Your propertyis worthit tanya.maich@bayleys.co.nz Ibayleys.co.nz 021247 4274 MACKYS REALESTATELTD,BAYLEYS,LICENSEDUNDERTHEREA ACT2008 Business Growth Award, 2022 Bayleys AuctionClub, 2021/2022 #5SettledSales Nationwide, April2022 PLUS: Housepricesin your suburb —havetheyresistedthedownturn? Monday,September12,2022 PROPERTY REPORT

TutukakaCoast 33RauhomaumauRoad 4 3 3 2 SetSaleDate (unlesssoldprior) 4pm,Thu22Sep2022 84WaltonStreet,Whangarei View byappointment DamienDavis 021387345 damien.davis@bayleys.co.nz SueMaich 021793822 sue.maich@bayleys.co.nz MACKYSREALESTATELTD,BAYLEYS,LICENSEDUNDER THEREAACT2008 Grandstand, waterfront position... Thisbeautifulmodern-dayvillawithseparateguestcottagesitsonsome4904squaremetresofclifftop,waterfrontlandwith vast,sweepinglawnsoverlookingTutukaka’sstunningcoastlineandbeyond.Withdirectaccessto asecludedbeach,the turquoisewatersareaccessibleforyourdailydip.Designedtocapitaliseontheoceanviews,thehousecomprisesgenerous livingspace,largebedroomsandmultipleoutdoorentertainingareas,andiscladwithtimelessweatherboardandstately bullnoseverandahs.Theseparateguestcottageoffersan equallyluxuriousexperienceandinspiringoceanvistasforextended familyorguests.Theproperty’socean-facingaspectensures achoiceofeithersun-filledorshade-protectedpanoramasforall dayenjoyment.Thetimehascomeforthislegacypropertytobepassedontothenext owners, to makenewmemoriesofthis iconicresidence,forgenerationstocome. bayleys.co.nz/1052849 Residential /Commercial /Rural /Property Services 2 OneRoof.co.nz

Ride the tide

Catchthe wave of successwithBayleys’ Waterfront

The28thissue of Bayleys’annual Waterfront portfolio will showcase an aspirational line-up of waterfront property forsale around NewZealand and the Pacific.

Thelastfew yearshaveebbed and flowedjustlikethe tide,with change aprevalent theme

We understand thelureofawaterfront position and appreciate the push-pull emotions in sellingaproperty locatedclose to the sea, harbour,lakeorriver

Bayleys’team of provenwaterfront specialists will castyour waterfront property outtodiscerningand motivated buyers, reel in theinterestand landthe bestresult.

Shore up your future–let us assess the conditions and help younavigate the waters

Groundwork has started on the 2022-2023 edition of Waterfront,sooptimise your opportunities with Bayleys

Call 0800 80 20 40 or see bayleys.co.nz/waterfront

Residential /Commercial /Rural /PropertyServices MACKYS REAL ESTATELIMITED,BAYLEYS, LICENSED UNDER THE REA ACT2008

OneRoof.co.nz 3

EALESTATELTD,BAYLEYS,LICENSEDUNDERTHERE TOP SALESPERSON BAYLEYS WHANGAREI TOP SALESPERSON BAYLEYS WHANGAREI 2018 TOP SALESPERSON BAYLEYS WHANGAREI 2019 TOP SALESPERSON BAYLEYS WHANGAREI 2020 TOP SALESPERSON BAYLEYS WHANGAREI 2021 TOP SALESPERSON BAYLEYS WHANGAREI 2022 MACKYSRE AACT2008 DamienDavis 021387 345 damien.davis@bayleys.co.nz SueMaich 021793 822 sue.maich@bayleys.co.nz 4 OneRoof.co.nz

Theriskiest move afirst homebuyer can make

WelcometothelatestOneRoofProperty ReportandourfirstOneRoofFirstHome BuyerGuide. We wantedtoputour expertisetouseandhelpnervousfirst-homebuyers andpropertynovicesmakesenseofthebuying process.Inthefollowingpageswe’llprovidetipsthat willsupportKiwisontheirpropertyjourneyand set outwhatgrantstheycandrawonwhenmakinga purchase.

Forthosewhocan’ttelltheirdeadlinesalesfrom theirtenders,andareterrifiedbyauctions,thisisthe perfectguide.

We’veaskedNZ’sleadingpropertyexpertsto explainwhythehousingmarkethaschangedinsuch ashortspaceoftimeandwhateffectinflationand interestratesarehavingonhouseprices.

Alsoinsidearethelatestsuburbvaluesforallof NewZealand,providedbyourdatapartner,Valocity, andinsightsandcommentaryfromindependent economist TonyAlexander,propertycommentator AshleyChurchandmortgagebrokerRupertGough. Keepintheknow!

OnaverageeachyearinNewZealandabout 80,000housesareboughtandsoldaroundthe country.Thisisabout4.4%ofthetotalhousing stockandmeansthatforthevastmajorityof peoplethesometimeslargeupsanddownsofhouse pricesareirrelevant.Sowhydowepaysomuchattention towhatishappeninginthehousingmarket?

Mainlyitis because we considermorewealth to be betterthanless.Ifhousepricesarerising,wefeelricher, potentiallymorecleverandpleasedwithourselves, happier aboutourabilitytofundour retirementby downsizingifnecessary,and perhapswelike areason to justifyspendinguplargeon aholidayor newfurniture.

Butfor thoseofus whomadeour firstpurchase beforegovernmentstoldusweneededtobuildwealth for retirementbecausenationalsuperannuationmight notbeaffordableoneday, lifetimewealthaccumulation wasnot reallythemotivation.Ourfocuswason securing ahomeinwhich toraise afamily. We wanted somethingnot too farfromourworkplace,perhapswith someoutsidespaceforplaying,gardening,andhanging the washing.

othersideofthetransaction givingyou the abilityto pickandchoose.

Thatis,yousellwhenmarketsareexceptionally frothyandthereisnotroublefinding abuyerwhosets noconditionsforthe lesserqualityassetyoumight wanttosell.Youbuywhenthereare ahighnumberof sellers,youcanuseeachas abargainingchipagainst theothers,andyoucanpickandchoosethe bestquality assetswith greatestlong-termoryield growth potential.

Mymonthlysurveyof realestateagentsundertaken alongsideREINZhasjust shownthat45%ofinvestors lookingtomake apurchasearemotivatedbyhopesof findinga bargain,up from30%inFebruary.Thesmallest netproportionofagentsareseeinginvestorsstanding backfromthemarketsince Septemberlastyear.

Second,ifyourfocus is whereitshouldbeon securing ahomeratherthanthefirsthousingassetfor yourportfolio,then wherethemarketsits rightnow, potentiallyeventhis month,isasgoodasitisgoingto getfor averylongtime.

Youcan pickupapropertyforasmuch as 15% -20% lessinAucklandthanyouwouldhavepaidlatelast year.InAucklandyouhave80%morehousestochoose fromthanayearago,outsideofAucklandalmost 130%more. Vendorshavelikely reached their pointof capitulationto market reality, witha recentASBsurvey showinga net31%ofpeopleexpectpricestofallfurther (28%inAuckland).Thissurveyis notagoodpredictor ofwhatwillhappen,butitdoes in thisinstanceallow ustosayvendors havealmostcertainlylost faithinany beliefthatwaitingwill yield abetterprice.

Whenwe talkedaboutgettinga footontheproperty ladderit wasinthecontextofstartingsmall,thenlater upgradingtoaccountformorechildrenand ahigher incomefurtherupthe workladder.Thesedaysit seemsmore to refertooutrightbuildingofafinancial wealthportfolio andavoidingmissingoutonwealth accumulationbeingenjoyedby others.

Thisis aproblemfor currentfirst-homebuyersright thismomentbecauseofthestagewhichourhousing cyclehas just reached.Currentlythereisadominant focus onhow muchfurtherprices have tofallafter alreadydeclining10.4%fromtheir nationwidepeak lastNovember.Aucklandpricesare down16%.The commonexpectationisthatpriceswilldeclinemaybe another5%.Afterthatitseemstheprevalentview isthingswillsit flatfor anextendedperiod of time. Actually, Iexpectrises of5% -10%in2023.

Ifyouareafirst-homebuyerand yourfocusison wealthgrowth,thenyouthinkyouareincentivisedto holdoff untilprices havebottomed.Thisis adangerous strategy easilychallengedintwoways.

First,as anewbieintheinvestment fieldyouwon’t yet havelearnt akeylessontheexperiencedinvestors have.Don’ttrytopickthetopsandthebottoms.You’ll feelfarworsewaitingtoolongand missingeitherthan takingadvantageofthelargenumberofpeopleon the

Shouldyoutryandbecleverandhold outforthe final5%of pricedeclines? Considerthis.Haveyouever heardyour parentsorgrandparentsbemoanthefact theyboughttheir firsthousefor$65,000 buthadthey waitedthreemonthscouldhavegot it for$61,750?

So,arefirst-homebuyersinfactstartingtofocuson thenewopportunitytosecureahome?Maybe.My latestsurveyof real estateagentsshowsthatfor the firsttimesinceSeptemberlastyearmoreagents are seeingincreasednumbersoffirst-homebuyersthan decreasednumbers.Lastmonth anet 36%wereseeing fewer. Thingsmaybechangingveryquicklyamongst first-homebuyersandif youhave amisplacedfocus on gettingyour firsthousingassetatthebottomof the pricecycleratherthanyourfirst ownedhome,thenthe clockistickingagainstyou.

MysurveywithREINZshows thatworriesabout highinterestrates,accessto finance,andevenfalling prices,areallabating.Italsoshows numbersattending openhomesrisingforthe firsttimesinceFebruary2021. The housingcyclehasnowentered thepreparatory phaseforturningbackupward.

MOVING INTOA NEW HOUSE? We canmatch youto theperfectsleepwith Northland’slargestrangeof NZmadeSleepyheadbeds Mattressonly From$339 Mattress &Base From $639 AMAZING SAVINGS IN STORE CnrofPorowini Ave&TarewaRd Phone094383550 Open 7Days •Backissues? •Partnerdisturbance? •Hotsleepers? •Bedbugs? Getyourbedroomsorted withBedsRusWhangarei! BedsRus Whangarei MARKET WATCH

•TonyAlexanderisanindependenteconomics commentator.Additionalcommentaryfromhimcanbe foundatwww.tonyalexander.nz

Whyholdingoff untilpriceshavebottomedisthewrongchoiceforKiwis tryingtoget afootonthepropertyladder, writes TONYALEXANDER “RIGHTNOW,POTENTIALLY EVENTHISMONTH,ISAS GOODASITISGOING TO GET FOR AVERYLONGTIME.” From theeditor 6 Coverstory:Beginner’sluck 13 OneRoofFirstHomeBuyerGuide 29 Moneymatters:RupertGough 30 OneRoof-ValocityHousePriceReport 46 Comment:AshleyChurch Inside Designandcover BethWalsh │ Artwork Derek Watts Subeditor Akanisi Taumoepeau Photos FionaGoodall, TedBaghurst,PeterMeecham,GettyImages OneRoof.co.nz 5

BEGINNER’S LUCK

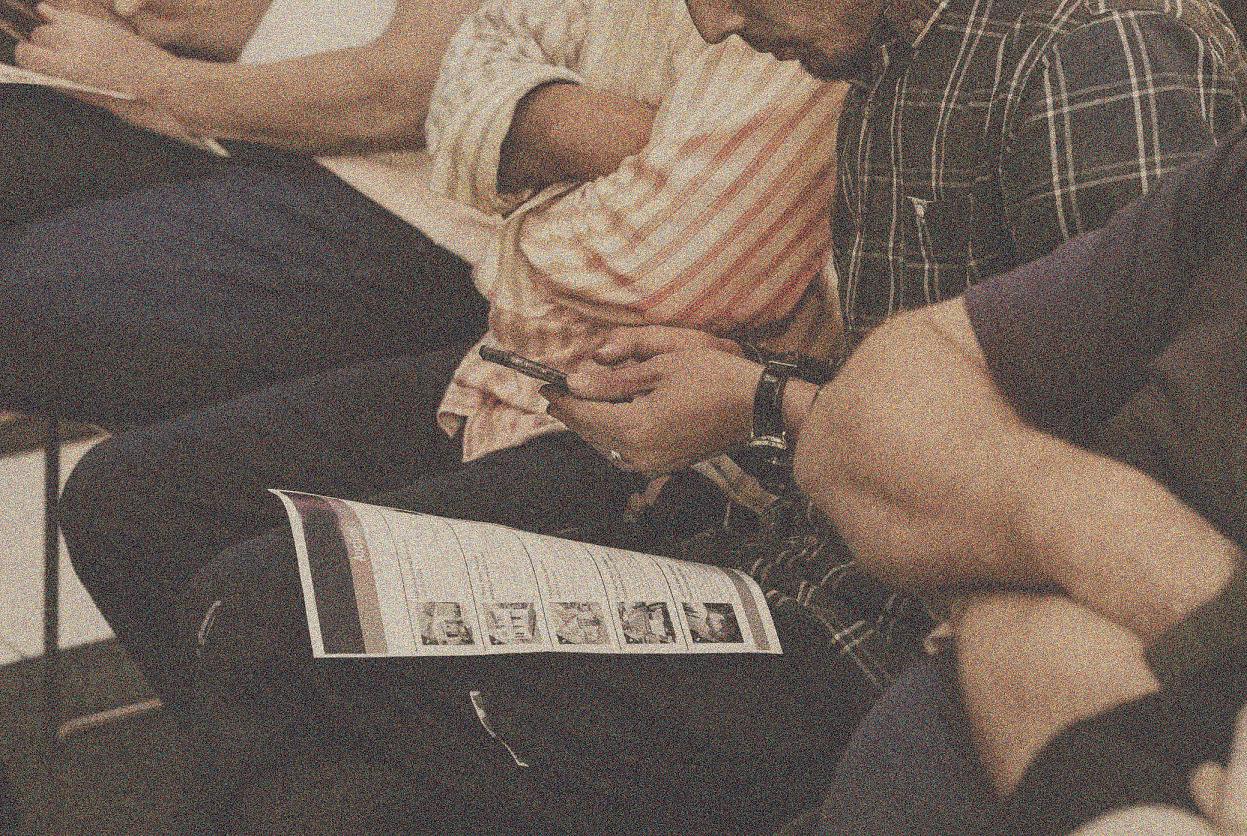

Listings areup, pricesare down andcredit rulesare loosening. Can first home buyers getahead, when so muchhas beenstacked against them? CATHERINE MASTERS checks out the state of the market.

PHOTO /T ED BAGHURST

PHOTO /T ED BAGHURST

? FIRST HOME BUYERS | COVER STORY

6 OneRoof.co.nz

IRST HOME BUYERS areemergingfroman enforcedhouse buying slumber,although the road to home ownership is still noteasy.

Tweaks to Government regulations and home loan schemes, however,have eased the pain abit after adifficult few years, say agentsand commentators.

The relaxation of the stringent CCCFA(Credit Contracts andConsumer FinanceAct) lending rules banks have been applying around home loan applications has seen newbies being able to dip their toes in thewater again -and those rules aredue to befurther loosened, although the next wave of changes won’t take place until March.

Some have said next year is notsoon enough because the CCCFA, which has seen banks examining expenses on the bank statements of would-beborrowers with a magnifying glass, has stopped many firsthome buyers in their tracks.

Awin for first home buyers, though, was this year’s Budget announcement of the removal of first home loan caps nationwide and theincreasing of the price caps for first home grants.

But even with the tweaks and the housing market having turned alittle in the favour of firsthome buyers, meaning they can take abit of time to look around and put in offers with conditions attached instead of trying to buyunconditionally at auction, many say new buyers should not taketoo long to make up their minds.

suburbs and also other parts of the country

“Some of that is not necessarily because of theallure of the place they’ve moved too, it’s morethat they think they need to have ahouse at all costs.”

Patterson says he haspeers who are“not completely comfortable” with wherethey have ended up and some have found themselves stuck in aplace that doesn’t quite fit them and far from their social connections.

If they were entering the market now,with the FOMO having dissipated, they may have decided not to uproot themselves, he says.

CHANGING MINDSET

Patterson also saysfirsthomebuyers shouldworkout their own mortgage repaymentbudget on very high interest rates, regardless of whatever thebanks’ shortterm stress test rates are, because anything canhappen.

He says he bought when rates wereabout 5per cent but was alwayslooking at how he would cope if they were10per cent or more.

”If the unthinkable ever happened and they went to something like 12 or 15 percent would Ihaveaway to get through?”

While high inflation has grabbed headlines with stories of people cutting back on their spending, Patterson says the untold story is whathappenswhen people refix their mortgages.

That’s because they have to find alot moremoney to pay back theloan.

“If you have half amillion dollars of debt,for every percent your mortgagerate goes up,that’s $5000 of additionalinterest.”

But mortgage broker Solomon Kurukuntala,fromthe Loan Market, who works in firsthome buyer areas in Auckland’s south, says he’s noticed changes in the first home buyer psycheoflate.

Forastart,thephonesareringingagain–but Kurukuntalasaysfirsthomebuyersarealsocomingback tothemarketfarmoreeducatedandmuchmoresensible.

The rollercoaster housing market changes direction quicklyand not-if-but-when it flips back to asellers’ market firsthome buyers could again struggle to compete.

Caveats to thegoodnews for firsthome buyers is not just high inflation and risinginterest rates but the fact banks aretesting people’s abilitytorepaymortgages on much higher rates.

INTEREST RATE PRESSURE

RupertGough, CEOandowner of the MortgageLab, says interest rates arethe really big problem in thefirst home buyer market because higher rates meanpeople lose asignificant amount of their buying power

“If they could have afforded $1m last year for a mortgageitwould be about $850,000 this year”

Given house prices have dropped, this is still amore preferable scenario to being approved for $1m but not being able to snareahouse at all amid thebuying frenzy last year,Gough says.

“I think therewas alot of despair around ‘I can’t find a house’ ayear agoand nowit’s back to ‘I can’t affordthe house Iwant’. That’s ahuge change.”

Gough also sayspeople haven’t grasped the magnitude of geographical barriers being removed from the firsthome loan price caps, saying anyone earning less than$150,000 can access the first home loan scheme and withalow deposit.

“That kind of salary gets you about $800,000 of borrowing. That’s anywhereinNew Zealand and $800,000insome parts of New Zealand buysalot –you could get afour-bedroom house in the provinces.”

Economist Benje Patterson, however,urges caution about buying far from home just for the sakeofgetting on the property ladder

“Over recent years we’ve seenalot of people pushed in to places they don’t actually really want to live,both

They aremoreaccepting of the higher interest rates whereas at the beginning of the year they wereshocked at how theyweresoaring: “Now they realise that is the reality and people do understand inflation and everything.”

And while the banks have dialleddown on the CCCFAstringency,Kurukuntala says the strictness over the firsthalf of the year contributed to achange in the cultureofhow first home buyers managetheir finances.

“They realise they can’t keep spending theway they used to beforeand alsohave amortgage.”

People arealso realising thereisnopoint stretching their budgets to the maximumoftheir loan approval, he says.

“In 2020 and 2021 if peoplegot approved for $1m they wanted to buy ahouse for$1.2m but now the trend is if they’reapproved for $1m they arelookingathousesat $900,000.

“Theyknowverywellthewaythingsaregoingwith interestratesandothercostsiftheywanttospend$1mor morethenthatit’sgoingtoputalotofburdenonthem.”

Kurukuntala also thinks firsthome buyers arerelying on brokers morethan banks, and shoppingaround among brokers, to make surethey aregetting theright information andthe best deal.

Developers have become morerealistic, too, he says, which helps because they areselling property for afair price as opposed to wanting morethan what the house was worth in last year’s market

“As abroker Icalled all my firsthome buyers who couldn’t buylast year and told them themarket is changing; nowinvestors areout; now it’s your time to get in and buy.”

MISSED OPPORTUNITIES

James Wilson, head of valuations forOneRoof’sdata partner Valocity,saysfirst homebuyers who think they

“USUALLY, BEFORE YOUREALISE IT’S HAPPENING,YOU’RELOCKED OUT AGAINSODON’T FALL INTOTHE TRAP OF SITTING BACK AND WAITING.“

JAMESWILSON, VALOCITY HEADOFVALUATIONS

OneRoof.co.nz 7

BuiltforWhangarei Builtwithunmatchedvalueandquality SAT17TH &SUN18THSEPTEMBER FROM11AMTO3PM Bethefirsttoview! NEWSHOWHOME OPENING 24TironuiDrive,Maunu,Whangarei JulieScott 021930310 JuliaRussell 0276308849 DiscoverWhangarei’snewfavouritehome.Experience thesuperiorfeaturesandarchitecturaldesignsthathave madeourhomes afavouriteofNewZealandfamilies. (justoffTeHapeRoad) stonewood.co.nz 8 OneRoof.co.nz

can’t affordtobuy ahomeshouldnot be swayed by advice from mum or dad or familybut should talktotheirbank or abroker

“Go and find out the factsbecause you may be surprised, you could be alot closer to being able to buy than you think.”

But he says even though house prices have fallen first home buyers shouldn’t be fooled intoexpecting the market to fall further,saying while that mayhappen the minute the market stops softening it could take off upwards again quickly

“Usually,beforeyou realise it’s happening, you’re locked out again so don’t fall into thetrap of sitting back and waiting.”

TheASB’s chief economist,Nick Tuffley,says he sees two bigpositivesfor first home buyers at the moment one is house prices arelikely to keep falling into the early parts of next year,and the other is the disappearance of the FOMO factor

“They’reable to buy properties alot moreontheir own terms of howthey go about it and any potential conditions they put on the purchase.”

With interest rates the way they aredebt servicing affordability is an issue as first home buyers generally start from lowdepositsbut want to borrow alot.

But Tuffley pointsout therehave always been, and always willbe, cycles in prices and interest rates.

“We’ve gottotake that perspective that we get these periods whereinterest rates maybequitehigh and that can make life abit challenging for ayear or two butthey arenot always goingtoremain at those levels.”

‘Firsttime buyers juststopped looking’

WHANGAREI HAS SEEN abigupswingin firsthomebuyeractivityaftertheywere stoppedintheirtracksbytheCCCFA regulations,saysSteveSharp,branch managerforBarfoot&Thompson.

Sincetheruleswererelaxed,first-home buyershavebeenoutandaboutagainand thefallingmarkethasmadehomesmore affordableforthem,hesays.

Thefirsthomebuyerpricerangeis nowaround$500,000to$800,000in thecityandthereareplentyofoptions inthatrange

ButwhileSharphasnoticedabig upswinginactivity,it’snotfullforceyet

“Theproblemis,onceyoustop somethingpeoplegetoutofthehabitso whentheCCCFAcameinfirsttimebuyers juststoppedlooking

“Togetthemmovingagain,it’snot somethingthathappensinstantly.It’sgoing totakeawhileforustobuildbackuptothe pointwherewewerebefore.”

First-homebuyerlocationsinWhangarei includeTikipunga,Morningside,Otaika, HorahoraandalsoHikurangi,whichisalittle bitoutoftown.

Buyersarelikelytobeabletopickup a1960sweatherboardhomeoraformer statehomeonadecentsection,Sharp says.

FurthernorthinKaitaia,GerardPonsonby, LJHookerfranchiseowner,reportsaquiet firsthomebuyermarket,mainlybecause therearesofewlistings.

Firsthomebuyerstocktheregoesfor under$400,000butpeoplewiththose homesaren’tlistingbecausethere’s nothingforthemtomoveinto,hesays.

“Therearenooptionsforpeopletoshift tosothey’renotputtingitonthemarket We’vegotpeopleonourdatabasewaiting buttheoptionsarenotthere.”

Ponsonbytellsbuyerstobepatient, sayinghe’sneverseenitsoquietbuthe expectsthemarkettopickupinspring

GarySteed,managingdirectorforRay WhiteKaitaia,however,saysthefirsthome buyermarketisstillactive, addingthat thereareopportunitiesforthemandthat theyneverleftthemarket

MostofthehomesinKaitaiaare affordable,hesays,sothereisagood rangeofpropertiesforfirst-homebuyers, andtherearealsoopportunitiesinKaikohe, AhiparaandAwanui,northofKaitaia.

“Thereareopportunitiesinmostofthe markets,itjustdepends[on]wherethey wanttolive.”

PHOTO: FMICHAEL CUNNINGHAM

PHOTO /TED BAGHURST

FIRST HOME BUYERS | COVER STORY

WHANGAREI

“IF YOUHAVEHALF A MILLIONDOLLARS OF DEBT, FOR EVERYPERCENT YOUR MORTGAGERATE GOES UP,THAT’S $5000OFADDITIONAL INTEREST.” ECONOMISTBENJEPATTERSON

OneRoof.co.nz 9

AGENTSIN AUCKLAND agreethefirst homebuyermarketiswakingup.

DiegoTraglia,atop-sellingagentfor HarcourtsNorthwestRealty,whosellsall overthecity,saystherecentsoftening oftheCCCFAandchangestoprice capsandgrantshadmadelifeeasierfor buyersbuthigherinterestratesand,more importantlyhighertestrates,werestilla problem.

“Therehavebeentwoorthreedifferent changesofheartintermsofregulations andincentivesfromtheGovernmentbut it’sstillveryhardbecauseoftheinterest rates.”

Pricedropshaveputmoresuburbs withinreachoffirsthomebuyerswith lessthan$1mtospend,withTraglia highlightingopportunitiesinGlenfield, BirkdaleandBeachHavenonAuckland’s NorthShoreandthewholeofWest Auckland,includingMassey,Henderson andpartsofWestHarbour.

Traglianotesthatsomefirsthome buyerscanbepicky,wantingchampagne onabeerbudget.“Theywantthe dream-theywantthequarteracrewith thedoublegarageandtherenovated house.Thereareplentyofoptionsfor townhousesbutKiwisdon’tlikethattype ofpropertysotheystillwantwhatthey

can’taffordalotofthetime.”

TomRawson,co-ownerofRayWhite Manukau,inSouthAuckland,isseeing farmorefirsthomebuyerslooking inareaslikeWattleDowns,Conifer Grove,WeymouthandManurewa. “Thatsouthwesternsideseemstobea desirableparttobebuyinginandit’sat pricepointswefindfirsthomebuyers areshoppinginaswell.The$600,000to $850,000rangeseemstobegoodfirst homebuyerterritory,”hesays.

Rawsonsaysthateventhoughmany firsthomebuyerswouldprefertomake conditionaloffers,theyshouldstilllookat what’sonofferatauction.That’sbecause he’sseeingalotofinvestorswhohave hadenoughandaresellingupbutthey wantthedealdoneontheday.

“Someofthemaredrivingfromallover Aucklandtoouroffices.Theywantto doadealandoftenthey’renothanging arounduntilthenextdaytodoadealwith aconditionalmarket,”hesays.

Rawsonaddsthatfirsthomebuyers strugglingtogettheirheadsaroundhigh interestratesshouldrealisethey’renot thathigh.Heboughthisfirsthousewhen rateswereatninepercent:“Theseare normalinterestrates-wejusthadatwoyearperiodofincrediblylowrates.”

‘We’re themostaffordable cityinNewZealand’

ALOT OF firsthomebuyershavemovedto Christchurchbecauseoftheaffordableprices, saysJustinHaley,residentialandprojects divisionalmanagerforBayleysChristchurch.

Incentivesforfirsthomebuyerstobuyoff the-plantendtodrivemanythroughtonew subdivisions,hesays,althoughChristchurch hasplentyofoptions.

“Predominantlyalothavebeenlandingin HalswellthroughtoLincoln.It’sgoodtosee themre-enteringthemarketastheCCCFA easementsstarttotakeeffectalittlebit.”

Firsthomebuyersstarteddisappearing fromthemarketlastSeptember/Octoberand Bayleysisreadyfortheirreturnwithaninhouseteamsetuptohelpthemworkthrough allthechangesand helpthemdealwithbanks sotheycangettheirfinancepre-approved andbereadytogo.

“You’vegotanexpertworkingforyourather thanyouworkingagainstyourbank.We’re seeingbrokersgetpeopleapprovedwhereas theyhavealreadybeendeclinedbytheirown banksoit’sdefinitelyhighlyrecommended.”

Havingthefinancealreadyapprovedmakes abigdifferenceoutinthemarketplaceif peoplegointoadeadlinesaleormulti-offer situation,Haleysays.

Hesayssubdivisionsthroughoutthe northwestofthecityarepopularareasfor first-timebuyerswithbudgetsofbetween $400,000and$850,000,aswellascity suburbs.

Opawa,Woolston,Linwoodandthe outskirtsofRichmond,BishopdaleandSt Albansareallgreatplacestobuy,asareparts ofAvonhead,BurnsideandSummerfield.

It’salsopossibleforfirsthomebuyersto breakintosomeoftheposhersuburbs,such asMerivale,whereHaleysaystheycould pickupatwo-bedroomproperty,which mightbeoneoftwoorthreeunits,foraround $600,000-$700,000.

Anotheroptionisanew-buildinthecentral citywhere$600,000-pluswouldbuyan apartmentorpossiblyaterracehouse.

Thatsameamountinsomeoftheotherfirst homebuyersuburbswouldgetafreestanding 1960sfamilyhomeon600sqmto800sqm.

“Christchurchunashamedly-it’sbeen oursecretforawhile-butwe’rethemost affordablecityinNewZealandandpeopleare startingtowakeuptothatnow.”

Haleysaysmorethan25,000peopleleft AucklandsinceCovidandalotofthemended upinChristchurchwherethereisbrand-new infrastructureandeasyaccesstomountains andsea,plusaffordablehousing.

Thefirst-timebuyerswhodoarriveinthe cityarepartofitsrevitalisation,Haleysays.

CHRISTCHURCH

PHOTO:PETERMEECHAM

PHOTO:FIONAGOODALL

CHRISTCHURCH

PHOTO:PETERMEECHAM

PHOTO:FIONAGOODALL

If aNorthlandpropertyhasbeen soldanytimeoverthepast 26years,chancesare... 'The Butler Did It!' Contact TraceyLovelock-Butler forexceptional 5star serviceandresults 0278595777 /www.traceylovelockbutler.co.nz/ IndependentAgentLtd -LicensedREAA(2008) FIRSTHOMEBUYERS | COVERSTORY ‘A lotofinvestorshave had enoughandaresellingup’

AUCKLAND

10 OneRoof.co.nz

OUTSTANDING

INALL

“Tanya hasbeen wonderful to deal with.Shehas keptin touch regularly, helpedwithproblem-solving,andhas gonethe extramile to assist us.”

“I wouldnothesitateto use Tanyato sell aproperty formeandwillhighly recommendher to friendsand family.” 021247 4274 tanya.maich@bayleys.co.nz

Contact me today foraw service ward-winning MACKYS REALESTATE LTD, BAYLEYS,LICENSEDUNDERTHEREAACT2008.*EOFY 2021/2022 JANE ANDROBERT, JAN2022 TOPPERFORMING RESIDENTIAL SALESPERSON JANUARY- APRIL2022 BAYLEYSWHANGAREI

RESULTS

MARKETS

OneRoof.co.nz 11

With over adecade of sales andmarketingexperience, Jules has asolid understanding of whatit takes to get results. Herbackground in media gives her an edgeonhow to market your property

Whether it be digital, printorradio,she has the advertising skillsto implement an effective campaign to market your property

GiveJules acall to see howshe can helpwith your property journey.

Residential /Commercial /Rural /Property Services

Jules Shinyei 022671 4274 jules.shinyei@bayleys.co.nz MACKYS REAL ESTATELTD,BAYLEYS, LICENSED UNDER THEREA ACT2008 JULES SHINYEI BAYLEYSREAL ESTATE 12 OneRoof.co.nz

BY DIANACLEMENTguide to The

OneRoof buying your firsthome

Buying your first homeis abig step. Butevery yearthousandsofNew Zealandersmanagetodo it and becomehomeowners.

Withproperty pricesfalling, moreand morefirsthome buyers willachieve theirdreamoverthenext 12 to24 months,picking upthekeys totheir veryownhome.It’sdo-able withthe rightknowledgeandattitude.

Discoverwheretostartandhowto buywith OneRoof’scomprehensive guide.

We’vecmpiled aseriesofarticles coveringthehome-buyingjourney fromdreamto reality.Thisguide coverseverythingfrom:howtosave for adeposit,tosettlementday,when thehomebecomesyours.

Findouthowmuchdeposityou need,howto qualifyfor amortgage, thedifferentsalesmethods,buying new,andthelegalprocess. We cover allthemainquestions andissuesthat first-homebuyerswillencounteron thejourney.

SETTING

A BUDGET

When buying your first home, it’scritical to set arealistic budget.It’s thefirst step in working outhow much youcan affordand how much thebank is likelytolendyou

How much canIborrow?

The first step in working out howmuch you can affordand how much the bank is likely to lend you is to crunch the numbers to determine howmuch you can affordtospend on ahome. This helps you focus on the right housesin your price range.

Most banks have affordability calculators, which crunch your income andspendingtodetermine how much youcan comfortably payeach fortnight or month.

Most buyers need 20% of thehome’s purchase price as adeposit in order to borrow therest as amortgage.With a brand-new home,the deposit is 10%.If youqualify for schemes such as Kāinga Ora’s FirstHome Loan andFirst Home Partner,itispossibletobuy with a5% depositprovidedyou meet certain income and propertyprice thresholds.

Tocalculatehowmuchyouhave foradeposit,adduphowmuchyou havesavedalreadyinKiwiSaver,other investmentsandinthebank.Youmaybe abletoborrowmoneyfromthebankof mumanddad,or,ifyou’relucky,receive agiftthathelpsyougathersufficient deposittobuy

Once you’ve worked out how much deposityou have, youwill have an indication of how much youcan afford to payfor ahome.Itisimportant to understand howmuch homes are sellingfor in theareayou areinterested in moving to.Youcan find sale prices for recently sold houses, estimates based on sales in the area and alsouse our house prices report updated monthly on OneRoof.co.nz.

Supplementing income to affordrepayments

How much you canborrow fora mortgage comes down tohow much the bank believes you can repay comfortably

Often, first-home buyerswill seek to supplement their income to helpcover therepayments:

● Buying as asingle or acouple: Buying with two incomes is usually

easier than one. If you are applying for ajoint mortgage (with apartner,family member or friend) the bank will calculate how much it will lendyou based on your joint income and expenses. If the mortgage is 100% in your name the amount you can borrow will be based solely on your income and expenses

● Having atenant, flatmate or boarder: If youplantolivewith aflatmate in yournew home,you mightbeable to count some of the rent as income in the mortgage calculation. Be aware that lenders won’t count theentirerent paid to youasincome.

Speak to thebank or a mortgageadviser

Yourbank’smobilemortgage manageroranindependent mortgageadviser(broker)canhelp youdothenumbers.Theservice isusuallyfree.Yourmanager oradviserwillgothroughyour financesandadviseonissuessuch asconsumerdebt,andsuggestways toincreasetheavailablesurplus youhaveformortgagerepayments.

You’ll need to learn some of thejargon:

● Loan-to-value ratios (LVRs): the percentage of theloan that the bankiswilling to lend. It adds up to 100%. So if the LVRis80%,you needa20% deposit.

● Debt-to-income ratios (DTIs): some banks will onlylend you a certainmultiple of your income, such as six timesyour salary

● CreditContracts and Consumer Finance Act (CCCFA): alaw thatrequireslenderstoact responsibly.Itcan, however, restrict how muchhome buyers can borrow because banksare required by lawtoensurethe loan is affordable forthe home buyer

Paymorethan theminimum repaymentif youcan

Whatyou canaffordnow mightchange in thefuture

When banks assess whether they will lend to you, they use atest rate which is several percentage points higher than the actual interest rate. This helps ensureyou can affordthe mortgage if interest rates goup.

It is still agood ideato create apersonal budget based on your actualexpenses.

Thingstoconsider

●

Mostfirst-home buyerstakeouta 30-yearmortgage becausethe repaymentsare lowerthanshorter mortgageterms However,thelonger themortgageterm themoreinterestyou willpayintotalover thelifetimeofthe loan.

Ifyoucanafford to,it’sworth budgetingforhigher repaymentsora shorterloanterm(25 or15years).

Ahome-buyingbudgettakesintoaccount howmuchyouearn,howmuchdeposit youhave,thecostsofbuying,andwhat yourone-offandongoingexpenseswillbe afteryoumovein.

Makesureyou calculatethe upfront costs of buyingahomesuch as lawyers’ fees and LIMs, and alsonew ongoing costs such as council rates, body corporatefees andhouseinsurance.

Using KiwiSaver

Saving for ahousedeposit requires that you spend lessthan you earn. Most firsthome buyers save with KiwiSaver.There aremany advantages to this:

● Good an additional 3%, although some employers use a“total remuneration” clause in the employmentagreement to avoid paying this.

● You’ll receive the annual government contribution of up to $521.

● Youmay also qualify for aFirst Home Grant. The grantranges from $3000 to $20,000 depending on the number of yearsyou’ve been saving,whether the home is existingorbrand-new,and if you’reasingle or acouple, buying.

● Youwon’t be tempted to dipinto your savings for everyday spending

Whatare the upfront costs and legalfees?

Thetotal amount of money you need to buy ahome is more than just the deposit.

Upfront expenses forbuying ahome include:

● $1000 to $1500 forconveyancing/legal fees

● At least $400 for each building inspection

1 FIRST HOME BUYERS GUIDE

14 OneRoof.co.nz

● Around $300foreachLIM(Land InformationMemorandum)

If ahousepurchasefalls through andyou havetostartagain,you mayhavetopaymorethanoncefor buildinginspectionsandlegalfees.It’s unfortunate,howeveryourbuilding inspectorand/or lawyercansaveyou frombuying alemon.

Additional costs Movinginalsocostsmoney.Thereare removaltruckcostsifneeded,utility connection feesandyouwill needtobuy furniture andfurnishings(unlessyou alreadyownthese).

The costofbuying ahomedoesn’t stop withmovingin. Youmayneedto budgetfor renovationcosts.

Ongoing expensesincludefortnightly ormonthlymortgage repayments, utilitiesbills,councilrates,home insurance,andmaintenance.Inmany apartmentcomplexesyouwillhave body corporatefeesto pay, which do atleastcoveryourmaintenanceand insurance.

Yourmortgagealsocan have hiddencosts suchaslendersmortgage insurance (LMI)/LowEquity Premiums(LEP)ifyourdepositis lessthan20%.

OneRoof.co.nz 15

SAVING FORA DEPOSIT

Work outhow much youneed to save

To set your savings target for the deposit, work out approximately what you expect your first hometo cost at the time when you’reready to buy.With that figureyou can work out howmuch your 5%, 10% or 20% deposit will be in dollar terms

If your first home is likely to cost $600,000, a5%depositis$30,000, a10% deposit is $60,000, and 20% is $120,000. For an $800,000 house, that’s $40,000, $80,000 and $160,000. You’ll probably need another$5000 to $10,000 for your purchase and moving costs.

Start by searchingOneRoof to get an ideaofhow much you’ll pay for a home in yourcriteria.

How long will it take?

How long it will take you to save for a deposit on your first home will depend on:

● What the home willcost

● How much deposit you willneed, and

● How much disposable income you have to save after necessitiesare paid for

With abrand-new home, thedeposit is usually 10%. Those who qualify for schemessuchas Kāinga Ora’sFirst Home Loan it could be 5% if youmeet certain incomeand propertyprice thresholds.With First Home Partner, the deposit will vary according to how much aparticipating lender is willing to lend to you andthe percentage contributionKāinga Ora will make towards purchasing the homewith you.

Once you know how much deposit you need, dividethat by the sum you plantosave weekly or monthly,and from this you canworkout how many years it will taketoget your deposit together

If you can, savingmorethan the minimum deposit makes sense. With a

higher deposit, you will sometimes get alower interest rate.Also, because you’reborrowing less, your regular interest payments will be lower.They’recalculated on the outstanding mortgage balance.

Toolstohelp yousave

All the banks have mortgage calculators, which give you an indication of how much your mortgage will cost each fortnight or month. Sorted.org.nz also has amortgage calculator.Some banks have goal planners.

The banks may be able to split your pay into various accounts as it comes in, which makes saving easier

How to createabudget

Budgeting is essential for anyone who is serious about saving for afirst home. It will help you prioritise spending in order to reach your goal faster

First, download your bank account, credit cardand loan statements for the past three months and then categorise the spending under headings such as: food, utilities, rent, giving, saving, and fun money

Next, compareyour expenses with your earnings.

● If you arespending morethan you earn: you will need to cut costs.

● If you break even each month: you may have enough income to cover mortgage repayments.

● If you have asurplus income each month: this is agood place to be, but you might still need to reduce your outgoings to reach your savings goal.

Budget apps and spreadsheets are available on the Internet. Sorted has a simple budgeting tool. Most banks also have tools to help you budget.

Thereare many budget apps on GooglePlay and theApp Store. Make surethe one you choose works for New Zealand. Some budgeting apps such as Booster’s mybudgetpal (free) and PocketSmith (paid) download your bank transactions automatically,which makes budgeting quicker

Using Kiwisaver

Theverybestplaceto keepyourfirst-home savingsisinKiwiSaver becauseofthebenefits forfirst-homebuyers. You’llneedtosavefor atleastthreeyearsin KiwiSaverbeforeyou canuseittobuyyour firsthome.Togetthe mostoutofKiwiSaver youneedtosaveforfive yearsormore.

AllKiwiSavers receiveagovernment contributionofupto $521.43eachyearon thefirst$1042.86saved. Ifyou’reemployed,you shouldalsoreceivea contributionfromyour employerequalto3% ofyourgrossincome Anotheradvantageof savingforahomeloan withKiwiSaverisyou can’tbetemptedtodip intoyoursavings.

Afterthreeyears youcanwithdrawallof yoursavings,except for$1000,tobuyyour firsthome.Saverswho qualifycanalsogeta FirstHomeGrantofup to$5000perperson foranexistinghome,or $10,000forabrand-new home.That’sdoubled iftwopeoplesuchas acouplearebuying together

Topsavingstips

Saving for ahouse deposit is not easy, but the sooner you have adeposit, the sooner youcan buy

Earning moremoney makessaving for adeposit easier.Italso increasesthe amount you can borrow

Decreasingwhatyou spend now can pay off.Ifyou’relike most New Zealanders, you’ll spend morethan you needto, and smallexpenses addupvery quickly

Trygaming yourself to spend less and savemore. That might encourage you to thinkbeforespending unnecessarily

If youwantyour budget to succeed, always makesureyou give yourself afixedsum of “fun”moneyeachpay packet to spend on whateveryou want, then manage the rest carefully

● Increase your KiwiSaver contributions. If you’re already saving all you can, great. If you needsome encouragement, you could increase your KiwiSaver contributions because it comes out of yourpay before you receive it.You can choosecontributionsrates of 3%, 4%, 6%,8% or 10%. Then just adjust yourbudget aroundyour newnet pay.Ifyou can’t committoputting away moreinKiwiSaver because you might need it in emergencies, at least set up automatic payments from your bank accountintosavings.

● Payoff consumer debt. If you’re paying interest on storecards, credit cards, hire purchase, or otherdebts, it’s slowingdown your savings. Pay off thehighest interest debtfirst if you can. Paying downconsumer debtisimportant if you’regetting ready to buy.Any debt youstill have, including student loans and buy now pay later, willreduce the amount you can borrow because youhaveless spare money to payyour mortgage. If youcan’t increase payments on the existing debt as wellassave for a deposit,then at least stoptaking out new debt. If youcan’t trust yourself, cut up your credit andstorecards.

● Ask parents forhelp. Some parents areinthe financial position to help

If you’ve decided to buy yourfirst home, you’ll need to save fora depositand the sooner youstart the better.Hereare some practical tipstohelp you startsaving

2 FIRST HOME BUYERS GUIDE

16 OneRoof.co.nz

andmaybeabletolendorgiftyou someofthedeposit.

● Find an additionalsourceofincome. Somesaversget asecondjob,or aside hustle to makeextramoney.Youmight alsowanttoselloff someunwanted belongings.Doingsocouldadd afew thousanddollars to yoursavings,but alsoteachyounot to confuseneeds andwantsinthefuture.

● Getapay riseorswitch jobs.You canincreaseyourincomebyseeking apromotion,orswitchingemployers. Earningmoreatworkisn’talways easy.Lookatyourskillsetthentalk toyourbossorhuman resources departmentabouthowyoucanmove upintheorganisation.Ifthereare nopossibilitieswithinyourexisting organisation,itmay be timetomove.

● Reduce yourday-to-day expenses. Makingsavings is easierthanyou think. Take areallyhardlookatyour bankandcreditcardstatements.Most peoplehavemoreentriesforlunches, coffees,takeaways,and restaurants thanthey think.Take alonghardlook atyoursubscriptionsfromsoftware toNetflix.Cutthemout,orlimitthe numbertomakethem atreat.

● Watch living costs. Renteatsupa huge chunkof yourincome.Saving for

adepositcouldbeeasierifyoumove backhome,takeinflatmates,orget acheaper rental.It’snotforeverand canspeedupyourhomepurchase considerably.

● Learnhow to savemoneyon groceries. Oneofthe bigexpenses whereweconfusewantsandneeds isoursupermarkettrolley.Planyour meals,learnto cook,andaskyourselfif everyiteminyour trolleyisa necessity. Manyaren’t.Comparepricesbetween mainstreamsupermarketsandother suppliers.Youmay havea Chineseor Indian supermarketnearyou, acheap fruitandvegetableshop,or afarmers market.Savingscanbeconsiderable.

● Shoparound forbetterdealson

yourpower, broadband andmobile Ifyou haven’t done this for 12

phone. Ifyouhaven’tdonethisfor12 monthsmostlikelyyou’reonan old plan,whichcostsmorethanthelatest onebeingofferedto newcustomers.

● Speaktoanaccountant,mortgage adviser(broker)orfinancialadviser earlyon.Theycangiveusefuladvice.

Treatyourself to anewbed togowithyour new home

BedsRusWhangarei 094383550 •Open 7Days Cnr PorowiniAve &TarewaRd

$ $

if y. n OneRoof.co.nz 17

Starting out

How much you canborrow forahome loan depends on the size of your deposit.

If you’rebuying an existing property, you’ll usually need a20% deposit. For abrand-new home, that percentage drops to 10%. Buyers who qualify for the government’s First Home Loan scheme only need a5%deposit.

The first hurdletopassfor buyers is thebank’s affordabilitytest, which considers whether the surplusleftover onceyour expenses arededucted from your incomeissufficient to cover mortgagerepayments.

GETTING

A HOME LOAN

Most people needtoborrowtobuy ahome. The mortgage (also known as ahome loan)combined withyourdeposit make up the purchase price of the property.Inmost casesyou’ll need to have 20% of the purchase price of the house saved as adeposit beforethe home loan application process starts.

If youdon’t qualifyto borrowfrom abank or can’tget as much as you need,there areother options.

Youcould delay your purchase. That allows you to build up abiggerdeposit and/orincrease your income, both of which allow you to borrow more.

Asmall proportion of buyers who can’t borrow from thebank anddon’t want to wait borrow instead through “non-bank lenders” such as building societies and finance companies.Amortgage adviser can arrange this. But the trade-off is that usually you’llpay ahigherinterest rate for loansfromnon-bank lenders.

Mortgage /income calculatortools

Mortgage calculatorscan give you an indication of how much you may be eligible to borrow

Differenttypes of homeloans

Thereare different types of homeloans. The most common ones are:

Tableloans

Howmuch shouldyou beearningto payoffyour mortgage?

There’snomagicsum youneedtoearntobe eligibleforamortgage It’slessabouthow muchyouearnand moreaboutbeing prudentwithyour finances.

Thegeneralruleis thatyouwillneedto earnsufficientmoney tocoverrepayments afteryourexpenses.

interest payments component.

Floating versus fixed interest rates

As well as choosing the most appropriate type of home loan for your circumstances, you also need to consider floating versus fixed interest rates.

Afloating(variable) interest rate can rise or fall at any time, affecting your repayments.Afixedinterest rate(for anywherebetween one andfive years) ensures that the interest rate youpay on your loan is fixedfor theentirety of that period.Your repaymentsdon’t change until thefixed-rate period expires.

Acommon tactic for homebuyersis to split amortgage overmorethan one fixed-rateterm, and to keepaportion on afloating rate, which allows extra repayments, paying down the home loan faster

● Consumerdebt(including studentloans)

● Yourcreditrecord

● Whetheryou’reacasualor permanentemployee,orselfemployed

loans,reducestheamountyoucan borrowbecauseanyrepayments aredeductedfromyouravailable income.Youshouldalwaysbe upfrontwithyourmortgageadviser (broker)orbankmortgagemanager aboutyourdebtswhenyou’re applyingforamortgage

With table loans, you pay afixedamount each fortnight or month. In the beginning, most of the payment is interest, but as the balance slowly reduces, agreater portion of your payments goesto pay off the capital.

Revolving credit home loan

Arevolving credit home loan is like a giant overdraft.Yousave interest when your wages gointo the account each month becauseit reduces the outstanding balance.Youneed to be very disciplined for thissort of home loan to work, but it’s an option forthose who arefinancially prudent.

Reducing balance loans

Areducing loan is similar,but has higher repayments at the beginning because you’repaying moreofthe capital than a table loan.As the amount outstanding to the bank goes down, so too does the

Whenassessing yourabilitytopay, thebankwilltakeinto accountexpenses thatyoudidn’thave beforebuying.They includecouncilrates, maintenanceandhome insurance,whichis compulsoryifyouhave amortgage.

Evenifitlookslike youcanaffordto borrow,sometimes thebanksdecline That’sbecausethey determineaffordability usinga“testrate”, whichisseveralpercent higherthantheactual interestrateyou’llpay. Thereasonforthisis thatthelenderwants tostress-testyour financestoensureyou canstillaffordtopayif mortgageratesrise.

If you’reunsure about which home loan options arebest foryou,your mortgage adviser or manager can help identify the most appropriate for your financial circumstances.

Applying foramortgage

Thehome loan application process

Beforeyou applyfor ahome loan, you’ll need to getsome documentationtogether Regardless of whether you’regoing direct to abank as your lender orgoing through amortgage adviser you’regoing to need the following:

● Proof of income

● Arecordofoutgoings and debts

● Evidence of yourdeposit

● Bank statements from thelast six months

● Acopy of your photo ID, and

● Proof of address.

It costs the same to completethe application witha mortgageadviser or thebank’s mobilelendingmanager as doing it online. They can give you a clear pictureofwhattoexpect from your lender beforeyou sign the mortgage documentation

If going directly to thebank rather than via amortgage adviser,make sure you ask thebank aboutthe interest rate, its

3 FIRST HOME BUYERS GUIDE

Home loan eligibilitycriteria Whenbanksassessyourloan,they wanttodetermineifyouareagood risktolendto.UndertheCredit ContractsandConsumerFinance Act(CCCFA),banksandother lendersmustlendresponsibly Cuttingbackyourspendingsix monthspriortoapplyingfora mortgagecanhelpyourapplication considerably Ingeneral,yourhomeloan eligibilitywillbeassessedonthe following: ● Income ● Expenses(bothessentialand non-essential)

Consumerdebt,includingstudent

18 OneRoof.co.nz

fees,yourabilitytomakechangesto your mortgageonceset up,andwhat happens if youbreak afixed-rateterm. Youare not limitedto borrowingfrom your ownbank.Shop around.When competitionis highbetweenbanks, youcanoftennegotiatetheinterestrate downor getthe loanapplicationfees reduced.

KiwiSaverFirst Home Grantconsiderations

Ifyoualreadyhave apropertylined up,thenit’s agoodideatogetyour KiwiSaverwithdrawalandFirstHome Grantapplicationsinatthistime. As aruleofthumb,FirstHome Withdrawal andFirstHome Grants cantake anywherebetween 20 days andfourweekstosortout.Sogetthe paperwork togetheratthesametime aschoosing alender.Ifyou’reunsure abouttheapplications requiredforyou to accessyourKiwiSaverfundsfor buyingyour firsthome,orifyou have questionsaboutyour owneligibility, OneRoof has aKiwiSaver firsthome buyer’sguide.

How long does applying fora home loan take?

Typicallyyouneed14daystothree weeksforthebanktoassessand approveyourhomeloanapplication. Makecontactwiththebankormortgage advisermuchearlierthanthat.

Applying fora home loan whileyou’reself-employed

As aself-employedhomeloanapplicant, you’regoingtoneedthefollowing ontopofthestandardsupporting documentation:

● Proofofincome(suchasyour balancesheet profitandloss,orcash flowstatements)

● IRDdocuments (GSTandIR4 returns).

Itcansometimesbehardertoget amortgageifyou’reself-employed becausethestandardeligibilitycriteria ismoresuitedto employees.Ifyou don’tqualifyforahomeloan froma bank,mortgageadviserscan placeyour business withalternativelenders.That usuallycomesatthecostof ahigher interestrate.

Mortgage adviserscanworkwithyou topickthemostappropriatealternative lenderforyourpurchase.

Gettingpreapproval homforyour eloan

Homebuyersoften applyto getpreapprovedby abanktogetanideaof theirpotentialbuyingpowerandprice range. Thisgivesyou more confidence toshoparoundforaproperty.Itshows to realestateagentsand vendorsthat youareaseriousbuyer.

Pre-approvalisanindication

FIXED RATE

F l O a t i

ofwhatyoucan borrowifthe bank approvesof thepropertyyouwantto buy.Ifinterestratesrise,loan-to-value ratios(LVRs)andother ruleschange, oryoudon’tmanagetosettlewithin thepre-approval period, youwillmost likely need to reapplyfor pre-approval. Thisis somethingtobevery waryofif buyingatauction,goingunconditional onanyproperty,orbuyingoff-the-plan whenthebuildcouldtakelongerthan expected.

Contact amortgageadviseror your lenderofchoiceanddiscussyour circumstanceswith them.Theywillbe abletoassessyourmortgageeligibility and tellyouwhatthey’rewillingto lend yousubjecttoconditions.

Gettingpre-approvalcostsnothing. Nor doesitlockyou intothelender.

Theadvantages of usinga mortgagebroker

Mortgageadvisersare ago-between, workingonyourbehalf.Theycan adviseyouonhowtoimproveyour abilitytoborrow,shoparoundfor you,andnegotiatewiththebanksand otherlenders.Theserviceisfreeifyour mortgageisplacedwith abank.Ifyou don’tfitthebankcriteriaandborrowfrom anon-banklender,youwillneedtopaya feeforthis.

nMortgageadvisersalsosaveon legworkbecausetheyknoweach bank’scriteria,andtheycan argue yourcaseif yourloan is borderline.Theycan alsonegotiateconditions suchasguarantees.If youhaveconsumer debtthat’sstandingin yourwayofgettinga mortgage,mortgage adviserscanhelp restructure thatdebt orgiveadviceabout payingitoff faster. First-homebuyers canfindthepurchase process daunting. Having amortgage adviserinyourcorner takes someofthe uncertainty out. They’reexpertsintheirfieldand workfor you.

Thingstokeep in mind when ahgetting ome loan

● Youcanonlyborrowasmuchasyour depositandincome/expenseswill allowyou

● Makesure youbudgetin expenses such as councilrates,maintenanceand insurance

● Banks’mortgagemanagersand independentmortgageadviserscan helpyou navigatetheprocess

● Pre-approvalisn’t aguaranteethat youcanborrow.It’s anindicationand expiresafteraperiodoftime

● Self-employedapplicants need additionaldocumentationandmay havetoconsideralternativelenders

%

OneRoof.co.nz 19

Schemesthatcan contribute toward your deposit

Buying afirst homeisn’t easy. KiwiSaver andother government schemes canhelp.The earlier youlearn aboutthem, thebetterprepared youcan be to use them.

Both First Home Withdrawal and First HomeGrant schemes can boost your deposit providingyou have been saving into KiwiSaver for at least three years andpreferably five or more.

The KiwiSaver rules allow first-home buyers, or those in asimilar position, to withdraw all but $1000 from their KiwiSaver to buy afirst home.Youmay also qualify for aFirst Home Grant

How does theFirst Home Grantwork?

The FirstHome Grant is overseen by Kāinga Ora and provides up to $10,000 per coupletowards the purchase of an existing first home or $20,000 fora brand-new home.

Youcan only receive the First HomeGrant once. That includesits predecessors, HomeStartgrantor KiwiSaver deposit subsidy

To be eligible youneed to:

● Havesaved at least 3% of your total income into your KiwiSaver for a minimum of threeyears

● Earn less than $95,000for asingle or $150,000for twobuyers or an individualbuyerwithone or more dependants

● Chooseahomethatfallsunder thecurrentpurchasepricecapfor thearea

Underthe First Home Grant, firsthome buyerslooking to purchase an existing home areeach eligible to receiveup to $1000 peryearfromtheir three-year savings mark,capped at $5000. Thoselooking to buyanew home or landwillqualify for $2000per yearupto$10,000 each.Where two people arebuying the house andboth qualify,the grant is doubled.

FIRSTHOME BUYERGRANTS ANDKIWISAVER

Using your Kiwisaver

KiwiSaverisagreatplace tosaveforyourfirsthome AsaKiwiSavermember youcancontribute3%, 4%,6%,8%or10%of yourbefore-taxpaytoa providerandfundofyour choice.Youremployer shouldcontribute3%as well.Youcanalsomake regularorone-offvoluntary contributionstoKiwiSaver. Ifyou’reunemployedorself employed,youcanmake voluntarycontributions.

TheGovernment contributes50cforevery $1yousaveeachyearupto $1042.86.Thatmeansup to$521.43offreemoney, whichthencompoundsand growsovertime,boosting yourdeposit.Theannual cut-offdateforKiwiSaver contributionsisJune30. Yoursavingsand employer/government contributionsareinvested byyourfundproviderand growovertime.Typically,the returnishigherthanyou’d getinatermdepositand youpaylesstaxthanyou wouldonastandardsavings account,meaningyour moneygrowsfaster BecauseKiwiSaveris lockedin,it’sagreatwayto stopyoufromdippinginto savingswheneveryou’re tempted.

of up to $10,000 for asingleordouble that for twoormorepeople buying, providing you meet the eligibility criteria.

Purchaseprice caps

What youwanttobuy must fallunder the purchaseprice capfor theregion you live into be eligible forthe First Home Grant.Thosecapswill also vary dependingonwhetheryou’re buying an existinghome or anew home Make sureyou apply early to ensure your grant is approved in time. The First Home Grant is paid out either as a deposit or at settlement.

Theapplication process

Thereare two ways to apply foryour First Home Grant:

● Apply for pre-approval beforeyou decide on aproperty to giveyou adegree of certainty about your eligibility; or

● Apply once you findaproperty and have asigned sale and purchase agreement.

The applicationprocessstarts online via Kāinga Ora’s KiwiSaver portal. For preapproval you will need thefollowing documents to hand:

● Proof of income

● KiwiSaver contributionstatements

● Photo ID

If youhavefound ahometobuy already, you willalsoneed:

● Acopy of the agreement or asigned sale and purchase agreement or a contract fora new build

● Asettlement date or adate when the money is needed to pay the deposit, which is at least four weeks away

● Other supporting documentation relevant to your purchase.

If you have any questions about the First Home Grant, speak to amortgage adviser (broker) or amobile mortgage manager, who can help younavigate the application process.

Using your FirstHome Grantonanew-build

Buying anew build withthe FirstHome Grant involves afew more steps.For example, for aproperty to qualify asa new-build,itmust have received itsCode Compliance Certificate (CCC) within six monthsof the date of yourFirstHome Grant application.

Additional considerations forfirst-timebuyersof new-builds

Getalawyerinvolvedassoonaspossible New-buildcontractsveryoftenhave clausesthatstandardsaleandpurchase agreementsforexistinghomeswillnot have.Itisbesttogetalegalopinionon thesaleandpurchaseagreementbefore yousubmityourFirstHomeGrant application.

If you’rebuying aproperty where you have to make progress payments at specificpoints during the build, then any funds that you’reeligible for under the First Home Grant must be held in trust or escrow by an independent organisation and not the developer

Using your FirstHome Granttobuy land

It’salsopossibleforfirst-homebuyers tousetheirKiwiSaverFirstHomeGrant topurchaselandtobuildapermanent house.Buyersneedtoliveinthehome foratleastsixmonthsfromtheissueof theCCCforthehouse.TheFirstHome Grantisthesameasforanew-build.The FirstHomeGrantruleshaveacapon themaximumcostofthelandandhome combined.

To qualify for the First Home Grant on land you need to apply and getpre approval. Make sureyou:

● Submit yourapplication online at least four weeks beforesettlement

● Supply the plans for building work or relocation related to thelandthat you arebuying

● Have afixedprice building contract showing the cost of construction and estimated start and finish dates

● Include asigned sale and purchase agreement

Find out how theKiwiSaver First Home Withdrawal andFirst Home Grant schemes can boostthe deposit and makeit easier for youtobuy your first home.

4 FIRST HOME BUYERS GUIDE

20 OneRoof.co.nz

Someprevioushomeownersina similarpositiontofirst-homebuyers mayalsoqualifyfortheFirstHomeGrant andFirstHomeWithdrawalschemes.

KiwiSaverFirst Home Withdrawal scheme

TheFirstHomeWithdrawalschemeenables first-homebuyersand othersin asimilar financialpositiontowithdrawallbutthe last $1000ofKiwiSaverfundsfor thedeposit ortowardssettlementontopof anyFirst HomeGrantentitlement.

Aswellasanexistinghome,theFirst HomeWithdrawalcanbeusedtobuyanewbuild,landyouintendtobuildon,ortobuild ahomeonmultiple-ownedMāoriland.

thefollowingprovidingyouleavebehind $1000inyourKiwiSaver savings account:

● KiwiSavercontributionsyou’vemade personally

● KiwiSavercontributionsyour employerhasmade

● Anyfeesubsidiesyou’ve received

● Governmentcontributionstoyour KiwiSaveraccount,and

● Thegrowthyou’veearnedonyour KiwiSaverfunds

Applying fora First Home Withdrawalgrant

Beforeyouapplywithyourscheme providerfor aKiwiSaverFirstHome Withdrawal,youwillneedthefollowing readytogo:

● Certified photoID

● Certified proofofaddress

● Yoursolicitor’strust accountdetails

● Acopyofthesaleandpurchase agreement foryour property

Grant,except

Yourmortgagebrokerormobile mortgagemanager willconfirmthe amountthatyou needtowithdraw. Once youhaveapplied,yourscheme providerwillliaise withyourlawyer. Themoneyispaidbytheproviderinto your lawyer’strustaccount.

Additional optionsfor first homebuyers

TheKiwiSaverFirstHomeGrantis justoneofthemanyoptionsfirst-home buyerscanaccesstohelppurchase theirfirsthome.Thereare anumber ofotherschemesforfinancingpartof thepurchasepriceorprovidingmore affordablehomes.

Theyinclude:

● KiwiBuild. Thisis aprogramme toencouragedevelopers,iwiand councilstocreateaffordablehomes withinpricecaps.KiwiBuild homes aretypicallycheaperthanequivalent homesonthe openmarketandare verypopular.Allnormal KiwiSaver criteriaapplyforthe FirstHome Withdrawal andFirstHome Grant schemeson aKiwiBuild home.Tobuy one, youneedtobechosen by ballot. Moreinformationcanbefoundat www.kiwibuild.govt.nz

● FirstHomeLoan. TheFirst Home Loanscheme runbyKāingaOra enablesqualifyingbuyersto purchase ahomewitha5% deposit.KāingaOra doesn’tprovidethedeposit.Instead, itprovidesaguarantee,enabling your banktolendmoretoyouthan itsnormallendingstandards would otherwise allow. LiketheKiwiSaver FirstHomeGrant,thereisan income capandaregional housepricecap.

● FirstHome Partner is another governmentschemethatallows qualifyingbuyerstoshareownership of abrand-newhomewithKāinga Ora.KāingaOrabuysupto25%ofthe propertythatyou’reinterestedin, and becomesaco-owner on thetitle.Over time,thehomeowner willeventually buyout Kainga Ora’sshare.

● KāingaWhenuaLoan Scheme. The KāingaWhenuaLoanSchemerun byKāingaOra and Kiwibankhelps Māoribuildor relocatehomesonto ancestralland.Ifyou’reeligiblefora KiwiSaverFirstHome Withdrawal, youcan alsoputanyfundsobtained that waytowardsthepurchaseofa KaingaWhenuaproperty.

CnrofPorowini Ave&TarewaRd Phone094383550 Open 7Days BedsRus Whangarei We’vegotbedsofallsizes to go inhousesofallsizes, comeseeustoday

Whatdoyouneed to make aKiwiSaverFirst Home Withdrawal? TheeligibilitycriteriaforFirstHome Withdrawalisthesameas theFirstHome

there arenoincomeorhouse pricecaps. Whatcan youwithdraw from yourKiwiSaver? Ifyou’reeligibletomake aKiwiSaver withdrawaltowardsyourfirsthome purchasethen you’ll beabletowithdraw

OneRoof.co.nz 21

FINDING THE RIGHT PROPERTY

Gettingstarted

We’d all like to liveinabeautiful home in aperfectlocation.Your firsthomeis not your forever home, however You’ll almostcertainly need to make compromises and start your journey with amoremodest home. That might be an apartment or terrace house to begin with beforeyou can trade up the property ladder to astandalonehome in your suburb of choice.

Finding thebest suburb foryou

Consider what’s important to you in a suburb. Depending on yourstage of life and priorities,different amenities might be important to you.

Ask yourself questions such as:

● Which schools areinzone?

● What is the proximity to public transport or main highways?

● What about local shops, cafes and night life?

● Whereare the nearest parks, beaches or other recreational areas?

Think of howyou could compromise. Forexample, you mightbe able to movefurther out of town where homes arecheaper if thereisgood public transport.

Workingout prices

The average property value varies according to suburb. Some suburbs wherethereare alot of large expensive homes with water views have ahigher average property value, while others on city fringes or dominated by apartments have alower average property value.

But most suburbs have arange of properties within them,which means that even the most popular and expensive suburbs have options for first-home buyers.

Youmay have grown up dreaming of owning astandalone home on aquarter acresection, but to get on the property ladder you may need to begin with an apartment, or terrace home, that is joined to neighbouring properties.

The different typesof property

FREE STANDING HOMES

arethemostcommon stylesofhomesinNew Zealand.Theyare detachedandsiton theirownsection.

To get an indication of what a property is worth, searchfor it on OneRoof.co.nz. TheAVM(automated valuationmodel) will giveyou agood indication of what the property is worth, while recent sales information will tell you what propertiesare selling for in individual suburbs.

and may even limit things likepet ownershiporpaint colours

Whatare bodycorps?

Before you gettoo far into your house-hunting journey,find out how much you canaffordtopay for ahome and how much you canborrow by checking with your bank or mortgage adviser(broker).They will look at your savings, salary,spending,and the variouscosts associated with buying homes such as lawyers’ fees and moving costs. Banksalso have useful calculators on their websites thatcan give you ageneral indication of how much you mightbeapproved to borrow

All owners in unit title developments, suchas apartment buildings, automatically become members of thebody corporate.

With many apartments you needtobudget for annual body corporate levies, which cover the building management, upkeep of shared areas and lifts, insurance and maintenance costsofthe building.

TOWNHOUSES arehomesthathave theirownexittooutside, butareusuallyconnectedto theneighbouringproperty. Usuallyit’saterraceof townhouses.

Freehold,leasehold or crosslease?

FLATS AND APARTMENTS areusuallyhomesin multi-unitblocks orhighrise buildings.

Therearethreemain propertytypesin NewZealand: Freestandinghomesare generallythemostsought afterinNewZealandand sitonlargerpiecesof land,whichmeansthey costmore.Thesmallerthe sectionthelowertheprice, whichiswhytownhouses willusuallybecheaper thanastandalonehome andapartmentsandflats thecheapest

Freehold: Most traditional homes in New Zealand arefreehold whereyou own the house and the land it sits on. Leasehold: is where you own the building, butnot theland.Youpay annual ground rent to the landowner Leasehold is common overseas,but apart from someapartment buildings isn’t oftenseen in New Zealand. The lease may be fora fixed number of years, such as 100,after which youno longerhave theright to havea home on it.Orthe lease can be in perpetuity The shorter the lease and the higher the groundrent, thelowerprice thehome will fetch when sold.

Cross lease: This is aform of home ownership whereeach home on a cross-lease section owns ashare of the underlying land. Historically these came about whensomeone subdivided their section into two or three. Instead of eachowner buying theland beneath their home, they took ashareinthe entirelandand alease for thebuilding Some New Zealanders arehesitant to buy cross leased properties because the ownershipstructurerestricts them from alteringorextendingtheirhome,

Your lender will take into account the body corporate fees when assessing how much youcan afford to borrow.Don’t letbodycorporate fees putyou off buying.You’d needtospend moneyeachyear on maintenance of ahome,somay find the cost of owning is little different whether thereisabodycorporate or not

Buying off theplan

Buying off the plan means you sign up to buy ahomewhen it’saplan only and isn’t built.Yousign asale and purchase agreement upfront and pay adeposit to securethe property,but don’t settleuntil the home is built.

This hassomeadvantages forfirst-home buyers.

● Brand-newhomes come with a guarantee against defects,and usually they won’tneedmuch in the wayofmaintenance for thefirst sevento10years.Thiscan be abonus in theearly years when mortgage repayments can be adrain on finances.

● 10% Deposit. You’ll typically only pay a10% deposit on anew home instead of 20% requiredfor existing homes under the ReserveBankof New Zealand’s loan-to-value ratio (LVR) rules.

● Some homes bought off the plan can be alteredduring the build.

Buying your first home is abig step in life. It will take time to find the right propertyinthe right suburbata price you can afford.

5 FIRST HOME BUYERS GUIDE

22 OneRoof.co.nz

Ifit’s astandalonehome you mightbeabletochangethedesign orarrangeforcosmeticorappliance upgradesatyourcost.

● Typically it’s cheaper to buy ahome off the planthanonce it’s complete. Thisisbecausedevelopersneedto secureapercentageofpre-salestoget theirfinancetobuild.They’reoften willingtosellslightlymorecheaply tothefirstbuyerswhosignsaleand purchasecontracts.

● KiwiBuild: Youcangointo aballotto buy aKiwiBuildhomeoff theplan. Theyaretypicallypricedlessthanan equivalent homebeingsoldonthe openmarket.

Therearepotential downsides to buying offtheplan

Buyingoff theplan ismoreriskythan buying aturnkey (completed)home.

Someofthoserisks are:

● Thedevelopergoesbustanddoesn’t completethe build

● Thebuildisdelayedandyourpreapprovalforfinance runsout

● A“sunsetclause” is invokedbecause thebuildhastaken toolong,and thedevelopercancelsthesaleand purchaseagreement.Itmaybe considerablymoreexpensivebythen tobuyanotherhome

● “Materialdifferencesclauses”are usedtomakechangestoproposed

floororcarparkplans,thedeveloper usesthe‘specificationslist’to substituteitemsthatarenotalways like-for-like

● The homeissmallerthanitappeared inthe “renders”onthemarketing material,oritis poorqualitywhen built.

Building ahouse as afirst-home buyer

NewZealandhasalongstanding traditionofgetting ahouse builttoyour ownspecifications.Youeitherbuya houseand landpackage wherethehome isbuilttoyourliking,oryoubuy the landseparatelyand employanarchitect andbuilder, orchoose agroupbuild home.

Theadvantageofbuildingisthatyou get ahomethat’suniquely yoursinthe locationofyourchoice.Butthereare risks:

● The projectmaybedelayedandyour pre-approval runout

● Therecouldbebudgetblowouts

● Thebuildermightdopoor workmanship,or

● Otherissuessuchasfailuretogeta

10-year-guaranteeon thework Averyspecificriskforfirst-home buyersusingKiwiSaveristhatthe costtobuildincreases(thanksto“cost adjustments”clauses)anditexceedsthe pricecapsfortheFirstHomeGrant.This couldspelldisastersobecareful.

Getting amortgage

Typically,youwillpay a10%deposit andthenprogresspaymentsasthebuild progresses.Banksoffer construction loansdesignedtopayforthebuildin stages.It’sa goodideatoseekadvice from amortgageadviserorbank’s mortgage managertoensureyou understand howtheseloansworkand getthemostappropriateoneforyour situation.

CanyouuseKiwiSaver to builda house?

Youcan useKiwiSaverFirstHome WithdrawalorFirstHomeGrant to paythe deposit,andorwithdraw at settlement.TheKiwiSavermoney mustbeheldintrustorescrowby the developeruntilthecertificate of titleand theCodeCompliance Certificate(CCC)

OneRoof.co.nz 23

areissued.Oncethathappensthe saleis settledandthebuyercanmovein.

Buying to renovate

Manyfirst-homebuyersoftenbuyfixeruppersas awayofgettingontheproperty ladderat alowerprice.

Pros and cons

Thetwomainadvantagesoffixer-uppers arethattheycanbepricedconsiderably cheaperthansimilarhomes,andyou cangrowyourequityinthehomeby doing renovations.Onthedownside, youwillfindthatdoingup ahomeis nowherenearaseasyasitappearson TV renovationprogrammes.Renovators oftenunderestimatethecostandtheir ownskills.Bylawmanyjobs requirea licensedbuildingpractitioner(LBP)such as abuilderorelectrician.Theycanbe expensive.

How much does it cost to renovate?

Thecost of renovatingdepends onthe scopeofthework.Some renovationsareaestheticandothers arestructural.Thelattercanbevery expensiveindeed.

Whencalculatingthe costof buying ado-up house, makesure youfactorinthecostof renovating. Youcanonlyborrow topayfor renovations ifyou’renot already stretchedtothelimit.Bankswill runyourapplication throughan affordabilitycalculator andifyou don’thavesu

cientequityand/ or income to make repaymentsyou won’tbe abletoborrowmore.

Valuations

calledthegovernmentvaluation(GV) orconfusinglybecauseofitsacronym, theratingvaluation(RV),areproduced forratingspurposes.Theydon’tgive anaccurateindicationofhowmucha propertymightsellfor.Youcanalsoget insurancevaluations,whichtellyouthe costto replacethehomeifit’sdestroyed. Realestateagentscan giveyouan estimateof what ahouse mightsellfor. Registered valuations(RV)are betterto relyon.Theyoftencost around$1000, but willgive amoreaccurate valuationofthe home. Valuersare trainedtoassess the marketworthof apropertybasedonan inspectionandcomparablesales.

WhydoI needone? Aregistered valuationwillhelp ensure youa)don’tpay toomuchfor ahomeand b)don’toffertoolittleandloseoutifyou

Banksoftenrequirearegistered valuationbeforetheywilllendona property. That’stoensurethatshouldyou defaultonyourmortgage, theycansell thepropertyand recouptheirmoney. If you arebuyingthehouseformorethan thevaluationit’sunlikelyyou’llbeloaned asmuch moneyas youexpect.

Building reports

andLIMs

Yourhomeis averybiginvestment. It’s agoodideatoget reportsdoneto ensureit’singoodorderandthereare nosurprises.

● Apre-purchase report(AKA building report) canidentify defectsin ahome.It’sbesttoget yourownand notrely on one providedbytheseller.Aprepurchaseinspectionby abuilder willhelpyou avoid expensive mistakesbybuying aproperty with expensiveproblemssuchas rot,leaky roofs,oldwiring, and wornoutpipes.Itcanalsogiveyou negotiatingpowerwhenbuying, or helpyouchoose betweentwo properties.It’spainfultopayfor apre-purchaseinspectionbecause itcouldcost$1000or more,justto missout,and need anotherone on the nextproperty.

● ALandInformationMemorandum (LIM) is afile heldbylocalcouncils thatsummarisestheinformation heldonthatproperty. Itcontains arangeofinformationsuchas rates information,stormwaterand seweragepipeson theproperty, consents, andpotentialerosion, subsidence, slippageorflooding, andthepossiblepresenceof hazardousmaterials.

ManyhomesinNewZealand aresold without apriceonthembyauction, tenderordeadlinetreaty.Itcanbeha knowwhattobidoro

erinthatcase.

Whatisahousevaluation?

Homescanbevaluedfordi

purposesandit’s importantto understandwhattheymean.Thecou valuation(CV),whichcanalsobe

hansimply

izeandconditionofa tslayout,elevation,views,and

● Theproperty file contains all thedocuments that relatetoa LIM reportsuchas building and resourceconsents,and correspondence withthecouncil aboutthe property. Be aware thatbuildingworkdonewithout consentisn’tincluded in thefile.

Whypaymore whenyoucouldbuy, sell,or refinance yourpropertyfora low,fixedfee?

Whathappens at ahouse

FIRSTHOMEBUYERSGUIDE

ff

fferent

ffi

be sold hardto se n? ouncil b) yo couldaffordmore.

valuation? When aregisteredvaluervisitsthe propertytheydoalotmorethansimply compareittonearbyhomes.They willlookatthesizeandconditionofa property,itslayout,elevation,views,and surroundings. hers very e ng. u ou 24 OneRoof.co.nz

Residential /Commercial/Rural /PropertyServices Homeprepguide If youfail to plan,thenplan tofail… Whengettingreadytosellyourhome,it’svitaltomakeitasvaluableaspossible to yourpotentialbuyers. By properlypreparing yourhome forsale, yougiveyourself thebestchanceofachievingthebestpossibleresult. Thisguidewillhelp youwith: Making agreat first impression. Giving youclarityonwhat areasinyourhometofocuson. Formingpartof awinninggameplan,whenworkingwithanagentthatwillhelpyou at every stage ofthesellingjourney. ALTOGETHER BETTERPREPARED MACKYS REALESTATELTD,BAYLEYS,LICENSEDUNDERTHEREAACT2008 PaulSumich 021606460 |paul.sumich@bayleys.co.nz JustscantheQR code to get yourdigital copy oftheguidedelivereddirectly to you.Orgo to www.paulsumich.co.nz/ home-preptodownloadit. OneRoof.co.nz 25

Getting started

You’ve fallenin lovewith aproperty and want to buy it.You’ll need to have your ducks linedup. That includes your mortgage, your KiwiSaver withdrawal, FirstHomeGrant if you qualify,aproperty inspectorto write a pre-purchasereport, anda lawyer (or conveyancer) to handlethe salefor you.

Trynot to become too attached. If you’rebidding at auction, youmay not win. Propertysales fall through for other reasons as well, such as the vendor asking too much, or hidden issues that the property inspector or lawyer discovers.

Buying at auction

Biddingatauctionisoneofthemost commonwaystobuypropertyinNew Zealand.Atauctionyoubidagainst otherstobuythehome.Theauction isrunbyanauctioneerwhoopensthe biddingatafigurethatisusuallyless thanthereserve,thepricetheselleris willingtoaccept.Eachbidneedstobe higherthanthepreviousbid.

Whenbuyingatauctionyouare usuallybuyingunconditionally,so youcannotbackout.Sometimes thesellerwillagreetoavariation ofagreementinadvance,suchas alowerdepositamount,orthe settlementdate.

Iftheauctiondoesn’treachits reserve,itwillveryoftensellshortly after,bynegotiationwiththehighest bidder.Sometimesconditional buyerswhoneedtimetogetfinance willbeconsiderediftheauctionfails toresultinasale.

Ifyouwinatauction,youwillneed topaythedeposit,usually10%,on thesameday.Youwillalsohaveto signthesaleandpurchaseagreement.

Othermethods of sale

Sold by negotiation

When ahouse is sold by negotiation, buyers make offers whichsellers

THE BUYING PROCESS

can accept or negotiate on(called countersign or counter offer).

Sold at tender or ‘bydeadline’

Some properties aresold at tender or by deadline sales (also called “treaties”). With atender youmake writtenoffers by acertain date, which areconsidered by the seller.Adeadline sale is similarwithbuyers able tomake an offer any timeuptothe deadline.

For tenders and deadline sales you usuallyonly getone shot at making an offer,soneed to make it your best first time. The seller chooses between the offers presented.

How to make an offer on ahouse

If the house isfor sale by negotiation, you offer an amount you areprepared to pay.Usually you don’t makeyour best offer immediately

Offers aremade to the vendor via the real estate agent who is selling the property.The offer is made on asale and purchase agreement document, noting any conditions, such as subject to finance, building reports, LIM (land information memorandum), or due diligence (investigation). The seller can either accept your offer,ormake a counter offer

Buyer and seller continue to negotiate in this wayuntil an agreement is reached. If you areinamulti-offer situation wherethereare other potential buyers you might need to put your best offer on thetable early

Beforemaking your starting offer,it’s averygood idea to get your lawyer to check the contract and property records of title (showing ownership and other information).Your lawyer will also check the title for any defects.

Most existing homes in New Zealand aresold using thestandardADLS/ REINZ Sale Purchase of Real Estate Agreement. Eventhen, therecan be different clausesused.

Sale and purchase agreements for new-builds areoften bespoke and could

have worrying clausesthat alawyer will spot

Typesofoffers youcan make Unconditional and conditional offers

Your offer canbeunconditional, or conditional. Some of the common conditions include:

● Securing finance

● Getting asatisfactory building report

● Alonger than normalsettlement period

● Asunset clause which voids the agreement afteracertain period of time

● Early access to do renovations prior to settlement

Sellers tend to prefer unconditional offers or at leastas few conditions as possible. As aresult, your offer is more likelytobe accepted if it has fewer conditions.

Whathappens after youmakeanoffer?

An offer by negotiation or tender is not legally bindinguntil it is accepted and both the buyer and sellersign the saleand purchase agreement (contract).

Buyers should notmake offers on multiple properties at the same time, because they areduty-boundtobuy both properties if theoffers areaccepted.

Once both buyer andseller have signed, thecontract is “unconditional”. This meansyou can’t back out evenif you change your mind. Buyers willneed to paythe deposit as soon as thecontract is signed.

Legalfeesand paperwork

Buying ahomeis abigcommitment and thereisquiteabit thatcould go wrong. Alawyer works for you and checks the sale and purchase agreement, the title, the LIM, and does the transfer of the property on settlement day.It’sbest to choosea specialistproperty lawyer to do this work.

Whether you’rebidding at auction or making an offer,you’ll need your ducks in arow to win that dreamhome

Anofferby negotiationor tenderisnotlegally bindinguntilitis acceptedandboth thebuyerandseller signthesaleand purchaseagreement (contract).

6 FIRST HOME BUYERS GUIDE

26 OneRoof.co.nz