07 Chinese economic data piles pressure on leadership to take bold steps

08 Intel rolls the dice on foundry spin out, but will it be enough? 09 Shares in International Consolidated Airlines reach for the sky 09 Building materials group SIG hits rock-bottom on weak European sales

10 Can Raspberry Pi’s maiden results revive its stalling share price? 11 Can Costco continue to deliver the goods? 12 Week of rate cuts and central bank comments to dominate markets

14 Why the tide is about to turn for Diageo 16 HVIVO is in pole position to capitalise on increasing interest in human challenge trials

18 Trainline can regain momentum as it upgrades guidance 19 Why Trustpilot is a tricky call to make 20 MY PORTFOLIO

Why portfolio construction matters and how it can help you reach your investments goals

Three important things in this week’s magazine

1 2

25 years of bumper returns

As Shares marks its quarter of a century milestone, discover the best performing stocks, funds and trusts over that time.

Alphabet’s anti-trust challenge

The story behind the recent negative headlines for the Googleowner and how analysts see the situation.

3

Portfolio primer

In the first entry for a new section in the digital magazine, find out the basics of assembling an investment portfolio.

Visit our website for more articles

Did you know that we publish daily news stories on our website as bonus content? These articles do not appear in the magazine so make sure you keep abreast of market activities by visiting our website on a regular basis.

Over the past week we’ve written a variety of news stories online that do not appear in this magazine, including:

A quarter of a century of helping people with their investments

The focus over the last 25 years has been on you and that will continue to be the case

It’s time to break out the birthday candles as Shares marks 25 years since its first issue hit the newsstands in September 1999.

I’m just the latest custodian of this publication, having had the pleasure of editing Shares for a just under a year, and while there has been an enormous amount of change over the last quarter of a century both internally and in the broader financial markets, the one constant is you, the reader.

All our efforts, past, present and future, are about making investing easier for you. Whether by educating you on the principles behind investing, keeping you updated on the latest trends and themes or generating ideas to help you build your own portfolios.

In this anniversary edition we introduce a new section: My Portfolio. To kick things off, Martin Gamble will explain the basics of portfolio construction and management in a three-part series.

There’s no one-size-fits-all approach to investing, and after that it’s over to you to discuss how you manage your own investment portfolios. You can read more about how to get in touch in Martin’s article and the reward on offer for doing so.

You may also see some other small changes to this issue – very much evolution rather than revolution – including giving greater prominence to our Great Ideas section where we showcase our two best investment ideas of the week.

We are also planning some tweaks to our website to make it more useful and user-friendly and I’ll keep you posted on these developments in this column. We’re always keen to hear your feedback, positive and negative, and any suggestions you have

for potential article topics or areas we should cover. You can get in touch at shareseditorial@ajbell.co.uk.

One of the best calls we ever made in the magazine was on fast fashion business ASOS (ASC). It was flagged at just 4.5p in March 2003 when the idea of ordering clothes online was very much in its infancy.

At their all-time high in the late 2010s the shares had increased 1,679 times to more than £75, meaning a hypothetical £1,000 investment in 2003 would have been worth nearly £1.7 million.

However, you can never rest on your laurels in investing and ASOS is now worth just a fraction of its peak market value as industry trends, costs and the cost of borrowing have all moved against the company.

A lesson we can all take moving forward is to keep on top of our best ideas and when it might be time to change our mind.

Chart: Shares magazine•Source: LSEG

Chinese economic data piles pressure on leadership to take bold steps

Trillions of dollars wiped off the market since the peak three years ago

The mood music coming out of China hasn’t improved over the summer, with the latest figures showing factory output, consumption and investment all fell more than forecast in August.

At the same time, the decline in residential property prices seems to be accelerating with new-home prices in 70 cities dropping by 0.7% on a monthly basis in August after a 0.65% fall the month before and existing-home prices falling by 0.95% against 0.8% the previous month.

Although the Chinese market was closed on Monday due to holidays, the news added to the gloomy investor sentiment towards local stocks after a slump which has lasted since May and increases the pressure on the government to come up with some kind of stimulus package to rescue the economy.

‘The fear is the authorities are losing control of the economy and they won’t admit it,’ said Gary Dugan, chief executive officer of the Global CIO Office, in an interview with Bloomberg.

‘The market looks set to go to significantly lower levels in the absence of real, substantial new policies,’ added Dugan.

Chart: Shares magazine•Source: LSEG

‘The real problem is the entrepreneurial impetus is missing, with lots of businessmen unwilling to invest,’ he told Bloomberg.

‘It will be necessary for the government to loosen up on private enterprise restrictions and regulations so the private sector can be stimulated and help grow the economy.’

Meanwhile, measures to revive the property market such as a campaign to buy up unsold homes to ease the oversupply have had little effect as local authorities have dragged their feet over implementing them.

Current support measures such as interest-rate cuts and the buying of ETFs (exchangetraded funds) by state-owned funds have done little to change sentiment, with an estimated $6.8 trillion having been wiped off the value of Chinese and Hong Kong-listed stocks since the market peaked in 2021.

Renowned emerging-markets veteran Mark Mobius believes government stimulus can only do so much in the current business climate.

The fear is the authorities are losing control of the economy and they won’t admit it”

The government also rejected a call by the IMF (International Monetary Fund) to use public funds to complete and deliver unfinished properties, insisting it apply ‘market-base and rule-of-law principles’ instead.

In response, developers have cut the price of new homes, which in turn has sent shares in the Shanghai Property Index down roughly 25% since its peak in May, wiping out yet more investor wealth and compounding the problem. [IC]

Intel rolls the dice on foundry spin out, but will it be enough?

Chip maker Intel (INTC:NASDAQ) plans to split out its chip manufacturing operations from its design capabilities in a strategic move that it hopes will help reinvigorate growth and halt its dismal share price performance.

The Santa Clara-based business hopes that spinning out its Intel Foundry Services arm will provide external foundry customers and suppliers with greater separation from Intel’s core operations, while also allowing the unit to tap independent funding, spurring growth and shareholder value.

Pat Gelsinger, Intel’s chief executive officer, assured employees that the leadership team of Intel Foundry Services would remain unchanged and continue to report directly to him. An operating board, including independent directors, will be established to govern the subsidiary.

were ‘very encouraged’, by the move, praising Intel’s management for being proactive regarding the initiatives that it controls, or in other words, costs. ‘We’re encouraged by the decision to make Intel Foundry Services a separate independent subsidiary, which should reduce conflicts of interest between IFS and IDM (Integrated Device Manufacturing),’ they wrote in a note to clients.

But the move stops well short of the complete shift out of manufacturing that some analysts and investors had hoped for. In a recent analysis of Intel’s business, Citi analysts stated their belief that the company could significantly improve its profitability by exiting the foundry business.

Intel shares rose more than 7% on the announcement to $22.50.

Analysts at KeyBanc Capital Markets said they

‘We continue to believe Intel would be better off exiting the foundry business in the best interest of shareholders,’ Citi analysts wrote, citing the division’s massive losses. The foundry business, which lost $2.8 billion last quarter, is projected to lose at least $8 billion annually.

If Intel were to exit the foundry business, Citi estimates the company could see a substantial boost in both earnings and margins. ‘We estimate if Intel exits the foundry business, the company could ultimately see EPS (earnings per share) in the $3 to $4 range and gross margins somewhere in the lowto-mid 50% range,’ Citi noted.

In 2023, Intel reported $1.05 of EPS and consensus forecast data from Koyfin has EPS falling sharply in 2024 to just $0.26.

While one of the most familiar chip names to retail investors, Intel has struggled to adapt beyond its core PC and servers markets, crucially failing to capture meaningful share in the AI space. Intel shares have more than halved this year and Morningstar data shows the stock delivering negative total returns for investors over the past three, five and 10 years. [SF]

Shares in International Consolidated Airlines reach for the sky

Investors applaud the flag-carrier’s new-found financial discipline

With little fanfare, shares in British Airways and Iberia owner International Consolidated Airlines Group (IAG) have climbed 25% over the last two months to hit a new 12-month high of 200p.

In a surprise turn of events, the firm announced at the beginning of August it had terminated its agreement to buy the remaining 80% of Air Europa on the basis ‘it

would not be in the best interests of shareholders to continue in the current regulatory environment’.

The group returned to the dividend list last month with a small interim payout after first-half revenue rose 8.4% to €14.7 billion and pre-tax profit edged up to €1.05 billion.

A week later, IAG announced it would stop flying to Beijing, previously one of its most important routes, due to the cost, complexity and inconvenience to having to avoid Russian airspace.

Building materials group SIG hits rock-bottom on weak European sales

The insulation and roofing supplier cut full-year guidance at its interim update

Shares in Sheffield-based FTSE 250 building products firm SIG (SHI) hit their lowest level since the pandemic this month, bringing year-to-date losses to almost 40%.

In its interim trading update the company revealed sales in May and June were below forecasts, having failed to recover from the downturn of the first

four months of the year, and said it was ‘cautious’ in calling a second-half recovery.

As a result, it lowered its full-year operating profit forecast to between £20 million and £30 million against market expectations of £37 million to £43 million.

The firm blamed ‘prolonged’ weakness in the construction sector in the French and German markets for disappointing volume sales, as well as ‘softness’ in its UK interiors business.

Last month, SIG reiterated its lower full-

As one industry observer commented, ‘Why bother when you can send the same plane to the US instead where demand for premium cabins remains sky-high?’ Shares notes IAG is a recent addition to the JOHCM UK Equity Income Fund (B03KR50), with the managers flagging its low single-digit price to earnings ratio as one of the attractions. [IC]

year guidance but said hitting its targets would depend on a recovery in its European markets and its operational gearing – which means small changes in sales can translate into big moves in profits – while also noting prices had fallen partly as a consequence of lower inflation. [IC]

UK UPDATES

OVER T HE NEXT 7 DAYS

FULL-YEAR RESULTS

23 Sep: Transense Technologies

24 Sep: Close Brothers, Smiths

25 Sep: Time Finance

FIRST-HALF RESULTS

20 Sep: Biome Technologies

23 Sep: Real Estate Investors, Oxford Biomedica, Alphawave IP

Can Raspberry Pi’s maiden results revive its stalling share price?

UK tech play has lost momentum since blockbuster IPO

Affordable computer outfit Raspberry Pi (RPI) made an excellent debut on the UK stock market back in June but excitement around the stock has fizzled out.

While the shares are still up materially on their 280p issue price, they are some way below their 500p high. The company and its shareholders will hope it can revive enthusiasm for the story when it unveils its results for the six months to 30 June 2024 on 24 September.

Founded by chief executive Eben Upton in 2012 with the premise of ‘making computing more accessible to young people’, Raspberry Pi designs and develops low-cost SBCs (single board computers) and computer models for industrial customers, enthusiasts, and educators around

the world.

Since the company began trading in 2012, it has sold more than 60 million SBCs and computer modules, 7.4 million of which were sold in the year to December 2023, when revenues ripened up 41% to $265.8 million.

Pre-tax profit powered 90% higher to $38.2 million in 2023. However, the company has flagged volatility in customer demand in 2024-todate, which has led to ‘higher than usual levels of inventory’, although management expects this to normalise over the course of 2024 ‘resulting in stronger results in the second half of the year than in the first half’. Investors will be hoping for reassurance on this second-half improvement when the company reports. [TS]

Raspberry Pi (p)

Chart: Shares Magazine•Source: LSEG

Can Costco continue to deliver the goods?

Commentary around the US consumer and the reaction to a recent membership fee hike will be in focus when the warehouse membership retailer reports

Disappointing results from US discounters Dollar Tree (DLTR:NASDAQ) and Dollar General (DG:NYSE) have confirmed the US consumer is under pressure, but the quest for value is playing to the strengths of retail goliaths such as Walmart (WMT:NYSE) and high-flying Costco Wholesale (COST:NASDAQ), whose compelling value propositions are enabling them to gain market share.

Shares in the latter, which posts fourth-quarter earnings on 26 September, are testing fresh all-time highs north of $900 and trade on a forward PE (price to earnings) multiple approaching 60 times, which reflects the warehouse membership retailer’s winning proposition for cash-strapped consumers and the earnings visibility arising from its membership model.

Costco offers low prices to members, including individuals and cash-strapped small- and mediumsized businesses, by focusing on a small number of items and eliminating all the frills

and costs historically associated with conventional wholesalers and retailers. By selling a limited range of cheap items, Costco can pass through any price increases to the customer and makes additional money via the annual membership fee, which it recently hiked for the first time in seven years.

On 5 September, Costco reported a 7.1% rise in net sales to $19.83 billion for the month of August, and said sales edged up 1% to $78.2 billion for the fourth quarter ended 1 September 2024, which included 5.3% US comparable sales growth as well as an 18.9% surge in e-commerce revenues.

Having already announced Q4 sales, investors’ attention will be focused on management’s utterances around the consumer outlook and any resistance to the membership fee increase. [JC]

UPDATES OVER THE NEXT 7 DAYS

QUARTERLY RESULTS

24 Sep: Cintas, AutoZone

25 Sep: Micron, Paychex

26 Sep: Costco, Accenture, Carnival Corp, CarMax

Week of rate cuts and central bank comments to dominate markets

We expect the Fed to take a softly-softly approach to lowering rates

We aren’t in the habit of betting on central bank decisions but it seems a racing certainty the Federal Reserve will cut interest rates this week as more evidence emerges that the US economy and inflation rate are slowing.

The only question in investors’ and economists’ minds was by how much the Fed is likely to cut, with the odds favouring a 0.25% reduction in the Fed Funds rate rather than 0.5% which

might be seen as a panic response. There will have been particularly close attention paid to central bankers’ comments for clues as to how far and how fast (or more likely how slowly) rates might come down.

Some commentators have called for a 100 basis point or 1% cut by the end of this year followed by a further 100 basis points next year, but we can’t see the Fed, which has trodden cautiously every step of the way, lowering the cost of borrowing so far in such a short space of time.

In fact, the opposite is true – what the Fed really doesn’t want to see is inflation heading back up again in a year’s time because lower rates have encouraged people to spend with impunity.

Looking at the week ahead, most of the economic data is what we would call ‘soft’ as in it consists of surveys like consumer confidence and PMI (purchasing managers’ index) surveys.

The US and the Eurozone both show a clear divergence between confidence in the services sector and that in the manufacturing sector, with 50 being the dividing line between expansion and contraction.

The one piece of ‘hard’ data which will be of interest is the revision to US second-quarter GDP (gross domestic product) and the extent to which prices rose, which come out in a week’s time. [IC]

Temple Bar Investment Trust is managed by Redwheel’s Ian Lance and Nick Purves, who have more than fifty years of investing experience between them.

Experts in the UK stock market, Ian and Nick are classic value investors, looking to build a diversified portfolio of the most compelling undervalued companies they can find.

With the UK stock market currently among the most attractively valued assets that investors can buy anywhere in the world, they are currently very excited about the potential opportunity that lies ahead for the Trust.

Think value investing Think Temple Bar

“UK stocks look very attractively valued in a global context and when compared to history. Overseas businesses are already recognising this potential through acquisitions, and management teams are buying back shares at a record pace. These could represent meaningful catalysts for unlocking the inherent value in UK stocks. The long-term opportunity for UK value investors is significant.”

Ian

Lance,

Portfolio Manager

Temple Bar Investment Trust

For further information, please visit templebarinvestments.co.uk

Why the tide is about to turn for Diageo

The Johnnie Walker-to-Don Julio produceris a quality pick to quench investors’ growth and income thirsts

Diageo (DGE) £25.12

Market cap: £55.9 billion

Investors seeking a high-quality consumer staple that is currently on sale should consider buying Diageo (DGE), the world’s largest premium spirits company which is growing its market share around the globe. Shares in the premium drinks maker behind iconic brands Johnnie Walker whisky, Smirnoff vodka and Guinness stout are down 20% over one year. This reflects disappointment around its performance in the Latin America and Caribbean (LAC) region, and concerns over China’s slower than anticipated post-Covid recovery and a cautious consumer environment in North America.

The sell-off has left the shares looking cheap relative to their historical average and it feels as though the point of maximum pessimism has now passed with a margin of safety built into the stock. Admittedly, recent news flow from Diageo has been downbeat, but the company is delivering productivity savings and CEO Debra Crew is confident that ‘when the consumer environment

improves, organic net sales growth will return’. Diageo could even be a takeover candidate for a bidder looking to snap up an industry giant at a big discount.

DISTILLING DIAGEO’S STRENGTHS

Guided by Crew, successor to the late Ivan Menezes, Diageo is a veritable beverages behemoth whose unrivalled portfolio of brands span the likes of Captain Morgan rum, Tanqueray premium gin, Baileys cream liqueur, the Don Julio and Casamigos tequila labels and Chinese white spirit Shui Jing Fang.

This formidable strong portfolio confers pricing power on the business, which is key during inflationary periods, while the drinks giant’s myriad strengths also include its worldwide distribution footprint, massive marketing clout and a cash generative business model that has enabled the FTSE 100 group to establish

Chart: Shares magazine • Source: LSEG

Diageo key metrics

an enviable dividend growth record, while investing in the organic growth opportunities and acquisitions and returning additional capital to shareholders through earnings-enhancing share buybacks. Diageo also has scope to expand its operating margin thanks to ‘premiumisation’, the consumer trend towards quality over quantity and drinking better, not more.

DOWNGRADES HAVE LEAVE SOUR TASTE

Diageo’s shares are still nursing a hangover from a surprise November 2023 profit warning followed by downbeat results for the year ended 30 June 2024, which undershot consensus expectations with group sales declining for the first time since the pandemic.

who aren’t traditionally Guinness drinkers. Despite facing numerous challenges, Diageo’s free cash flow jumped 18% to $2.6 billion last year, which allowed the company to increase the annual dividend by 5% to $1.0348 per share and complete a $1 billion share buyback programme. Having always traded on a price to earnings comfortably above 20 times, Stockopedia data shows Diageo’s shares currently swapping hands for 18.7 times forecast 2025 EPS (earnings per share), falling to below 18 times for fiscal 2026.

One fund manager convinced the shares are undervalued is Nick Train, who holds Diageo in the Finsbury Growth & Income Trust (FGT). Train has long held the view that ‘a company with brands of Diageo’s calibre and, crucially, half of its earnings generated in the world’s biggest, and most dynamic economy, the United States, could be valued on up to 33 times EPS, for an earnings yield of 3%.

The company was unable to give an indication when its current period of poor trading will end, again given the difficult outlook for consumer spending, and reported an operating profit decline in four out of its five operating regions, while organic net sales were down 3% in North America, which accounts for 40% of the group’s global sales. Nevertheless, Crew noted that excluding LAC, organic net sales grew by 1.8%, driven by ‘resilient growth’ in the Africa, Asia Pacific and Europe regions, and the company ended the year with 75% of its brands gaining or holding market share.

Encouragingly, two of Diageo’s big long-term growth drivers, Guinness and Tequila outside the United States, grew their revenues at a double-digit clip. Bears will flag that spirits consumption is down among younger, more health-conscious drinkers, but Diageo has a secret weapon in Guinness Zero, which is selling hand over fist including to those

‘Or put differently, we would not even consider selling out of an asset as advantaged as Diageo at anything less than a 30 times or more multiple.’

One sticking point to a bid is the fact such a takeover deal would require a significant cash outlay, even if the bidder got a bargain price, since Diageo is currently worth the best part of £56 billion. One route might involve breaking up Diageo, with a beer company taking on Guinness and another company taking on the spirits brands. [JC]

Delivering productivity gains

H VIVO is in pole position to capitalise on increasing interest in human challenge trials

The contract research organisation sector has seen increasing M&A activity in recent years with average takeover premiums of around 30%

H VIVO (HVO:AIM) 28.2p

Market cap: £191.9 million

FluCamp does not sound like much fun for volunteers, but for leading CRO (contract research organisation) HVIVO (HVO:AIM) it represents a flagship service which is attracting growing interest from big pharma and biotechnology companies.

The company is at the forefront of HCTs (human challenge trials), a fast-growing niche within the large CRO industry which experts predict will grow from its current size of between $100 million and $150 million to between $700 million and $1 billion.

Having reached breakeven, HVIVO has ambitious plans to grow revenue to £100 million by 2028 from £62 million expected in 2024.

Increasing efficiencies and greater utilisation of new facilities is expected to lead to profitable growth. In the first half of 2024 generated £37.1 million of cash, up from £31.3 million in 2023, and the business is debt free.

The shares trade on a 2026 EV (enterprise

Chart: Shares magazine•Source: LSEG

value) to EBITDA (earnings before interest, tax, depreciation and amortisation) of eight times according to Panmure Liberum’s estimates, an unjustified discount to CRO peers and not reflecting growth prospects and high barriers to entry.

WHAT IS A HUMAN CHALLENGE TRIAL?

HVIVO specialises in conducting HCTs and has deep experience in testing infectious and respiratory disease with a heritage dating to the 1940s

Common Cold Unit.

HCTs differ from traditional clinical trials in that they involve infecting a healthy group of carefully selected volunteers with a specific virus in a controlled environment rather than testing safety and efficacy on participants who are sick.

HCTs have been around a long time, but it was only after the company led the first successful Covid HCT, funded by the UK government, that interest from regulators and drug manufacturers began to stir.

There are several factors driving demand. The US FDA (Food and Drug Administration) recently increased the rate at which it grants Breakthrough and Fast Track designations, to drugs supported by HCTs.

This has resulted in more drug developers adopting HCTs to speed up routes to regulatory approval, creating a surge in demand. Demonstrating the traction being achieved, HVIVO has expanded its order book six-fold over the last three years.

In drug discovery, identifying failure early can sometimes be as important as drug discovery itself.

WHAT IS THE GROWTH STRATEGY?

Yamin Mo Khan became chief executive in February 2022 and is the architect of the company’s growth strategy. Mo has 25 years’ industry experience, during which he transformed Pharm-Olam from a specialist clinical monitoring firm to a global full-service CRO.

His priority is to expand the order book, increase revenue visibility and promote cross-selling into broader capabilities while increasing utilisation of resources.

A high proportion (around 70%) of fixed costs in the business means increasing scale can drive profitable growth and margin expansion.

Signs are already visible with the firsthalf EBITDA margin expanding to 24.5% from 19.1% in 2023.

HVIVO is the world’s only specialised HCT CRO and is uniquely positioned to capitalise on the expected growth. The company has conducted around 70 trials and performed more than 4,000 volunteer inoculations, and claims to have more than 90% market share in the commercial HCT market.

Effectively HCTs derisk the route to market for new drugs and help refine optimal dosing levels.

Management has stated that HCTs can cost around 20% of conventional phase two trials. They require fewer volunteers (10s) compared with the thousands enrolled in conventional trials and can be completed in a shorter timeframe.

This is crucial because drug development costs tend to escalate, with phase two trials accounting for between a third to a half of total trial costs.

The company opened the world’s largest purpose-built challenge trial facility this year in Canary Wharf with 90% of the build costs funded by its clients to accelerate their studies.

The high-level three biosafety containment facility will unlock new revenue streams and increase the breadth of challenger models, increasing potential revenue by 50% to £90 million.

The flexible space will allow transmission studies designed to test whether a vaccine or drug can prevent transmission to a recipient volunteer.

The company is increasingly looking to leverage its world-class database of 300,000 volunteers, which can screen an additional 1,000 per week.

In summary, HVIVO is well-positioned to capitalise on the growth stemming from higher demand for HCTs and use its unique assets to broaden its revenue stream and diversify risk. [MG]

Trainline can regain momentum as it upgrades guidance

Shares rise as the rail app confirms it is now the most downloaded in Europe

Trainline (TRN) 333p

Gain to date: 2.1% Market cap:

£1.5 billion Trainline

We first flagged rail and booking site and app Trainline (TRN) in February, excited by the potential of a business which has already acquired a 60% share of the UK online market and has tapped into the growing European market.

It is now the most downloaded rail app in Europe with international consumer net ticket sales recently surpassing £1 billion.

WHAT HAPPENED SINCE WE LAST SAID BUY?

Trainline shares have endured a mixed showing. On 3 May the company reported a positive set of results for the year ending 29 February – revenue was up 21% to £397 million and net ticket sales were up 22% year-on-year to £5.3 billion, at the top end of guidance.

Despite ongoing rail strikes in the UK, Trainline unveiled a strong outturn in the six months to 31 August (12 September) with performance tracking ahead of expectations, helping to give the stock a meaningful lift.

Trainline raised its full year 2025 guidance – which translated into a rough 5% upgrade to Shore Capital’s adjusted EBITDA (earnings before interest taxation, depreciation, and amortisation) forecast for the 12-month period.

Shares magazine•Source: LSEG

WHAT SHOULD INVESTORS DO NOW?

We remain upbeat about Trainline due to the rapid progress it is making into Europe, particularly in Spain and Italy, and would back it to regain some of the momentum it lost earlier in the year.

Group revenue increased by 16% to £229 million for the six months ending 31 August and net ticket sales increased year-on-year by 13% to £3 billion.

France and Germany are in decline, with net ticket sales falling by 3% year-on-year in the first half of its financial year, but that’s due to a previously flagged pause in marketing and deprioritisation of the countries by the group.

Trainline has been able to position itself as a straightforward way to navigate the complex travel system and get good deals. Shore Capital analysts said that Trainline has an unmatched presence in the UK which will grow further due to the digitalisation of the industry. There are also opportunities for the company to increase its market share in Europe and tap into inbound foreign travel. [SG]

Chart:

Why Trustpilot is a tricky call to make

Still an attractive long-term play, but taking profit seems like a reasonable decision right now

Trustpilot (TRST) 222p

With more and more of us buying stuff online, is it any wonder that we are increasingly reaching out to fellow consumers for their seal of approval (or gripes) about products and services, and that’s great news for reviews business Trustpilot (TRST).

The platform now hosts more than 300 million consumer reviews of products and services across hundreds of thousands of websites, according to half year results. Thousands of businesses now turn to Trustpilot for customer transparency and the underlying consumer data analytics it provides to clients, and its value to them is being proved by client retention rates of 101%.

WHAT HAS HAPPENED SINCE WE SAID TO BUY?

Plenty of growth, and happily, that’s being reflected in the share price, which continues to rally. The latest sharp jump followed management’s upping of guidance (11 September).

‘Management now expects adjusted EBITDA (earnings before interest, tax, depreciation and amortisation) to be at the top end of market expectations ($18 million to $22 million)’, noted Berenberg in a note to clients. ‘Current full year 2024 (to Dec) adjusted EBITDA consensus is at $20 million, so we would expect a circa 6% to 10% upgrade.’

That revenue, bookings and ARR (annual recurring revenue) increased 18%, 16% and 16% respectively is great news for investors, as are plans for a £20 million share buyback, around 3% of the shares in the market.

WHAT SHOULD INVESTORS DO NOW?

Up nearly 40%, we must recognise the temptation to lock in gains, especially now that the 12-month rolling PE (price to earnings) multiple has shot beyond 80, according to Stockopedia data. If that suits your investment remit, you might consider selling a partial stake – a two-thirds sale should cover your outlay and leave you with a free ride on any further upside.

The consensus price target ahead of today’s results was 230p, according to Stockopedia data. Berenberg was already ahead of that at 260p, and has now lifted its projection to 270p, implying another 20%-odd upside from current levels.

We still like the long-term Trustpilot growth story, and if you agree, it’s probably best to let the investment run. But for our purposes here, taking a profit looks like a reasonable risk-adjusted decision.[SF]

Why portfolio construction matters and how it can help you reach your investments goals

Diversification smooths out investment returns and ensures you get the best bang for your buck

This feature marks two new beginnings.

The first is a three-part-series exploring portfolio construction, management and how to adapt for major life milestones.

It is also the start of a brand-new section in the magazine. We want to find out how readers approach their own investment portfolios and the methods they use to construct and manage them. You can read more about how to get involved at the end of this article.

To kick things off we explain why portfolio construction is important and will run through an example of how to construct a portfolio using passive ETFs (exchange traded funds).

Whether you are a complete beginner starting out on your investment journey or a more experienced investor, we hope the series will become a helpful resource.

At first glance portfolio construction can appear a bit dry, but its importance cannot be overstated. AJ Bell’s investments managing director Ryan Hughes puts it succinctly: ‘One of the mistakes that beginners make is that they act like a collector, buying investments without regard to the way that each fit into the portfolio.

‘Each investment should bring something different. The aim is to achieve the highest returns with the lowest risk.’

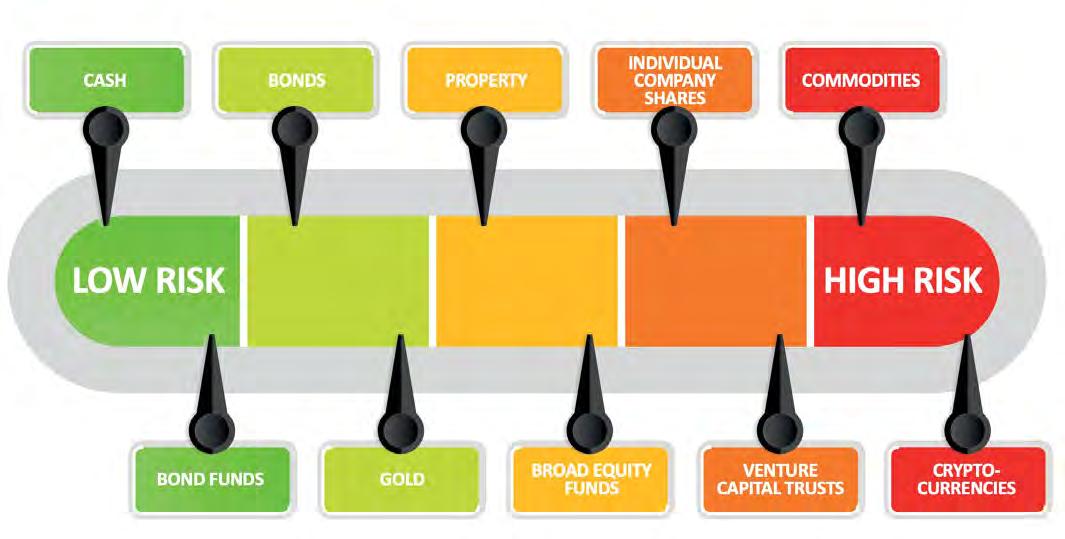

UNDERSTANDING THE RISK

In the context of investing, risk refers to the amount of uncertainty associated with an investment’s return.

Some asset returns are more uncertain than others, so it is best to think about uncertainty or risk, as a spectrum, from very certain to highly uncertain.

Risk and return are inextricably linked. Safer assets such as cash in the bank have historically

delivered the lowest returns. Riskier assets like stocks have historically produced the highest returns. The catch is that stock returns are far more variable and can inflict painful losses over shorter periods.

Many decades ago, some clever academics discovered an answer to this thorny issue. It turns out that combining assets with different risks and expected returns can reduce the overall variability of a portfolio’s return.

They invented a mathematical framework which, in theory, allows investors to maximise expected return for a given level of risk. Each investor should aim to define their own risk appetite which sits at the core of an investment plan.

For example, James may be comfortable seeing the value of his portfolio moving up and down by around 10% a year while Jane isn’t flustered if her portfolio value swings around by 15% to 20%. James would ideally own a bigger proportion of lower risk, lower return assets than Jane.

The idea of spreading risk is referred to as diversification. Nobel laureate Harry Markowitz described diversification as the only free lunch in investing. Diversification principles can also be

applied to the stock portion of a portfolio, which we discuss later in the article.

THE RISK SPECTRUM

Government bonds (a type of I.O.U issued by the state) are close to risk-free investments because the state can always raise taxes to service its debts. Bonds provide a relatively safe, fixed income.

Bonds have another feature which makes them potentially useful in portfolio construction. During periods of stock market volatility, when stocks are often falling, investors tend to flock to bonds for their relative safety and positive return.

Increased demand for bonds pushes up their prices which offsets some of the losses incurred by stocks. That is the theory.

In practice, this relationship does not always hold. It can flip around with bonds prices dropping at the same time as stock prices.

The steep rise in interest rates since the pandemic is a good example with government bonds inflicting bigger losses than stocks in 2023. It is worth bearing in mind that bonds are very sensitive to changes in inflation because the income they pay is fixed.

Stocks are towards the riskier end because most of their potential return comes from rising share prices. These in turn, are linked to unknowable factors like profit growth and dividend income.

Not only are stock prices unpredictable, but

there is no protection for shareholders if things go wrong. Another reason not to put all your eggs in one basket. By contrast bonds have legal protection for bond holders.

DIVERSIFICATION IN A STOCK PORTFOLIO

Not all stocks have the same risk and return characteristics, so investing in a variety of stocks can be beneficial. The most common way to achieve stock diversification is to spread investments across different industries, sectors and geographies.

On top of that, it is also worth considering key factors like size, cheapness and momentum which are known to drive stock returns over the long run. Studies have shown that small-cap value stocks tend to outperform.

Remember, investment styles come into and out of favour, so it might be better to have a mixture or

A RISK LADDER Source: Shares

be style agnostic.

How many stocks do you need to achieve most of the benefit of diversification? There is no precise answer, it depends on the portfolio. If you tend to invest in large cap stocks which pay dividends, as few as 15 names should be enough.

If you prefer small caps, then 25 names might be needed to account for the higher volatility of small cap shares.

Beyond a certain level of diversification, the costs start to outweigh the benefits. Summing up, we have discovered that spreading investments across many risk factors creates portfolio stability and helps to maximise return for a given level of risk.

bonds while adventurous types will want more equities exposure. Those in the middle will aim for a balance between the two.

Age is another important factor in defining risk appetite. Younger investors have a longer investment runway and therefore can take on more risk.

Finally, remember to define your investment goals and timeframe and never lose sight of the fact investing is a marathon and not a sprint.

DISCLAIMER: AJ Bell, referenced in this article, owns Shares magazine. The author (Martin Gamble) and editor (Tom Sieber) own shares in AJ Bell.

By Martin Gamble Education Editor

WE WANT TO HEAR FROM YOU

We are looking for individuals or couples to share their experiences of managing their own investment portfolios.

BUILDING A PORTFOLIO WITH ETFS

Next, we look at how to build a portfolio using passive funds. ETFs track major stock and bond indices and, increasingly, popular investing themes.

They are an effective way to achieve broad diversification at a competitive price. They enable an investor to get exposure to thousands of companies and bonds by buying just a few products.

This approach also means you do not need to take any risk backing an active fund manager or go through the stress of analysing and picking individual companies.

The first step is to figure out your own individual risk appetite. Are you the type to get nervous when markets take a fall amid scary headlines about recession, or the cool, calm and collected individual who takes it all in their stride?

Referring to the risk spectrum mentioned earlier, cautious types will probably feel more comfortable allocating a bigger proportion to safer assets like

If you would like to take part, we want to know why you chose certain stocks, funds or bonds, why you might have subsequently sold some of them, and what you hope to achieve from investing.

We will pay £50 in John Lewis vouchers as a thank you to anyone whose story is published in the digital magazine.

Drop us a line with your name and two lines describing your investment experience. For those picked to feature in the magazine, we’ll be in touch to get the full story.

CONTACT: shareseditorial@ajbell.co.uk with the words My Portfolio in the subject line.

DISCLAIMER: Shares/AJ Bell does not provide advice or personal recommendations. The My Portfolio articles are for information only. You must do own research and consider your own personal circumstances before making investment decisions.

PORTFOLIO CONSTRUCTION IN PRACTICE

Karen's asset allocation profile

Karen is 36 years of age, married with two children and works as a dental hygienist. She has a happy-go-lucky approach to life and feels comfortable taking a little more risk to bag a potentially better long-term return.

STOCKS

Karen is pursuing a global approach to investing in stocks and researched some popular ETFs which track the MSCI World index. Karen applied the same thinking to other assets which comprise her total portfolio.

The stock product she landed on is the iShares Core MSCI World ETF (SWDA) which is the largest ETF tracking the index with assets of £61 billion. It gives exposure to more than 1,400 stocks across 23 developed stock markets for a cost of 0.2% a year.

The manager tracks the MSCI World index by buying a selection of the most relevant constituents.

BONDS

The broadest index which tracks global bond markets and is used by fund managers as a global benchmark is the Bloomberg Global Aggregate Bond index.

It is comprised of more than 15,000 investment grade (higher quality) bonds issued in developed and emerging markets across the globe. An

efficient way to track the index is via the Vanguard Global Aggregate Bond ETF (VAGS) which is the largest tracker with assets of £1.6 billion.

The ETF gives exposure to around 9,000 bonds by selecting the most relevant constituents and has a total expense ratio of 0.1% a year.

PROPERTY / INFRASTRUCTURE

Property and infrastructure funds aim to provide some inflation protection and a stable, reliable income. Karen believes they are a good diversifier for her portfolio.

A relevant property benchmark for UK investors is the FTSE EPRA/NAREIT index which tracks UK listed real estate companies and trusts. The £627 million iShares UK Property ETF (IUKP) tracks the index by using the full replication method.

This means it invests in all 40 constituent stocks of the index it tracks and has a total expense ratio of 0.4% a year. The fund has a yield of 3.8% and dividends are paid quarterly.

The iShares Global Infrastructure ETF (INFR) tracks the FTSE Global Core Infrastructure index which invests in the largest global infrastructure stocks across the globe.

The £1.2 billion fund fully replicates the underlying index for a total expense ratio of 0.65% a year giving investors exposure to nearly 260 companies. Dividends are distributed quarterly, and the fund has a yield of 2.3%.

25 YEARS OF BUMPER RETURNS

Anniversaries are often an opportunity to take stock so the Shares team has had a look at the best performing shares, funds and investment trusts since the magazine’s first issue in September 1999.

Read on to discover the identity of the top performers and find out names we think will continue to impress in the years to come and those where we think the good times might be over. But first, Ian Conway provides a personal perspective on the last 25 years in financial markets.

TWENTY-FIVE YEARS OF CHANGE BUT MUCH REMAINS FAMILIAR

As the two Ronnies – in this case Lane and Wood –put it so succinctly, I wish that I knew what I know now, when I was younger.

Twenty-five years ago, we were in the midst of the tech bubble, when ‘clicks’ and ‘sticky eyeballs’ were enough to justify sky-high PE (price to earnings) multiple, although in honesty most of the companies coming to market back then had no earnings to speak of.

If memory serves, at one point National Grid (NG.) was co-opted into the tech rally on the basis it was going to send broadband ‘waves’ through its power lines. So much for that idea.

There was without question a colossal misallocation of capital and many of the firms which were purported to be the biggest beneficiaries of the internet ‘revolution’ ended up going bust, losing investors

Discover the superstar stocks and funds of the last quarter century

By Ian Conway Deputy Editor

25 years of ups and downs for UK stocks

FTSE All-Share

25 years of ups and downs for UK stocks

Chart: Shares magazine•Source: LSEG

billions of pounds.

Yet the over-investment in high-speed networks paid off, paving the way for much of what we take for granted today – low-cost 4G mobile, data centres, streaming services, even video conferencing and remote working.

In 1999, five years after it was founded, Amazon (AMZN:NASDAQ) was still a book seller in Seattle with its headquarters nestled between a needle exchange and a porn shop and Jeff Bezos was driving a Honda. Allowing for stock splits, if you had invested $1,000 in Amazon at its IPO (initial public offer) in 1997 your shares would be worth just shy of $2.5 million today.

Similarly, Google, launched in 1998 by Larry Page and Sergey Brin, was a pure search engine with ‘no weather, no news feed, no links to sponsors, no ads, no distractions, no portal litter’, according to the

trade press of the time.

An investment of $1,000 at Google’s IPO in 2004, again adjusting for stock splits and allowing for Alphabet (GOOG:NASDAQ) shares having fallen over 20% from their recent highs, would now be worth around $1.7 million. Ho hum.

FOREVER BLOWING BUBBLES

As the tech rally deflated through the mid-noughties, another bubble was forming in US real estate, helped partly by aggressive rate cuts from the Fed and by compliant banks, who were playing both sides by lending willy-nilly to buyers and securitising those loans to sell on to yield-hungry institutions.

Eventually the whole house of cards came tumbling down in 2007, as author Michael Lewis captured so well in The Big Short’, but not before hundreds of billions more dollars had been misallocated.

The fall-out from the housing crash led to the demise of several eminent Wall Street institutions and presaged another round of Fed rate cuts, but it would be a long time before the US economy found its feet again. Meanwhile, on the other side of the world, China had emerged as a new economic powerhouse.

Its insatiable appetite for raw materials, especially copper and other metals, led to a creeping bubble in commodity stocks which culminated in the mining sector becoming the largest component of the FTSE 100 index.

Miners reached their apotheosis in 2011 when South African-based producer and distributor Glencore (GLEN) came to market in the biggest UK IPO in history, generating a fortune for its founders and traders, many of whom made personal windfalls

Asset classes over 25 years

How major global indices have fared

How major global indices have fared

of more than $500 million, yet within five years its stock price had collapsed almost 90%.

In the last decade we have seen more minibubbles – in the shares of electric vehicle makers, in crypto-currencies, in government bonds (remember negative real yields?), in leverage itself and arguably in the valuation of AI (artificial intelligence) and obesity-related stocks.

SAME AS IT EVER WAS

So, 25 years after Shares first rolled off the press, what hasn’t changed? Human nature, for one – there will always be those who love to speculate, and no matter what ‘guard rails’ are put in place to try to stop the worst excesses of over-trading, we are still going to get booms and busts, of that much we are sure.

In terms of assets, shares have continued to outperform bonds on a total return basis over the last quarter-century and we can’t see that changing, but as ever price is what you pay, value is what you get, so if you overpay for a stock you still face the possibility of losing capital.

Despite regular claims that the era of fiat money is over, the dollar remains the world’s reserve currency and we don’t see that changing either. For the same reason, speculators are always going to look for a ‘carry’ trade, where they can borrow heavily in one currency and invest the proceeds in another, and as recent experience has shown, when these trades eventually unwind they can cause massive volatility.

Finally, markets today are just as inefficient as they were 25 years ago, which is good news for professional stock pickers and those with the skill and the knowledge to know where to look for bargains.

BEST PERFORMING UK STOCKS OF THE LAST 25 YEARS

Ashtead (AHT)

£52.30

When considering which of the winners of the past 25 years to back for the future we weighed up a variety of factors – not just the quality of the company in terms of its return on capital employed and how it allocates that capital but its ability to set prices, the markets in which it operates and the big drivers of its business.

For equipment hire firm Ashtead (AHT), that means the US and Canada where it does most of its business, and the infrastructure market which drives demand for its products and services.

In the US the firm operates close to 1,200 hire centres, while in Canada it has 135 outlets, and it grows that number each year by reinvesting its cash flows into opening more centres and buying small local rivals which it quickly absorbs.

On top of a multi-billion-dollar annual hire market which is continually growing, the firm is seeing an accelerating structural change from ownership to rental as well as increased demand from nonconstruction sectors and new markets.

The shares are priced at around 15 times forward earnings, which we believe it can continue to grow by around 15% per year, making the valuation appear reasonable.

JD Sports Fashion (JD.)

The self-styled ‘King of Trainers’ has been a stand-out performer over the last 25 years and has grown its earnings at a compound annual rate of around 18%, but we can’t see it maintaining a similar growth rate going forward.

144p

given it pricing power over retailers and wholesalers. In August, JD confirmed full-year earnings would be in the bottom half of the range of estimates, despite what should have been a strong 2024 due to the Euros and the Olympics, and while the rating isn’t overly demanding we think the risks are to the downside.

Top

performing UK stocks of the last 25 years

Retailing is a difficult market at the best of times given changing consumer tastes, and the athletic footwear market is incredibly competitive, especially in the US which is JD’s big bet following the acquisition of rival Hibbett.

Established brands like Adidas (ADS:ETR) and Nike (NKE:NYSE), which form the backbone of JD’s business, face growing competition from newcomers like ON Holdings (ONON:NYSE) and Hoka, owned by Deckers Outdoor (DECK:NYSE)

In particular, On’s strategic partnerships with high-profile figures like Zendaya and Roger Federer and its investment in innovation have boosted its visibility and credibility as a premium sportswear brand, while its multi-channel strategy has

BEST PERFORMING FUNDS OF THE LAST 25 YEARS

Janus Henderson Global Select Acc (B68SFJ1) 466.4p

In existence for more than 40 years, over the last quarter of a century Janus Henderson Global Select (B68SFJ1) –previously known as Janus Henderson Global Equity – has chalked up an impressive performance which compares favourably with more illustrious counterparts.

The name change followed the appointment of Julian McManus as lead portfolio manager in 2023 with the portfolio becoming less concentrated than it had been historically, although at between 40 and 65 names this remains a fairly focused fund.

It is also a fund which deviates significantly from its benchmark, and we think a balanced approach with a mix of stocks from sectors like energy, financials and defence alongside technology could be a successful one in the years and decades to come.

The likes of Microsoft (MSFT:NASDAQ), Amazon (AMZN:NASDAQ) and Taiwan Semiconductor Manufacturing (TSMC:NYSE) will be holdings in lots of global funds but others, like Japanese insurer Dai-ichi Life (8750:TYO) and US power generation company Vistra (VST:NYSE), not so much.

The aim is to beat the MSCI All-Countries World index by 2.5% per year over a five-year period. This is underpinned by investing in stocks where McManus and fellow manager Christopher O’Malley believe free cash flow growth potential is being underestimated by the market. Ongoing charges are reasonable at 0.86%. [TS]

INDIAN FUNDS

Several India-focused funds populate the list of best performers over the last quarter century, but there are reasons to think the path ahead may not be so smooth, not least high valuations. India’s equity market has been on a relentless bull run since the pandemic, but recent lacklustre earnings and slowing GDP growth may mean stocks take a pause, for a bit anyway.

Since the low of the Covid outbreak in March 2020, the blue-chip NSE Nifty 50 index (the equivalent of the FTSE 100) has soared nearly 200%, lifting the total market cap of Indian equities to more than $5 trillion. In February 2024, the UK market was worth about $3.1 trillion.

‘ The attractiveness of the Indian stock market depends largely on whether earnings growth remains strong,’ says Herald van der Linde, head of Asia Pacific stock strategy at HSBC. He called India’s earnings in the second quarter of 2024 ‘worrying’, with earnings growing at double-digits, but slower than in the past few years.

While experts almost uniformly see India as a long-run growth opportunity, recent data might suggest that Indian stocks are a bit too hot to handle right now and there is the potential for growing pains in the economy.

This can partly be blamed on seasonal factors (heatwaves, monsoon season) while an election that dragged on for months crimped consumption and investment. India’s GDP growth for the April to June quarter, which clocked 6.7% year-onyear, was also shy of Reserve Bank of India’s (7.1%) and market consensus (6.9%) projections.

Sandeep Bhatia, head of equity India Macquarie Capital, doesn’t expect major earnings surprises for the next 12 to 15 months. No one is suggesting widespread selling of Indian stocks or funds. But geopolitical uncertainties are likely to trouble sentiment in the short to medium term and inflation needs careful managing. [SF]

BEST PERFORMING TRUSTS OF THE LAST 25 YEARS

Worldwide Healthcare Trust (WWH)

It is no surprise that the Worldwide Healthcare Trust (WWH) has performed so well over the last quarter of a century.

There is likely more to come given the sector continues to benefit from the structural growth drivers of ageing global populations and accelerating innovation which is boosting drug discoveries.

The trust’s portfolio manager, OrbiMed Capital, is one of the largest dedicated healthcare investment firms in the world which has managed the portfolio since launch in 1995.

Since inception lead managers Trevor Polischuk and Sven Horho have delivered an annualised total return in net asset value of just over 14% a year, comfortably outperforming the MSCI World Healthcare index return of 10.5% a year.

The investment team have a global focus and attempt to identify sources of outperformance across the whole sector from the early-stage start-ups to large integrated biopharmaceutical companies.

The fundamental investment approach is designed to unearth opportunities in companies

AVOID

with

products, with high quality managements and solid financial resources.

The manager has assembled a basket of companies it believes are likely to benefit from increasing mergers and acquisitions activity which represents the portfolio’s largest holding, worth around 8% of assets.

Weight-loss market leaders Eli Lilly (LLY:NYSE) and Novo Nordisk (NOVO-B:CPH) feature in the top 10 holdings. The trust has an ongoing charge of 0.9% a year. [MG]

Pacific Horizon Investment Trust (PHI)

569.7p

This Asia-focused fund has an enviable track record but, as it stands today, its large weightings towards India and China, accounting for more than 40% of the portfolio, make us unsure on its prospects of continuing to outperform in the future.

On a really long-term view performance is undoubtedly impressive but, more recently, the trust has found things more difficult. It is down 34.6% in total return terms on a three-year view. While it dominates Asia in economic terms, China is something of an outlier in one important respect. Unlike many other developing economies in that part of the world, the country has a demographic profile more akin to the West. In other words, its population is getting older, its working age population is shrinking and this could act as an obstacle to growth. In part this is a legacy of China’s one-child policy which was in place from 1980 to 2016. China is also enduring a fairly painful transition from an exportdriven economy to one powered by domestic consumption. Indian stocks, meanwhile, trade on very lofty valuations which, as discussed earlier in this feature, make us pretty nervous. [TS]

Top

Top performing investment trusts of the last 25 years

AVOID

Schroder Oriental Income Fund Capturing the artificial intelligence opportunity in Asia

Artificial intelligence (AI) has become a major force in global stock markets, driving significant returns over the past couple of years.

Although much of the attention has focused on Nvidia, the US technology company that designs the advanced chips which are essential for AI processing, there is a robust ecosystem of other technology companies that contribute at various stages of the AI value chain. Asia has become a pivotal hub in this AI revolution and whilst the AI related revenues for many of these Asian companies are starting from a low base it is a fast-growing area often utilising leading-edge products and technologies thus enhancing returns for companies that can successfully supply into the space. These include companies that not only fabricate and package the chips but also those that can supply the high-end servers required or fabricate parts

and components to meet the demands of AI. These include items such as the power supply for servers which have to be able to cope with much higher loads than for ordinary applications. The Schroder Oriental Income Fund is strategically positioned to capitalise on this growing opportunity and is currently exposed to all of those areas.

It should be remembered that whilst AI should continue to be a positive driver for the IT sector it is not the only driver and the industry should continue to benefit longer term from positive trends around digitisation, cloud and 5G.

With more than 30% of its portfolio allocated to the Information Technology sector, the Schroder Oriental Income Fund is well ahead of its benchmark index (MSCI AC Pacific ex Japan Index, 26.3%). In recent years, this positioning has added value through outperformance and as a strong source of dividends and dividend growth.

means it has exposure to the mobile, display and foundry sectors.

Elsewhere amongst the portfolio holdings is Hon Hai, not only a manufacturer of smartphones and other high end consumer products but also a manufacturer of servers key to the growth of AI and MediaTek, which has successfully forged a position as a global leader in mobile chipsets, which have the potential for greater AI-driven applications. As an asset light, cash generative business, it has also been steadily growing its dividend as it returns significant cash to shareholders.

CAN THE AI BOOM CONTINUE?

Although returns from Asian technology stocks have been strong in recent years, the key question for investors right now is, can the growth continue? Some industry commentators worry that the stock market’s enthusiasm for AI and technology may have fuelled an investment bubble, similar to the one that greeted the internet boom in the late 1990s.

For Richard Sennitt, portfolio manager of the Schroder Oriental Income Fund, there are reasons for cautious optimism.

“We remain positive about the role that Asian technology companies can play in AI’s continued development. We are still in the early chapters of the AI story, and there is plenty of growth and innovation still to come, with implications for all industries and, indeed, all parts of daily life. This will inevitably drive risk as well as opportunity. However, expectations in parts of the IT sector related to AI are now high and longer-term question marks around the monetisation of the technology remain. Therefore, one needs to be disciplined when assessing stocks associated with the theme. Whilst Asia remains an interesting way for investors to gain exposure to the AI theme the broader sector also has longer term attractions and on balance, valuations for Asian technology stocks as a whole have not yet responded to the extent that they have in the US.”

DISCIPLINE IS KEY

Nevertheless, investors should be mindful of potential volatility in the near term. Although Asian technology stocks have not risen as far or as fast as those in the US, they are unlikely to be immune should US technology stocks suffer a correction.

The best protection against this risk is a long-term, disciplined investment approach, such as the one that Richard adopts for the Schroder Oriental Income Fund.

“We are pragmatic stock pickers and aim to look beyond the day-to-day swings in sentiment to which markets have always been prone. We are looking for the genuine long-term winners across a wide range of sectors, and maintain a strong valuation discipline to ensure that, when we find them, we don’t overpay for them.”

Richard and his team focus on quality companies that have strong management, appropriate balance sheets and sustainable long-term competitive advantages. Richard draws on Schroders’ extensive research resources in Asia, where on-the-ground analysts engage directly with company management teams, ensuring that the fund remains focused on opportunities that can deliver attractive

Risk Considerations: Schroder Oriental Income Fund Limited

• China risk: If the fund invests in the China Interbank Bond Market via the Bond Connect or in China “A” shares via the Shanghai-Hong Kong Stock Connect and Shenzhen-Hong Kong Stock Connect or in shares listed on the STAR Board or the ChiNext, this may involve clearing and settlement, regulatory, operational and counterparty risks. If the fund invests in onshore renminbi-denominated securities, currency control decisions made by the Chinese government could affect the value of the fund’s investments and could cause the fund to defer or suspend redemptions of its shares.

• Concentration risk: The Company may be concentrated in a limited number of geographical regions, industry sectors, markets and/or individual positions. This may result in large changes in the value of the company, both up or down.

• Counterparty risk: The Company may have contractual agreements with counterparties. If a counterparty is unable to fulfil their obligations, the sum that they owe to the Company may be lost in part or in whole.

• Currency risk: If the Company’s investments are denominated in currencies different to the

dividend profiles.

Having grown its dividend every year since its launch, this approach has served the Schroder Oriental Income Fund well in the past. Richard comments.

“We have a robust and repeatable investment process. The disciplined focus on valuation ensures we can adapt to evolving market conditions, allowing the portfolio to deliver its continued focus on income, while still being able to capture some of the best opportunities in Asia, in technology and beyond.”

currency of the Company’s shares, the Company may lose value as a result of movements in foreign exchange rates, otherwise known as currency rates.

• Derivatives risk: Derivatives, which are financial instruments deriving their value from an underlying asset, may be used to manage the portfolio efficiently. A derivative may not perform as expected, may create losses greater than the cost of the derivative and may result in losses to the fund.

• Emerging markets & frontier risk: Emerging markets, and especially frontier markets, generally carry greater political, legal, counterparty, operational and liquidity risk than developed markets.

• Gearing risk: The Company may borrow money to make further investments, this is known as gearing. Gearing will increase returns if the value of the investments purchased increase by more than the cost of borrowing, or reduce returns if they fail to do so. In falling markets, the whole of the value in such investments could be lost, which would result in losses to the Company.

• Liquidity Risk: The price of shares in the Company is determined by market supply and demand, and this may be different to the net asset value of the Company. In difficult market conditions, investors

may not be able to find a buyer for their shares or may not get back the amount that they originally invested. Certain investments of the Company, in particular the unquoted investments, may be less liquid and more difficult to value. In difficult market conditions, the Company may not be able to sell an investment for full value or at all and this could affect performance of the Company.

• Market Risk: The value of investments can go up and down and an investor may not get back the amount initially invested.

• Operational risk: Operational processes, including those related to the safekeeping of assets, may fail. This may result in losses to the Company.

• Performance risk: Investment objectives express an intended result but there is no guarantee that such a result will be achieved. Depending on market conditions and the macro economic environment, investment objectives may become more difficult to achieve.

• Private market valuations, and pricing frequency: Valuation of private asset investments is performed less frequently than listed securities and may be performed less frequently than the valuation of the Company itself. In addition, in times of stress it may be difficult to find appropriate prices for these investments and they

IMPORTANT INFORMATION

This communication is marketing material. The views and opinions contained herein are those of the named author(s) on this page and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds.

This document is intended to be for information purposes only and it is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment recommendations. Information herein is believed to be reliable but Schroder Investment Management Ltd (Schroders) does not warrant its completeness or accuracy.

The data has been sourced by Schroders and should be independently verified before further publication or use. No responsibility can be accepted for error of fact or opinion. This does not exclude or restrict any duty or liability that Schroders has to its customers under the Financial Services and Markets Act 2000 (as

may be valued on the basis of proxies or estimates. These factors mean that there may be significant changes in the net asset value of the Company which may also affect the price of shares in the Company.

• Share price risk: The price of shares in the Company is determined by market supply and demand, and this may be different to the net asset value of the Company. This means the price may be volatile, meaning the price may go up and down to a greater extent in response to changes in demand.

For help in understanding any terms used, please visit address www.schroders.com/en-gb/uk/individual/ glossary/

We recommend you seek financial advice from an Independent Adviser before making an investment decision. If you don’t already have an Adviser, you can find one at www.unbiased.co.uk or www.vouchedfor.co.uk. Before investing in an Investment Trust, refer to the prospectus, the latest Key Information Document (KID) and Key Features Document (KFD) at www.schroders. co.uk/investor or on request.

amended from time to time) or any other regulatory system. Reliance should not be placed on the views and information in the document when taking individual investment and/or strategic decisions.

Past Performance is not a guide to future performance. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. Exchange rate changes may cause the value of any overseas investments to rise or fall.

Any sectors, securities, regions or countries shown above are for illustrative purposes only and are not to be considered a recommendation to buy or sell.

The forecasts included should not be relied upon, are not guaranteed and are provided only as at the date of issue. Our forecasts are based on our own assumptions which may change. Forecasts and assumptions may be affected by external economic or other factors.

Issued by Schroder Unit Trusts Limited, 1 London Wall Place, London EC2Y 5AU. Registered Number 4191730 England. Authorised and regulated by the Financial Conduct Authority.

Is Alphabet antitrust case a threat or an opportunity?

What analysts say about US government’s Search monopoly claims

Once peerless, there’s an argument that Alphabet (GOOGL:NASDAQ) is now facing its own ‘Hobson’s choice’. On the one hand, it is being threatened by enormous potential disruption as competitors like OpenAI and its SearchGPT chase share of its valuable search market, forcing it to throw billions of dollars at AI (artificial intelligence) infrastructure to stay ahead.

On the other, there’s a nightmarish labyrinth of tightening antitrust rules as regulators around the world show a willingness to bare their teeth to bring big tech to heel. On 10 September, the European Union’s top court backed a €2.4 billion EU antitrust fine for Alphabet after the Court of Justice said the company’s practice of favouring its own shopping search results over rival services ‘was discriminatory’. The ruling can’t be appealed.

This was just a taste of the bitter pill Alphabet could be forced to swallow if US regulators get their way. On the same day the EU fine was handed out, the US government launched a trial against Alphabet accusing the company of illegally monopolising the ad tech market.

The lawsuit, originally filed in 2023, comes after a combined investigation by the US government and more than a dozen states. The case focuses on a $31 billion component of Alphabet’s Google ad business responsible for placing banner ads on millions of websites, called Google Admob.

It’s a big deal. Search, which includes Google Admob, is Alphabet’s crown jewel, generating $237.9 billion of revenue in 2023, about 77% of its $307.4 billion total. For context, Google Play and Google Cloud produced $34.7 billion and $33.1 billion respectively last year.

TURNING UGLY

Alphabet will, of course, put up a stiff defence and it has already described the monopoly allegations as ‘unfounded’, claiming that it is just one of several hundred companies in the online ad business, including other tech giants like Meta Platforms (META:NASDAQ), Apple (AAPL:NASDAQ), Amazon (AMZN:NASDAQ), and TikTok, and that competition in the digital ad space is increasing,

not decreasing as the lawsuit suggests, as more companies enter the lucrative sector.

But rare extreme measures are said to be under consideration by US rule makers, including an enforced break-up of Alphabet, a move that would be Washington’s first to dismantle a company for illegal monopolisation since unsuccessful efforts to break up Microsoft (MSFT:NASDAQ) two decades ago.

Less severe options could include forcing Alphabet to share more data with competitors and measures to prevent it from gaining an unfair advantage in AI products, according to reports. Normally, markets tend to shrug off regulatory threats aimed at big tech firms, but not this time. Since the investigation findings were made public in July, Alphabet’s share price has fallen sharply, down more than 18%, a decline that has eaten away at much of the stock’s year to date gains and leaving the stock a poor relation to other big tech names.

Meta, Amazon, and Apple are up 51%, 24% and 19% respectively since the start of the year. Clearly, investors have been given plenty to chew over.

HOW

REAL IS BREAK-UP

THREAT

But would a break-up really be so bad? Not according to Needham analysts, who have argued that Alphabet is worth more in pieces than as a whole.

‘YouTube would be worth $455 billion to $634

billion if separately traded,’ they say, representing 25% to 35% of Alphabet’s current $1.87 trillion total enterprise value today, based on assumptions that investors typically pay more for pure-play assets. Additionally, increased disclosures and improved employee retention could further enhance shareholder value, says Needham.

Needham are far from alone in seeing Alphabet as an attractive opportunity even with daunting antitrust pressures. Target prices for the stock over the next 12 months range from $151 to $230, but consensus is pitch at $202, implying almost 30% upside from currently levels.

Analysts at Piper Sandler and Wolfe Research have also encouraged long-term investors to take advantage of the recent pullback in Alphabet stock. ‘The antitrust case, particularly regarding Google’s dominance in Search, poses near-term headline risks,’ said Piper Sandler, but the litigation process is lengthy, with appeals and potential changes in government mitigating the immediate impact.

‘We spoke with an antitrust lawyer to discuss Alphabet’s DoJ litigation and his view was that the government has successfully argued the merits within two of three cases, but time is on Alphabet’s side.’

The Search trial, which is most significant, has a lengthy remedies and appeals process ahead. Meanwhile, there could be a new administration in the interim and technology is advancing fast, they

ALPHABET Q2 FY24 INCOME STATMENT

also noted. The recent ruling by judge Amit Mehta is characterised as ‘measured’ by the antitrust lawyer that Piper Sandler spoke to, with findings of monopoly power in Search and General Text Ads but without evidence of consumer harm.

‘A break-up or forced divestiture of Android/ Chrome is unlikely,’ according to Piper Sandler’s legal expert. On this basis the investment bank argues: ‘Long-term investors should use recent weakness to accumulate shares.’

REMEDIES AT THE READY

Wolfe Research notes potential remedies that might include implementing choice screens and/ or Apple entering a distribution agreement with a competitor, likely Bing, which would become the default search engine. They said their ‘incrementally positive view’ on Alphabet stock is grounded in four key factors:

First, in the choice screen scenario, their base case analysis suggests a 10% upside to consensus EPS (earnings per share) estimates and a more than 35% increase in the current share price. Secondly, even in a severe scenario where Apple switches its default search engine and Google loses 20% of its market share, the analysts project only a 5% downside to consensus EPS and around a 12% decline in share price.

Third, changes in the Network business

are expected to have little effect on core EPS. Lastly, Wolfe points out that third quarter (to end September) Search revenue may exceed expectations, despite fears of a modest miss.

Alphabet shares are currently trading on about 21-times 2024 EPS and 18 2025 estimates, or 18.9 based on Stockopedia’s rolling next 12 months EPS. That’s a 16% discount to Meta stock (22.5) and a hefty 60% to Apple (29.9) with comparable growth expected to the former and twice that of the latter. The S&P 500 trades on a forward PE (price to earnings) of about 21, according to Wolfe Research.