A PUBLICATION OF THE AMERICAN BAR ASSOCIATION | REAL PROPERTY, TRUST AND ESTATE LAW SECTION VOL 37, NO 1 JAN/FEB 2023 LEONA HELMSLEY The Queen of Probate & Property? TAX ASPECTS OF THE INFLATION REDUCTION ACT WEEKEND TAXABLE GIFTS OF SECURITIES FROM BROKERAGE ACCOUNTS PROPERTY CONSIDERATIONS IN RENEWABLE ENERGY PROJECTS

REGISTER NOW

LETTER FROM THE SECTION CHAIR

Please join me as we celebrate the 35th Anniversary of the Section of Real Property, Trust and Estate Law’s National CLE Conference in Washington, D.C. on May 10-12, 2023. This marks RPTE’s first time back in the nation’s capital in eight years and our return to an entirely in-person program.

This year’s Conference will present the latest developments in real estate and trust and estate law, as you capture a year’s worth of CLE credits. Our speakers feature leading practitioners and professionals, as well as governmental and judicial insiders. The Conference will also offer valuable networking opportunities with attorneys from across the country, including working lunches hosted by our substantive committees.

To take advantage of this wonderful venue, a variety of social events are planned for your enjoyment, highlighted by a private reception on Thursday evening at the Smithsonian National Museum of African American History and Culture.

I look forward to seeing you in Washington, D.C. in May!

Sincerely,

Hugh F. Drake Chair of the American Bar Association’s Section of Real Property, Trust & Estate Law

www.rptecleconference.com

January/February 2023 1 Published in Probate & Property, Volume 37, No 1 © 2023 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. PROFESSORS’ CORNER Explore opportunities to get exposure to more than 15,000 Real Property, Trust and Estate Law Attorneys at conferences and all media platforms. KELLY LAIDLER | Corporate Opportunities 410.584.8356 | kelly.laidler@wearemci.com BRYAN LAMBERT | Law Firm Opportunities 312.835.8978 | bryan.lambert@americanbar.org Partner with us www.ambar.org/rptesponsorships A monthly webinar featuring a panel of professors addressing recent cases or issues of relevance to practitioners and scholars of real estate or trusts and estates. FREE for RPTE Section members! Register for each webinar at http://ambar.org/ProfessorsCorner POSSIBILITIES AND PITFALLS OF MIXED-USE DEVELOPMENT Tuesday, January 10, 2023 12:30-1:30 pm ET DANIEL MANDELKER, Washington University St. Louis DON ELLIOT, Clarion Associates LEE EINSWEILER, Code Studio Moderator: ANDREA J. BOYACK, Washburn University FAIRNESS IN REAL ESTATE APPRAISALS: VALUATION, SUBJECTIVITY, AND BIAS

ET

Tuesday, February 15, 2023 12:30-1:30 pm

HEATHER ABRAHAM, SUNY-University Buffalo School of Law SHELBY D. GREEN, Elisabeth Haub School of Law

January/February 2023 2 Published

Probate

Property

37,

©

the

Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association. January/February 2023 • Vol. 37 No. 1 CONTENTS 26 12 Features 12 Leona Helmsley: The Queen of Probate & Property? Practical Drafting Tips from Her Majesty’s Wills

26 Let Your Light Shine Even When the Wind Blows: Special Real Property Considerations in Renewable Energy Projects By

Spencer Davis, Olufunke Leroy,

Ward 36 Patagonia, Purpose Trusts, and Stewardship Trusts—Business with a Purpose By Beck Groff and Susan N. Gary 42 Tax Aspects of the Inflation Reduction Act of 2022

Parthemer 48 Attempting a Weekend Taxable Gift of Securities from a Brokerage Account (If You Must) By Paul M. Cathcart Jr. 52 Perfect Pairings By Jo Ann Engelhardt and Toni Ann Kruse Departments 6 Young Lawyers Network 8 Uniform Laws Update 20 Keeping Current—Property 32 Keeping Current—Probate 56 Technology—Property 61 Career Development and Wellness 62 Land Use Update 64 The Last Word

in

&

, Volume

No 1

2023 by

American

By William A. Drennan

Karen M.T. Nashiwa,

and Darnella J.

By Mark R.

A Publication of the Real Property, Trust and Estate Law Section | American Bar Association

EDITORIAL BOARD

Editor

Edward T. Brading 208 Sunset Drive, Suite 409 Johnson City, TN 37604

Articles Editor, Real Property Kathleen K. Law Nyemaster Goode PC 700 Walnut Street, Suite 1600 Des Moines, IA 50309-3800 kklaw@nyemaster.com

Articles Editor, Trust and Estate

Michael A. Sneeringer Porter Wright Morris & Arthur LLP 9132 Strada Place, 3rd Floor Naples, FL 34108 MSneeringer@porterwright.com

Senior Associate Articles Editors

Thomas M. Featherston Jr. Michael J. Glazerman Brent C. Shaffer

Associate Articles Editors

Robert C. Barton Travis A. Beaton Kevin G. Bender Jennifer E. Okcular Heidi G. Robertson Aaron Schwabach Bruce A. Tannahill

Departments Editor James C. Smith

Associate Departments Editor Soo Yeon Lee

Editorial Policy: Probate & Property is designed to assist lawyers practicing in the areas of real estate, wills, trusts, and estates by providing articles and editorial matter written in a readable and informative style. The articles, other editorial content, and advertisements are intended to give up-to-date, practical information that will aid lawyers in giving their clients accurate, prompt, and efficient service.

The materials contained herein represent the opinions of the authors and editors and should not be construed to be those of either the American Bar Association or the Section of Real Property, Trust and Estate Law unless adopted pursuant to the bylaws of the Association. Nothing contained herein is to be considered the rendering of legal or ethical advice for specific cases, and readers are responsible for obtaining such advice from their own legal counsel. These materials and any forms and agreements herein are intended for educational and informational purposes only.

© 2023 American Bar Association. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of the publisher. Contact ABA Copyrights & Contracts, at https://www.americanbar.org/about_the_aba/reprint or via fax at (312) 988-6030, for permission. Printed in the U.S.A.

ABA PUBLISHING Director

Donna Gollmer

Managing Editor Erin Johnson Remotigue Art Director Andrew O. Alcala

Manager, Production Services Marisa L’Heureux Production Coordinator Scott Lesniak

ADVERTISING SALES AND MEDIA KITS

Kelly Laidler 410.584.8356 kelly.laidler@wearemci.com

Cover

Leona Helmsley image courtesy of Wikimedia Commons. Getty Images Photo illustration by Andrew O. Alcala

All correspondence and manuscripts should be sent to the editors of Probate & Property

Probate & Property (ISSN: 0164-0372) is published six times a year (in January/February, March/ April, May/June, July/August, September/October, and November/December) as a service to its members by the American Bar Association Section of Real Property, Trust and Estate Law. Editorial, advertising, subscription, and circulation offices: 321 N. Clark Street, Chicago, IL 60654-7598.

The price of an annual subscription for members of the Section of Real Property, Trust and Estate Law ($20) is included in their dues and is not deductible therefrom. Any member of the ABA may become a member of the Section of Real Property, Trust and Estate Law by sending annual dues of $70 and an application addressed to the Section; ABA membership is a prerequisite to Section membership. Individuals and institutions not eligible for ABA membership may subscribe to Probate & Property for $150 per year. Single copies are $7 plus $3.95 for postage and handling. Requests for subscriptions or back issues should be addressed to: ABA Service Center, American Bar Association, 321 N. Clark Street, Chicago, IL 60654-7598, (800) 285-2221, fax (312) 988-5528, or email orders@americanbar.org.

Periodicals rate postage paid at Chicago, Illinois, and additional mailing offices. Changes of address must reach the magazine office 10 weeks before the next issue date. POSTMASTER: Send change of address notices to Probate & Property, c/o Member Services, American Bar Association, ABA Service Center, 321 N. Clark Street, Chicago, IL 60654-7598.

Published in Probate & Property, Volume 37, No 1 © 2023 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association.

January/February 2023 3

Check out our library of New Real Property, and Trust and Estate Law Books!

NEW RPTE

Anatomy of Mortgage Loan Documents: Understanding and Negotiating Key Commercial Real Estate Loan Documents, Third Edition

LAWRENCE UCHILL

PC: 5431130 358 pages Price: $139.95 / $125.95 (ABA member) / $111.95 (RPTE Section member)

Providing a thorough analysis of the provisions in a real estate mortgage, the analysis and commentary for each provision is useful both for lawyers well-seasoned in commercial mortgage loan practice, as well as for attorneys new to real estate law.

ambar.org/anatomyofmortgage3

The Lease Manual: A Practical Guide to Negotiating Office, Retail, and Industrial Leases Second Edition

APRIL F. CONDON WITH RODNEY J. DILLMAN

PC: 5431131 Price: $159.95 / $143.95 (ABA member) $127.95 (RPTE Section member) 558 pages

This wholly-revised practical manual describes and analyzes typical lease paragraphs for office, retail, and industrial leases, examining and exploring the concerns, needs, and desires of landlords, tenants, lenders, and brokers by analyzing typical lease paragraphs from each point of view. ambar.org/leasemanual

4

Published in Probate & Property, Volume 37, No 1 © 2023 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association.

Domestic Asset Protection Trusts: A Practice and Resource Manual EDITOR, ALEXANDER A. BOVE JR. PC: 5431122 527 pages Price: $169.95 / $152.95 (ABA member) $134.95 (RPTE Section member) Many states have established trusts that offer the protection of the trust assets from the settlor’s creditors. This resource provides information on the trust rules and regulations in the states that have allowed DAPTs, as well as general guidance on key issues. ambar.org/domesticassetrpte Title Insurance, Fifth Edition: A Comprehensive Overview of the Law and Coverage JAMES L. GOSDIN PRICE: $229.95 / $206.95 (ABA MEMBER) / $183.95 (RPTE SECTION MEMBER) 1130 PAGES (AND HUNDREDS OF PAGES OF EXHIBITS ONLINE) Title insurance is an increasingly complex and critical factor in real estate transactions, and lawyers must be prepared to play equally critical roles as advisors to their clients. This updated and expanded edition provides practical tools and essential information for real estate attorneys who need to understand title insurance coverage. ambar.org/titleinsrpte ambar.org/rptebooks PUBLICATIONS

YOUNG LAWYERS NETWORK

Origin of the Young Lawyers Network

In writing this issue’s column for Young Lawyers Network, I’m reminded of its origin story. The Young Lawyers Network was created several years ago by RPTE member Hugh Drake (now Chair of the Section) as a means to connect, engage, and recruit young lawyers to the Section who did not find their way into the Section through its fellowship program. If you have considered becoming more involved in the Section, but you’re not sure how, please read on for the best ways to do so and, as a result, raise your level of practice as a lawyer.

Apply to Be a Fellow for the 2023–2024 Bar Year

In my opinion, the best way to get involved in the Section is to apply to be a Section Fellow for the upcoming bar year. The fellowship program is how I became involved in the Section. I was a Section Fellow from 2016-2018. Each year, the Section selects 10 applicants for its fellowship program. Typically, the Section chooses five individuals for the Trust & Estate division and five individuals for the Real Property division. To be considered for selection, a person must (1) have practiced in the trusts and estates or real property area for at least one year, (2) be younger than 36 years of age or have been admitted to the bar within the last 10 years, and (3) have demonstrated leadership at the state or local bar level or in the ABA Young Lawyers Division. If selected, you are assigned to work with the chair of a substantive committee of the Section. In my case, I was selected to participate in the retail leasing committee, which is

For more information on the RPTE YLN, please contact: Josh Crowfoot, Crowfoot Law Firm, 200 W. M.L.K. Boulevard, Suite 1000, Chattanooga, TN 37402, josh@ crowfootlaw.com.

part of the Leasing Group. The committee chair then gets you involved in the substantive work of the Section. In my case, I wrote a brief article for Probate & Property magazine and assisted colleagues in the Leasing Group with a presentation for the spring RPTE conference. Throughout the year, I learned the mechanics of how the Section works by attending membership committee calls. I also learned a lot by sitting on calls that organized and planned programming for the Section. As you read this, please know there is always an opportunity for you to write an article for the Section or put together an e-CLE or webinar.

Attend the ABA RPTE Spring Conference

This year the 2023 ABA RPTE Spring Conference will be held May 10 – May 12 in Washington, DC. The spring conference is stacked with excellent CLE programming, and you can get all your CLE credits for the entire year in one place. Many of the speakers at the conference also hold leadership positions within the Section, so it is also an opportunity to meet the lawyers in the Section who are most active and who can connect you with a fellow member in your practice area.

Write for the Section

The Section has three publications: Probate & Property magazine, the eReport, and the RPTE Journal. Probate & Property releases a bi-monthly issue. Articles for the magazine can be written in a longer format (i.e., featured article) or a shorter format (i.e., the article you are currently reading). If you have an idea for Probate & Property, you can contact the articles editors for Probate & Property listed in the masthead at the front of this issue, and they can assist. Or you can reach out to me, and I’ll make sure you get connected with the right person in the Section. The

eReport is a quarterly electronic publication that includes more practical information and provides news on the Section’s activities and upcoming events.

The RPTE Journal is published three times each year with assistance from the University of South Carolina and best suited for a more in-depth, scholarly article. Each of these publications is always looking for worthwhile content for Section members, and getting published is the easiest way to raise your visibility as a lawyer and within the Section.

Speak for the Section

The Section is always looking for quality CLE programming in the form of webinars, eCLEs, and presentations at the spring conference. If you have an idea for a program, please reach out to the committee chair for your specific practice area. If you have difficulty finding that information online, feel free to reach out to me, and I’ll put you in touch with the right person. One of the benefits of my serving as an active member of the Section for many years is that I am confident I can connect you with the right person to the extent you want to get more involved in the Section.

Parting Remarks

Being involved in the ABA RPTE Section has introduced me to an incredible network of top-notch lawyers within our profession. Through my participation in the Section, I’ve learned and improved my skills as a speaker, writer, and practitioner. Also, fellow Section members have even referred business to me, and I have referred business to other members. As with most things in life, you get out of the Section what you put into it. It’s my sincere hope you’ll become an active member of the Section and have the same experience. n

Published in Probate & Property, Volume 37, No 1 © 2023 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association.

January/February 2023 6

Lorem ipsum SEPTEMBER 22-24, 2022 ANCHORAGE, ALASKA THANK YOU TO OUR SPONSORS FOR MAKING OUR FALL LEADERSHIP MEETING A SUCCESS SILVER LAW FIRM SPONSORS GOLD

State legislatures during their 2022 legislative sessions considered and enacted the following uniform acts and model acts of interest to RPTE members.

The Model Assignment of Rents Act was enacted in Michigan, the sixth state to do so. The act provides a comprehensive statutory system for the creation, perfection, and enforcement of security interests in rents from real property.

The Uniform Commercial Real Estate Receivership Act was enacted in Rhode Island and West Virginia, bringing the total number of enacting states to 12. This act standardizes the rules for receivers appointed to manage commercial property, resulting in greater predictability for litigants, lenders, and parties doing business with a company under receivership.

The Uniform Directed Trust Act was enacted in Kansas, the latest of 16 states to do so. This act clarifies the fiduciary duties and powers of trustees and other persons appointed under the terms of a trust to exercise some of a trustee’s traditional powers. The act was also introduced in New York and Rhode Island.

Utah enacted the Uniform Easement Relocation Act, becoming the second state to adopt this act, which encourages access easement holders to allow benign relocations and provides a procedure to obtain a court order for relocation when it would not harm the easement holder’s access rights. Nebraska has also adopted this act.

The United States Virgin Islands became the fifth jurisdiction to enact the Uniform Electronic Wills Act,

Uniform Laws Update Editor: Benjamin Orzeske, Chief Counsel, Uniform Law Commission, 111 N. Wabash Avenue, Suite 1010, Chicago, IL 60602.

UNIFORM LAWS UPDATE

2022 Legislative Update

Uniform Laws Update

provides information on uniform and model state laws in development as they apply to property, trust, and estate matters. The editors of Probate & Property welcome information and suggestions from readers.

which was also introduced in Georgia, Massachusetts, New Jersey, and the District of Columbia. This act allows estate planners to offer online services, including the execution of wills, with appropriate security procedures. (A companion act, the Uniform Electronic Estate Planning Documents Act, was approved by the Uniform Law Commission in 2022 and is now available for states that wish to adopt more comprehensive reforms.)

The Uniform Fiduciary Income and Principal Act was enacted in Virginia, the sixth state to adopt this modern update of the 1997 Uniform Principal and Income Act. The new act has comprehensive rules for unitrust conversions. The act was also introduced in California, Missouri, and Tennessee.

The most-enacted uniform law in 2022 was the Revised Uniform Law on Notarial Acts, the latest version of which includes optional provisions for remote ink notarization (RIN) in addition to remote online notarization (RON). Delaware, the District of Columbia, Maine, Rhode Island, Vermont, and the US Virgin Islands adopted the latest version of this act, with all but Rhode Island and Vermont electing to allow RIN. They join New Jersey, which enacted the latest revision last year, and 22 other states that have adopted the

2018 version that included the RON option only.

The Uniform Partition of Heirs Property Act was adopted in Maryland and Utah and considered by eight more legislatures last year. This act deters abusive partition actions that can force the sale of family-owned real estate, often resulting in sales prices at public auctions that are far below the fair market value. The act implements a series of due-process protections, including independent appraisal, an option for current owners to purchase the shares of selling owners, and a requirement for open-market sales rather than auctions. Twenty-one states have adopted this act.

Vermont enacted the Uniform Real Property Electronic Recording Act, becoming the thirty-ninth state to do so. This act enables but does not require recording offices to accept deeds and other documents in electronic form for recording. The Missouri Legislature also considered the act this year.

Oklahoma updated its statutes by adopting the Uniform Testamentary Additions to Trusts Act, a more comprehensive version of an earlier uniform law that overrode the common-law prohibition on pour-over wills. Twenty-seven states have adopted the latest version of this act.

Indiana became the thirteenth state to adopt the Uniform Trust Decanting Act, which governs the distribution of trust assets into a new trust with different terms. The act allows decanting for permissible purposes and clarifies when decanting is restricted.

Finally, the Uniform Transfers to Minors Act was adopted in South Carolina, the final state to do so—proving that true uniformity of state law is still possible!

A few other uniform RPTE acts were

Published in Probate & Property, Volume 37, No 1 © 2023 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association.

January/February 2023 8

introduced last year but did not cross the finish line: The Uniform Adult Guardianship and Protective Proceedings Jurisdiction Act in Florida, the new Uniform Community Property Disposition of Death Act in Nebraska, the Uniform Power of Attorney Act in the District of Columbia and Vermont, the Uniform Real Property Transfer

on Death Act in Maryland, New Hampshire, and Tennessee, and the Revised Uniform Residential Landlord and Tenant Act in Kentucky. In two states that have year-long legislative sessions, bills were pending at press time: the Uniform Trust Code in New York and the Uniform Power of Attorney Act in Michigan.

ULC Legislative Counsel provides support for the enactment of uniform laws in your state. Contact ULC Chief Counsel Benjamin Orzeske at (312) 4506621 or borzeske@uniformlaws.org. More information about these acts and other ULC drafting projects is available at www.uniformlaws.com. n

Published in Probate & Property, Volume 37, No 1 © 2023 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association.

January/February 2023 9

UNIFORM LAWS UPDATE

MEMORANDUM FOR AUTHORS IS NOW ONLINE

The Editorial Board of Probate & Property magazine is interested in reviewing manuscripts in all areas of trust and estate or real property law. Probate & Property strives to present material of interest to lawyers practicing in the areas of real property, trusts, and estates. Authors should aim to provide practical information that will aid lawyers in giving their clients accurate, prompt, and efficient service.

The complete Memorandum for Authors is available online at ambar.org/ppmemo.

January/February 2023 10

UNIFORM LAWS UPDATE

Published in Probate & Property, Volume 37, No 1 © 2023 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association.

2022 EXCELLENCE IN WRITING AWARDS

The editors of Probate & Property are pleased to announce the winners of the magazine’s 2022 Excellence in Writing Awards:

BEST TECHNOLOGY/LAW PRACTICE MANAGEMENT ARTICLE

Protect Your Practice: Necessary Engagement Letter Clauses to Revisit

By Maria E. O’Sullivan, Laura Joy Lattman, Soo Yeon Lee, and Sahmra A. Stevenson (January/February)

BEST CUTTING-EDGE ARTICLES

REAL PROPERTY

The Remotest Idea—Practical and Ethical Lessons Learned During the Pandemic

By Pamela E. Barker, Melissa G. Powers, and Ben Lund (September/October)

TRUST & ESTATE Crypto and Retirement Accounts—Can You?

By Mark R. Parthemer (September/October)

BEST PRACTICAL USE ARTICLES

REAL PROPERTY

Key Lease Provisions to Consider in Due Diligence

By Amy Lawrenson, Imran Naeemullah, and Karen Nashiwa (July/August)

TRUST & ESTATE

Speechifying and Scribbling—A Candid Discussion about the “Why” and “How” of Integrating Public Speaking and Presentations into Your Trusts and Estates Career

By Stephen R. Akers, Carol A. Harrington, Paul S. Lee, Dana G. Fitzsimons Jr., and Terrence Franklin (November/December)

BEST OVERALL ARTICLES

REAL PROPERTY

The Aerial View of Land Use: Preempting the Locals for Improved Housing Access

By Shelby D. Green and Bailey Andree (September/October)

TRUST & ESTATE

Celebrity Estate Planning: Misfires of the Rich and Famous V

By Jessica Galligan Goldsmith, Stacia C. Kroetz, David E. Stutzman, Daniel J. Studin, Erica Howard-Potter, Lauren G. Dell, and Samuel F. Thomas (September/October)

All articles published in Probate & Property during the current year will be eligible for the 2023 Excellence in Writing Awards. Any author interested in submitting an article should contact either Michael Sneeringer or Kathleen Law at the addresses listed on page 3. The magazine’s “Memorandum for Authors” is posted on the ABA website at ambar.org/ppmemo.

Published in Probate & Property, Volume 37, No 1 © 2023 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association.

January/February 2023 11

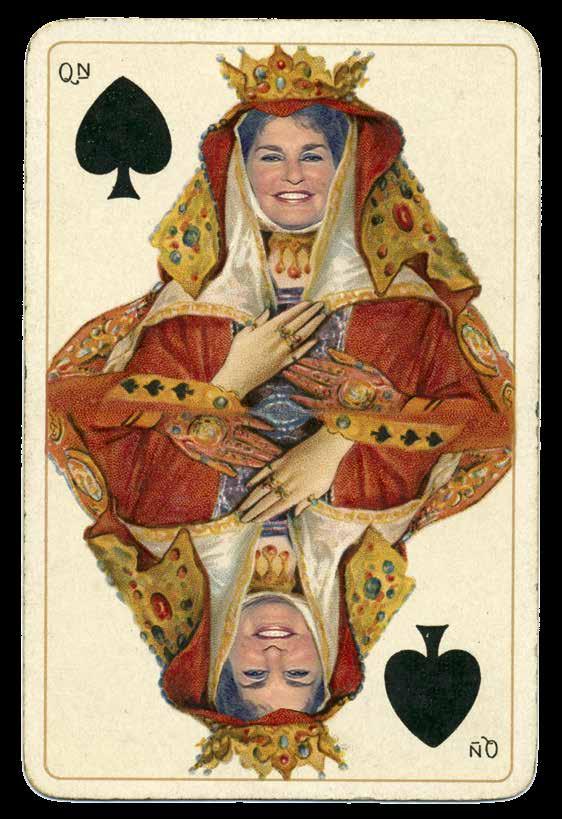

LEONA HELMSLEY The Queen of Probate & Property?

Practical Drafting Tips from Her

Majesty’s Will

By William A. Drennan

Leona Helmsley image courtesy of Wikimedia Commons. Getty Images. Photo illustration by Andrew O. Alcala

Sensational sobriquets include the King of Swing, the Queen of Soul, the Sultan of Swat, Satchmo, the Say Hey Kid, the Manassas Mauler, and the Man in Black. A worthy addition is that unflattering moniker bestowed upon Leona Helmsley, a/k/a the Queen of Mean. This article proposes a new title for the late Leona—The Queen of Probate & Property. (The common or given names for those highlighting the start of this article, along with many more amazing appellations, are at the end of this article in The 100 Nickname Quiz! Take the quiz and see if you can identify all 100.)

Leona Helmsley established her place in the pantheon of wildly wealthy real property titans over decades, moving from high school dropout, to successful agent, to owning an amazing array of prized properties, including the Empire State Building. Along the way, she married real estate mogul Harry Helmsley in 1972, was convicted of federal tax fraud and spent 18 months in prison before being released on January 26, 1994, and inherited her husband Harry’s fortune upon his death in 1997 under a will he signed the day before Leona was released from prison.

A.

Published in Probate & Property, Volume 37, No 1 © 2023 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association.

January/February 2023 13

istockphoto

William

Drennan is a professor at Southern Illinois University Law School and a former editor for the Books & Media Committee of the Real Property, Trust and Estate Law Section of the ABA.

After accumulating an estate conservatively estimated at more than $5 billion, she passed away on August 7, 2007. But this article leaves the real property tale for others. See, e.g., Ransdell Pierson, The Queen of Mean: The Unauthorized Biography of Leona Helmsley (1989); Richard Hammer, Helmsleys: The Rise and Fall of Harry and Leona Helmsley (1990).

Instead, this article focuses on the probate side. Leona left a will addressing a cornucopia of issues with practical implications for even not-so-wealthy souls. With the 15th anniversary of Leona’s departing, we can reflect upon a few of her likely estate planning desires, review the related legal techniques used, assess the successes and failures of that planning, and distill some practical implications for today.

This article surveys six probate issues or opportunities, specifically: (i) using a will as the client’s primary dispositive vehicle; (ii) directing that the deceased be buried with valuable property; (iii) directing burial next to a pet; (iv) including long-term burial wishes in a will; (v) bequeathing money for the benefit of a pet or for the maintenance of a mausoleum; and (vi) tying behavior-incentive conditions to a bequest in trust.

Topic #1: Will as Primary Dispositive Document

Leona put out the family laundry, and her misanthropy, for the world to see. A copy of her will is available to all. Last Will and Testament of Leona Helmsley, Living Trust Network, https://bit. ly/3WauoJk. She left $12 million for the benefit of her nine-year-old, four-anda-half-pound dog, which was more than she left outright to any human being.

Despite the typical reluctance to speak ill of the dead, the public disclosure of her will inspired venom. See, e.g., Jeffrey Toobin, Rich Bitch: The Legal Battle over Trust Funds for Pets, New Yorker, Sept. 22, 2008, at 38. One philosophy professor compared her $12 million doggie transfer to “setting money on fire in front of a group of poor people.” Id. at 48 (quoting Professor Jeff McMahan of Rutgers University).

For some clients, this could be a cautionary tale. In the interest of

minimizing public scrutiny, clients can use a simple pour-over will and then a trust containing any unusual terms. The standard pour-over will would be a public document, but the trust with the juicy bits would be available to only the trustees, the beneficiaries, and their advisors. See Susan N. Gary, Transfer-onDeath Deeds: The Nonprobate Revolution Continues, 41 Real Prop., Prob. & Tr. J. 529, 537 (2006) (“[Unlike a will or deed] a revocable trust is not a public document . . . so the owner’s plan of distribution will not be public.”).

Topic #2: Burying Property at Death and

Keeping It Buried Leona’s will directs that she be “interred wearing [her] golden wedding band (which is never to be removed from [her] finger).” One generally can destroy his own property during lifetime, but a direction to destroy property at death may be capricious or violate public policy. One cannot validly bequeath $1,000 to a trustee with the direction to throw the $1,000 “into the sea,” and a trustee who followed such a direction would be liable to the estate for the loss. Restatement of Trusts § 124, cmt. g, Illus. #5. A Pennsylvania court declared invalid a decedent’s direction in her will that she be buried with her “diamonds and other jewelry.” Meksras Estate, 63 Pa. D.&C.2d 371 (Penn. Ct. Common Pleas 1974). The court reasoned that because the will was a public document, obeying the decedent’s direction would encourage grave robbing and thereby violate public policy.

On the other hand, there are many reports of decedents being buried in their cars or with their prized possessions. See Abigail J. Sykas, Waste Not, Want Not: Can the Public Policy Doctrine Prohibit the Destruction of Property by Testamentary Disposition, 25 Vt. L. Rev. 911, 926 (2001). When such a direction, which effectively destroys the property for the living, would be capricious or contrary to public policy is not clear. Id. (referring to the “abstract, amorphous public policy rationale”). A tome voted the creepiest book commonly found in U.S. law libraries indicates that a request to be buried wearing a wedding ring is

common. Percival Jackson, The Law of Cadavers 127, 183 (2d ed. 1950).

There are at least two takeaways regarding Leona’s approach. First, in light of concerns about grave robbing, it may be advisable to delete words like “golden” or other modifiers indicating significant value from the description. Second, Leona’s direction that the band should “never be removed from [her] finger” is insightful, as relatives reportedly have reopened graves to recover jewelry. See Kate Meyers Emery, More Famous Dead, Bones Don’t Lie (Dec. 20, 2012), https://bit.ly/3Didsba (discussing the reopening of Sammy Davis Jr.’s grave to grab $70,000 worth of jewelry). Although with decomposition the wedding band may fall from Leona’s finger eventually, she likely received some comfort from this will provision.

Topic #3: Burial Alongside a Pet

The media often reported that Leona wanted to be buried with her dog, but actually Leona’s will directed that the dog’s “remains shall be buried next to [Leona’s] remains.” It could have been crowded around Leona, as her will also directed that she be buried “next to” her predeceased husband, as well as “next to” her predeceased son. Leona and her planners were criticized for including this doggie provision because at the time an animal burial with a human was not authorized under either New York law or the rules of her chosen cemetery. Toobin, supra

Nevertheless, in hindsight, if consistent with the testator’s wishes, it may be wise to include such a provision. State laws are changing. In 2016, New York changed its law to provide that the cremated remains of a domestic animal could be buried with a human being. Many states are still silent on the issue, some states are on the road to change, and some states allow “whole-family” cemeteries with “full-body burial of a pet’s remains in the family burial plot.” See Elder Law 101: Can You Be Buried with Your Pet? (Mar. 4, 2020), http:// www.elderlawanswers.com; Sara Redding Ochon, Can Pet Ashes Be Buried with Humans? USA State by State Laws, hppts://farewellpet.com (offering a

Published in Probate & Property, Volume 37, No 1 © 2023 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association.

January/February 2023 14

50-state click-on guide to burying pet ashes with a human).

In this evolving era, what was prohibited today may be authorized tomorrow. As the testator may not die for some time, it may be advisable to include these clauses in a will and also to spell out the client’s “second choice” if legal or cemetery restrictions interfere with the most-favored plan. For example, if either law or cemetery restrictions prohibit human burial with a particular type of pet, would the testator want the animal cremated and the ashes sprinkled on the decedent’s grave (or deposited in an urn that could be buried at the foot of the testator’s plot)? Speaking back in 2013, one industry insider remarked that undertakers “will tell you ‘not a day goes by when I don’t put an urn of an animal into the casket of a human being secretly for a family.’” Elder Law 101, supra

Her dog died about four years after Leona. Because the dog could not be buried next to Leona, the dog was cremated and the ashes placed in an urn that was “privately retained.” Cara Buckley, Cosseted Life and Secret End of a Millionaire Maltese, N.Y. Times, June 9, 2011. When asked if the dog’s urn had been, or would be, added to Leona’s mausoleum, a member of the cemetery’s board stated, “In all honesty . . . we don’t know.” Id.

Topic #4: Including Long-Term Burial Instructions in a Will

Deeply rooted tensions dominate the law regarding who controls the disposition of human remains. The refusal to find that the decedent has a traditional property right in his corpse suggests that the right of sepulcher rests with the living—usually first a spouse, and if none, the next of kin. Consistent with this view, most states allow an individual to designate an agent to make the decisions under a power of attorney or other document. See, e.g., Kimberly E. Naguit, Letting the Dead Bury the Dead: Missouri’s Right of Sepulcher Addresses the Modern Decedent’s Wishes, 75 Mo. L. Rev. 249 (2010). In reliance on a state statute, the Iowa Supreme Court famously refused to follow a decedent’s clear direction in

her will and a signed letter that she be buried in Montana, and instead found that her husband had the right to bury her in Iowa. In re Estate of Whalen, 827 N.W.2d 184 (Iowa 2013).

On the other hand, Roman law and long-standing common law principles respect “that decedents have the right [by will] to determine the manner and location of the disposition of their remains.” Tanya D. Marsh, You Can’t Always Get What You Want: Inconsistent State Statutes Frustrate Decedent Control over Funeral Planning, 55 Real Prop., Tr. & Est. L.J. 147, 150 (2020) (providing a thorough analysis of the history, policy, case law, and legislation for this issue, and including “a comprehensive appendix listing and summarizing each states’ . . . laws as an aid to practitioners”).

Leona’s will not only directed that she be buried next to her predeceased husband and her son at the Woodlawn Cemetery, but also it addressed a possibility far in the distant future. Her will directed that if her husband and son should be relocated, then she also should be relocated and reinterred next to them. She also directed that her brother and his wife be permitted to be buried in the Helmsley mausoleum, “but no other person.” Whether this latter desire would be achieved likely will depend on the applicable deed, agreement, and affidavit regarding the mausoleum and its use. See generally Anne K. Hansen, Who Is in My Grave? A Comparison of State and Local Laws in Illinois and Utah That Guide Resolution of Grave Plot Ownership Claims, 45 S. Ill. U. L.J. 139 (2020).

A will may be strong evidence of the decedent’s intentions regarding the

treatment of the body. “For centuries the last expression of bodily autonomy has been received with solemnity and honored by our laws to the fullest practical extent when declared with the formality of the last will and testament.” In re Estate of Whalen, 827 N.W.2d at 195 (Cady, C.J., dissenting). Anticipating the future may be especially relevant when there are doubts about the intended duration of the burial. In some cultures and geographic areas, burial frequently is only for a term of years based on an estimate of the time expected for the body to decompose to a certain extent.

Topic #5: Bequests to Pet Trusts or Burial Maintenance Funds

Leona’s estate may be best known for its influence on estate planning for pets. Her will left $12 million in trust for the benefit of her nine-year-old, four-anda-half-pound Maltese named Trouble. Honorary trust statutes typically provide that only a reasonable amount may be held in a pet trust and that any excess must pass to the designated subsequent taker or the residuary beneficiary. In response to a request from Leona’s fiduciaries, a New York judge ruled that only $2 million was reasonable for her dog and that the other $10 million was excessive. Nevertheless, a leading pet trust expert astutely observed, “It’s not the reduction that is important; it’s that the judge said two million was appropriate. It’s a landmark case.” Toobin, supra, at 43 (quoting attorney Rachel Hirshfeld). That expert also said, “One of the greatest moments in my life was when the judge awarded $2 million [for the Helmsley dog].” Id.

Although it did not get the media

Published in Probate & Property, Volume 37, No 1 © 2023 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association.

January/February 2023 15

Decedents have the right [by will] to determine the manner and location of the disposition of their remains.

barking like the transfer to the dog trust, Leona’s will also created a $3 million mausoleum fund to maintain, in “excellent condition,” the “final resting places” for herself, her husband, her son, and her mother, father, sister, and brotherin-law. The will also stated that all these final resting places would be inspected at least quarterly and “acid washed or steam cleaned at least once a year.” In addition, the fund may maintain subsequent final resting places if any of them are relocated. Apparently, there has been no challenge to the amount of the Helmsley mausoleum fund, perhaps because there is New York precedent for spending amazing amounts on burial and maintenance. See, e.g., In re Baeuchle’s Will, 82 N.Y.S.2d 371 (N.Y. 1947) (rejecting an argument that spending approximately $150,000 for the decedent’s burial and mausoleum maintenance fund in 1946 was unreasonable when the decedent’s entire estate was $175,000; in today’s dollars the amount spent on burial and maintenance in that case was approximately $2.15 million).

For both honorary trusts, Leona and her planners presumably anticipated the amounts would be challenged and smartly designated a subsequent taker for any amounts determined excessive. With honorary trusts, a common concern is enforcement because, by definition, there will be no surviving human beneficiary with standing to sue to police compliance. Leona, however, appointed five trustees for the mausoleum maintenance trust, so presumably there will be one or more individuals who will monitor compliance. In addition, Leona used her will to help justify the amounts contributed to the mausoleum trust. The will stated the mausoleums are to be inspected at

least quarterly, maintained in “excellent condition,” and acid-washed or steamcleaned at least annually.

In contrast, her will failed to list anticipated expenses that could justify the contribution to the pet trust. It may be advisable for a testator to explain why he is contributing to a pet trust by listing and explaining the expected expenses, such as veterinarian fees, special food, the expenses of a companion animal, and perhaps, most important, a fund for extraordinary drugs and medical care because the testator would prefer that the pet undergo surgery or other complicated procedures rather than being put to sleep. Some owners spend incredible amounts on drugs, surgery, dental care, and various medical treatments for their pets.

Topic #6: Behavior Incentive Conditions

A decedent may desire to exert deadhand control over the future behavior of the living. Some testators provide incentives for children or grandchildren to end a drug habit and enter a rehab program, end an alcohol addiction, go to college or obtain an advanced degree, wed a member of a particular religious faith, or cease or pursue other activities. See Ellen Evans Whiting, Controlling Behavior by Controlling the Inheritance: Considerations in Drafting Incentive Provisions, 15 Prob. & Prop., Sept/Oct. 2001, at 6. Generally, these incentive clauses can be enforced if they are not too vague and do not violate public policy. Id.

For each of her favorite grandchildren, David and Walter, Leona left $5 million to a charitable remainder trust paying a five percent annual unitrust amount, which would be approximately $250,000 per year (initially) to David

and Walter. Leona’s will provided that a grandchild would continue to receive the annual payouts only if the grandchild visited the grave of his father (Leona’s son) “at least once each calendar year, preferably on the anniversary of [his] death (March 31, 1982).”

The will directs the five trustees of the charitable remainder trust to place a visitor book in the mausoleum, and the trustees are to rely on the visitor book in deciding if the grandchild satisfied the requirement. The trustees have no further duty to inquire and “shall have the right to presume that the [grandchild] did not visit the grave during that calendar year if [the grandchild’s] signature does not appear on the register for such calendar year.” This forfeiture provision will not apply if the trustees, in their discretion, determine a grandchild could not visit “by reason of physical or mental disability.”

While these provisions have been criticized as controlling, it seems unlikely that they would violate public policy. See Toobin, supra. Furthermore, the provisions appear sufficiently clear to avoid being invalidated for vagueness. Those drafting similar clauses may take away a few points—include exceptions when the restriction would no longer be appropriate (such as upon disability), be precise about the timing (such as clarifying that an annual requirement must be performed within each calendar year), and spell out how the trustees are to determine if the beneficiary met the condition.

Conclusion

On the probate side, Leona Helmsley merits the title Queen of Probate & Property because her will presents and addresses an astounding array of issues. For drafters, a recurrent lesson from her majesty’s will is the importance of anticipating post-death contingencies. Although few clients will have the wealth and personality of the Queen of Mean, many clients may appreciate a planner who can raise and address many of the concerns reflected in Leona’s will. n

Published in Probate & Property, Volume 37, No 1 © 2023 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association.

January/February 2023 16

Incentive clauses can be enforced if they are not too vague and do not violate public policy.

The 100 Nickname Quiz! How Many Can You Get?

The answers are at the end. Many of these nicknames are discussed in Peter Carlson, A Short History of Nicknames, Wash. Post, Apr. 2, 1998. “American history can be written in a rollicking roll call of nicknames.” Id.

50 Non-sports Nicknames

Singers

#1: The Boss ____________________________________ #2: Godfather of Soul ____________________________________ #3: King of Pop ____________________________________ #4: The Man in Black ____________________________________ #5: Old Blue Eyes ____________________________________ #6: P. Diddy/Puffy ____________________________________ #7: Queen of Soul ____________________________________ #8: The Singing Cowboy ____________________________________

Other Entertainers

#9: Dizzy (trumpeter/jazz musician) _________________________________

#10: The Duke (actor) _________________________________

#11: J. Lo (actor) _________________________________

#12: King of Swing (clarinetist/band leader) _________________________________ #13: The Little Tramp (actor) _________________________________ #14: Muscles from Brussels (actor/martial artist) _________________________________ #15: Satchmo (trumpeter/singer) _________________________________ #16: Mr. Warmth (comedian) _________________________________

Authors

#17: The Bard of Avon (1564–1616) ________________________________

#18: Doctor Seuss (1904–1991) ________________________________

#19: King of Horror (1947–) ________________________________ #20: Papa (1899–1961) ________________________________

US Presidents

#21: Bubba ________________________________ #22: Dubya ________________________________ #23: Father of the Constitution ________________________________ #24: Gipper ________________________________

#25: Ike ________________________________

#26: Old Hickory ________________________________ #27: The Rail Splitter

#28: Sage of Monticello

#29: Silent Cal

#30: Tricky Dick ________________________________

#31: The Trust Buster ________________________________

Other Politicians

#32: The Body (Minn.) (1951–) ________________________________

#33: The Governator (Calif.) (1947–) ________________________________

#34: Governor Moonbeam (Calif.) (1938–) ________________________________

#35: The Iron Lady (England) (1925–2013) ________________________________ #36: Kingfish (Louisiana) (1893–1935) ________________________________

Published in Probate & Property, Volume 37, No 1 © 2023 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association.

January/February 2023 17

________________________________

________________________________

________________________________

Roger Woolman, CC via Wikimedia Commons via Wikimedia Commons

Military/Rulers

#37: Black Jack (General) (1860–1948) ______________________________

#38: Lionheart (King) (1157–1199) ______________________________

#39: The Little Corporal (Emperor) (1769–1821) ______________________________

Other

#40: Blackbeard (pirate) (c.1680–1718) _____________________________

#41: Buffalo Bill (American old west) (1846–1917) _____________________________

#42: Jackie O. (first lady) (1929–1994) _____________________________

#43: Jack the Dripper (abstract painter) (1912–1956) _____________________________

#44: Scarface (gangster) (1899–1947) _____________________________

#45: Lady Bird (first lady) (1912–2007) _____________________________

#46: Lucky Lindy (aviator) (1902–1974) _____________________________

#47: The Oracle of Omaha (investor) (1930–) ______________________________

#48: R.B.G. (justice) (1933–2020) ______________________________

#49: The Unabomber (criminal) (1942–) ______________________________ #50: Wizard of Menlo Park (inventor) (1847–1931) ______________________________

50 Sports Nicknames

Baseball Players

#1: All Rise _________________________________

#2: Big Hurt _________________________________

#3: Big Papi _________________________________

#4: Catfish _________________________________ #5: Charlie Hustle _________________________________ #6: Cool Papa _________________________________ #7: Mr. Cub _________________________________ #8: Georgia Peach _________________________________ #9: Hammerin’ Hank _________________________________ #10: Joltin’ Joe _________________________________ #11: Mr. October _________________________________ #12: The Ryan Express _________________________________ #13: Satchel _________________________________ #14: The Say Hey Kid _________________________________ #15: The Splendid Splinter _________________________________ #16: The Sultan of Swat _________________________________ #17: Yogi _________________________________

Football Players

#18: Broadway Joe _______________________________ #19: The Bus _______________________________ #20: Joe Cool _______________________________ #21: Mean Joe _______________________________ #22: Prime Time/Neon Deion _______________________________ #23: Refrigerator ________________________________ #24: Sweetness ________________________________

Basketball Players

#25: Black Mamba _______________________________ #26: CP3 _______________________________

#27: Dr. J _______________________________ #28: Earl the Pearl _______________________________ #29: His Airness _______________________________

#30: King James _______________________________ #31: Larry Legend _______________________________ via Wikimedia Commons

Published in Probate & Property, Volume 37, No 1 © 2023 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association.

January/February 2023 18

#32: Magic _______________________________ #33: Pistol Pete _______________________________ #34: Wilt the Stilt _______________________________ #35: Wizard of Westwood _______________________________ #36: Zen Master _______________________________

Ice Hockey Players

#37: The Great One __________________________ #38: Mr. Hockey __________________________ #39: Super Mario __________________________

Wrestlers

#40: Hulk ____________________________ #41: Nature Boy ____________________________ #42: The Rock (also an actor) ____________________________

Golfers

#43: The Black Knight _________________________ #44: The Golden Bear __________________________ #45: The Great White Shark __________________________

Prize Fighters

#46: The Greatest ___________________________ #47: Manassas Mauler ___________________________ #48: Raging Bull ___________________________ #49: Smokin’ Joe ___________________________ #50: Sugar Ray ___________________________

Answers:

via Wikimedia Commons

#38=Gordie Howe; #39=Mario Lemieux; #40=Terry Bollea (Hulk Hogan); #41=Richard Fliehr (Ric Flair); #42=Dwayne Johnson; #43=Gary Player; #44=Jack Nicklaus; #45=Greg Norman; #46=Muhammad Ali; #47=Jack Dempsey; #48=Jake LaMotta; #49=Joe Frazier; #50=Walker Smith Jr. (Sugar Ray Robinson or Sugar Ray Leonard)

Paige; #14=Willie Mays;#15=Ted Williams; #16=Babe Ruth; #17=Lawrence Berra; #18=Joe Namath; #19=Jerome Bettis; #20=Joe Montana; #21=Joe Greene; #22=Deion Sanders; #23=William Perry; #24=Walter Payton; #25=Kobe Bryant; #26=Chris Paul; #27=Julius Erving; #28=Earl Monroe; #29=Michael Jordan; #30=LeBron James; #31=Larry Bird; #32=Earvin Johnson; #33=Pete Maravich; #34=Wilt Chamberlain; #35=John Wooden; #36=Phil Jackson; #37=Wayne Gretzky;

Answers: Sports Nicknames: #1=Aaron Judge; #2=Frank Thomas; #3=David Ortiz; #4=Jim Hunter; #5=Pete Rose; #6=James Bell; #7=Ernie Banks; #8=Ty Cobb; #9=Hank Aaron; #10=Joe DiMaggio; #11=Reggie Jackson; #12=Nolan Ryan; #13=Leroy

#48=Ruth Bader Ginsberg; #49=Theodore John Kaczynski; #50=Thomas Edison

#38=Richard I of England; #39=Napoleon Bonaparte; #40=Edward Teach; #41=William Cody; #42=Jacqueline Kennedy Onassis; #43=Jackson Pollock; #44=Al Capone; #45=Claudia Alta Johnson; #46=Charles Lindbergh; #47=Warren Buffett;

#27=Abe Lincoln; #28=Thomas Jefferson; #29=Calvin Coolidge; #30=Richard Nixon; #31=Teddy Roosevelt; #32=Jesse Ventura; #33=Arnold Schwarzenegger; #34=Jerry Brown; #35=Margaret Thatcher; #36=Huey Long; #37=John J. Pershing;

Sinatra; #6=Sean Combs; #7=Aretha Franklin; #8=Gene Autry; #9=John (Dizzy) Gillespie; #10=John Wayne; #11=Jennifer Lopez; #12=Benny Goodman; #13=Charlie Chaplin; #14=Jean-Claude Van Damme; #15=Louis Armstrong; #16=Don Rickles;#17=William Shakespeare; #18=Theodor Seuss Geisel; #19=Stephen King; #20=Ernest Hemingway; #21=William Clinton; #22=George W. Bush; #23=James Madison; #24=Ronald Reagan; #25=Dwight Eisenhower; #26=Andrew Jackson;

Answers: Non-sports Nicknames: #1=Bruce Springsteen; #2=James Brown; #3=Michael Jackson; #4=Johnny Cash; #5=Frank

Published in Probate & Property, Volume 37, No 1 © 2023 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association.

January/February 2023 19

KEEPING CURRENT PROPERTY

CASES

BROKERS: Construction contractor who is not licensed as broker is not entitled to compensation for finding buyer for property. Choice Homes LLC (Choice), a construction contractor, was owned by two individuals who were the only employees. Choice delegated all office work and actual construction to subcontractors, who were, like the owners, unlicensed to sell real estate. In 2018, Choice entered into an oral agreement to buy a residential property if Choice found buyers who would purchase the property from Choice. Choice found buyers and executed contracts for the owners of the property to sell to Choice for $750,000 and the buyers to purchase from Choice for $1.3 million. Choice never completed its contractual obligations under the buyers’ contract, causing the buyers to not proceed to closing. After talks with both parties regarding disclosures over the condition of the property, Choice never sought to enforce either contract. Later that year the property owners did sell the property to the buyers without Choice’s involvement. Choice sued the buyers to get “what’s fairly due” for introducing the parties and finding the buyers their “dream property.” The trial court granted the buyers summary judgment in full and dismissed Choice’s complaint, citing Nebraska Real Estate License Act (Act), Neb. Rev. Stat. §81.885.01-81.885.55, which requires licensing as a broker or salesperson to collect a fee or commission on the sale of real estate. The court looked beyond the labels used by the parties as to their roles and concluded that Choice acted

Keeping Current—Property Editor: Prof. Shelby D. Green, Elisabeth Haub School of Law at Pace University, White Plains, NY 10603, sgreen@law.pace.edu. Contributor: Prof. Darryl C. Wilson.

Keeping Current—Property offers a look at selected recent cases, literature, and legislation. The editors of Probate & Property welcome suggestions and contributions from readers.

to negotiate a sale of the property with the expectation of receiving compensation for its actions. Choice appealed, and the supreme court affirmed, noting that the Act prohibits lawsuits for compensation by non-licensees, broadly defines the term “broker,” and provides that a single act committed by a person required to be licensed violates the Act. The court found that Choice performed a plethora of prohibited acts for the sellers and buyers, including finding and soliciting the sale to the buyers, introducing the sellers and buyers, and negotiating the terms of the sale to the buyers. It rejected Choice’s claim to the statutory exception that it was acting on its own behalf as an owner of the property instead of on behalf of others. In fact, Choice performed multiple prohibited acts before and after its purported ownership period, all with the expectation of receiving compensation. Choice Home, LLC v. Donner, 976 N.W.2d 187 (Neb. 2022).

EMINENT DOMAIN: Taking of a temporary limited easement is not compensable under the before-andafter evaluation methodology used for permanent easements. A county’s highway bypass project included the reconstruction, relocation, and expansion of a highway abutting the backyard of the Backuses’ residence. As part of the project, the county separately acquired a temporary limited easement (TLE) within the greater

highway easement already owned by the county. Backus sought compensation from the county, alleging various damages stemming from the TLE. The county granted compensation, but Backus appealed the amount, claiming he was owed the difference in the value of his property before the project and after the project’s completion under Wis. Stat. § 32.09(6g). The supreme court noted that although the statute does not specify whether the beforeand-after formula applies to both permanent and temporary easements, the formula addresses severance damages, which is compensation awarded to a landowner for loss in value after a partial taking of land. The before-andafter valuation is intended to capture the effect of the entire public improvement project on the fair market value of the property. Because the methodology attempts to address permanent reductions in fair market value, the statute cannot be read to apply to TLEs. A TLE is only a temporary use, with the owner regaining all rights when the TLE terminates. Applying the before-and-after measure for TLEs would be inconsistent with the statute, as it would never capture the actual effect on the value of the TLE while it existed; instead, it would capture the effect on the value of the same property interests—the whole property burdened with the permanent easement but not the TLE. Because the statute does not apply, compensation for the taking of TLEs must be calculated under constitutional and common-law principles. Backus v. Waukesha County, 976 N.W.2d 492 (Wis. 2022).

FORECLOSURE: Ad stating that sale is subject to first deed of trust may render foreclosure of condominium super-priority lien invalid. Snowden defaulted on her condominium assessments with more than $12,000 in

Published in Probate & Property, Volume 37, No 1 © 2023 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association.

January/February 2023 20

arrears. The condominium association, Capital Park, initiated foreclosure and, in the newspaper ad for the sale, stated that the property would be sold “subject to any prior liens, encumbrances, and/or municipal assessments, if any, including subject to the first mortgage lien.” The highest bid at the sale was $63,000 by Omid Land Group. The trustee’s deed to Omid stated that conveyance was “subject to any prior liens and mortgages, including the first mortgage lien.” Nearly a year and a half later, U.S. Bank filed a complaint for judicial foreclosure, alleging that Snowden owed $545,769 secured by a first mortgage on the condominium unit. Omid filed an answer and counterclaim, alleging ownership of the property based on the trustee’s deed. U.S. Bank answered, asserting that the sale was invalid as not conducted in compliance with the law and that the terms of the sale were unconscionable. U.S. Bank later claimed that the condominium foreclosure sale was void as a matter of law because Capital Park advertised the sale as subject to existing mortgage liens. The trial court granted summary judgment to Omid. The court of appeals reversed, largely on the ground that the trial court failed to apply current law on the operation of super-priority liens. As made plain by recent court decisions, the foreclosure of a condominium “super-priority” lien extinguishes all other liens on the property. This is the case even if the condominium association tries to preserve the mortgage holder’s lien by advertising the sale as subject to the first mortgage or deed of trust and even if the association tries to recover more than the most recent six months portion of arrearages in assessments entitled to super-priority status. But, as a matter of equity, the holder of the first deed of trust can seek to avoid extinguishment by challenging the validity of the sale on the ground that the unit sold at a price greatly below the amount of the mortgage and the apparent value of the unit. The erroneous statement in the advertisement of sale that the title would be subject to the first deed of trust resulted in an insufficient and unconscionably low sales

price by misrepresenting the effect of the foreclosure sale on the bank’s deed of trust. Omid’s bid was only 20 percent of the original mortgage and significantly smaller than the mortgage debt at the time of foreclosure. The appellate court remanded for further proceedings. U.S. Bank Trust v. Omid Land Grp., 279 A.3d 374 (D.C. 2022).

LANDLORD-TENANT: Tenants exposed to lead poisoning, who have not obtained a judgment or settlement against landlord, are not third-party beneficiaries under landlord’s liability insurance. Two classes of former and present tenants sued landlords for exposure to lead paint in their apartments. Between the two groups’ filings, the landlord’s liability insurers were successful in either rescinding the policies or reducing the coverage on the basis that the landlords misrepresented that there was no lead paint on the premises, when in fact the city health department had issued citations for lead paint. The tenants sought recovery under the original policy limits. At trial, the insurers moved to dismiss on the basis that the tenants were not thirdparty beneficiaries under the original policies instead, only incidental beneficiaries without enforcement rights. The trial court denied the motion, ruling that the tenants were third-party beneficiaries with vested rights in the policies as they existed before rescission or modification and that any agreements between the insurers and the landlords did not affect the tenants’ rights. The intermediate appellate court affirmed, ruling that the claimants obtained vested rights in the policies when they suffered their injuries. On further appeal, the tenants lost. The court explained the difference between the two types of contract beneficiaries. A third-party beneficiary is such because the parties intend for the third party to have that status, with the right to enforce the terms of the agreement. In the insurance context, under the common law and by the express terms of the insurance policy, a party who has obtained a judgment or settlement against the named insured is

a third-party beneficiary, entitled to rights under the policy as it existed at the time of judgment or settlement. Although nothing in the landlords’ policies required the insurer or the named insured to obtain the consent of any other person before canceling or changing the policy terms, any such changes would not affect the vested rights of tort claimants who had secured judgments against or entered into approved settlements with their landlords before cancellation or modification of coverage. In contrast, a party who is only injured by the insured is viewed as an incidental beneficiary but with no affirmative rights against the insurer. Thus, the tenants who had only suffered injury from the lead paint, but had not yet reduced their claims to judgment or settlement at the time the policies were changed, were bound by the reduced insurance amounts. CX Reinsurance Co. v. Johnson, 282 A.3d 126 (Md. 2002).

MECHANICS’ LIENS: General contractor’s failure to post notice of commencement of work to internetbased registry does not impair priority of later-filed subcontractors’ mechanics’ liens. In 2017, Dostal Developers, the owner of five lots in a new residential subdivision, served as a general contractor and hired two subcontractors, Borst and Kelly, to install utilities and roads and to grade the lots. The Iowa mechanics’ lien statute required Dostal to post a notice within ten days after the commencement of work to the Iowa Mechanic’s Notice and Lien Registry (MNLR) website, Iowa Code §572.13(A)(1), but Dostal never posted a notice. Later in 2017, Dostal obtained construction loans for work on the five lots from Finance of America Commercial (FAC), which promptly recorded its construction mortgages. In 2018, the two subcontractors posted notices and mechanics’ liens for work done in 2017. Dostal defaulted on the mortgages in 2018, and the subcontractors were not paid. The subcontractors filed foreclosure actions and FAC moved to dismiss, pointing to failures of the subcontractors to post notice of the liens within ten days of the commencement of work

Published in Probate & Property, Volume 37, No 1 © 2023 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association.

January/February 2023 21

KEEPING CURRENT PROPERTY

by Dostal. FAC claimed that the failure to comply with Iowa Code §572.13A(1) rendered the liens inferior, as a matter of law. FAC then filed a foreclosure action as well. The trial court found that all parties were entitled to foreclose, but that the mechanics’ liens had priority because Iowa Code § 572.13 gives a timely posted mechanic’s lien priority over all other liens that are perfected after the beginning of the contractor’s work. Because the subcontractors posted their liens within 90 days of completing their work, under Iowa Code §572.18(1), and FAC’s mortgages were recorded after they began their work, the subcontractor liens were superior. The supreme court affirmed, finding that the ten-day deadline for posting the notice of commencement to the registry applies only to general contractors and owner-builders, not to subcontractors. In the court’s reading of the statute, it would be absurd to require subcontractors to comply with the same ten-day deadline, not knowing when or if the general contractor had met the deadline; the ten days would necessarily expire before the condition precedent for posting was even satisfied. Because Borst and Kelly started their work before FAC’s mortgages were recorded, their liens had priority over FAC’s construction mortgage. Borst Bros. v. Finance of America Commercial, LLC, 975 N.W.2d 690 (Iowa 2022).

MECHANICS’ LIENS: Time for recording lien was not extended by COVID-19 emergency order tolling court proceedings. During the early months of the COVID-19 pandemic, a contractor sought to establish a mechanic’s lien on land leased to a developer for whom the contractor had performed work but had not been paid. In April 2020, the contractor recorded a notice of contract in the registry of deeds, but the notice failed to name the actual owner of the property land and also incorrectly described a neighboring parcel as the land. In July, the contractor filed a complaint seeking to enforce its mechanic’s lien. Then in September, the contractor corrected its error by recording an amended notice of

contract, properly identifying the owner and the land, but the statutory deadline of 90 days after completion of the work had elapsed. The landowner filed a motion to discharge the mechanic’s lien based on a late recording. The contractor argued that the 90-day statutory deadline was extended by four emergency orders of the Supreme Judicial Court, issued on April 1, April 27, May 26, and June 24, 2020, which modified in-person court operations and tolled “all deadlines set forth in statutes” that expired between March 17, 2020, and June 30, 2020. The trial court concluded that the deadline had been tolled. On appeal, the court explained that the referenced orders, issued pursuant to its superintendence authority under Mass. Gen. Law ch. 211, § 3, concerned court operations and pertained only to cases pending in court or to be filed in court, and did not apply to executive agencies such as the registry of deeds. Thus, the contractor lost its mechanic’s lien because it recorded a proper notice of contract too late. Graycor Constr. Co. v. Pacific Theatres Exhibition Corp., 193 N.E.3d 1083 (Mass. 2022).

MORTGAGE: Recording notice of trustee’s sale does not accelerate debt. In 2007, Bridges obtained a $500,000 loan to purchase a residential property, secured by a deed of trust. The promissory note and deed of trust included optional acceleration clauses authorizing the lender to accelerate the debt if Bridges defaulted. Both instruments required that the lender give notice of acceleration to Bridges, and the deed of trust also required that the lender provide notice of “(a) the default; (b) the action required to cure the default; (c) a date . . . by which the default must be cured; and (d) that failure to cure the default . . . may result in acceleration . . . and sale of the property.” In 2008, Bridges defaulted on the loan. The lender sent Bridges a notice of default, but it did not state that failure to cure the default would result in the acceleration of the loan or sale of the property. Bridges did not cure the default, which led to two notices of trustee’s sales,

one recorded in January 2009 and another recorded in May 2009. Neither notice invoked the optional acceleration clause, however, and the property was not sold. Seven years later, Bridges sought declaratory relief, arguing that the deed of trust could not be foreclosed because the six-year statute of limitations had expired. Bridges contended that the 2009 notices of trustee’s sales accelerated the debt, triggering the statute of limitations, Ariz. Rev. Stat. § 12-548(A)(1), which ran out in either January or May 2015. The trial court granted Bridges’s summary judgment motion, but the court of appeals reversed. The supreme court affirmed. It stated that as a matter of law, recording a notice of a trustee’s sale does not accelerate a debt. The plain language of the deed of trust showed that the acceleration was not self-executing; instead, it required specific notices and warnings. None of the notices of sale referred to or invoked the acceleration clause. Nothing in the communications to Bridges indicated that the lender was accelerating the debt. The court explained that the main reason why an express act of acceleration is required is that after a notice of sale under Ariz. Rev. Stat. § 33-813(A), a debtor can cure the default and reinstate the contract by paying only the “amount then due” before a trustee’s sale is held. Finding that mere notice amounts to an acceleration would nullify this right. Bridges v. Nationstar Mortg. L.L.C., 515 P.3d 1270 (Ariz. 2022).

RECREATIONAL USE IMMUNITY: Bollard placed in middle of biking trail may be a dangerous, latent condition subjecting landowner to liability. A bicyclist was riding on a biking trail developed by King County and hit a bollard placed in the middle of the trail, suffering severe injuries. The bollard was painted white and had a small red reflector attached to it. Years before the crash, an unknown person used fluorescent paint to write “POST” and other warnings on the pavement near the bollard to caution trail users as they approached it. But these conspicuous warnings had since faded.

Published in Probate & Property, Volume 37, No 1 © 2023 by the American Bar Association. Reproduced with permission. All rights reserved. This information or any portion thereof may not be copied or disseminated in any form or by any means or stored in an electronic database or retrieval system without the express written consent of the American Bar Association.

January/February 2023 22

KEEPING CURRENT PROPERTY

On the morning of the accident, the weather was wet and the skies were gray. The bicyclist sued the county to recover for his injuries, and the county defended by claiming immunity under the recreational use statute that shelters landowners from liability to persons using their land for recreational purposes. Wash. Rev. Code § 4.24.210. At issue was a statutory exception “for injuries sustained to users by reason of a known, dangerous, artificial, latent condition for which warning signs have not been conspicuously posted.” Wash. Rev. Code § 4.24.210(4)(a). All four terms—known, dangerous, artificial, latent—modify “condition,” not one another, such that all must be present for the exception to apply. Jewels v. City of Bellingham, 353 P.3d 204 (Wash. 2015). The trial court granted summary judgment to the county, and a divided appellate court reversed. On appeal, the supreme court affirmed, finding questions of fact on the grounds for the exception. In particular, the court found that the bicyclist had offered evidence that the county’s placement of the bollard created a “dangerous” condition, using the ordinary meaning of that term. The bicyclist also presented expert testimony that, depending on

the weather conditions, such as gray days, the bollards quickly faded into the background and were not perceptible by bicyclists while riding. The court distinguished a prior case that held that a condition is not latent if a user standing nearby can perceive the condition. The court reworked the Jewels test, stating that latency should be determined from the vantage of the recreational user, that is, the moving cyclist. A strongly worded dissent chastised the majority for overruling Jewels sub silentio Schwartz v. King County, 516 P.3d 360 (Wash. 2022).

RESTRICTIVE COVENANTS: