TEXAS REAL ESTATE RESEARCH CENTER

TEXAS REAL ESTATE RESEARCH CENTER

TEXAS A&M UNIVERSITY

TEXAS A&M UNIVERSITY

Summer 2023

TM

TEXAS A&M UNIVERSITY

Texas Real Estate Research Center

COLLEGE STATION, TEXAS 77843-2115

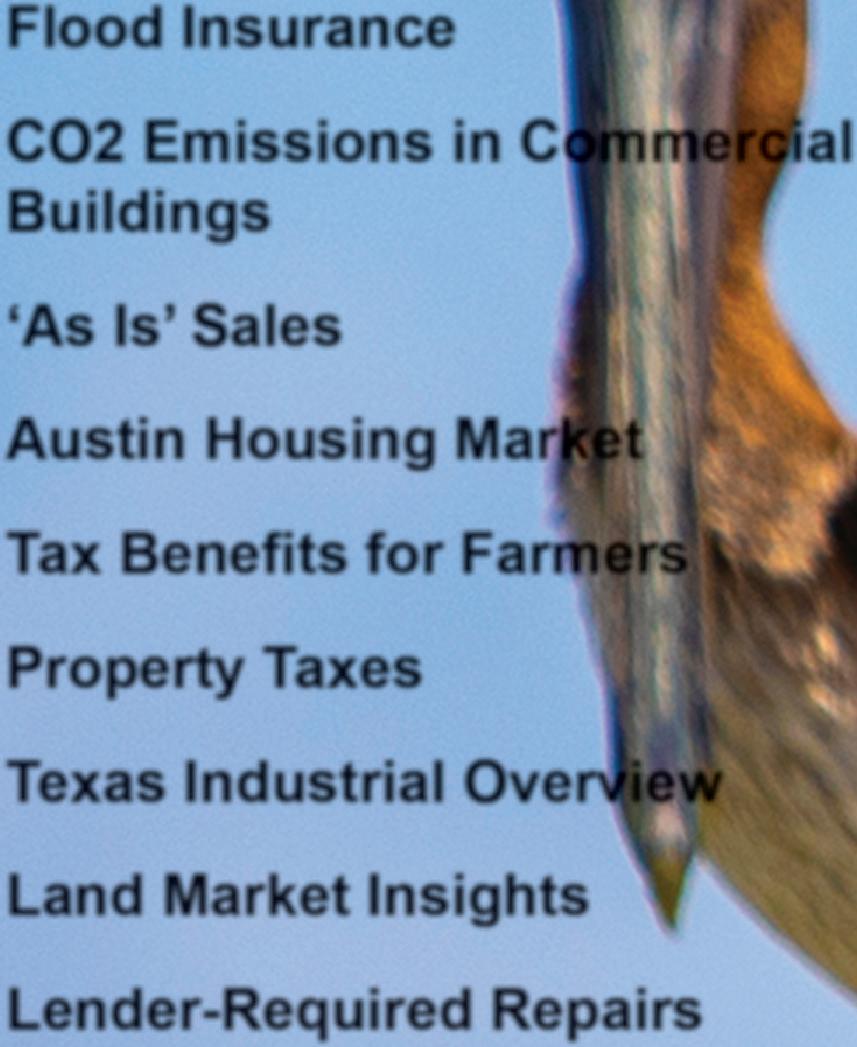

In This Issue

Flood Insurance

CO2 Emissions in Commercial Buildings

‘As Is’ Sales

Austin Housing Market

Tax Benefits for Farmers

Property Taxes

Texas Industrial Overview

Land Market Insights

Lender-Required Repairs

Helping Texans make the best real estate decisions since 1971

TEXAS REAL ESTATE RESEARCH CENTER

TEXAS REAL ESTATE RESEARCH CENTER

TEXAS A&M UNIVERSITY

TEXAS A&M UNIVERSITY

Summer 2023

TM

iii

you’re

Available on our website. . . . read our LandOccupier’sLiability Guide.

inviting friends to enjoy the great outdoors at your place . . . TR TECHNICAL REPORT MAY 2023 2380 Texas Real Estate Research Center Rusty Adams Research Attorney Land Occupier’s Liability Guide

Learn how you could be held liable for an injury that occurs on a piece of land you occupy—even if

not the landowner.

Before

Commercial’s Carbon Conundrum

Carbon-dated? Not quite, but CO2 emissions could soon impact the fate of aging buildings. By

Harold D. Hunt and Bucky Banks

Harold D. Hunt and Bucky Banks

2 | Come Rain or High Water

Flood, Water Damage, and the Homeowners’ Insurance Policy

With recent deluges, Texans need to check more than their rain gauges. Insurance needs and policy coverages should be on the radar as well. By

Richard Rudolph

8 | Navigating ‘As Is’ Sales

When it comes to an “As Is” home sale, what the buyer sees is what the buyer gets, right? Actually, it’s not as simple as that. Here’s what you need to know to help your client sell that fixer-upper. By

Kerri Lewis

10 | Austin’s Power

Why the Capital City’s Home Prices Surged

The city that flaunts its reputation for being “weird” has become a major destination city for technology and science-based companies. That, along with other factors, has taken its toll on area home prices. By

Joshua Roberson and Mallika Natarajan

18 | Texas’ Property Tax Puzzle

23 | A Bumpy Ride

Mostly ‘Ups’ for Texas Industrial Markets

Over the past four decades, the state’s industrial markets have had more ups and down than the Texas Giant. But geographic patterns emerge when you take a closer look at individual markets.

By Daniel Oney

26 | For Land’s Sake

Texas Land Market Outlook and Issues

The Center’s Outlook for Texas Land Markets conference has always yielded a bumper crop of practical insights and takeaways for landowners, and this year was no different.

Greener Pastures

Tax Benefits for Farmers

Attention, investors: That large piece of rural land you just purchased could be rich with potential tax benefits . . . provided you don’t mind a little thought, planning, and getting your hands dirty. By William

Executive Director, GARY W. MALER

Operations Director, PAMELA CANON

Research Director, DANIEL ONEY

Senior Editor, BRYAN POPE

Associate Editor, KAMMY BAUMANN

Creative Manager, ROBERT P. BEALS II

Graphic Specialist/Photographer, JP BEATO III

Graphic Designer III, ALDEN DeMOSS

Communications Advisor, DAVID S. JONES

Circulation Manager, MARK BAUMANN

Lithography, RR DONNELLEY, HOUSTON

D. Elliott

Texans want tax relief, but attempted solutions in other states have had unintended consequences. This report explains the factors that are at play as the Texas Legislature looks for some middle ground. By

Charles E. Gilliland and Lynn D. Krebs

28

|

Practically Speaking

Real Estate Questions Answered

The mortgage lender is requiring an outdated septic system be replaced before closing on a loan. The cost is expensive, and the option period has already ended. It’s enough to leave a buyer flushed with anxiety. But there are options. By

Kerri Lewis and Avis Wukasch

ADVISORY COMMITTEE: Doug Jennings, Fort Worth, chairman; Doug Foster, San Antonio, vice chairman; Troy C. Alley, Jr., Arlington; Russell Cain, Port Lavaca; Vicki Fullerton, The Woodlands; Patrick Geddes, Dallas; Besa Martin, Boerne; Rebecca “Becky” Vajdak, Temple; and Barbara Russell, Denton, ex-officio representing the Texas Real Estate Commission.

TG (ISSN 1070-0234) is published quarterly by the Texas Real Estate Research Center at Texas A&M University, College Station, Texas 77843-2115. Telephone: 979-845-2031.

VIEWS EXPRESSED are those of the authors and do not imply endorsement by the Texas Real Estate Research Center, Division of Academic and Strategic Collaborations, or Texas A&M University. The Texas A&M University System serves people of all ages, regardless of socioeconomic level, race, color, sex, religion, disability, or national origin. Nothing in this publication should be construed as legal or tax advice. For specific advice, consult an attorney and/or a tax professional.

PHOTOGRAPHY/ILLUSTRATIONS: Alden DeMoss, pp. 1 (top), 2-3, 4, 26-27; Robert Beals II, pp. 1 (bottom), 8; Center files, pp. 7, 10-11, 12-13, 14-15, 16-17, 18-19, 22, 23.

LICENSEE ADDRESS CHANGE. Log on to your Texas Real Estate Commission account to change your mailing address. © 2023, Texas Real Estate Research Center. All rights reserved.

SUMMER 2023 TEXAS REAL ESTATE RESEARCH CENTER

SUMMER 2023 VOLUME 30, NUMBER 3 www.recenter.tamu.edu @recentertx ON THE COVER: Brown pelicans perched at Port Bolivar ferry landing. Photographed by JP Beato III. 14 TM

5

Flood, Water Damage, and the Homeowners’ Insurance Policy

Homeowners should consider their insurance needs for the likely types of “water damage” loss that could occur, then read their policies carefully to understand what is and is not covered.

By Richard Rudolph

spray from any of these, whether or not driven by wind, (2) water or water-borne material which backs up through sewers or drains or which overflows or is discharged from a sump, sump pump, or related equipment,” or seepage.

According to the Insurance Information Institute, the second leading cause of homeowners’ claims is water damage and freezing. This type of loss accounts for 29 percent of claims, with an average claim paid of $11,097 in 2021.

Because water damage is the cause of nearly one-third of all homeowners’ claims, homeowners should understand what coverage is provided in the typical homeowners’ policy and, just as importantly, what coverage is not. This will allow them to take appropriate actions to address this common source of losses and claims and avoid unpleasant surprises and expenses.

Unfortunately, the overly broad and loose interpretation of the term “water damage” makes this relatively simple step challenging. Floods, leaks, seepage, backups, heavy rains, overflowing rivers or lakes, and tidal surges are common examples of water damage, and various insurance coverages respond differently to each.

WHAT CONSTITUTES A ‘FLOOD’?

One of the most widely misunderstood words in the typical homeowner’s insurance policy is “flood.” The reason is simple: the term “flood” appears as an exclusion to coverage but is not defined in the policy. For example, the Insurance Services Office (ISO) Homeowners Policy form has several exclusions addressing perils that may be considered a “flood”:

• under “earth movement,” a “landslide, mudslide or mudflow, subsidence or sinkhole, or any other earth movement,” and

• under “water damage,” “(a) flood, surface water, waves, tidal water, overflow of a body of water, or

The Texas HOB Homeowner’s Policy form has similar wording:

“We do not cover loss . . . caused by settling, cracking . . . of foundations, walls, floors, . . . retaining walls . . . We do not cover loss caused by or resulting from flood, surface water, waves, tidal water or tidal waves, overflow of streams, or other bodies of water or spray from any of these whether or not driven by wind.”

Both forms have a similar weakness because of the lack of definitions in the policy terms and conditions. In the ISO form, the only terms found in the exclusion that are defined in the policy are “earth movement” and “water damage.” The Texas form defines none of the specific terms. What constitutes the terms “earth movement” and “water damage,” or “flood, surface water, waves, etc.,” is also not found in the Texas form. In short, many important terms and definitions are found in neither of the insurance contracts.

When a specific term is not defined by the insurance policy, other sources must provide the definition. Therein lies the problem. According to three popular dictionaries, “flood” broadly means a large amount of water covering an area that is usually dry. As such, these definitions would appear to be commonsense interpretations of what constitutes “flood” in the homeowner’s insurance policy.

However, the standard practice in the insurance industry is to use the Federal Emergency Management Agency’s (FEMA) definition of “flood” (and, by extension, “earth movement”) without specific reference to that source. That definition is not closely aligned to a commonsense definition of the term “flood.”

2 TG Residential

According to FEMA’s National Flood Insurance Program (NFIP) Dwelling Form F-122, a flood is:

• a general and temporary condition of partial or complete inundation of two or more acres of normally dry land area or of two or more properties (one of which is your property) from:

0 overflow of inland or tidal waters,

0 unusual and rapid accumulation or runoff of surface waters from any source, or

0 mudflow (as defined in the policy form); or

• collapse or subsidence of land along the shore of a lake or similar body of water as a result of erosion or undermining caused by waves or currents of water exceeding anticipated cyclical levels that result in a flood as defined . . . above.

Because “flood” is clearly excluded from the standard homeowners’ insurance, the homeowner must seek coverage from the NFIP. To start, the homeowner must determine the property’s flood zone. This is easily accomplished by going to fema.gov and selecting “Floods & Maps,” then following the link to Flood Map Service Center to determine if the property is in a designated flood zone. This step is important because it gives the likelihood of the location flooding, which helps determine the amount of the insurance premium. The average flood insurance premium for properties in Special Flood Hazard Areas (SFHA), noted as a zone beginning with A or V, is almost 50 percent higher than the premium for properties in low- to moderate-risk zones (any zone labeled B, C, or X).

Homeowners who have a governmentbacked mortgage and are in a designated flood zone must purchase flood insurance from the NFIP. So must recipients of federal disaster relief money. Mortgage holders may also require flood insurance as a condition for making a loan even if the mortgage is not governmentbacked.

Homeowners who do not have a government-backed mortgage or have not received federal disaster relief and are not in a high-risk flood zone may still purchase flood insurance from the NFIP.

The most serious drawback of NFIP coverage is that its limits are relatively low, at $250,000 for an ordinary dwelling and $100,000 for contents. In addition, the “flood” insurance coverage offered by NFIP only covers

“flood” as defined by FEMA. Other types of “flood” losses, such as backup of sewers or septic systems, burst pipes, overflow from a washing machine, or damage caused by rain, sleet, snow, or hail, are not included in FEMA’s definition and are, therefore, not covered by an NFIP policy.

NOW A WORD ABOUT WATER DAMAGE

In addition to the matter of “flood,” homeowners must consider “water damage,” a term that is more broadly defined in the homeowners’ insurance policy than FEMA’s definition of “flood.” Fortunately, homeowners’ insurance coverage with higher limits is widely available in the homeowners’ insurance marketplace at relatively reasonable rates. Additional coverage options beyond the standard homeowners’ policy may also be available through the broader insurance marketplace. The homeowners’ insurance agent may have knowledge of or access to these.

The key to covering water damage is realizing that the damage must be sudden and accidental. For example, water pouring from a burst pipe qualifies, but water seeping in from a foundation does not. The typical homeowners’ insurance covers water damage caused by:

• burst pipes,

• accidental leaks from plumbing or appliances,

• wind-blown snow or rain,

• a roof leak following damage from a storm or wind,

• water used to extinguish a fire, and

• water that enters the dwelling because of ice dams on the roof.

Related to the water damage is damage caused by mold and mildew from unknown leaks or seepage.

3 SUMMER 2023

THINGS POLICIES GENERALLY DON’T COVER

There are also common policy exclusions that address the peril of water damage. For example, water damage is not covered if the damage arises from a lack of maintenance or negligence.

Damage from a burst pipe is covered unless the damage arises from freezing caused by a lack of sufficient heat. Related to that exclusion is water damage caused by an intentional act, such as turning heat off in the winter. However, damage caused by filling a bathtub with water and then simply forgetting to turn it off is covered.

PLAN AHEAD AND AVOID PESKY PAPERWORK

While purchasing appropriate insurance coverage is always prudent, so is taking steps to prevent losses before they occur or mitigate damages.

Practical measures include stockpiling sandbags for building dams around openings in the dwelling, having emergency pumping equipment on hand, keeping personal property off the floor, and storing property in waterproof containers.

For new construction, homeowners might consider building away from designated flood zones or on the highest elevation in the area, or building the dwelling on stilts or a concrete foundation that raises it above the expected high-water level.

In addition, the following simple steps could help homeowners avoid the irksome task of filing an insurance claim:

• Drain water heaters twice a year to prevent sediment buildup that can lead to corrosion of the tank, thus preventing leaks.

• Install smart water leak detectors on appliances such as dishwashers or washing machines. These smart devices will send a message to a cell phone alerting the homeowner of a leak. Some of these smart devices can also automatically shut off the water supply to an appliance that suddenly springs a leak, and others detect an overflow from sump pumps.

Leaks from a swimming pool or similar structure and seepage or leakage through a foundation are excluded. Damage caused by mold and mildew is excluded if the leakage or seepage is known to the homeowner or arises out of normal maintenance or negligence.

The last exclusion addresses the cost to repair or replace the source of water damage. While the damage itself may be covered, the cost of repair or replacement of the device causing the leak is not.

OPTIONAL COVERAGES

Homeowners can purchase optional endorsements that provide coverage for water damage normally excluded from the policy.

Water backup coverage fills the gap created by the exclusion that addresses “water or water-borne material that backs up through sewers or drains or that overflows or is discharged from a sump, sump pump, or related equipment.” This endorsement covers backup of sewers, drains, septic systems, and sump pumps.

Another available endorsement covers damaged utility lines under the homeowners’ property, including the expense to excavate and reseed.

• Regularly inspect hoses on appliances and replace those worn or cracking before a leak occurs.

• Inspect the roof for damage, particularly following a severe storm with high winds or hail. Replace any loose or missing shingles or tiles and secure flashing that has been pulled away.

• In cold climates, insulate pipes or wrap them with heating tapes. Insulate, heat, or leave open any enclosed areas with pipes, such as attics, to prevent freezing. Do not turn off or significantly lower heat in areas where water pipes are present.

• Use a rake to safely remove snow from roofs to prevent buildups that result in ice dams. Ice dams allow for snow/ice melt to pool during the day and seep under shingles.

• Clean leaves out of gutters in the fall to prevent clogged drains and downspouts that can lead to the formation of ice dams.

For more on the information covered in this article, consult a licensed insurance agent.

Dr. Rudolph (famousreindeer2@yahoo.com) has 20 years in insurance brokerage and 30 years of experience in insurance and risk management consulting and education.

Commercial’s Carbon Conundrum

The U.S. Green Building Council estimates that buildings and construction account for at least 31 percent of energy-related CO2 emissions globally. Although no strict timeline has been established, commercial building owners in Texas may have to one day consider the level of emissions created throughout the life of their properties when deciding what to do with aging structures.

By Harold D. Hunt and Bucky Banks

T

In real estate, the environmental impact of a decision to either refurbish or demolish and rebuild an existing commercial property is a perfect example of pressures on the horizon that will force more attention on this subject. The Carbon Leadership Forum reports that approximately 30 percent of all global carbon emissions are attributed to the building sector.

When attempting to quantify the environmental impact of decisions regarding existing properties, one of the challenges commercial property owners may soon face will be minimizing “embodied carbon.” According to the U.S. Green Building Council (USGBC), eight states already have policies in place addressing the issue: Washington, Oregon, California, Colorado, Minnesota, Connecticut, New York, and New Jersey.

he global movement to address environmental, social, and governance (ESG) concerns continues to accelerate. Government regulations are becoming more stringent in an attempt to protect the environment. Businesses large and small are also increasingly sensitive to their impact on energy usage, resource conservation, and the climate.5 SUMMER 2023

Commercial’s Carbon Conundrum Commercial

Life Cycle of Commercial Buildings

Embodied carbon is defined as the greenhouse gas emissions produced by the manufacture, transportation, installation, maintenance, and disposal of building materials. All of these factors combine to make up the life of a commercial building. Numerous publications separate a building’s cradle-to-grave life cycle into four discrete stages:

1. Product stage: Involves the extraction, transportation, and manufacture of the materials needed to construct a building.

2. Construction stage: Involves the transportation to and installation of material components at the site to erect the building.

3. Use stage: Involves the operation, maintenance, repair, and possible refurbishment of the finished building.

4. End-of-life stage: Involves the deconstruction, transportation, waste processing, and disposal of building materials.

The embodied carbon in a commercial building comprises all greenhouse gases (GHGs) produced in every life cycle stage except the use stage. GHGs produced in the use stage are defined as “operational” carbon that can be heavily impacted by the building’s energy efficiency. Historically, much more attention has been paid to the level of operational carbon in commercial buildings than levels of embodied carbon. The formula used to calculate embodied carbon is typically:

Embodied carbon = quantity of each material or product × a carbon factor for the product

According to the Institution of Structural Engineers (ISE), approximately 55 percent of the carbon embodied across a building’s life cycle occurs before a building is even occupied. The highest levels of embodied carbon will be produced in the production stage followed by the construction stage.

A quick online search reveals several available software products for estimating embodied carbon in new construction. ISE also provides a detailed analysis and discussion of the subject in its 2020 publication How to Calculate Embodied Carbon

These numbers can provide a reasonable estimate for a proposed building’s environmental impact from construction to demolition, so long as the exact materials and quantities or volumes are known. However, the availability of embodied carbon statistics for the materials being used in construction is a limiting factor.

The USGBC reports that levels of embodied carbon in building materials and products can be identified through a reporting system known as Environmental Product Declarations (EPDs). The system can assess a material’s environmental impact throughout every life cycle stage. Although EPDs are largely voluntary in the U.S., their use is on the rise.

The USGBC’s LEED rating system does offer “materials and resources” credits to reduce embodied carbon. However, they also note that changes to the LEED requirements and credits are ongoing as new information, strategies, and policies become available.

The Inflation Reduction Act (IRA) is a recent attempt at the federal level to decrease embodied carbon. The legislation aims to reduce total carbon emissions by 40 percent by 2030. Approximately $5 billion will be allocated to low-carbon spending to improve physical infrastructure. The distribution of funds will include money for developing and standardizing EPDs as well as labeling and using low-embodied carbon materials, technologies, and products.

Regulatory Response and Developer Dilemmas

Real estate professionals should expect more legislation at all levels of government addressing the environmental impact of commercial development and redevelopment. The USGBC, EPA, and the Urban Land Institute (ULI) are all advocating and adopting increasingly stringent standards for limiting GHG emissions through improved designs and materials.

While the cost of altering or removing dated properties may prove beneficial to the environment, it can simultaneously lower the return on a property owner’s investment. How landlords respond will have a significant impact on the future of commercial real estate development. If a meaningful shift in demand or supply for commercial space occurs along with GHG restrictions, many properties may have trouble maintaining positive cash flow, thus reducing any financial benefits from a renovation. Destruction of property value and a loss of appeal for new development will follow.

A newly constructed building using superior materials can produce a property that is more energy efficient and lower in embodied carbon. However, developers will also factor in the tradeoff in extra cost for constructing such a property. Furthermore, calculating the amount of embodied carbon in older existing buildings is a much more complex task. Again, cost will play an important role in the decision to refurbish or demolish an existing building.

Cost benchmarking data for determining acceptable embodied carbon in a commercial retrofit project is another limiting factor in the process. Due to a lack of building-level data, no consensus has formed around any benchmark for embodied carbon levels in a building.

6 TG

Real estate professionals should expect more legislation at all levels of government addressing the environmental impact of commercial development and redevelopment.

Author Harold Hunt talks more about this on TRERC’s YouTube channel.

To quantify GHGs and their potential effects on climate change, a method known as a life cycle assessment (LCA) is used to track the emissions produced over the full life cycle of a material or construction process. The emissions are then converted into specific metrics that reflect their potential effects on the environment.

LCA tools are becoming more popular for deciding whether to refurbish or demolish and rebuild commercial properties. However, users should be aware that different LCA tools will generate different results. Unfortunately, some underlying databases are not regularly maintained, while documentation of some data sources and methodologies are not always easily available. Furthermore, most LCA tools have been primarily focused on specific material characteristics and not whole buildings. Data collection and reporting guidelines are needed for data standardization and transparency. Material manufacturers must increase participation in this process as well.

Users should also remember that embodied carbon calculations in LCAs are only estimates. Many variables and assumptions are included in the calculations. For example, estimates of the embodied carbon generated can vary widely based on the location where materials are produced, the transportation distance from production to final destination, and the method of production. Uncertainty in results can increase even further when estimating embodied carbon in older buildings.

Refurbish or Demolish? That is the Question

The decision to refurbish an older commercial building or demolish it for new construction will generally be based on which choice produces the highest return on investment. The answer may often be in favor of demolishing and redeveloping the property. Unexpected problems can always arise when the choice is refurbishment. Newly constructed buildings have the advantage of newer, possibly higher quality materials that abide by more stringent energy codes that many cities have put in place.

RESPONDENTS TO A RECENT U.S. GREEN BUILDING Council survey on green building trends and sentiments ranked passive design principles, energy efficient equipment, and reducing embodied carbon of key materials such as concrete, steel, and glass as the top three strategies for achieving building decarbonization.

The result of implementing such products should be an improved tenant experience and higher rents, a win-win for both developers and tenants. Practically speaking, owners should be committed to supporting the refurbishment of an existing building if there is tenant demand. However, most owners will remain committed to maintaining the attractiveness and energy efficiency of a property only if it supports improved cash flow growth. Although studies have shown that refurbishing buildings has only half the embodied carbon impact of new construction, energy efficiency does not necessarily guarantee a building will command superior rents. Building owners have little reason to support any costly renovation that does not increase tenant demand or utility.

The current, post-COVID economic environment has initiated the conversation between building owners, developers, and municipalities regarding what to do about existing commercial buildings, especially office properties. As a result, expect refurbishment or demolition to make way for new construction to be a higher priority for many office buildings.

Before the pandemic, trophy-class office properties were often assumed to be insulated from near-term market forces. Such properties are no longer shielded by the perception of continued strong demand for office space in the years ahead. This trend appears to be entrenched, and the negative value shift may provide property owners with an incentive to seek returns through alternative uses. Such a decision will invariably result in a greater release of GHGs.

As more older commercial buildings of every type become increasingly inefficient or obsolete, the concern over the environmental impact of any type of change or removal of the structures will only grow.

Dr. Hunt (hhunt@tamu.edu) is a research economist with the Texas Real Estate Research Center at Texas A&M University and Banks (bbanks@ mays.tamu.edu) is associate director and executive assistant professor for Texas A&M’s Master of Real Estate program in Mays Business School.

7 SUMMER 2023

Understanding the mechanics of an “As Is” contract and the interplay of the option period is important for agents and their clients when negotiating the original sales price of a contract or renegotiating the sales price during an option period. By

Now that the COVID-era feeding frenzy for buying properties has subsided and interest rates are on the rise, buyers and sellers are on more equal footing. This is a good time to remind buyers, sellers, and their agents how the property’s condition affects the sales price at various stages of the real estate transaction.

A logical place to start is by looking at the importance of the Seller’s Disclosure Notice, the meaning of “As Is,” the inspection provisions of Paragraph 7 of the One to Four Family Residential Contract (Resale), and use of the option period when renegotiating the sales price following an inspection.

Seller’s Disclosure Notice

Although the Seller’s Disclosure Notice is a separate document from the sales contract, it’s no coincidence that it’s part of the contract’s Paragraph 7 on Property Condition. The Seller’s Disclosure Notice is required by Texas Property Code Section 5.008. That statute sets out the minimum information about a property’s condition that a seller must disclose to a buyer in a residential sales transaction, including prior flooding events.

The Texas Real Estate Commission (TREC) has a Seller’s Disclosure Notice

that parallels the statutory provisions. Some real estate trade associations and brokerages have Seller Disclosure Notices that contain more information than is required by the statute.

Paragraph 7B of the sales contract indicates whether the buyer has received the notice before signing the contract, the buyer has not yet received the notice, or the seller is not required to give the notice under specific exemptions contained in the property code.

If the buyer has not yet received the notice, the seller has a negotiable number of days to deliver it, and the buyer has the right to terminate the contract within seven days after receiving the notice. Paragraph 7B is structured this way because the sales contract is an “As Is” contract (more on this in a moment), and knowing information about the property’s condition prior to signing the contract will affect how much the buyer is willing to pay for the property. The seven-day period allows the buyer time to review the disclosures made by the seller and possibly renegotiate the sales price or repairs based on the new information. If the parties reach an agreement during that period, they will execute an amendment to the sales contract. If no agreement is reached, the buyer has the right to terminate the sales contract and get his earnest money back.

Kerri Lewis

Not only is the Seller’s Disclosure Notice important for negotiation of the sales price of a property, but it could also affect a buyer’s decision to purchase the property at all. Knowing this, some sellers may get “selective amnesia” when filling out the notice to make their property more attractive to buyers. But sellers beware: failing to properly disclose the condition of a home can bring a lawsuit from the buyer months or years after the sale.

Keep in mind that Texas law requires sellers and real estate agents to disclose any known material defect on the property to the buyer, whether or not it is an item listed on the Seller’s Disclosure Notice. Real estate agents do not want to get drawn into a lawsuit, so here are a few best practices concerning the Seller’s Disclosure Notice:

• The seller’s disclosure is only the seller’s disclosure, and agents should never assist the seller in filling out the form. Sellers who need assistance should contact a real estate attorney or use an online program that takes them through a step-by-step program to complete the notice. Agents are certainly able to refer their clients to either.

• An agent should offer the seller every form of Seller’s Disclosure

8 TG Residential

Notice available in the market area, (unless her broker has told them otherwise) and let the seller decide which one to complete.

• An agent should talk to his clients about the importance of completing the form fully and truthfully.

• If an agent knows about a material defect and the seller does not disclose it, the agent has an obligation under the law to disclose it to the buyer.

Paragraph 7D, “As Is” Provision

The language making the sale of the property “As Is” can be found in Paragraph 7D entitled “Acceptance of Property Condition.”

The contract language defines “As Is” to mean “the present condition of the Property with any and all defects and without warranty except for the warranties of title and the warranties in this contract.” Knowing the condition of the property by receiving and reviewing the Seller’s Disclosure Notice and walking through the property to observe its current, visible condition are important steps for a buyer to take before entering into a contract and will determine what price she is willing to pay for the property.

Paragraph 7D provides two options for buyers: (1) the buyer accepts the property As Is; or (2) the buyer accepts the property As Is provided the seller, at the seller’s expense, completes certain specifically named repairs and treatments.

It is important for agents and their buyer clients to understand that the blank to be filled in for Paragraph 7D(2) is not a catch-all to be used for anything found in a future inspection (more on inspections in a minute) but for specific items that may have been noted in the Seller’s Disclosure Notice as not being in working condition, or for visible items of disrepair the buyer observed when viewing the property.

Agents and their buyer clients should also understand this paragraph provides that accepting the property “As Is” under either 7D(1) or 7D(2) does not preclude them from performing any inspections under Paragraph 7A or from negotiating an amendment based on what they find.

An example of the proper use of 7D(2) would be where the Seller’s Disclosure

Notice indicates that the HVAC system is not in working order. A buyer could submit a contract noting in Paragraph 7D that the seller must repair or replace the HVAC system prior to closing. Of course, because the seller noted the issue prior to the contract, she may counter at a higher price to take into account the cost of the repair.

Paragraph 7A Inspection Provision

Under Paragraph 7A of the sales contract, sellers must allow buyers and their chosen inspectors (licensed by TREC or otherwise permitted by law to make inspections, like a plumber, electrician, or termite inspector) access to the property at reasonable times to perform any inspection of the property the buyer deems necessary.

The seller is also required to keep the utilities on while the contract is in effect to facilitate inspections.

sale price or have seller perform certain repairs should the inspection report reveal issues with the property that were not noticeably visible or otherwise disclosed by the seller. That last point is important when a buyer is asking for sales price reduction or repairs to be paid for by the seller under an “As Is” contract.

Remember that an “As Is” contract is one where the buyer is submitting an offer to the seller based on the property’s current condition. Generally, the listing price set by the seller is what the seller thinks the property is worth in its present condition. The seller rightfully assumes that the offer brought by the buyer is based on what the seller has revealed about the property in the Seller’s Disclosure Notice and what the buyer observed about the property’s condition during a walk-through. This is why many sellers are put off by a buyer who tries to renegotiate the contract terms based on items in an inspection report that were previously disclosed or readily observable at the property—because the seller agreed to a sales price based on the property’s present condition

Only hydrostatic testing requires written approval by the seller.

All inspections are at the buyer’s expense.

The buyer’s right to have inspections performed is not tied to the option period. This right is available regardless of whether the buyer purchased an option period, or whether or not the option period has expired.

Option Period and Renegotiation of Price After an Inspection

The option period provides the buyer with some leverage to renegotiate the sales price following an inspection, so it is advisable that a buyer pay an option fee to obtain an option period under Paragraph 5 of the contract. It is also advisable that the buyer get an inspection performed during the option period with enough time left to renegotiate the

It is important that the parties and their agents understand that under an “As Is” contract, renegotiation of the sales price or seller-paid repairs should be limited to items that were not previously disclosed or not readily observable. That is the value that an inspection report brings to the transaction.

If the buyer is still in the option period, he can try to renegotiate the contract terms based on new items found. Although the seller does not have to agree to a price reduction or repairs, he risks losing the deal if the buyer walks and gets her earnest money refunded. In a hot market, this was not such a big deal for the seller. But in a more balanced market, the seller should consider whether he will get another offer and how much longer that will take.

Also keep in mind that if the inspection report reveals material defects, and the seller is made aware of those defects, the seller is obligated to reveal those to the next buyer, and that buyer might want equal or greater price concessions.

Lewis (kerrilewis13@gmail.com) is a member of the State Bar of Texas and former general counsel for the Texas Real Estate Commission.

9 SUMMER 2023

Texas law requires sellers and real estate agents to disclose any known material defect on the property to the buyer, whether or not it is an item listed on the Seller’s Disclosure Notice.

Why the Capital City’s Home Prices Surged

Austin’s reputation as a technology and science hub has attracted a growing number of residents in recent years, many of them high earners from out of state. This increase in housing demand, coupled with higher buying power and a still-low housing inventory, will likely keep area home prices

elevated.

By Joshua Roberson and Mallika Natarajan

By Joshua Roberson and Mallika Natarajan

In response to 2020’s COVID-19 pandemic, the U.S. government executed a series of steps, including interest rate cuts, to hold off economic calamity. What followed was an unprecedented increase in housing sales set off by a fall in mortgage rates to historically low levels. Housing markets across the country experienced a major boost in activity, but some markets stood out more than others.

Take Austin, for example.

The capital city already had a reputation for high-priced housing in a state that boasted affordability. It had a strong

10 TG Residential

1992 1996 2000 2004 2008 2012 2016 2020 2024

Number of Migrants (Thousands) Sources: U.S. Census Bureau and Haver Analytics 250 200 150 100 50 0

Figure 1. Texas’ Net Domestic Migration

economy, attracted young talent, and had a migration boom, factors that only intensified beyond 2020. What followed was a price surge that drew much national attention.

Which Way to Austin?

Texas has been a popular destination over the past ten years, welcoming a steady flow of migrants from other states. After 2020, Texas experienced a spike of inbound migration not seen since migrants from New Orleans relocated following the devastation of Hurricane Katrina (Figure 1).

Austin, especially, has been one of the state’s top destinations for new residents. Before 2020, Austin received an average of 48,335 new households. By 2021, that number spiked to 75,555. The city had already been trending upward since 2016, with 2019 setting a record of 53,680 new households.

Before COVID, the majority of households that moved to Austin were from other parts of Texas (Table 1). Moves from other states were second, and international moves a distant third. Deep into the pandemic,

the number of movers from other states exceeded the number from within Texas.

From which state did most movers come? California, but that’s true every year given the Golden State’s massive size. However, in 2020 and 2021 the number of households from California was more than double that of prior years (Figure 2). As a result, the proportion of out-of-state moves from California increased to almost 30 percent of all inbound moves by 2021 (Table 2).

One would think Austin would be a major destination for Californians, especially from the Bay Area, given both cities’ connection to technology and innovation. According to consumer data from Infutor Data Solutions, almost a third of California moves in 2021 came from the Bay Area and surrounding communities. Movers with a prior San Jose address accounted for 4.6 percent of moves, while San Francisco accounted for an additional 4.3 percent.

The largest overall city source in 2021 was Los Angeles with 6.5 percent of moves. That’s a bit underwhelming considering

11 SUMMER 2023

Year International Moves Out-of-State Moves In-State Moves 2012 10% 37.8% 52.3% 2013 7.6% 42.8% 49.5% 2014 9.1% 45.3% 45.6% 2015 7.1% 49% 44% 2016 6.4% 46.2% 47.4% 2017 8.7% 43.2% 48.1% 2018 7.3% 44.6% 48.1% 2019 6.4% 46.6% 47.1% 2020 8.1% 48.6% 43.3% 2021 7.9% 51.4% 40.7%

Table 1. Percentage of Household Moves into Austin-Round Rock

Source: IPUMS USA, University of Minnesota, www.ipums.org

L.A. is many times larger than both San Francisco and San Jose combined. Probably the biggest surprise was San Diego with 5.6 percent of moves.

While California received a lot of attention in Texas during the pandemic, data show migration to Texas increased from many other sources. For example, the number of moves from New York climbed from 6 percent of total moves in 2019 to 9 percent in 2021 (Table 2). North Carolina was another top state in the inbound pipeline, likely because of similarities between Austin’s and Raleigh-Durham’s economies and demographics.

Regardless of where people came from, they brought a lot of earning power. In 2021, the average household income of out-of-state movers was $130,000 (Table 3). Households moving to Austin from other parts of the state earned $87,000 on average. Up until 2017, the earnings differential was minimal. After that, the gap widened, with the largest difference occurring during COVID.

Tech-Driven Employment Explosion

Like migration, Austin employment growth exploded during COVID, making the metro’s economy one of the quickest to recover. That growth was driven largely by professional and business services, which include a lot of higher-income jobs.

Growth in Austin’s professional and business services sector was already strong, ranging from 3 to 8 percent year-over-year growth in the decade leading up to COVID (Figure 3). Texas’ growth in this sector was closer to 5 percent year-over-year in 2019. Like elsewhere, Austin’s job numbers fell drastically in April 2020 but quickly bounced back by that August. After that, growth continued to expand at double-digit rates before hitting the ceiling in October 2022. Since then, month-tomonth growth has been minimal, but overall employment levels remain considerably higher than 2019 levels.

In most major metros, such as Dallas-Fort Worth, professional and business services includes white collar jobs such as accountants, lawyers, and executives. In Austin, however, that category leans heavily in the technology and sciences sectors, and jobs in those sectors grew at the fastest rates between 2020 and 2021.

For example, computer systems design expanded over 40 percent in just two years, resulting in 17,600 new jobs. Estimated annual wages for this occupation also grew quickly during this

12 TG

Source: IPUMS USA, University of Minnesota, www.ipums.org

Number of Households 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 9,000 6,000 3,000 0

Figure 2. California Households Migrating to Austin

Inbound State 2015 2016 2017 2018 2019 2020 2021 California 12.6% 18.5% 16.2% 19.2% 21.5% 31.9% 29.1% Florida 3.4% 6.1% 5.3% 5.2% 7.1% 2.1% 6.8% Illinois 7.7% 2.0% 10.6% 3.5% 5.3% 1.9% 2.8% New York 10.4% 5.7% 6.4% 7.1% 6.1% 3.2% 9.1% Other 65.8% 67.7% 61.6% 65.0% 60.0% 60.8% 52.1%

Table 2.Top States for Migration to Austin

Source: IPUMS USA, University of Minnesota, www.ipums.org

Year Out-of-State In-State 2011 $89,760 $54,096 2012 $55,280 $60,193 2013 $83,224 $70,427 2014 $89,521 $67,995 2015 $91,978 $80,050 2016 $89,787 $77,235 2017 $87,995 $78,643 2018 $124,438 $77,191 2019 $115,061 $84,312 2020 $152,036 $102,699 2021 $130,327 $86,751 Source: IPUMS USA, University of Minnesota, www.ipums.org

Table 3. Average Austin-Round Rock Household Income, In-State vs. Out-of-State Moves

period, expanding from almost $140,000 to $164,000. These jobs earn more than the mean household income in Austin, which was $115,863 in 2021.

Hot Housing Market

Regardless of where they came from, plenty of potential homebuyers came to Austin with major buying power amplified by record-low mortgage rates. The result was one of the most intense housing markets nationally.

Even with the April 2020 statewide shutdown of housing activity, Austin reached a new milestone for monthly home sales by July: 4,481 sales, an almost 20 percent increase from the year before.

The housing market was hot, but the supply was not enough to keep up. Despite strong demand, home listings never matched the sales pace, resulting in tremendous pressure in home prices.

4. Austin Median Home Price

Home Prices’ Rapid Rise

While home sales peaked in the summer of 2020, home prices would not peak for almost another two years. The most notable change in prices occurred during the first half of 2021. The highest point was in May 2022 when the median home price reached $550,000 (Figure 4), a far cry from the $328,000 recorded in May 2020.

For the next few months, Austin home prices declined in large part due to the drastic rise in mortgage interest rates influenced by the Federal Reserve’s inflation-fighting policies.

During this time, concerns about housing bubbles and crashes began to intensify. By December 2022, the median home price retreated to $450,000. Between then and March 2023, home prices hovered there, signaling that the worst may be over.

Looking Ahead

Going forward, general speculation remains concerning Austin’s housing market.

So far this year, sales have been underwhelming compared with the past five years. Homes took far longer to sell in March 2023 (80 days on average) than they did 12 months before (22 days on average).

Home prices have remained stable for the past few months with the help of chronic low listing counts. While listings have increased since 2021 and 2022, they are essentially back to pre-COVID norms, which at that time meant tight markets. Combined with strong migration, low inventory levels may keep Austin prices elevated even after the initial drop at the height of the market.

13 SUMMER 2023

600 500 400 300 200 100 2000 2003 2006 2009 2012 2015 2018 2021 2024

Source: Texas Real Estate Research Center at Texas A&M University

MSA Price (Thousands of Dollars)

Figure

Thousands 180 150 120 90 60

Roberson (joshuaroberson@tamu.edu) is a lead data analyst and Natarajan (mallika@tamu.edu) a senior data analyst with the Texas Real Estate Research Center at Texas A&M University.

2010 2012 2014 2016 2018 2020 2022 2024 Sources: U.S. Bureau of Labor Statistics, Texas Workforce Commission, and Haver Analytics

Figure 3. Austin-Round Rock Professional and Business Services Job Growth

For more on Austin’s housing market, read Dr. Adam Perdue and Reece Neathery’s report, “What’s Driving Austin Home Price Affordability?,” by scanning the QR code.

People purchase rural land for a variety of reasons. Many want the serenity of living on a few acres in a rural area. Others just like the idea of purchasing and holding on to it, waiting for the metropolis to come to them.

Investors generally want two things: return of their money (initial investment) and an economic return on the money invested. Investing in rural land has traditionally been thought an effective way to accomplish these twin goals. Given sufficient time, an economic return in rural land can almost certainly result from appreciation in land value. Many investors purchase land to hold long term, waiting for the marketplace to create the favorable profit.

One idea for investors to consider while holding rural land and waiting for it to turn a profit is to operate a farm on the land. That may not be the first idea that comes to most people’s minds, but farms and farmers enjoy significantly favorable tax treatment. In fact, there is a strong pro-farm current

By William D. Elliott

By William D. Elliott

throughout many U.S. laws (and not only tax laws). The most prominent federal law oriented toward farming is the periodic subsidy bills that congress enacts about every five years or so. The average person might be surprised at the degree to which the federal government subsidizes U.S. farms.

Harvesting Tax Savings

In Texas, one of the most sought-after property tax benefits is the agriculture use valuation, commonly referred to as an “ag exemption.” This treatment represents a tremendous cost savings. However, it’s not an exemption, but rather a special method of valuing the real estate. In 1978, the Texas Constitution was amended to allow open-space land to be appraised based on its productivity value. In 1995, it was amended again to permit agriculture appraisal for land used to manage wildlife. Property tax valuation is generally based on the best use of the land, but agriculture landowners are entitled to have their

Taxes

Investors purchase rural land for a host of reasons, including the hope of making money when land values appreciate. Powerful tax provisions favoring farms are another reason rural land is an attractive investment option.

14 TG

property taxes computed based on the productive agriculture value. Obtaining the agriculture exemption can yield significant cost savings, so anyone acquiring rural land should pay attention to the requirements for an agriculture exemption.

Generally, about ten acres of qualified agricultural land is required for the special agricultural valuation. The land must have been primarily used for agricultural purposes for five out of the seven preceding years. The landowner applies for the special agriculture valuation with the local appraisal district.

In addition to property taxes, farmers also enjoy relief from sales and use and various fuel taxes when purchasing certain items used exclusively to produce agricultural products. To claim the tax exemption, the landowner must apply to the Comptroller of Public Accounts for an agriculture registration number, which is then used when purchasing qualifying items. The cost savings from an agriculture tax exemption from sales and fuel taxes can be significant.

What is Agriculture Use?

The definition of “agriculture use” is broad. As a principal guideline, the comptroller publishes a Manual for the Appraisal of Agricultural Land (scan QR code to view), which says agricultural use is cultivating the soil; producing crops; raising or keeping livestock, poultry, or fish; or planting cover crops. The land can be used to raise exotic animals or birds (or even bees), harvest timber, or for wildlife management. Local appraisal districts also publish guidelines concerning the degree of intensity of agricultural use generally accepted in the county.

For federal tax purposes, IRS guidelines indicate farming could include:

• operating a nursery or sod farm;

• raising or harvesting trees bearing fruits, nuts, or other crops;

15 SUMMER 2023

• raising ornamental trees (but not evergreen trees that are more than six years old when severed from the roots);

• raising, shearing, feeding, caring for, training, and managing animals; and

• leasing land to a tenant engaged in a farming business, but only if the lease payments are based on a share of the tenant’s production (not a fixed amount) and determined under a written agreement entered into before the tenant begins significant activities on the land. But the IRS cautions that farming does not include:

• contract harvesting of an agricultural or horticultural commodity grown or raised by someone else, or

• merely buying or reselling plants or animals grown or raised by someone else.

Hobby Losses

Another important tax benefit of owning and operating a farm is using economic losses from the farm to offset other ordinary income. The weekly release of current tax developments routinely includes at least one Tax Court case involving someone attempting to sustain tax losses from rural property that is said to be a farm (or ranch), and the IRS arguing that the taxpayers are merely engaging in a hobby.

The basic rule of “hobby losses” is often quoted but perhaps not readily understood. The governing statutes from the tax code distinguish trades or business from activities other than those engaged in for profit–or those engaged in as a hobby. The Internal Revenue Code allows a taxpayer to deduct “all the

ordinary and necessary expenses paid or incurred during the taxable year in carrying on any trade or business” [IRC §162(a)]. However, if the activity giving rise to the expenses “is not engaged in for profit,” deduction of expenses incurred in the activity is permitted “only to the extent that the gross income derived from such activity (i.e., the not-for-profit activity) for the taxable year exceeds the deductions.”

Activities not engaged in for profit are usually referred to as “hobbies.”

Hobby expenses may be deducted from hobby profits but not from any other income the taxpayer may have. Of course, this is exactly what a taxpayer hopes to achieve by owning rural property—to deduct large sums of money year after year against other income the taxpayer derives from other (and genuine) businesses or trusts or other conventional sources of income.

Hobby loss rules are based on a presumption. An activity is presumed to be engaged in for profit if the activity shows a profit for any of three out of five consecutive years ending with the year for which tax deductions are taken. For horse breeding, training, showing, or racing, the period is extended to two out of seven years. This presumption is not an absolute bar from using the losses against ordinary income. Rather, the hobby loss rule is a presumption in favor of a hobby. This means the taxpayer can take deductions in excess of income over a longer period provided the taxpayer can overcome the presumption that the losses are engaged in for a hobby (i.e., not engaged in for profit).

An activity constitutes a “trade or business”—and it escapes the hobby loss limitations—if the taxpayer has an actual and

16 TG

honest objective to realize a profit. The courts look at all surrounding facts and circumstances.

In one of the more prominent cases, an Indianapolis restaurant owner and operator maintained a horse-training activity outside of the city. The Tax Court denied him the deductions on the grounds that he was engaged in a hobby, but the U.S. Court of Appeals (Seventh Circuit) upheld the deductions stating that the Tax Court misapplied the usual factors considered. The Circuit Court rejected the Tax Court’s explanation that a profit motive will not be found when a taxpayer combines horse-racing activities with social and recreational activities. The Circuit Court explained that a business owner’s enjoyment of his business doesn’t automatically make the activity a hobby.

Income Averaging for Farmers

Although income averaging is no longer generally available, farmers retain this helpful feature. They can average their incomes over three years.

Since farm income can vary widely from year to year, the ability to average becomes an important benefit. It provides a way to balance an income tax burden over several years, reducing the effects of both lean and bounty years. Tax brackets increase as one earns more income. Thus, for bounty years, taxes increase because the tax bracket increased. Averaging allows the taxpayer to reduce the harsh effect of the higher brackets in the bounty years.

Special Rules for Debt Relief

Special relief from cancellation of indebtedness income is an important tax provision for the farmer.

For most taxpayers, when debt is cancelled, the relieved debt is income. The principal exception is when the taxpayer is insolvent. If debt is cancelled when the taxpayer is insolvent, there is no income. Farmers do not have this requirement. They can avoid debt cancellation income if the debt was incurred directly in connection with the farm’s business activity and

the taxpayer’s predominate income (over 50 percent) for the past three years comes from farming. The lender or creditor of the debt in question must also be in the business of lending money.

Conservation Improvements and Restoration

Expenditures for conservation expenses is an important area of favorable tax rules for farmers. These types of expenses are normally capitalized, but for farmers they are deductible. The tax code provision describes the pertinent conservation expenses as those for the purposes of soil and water conservation with respect to land used in farming, or for the prevention of erosion or farmland.

The farmer is required to have a conservation plan, which the U.S. Department of Agriculture must approve. If there is no plan, the improvements must be consistent with a soil conservation plan of another state agency concerned with farming.

Deductions for conservation expenses are limited to 25 percent of farm gross income, but a carryforward is permitted. The limitation being expressed as a percentage of gross farm income is an important feature, suggesting the potential for offsetting other nonfarm income.

Vehicle Expense

Farmers receive liberal treatment for their auto and vehicle expenses.

The normal requirement of documentation to support auto or truck expense is waived for farmers. Up to 75 percent of vehicle expenses are deductible even without documentation.

Nothing in this publication should be construed as legal or tax advice. For specific advice, consult an attorney and/or a tax professional.

Elliott (bill@wdelliottlaw.com) is a Dallas tax attorney, Board Certified, Tax Law; Board Certified, Estate Planning & Probate; Texas Board of Legal Specialization; and Fellow American College of Tax Counsel.

17 SUMMER 2023

Texas’ Property Tax Puzzle

Texas citizens have been clamoring for property tax relief. In California, Proposition 13 was supposed to keep taxes down by limiting appraisal growth rates, but the results have been far from beneficial. Texans can learn from the changes California made and what ultimately went wrong.

By

Charles E. Gilliland and Lynn D. Krebs

By

Charles E. Gilliland and Lynn D. Krebs

Concerns about persistently increasing property tax burdens, especially on homeowners, have dominated the Texas legislature over the current and past two sessions. While property values have risen steadily, most tax entities grew their budgets even more by raising rates prior to 2019, when the legislature curbed the growth rate of Texas property taxes.

Despite the legislative change, concerns of seemingly everincreasing property taxes persist. Currently, an unprecedented state budget surplus, largely driven by sales tax revenues, provides the legislature a unique opportunity to take another bite out of property taxes. The challenge is to do this without creating economic distortions related to real estate and other taxable property.

Property Taxes and Public School Funding: A Brief History

Beginning in the 1970s, a series of lawsuits challenging Texas state public school financing produced a system that inexorably links Texas property tax policy with school funding issues. Lacking public support for a personal income tax to equalize available resources across school districts, the Texas Legislature came to rely on local property taxes to meet those needs. This dependence dramatically inflated tax burdens for Texas property owners. Effective tax rates increased from approximately 1 percent of market value in the early 1980s to rates exceeding 3 percent in some areas of the state.

In addition to rate increases, administrative reorganization created a single appraisal district in each county except for Randall and Potter, which share a single district. That move necessitated a comprehensive overhaul of the entire property tax system.

Because home values tend to increase more rapidly than those of other property types, this new system shifted a growing proportion of total property taxes to homeowners. Frequent reappraisals caused sizable increases in taxes as rising values, coupled with steady or rising tax rates, increased tax liabilities.

To counteract that tendency, the legislature crafted a number of measures designed to soften rising tax burdens. Concentrating the efforts on homeowners, various measures addressed the problem on three fronts. First, to ease homeowners’ tax burdens, various measures exempt part or all of the taxable value of qualified homes. Second, to cushion homeowners from unanticipated tax increases, appraised value increases were limited to 10 percent each year for qualified homes. Third, so-called “truth in taxation” provisions created a process to empower taxpayers to roll back proposed tax rate increases by taxing units.

In 2019, Senate Bill 2 and House Bill 1 changed “rollback tax rate” to “voter-approved tax rate” and lowered that rate from 8 percent to 3.5 percent for cities and counties and 2.5 percent for school districts. The change also came with a requirement for cities to hold automatic elections to approve tax rates exceeding the voter-approved tax rate.

18 TG Property Tax

The rollback rule came with some exceptions. It did not apply to special taxing units, such as groundwater conservation districts, junior college districts, and hospital districts. Also, cities with populations of less than 30,000 are not subject to the automatic election requirement. Additionally, a city may add its “unused increment rate” to the annual 3.5 percent limit on maintenance and operations increases.

How Texas Tax Rates Measure Up Nationally

Despite these measures, property tax increases have propelled Texas 2020 effective tax rates for homeowners to the sixth highest in the nation according to research published by the Tax Foundation, indicating a substantial property tax burden for Texans compared with other states (Table 1).

Texas sales tax rates were also among the highest, ranking 14th nationally as of 2023 according to the Tax Foundation (scan the QR code to view).

Another Tax Foundation report analyzes the overall burden of state and local taxes for each state (Table 2). In this study, the Tax Foundation defines “a state’s tax burden as state and local taxes paid by a state’s residents divided by that state’s share of net national product” (scan the QR code for Tax Foundation, Page 3, “State and Local Tax Burdens, Calendar Year 2022,” April 7, 2022). Texas ranks sixth lowest among the

Table 1. Effective Property Tax Rates

19 SUMMER 2023 s

Rank State or District Effective Rate 1 New Jersey 2.21% 2 Illinois 2.05% 3 New Hampshire 1.96% 4 Vermont 1.82% 5 Connecticut 1.76% 6 Texas 1.66% 7 Wisconsin 1.63% 8 Nebraska 1.61% 9 Ohio 1.58% 10 Iowa 1.50% 11 Pennsylvania 1.49% 12 Rhode Island 1.43% 13 New York 1.38% 14 Michigan 1.38% 15 Kansas 1.32% 16 Maine 1.25% 17 South Dakota 1.18% 18 Massachusetts 1.14% 19 Minnesota 1.10% 20 Maryland 1.04% 21 Alaska 1.02% 22 Missouri 0.99% 23 North Dakota 0.95% 24 Oregon 0.94% 25 Georgia 0.91% 26 Florida 0.91% 27 Oklahoma 0.88% 28 Washington 0.88% 29 Virginia 0.87% 30 Indiana 0.84% 31 North Carolina 0.82% 32 Kentucky 0.82% 33 Montana 0.75% 34 California 0.73% 35 Idaho 0.70% 36 Tennessee 0.68% 37 New Mexico 0.66% 38 Mississippi 0.65% 39 Arizona 0.65% 40 Arkansas 0.64% 41 District of Columbia 0.61% 42 Nevada 0.60% 43 Delaware 0.59% 44 Utah 0.59% 45 Wyoming 0.56% 46 South Carolina 0.56% 47 West Virginia 0.55% 48 Colorado 0.54% 49 Louisiana 0.54% 50 Alabama 0.39% 51 Hawaii 0.31% Source: Tax Foundation

Table 2. State and Local Tax Burdens by State, Calendar Year 2022

50 states and District of Columbia with an overall 8.6 percent effective state and local total tax rate. That amounts to 45.9 percent below New York, the highest state at 15.9 percent. Texas’ burden is well below the average of 10.6 percent (Pennsylvania) and the median burden of 10.2 percent (Arkansas and New Mexico).

Texas has consistently ranked among the lowest six states in this study over the last several years, though it declined from third place in 2020. However, the state’s burden in 2020 was 8.7 percent, a tick higher than in 2022. Texas’ effective state and local tax burden, as measured by this study, has been as high as 8.9 percent (1977) and as low as 7.7 percent (1980), but has been remarkably consistent in a range of 8.2 percent to 8.7 percent since 2010.

Relief Efforts . . . and Results

Despite Texas’ relatively low overall tax burden, the effective property tax rate of $1.66 per $100 of value indicated in Table 1 continues to prompt outcries from taxpayers for further relief. This in turn has some lawmakers casting about for a measure that would provide significant tax relief through more restrictive caps on appraisal increases.

An appraisal increase limit of 5 percent was recently proposed in the Texas House. However, the intended benefit of such a cap could be undone, at least partially, by higher rates set by cities and counties across the state, as would be permissible to maintain their budgetary needs, even with existing budget growth limits (see analysis later in this article).

Furthermore, caps on assessed values spawn several market distortions and inequities. For example, it creates a disincentive to mobility and investment and disadvantages for newer real estate buyers, including homeowners. The longer one owns a property subject to an assessment cap, the greater the benefit (and incentive to stay put without making improvements that could trigger a reassessment). Additionally, new entrants to the market, even neighbors to existing owners, would face a disproportionate share of the local tax burden. Finally, other (non-capped) classifications of property would increasingly be subject to rising effective rates.

Similar pressures in California inspired the famous Proposition 13 tax measure in the late 1970s, which limited annual increases on appraisals to 2 percent so long as ownership continued in the same hands. This provision led to predictions that assessed values would lag market values in areas with rapidly rising prices. Decades later, circumstances confirmed that forecast. As stated in the report Property Tax Limitations and Mobility: The Lock-in Effect of California’s Proposition 13, “longer tenure itself leads to higher subsidies whenever property values increase by more than 2 percent per year,” among other issues. Scan the QR code to view the report

Source: Tax Foundation (taxfoundation.org/publications/state-localtax-burden-rankings)

Further unanticipated consequences of the limits continued to roil taxpayers. Newer homebuyers began to notice substantially lower taxes applied to long-term homeowners, with

20 TG

State Effective Tax Rate Rank Alabama 9.8% 20 Alaska 4.6% 1 Arizona 9.5% 15 Arkansas 10.2% 26 California 13.5% 46 Colorado 9.7% 19 Connecticut 15.4% 49 Delaware 12.4% 42 District of Columbia 12.0% (39) Florida 9.1% 11 Georgia 8.9% 8 Hawaii 14.1% 48 Idaho 10.7% 29 Illinois 12.9% 44 Indiana 9.3% 14 Iowa 11.2% 34 Kansas 11.2% 33 Kentucky 9.6% 17 Louisiana 9.1% 12 Maine 12.4% 41 Maryland 11.3% 35 Massachusetts 11.5% 37 Michigan 8.6% 5 Minnesota 12.1% 39 Mississippi 9.8% 21 Missouri 9.3% 13 Montana 10.5% 27 Nebraska 11.5% 38 Nevada 9.6% 18 New Hampshire 9.6% 16 New Jersey 13.2% 45 New Mexico 10.2% 25 New York 15.9% 50 North Carolina 9.9% 23 North Dakota 8.8% 7 Ohio 10.0% 24 Oklahoma 9.0% 10 Oregon 10.8% 31 Pennsylvania 10.6% 28 Rhode Island 11.4% 36 South Carolina 8.9% 9 South Dakota 8.4% 4 Tennessee 7.6% 3 Texas 8.6% 6 Utah 12.1% 40 Vermont 13.6% 47 Virginia 12.5% 43 Washington 10.7% 30 West Virginia 9.8% 22 Wisconsin 10.9% 32 Wyoming 7.5% 2

properties of equal market values incurring vastly different tax liabilities. This horizontal inequality tended to inhibit sales by those with longstanding tenure and impose higher taxes on newcomers and younger homeowners. These conditions led a taxpayer to take the matter to the U.S. Supreme Court contending that such a scheme violated the Equal Protection Clause of the U.S. Constitution (Nordlinger v. Hahn). The court ruled for the assessor, affirming the Prop 13 limitations. Thus, the unequal treatment of homeowners persists in California.

This history suggests that those advocating tax policy changes should examine anticipated outcomes before adopting particular measures to avoid unintended consequences. A review of economic studies suggests that evaluation of alternative tax policies should consider the following issues:

• Will it provide an adequate tax base to support the budgeted activity at an acceptable rate?

• Will the tax inflict a minimal distortion to the signals guiding economic decision-making?

• Will the tax system be readily understandable?

• Will the tax policy be regarded as “fair”?

Scan the QR code to see Texas Real Estate Research Center publication 2037, Property Taxes: The Bad, The Good, and the Ugly, for a discussion of these criteria.

Total tax levies by the various taxing entities in Texas from 1985 through 2021 are shown in Figure 1. In 2021, the $38.9 billion school tax levy represented 53 percent of the total, down from 60.3 percent in 2005 and from 54.9 percent in 2013. Obviously, school taxes still compose the major portion of property taxes statewide.

Consider the index of tax levies adjusted for inflation to 1994 dollars (Figure 2). Values greater than one indicate a real increase in tax revenues. At 2.514, school tax levies have more than doubled (approximately 2.5 times) in real terms since

1994. Other units’ levies have increased by even more since that time. From 1994 through 2005, school levies increased faster than other units.

Tax relief measures taking hold in 2007 halted that trend. School tax rate compression legislation that passed in 2019 also curbed the increases, whereas the rate growth peaked in 2020 at 2.6 times the 1994 level. The 2021 rate fell just below the 2019 level of 2.521. Special district levies, fueled in part by the addition of numerous groundwater conservation districts after 1997 and not being restrained by the same rate rules that apply to cities, counties, and schools, expanded most rapidly from 2005 to 2013 and then again from 2016 to 2021. Both city and county total levies also expanded rapidly from 2005 through 2008. From 2009 through 2011, levies did not grow for cities, counties, and schools. However, in 2012, cities, counties, and schools began to expand their total levies once more until 2019 (or 2020, when the 2019 legislation took effect).

These expanding numbers reflect the combined influence of local growth and local decisions to provide more revenue to the various taxing units. Some, perhaps a major share, of the expansion of special district levies can be traced to the implementation of statewide water policy provisions in response to regional water planning. Arguably, supporting this planning effort involves prudent outlays designed to provide water for future generations of Texans. Increasing city and county levies reflect individual local governmental decisions to pursue activities requiring local public expenditures. These locally focused actions presumably address concerns of the local citizenry.

Possible Effects of Appraisal Cap Reductions in Texas

The Texas Real Estate Research Center conducted a comparative static analysis of the potential tax shifting effects of proposed property tax reforms envisioned in HB 2 of the 2023

21 SUMMER 2023

Billions of Dollars 80 70 60 50 40 30 20 10 0

Source:

School Levy City Levy

Levy Special Purpose District Levy 1985 1989 1993 1997 2001 2005 2009 2013 2017 2021 1994 1997 2000 2003 2006 2009 2012 2015 2018 2021 Billions of Dollars 4.0 3.5 3.0 2.5 2.0 1.5 1.0 0.5 0.0

Figure 1. Texas Property Tax Levies by Taxing Unit

Texas Comptroller of Public Accounts

County

Figure 2. Trends in Texas Tax Levies by Taxing Unit

Note: Index of Texas deflated tax levies by taxing unit 1994 = 1.0

Source: Texas Comptroller of Public Accounts

Special District Levy County Levy City Levy School Levy

Texas regular legislative session. This included school tax rate compression and a more broadly applied 5 percent appraisal cap.

As shown in the appendix (see QR code and note below), though the school tax rate would be reduced, the proposed appraisal cap would most likely lead to higher tax rates imposed by cities and counties because of the more limited tax base. Applying the new total tax rate to the indicated adjusted taxable values for each property category reveals how the tax burden would shift among properties post reform. Singlefamily homestead taxpayers would see a 7.8 percent reduction in taxes. Other real estate property (as defined in the appendix) owners would experience a 10.1 percent reduction while personal property and all other property category taxpayers would face a 2 percent increase in property taxes.

However, these estimates do not account for the new construction exempted from the value cap. Adjusting the potential value loss to the 5 percent cap to 80 percent of total in the initial estimates allows an evaluation of the potential effects of new construction in these shifts. Reducing the cap loss would result in a 6.2 percent decrease for single-family homesteads, a nearly 11 percent decrease for other real estate, and a 1.6 percent increase for all other taxpayers.

Expected impacts by property category in the first year:

These estimates illustrate the shifting effects that would accompany the imposition of the 5 percent cap along with a 15-cent tax rate compression. Homeowners and other real estate owners would benefit at the expense of other property owners, including rural landowners, who would see tax increases as well. This is the expected impact in the first year following such a policy change, assuming similar market conditions as 2022. However, as previously explained, the outcomes in the years following will be varied, and impacts on homeowners will vary based on local market conditions and length of ownership.

Scan the QR code to see the online version of this article, which includes an appendix for additional analysis assumptions and calculations.

Weighing Merits and Potential Impacts of Reducing Property Taxes

When weighing the merits of proposed policy changes, Texans should keep in mind the criteria of an effective and efficient

tax previously listed and the redistributive impact of appraisal caps shown in this analysis.

Currently, some citizens argue that the property tax base as it is configured does not provide adequate funding at a reasonable tax rate. Further restricting tax caps would aggravate that situation. A restrictive cap, such as the one California has adopted, could eventually foster noticeable and growing distortions to the efficient operation of housing markets.

Attempting to reduce tax liabilities by capping appraisal increases multiplies inconsistencies in the tax system over time. Furthermore, appraisal caps do not necessarily reduce tax liabilities proportionately. Although Californians decided that unequal treatment of homeowners is justified, Texans need to carefully weigh these long-term effects resulting from tightened caps.

In addition to these factors, imposing the cost of supplying public goods on those enjoying them through higher taxes causes taxpayers to weigh cost and benefits before supporting spending measures. Reducing tax burdens for homeowners, arguably the main beneficiaries of local government expenditure, could bias them in favor of more spending because they bear a lesser burden than they would face without the caps.

As the debate over high property tax burdens progresses, Texans should be cautious to avoid even larger problems for the future.

22 TG

-6.2%

taxes -10.98% Personal

+1.62%

Single-family residential taxes

Other real property (as defined in appendix)

property and all other property taxes

Dr. Gilliland (c-gilliland@tamu.edu) and Dr. Krebs (lkrebs@tamu.edu) are research economists with the Texas Real Estate Research Center at Texas A&M University.

A Bum ide o p

Growth in Texas industrial markets has been uneven over the business cycle. That growth has also been more consistent in some markets than others with the I-35 corridor and oil-related metros outgrowing the rest of the state.

By Daniel Oney

Texas is a large, diversified state boasting the ninth largest economy in the world. At $2.4 trillion, its gross state product accounts for almost 10 percent of all economic activity in the U.S. In an economy of such size, it should be no surprise that parts of the state perform better than others. One example is the wide-ranging performance of industrial real estate in the state’s 25 Metropolitan Statistical Areas (MSAs) during the last 40 years.