deal in the United States, which was publicly announced, was the sale of 12 seniors housing communities in seven states to an undisclosed institutional investor. Located in Virginia, Massachusetts, Missouri, North Carolina, New Jersey, South Carolina and Texas, the portfolio consisted of 1,809 total units, with independent living, assisted living and memory care services. Both parties involved were likely large, institutional entities, but the companies were not disclosed. The estimated price came to $500 million, or $277,000 per unit, and Newmark handled the transaction.

The deal, which was announced in December, was the first of several portfolios that sold before the end of the year. Another was the $225 million, or $241,700 per unit, acquisition of seven seniors housing communities in Michigan, Pennsylvania and Virginia. They consisted of 931 units, with independent living, assisted living and memory care services, and experienced positive leasing and

Source: The Senior Care Acquisition Report, 2024

2.5 3.4 6.9 22.6 16.6 1.8 4.1 11.9 16.3 9.2 11.65 25.6 14.4 14.5 15.9 13.6 16.95 7.9 19.1 14.4 7.6 0 5 10 15 20 25 30 Dollar Value (in $ billions)

The Senior Care Acquisition Report, 29th Edition, 2024 2

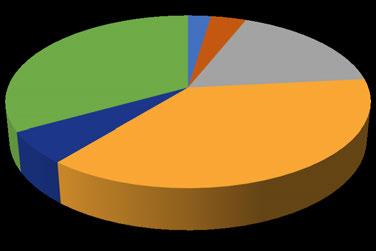

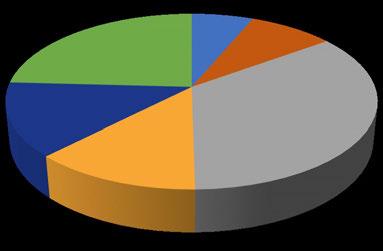

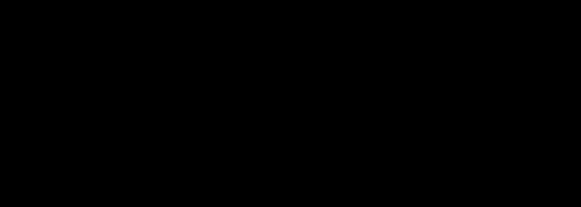

Looking at the distribution of prices per bed, the top end of the market, involving sales of facilities valued at $125,000 per bed or above, shrank from 33% of facilities sold in 2022 to 24% in 2023. These facilities tend to be located in attractive markets, are newly built and attract mostly Medicare and private pay patients. Those patients also tend to require higher levels of care, which are reimbursed at higher rates, especially since implementation of the Patient Driven Payment Model, or PDPM. So, they can be very profitable, justifying high per-bed prices.

However, the next category, facilities valued between $100,000 and $124,999 per bed, jumped in proportion to 13% in 2023 from just 6% in 2022. This makes the market for facilities valued above $100,000 per bed close to the same size, year over year, going from 39% of facilities sold in 2022 to 37% in 2023. Clearly, only the highest priced deals dropped out of the market in 2023, and the market retained some strength.

Facilities priced between $70,000 and $99,999 per bed fell in proportion year over year from 38% in 2022 (the plurality of facilities sold in that year) to 13% in 2023. Instead, the plurality of facilities sold for between $50,000 and $69,999 per bed in 2023 (35%), and about 50% of facilities sold for under $69,999 per bed in 2023, as opposed to 23% of facilities selling for under that figure in 2022. This is where the low end of the market made its impact, with sales of more struggling facilities factoring into the average price per bed in 2023. But it appears that facilities of all types fell in value, year over year.

Distribution of Skilled Nursing Facility Prices, 2022 vs 2023

2022

Source: The Senior Care Acquisition Report, 2024

ABSTRACTMISSING50+Pages HTTPS://LEVINASSOCIATES.COM/SENIORCARE-ACQUISITION-REPORT-2024

2023

Prices fell for stabilized (with occupancy at 85% or above) and non-stabilized facilities, alike. For stabilized SNFs, the fall was dramatic from $234,000 per bed in 2022 to $149,200 per bed in 2023, but that is perhaps more of a reflection of the frenzy that drove 2022 pricing. There was still a premium for stabilized facilities in 2023, with non-stabilized SNFs selling for $105,600 per bed, or down 3% from $109,200 per bed in 2022. However, both averages surpass the average price per bed for the sector, which can be explained by the dozens of facilities without reported occupancy factoring into the overall average price per bed but not into these separated averages. Most of those facilities with undisclosed occupancies feature struggling facilities that usually sold for less than $100,000 per bed, helping to explain the anomaly.

Because census is not usually the best measure of a SNF’s success, since an all-Medicare facility can operate quite profitability at 70% or 80% occupancy, we have also studied the average prices

Under $30,000 6% $30,000$49,999 9% $50,000$69,999 35% $70,000$99,999 13% $100,000 -$124,999 13% $125,000 & Over 24%

Under $30,000 2% $30,000$49,999 4% $50,000$69,999 17% $70,000$99,999 38% $100,000 -$124,999 6% $125,000 & Over 33%

The Senior Care Acquisition Report, 29th Edition, 2024 7

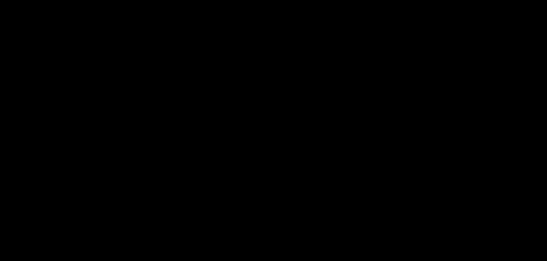

Average Occupancy (SNF) (2011 - 2023)

Source: The Senior Care Acquisition Report, 2024

Already before the pandemic, skilled nursing facilities were facing the twin forces of shortening lengths of stay and dropping average occupancy. Some SNFs can still operate profitably despite this, but that is usually only with a high Medicare and private pay census. For older facilities, which rely on Medicaid to both cover overhead expenses and still make a profit, these trends are more concerning and more detrimental to their value.

ABSTRACTMISSING50+Pages

Unsurprisingly, the average occupancy for facilities sold collapsed in 2020 and 2021 to an average of 73.5% and 69.8%, respectively The median also dropped to 71.8% in 2021, and to think that half of the skilled nursing facilities that sold in 2021 (and reported their occupancies to us) were 71.8% occupied or less was alarming, to say the least. SNF providers rebounded in 2022 and 2023, rising to 76.1% and 75.6%, respectively, based on facilities sold. However, national occupancy could still improve significantly.

The SNF market is a localized one, with referral networks carrying more weight than national occupancy averages. And even though no region or locality avoided the ravages of the pandemic, individual health systems and payors have varied with how they dealt with their post-acute patients. The effects were also likely harder on the older, all-Medicaid facilities that need a more robust census than transitional care facilities to both cover overhead costs and hopefully turn a profit. As will be discussed later in the Report, census has become a less important mark of operational success for SNFs. Census mix and rates matter more, but in the end, cash flow has always been key.

HTTPS://LEVINASSOCIATES.COM/SENIORCARE-ACQUISITION-REPORT-2024

77.1% 79.4% 82.5% 84.2% 82.4% 83.4% 78.5% 82.1% 79.7% 73.5% 69.8% 76.1% 75.6% 65% 70% 75% 80% 85% 90% 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

The Senior Care Acquisition Report, 29th Edition, 2024 16

The Seniors Housing M&A Market

Average and Median Price per Unit AL/IL Combined (2013 - 2023)

Source: The Senior Care Acquisition Report, 2024

This section of the Report covers the seniors housing market, which includes both the independent living and the assisted living markets, and any reference to “seniors housing” means a combination of the two property types. At times, for specific statistics, we will separate out those transactions that are primarily assisted living from those sales that are primarily independent living, and these will be so noted. But there are few new independent living developments today that do not have either an assisted living component or a memory care wing, and often both. Plus, some IL communities are contracting out assisted living services through home health agencies, blurring the distinction between assisted and independent living.

ABSTRACTMISSING50+Pages

Many AL sales also include memory care or Alzheimer’s units, and they are considered to be assisted living unless otherwise broken out. Since the turn of the century, assisted living communities have accounted for the majority of sales and of dollar volume in the overall seniors housing market, and 2023 was yet again no exception, with assisted living representing more than four of every five seniors housing properties sold. It did not help that the IL deals grew increasingly unpopular as interest rates surpassed the historic range of IL cap rates, giving buyers little room for error and owners little incentive to sell at higher cap rates.

The average price paid per unit for seniors housing communities continued on a generally upward trajectory for much of the 2010s, peaking at $244,200 in 2019. Since then, with a pandemic and inflation hitting, values have dropped at the same time operating a seniors housing community became a riskier prospect. Buyers priced that risk into their deals, and sales of struggling communities also rose. The exceptionally difficult capital markets environment and rising interest rates led to a collapse in average price per unit to $156,300 in 2023, the lowest level recorded in more than 10 years. Owners of the well-performing, Class-A communities avoided selling (if they could help it) and most sales in 2023 featured distressed or value-add properties being sold by highly motivated owners, either because their fund life was ending, the lender was directing the sale, or they were running out of money.

HTTPS://LEVINASSOCIATES.COM/SENIORCARE-ACQUISITION-REPORT-2024

$164,000 $208,150 $189,900 $206,700 $223,200 $203,500 $244,200 $196,200 $182,300 $211,800 $156,300 $100,000 $120,000 $140,000 $160,000 $180,000 $200,000 $220,000 $240,000 $260,000 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Average Median The Senior Care Acquisition Report, 29th Edition, 2024 21

Seniors Housing Valuation Statistics

In this section, the average cap rate for independent and assisted living sales (seniors housing) is based on those sales that are arm’s length and include both the real estate and the business operations. The net operating income (NOI), which is interchangeable with “cash flow” and “EBITDA” in this Report, is divided by the purchase price to derive the cap rate. And just like for skilled nursing facilities, the NOI is figured after a management fee (usually 6% of revenues for seniors housing) and before any replacement reserves because of the wide range in replacement reserves used in the market, which can be more than $1,000 per unit. The NOI is usually based on the most recent 12month period before the sale or the most recent period annualized, which sometimes mattered more as operations deteriorated throughout the past couple of years. At times when these have not been available, or when it is appropriate, a pro forma NOI has been used, but this is not the norm.

The average seniors housing cap rate has steadily decreased since the turn of the century, with the exception of a sharp rise during the Great Financial Crisis. Since then, as investors poured into an industry they viewed as “recession-resistant,” cap rates continued to fall, first below 9% then below 8%. Persistently low interest rates helped depress the cap rate over the years, as did low cap rates in the multifamily and other commercial real estate industries. Over the years, however, the risk of owning seniors housing properties has not necessarily dropped, especially in the face of overdevelopment issues from 2015 onward.

However, persistent inflation in late-2021 and 2022 led the Fed to raise interest rates at a pace and scale not seen since the early 1980s. The operational risk of owning seniors housing assets, combined with the financial risk of buyers not being able to keep up with their debt service payments (since these properties are almost always acquired with variable-rate debt), shot up. The higher capital costs caused the average cap rate to rise accordingly to the highest level since 2013 to an average of 8.3% in 2023

5.0% 6.0% 7.0% 8.0% 9.0% 10.0% 11.0% Trend in AL/IL Cap Rates (2003 - 2023) Average Cap Rate Median The Senior Care Acquisition Report, 29th Edition, 2024 36 ABSTRACTMISSING50+Pages HTTPS://LEVINASSOCIATES.COM/SENIORCARE-ACQUISITION-REPORT-2024

Source: The Senior Care Acquisition Report, 2024

The CCRC (Continuing Care Retirement Community), or LPC (Life Plan Community), acquisition market is the thinnest of all the major sectors of seniors housing and care. The number of potential buyers is smaller, the pool of lenders and investors is smaller, and the number of communities for sale each year is smaller. Because the market is not very active, we have grouped our statistics in two-year intervals (with the exception of the four-year periods before and after the Great Financial Crisis) to minimize the impact of outlier sales at both extremes.

Luckily, the sector was in decent shape going into 2020, with new development far below levels in the rental seniors housing market. And there was still persistent demand for the continuum of care CCRC model. Also, CCRCs generally have a lower move-in age, putting them a lot closer to attracting the older boomers in the next few years. After a quiet 2020, the CCRC market rebounded in 2021, in terms of activity. Owners learned how to deal with infection control at their campuses, for the most part, and census was able to stabilize across all sectors. A booming housing market also increased the customer base for CCRCs, with many seniors choosing to sell their homes and downsize early. M&A activity dropped by about 40% in 2022 in the CCRC sector, and stayed around that level in 2023.

The sector’s majority of not-for-profit providers tend to be long-term owners unless one of their communities runs into financial problems. Usually, that means at least half of the transactions involve underperforming CCRCs, which is why they are being sold and why the average value for CCRCs regularly falls below that of seniors housing overall on a per-unit basis. And several not-for-profits were subsidizing multi-million-dollar losses at their CCRCs for years since the pandemic, with patience (and cash) running out in 2023. With that, the average price per unit for the most recent period from 2022 and 2023 fell further to $108,700 from $113,800 per unit in 2020 and 2021

ABSTRACTMISSING50+Pages

$140,300 $76,800 $157,800 $117,100 $157,600 $113,800 $108,700 $0 $20,000 $40,000 $60,000 $80,000 $100,000 $120,000 $140,000 $160,000 $180,000 2006-2009 (pre-Recession) 2010-2013 2014-2015 2016-2017 2018-2019 2020-2021 2022-2023 Average Price per Unit: CCRCs The Senior Care Acquisition Report, 29th Edition, 2024 49

Source: The Senior Care Acquisition Report, 2024

HTTPS://LEVINASSOCIATES.COM/SENIOR-

CARE-ACQUISITION-REPORT-2024