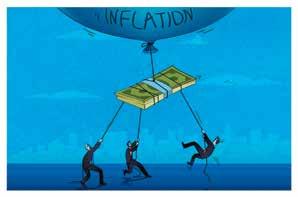

Fearing a Recession, Many Express Misgivings About a Looming Downturn

By Stacy M. Brown NNPA Newswire Senior National Correspondent

In the past, it hasn’t always been clear when a recession loomed, let alone when it has already begun. However, the silver lining now is that, unlike in previous downturns, the Federal Reserve and the U.S. government have already taken action by making critical adjustments to fiscal and monetary policies to regulate economic activity.

“The United States currently has certain interim policies and tools, such as automatic stabilizers like the Earned Income Tax Credit and Unemployment Insurance that are automatically triggered to inject funds into the economy and don’t require any government action to take hold in the event of a downturn,” said Mila Garcia, a finance expert, and the founder of iPaydayLoans.

“And while such programs have proven effective, they should have an even stronger effect with congressional action being taken alongside them. So, if a downturn does hit, we can at least expect to be less vulnerable to economic troubles than before,” Garcia stated.

Amid rising inflation and concerns of a looming recession, many have shared their fears and what America should learn from the pandemic-induced economic downturn.

“Given that Americans are struggling to pay their medical bills, inflations is rising quickly at a pace of 9 percent, and gas and food prices are at all-time highs, this subject is one of the most popular and alarming ones for all Americans,” said Rinor Zejna, a digital public relations specialist.

Zejna offered some findings from research regarding bankruptcy in the United States, noting that one in three Americans struggle to pay medical bills and 750,000 file for bankruptcy each year.

“Medical debt is the number one cause of bankruptcies,” Zejna offered. “And 58 percent of Americans live paycheck to paycheck.”

Home sales and building have dropped substantially over the past year, and consumer confidence has fallen to its lowest point since the pandemic’s beginning.

Still, President Joe Biden remains optimistic.

“Coming off last year’s historic economic growth and regaining all the private sector jobs lost during the pandemic, it’s no surprise that the economy is slowing down as the Federal Reserve acts to bring down inflation,” Biden said in a statement.

“But even as we face historic global challenges, we are on the right path, and we will come through this transition stronger and more secure,” the President continued.

He insisted that the job market remains historically strong, with unemployment at 3.6 percent and more than 1 million jobs created alone in the second quarter.

“My economic plan is focused on bringing inflation down without giving up all the economic gains we have made,” Biden asserted.

“Congress has a historic chance to do that by passing the CHIPS and Science Act and Inflation Reduction At without delay.”

Still, corporations have experienced a decline in sales and earnings during recessions and continue to fear what may come.

According to reports, the average U.S. corporation’s after-tax profit margin is around 16 percent.

In traditional recessions, the rate drops down to single digits.

Meanwhile, those corporations are collectively sitting on a record level of over $4 trillion in cash.

“Companies may have raised these funds during the era of easy money and lowinterest rates over the past decade,” Vishesh Raisinghani wrote for Yahoo Finance.

“Now, this cash is acting as a buffer and could allow companies to retain staff despite the economic slowdown.”

Source: National Newspaper Publishers Association (NNPA)

Community Weekly Report 2 | September 29 - October 5, 2022 Experience Our World of Advertising, Marketing, Media and Communication

FINANCE

Understanding the Real Estate COUNTEROFFER

By Marla Lewis President of the Houston Black Real Estate Association

Many real estate transactions would never come to pass if not for counteroffers. Sure, some deals get done with an acceptance of the original offer, but the fact is that many offers to buy are met with a counteroffer – even when the price is right.

There often is a lot of negotiation before buyers and sellers agree to terms. But you can get through the counteroffer phase with your sanity intact. You just need to know what to expect.

What’s involved in a counteroffer? At its most basic, the buyer submits an offer with specifics on the purchase price, down payment amount, financing, timing, and other business details. After receiving the buyer's offer, the seller sends it back with changes to one or more terms. Counteroffers are simply responses to original offers - whether it's a change to the purchase price or a change of closing or possession dates.

Once a counteroffer has been made, the proverbial ball is in the other party's court; they can accept the counter, make another counteroffer, or not respond at all. And so it goes.

So how do you know if a counteroffer is a good thing? Much depends on what you want. For example, if you're selling and you get an offer with an acceptable price but a closing date that isn't, you can counter with a closing date that suits you.

By the same token, if the offer is lower than you'd like, you can make a counteroffer with an amount that would make you happy. Once everyone agrees, you're on your way to closing day.

Of course, this is a gross oversimplification of only one part of a real estate transaction; there are still plenty of details to take care of between an accepted offer and closing.

offers and contracts aren't binding, and, despite our increasing dependence on them, the same goes for email. A contract must be signed to be enforceable. Having all communications in writing ensures that you have documentation should problems or questions arise.

or the past several years, homebuyers have faced a hot housing market and home prices have risen at what can seem like an intimidating rate. In today's market, it could take a family earning the national median income up to 14 years to save for a 20% down payment plus closing costs, according to U.S. Mortgage

Problems with counteroffers

with counteroffers

It sounds easy enough, but what if there are problems? Many people don't realize that any change to a contract that results in a counteroffer – even if it's as minor as asking to keep the refrigerator – automatically voids previous offers, and the buyer (or seller) can completely ignore the new offer if he desires. In other words, if you submit an offer to purchase a home, the seller comes back with a counteroffer, you counter his counteroffer, and he rejects it, the deal is off. You can't officially go back to his first counteroffer and accept it.

So, before you before make one last counteroffer to try to keep the refrigerator, make sure that appliance is worth potentially losing the deal because a counteroffer gives the other party the power over whether the transaction moves forward or comes to an end.

Some sellers will respond to a buyer's offer not with a counteroffer but with an invitation for the buyer to submit a new offer. The invitation to submit a new offer typically spells out what terms will make a more favorable impression on the seller. This approach keeps the seller's options open to continue to receive offers from other potential buyers.

If you find yourself in the offer-counteroffer stage, make sure you are reachable, so you don't miss out on a house you want or, if you’re the seller, on a potential sale. Finally, be sure to get everything in writing. Verbal

Insurers (USMI). It is understandable that prospective homebuyers might be discouraged and want to wait. However, purchasing a home in an affordable and sustainable way is possible with a low down payment mortgage backed by private mortgage insurance (MI).

Here is how it works.

Private MI helps a borrower with less than 20% down qualify for a home loan and the average down payment for purchasing a home with private MI is 7%, according to USMI. Private MI is typically paid monthly along with the mortgage payment. The benefit is not just that the borrower is able to qualify for a home sooner, but also that the cost is tempo -

Your Realtor is obliged to convey a verbal offer or counteroffer or verbal acceptance to the other party, but a contract is not enforceable until it is in writing and signed by all parties. Once an offer is signed, it is much more difficult for either party to terminate without being penalized.

The bottom line is to communicate with your Realtor and revisit all considerations before making or accepting any counteroffers.

For more information or to find a Realtor, visit HAR.com. And for information about the Houston Black Real Estate Association, please visit HBREAHouston.org.

rary. Unlike government-insured mortgages backed by the Federal Housing Administration (FHA), private MI cancels once a homeowner establishes 20% equity either through payments or home price appreciation. When the private MI is canceled, your monthly mortgage bill goes down.

Let's look at how this would work in today's market.

Consider you want to purchase a $407,600 home, the median sales price for a single-family home in 2022. A 5% down payment is $20,380 versus $81,520 for 20% down. With a 740 credit score at today's MI rates, your monthly MI payment would be about $171. This is included in your monthly mortgage payment and can be canceled, typically after five years once you reach 20% equity in your home.

prices mean homes will cost much more in the coming years. With higher home prices come higher down payments and, thus, more time required to save. Other factors such as rapidly changing interest rates can also make mortgage financing pricier down the line. Purchasing a home sooner allows you to begin building equity and the long-term wealth that comes with homeownership.

As we adapt to this changing world, it is important to know that it is possible to purchase a house now without exhausting your savings. Mortgage financing backed private MI makes this possible, helping borrowers gain access to housing sooner and succeed as sustainable homeowners.

According to USMI, private MI has helped more than 37 million families become homeowners over the past 65 years. In 2021 alone, nearly 2 million families accessed mortgage financing sooner because of private MI.

But is it the right time to buy?

But is it the right time to buy?

The right time to purchase a home is different for everyone, especially nowadays. Rising home

If you're interested in learning more about private MI, check out lowdownpaymentfacts.com to calculate your cost and learn more about your options.

Source: BPT

Community Weekly Report September 29 - October 5, 2022 | 3 Experience Our World of Advertising, Marketing, Media and Communication

Let’s look at how this would work in today’s market.

REAL ESTATE By

F Why Wait? Get Into a Home Sooner With Private Mortgage Insurance REAL ESTATE

d-mars.com News Provider

Here is how it works.

Problems

Community Weekly Report 4 | September 29 - October 5, 2022 Experience Our World of Advertising, Marketing, Media and Communication