06 Burberry exits FTSE 100 after 15 years but EasyJet looks to have dodged relegation 07 Investors bet on Rolls-Royce recovery after engine trouble sparks sharp sell-off 08 Shares in maritime artificial intelligence company Windward are flying 08 Why investors have dumped Dollar General stock 09 Gym Group raises outlook ahead of first-half results

US non-farm payrolls in the spotlight after Jackson Hole speech

12 Why Foresight Solar Fund is beginning to radiate optimism

14 There are several catalysts to unlock the hidden value in Entain

15 Hold on to Rightmove shares amid takeover interest

Why you should still own highquality Kainos

Is bigger better when it comes to investment trusts?

Three important things in this week’s magazine

An ageing world

As the global population gets older we look at the implications for both governments and the private sector and the financial markets.

Is bigger better when it comes to investment trusts?

Closed-ended funds are combining amid persistently wide discounts, find out the pros and cons of this trend for investors.

Visit our website for more articles

Did you know that we publish daily news stories on our website as bonus content? These articles do not appear in the magazine so make sure you keep abreast of market activities by visiting our website on a regular basis.

Over the past week we’ve written a variety of news stories online that do not appear in this magazine, including:

Five sneaky ways you could be hit with tax on your savings

Examining how you can avoid falling into the trap of facing a levy on cash you’ve squirrelled away.

Burberry exits FTSE 100 after 15 years but EasyJet looks to have dodged relegation

Quarterly rebalancing sees luxury goods firm exit the UK’s flagship index and Raspberry Pi enter the FTSE 250

Luxury goods brand Burberry (BRBY) has ended its 15-year sojourn in the FTSE 100. The relegation comes after dramatic share price falls for the company in 2024. EasyJet (EZJ), which had been on course to suffer the same fate, looks to have saved itself with a recent rally (confirmation of the outcome of the reshuffle was due after market close on 4 September) .

In May this year, EasyJet investors became rattled as its chief executive of seven years Johan Lundgren said he was to step down in early 2025.

Lundgren’s decision to fly the coop was surprising given it came the same day the budget carrier reported a 22% increase in total revenue to £3.26 billion and a 17% increase in passenger revenue to £2.04 billion for the six months ending 31 March 2024.

Year-to-date Burberry shares are down 53%. It has been beset by issues not only the pandemic, but a slowdown in the global luxury goods market (especially in China) and a succession of senior staff changes.

In July 2017, Marco Gobbetti took the reins as CEO, but then left in 2021, followed by CFO Riccardo Tisci and COO Julie Brown. In 2021, Jonathan Akeroyd become CEO only to be replaced by former Coach, Jimmy Choo, and Michael Kors head Joshua Schulman this year.

Any company in the FTSE UK indices falling to 111th position or below in market cap terms is automatically deleted from the FTSE 100 and any company rising to 90th position or above is automatically added to the FTSE 100. If a company leaves the FTSE 100 because it has fallen to 111th position or below, the highest ranking FTSE 250 company, even if it is below 90th position, will enter the FTSE 100 as the number of constituents must remain at 100.

A similar process occurs for changes to the FTSE 250 index, although the bands for these changes are 325th or above or 376th or below.

Changes to the index are significant because of the flows from tracker funds, which have to buy the shares of the constituents of the index they track.

There was good news for affordable computer developer Raspberry Pi (RPI) which enters the FTSE 250 index, several months after making a strong debut on the London Stock Exchange with its IPO (initial public offering) priced at 280p (the top end of the range).

Bermuda-based insurer Hiscox (HSX) and largescale logistics warehouse investment company Tritax BigBox REIT (BBOX) were vying to take Burberry’s spot in the UK’s flagship index as we went to press.

Hiscox reported a solid set of full year results in March, doubling its pre-tax profit for 2023 to $625.9 million. its shares have gained 19% over the past year. [SG]

Burberry

Investors bet on Rolls-Royce recovery after engine trouble sparks sharp sell-off

Analysts say parallels to Trent 1000 problems wide of the mark

Aeronautical engineer Rolls-Royce (RR.) is not going to be caught up in a new crisis after airline Cathay Pacific (0293:HKG) found a fault with the engines used ’on its fleet of Airbus (AIR:EPA) A350 jets.

This was the prevailing mood among investors and analysts as the dust settled on a late afternoon trading session on 2 September following reports that a Rolls-Royce component failure led Cathay Pacific to cancel dozens of flights and ground A350 aircraft.

Rolls-Royce shares plunged more than 6.5% as news first emerged, before bouncing back strongly in early trading the following day 3 September.

The issue was discovered during a Cathay Pacific flight from Hong Kong to Zurich, leading to a widespread inspection of its A350 fleet. The inspections revealed similar problems in other engines, requiring component replacements.

Another serious problem with plane engines could throw Rolls-Royce’s recovery efforts into doubt. ‘A lot of people will remember the company’s previous crisis involving its Trent 1000 engines, which damaged the British engineer’s reputation and led to significant extra costs,’ said Russ Mould, investment director at AJ Bell.

Drawing parallels to past challenges faced by Rolls-Royce, particularly the Trent 1000 issues, Jefferies analysts note that those were far more complex and costly.

‘The Trent 1000 issues at Rolls-Royce led to circa £2.4 billion of excess cash costs over 2017 to 2022, with IPC, IPT and HPT blades affected across different subset of the Trent 1000 fleet,’ the analysts said.

In contrast, the current issue with the Trent XWB97 appears to be more contained and less likely to lead to such extensive costs. Reuters reported that the affected parts are thought to be fuel nozzles, which are easier to reach and examine than more crucial components like blades.

Shares magazine • Source: LSEG

Jefferies estimates that the market’s reaction, which led to a £2.7 billion loss in market cap, is pricing in an excessive cost impact. This valuation implies an average cost of £32 million per in-service A350-1000, £4 million if the A350-900 fleet is included, and £2 million if all engines, including those on order, are considered, according to Jefferies calculations.

‘These figures would only be justified in a worst-case scenario involving extensive parts replacements and significant flight disruptions across a broad fleet.’

Rolls-Royce stock has rallied hard during the past two years as the company worked tirelessly on recover efforts. ‘Given this is still a fluid situation, shareholders need to brace themselves for more share price volatility,’ said AJ Bell’s Mould. [SF]

DISCLAIMER: Financial services firm AJ Bell referenced in this article owns Shares Magazine. The author (Steven Frazer) and editor (Tom Sieber) own shares in AJ Bell.

Chart:

Shares in maritime artificial intelligence company Windward are flying

In June Winward launched an AI-powered virtual agent for the maritime and logistics industries

Maritime artificial intelligence specialist Windward (WNWD:AIM) clearly has the wind in its sails with its shares up 63% in 2024 and 192% over the last year driven by structural industry drivers which are helping the business reach break-even point ahead of expectations.

First-half results (20 August) showed revenue up 37% to $17.6 million, gross margin rising 3% to an impressive 81% and EBITDA (earnings before interest, tax, depreciation, and amortisation) loss shrinking by twothirds to $1.3 million.

Company-provided consensus analyst forecasts are calling for full year revenue of $36.2 million,

an adjusted EBITDA loss of $1.6 million and cash of $16.1 million. Management is confident of achieving break even adjusted EBITDA run rate during the financial year to 31 December 2024.

CEO and co-founder Ami Daniel summed up the group’s prospects: ‘With a high rate of renewal from existing customers, continued trading momentum into the second half, a highly competitive and differentiated offering, and high margin business, we anticipate the opportunity to keep building the company as the leader in Maritime AI for global trade.’

Windward’s growth is being driven by geopolitical risk, demand for

AI products, decarbonisation and supply chain pressures, all of which are creating more demand for the company’s insights and analytics. [MG]

Why investors have dumped Dollar General stock

Discount retailer Dollar General (DG:NYSE) was supposed to thrive during a period of higher interest rates, the rationale being its ultra-low price points would attract a broader cohort of customers during a cost-of-living crisis.

But the company, which caters to more rural areas across the pond, is struggling big time with wage cost pressures, greater markdowns to help shift unpopular products and ‘a core customer who feels financially constrained’, in the words of CEO Todd Vasos.

The shares have dropped 40%

year-to-date to $83, with the latest steep plunge triggered by dire second quarter results (29 August). These missed Wall Street expectations on both the top and bottom lines and demonstrated how parts of America are feeling the pinch from high borrowing costs, a softening jobs market and political uncertainty.

With its lower income customer cohort struggling and shrink, an all-encompassing term covering shoplifting, administrative errors and damaged goods, on the rise, the company slashed its sales and profit guidance for the full year.

Dollar General now expects samestore sales to be up 1% to 1.6%, lower than its prior outlook for growth of between 2% to 2.7%, while earnings per share is forecast to be in the $5.50 to $6.20 range compared with management’s previous guidance of between $6.80 to $7.55. [JC]

Poorer US shoppers are under pressure and the discounter is struggling with rising levels of ‘shrink’

UK UPDATES OVER T HE NEXT 7 DAYS

FULL-YEAR RESULTS

11 Sept: Dunelm, Frontier Developments, Pan African Resources

Gym Group raises outlook ahead of first-half results

Company is targeting opening 50 new sites over three years

Low-cost gym operator Gym Group (GYM) looks to be in good shape ahead of its first-half results, due to be released 11 September.

In a pre-close statement on 10 July the company raised its full-year profit expectations to the top end of market forecasts after continued positive trading.

Company-compiled analysts forecasts for EBITDA (earnings before interest, tax, depreciation, and amortisation) less normalised rent sit in the range of £38 million to £43.1 million.

First-half revenue increased by 12% to £112.1 million driven by the opening of four new gyms, a 9% increase in average revenue per member per month and higher memberships which reached 905,000 on 30 June. Like-for-like revenue was 9% ahead compared with the first half of 2023.

Analyst Douglas Jack at Peel Hunt expects full year revenue growth to be first half-weighted due to the timing of price increases, reduced

Group

promotional activity and tougher second-half comparisons.

By contrast Jack sees expansionary growth to be second-half weighted with 11 new sites slated to open during the period. He believes the new openings have been performing well.

The business has been raising headline prices more than peers and Jack thinks there is room for further increases given Peel Hunt’s in-house survey indicates its prices are around £1.50 per month below rival PureGym’s on average. [MG]

the market expects of Gym Group

Chart: Shares magazine • Source: LSEG

Oracle facing growth acceleration acid test

Move to AI, cloud and subscriptions has lots of potential but remains unproven ‘Magnificent Seven’ earnings are behind us and Oracle (ORCL:NASDAQ) is one of just a handful of S&P 500 stocks still to report. There could be fireworks when it does on 9 September.

While AI (artificial intelligence) excitement dominates the headlines Oracle has been quietly going about its own AI transformation, with vigorous expansion into cloud services a strategic move that provides customers with lots of options. Avid Premier League fans will be familiar with match data powered by Oracle Cloud, for example.

The transition from traditional licencing to cloud-based subscription services is expected to fuel accelerated sales growth for Oracle and continue the rapid rise of the shares, which are up 35% this year alone.

Crucial to keeping markets onside will be evidence that Oracle’s profitability is becoming more powerful, which should be aided by the full integration of health tech firm Cerner, bought for $28 billion in 2022. Oracle has also made considerable efforts to cut out excess cost.

This anticipated improvement in profitability is seen as a key factor that could influence the company's financial performance positively. Analysts at Edward Jones recently suggested that the current $141.29 share price may not fully reflect the firm’s optimism for sales growth acceleration.

This is the acid test, and recent quarterlies have left investors a bit underwhelmed, with mild forecast misses in June’s fourth quarter update. [SF]

UPDATES OVER THE NEXT 7 DAYS

QUARTERLY RESULTS

6 Sept: Kroger, BRP, ABM Industries, Brady, Tsakos Energy, Genesco, Hurco, BeyondSpring, Champions Oncology, Big Lots

9 Sept: Oracle, Rubrik

10 Sept: Petco Health and Wellness, InnovAge Holding, Adriatic Metals

11 Sept: Designer Brands

12 Sept: Adobe, Signet Jewelers

US non-farm payrolls in the spotlight after Jackson Hole speech

US and European central banks poised for September rate cuts

Federal Reserve chair Jay Powell’s speech at the Jackson Hole symposium made it clear that the central bank believes its work is more or less done in taming inflation and the focus now is to keep the US labour market in rude health.

The change of tone puts August’s non-farm payrolls data on 6 September firmly into the spotlight. The prior month’s 114,000 print fell way short of market expectations and briefly upset the stock market which worried the Fed’s decision not to cut interest rates in August was a policy error.

The Bureau of Labour Statistics’ 818,000 downward revision to the number of jobs created in the 12-months to the end of July did not help matters.

The consensus forecast for August is for a

Macro diary 05 September to 12 September

bounce back in the number of jobs created to 165,000 and investors will be watching closely for signs of weakness, including the rate of unemployment which has been nudging-up in recent months.

A weak jobs report may rekindle speculation of a half a percentage point interest rate cut in September although that could also be interpreted as a sign the central bank believes it is ‘behind the curve’.

Complicating matters, a bigger cut also runs the risk of being interpreted as political, given the proximity of the US election in November.

The European Central Bank has already started cutting interest rates and it will get a reading of how the Eurozone economy performed in the second quarter on 6 September before its next policy meeting.

The consensus view is for another quarter of a percentage point cut in interest rates on 12 September after a flash reading by the European Statistics office Eurostat showed Eurozone inflation slowed to 2.2% in August, its slowest pace since July 2021 and close to the central bank’s 2% target. [MG]

Next Central Bank Meetings & Current Interest Rates

Why Foresight Solar Fund is beginning to radiate optimism

Falling rates will boost the relative yield attractions of this sustainability-focused fund

Foresight Solar Fund (FSFL) 93.5p

Market cap: £533 million

Over 2023, infrastructure funds were among the worst performers in the investment trust universe as higher rates made assets like bonds and cash relatively more attractive. Caught up in the wider renewable infrastructure trusts de-rating was the Foresight Solar Fund (FSFL), a sustainabilityfocused vehicle invested in solar and battery storage assets in the UK and overseas.

Shares believes the turn in the rate cycle will bring a brighter future for the sector as gilt yields come down, leaving the high yields on offer looking more attractive to income-hungry investors.

Well positioned to capitalise on this shift, Foresight Solar’s shares have scope to re-rate from an 18.2% discount to NAV (net asset value) as debt falls and the FTSE 250 firm sells non-core assets at attractive prices. Based on its full year 2024 target dividend of 8p, Foresight Solar offers a bumper 8.6% yield and a share buyback programme of up

to £50 million, supported by the robust cash flows generated from a highly contracted revenue base, should limit the downside from here.

SUNNIER OUTLOOK

Foresight Solar is invested in and manages approximately 1GW (gigawatt) of renewable energy infrastructure in the UK and internationally. Steered by Foresight Group’s Ross Driver, the fund’s objective is to provide investors with a sustainable, progressive quarterly dividend and capital growth through investment in a portfolio of groundbased solar farms and battery storage systems, predominantly located in the UK.

The core of the portfolio is represented by ROC (Renewable Obligation Certificate) subsidised operational UK solar PV projects, alongside UK battery storage assets, Australian solar PV and Spanish solar PV assets. The company argues its UK sites consistently outperform peers in converting solar irradiation into electricity thanks to its dedicated team’s consistent application of advanced techniques.

‘We’ve got a strong portfolio here in the UK,

Foresight Solar (p)

Chart: Shares magazine • Source: LSEG

Foresight Solar Fund's countries by installed capacity

which is where we are centred,’ explains Driver. ‘But we’ve also got our investments in Spain and Australia, so there is that international diversification to the fund. When the sun doesn’t shine over here, we should have some balance and diversification through those other markets.’

PORTFOLIO POWER

‘We’ve got the biggest share buyback programme in the sector relative to the size of the fund, we’ve increased that to £50 million,’ adds Driver, who believes that the renewables sector as a whole will benefit from a re-rating ‘once we start to see some more certainty in rate cuts coming through and now that power prices are settling down’.

Merely generating income isn’t enough in the current environment, so Foresight Solar Fund is now pursuing a refreshed strategy with a greater emphasis on total returns, specifically boosting returns through development and construction activities and with non-core portfolio assets being earmarked for sale. ‘Our yield is about 9%, but we also want to deliver a further 1% to 2% in capital growth and we are driving that through the development pipeline we are looking at,’ enthuses Driver.

In a second quarter update (8 August), Foresight Solar published an NAV of 114.9p per share, a

small 0.2p increase over the quarter as near and long-term power price forecasts in the UK trended up, although this impact was largely offset by below-budget irradiation and generation due to unplanned network outages and a small number of inverter issues.

Foresight Solar’s assets in Spain and Australia continued to perform poorly, again given poor weather and network outages, and overall production for the whole global portfolio was 7.1% below budget.

Yet despite this below-budget generation in the period, cash flow remained resilient, primarily due to Foresight Solar’s power price hedging strategy. Visibility is high too, with the proportion of contracted revenue for Foresight Solar’s global portfolio being 89% for 2024, 83% for 2025 and 63% for 2026.

At 65% of NAV, Stifel observes that Foresight Solar’s net leverage is a bit lower than some peers, although it ‘remains too high in our view given the costs of debt and volatility in power prices’. However, the trust will update the market on its disposal programme at the forthcoming first-half results (18 September), which may provide further clarity on debt reduction and share buybacks, while ongoing charges of 1.15% are reasonable for a specialist renewable energy trust. [JC]

Foresight Solar's key sustainability stats

Table: Shares magazine • Source: Foresight. Data for period 1 January to 30 June 2024.

Table: Shares magazine • Source: Foresight

There are several catalysts to unlock the hidden value in Entain

Growth, earnings, sentiment and valuation all look to be at trough levels

Entain (ENT) 630.4p

Market cap: £4.13 billion

Investing in the gambling sector may not be everybody’s cup of tea but we believe embattled sports betting and gambling firm Entain (ENT) has become so unloved and neglected that the upside potential now comfortably outweighs the downside risks.

With several activist investors on the share register pushing for change, rumours of private equity interest in breaking-up the group and a newly appointed CEO (Gavin Isaacs), there are numerous paths to unlock value which should act as a catalyst for the shares to recover.

Entain is the second worst performer in the FTSE 100 over the last year with the shares having lost 44% of their value and they sit 85% below their £22 peak in October 2021.

Long-suffering shareholders have seen the board turn down a shares and cash offer equivalent to £28 a share from US fantasy sports betting company DraftKings (DKNG:NASDAQ) in 2021 and a £14 per share offer from US its jointventure partner BetMGM a few months earlier.

Under the company’s previous strategy Entain had acquired leading brands and including Ladbrokes Coral in the UK, BWIN in Europe, while establishing a US presence via a 50/50 joint-venture with BetMGM.

which have not been integrated onto the firm’s technology platform.

These include BetCity, a Netherlands business which was bought for £398 million, Sweden-based Enlabs and CrytalBet in Georgia. The total revenue contribution from brands not on the tech platform equated to around 35% of Entain’s online gaming revenue in 2023.

Recent acquisitions under the prior CEO Jette Nygaard-Andersen were more questionable which is a particular gripe for activist Eminence Capital which has a seat on Entain’s board.

Based on sources familiar with the matter, analysts at Berenberg believe investment bank Moelis is advising Entain on the disposal of brands

Disposals are just one way to unlock value in the group. A key part of the investment case is the valuation of the group ascribed by the market is too pessimistic.

AVI Global Trust (AGT) has a stake in Entain and commentary from the manager suggests the company trades at a significant discount to its own history and listed peers of between 25% and 45% as well as valuations implied by recent merger and acquisition activity.

Greg Johnson at Shore Capital reckons that excluding the value of BetMGM, Entain is valued on a PE (price to earnings) ratio of just 13 times which he believes has the potential to re-rate ‘materially’ considering a move back to growth in the first half and momentum in the US. [MG]

Entain

Hold on to Rightmove shares amid takeover interest

Company should command a significant premium if any deal is to get over the line

Rightmove (RMV) 676p

Gain to date: 17%

Market cap: £4.4 billion

On 11 January Shares said that the UK’s biggest property portal Rightmove (RMV) was unloved and should be snapped up by investors due to a bargain-basement valuation.

WHAT HAS HAPPENED SINCE WE SAID BUY?

On 26 July the company reported a strong set of first half results with a 7% rise in revenue to £192.1 million as agents and new homes developers renewed contracts.

Rightmove also unveiled bumper returns to shareholders of £100.2 million through share buybacks and dividends.

The company maintained its guidance for the full year 2024 with expected revenue growth of 7-9% and full year ARPA (average revenue per advertiser) growth of £75-85.

Rightmove

Chart: Shares magazine • Source: LSEG

Fast forward to 2 September and it emerged Rightmove was subject to takeover interest from an Australian property listings company REA which has investments in property portals in Australia, India, Singapore, Vietnam, Malaysia, Thailand, and the US (it is controlled by Rupert Murdoch’s News Corp). No further details have been given by REA about any potential approach other than that it might be a cash and shares deal. REA has until 5pm on 30 September to formally make an offer or walk away. Not surprisingly Rightmove’s shares reacted positively to this takeover interest, up around 27% on the day.

WHAT SHOULD INVESTORS DO NOW?

Hold on for now. REA’s move looks opportunistic and we would expect for any bid to be successful it would have to be at a higher premium than the current share price implies. Panmure Liberum analyst Sean Kelly says a premium of up to 60% versus the undisturbed share price would be realistic and Berenberg thinks a take-out price of 830p would be in-line with the price tag of other platform businesses. [SG]

Why you should still own high-quality Kainos

Short-term issues are clouding its long-run attractions

Kainos (KNOS) 967.5p

Loss to date: 4.8%

Talking down growth is never a good sign and Kainos (KNOS) shares show the scars of that mood change. When we flagged the company in May (16 May) it was on the premise that slowing digital workloads bolstered by AI (artificial intelligence) scope to take out costs and provide growth for corporate clients was a theme ready to turn, but that improvement has thus far failed to emerge.

The net result is that the Belfast-based software supplier is now steering investors towards lower growth than hoped for, and crucially, below market consensus, which had been pitched at £416 million revenue for the year to 31 May 2024.

WHAT HAS HAPPENED SINCE WE SAID TO BUY?

It is sometimes said that timing is everything but getting it right remains very tricky.

Within days of our article, the stock had rallied 25% but those gains have drifted into the ether as the invisible hand of the market steered a

different course.

Yet Kainos remains one of those rarities, a UKlisted tech business capable of withstanding the slings and arrows of outrageous fortune and we fully anticipate management to be front footed when it comes to addressing its issues, be that seeking out new areas of growth, reeling back on running costs, or most likely some combination of the two.

WHAT SHOULD INVESTORS DO NOW?

It is worth bearing in mind that lowering forecasts is not something Kainos does lightly or frequently but against a backcloth of ongoing softness in the commercial sector, or delays in public sector projects, many impacted by the general election, its impressive built from the ground up Workday (WDAY:NADAQ) practice is untypically struggling.

The US enterprise software giant is experiencing slowing growth itself, albeit still 17%-odd in its second quarter report, and perhaps as Kainos continues to consolidate its positioning as a global Workday partner, we should expect its growth profile to converge.

With robust and firm operating margins (16%) and outstanding return on capital (36.7%), we still see Kainos as a great company own for investors playing a long game, especially on a price to earnings ratio below 20. [SF]

BECOME A BETTER INVESTOR WITH

SHARES

MAGAZINE HELPS YOU TO:

• Learn how the markets work

• Discover new investment opportunities

• Monitor stocks with watchlists

• Explore sectors and themes

• Spot interesting funds and investment trusts

• Build and manage portfolios

Is bigger better when it comes to investment trusts?

Closed-ended funds are combining amid persistently wide discounts

Eight months in, 2024 is already a record year for M&A (mergers and acquisitions) in the investment trust sector.

Trust boards are increasingly focused on value for money and shareholder returns amid persistently wide discounts to NAV (net asset value) and with activists nosing around. A major trend underway is mergers between sub-scale trusts with similar remits to create funds large and liquid enough to attract wealth managers and retail investors.

The investment trust sector faces some structural headwinds to demand which explain these stubbornly wide discounts. These include the rise of tracker funds, retail investors pulling in their horns due to cost of living pressures, not to mention the misleading cost disclosures casting a pall over sentiment towards closed-ended funds.

Due to this dicey backdrop, Deutsche Numis says trusts are ‘in a battle to stay relevant in the face of a lack of demand from many traditional buyers’ and with fixed income offering yields that offer a credible alternative to ‘alternatives’.

A consequence of smaller trusts combining with rivals or winding-up is that some good strategies will go to the wall in this process of creative destruction, but larger vehicles should be more liquid and reduce trading costs, and have scope to spend more on marketing, thereby gathering more assets and creating a virtuous cycle of growth.

This new landscape of investment trust giants has many positives, but there are also negatives for investors to be aware of.

THE URGE TO MERGE

The current spate of mergers is justified by calls for fewer, larger trusts from a dramatically consolidated wealth management sector, together with increased focus on costs. A merger can be a silver bullet for addressing a persistent discount, because combining two or more smaller trusts creates a single vehicle offering superior liquidity and economies of scale.

James Carthew, head of investment companies at QuotedData, says one justification for mergers is that the big wealth managers, who are themselves consolidating, ‘have to write such big tickets that they cannot contemplate investing in small funds for fear of dominating share registers.

‘That is a valid argument but the minimum size that they will accept has risen rapidly from a couple of hundred million a few years ago to a billion or more today.’

Cynics might reason that corporate advisers’ need to supplement their income in the absence of a lucrative IPO (initial public offering) market is another factor behind this urge to merge, while managers will be looking to add to their assets under management or find ways of preventing money from flowing out the door.

Running costs and bid-ask spreads are an issue for sub-scale trusts and both tend to increase as funds get smaller. In contrast, bigger investment trusts benefit from scale economies, appeal to a wider range of investors and can also negotiate better terms on debt to boot.

SURVIVAL OF THE FITTEST

Deutsche Numis believes it is healthy that trusts that have failed to live up to expectations are reinvented, merged or wound-down. This should mean that the remaining universe of trusts ‘becomes more attractive to potential investors, as the strong survive’.

Peter Walls manages the Unicorn Mastertrust Fund (3121801), which aims to achieve long term capital growth by primarily investing in a range of listed investment companies. ‘If you look back over the last 50 years, 85% of the trusts that existed in 1974 do not exist today,’ he informs Shares. ‘And throughout those decades many new trusts will have come and gone as well. I consider this process of sorting the wheat from the chaff to be an important feature for investors as it ensures that when things do not go according to plan there can be a solution.’

Walls thinks the Alliance Witan merger is one that makes a lot of sense. ‘It will create a large liquid trust which will give index funds a run for their money. The merged trust will have plenty of tools in its toolbox, including share buybacks and issuance, to incrementally enhance total return for long-term investors,’ he enthuses.

Also weighing in is Thomas McMahon, head of investment companies research at Kepler Partners, who thinks the current wave of consolidation is to be celebrated.

‘There have been plenty of trusts on persistent discounts for years that just haven’t been wide enough to prick boards into doing something about it, and the shakeout of the past 18 months or so has forced action,’ says McMahon. ‘There will be time for a thousand flowers to bloom, but now is the moment to cull the ancien regime.’

COME TOGETHER, RIGHT NOW

This year’s standout deals including the proposed mega-merger of Alliance Trust (ATST) and Witan (WTAN) to create a goliath called Alliance Witan with net assets north of £5 billion and a market cap big enough for FTSE 100 inclusion. This bigger investment trust beast will also carry lower ongoing charges with a target around the high 50s basis points in future, below Witan’s and Alliance Trust’s current ongoing charge ratios of 0.76% and 0.62% respectively.

2024 has also witnessed several mergers between trusts sharing the same management group, including JPM MultiAsset Growth and Income into JPMorgan Global Growth & Income (JGGI), a trust whose assets have risen rapidly through strong performance and mergers, having previously absorbed stablemate JPMorgan Elect and also The Scottish Investment Trust. The sector has also seen a combination of JPMorgan UK Smaller Companies and JPMorgan Mid Cap, two trusts which shared the same managers and had portfolio overlap aplenty, to create JPMorgan UK Small Cap Growth & Income (JUGI), not to mention the merger of two Janus Henderson Investors-managed Europe funds to form Henderson European Trust (HET). On 2 September Artemis Alpha Trust (ATS) announced it had agreed to be taken over by UK All Companies sector rival Aurora Investment Trust (ARR).

Other examples include the rolling of the Troy Income & Growth into STS Global Income & Growth (STS) and abrdn China into Fidelity China Special Situations (FCSS), while RTW Biotech Opportunities (RTW) has also acquired Arix Biosciences.

McMahon highlights JPMorgan Global Growth & Income as an acquisitive trust that is giving investors what they want. Over the past two years or so, it has absorbed three trusts with very different approaches to investing globally that had struggled to get to scale.

CASH ME OUT PLEASE

Charlotte Cuthbertson, co-manager of MIGO Opportunities Trust (MIGO), says that with discounts at historically wide levels, it is reassuring to see boards ‘not resting on their laurels and the fact that there has been lots of acquisitions, mergers, realisations etc. It is important for boards to be very thoughtful about their shareholders and do the best thing for them. Liquidity is important, especially in a world that is becoming ever more illiquid. However, it can be a bit of an easy way out, because what’s very important for all investors, whether it is retail or institutional when you are going through these merger processes, is for there to be a cash exit option.’

For the uninitiated, it is considered good practice for boards to offer shareholders the chance to redeem some or all of their shares for cash as part of a merger deal. Cuthbertson reasons: ‘Otherwise you end up with an overhang of shareholders that just want out and actually that doesn’t improve liquidity, because what you’ve now got is a big trust with an overhang. Cash exits are very, very important so that you can head off if you want to.’

‘The combination of a quality growth portfolio with an optional income is clearly highly appealing to a broad variety of investors, while the successful execution of the strategy, evident in strong performance numbers, has built confidence in the managers,’ explains McMahon. ‘Or take the absorption of UK Commercial Property’s assets by Tritax Big Box REIT (BBOX). Just as consumers want cheap Amazon deals, investors want to own the

Investment trusts: Mergers

logistics network that makes them possible, and the market is giving them what they want.’

BIG ISN’T NECESSARILY BEAUTIFUL

A major negative arising from this Darwinian process for the private investor is reduced choice. One thing keeping James Carthew awake at night is the degree to which investors are encouraging these deals ‘because they have been disappointed by short-term performance, and funds that might rally when the cycle turns will no longer exist.

‘This is most evident in the property sector, where the number of funds on offer is shrinking rapidly and just ahead of a likely rally in the sector as interest rates fall.’

Other areas of the market where this could also be the case include Japan, where following a bout of underperformance by small cap trusts, there has been a rush for the exit, most recently with the proposed absorption of JPMorgan Japan Small Cap Income & Growth (JSGI) by JPMorgan Japanese (JFJ). ‘One of the strengths of the investment companies industry is that a fund with a fixed pool of capital can take advantage of short-term swings in sentiment - acting as a buyer of last resort and therefore picking up bargains,’ Carthew informs Shares. ‘However, this wave of M&A is disrupting that.’

Unicorn’s Walls adds: ‘Big isn’t necessarily beautiful of course. There has to be a place for smaller investment trusts if the sector is to offer diversity and provide a launch pad for the successful trusts of the future. The trust sector would be a poorer place without the likes of Rockwood Strategic (RKW), Odyssean (OIT) and Strategic Equity Capital (SEC). Elsewhere, I need to be able to consider investing in smaller specialist trusts such as Literacy Capital (BOOK) or RTW Biotech Opportunities.’

Walls also makes the point there needs to be a place for bringing new strategies to the market to invest in less liquid specialist investments, ‘otherwise trusts that could emulate the success of AVI Japan Opportunity (AJOT) and Nippon Active Value Fund (NAVF) will never get off the ground’.

By James Crux Funds and Investment Trusts Editor

AN AGEING WORLD

How to invest for a demographic dividend

It’s said there are only two certainties in life –death and taxes – and as it stands the world is steadily getting older, with not enough births or young people coming through to offset the increasing ranks of the middle-aged and old-aged.

By Ian Conway Deputy Editor

Moreover, according to the United Nations’ latest World Populations Prospects study which came out earlier this year, the global population is likely to peak this century with one in four people already living in a country whose population has peaked in size.

So, what are the implications for say the UK in terms of the economy, government spending and the consumption of goods and services, and how should investors think about these factors in terms of their portfolio?

WHAT ARE THE BIG TRENDS?

One of the tricky aspects of studying demographics is it is constantly changing – for example, a decade ago the probability of the global population peaking this century was only 30%, but rapid fertility declines in populous countries mean in just 10 years that probability has risen to 80%, while in 63 countries, containing 28% of the world’s population, the size of the population has already peaked.

Women today bear one child fewer than they did on average in 1990, with more than half of countries and areas having a fertility rate below 2.1 which is the level needed to maintain a constant population size without migration.

On the other hand, we are all living longer as global life expectancy has already returned to preCovid levels is expected to reach around 77 years by 2054 compared with just over 73 years today.

In about 100 countries or regions the working-age population (20 to 64) will grow over the next three

decades, offering a window of opportunity known as ‘the demographic dividend’, but the UN cautions these countries need to invest in education, health and infrastructure in order to capitalise on this opportunity.

WHAT ARE THE TRENDS IN THE UK?

Since 1950, the UK population has grown from just under 50 million to just under 69 million as of 1 July last year, with women slightly outnumbering men (34.9 million against 33.8 million).

The median age of the population is just under 40, and average life expectancy from birth has risen from 68.6 years in 1950 to 81.3 years with women generally outliving men by around four years (83.2 years versus 79.4 years).

Over the same period, life expectancy from the age of 65 – and this is key when we come to consider peoples’ need to save for their retirement as well as things like demands on the NHS – has risen from 13.2 years to over 20 years, with women once again outliving men (20.9 years against 18.9 years).

The other good news is the natural change in

terms of births minus deaths is 35,000 per year, so for now the population is replenishing itself slowly but steadily.

Looking forward to 2054, the UN forecasts the UK population will rise to 75.8 million, which is more or less the peak, before steadily declining through the end of the century.

The median age will have crept up to around 44, but more importantly, the rate of natural change, ie births minus deaths, will have turned negative to the tune of 125,000 people per year.

Life expectancy at birth will have crept up to 85.6 years, with women still outliving men by more than two years on average, while life expectancy at age 65 will have risen to over 23 years meaning those approaching retirement will need to make their pensions and savings stretch that bit further than if they were retiring today.

Finally, while the data applies to ‘more developed countries’ in Europe rather than just the UK, the proportion of working age people (24 to 64) to those in retirement (65-plus) is set to swing from 53.5%/20.5% to 53.7%/29.5% so income tax and other taxes will probably have to rise in order to fund the pensions of those no longer in work.

Obviously, this is just a recommendation from a trade body rather than government policy but were something similar ever implemented it would substantially increase the financial burden on companies and could eat into their spending in other areas like marketing or R&D (research and development).

THE HEALTHCARE BURDEN

According to the ONS (Office for National Statistics), over the next 25 the fastest-growing age segment will be the over-75s, who are expected to make up almost half the increase in headcount (3.6 million out of roughly 8 million) and account for 13% of the UK population against less than 9.5% today.

An ageing population will need more medication and more replacement knees and hips, as well as glasses and hearing aids, so makers of pharmaceuticals and medical products are onto a winner in the long term.

In terms of care, however, the NHS was already struggling well before the pandemic, and although the new government has made cutting waiting times a priority the job is going to be that much harder with a larger cohort of elderly, infirm patients.

WHAT ARE THE IMPLICATIONS?

The most obvious consequence of more people living to a greater age and a population which is ageing in general is the need for those in work now to make sure they have enough put aside to live on once they are no longer getting a salary.

That means greater demand for pensions and savings products, which is good news for providers like Aviva (AV.), Phoenix Group (PHNX) and Just Group (JUST).

Aviva is the largest UK provider of individual annuities and of workplace pensions and manages the largest book of equity release mortgages, making it a major beneficiary of the potential increase in demand for savings and retirement products.

In its report ‘Five Steps To Better Pensions’, the PLSA (Pension and Lifetime Savings Association) argues over the next decade contributions into workplace pensions need to rise from 8% to 12%, with employees putting in an extra 1% and companies putting in an extra 3% so both sides contribute 6% each and sharing the burden equally.

Adding to this burden, diseases such as dementia are much more prevalent in the over-75s (86% of all sufferers according to the NHS), with the number of cases diagnosed each year set to rise from around 900,000 in 2020 to 1.23 million in 2030 using projections from the Alzheimer’s Society.

Care homes are a critical and growing part of the health infrastructure as they provide a better environment for frail and elderly patients who don’t need intensive medical care than hospital wards, and they are cheaper.

There are currently around 13,000 patients in hospital simply because they aren’t being offered care in the community such as step-down, nursing or residential homes, and half of this number have been in hospital for more than three weeks.

Investment trusts such as Impact Healthcare REIT (IHR) are an essential stopgap for the NHS, and demand for residential care is only going to grow over the next couple of decades.

THE LIFE OF RILEY

Assuming we are fortunate enough still to have all our faculties by the time we reach 75, we may feel

THE TECH EDGE FOR A HEALTHIER, HAPPIER AGING POPULATION

Technological advances can provide many tools that can help us to combat common problems that older people are likely to encounter. If we can match technology with the needs and wants of seniors, improvements can be made to individuals’ lives and society.

A World Economic Forum report in 2021 explored the topic of tech assisted aging by combining recent academic research on innovation in healthy ageing, splitting their findings into eight segments based on their areas of impact in the human ‘healthspan’ and then split across three categories representing the stages of the ageing process as the graphic shows.

‘Digital tools and services can play critical roles in and enabling healthy and active ageing by promoting independence, enabling social participation, and ensuring healthcare access’, the report said.

According to the WEF, the global technology market for older adults’ care increased from approximately $5.6 billion to an estimated $13.6 billion in 2022 but this is merely scratching the surface of what will likely be required in the future.

A healthier, more independent, and more content older adult population represents ‘a huge market opportunity to create products and services to support the increased life expectancy and empower older adults, ’ the report said.

Imagine a scenario. A 75-year-old has checked

in to hospital to receive some minor surgery, but the surgeon is miles away from the theatre. No problem, they connect remotely, and a robotic surgical system conducts the procedure. The patient is then sent home via a self-driving taxi, helped into their home by a humanoid home help, who settles you into your favourite chair to begin recuperation, managing the daily chores (preparing a meal, washing up) for you.

Their ongoing well being is being remotely monitored by an automated healthcare assistant via internal and external sensors, while a recovery physiotherapy programme is administered by your humanoid home help. In the meantime, a robotic exoskeleton suit allows them to move more easily around, while a home hub allows them to stay in touch with friends and family while they rest, entertainment and intellectual stimuli provided by a series of apps help keep boredom at bay while they are confined at home.

This might all sound fanciful right now, much like watching your favourite TV shows on the go or checking your blood-sugar levels with your mobile phone did a couple of decades ago did. Yet it is the sort of connected and automated care system that is already making strides through advancements from companies like Intuitive Surgical (ISRG:NASDAQ), Uber (UBER:NYSE), Tesla (TSLA:NASDAQ), DexCom (DXCM:NASDAQ), Amazon (AMZN:NASDAQ), Keyence (6861:TYO), Cyberdyne (7779:TYO) and many others. [SF]

like spending our hard-earned wealth and enjoying our golden years.

Travel and leisure has seen a huge boom since lockdowns were eased, but far from ‘normalising’ as many expected demand continues to grow and the industry has homed in on the wealthy retired segment of the market in a big way.

It is virtually impossible to turn on the TV of an evening and not see at least one advert for a cruise: even Antarctica, the seventh continent and the world’s largest wilderness, is no longer beyond the reach of thrill-seeking septuagenarians.

Tour operators, hotel companies and holiday rental portals all stand to gain as wealthy ‘seniors’ take to spending on experiences rather than things like the rest of us – as the saying goes, you can’t take it with you.

AN ETF TO TAP INTO THE AGEING POPULATION THEME

An obvious way to invest to benefit from shifting demographic dynamics is through a dedicated exchange-traded fund which offers a combination of low charges and diversification benefits. The main option is iShares Ageing Population (AGES). This is comfortably the largest and most liquid product and it has relatively modest ongoing charges for a specialist ETF of 0.4%.

Its performance has been relatively uninspiring – with an annualised total return of 4.3% over five years. But over one year it has achieved a 10.2% total return and, given the trends it is looking to tap into are likely to accelerate, there is scope for performance to pick up.

Looking at the names within the ETF is an interesting exercise and could provide some ideas if you want to go down the road of buying individual

stocks. The top 10 is a balance between health care and pharmaceutical names and financial institutions selling pensions, life insurance and other retirement-related savings products. Together the financial and health care sectors account for nearly 90% of the portfolio.

Beyond this there are names like Ventas REIT (VTR:NYSE) – which owns and rents out research, medicine and health care facilities –as well as Expedia (EXPE:NASDAQ), to tap into travel demand among an older cohort, and RV (recreational vehicle) manufacturer Thor Industries (THO:NYSE). [TS]

TWO HEALTH CARE PICKS WITH DEMOGRAPHIC DRIVERS

Although undeniably a good thing, living longer exposes

as

higher consumption of healthcare services over time.

One caveat to be aware of in this otherwise rosy prognosis for healthcare is the increasing demands on healthcare systems and government budgets, potentially putting pressure on drug prices, but this is nothing new.

While some investors might be comfortable researching and choosing the companies most likely to benefit from these trends, for many the prospects look akin to searching for the proverbial needle in a haystack.

A lower risk option is to invest in a diversified, actively managed portfolio run by seasoned investors.

Portfolio managers Ailsa Craig and Marek Poszepczyski, portfolio managers at International Biotechnology Trust (IBT) believe demographic trends underpin a particularly strong growth story in biotechnological innovation.

More clinical trials are being registered than ever before with nearly 40,000 in 2023, a new annual record. Many of the new drugs are being discovered by biotechnology companies rather than in the research and development departments of large pharmaceutical companies.

This means big pharma is often on the hunt for innovative biotechnology firms to fill their innovation pipelines. Mergers and acquisitions have picked up significantly in recent months and the trust has seen several investee companies taken over at premium prices.

Craig and Poszepczyski believe selective investments in biotech businesses which focus on high unmet medical needs, with attractive valuations and strong earnings potential are key to unlocking outperformance in the years ahead.

The trust trades at an underserved 10% discount to NAV (net asset value) and unusually, pays a dividend of 4% a year paid out of NAV. The trust has outperformed the Nasdaq Biotechnology index over the last five and 10 years and delivered a smoother return.

This is due to the team’s risk mitigation policy and the wide diversification achieved by investing across different therapeutic areas and stages of drug development.

The managers also reduce risk by trading around binary events such as the results of clinical trials, reducing weightings ahead of an event and topping up once the results are known, if appropriate.

The trust focuses on therapeutic areas which have strong pricing power such as cancer and orphan drugs. It has a relatively high ongoing

charge of 1.44% a year compared with a 1.16% sector average.

Danaher DHR:NYSE $267.87

Market cap: $194.5 billion

US-listed Danaher (DNR:NYSE) is an unusual company in that the business as it exists today has been pieced together by strategic acquisitions.

Technically it is a holding company with three divisions or franchises comprising diagnostics (40% of sales), biotechnology (30% of sales) with life sciences accounting for the rest.

Danaher was established by the reclusive Rales brothers in the 1980s who envisioned building a company with a focus on continuous improvement and customer satisfaction.

Today they call this DBH (Danaher Business System) and it is inspired by the Japanese business philosophy of Kaizen which means change for the better.

From the 1990s the company started to focus on science and technology and built leadership positions in fast growing end markets with secular growth drivers.

With a keen focus on innovation and improvement, we believe the company is well positioned to benefit from changing demographics.

The company has impressive financial metrics, having converted more than 100% of net profit into free cash flow for the last 32 consecutive years.

Disclaimer: The author (Ian Conway) owns shares in Phoenix Group.

Discover the most shorted stocks on the UK market

From the list, Ocado and Burberry have been relegated from the FTSE 100 and Pennon faces regulatory scrutiny

You might not think online grocery retailer Ocado (OCDO), luxury goods group Burberry (BRBY) and UK water utility giant Pennon (PNN) have much in common. However, they are all among the most shorted stocks according to data from the FCA (Financial Conduct Authority) daily short position report which you can find on the published on the ShortTracker website.

WHAT IS SHORT SELLING?

Short selling also known as shorting or going short is a trading strategy which involves an investor speculating that a stock will go down in value with the aim of profiting from such a move.

Short selling can be applied to other financial markets including foreign exchange, commodities, and indices and is typically conducted by hedge funds but not exclusively.

For example, VT Argonaut Absolute Return (B7FT1K7), steered by Barry Norris, takes both ‘long’ and ‘short’ positions.

To execute a short you borrow shares with the aim of selling them and then buying them back later at a lower price.

Short selling positions above 0.2% of a listed company’s issued share capital must be disclosed to the FCA.

WHY ARE THESE STOCKS BEING SHORTED?

It is no surprise that stocks like Ocado, Burberry and Pennon have attracted the attention of short sellers thanks to their past performance.

Bad news has engulfed Burberry. The monobrand fashion firm has suffered due to a slump in demand for luxury goods globally.

The recovery in the Chinese market hasn’t materialised (so far) this year and the company has suspended dividends, issued profit warnings, and replaced its chief executive Jonathan Akeroyd with former Coach, Jimmy Choo, and Michael Kors head Joshua Schulman to steady the metaphorical ship.

Short sellers have piled in as shares continue to trade at 10-year lows. Over the past year the shares are down 69%. There are four institutions with disclosed short positions and 5.4% of the issued share capital was being shorted as of 28 August.

Burberry has also been relegated from the FTSE 100 (recently) after 15 years, a fate which befell fellow shorting target Ocado in June 2024.

SHORT SELLERS ON OCADO’S BACK

Despite some recent good news from the online

UK's most shorted stocks

Table: Shares magazine • Source: ShortTracker website, 28 August 2024

grocery retailer concerning delivery hub expansion in Australia and Japan, five institutions are short selling Ocado.

Once a stock market darling, it has had a dramatic fall from grace. In June the company crashed out of the FTSE 100 after its valuation fell from £22 billion (at the height of the pandemic) to £3.1 billion.

There have been rumblings about the company’s tie-up with Marks & Spencer (MKS) in the UK and about its ability to close new deals with global supermarkets –which was seen as the big growth engine for the group.

Now Pennon and other water utilities are locked in a battle with the regulator over the level of bill increases they will be able to levy on customers. Management instability hasn’t helped. In July Pennon’s CFO Steve Buck stood down with immediate effect (due to personal reasons) to be replaced by Laura Flowerdew – Pennon’s third CFO in a year.

COULD SHORT SELLERS BE GETTING IT WRONG?

Despite the criticism they attract, short sellers do play an important role. Because a short seller’s losses are potentially unlimited they tend to do their homework and therefore they can help shine a light on problems at a company which other market observers have missed.

That doesn’t mean they always get it right. In Shares view they are off base with Kingfisher (KGF) the home improvement giant behind B&Q and the Screwfix store chains.

In February we added Kingfisher to our Great Ideas portfolio against an improving backdrop.

The UK housing market is in recovery mode after the Bank of England cut interest rates on 1 August and consumer confidence has started to return.

There are five individual short positions in Pennon accounting for 4.4% of the company’s shares.

In 2023, Pennon along with other water firms were under investigation from Ofwat over the dumping of raw sewage.

Southwest Water – owned by Pennon – was fined £2.1 million by the UK Environment Agency for pollution offences across Devon and Cornwall spanning a period of four years.

In May, Kingfisher pleased investors by maintaining its full-year outlook even after seeing mixed sales in the three months to the end of April. Group first-quarter sales hit £3.3 billion, an increase of 0.3% on a constant-currency basis but a dip of 0.9% on a like-for-like basis.

UK sales were up 2.6% on a reported basis and 1.2% on a likefor-like basis at £1.63 billion, with a particularly strong showing from Screwfix which saw a 6.3% increase in reported revenue thanks to new store openings on top of underlying growth.

DISCLAIMER: The author of this article (Sabuhi Gard) owns shares in Ocado.

By Sabuhi Gard Investment Writer

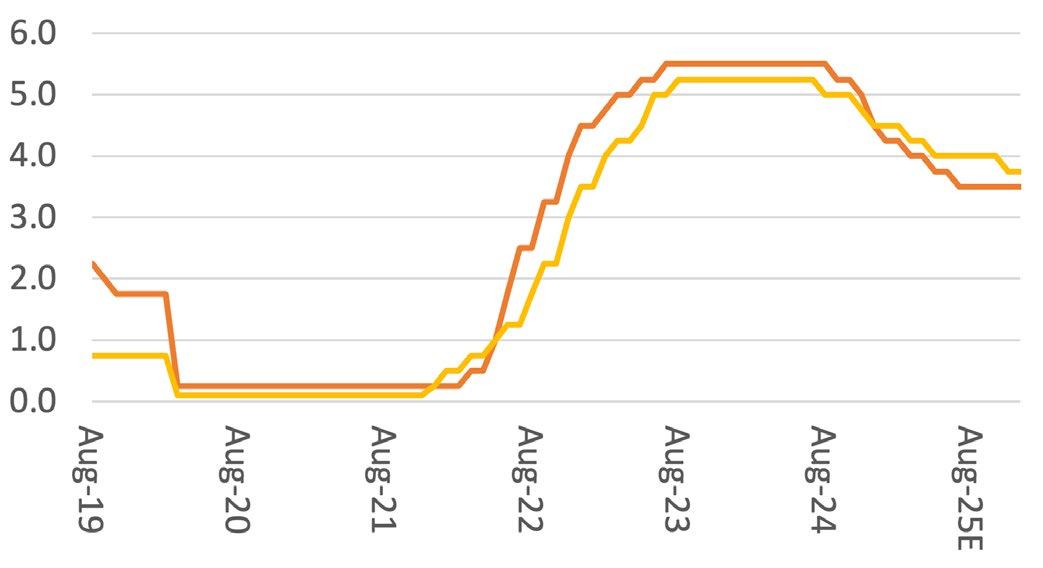

How to ride central bank rate cut cycles (without falling off)

Looking at how markets have reacted to previous moves by the Bank of England and Federal Reserve

Interest rate cuts in the month of August in the UK, Sweden and New Zealand, to name but three, take the global total to 108 this year, according to the website www.cbrates. com. That is more than 2022 and 2023 combined, and the US Federal Reserve is now dropping very unsubtle hints that it will be joining in at the next meeting of the Federal Open Markets Committee on 18 September.

This all seems to be in keeping with the core narrative that is doing so much to boost equity

Financial markets are pricing in a shallow rate cutting cycle, relative to historic averages

Source: Bank of England, US Federal Reserve, CME Fedwatch, LSEG Refinitiv data

The average rate cutting cycle is more than four percentage points

The average rate cutting cycle is more than four percentage points

Source: LSEG Refinitiv data, Bank of England, US Federal Reserve. Covers period since 1962 in UK and post 1971 in USA.

Source: LSEG Refinitiv data, Bank of England, US Federal Reserve. Covers period since 1962 in UK and post 1971 in USA.

and government bond markets alike, namely that inflation will cool, economies will enjoy a soft landing (if indeed there is any landing at all in the US) and that central banks will therefore be able to cut the headline cost of money.

Those rate cuts are in turn expected to stimulate demand for credit and thus economic activity, boost corporate earnings and cash flows thanks to higher demand (and lower interest bills) and persuade investors to take more risk, with asset classes such as equities, as the yield available from cash and fixed-income decline.

Such a scenario sounds very beguiling, but market history suggests equity investors might like to be a little careful about what they wish for, with regard to monetary policy for three reasons, even if the FTSE All-Share and S&P 500 have, on average, benefited from cheaper money on a two-year view, once the initial rate cut has been announced:

• First, equity markets do not always initially respond favourably to rate cuts, not least as they have had time to price in the first moves, and volatility often ensues, as markets assess the reasons for the reductions (victory against inflation, a recession or a financial crisis).

• Second, rate cuts did nothing to stave off

recessions (or equity bear markets) in 2001-03 and 2007-09 when corporate earnings estimates fell faster than borrowing costs and lofty valuations proved unsustainable.

• Finally, the Fed and the Bank of England cut by an average of four-and-a-half percentage points from peak to trough during a typical downcycle. That is more than markets are expecting this time around, to suggest that equity and bond markets may be underestimating how far central bankers may move – to the potential detriment of the former (if they have to go that far, then an unexpected economic downturn would presumably be the most likely cause) and benefit of the latter (at least unless stagflation takes hold).

CUT AND RUN

Faith in the US Federal Reserve’s ability (and willingness) to support stock markets dates back to when then-chair Alan Greenspan waded in with a pair of quick-fire interest rate cuts and a $3.6 billion bail-out plan in the wake of Russian debt default and the collapse Long-Term Capital Management hedge fund in 1998. That set the scene for another leg-up in the 1990s US equity bull run. Since then, central bankers have responded with interest rate cuts, quantitative easing and other unconventional tools and interventions to the Great Financial Crisis of 2007-09, the European debt crisis of the 2010s, dislocations in the American inter-bank lending markets in 2019, the pandemic in 2020 and a US

(and Swiss) banking wobble in 2023. All of these actions helped financial markets, ultimately, to come through relatively unscathed although sceptics may latch on to the words ‘ultimately’ and ‘relatively.’ Even former Reserve Bank of India governor Raghuram Rajan has opined recently in the Financial Times that central bankers should set a higher bar for interventions, so that their quest for financial and economic stability does not provide too big a safety net, encourage risk

Recessions now happen less frequently but come with greater severity when they do”

taking and promote the very instability they were seeking to avoid as a result.

The way in which the post-LTCM rate cuts helped to stoke the technology, media and telecom bubble

Bank of England rate cutting cycles: performance of FTSE All-Share

Bank of England rate cutting cycles: performance of FTSE All-Share

Before first rate cut

Before first rate cut

Before first rate cut

Table: Shares magazine • Source: Source: LSEG Refinitiv data, Bank of England

After first rate

After first rate cut

After first rate cut

US Federal Reserve rate-cutting cycles: performance of S&P 500

US Federal Reserve rate-cutting cycles: performance of S&P 500

Before first rate cut

Before first rate cut

Before first rate cut

Table: Shares magazine • Source: LSEG Refinitiv data, US Federal Reserve

Table: Shares magazine • Source: LSEG Refinitiv data, US Federal Reserve

of 1998-2000, and asset prices have soared across the board since 2009 support that view. Moreover, it does seem as if recessions now happen less frequently but come with greater severity when they do, while financial crises feel more common.

NIP AND TUCK

To start with the UK, the good news is that over the thirteen rate-cut cycles since the inception of the FTSE All-Share in the early 1960s, the index has made an average gain of 16% in the two years after after the first decrease in borrowing costs. Yet the hit rate over the first three to six months is patchy and the 2001-03 and 2007-09 rate-cutting cycles started disastrously for buyers, with losses over a two-year period as recessions bit hard, earnings disappointed and equity valuations faltered.

After first rate cut

After first rate cut

The two-year post-cut performance from the S&P 500 is similarly compelling, on average, but again the trick for investors is to safely navigate the volatility in between. The S&P 500 historically does not make much initial progress after the first cut, not least because it runs up strongly in anticipation. The scenario that markets are still discounting is lower inflation, a soft landing and a gentle reduction in rates. If anyone of those three trends diverges from current expectations, then equity markets may move, potentially with some violence, as we saw briefly back in August.

By Russ Mould AJ Bell Investment Director

WATCH RECENT PRESENTATIONS

Verici Dx (VRCI)

Sara

Barrington, CEO

Verici Dx is developing a complementary suite of proprietary, leading-edge tests forming a kidney transplant diagnostics platform for personalised patient and organ response risk to assist clinicians in medical management for improved patient outcomes.

abrdn Asian Income Fund (AAIF)

Yoojeong Oh, Investment Director

abrdn Asian Income Fund Limited (AAIF) targets the income and growth potential of Asia’s most compelling and sustainable companies. It does this by using a bottom-up, unconstrained strategy focused on delivering rising income and capital growth by investing in quality Asia-Pacific companies at sensible valuations.

Yellow Cake (YCA)

Andre Liebenberg, Executive Director & CEO

Yellow Cake (YCA) is a specialist company providing investors with direct exposure to the uranium market through the physical holding of uranium oxide concentrate (U3O8) and uranium-related commercial activities.

Five sneaky ways you could be hit with tax on your savings

How to avoid falling into these traps

Cash interest rates have risen, more people are being pushed into the next tax bracket and millions of people are expected to pay tax on their savings income this year. While lots of people are using ISAs to protect their money from tax or organising their savings to cut their tax bill, there are some sneaky tax traps that will catch some savers out without even realising it.

The personal savings allowance protects lots of people from paying tax on their savings. The taxfree allowance means that basic-rate taxpayers can earn £1,000 in savings income before they pay tax on it, while higher-rate taxpayers have a £500 allowance. Additional-rate taxpayers have no

allowance. But lots of people will breach this limit this year – maybe without knowing. Here are the five traps that might catch savers out.

TRAP 1: FIXED RATE ACCOUNTS

Lots of people are picking fixed-rate savings accounts now, locking their money up for one, two, three or even five years to get a guaranteed interest rate. However, many people won’t realise that this could leave them with a tax headache in the future. You are taxed on the interest on your savings when it is accessible by you. So, if you pick a fixed-rate savings account that pays out all the interest at maturity, for tax purposes all that interest will be counted in one tax year. This means that the interest from just one account could take you over your Personal savings allowance on its own.

It’s particularly a problem for longer-term fixed accounts, as you would have three or even five years of interest paid out in one go. For example, £7,500 in savings in the current top three-year fixed-rate account paying 4.51% would pay out £1,015 interest at maturity, taking a basic-rate taxpayer over their personal savings allowance for that year.

To get around this trap you could opt for an account where the interest is paid out monthly or annually, meaning it is spread across different tax years. Or you can opt for a fixed-term ISA savings account, where you won’t pay any tax on the interest.

TRAP 2: TAX ON YOUR CHILD’S SAVINGS

A little-known rule means that you might have to pay tax on interest that’s earned on your child’s savings. This sneaky tax rule means that once a child earns £100 or more in interest on their savings account on money that has been gifted by parents, it is taxed as though it is the parent’s money.

When interest rates were at historic lows, it was not much of a concern. But, as of late August 2024, the top children’s easy-access account paid 5.25% (according to Moneyfacts.co.uk), which means that once you have more than £1,900 saved, you will hit that £100 limit. If you reach £100 then all that interest (not just the interest over £100) is counted as though it’s the parents’ and will count towards their personal savings allowance.

This won’t be a problem if you haven’t earned much taxable interest yourself, but if you’re near (or already over) your Personal savings allowance you’ll be hit with unexpected tax. This rule only applies to money gifted by parents, not by money given by other family or friends. And the limit is also per parent.

One way around it is to use a Junior ISA account, where all interest will be protected from tax and won’t count towards the parents’ limit. Or you can carefully split the money you give between parents, to ensure that you are making equal payments to

their children, rather than one of you making all the transfers to the child’s savings account. If you have a joint account, the money will be assumed as coming 50:50 from each of you. Or if one of you has any personal savings allowance remaining, you could consider being the one to give your child/ children money, as any interest will be added to your own.

TRAP 3: TIPPED INTO THE NEXT TAX BRACKET

The personal savings allowance is cut in half or wiped out altogether if you move into the next income tax bracket. So, if you earn more than £50,270 (even by £1) you’ll become a higher-rate taxpayer and see your personal savings allowance cut from £1,000 to £500. And if you earn more than £125,140 you’ll become an additional-rate taxpayer and see your personal savings allowance drop to nothing – meaning that all your savings income will be taxed at 45%.

One thing lots of people aren’t aware of is that savings interest counts towards this limit. So, if you have a £50,000 annual salary you would be in the basic rate of income tax, pay tax at 20% and have a £1,000 Personal savings allowance. However, if you also had £1,000 in savings income you will tip into the higher-rate tax bracket and see your personal savings allowance cut to £500. This means £500 of your savings interest will be taxed and your highest tax rate will 40%.

One way around this is using an ISA for your savings, as then the interest won’t count for income tax purposes. Alternatively, you could pay some of your income into your pension, which could bring you back into a lower tax bracket.

Another option is moving cash savings into an account in your partner’s name, if they pay tax at a lower rate than you or haven’t used up their personal savings allowance yet.

TRAP 4: JOINT SAVINGS ACCOUNT

Lots of people might have savings accounts in joint names, but they may not realise that this means the interest is split 50:50 between the two account holders. It could mean you have taxable interest that you hadn’t

realised. For example, a joint savings account that generates £1,000 interest each year would be split so that each partner has £500 interest to count towards their personal savings allowance.

If one half of a couple is a lower earner, and so in a lower tax bracket, it could make sense to move the savings into an account in their name, as any interest that’s taxable will be paid at a lower rate. For example, a higher-rate taxpayer who had £1,000 of taxable interest would pay £400 in tax on the money, while a basic-rate taxpayer would only pay £200 in tax.

Even if both partners are in the same bracket, if one half hasn’t exhausted their personal savings allowance you could move savings into their name to maximise their tax-free amounts.

TRAP 5: NOT REALISING IT’S NOT JUST SAVINGS INTEREST THAT COUNTS

Lots of people are aware that their savings interest could be taxed, but many aren’t aware that interest and income from other products counts towards their personal savings allowance and could be taxed too. For example, the interest paid on peer-

Personal Finance: Tax traps

to-peer lending will count towards your savings limit and could be taxed.

Equally, the interest from some investments and funds could count as interest and count towards your personal savings allowance. With a fund, if the fund invests more than 60% in bonds and cash, then payments from the fund are classed as interest rather than as dividends. Your investment platform or provider will usually send you a tax statement each year to show you how much you’ve made in interest in that tax year, to help with your calculations.

The easiest way to avoid this is to use a stocks and shares ISA for your investments or an Innovative Finance ISA for any peer-to-peer investments you have, so no tax will be due. Another option is moving investments into a spouse’s name if they are in a lower tax bracket or haven’t used up their tax-free allowances yet.

By Laura Suter AJ Bell Head of Personal Finance

17 SEPTEMBER 2024

NOVOTEL TOWER BRIDGE

LONDON EC3N 2NR

Registration and coffee: 17.00

Presentations: 17.55

During the event and afterwards over drinks, investors will have the chance to:

• Discover new investment opportunities

• Get to know the companies better

• Talk with the company directors and other investors

Sponsored by

COMPANIES PRESENTING LIVE EVENT

ANEXO GROUP

Anexo Group (ANX) is a specialist integrated credit hire and legal services group focused on providing replacement vehicles and associated legal services to customers who have been involved in a non-fault accident. The company provides an integrated end to end service to the customer including the provision of a credit hire vehicle, upfront settlement of repair and recovery charges through to the management and recovery of costs and the processing of any associated personal injury claim.

ECORA RESOURCES

Ecora Resources (ECOR) strategy is to acquire royalties and streams over low-cost operations and projects with strong management teams, in well-established mining jurisdictions. Our portfolio has been reweighted to provide material exposure to this commodity basket and we have successfully transitioned from a coal orientated royalty business in 2014 to one that by 2026 will be materially coal free and comprised of over 90% exposure to commodities that support a sustainable future.

HARBOURVEST GLOBAL PRIVATE EQUITY (HVPE)

HarbourVest Global Private Equity (HVPE) is a listed investment company that provides investors with access to private company investments. We invest exclusively in funds managed by HarbourVest Partners, an independent and global private markets asset manager with over 40 years of experience. Launched in December 2007 on the Euronext Amsterdam, today.

SYSGROUP (SYS)

SysGroup (SYS) is a managed service provider of end-to-end data solutions enabling us to take our customers on their AI data journey. The Group offers an integrated set of modern technologies that collectively meets our customers end-to-end data needs including connectivity, cloud hosting, delivery, analytics and governance of customer data, as well as a security layer for users and applications. Reserve your place now!

A tricky transition for miners to manage

Why the sector is at an inflection point and why Rightmove should show resolve

The mining sector is at an inflection point. Historically associated with polluting materials like coal, the industry has a huge role to play if the world is to transition itself away from fossil fuels.

However, while long-term targets remain around net zero, there are hints of governments backsliding on these commitments and prioritising other things like energy security.

That makes it very difficult for the sector. Mining executives know that, very likely, significant demand is coming down the track but it’s harder to judge exactly when and how this demand will come through.

And miners can’t just start up operations at the drop of a hat. It takes years to bring a mine on stream and there is a danger of big constraints on supply in the future.