6 minute read

References

The authors fnd that having a bubble in equity does not increase the probability that the recession is fnancial. However, when the bubble is in housing, the probability that the recession is fnancial increases. Finally, they analyze whether the economic effects of the crash of an equity bubble and a housing bubble are different. They document that the bursting of equity bubbles does not signifcantly increase the economic costs of recessions. However, the burst of housing bubbles has large and lasting negative economic effects. The crash of housing bubbles has an especially negative effect when the bubble goes hand in hand with excessive debt. For example, given their estimates, in this case, the GDP of the economy may still be 7.5% below the pre-recession level fve years after the onset of the recession.

To conclude, from this historical analysis we highlight three fndings: (i) fnancial crises are worse than normal crises, (ii) housing bubbles are conducive to fnancial crises, and (iii) the bursting of housing bubbles exacerbates the economic costs of recessions. Therefore, if episodes of shortage of assets (or irrational exuberance) are recurrent over time and asset price bubbles are the natural response of fnancial markets, policymakers should guide investors so that the bubble is not attached to houses.

Advertisement

5.2 An ApplicAtion: misAllocAtion in spAin

This fnal section discusses the economic consequences of housing bubbles in the case of Spain. As discussed in Chapter 4, the recent housing bubble in Spain was very large by international standards (see also Fig. 4.1). For example, the cumulative average growth rate of real house prices in Spain between 2002 and 2007 (the peak) was 11%. In contrast, the average growth rate between 2002 and 2006 in the United States was just 6%. Another metric to compare the size of the two bubbles is the peak-to-bottom change in real house prices. In Spain, the fall in real house prices was 42%, whereas in the United States the fall was 27%.

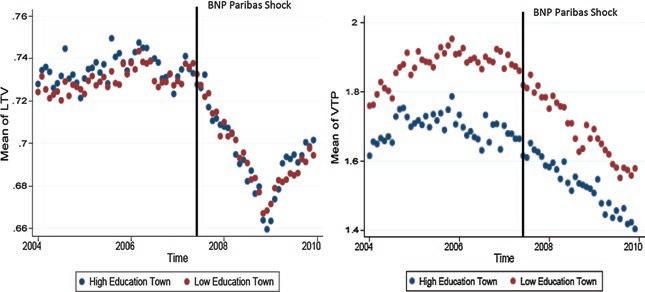

We have emphasized in the previous section the usefulness of considering municipalities to assess the effects of the housing bubble. Basco and Lopez-Rodriguez (2018) built a house price index for all municipalities in Spain between 2004 and 2007. In addition, they developed a measure of land availability based on the housing supply elasticity of

Saiz (2010). This measure is the ratio of potential plot surface over built urban surface in a given municipality before the start of the housing bubble. This measure has the same interpretation as the one developed by Saiz (2010) for the United States. In municipalities with a lot of land available, an increase in housing demand will translate into an increase in the stock of houses but it will not affect house prices. Analogously, if the municipality does not have land available, the increase in housing demand will raise house prices. This interpretation is confrmed in the data. Municipalities with lower land available before the housing bubble (low housing supply elasticity) experienced higher growth between 2004 and 2007. In addition, they document that, during this period, the average house price growth was 16.3% higher in bubbly municipalities. We have used the same terminology as above to label as bubbly and non-bubbly municipality those municipalities in the bottom and top quartile of the land availability distribution, respectively. Thus, during the housing bubble, Spain experienced the same distortion in housing demand, and thereby, house prices as in the United States.

Before we discuss how the housing bubble distorted the allocation of capital of frms, we need to derive the most salient empirical predictions that we want to test in the data. We begin by doing two small modifcations to the model discussed above. First, we assume that the only difference across municipalities is their housing supply elasticity. Second, we allow for the possibility that frms own both real estate assets and nonreal estate assets in different proportions. In particular, the stock of housing of frm f is hf = sf H and the endowment of non-real estate assets is nhf = (1 − sf )NH, where f sf = 1. Therefore, the relative investment of two frms, f and f′, in municipality i is given by the following expression,

Equation (5.9) means that the relative investment depends on the price of housing in the municipality and the different shares of real estate assets. Let us assume that the share of real-estate assets (over total assets) of frm f is higher than the share of frm f′ (i.e., sf >sf ′ ). First, let us consider that there is no housing bubble. Given our assumption that the value of real-estate assets is the same as the value of non-real estate assets, Eq. (5.9) implies that both frms invest the same (i.e., ϕ pNoBubble i , sf , sf ′ = 1).

ki,f ki,,f ′ sf piH + sf ′ piH + 1 − sf

NH

1 − sf ′ NH = ϕ pi , sf , sf ′ . (5.9)

Imagine that a housing bubble emerges in municipality i, in this case, Eq. (5.9) implies that frm f is going to invest more than frm f′ (i.e., ϕ pBubble i , sf , sf ′ > 1). This implies that the housing bubble generates misallocation of capital because the frm who owns more real estate assets will be able to invest more than the other frm. This is the same type of misallocation we discussed above for a given municipality. Note that Eq. (5.6) is a particular case of Eq. (5.9) for sf = 1 and sf ′ = 0. We label this misallocation as “industry misallocation”.

Given the same model, we can make another comparison. Let us consider two frms f and f′, with the same composition of assets and industry but located in two different municipalities: B and NB. Municipality NB has a high housing supply elasticity and, thus, house prices do not react much to changes in housing demand. In contrast, municipality B has a low housing supply elasticity and house prices increase a lot if there is an increase in housing demand. In this case, the relative investment of both frms becomes,

Equation (5.10) says that the relative investment of these two frms will be different if the evolution of house prices is different in the two municipalities. Let us assume that a housing bubble emerges in the country. Given the difference in the housing supply elasticity, house prices will greatly increase in municipality B and they will remain constant in municipality NB. This implies that the frm located in municipality B will be able to increase more its investment than the frm located in munici pality NB. That is, ϕ pBubble B , pBubble NB , sf >ϕ pNoBubble B , pNoBubble NB , sf . This is also misallocation of capital. Investment increases more in municipality B because house prices have increased more than in municipality NB. We label this misallocation as “geographical misallocation”.

Finally, we can obtain a measure of misallocation for each municipality. Let us, for ease of exposition, consider the special case in which the share of real estate assets is one for one-half of the frms (i.e., sf = 1) and it is zero for the rest of frms (i.e., sf = 0). In this case, the production function of municipality i is

Yi = τ(ϕi)K α i ,

kB,f kNB,f ′ sf pBH + 1 − sf NH

sf pNBH + 1 − sf NH = ϕ pB , pNB , sf . (5.10)