STORY page 72

Companies like SpaceX and Blue Origin are leading a boom in America’s space industry. The supply chain that helps them reach orbit has been expanding out of Florida and Texas.

PAGE 16

Green Jobs Boom in 2023: Is the IRA a Leading Factor?

It’s still too early to tell how much of an impact the funds allocated from the Biden administration’s signature legislation have made, but the early signs are promising.

PAGE 20

Permitted Power Capacity Foreshadows Health of Regional Economies

It’s no secret that the United States doesn’t have enough power to go around, though it might be shocking to learn just how few new energy projects are in the pipeline.

PAGE 26

Semiconductors’ fragile relationship with water may be tested

The United States is pushing to become a leader once again in semiconductor production with huge investments. Money’s not a problem, but water might be.

PAGE 32

Top States for Doing Business

Area Development’s annual ranking of the best states for site selectors, as ranked by our panel of expert consultants, has a few surprises in store, and some familiar results.

PAGE 60 Cold Storage: The Next Big Thing in Industrial Real Estate

A recent spike in construction of temperature-controlled facilities is only scratching the surface of what’s on the horizon. But building these projects can be complex.

PAGE 84

What the Latest EPA PFAS Rule Means for Site Due Diligence

A tidal wave of forever chemicals lawsuits is coming, and site selectors must proceed with caution with socalled reopeners.

“One of the basic rules of the universe is that nothing is perfect. Perfection simply doesn’t exist… Without imperfection, neither you nor I would exist.”

Stephen Hawking (1942-2018), famous theoretical physicist, cosmologist, and author.

63 Guest Editorial: Electric Cars and Economic Development

64 The Challenge of Securing Sufficient Electrical Power for Battery Cell Plants

67 Can the UAW Make Substantial Inroads in the Southern States?

70 The Cost of Labor and Workforce Skills Necessary for an Electrified Auto Industry

74 Emerging Markets for Aerospace Production

76 Moonshot: How a Dynamic Space Production Facility Took Off

78 Canada Pushes Its Hydrogen Energy Edge

82 FDI in Canada: Grace

4 Editor’s Note

Pardon our dust. We’re making some changes.

6 In Focus

Data driven site selection rules

8 Frontline

Quantum campus takes shape in Chicago

10 First Person

Scott Kuppermann answers questions about food processing trends

12 Around the Horn

Let’s talk about rail service with a trio of experts in supply chain

94 Ad Index

95 Last Word

Time to audit your real estate portfolio?

Dennis Cuneo helped Area Development arrange coverage of the automotive industry for its annual Auto/Aero special section. Dennis is the owner of DC Strategic Advisors and the former Senior Vice President for Toyota Motor North America. He has served on over 20 fiduciary boards, including two Fortune 500 companies, a regional federal reserve bank, a stock exchange, a major league stadium authority, an automotive think tank, a civil rights museum, and several universities, one of which he chaired. He held gubernatorial appointments in California, Kentucky and Mississippi. Making him the perfect choice for this assignment.

PrintedintheUSA.Copyright2024AreaDevelopment®magazine.Allrights reserved.Nopartofthispublicationmaybereproducedortransmittedin anyformorbyanymeans,electronicormechanical,includingphotocopy, recordings,oranyinformationstorageorretrievalsystem,withoutpermission. AreaDevelopment®magazinedoesnotassumeandherebydisclaimsany liabilitytoanypersonorcompanyforanylossordamagecausedbyerrors oromissionsinthematerialherein,regardlessofcausation.Theviewsand opinionsinthearticleshereinarenotthoseofthepublishers,unlessindicated. Thepublishersdonotwarrant,eitherexpresslyorbyimplication,thefactual accuracyofthearticlesherein,orofanyviewsoropinionsofferedbythe authors of said articles.

I joined Area Development Magazine this year as its fourth-ever editor and will be attempting to fill the shoes of the inimitable Gerri Gambale, which is no easy task. She held this position for nearly three decades! I am truly excited for the opportunity to steer the coverage of corporate site selection and facility planning during such an incredibly exciting time, for economic development and America’s manufacturing sector. Me and the rest of the Area Development team have been busy the past few months making changes to the look of our publication. We hope you’ll notice the updates, which include clean, modern lines and vibrant imagery. Shout out to our superbly talented designer, Victoria Corish, who has brought an artist’s vision to these pages. You’ll see her fingerprints on every page.

One thing that isn’t changing is our commitment to smart, nuanced coverage of site selection and facility planning.

In this issue — which I’ve dubbed the planes, trains, and automobiles edition — we bring you a stellar lineup of thought leaders. To begin with, our esteemed guest editor

2024 EDITORIAL ADVISORY BOARD

Scott Kupperman

Founder KUPPERMAN LOCATION SOLUTIONS

Eric Stavriotis Vice Chairman, Advisory & Transaction Services

CBRE

Brian Corde

Managing Partner ATLAS INSIGHT

Amy Gerber

Executive Managing Director, Business Incentives Practice

CUSHMAN & WAKEFIELD

Alexandra Segers General Manager

TOCHI ADVISORS

Dennis Cuneo

Former Senior Vice President, Toyota Motor North America, Owner

DC STRATEGIC ADVISORS

Publisher Dennis J. Shea dshea@areadevelopment.com

Sydney Russell, Publisher 1965-1986

Events / Business Development Director

Matthew Shea (ext. 231) mshea@areadevelopment.com

Media / Accounts Director

Justin Shea (ext. 220) jshea@areadevelopment.com

Courtney Dunbar

Site Selection & Economic

Development Leader BURNS & MCDONNELL

Stephen Gray President & CEO GRAY, INC.

Bradley Migdal

Executive Managing Director, Business Incentives Practice CUSHMAN & WAKEFIELD, INC.

Brian Gallagher Vice President, Corporate Development GRAYCOR

Marc Beauchamp President SCI GLOBAL

David Hickey

Managing Director HICKEY & ASSOCIATES

Editor Andy Greiner editor@areadevelopment.com

Staff and Contributing Editors

Mark Crawford

Dan Emerson

Steve Kaelble

Mark Schantz

Circulation/Subscriptions circ@areadevelopment.com

Dennis Cuneo leaned on his years of experience and deep network of automotive executives to bring together comprehensive coverage of America’s automotive sector. Tom Taylor adds his expertise on aerospace and defense. Mike Chmura from Chmura Analytics looks at growth in US green jobs. We have a robust discussion on rail infrastructure with Joe Dunlap, JC Renshaw, and Matt Powers. From up north, Gabriel Dion and Marc Beauchamp offer insights into Canadian investments. Scott Kuppermann discusses the current state of food processing, and Courtland Robinson looks at America’s energy project pipeline. Oh, and let’s not forget the annual Area Development ranking of the Top States for Doing Business, which is based on surveys with Americas leading site selection consultants. Have fun reading! Andy Greiner Editor

Chris Schwinden

Partner

SITE SELECTION GROUP

Chris Volney

Managing Director, Americas Consulting CBRE

Matthew R. Powers

Partner ONPACE PARTNERS

Scott J. Ziance

Partner and Economic Incentives Practice Leader VORYS, SATER, SEYMOUR AND PEASE LLP

Chris Chmura, Ph.D. CEO & Founder

CHMURA ECONOMICS & ANALYTICS

Alan Reeves

Senior Managing Director NEWMARK

Production Manager Jessica Whitebook jessica@areadevelopment.com

Web Designer Carmela Emerson

Print Designer Victoria Corish

Business/Finance Assistant Barbara Olsen (ext. 225) olsen@areadevelopment.com finance@areadevelopment.com

Lauren Berry

Senior Manager, Location Analysis and Incentives

MAXIS ADVISORS

Courtland Robinson Director of Business Development BRASFIELD & GORRIE

Dianne Jones

Managing Director, Business and Economic Incentives JLL

Joe Dunlap Chief Supply Chain Officer LEGACY INVESTING

Halcyon Business Publications, Inc.

President Dennis J. Shea

Correspondence to: Area Development Magazine 30 Jericho Executive Plaza Suite 400 W Jericho, NY 11753

Phone: 516.338.0900

Toll Free: 800.735.2732 Fax: 516.338.0100

/

/ SUSTAINABLE SHIPPING

TBy Doug Heinz Manager, Site Selection & Incentives Advisory at Kroll

he landscape of site selection is evolving. Historically, site selection was driven largely by relationships and subjective assessments. However, the advent of data-driven methodologies is transforming how companies identify and evaluate potential locations. This shift towards objective, data-driven site selection is crucial for manufacturing executives seeking to make informed decisions that maximize operational efficiency and profitability.

One of the most significant advancements in data-driven site selection is the development of scoring matrices. These matrices allow companies to evaluate potential sites based on a wide range of criteria, ensuring a comprehensive and objective assessment. The scoring matrix developed by Kroll evaluates criteria at the county level, including property tax, sales and use tax, income tax, land costs, and payroll expenses. By analyzing these factors, companies can ensure that they are considering all relevant aspects of a potential site, rather than relying solely on existing relationships or anecdotal evidence.

Adopting a data-driven approach to site selection offers several key benefits. First, it helps avoid the pitfalls of overlooked communities and counties. Traditional methods often rely on existing relationships, which can result in potentially excellent sites being ignored simply because they are not on the radar of key decision-makers. By using a scoring matrix, companies can objectively

evaluate all potential sites, ensuring that no stone is left unturned.

Second, data-driven site selection enables companies to make informed decisions based on comprehensive data. This approach reduces the risk of unforeseen costs or challenges that can arise from subjective assessments. For example, a site that appears attractive based on relationships might have hidden costs or regulatory challenges that become apparent only through a detailed, data-driven analysis.

Several case studies illustrate the benefits of data-driven site selection. For instance, Kroll’s use of their scoring matrix helped identify a rural community that was well suited for a large company’s relocation project. Despite its rural location, the community’s strong collegiate presence and cohesive local leadership made it an ideal site that might have been overlooked using traditional methods.

Another example is the site selection for a petroleum company. By leveraging data on existing pipelines and operations, Kroll was able to identify the optimal site

for a carbon capture project, demonstrating the power of data-driven selection in making informed decisions.

Data-driven site selection represents a significant advancement in the way manufacturing executives can identify and evaluate potential locations. By utilizing tools like scoring matrices, companies can ensure a comprehensive and objective assessment of all potential sites. This approach not only helps avoid overlooked communities but also reduces the risk of unforeseen costs and challenges, ultimately leading to more informed and profitable site selection decisions. Manufacturing executives are encouraged to adopt data-driven methodologies to stay competitive in an increasingly complex site selection landscape.

This article is part of the Site Selection Playbook series, providing strategic insights and practical advice for manufacturing executives. Published by Area Development Magazine, the series aims to guide businesses through the complexities of site selection to ensure successful project outcomes.

OHIO RIVER MEGASITE

/ HAVERHILL, OH

/ 875 ACRES

/ RAIL SERVED

/ POWER INFRASTRUCTURE

/ RIVER FRONTAGE

/ SUSTAINABLE SHIPPING

The $2.2 million project will transform the former industrial site into a cuttingedge quantum computing facility, advancing Chicago’s role in the tech industry.

By Dan Emerson, Area Development Staff Editor

Chicago’s South Works site once housed the bustling heart of America’s steel industry, but soon it will be home to the future of computing, as PsiQuantum partners with Illinois to build the nation’s largest quantum computing facility on the shores of Lake Michigan.

The 128-acre Illinois Quantum & Microelectronics Park campus, anchored by PsiQuantum, will house a quantum computer containing up to 1 million quantum bits, or qubits, within the next decade, officials said. Currently, the largest quantum computers have around 1,000 qubits.

The project, now in the early planning stage, will be the initial phase of a broader 400-acre master plan for the site. New York-based commercial real estate firm Related Group and industrial developer CRG will co-develop IQMP for anchor tenant PsiQuantum, a leader in quantum computing, using a combination of private financing and funds granted by the state. Chicago-based Lamar Johnson Collaborative (LJC) will be the lead designer, with Clayco as the general contractor for the facility.

Landowner U.S. Steel completed an EPA-supervised remediation after the plant closed in 1992. However, several subsequent efforts to redevelop the site at 8080 S. Lakeshore Drive never came to fruition.

One of those proposals was an estimated $4 billion mixed-use project announced in

2004, with developer McCaffrey partnering with U.S. Steel. The partnership dissolved in 2016 without building anything.

Also in 2016, an Irish developer terminated its agreement to buy the 440-acre parcel and build about 20,000 new homes due to the unknown cost of remediation.

Tim O’Connell, vice president of marketing for CRG, noted that “significant remediation of the site was conducted under prior ownership in the 1990s. As a result of those efforts, a No Further Remediation notice was issued by the Illinois Environmental Protection Agency in 1997 and subsequently reconfirmed, indicating the site met the agency’s requirements for both residential and commercial uses,” O’Connell told Area Development.

Last August, the state of Illinois announced a preliminary $2.2 million grant from the Illinois Department of Commerce and Economic Opportunity toward

“We’ve seen people waking up to the fact that small quantum systems are not going to be useful. You have to build a big system.”

—Pete Shadbolt

environmental remediation of the South Works property, part of a series of state investments in underutilized properties and former industrial sites that are good candidates for redevelopment.

Clayco’s chief growth officer and Chicagoland president, Michael Fassnacht, said the partnership with PsiQuantum represents “a tremendous opportunity for the city of Chicago.” He said it will be a “cornerstone” for advancing the relatively new science of quantum computing.

One of the appealing qualities of the South Works site is its sheer size, officials said, along with its proximity to a quantum computing center at the University of Chicago.

Pete Shadbolt, PsiQuantum’s cofounder and chief scientific officer, told MIT Technology Review, “Just in the last few years, we’ve seen people waking up to the fact that small (quantum computing) systems are not going to be useful.” To correct the errors that inevitably occur in the complex quantum computing process, “you have to build a big system with about a million qubits,” he said.

Quantum computers can perform a wide range of tasks, from drug discovery to cryptography, at unprecedented speeds. A number of companies are working to develop the systems using different methods. Both Google and IBM, for example, make the qubits out of superconducting material. IonQ makes qubits by trapping ions using electromagnetic fields. PsiQuantum is building qubits from photons.

LIGHTHOUSE ROAD

/ GUILDFORD SPRINGS, PA

/ 248 ACRES

/ RAIL SERVED

/ AVAILABLE WORKFORCE

/ POWER INFRASTRUCTURE

/ SUSTAINABLE SHIPPING

Rail shipping is up to seven times more fuel-efficient than trucks. We can help you move more freight and build a better, smarter supply chain.

Explore more than 800 rail-served sites at NorfolkSouthern.com.

We conducted a fascinating discussion with JC Renshaw, Senior Supply Chain Consultant in Savills, Joe Dunlap, Chief Supply Chain Officer at Legacy Investing and Matt Powers, Lead for Site Selection and Supply Chain Strategy Solutions for OnPace Partners, about the current state of rail infrastructure for site selectors. This conversation has been edited for style and space.

Area Development: How does access to rail infrastructure influence the overall cost-effectiveness and efficiency of the supply chain?

Matt Powers: For retail, rail is crucial for transporting materials like lumber for companies such as Home Depot and Lowe’s. While not typically used for e-commerce, regional distribution can benefit from rail. Rising fuel prices make rail an attractive option even for retailers, offering a future-proof solution amidst driver shortages and fuel costs.

Joe Dunlap: Certain goods, especially in e-commerce, are not suitable for rail due to incompatibility with LTL shipping. Rail is often cheaper per mile but not always applicable. It’s important to understand that rail’s cost advantages apply primarily to specific types of freight, not all.

JC Renshaw: Rail has a smaller carbon footprint compared to road transport. Companies tracking carbon usage and aiming to meet sustainability goals find rail advantageous. Using rail addresses carbon footprint reduction and helps overcome transportation capacity issues related to labor shortages.

Joe Dunlap: Electrification of rail is a possibility in the future, enhancing its sustainability benefits. However, even without electrification, rail is more sustainable than trucking due to its lower fuel consumption and emissions.

Matt Powers: Rail reduces noise pollution and traffic, which is significant for communities near distribution centers. Using rail can help companies avoid public relations issues associated with increased truck traffic.

Area Development: What about the environmental and sustainability benefits of rail? Does rail help mitigate delivery delays?

JC Renshaw: Rail reliability varies. Single-railroad routes are generally dependable, but switching between multiple railroads can cause delays. Traffic jams are less of an issue with rail, but capacity issues and chassis availability can still create backups.

Joe Dunlap: For distances over 400 miles, rail can be effective, but switching between railroads over longer distances can introduce delays. Consistent coast-tocoast routes, like LA to the Northeast, tend to be more reliable and cost-effective.

/

/

/

/

Matt Powers: Sophisticated supply chain users can better plan and utilize rail. Smaller users often rely on trucking due to a lack of scale and knowledge. Understanding the nuances of rail transport is crucial for mitigating delays and optimizing logistics.

Q: Are there any recent innovations or trends in rail that our readers should know about?

JC Renshaw: Longer trains are a trend, though they face resistance due to increased wait times at crossings. Development of electric and hydrogen-powered trains is ongoing, though diesel remains dominant. These innovations promise greater sustainability and efficiency in the long run.

Joe Dunlap: The use of IoT and smart sensors for predictive maintenance is increasing. Digital twins are being used to predict and plan maintenance to minimize disruptions. While autonomous trains may not be imminent, automation to prevent accidents is likely to grow.

Matt Powers: Automation and AI are emerging within the industry, making fleet maintenance more automated. Despite perceptions, the rail industry is keeping up with technological advancements. The use of data mining and AI is helping to improve efficiency and safety.

Q: How important is it to collaborate with rail service providers when selecting a site?

JC Renshaw: For volume users, it’s crucial to ensure capacity and infrastructure. Railroads compete for large projects like gigafactories, offering infrastructure and pricing incentives. Effective collaboration with rail providers is essential to secure the necessary capacity and infrastructure.

Joe Dunlap: Understanding which rail lines can have spurs cut into them is vital. Some lines, called expressways, don’t allow for this, affecting site feasibility. Site selectors must work closely with rail providers to determine which locations can accommodate rail spurs.

Matt Powers: Short-line railroads are generally more flexible. Building relationships with both major and short-line providers is important for successful site selection. Developers are increasingly proactive in identifying sites near rail to secure future advantages.

Q: What should an executive in charge of facility planning consider about rail?

JC Renshaw: One pro is cost and risk mitigation compared to other transportation modes. Rail can be more costeffective and less vulnerable to driver shortages. A con is potential delays due to switching yards and changes between railroads. Understanding specific rail route limitations, such as stacking capabilities, is crucial for optimizing logistics.

Joe Dunlap: Flexibility with multiple rail carriers is crucial. A site with dual rail service offers alternatives if one line faces issues. This redundancy can prevent disruptions and provide cost-effective alternatives.

Matt Powers: The pro is the increasing availability of rail-served sites, as developers anticipate demand. The con is the limited and finite nature of these sites. Competition for prime rail-served locations will intensify, making it essential to secure these advantages early.

To read a full, unedited transcript of this conversation and to listen to the audio, visit AreaDevelopment.com.

A ROBUST NETWORK THAT FULLY CONNECTS YOUR SUPPLY CHAIN

/ 800+ RAIL-SERVED SITES

/ SERVICE IN 22 STATES

/ 19,500 MILES OF NS TRACK

/ 250 SHORT-LINE PARTNERS

/ BUILT FOR SUSTAINABLE SHIPPING

/ READY TO POWER YOUR BUSINESS

We offer more than 800 development-ready sites and the expertise to help you grow sustainably with rail. We’re ready to help you build your business for the future. Find your next location at NorfolkSouthern.com.

Area Development interviewed Scott Kupperman about factors affecting food processing site selection, including cost pressures, geographic preferences, financial considerations, automation, labor shortages, and sustainability.

Area Development: Scott, can you start by sharing any industry trends you are seeing that affect food processing related site selection?

Scott Kupperman: As has been the case, companies in this industry must be responsive to consumer demands. These demands are pretty volatile, but typically relate in some manner to cost, convenience, and purchaser benefits of the product. It seems that lately, consumers have been focused on value in a climate of rising prices at points of retail.

Area Development: What are some of the cost pressures which have driven up prices ?

Scott Kupperman: Cost of transportation, fuel, certainly labor, cost to occupy, build or modify a building. All those have continued to go up steadily, and to maintain margins, they have to pass those costs on and do anything they can to remain profitable but still be deemed a product of interest and a good value for the people out there who they’re selling it to.

Area Development: How does this impact site selection?

Scott Kupperman: F&B companies fear large cost fluctuations. They want to be in a location where the cost to occupy and operate, are both predictable and ideally more competitive than other locations

where competition and local factors drive up acquisition and operating costs.

Area Development: Are these concerns affecting the industry’s structure?

Scott Kupperman: what product they’re making, or what subsector of the industry they’re in, companies worry about margins and cost, and that’s affecting where you want to look, and in many cases, decisions that relate to consolidation. Do we consider closing this facility that has become a high-cost and/or unpredictable place to operate, and either adding on to another facility that we feel is better positioned, or maybe opening a new one.

Area Development: Consolidation seems like a big trend how is that impacting site selection?

Scott Kupperman: companies, like Nestlé, Hershey, and PepsiCo, are optimizing their brand portfolios. They’re acquiring companies with synergies and divesting brands that don’t fit growth strategies. Possibly leading to recently

constructed or renovated buildings becoming available in high-cost locations.

Area Development: Can you give an example?

Scott Kupperman: Hershey, for example, has become a big player in popcorn and salty snacks. They’ve invested a lot of money in products and operators that they feel they have expertise and synergy to build up that specific portfolio. They’ve also focused on ways to modify production lines in as little as a week, in order to meet consumer demand. That ability to innovate is crucial.

Area Development: What about smaller companies?

Area Development: What are the impacts of this buying and selling?

Scott Kupperman: There’s a lot of buying and selling and strategizing out there, which in some cases impacts recently constructed or renovated food buildings becoming available. I think it’s tending to happen in higher-cost locations, which is kind of a double-edged sword. You get a new building available, but lies in a higher cost location. You therefore need to evaluate the value proposition carefully for a specific need and client use.

Scott Kupperman: There’s an influx of emerging companies creating innovative products, often moving production from third-party manufacturers to their own facilities to grow market share. Others are looking to put a second facility into their manufacturing network, and take a leap from, say, the West Coast and try to find a location to be closer to population and product growth in other areas of the country.

Area Development: Are there international factors at play as well?

Scott Kupperman: FDI is landing in the US, by companies from Europe or Asia or elsewhere , and are getting some real sales traction here in the US. And they come to the logical conclusion that says we can’t make this product overseas and continue to ship it here. We’ve got to start making it somewhere in the US, because of supply chain, quality control and speed to market, and because our grocery chains and distributors are pressuring us to have production here.

Area Development: Are there particular geographic areas seeing more growth?

Scott Kupperman: The Mid-Atlantic and Southeast regions are popular, largely due to lower costs and demographic trends. These areas offer affordable real estate compared to higher-cost metro areas and have growing, diverse populations, making them attractive for ethnic and foreign product distribution.

Area Development: How are financial aspects influencing site selection decisions?

Scott Kupperman: Smaller companies are very conservative about capital deployment, and have been waiting for construction costs and interest rates to stabilize. However, many are realizing that 3 percent debt isn’t coming back and it’s going to stay around 5 or 6 percent, and current construction costs are likely here to stay.

By Mike Chmura Economist, Chmura Economics & Analytics.

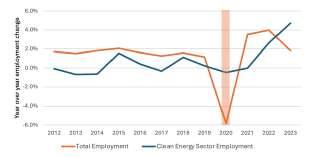

The potential for new, good-paying jobs from investing in a clean energy ecosystem has long been highlighted by proponents of expanding clean energy in America. John Kerry, President Biden’s former Envoy for Climate, famously predicted the energy transition would be the “new industrial revolution.”

While clean energy production and related industries steadily grew in the United States over the past decade, the growth was far from a “new industrial revolution.” Green jobs in the energy sector underperformed the growth of the wider economy in all but two of the last ten years –those being during the COVID lockdowns, and now as of 2023. As of the end of 2023, clean energy jobs grew year over year by 4.7%, compared to 1.8% employment growth for the overall economy. The figure below shows jobs directly involved in clean energy production and transmission/distribution. Other “green” jobs like battery manufacturing for electric vehicles also grew over the past few years.

Using Chmura’s JobsEQ software to dig into these trends, we notice distinct differences between geographies, with a unique mix of states leading the way. Two New England states (Rhode Island and Massachusetts) place in the top 5. These states recently expanded solar and wind projects with the new Vineyard Offshore Wind project beginning construction in late 2021, and the solar market (especially in Massachusetts) continuing its steady growth. Also taking advantage of the fast-growing solar market are southwestern states such as Nevada, Arizona, Colorado, and Texas— all of which made the top 10 for 2023 clean energy job growth. Interestingly, West Virginia was the number 7 state for clean energy growth in 2023, although most of this job growth seems to be concentrated in clean energy support functions rather than in generation.

Breaking this out further by MSA, Table 2 shows the top 10 MSAs for cumulative green energy job growth

#2

In air cargo by weight

There’s no better place to do business than the Bluegrass State ced.ky.gov @cedkygov

In automotive production per capita

In aerospace-related exports

In percentage of workers employed by international companies

Manufacturing by percentage of workforce

Amount invested in new cleanenergy projects announced since IRA passage.”

in 2023. Houston, TX led the way in total job creation, with a net gain of 1,202 clean energy jobs in 2023. Tucson, AZ also had an explosive growth year for clean energy jobs – more than doubling their total. Other large metropolitan areas, like New York and Chicago, round out the top 10, joining Florida, California, Arizona, and Texas metros.

We also see that, within these metropolitan areas, business leaders and researchers credit the IRA with some of these job increases. For example, in their 2023 report, Climate Power found 13 clean energy projects that advanced after the IRA passage in Arizona, with many business leaders crediting the IRA for spurring the investment. Among these projects, LG Energy Solutions resumed plans for its previously paused Arizona gigafactory, the American Battery Foundation announced a $1.2 billion investment for a new gigafactory in Tucson, and after the passage of the IRA, Longroad Energy finally completed financing for a solar generation project.

Similar stories are seen in other states and cities across the country. In Houston, TX (top MSA for clean energy job growth in 2023), SEG Solar and PV Hardware announced new solar projects to meet the demand driven by the IRA.

SEG Solar specifically mentioned that they would be looking to create even more jobs using savings from the IRA tax credits.

Overall, since the passage of the IRA, Climate Power finds that more than $278 billion in new clean-energy related projects were announced nation-wide.

While this “boom” in the green energy economy is welcome news, it is intriguing to question what is fueling this growth and if it is sustainable. On August 16, 2022, President Biden signed into law the Inflation Reduction Act (IRA), which among other features, provided $369 billion in direct grants and tax credits for green and sustainable energy initiatives. These include clean energy production and electric vehicle tax credits all the way down to rebates for new and efficient personal appliances.

On top of the surface-level benefits, the President promised these tax credits would “create thousands of good-paying jobs.”

A year after the IRA’s integration into official U.S. federal regulation, we are already seeing above-average job growth in the green energy sector. Green energy jobs also pay much more than other industries, with the annual wages for green energy jobs averaging almost twice as much as the national average ($130,441 versus $70,183). Other government incentives for green energy include initiatives like the Bipartisan Infrastructure Law (BIL).

Do we have the IRA and other federal incentive programs provided through legislation like the BIL to thank for all this recent growth? Well, given other key drivers in

the clean energy space are not improving, perhaps the IRA is driving a large portion of the boost. Those in the energy industry often cite the decreasing cost of green energy and the increase in Environmental, Social, and Governance (ESG) as promising developments for the proliferation of zero-carbon energy. However, as discussed below, improvements in these metrics have stagnated at best.

For economic feasibility, cost is king, and the cost difference between separate energy technologies is typically measured by the Levelized Cost of Electricity (LCOE). Simply put, LCOE is the average cost to produce one MWh of electricity using a specific technology. The lower the LCOE, the cheaper it is to produce electricity. Over the past decade, core green energy production methods have significantly decreased in price (see figure 2). This decrease includes large-scale solar and wind, which on average has been cheaper to use than natural gas since at least 2016.

However, these cost decreases have stagnated recently, with LCOE estimates indicating increases in price for 2023. While low LCOE for green energy is helpful to industry prospects, it is likely not the core driver of the recent employment surge as costs have stagnated recently.

As for ESG investing, trends here also fail to paint a clear picture for its positive impact on green energy employment. While ESG investing increased 14-fold from 2018 to 2021 in the United States, a down-market year in 2022 decreased the assets under management of ESG funds by 29%. Yet, in that same year, green energy employment grew contrary to what we would expect if ESG investing was a primary factor. While ESG assets under management likely increased along with the overall market in 2023, it is still unlikely this investing trend is a primary driving growth factor.

Ultimately, very few changes in the economy can be attributed to one simple causal factor. Of the three factors discussed above (IRA, LCOE decreases, ESG investment), however, only one is trending in a direction which can explain the increase in green jobs – that being the IRA. In reality, it is likely a combination of a solid economic baseline (aided by low LCOE and a willingness in corporate America to expand green operations) along with the extra financial and regulatory boost which the IRA has provided that is driving the recent above-average employment growth in green energy clusters.

One must question if this employment growth is sustainable. While the majority of IRA funds allocated to green energy have yet to be distributed, it may still be too early to definitively declare the IRA a success for the green energy sector. Nonetheless, the early signs are quite promising.

Diverse energy projects are addressing unique resource and climate considerations, with solar and wind power leading the charge in the transformation of America’s energy landscape.

By Courtland Robinson Director of Business Development at Brasfield & Gorrie

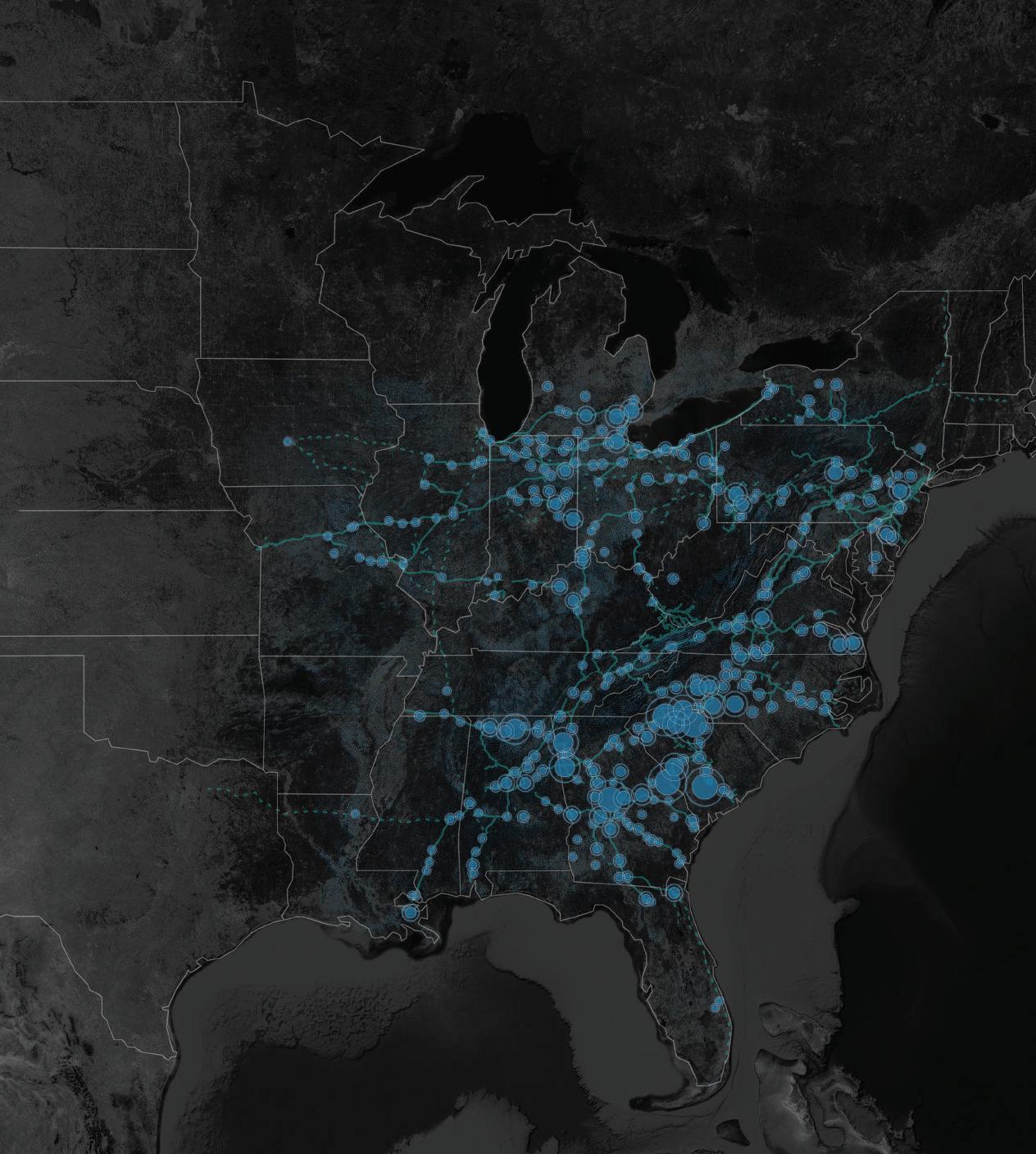

The U.S. electric grid, a trusted engine for economic sovereignty and growth, is struggling to keep pace with the demands of a modern economy. Sputtering along on today’s 1.3 million megawatts (MW) of generation, booming industries plead for the supplementary generation commanded by computational power, superior process design, and electrification. A growing currency in the 21st century economy, investors track the proliferation of new generation across the country – construction projects bound to incite investment and expansion into these contending regions .

Some help is on the way. At the moment, 132,000 MW of new generation capacity projects are either permitted or under construction, according to the American Public Power Association’s 2024 Generation Capacity Update. Projects that could generate an additional 335,000 MW are pending review.

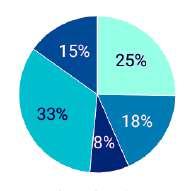

Compelled to reduce carbon emissions and emboldened by advances in distributed energy resources, this new wave of energy projects doesn’t look like its 20th-century counterparts. Much of the new generation capacity under development is for solar energy (51%), followed by wind (33%) and natural gas (7%).

Where are these new projects going? Roughly 75 percent of all capacity either permitted or under construction is going to just four of the six regional authorities, stretching from the Nevada sagebrush, down to the grasslands of Texas, and east to the salty Atlantic coastlines.

The largest of six regional entities given authority by the North American Electric Reliability Corporation and the Federal Energy Regulatory Commission, WECC has the largest share of plants under construction. However, WECC only holds 13 percent of all U.S. permitted generation.

Proposed Permitted

Under Construction

Pending Application

2023 Generation

Montana, Nebraska, New Mexico, South Dakota, Texas, Wyoming, Mexico Arizona, California, Colorado, Idaho, Nevada, Oregon, Utah, Washington Canadian provinces of British Columbia and Alberta.

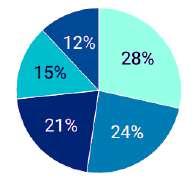

Covering portions or the entirety of these sixteen states on either side of the Mississippi River, SERC has a quarter of all U.S. plants under construction and the second-largest share of permitted plants.

Proposed

Permitted

Under Construction

Pending Application

2023 Generation

Florida, Georgia, Alabama, Mississippi, Louisiana, Texas, Oklahoma, Arkansas, Missouri, Iowa, Illinois, Kentucky, Tennessee, Virginia, North Carolina, and South Carolina

Both SERC and WECC make up most of the capacity under construction in the U.S., but vast amounts of capacity are also planned in ERCOT (Texas), which manages 90% of the state’s electric load. Nearly half of all permitted projects fall within ERCOT, a nod to future capacity hunters that Texas is loading up for the energy arms race.

Proposed

Permitted

Under Construction

Pending Application

2023 Generation

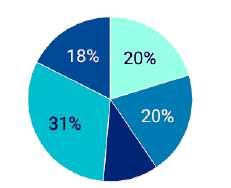

Serving the Mid-Atlantic and Great Lakes within the eastern interconnection, RFC held 23% of all 2023 U.S. Generation. Yet it comes in fourth at 15% of new capacity under construction and only 13% of all permitted plants.

Proposed

Permitted

Under Construction

Pending Application

2023 Generation

Delaware, New Jersey, Pennsylvania, Maryland, Virginia, Illinois, Wisconsin, Indiana, Ohio, Michigan, Kentucky, West Virginia, Tennessee, District of Columbia.

A relic term still recited despite its pervasiveness across the grid, alternative energy is dominating new energy construction projects. Tribute to the pace of adoption, today 66% of plants permitted or under construction are using solar energy technology. The U.S. Energy Information Administration anticipates that solar and battery storage will make up 81% of new U.S. electric-generating capacity this year. Faster and cheaper to deploy, and insulated from the volatility of traditional fuel sources, solar capacity has skyrocketed in most areas. However, the generating capabilities of today’s solar, wind, and battery storage solutions are a mere taste of what data hungry enterprises desire.

Natural gas is the largest source of U.S. generation capacity today (44%) and makes up a significant share of the capacity added over the last decade. While many utilities around the country have signaled an interim dependence upon new gas-fired generation to bridge power deficits, including those associated with coal retirements, these solutions are not as imminent as some would hope, as natural gas generation makes up only 9.5% of all capacity under construction. Even so, discounting the role of natural gas in the context of swelling energy demand would prove myopic. A pillar of the U.S. grid system and trustworthy dispatchable resource under today’s demanding conditions, natural gasfired power generation might soon have its second act.

Don’t call it a comeback – nuclear has been powering roughly 20% of the U.S. economy for decades, and the pros and cons of a nuclear renaissance have been debated for years. That said, there are signs of progress. In June 2024, TerraPower broke ground on the construction of the Natrium Reactor demonstration project, a Bill Gates and GE-Hitachi technology venture claiming the first advanced reactor project to move from design into construction. The project features a 345-500 MW sodiumcooled fast reactor with a molten salt-based energy storage system. Alas, only non-nuclear construction has commenced, the rest pending application approval.

While similar advanced nuclear pronouncements can be found across the U.S., zero U.S. nuclear reactors are under construction today and none have both approvals and funding in place. To further place this in context, there are sixty reactors under construction in sixteen countries around the world. China has twenty-six reactors under construction, while India has seven, Russia four, and the U.K. two.

While many other fuel types are being evaluated in an attempt to wrestle with the pressures of digitization, few energy solutions offer regional planning organizations the requisite deployment and scalability means to overcome both high-voltage transmission constraints and federal approvals in a timely manner

of new generation capacity is either permitted or under construction in the United States.

Brendan Jones President and CEO Blink

We searched for a place that was well connected, bursting with innovation, and aligned with our mission of creating a greener future. Maryland won, hands down.

Middlesex County, NJ, boasts a legacy of innovation, from Thomas Edison’s Menlo Park Laboratory and his 300+ patents to Johnson & Johnson’s global headquarters since 1886. Modern pioneers like Sampled and GenScript Biotech continue this tradition. With robust infrastructure, cutting edge technology, a skilled workforce, a pro-business climate, and comprehensive supply chain support, Middlesex County nurtures a vibrant, diverse economy and thriving business community.

Middlesex County is a top global R&D center, ranking in the top 1% for university-based spending in engineering, geosciences, life sciences, computer science, and physical sciences. Home to Rutgers and Princeton universities, the county’s robust academic foundation supports a thriving life sciences corridor along Route 1, attracting companies like Bristol-Myers Squibb, Novo Nordisk, and Genmab.

By Mark Crawford

tracting over $2 billion in private equity and venture capital investment since 2022.

Food technology. Middlesex County’s vibrant food science industry, encompassing R&D, manufacturing, and distribution, ranks in the top 4% of U.S. counties for food processing. It excels in the flavor, fragrance, and extract markets with a modernized supply chain, employing over three times the national average of food scientists and technologists.

The Office of Business Engagement within Middlesex County’s Department of Economic Development plays a pivotal role in supporting the county’s business retention, expansion, and attraction efforts. In December 2023, Nokia Bell Labs announced its plan to occupy a high-tech, custom laboratory at HELIX 2, an advanced research facility under construction in New Brunswick. “New Jersey has long been home to cutting-edge innovation,” states Nokia Bell Labs. “Nokia Bell Labs is affirming its commitment to the East Coast and New Jersey and upholding our longstanding tradition of groundbreaking research and development in the region.”

Talent drives Middlesex County’s economic development. Workforce-training partnerships with employers build a robust talent pipeline to support growing industries. For example, the RWJBarnabas Health Workforce Partnership offers unique educational pathways for Middlesex College and Middlesex County Magnet Schools students. Leveraging this strong foundation, Middlesex County fosters a favorable business climate and serves as an incubator for innovation.

Life sciences. Middlesex County’s life sciences industry is bolstered by significant investments, including the new $25 million Jack & Sheryl Morris Cancer Center—New Jersey’s first freestanding cancer hospital opening in late 2024. The county’s biopharmaceutical sector ranks in the top 1% nationwide, at-

“Middlesex County is at the forefront of technological innovation and economic growth”

Sho Islam

Autonomous technologies. Middlesex County boasts a high concentration of experts in automation, robotics, AI, and machine learning. To harness this expertise, the county launched DataCity, an urban living lab for smart mobility. In partnership with Rutgers University and the NJ Department of Transportation, DataCity tests autonomous vehicles and advanced navigational software in real-world environments.

“Middlesex County is at the forefront of technological innovation and economic growth,” said Sho Islam, director of the county’s Office of Business Engagement. “Our commitment to fostering a business-friendly environment and supporting industries that drive the future is unwavering. Middlesex County is more than a location— it’s a community where innovation meets opportunity.”

Middlesex County’s Office of Business Engagement assists businesses with relocation to this growing region.

Contact biz@co.middlesex.nj.us or visit www.discovermiddlesex.com/biz for more information.

This article was written for Middlesex County’s Department of Economic Development which sponsored and approved this post.

Exploring the water dilemma in semiconductor manufacturing: how the industry’s growth is increasing demand for a scarce resource and the innovative strategies companies are adopting to manage their water use in water-stressed regions.

By Catherine Tymkiw

Semiconductor manufacturing is having a moment, and with good reason. The global semiconductor market is forecast to top $1 trillion by 2030, compared with a mere $600 billion just three years ago, according to McKinsey & Company. And the United States wants a big chunk of that.

The U.S. CHIPS and Science Act—signed into law in 2022 and aimed at reviving America’s domestic manufacturing sector—has so far resulted in $29 billion worth of deals with eight manufacturers for projects across 11 states. Add the $450 billion of private investments for 80 projects across 25 states inspired by the CHIPS Act, and the United States is well on its way to reclaiming its position as a leader in semiconductor manufacturing.

“America invented these chips, but over time, we went from producing 40% of the world’s capacity to just over 10%, and none of the most advanced chips,” President Biden has repeatedly stated.

That’s about to change. The billions of dollars companies and investors are pouring into this industry is expected to lead to a 203 percent surge in U.S. fabricating capacity by 2032, according to a new report from by the Semiconductor Industry Association (SIA) and the Boston Consulting Group (BCG) entitled Emerging Resilience in the Semiconductor Supply Chain. On top of that, advanced chip production in the United States is forecast to jump 28% by 2032, compared with 0% in 2022.

That will undoubtedly create thousands of new jobs and boost the economy.

But semiconductor manufacturing is a thirsty business—using millions of gallons of water per day—and many of these projects to build or expand facilities are in water-stressed regions in states like Arizona and Texas.

To put it in perspective, one person uses around 80 gallons of water per day, on average. A fabrication plant can use up to 10 million gallons of water per day, depending on the size of the plant and type of chip being produced. That’s nearly equivalent to the water needs of a small city like Santa Clara, California, which has a population of 126,215.

Chipmakers around the world are already consuming as much water as Hong Kong, a city with a population of 7.5 million, according to analysts at S&P Global Ratings.

Advanced chips power everything from the latest iPhone to electric vehicles, medical devices, high performance computing (HPC), and devices powered by Artificial Intelligence (AI). As technology continues to become more sophisticated, demand for more advanced

chips will grow, which, in turn, will lead to an increase in water demand.

Just last year, more than one trillion semiconductors were sold around the world, according to the SIA. And that figure is expected to continue to grow. Having a steady water supply to meet that demand will remain top of mind.

“We view water scarcity as a risk in the coming decade for the tech hardware industry, particularly the water-intensive semiconductor subsector,” the S&P analysts wrote.

That’s because advanced chip production uses ultrapure water (UPW)—highly refined fresh water—to clean and purify wafers. These wafers will typically go through a several-step process and UPW is used each time so the more advanced they become, the more processing they need. Water is also used to cool machines and for general use.

Taiwan Semiconductor Manufacturing Company (TSMC), which makes 90 percent of the world’s advanced chips, reported that the annual capacity for its manufacturing facilities and its subsidiaries exceeded 16 million 12-inch equivalent wafers in 2023.

“The semiconductor sector is on track to increase water consumption by a mid to high-single-digit percent each year, driven by capacity expansion and the demands of advancing process technology,” according to S&P analysts.

According to TSMC’s 2022 Sustainability Report, the manufacturer used approximately 35 billion gallons (132.1 million metric tons) of UPW throughout its global operations in 2022, marking a 21 percent increase from 2021.

TSMC also said it continued to implement four major water saving measures throughout its operations in 2022: reducing facility system water consumption, increasing the wastewater recycling of facilities, improving the water production rate of the system, and decreasing water discharge loss from the system.

Still, the renewed resurgence of water intensive semiconductor manufacturing in the United States begs the question: Where will the water come from?

Take Arizona, for example. Two of the largest manufacturers—TSMC and Intel—are growing their footprints in and around Phoenix, a city that’s not considered a water oasis. But the advantage, say city officials, is that “desert cities know that drought is a constant threat and plan accordingly.” It’s that type of planning that has helped Phoenix make it through every drought without any major water restrictions.

Manufacturers and local municipalities continue to work closely together to address the anticipated increase in water demand and infrastructure needs.

In 2020, TSMC signed a $12 billion agreement to build its first U.S. fabrication plant in Phoenix. In exchange, the city committed to spending $205 million in infrastructure improvements to support the project, comprising three miles of full arterial streets including streets, curb, gutter, sidewalk, streetlights and landscaping, new regional public water infrastructure improvements, and new public wastewater infrastructure improvements.

More recently TSMC announced it was building two more fabs and modernizing existing facilities in Arizona, helped by a $6.6 billion investment under the CHIPS Act.

facilities in New Mexico, expand R&D in Oregon and built two new fab plants in Ohio.

Intel has already started work on its two new fab plants in Chandler, having poured more than 430,000 cubic yards of concrete—enough to fill 132 Olympic-size pools, according to its latest Corporate Sustainability Report. It takes about three years to complete construction on a new plant, according to an Intel fact sheet, so these won’t be coming online for a few years.

But between TSMC and Intel, the demand for water will grow, not only for the fab plants, but also for the surrounding communities. In Arizona alone, that means a lot of water being sucked up from areas already

“The semiconductor sector is on track to increase water consumption by a mid to high-single-digit percent each year, driven by capacity expansion and the demands of advancing process technology.”

The first fab, which is expected to start production in 2025, will leverage 4nm technology and produce 20,000 wafers per month. The second fab, expected to start production in 2028, will produce the most advanced 2nm technology alongside 3nm technology. The third, most recently announced fab, is slated to produce chips using 2nm or even more advanced processes by the end of the decade.

In total, TSMC is investing $65 billion in Phoenix, making it the largest foreign direct investment in Arizona, and the largest foreign direct investment in a greenfield project in the United States.

“By increasing our capacity for leading-edge technology in Arizona, we will enable our customers to unleash innovations across mobile, AI and HPC applications for all industry sectors,” TSMC stated.

Meanwhile, Intel has been in the state since 1979, with four fabs operating and two more on the way. The chipmaker has committed $32 billion to build those new fabs, as well as modernize an existing one in Chandler (near Phoenix), where it will produce advanced logic chips used in a number of different U.S. industries, including automotive, medical device and aerospace. Intel will receive up to $8.5 billion under the CHIPS Act to help fund the Arizona projects, as well as modernize packaging

considered highly water stressed, according to World Resources Institute’s Aqueduct Water Risk Atlas.

“We work very closely with local officials in all the communities in which we operate, including the City of Phoenix Water Department,” said a TSMC spokesperson. The company is focusing on recycling and reclamation at its Arizona site with roughly 65 percent of the water at the first fab plant coming from its in-house recycling systems at startup. The recycled water will be used in air scrubbers and cooling tower systems.

On the reclamation side, TSMC is working toward 90 percent water reclamation by building an advanced water treatment facility to achieve ‘near zero liquid discharge.’ “This means the fabs will be capable of reusing nearly every drop of water back into the facility,” said the spokesperson.

The company says it is always looking for ways to be more efficient about its water usage, which includes wastewater and byproduct treatment. The spokesperson noted that TSMC has invested considerable effort into building a comprehensive wastewater treatment system, a water reclamation system, and a waste material recycling system to reduce water consumption, decrease wastewater discharge and increase overall water efficiency.

Furthermore, as part of its effort to reduce total water usage, TSMC’s discharged water is graded by purity, said the spokesperson with the cleanest being reused in the manufacturing process. The second grade will be used in other ways such as cooling-tower water. And finally, wastewater that cannot be recycled will be discharged to treatment facilities for final wastewater treatment. The spokesperson also noted that all tap water used at TSMC is completely reclaimed every day through layers of recycling, and that each drop of water is used an average of 3.5 times.

Meanwhile, Intel has a goal to achieve net positive water by 2030. Net positive is defined as water returned through water management practices plus water restored to local watersheds for more than 100% of its freshwater consumption.

To meet this goal, the chipmaker is taking a threepronged approach: reducing its water footprint through innovative conservation projects, treating water to reuse within its operations, and working with local communities to restore water to watersheds.

In Arizona, Intel has created 21 water restoration projects that are already achieving net positive water. The chipmaker has also restored 1.7 billion gallons of water and treated more than 14.5 million gallons of water per day at its 12-acre on-site water reclamation facility and the Ocotillo Brine Reduction Facility, a partnership with the city of Chandler.

The Arizona Department of Water Resources has already been investing in water conservation and reuse. In fact, Arizona has already stored nearly 3 trillion gallons of water in underground aquifers should it face a water crunch. That’s enough to supply the city of Phoenix for 30 years. Phoenix, where TSMC is building its plants and not too far from Intel’s Chandler location, is also located near five water sources, including the Colorado River, Verde River, and Salt River. The Colorado River, which starts in Colorado and runs 1,400 miles to the Gulf of California, supplies the state with roughly 36 percent of its water. It should be noted that the Colorado River is also one of the most closely managed and regulated, as well as one of the most water stressed river basins in the world, according to the Water Resources Institute. However, these are widely known issues and, much like your stock portfolio, Arizona’s state agencies have taken a diversified approach to water management. In addition to the Colorado River, Arizonians get water supply from groundwater (41 percent), in-state rivers (18 percent), and reclamation (5 percent).

Earlier this year, the Phoenix City Council announced plans to reopen and expand the Cave Creek Water Reclamation Plant, which was shuttered in 2009 due to an economic slowdown. The plant, which is expected to be operational by the end of 2026, could eventually produce 6.7 million gallons of potable water a day—enough to supply 25,000 households a year.

“Phoenix takes seriously the need to secure our water future and continues to bring new solutions to the table to do so,” said Phoenix Mayor Kate Gallego.

Ohio is another state attracting attention from chipmakers. Intel is investing more than $28 billion to build two new fab plants at a site just outside of Columbus that will produce advanced chips. The Ohio mega site, known as Ohio One, is in the city of New Albany and will span 1,000 acres—enough to accommodate eight plants.

So, where will the water for these new fabs come from? Intel says New Albany will supply the water, which originates from the Hoover Reservoir along Big Walnut Creek. Intel will treat the water onsite at its own water system that will have the capacity to process millions of gallons of water daily and create UPW that will be used to process the wafers as part of the chipmaking process.

Intel plans to take that water, after it’s been used in the manufacturing process and treat it for reuse in multiple ways at its mega site before treating it again to meet approved water quality standards and discharged into the sanitary sewer system, where it will be treated at the Columbus city wastewater treatment plant.

Intel has firmly stated that there will not be any direct wastewater discharges from its manufacturing facilities. The only permissible discharge will be stormwater and even that will be diverted first into retention basins that are designed to manage runoff by storing stormwater and releasing it on a gradual basis to prevent flooding and erosion.

The chipmaker is also investing in a water restoration project near Dillon Lake, located in the Licking River watershed near the chipmaker’s Ohio One campus. The project will convert roughly 90 acres of cropland into a wetland and floodplain treatment plain that will reconnect the lake to the Licking River, reduce sediment and nutrient loading to Dillon Lake. Ultimately, Intel’s

that’s the amount of ultrapure water (UPW) used throughout Taiwan Semiconductor Manufacturing Company’s global operations in 2022, marking a 21 percent increase from the previous year.

share of this project is expected to restore about 27 million gallons of water annually.

“More than 10 years ago, we began to explore how we could better understand and reduce our water footprint. Five years ago, we set a public goal to restore 100 percent of our consumption and became the first tech company to set a companywide water restoration goal,” said Todd Brady, Intel chief sustainability officer and vice president of Global Public Affairs, in a statement.

According to its most recent Corporate Responsibility Report, Intel said it conserved approximately 10.2 billion gallons of water last year in all of its operations and through community collaborations, as well as enabling the restoration of 3.1 billion gallons of water through watershed restoration projects. The chipmaker said it maintained net positive water in the United States and India in 2023 and reached net positive water in Costa Rica and Mexico.

Meanwhile, Samsung, which was awarded $6.4 billion under the CHIPS Act, has plans to build leading edge logic, R&D and advanced packaging fabs in Taylor, Texas, as well as expand its current-generation and maturenode facility in Austin, where Samsung Semiconductor has been operating two fab plants since 1996. With the additional funding, Samsung plans to invest more than $40 billion in the region.

Samsung Semiconductor Chief Executive Kye Hyun Kyung said in a statement that the chipmaker is committed to implementing sustainable water resource management technologies, pledging to boost water recycling rates and purifying discharged water.

“Our water strategy is focused on conserving water in our operations, collaborating with our community and creating programs to proactively prevent pollution and expertly manage wastewater discharge,” said Michele Glaze, Director of Communications, Samsung Austin Semiconductor, adding that the new fab being built in Taylor will have a minimal impact on the environment. “The primary water for Taylor will be groundwater that should not tax the existing surface water sources that municipalities use.”

Glaze said that the city of Taylor will supply the domestic water, which is used for daily personal use such as drinking, food prep and flushing toilets, while private utility firm Epcor will supply the industrial water, which will be used for washing, cooling, processing, and fabricating. In other words, Epcor will be supplying most of the water needed for processing Samsung’s wafers.

It’s not clear how much water Epcor will be supplying but it’s been widely reported that it will come via pipeline from the Carrizo-Wilcox Aquifer in Milam County. The aquifer is the third most important groundwater resource in Texas, according to a report from Texas A&M AgriLife, which also noted that the aquifer’s water table has dropped more than 150 feet over the past several decades as recharge rates appear to have slowed, possibly due to changes in land use that may have created unfavorable conditions.

“The target is to reclaim or reuse 75 percent of the process water within the fabrication facility, with the balance purified and returned to the environment to help sustain the natural water cycle and support the local ecosystem,” Epcor said in a statement.

What about climate change? That’s a wild card that semiconductor manufacturers and the regions in which they are growing are already contending with and will continue to do so well into the future.

“Climate change is testing chipmakers,” noted the S&P analysts, adding that it is already “raising the rate of extreme weather, the frequency of drought, and the volatility of precipitation, limiting chipmakers’ ability to manage production stability.”

As semiconductor processing technology advances, there will be greater demand for water, and particularly UPW. It brings us back to the central question around where will the water come from?

“Water is a critical input to the chipmaking industry. Yet continued access to the resource may increasingly become challenging if droughts and water shortages are more frequent” wrote the S&P analysts.

The Colorado River is a notable example of the unpredictability of the effects of climate change. While the river basin is among the most water stressed in the world, it’s future may not be as dire as some may have thought.

The river supports the water needs of seven states— Arizona, California, Colorado, Nevada, New Mexico, Utah, and Wyoming—and Mexico. The Colorado is also among the most tightly regulated and managed, with a system of dams, reservoirs, and pumps in the lower basin designed to capture and store and supply water.

However, warming temperatures created multidecade drought conditions and raised concerns about more reductions in water flow, according to researchers at the Pacific Institute, a global water think tank.

“The combination of a crippling drought that began 24 years ago, the historic over-allocation of the river’s declining runoff, and climate change have exacerbated a structural deficit—where more water leaves the system than enters it,” wrote Pacific Institute researchers Dr. Christine Curtis, Cora Snyder, and Michael Cohen in a report entitled Pathways and Barriers to Corporate Water Stewardship in the Colorado River Basin.

As state agencies, policymakers and corporations continue to work on water mitigation plans, researchers at the Cooperative Institute for Research in Environmental Sciences (CIRES) at the University of Colorado Boulder suggest there may be less of an issue than previously thought when it comes to precipitation, which feeds into the river flow.

Using various climate modeling and working alongside analysts at other institutions, the CIRES researchers, who published their findings in the May 1, 2024, issue of the Journal of Climate, noted that “precipitation falling in the river’s headwaters region

is likely to be more abundant than during the prior two decades.”

According to their research, which included analyzing data back as far as 1895, precipitation in the headwater region, which provides 85 percent of the water that flows through the Colorado River, should remain high enough to help offset the negative impact of rising temperatures due to climate change.

It’s not just Mother Nature who has a role to play in mitigating water stress.

“Despite the brief reprieve provided by last winter’s exceptional snowpack, we still need all hands on deck, from everyone who depends on Colorado River water, to lean in and help get the system into balance,” noted Curtis, Snyder, and Cohen.

Semiconductor manufacturers are being proactive to ensure they are helping and not hindering the environment in which they operate.

“We found that corporations are pursuing multiple pathways to address water stress, including funding onthe-ground water projects, improving water management in their owned and operated facilities, using their brand to raise awareness about water challenges, and developing innovative products and services,” said Curtis, Snyder, and Cohen. The Pacific Institute researchers held 20 interviews with corporate and non-corporate stakeholders as part of their research.

TSMC, for example, is no stranger to nature’s twists and turns. In 2021, just as the U.S. federal government declared a shortage at the Colorado River for the first time ever, due to drought conditions, Taiwan experienced its worst drought in half a century. TSMC managed to keep its Taiwan operations running without disruption, thanks to having a detailed response plan in place designed to handle water shortages at different stages.

“Increasing TSMC’s resilience against natural events—such as drought—is a regular focus,” said the company spokesperson, noting that TSMC was the first semiconductor manufacturer to receive the highest

certification, known as the Platinum certification, from the Alliance for Water Stewardship (AWS) for its commitment to and implementation of sustainable water management.

AWS, a global membership organization comprising businesses, nonprofits, and the public sector, promotes “the use of water that is socially equitable, environmentally sustainable and economically beneficial.” Achieving an AWS standard signals a company’s commitment to sustainable water management.

Intel was the second to earn Platinum certification from AWS for its Ocotillo, Arizona Campus in Chandler. “With our proactive efforts, we seek to mitigate climate and water impacts,” Intel stated in its Corporate Responsibility report.

Those efforts include nine projects along the Colorado River, four along the Verde River basin and seven others that feed into Arizona. In all, these projects are expected to restore nearly 2.2 billion gallons of water per year to the state, once fully implemented.

Even with all this planning, the relationship between semiconductor manufacturers and water supply remains a fragile one. Apart from Intel’s Ohio facility, the remaining six planned across the United States are situated in watersheds classified as at high- or extremely high risk of water stress, according to an analysis by Josh Lepawsky, a geography professor at Memorial University of Newfoundland and Labrador.

On the bright side, companies like Intel and TSMC “are making impressive progress in water use reduction techniques,” writes Lepawksy. Still, that may not be enough to combat the effects of climate change.

“No matter how dramatic those ductions are, they cannot create a situation in which the water needed for semiconductor manufacturing is simultaneously accessible to other water users,” Lepawsky notes, adding that without a steady, and stable, supply of large amounts of water, there will be no semiconductors and without semiconductors there will be no electronics. Stay tuned.

By Andy Greiner Editor, Area Development

Certain states just have the right ingredients for attracting and nurturing business growth. The 2024 Top States for Doing Business rankings are in, and guess what? The Southern states are shining bright once again.

The Top States for Doing Business know a thing or two about creating an attractive business environment. The top states closely manage their taxes and incentive programs, keep their labor force fresh, trained and accessible and maintain infrastructure like energy and water. They’re also responsive to business needs and to changes in climate.

Area Development’s Top States for Doing Business results are derived from a detailed survey

of expert consultants, and shed light on what makes a state a great place for businesses to thrive. We surveyed smart individuals across a range of 14 key questions, including overall cost of business, to tax incentives, availability of energy and water, climate resilience, workforce and site readiness.

Join us as we celebrate the states that are leading the way and analyze why they are making such a big difference in the business world.

For the eleventh consecutive year, Georgia claims the top spot, a testament to its robust pro-business environment. The Peach State›s consistent performance across various categories makes it a perennial favorite for businesses looking to expand or relocate. Georgia›s ability to sustain its leadership position speaks volumes about its strategic investments in infrastructure, education, and policy frameworks that foster business growth and economic resilience.

A key factor in Georgia’s sustained success is its nationally acclaimed workforce development program, Georgia Quick Start. Offered through the Technical College System of Georgia, Quick Start provides customized training for new and expanding businesses, particularly in manufacturing, biotechnology, and information technology. This program has been pivotal in attracting companies that require techsavvy workers with specific skills, bolstering the state’s competitive labor market.

Georgia’s logistics and infrastructure capabilities are another major contributor to its top ranking. The state is home to the world’s

busiest airport, Hartsfield-Jackson Atlanta International Airport, and the fastestgrowing container port in the nation, the Port of Savannah. These assets, combined with a robust road and rail network, enable efficient movement of people and goods across the state and globally. This strategic advantage supports a wide range of industries and enhances Georgia’s appeal as a prime business location

Additionally, Georgia’s favorable cost of doing business, characterized by competitive tax rates and incentives, makes it an attractive destination for companies. The state’s business-friendly policies, coupled with its commitment to maintaining a low operational cost environment, create an ideal climate for business growth and investment

The overall cost of doing business is a critical factor for companies when choosing a location. States that offer a favorable cost environment, including low taxes, affordable labor, and competitive utility rates, are highly attractive to businesses. Tennessee ranks first in the overall cost of doing business, thanks to its low tax burden, right-towork status, and reasonable utility costs. The state’s fiscal responsibility

Being recognized as the Top State for Business for 11 years is no accident.

Learn why Georgia’s investments in infrastructure, workforce training, and renewable energy, and much more are just the start of what “partnership” means here.

and business-friendly policies create an environment where companies can thrive with lower operational expenses. Tennessee’s commitment to maintaining a low cost of doing business makes it an attractive destination for a wide range of industries. Tennessee has made significant strides in enhancing its business environment through recent policy changes. The Tennessee Works Tax Act, effective July 1, 2024, includes several tax reforms aimed at reducing the tax burden on businesses. Key changes include transitioning to a single sales factor apportionment method, which benefits businesses with significant out-of-state sales, and the introduction of a $50,000 standard excise

Today, site-seeking companies want to have the greatest inventory of real estate, workforce, infrastructure and incentives during their searches. These are demands that Texas delivers well on given its massive size, diversity and its links to the global marketplace via DFW, The Port of Houston, its new stock exchange (TXSE) coming to Dallas and its links to the space industry via NASA operations in Houston and Elon Musk’s SpaceX in Cameron County.

tax deduction.

Additionally, Tennessee has expanded its property tax exemptions and increased the carryforward period for tax credits, further reducing the cost of doing business in the state. These changes, combined with the state’s commitment to maintaining low utility costs and a favorable regulatory environment, reinforce Tennessee’s position as a top state for business.

Attracting and retaining skilled labor is a cornerstone of any state’s economic success. In 2024, North Carolina leads the pack in this critical category, offering a rich talent pool and exceptional educational institutions. The state’s commitment to workforce development is exemplified by its numerous educational initiatives and a strong network of universities and community colleges.

Georgia, Texas, and Indiana also rank highly in this category, benefiting from strong educational systems and attractive living conditions that draw talented individuals. Georgia’s workforce initiatives,

Texas’ rail and highway linkages to Mexico are also creating new, near-shoring logistics opportunities, especially along the SH 130 Corridor, a national model for “intelligent infrastructure” which links Austin and San Antonio. The Corridor, home to trophy employers like Tesla, Samsung, Toyota, Dell and others, is monitored by drones and equipped with high-speed broadband to minimize accidents and maximize traffic flow and to accommodate

John Boyd, Jr., Principal, The Boyd Company, Inc.

autonomous and hydrogen and EV powered vehicles.

Texas’ tech sector is distinguished by two new federal tech hub designations: The Texoma Semiconductor Hub lead by SMU and the Gulf Coast Hydrogen Hub lead by The University of Houston. UT Austin houses one of the nation’s top-ranked quantum computing programs and Texas A&M RELLIS and the Cyber Command Center at Joint Base San Antonio are both homes to leading cybersecurity centers.

In Arizona, you’ll find the perfect balance of business opportunity and high-quality lifestyle that makes it a top state to live and work. Businesses benefit from pro-innovation policies and business stability. Residents enjoy a reasonable cost of living compared to other major metros and beautiful scenery, all while taxes remain low for everyone. With a highly skilled talent pool and a commitment to future-forward industries like semiconductors, electric and automated vehicles, and battery manufacturing, we’re maximizing our potential for generations to come.

such as the Georgia Quick Start program, provide businesses with access to a welleducated and skilled labor pool, ready to meet the demands of today’s competitive market. Texas, with its vast educational system and workforce development programs, ensures that businesses can find the talent they need.