and, as such, are written by the companies in question and reproduced in good faith.

and, as such, are written by the companies in question and reproduced in good faith.

WWelcome to Spotlight, a bonus report which is distributed eight times a year alongside your digital copy of Shares.

It provides small caps with a platform to tell their stories in their own words.

The company profiles are written by the businesses themselves rather than by Shares journalists.

They pay a fee to get their message across to both existing shareholders and prospective investors.

These profiles are paidfor promotions and are not

independent comment. As such, they cannot be considered unbiased. Equally, you are getting the inside track from the people who should best know the company and its strategy.

Some of the firms profiled in Spotlight will appear at our webinars and in-person events where you get to hear from management first hand.

Click here for details of upcoming events and how to register for free tickets.

Previous issues of Spotlight are available on our website.

Members of staff may hold shares in some of the securities written about in this publication. This could create a conflict of interest. Where such a conflict exists, it will be disclosed. This publication contains information and ideas which are of interest to investors. It does not provide advice in relation to investments or any other financial matters. Comments in this publication must not be relied upon by readers when they make their investment decisions. Investors who require advice should consult a properly qualified independent adviser. This publication, its staff and AJ Bell Media do not, under any circumstances, accept liability for losses suffered by readers as a result of their investment decisions.

Despite an extended period of uncertainty, exacerbated by the COVID-19 pandemic, AIM continues to play an important role in supporting business growth and in doing so delivering notable economic value to the UK.

AIM is the LSE’s (London Stock Exchange) international market for smaller growing companies. It provides access to capital and ongoing finance to ambitious companies and in doing so plays an important role in supporting business growth, through enabling companies to access external finance so that they can make a step change in their development. In doing this, AIM provides a range of investor opportunities and continues to make an important contribution to the UK economy.

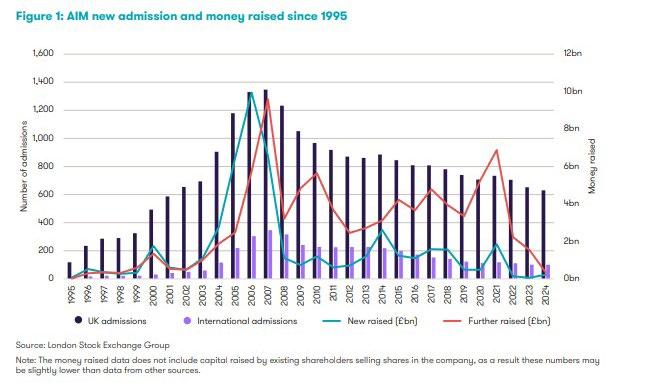

Since its inception in 1995, AIM has supported over 4,000 quoted companies.

AIM continues to welcome a broad range of companies incorporated overseas or with significant international operations, although the vast majority (83% of new admissions since 2015) of these companies have been UK incorporated.

Since its inception, AIM companies have raised £48 billion at admission and followed this with further

fundraising amounting to £87 billion. In the first 10 years of AIM, 54% of the money raised was through new admissions compared to an average of 19% in the last 10 years.

Since 2007, 75% of all funds have been raised through secondary issues (£72 billion of £95 billion), however, total money raised has fallen by 71% between 2020 and 2023.

The health of an economy is measured by its scale and its growth in terms of the goods and services it produces over a specific time period, at a national level this is measured in terms of GDP (Gross Domestic Product).

In 2023, AIM companies contributed £35.7 billion GVA (Gross Value Added) to UK GDP and directly supported more than 410,000 jobs. By comparison, the UK’s agriculture, forestry, and fishing sector contributed £19.2 billion; advertising and market research contributed £21.6 billion; the motion picture, video, TV programme

and broadcasting sector contributed £21.8 billion; and the arts entertainment and recreation sector contributed £31 billion.

In addition, AIM companies made a significant corporation tax contribution of £5.4 billion to the Exchequer.

Over the last four years (pre- and post-Covid) the direct economic contribution made by AIM companies has grown by 6.6% from £33.5 billion although employment has fallen by 4.7%.

By way of context the UK employment rate (the number of working age population in work) fell from 76.1% in 2019 to 74.8% and changes in employee numbers were not uniform across all sectors with AIM companies in consumer, industrial and technology sectors actually growing.

In addition to this direct contribution, AIM companies support further economic activity through both their supply chains and the expenditure of employees in their local economies.

Through their supply chain expenditure, AIM companies support a further 212,800 jobs and £18.6 billion of GVA. This indirect impact includes a broad range of suppliers to AIM companies such as financial services (nominated advisers and stockbrokers), business

services (registrars, financial public relations, legal, tax, accounting, and audit) as well as wider goods and services.

Both those employed directly by AIM companies as well as those employees supported through the supply chain will spend their wages on goods and services supplied by UK businesses. These so-called induced effects generate further employment and GVA. The induced impact is estimated to support a further 155,778 jobs and a £13.6 billion GVA contribution to GDP.

Taken together, the overall economic impact is equivalent to £68 billion in GVA and over 778,000 jobs.

AIM has an important role to play in the funding continuum, by enabling companies to raise external finance. This is coupled with a further requirement to go through a number of processes as part of the preparation for IPO that enhance and strengthen the business’s operations, this includes working through processes that optimise business performance, financial disciplines that underpin public company reporting and the adoption of a recognised corporate governance code. Together these help to create more resilient and sustainable businesses.

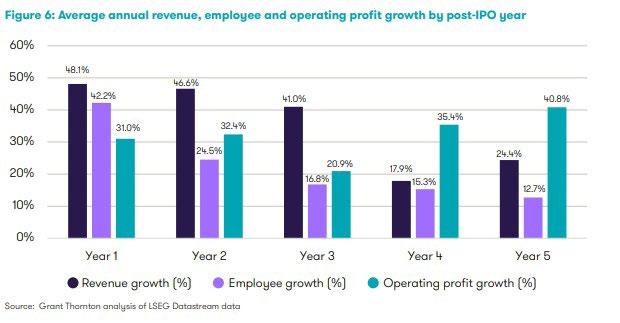

Continued growth remains a key feature of AIM companies who not only deliver impressive growth immediately following IPO but who continue to deliver this year on year, in terms of increases in both revenue and employees.

The chart shows both the scale of revenue and employment growth following IPO as well as how this growth persists, with revenue growth above 40% year on year for the first three years and 17% for the fourth- and fifth-years following IPO.

This suggests that an AIM IPO does not just deliver immediate growth but rather enables companies to scale and grow the business over the longer term.

Significantly these companies also become more profitable with operating profit increasing to 35% and 41% in years 4 and 5 respectively. Average annual revenue, employee and operating profit growth by post-IPO year

THIS IS AN EXTRACT FROM A REPORT ‘ECONOMIC IMPACT OF AIM’ PRODUCED BY GRANT THORNTON UK LLP IN 2024

MAGAZINE HELPS YOU TO:

• Learn how the markets work

• Discover new investment opportunities

• Monitor stocks with watchlists

• Explore sectors and themes

• Spot interesting funds and investment trusts

• Build and manage portfolios

EnSilica (ENSI:AIM), the aim quoted fabless ASIC supplier has been listed on AIM since May 2022. Listing on AIM was a natural next step in putting the foundations in place to fund its evolution from a design consultancy to a fabless chipmaker. The company operate a ‘Fabless’ model which means we design and sell semiconductors but do not own the fabrication facilities used to manufacture the silicon wafers – which would obviously require billions of capital investment. This is a proven business model used by many semiconductor companies such as Qualcomm (QCOM:NASDAQ), Nvidia (NVDA:NASDAQ) and AMD (AMD:NASDAQ)

Since listing, EnSilica has performed strongly, securing twelve high-value additional supply contracts, alongside the recent chip design and supply contract win for Oriole Networks. The company’s current pipeline of supply revenues continues to grow, underpinning EnSilica’s future revenue base as current customer chips start generating recurring supply revenues, alongside delivering their associated cash generation.

EnSilica is focused on four key growth markets: satellite communications,

automotive, industrial, and healthcare, owning valuable IP positions across all these sectors. The recent Oriole Networks contract win further demonstrates the company’s versatility and our IP platform, encompassing both digital processing and analogue interfacing, including high frequency radio wave (known as millimetre waves or mmWaves), used in the equipment each user has to enable a broadband internet connection to lower earth orbit satellites.

Our mixed signal design experience, IP, and a track record of bringing chips to volume production made us the ASIC partner of choice for Oriole Networks as they set out to make the fastest

and most energy-efficient networks.

In terms of growth opportunities, EnSilica is well placed to secure additional contract momentum within the growing satellite communications market. The cost of satellite launches have reduced dramatically and enabled the low earth orbit satellite constellation market to grow quickly, with examples including the recent successes of Starlink and SpaceX. The company holds relevant differentiated IP and expertise, to be a key player in this market. As an example, we have been working with Texas based mobile satellite telecoms business AST Space Mobile (ASTS:NASDAQ), EnSilica have been developing

the chip for their satellite to deliver 10 times improved performance over their existing solution, AST can provide satellite broadband connection directly to an unmodified mobile phone using very large high performance satellites.

EnSilica also has particular focus in high volume ground based user terminals which require hundreds of mmWave and digital beamforming chip at a low cost and low power that positions the

company to address the emerging resilient satellite connectivity for automotive, public safety and residential applications.

The chips designed by EnSilica are manufactured to customer specifications and utilise our extensive IP portfolio enabling our team to deliver innovative solutions and maintain our competitive edge.

The company’s ‘Fabless’ business model will provide a recurring revenue base in

the medium term, and the diverse markets addressed has the potential to insulate the business from the current uncertain political and economic macro climate. The push towards the localisation of semiconductor supply chains has benefitted EnSilica and we continue to leverage our expertise and strategic partnerships to ensure a resilient supply for both current and potential customers.

Our business model is also secured by the short to medium term sales projections of the chips that are already in supply or are being designed. As these and other chips reach the supply stage, the company hopes to continue its track record of growth in revenues and to improve our return on ROCE (return on capital employed).

Investment Evolution Credit (IEC) presents a potential opportunity for investors interested in the evolving consumer finance sector, particularly in online subprime lending.

Founded by Paul Mathieson, a successful Australian entrepreneur and former investment banker, IEC is headquartered in London and listed on the Aquis Stock Exchange.

It focuses on offering unsecured personal loans between £2,000 and £10,000.

Since establishing a foundation in six states of the US in 2010, IEC is now positioning itself to expand into the UK market, pending authorisation from the FCA (Financial Conduct Authority).

It is also seeking possible UK acquisitions and looking to expand its US state coverage.

In the UK, tighter regulation has closed over 250 lenders, forcing half a million people into the hands of unregulated lenders reducing their access to credit and in the worst cases leading to their exploitation.

IEC in the UK aims to support these underserved borrowers in the UK by utilising fintech-driven solutions that provide compliant, fair, accessible,

affordable, and consumerfriendly lending options.

The IEC leadership team brings extensive expertise in finance and consumer lending, making them well-prepared for industry changes driven by regulatory, economic, and technological factors.

The IEC product offering, and strategy aligns perfectly with these new market conditions.

CEO Marc Howells, with nearly four decades in financial services, has experience from senior roles at CitiFinancial and Barclaycard, focusing on risk management, cost control, and revenue growth.

His skills in strategic partnerships, mergers, and acquisitions add significant value as IEC scales its UK presence.

Neil Patrick, non-executive

chairman, brings a history of success in consumer credit, having co-founded Firstplus Financial and Picture Financial.

His background in business planning, investment, and operational scaling will help guide IEC in capitalizing on market opportunities.

Bob Mennie, the CFO, contributes strong financial oversight and has worked with both FCA-regulated and publicly traded companies.

His experience in scaling high-growth firms supports IEC’s ambitions to expand while adhering to regulatory frameworks.

Glendys Aguilera, executive director and lending manager, brings operational experience from Mr Amazing Loans, IEC’s US -based subsidiary, and her background in compliance from Wells Fargo (WFC:NYSE) is essential as IEC seeks UK market entry.

Dr Richard Leaver is advising the board on technology.

He’s a recognised expert in AI (artificial intelligence) and its applications across various industries.

Dr Leaver’s career combines technological innovation, investment management, and the commercialisation of innovative AI solutions.

Together, this team’s expertise spans consumer finance, regulatory compliance, technology, and strategic growth, establishing a solid foundation for IEC’s expansion.

The UK subprime consumer loans market is ready for change, driven by economic conditions, regulatory changes, and large pent-up demand for affordable lending options.

Rising living costs and economic pressures have left many consumers financially vulnerable, amplifying the need for accessible small loans.

Traditional banks often avoid lending to individuals with lower credit scores, leading many to turn to unregulated lenders that often come with inflated costs and create circles of debt.

These challenges highlight the demand for more transparent, fair, and innovative lending

solutions, particularly those that leverage technology to offer a smoother, customerfocused experience.

Consumer expectations are also shifting, with younger, tech-savvy borrowers demanding accessible, convenient, and fast loan services. Digital-first platforms that provide straightforward applications, fairer pricing, clearer terms, and faster loan processing times are essential.

IEC’s fintech-driven platform positions it well to meet these expectations and serve the subprime market effectively. Advances in AI and machine learning enable better credit risk assessments by analysing alternative data sources, such as utility payments and employment history. This approach can offer fairer rates by evaluating creditworthiness more accurately, helping IEC reach a broader market while reducing the cost of lending.

IEC’s transparent operational framework and adherence to rigorous accounting standards further strengthen its attractiveness as an investment.

The company’s policies for revenue recognition on loan interest and origination fees align with international accounting standards, demonstrating a commitment to sound financial management and solid regulatory compliance. Overall, IEC is well-positioned to capitalise on the rapidly evolving UK consumer finance market. The combination of a supply starved marketplace and IEC’s ability to deploy technology to deliver cheaper and fairer credit, make its UK market entry exceptionally well-timed.

The company’s scalable online lending model and experienced leadership team create a solid growth path, supported by a robust operational structure and a commitment to regulatory integrity. The UK also presents attractive acquisition opportunities.

As IEC continues to expand and enhance its digital capabilities, it represents a promising investment with substantial potential for returns in a high-demand market.

It is approaching three years since the oversubscribed initial public offering of the Pantheon Infrastructure investment trust (PINT) on the LSE (London Stock Exchange).

The offering raised £400 million from investors seeking exposure to growth-oriented infrastructure assets.

PINT has since deployed those proceeds, along with the £80 million raised through a subsequent subscription share conversion. PINT now has a portfolio of 13 infrastructure companies in Europe and North America across a variety of subsectors including digital, power and utilities, and renewables and energy efficiency.

The company targets underlying enterprises engaged in the development and operation of physical infrastructure assets with strong defensive characteristics and sustainability credentials, focusing on sectors benefitting from long-term growth drivers and downside protection. This is achieved through a coinvestment model where the company invests directly in the equity of these companies, alongside leading private infrastructure fund managers.

Careful asset selection has enabled PINT to deliver recent returns ahead of its net asset value total return target of 8–10% per annum. Looking

ahead, Pantheon, the company’s investment manager, is optimistic about the company’s continued trajectory.

Infrastructure has emerged as an alternative asset class that combines a range of attractive characteristics for long term investors. Infrastructure assets provide an income generating alternative to traditional fixed income, backed by tangible assets that provide downside protection across market cycles. Underlying cash flows are typically supported by longterm contracts with robust counterparties or established regulatory frameworks. Many of PINT’s underlying investments share these characteristics. Within infrastructure, PINT focuses on investing in sectors benefiting from long

term secular tailwinds with significant growth potential. These include: digitisation, which supports digital infrastructure assets such as mobile towers, fibre and data centres, all of which have become modern day utility assets as data and connectivity become essential services; decarbonisation, which favours investment in renewables and energy efficiency in pursuit of emissions reductions; and deglobalisation, which focuses on opportunities emerging from geopolitical trends such as ‘re-shoring’ and ‘friendshoring’, where supply chains are re-routed to countries deemed to carry lower levels of economic and political risk.

PINT invests through a co-investment approach, alongside leading

infrastructure fund managers in specific underlying companies. This form of direct investment enables the company to reduce costs by typically avoiding deal level management fees or carried interest. Investments are typically made in the form of a minority portion of the common equity of a company, with an expected ownership period of around 5–7 years before sale. Alignment is achieved through specific contractual provisions that enable PINT to exit investments alongside those fund managers that contribute the rest of the equity. Co-investments can be an attractive route to access private infrastructure for several reasons, including: access – there are fewer public market opportunities to directly access infrastructure companies; enhanced economics – the use of coinvestments can reduce the fee load of a portfolio; alignment – co-investments provide significant alignment with both the underlying company management and the fund managers

PINT invests alongside; portfolio construction and diversification – Pantheon can utilise co investments to tilt the portfolio composition towards specific sectors and to diversify

across sectors, geographies, stages, and fund managers; exposure to nascent sectors – co-investments can provide access to emerging sectors that may not be directly accessible through other investment products; and sponsor specialisation – co-investors have the ability to choose deals alongside specialised sponsors best placed to create value.

The company seeks to generate attractive risk adjusted total returns for shareholders over the longer term, through capital growth and a progressive dividend. The company targets a net asset value (NAV) total return per share of 8-10% per annum and currently a 4.2p per share dividend.

At 30 June 2024, PINT’s aggregate portfolio of 13 assets was valued at £516 million. Notable investments include stakes in: Calpine, an independent North American power producer benefitting from growing power demand; CyrusOne, a global owner and developer of data centres with hyperscale counterparties benefitting from the emergence of AI; National Broadband Ireland, a developer of rural fibre in Ireland through

a public-private-partnership; and Zenobē, a specialist international provider of EV bus fleets and grid scale battery storage.

PINT is managed by Pantheon, a leading global private markets specialist that provides a range of investment solutions spanning private equity, private credit, infrastructure, and real estate. Founded in 1982, the firm has discretionary assets under management of $67 billion and employs over 450 staff, including more than 125 investment professionals, across 12 global offices.

As demonstrated in PINT’s NAV performance since IPO, the company’s disciplined approach to asset selection has generated returns exceeding its targets. The company’s strong track record and the increased visibility of cash flows supported its decision to increase the target dividend for 2024 by 5%.

PINT expects infrastructure assets to provide muchneeded resilience in an ever-changing world, and Pantheon is well positioned to continue to execute on a highquality pipeline of potential investments. Along with recent legislative developments around cost disclosures for investment trusts, the company sees a positive outlook for investors.

Selkirk Group PLC is an AIMlisted (alternative investment market) acquisition company founded in 2024.

The company focuses on buying undervalued or overlooked divisions within larger UK companies in sectors such as consumer, technology, and digital media, where the team has strong expertise.

The company was cofounded by Kelso Group Holdings PLC (KLSO) and Belerion Capital.

Initially conceptualised by Kelso, the idea led to a joint venture with Belerion to leverage their combined expertise.

Selkirk aims to buy a single business from a larger parent company allowing parent companies to concentrate on core operations, monetise a portion of the division, and retain equity in the newly spun-off company.

Selkirk debuted on the AIM market on 7 November 2024, with an experienced leadership team, including Iain McDonald of Belerion Capital as executive chairman, Angus Monro (former M&S, Matalan, and THG executive) as senior non-executive director, and Alan Bannatyne, former CFO of Robert Walters, as NED (non-executive director).

High-profile investors such as Sir Terry Leahy, former Tesco CEO, Oliver Hemsley, founder of Numis; Martin Bolland, co-founder of Alchemy Partners; David Speakman, founder of Travel Counsellors, Edward Woodward, former CEO of Manchester United and Nick Robinson – former CEO of Phoenix IT Plc; hold significant stakes, and Selkirk‘s advisory board includes Kelso’s founders: John Goold, Jamie Brooke, and Mark Kirkland.

The company raised £7.5 million in its IPO, at 2.4 pence per share, valuing Selkirk at £10 million.

Led by Zeus Capital Limited, the IPO saw a strong market response with a 25% share price increase on the first day and this premium has been maintained.

Selkirk’s strategy centres on creating value through spin-

offs, acquiring divisions from UK companies where financial markets are undervaluing their potential.

By establishing independence for these divisions, Selkirk enables them to achieve growth that may otherwise be limited within a larger corporate structure and for the re-focussed investment proposition to produce a higher multiple on those earnings.

While spin-offs are common in the US, with numerous successful examples, they are less so in the UK despite proven value-creating potential.

High-profile US cases—such as PayPal (PYPL:NASDAQ) from eBay (EBAY:NASDAQ), and Dow (DOW:NYSE), DuPont (DD:NYSE), and Corteva (CTVA:NYSE)—show that spin-offs can deliver strong standalone value.

Studies indicate that spinoffs often outperform market indices, with spun-off units generating an average 15-20% return within the first year, and parent companies also benefiting as they focus on remaining core businesses.

US examples underscore how spin-offs can create

substantial returns. Studies from Investopedia show that both parent companies and spun-off entities tend to outperform market averages over two years, as these examples illustrate:

eBay/PayPal: PayPal’s separation enabled it to grow as a digital payment leader, with its valuation growing from $45 billion to over $300 billion by 2024.

McGraw Hill/S&P Global: The spin-off of S&P Global allowed it to focus on financial data and analytics, achieving strong growth in valuation. Dow, DuPont, and Corteva: DowDuPont’s three-way split resulted in focused companies, leading to a combined valuation that exceeded the pre-split value.

In the UK, spin-offs are rare despite the success seen in the US markets.

According to McKinsey and the Financial Times, UK conglomerates often have divisions that are undervalued

Spin-offs create value in several ways: management focus and accountability: spin-offs allow divested entities to set specific goals rather than align with broader corporate priorities, fostering agility and growth driven by focused management.

Strategic clarity and market positioning: both the parent company and the new entity benefit from clearer market positioning, enabling investors to better understand their value propositions.

Investor appeal and valuation upside: spin-offs reveal hidden value, giving investors greater insight into each entity’s growth potential and risk profile.

Access to capital: as independent companies, spun-off units can raise funds more effectively, focusing resources solely on their own growth initiatives without competing with other divisions for parent company capital.

within their group structure, being perceived by investors as complex and unfocused.

This frequently results in sales of UK subsidiaries to overseas buyers, leading to immediate returns but limiting long-term shareholder upside.

Selkirk’s experienced team is positioned to capitalise on undervalued UK divisions.

By buying and focusing on a single asset, Selkirk can apply tailored strategies to enhance operational performance and market positioning.

Importantly, Selkirk’s model allows sellers to retain equity, with the option to take part of the consideration in Selkirk shares rather than cash, preserving long-term upside potential.

Selkirk’s structure also incentivises operational management teams through a private equity-style MIP (management incentive plan), which can be deployed for existing or new management to drive performance. This will be based purely on share price accretion (above a minimum hurdle) so is well aligned with shareholders.

Funds raised from the IPO will support due diligence, working capital, and the initial investment for the targeted acquisition.

Selkirk aims to complete its first acquisition within 18 months funded by a larger equity placement with institutional or trade partners and potentially new debt facilities.

Shares Spotlight

Touchstone Exploration www.touchstoneexploration.com

Trinidad, with its rich geological history, is one of the largest oil and natural gas producers in the Caribbean.

Touchstone Exploration (TXP) is one company that has been reaping the benefits of the significant hydrocarbon reserves.

Established in 2010, Touchstone has over a decade long history of successfully operating in the onshore upstream oil and gas sector in Trinidad, establishing an unparalleled footprint on the island, as well as a unique knowledge of the geological composition and opportunities within the region.

Since then, the company has steadily grown its onshore presence, initially building a portfolio of low-risk legacy crude oil assets prior to successful exploration and development activities on the Ortoire field on the Eastern side of the island.

Whilst the prolific southern basin of Trinidad was instrumental in Touchstone’s early years, the focus for growth is now very much on that Ortoire block, where the company has multiple development and exploration targets across a land package totalling approximately 30,000 working interest acres.

It is the focus on this geological area of Trinidad

that has seen Touchstone transform over the last two years into the largest independent onshore oil and gas producer on the island, set to deliver further operational growth in years to come.

The initial discoveries on the Ortoire block, and the future development and exploration opportunities identified by the team, have completely reshaped Touchstone’s investment case and potential upside for investors.

Over the course of the past two years, the addition of the Coho-1 well and the discovery of the impressive Cascadura field have led to the

company’s production profile increasing materially.

Touchstone recently reported production of 6,223 BOE/D (barrels of oil equivalent per day) at its half year 2024 results, representing a 214% increase on the half year 2023 results.

The impact on the financial side of the business has also been material, with Touchstone reporting half year funds flow from operations of $10.1 million in 2024 compared to $800,000 in the prior year period.

The Cascadura field has been pivotal in this stepchange for Touchstone.

With a processing facility designed to accommodate for peak capacity of around 200

million cubic feet per day of natural gas, and 5,000 barrels of associated liquids per day, this world-class discovery is the largest onshore development in Trinidad in decades.

Since commencing production in 2023, Cascadura has reached several milestones that have had a significant impact on Touchstone’s production and finances.

In early November, the company announced initial production at the Cascadura C well pad on the eastern edge of the Ortoire block. By bringing two wells online, alongside the installation of a new natural gas separator, Touchstone is not only generating additional revenue, but it is also establishing a network of strategic infrastructure that is helping create efficiencies across operations.

A few days later, Touchstone announced positive test results at two wells, which further underscored the potential of the Cascadura field. The results not only provided a material increase in production, but also unlocked a new oil and natural gas play on the eastern side offering strong cash flow generating capabilities.

But the potential for Cascadura doesn’t stop there, and with most of the infrastructure now complete, Touchstone is well-positioned to execute its ‘drill to fill’ strategy to optimize and further enhance production, while benefitting from faster timelines between drilling to production.

From its current position, Touchstone has established a platform from which it can grow exponentially in the years ahead, with a clear fiveyear growth plan in place.

Given the recent success, this plan unsurprisingly starts on the Ortoire block, where the team has multiple development wells to drill at the Cascadura and Coho fields.

Multiple high- quality exploration targets have also been identified along the prolific Herrera fairway, with 21 key prospects providing the company with an exciting multi-year drilling programme to focus on.

At the same time, Touchstone continues to build up its land position for long term growth.

This year, the company successfully acquired the Cipero and Charuma blocks to the north of the Island,

following an onshore bid round conducted by the ministry of energy.

A new land package deal in Rio Claro followed, marking a vital extension of Touchstone’s exploration and development focus within the Herrera Formation fairway, and supporting long-term drilling and production, positioned adjacent to the Cascadura wells.

With an abundance of organic growth opportunities, management is now focused on efficiently drilling wells to fill the capacity available to them on the island.

With the demand there from the Trinidad market, and the infrastructure to support gross processing capacity more than 32,000 BOE/D, Touchstone is on track to further drive production growth, profitability, and responsibility in the Trinidad energy industry.

In a challenging economic environment, UK businesses face increasing difficulty accessing finance from traditional lenders, while contending with an inhibitive interest rate landscape, macroeconomic uncertainty, and poor domestic GDP growth. This is where Bath-based Time Finance (TIME) stands out.

For over twenty years it has lent UK-based SMEs (smallto-medium term enterprises) hundreds of millions of pounds, empowering tens of thousands of UK businesses. Specialising in flexible financing solutions for SMEs needing between £5,000 and £3.5 million, Time operates through two core lending divisions: asset finance, which funds essential equipment, and invoice finance, which supports cash flow management.

While very much focussed on being an own-book lender, Time can also broker deals when beneficial, ensuring adaptable support and optimised utilisation throughout economic cycles.

With a diverse network of supportive funders, including over £225 million in facilities, Time is well-equipped to continue its sustainable growth trajectory.

Time has established a sweet spot whereby its flexibility, speed of service, personal approach and range of products set it apart from other lenders such as traditional and challenger banks and alternative finance platforms. Importantly, it diversifies risk by providing funding for SMEs across a diverse range of sectors.

Time lends against soft and hard assets, through brokers, suppliers, and manufacturers. Typically, deals range in value from £5,000 to £1 million, with the sweet spots being £15,000 to £25,000 soft assets and £75,000 - £150,000 for hard assets. Yields range between 9% and 19% and funding comes primarily from wholesale block funders, such as challenger banks and the Government backed British Business Bank.

Disclosed and confidential invoice finance, via financial introducers and financial advisors.

Finance agreements can vary from £50,000 - £3.5 million, with the sweet spot being £250,000 - £1 million, yielding 10-20%.

Funding comes from a backto-back corporate banking facility. This is the fastest growing division with the highest margins.

Lending proposals originate through a variety of channels. These include finance brokers and other professional firms, equipment vendors, suppliers, and dealers, and direct from borrowers.

Recent trading at Time has been strong – with 13 consecutive quarters of sustained lending book growth underpinning three upgraded earnings announcements in less than a year.

Importantly, its trading model continues to provide increasing profit and revenue growth in addition to strong visibility of future earnings.

With an unbroken 10-year plus history of profitability the company is positioned to increase market share and provide larger lending.

Importantly, the quality of the lending book is evident with strong financial controls keeping arrears stable in the

Proven sustainable model: 13 consecutive quarters of consistent lending book growth highlights the resilience. Experienced leadership: over 150 years of senior management expertise in UK business lending.

Strong financial performance: excellent growth in pre-tax profit and earnings per share, supported by solid progress on its mediumterm strategy, focused on own-book growth and improved margins.

Diverse operations: by serving a wide range of sectors, Time diversifies its risk profile effectively.

Significant growth potential: With over £90 million in lending facility headroom, Time is wellpositioned for future expansion.

Robust financial controls: arrears continue to trend downward, demonstrating the strength and quality of the lending book.

Time recently packaged a £500,000 confidential invoice finance facility and a £130,000 asset finance facility to a fourth-generation family-owned bakery, known for their established local retail presence, who also run a growing wholesale division.

Its wholesale division, which provides the biggest opportunity for growth but also experienced cashflow issues.

They also needed to invest in new commercial equipment to maintain their expansion and fulfil order book demand.

The owners were already in talks with an alternative invoice finance provider, but Time’s ability to provide a multi-product solution, which solved both problems, meant that Time has able to secure the deal ahead of the competition. The facility has enabled the bakery to increase its output and expand its market footprint, demonstrating the transformative boost it can have for customers, and Time’s strength in the market.

broad 5% to 6% range, with net bad debt write offs at circa 1%, underpinning stability and mitigating downside.

Positive full year 2023/2024 annual results showed progress and growth as the gross book hit £200 million and pre-tax profit increased over 40% to £5.9 million.

Momentum continued into the first quarter of 2024/2025 with revenue increasing 20% year-on-year to £9.1 million (first quarter 2023/2024: £7.6 million).

Pre-tax profit rose 46% to £1.9 million (first quarter 2023/2024: £1.3 million) which represented a pre-tax profit margin improvement of 4 pence to 21%. Additionally, NTAV (net tangible asset value) surpassed £40 million at the end of August.

Importantly, the wider macro-economic environment suits Time.

For example, because it’s not a bank, and therefore does not have deposits, it is not impacted by the same net interest compression.

Instead, it benefits from lending being a more attractive

source of funding as interest rates fall.

Additionally, it still has over £90 million of headroom available from lenders which could comfortably support a 50% plus increase in book size to well over £300 million.

In 2021, Time laid out a fouryear growth plan to establish itself as a leading national SME funder. With goals to double its lending book, significantly increase profit levels, and to strengthen its balance sheet, Time has made considerable progress on all fronts. As it nears the conclusion of this strategy, Time plans to unveil its next growth phase, underpinned by strong fundamentals and market opportunities.