A growing demand for 1990s-2000s office buildings? It’s happening in the Twin Cities

By Dan Rafter, Editor

It’s no secret that a growing number of tenants are choosing higher-quality Class-A office space when making leasing decisions today. But a new report from Avison Young shows just how strong this trend has become in the Minneapolis-St. Paul market.

As Avison Young notes in its report, a growing number of tenants have sought higher-quality office spaces since the start of the COVID pandemic.

The theory is that by offering their employees quality office spaces with high-end amenities, companies

will be able to convince these workers to return to the office at least on a part-time basis.

Avison Young said that what it terms new-age office buildings -- office properties built after 2010 -- saw steadily increasing leasing volume each year from 2021 through 2023 in the Minneapolis-St. Paul market.

Last year, though, saw a change. Avison Young reported that office leasing activity fell across all office property types except for those properties built in the next-newest era of the 1990s and 2000s.

Tenants don’t have as many choices today if they are seeking office space in the Twin Cities area built in 2010 or later. Vacancy rates in these properties are lower than they are in older office buildings. Because of this, many are choosing space in the next-newest range of office buildings, those built in the 1990s and early 2000s.

to page 20

Onward Investors’ purchase of Minneapolis’ Ameriprise Financial Center just more evidence of office sector’s struggles

By Dan Rafter, Editor

Onward Investors’ recent purchase of the Ameriprise Financial Center in downtown Minneapolis highlights the challenges that the office sector faces across the country.

Why? The 31-story office tower at 707 2nd Ave. South sold in 2016 for $200 million. Onward Investors purchased the same property for just $6.25 million earlier this year, according to the Minneapolis-St. Paul Business Journal.

And, yes, that does represent a price drop of 97%. This isn’t overly surprising, though. The office market in Minneapolis and across the country has been struggling since the COVID pandemic hit. Today, com-

Photo courtesy of Pixabay

What’s behind last year’s shift? Avison Young pointed to a limited supply of newer buildings.

Office

The Vision To See Banking Differently

Discover Bridgewater Bank.

CONTENTS February 2025

1

1

A growing demand for 1990s-2000s office buildings? It’s happening in the Twin Cities:

It’s no secret that a growing number of tenants are choosing higher-quality Class-A office space when making leasing decisions today.

Onward Investors’ purchase of Minneapolis’ Ameriprise Financial Center just more evidence of office sector’s struggles:

Onward Investors’ recent purchase of the Ameriprise Financial Center in downtown Minneapolis highlights the challenges that the office sector faces across the country.

10 Today’s apartment buildings need more bells and whistles to attract choosier renters:

The owners of multifamily properties have long relied on amenities to set their buildings apart from their competitors.

12

Twin Cities industrial market prepped for an even stronger showing in 2025:

The industrial market in the Minneapolis-St. Paul region experienced a slight decline in vacancy rates during the fourth quarter of 2024, according to the latest report from Avison Young.

4

6

8

Multifamily remains a top investment choice in Minnesota and across the Midwest

As managing director of Midloch, a private real estate investment company with offices in Minneapolis, Milwaukee and Chicago

Get ready for Trump tax cuts: How real estate investors can position themselves for upcoming tax breaks:

As members of the US Congress debate the future of the 2017 Tax Cuts and Jobs Act, real estate investors should prepare for potentially favorable tax changes that could impact their portfolios.

The supply wave: Industrial moves to stabilization: During the COVID-19 pandemic, lockdowns and restrictions

14

Demand finally falling for single-family rentals?

A new survey suggests that it might be:

Is demand for single-family rental homes starting to slow? The latest research from Rentometer suggests that it might be.

16 From retail closures to comebacks:

Recent headlines have been filled with bankruptcy announcements, failed mergers and acquisitions and going out of business sales.

18 Some relief for the office sector? Planned office-to-apartment conversions hit record high: It’s a big jump: The number of apartments set to be converted from office spaces has soared from 23,100 in 2022 to a record-setting 70,700 in 2025, according to the latest research from RentCafe.

President | Publisher Jeff Johnson jeff.johnson@rejournals.com

Managing Editor Dan Rafter drafter@rejournals.com

Senior Vice President Jay Kodytek jay.kodytek@rejournals.com

Art Director | Graphic Designer Alan Davis alan.davis@rejournals.com

Managing Director

National Events & Marketing Kaitlyn LaCroix kaitlyn.lacroix@rejournals.com

Midloch’s Tim Donovan: Multifamily remains a top investment choice in Minnesota and across the Midwest

By Dan Rafter, Editor

As managing director of Midloch, a private real estate investment company with offices in Milwaukee, Chicago and Minnesota, Tim Donovan understands the Midwest’s multifamily market and the demand for it. And his prediction? Investors will continue to sink their dollars into multifamily assets in 2025. Why? Despite the challenge of high interest rates, the multifamily sector remains an attractive one for investors, especially as the demand from tenants for apartment units continues to rise.

We spoke with Donovan about the strength of the multifamily sector and what investors are looking for from this investment type. Here is some of what he had to say.

Are investors still looking at multifamily properties as a home for their investment dollars?

7767 Elm Creek Boulevard, Suite 210 Maple Grove, MN 55369

Tim Donovan: It certainly remains a popular investment choice. I was at the National Multifamily Housing Council conference in Las Vegas last month. The amount of positive buzz around the conference was strong. The industry is adapting to the new reality that interest rates might be higher for a longer period. That has not taken the wind out of the sales of people’s interest in it as an asset class. If anything, investors’ interest in multifamily is picking back up. The industry had been a little turbulent during the last 12 to 24 months. With that comes a lot of opportunity for investors. Investors will see some of the better buying opportunities in multifamily during the next 12 to 24 months. Why is this such a good time to buy multifamily properties?

Donovan: It has been more challenging for investors to find compelling opportunities in this space in the last year than it had been for quite a while. The gap between sellers’ expectations and what buyers were willing to pay has been a very real challenge for the last 18 months. Sellers wanted pricing from six months prior, while buyers wanted pricing that was more indicative of the here-and-now environment. Now that we are in a more stable interest rate environment, the bid-ask spread has come down a bit. Sellers realize that this is the new normal for the time being, so they are being more realistic with their pricing.

There are also quite a few multifamily buildings that buyers purchased in 2021 and 2022 that were financed with too much leverage. People are forced to sell these properties because of the way interest rates have moved. They are forced to sell at prices below what they bought these multifamily properties for a couple of years ago. Prices now

look more like they did in 2017 and 2028 than they did in 2020 and 2021. That is a little alarming for the investors who closed these deals in the early 2020s. But it is also refreshing for investors today to see these opportunities to buy at the pricing of five to six years ago, especially when new construction costs are so high.

I suppose that if the costs of new construction remain elevated, that makes investing in an existing multifamily building even more attractive, right?

Donovan: Construction pricing remains well above what it was five or six years ago. At the same time, the pricing of existing product has been pulled back. If you think that construction pricing isn’t going to fall significantly in the next few years, and that new buildings being built today are more expensive to build, it does feel like a good time to buy existing multifamily properties at a discounted price. Are there any parts of the United States in which you prefer to invest in multifamily properties?

Donovan: It depends. We do tend to favor the Midwest, though. We have our hometown bias, of course, but this is a good time to invest in places that routinely miss the highest highs or the lowest lows. In some of the more popular Sunbelt markets today, markets in which we saw historically strong rent growth, we see that the new supply

to page 15

Midloch owns The Oscar, a 240-unit Class A apartment community in Sheboygan, Wisconsin. (Photo courtesy of Midloch.)

Tim Donovan (Photo courtesy of Midloch.)

Midloch

Get ready for Trump tax cuts: How real estate investors can position themselves for upcoming tax breaks

By Todd Phillips

As members of the US Congress debate the future of the 2017 Tax Cuts and Jobs Act (TCJA), real estate investors should prepare for potentially favorable tax changes that could impact their portfolios. The proposed extensions of TCJA provisions—including 100% bonus depreciation, a reduction in the corporate tax rate to 15%, and the indefinite extension of the Qualified Business Income (QBI) deduction— offer substantial incentives for investors. However, these cuts come with a major hurdle: funding them. With an estimated $4.5 to $5 trillion price tag over the next decade, some form of compromise may be required.

Key Provisions to Watch

100% Bonus Depreciation

One of the most significant tax incentives for real estate investors has been 100% bonus depreciation, which allows the immediate expensing of certain property components. This provision, which started to sunset in 2023, was a game-changer for investors who were ready for it, enabling them to deduct the full cost of certain property improvements in the year of acquisition.

In a speech Wednesday, Trump reiterated its importance to tax bill. If successfully reinstated, this deduction would allow real estate investors to again front-load much their depreciation, significantly reduc-

ing taxable income in the early years of ownership. Cost segregation studies—which break down property components into shorter depreciable lives—will be essential for investors looking to maximize this tax break. Leverage is also very important here. The ratio

of tax savings to dollars invested can drive investment decisions.

Reduction of Corporate Tax Rate to 15%

A key element of Trump’s tax plan—at least what he ran for office on—is cutting the corporate tax rate from 21% to 15%. While critics argue that such a reduction would increase the deficit, proponents believe it would make the U.S. one of the most tax-competitive jurisdictions in the world, encouraging more businesses to domicile in the U.S. and broadening the corporate tax base.

Republican lawmakers point to the success of the 2017 Tax Cuts and Jobs Act (TCJA) in reversing corporate inversions as evidence that another rate cut could further strengthen American competitiveness. Prior to the TCJA, 28 U.S. companies moved their headquarters overseas under the Obama administration to avoid the then-35% corporate tax rate. Once the corporate rate was lowered to 21%, corporate inversions stopped entirely, according to House Ways and Means Committee Chairman Jason Smith (R-MO).

For real estate professionals with an operating business, a lower corporate tax rate could make the C-Corporation a more attractive structure, especially for those reinvesting profits rather than distributing them.

Tax to page 17

Todd Phillips

The supply wave: Industrial moves to stabilization

By Spencer Mason, Matthews Real Estate Investment Services

During the COVID-19 pandemic, lockdowns and restrictions meant that consumers spent significantly more time at home, leading to a surge in the reliance on e-commerce to obtain goods. As a result, e-commerce saw unprecedented growth, with global online sales increasing by 27% in 2020 alone, marking one of the sharpest yearly upticks in history. This growth spurred distributors to rethink their sales strategies, with as many as 84% of them projecting a shift to selling 100% of their product online in the future to align with changing consumer behaviors.

To keep up with this demand, distributors embarked on an aggressive expansion of industrial facilities, including warehouses, fulfillment centers, and distribution hubs, aimed at faster last-mile delivery and reduced supply chain lag. Since 2020, over 1.8 billion square feet of industrial construction was added across the U.S., a record-breaking figure that doubled the average industrial space delivered in the years preceding the pandemic.

However, post-pandemic demand dynamics shifted, and the intense growth in e-commerce moderated as consumers returned to in-person shopping and supply chain issues began to stabilize. This deceleration in demand led to a cooling of industrial real estate activity, resulting in an uptick in vacancy rates. The industrial sector now faces the challenge of filling these vacant spaces that were catalyzed by the pandemic-driven e-commerce boom.

Industrial properties adjust to new supply

The surge in new industrial facilities built during the pandemic caused an oversupply, outpacing demand and keeping vacancy rates high. By year-end 2024, the national industrial vacancy rate reached 6.9%. This metric rose for nine consecutive quarters, with a 30-basis-point average increase month-over-month.

Tampa noted one of the highest vacancy rates nationally as it reached 5.6% at the end of Q3 2024—a level not seen in the market in over eight years. The significant influx of new supply in Tampa outstripped absorption, with a notable -1.2 million square feet in absorption recorded during Q2 2024 alone.

Across the country, San Diego was also heavily impacted by the supply flood. At the end of Q3 2024, the market’s industrial segment noted a 10-year high vacancy rate of 7.6%, driven by a significant uptick in speculative construction and sublet space. Around 2 million square feet remains up for lease due to the new supply additions. Leasing activity for industrial facilities here is not expected to pick back up until the second half of 2025.

Construction costs contribute to industrial environment

To balance the absorption rate of new industrial properties and adjust for softer demand post-pandemic, construction starts have decreased significantly across the U.S. From 2022 to 2023, construction starts fell by more than 40%, with 341.9 million square feet breaking ground in 2023. At the end of Q3 2024,

industrial square footage underway fell 43% from 2023. Only 90 million square feet of industrial space was delivered during Q3 2024, the lowest level of deliveries since Q2 2020, when completions totaled 86.9 million square feet.

Increased construction costs were a contributing factor to the decrease in industrial developments as well. As of March 2024, construction pricing grew 2.6% on a year-over-year basis; at the same time, building costs jumped by 3.8%. The pricing for smaller-sized projects increased the most across the country, growing by 17% over 2023 costs and now averaging $142 per square foot.

The Denver market was strongly affected by the increase in construction costs. It currently stands as one of the most expensive cities to fund medium- and large-sized industrial developments. This pricing pressure, along with the abundance of new supply over the past decade, contributed to Denver’s vacancy rate of 7.6% at the end of Q3 2024, which is among the highest industrial vacancy rates nationally. Together with economic uncertainties, these factors contributed to a significant slowdown of new developments, allowing vacancy rates to normalize in the quarters ahead.

noted more than $2 billion in transactions over the past 12 months. Logistics-focused properties—including warehouse and distribution, plus flex buildings—have been pivotal, with these properties trading at $330 and $400 per square foot, respectively. Following this trend, the largest sale for Los Angeles in 2024 was a warehouse facility that sold for $86 million, or $426 per square foot.

Although developments across the U.S. decelerated compared to the pandemic peak, construction activity is still high compared to historical standards. By the end of 2024, about 195.8 million square feet will be delivered, aligning with the pre-pandemic construction levels seen in 2019.

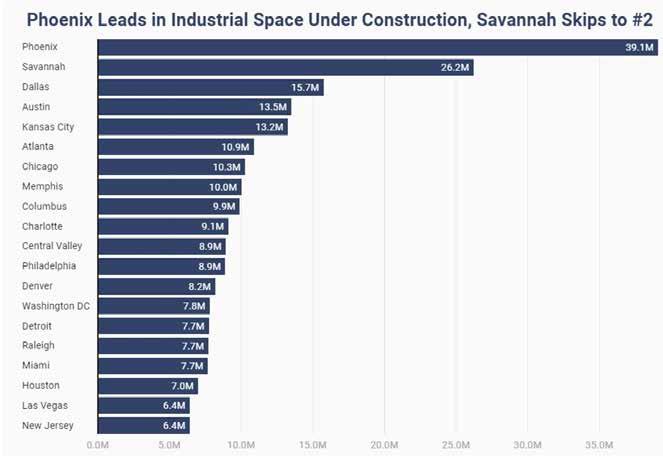

Phoenix is a market that stands out nationally for its active industrial development pipeline. Since 2021, around 90 million square feet of industrial space has been added to the metro, and an additional 36.8 million square feet is currently under construction. The new additions make Phoenix the most active market for industrial activity across the country. Many of the projects cater to larger properties that are greater than 100,000 square feet, contributing to the vacancy rate for industrial facilities in this category reaching 14.8% by Q3 2024.

With that said, smaller properties here have seen the highest level of absorption, with around half of new leases signed over the past year involving properties under 100,000 square feet.

Sales remain stable as new construction is underway

Other West Coast markets have been instrumental in sustaining transaction velocity—particularly in California, which noted increased sales compared to other regions in the country. Los Angeles, specifically, ranked third nationally for sales volume as the market

Source: AZBigMedia

Looking ahead to industrial balance

E-commerce demand is on the rise again, with $288.8 billion in online sales occurring in Q3 2024, a 2.2% uptick from Q2 2024. This marks the seventh consecutive quarter of increased activity, translating to a sustained need for additional square footage for warehousing, distribution centers, and last-mile delivery facilities. The increase in sales activity for e-com-

The power of amenities: Today’s apartment buildings need more bells and whistles to attract choosier renters

By Dan Rafter

The owners of multifamily properties have long relied on amenities to set their buildings apart from their competitors. But as monthly apartment rents continue to rise, renters today expect even more amenities in their common areas.

We interviewed Jonathan Treble, founder and chief executive officer of WithMe, Inc. about this trend. WithMe provides wireless printing and barista-quality coffee machines for multifamily properties and offices.

Here is some of what Treble had to say about the power of common-area amenities and how they can help multifamily owners keep their properties full.

What are some of the more innovative ways you’ve seen multifamily buildings use their common areas to help make thei properties more attractive to tenants?

Jonathan Treble: The best properties aren’t just checking the “amenity” box – they’re designing spac-

es that actually enhance how people live, work and connect.

One of the biggest shifts? Workspaces that actually work. With remote jobs now the norm, the smartest communities aren’t just setting up a few desks and chairs in an empty room and calling it a day. They’re curating true coworking experiences – soundproof booths for deep work, flexible seating for collaboration and seamless on-demand printing (because we all know the struggle). Some spaces even double as event spaces at night, giving residents more reasons to engage.

Then there’s the outdoor experience. A lonely firepit and some scattered chairs won’t cut it anymore. Now, we’re seeing rooftop lounges that feel like boutique hotel terraces, outdoor kitchens built for actual cooking (not just a mediocre grill) and green spaces that bring nature into city living. The best properties turn outdoor areas into an extension of home – a space where people genuinely want to spend time.

But here’s the real game-changer – programming. A great space is nothing without great experiences. Communities that are winning are activating these

spaces with curated events – chef-led cooking classes, yoga under the stars, movie nights, book clubs in cozy lounges. It’s not just about giving residents a place to gather – it’s about giving them a reason to. That’s how you build community. That’s how you turn an apartment into a home.

Multifamily living isn’t just about four walls and a roof. It’s about creating a place where people want to be.

How important are common spaces to renters? I’m sure renters focus first on their individual units, but do common-area amenities and spaces make a big difference when looking for a new place to rent?

It’s true that when people start their apartment search, they’re often focused on the unit itself – the layout, the finishes, maybe the view. That’s the first impression. But what I’ve seen over and over again is that it’s the common spaces that shape the actual living experience and, ultimately, impact whether someone chooses to sign a lease – or renew one.

A great apartment can attract interest, but what sets a community apart is how it feels beyond those four

Photo by R. Swafford, Pexels.

Avison Young report: Twin Cities industrial market prepped for an even stronger showing in 2025

By Dan Rafter, Editor

The industrial market in the Minneapolis-St. Paul region experienced a slight decline in vacancy rates during the fourth quarter of 2024, according to the latest report from Avison Young. The dip in vacancy rates was largely attributed to an increase in leasing activity and positive net absorption, signaling continued strength in the local industrial sector.

The market’s industrial vacancy rate dropped to 5.3% in the fourth quarter, down from a peak of 5.7% in the third quarter of 2024. This marked the first decrease in vacancy rates since the fourth quarter of 2022. According to Avison Young, the Twin Cities’ vacancy rate remains notably lower than the national average of 7.3% and is the second lowest among Midwest markets, trailing only Detroit’s 4.4% vacancy rate.

Avison Young credited a surge in leasing activity at the end of the year for the improved vacancy rates. The market also benefited from positive net absorption, with 1.4 million square feet absorbed in the fourth quarter. The report highlighted strong demand for high-quality industrial space and the completion

of several significant build-to-suit developments as key drivers of this positive trend.

“With much of the construction pipeline comprised of build-to-suit developments, vacancy rates should continue to stabilize as these projects are delivered fully occupied,” the report stated. Avison Young noted that the limited amount of speculative construction is being quickly absorbed due to high demand for modern industrial facilities.

The Minneapolis-St. Paul industrial market also recorded robust sales activity in 2024, reaching $1.35 billion in sales volume, the highest since 2022. This represents a year-over-year increase of over $402 million compared to the $948 million transacted in 2023. According to Avison Young, 2024 marked one of the strongest years for industrial sales volume since 2015, surpassed only by the heightened demand seen in 2021 and 2022 during the post-COVID recovery period.

The 2024 sales volume exceeded the pre-COVID (2015-2019) average of $803.3 million by more than 68%, although it fell slightly short of the 2020-2023 average of over $1.48 billion.

The report also noted that the Minneapolis-St. Paul industrial market continues to outperform many other Midwest markets in terms of vacancy rates and demand for space. “The Twin Cities’ low vacancy rate and strong absorption figures reflect the ongoing strength and resilience of the region’s industrial sector,” said Avison Young.

Looking ahead, Avison Young expects vacancy rates to remain stable as new build-to-suit projects come online fully occupied. The high demand for modern, high-quality industrial space is anticipated to support continued leasing and sales activity in 2025.

DOUBLETREE BY HILTON HOTEL BLOOMINGTON 7800 NORMANDALE BOULEVARD, MINNEAPOLIS, MN

Nominate and Submit Your Projects, People and Company Today! SUBMISSION DEADLINE: MARCH 7, 2025

By Dan Rafter, Editor

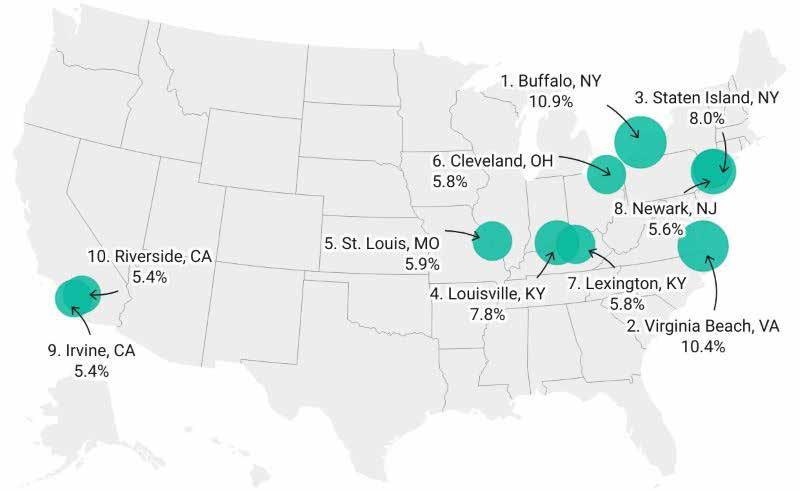

Is demand for single-family rental homes starting to slow? The latest research from Rentometer suggests that it might be.

Rentometer recently released its annual single-family rentals report for 2024, a report that highlights rent prices and trends for three-bedroom single-family homes in 857 cities across the United States.

According to the report, rent growth in these markets slowed in 2024. Although the average monthly rent for a three-bedroom single-family home rose to $2,357, that represented a jump of just 0.8% from the average figure in 2023.

That rent growth is significantly smaller than the year-over-year rent growth of 4% in 2023 and 7.1% in 2022.

Vacancy rates also rose in 2024, with Rentometer saying that this figure hit 6% in the third quarter of last year, the highest in 26 quarters. That helped put downward pressure on monthly rents, Rentometer said.

Not all regions of the country saw sluggish rent growth in the single-family rental market last year. Rentometer reported that monthly rents grew 5.26% on a year-over-year basis in 2024 in the single-family rental market in the Midwest last year.

That increase ranks as the biggest year-over-year rent jump of any region in the United States.

Despite this rent growth, the Midwest was home to some of the more affordable single-family rental homes last year. In Toledo, Ohio, the average monthly rent for single-family homes in 2024 stood at a low $1,217, while this figure stood at $1,308 in Detroit.

The Midwest was home to several cities that saw bigger year-over-year increases in average single-family home rentals, according to Rentometer. This includes Cleveland, where year-over-year average rents for single-family homes rose by 5.8% last year when compared to a year earlier.

In St. Louis, average single-family home monthly rents rose 5.9% on a year-over-year basis last year while this number was an even higher 7.8% in Louisville. In Lexington, single-family home monthly rents jumped by 5.8% in 2024.

there is showing some occupancy weakness. We are not seeing that in the Midwest markets. In the Midwest we see stable occupancy.

We are most excited about Midwest markets with long-term stability. You are still able to get those good value buys in the Midwest. There is also less competition with other investors in the Midwest historically. We are a fan of the slow-and-steady Midwest markets. At times like this, you are glad to have those reliable cash flows.

It look like preferred equity is playing a big role in helping some of these investment deals close today.

Donovan: Yes. We are starting to see deals now in which the buyers can’t get the leverage they historically would have gotten because of the interest rate environment. Private equity helps fill the gap. Traditionally, senior debt would have covered about 70% to 80% of a deal. Now it might only cover 60%. Private equity can fill the gap that this leaves.

We are also seeing deals coming out of construction loans or that were financed with a shorter-term bridge loan. Private equity can help pay the debt down and recapitalize the deal, set it up with more success going forward.

What are you seeing with multifamily investors who must now refinance their existing loans? What challenges do they face now that interest rates are so much higher than they were when they originally took out their loans?

Donovan: We are seeing that lenders are being amicable to working with owners when they are missing a loan covenant here or there. Lenders are doing

everything in their power to work with their borrowers, which is refreshing to see. But that is also keeping deal flow from hitting the market. Lenders are not forcing their hands on making people realize a paper loss in today’s world. Lenders might give you a nine- or 12-month extension to give you time to get your operations in line. Lenders understand the circumstances of today’s market. They are not in the business of owning

real estate. They are giving owners more time to let the market work itself out.

There are some instances where lenders would not be made whole in a market sale. If the deal was to go to market, the lender would only get 70% or 80% of the loan amount back. Lenders don’t want to take a loss. Instead, they’ll roll up their sleeves and let the market work itself out. In that instance, everyone gets to the other side and gets their capital back.

Midloch is an investor in LaSalle Plaza, an office building in Minneapolis owned by Hempel Real Estate (Photo courtesy of Midloch.)

Today’s retail landscape: From closures to comebacks

By Lanie Beck, Senior Director of Content & Marketing Research at Northmarq

Recent headlines have been filled with bankruptcy announcements, failed mergers and acquisitions and going out of business sales. But the future is expected to be brighter across the retail sector as brands across a variety of industries look to expand.

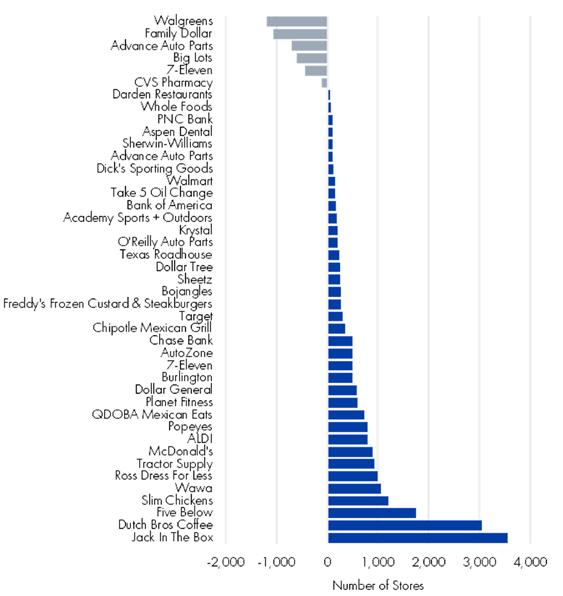

Closed doors lead to opportunities

In the coming months, tenants like Big Lots, Party City, CVS Pharmacy and Walgreens, among others, will shutter locations across the country, leaving significant vacancies in both the net-lease retail and shopping center markets.

While some of the storefronts are likely to remain vacant for the foreseeable future, opportunistic tenants in growth mode will be quick to identify the most attractive locations and backfill those spaces.

Ollie’s Bargain Outlet, Barnes and Noble, Burlington, Michaels and Haverty’s are among the retail brands that have recently acquired leases as other big box stores go out of business. This strategy has allowed tenants to not only capitalize on high-quality, high-traffic sites, but also solves the challenge of expanding in a low-vacancy market.

As shopping center anchors and big-box retailers continue to explore these opportunities, it’s not quite as easy in the single-tenant net-lease market. Net-lease retailers often have strict construction and branding guidelines, requiring build-to-suit solutions. For example, we wouldn’t see Dutch Bros Coffee explore a former Walgreens property as it looks to identify thousands of new potential locations over the coming years.

Instead, it is more likely that shuttered freestanding and junior box locations will be targeted by tenants with more flexibility, such as independent businesses looking to serve their local consumer base from an upgraded location.

Redevelopment or demolition also becomes an option, especially for sites with good ingress/egress

in high-traffic areas. While a vacant CVS Pharmacy won’t solve the physical real estate requirements of a Chick-fil-A, for example, the site itself might justify a tear-down.

2025 and beyond

Over the next several years, thousands of new stores and restaurants are expected to open as retailers look to expand their customer reach.

Quick-service restaurants and convenience stores are among the sectors expanding most aggressively, with Jack In The Box, Slim Chickens, Wawa and Sheetz all targeting massive growth. Discount retailers, like Five Below and Ross Dress For Less, have also announced significant growth plans, as consumers remain cost-conscious. Additionally, retailers that have maintained their footprints in recent years, including Lowe’s and Walmart, have identified now as the time to start growing again.

Will 2025 be a pivotal year for closures and consolidation, or will it instead be a year remembered for substantial growth among established and emerging brands?

Note: Graph below includes a sampling of announced or planned openings and closings beginning in 2025 and may represent long-term plans or estimated counts. Retailers listed twice have announced both significant openings and closings.

Sources: Northmarq Research, various retailer websites, and public news articles; information deemed accurate but not guaranteed, with data gathered in December 2024. Tenants are selected for the Top 100 list based on a combination of factors including but not limited to expansion rate, frequency of investment sale transactions, and brand recognition, and tenants may be added to or removed from future reports; the Top 100 list does not suggest a better or less risky investment.

Expected store openings will exceed anticipated number of closings in coming years

Image by Pexels from Pixabay,

Investors who currently operate through pass-through entities may want to reevaluate their tax structures if this cut becomes law.

Indefinite Extension of the QBI Deduction

The QBI deduction allows pass-through entities, such as LLCs and S-Corps, to deduct up to 20% of their business income. However, this provision is set to expire in 2025 unless extended. Making it permanent would provide long-term tax planning stability for real estate investors who structure their businesses as pass-through entities.

Investors who rely on this deduction should monitor the legislative process closely, as its extension—or lack thereof—could impact whether pass-through structures remain advantageous compared to C-Corporations.

Legislative Hurdles and Fiscal Implications

Extending these tax provisions is expected to add anywhere from $4.5 to $5 trillion to the federal deficit over the next decade. With rising interest rates and growing concerns over government spending, finding offsets will be a key challenge.

While some Republicans argue that economic growth from tax cuts will help cover the cost, others acknowledge the need for a plan to address the fiscal impact. House Budget Committee Chairman Jodey Arrington (R-TX) recently emphasized, “We’re looking for ways to lower the tax burden, but we must do it in a way that encourages economic growth while not adding to our national debt.”

Many Republican lawmakers are hesitant to pass tax extensions without addressing the deficit. While there is strong support for business-friendly tax cuts, some

members of Congress are advocating for spending reductions or alternative revenue sources to offset the cost.

Smith notes that while tax cuts remain a priority, “We have to be mindful of the long-term fiscal impact and ensure that we’re enacting policies that don’t just provide temporary relief but create sustained economic growth.”

While many Republicans want a full extension of the TCJA tax cuts, compromise may be necessary to get the bill through Congress. Some provisions, such as the 15% corporate tax rate and full bonus depreciation, may not pass in their entirety. Instead, negotiators could look at adjustments to the SALT deduction cap, a phased-in corporate tax cut, or a revised depreciation schedule to make the bill more politically viable.

Even Rep. Kevin Brady (R-TX), the architect of the original TCJA, acknowledged that not everything in the 2017 bill will make it through unscathed. “We want to make these tax cuts permanent, but we also have to navigate the realities of Washington,” he said. “The focus will be on delivering as much relief as possible while maintaining the support needed to get it across the finish line.”

Strategic Planning for Real Estate Investors

Get Your Cost Segregation Studies Queued Up If bonus depreciation is reinstated, cost segregation studies will be one of the most effective strategies for real estate investors. These studies break properties into different asset classes with shorter depreciable lives, allowing investors to claim larger deductions upfront. Investors should proactively conduct these studies in preparation for potential changes, ensuring they can take full advantage of immediate expensing.

Targeting Investments with High Depreciation Potential

Certain property types are particularly well-positioned to benefit from tax cuts. Properties such as gas stations, car washes, manufacturing facilities, data centers

…often have substantial short-life assets that qualify for bonus depreciation. Investors should consider adding these property types to their portfolios before any tax changes take effect, allowing them to lock in larger depreciation deductions immediately.

Evaluating Entity Structures

A corporate tax rate reduction could make C-Corporations more attractive for certain investors, particularly those who reinvest profits rather than distributing them. Investors should work with tax advisors to determine whether restructuring their business entity could lower their overall tax liability under new tax laws.

Consider the SALT Deduction Cap and PTE

The $10,000 cap on state and local tax (SALT) deductions remains a major sticking point in tax negotiations. While some Republicans support raising the cap to $20,000, others oppose any changes, arguing that it primarily benefits high-income taxpayers in blue states.

One workaround that many businesses have used is the pass-through entity (PTE) tax, which allows state taxes to be deducted at the entity level, bypassing the SALT cap. Investors in high-tax states should continue to utilize PTE elections where available, as SALT cap changes remain uncertain.

Todd A. Phillips, JD, is a tax attorney, CEO, author and investor. As he says, “I make the tax code work for you, not against you.” Visit his website at SmarterAboutTaxes.com.

Some relief for the office sector? Planned office-toapartment conversions hit record high

By Dan Rafter, Editor

It’s a big jump: The number of apartments set to be converted from office spaces has soared from 23,100 in 2022 to a record-setting 70,700 in 2025, according to the latest research from RentCafe.

RentCafe in its Feb. 10 Market Insights report said that office conversions now make up nearly 42% of the nearly 169,000 apartments planned from future adaptive reuse projects.

Minnesota

This is good news for the office sector. It’s no secret that older, outdated office spaces are struggling to attract tenants. By removing these buildings and con-

WOMEN IN REAL ESTATE summit

Image courtesy of Freepik.

Apartment to page 19

verting them to offices, owners can gain some relief from high vacancy rates.

Conversions can also help with the shortage of apartment units that many cities across the country face.

The problem? Not many office properties are good candidates for conversions to multifamily. Conversions are expensive, and many office buildings don’t come with floor plates that lend themselves to conversion. Others are in locations that don’t make sense for multifamily.

Still, RentCafe reported that office-to-apartment conversions are increasing in popularity, with 2025 set to reach a record-breaking milestone of almost 71,000 multifamily units in the pipeline.

While office properties make up the greatest share of future conversions, other property types are slated for conversion to new uses, too.

RentCafe reported that hotel properties make up 22% of future planned conversions, while factories make up 11% and warehouses 6%.

The number of upcoming office-to-apartment conversions totaled just 23,100 units in 2022 before doubling to 45,200 in 2023. This growth continued in 2024 when the pipeline of future office-to-apartment conversions reached 55,300, RentCafe said.

New York leads the country with an office-to-apartment pipeline of 8,310. In the Midwest, Chicago leads the way with a pipeline of 3,606 apartments set to be converted from offices. And in Texas, Dallas leads the

way with 2,725 office-to-apartment conversions in the pipeline.

Minneapolis has a pipeline of 1,873 planned apartments, while Cincinnati’s stands at 1,753 and Kansas City, Missouri’s, at 1,676. In Cleveland, the pipeline is at 1,619, while it stands at 1,294 in Omaha.

BUILDINGS ARE COOL

from page 1

Avison Young predicts that this trend will continue until developers add newer office properties to the market. When will that happen? Not anytime soon, considering the struggles of the office sector not only in Minneapolis and St. Paul but across the country.

This shortage of newer buildings is good news, though, for what Avison Young terms the next-newest tier of office properties, those built in the 1990s and early 2000s. These properties should continue to see an increase in leasing volume in the coming years, Avison Young said.

What do the office leasing numbers in the Minneapolis-St. Paul market show?

In 2024, tenants leased 1.4 million square feet of office space built in the 1990s and early 2000s in the Twin Cities market. In the same year, tenants only leased 0.2 million square feet in office buildings built in 2010 and later. That’s a significant drop from 2023, when this figure was closer to 2 million square feet.

What’s interesting is that in 2024, tenants leased 1.9 million square feet in office buildings built in the 1970s and 1980s in the Twin Cities market. That amount of

leasing activity beats out all other era of Twin Cities office properties.

But these buildings have seen their office leasing activity drop significantly in recent years. In 2015, tenants leased more than 6 million square feet in office properties of that era in the Twin Cities market.

merce will contribute to absorption metrics moving forward.

Similar to Amazon’s pandemic-era expansion, where the company secured large industrial spaces to meet growing demand, Amazon has recently leased over 1 million square feet across California and Arizona, pushing absorption levels up more than 30% compared to 2023. In line with this growth, Amazon has increased its warehousing and storage workforce, adding 10,700 employees in July 2024. This hiring boost parallels the spike in employment seen when Amazon expanded its footprint during the pandemic, signaling that the e-commerce resurgence is driving both square footage demand and employment in the industrial sector.

Beyond e-commerce, data center demand is also aiding industrial absorption, driven by the growth in artificial intelligence (AI). For example, in June 2024, OpenAI announced that it would rent out a space in Abilene, Texas that would be capable of delivering up to one gigawatt of power by 2026.

Phoenix is set to benefit from similar data center growth, with data centers comprising 18% of the existing industrial market inventory. Stream Data Centers is developing four new facilities in Goodyear, adding 403,000 square feet by August 2025. This expansion is anticipated to boost absorption rates, reducing vacancy in the Phoenix industrial market and strengthening its position as a key data center hub.

Another Texas market that has seen increased industrial absorption is Dallas-Fort Worth. Since 2020, big bomber industrial properties made their way into the metro, and now make up 118 facilities. These sites are over 500,000 square feet, and are favorable because of their long-term leasing capabilities. Google is one tenant that was enticed by these spaces in the metro. Over the last six months, the firm took up more than 2 million square feet in two leases.

Apart from recent trends boosting leasing demand for industrial spaces, construction activity is expected to taper by mid-2025, which should begin to balance leasing activity with the supply wave left over from recent years. New addition activity nationally was noted at 147 million square feet during the second half of 2023 and has continued to fall since then. By the end of 2025, industrial construction is expected to note a 10-year low.

Spencer Mason is a real estate professional at Matthews Real Estate Investment Services specializing in the acquisition and disposition of industrial properties.

Source: Statista

Spencer Mason (Photo courtesy of Matthews.)

Office from page 1

panies are leasing smaller amounts of office space as most continue to embrace the hybrid work model.

While some larger companies are requiring their workers to return to the office five days a week, most mid-size and smaller firms are still allowing them to split time both at home and in the office.

Ameriprise will leave the 960,000-square-foot building and consolidate its downtown Minneapolis offices into a single building at 901 3rd Ave. S, property that it already owns.

In a statement sent by Onward Investors, the company says that it is exploring several options for the office tower. Onward Investors said that it this includes the possibility of converting some or all of the office tower to alternative uses.

This, too, isn’t surprising. Many owners are converting outdated office space to other uses, often multifamily. This isn’t a cure-all for the struggling office market, though. Conversion requires finding the perfect building on the ideal site. Not all office properties are good candidates.

“The purchase of the Ameriprise Financial Center is another demonstration of our desire to be an active participant in the recovery of downtown Minneapolis,” said Jon Lanners, partner at Onward Investors, in a written statement. “We believe that now is a great time to be investing in the city’s future and look forward to engaging a multitude of stakeholders in the coming months as we re-imagine this well-known asset in the Minneapolis skyline.”

Photo courtesy of Onward Investors.

walls. People want to be part of something bigger than just their unit. Thoughtfully designed coworking lounges, inviting outdoor spaces or even something as simple as a well-stocked coffee bar can foster that sense of connection and make a place feel like home. And in competitive markets, those details really matter. A renter might tour two or three places with similar floor plans and rent prices, but if one offers spaces and amenities that genuinely enhance their daily life –like a flexible work environment, a high-quality fitness center or vibrant communal areas – that’s often the deciding factor.

While renters may initially focus on their unit, the reality is that common spaces play a huge role in how people experience where they live. When they add value, make life easier or create opportunities for connection, that’s what turns a building into a true community. And that’s what keeps people around long-term.

How do shared spaces differ in urban vs. suburban locations? Is there a difference in the amenities and spaces that suburban and urban properties tend to offer?

Absolutely. The way shared spaces are designed really depends on the lifestyle of the residents and the space constraints of the location.

In urban communities, where square footage is at a premium, efficiency is key. You see amenities that are compact but high-impact – coworking lounges, rooftop gardens and boutique-style fitness studios. Convenience also plays a huge role. Smart lockers, premium coffee stations and secure bike storage cater to city dwellers who are always on the move. Every square foot needs to work harder in an urban setting.

Suburban communities, on the other hand, have more room to play with – and that changes everything. You’ll often find larger, more family-friendly spaces like playgrounds, pet parks and expansive pools. There’s also a bigger emphasis on outdoor living – walking trails, barbecue areas and community gardens are common because residents value having more room to spread out and connect with family, friends and nature.

So while both urban and suburban properties focus on creating a sense of community, they do it in different ways. City properties lean into efficiency and convenience, while suburban communities take advantage of space to encourage relaxation and gathering. It all comes down to understanding what enhances the lifestyle of the people who live there.

How can the owners of older apartment properties that might not have as many shared spaces compete with newer properties that can offer amenities such as fitness centers, pools and package pick-up rooms?

Owners of older properties actually have a huge opportunity to stand out. It’s not always about having the biggest or newest amenities – it’s about meeting residents where they are and making thoughtful improvements that enhance their daily experience.

One of the best ways to do that is by repurposing underused spaces. A storage room or outdated lounge can be reimagined as a coworking space, while a flexible community room or a dedicated fitness corner with on-demand workouts can add even more value. Even small, intentional upgrades – like adding high-speed Wi-Fi, installing smart locks or offering a

community printer – can go a long way in showing residents that their needs are top of mind.

Beyond physical upgrades, experience matters. Hosting pop-up fitness classes, bringing in food trucks or creating resident appreciation events can build community without major capital investments.

At the end of the day, great property management is a competitive edge. When residents feel heard and supported, it builds loyalty that’s hard to shake – even when a flashier, newer property moves in down the street.

Older communities might not have all the bells and whistles, but with the right strategy, they can offer something just as valuable – a place that feels like home.

What are some of the most important common-area amenities that apartment owners can offer today?

The best common-area amenities are those that reflect modern priorities and improve daily life. It’s less about the flashiest features and more about understanding what residents really need and designing spaces that make their lives easier, better and more connected.

Fitness centers are a great example. A decade ago, they were a luxury. Now, they’re an expectation. But it’s not just about throwing in some treadmills. The best communities are thinking beyond that with

functional training areas, yoga spaces and even virtual fitness classes.

Convenience is huge, too. App-controlled package lockers, self-serve printing stations and smart home tech aren’t just perks – they’re problem solvers. These features save time, reduce hassle and make everyday tasks smoother. And that’s what renters really value.

Social spaces still matter. A great coffee lounge, a well-designed outdoor space or a cozy clubhouse can completely change how people interact in a building. People want a sense of community, whether it’s through casual conversations or organized events. The right common areas make that happen naturally.

For environmentally conscious renters, sustainability-focused amenities like EV charging stations, recycling programs and energy-efficient lighting are also becoming key differentiators.

At the heart of it, the best amenities are the ones that improve residents’ daily lives while demonstrating that the property is forward-thinking and in tune with what matters to them.

Jonathan Treble (Photo courtesy of WithMe Inc.)

E S T B E S T O F O F

B O M A B O M A

G a l a G a l a

BOMA Greater Minneapolis announces the 2025 Best of BOMA & TOBY Award Winners

The 12th Annual Best of BOMA Gala was held on February 13, 2025 to recognize and celebrate professionals and outstanding properties in the greater Minneapolis commercial real estate industry

Best of BOMA Award Recipients

Best of BOMA Award Recipients

Often the public only sees architecture without recognizing the tremendous amount of work and dedication exerted to make buildings energy efficient, comfortable for tenants, and high performing assets for their owners and communities

Lee Davis Lee Davis Target Corporation Executive Management Professional of the Year

Nate Ursel Nate Ursel Future City Commercial Painting Service Partner of the Year

Ashley Lair Ashley Lair Cushman & Wakefield Senior Property Management Professional of the Year

Josh Yates Josh Yates McGough Engineering Professional of the Year

Dave Fox Dave Fox Transwestern Senior Engineering Professional of the Year

Emily Culpepper Emily Culpepper JLL Property Management Professional of the Year

Natalie Bowers Natalie Bowers Hines Emerging Leader of the Year

Monique Slaughter Monique Slaughter Schafer Richardson Chair's Award

TOBY (The Outstanding Building of the Year) Award Recipients

TOBY (The Outstanding Building of the Year) Award Recipients

The TOBY Awards are the most prestigious and comprehensive awards in the commercial real estate industry, honoring the properties that best exemplify superior building quality and excellence in building management

Norman Pointe 1 Norman Pointe 1 Piedmont Office Realty Trust

100,000 - 249,000 Sq Ft Category

Northland Center Northland Center Cushman & Wakefield

Crescent Ridge II Crescent Ridge II Piedmont Office Realty Trust

250,000 - 499,999 Sq Ft Category

a t i o n F r a s e r - M o r r i s E l e c t r i c C o ∘ D a v i s H e a l t h c a r e R e a l E s t a t e ∘ C S M C o r p o r a t i o n

P i e d m o n t O f f i c e R e a l t y T r u s t ∘ G a r d a W o r l d S e c u r i t y ∘ N E L S O N W o r l d w i d e P i e d m o n t O f f i c e R e a l t y T r u s t ∘ G a r d a W o r l d S e c u r i t y ∘ N E L S O N W o r l d w i d e H i n e s M a n a g e m e n t ∘ S c h i n d l e r E l e v a t o r ∘ K r a u s - A n d e r s o n H n e s M a n a g e m e n t ∘ S c h i n d l e r E l e v a t o r ∘ K r a u s - A n d e r s o n

∘ L V C C o m p a n i e s ∘ T h e R M R G r o u p ∘ J L L ∘ L V C C o m p a i e s ∘ T h e R M R G r o u p ∘ J L L