The Scottish Mortgage Investment Trust is a global fund seeking out the world’s most exciting growth companies and investing in them for the long term. We believe this is the best way for you to enjoy strong returns for decades to come. And we explore a number of exciting themes in order to seek out these world-changing businesses. Energy is just one of them. Why not discover them all?

As with any investment, your capital is at risk. A Key Information Document is available on our website. Discover what’s next. Explore the future at scottishmortgage.com Connect with us:

Three important things in this week’s magazine

1

Time for US rate cuts

How far and fast might interest rates fall in the US and what will be the impact across different asset classes – Shares canvassed the experts to get their views.

2

Get to grips with Palantir

Part software company, part consultancy, its work with US government agencies and intelligence communities lends it a mystique that not all investors embrace.

3

Find out what’s going on with UK small caps From I3 Energy to Intercede we look at some of the biggest stories among London’s market minnows.

Visit our website for more articles

Did you know that we publish daily news stories on our website as bonus content? These articles do not appear in the magazine so make sure you keep abreast of market activities by visiting our website on a regular basis.

Over the past week we’ve written a variety of news stories online that do not appear in this magazine, including:

Apple set for new finance chief for first time in a decade: what should investors expect?

Bunzl boosted by profit upgrade and bumper share buyback

Nestle shares tumble as CEO Schneider departs after a tricky year

JD Sports Fashion rallies 6% on improving sales trend and maintained profit guidance

Will UK shop price deflation open the door to a September rate cut from the Bank of England?

Pound heads to 29-month highs against the dollar amid diverging tones from central bank chiefs

UK shop prices experienced deflation for the first time in almost three years in August with a fall of 0.3%, according to the latest data from the monthly BRC-NIQ (British Retail Consortium-NielsenIQ Shop Price Index).

The price deflation was driven by the nonfood segment which came in at -1.5% in August, deepening by 60 basis points month-on-month, year-on-year, and 40 basis points below the threemonth rolling average rate of -1.1%.

‘The price deflation was driven by the non-food segment where discretionary goods demand has been weak, food, as we have argued for some time, remained in inflationary territory, coming in at 2%, a broadly manageable level for households.

‘The [Bank of England’s] MPC (monetary policy committee) may be concerned about UK wage and service inflation, but it should sleep easy on the retail component, where, if anything, the grounds for a base rate cut is evident, if it takes note of the data,’ says Shores Capital’s head of consumer research Clive Black.

The fall in UK shop prices creates space for the Bank of England to cut rates further when it meets on 19 September. This event which will be overshadowed by the US Federal Reserve’s two-day meeting on 17-18 September when it is widely expect to cut rates for the first time in this cycle –the Bank of England having taken the plunge at the beginning of August.

US $ to British £

Shares magazine • Source: LSEG

to leave rates unchanged. Federal Reserve chair Jerome Powell said last Friday (23 August) that the ‘time has come’ to begin lowering interest rates at the Jackson Hole economic policy symposium. Powell confirmed at the three-day meeting of central bankers, policymakers, and global economists that the Fed would not welcome any further downturn in the US jobs market. Sterling soared against the US dollar to a 29-month high after Powell’s remarks reaching above $1.32 –more than a cent up on the day – the highest level since March 2022.

Then five members voted in favour of cutting rates from 5.25% to 5% and four members voted

While Powell seems confident of the US central bank’s next move, the governor of the Bank of England Andrew Bailey is cautiously optimistic about the UK inflation outlook, but added in his own speech at Jackson Hole he will not be rushed into further rate cuts. Bailey said on 23 August: ‘The second-round inflation effects appear to be smaller than we expected. But it is too early to declare victory.’ [SG]

Chart:

Temu parent PDD sends warning on Chinese consumers

cheap products.’

Missed second quarters expectations and soft growth guidance has sparked the biggest ever oneday sell-off in PDD Holdings (PDD:NASDAQ), the parent of online shopping platforms Temu and Pinduoduo.

ADR (American Depositary Receipts) in the company fell as much as 40% in intraday trading, eventually closing 28.5% lower at $100 on 26 August, a decline that wiped more than $55 billion off PDD’s market cap.

PDD reported second-quarter revenue of 97.06 billion yuan, or $13.6 billion, rising 86% from the same period the year before. But this fell short of Wall Street expectations for quarterly revenue of 99.4 billion yuan (about $14 billion) from analysts polled by Investing.com.

‘The market has been caught out by weaker than expected results from PDD and gloomy comments from management’, said AJ Bell investment director Russ Mould. ‘It looks like consumers are being even more cautious about spending and perhaps realising they don’t need to fill their house with oodles of

Lei Chen, chairman and co-CEO of PDD, wrote in the earnings release that ‘while encouraged by the solid progress we made in the past few quarters, we see many challenges ahead’.

Chen added the company is ‘prepared to accept short-term sacrifices and potential decline in profitability’ as it invests heavily in areas like trust and safety, as well as improving its merchant ecosystem.

PDD is not the only online marketplace in China to have reported missed expectations as the country experiences an economic downturn with high unemployment rates and falling household income. Alibaba (BABA:NYSE), a similar online marketplace selling ultra-discounted goods, reported net income down 28.8% in June and JD.Com (9618:HKG), listed in Hong Kong, missed its revenue projection in the same month.

‘The group’s stellar run has come to a crashing halt,’ said AJ Bell investment director Russ Mould. ‘There is a perfect storm of uncertain economic conditions, cautious consumers and competitive pressures. It suggests that even bargain basement operators can struggle if consumers are thinking hard about where they spend money.’

Reports emerged in July that young consumers in China are saving more than generations past and that the idea of setting ultra-low spending targets has even become a viral social media trend called ‘revenge saving’, sparked by the country’s weakening economy.

The sharp fall in PDD’s share price will prompt the market to reappraise the business and its prospects even as it continues to post rapid growth. ‘The latest results are a reminder that even the most successful companies cannot maintain very high levels of growth forever,’ said Mould. [SF]

DISCLAIMER: Financial services company AJ Bell referenced in this article owns Shares magazine. The author of this article (Steven Frazer) and the editor (Tom Sieber) own shares in AJ Bell.

Beeks Financial Cloud scales new all-time high after record results and contract extension

Cloud computing play has conditionally secured a third cloud contract with one of the largest global exchanges

Shares in cloud computing, connectivity and analytics provider Beeks Financial Cloud (BKS:AIM) scaled a new all-time high of 282p after the firm announced (20 August) it had won a contract extension with the Johannesburg Stock Exchange.

The latest advance takes the year-to-date gain for the stock to 181%, supported by positive fundamental news flow over the last 12 months. Following the initial contract win in the summer of 2023, Beeks announced a ‘significant’ extension in March 2024.

Under the latest multi-year extension, the service provided will allow the JSE to meet the needs of large banks’ regulatory requirements for dual-location disaster recovery.

Beeks chief executive officer Gordon McArthur said: ‘Exchange Cloud continues to be a unique offering in the market, and the success of the solution at the JSE is supporting our discussions with other global exchanges, underpinning our confidence in continued momentum.’

Analysts at Canaccord Genuity

believe the success of the ‘land and expand’ strategy deployed at JSE supports their confidence in their financial projections for Beeks. In its latest trading update (22 July), Beeks delivered another set of record results with revenue rising 27% and underlying pre-tax profit rising 67% for the full year to June 2024. [MG]

Watkin Jones shares pummeled on cut to guidance

Shares in Watkin Jones (WJG:AIM), the UK’s leading for-rent developer and operator, sank 30% in a day last week after the firm cut its operating profit forecast for this year and warned profit next year would likely be even lower rather than rebounding.

The group, which focuses mainly on student accommodation but also develops mixed-tenure schemes of affordable housing, said market activity had been ‘slower than anticipated’ due to continued uncertainty over the pace of interest rate cuts and it was unlikely to close any deals before its financial year end in September.

As a result, adjusted operating

profit will be in the range of £10 million to £12 million compared with the previous guidance given in May of ‘at least £15 million’.

Worse still, the lower number of transactions this financial year will impact next year’s results, given schemes don’t contribute to revenue in future periods until they are forward-sold, so profit for the year to September 2025 will be below this year’s level.

The group also cautioned that while its net cash position underpins its committed spending requirements, ‘it is a limiting factor on the extent to which we can take advantage of market conditions and further develop

our pipeline.

‘In light of this, the board is undertaking a review of a range of options that may be available to enhance its medium- and longer-term funding position, thereby allowing the group to capitalise on a market recovery.’ [IC]

Forecasts

INTERIM RESULTS & TRADING UPDATES

2 Sept: Ashtead Technology, Concurrent Technologies, Kainos Group

3 Sept: Ashtead, DS Smith, Johnson Service Group, Michelmersh, Midwich Group, Stv Group, Uniphar, Watches of Switzerland

4 Sept: Ascential, Cairn Homes, Dalata Hotels, Direct Line, Hilton Food Group, James Cropper

Direct Line needs to show progress after rejecting takeover bid and revealing a new strategy

The insurer has ambitious plans to grow in Home, Rescue and Commercial

Investors will be keen to discover if insurer Direct Line Insurance (DLG) has continued its positive start to the year when it reports first-half results on 4 September after a tumultuous 12 months.

The business delivered a strong first quarter, with double-digit written premium growth in Motor, Home and Commercial businesses and overall growth of 15% for ongoing operations.

Chief executive Adam Winslow, who only took charge in March, has already made significant senior hires to reinvigorate the business and presented a bold new business strategy at the firm's Capital Markets Day on 10 July.

This included a return to pricecomparison websites, making at least £100 million of gross run-rate cost savings by the end of 2025 and targeting a 13% net insurance margin in 2026.

The company also announced a new capital allocation framework and a policy to pay around 60% of operating earnings as a regular dividend, while an improving solvency capital ratio is expected to provide scope for additional shareholder returns.

Analysts at Jefferies noted that while management were reluctant to provide a timeframe for returning to a 180% solvency ratio, they believed there was potential for ‘material’ special capital returns by 2026. Investors will no doubt want to see tangible evidence of this progress given the board rejected a £3.2 billion takeover approach from Belgian insurer Ageas (AGS:EBR) in March. [MG]

Chart: Shares magazine • Source: LSEG

Hormel Foods is ready to talk turkey

The turkey, sausage and peanut processor is cutting costs and benefiting from continued foodservice sector strength

Investors lost their appetite for Hormel Foods (HRL:NYSE) after the global branded food group served up mixed second-quarter results in May, but the stock has been shaken from its torpor in recent weeks on optimism surrounding management’s turnaround plan and Mars’ takeover of Kellanova (K:NYSE), which has highlighted the resilience and growth potential of selective food sector names.

Bulls will be hoping for positive noises on premium meat demand and progress against Hormel’s ‘transform and modernise’ initiative, which involves delivering supply chain savings and improving margins, when the Minnesota-based firm delivers thirdquarter earnings (4 September).

May saw the company behind turkey products leader Jennie-O, Planters

peanuts, SPAM luncheon meat and Applegate Naturals bacon post a surprise second-quarter earnings beat as robust demand for premium meats combined with the fruits of cost savings.

Unfortunately, quarterly sales dipped from $2.98 billion to $2.89 billion and operating income fell 15% to $252 million amid challenges in Hormel’s retail business, including a ‘significant’ year-on-year decline in whole-bird turkey volumes and prices.

However, continued food service strength gave Hormel the confidence to hike its full-year earnings forecast from the $1.51 to $1.65 per share range to between $1.55 and $1.65. [JC]

Powell signals start of interest rates cuts at Jackson Hole

The Fed appears to have achieved a soft landing for the economy

With markets betting heavily the Federal Reserve would start cutting interest rates at its next meeting, chair Jerome Powell did not disappoint after delivering a dovish speech at the Jackson Hole symposium on 23 August.

‘The time has come for policy to adjust’ announced Powell, immediately sending stock and bond prices higher while the dollar sank against the major currencies. Sterling trading around 1.31 against the dollar, its highest in over a year.

Macro diary 30 August to 05

Macro diary 30 August to 05

30 August to 05

While Powell said the direction of travel is clear, he left open the timing and pace of future rate cuts, sticking to his playbook of relying on incoming data to determine the evolving balance of risks.

Remarks on increasing risks to a US labour market which has remained surprisingly resilient thus far to rising interest rates increase the importance of August’s non-farm payrolls data due on 6 September.

Before that investors get another inflation reading on 30 August with consensus economists’ forecasts looking for an unchanged core PCE (personal consumption expenditures) year over year reading of 2.5%.

Considering Powell’s Jackson Hole comments of ‘diminishing upside risks’ to inflation, a higher reading may once again put the cat among the pigeons and potentially thwart near-term cuts.

According to the CME’s Fedwatch tool, markets are pricing in a 71.5% chance of a quarter of a percentage point cut and a 28.5% chance of a half a percentage point cut in interest rates in September. [MG]

Go for growth with The Global Smaller Companies Trust

Falling interest rates around the world will create strong tailwinds for this small and mid caps one-stop shop

The Global Smaller Companies Trust (GSCT) 166p

Market cap: £794.4 million

Despite the recent stock market dominance of mega-cap US tech companies, high-quality smaller caps have a longer term record of outperforming. With greater inherent growth potential than their large cap brethren, small caps tend to fare well in a falling interest rate environment and with borrowing costs on the way down in the UK, US and elsewhere, the stage looks set for a smaller companies revival.

As such, Shares believes this is an opportune moment to put money to work with The Global Smaller Companies Trust (GSCT). A near-9% discount to NAV (net asset value), narrowed from 17.7% in July 2023, demonstrates there is still value on offer at this well-diversified trust, which offers portfolio builders a simple way to access the growth potential of exciting growth companies around the globe for a reasonable ongoing charge of 0.78%. As rates edge down and sentiment towards small and mid caps improves, the £794.4 million cap should build on its robust long-term track record which shows a 10-year share price return of 114%.

Columbia Threadneedle Investment’s Nish Patel is the lead manager following the recent retirement of Peter Ewins and the trust benefits from a strong dedicated small company investment team who focus on high-quality, well-managed, soundly financed and profitable companies.

Smaller Companies Trust

and mid cap stocks, but in an ultra-diversified way that dampens down volatility.

Reassuringly balanced in terms of its weighting in growth versus value stocks, the fund provides exposure to a broad spread of geographies. As of 31 July, 42.3% of its assets were in North America, 23.9% in the UK and 11.2% in Continental Europe, with 13.2% and 9.6% in the Rest of World and Japan respectively.

Company exposure is provided through more than 200 directly-held companies plus five collective fund investments, which means company-specific risk is negligible. The trust’s top 10 stock positions include building materials producer Eagle Materials (EXP:NYSE), tank barge operator Kirby (KEX:NYSE) and actuators-toaircraft controls maker Curtiss Wright (CW:NYSE), while the five funds include Eastspring Investments Japan Smaller Companies, investment trust Scottish Oriental Smaller Companies (SST) as well as the Schroders Global Emerging Market Smaller Companies Fund.

Global Smaller Companies Trust’s portfolio is a good one-stop shop for investors seeking exposure to the dynamic growth of UK and overseas small

Global Smaller Companies Trust is one of the Association of Investment Companies’ ‘dividend heroes’, its 22.2% hike in the divided to 2.81p for the year to April 2024 taking its unbroken payout growth record to 54 years, although strong share price performance over the period means the yield is relatively skinny at 1.7%. [JC]

Industrial chains business Renold is a lot more exciting than you think

The growth, quality and value on offer here is a rare combination not to be missed

Renold (RNO:AIM) 54.71p

Market Cap: £123.9 million

Making industrial chains and specialist torque transmission products doesn’t sound very exciting but 150-year-old Renold (RNO:AIM) happens to be rather good at it and today is the second largest player globally.

The global market is very fragmented and despite being a big fish Renold’s market share is under 10% in terms of revenue, providing a significant opportunity to consolidate the market through acquisitions.

This means Renold can grow faster than the slow growing underlying markets which it serves. That is one leg of the investment case and key to creating shareholder value.

The business has also built a global reputation for engineering branded premium quality products and engineering solutions that customers can trust. Its products are built to a high specification and designed to last longer and be more reliable.

This is important for customers because a faulty or broken chain can be highly impactful and therefore, they are prepared to pay a premium price for a premium product. A trend towards increasing premiumisation is another leg of the investment case.

Management told Shares that increasing automation across many industries that use chains is acting as a tailwind for the business.

It is easy to fall into the trap of thinking that industrial chains serve traditional, low growth industries, yet increasingly Renold’s products are used in faster growing, high-tech and cutting-edge applications.

The final leg of the investment case is the potential for the business to increase operating margins towards a mid-teen’s percentage over time. Two factors are driving this expectation.

The group can grow two to three times larger than its current size with the infrastructure it has already, and with relatively fixed costs this means a bigger proportion of revenue can be turned into profit. This is often referred to as positive operating leverage effects.

In addition, central overheads can be removed from acquired businesses. It is worth mentioning ‘soft’ synergies like cross-selling higher value products which also drive incremental revenue and profit.

Financial metrics for Renold support the investment case.

Over the last four years revenue has increased at a compound annual growth rate of 6.25% a year, operating margins have expanded from 7.1% to 12.3% and return on capital is a healthy 22.5% % compared with 10.7% in 2020.

The company has reintroduced a dividend for the first time since 2005 reflecting strong cash flow generation.

In short, the potential for double digit profit growth and increasing cash generation is not reflected in a lowly seven times forward PE (price to earnings) ratio. Growth, quality and value is a rare combination not to be missed. [MG]

Discover why Currys’ shares are still far too cheap

Panmure Liberum sees ‘significant alpha on offer’ at the FTSE 250 electricals retailer

Currys (CURY) 79.25p

Gain to date: 31.9%

We flagged the recovery potential of electricals retailer Currys (CURY) on 21 March and urged readers to buy the stock at 60.1p on the basis self-help measures were beginning to pay off and the super-size TVs-to-smartphones seller offered a compelling play on an improving consumer backdrop. Recent takeover interest had only served to highlight the underlying value on offer at the FTSE 250 technology products hawker.

WHAT HAS HAPPENED SINCE WE SAID TO BUY?

Currys’ shares have rallied 31.9% amid growing investor awareness of the company’s turnaround potential. On 14 May, the company upgraded pretax profit guidance once again following a ‘strong finish’ to the year ended 27 April 2024, with results (27 June) showing a pleasing 10% jump in adjusted pre-tax profit to £118 million.

CEO Alex Baldock flagged encouraging momentum in the UK & Ireland, insisted the Nordics business was getting back on track and

Currys

Shares magazine • Source: LSEG

guided for profit and free cash flow growth in full year 2025 driven by growth in high margin recurring revenue services, including reaching at least two million iD Mobile subscribers before year end.

WHAT SHOULD INVESTORS DO NOW?

Keep buying Currys. In a note published on 13 August, Panmure Liberum argued Currys’ 35% valuation discount to any others in the electricals sector is ‘overdone’ and noted the quality of revenues has massively improved with nearly £700 million of Currys’ sales now high margin service related.

The broker said Currys’ margins ‘can double from here and due to the sensitivity of the model, Currys probably offers more Alpha than most’. Even after the recent rally, the shares are swapping hands for a lowly prospective price to earnings ratio (PE) of 9.1, based on Panmure Liberum’s 8.7p year-to-April 2025 earnings estimate, which is forecast to rise to 10.3p and 11.9p in 2026 and 2027 respectively. Panmure Liberum also observed that ‘the tech replacement cycle is upon us (post Covid boom) and new AI infused products will drive incremental interest’ in Currys. [JC]

BECOME A BETTER INVESTOR WITH

SHARES

MAGAZINE HELPS YOU TO:

• Learn how the markets work

• Discover new investment opportunities

• Monitor stocks with watchlists

• Explore sectors and themes

• Spot interesting funds and investment trusts

• Build and manage portfolios

TIME FOR

RATE CUTS

What a first move by the Fed means for markets

At the end of last year the market was pricing in 1.7% worth of US rate cuts for 2024 but here we are in late August and the Federal Reserve is yet to pull the trigger, largely due to stickier-than-expected inflation.

US inflation proved sticky at the start of 2024

for a big 50 basis-point (0.5%) move.

This matters outside of the US. The world’s largest economy inevitably has the world’s most influential central bank and, while its counterparts in the UK and Europe (and elsewhere) have already started the rate-cutting process, when the Fed cuts it could really shift the dial.

Ahead of this major market milestone, Shares has canvassed the opinion of myriad market experts to get an impression of how different stocks, sectors and asset classes might react.

WHAT IS THE LIKELY TRAJECTORY OF RATES?

First, it is worth considering what the trajectory of rates may look like. Some forecasters think we might see two rate cuts before the year is out, while Bank of America notes a big driver for cuts could be the state of the US public finances.

However, after a series of false dawns, we may finally be approaching the point where the Fed acts, with a rate cut widely expected on 18 September. The debate largely centres on whether the central bank cuts rates by 25 basis points (0.25%) or opts

National debt across the Atlantic is up more than $1 trillion so far in 2024 to $35 trillion with the annual interest payment at $900 billion, accounting for 13.4% of government spend.

If rates were left unchanged then Bank of

America sees this figure rising to $1.4 trillion by July 2025, and even if there are 200 basis points worth of cuts in the interim payments would rise to $1.2 trillion. As the investment bank concludes the net result is ‘many Fed cuts a-coming’.

The consensus view is for rates to end 2025 at around 3.75%. While lower interest rates are usually perceived as good news for stocks, as the relative appeal of lower-risk assets like cash are reduced, the portents are actually not great for the markets based on what has happened in the last few rate-cutting cycles.

US interest rates forecast

However, it is worth adding that these were accompanied by significant crises, namely the dotcom crash, the great financial crisis and the pandemic.

Much will depend on whether the Fed has been able to engineer a soft landing for the US economy, steering it through an inflationary period with a restrictive policy without inflicting too much economic damage.

While the US consumer has proved impressively resilient and growth has largely held up, interest rate hikes have a lagged effect and the full impact of the surge in rates which started in late 2021 may not be felt until we are already well into the ratecutting cycle.

Charles-Henry Monchau, chief investment officer of boutique Swiss bank Syz Group, observes: ‘It all depends on which type of rate cut(s) we get. There are historically three types of Fed cuts: "panic cuts", "soft cuts", and "hard cuts".

‘Panic cuts, such as those in 1987 and 1998, are positive for stocks if the event does not impact Main Street. Soft cuts, like those in 1984, 1995 and 2019, are positive for both stocks and bonds. Hard cuts, as in 1973, 1974, 1980, 1981, 1989, 2001 and 2007, are negative for stocks but positive for bonds. Therefore rate cuts are not always positive for stocks.’

BETWEEN A HARD AND A SOFT LANDING

Paul Middleton, senior global equities portfolio manager at Mirabaud Asset Management, says: ‘We have just witnessed a very rapid fall in US yields. There have been two distinct periods of stock performance during this decline, and this gives us a very good feel for how stocks will behave around rate cuts.

“The first part of the decline in yields was accompanied by data suggesting a soft landing: slightly weaker inflation reported against expectations, and slightly stronger than expected employment. In this soft-landing phase, recovery

names worked well – names that tend to perform strongly as we are exiting a macro slowdown period, such as housing-related companies, or autos.’

‘The second part of the decline in yields saw the narrative switch from soft landing to hard landing, with weaker inflation and weaker employment. There has been a significant and rapid move into safe haven names – staples, utilities, healthcare, and REITs.

‘The market narrative has shifted rapidly between these two extremes, and the truth will likely fall somewhere in between. History suggests a soft landing is a much less likely outcome of the two, and markets tend to stay defensive post first cut, so within the portfolios we have a slightly more defensive tilt than usual, but as always we keep some attackers on the pitch for when the macro data turns.’

Darius McDermott, managing director of Chelsea Financial Services, observes: ‘Anticipation of global interest rate cuts has already fueled a broader risk asset recovery this year. The interest rate cut by the Bank of England is significant and will likely embolden investors to increase their level of risk. With the Fed widely expected to follow suit in September, the stage is set for a surge in “animal spirits” in markets.’

SMALL-CAPS TO SHINE?

McDermott notes that, historically, small-caps have performed well when rates fall and he expects this space to build on its recent momentum.

‘Despite history suggesting they considerably outperform large-caps over the long term, especially in recovering markets, they still trade at compellingly low valuations,’ he adds.

McDermott highlights ‘talented stock pickers’ who can take advantage such as Liontrust UK Smaller Companies (B8HWPP4), WS Amati UK Listed Smaller Companies (B2NG4R3), and Unicorn Smaller Companies (3178506) funds.

There isn’t necessarily a consensus on smallcaps' ability to shine. T. Rowe Price’s solutions strategist in its multi-asset team, Michael Walsh, says: ‘While expectations the Fed will start to cut rates has hardened, small-cap stocks in the US have advanced sharply in recent weeks. We question whether fundamentals will improve sufficiently to justify this rally.’

McDermott also flags emerging markets as a beneficiary of rates moving lower. ‘While market volatility and uncertainties persist,

WHAT RATE CUTS MEAN FOR THE PROPERTY SECTOR AND REITS

Rich Hill, head of real estate strategy and research at US asset manager Cohen & Steers, says: ‘Over the past several years we have seen some of the largest and fastest interest rate increases in more than 40 years. This has negatively impacted global REITs (real estate investment trusts) over the last two years with the sector down 12.2% from its peak in 2021. However, efforts by global central banks to bring down inflation are working, and we believe we are moving towards a macroeconomic environment that should be more accommodative to listed REITs as interest rates are potentially cut.

‘This, coupled with fundamental growth which remains on a solid footing, and valuations which are attractive relative to equities, sets the stage for the listed REIT rally to continue. Indeed, globally-listed REITs have risen almost 32% since their post-Covid lows in the fourth quarter of 2024.

‘In fact, US-listed REITs are the secondbest performing sector of the S&P index over the last four months. We expect to see more volatility as global central banks try to navigate a soft landing, and we believe pullbacks can act as entry points, while volatility may provide active managers with opportunities to outperform.

‘Within the US, we like data centres, senior living facilities, single-family rentals and cell towers. In Europe, we favor high-quality continental retail, logistics, self-storage and cell towers, which offer attractive valuations and solid fundamentals or relatively attractive pricing. We also like the German residential sector as values stabilise and discounts to NAV (net asset value) are historically wide.’

particularly around China, the sector's compelling demographics – young, growing populations, and expanding middle classes – offer the potential for strong long-term returns. This potential outperformance could also be amplified by the prospect of a weakened US dollar,’ he says.

He highlights FP Carmignac Emerging Markets (BQXJRP9), FSSA Global Emerging Markets Focus (BZ8GV67), and Invesco Global Emerging Markets (3303030) as ‘strong contenders in this space’.

Walsh believes much will depend on the pace and length of the current easing cycle. ‘Rate cuts are expected to continue at a leisurely pace by the markets, as monetary easing helps major economies achieve a soft landing. We see this relatively rosy view as the most likely outcome and maintain a small overweight position to selected areas of the equity market and other risky assets such as high yield debt, as corporate profitability remains strong,’ he says.

WHAT ABOUT BONDS?

Walsh concludes: ‘It would be a different story for instance if a sharp downturn in the labour market soured sentiment on the economic outlook. Then we would be likely to see a much quicker series of rate cuts and a general flight to quality, boosting high-quality fixed income, such as US treasuries, at the expense of riskier asset classes.’

Typically, when rates go up so do bond prices, although conversely this also means the yields on bonds fall. The co-managers of Aegon Strategic Bond Fund (B00MY36), Alex Pelteshki and Colin Finlayson, say: ‘Going forward, we continue to see an unusual set of opportunities in global fixed income markets. We expect to see the commencement of one of the largest synchronised easing/rate cutting cycles in recent history across developed markets, therefore we maintain an above- average interest rate risk position.’

Interest rate risk is the potential for investment losses triggered by a move upward in the prevailing rates for new debt instruments, and the managers at Invesco Bond Income Plus (BIPS), Rhys Davies and Edward Craven, see a similar picture: ‘There have already been some rate cuts and we think there will be room for more over the rest of the year. We are comfortable holding more interest rate risk. Current yields are satisfactory and there is potential for capital return as interest rate expectations evolve.’

GOOD NEWS FOR INVESTMENT TRUSTS?

Nick Greenwood is co-manager of MIGO Opportunities Trust (MIGO), which seeks to take stakes in investment trusts trading below the market value of their underlying assets. With the direction for rates set lower, he believes this is a good time to revisit bombed-out ‘alternative’ trusts.

‘Most of these were created to solve yield starvation by offering a decent dividend at a time when deposit rates were effectively zero,’ he says. ‘Demand has evaporated now it is possible to get a decent income from conventional sources such as gilts. This has led to an oversupply situation and given investment trust share prices are decided by the balance of supply and demand, it is not surprising many of these funds can be acquired at steep discounts. At these depressed levels the dividend yield is high relative to share prices.

‘This represents an arbitrage opportunity as the lack of demand is for the structure whereas the market for the assets the trust owns is often buoyant. Yields on funds such as Cordiant Digital Infrastructure (CORD) and VH Sustainable Energy Opportunities (GSEO) will attract new buyers as a decline in interest rates reduces what is on offer elsewhere.

‘The general oversupply situation is steadily resolving itself via widespread buybacks, returns of capital and mergers. In the not-too-distant future demand will no longer be swamped by supply, allowing shares to trade closer to the value of their portfolios. This should mean share prices will rise even if net asset values make no progress.’

DISCLAIMER: The editor (Ian Conway) of this article has a personal holding in Invesco Bond Income Plus.

Small World: a whirlwind tour of some of the month’s big small-cap stories

From takeovers to new contracts, new projects and new customers

We start this month’s round-up with news of a bid at just shy of a 50% premium for oil and gas exploration company I3 Energy (I3E:AIM) from US-listed Gran Tierra Energy (GTE:NYSEAMERICAN).

The US firm, which has a market cap of $260 million, is paying roughly $225 million or £174 million for the UK company through a combination of cash and shares.

I3 Energy operates in the Western Canadian Sedimentary Basin, which is one of the priority areas Gran Tierra had earmarked for expansion due to the high quality of the assets in place and access to infrastructure.

Hub) project in the Irish Sea.

The ‘energy transition’ firm, which only came to market in December 2023, has ambitions to create a new energy storage facility to provide ‘a secure and dependable supply of natural gas and green hydrogen for the UK market for at least 20 years’.

The MESH facility off the Lancashire coast has the capacity to store some 50 billion cubic feet of gas, around the same as the Rough facility in the North Sea, which is currently the UK’s largest, and enough to heat 2.2 million average UK homes over winter.

LIGHTING UP

The deal will create ‘a more diverse international energy company operating across the Americas in regions with substantial oil and gas production, well-established regulatory regimes, stable contracts, access to markets and attractive fiscal terms’ according to Gran Tierra.

From an energy firm about to end its life as a quoted company to one just starting out on its journey, nano-cap EnergyPathways (EPP:AIM) reported it had submitted a gas storage licence application for its MESH (Marram Energy Storage

There was a double helping of positive news from futuristic-sounding Light Science Technologies (LST:AIM), which won new contracts from an agriculture producer and a customer in the sports entertainment sector.

The Ashbourne, Derbyshire-based micro-cap signed one contract to provide its nurturGROW lighting solution over a 0.5 hectare aeroponic glasshouse in Germany designed to grow leafy greens from the start of 2025.

The company’s Controlled Environment Agriculture division, which includes the nurturGROW system, generated sales of close to £0.5 million in the eight months to the end of July and has a quoted pipeline of over £40 million.

The second contract, for £134,000, takes orders for its Contract Electronics Manufacturing division from the sports entertainment sector to £400,000 this year with the prospect of more orders to come as the customer rolls out more venues in the US.

MICROSOFT TIE-UP EXCITES

Meanwhile, cybersecurity software firm Intercede Group (IGP:AIM) announced it had signed a strategic agreement with tech behemoth Microsoft (MSFT:NASDAQ).

The Lutterworth-based firm, which has a

market cap of £100 million against Microsoft’s $3 trillion, will combine its expertise in credential management systems with the Seattle-based giant’s Entra ID to allow administrators to create and register FIDO passkeys on behalf of users.

The deal will enable companies to comply with US federal government security legislation at the highest levels of assurance and is a major coup for Intercede, whose shares leapt 18p or 10% to a 10year high of 191p on the news.

Continuing in a positive vein, clinical diagnostic firm LungLife AI (LLAI:AIM) shared positive news from the US regarding its LungLB test designed to provide early detection of lung cancer via blood samples.

In January 2023, Medicare established a price of around $2,000 per LungLB test, and this month the California-based micro-cap said it had won ‘a local coverage determination’ for risk-testing of indeterminate lung nodules from the Medicare Administrative Contractor, meaning it can apply for coverage to receive payment from Medicare from the end of September.

TESTING THE WATERS

There was also a positive development for testing and monitoring firm Tan Delta Systems (TAND:AIM), which signed a £200,000 deal with a global engine OEM (original equipment maker) to produce a real-time sensor to measure the condition and degradation of coolants and other fluids.

Intercede Group

Tan Delta expects to have the product ready for live trials by the end of this year and is eying potential revenue of £2 million over the next five years.

Unfortunately, that’s where the good news for small-cap investors ends this month as we finish with Sheffield-based linear generator technology firm Libertine Holdings (LIB:AIM)

In June, the firm ended its formal sale process as no bidders had come forward, but it said it had received two offers of investment worth £1 million each, which would provide enough funds to keep the company ticking over until June next year when it hoped to break even.

Ahead of the investment, a firm called Reliant FZC offered to provide a bridging loan of £220,000 in two tranches, but last week Libertine reported it had received no outside funding and only had enough cash to continue operating until the end of this month.

After that, the company ‘may not be able to meet its liabilities as they fall due and it may enter into administration or another form of insolvency procedure, under which the timing or level of return, if any, to shareholders would be uncertain’.

Disclaimer: The author (Ian Conway) owns shares in Tan Delta Systems.

By Ian Conway Deputy Editor

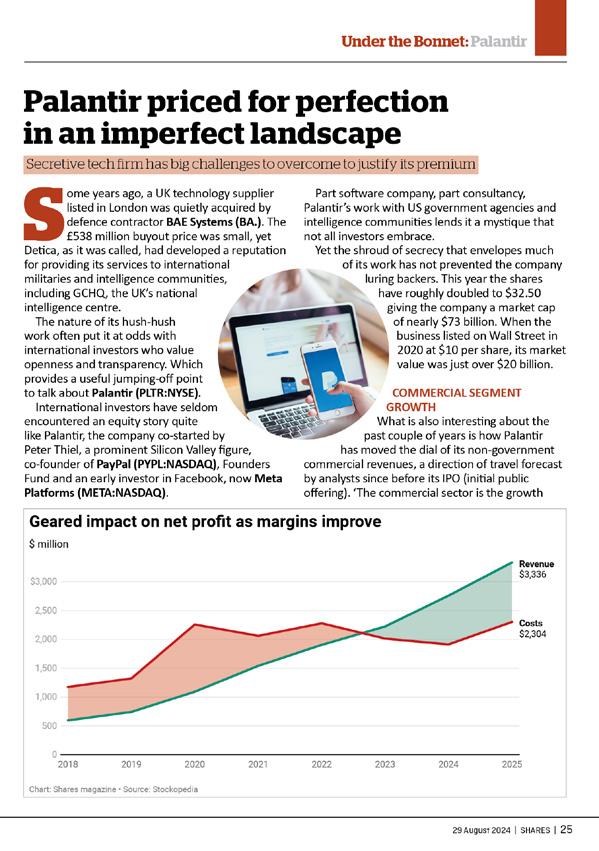

Palantir priced for perfection in an imperfect landscape

Secretive tech firm has big challenges to overcome to justify its premium

Some years ago, a UK technology supplier listed in London was quietly acquired by defence contractor BAE Systems (BA.). The £538 million buyout price was small, yet Detica, as it was called, had developed a reputation for providing its services to international militaries and intelligence communities, including GCHQ, the UK’s national intelligence centre.

The nature of its hush-hush work often put it at odds with international investors who value openness and transparency. Which provides a useful jumping-off point to talk about Palantir (PLTR:NYSE). International investors have seldom encountered an equity story quite like Palantir, the company co-started by Peter Thiel, a prominent Silicon Valley figure, co-founder of PayPal (PYPL:NASDAQ), Founders Fund and an early investor in Facebook, now Meta Platforms (META:NASDAQ).

Part software company, part consultancy, Palantir’s work with US government agencies and intelligence communities lends it a mystique that not all investors embrace.

Yet the shroud of secrecy that envelopes much of its work has not prevented the company luring backers. This year the shares have roughly doubled to $32.50 giving the company a market cap of nearly $73 billion. When the business listed on Wall Street in 2020 at $10 per share, its market value was just over $20 billion.

COMMERCIAL SEGMENT GROWTH

What is also interesting about the past couple of years is how Palantir has moved the dial of its non-government commercial revenues, a direction of travel forecast by analysts since before its IPO (initial public offering). ‘The commercial sector is the growth

Operating margins have doubled in past 12 months

story for the company as it expands beyond government clientele,’ wrote Beth Kindig, lead tech analyst at the IO Fund, in 2020.

Heading into 2024, Palantir had been demonstrating multiple signs of acceleration from strong growth in its US commercial segment, driven by AIP, its Artificial Intelligence Platform which lets customers lever its AI (artificial intelligence) and ML (machine learning) tools and harness the power of the latest large language models of data.

Palantir’s first-quarter government/commercial revenue growth split was 16%/27%, rising to 23%/33% in the second quarter. Commercial is still the junior partner, but only just, at $307 million in Q2 versus $371 million for government revenue.

In the first quarter of this year, the firm added 41 net new customers in the commercial segment, an increase of 69% year-on-year and 19% quarteron-quarter, accelerating from 55% year-on-year in the previous quarter. Interestingly, Palantir is also successfully expanding beyond its US backyard.

As has been the case since the launch of AIP just over a year ago, Palantir is continuing to witness elevated interest and high demand with management saying ‘continued interest is loud and clear’.

Seeding the demand are Palantir’s AIP bootcamps, which bring potential customers and developers together for intense teach-ins to demonstrate what AIP can do for them.

Palantir had completed 560 bootcamps across 465 organisations by February 2024, tacking on an additional 450 organizations in the months since.

As one example, a leading utility company signed a seven-figure deal just days after completing a bootcamp, Palantir said. Another customer immediately signed a paid engagement after just one day of their multi-day bootcamp and then converted to a seven-figure deal three weeks later.

‘We have seen Palantir’s quarterly deals accelerate following AIP’s launch, but we have also seen a larger proportion of deals on the smaller end, between $1 million and $5 million,’ said IO Fund’s Kindig.

SIGNIFICANT CHALLENGES

There are challenges to deal with, not least the admission from Palantir itself that its AIP sales

Chart: Shares magazine • Source: Stockopedia

PALANTIR Q2 FY24 INCOME STATEMENT

Source: Quaterly results, App Economy Insights

execution is far from optimal. ‘We are good at educating customers on what is the art of the possible, and then some portion of those customers buy it. So, I expect as we get better and better at that, our numbers will increase,’ said Alex Karp.

‘But it is really early days. We’re not flawlessly executing on our sales motion.’

Europe presents another possible headache. About 16% of Palantir’s business is in Europe but the region is ‘gliding towards zero percent GDP growth over the next couple of years. That is a problem for us. There is no easy remedy for that.’

Then there’s the battle to change the narrative around the company, seen by some as the face of Big Brother, gobbling up individuals’ private data. This became evident following a public backlash from some quarters after Palantir was awarded a £330 million NHS England contract to develop a new patient data platform.

the challenges it faces, in time. But with the stock priced for perfection, don’t expect smooth sailing.

Full year 2024 (to Dec) revenue estimates range from $2.68 billion at the low end to $2.80 billion on the high end. ‘That’s about 4.4% higher than Palantir’s guidance, suggesting analysts are expecting business momentum to accelerate each quarter with a beat and raise,’ says Kindig.

Looking further out, Stockopedia has the stock trading on a 12-month rolling PE (price to earnings) multiple of 79, a hefty premium to other leading software stocks: Salesforce (CRM:NYSE) and Microsoft (MSFT:NSASDAQ) trade on rolling PEs of 25 and 31 respectively.

Palantir’s earnings growth is seen around 22% in 2025. If that pace were to dip below 20%, the stock’s substantial premium could quickly be whittled away.

Palantir only turned an annual net profit for the first time in 2023 so it is early days and there seems no fundamental reason why it cannot overcome

By Steven Frazer News Editor

Summer sell-off encourages savvy investors to buy at cheaper prices

Not

everyone panicked when

markets tanked in July and August

Anyone lucky enough to have enjoyed a long summer holiday and focused on the beach rather than their portfolio might not have noticed the recent jolt in global stock markets.

While the second half of July was a miserable time markets amid fears of a US recession, the scale of the subsequent rebound has been remarkable.

Glance at your portfolio now and you might only see a small dent. There is certainly none of the panic that gripped markets in July, and the VIX measure of market volatility has more than halved since spiking in August.

The S&P 500 index of US shares even registered its best week of the year, rising 3.9% for the five days to 16 August 2024.

While an investor who held their nerve and did nothing with their portfolio might now be glad of their inaction, what about those who felt compelled to transact in their ISA or SIPP because share prices were moving fast?

TIMING THE MARKET

A few nimble-footed investors might have been

lucky enough to lock in profits before the sell-off accelerated and then buy back at a cheaper level, but they will be few and far between.

In reality, timing the market correctly is extremely tricky and inevitably some investors will have sold at the height of the market panic and then seen markets rebound and bought back at a higher level. That is not sound investment practice.

To find out how investors behaved during the summer market whirlwind, AJ Bell analysed nonadvised customer transactions across the peak to trough (10 July to 7 August) for the Nasdaq Composite, an index of US stocks with large exposure to the big technology names which have helped drive markets in recent years.

Admittedly, this is a brief period, and investors should judge their investments over years not months, but that said the data does provide an interesting snapshot of how investors were thinking during a time of market stress.

RAPID SELL-OFF

The Nasdaq fell by 13% during the sell-off in July and August, a large drawdown in such a brief

period by historical standards.

From late 2023 through July 2024, investors had been content with the idea inflationary pressures would ease and lead to interest rate cuts, particularly in the US. This was the idea that ‘good news’ would encourage the Federal Reserve to reduce the cost of borrowing as there was no reason to keep it high.

Most investors probably had not considered a scenario where central banks might have to cut interest rates to revive the economy because businesses were worried, labour markets were weakening and spending from corporates and consumers had waned.

The realisation we might be heading towards a state of peril meant the narrative was flipped on its head, implying ‘bad news’ would drive interest rate cuts.

Stirring investors into a panic during the summer was gloomy economic data which supported this ‘bad news’ scenario.

Between 10 July and 7 August, the biggest number of stocks sold by AJ Bell customers were a mixture of the best-performing shares of recent years, including Nvidia (NVDA:NASDAQ) and RollsRoyce (RR.); high-yielding UK names which have been staples of many pensions and investment accounts, such as Lloyds (LLOY) and British American Tobacco (BATS); and more speculative names which have been popular among individuals who regularly trade in and out of the market, such as Microstrategy (MSTR:NASDAQ) and Ocado (OCDO).

There is a certain logic behind these stock choices. Faced with a gloomier backdrop, it is natural to think first about locking in gains from shares which have done well, then about trimming positions in names which might represent a large part of your portfolio, and finally stepping away from higher-risk names when the market goes into full risk-off mode.

Vanguard S&P 500

Chart: Shares magazine • Source: LSEG

TAKING ADVANTAGE OF CHEAPER PRICES

Two of the most widely-sold stocks during the 10 July to 7 August period were also among the biggest net buys, namely Nvidia and Vanguard S&P 500 ETF (VUSA), a passive fund which tracks specific parts of the US stock market.

The real nugget from the data was the number of people buying these specific stocks was several multiples of those selling in all three instances.

In the case of the Vanguard S&P 500 ETF, six times more AJ Bell customers bought the stock than sold it which implies savvy investors took a long-term view and pounced on the opportunity to buy at a cheaper price.

However, there is a much more interesting story once you delve deeper into the transaction trends. The ‘net buys’ figure aggregates the total number of buys and sells for a particular stock. A ‘net buy’ is when more people have bough the stock than sold it, while a ‘net sell’ is the opposite.

Fruitful investment decisions can happen when investors go against the crowd and buy when broad market sentiment is weak. This strategy doesn’t always work out, but history suggests it can be a wise move if nothing has changed in terms of the core investment case for a stock.

It takes nerve to deploy more money into the markets when the headlines are negative, but there is merit in forming an investment plan and sticking to it.

DISCLAIMER: AJ Bell, referenced in this article, owns Shares magazine. The author (Dan Coatsworth) and editor (Tom Sieber) own shares in AJ Bell.

WATCH RECENT PRESENTATIONS

1Spatial (SPA)

Claire

Milverton, CEO

1Spatial is a global leader in providing Location Master Data Management (LMDM) software and solutions, primarily to the Government, Utilities and Transport sectors.

Cake Box (CBOX) -

Mike Botha, CFO & Sukh Chamdal, CEO

The company generates revenue from the sale of goods and services. Geographically, it derives revenue from the United Kingdom. All of our products are 100% egg free. The founders of Eggfree Cake Box follow a strict lacto vegetarian diet, and that is how they came up with idea for the company.

Karen Cockburn, Chief Financial Officer

Impax Asset Management Group (IPX)

Impax Asset Management Group offers a range of listed equity, fixed income and private markets strategies. All strategies utilise the firm’s specialist expertise in understanding investment opportunities arising from the transition to a more sustainable economy.

Emerging markets outlook

Sponsored

How emerging market small caps compare with their larger counterparts

Examining performance, valuation and sector weightings for developing world minnows versus giants

Emerging markets small caps have outperformed recently

Shares magazine • Source: LSEG

Some of the big names in emerging markets like Taiwan Semiconductor Manufacturing Company (2330:TPE) and Chinese internet giant Alibaba (BABA:NYSE) will be well known to investors but there is a whole gamut of listed companies running all the way up and down the market value spectrum in the developing world.

As the chart shows, the MSCI Emerging Markets Small Cap index has outperformed the broader MSCI Emerging Markets benchmark over recent times. According to MSCI, the annualised total return over the last five years from the former is 10.3% (as at 31 July 2024) compared with just 3.4% for the latter. The small-cap emerging markets index has also done better than the 8.5% five-year annualised total return from the global MSCI ACWI Small Cap index.

The average forecast price to earnings ratio for MSCI Emerging Markets Small Cap is higher than the broader index at 13.5 times versus 12 times although they trade on a lower price to book at 1.55 times versus 1.79. The dividend yield on offer from MSCI Emerging Markets is a smidge higher than its small-cap counterpart at 2.7% against 2.3%.

China has a significantly lower weighting in the small cap index, which is dominated by India, and there is a notably lower allocation towards the technology and financial sectors.

Chart:

Sponsored by Templeton Emerging Markets Investment Trust

Emerging markets: small-cap outperformance, second quarter earnings and rates outlook

Three things the Templeton Emerging Markets Investment Trust team are thinking about today.

1.

Rotation into small caps: Smallcapitalisation (small-cap) stocks in emerging markets (EM) rose in July but performed in line with large-cap peers. In the second quarter (Q2) there was a pause in their outperforming trend. The likely catalyst we see for small caps to resume outperformance centres on increased conviction that central banks will cut interest rates in the coming months as inflationary pressures ease. (Japan is the exception to this trend—raising rates at its most recent meeting). Historically, lower interest rates have benefited small-cap stocks to a greater degree than their large-cap peers, as the former tend to have higher financial and operating leverage.

2.

Earnings season: The Q2 earnings season is in full swing, with South Korea and Taiwan leading the way in beating expectations. This upswing is due in part to a low base for comparison in the year-earlier period, but it also reflects the recovery in the heavilyweighted semiconductor industry group. The consensus expectation for the EM earnings growth rate in 2024 is 18% reflecting the recovery in the technology sector and the contraction in earnings in 2023, which declined 9%.

3.

Interest-rate outlook: Central banks have adopted a data-dependent stance on the probability of interest-rate cuts. Investors are expecting dovish inflation data in the United States and the euro area to act as the data catalyst for rate cuts starting in September 2024. The prospect of lower interest rates has weighed on the US dollar over the past month; a weaker dollar is usually positive for EMs. However, weakness in

the Chinese yuan has weighed on equity markets as investors fret about the impact of a weaker yuan on the competitiveness of EM exporters outside

Chetan Sehgal Singapore

Portfolio Managers

Andrew Ness Edinburgh

The best and worst performing investments of the cost of living crisis

It’s now three years since the cost of living crisis began to grip the nation. In August 2021, CPI inflation jumped to 3.2%, up from 2% in July of that year. It then climbed all the way up to a peak of 11.1% in October 2022 before gradually, and painfully, falling back to current levels.

Consumers are undoubtedly still finding things hard after such a big price shock, but the worst now looks firmly in the rearview mirror. The inflationary crisis had a profound effect on the savings and investment landscape, and looking back on performance over the last three years, it’s clear some investments have helped investors grow their wealth in the face of rising inflation, while others have capitulated in its presence.

GOLD AND BITCOIN

case for bitcoin relies on it being adopted by consumers, businesses and investors, which is still a highly speculative snapshot of the future.

As ever gold remains worthy of consideration as a portfolio diversifier because it behaves differently to other asset classes, but it shouldn’t make up more than 5% to 10% of your portfolio at most. While gold is known as a safe haven, it is volatile, and despite having a reputation for being an inflation hedge, it has endured long periods of below inflation returns. Meanwhile those who wish to take a punt on bitcoin should do so with only a small amount of money which they are willing to lose in its entirety.

CASH AND GILTS

Gold in particular has made good on its promise as an inflationary hedge over the last three years, carving out a healthy real return of 24.8% for investors (see table). That’s despite rising interest rates, which should in theory take the shine off the precious metal. The economic and geopolitical uncertainty of recent years has helped propel gold upwards.

Meanwhile central banks have been attracted to gold because it’s liquid, carries no credit risk, and is free from any geopolitical interference.

Gold has also trumped bitcoin over the last three years. While some may view Bitcoin as a store of value or an inflation hedge, the wild swings in the price of the cryptocurrency suggest it can’t be relied on to fill either role. In the short term, the US presidential election may exert a gravitational pull on bitcoin now Donald Trump has thrown his weight behind crypto. The longer-term investment

It will perhaps come as a shock to learn that against a backdrop of rising interest rates, the average Cash ISA has registered a negative real return of -12.0% over the last three years, meaning £10,000 saved would now be worth £8,802 after accounting for inflation.

That’s partly because cash rates have only risen gradually, and partly because not all accounts are offering competitive rates. Inflation has also provided a high bar in the last three years, which even the most competitive current rates wouldn’t have hurdled.

Now inflation has become more temperate, the best cash rates are offering an inflation-beating rate of return, but for long-term holdings savers are likely to get a better return from the stock market. Data from Barclays shows that over a 10-year holding period, UK stocks have beaten cash over 90% of the time.

Among other supposedly safe assets, gilts were big losers from the inflationary spiral. Low interest rates and QE pushed up government bond prices

Gold, bitcoin and stocks have outshone cash by a distance

Personal

Investment returns over the last three years

3 year total return % £10,000 invested

100 TRACKER (iShares Core FTSE 100 ETF)

STRATEGY (Vanguard LifeStrategy 60% Equity)

(FTSE Actuaries UK Conventional Gilts Index)

Total return in GBP to 12 August 2024, CPI and cash returns to July 2024

for over a decade, priming the gilt market for a big spill. In real terms gilts have lost over a third of their value in the last three years. This has had knock on effects on diversified strategies which invest in gilts such as 60-40 funds and mixed asset funds more generally.

The pain has been particularly acute and untimely for those approaching retirement in life-styled pension schemes, which hedge against annuity rate movements by investing in longdated bonds. The typical annuity-hedging fund has lost almost half its value in real terms over the last three years, with £10,000 invested now being worth £6,306, or £5,246 after accounting for inflation. Annuity rates have risen by a similar amount but that’s cold comfort if, like 90% of retirees, you’re not buying an annuity with your pension pot.

GLOBAL AND UK SHARES

Both the global and domestic stock market have managed to stay ahead of inflation over the last three years, which given soaring price rises is no mean feat. The FTSE 100 in particular has stood up well, and its performance is in line with the global stock market. This isn’t an entirely congruous result seeing as the UK stock market has been a laggard on the international stage for a while now, but the inflationary nature of the last three years has actually helped large cap UK stocks regather some lost ground.

That’s partly because the FTSE 100 contains a large dollop of oil and gas companies, which have benefited from higher energy prices. The FTSE 100 also has more jam today stocks which prospered in the market rotation that took place when inflation started its ascent, eroding the value of more distant cash flows and the appeal of jam tomorrow companies.

The recent AI-fuelled technology rally might well have banished memories of 2022, but in that calendar year the S&P 500 fell by 8% in sterling terms while the FTSE 100 eked out a 4.7% return, an uncharacteristically favourable performance wedge for the UK stock market.

Overall, these performance figures show the inflationary crisis interrupted trends which had been going on since the aftermath of the financial crisis, in particular puncturing the invulnerability of technology stocks and bonds. The tech sector has since reasserted its dominance, but bond yields remain much higher than they were. These yields are much more normal by historic standards though, and while the increase has been painful for bond holders, these assets now at least offer a reasonable level of return for those looking for income in the here and now.

By Laith Khalaf AJ Bell Head of Investment

2024 at 18:00

ANGLE (AGL)

ANGLE is a world-leading liquid biopsy company commercialising a platform technology that can capture cells circulating in blood, such as CTCs, intact living cancer cells, even when they are rare in numbers, and harvest the cells for analysis. ANGLE’s cell separation technology is called the Parsortix system and is the subject of granted patents in multiple jurisdictions.

ENSILICA (ENSI)

EnSilica is a leading fabless chipmaker focused on custom ASIC for OEMs and system houses, as well as IC design services for companies with their own design teams. EnSilica has world-class expertise in supplying custom RF, mmWave, mixed signal and digital ASICs to its international customers in the automotive, industrial, healthcare and communications markets.

JP MORGAN ASIA GROWTH AND INCOME

JPMorgan Asia Growth and Income (JAGI) provides access to the Asian equity market and targets predictable quarterly income without compromising its focus on growth. Managed by a locally based team of investment experts to provide access to Asia’s fast growing markets and benefits from our long experience in the region.

MENHADEN RESOURCE EFFICIENCY (MHN)

Menhaden Resource Efficiency is a UK-listed investment company that seeks to generate long-term shareholder returns, by investing in businesses and opportunities, delivering or benefitting from the efficient use of energy and resources.

What could happen with oil prices and why investors should care

ExxonMobil predicts demand for crude will be unchanged by 2050

The recent escalation between Israel and Lebanese militant group Hezbollah offered the latest reminder of what a tinderbox the Middle East is right now and the implications that has for oil prices.

The black stuff moved back through $80 per barrel after a period of weakness, offering a reminder of why forecasting oil prices is often a fool’s errand.

Nonetheless, there are plenty of professionals who are willing have a go. Analysts at Bank of America reckon oil prices will dip a little from the $83 per barrel they averaged across 2023 and 2024 (to date) to around $80 per barrel in 2025. Although this prediction is heavily caveated.

‘There are plenty of unknowns. First, Middle East tensions could drive prices much higher if volatile geopolitics lead to energy infrastructure damage. Second, our central scenario encompasses lower US interest rates, a weakening dollar, and China stimulus heading into 2025. This is a positive cyclical macro backdrop that should lend support to oil prices. Third, energy prices are already cheap relative to history, particularly when adjusted for inflation, and oil is cheap versus other thermal fuels.’

There are several reasons why a move higher in oil matters. Most broadly, in global economic terms, a high oil price acts as a tax on growth as businesses and consumers bear the financial impact of higher energy prices.

You might, or might not, get the same level of GDP but it will come at a higher cost.

It is also important for investors

who have exposure to the FTSE 100, given the continuing heavyweight status of BP (BP.) and Shell (SHEL). But the energy transition will change all this right? As the world weans itself off the black stuff this kind of volatility will be a thing of the past. Not according to ExxonMobil (XOM:NYSE). It’s obviously a partial viewpoint but the US oil giant argues pretty robustly that crude demand will actually be virtually unchanged by 2050 and that if industry investment is curtailed it will result in a big energy price shock.

After the surge in oil and gas prices following the invasion of Ukraine in 2022, Western governments are increasingly cognisant of the risks associated with such a shock and the inflationary pressures this could help to unleash.

In global economic terms, a high oil price acts as a tax on growth as businesses and consumers bear the financial impact of higher energy prices”

Obviously, environmental concerns will come into play too but long-term thinking isn’t always a strength of politicians looking at four or five-year election cycles. All told, investors may well have to keep an eye on oil prices for some time to come.

What

happens

if I name one of my daughters as a beneficiary of my SIPP and she lives abroad?

Helping with a question around leaving pension funds to someone outside the UK

I’m over 75 and have a SIPP. My beneficiaries are my daughters, one who has a SIPP already, and one who doesn’t as she lives in France.

So, when I die, the daughter based in the UK can receive her share in her SIPP.

Can you tell me what happens to the other daughter’s share, the one who lives in France? Could she open a SIPP with a UK provider to accept the proceeds, and hence keep the tax benefits on growth. Or how is it paid to her in France?

John

Rachel Vahey, AJ Bell Head of Public Policy, says:

The rules around whether foreign-based individuals can set up, and/or accept payments from SIPPs in the UK can be complicated.

Let’s start with some basic groundwork. When someone dies, their dependants or those they have nominated to receive inherited pension pots – their beneficiaries – usually have three options. They can take the money as a lump sum; they can set up a beneficiary’s drawdown plan; or they can buy an annuity with the pension pot.

If the beneficiary lives abroad, then the options open to them will depend upon the pension provider or pension scheme’s rules and terms and conditions.

If we first consider setting up a beneficiary’s drawdown plan – in theory, the pension tax laws generally allow anyone to set up a UK pension plan. But in practice, it may not be as simple. Many pension providers’ terms and conditions will have restrictions. So, it’s worth checking with the individual provider.

For example, many pension providers will simply not allow any non-UK residents to set up a SIPP.

This is because the pension contract is between the pension provider and the individual, and the financial services regulator – the FCA – requires that the provider is satisfied that it’s meeting the regulatory requirements of the specific country in which the individual is living.

WHAT HAPPENS IF THE SIPP PROVIDER WON’T ACCEPT AN APPLICATION

If the SIPP provider won’t accept an application, then the beneficiary may want to transfer the inherited pension pot to another UK registered pension scheme that can accept an inherited drawdown transfer for someone living where the beneficiary lives. Or they may consider becoming a member of a qualifying recognised overseas pension scheme (QROPS), if they can both find one which is appropriate for where they live and one that accepts transfers of inherited drawdown transfers.

But in practice, many beneficiaries living abroad will probably be left with the option of accepting a lump sum payment (without setting up a SIPP) and lose the flexibility of being able to take an income from the inherited pension as and when it suits them.

Ask Rachel: Your retirement questions answered

How any lump sum is paid to them again depends upon the pension provider. Theoretically, the lump sum could be paid directly to a bank in the beneficiary’s country of residence in the local currency using the Transcontinental Automated Payment Service (TAPS), or via a cheque in pounds sterling, or paid in pounds sterling into a UK bank account.

But in practice the options available depend on the provider. Pension providers may insist on only paying to a UK bank account. This is for practical reasons; payments overseas require more handson administration and can be time consuming. But providers’ decisions can also be related to helping stop money laundering and the worry foreign bank accounts may be used for that reason.

If a pension member dies after the age of 75 then any payments made to their beneficiaries will be taxed as earned income.

A beneficiary living abroad may be a non-UK taxpayer, so they may be eligible to receive their UK pension without deduction of UK income tax.

Money & Markets podcast

However, in practice the UK tax will often be deducted before the lump sum is paid and the beneficiary will have to reclaim the tax.

As you can see this is a complicated area. You and your daughter may want to speak to your pension scheme as well as a specialist tax adviser who can help you understand the options, and how any inherited pension money can be paid to your loved ones. Or you may want to consider an alternative way of passing on wealth when you die.

DO YOU HAVE A QUESTION ON RETIREMENT ISSUES?

Send an email to askrachel@ajbell.co.uk with the words ‘Retirement question’ in the subject line. We’ll do our best to respond in a future edition of Shares. Please note, we only provide information and we do not provide financial advice. If you’re unsure please consult a suitably qualified financial adviser. We cannot comment on individual investment portfolios.

WHO WE ARE

EDITOR: Tom Sieber @SharesMagTom

DEPUTY EDITOR: Ian Conway @SharesMagIan

NEWS EDITOR: Steven Frazer @SharesMagSteve

FUNDS AND INVESTMENT

TRUSTS EDITOR: James Crux @SharesMagJames

EDUCATION EDITOR: Martin Gamble @Chilligg

INVESTMENT WRITER: Sabuhi Gard @sharesmagsabuhi

CONTRIBUTORS:

Dan Coatsworth

Danni Hewson

Laith Khalaf

Laura Suter

Rachel Vahey

Russ Mould

Shares magazine is published weekly every Thursday (50 times per year) by AJ Bell Media Limited, 49 Southwark Bridge Road, London, SE1 9HH. Company Registration No: 3733852.

All Shares material is copyright. Reproduction in whole or part is not permitted without written permission from the editor.

Shares publishes information and ideas which are of interest to investors. It does not provide advice in relation to investments or any other financial matters. Comments published in Shares must not be relied upon by readers when they make their investment decisions. Investors who require advice should consult a properly qualified independent adviser. Shares, its staff and AJ Bell Media Limited do not, under any circumstances, accept liability for losses suffered by readers as a result of their investment decisions.

Members of staff of Shares may hold shares in companies mentioned in the magazine. This could create a conflict of interests. Where such a conflict exists it will be disclosed. Shares adheres to a strict code of conduct for reporters, as set out below.

1. In keeping with the existing practice, reporters who intend to write about any securities, derivatives or positions with spread betting organisations that they have an interest in should first clear their writing with the editor. If the editor agrees that the

reporter can write about the interest, it should be disclosed to readers at the end of the story. Holdings by third parties including families, trusts, selfselect pension funds, self select ISAs and PEPs and nominee accounts are included in such interests.

2. Reporters will inform the editor on any occasion that they transact shares, derivatives or spread betting positions. This will overcome situations when the interests they are considering might conflict with reports by other writers in the magazine. This notification should be confirmed by e-mail.

3. Reporters are required to hold a full personal interest register. The whereabouts of this register should be revealed to the editor.

4. A reporter should not have made a transaction of shares, derivatives or spread betting positions for 30 days before the publication of an article that mentions such interest. Reporters who have an interest in a company they have written about should not transact the shares within 30 days after the on-sale date of the magazine.

and, as such, are written by the companies in question and reproduced in good faith.

Introduction

WWelcome to Spotlight, a bonus report which is distributed eight times a year alongside your digital copy of Shares.

It provides small caps with a platform to tell their stories in their own words.

The company profiles are written by the businesses themselves rather than by Shares journalists.

They pay a fee to get their message across to both existing shareholders and prospective investors.

These profiles are paidfor promotions and are not

independent comment. As such, they cannot be considered unbiased. Equally, you are getting the inside track from the people who should best know the company and its strategy.

Some of the firms profiled in Spotlight will appear at our webinars and in-person events where you get to hear from management first hand.

Click here for details of upcoming events and how to register for free tickets.

Previous issues of Spotlight are available on our website.

Members of staff may hold shares in some of the securities written about in this publication. This could create a conflict of interest. Where such a conflict exists, it will be disclosed. This publication contains information and ideas which are of interest to investors. It does not provide advice in relation to investments or any other financial matters. Comments in this publication must not be relied upon by readers when they make their investment decisions. Investors who require advice should consult a properly qualified independent adviser. This publication, its staff and AJ Bell Media do not, under any circumstances, accept liability for losses suffered by readers as a result of their investment decisions.

What have been the best-performing AIMlisted stocks in 2024?

Looking at companies from various sectors throughout the year

In this article we discuss how companies that are listed on AIM have performed in 2024, encompassing anything with a market cap of £30 million or more.

WHAT DOES THE DATA REVEAL?

The table shows that not one sector dominates the list of top AIM performers.