The EU is one of the world’s leading biodiesel producers and consumers, with an industry worth around US$34bn/year

Oil

24 Black Sea update

The ongoing Russia-Ukraine war continues to impact Ukraine’s land bank but new EU tariffs on Russian grain and oilseeds may open up opportunities for Ukrainian products

28 Insuring against risk

The global shipping of commodities can create issues before, during and after shipment, making it critical for sellers and traders to consider their insurance risk

30 Potential of red palm oil

Red palm oil can be used as a natural antioxidant due to its high carotenoid, Vitamin E and phytosterol content but its acceptance among consumers remains low, due to its red colour and environmental image

Oils & Fats International (USPS No: 020747) is published eight times/year by Quartz Business Media Ltd and distributed in the USA by DSW, 75 Aberdeen Road, Emigsville PA 17318-0437. Periodicals postage paid at Emigsville, PA. POSTMASTER: Send address changes to Oils & Fats c/o PO Box 437, Emigsville, PA 17318-0437

Published by Quartz Business Media Ltd Quartz House, 20 Clarendon Road, Redhill, Surrey RH1 1QX, UK oilsandfats@quartzltd.com +44 1737 855000

Printed by Pensord Press, Merthyr Tydfil, Wales

Tackling obesity

A new report from global medical experts says obesity needs a new definition to distinguish between people suffering health problems from the condition and those who are otherwise healthy (see p6).

“Obesity is a health risk – the difference is it’s also an illness for some,” says Prof Francesco Rubino, from King’s College London, who chaired the expert group.

Those with chronic illnesses caused by their weight should be diagnosed with “clinical obesity” but those with no health problems should be diagnosed with “pre-clinical obesity”, the group says in their report published on 14 January in The Lancet Diabetes & Endocrinology journal. This new definition would allow adults and children with obesity “to receive more appropriate care” while reducing the numbers being over-diagnosed and given unnecessary treatment, such as drugs and surgery.

Obesity is commonly defined as having a body mass index (BMI) of over 30 – a measurement that estimates body fat based on height and weight – but this reveals nothing about a patient’s overall health and fails to distinguish between muscle and body fat or account for the more dangerous fat around the waist and organs, the report says. However, there are concerns that this approach could mean less money for those in the “pre-obese” category, particularly with weight-loss drugs in such high demand.

The wildly popular Wegovy weight-loss drug has been flying off pharmacy shelves since its launch in the USA in 2021, propelling Danish manufacturer Novo Nordisk to become Europe’s most valuable listed company in 2023. It is available in more than 15 countries (USA, Denmark, Norway, Germany, UK, Iceland, Switzerland, UAE, Japan, Spain, Canada, Brazil, Italy, Australia, France and China) and costs around US$200-2,000 month, according to Reuters. Many of the public health care systems in these countries say they will not reimburse the cost. Denmark, for example, said in 2023 that reimbursing Wegovy would cost it as much as US$4bn/year while, in the UK, it is only prescribed by some specialist weight management clinics for two years.

Wegovy’s active ingredient is semaglutide, which mimics a hormone that is released when we eat, lowering appetite and making a person feel fuller. It is taken in weekly injections and can help people lose up to 15% of their body weight, although research suggests patients often put weight back on after stopping. Patients can also suffer digestive side effects such as nausea, and possible long-term side effects include pancreatitis and the risk of developing thyroid cancer.

The drug throws up many wider questions about obesity and society’s approach to this issue. For example, are we comfortable that weight-loss drugs are more widely available to those who can afford them? Are they only for those with a medical need or should they be used preventatively to stop people becoming obese, particularly when the patent on semaglutide expires in 2026 and it can be more widely prescribed. Should these drugs be prescribed to children? Does it matter if people use them for cosmetic reasons while still eating unhealthy food? Should the focus be more on tackling today’s obesogenic environment, which disproportionately hits poorer communities due to lack of access to affordable healthy food and physical activity such as walking or cycling? Or do governments need to get tougher on the food industry and control the amount of sugar, fat and salt companies put in their products?

One in eight people in the world are living with obesity today (according to World Health Organization figures from 2022) and the World Obesity Federation predicts that one billion people will be living with obesity by 2030. As yet, there are no clear answers to tackling the issue and what role weight loss drugs will play in this.

CMB S.p.A. Via Appia Km 55,900 – 04012 Cisterna di Latina (LT), Italy

CMB MALAYSIA ENGINEERING FOR OILS AND FATS SDN. BHD. D-23A-03, Menara Suezcap Tower 1 KL Gateway, Jalan Kerinchi 59200 Kuala Lumpur W.P. Kuala Lumpur Malaysia

CMB INDIA ENGINEERING FOR OILS AND FATS Pvt. Ltd. 501, A Pinnacle Corporate Park 5th Floor, Near Trade mark Center, BKC Bandra East, Mumbai, Mumbai City, Maharashtra, India

IN BRIEF

ARGENTINA: The government announced plans on 23 January to lower agricultural export duties on soyabeans, sunflowerseed and other crops, the Buenos Aires Herald reported on the same day.

Economy Minister Luis Caputo said the measure would last from 27 January until the end of June.

The plan would reduce export duty rates on soyabeans from 33% to 26%, soyabean derivatives from 31% to 24.5%, wheat from 12% to 9.5%, barley from 12% to 9.5%, sorghum from 12% to 9.5%, corn from 12% to 9.5% and sunflowerseed from 7% to 5.5%, the Buenos Aires Herald wrote.

Caputo said although President Javier Milei’s administration was aiming to lower taxes, it would need a US$8bn surplus to remove the duties permanently.

The decision to lower taxes came against a backdrop of ongoing drought in the country and a drop in commodity prices, he added.

Rosario Stock Exchange President Miguel Simioni supported the decision, saying the duty reductions would allow producers to improve their competitiveness, "which is essential to continue generating added value, employment and foreign currency for the economy".

To access the lowered duties, exporters would have to sell their dollars to the Central Bank 15 days after completing an “affidavit of sale abroad”, the Buenos Aires Herald wrote.

US pauses Canada and Mexico tariffs, not China

US President Donald Trump has agreed to hold off imposing 25% tariffs on Canada and Mexico for 30 days, pulling the region back from the brink of a potentially damaging trade war, the BBC reported on 4 February.

Trump agreed to pause the threat of tariffs after reaching a deal over migrants and drugs crossing borders with Canada and Mexico, the Metro reported on 5 February.

However, an additional 10% tariff on Chinese imports came into effect on 4 February.

In response, Beijing announced it would be imposing retaliatory tariffs on a range of US products, including 15% on coal and liquified natural gas and 10% on crude oil and agricultural machinery, to take effect on 10 February.

The Canola Council of Canada (CCC) had said in a statement on 1 February that tariffs would have had a devastating effect on the country’s canola sector. The USA is Canada’s leading market for canola exports. The total export value of Canadian canola products to the USA in

2023 was C$8.6bn (US$5.8bn), including almost 3M tonnes of canola oil valued at C$6.3bn (US$4.3bn) and more than 3.5M tonnes of canola meal valued at C$2bn (US1.4bn).

Argus Media also wrote on 31 January that if imposed, potential tariffs could lead to disruptions in US corn and soyabean sales to China and Mexico, creating substantial risks for US agriculture markets.

China and Mexico are the two largest purchasers of US corn and soyabeans, collectively accounting for 48% of US corn exports and 61% of US soyabean exports since 2019, according to US Department of Agriculture (USDA) data.

In 2018, during Trump’s first term as president, tariffs placed on China led to counter-tariffs on US agricultural exports and a substantial fall in trade, with US exports of corn and soyabeans to China dropping by 74% that year compared to the previous year, according to USDA data.

Trump has also threatened to introduce tariffs on the EU and BRICS member countries.

BASF to sell food ingredients unit to LDC

German chemical and biotech giant BASF is selling its Food and Health Performance Ingredients business to Louis Dreyfus Company (LDC) for an undisclosed sum.

The business includes aeration and whipping agents, food emulsifiers and fat powder grades; health ingredients such as plant sterols esters, conjugated linoleic acid (CLA), omega-3 oils for human nutrition (pictured) and some smaller product lines.

The transaction is subject to customary closing conditions and regulatory approval and includes BASF’s production site in Illertissen, Germany.

BASF said on 23 December that the business had limited synergies.

“The divestment will allow us to focus on our core businesses in Nutrition & Health. We remain committed to ... expanding our business in key

areas such as vitamins, carotenoids and feed enzymes,”

LDC said, adding that the deal was its first investment in facilities to produce food and health performance ingredients at scale.

Codex approves GOED standard for microbial omega-3s

The Codex Alimentarius Commission (CAC) has approved the Global Organization for EPA and DHA Omega-3s (GOED)’s framework to establish a global standard for microbial omega-3s, Nutraceutical Business Review reported on 11 December. Under development for more than a year, the proposal aimed to ensure that omega-3s

– specifically algal eicosapentaenoic acid (EPA) and docosahexaenoic acid (DHA) oils – could be freely traded worldwide.

CAC is part of the UN Food and Agriculture Organization and is responsible for developing industry codes of practice which boost the safety, quality and fairness of international trade in food and nutrition.

The CAC approval would mark the next step in adopting a global industry standard for omega-3 ingredients, Nutraceutical Business Review wrote.

GOED estimated the first draft of the industry standard would be presented at the 29th session of the Codex Committee on Fats and Oils in 2026, the report said.

Photo: BASF

USA: The Food and Drug Administration (FDA) has updated the definition of what counts as 'healthy' in a bid to help consumers make healthier choices.

To qualify as 'healthy', a food product must contain certain amounts of at least one of the food groups included in the Dietary Guidelines for Americans. This includes dairy, grains, fruits, vegetables and protein-rich foods such as beans, lean meats, nuts, seafood and soya. Products must also fall below certain limits on added sugars, sodium and saturated fat.

Food companies could voluntarily use a 'healthy' claim on their packages if their products met the new definition, the FDA said.

As a result of these changes, the FDA said more foods that were key to healthy eating patterns – such as nuts and seeds, higher fat fish such as salmon, olive oil and water – would qualify for the 'healthy' claim.

“This rule will help ensure that consumers have access to more complete, accurate and up-to-date nutrition information on food labels,” the FDA said on its website on 19 December.

“It is vital that we focus on the key drivers to combat chronic disease, like healthy eating,” FDA commissioner Robert M Califf added.

The FDA was also developing a 'healthy' symbol manufacturers could use.

Canada approves Bunge deal to acquire Viterra

Canada has approved global agribusiness giant Bunge Global SA’s acquisition of Glencore’s agriculture division, Viterra, but with a range of conditions, World Grain wrote on 16 January.

On 14 January, Canadian Minister of Transport and Internal Trade Anita Anand announced approval of the US$18bn deal, which would create one of the world’s largest agribusiness companies, close in size and scope to agribusiness leaders Cargill and ADM.

Anand said the government aimed to prevent the merger – first announced in June 2023 – from infringing on competition in the country’s grain and oilseed sector.

Bunge would be required to divest six grain elevators in Western Canada and retain Viterra’s Saskatchewan head office for at least five years. A price protection programme was required

“for certain purchasers of canola oil” in Central and Atlantic Canada, along with “legally binding controls” on Bunge’s minority ownership stake in G3 Canada to ensure Bunge “cannot influence G3’s pricing or investment decisions”.

However, the Grain Growers of Canada (GGC) said on 17 January that the conditions did not go far enough to protect market competition for Canadian farmers, and it was particularly disappointing that the conditions did not include Bunge’s divestment of G3, in which Bunge had a 25% stake. G3 Canada operates 19 grain elevators in Western Canada and one in Quebec, as well as port terminals in Thunder Bay and Hamilton, Ontario; and Quebec City and Trois Rivieres, Quebec. GGC also raised additional concerns including the market concentration of grain terminals at ports in Quebec.

COFCO delivers deforestation-free soyabeans

China’s largest food processor and manufacturer COFCO International sold its second shipment of deforestation-free soyabeans to COFCO Oils & Oilseeds in China, the com-

pany said on 3 December. Produced as a rotational crop at COFCO International’s sugar plantations in the Brazilian state of São Paulo, the soyabeans had also passed

third-party audits certifying they were produced in compliance with the COFCO International Responsible Agriculture Standard, which required the use of sustainable farming practices including water management, biodiversity conservation and ethical labour standards, the firm said. COFCO said it had also completed pilot shipments of soyabean products from Brazil and Argentina in preparation for compliance with the EU Deforestation Regulation, which required a segregated trade system for soyabeans, palm oil, coffee, cattle, cocoa, wood and rubber or their derived products.

Medical experts call for better definition of obesity in

Classing people as obese is medically ‘flawed’ and the definition should be split in two, according to a study by global experts reported by the BBC on 15 January. Although the term “clinical obesity” should be used for patients with a medical condition caused by their weight, the term “pre-clinically obese” should be applied to those remaining fat but fit, although at risk of disease, the group of more than 50 medical experts said in study published in The Lancet Diabetes & Endocrinology journal.

This was a better approach for patients rather than relying exclusively on body mass index (BMI) – a measurement that estimated body fat based on height and weight – the study said. Many countries defined obesity as having a BMI of over 30 but this failed to distinguish between muscle and body fat, or measure the more dangerous fat around the waist and organs, the study said.

Prof Francesco Rubino from King’s College London, who chaired the expert group,

study

said the current definition of obesity meant too many people were being diagnosed as obese but not receiving the most appropriate care.

While the Royal College of Physicians said the report laid a strong foundation “for treating obesity with the same medical rigour and compassion as other chronic illnesses”, others had raised concerns that pressure on health budgets could mean less money for patients in the “pre-obesity” category.

Photo: Adobe Stock

IN BRIEF

EU/MERCOSUR: A new free trade deal between the EU and Argentina, Brazil, Paraguay and Uruguay was agreed on 6 December, Olive Oil Times wrote on 16 December.

The landmark agreement would set up the largest free trade area in the world and aimed to increase bilateral trade and investment, and lower tariff and non-tariff trade barriers, the European Commission (EC) said.

With EU exports of goods and services to Mercosur totalling more than US$82.5bn/year and European countries accounting for more than US$395.7bn in investments within Mercosur economies, the region is the EU’s tenth largest trading partner, Olive Oil Times said.

EU olive oil exports to Mercosur currently faced a 10% tariff, while Argentina applied a tariff of 31.5%. As the deal would remove these tariffs, this could boost the competitiveness of EU olive oil in Mercosur markets.

However, Mercosur olive oil producers had raised concerns that cheaper European olive oils would impact their domestic market share, Olive Oil Times wrote.

In 2023, EU olive oil exports to Mercosur totalled more than US$508M.

Brazil is one of the world’s largest olive oil importers, averaging some 90,000 tonnes/year in the past three seasons, according to International Olive Council data.

EU to revise palm biofuel rules following WTO ruling

The EU is set to revise its palm oil-based biofuel rules following a World Trade Organization (WTO) ruling that part of its Renewable Energy Directive (RED III) unfairly discriminated against Indonesia’s palm oil exports, the Jakarta Globe wrote on 17 January.

Announced on 10 January, the ruling was seen as a major victory for the world's largest palm oil producer in its long-standing dispute with the EU over biofuel trade restrictions, the report said.

Indonesia brought the case to the WTO dispute body in 2019 after the EU classified palm oilbased biofuel as “high risk” due to its links to deforestation, and ruled that its use in transport fuel would be phased out between 2023 and 2030, Reuters wrote on 17 January.

While the WTO decision upheld the EU’s

classification, it found flaws in how the directive was implemented, the report said.

Specifically, the WTO found that the EU’s Delegated Regulation 2019/807 (delegated act), which classified palm oil as a high-risk biofuel source, was inconsistent with international trade rules.

French tax incentives that excluded palm oil-based biofuels while favouring rapeseed and soyabean alternatives were also deemed discriminatory, according to the Jakarta Globe report.

In a statement on 10 January, the EU pledged to address the issues, which were already under review as part of its regulatory framework, to bring its policies in line with WTO obligations.

The adjustments were expected to be finalised within 60 days unless the ruling was appealed, the report said.

Efforts to revive Syrian olive oil exports

The announcement by Syria’s new governing coalition announced that it would introduce free-market reforms and stimulate exports could revive the country's olive oil exports, effectively banned

since 2023.

Former president Bashar al-Assad Assad fled to Russia on 8 December after a coalition of rebels led by Hayat Tahrir al-Sham toppled his government.

Acting Finance Minister Riad Abd El Raoud was quoted in the Financial Times as saying the new government would undertake “a re-examination of all current monetary and economic policies”. One of these policies was the Ministry of Economy and Foreign Trade’s decision, announced last October, to give the go-ahead for 10,000 tonnes of olive oil exports.

According to the Ministry of Agriculture, Syrian olive farmers expect to harvest 11% more olives in 2024/25 compared to 2023/24, with oil production expected to reach 55,000 tonnes in areas controlled by the former Assad regime. Consumption in Syria was around 48,000 tonnes/year.

Peruvian palm oil producer linked to deforestation in report

Peruvian palm oil producer the Ocho Sur group has been linked to deforestation in the country in a 31 December report by journalism organisation, the Pulitzer Center. Documents obtained from a criminal investigation into Ocho Sur – along with internal company e-mails and bank records covering eight years of plantation operations – linked the company to US businessman Dennis Melka, the report said. A Peruvian prosecutor claimed Melka was the

ringleader of a “criminal organisation” that passed mature plantations from one firm his company had bankrolled, United Oils, to Ocho Sur. After the transfer, key personnel from United Oils remained in place, including Melka. Prosecutors claimed United Oils had illegally cleared much of the plantation land, and that Ocho Sur –despite its sustainable initiatives – was in many respects the same entity as its predecessor.

Ocho Sur has denied claims that the

company is a continuation of a previous company. “It is incorrect ... to attribute to it any alleged actions that occurred before its existence,” it wrote in response to a report by the Environmental Investigation Agency.

The US$160M that Ocho Sur’s backers, primarily US venture capitalists and private equity funds, have spent on its operations are the largest foreign investment in agriculture in the Peruvian Amazon's history, according to the Pulitzer Center.

Photo: Adobe Stock, generated by AI

Russia, Ukraine soyabean sector expands

The soyabean sector in Russia and Ukraine is expanding despite the ongoing conflict between the two countries, according to a 17 January World Grain report citing International Grain Council (IGC) data.

Although still relatively small players in the global soyabean market, Russia and Ukraine were expected to harvest a combined 13.1M tonnes of the oilseed in the 2024/25 marketing year, a 10% increase compared to the previous year.

With yields improving modestly but still

IN BRIEF

AUSTRALIA: Agricultural network firm Viterra has dropped its plans to acquire five sites in South Australia from agribusiness giant Cargill, World Grain wrote on 16 December.

Details of the proposed agreement were first announced by the companies in September. The five Cargill GrainFlow sites that were part of the transaction are located at Maitland, Crystal Brook, Mallala, Pinnaroo in South Australia and Dimboola in Victoria.

Viterra said Cargill would continue to be a major exporter purchasing grain through its network and remained committed to increasing its volumes as a key exporter from the state.

Cargill Australia acquired the GrainFlow storage and handling business in 2011.

Viterra is active in 130 countries and handles over 125M tonnes/year of agricultural products including grains, oilseeds, pulses, rice, sugar and vegetable oil, as well as a range of animal feed products.

Cargill’s Australian operations include grain and oilseed marketing, storage and handling, oilseed processing, and vegetable oil refining.

GrainFlow operates 16 grain and oilseed storage centres in Queensland, New South Wales, Victoria and South Australia states.

well below the global average, the IGC said most of the increase had been due to an expansion in planted area.

In Russia, which had seen rising local demand for soyabean products from the feed and food sectors, the crop was chiefly grown in the eastern and central parts of the country, the IGC said. The council estimated Russia’s 2024/25 soyabean production at 7M tonnes, up from 6.7M the previous year. Russian soyabean exports had increased sharply, reaching a peak of

1.3M tonnes in 2022/23 and averaging 1M tonnes over the last five years, with almost all shipments going to China, the IGC said. Ukraine ranks just behind Russia in soyabean output among Commonwealth of Independent States (CIS) countries and is forecast to produce 6.1M tonnes of the crop in 2024/25, an 18% rise compared to the previous year, according to the IGC. The country remained the largest CIS soyabean exporter and is forecast to export a record 3.7M tonnes of soyabeans in 2024/25.

Deforestation from coconut plantations

A new study shows coconut plantations have led to deforestation on more than 80% of Pacific atolls, with coconut palms covering over half of their forested areas, global conservation group The Nature Conservancy (TNC) writes.

Published in Environmental Research Letters, research from TNC and the University of California, Santa Barbara, (UC Santa Barbara) mapped the footprint of coconut palm agriculture across almost every Pacific atoll.

Over the last 200 years, this land cover change has profoundly altered ecosystems and hydrologic resources, potentially affecting atoll communities’ resilience to climate change and other environmental stressors, according to the 4 December TNC report.

“Coconut oil used to be essential to atoll economies, but, today, most coconut palm plantations are abandoned

and overgrown,” lead author Michael Burnett of UC Santa Barbara said. “With the growing climate threats facing Pacific atolls, it’s critical to figure out where these abandoned plantations are using up critical land and water resources, and where there may be opportunities to restore the native forests to the benefit of islands and islanders.”

At the time of the report, coconut palms represented over half of the tree covering

in this region.

“[The] replacement of broadleaf forests with coconut monocrops has been linked to groundwater depletion, declining seabird populations and adverse impacts on adjacent coral reefs,” Burnett added.

“Understanding the present extent of coconut plantations is crucial for confronting sustainability challenges facing communities across the Pacific’s 266 atolls.”

New system to track stolen Ukrainian grain

Ukraine, the UK and Lithuania have signed an agreement to launch a new system to track stolen Ukrainian grain, World Grain wrote on 22 January.

The Grain Verification Scheme (GVS) was aimed at preventing the illegal export of Ukrainian grain from Russian-occupied territories, the report said. The Wall Street Journal wrote in September 2024 that Russia had sold nearly US$1bn of stolen grain since its invasion of Ukraine in February 2022.

The GVS system was “the first step at the ministerial level in the implementation of a strategic agreement between Ukraine and the UK,”

Ukraine’s Minister of Agrarian Policy and Food Vitalii Koval was quoted as saying in a government press release.

The pilot of the initiative would be launched in the Lithuanian port of Klaipeda, which would become a key hub for verifying the origin of Ukrainian agricultural products, Koval said. The system would identify stolen grain and stop its illegal transportation and would also include a database from the UK in which advanced technologies for determining the place of cultivation would help protect the interests of Ukrainian farmers and market transparency, he added.

Photo: Adobe Stock

IN BRIEF

WORLD: The International Air Transport Association said on 10 December that sustainable aviation fuel (SAF) production totalled 1M tonnes in 2024, double the 0.5M tonnes produced the previous year. SAF accounted for 0.3% of global jet fuel production and 11% of global renewable fuel.

Volumes for 2024 were significantly below previous estimates that had projected SAF production in 2024 at 1.5M tonnes, due to key US production facilities postponing production rises to the first half of 2025, IATA said. In 2025, SAF production is expected to reach 2.1M tonnes, or 0.7% of total jet fuel production and 13% of global renewable fuel capacity.

CANADA: Canadian biofuels producer Tidewater Renewables has asked the federal government to impose countervailing and anti-dumping duties on US renewable diesel imports.

In a complaint to the Canada Border Services Agency (CBSA), Tidewater said on 8 January that the nation’s renewable diesel market was being impacted by US producers exporting volumes to Canada at artificially low prices due to US tax incentives. The complaint must have support from producers representing at least 25% of Canadian output to proceed.

UK: The government’s new sustainable aviation fuel (SAF) mandate came into force on 1 January and will require 2% of all jet fuel to come from sustainable sources, increasing to 22% by 2040. Alongside the mandate, the Department for Transport also launched a Jet Zero Taskforce on 25 November to support SAF production, delivery, zero emission flights and improved aviation systems.

Indonesia delays countrywide introduction of B40

The Indonesian government delayed the nationwide introduction of its B40 blending policy from 1 January until February to give businesses a grace six-week period to adapt, Reccessary reported on 7 January.

In addition, the government announced that by 2026, the biodiesel blend would increase to a 50% palm oil mix with diesel fuel (B50), with plans to completely halt diesel imports.

Indonesia’s Ministry of Energy and Mineral Resources (ESDM) vice minister Yuliot Tanjung said the six-week grace period would allow businesses to use up their remaining stock of B35 biodiesel, while related technologies would be adjusted accordingly.

State-owned oil company Pertamina had already prepared two refineries to produce B40,

the report said.

However, the palm oil industry has raised concerns that the upgraded biodiesel programme, – alongside a higher 10% export duty on crude palm oil (CPO) – would lower the volume of CPO exports, particularly against a backdrop of stagnant domestic production, according to a 25 December

The Star report.

On 19 December, the government announced that it would raise the CPO export from 7.5% to 10% to fund higher subsidies for biodiesel.

“Increasing the export levy will make Indonesian palm oil (exports) less competitive compared to neighbouring countries,” Indonesian Palm Oil Association (GAPKI) chairman Eddy Martono was quoted as saying on 22 December by Bloomberg Technoz (see also Statistics, p32).

Indonesia restricts UCO and POME exports

The Indonesian government has issued a new regulation, effective immediately, to curb exports of used cooking oil (UCO) and palm oil residue in a bid to ensure supply for its domestic market, Reuters reported on 8 January.

The move was aimed at helping it to attain its new B40 blending mandate (see above).

The new regulation requires all exporters of UCO and palm oil residue, including palm oil mill effluent (POME), to acquire an export allocation from the government.

Although authorities in Indonesia had been looking into ways to curb UCO exports for some time, the extent of potential restrictions was unclear, the report said.

In December, an official alleged that some cooking oil sold under a government programme called ‘Minyakita’ had been mislabelled as UCO and shipped overseas for use as biodiesel feedstock, media reports said.

Indonesia mandates all palm oil exporters to

sell some of their crude palm oil domestically at a capped price to be made into Minyakita cooking oil, which is then sold at a regulated price.

From January-November 2024, Indonesia’s UCO and palm oil residue exports totalled 3.95M tonnes, down 13.75% from the same period the previous year, Statistics Indonesia data shows.

EU governments approve Chinese biodiesel duties

EU national governments approved definitive anti-dumping duties on biodiesel (HVO and FAME) from China on 8 January during the EU Trade Defence Instruments Committee, the European Biodiesel Board said on 9 January.

The duties were approved in July 2024, following a probe by the EBB but subject to approval by EU national governments.

While welcoming the decision, the EBB said the protection against Chinese biodiesel imports was not perfect and there was still work to do to ensure proper implementation.

“It has been a long journey since the EBB started this case through. first. the circumven-

tion case and later this anti-dumping case. After Indonesia, Argentina and the USA, we now have measures in place against China,” EBB secretary general Xavier Noyon said.

“It will be crucial to monitor the evolution of all biodiesel imports particularly in light of the recent Chinese export tax on used cooking oil. We will also closely monitor for circumvention as there are no duties imposed on sustainable aviation fuel (SAF), and the fact that some companies received lower anti-dumping duties than others.”

The duties will come into effect for five years following publication in the EU Official Journal by 14 February.

Photo: Adobe Stock

t

e.

t.

e

Sasol launches rapeseed stearyl alcohol

Speciality chemical firm Sasol Chemicals – a business unit of global chemicals and energy company Sasol – has launched a rapeseed-derived stearyl alcohol for the personal care industry.

Produced exclusively from segregated rapeseed oil, the NACOL 18-98 product had been designed as a palm oil-free, bio-based stearyl alcohol solution for the personal care industry, the company said on 18 November.

The new product complies with the

IN BRIEF

BRAZIL: Leading Brazilian biofuel producer Be8 signed an agreement on 21 January with US synthetic biology firm Cemvita to develop glycerine into a low carbon feedstock to produce sustainable aviation fuel (SAF).

Be8 is Brazil’s largest exporter of glycerine, a byproduct of biodiesel production. It has biodiesel plants in Rio Grande do Sul, Paraná, Mato Grosso, Piauí and Pará states, as well as in Paraguay and Switzerland.

The firms said a working group would now conduct feasibility studies on the project and investment estimates for a glycerine-to-SAF raw material conversion plant in Brazil. The studies would also look at using the oil obtained from the new partnership as a feedstock in the Omega Green Project, an industrial complex to produce SAF, renewable deiesel and green naphtha in Paraguay.

European Union Deforestation Regulation (EUDR), which requires companies importing seven commodities linked to deforestation into the EU – including palm oil and its derivatives to prove that their products are not sourced from deforested land.

“Responding to the EU’s Deforestation Regulation, we developed this [product] as a readily-available alternative to palm oil derivatives,” Sasol Chemicals vice president (Care Chemicals) Louis Snyders said.

The product could be used as a con-

ditioning agent, stabiliser, consistency regulator, structuring agent and opacifier in conditioners and moisturisers for personal care, Sasol said.

South Africa-based Sasol Chemicals offers a portfolio of speciality chemicals for a wide range of applications and industries.

The company operates in 17 countries and is organised into four business divisions: Advanced Materials, Base Chemicals, Essential Care Chemicals and Performance Solutions.

BASF to scale up macaúba oil supply

German chemical firm BASF and Brazilian-German company INOCAS announced a partnership on 11 December to scale up macaúba oil supply for the personal care product sector.

The deal includes financing INOCAS’ plans to expand macaúba oil production in Brazil on an industrial scale.

Macaúba or acrocomia aculeata (pictured) is native to Brazil and adapted to semi-arid conditions and low-quality soils. Its fruits can be processed into pulp oil and kernel oil, with INOCAS supplying BASF with both in their deal.

BASF would use the macaúba kernel oil in its personal and home care portfolio in Brazil and Europe with commercial pilot volumes available this year.

“A significant portion of our products are derived from renewable sources such as natural oils [and] “macaúba kernel oil represents a new sustainable opportunity,” BASF

The pulp oil could be used in the process of obtaining bio-naphtha, which could be converted into polymers, solvents, detergents, lubricants, synthetic fibres, fuels and other products.

Regular macaúba pulp oil offtake for use as an alternative feedstock to substitute fossil resources would start in 2027, the companies said.

INOCAS has been develop-

ing, implementing and refining a model to cultivate macaúba trees on degraded pastureland since 2015. Working in partnership with smallholder farmers, INOCAS said it aimed to plant at least 50,000ha of Macaúba by 2030. The system supported regenerative agriculture by combining forestry and livestock farming without an additional land use change and also had positive impacts on soil quality, erosion control and biodiversity, the firm said.

Unilever and Nufarm to develop oils for cleaning ingredients

Consumer goods giant Unilever has formed a partnership with Australian agricultural chemical firm Nufarm to develop plantbased oils for cleaning ingredients.

Nufarm had previously developed and commercialised a variety of sugarcane called energy cane, a sustainable crop which generated significantly more plant matter and sugar than traditional sugarcane, Unilever said on 26 November.

As part of the partnership, biotechnology would be used to develop a new, commercially viable variety of energy cane that

could also produce biomass oil.

Derived from plant material, including the leaves and stems, the biomass oil would be a source of fatty acids, a core base ingredient for Unilever’s laundry detergents and beauty and personal care products, the company said.

“This partnership enables us to identify alternative ingredients for our household, beauty and personal care brands which will further support our ambition to reach net zero emissions across our value chain by 2039,” Unilever head of biotechnology Neil

Parry said. The first phase of the project would focus on the research and development of the plant biotechnology.

In addition to biomass oil, the crop would also continue to produce sugar, which could be used in other biotechnology processes to generate speciality ingredients such as fragrances, enzymes and cleaning ingredients used across Unilever’s portfolio, the company said.

The company said it would also explore if the leftover plant fibre could be used to produce paper and board for packaging.

president of care chemicals Mary Kurian said.

Photo:

INOCAS

TRANSPORT NEWS

Poland to build grain terminal at Gdansk

The Polish government has announced plans for a US$123M state-owned grain terminal at the Port of Gdansk in a bid to strengthen the country’s food security, Lloyds List reported.

Polish Prime Minister Donald Tusk was quoted in the 3 December report as saying a new terminal was required due to the influx of grain from Ukraine since Russia invaded the country in 2022. The port handled 52% more grain in the first half of 2023 compared to the same period in 2022, when Russia invaded Ukraine.

In February 2024, Polish farmers held a

IN BRIEF

URUGUAY: Global agribusiness giant Louis Dreyfus Company (LDC) has acquired a grain and oilseeds storage facility in Nueva Palmira for an undisclosed sum after operating the warehouse for six years.

The acquisition consolidated LDC’s position in a strategic agricultural area 2.5km from Nueva Palmiraport, Uruguay’s main grains and oilseeds export terminal, LDC said on 3 December. With a static storage capacity of 38,000 tonnes and additional capacity of 12,000 tonnes in silo bags, LDC said the facility could store and condition a range of crops, including soyabeans, wheat, rapeseed and carinata, with plans to store camelina.

EGYPT: Suez Canal toll revenues fell by 60% in 2024, a loss of U$7bn, amid Houthi attacks on shipping in the Red Sea, FreightWaves wrote on 29 December. Diversions away from the Red Sea around the Horn of Africa had pushed up shipping rates and journey times. Meanwhile, a dredging project to test two-way vessel transit (which would increase the waterway’s capacity) had been a success, the Suez Canal Authority said. Currently only some canal sections allow twoway transits via a parallel waterway opened in 2015.

large protest on the Ukrainian border, calling for an import ban on grain and oilseed from their Eastern neighbour, which they claimed had impacted prices.

A lack of port infrastructure meant much of the grain making its way across the Ukrainian border was staying in Poland, the BBC reported at the time of the protest.

Tusk said the terminal, expected to be operational by 2026, “will not only perform commercial functions but will be a safety device in the hands of the Polish state ... protecting Polish interests and farmers”.

Gdansk has several grain terminals in

operation, but these are privately run.

Meanwhile, Polish Minister of Infrastructure Dariusz Klimcza was quoted as saying the Port of Gdansk would invest more than US$98M in developing road and rail infrastructure and building additional warehouse storage.

In a May 2023 press release, the Port of Gdansk said more than 1.9M tonnes of grain (meal, corn, wheat, rye, fava bean, rapeseed, oilseeds) passed through the port’s quays in 2022, with shipments mainly going to the UK, Germany, Finland, Sweden, Norway and Belgium.

Privatisation for Paraguay-Paraná route

Argentina’s president Javier Milei is planning to privatise operations on the Paraguay-Paraná waterway (pictured right), a key shipping route in the region, The Guardian reports.

Announcing the decision on 19 November, cabinet chief Guillermo Francos said Argentina would no longer manage or maintain the waterway. A 30-year concession would involve a “major modernisation of the management of the waterway” which would “gradually boost international trade”, Francos was quoted as saying in the 21 November report.

At more than 3,400km long, the Paraguay-Paraná waterway is of strategic importance for Argentina and neighbouring Paraguay, Bolivia and southern Brazil, transporting soyabeans and grains overseas, with almost 80% of Argentine foreign trade channelled through it, The Guardian wrote.

Milei has pledged to privatise several state assets since taking office in December 2023.

BOLIVIA

PARAGUAY

Asunción

ARGENTINA

Paraná

Rosario

Buenos Aires

Paraguay

River Cáceres

BRAZIL

River Rio de la PlataRi

URUGUAY

Nueva Palmira

Bill proposes US purchase of Panama Canal

The US Congress has introduced legislation that would allow the USA to buy the Panama Canal, FreightWaves wrote on 10 January.

Introduced by US representative Dusty Johnson, the Panama Canal Repurchase Act 2025 would allow US President Donald Trump, in co-ordination with the secretary of state, to “initiate and conduct negotiations with appropriate counterparts of the government of Panama to reacquire the Panama Canal”.

“China’s interest in, and presence around, the canal is a cause for concern,” Johnson said.

Johnson pointed out that in 2018, Panama was the first country in Latin America to join China’s Belt and Road Initiative and Chinese-backed companies had managing rights for the two ports at each end of the canal, FreightWaves wrote.

“Without access to the Panama Canal, ocean shippers would be forced to travel 8,000 addi-

tional miles around South America,” he said.

According to US State Department data, 72% of all vessel transits through the canal are coming from, or destined for, US ports.

Panamanian President José Raúl Mulino has dismissed Trump’s claims of growing Chinese influence over the waterway and of higher fees being charged to US ships using it.

“The tolls ... are set in a public and open process in which clients and other actors participate,” Mulino said in a 26 December news conference.

Built by the USA, the Panama Canal opened in 1914. Connecting the Atlantic and Pacific oceans, the 82km waterway was administered by the USA until 1999, when control of the waterway was given solely over to Panama.

The USA is the largest user of the canal, including US grain and soyabean exports to Asia.

BIOTECH NEWS

IN BRIEF

CHINA: The Ministry of Agriculture and Rural Affairs has approved five gene-edited (GE) crops – including two soyabean varieties –and 12 genetically modified (GM) soyabean, corn and cotton varieties in a bid to boost high-yield crops, reduce reliance on imports and ensure food security, Reuters wrote on 31 December.

The ministry issued safety certificates for the 17 crops, valid for five years starting from 25 December, according to a document on its website on 31 December.

Approved varieties include seeds from Beijing-based feed group Dabeinong and China National Seed Group, a subsidiary of seeds and pesticides company Syngenta Group, according to the report.

In addition, China had authorised the import of an insect-resistant and herbicide-tolerant GM soyabean variety from German chemical and biotech firm BASF exclusively as a processing material, the ministry added.

Over the past year, the country had increased approvals for higher-yielding GM corn and soyabean seeds to raise domestic production and reduce grain imports, Reuters wrote.

China mainly imported GM crops such as corn and soyabeans for animal feed, while producing non-GM varieties for food consumption, the report said, adding that many Chinese consumers remained concerned about the safety of GM food crops.

Panel rules in favour of USA in GM corn dispute

A trade dispute panel has ruled that restrictions placed by Mexico on genetically modified (GM) corn exports from the USA violate the US-Mexico-Canada (USMCA) agreement, World Grain wrote on 23 December.

The three-member panel ruled in favour of all seven US legal claims, saying the restrictions were not based on science and violated the USMCA’s chapters on sanitary and phytosanitary measures and on market access.

The dispute started in 2020 when Mexico called for a ban of GM corn by the end of 2024, claiming it was harmful to human health.

After former Mexican President Manuel Lopez Obrador signed a decree banning GM corn imports in 2023, the US Trade Representative requested arbitration, challenging Mexico’s decree that immediately banned use of GM corn in tortillas and dough and the gradual elimination of

GM corn in other foods and in animal feed.

Following the panel decision on 20 December, Mexico’s economy and agriculture ministries issued a joint statement saying they were disappointed by the ruling but would respect it.

“The government of Mexico does not agree with the panel’s decision, as it considers that the measures in question are aligned with the principles of public health protection and the rights of Indigenous peoples,” the agencies said.

Mexico now had 45 days to bring its corn trade policies into compliance with the USMCA. Failure to do so under the trade deal’s rules could result in punitive duties on some exports to the USA, World Grain wrote.

Mexico accounts for almost 50% of total US corn export sales, importing some 17M tonnes/ year of US corn with a value of around US$3bn/ year, according to the report.

Bayer buys camelina germplasm and IP

German chemical giant Bayer announced on 9 January that it had acquired camelina (pictured) germplasm, intellectual property assets (IP) and materials from Canadian camelina company Smart Earth Camelina.

Bayer said it planned to develop the product further, using its expertise in oilseeds.

The acquisition's aim was to increase the supply of feedstocks to meet growing demand for low carbon fuels, including renewable diesel and sustainable aviation fuel (SAF).

“The acquisition of camelina germplasm from Smart Earth Camelina enables us to offer farmers a … low-carbon intermediate crop option,” Bayer’s crop science division’s head of

crop strategy, soya & biofuels, Jennifer Ozimkiewicz, said.

products for the pet and equestrian markets. Its camelina range includes a non-genetically modified variety resistant to group 2 herbicides.

▪ Bayer is working with Finnish renewable fuels producer Neste to develop a winter canola ecosystem in the USA to meet increasing demand for biomass-based renewable fuel feedstocks.

Adobe Stock

The firms expected to finalise a definitive agreement this year, Bayer said on 8 January, adding that it aimed to launch hybrid TruFlex winter canola in the USA in 2027.

TruFlex included Roundup Ready herbicide and pod shatter resistance technology to improve product stability and performance, Bayer said.

Corteva partners with bp to develop SAF feedstocks

US crop protection and seed producer Corteva and global energy giant bp have agreed to form a joint venture to develop crop-based feedstocks for sustainable aviation fuel (SAF) production.

The joint venture’s aim was to introduce new cropping systems to produce oil that met with EU Renewable Energy Directive (RED) III criteria, and qualified for US Low Carbon Intensity policy incentives, while

creating a new revenue stream for farmers, Corteva said on 18 November.

Corteva said it planned to form contracts with farmers in North and South America and Europe, to grow its mustard seed, sunflower and canola feedstocks for SAF production to progressively scale up volume to reach 1M tonnes/year of biofuel feedstocks for SAF production by the mid-2030s.

Emma Delaney, bp executive vice

president, customers & products, said the partnership – due to be finalised this year – would combine Corteva’s technology with bp’s refining and trading capabilities. Corteva Agriscience’s portfolio includes a range of crop protection products and seed treatments. Through its Pioneer Hi-Bred International subsidiary, it supplies genetically modified and genetically engineered seeds including canola and soyabean.

Calyxt says seedless hemp offered improved yields and quality

Sustainable Aviation Futures North America Congress

Marriot Marquis Houston, USA www.safcongressna.com

20-22 October 2025

Argus Biofuels Europe Conference & Exhibition London, UK www.argusmedia.com/en/events/ conferences/biofuels-europe-conferenceand-exhibition

22-25 October 2025

North American Renderers Association Annual Convention Ritz Carlton Bacara, California, USA https://convention.nara.org

6 November 2025

FOSFA Annual Dinner

La Quinta de Jarama, Madrid, Spain www.fosfa.org/news/events/

18-20 November 2025

MPOB International Palm Oil Congress and Exhibition (PIPOC 2025) Kuala Lumpur Convention Centre, Malaysia https://pipoc.mpob.gov.my/

EU/BIOFUELS

Industry snapshot

The European Union is one of the world’s leading biodiesel producers and consumers, with an industry worth around US$34bn/year

Gill Langham

Although historically the leading global producer of biodiesel – comprising both hydrotreated vegetable oil (HVO) and fatty acid methyl esters (FAME) – Europe’s dominance of the sector started to decline in the early 2020s with Asia overtaking it in output in 2022.

During that time, the EU biodiesel sector faced an increase in allegedly fraudulent imports from outside the bloc, an issue which it has had some success in mitigating.

Despite the challenges, the EU’s biodiesel sector is a robust industry worth around US$34bn (€31bn)/year, according to the European Commission (EC).

In addition, biodiesel production uses millions of hectares of EU arable land, forming an important part of Europe’s agricultural and energy economies, according to the European Biodiesel Board (EBB), the association representinig companies producing biodiesel in the EU.

Regulated in the current Renewable Energy Directive (REDIII), biodiesel allows the economic value of oilseed production and transformation to be maximised, providing additional income for farmers.

It encourages efficient use of existing resources, the association says.

In the near future, “intermediate crops” and cropping on degraded land will allow carbon farming to be combined with increased availability of sustainable feedstocks.

Production forecasts

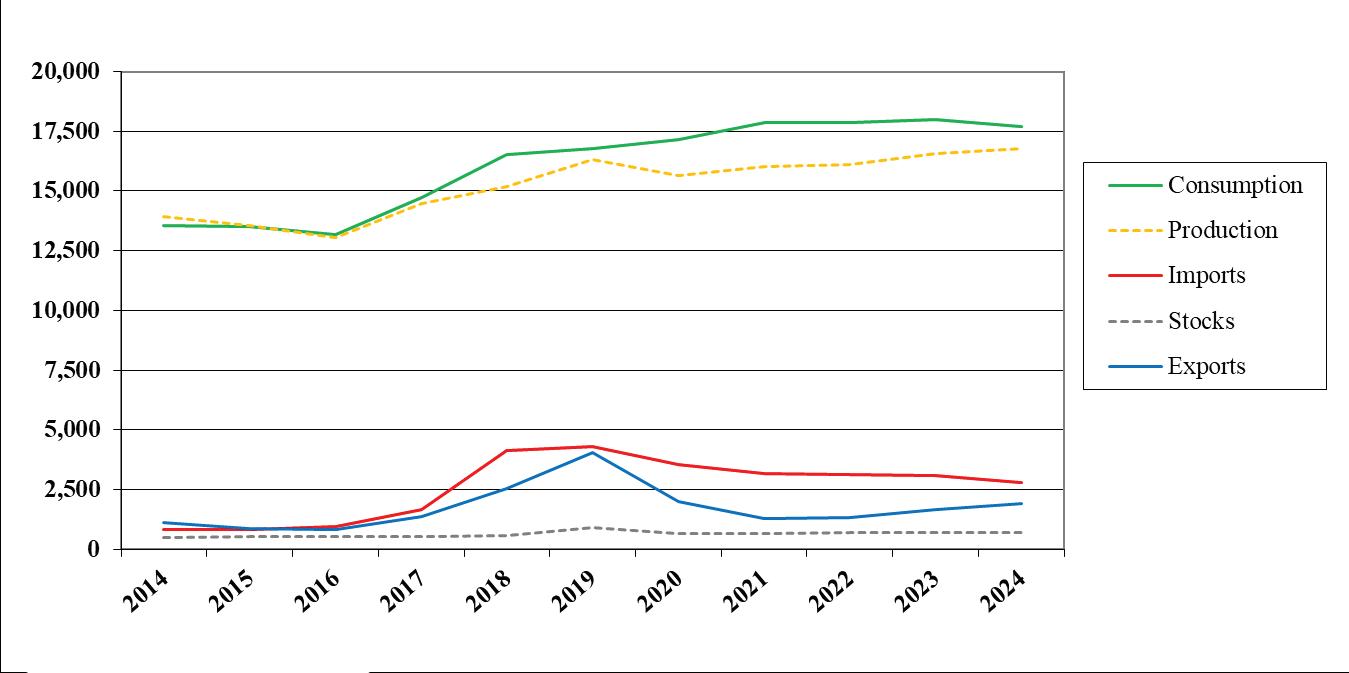

EU bio-based diesel (BBD) production is forecast to increase by 1.3% to 16.8bn litres in 2024, largely driven by strong demand from export markets such as the USA and the UK, according to the US Department of Agriculture (USDA)’s 13 August 2024 EU Biofuels Annual (see Figure 1, opposite page).

“Germany is the leading producer of biodiesel (FAME and HVO) with about 22% (2023) of production taking place in the country”, EBB secretary general Xavier Noyon says. “Next up is France with about 15% (2023). After that, it’s Spain and Italy with about 10%.”

Although some EBB members have sites in the UK, these are not considered EU production facilities, Noyon explains.

However, he says the industry – being as intertwined as it is– does its best to align policies and trade defence measures between the EU and the UK.

“Not just for the members that have production facilities in both, but also for the interest of the EU industry at large,” he adds.

Asia leads imports

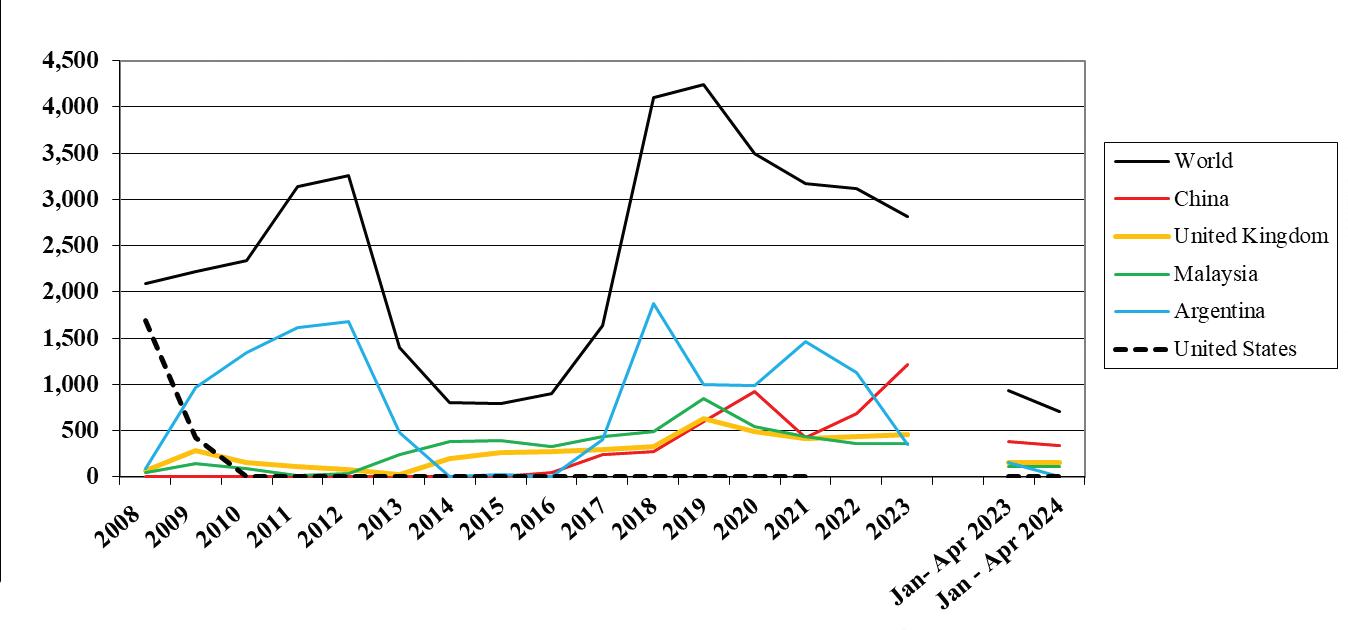

In 2023, the dominant suppliers of biodiesel to the EU were China, the UK,

Malaysia, Argentina and South Korea, accounting for 43%, 16%, 13%, 13% and 4% of EU biodiesel imports respectively, according to the USDA report (see Figure 2, p22)

Imports from China increased by 76% in 2023 compared to the previous year at the expense of shipments from Argentina and Indonesia.

According to an EBB-commissioned study by Stratas Advisors, Asia remains Europe’s primary source of biodiesel interregional imports, contributing 50% of the total from 2018-2023.

Despite a decline due to the COVID-19 pandemic between 2019-2021, imports from Asia increased consistently up to 2023, amounting to about 1.6M tonnes, a 29% year-on-year increase.

China represented over half of the region’s biodiesel exports to the EU, reaching about 0.9M tonnes in 2023, an 87% increase from 0.5M tonnes the previous year.

Latin America accounted for 29% of the EU’s total import volume between 2018 and 2023.

However, due to an unusual low-price environment for biodiesel in the EU, arbitrage opportunities have been limited.

This resulted in a severe decline in Latin American biodiesel import volumes to 0.4M tonnes in 2023, down 58% from the previous year, according to the study.

In contrast, non-EU countries emerged as the second-largest origin of biodiesel imports moving into the EU in 2023, totalling approximately 0.7M tonnes, with the UK representing 85% of total share.

Photo: Adobe Stock, AI generated

Anti-dumping duties on China

Against this backdrop and prompted by an anti-dumping complaint filed by the EBB, the EC launched an investigation in December 2023 into allegations that biodiesel imports from China were coming into the region at artificially low prices.

Germany had already asked the EC earlier in 2023 to investigate shipments from China amid industry concerns that imported biodiesel declared as based on recycled feedstock could contain cheaper oils, according to Reuters

“EU producers claim these imports are seriously harming their industry because they cannot compete with such low prices,” the EC was quoted as saying in a statement at the time.

The EC announced in July 2024 it would impose provisional anti-dumping duties on Chinese HVO and FAME imports, ranging between 12.8% and 36.4%.

Following the introduction of the antidumping duties, EU imports of biodiesel from China fell by 91% to 9,835 tonnes in July, compared to 109,457 tonnes in June – the lowest level since April 2021, according to Eurostat data.

In January this year, EU national governments approved the definitive duties on biodiesel (HVO and FAME) from China, set to be implemented for five years.

While welcoming the decision, the EBB said the protection against Chinese biodiesel imports was not perfect and there was still work to do to ensure the proper implementation of the duties and their efficiency.

“It has been a long journey since the EBB started this case, through first the circumvention case and later this antidumping case.

“After Indonesia, Argentina and the USA, we now have measures in place against China,” EBB’s Noyon says.

“It will be crucial to monitor the evolution of all biodiesel imports particularly in light of the recent Chinese export tax on used cooking oil (UCO). We will also closely monitor for circumvention as there are no duties imposed on sustainable aviation fuel (SAF), and the fact that some companies received lower anti-dumping duties than others.”

Indonesian biodiesel

Prior to the investigation into Chinese biodiesel imports, the EU launched a probe in 2023 into Indonesian biodiesel producers circumventing duties by transshipping their product via China and the UK.

The EU probe was also prompted by an

investigation by the EBB, which estimated that the circumvention practices could have cost the EU around €221M ($US241M) in 2022 alone.

The EU first imposed tariffs on Indonesian biodiesel in November 2019 to counter subsidies given to producers in the country.

On 14 December 2022, the European General Court (EGC) upheld the imposition of these tariffs, which ranged from 8-18%.

On 17 October 2024, the Court of Justice of the EU (CJEU) rejected the appeal by Indonesian exporters PT Pelita Agung Agrindustri and PT Permata Hijau Palm Oleo against the 2022 EGC decision, putting an end to four years of litigation.

“The ruling marks a new milestone for EBB in its long and continuous battle to fight against unfair imports of biodiesel and restore a level playing field in the EU,” EBB’s Noyon said at the time.

Noyon said the EBB has been fighting against unfair competition for more than 16 years.

“The EBB remains committed to fight against any unfair trading practices that could jeopardise the full development of the EU biodiesel industry,” he added.

Top EU exporters

According to figures published by the German Federal Statistical Office, Germany exported around 1.7M tonnes of biodiesel in the first half of 2024 while imports totalled 906,719 tonnes.

The Netherlands continued to be Germany’s primary trading partner, accounting for 47% and 52% of total exports and imports respectively.

It was the third consecutive year of increased Dutch imports, the report said.

The main importers of German biodiesel were EU countries, headed by the Netherlands, Belgium, Poland, Austria and France.

According to research by Agrarmarkt Informations-Gesellschaft, imports also increased from Malaysia and Belgium, while imports from Poland, Finland and Austria were lower than the previous year’s volumes.

Although US imports dropped around 46% to just under 131,000 tonnes in the first half of 2024, the USA was the most important non-EU country for shipments from Germany.

Domestic consumption

Bio-based diesel consumption in the EU is driven almost exclusively by member state blending and greenhouse gas (GHG) reduction mandates and, to a lesser extent, by tax incentives, according to the USDA’s EU Biofuels Annual

Mandates were raised from 2023 to 2024 in Austria, Finland, Germany, Ireland, Italy, Lithuania, the Netherlands, Poland, Portugal, Slovakia, Slovenia and Spain, while Sweden lowered its mandates substantially. In all other countries, the mandates remained the same as in 2023.

In 2024, EU BBD consumption was expected to decrease by 1.6% to 17.7bn litres, mainly due to Sweden’s drastically reduced mandate from 30.5% in 2023.

Additional minor reductions in consumption were forecast for Greece, Romania and Denmark.

The largest increase in consumption was forecast for Germany due to a greenhouse gas (GHG) reduction mandate and the approval of B10 and HDRD100 in May 2024.

Positive effects from increased mandates were also forecast for consumption in Ireland, the Netherlands, Italy, Bulgaria and Hungary.

Feedstocks

As there is no official data on biodiesel, HVO and SAF feedstock use in most EU member states, the USDA says the figures

Figure 1: EU supply and demand of bio-based diesel (million litres)

EU/BIOFUELS

and analysis in its EU Biofuels Annual were based on Foreign Agricultural Service (FAS) EU estimates.

u sunflower oil accounted for only 1.7% of the total biodiesel feedstock in 2023. It is mainly used in Greece and Bulgaria – together accounting for 59% of EU sunflower-oil based biodiesel production.

“In recent years, EU biofuel producers have substantially diversified their feedstocks away from crop-based vegetable oils towards waste oils and fats,” the USDA says.

According to the report, this trend was driven by the eligibility of some waste materials for double counting in some member states and, more recently, the phase out of palm oil which is due to be completed by 2030.

“As a result, over the course of the 10 years covered in this report, the share of virgin vegetable oils – rapeseed oil, soyabean oil, palm oil and sunflower oil – in the feedstock mix has decreased from 72% in 2015 to 52% in 2023 and is forecast to drop to 50% in 2024,” the USDA says.

Rapeseed oil remains the primary feedstock, accounting for 41% of total BBD feedstock use in 2023, according to the report.

For 2024, rapeseed oil use is forecast to increase by 1.6% as the phase-out of palm oil progresses, the USDA says.

Palm oil use as a feedstock has been in “sharp and steady decline” since 2020 and its phase-out is nearly complete after years of growth and an estimated record use of 2.6M tonnes in 2019.

“By 2023, palm oil use had dropped to 240,000 tonnes and only accounted for 1.5% of total feedstock,” the USDA says.

In 2024, palm oil use was forecast to decline by a further 57%, contributing less than 1% to the EU feedstock mix.

After rapeseed oil, UCO was the second most important feedstock in 2023, accounting for 24% of total feedstock, with soyabean oil third in terms of use, accounting for 8%.

According to the USDA report,

Smaller volumes of sunflower oil are also used in France, Hungary, Poland, Romania and Lithuania.

Although at a low level, the share of soyabean oil is stable and its consumption is concentrated in a few EU countries, such as Spain, which has not introduced a ban on its use for biodiesel production, according to the USDA report.

While a large share of EU soyabean oil is crushed from imported soyabeans, most of the rapeseed oil is of domestic origin, the report says.

Shifts in feedstocks

The feedstock for production of EU biodiesel is expected to continue to shift to residues and waste as a result of increasing mandates for advanced biofuels, and to rapeseed due to good availability from 2023/24, according to the European Commission report Short-term Outlook for EU agricultural markets in 2024.

Due to sustainability concerns, palm and soyabean oil supply are expected to decline further.

Meanwhile, demand for UCO is expected to stabilise after significant growth in its use in recent years, the report says.

According to the EBB’s Noyon, the allocation of different feedstocks in the EU production of biodiesel (HVO and FAME) remains relatively stable.

“Overall, you could say the use of Annex IX* feedstocks is increasing and, in particular, we would point out an increase in palm oil mill effluent (POME).

“In the feedstock use for FAME production, there is a trend towards balanced allocation between crop-

based and Annex IX (a and b combined). HVO production in Europe remains predominantly Annex IX based.”

Outlook

With the USDA forecasting rising demand from export markets such as the USA and the UK, the EU biodiesel sector is expected to remain strong.

Growth is expected to be driven by a combination of environmental concerns and government directives to increase the use of renewable energy sources in the transport sector and reduce GHG emissions.

“According to Eurobarometer surveys, over the past five years, the cost of living and climate change have consistently featured in the five most important issues facing the EU,” Noyon says. “This confirms that the EU cannot afford to choose between climate and the economy; between sustainability and affordability –we must do both.”

Challenges ahead

Although approximately one-third of all energy is used in transport – making the sector the largest final energy consumer in the EU – transport is still lagging in terms of decarbonisation, he adds.

“About 90% of fuels used in transport are fossil-based. There is a drive in demand for sustainable alternatives.

“In about six years’ time, at least 29% of the final consumption of energy in the transport sector must be renewable, or we need to achieve a 14.5% reduction in GHG intensity. It’s a key target of the Renewable Energy Directive.”

With the road sector accounting for 74% of all transport energy use, the RED sets out clear mandates for road decarbonisation up to 2030.

However, post-2030 mandates have not been set out, Noyon says.

“That means: no targets for biofuels in road transport. No certainty for business or investors. And no clear strategy to decarbonise the biggest energy user.”

Looking at the wider picture, Noyon says the effect of ReFuel Aviation and Maritime regulations introduced to drive the uptake of renewables in these hardto-abate sectors have to be factored in.

Additionally, the effects of the EU carbon trading Emissions Trading System II to address CO2 emissions from fuel combustion in the road transport, buildings, energy, manufacturing and construction industries should not be underestimated, he adds. ● Gill Langham is the assistant editor of OFI *Annex IX is the EC’s approved list of sustainable biofuel feedstocks

Figure 2: EU biodiesel imports (million litres)

Source: USDA Foreign Agricultural Serive (FAS) EU posts based on data from Trade Data Monitor

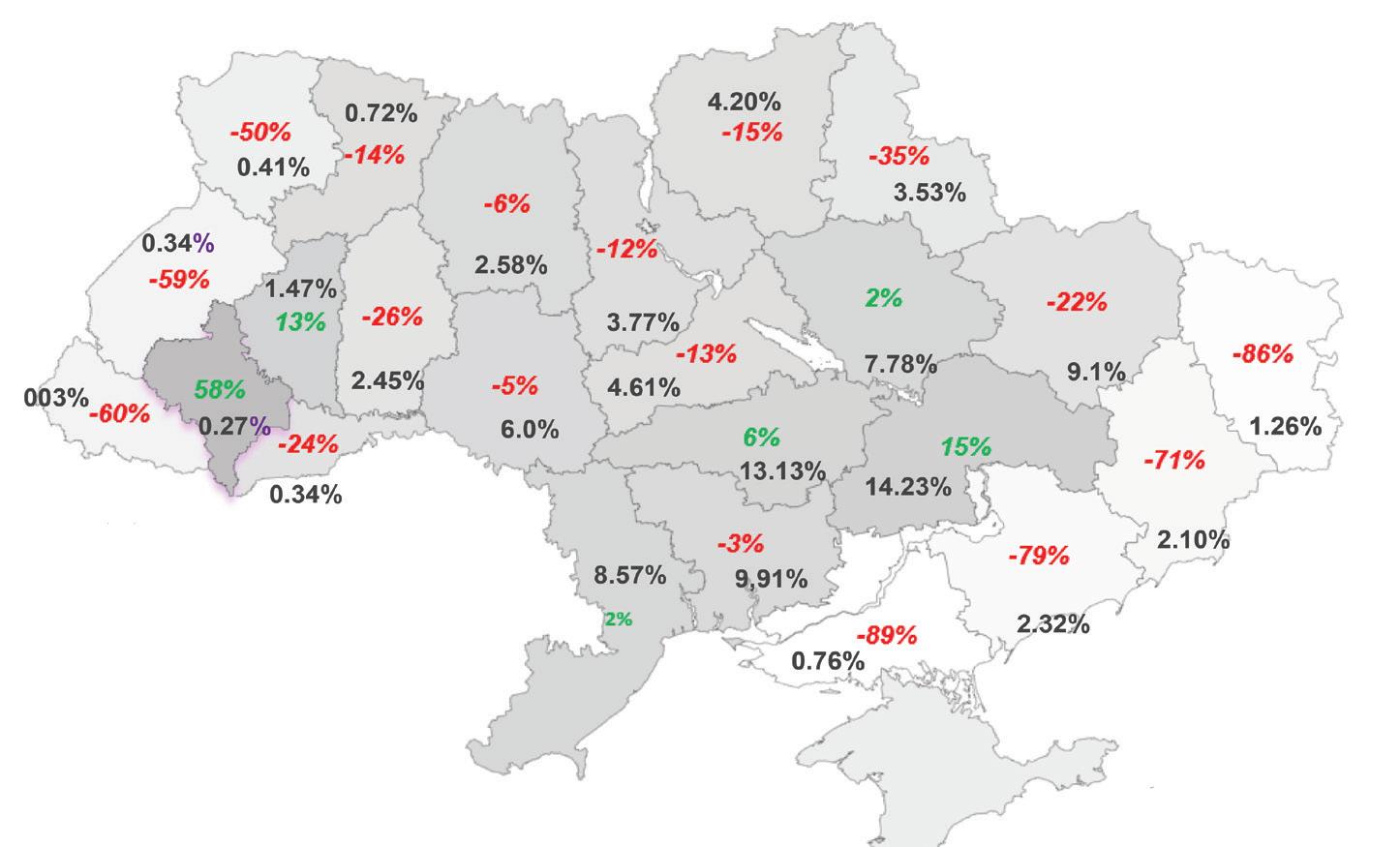

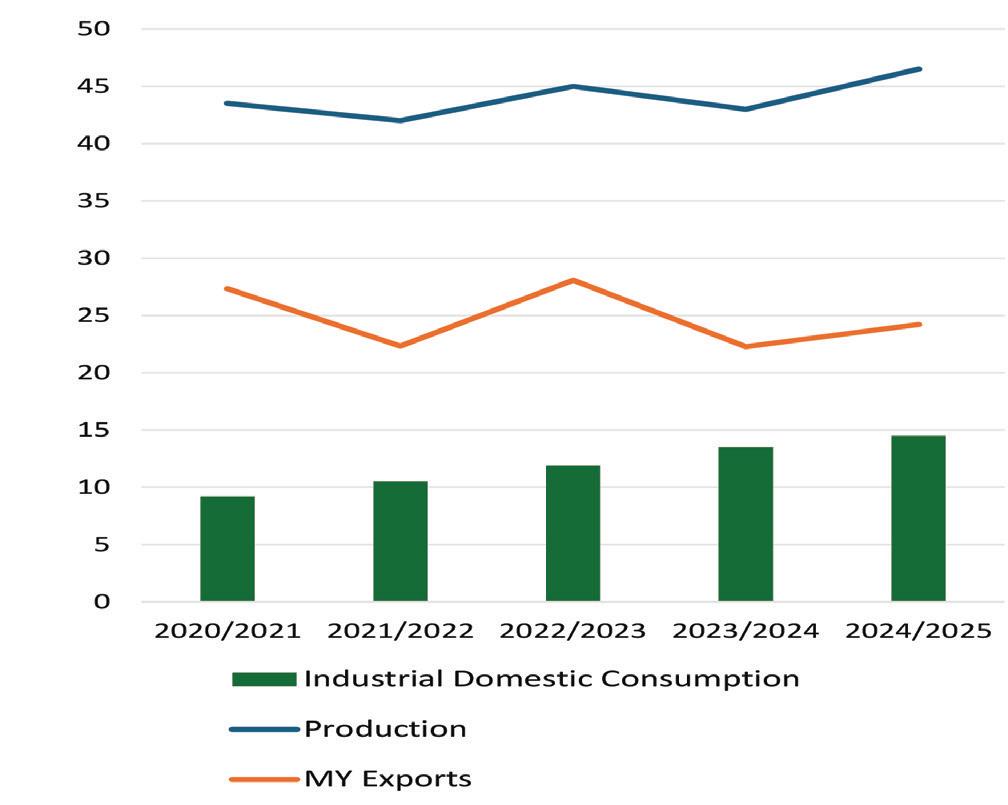

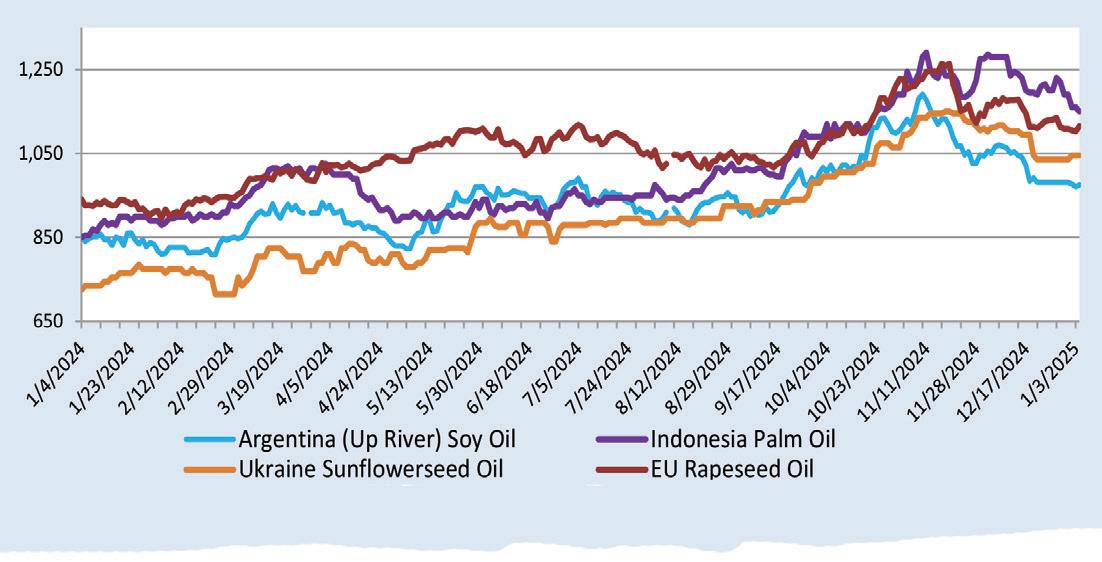

Black Sea update Black Sea update

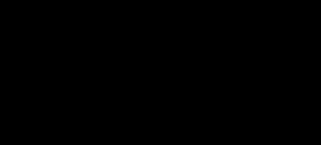

The Black Sea countries of Ukraine and Russia account for almost 78% of world sunflowerseed production, the Grain Academy 2024 conference heard in Bulgaria on 31 October last year.

In 2023/24, world sunflowerseed production totalled 56.1M tonnes with Russia accounting for 17.1M tonnes, Ukraine with 15.5M tonnes, the EU with 10.1M tonnes, Argentina with 3.9M tonnes and Turkey with 1.6M tonnes, Anna Platonova, senior vegetable oil market price reporter at Fastmarkets, told the conference.

In 2024/25, global production is forecast at 50.5M tonnes, according to the US Department of Agriculture (USDA). The Russian share is projected at 16.6M tonnes and Ukraine’s at 12.9M tonnes.

Russia and Ukraine account for nearly 80% of sunflowerseed production and close to 60% of sunflower oil output globally. Their ongoing war continues to impact Ukraine’s land bank and export logistics but new EU tariffs on Russian grain and oilseeds may open up opportunities for Ukrainian products

Meanwhile, Romania and Bulgaria have had their lowest sunflowerseed harvest for at least 10 years, with estimated Romanian production of 1.8M tonnes and 1.45M tonnes for Bulgaria, Platonova said (see Figure 1, below).

Ukraine

Agricultural products are Ukraine’s most significant exports, accounting for about

41% of the country’s shipments, according to a World Grain report in November. Wheat, corn and sunflower oil comprising its top three commodities.

“The agriculture industry is the third largest contributor to Ukraine’s economy and has been a primary military target for Russia,” the report said. “In addition to taking land, Russia has blockaded key Ukrainian Black Sea ports to stop grain exports and stolen machinery and crops.”

Damage and losses to the agriculture industry from the war, which began in Feburary 2022, had exceeded US$80bn by the end of 2023, with rebuilding expected to cost US$56.1bn and an additional US$32bn for demining, the report said, quoting the European Parliamentary Research Service (EPRS).

The EPRS said Ukraine was well suited for agriculture production with a third of the world’s most fertile land. “The nation is mostly flat, and the primary weather is moderate continental with a temperate climate and adequate rainfall. It has an abundant supply of water with several large rivers, more than 3,000 lakes and 1,100 artificial water reservoirs.”

However, the World Grain report said Ukraine’s amount of arable under its

Photo: Adobe Stock

control has dropped to 26.5M ha from 32.7M ha since the Russian invasion.

Platonova told the conference that according to various estimates, Ukraine’s arable area had fallen by 30% from 40M ha to 27M ha due to military action in the east and southeast of the country and the presence of mines.

Ukraine used to lead sunflowerseed production in the Black Sea before its invasion by Russia, she said.

In 2021/22, Ukraine produced 17.8M tonnes of sunflowerseed compared with 16.07M tonnes by Russia (see Figure 1, previous page). It had since fallen behind Russia in 2022/23 and 2023/24.

Climate change in the last six years had made the country’s western and southern regions increasingly suitable for sunflower cultivation, she said (see Figure 3, p26).

Due to the lower profitability of grain and more expensive logistics, a growing number of farmers were interested in sowing sunflower and other oilseeds.

The USDA Foreign Agricultural Service (FAS) said Ukraine’s total grain production in 2023/24 was estimated at 60.1M tonnes, up from 54.6M tonnes in the previous marketing year, but “grain production has remained unprofitable since Russia’s invasion and this is expected to translate into a decreased grain area for 2024/25”.

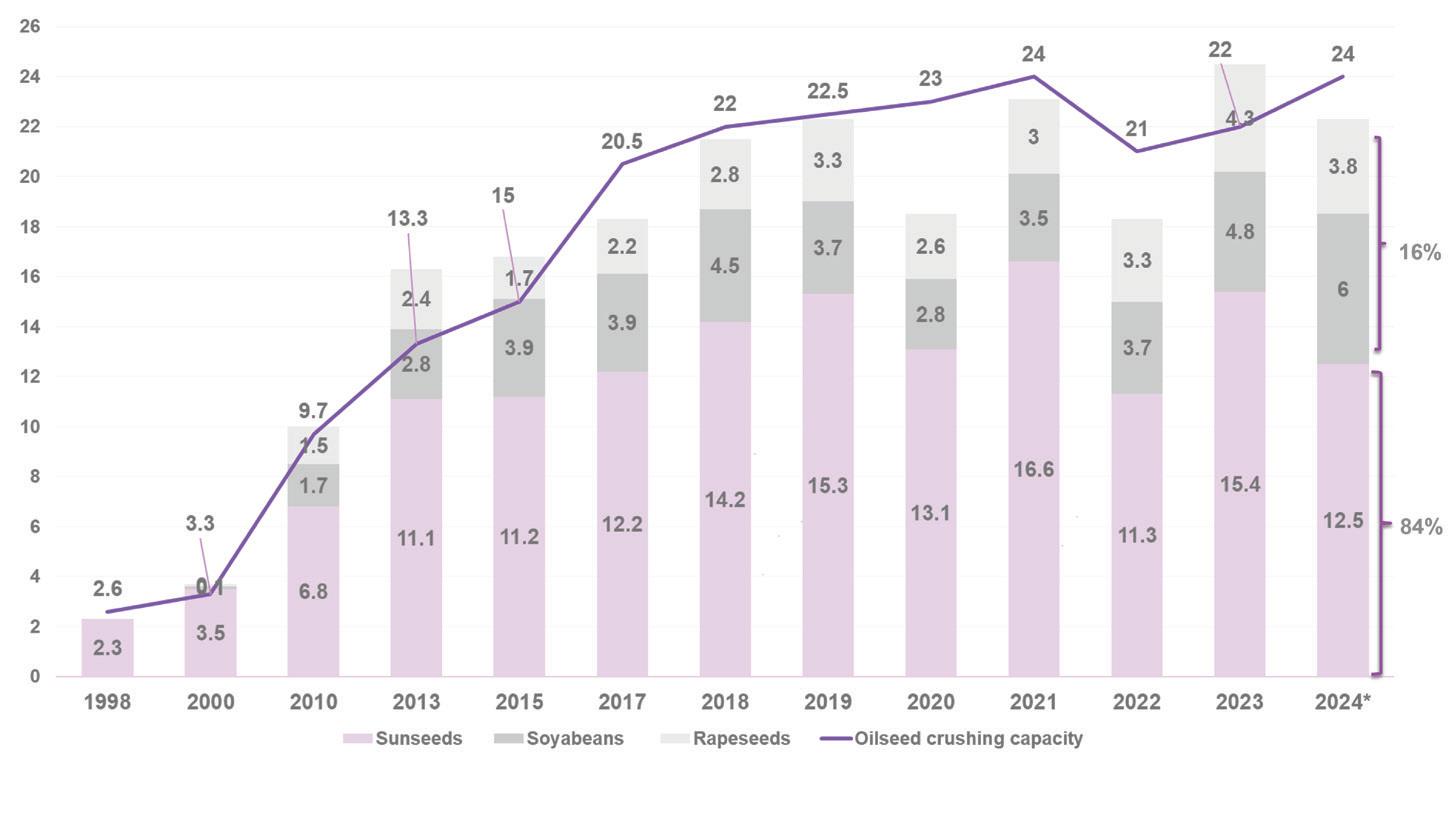

Platonova told the conference that Russian occupation and the destruction of plants had caused oilseed processing capacity to fall by 12.5% in 2022 to 21M tonnes but the construction of new processing plants had now raised capacity to 24M tonnes, of which 84% was for sunflowerseed crushing (see Figure 4, p26).

However, sunflowerseed crushing for the 2024/25 season is expected to fall by at least 11.5% to 12.3M tonnes.

Meanwhile, sunflowerseed prices in Ukraine reached a three-year high in November 2024 at UAH 27,200 (US$633)/tonne. Sunflowerseed prices

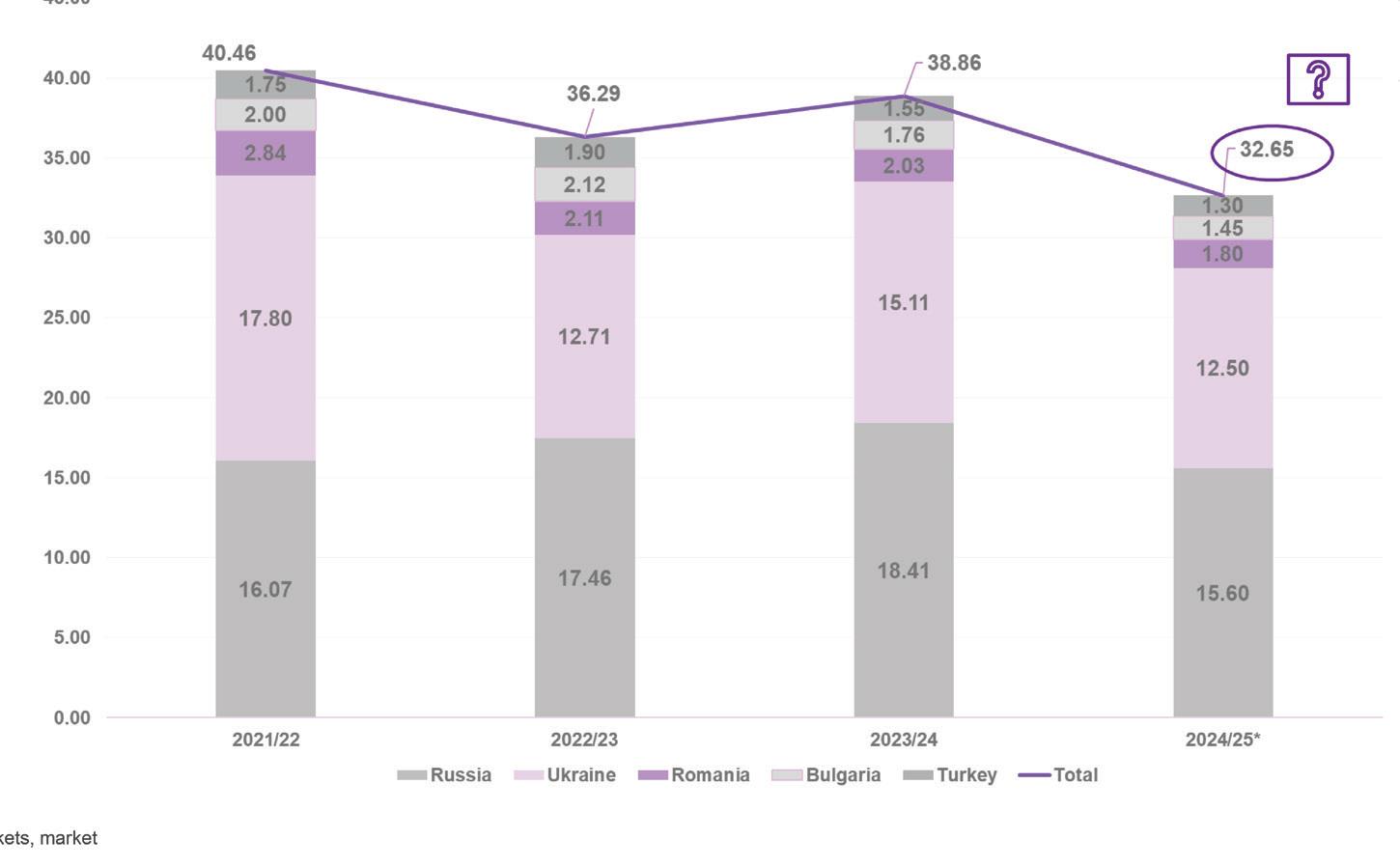

Figure 2: Monthly Ukrainian sunflower oil exports by mode of transport

u

SUNFLOWERSEED & OIL

in Russia also reached a two-year high in October 2024 to a level of 97,23100 ruble (US$477.97/tonne), she said. Russia’s sunflowerseed production is expected to reach 15.6M tonnes in the 2024/25 season, with crushing expected to fall by at least 14% compared with 2023/24 to total 15.9M tonnes.

Sunflower oil

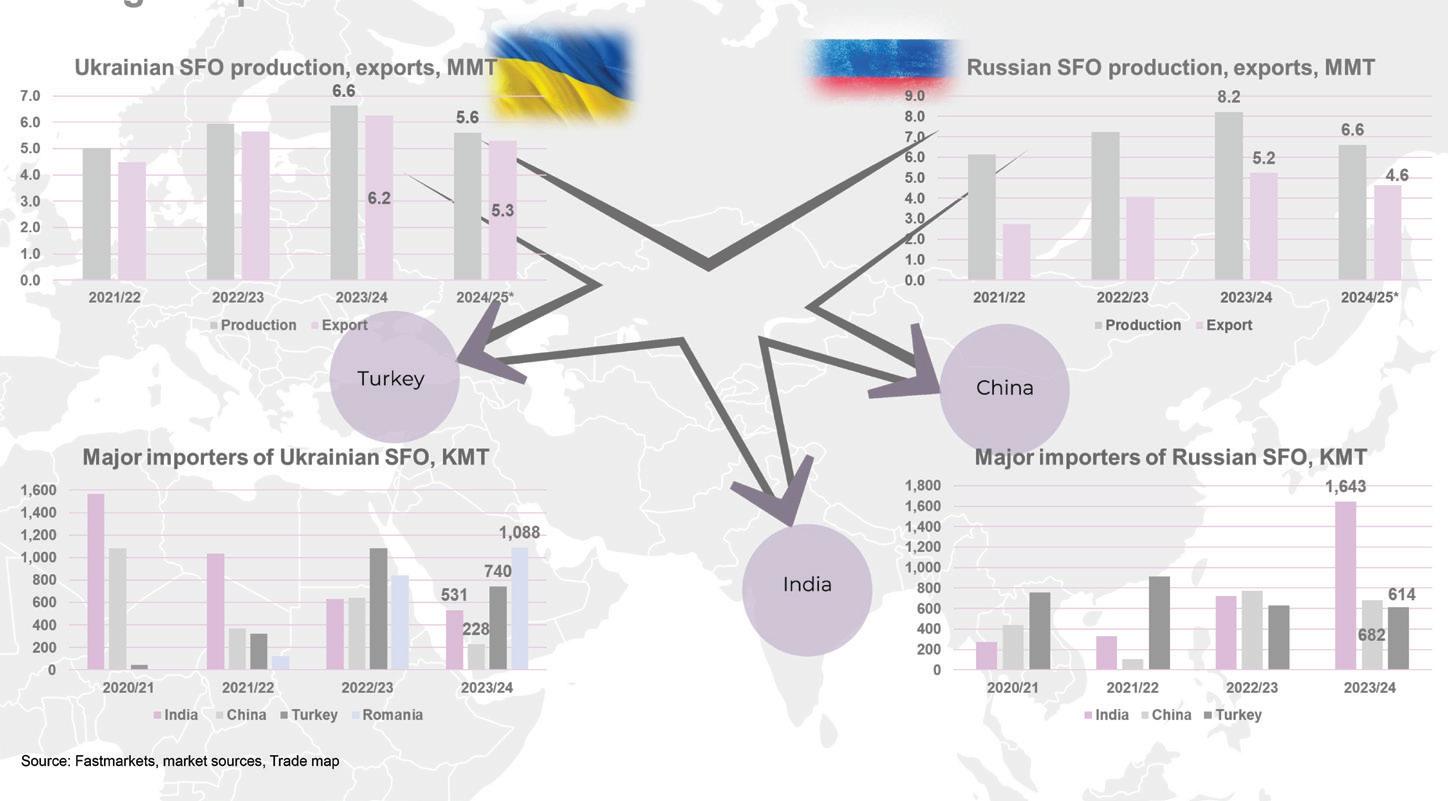

Ukraine and Russia produce nearly 60% of sunflower oil globally. In 2023/24, global sunflower oil production was 22.1M tonnes. For 2024/25, world sunflower oil production is projected at 20M tonnes, with Russia accounting for 8.2M tonnes and Ukraine 6.6M tonnes.

Black Sea sunflower oil prices rose by at least 15.5% at the start of the 2024/25 marketing year, with Ukrainian oil priced some US$50/tonne above Russia’s.

Source: USDA, APK-Ukraine, market sources

The EU and Asia drive global demand for sunflower oil production, with China, the EU, India and Turkey leading imports (see Figure 5, left).

Through EU Solidarity Lanes, the Black Sea Initiative and most recently the Ukrainian Corridor, Ukraine has managed to keep its economy afloat and export commodities, the World Grain report said.

Currently, around 83% of Ukraine’s sunflower oil exports travel by sea, and 6% by railway. This compares with 22% by sea in March 2022, following Russia’s invasion (see Figure 2, previous page).

There is strong competition between Ukraine and Russia for a share in the global sunflower oil market (see Figure 5, left), Platonova told the Grain Academy conference. Ukrainian exports to the EU may also benefit from EU tariffs on Russian grains and oilseeds, which came into force on 1 July, she said.

The tariff rate is €95 (US$102.76) per tonne for cereals and 50% of their value for oilseeds, Aljazeera reported on 30 May.

Belgium finance minister Vincent Van Peteghem, who holds the rotating presidency of the EU, said in the Aljazeera report that the new tariffs were intended to stop imports of grain from Russia and Belarus into the EU “in practice”.

“These measures will, therefore, prevent the destabilisation of the EU’s grain market, halt Russian exports of illegally appropriated grain produced in Ukrainian territories and prevent Russia from using revenues from exports to the EU to fund its war of aggression against Ukraine.“

Outlook

The main factor impacting Black Sea oilseed production in 2024/25 is the ongoing war in Ukraine, with restrictions on the country’s electricity use and possible black-outs, Platonova told the Grain Academy conference.

Lower sunflowerseed supply is expected, with high competition for the crop between crushes. Soyabean and high oleic sunflowerseed processing are expected to rise due to the sunflowerseed shortage.

Ukraine and Russia will continue to compete for the Asian sunflower oil and meal market. And there will be opportunities for Ukrainian products on the European market due to the introduction of EU duties on Russian and Belarusian oilseeds and their processed products, she said. ●

Figure 3: Changes in areas under sunflowerseed in Ukrainian regions, 2021-2024

Figure 5: Competition between Ukrainian and Russian sunflowerseed oil

Ukraine SFO production, exports, MT

Major importers of Ukraine SFO, KMT

Major importers of Russia SFO, KMT

Russia SFO production, exports, MT

Insuring against risk

The global shipping of commodities including oils and fats can create issues before, during and after shipment, which makes it critical for sellers and traders to consider their insurance risk

Yavor Velchev

In today’s volatile world of global commodity shipping, the importance of risk management and protection is more critical than ever to ensure the sustainable supply of food across the world.

While trading contracts and insurance policies have been refined over decades to clearly define the obligations and responsibilities of all parties, the adage “good from far, far from good” often holds true when unexpected circumstances arise.

Such situations introduce variables that challenge the application of insurance coverage.

The unique factors surrounding each case – freight fixture, vessel chartering, sale and purchase agreements, warehouse arrangements, pre-loading surveys, and unplanned casualties – can create complexities in commodity shipments.

Even the most robust free on board (FOB) contracts may fall short in providing sufficient protection to sellers.

FOB is an international commercial term that defines when a seller’s responsibility for goods ends and the buyer takes over.

The seller is responsible for delivering goods to the port of departure, clearing them for export and loading them on the

vessel. The buyer is responsible for all costs after the goods are on the vessel. This article explores scenarios that can arise during shipping and highlight why it is crucial for prudent oilseeds, oils and fats traders to consult their risk advisers and insurance consultants before signing off on the next contract sale.

Breaking down the risks

Risks can be broken down into before, during and after shipment.

Risks before shipment

The primary risks before shipment include hidden loss or damage to the goods.

• Loss refers to the quantity of goods, potentially leading to quantity-related claims.

• Damage refers to the condition of the goods, often causing disputes over quality.

Hidden loss or damage implies that goods may appear acceptable before shipment but reveal issues upon arrival, creating false confidence for both sellers and buyers. Inadequate or nonexistent surveys at the loading stage can exacerbate these risks, leading to

Photo: Adobe Stock, AI generated

disputes about whether the seller fulfilled contractual obligations. Buyers’ insurers may even seek subrogated recovery against the seller in such cases.

To address these risks, insurance markets offer tailored solutions, such as pre-shipment insurance cover. Risks “at storage” (such as bad packing, theft or improper storage) and “en route to ship” (including delays, port closures or strikes) can also jeopardise goods before shipment.

Risks during loading

Loading presents a dynamic risk phase where the responsibility transitions from the seller to the carrier or buyer.

A significant shift occurred with the introduction of the International Chamber of Commerce (ICC) Incoterms 2010, a set of rules that define the responsibilities of buyers and sellers in international trade.

The rules define the terms and conditions for selling physical goods that need to be transported and establish who is responsible for arranging and paying for transport, import and export procedures, and insuring goods

The omission of the term “ship’s rail” in the Incoterms 2010 rules represented a significant shift in how responsibilities are allocated between buyers and sellers in sea freight transactions.

“Ship’s rail” traditionally marked the point where risk and responsibility for the goods would transfer from the seller to the buyer. This could be a literal rail of the ship or a symbolic point at which the buyer assumed liability for the goods once they were loaded on board.

In previous Incoterms rules, terms like FOB and CFR (cost and freight) were defined in relation to the “ship’s rail,” meaning the seller’s responsibility ended when the goods crossed this physical point on the vessel.

However, in Incoterms 2010, the term “ship’s rail” was removed. For example, FOB no longer refers to the moment when the goods pass the ship’s rail, but when they are loaded on board the ship.

This reduces ambiguity so that the exact moment of transfer is clearer, rather than relying on a physical feature like the ship’s rail, which can vary between vessels or be ambiguous in certain situations.