Recreational, high-tech toys and small vehicles are fun, but watch out! Insurance coverage for them can vary, resulting in significant out-of-pocket costs. Find out how.

Collision Course

Insuring Drones, Boats, and Other Recreational Toys

Workplace Wellness | 2

How Healthy Work Environments Can Benefit Tenants and Brokers

Is your office building in need of a checkup? Studies suggest a healthy workspace can benefit both commercial building owners and their tenants. Harold D. Hunt, Stephen A. Ramseur, and Bucky Banks

20 | Where Should My New House Go?

Using Surveys to Avoid Legal Entanglements

A survey is much more than just a box you have to check off when improving a piece of property. If properly done, it can help you make informed decisions and avoid potential legal headaches. Reid Wilson

Executive Director, PAMELA CANON

Research Director, DANIEL ONEY

Director of Operations, JAMES LAIRD

Director of Strategic Initiatives, GARY W. MALER

Director of Communications, BRYAN POPE

Creative Manager, ALDEN DeMOSS

Graphic Designer, ROBERT P. BEALS II

Circulation Manager, RYAN PERRY

Lithography, RR DONNELLEY, HOUSTON

6 | The Verdict Is In Legal Industry Key to Texas Office Markets

If it pleases the court, TRERC Research Director Daniel Oney presents overwhelming evidence showing how the legal industry is a major driver in the state’s office markets. Daniel Oney

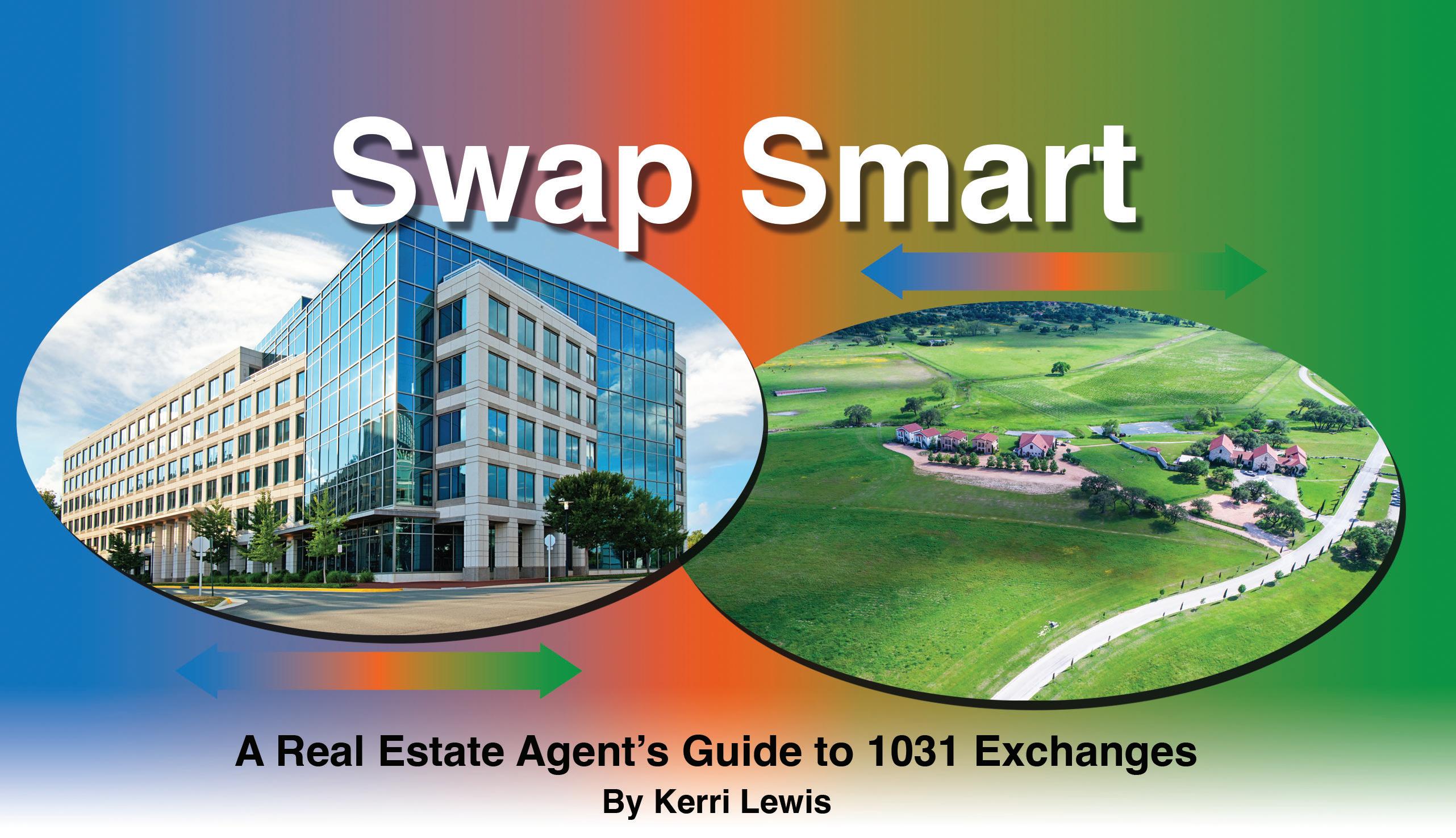

11 | Swap Smart

A Real Estate Agent’s Guide to 1031 Exchanges

A like-kind exchange is a powerful tax-deferment strategy for commercial investors, but there are nuances that real estate professionals need to understand to better help their clients. Kerri Lewis

14

|

Where There’s Smoke

Climate Change, Population Growth, and Wildfires

Over the years, Texas wildfires have resulted in the tragic loss of life, loss of thousands of homes, and billions of dollar in direct economic impact. What can be done to mitigate this? Wesley Miller and N. Lee May

In what will likely be regarded as the watershed legal moment of 2024, the U.S. Supreme Court has overruled the Chevron doctrine. Here’s what you need to know. Rusty Adams

ADVISORY COMMITTEE: Doug Foster, San Antonio, presiding officer; Besa Martin, Boerne, assistant presiding officer; Troy C. Alley, Jr., Arlington; Kristi Davis, Carrollton; Vicki Fullerton, The Woodlands; Patrick Geddes, Dallas; Harry Gibbs, Georgetown; Doug Jennings, Fort Worth; Rebecca “Becky” Vajdak, Temple; and Barbara Russell, Denton, ex-officio representing the Texas Real Estate Commission. TG (ISSN 1070-0234), formerly Tierra Grande magazine, is published quarterly by the Texas Real Estate Research Center at Texas A&M University, College Station, Texas 77843-2115.

VIEWS EXPRESSED are those of the authors and do not imply endorsement by the Texas Real Estate Research Center, Division of Research, or Texas A&M University. The Texas A&M University System serves people of all ages, regardless of socioeconomic level, race, color, sex, religion, disability, or national origin. Nothing in this publication should be construed as legal or tax advice. For specific advice, consult an attorney and/or a tax professional.

PHOTOGRAPHY/ILLUSTRATIONS: Center files, pp. 1 (top), 6, 8, 11-13, 23, 24, 26; JP Beato III, pp. 1 (bottom), 20-21, 22; Alden DeMoss, p. 5; Robert Beals II, pp. 14-15, 16-17; Bryan Pope, p. 19.

ON THE COVER: Caprock Canyons State Park embodies the natural beauty of the Texas Panhandle, a region that, in 2024, saw some of the most devastating wildfires in the state’s history. Photograph from Center files.

WELLNESSPLACE WORK

How Healthy Work Environments Can Benefit Tenants and Brokers

By Harold D. Hunt, Stephen A. Ramseur, and Bucky Banks

Key Takeaways

• Healthy buildings support physical, psychological, and social well-being, which can enhance productivity and employee engagement.

• Investments in healthy building strategies can lead to higher rent premiums and property values.

• There is growing demand from tenants for office spaces that prioritize health and well-being.

• Brokers who understand and promote healthy building features can gain a competitive edge.

Focusing on healthy buildings can make sense for commercial real estate brokers. Providing workers with office space that provides an optimal indoor environment could be one piece of the return-to-office puzzle as well as an economic opportunity.

The office asset class has been resilient for decades. Workers need an indoor environment to collaborate, think, and create. Business leaders, competing for top-tier talent, often view office space as a perk. Investors seek stable, long-term returns. However, these stalwart assumptions have been tested over the past three years, posing a threat to the office asset class. Office use hovers just above 50 percent of pre-pandemic levels according to research by CoStar, with national occupancy levels still near historic lows. As a result, these trends are negatively impacting brokerage commissions. According to a survey funded by

the Environmental Protection Agency (EPA), office workers spend up to 90 percent of their time indoors. The experience can significantly impact physical, emotional, and even spiritual well-being. Studies have shown that health-related changes implemented during a building’s construction, renovation, or operation can have disproportionately positive effects on workers. Could the science of healthy buildings be a knight in shining armor for real estate professionals? The research seems to show that it can be.

WHAT IS A HEALTHY BUILDING?

A healthy building is a space that supports the physical, psychological, and social health and well-being of workers—a space where they can be safe, comfortable, and productive. Worker well-being can be significantly improved, facilitating more and better

engagement, community, and interaction. When healthy building factors are not optimally aligned, the result can be Sick Building Syndrome (SBS), a term that began appearing in research in the early 1980s.

The EPA defines SBS as a situation where building occupants experience adverse acute health and comfort effects that appear to be linked to time spent indoors. Such underperforming environments can negatively impact a person’s health and a company’s bottom line. Poor environmental conditions in the workplace have been found to reduce employee productivity, with losses of up to 10 percent reported. Harvard researchers have discovered that enhanced indoor air quality can increase cognitive function by 61 to 101 percent, depending on the level of enhancement.

A2022 study by the International WELL Building Institute (WBI) found that the U.S. loses more than 175 million workdays and $150 billion every year from sickness-related absenteeism. A 20 to 50 percent reduction in SBS symptoms for office workers would produce an annual productivity gain of $20 billion to $200 billion in the U.S. according to the Indoor Air Quality Handbook

HOW CAN BUILDINGS BE HEALTHY?

Nine foundations of a healthy building have been defined by the Healthy Buildings Program at the Harvard T.H. Chan School of Public Health, led by Dr. Joseph Allen. Each of these elements can contribute to employees’ well-being and productivity as well as a company’s bottom line. The nine foundations are: 1) ventilation, 2) air quality, 3) lighting and views, 4) thermal heat, 5) noise, 6) moisture, 7) water quality, 8) dust and pests, and 9) safety and security (see sidebar for further reading).

Biophilic design has also emerged as a component of healthy buildings since 2015, when research by Yale Professor Stephen Kellert found that integrating natural elements such as indoor plants, outdoor gardens, natural light, water features, wood, and stone into built environments can enhance worker well-being. Biophilia is defined as the human tendency to interact or be closely associated with other forms of life in nature.

Kellert found that participants in biophilic indoor environments had consistently better recovery responses than those in the non-biophilic environment in terms of reducing stress and

Reference Material for Further Learning

The 9 Foundations of a Healthy Building

How Do We Make Healthy Buildings the Next Public Health Revolution?

Investing in Health Pays Back

anxiety. Specifically, Kellert found that participants recovered from reactions to stress such as heart rate variability and increases in blood pressure almost immediately after exposure to biophilic environments. The research can be a tool for architects, interior designers, and developers to increase well-being in office workers.

BENEFIT TO BROKERS

Brokers may want to become proactive and promote air quality and other healthy building factors upfront as a selling point to create a competitive advantage. Analysis by JLL indicates that demand for newer, high-quality properties continues to generate better economics, but supply is thinning due to a lack of new office development. Opportunities exist for brokers in the current market to identify office buildings in superior locations where healthy building factors can be used to attract high-quality tenants. Companies have become more willing to invest in high-quality space to make office destinations worthy of a commute.

Properties proactively designed and built to support the holistic health of their occupants are expected to reach $913 billion in the next four years, up from $438 billion in 2023, according to the Global Wellness Institute. A 2020 study by MIT’s Real Estate Innovation Lab found that effective rents for healthy buildings were 4.4 to 7.7 percent higher per square foot than those for buildings not classified as healthy in major U.S. cities. When polled by JLL, 71 percent of the workforce reported that they would like to work in office space that promotes a healthy lifestyle, safety, and well-being. However, only 21 percent stated that their employer is providing them with acceptable health and well-being solutions in their office environment.

Brokers should be aware that the

impact of technology on healthy office environments will only escalate. More workers have begun to bring their own sensors to the office to measure indoor environments. Websites like Glassdoor, a job search and career community platform, are also offering potential tenants and investors more detailed information about individual office properties. As a result, healthy buildings are becoming a risk-management tool for companies.

BENEFIT TO TENANTS

Why does employee engagement matter to tenants? According to analytics and advisory firm Gallup, which specializes in understanding and analyzing human behavior, engaged employees have higher well-being, better retention, lower absenteeism, and higher productivity. Their ongoing employee engagement survey has reported that highly engaged teams outperform others in business outcomes critical to the success of an organization. Annual employment engagement in the U.S. overall was estimated at 33 percent while engagement at bestpractice organizations registered 70 percent.

According to Gartner, a leading research and advisory company that provides insights, advice, and tools for business leaders, 96 percent of human resource leaders are more concerned about employees’ well-being today than before the pandemic. The global pandemic has forced corporate leaders to reassess every aspect of why, where, and how people work. Hybrid work is here to stay, and employees can select their work modality more than ever before. Positioning a healthy building at the center of a company’s workplace strategy can be another method employers use to lure workers back to the office.

According to the WBI, healthy build-

ing solutions can yield significant, economy-wide financial gains. These include an annual productivity gain of up to $200 billion, corresponding to a 20 to 50 percent reduction in SBS symptoms for office workers in the U.S. The same study estimated $38 billion in annual economic benefits by just increasing minimum ventilation rates in U.S. office buildings from 8 to 15 liters per second. Thus, corporations that occupy healthy buildings can improve employee performance along with their bottom line while contributing to their community’s overall well-being.

BENEFIT TO OFFICE LANDLORDS/ INVESTORS/OWNERS

Why should healthy buildings matter to office building owners and investors? Older office buildings are experiencing much more severe occupancy losses than newer properties. Since the beginning of 2020, buildings older than ten years have lost nearly 420 million square feet of occupancy nationally, according to CoStar. This suggests that office tenants today prefer new office buildings more than they have in the past. Tenants have become focused on landlords who are able to put additional capital into the buildings to help draw employees back.

Research has indicated a strong relationship between healthy building strategies and enhanced rent premiums and property values. MIT researchers examined this relationship in the Boston office market and found sizable rent premiums. Their results showed that buildings pursuing a healthy building standard such as WELL captured higher effective rents of 4.4 to 7.7 percent more per square foot when compared to nearby properties without healthy building standards.

Furthermore, the WBI found that

more biophilia in office properties created a 5.6 to 7.8 percent rent premium for offices in New York City. A 5 to 6 percent rent premium was reported for office spaces with high levels of natural light as well.

WHAT THE FUTURE HOLDS

Multiple sources believe the U.S. office market will have more than 300 million square feet of vacant or obsolete office space by 2030. Brokers who understand the dynamics of a healthy building will have a competitive advantage, resulting in more

commissions. Landlords and employers assumed that increased amenities would draw workers back to the office. However, it hasn’t been that simple. More and more, workers are demanding a healthy office environment. Recent data also indicate an uptick in workers returning to the office. As more workers return, healthy buildings will become increasingly important. Landlords, investors, and developers can invest targeted CapEx in the nine foundations of healthy buildings as another tool to make coming to the office attractive again. They should plan for a world where buyers and ten-

ants know all about the performance of their office space. Thus, health and human performance should be factored into the cost/benefit analysis and decisions impacting today’s office space.

Harold D. Hunt, Ph.D. (hhunt@tamu. edu) is a research economist with the Texas Real Estate Research Center; Bucky Banks (bbanks@mays.tamu.edu) is associate director and executive assistant professor for Texas A&M’s Master of Real Estate program in Mays Business School; and Stephen A. Ramseur is executive professor for Texas A&M’s Master of Real Estate program and holds the Julio S. LaGuarta Professorship in Real Estate.

425 Park Avenue, New York City

A recent, real-world example of a healthy office space is the 47-story, 667,000-square-foot trophy building at 425 Park Avenue in New York City. Completed in October 2022, this crown jewel in the Midtown Manhattan Plaza District has attracted world-class tenants not only because of its superior location and architecture, but also because of its status as New York’s first WELL-certified building. The building’s design optimizes natural light, air circulation, and other health-related factors that contributed to the designation.

The New York Post reported in 2020 that the building is the first in the city to have a WELL designation, which relates to the health of the occupants, whereas LEED is focused on the environmentally friendliness of the structure. Depending on the floor and square footage, annual asking rents posted on Metro Manhattan Office Space range from $225 to $245 per square foot for the remaining available lease spaces between 6,000 and 14,000 square feet. This represents a significant premium over average Class A office space in that market. Statista reported that the average annual asking rent for Class A office space in the Plaza District of Midtown Manhattan on Park Avenue for lease space between 6,000 and 14,000 square feet was $95.13 per square foot in April 2024.

The Verdict Is In Legal Industry Key to Texas Office Markets

By Daniel Oney

Key Takeaways

• Texas law firms lease over 14 million square feet of office space, mainly in downtown areas, making them pivotal tenants in the state’s office markets.

• Unlike many businesses, law firms have favored conservative office setups with private offices, reflecting their emphasis on prestige and confidentiality.

• Texas’ legal services sector is growing faster than the national average, boosting demand for office space, especially in larger cities.

• Law firms are adopting hybrid work policies and rethinking office layouts to optimize space and attract talent, despite traditionally conservative practices.

The legal industry has been growing slowly across the country, but much faster in Texas. The industry is a substantial employer in the state, with over 104,000 jobs by spring of 2024. Job growth in the legal services industry, which includes a few small sectors beyond law firms, has accelerated. Both before and after COVID, legal services grew faster in Texas than they did nationally. The industry also grew faster than Texas’ overall payroll employment (Figure 1).

The number of Texas law firms also increased. In the last decade the number of firms grew 13.3 percent (about 1.3 percent annually).

Firms with payroll employees now total almost 14,600 statewide. Despite this growth, the industry is less concentrated in Texas than it is nationally. Legal service employment is only 97 percent as prevalent in the state

as it is nationally. This growth means positive demand for office markets. Beyond raw growth, the structure of the industry also impacts office demand.

Mid-size and large firms are prime tenants taking down large blocks of downtown office space, but these firms are few in number. Most law firms are small (Figure 2), and they play an important role in many submarkets. Of the 41,000 Texas firms, 64 percent are single-person firms (that is, self-employed attorneys). Two-thirds of the 15,000 remain-

Post-COVID CAGR (since March 2020) CAGR (since March 2023) Pre-COVID CAGR (5-year to March 2020)

Figure 1. Texas’ legal services jobs outgrow the nation’s and Texas’ overall job growth

Figure 2. The vast majority of law firms are small

Texas Law firm employment has grown faster than number of firms

Source: Texas Real Estate Research Center analysis of Texas Workforce Commission data

ing establishments have fewer than five employees. Law firm size has increased slightly since COVID, and law firm employment has grown faster than the number of firms (Table 1).

Small firms with employees are likely to lease at least some office space. Self-employed attorneys have more options. They may work from home or at client locations, or they may pay for coworking or old-fashioned executive suites. Virtual offices are common. These arrangements provide a mailing address in a conventional building with on-demand access to conference and meeting room space. Some selfemployed attorneys sublet a desk at

larger firms. Cumulatively, small firms likely account for many millions of square feet of office space use, but in small increments.

The mix of employees in law firms represents ongoing changes in legal work and the adoption of technology. These occupational trends also impact the layout of offices and the total market demand for office space. In Texas, the industry has seen some changes in the mix of job types.

The top six occupations in legal services remained the same in 2019 and 2023 (Table 2), but all six made up a smaller share of total legal services employment in 2023. Legal

secretaries had the largest percent decrease in their share of total legal jobs at 2.6. This was followed by a 2 percent share fall for attorneys (even though the total number of attorneys increased). General clerks’ and paralegals’ shares fell by 1.6 and 1.4 percent, respectively. Bookkeepers, administrative supervisors, and general managers saw their shares of total employment grow. (See appendix in online version for a comparison of the Texas and U.S. legal workforce.)

The legal industry has, on the whole, grown in Texas, but the situation differs from market to market (Figure 3). Legal industry employment growth is associated with overall Metropolitan Statistical Area (MSA) job growth, as exhibited by the upward-sloping pattern. The largest metropolitan areas have the largest legal employment, and they tend to have faster-growing legal employment than smaller MSAs. Many smaller MSAs have lost legal services jobs.

While the industry in Texas overall is less concentrated than it is nationally, three Texas metros have a higherthan-national-average concentration: Corpus Christi, Houston, and Austin. These MSAs have location quotients (LQ) of 1.44, 1.23, and 1.04, respectively. All other Texas metro areas have a lower-than-average concentration. (See appendix in online version for details about each metro’s legal industry.)

A generally growing legal industry is a bright spot for office markets, but how these macro trends translate into net new demand will depend on law firms’ workplace and workspace policies.

Workplace and Workspace Trends

Note: Red indicates a smaller share in 2023 than in 2019, while green indicates a larger share. Source:

Firm business models, technology choices, staffing strategies, and

Table 2. Core legal occupations

Table 1.

Workplace Policies and Workspace Policies: What’s the Difference?

Workplace decisions apply to people, and workspace decisions apply to the physical environment where work happens. However, workplace policies generally influence workspace decisions, meaning they can impact demand for space in the market.

For example, a firm may adopt a hybrid workplace policy allowing employees to work remotely some days each week. In response, the firm may adjust its workspace by reducing the number of dedicated offices and adding “drop-in” or coworking spaces.

Another common example with large firms is to convert underused space or add new space to create more common-area amenities to improve its talent attraction and retention.

client location and activity ultimately determine demand for space. These influence factors like the location, amount, and quality of space leased. Before COVID, law firms were slowly rethinking their real estate policies. Firms realized they were underusing their space. Employee travel and early, limited work-from-home policies meant vacant offices many days of the week. For a generation at least, new technology had also been changing legal work. Personal computers and new habits by younger associates allowed firms to reduce the ratio of support staff.

More recently, e-discovery tools lowered the demand for associates. Support staff per attorney has fallen nationally to one per five, with reports of as few as one per seven onsite support staff in some firms, according to international construction firm Stantec. With fewer staff and a different mix of occupations within the firm, workspace impacts were inevitable. The amount of space allotted per attorney began falling across major markets long

Evolving Law Firm

Traditional Workplace

(maintained by many local firms, especially small ones)

Emerging Workplace

(common among large firms, even pre-COVID) “Extreme” Workplace (still rare)

Sources:

Christi

Source: Texas Real Estate Research Center analysis of U.S. Bureau of Labor Statistics and Texas Workforce Commission data

Figure 3. Legal industry is more concentrated and growing faster in the larger metro areas

2010-14 2015-19

695 to 1536 sf 675 to 1200 sf 619 to 935 sf

Note: Numbers represent the low and high values in Atlanta, Boston, Chicago, Dallas, Los Angeles, Miami, New York, Philadelphia, San Francisco, and Washington D.C.

Source: Newmark

before COVID (Table 3). The high-end range estimate fell by 39 percent, while the low end saw a less dramatic drop of only 11 percent. This implies firms across markets are adopting similar, smaller space-use policies.

COVID had a major impact on law firms’ real estate choices, as it did with all office users. As a conservative workspace policy industry, law offices across the country tended to use space the way their peers did. Major brokerages and architecture firm’s post-COVID experience shows law firms are now more likely to adopt a custom real estate strategy. Still, a few major themes have emerged.

Location and lease decisions are similar pre- and post-COVID. The largest law offices in Texas are overwhelmingly concentrated in downtown areas (for quick access to courthouses). Of the 53 offices with at least 50 attorneys, only three are outside of a downtown-area ZIP code. Lease

renewals before and after COVID remain less likely than relocations, and relocation leases are becoming more common, according to Cresa and CoStar. With much underused office space—and with many new trophy buildings delivered—firms can redefine workspace policies, improve efficiency, and rebrand for better talent attraction and retention.

Legal workplace policies mean better use of office space than by other industries. In early 2024, law firms’ space usage was 25 percent higher than the overall office sector at nearly 80 percent of pre-COVID levels, according to Kastle Systems. CBRE’s recent national survey of law firms found a spectrum of remote work policies in place. The most common policy was “primarily in-office” (3+ days a week in-office), a policy held by 47 percent of firms. This was followed by 28 percent with a “balanced” policy (equal days in- and out-of-office.) Fourteen percent were

Workplace and Workspace Models

In-office policy.

Many private offices for attorneys and senior staff. Senior attorneys along perimeter with windows. Staff members occupy open cubicles/desks.

Technology (e.g., AV, data) enabled only in board or conference rooms.

Desk-sharing is uncommon.

Hybrid work policy. Some desksharing for attorneys and staff; dedicated back-of-office hybrid/collaborative workspace. Standard size offices.

Fully flexible work-from-home policies.

“fully/primarily remote” (3+ days out-of-office). Eleven percent are fully in-office. Larger firms have more flexible policies than mid-size and small firms. Hybrid work policies seem entrenched.

Firms are adopting new workspace models, and the trend of everfalling space per attorney seems to be leveling off. Nationally, the evidence is mixed, but JLL reports that slightly more firms have taken less space in their new leases. This has been especially true of larger firms. Smaller firms have been as likely to add space as reduce it. Other space policies are notable. Law libraries and physical filing rooms are frequently converted to common amenity spaces like lounges or cafes or collaborative workspace. Nationally, universal office sizes for attorneys and senior professional staff are more common than not. This tactic increases flexibility to accommodate firm growth and attorney career progression. Refits or new finish-outs can demise floors in ways that allow easier subleases. Some large firms have bi-

Front-of-office spaces double for clients and teamwork. “Conservative” finishes (hardwoods, brass fixtures, overstuffed furniture, etc.).

More physical transparency and natural light across floorplate. “Technology” (AV, data) enabled throughout the workplace.

Multi-purpose training rooms for mock trials, case strategy; virtual courtrooms. More “modern” style furniture and fixtures with more attention to function and ergonomics.

Minimum onsite support staff (offsite in lower-cost location or work-from-home).

Open floor plans, hoteling, and desk sharing for most attorneys.

Many small collaboration spaces accommodating changing in-office teams and remote collaboration with clients and colleagues anywhere.

Table

firms

furcated their portfolio. They may have showcase offices in major markets and maintain simpler, working offices in low-cost cities for associates and administrative pools.

Law firms are in the driver’s seat and can take a more aggressive stance with landlords. Office oversupply in recent years makes this a tenant’s market. Firms are seeking and winning more flexible lease terms, significant free rent, and ample tenant improvements. Results vary by market, but one rent-free month per lease year and tenant improvements of between $90 and $150 per square foot are typical, according to Colliers. Owners of older buildings have accepted shorter leases than they preferred.

Texas Leasing Trends

Leasing behavior of Texas law firms has changed according to an analysis of 478 large law firm leases. Large leases are defined as those for more than 10,000 square feet and for tenants with at least 25 employees. These leases totaled almost 14.2 million square feet of office space spread across 14 of the state’s 25 metropolitan areas. DFW accounted for the most space at 5.9 million square feet, followed by Houston with 5.4 million, Austin with 1.6 million, and San Antonio with 700,000. The remaining 500,000 square feet were spread among ten smaller metro areas.

An analysis limited to a subset of large leases signed five years before and in the 51 months since April 2020 gives a preand post-COVID snapshot (Table 4.) Since COVID, there have been 49 fewer large leases than there were in the years before. There have been fewer leases per year since, and this likely reflects many firms still holding long pre-COVID leases. Post-COVID leases totaled 2.7 million square feet compared with 3.7 million square feet before. This resulted in larger average leases in recent years. Leased space per employee (not just attorneys) has, however, fallen by almost 100 square feet to 223. When evaluated year by year, however, more details emerge. The declining preCOVID space-use trend is reversing. Average space per employee has risen again in recent years (Figure 4). It is not clear whether this represents a new normal for law firms or is simply opportunistic behavior by firms while landlords are eager to close deals. Meanwhile, rents are higher and reflect moves to new, high-amenity, Class

A spaces rather than general rent increases (Figure 5).

The flight to quality began before COVID. After the Financial Crisis, as office construction resumed in most markets, law firms began moving to newer buildings. Nationally,

these shifts led to firms paying over 20 percent more rent per square foot from 2015 to 2019 than in the prior five years. In Texas, the increase was not so dramatic, but, starting in 2018, law firm leases’ average rent rates began increasing after years of flat rents.

Anchoring Texas Office Markets

Law firms remain anchors for Texas office markets. In coming years it should be a net positive for office demand.

Overall industry growth will offset the tendency for some firms to economize space. The distinctives of legal work—its hierarchical culture, its confidential content, and its dependence on downtown—means it will long maintain more “traditional” workplace and workspace practices than other office users.

The industry cannot revive anemic office markets alone, but, for some landlords, law firms will remain essential tenants on their rent rolls.

Daniel Oney, Ph.D. (doney@tamu.edu) is research director with the Texas Real Estate Research Center.

Figure 5. Law average rents increased slightly before COVID and jumped dramatically since

Figure 4. Texas’ leased space per employee has increased after long-term decreases

Table 4. Fewer, larger, higher-rent leases after COVID

Key Takeaways

• “Like-kind” refers to the nature or character of the property, not its type.

• Educate clients on the benefits of 1031 exchanges, including potential tax advantages and investment opportunities.

• Assist clients in identifying suitable replacement properties considering values, rental income, and market trends.

• Connect clients with reputable qualified intermediaries who ensure IRS compliance and refer them to experienced tax advisors and attorneys for handling complex tax and legal aspects.

• Ensure contracts allow for necessary adjustments and cooperation.

A1031 exchange, named after Section 1031 of the Internal Revenue Code, is a powerful tax-deferment strategy used by real estate investors when selling investment property. It allows an investor to defer paying capital gains taxes on the sale of certain types of investment property by reinvesting the proceeds into a similar property. That is why a 1031 exchange is commonly referred to as a “like-kind” exchange. The primary purpose of a 1031 exchange is to encourage investment, stimulate economic activity, and foster liquidity in the real estate market.

Real estate agents play a vital role in helping clients navigate the complexities of 1031 exchanges. Here are several ways they can support their clients throughout this process.

Know the Basics

What Types of Properties are Eligible?

To qualify for a 1031 exchange, the property being sold (referred to as the relinquished property) and the property being purchased or “exchanged” (referred to as the replacement property) must be held for investment, business, or productive use in a trade

or business. Personal residences and properties for personal use, such as vacation homes or hunting ranches, do not qualify. Property held for inventory, such as property bought to fix and sell, or just to sell in the future, is not eligible for a 1031 exchange. Also note that property within the United States cannot be exchanged with property outside the country. Interestingly, though, a foreign property can be exchanged for another foreign property.

Here are some common types of investment or trade/business properties that qualify for a 1031 exchange:

• Residential rental properties, including apartment buildings, duplexes, and single-family homes used for rental purposes.

• Commercial properties such as office buildings, shopping centers, and retail stores.

• Industrial properties such as warehouses and manufacturing facilities.

• Raw land that is unimproved and that can be used for investment purposes.

• Ranches, which are generally large tracts of land used for agricultural purposes.

What are the Requirements for a Like-Kind Exchange?

The concept of like-kind in a 1031 exchange is often misunderstood to mean that the properties being exchanged must be identical or similar in type. However, this is not the case. Rather, like-kind refers to the nature or character of the property, rather than its specific type or form.

In simpler terms, the IRS does not require that the properties being exchanged be the same in terms of their physical attributes, such as size, shape, or location. Instead, what matters is the underlying nature or purpose of the properties involved in the exchange.

For example, in a 1031 exchange, a commercial office building could be exchanged for a retail shopping center, or vacant land could be exchanged for a rental apartment complex. Despite being distinct types of properties, they are considered like-kind because they are all held for investment, business, or productive use in a trade or business.

The historical significance of the term like-kind was more relevant prior to 2018 when several types of personal and intangible property, in addition to real estate, could be exchanged. Since 2018, only real estate is eligible for a 1031 exchange.

The broad interpretation of like-kind for real estate properties allows for flexibility in structuring 1031 exchanges and enables investors to diversify their real estate portfolios without being limited to specific property types. It also aligns with the underlying purpose of the 1031 exchange, which is to stimulate investment and promote liquidity in the real estate market by deferring taxes on property transactions.

How Does the Property’s Value Figure In?

To avoid taxes, the value of the replacement property must be greater than or equal to the value of the relinquished property. If the replacement

TO QUALIFY FOR A 1031 EXCHANGE, the property being sold and the property being purchased (or “exchanged”) must be held for investment, business, or productive use in a trade or business.

property is less than the value of the relinquished property, there may be taxes due on the excess value, also known as “boot.”

Educate Clients

Many property owners may not be familiar with the benefits of a 1031 exchange. Real estate agents who represent investor clients can educate their clients about the potential tax advantages and investment opportunities associated with 1031 exchanges. By raising awareness, agents can help clients make informed decisions about whether a 1031 exchange aligns with their goals.

Refer Clients to a Qualified Intermediary . .

To facilitate a 1031 exchange, investors typically engage a qualified intermediary (QI) who acts as a thirdparty facilitator to ensure compliance with IRS regulations. The QI holds the proceeds from the sale of the relinquished property and disburses them to acquire the replacement property. The seller cannot hold the proceeds from the relinquished property, or the seller will realize taxable gain. Agents can provide valuable guidance by connecting clients with reputable QIs who can navigate the

complexities of the exchange process. Make sure to research before recommending a QI. Check references. There is no state or federal agency that regulates or oversees QIs. While there are many good and reputable QIs, there are also stories of bad actors who have absconded with money that was entrusted to them.

. . .

and to Qualified Tax/ Legal Consultants

1031 exchanges involve complex tax and legal implications that require specialized expertise. Real estate agents cannot give legal or tax advice and should recommend their clients work closely with tax advisors, attorneys, and other professionals to ensure compliance with IRS regulations and optimize the tax benefits of the exchange. Again, having a list of good tax professionals to recommend to clients who do not already have their own will help the transaction go more smoothly and keep the real estate agent from being put in a position of being asked for advice outside of their expertise.

Identify Replacement Properties

One of the key requirements of a 1031 exchange is the identification and

acquisition of replacement properties within specific timelines. Real estate agents can assist clients in identifying suitable replacement properties that meet their investment criteria and like-kind exchange requirements. This may involve evaluating property values, rental income potential, location dynamics, and market trends. Agents can provide valuable insights and guidance to help clients make informed decisions when selecting replacement properties for their 1031 exchanges.

Track Key IRS Deadlines

The IRS imposes strict timelines on 1031 exchanges, and keeping track of their deadlines is of the utmost importance.

The investor must identify potential replacement properties within 45 days of the sale of the relinquished property and complete the exchange by acquiring the replacement property within 180 days. These days are counted in calendar days, and there is no extension if the last day lands on a holiday or weekend.

Act as Coordinator

Agents can coordinate with the title company, tax or law firm, and the QI on the relinquished property closing.

They can help ensure that net proceeds go directly to the QI, not the seller. Agents who are involved in the replacement property transaction can assist in coordination between all parties in the transaction as well.

Negotiate Contracts for Replacement Properties

Once suitable replacement properties have been identified, real estate agents can negotiate favorable terms and manage the transaction process on behalf of their clients.

Although the IRS does not require a reference to a 1031 exchange be present in the contracts for the relinquished or replacement properties, it is important to have two provisions in the contracts to avoid potential issues with the other parties to the contracts.

The first provision is for the seller of the relinquished property and the buyer of the replacement property to have the ability to assign the contracts to the QI. This can be achieved by simply adding “or Assigns” to the listed seller or buyer as applicable in the contracts. A term allowing assignment by the relevant party to a QI can also be added to the contracts under Special Provisions.

The second provision is to notify the other party of the intent to perform a

1031 exchange and getting agreement from the other party to cooperate as needed in that process. A provision holding the other party harmless from any costs or liabilities resulting from the exchange (a hold harmless provision) is also often included. If attorneys are involved in the process, they will provide the necessary language. In addition, many commercial contracts have 1031 exchange language in the boilerplate of the form. Many QIs can provide clients with the necessary language as well if they are involved at the front end of the process.

Remember, real estate agents can add business terms only to Special Provisions. Noting the intention of one party to perform a 1031 exchange and having the other party agree to cooperate is considered business terms. Drafting a hold harmless provision, however, might be considered the practice of law. Real estate agents should check with their broker about inserting language regarding a 1031 exchange. Some brokers have standard language they want their agents to use.

Finally, Empower Clients

By understanding how 1031 exchanges work, educating clients, and negotiating and facilitating transactions, agents can empower their clients to better achieve their investment goals.

Keep in mind that a 1031 exchange transaction is a specific type of real estate transaction, and, under TREC Rule 535.2(i)(5), the first three times a sales agent performs a new type of real estate brokerage activity, that agent must receive coaching and assistance from an experienced license holder competent in that particular kind of transaction. So, agents should talk to their broker before adding 1031 exchanges to the services they provide to clients.

Kerri Lewis (kerrilewis13@gmail. com) is a research fellow with the Texas Real Estate Research Center and a member of the State Bar of Texas and former general counsel for the Texas Real Estate Commission.

Development

Key Takeaways

• Eighty-five percent of Texas fires ignite within two miles of a community, and economic exposure is projected to increase due to climate change and population growth patterns.

• There are several ways the population can adapt to higher wildfire risk,

including self-protection activities and insurance. Some policies may encourage additional building development in risky areas.

• The potential to rebuild depends on factors such as underlying demand and the condition of local infrastructure.

Over the past decade, wildfire losses in the United States have reached unprecedented levels. Nine of the ten costliest American wildfires have occurred since 2017, and the annual economic cost of wildfire in North America continues to rise. More than 238,000 wildfires have burned 12.6 million acres in Texas since 2005. The recent Smokehouse Creek Fire burned more than one million acres in February and March, making it the largest wildfire in Texas history and topping the state’s list in terms of agricultural losses. The East Amarillo Complex Fire of 2006

caused the largest loss of life with 13 fatalities, and the Bastrop County Complex Fire ranks as the state’s most destructive, with 1,673 homes lost in 2011.

Texas has two primary wildfire seasons, each of which are characterized by distinct determinants and risks. The winter (or early spring) wildfire season is concentrated in the western half of the state and depends on precipitation during the preceding summer to facilitate growth of vegetative fuel. Winter weather tends to kill this vegetation (or induce dormancy), creating conditions ideal for ignition and burning. Seasonal winds contribute to potential ignition events and rapid spread during the winter and early spring. In contrast, Texas’ summer wildfire season impacts the entire state and largely depends on intense heat that sufficiently dries out vegetation between rainfall events. Hotter temperatures are projected to amplify wildfire risk across Texas, particularly in the western portion of the state. Rising precipitation levels in more eastern regions serve to offset the impact of hotter temperatures on wildfire risk, but warmer winters may shift the current geography of wildfire seasons.

In addition to the impacts of climate change, population and land-use patterns directly affect the likelihood of wildfires and the magnitude of destruction. Between 2005 and 2021, 85 percent of Texas wildfires were ignited within two miles of a community. This two-mile distance often describes the wildland-urban interface (WUI) zone (i.e., the area of transition between unoccupied land and human development). While the WUI is a major source of ignition, it also carries complex challenges in terms of wildfire suppression. For example, wildland firefighting techniques and equipment emphasize the protection of natural resources, while structural firefighting focuses on saving human life and the built environment. The transitional nature of the WUI presents additional complexities in terms of

political, economic, and social dimensions, all of which affect investment in resilient infrastructure as well as potential disaster recovery.

Explosive Growth in the WUI

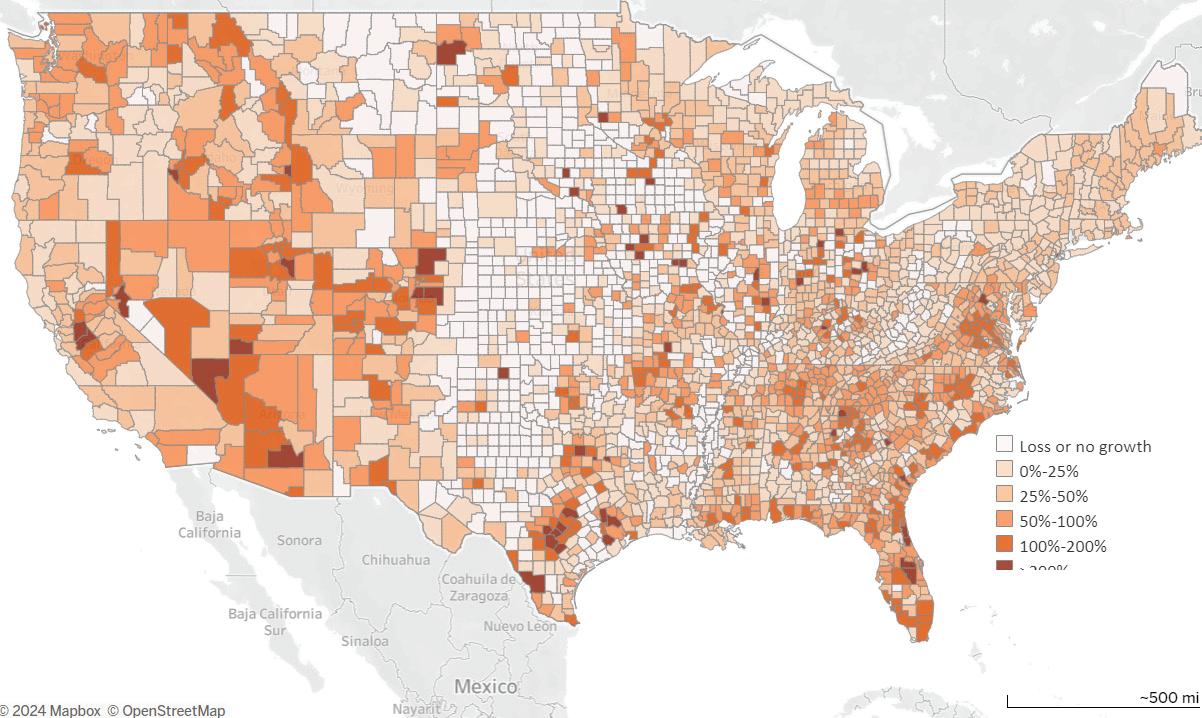

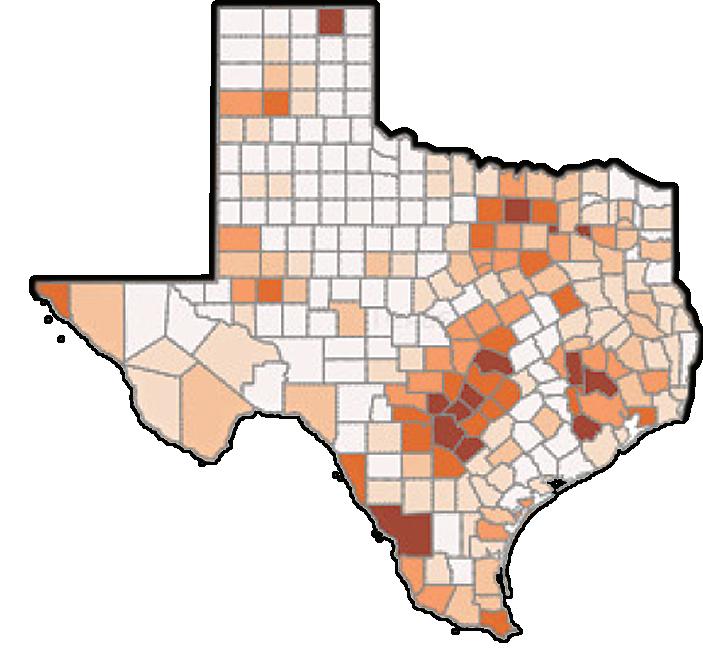

The Texas WUI stretches across 11 million acres and contains 3.2 million housing units (ranking second nationally behind California). More than 25 percent of Texas homes lie in the WUI, underscoring the significant intersection of residential development and the natural environment. While total land mass correlates with absolute rankings, the number of housing units in Texas’ WUI increased 82 percent from 1990 to 2020, outpacing 42 of the 48 contiguous states. Rapid development in the WUI exceeded statewide growth in housing units by 13 percentage points during the same period. While WUI growth has occurred across large swaths of the state, the map on page 18 illustrates hot spots of expansion northeast of Houston, outside Dallas and Fort Worth, between Austin and San Antonio, and along the Texas-Mexico border.

Disproportionate growth in the WUI aligns with several socioeconomic developments. Texas’ economic vibrance is attracting domestic and international migrants while retaining a substantial share of the Texas-born population. These population patterns translate into increased demand for housing, particularly within driving distance of major metropolitan areas. The scarcity of urban land combined with regulatory barriers to dense development (e.g., minimum lot sizes) inhibits the housing-supply response, creating local shortages that push prices upward and populations outward. The suburban landscape is often associated with infrastructure investment, lower crime rates, and larger homes that may be disproportionately preferred by certain subpopulations (e.g., households with children). Demand for these amenities contributes to development in the WUI, and the post-COVID-19 economy characterized by remote work and preferences for more physical space portend persistent demand for the foreseeable future.

Wildfire Adaptation Strategies

The combination of climate change and Texas’ growth patterns increases the state’s exposure to wildfire risk. Understanding the development and reconstruction of the WUI after wildfires is essential to quantify future risk and inform adaptation decisions. Wildfire adaptation depends on four primary pillars: self-protection, selfinsurance, public investment, and market insurance. These four channels interact together in complementary and/or counteracting ways.

Self-protection pertains to individuals reducing their probability of exposure, typically by relocating to less risky areas. Relocation decisions, however, depend on a variety of factors, including proximity to family, changes in household composition, labor market considerations, and financial standing. The cost of moving (and other transaction costs) inhibits relocation, particularly for lower-income households, even in the context of heightened risk. High levels of personal attachment to a location may also limit large-scale relocation.

IN FALL 2011, Bastrop (pictured here and on pages 14-15) was the site of the most destructive wildfire in the state’s history. The Austin AmericanStatesman reported that the wildfire “burned 34,356 acres, scorching countless neighborhoods, dozens of commercial structures, and around 1.5 million trees.”

Moreover, self-protective measures are available only to individuals, not to physical communities.

Self-insurance refers to individual actions that reduce the magnitude of potential losses. These actions include the adoption of nonflammable or fireproof construction materials and property-level vegetation management. Increased demand for these solutions will incentivize the innovation of new products, introducing new adaptation options. Individuals who invest in property-level improvements could become more attached to their property and reduce their likelihood of moving. As with the self-protection channel, the cost of self-insurance affects adaptation inequities. The cost of adaptive technology, however, may decrease over time due to subsequent innovation, economies of scale, or public subsidies. Individuals’ self-insurance actions may have benefits that spill over to neighboring properties (e.g., less fuel on one property reduces the probability of ignition or spread to nearby properties), suggesting a potential role for public subsidies to offset underinvestment.

Another adaptation channel is to rely on public investment in spatial protection such as fire management practices (e.g., controlled burns and allowance of “natural” fires) and fire suppression resources. Communitylevel improvements in wildfire resilience and quality of life directly impact property owners through higher land prices and rents, incentivizing a collective interest in advocating for public investment. While fire protection in urban areas is directly provided by local governments, fire management around the WUI often falls under state or federal responsibility.

Federal and state fire protection services incentivize growth in these higher-risk areas by lowering local infrastructure and maintenance costs, effectively forcing state and national taxpayers to subsidize investment in the WUI. The presence of state or federal resources serves as a placebased subsidy that encourages

people to take risks they would have otherwise avoided (known as a moral hazard effect).

For example, the spatial arrangement of houses and vegetation within the WUI impacts the extent of structural damage from wildfire, but homeowners do not fully take the expected costs of future fire protection into consideration when making residential decisions. Similarly, local communities do not fully incorporate these same costs in their land-use and buildingcode policies. Post-fire adaptation typically focuses on building standards and lot-scale vegetation management. Such policies that encourage self-investment, self-protection, or the internalization of public investment costs may mitigate moral hazard.

Market insurance is the fourth pillar of wildfire adaptations. The inevitability of risk makes the insurance system a necessary component for climate resilience, enabling wildfire victims to recover after destruction. Most standard homeowners insurance policies cover wildfire damage, and these policies are governed at the state level. Like most states, Texas requires insurance companies to file rate changes for review to ensure that rates:

• are adequate;

• are not excessive (i.e., do not produce an unreasonably high long-term profit compared to the coverage provided);

• are based on sound actuarial principles;

• are reasonably related to all costs (expected losses and expenses); and

• are not based on the insured’s race, creed, color, ethnicity, or national origin.

The Texas Department of Insurance approved 91 percent of rate filings in 2023, resulting in an average effective rate increase of 23 percent for owner-occupied homeowners’ filings. While higher insurance rates are often lamented, they play an important role in communicating risk. Rising rates have distributional consequences

and highlight the unequal exposure to environmental risk. In efforts to relieve pains caused by these price pressures, some states have implemented additional insurance-rate regulations, such as prohibiting increases above a fixed percentage. An unintended consequence of these efforts is a distortion in the price signal that makes at-risk land cheaper, thereby incentivizing excessive exposure to wildfires.

Rebuilding in the WUI

After Wildfires

Some wildfire risk is inevitable, and understanding the response to disasters provides an important framework for the future. Wildfire destruction is often discussed in the context of residential real estate. While destroyed buildings decrease housing supply, the net effect on the supply of developable land is ambiguous. Heat from fires can damage foundations and surrounding infrastructure, serving to impede redevelopment

(thereby potentially decreasing the supply of developable land in the short run). Not all damaged property, however, suffers this fate during wildfires, potentially muting the land-supply shock. If the supply of land exists and the demand for housing persists, then redevelopment would be expected to occur in the WUI.

In addition to the magnitude of reconstruction, several factors affect the pattern of redevelopment. First, the location of surviving infrastructure (e.g., roads and utility lines) offers incentives to rebuild using existing spatial arrangements. It may be cost-effective to reuse rather than to start anew.

Second, the complexities surrounding disaster aid and recovery may push efforts toward the pre-wildfire status quo. The WUI spans multiple municipal, state, and national jurisdictions, creating a patchwork of processes for community development, infrastructure management, and future disaster preparation.

Third, the demand for many amenities in the WUI corresponds directly to wildfire risk. For example, households may demand the “Arcadian” intermixing of houses and vegetation on large lots that typically characterizes development in the WUI, and this spatial arrangement is particularly susceptible to wildfire ignition and spread. The utility derived from these characteristics may outweigh their associated risks (from the household perspective), similar to a scenario of strong demand to live on a coastline faced with sea-level rise. The combination of these forces not only affects the magnitude and geography of development in the WUI but also its social and economic arrangements moving forward.

Wesley Miller, Ph.D. is a former senior research associate with the Texas Real Estate Research Center at Texas A&M University and N. Lee May (nleemay@tamu.edu) is a doctoral candidate with Texas A&M University’s Department of Ecology and Conservation Biology.

County-Level Percentage Change in Housing Units (1990-2020)

Source: Radeloff, Volker C.; Helmers, David P.; Mockrin, Miranda H.; Carlson, Amanda R.; Hawbaker, Todd J.; Martinuzzi, Sebastián. 2022. The 1990-2020 wildland-urban interface of the conterminous United States - geospatial data. 4th ed. Fort Collins, CO: U.S. Department of Agriculture, Forest Service, Research Data Archive. https://doi.org/10.2737/RDS-2015-0012-4

Land Insights

By Lynn D. Krebs

“Mixed” was the byword for the first quarter of this year when it came to land prices and sales volume declines across the state. This is true for the second quarter as well; however, prices are more uniform than in the prior quarter, with rates of increase slowing in some regions and rebounding in others.

Prices bounced back a bit in Region 1 (Panhandle & South Plains), slipped in Region 3 (West Texas), slowed in Region 4 (Northeast Texas), and turned from negative to a new high (at least temporarily) in Region 7 (Austin-Waco-Hill Country). Two things remained the same on a year-overyear (YOY) basis: the two regions with the best price growth (Northeast and South) saw the largest declines in quarterly sales volumes, while the two regions with negative price changes (West and Gulf Coast & Brazos Bottom) saw some of the smallest declines in annualized sales volumes.

Market Metrics

Statewide, the decline in annualized sales volume has eased (Table 1). It is still down YOY, but the rate of decline has dropped from around 45 percent a year ago to about 20 percent through the second quarter. This tapering is good, but hopefully the decline is near an end, because one must go back to

2Q2013 to see total sales this low.

The typical tract size retracted from the same quarter a year ago, down by 22.1 percent, but was up in Regions 1, 3, and 5. Total acres sold statewide was down 23.5 percent. Every region saw a decline in total acres sold, but Region 3 declined only 2.9 percent. Statewide total dollar volume declined by 20.7 percent over the prior annualized total.

Median price continued to rise through the second quarter, increasing 3.7 percent YOY to $4,702. The fiveyear compound annual growth rate (CAGR) was nearly constant around 10.5 percent across 2023. It slipped to 10.3 percent in 1Q2024 and currently sits at 9.9 percent.

While first-quarter prices were down in four of the seven regions (Table 2), second-quarter prices were down in only two (Regions 3 and 5). Of the 33 Land Market Areas (LMAs), 15 had negative price changes and 16 were positive. Only two of the negative price changes and one of the positive price changes indicated a statistically verifiable trend. The mixture of positive and negative results with few statistically significant shifts suggests a market searching for a sustainable price trend. It will be interesting to see if these prices hold up next quarter, as a continuation of low market activity is expected.

Overview and Outlook

Current financial circumstances and uncertainty about future economic conditions continue to subdue market activity. Contributing factors include constrained liquidity, declining personal net savings, domestic political uncertainty, and growing geopolitical risks. Consumer debt, including credit card debt, continues to rise, while aggregate personal savings is now well below 2019 levels. Another concern is the unprecedented rise in government debt accumulation. Meanwhile, recent national employment reports show signs of weakness.

Rural land markets are holding up well under the circumstances. Activity seems to be leveling off, and some regions show slight improvements in recent quarters. However, the lack of statistically significant shifts can indicate that prices of some categories of land are falling while others are increasing.

Our latest forecast model indicates statewide price per acre is likely to hold at current levels over the next two to three quarters and then begin to gradually decline about 5 percent by the end of 2025. However, it predicts total acres sold should reach a floor by year-end and then begin to gradually rise through 2025 and beyond. Like any forecast in a dynamic market, several factors could change unexpectedly and alter these predictions by next quarter.

Uncertainty in capital markets, specifically potential interest rate changes and recession fears, seem to be rumbling over investment activity like storm clouds. Nonetheless, savvy investors usually act before the clouds clear. Some are making moves and, most likely, many more are evaluating near-term opportunities.

Lynn D. Krebs, Ph.D. (lkrebs@tamu.edu) is a research economist with the Texas Real Estate Research Center.

Table 1. Annual Change in Statewide Land Metrics, 2Q2024

WheRE ShoUlD My New HoUse Go?

By Reid Wilson

Key Takeaways

• Surveyors’ specialized training ensures accuracy in identifying land/ improvements location and facilitates solving conflicts and encumbrances.

• Surveys are a crucial legal insurance policy, ensuring improvements are properly placed and compliant.

• A survey plat details land features, easements, flood zones, and boundary conflicts, essential for making informed decisions.

• Prioritize a certified American Land Title Association (ALTA) or Texas Society of Public Surveyors (TSPS) survey for reliability and avoiding pitfalls of outdated or incomplete surveys.

Surveys are the eyes and ears of a landowner. They help identify potential legal issues before work begins on a new home or an addition to an existing home. Think of them as a legal insurance policy that says an improvement to a piece of property is properly located. The science of surveying was once more of an art and less precise because of the lack of high-tech instruments available today. Mistakes are made and are most painful in expensive areas when land is in high demand and every foot (or inch) is worth fighting for. Sometimes in older areas, multiple surveys conducted over the years resulted in multiple, conflicting survey pins. Other times, the surveyor reported evidence of disturbed pins

or of monuments used in prior legal descriptions but that no longer exist, such as specified trees, rocks, or other physical features. A current survey will show these situations so the owner is aware of the disputes and can either cure them or simply accept them. While the idea of reducing project costs by skimping on the survey is tempting, be careful, because doing so could create major headaches. In some cases, a completed structure might have to be removed, could be uninsurable, couldn’t be used for loan collateral, or could have severely diminished marketability.

SurVeY SaYs

A survey is a graphic depicture of land and its legal encumbrances and improvements based on a physical inspection and various levels of title examination. Only the surveyor can precisely locate structures on the site and areas subject to legal claims like easements and restrictive covenants, or areas subject to ownership dispute. A survey drawing is sometimes called a “survey plat,” but it is not a plat in the sense of a “subdivision plat,” which is a government permit filed in the real property records as a requirement to the developer to divide the land.

So what does a survey identify about the piece of property? A lot. Easements. Easements are legal rights that a third party holds to use someone else’s land for a specified purpose (usually for the benefit of specific, adjacent piece of land owned by the third party), such as access, utilities, drainage, signage, landscaping, or parking. These types of easements are called “appurtenant” as they attach to the benefited land. Structures are typically limited or prohibited within those areas. Pipeline easements are similar, but float independently of specifically benefited land, and instead benefit the easement holder. These types of easements are called easements in gross. Easements may be for private or public use. Public-use easements are often called dedications and may occur by subdivision plat or separate instrument. A public-use easement for the benefit of the “public” (rather than for a specific governmental entity) is controlled by a city if within a city; otherwise, it’s controlled by the county. Most easements are express easements created by a written, recorded

document that should be referenced in a title commitment and are straightforward to plot on a survey. These easements typically “run with the land” benefited by the easement and inure to the benefit of the owner of that land, even if not specifically assigned. An easement’s use, scope, and location are determined by the surveyor’s review of the document, and the location is added to the survey. Some easements are equitable (unwritten) easements, created by a court applying equitable considerations, such as:

• necessity for access (usually required to be a continuing necessity),

• implied consent by actions of the parties,

• implied intent due to prior existence of a road when a larger tract is divided, or

• by prescription (legal rights gained from ten years continuous, open, and obvious use).

Most implied easements are based on conditions observable by a surveyor’s inspection and will be shown on the survey (such as a roadway or drainage ditch or fenced area), and they may require a higher level of surveying expertise to describe. The existence of roads, ditches, utilities, pipelines, and other physical features for which there is no express easement could give rise to

an equitable easement. Thus, items should be shown on a quality survey, and their existence warns a buyer of potential legal hazards.

Restrictive Covenants (aka Deed Restrictions). These are legal rights that a third party holds to limit how another owner may use his or her land, usually for the benefit of land owned by the third party (almost always located in the same area).

Examples include required setbacks from boundaries or streets, height limits, pervious area, size of structures, landscaping, tree protection, signage limits, lighting limits, architectural control, and permitted/ prohibited uses.

A surveyor will review the documents listed in the title

structures on the survey plat. Flood Zones. Government policy discourages development of habitable structures within certain flood zones, primarily the “flood way” (where water typically flows in storm events) and the 100-year floodplain (area that has a 1 percent likelihood of flooding in any year). Certain insurance and loans are not available to structures in these areas, or, if they are available, they require unfavorable terms. No one should build habitable structures in these zones. Their marketability is compromised.

Encroachments/Protrusions.

When improvements from land being surveyed extend over a boundary line or into an easement or setback area, that is called an encroachment. Encroachments should be shown on a survey, with specific dimensions showing the extent of encroachments. Encroachments are usually at risk of having to be removed. Sometimes encroachments can be solved by written recorded agreement specifically permitting the encroachment to remain, but they’re usually subject to requirements not to rebuild or expand them. Protrusions are the same as encroachments, but they come onto the surveyed tract from adjacent tracts. Fences are common problems, and older fences, which rarely are constructed with surveyor guidance, routinely encroach/protrude.

Topography. For a fee, a surveyor may show the geographic character of the land surface on a survey with lines showing the gradations of the land (in one-, two-, five-, or ten-foot increments). These surveys are important for developing hilly land, determining proper building sites, and maintaining proper drainage.

Trees. For a fee, a surveyor may show trees, not only by location, but by size and type. Some cities regulate removal of certain trees (usually only large, healthy, native, or other desirable trees) and may charge fees in lieu of compliance. Surveyors assist in calculating these fees and locating

trees that the owner wishes to preserve and protect during construction activities.

Minerals/Drill Sites. For a fee, a surveyor can locate what portion of a tract is subject to outstanding mineral reservations or designated drill sites provided as part of an agreement that otherwise waives the mineral owners’ rights to access the surface of the land to explore for and extract minerals. Typically, no structures are permitted within a drill site.

Boundary Conflicts. Occasionally (and more so with older developed urban and rural land), the deeds for abutting tracts have conflicting legal descriptions with overlapping claims, and sometime tracts are separated by oddly shaped (and unusable) pieces of land for which there is no documentation of ownership. Often these small intervening tracts can be resolved by applying the “strips and gores” legal doctrine to imply that each owner gets one half of the intervening tract. The best example for use of this legal doctrine is to eliminate an intervening strip of land originally intended to be a public road but that was never accepted by a local government, nor was it improved. Title is deemed split between the adjacent lot owners.

SurVeY Dos anD Don’tS

• The importance of hiring a highly qualified, thorough surveyor can’t be overstated. They require special training and experience, and they must be licensed. The surveyor should be a member of the TSPS and follow TSPS’ standards of practice. There are also separate (and equally acceptable) standards adopted by ALTA, which are commonly used nationwide. Surveyors are easy to find, but, while any licensed surveyor has the stamp of approval of the State of Texas, best practice is to ask for a referral from a knowledgeable real estate broker, attorney, title company, or contractor.

SURVEYS SHOULD CONVEY A GREAT DEAL OF INFORMATION about a piece of property. Do not accept a boundary-only survey.

site is not level, the additional cost of a topographic survey could be appropriate.

• The survey plat should be certified to the landowner, the title company, the lender, and the seller, if applicable. That way each of them may rely on the survey as an intended beneficiary. The surveyor, his or her company, and their professional errors and omission policy (assuming they have one) stand behind this certification. Ask if they have insurance. If they don’t, beware.

• Beware of unfair liability limitations, such as a statement that any claim against the surveyor is limited to recovery only of the amount paid for the survey. That is unfair and unacceptable. The landowner doesn’t want to work with that surveyor unless he or she removes the limit.

Use that title commitment. Be sure the title commitment is ordered early as possible. Landowners should not let anyone stampede them into accepting a survey not based on a title commitment.

• Consider purchasing survey coverage from the title company for an additional premium (15 percent upcharge). Landowners need to be sure they understand the extent of the additional coverage.

• Be sure the flood zone is shown or a certification is added indicating the land is outside a flood zone.

• If the land is inside a city, ask the charge for checking the zoning and subdivision platting ordinances of the city to determine current zoning classification and building setbacks and including those on the survey plat. This is a valuable service that will yield important information, and it is highly recommended.

proper survey and to review it.

SigNed, SeAleD, DelIVerED

When the survey is complete, it should be stamped with the surveyor’s seal showing their license number; signed; certified as to the standard applied; and addressed to the landowner, title company, buyer, and lender, as applicable.

The survey is a valuable document and should be saved electronically. Surveyors die, go out of business, or become unavailable, and landowners will need that survey as long as they own the land.

RESEARCH

Wilson (rwilson@wcglaw.net) is a board-certified commercial real estate attorney with Wilson, Cribbs & Goren P.C. of Houston, a fellow of the American College of Real Estate Lawyers and a Counselor of Real Estate.

• The U.S. Supreme Court’s decision in Loper Bright overturned the Chevron doctrine, which had allowed federal agencies broad discretion in interpreting ambiguous statutes.

• The court reaffirmed the judiciary’s role in interpreting laws independently, rejecting the idea that agencies should have final say on statutory interpretations.

• Expect increased judicial scrutiny of agency regulations and actions, potentially leading to more challenges and reversals of agency decisions deemed to exceed statutory authority.

• The decision may prompt Congress to provide clearer statutory guidance to agencies, and agencies themselves may need to be more precise in adhering to statutory limits in their rulemaking.

It is emphatically the province and duty of the judicial department to say what the law is.

v. Madison, 5 U.S. (1 Cranch) 137 (1803).

On Friday, June 28, 2024, the United States Supreme Court handed down its opinion in Loper Bright Enter v. Raimondo and its companion case, Relentless, Inc. v. Department of Commerce, 144 S.Ct. 2244 (2024). The decision may signal a dramatic transfer of power in terms of federal agencies. In a 6-3 decision, the Court examined and overruled its opinion in Chevron, U.S.A., Inc. v. Natural Resources Defense Council, Inc., 467 U.S. 837 (1984), which established the doctrine of “Chevron deference.” A short discussion of administrative law will set the stage.

I’m Just a Bill

How are federal laws made? As everyone of a certain age knows, they start with a sad little scrap of paper, sitting on the steps of the Capitol. He’s just a bill, only a bill. But if they vote for him

Marbury

on Capitol Hill, he’s off to the White House for the president to sign, and then he’ll be a law.

Indeed, Article I of the United States Constitution vests all legislative powers in the U.S. Congress, composed of 535 elected members. Article II grants executive power to the president, who shall take care that the laws be faithfully executed. Article III grants judicial power to the federal courts.

Schoolhouse Rock! notwithstanding, today the majority of federal laws are not made by Congress; they’re made by unelected officials in administrative agencies, which fall under Article II. Administrative agencies are created by Congress, and Congress delegates certain authority to them through enabling statutes, which define the scope of the agencies’ authority. Agencies are authorized to promulgate “rules,” which have the force of law. While administrative agencies have been around almost as long as the Constitution itself, they really proliferated during the New Deal era and have been an important part of law in the United States ever since.

Court challenges to federal agency rules often arise when an agency, in promulgating or enforcing a rule, is alleged to have exceeded the authority granted to the agency. The courts must then interpret the statutes and rules accordingly. The Chevron and Loper Bright cases deal with who has the final say in interpreting the statute that gives the agency its authority.

Pre-Chevron

Prior to Chevron, in interpreting federal statutes (dealing with agencies or otherwise), courts exercised their own independent judgment “according due respect to Executive Branch interpretations.” However, while courts showed respect to those views, they were not bound to follow them.

In particular, courts generally deferred to agencies’ findings of fact, as long as the requirements of due process were provided and the findings were not arbitrary. As to questions of law, however, the courts remained the final arbiters.

In 1946, Congress enacted the Administrative Procedures Act (APA), which set forth procedures for agencies and “delineated the basic contours of judicial review.” That portion of the Act says that “the reviewing court shall decide all relevant questions of law, interpret constitutional and statutory provisions, and determine the meaning or applicability of the terms of an agency action.” It also requires the court to set aside agency actions if they are—among other things—arbitrary, capricious, an abuse of discretion, or otherwise not in accordance with law; contrary to constitutional right, power, privilege, or immunity; in excess of statutory jurisdiction, authority, or limitations; or short of statutory right. 5 U.S.C. § 706. The Act does not set forth any standards for deference.

The Chevron Doctrine

In 1984, the Supreme Court decided Chevron, in which it set forth the following test. First, courts were to determine whether Congress had directly spoken to the precise question at issue. If the intent of Congress was clearly expressed in the statute, courts were to construe the statute accordingly. That is, they applied the intent of Congress. At the second step, if the statute was silent or ambiguous with respect to the issue, a court was required to defer to the agency if it had offered a “permissible” construction of the statute. That is, the court was required to approve any reasonable agency interpretation, even if the court disagreed.

The decision rested on the presumption—a judicial creation—that Congress left ambiguity in the statute with the intent that the agency resolve the ambiguity. Thus, delegation of interpretive authority was implied. Over the next 40 years, the doctrine caught hold and was invoked in thousands of cases, giving agencies a very loose rein. As long as a statutory ambiguity could be found, agencies had the freedom to adopt any interpretation they desired, and change it whenever they desired, as long as the interpretation was “permissible.”

Interestingly, Chevron did not even mention the APA.

Loper Bright

In Loper Bright, the Supreme Court overruled the Chevron doctrine.

Writing for the Court, Chief Justice Roberts said that Chevron was “fundamentally misguided,” and stated simply, “The text of the APA means what it says.”