6 minute read

5.1 Oops…the Housing Bubble Burst

Notice that, in the absence of a housing bubble, this household would not have asked for a loan from the bank. Thus, this overborrowing is a distortion created by the housing bubble. Another channel is through households who already own a house. Homeowners represent a large fraction of households in different countries and, thus, this is an important channel. For example, according to Mian and Suf (2011), in the United States, around 65% of households owned their primary residence prior to the recent housing boom. Households who own a house can use their house as a collateral to borrow. For example, the household goes to the bank and asks for a loan to go on a trip. The bank may agree to lend this money if the household uses the house as a collateral. As the reader may have noticed, the value of the collateral will depend on the price of the house. If there is a housing bubble, the value of the collateral will be higher than what it would have been without the bubble and the household will overborrow. To be clear, we say that there is overborrowing with the housing bubble because we compare the borrowing if prices were only driven by the fundamental demand with the borrowing with house prices above their fundamental value.

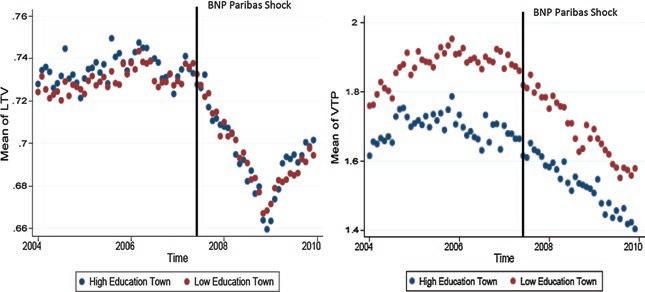

Mian and Suf (2011) analyze the effect of house prices on the evolution of borrowing of households in the United States during the recent housing bubble. First, they provide suggestive evidence consistent with the view that the housing bubble raised borrowing. In particular, they compare the evolution of household debt in municipalities in the top and bottom quartile of the housing supply elasticity distribution. They use the supply elasticity computed by Saiz (2010) and discussed in Chapter 4. They consider two borrowing variables: (i) total debt of households and (ii) debt-to-income ratio. The frst measure is a gross increase in borrowing. In the second measure, debt is normalized by income to capture the sustainability of the debt or the leverage of the household. They document that during this period mortgage debt amounts to 88% of total debt. Therefore, most of the changes in household debt will be driven by changes in mortgage debt. Mian and Suf show that, for the two measures, households living in housing supply inelastic (bubbly) municipalities borrowed more than households living in housing supply inelastic (non-bubbly) municipalities. To be specifc, they report that between 2002 and 2006 the increase in total debt was 20% higher in housing supply inelastic (bubbly) municipalities. Similarly, the change in the debt-to-income ratio was .6 higher in housing supply inelastic (bubbly) municipalities. Then, they formally

Advertisement

estimate the effect of house prices growth on total debt. They obtain an elasticity of debt with respect to house prices of .52. This number implies that a one percentage increase in house prices between 2002 and 2006 causes an increase of .52% in total debt. Remember that we have found that, between 2002 and 2006, house price growth was 37.2% higher in “bubbly” municipalities. Thus, the elasticity estimated in Mian and Suf implies that, without the housing bubble, household debt should have increased 19.6% (= .52*37.2%) less between 2002 and 2006.

A fnal dimension in which the choice of households may be distorted by the housing bubble is consumption. That is, we have seen that households were able to borrow more because of the increase in house prices. It could be the case that households used this extra money to consume more. More generally, there is a large academic literature emphasizing the wealth effect of house prices. The idea being that when house prices increase, homeowners feel richer because their house is more valuable and, thus, they adjust their consumption choice upwards. Case et al. (2005) provide empirical evidence supporting this wealth effect. They analyze how consumption is affected by changes in income, stock market wealth and housing market wealth. They perform this exercise for two samples: (i) 14 developed countries and (ii) the 50 US states. For both samples, they fnd that the impact of changes in housing market wealth on consumption is very large. Moreover, they fnd that the effect of changes in housing market wealth is much more important (quantitatively) than the effect of changes in stock market wealth. The work of Case et al. (2005) predates the recent housing bubble episodes. However, we expect that their fndings also apply for the recent housing booms. To analyze the wealth effect on consumption, it is better to use microdata, as Mian and Suf (2011) did to compute the effect of house prices on borrowing. Not surprisingly, Mian and Suf were also interested in how households used the money they borrowed. Unfortunately, they did not have consumption data at the individual level to answer this question. Nonetheless, by rejecting alternative uses of the money (e.g., reducing credit card debt or buying fnancial assets), they argue that households used a large fraction of the borrowed money for raising consumption.

To sum up, we have explained that a housing bubble distorts the choices of households. We have documented these distortions for US households during the recent housing bubble. In particular, we have shown that households purchase more housing, borrow more and

consume more because of the housing bubble. Although we have only discussed microevidence for the United States, we expect that these fndings can be extrapolated to other countries, as the macroevidence of Case et al. (2005) suggests. We now turn to the other relevant agent of the economy: the frm.

We consider a simple toy model based on Basco et al. (2018) to describe the effects of housing on the choices of the frm. The economy has only one sector. There are N municipalities in the country (indexed by i). These municipalities share the same capital and good market. This implies that the interest rate and price of the fnal good will be the same in all municipalities. However, each municipality has its own housing market. For simplicity, let us assume that all municipalities have the same number of frms (indexed by f), a mass of M. Firms have “ideas”. An idea means to have access to a production technology that allows the frm to produce f(kf) units of fnal good for each kf units of capital invested by frm f. We also assume that frms do not have money but they can use assets as collateral. That is, banks are willing to lend money to these frms if they have enough collateral. Firms own two types of assets: (i) real-estate (H) and (ii) non-real-estate assets (NH). Given these assumptions, the borrowing constraint of a frm is given by,

where df is the size of the loan, R is the interest rate on the loan, pi is the price of real estate assets in municipality i, Hf and NHf are real-estate and non-real estate assets of frm f, respectively. Finally, θ is an index of the quality of fnancial institutions.

The intuition behind Eq. (5.1) is that the bank will be willing to provide a loan to the frms only if the frm has enough assets (right-hand side) to repay the loan (Rdf). We assume that θ is smaller than one because not all assets can be collateralized. For example, the frm may hide some of these assets or there will be a (costly) delay if the frm does not pay the loan and the bank needs to take the frm to court. This is the reason why θ may be thought of as fnancial institutions. The better fnancial institutions are, the larger will be the fraction that can be collateralized. For the interested reader, Kiyotaki and Moore (1997) is the seminal paper on the effect of collateral constraints and they explain in detail the intuition behind this type of borrowing constraints.

Next, we assume that Eq. (5.1) is binding. The intuition behind this assumption is that the idea of the frm is so great that the frm would be

Rdf ≤ θ piHf + NHf , (5.1)