5 CONSEQUENCES OF HOUSING BUBBLES

67

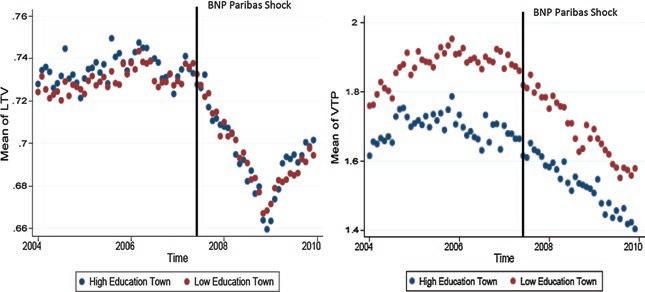

Notice that, in the absence of a housing bubble, this household would not have asked for a loan from the bank. Thus, this overborrowing is a distortion created by the housing bubble. Another channel is through households who already own a house. Homeowners represent a large fraction of households in different countries and, thus, this is an important channel. For example, according to Mian and Sufi (2011), in the United States, around 65% of households owned their primary residence prior to the recent housing boom. Households who own a house can use their house as a collateral to borrow. For example, the household goes to the bank and asks for a loan to go on a trip. The bank may agree to lend this money if the household uses the house as a collateral. As the reader may have noticed, the value of the collateral will depend on the price of the house. If there is a housing bubble, the value of the collateral will be higher than what it would have been without the bubble and the household will overborrow. To be clear, we say that there is overborrowing with the housing bubble because we compare the borrowing if prices were only driven by the fundamental demand with the borrowing with house prices above their fundamental value. Mian and Sufi (2011) analyze the effect of house prices on the evolution of borrowing of households in the United States during the recent housing bubble. First, they provide suggestive evidence consistent with the view that the housing bubble raised borrowing. In particular, they compare the evolution of household debt in municipalities in the top and bottom quartile of the housing supply elasticity distribution. They use the supply elasticity computed by Saiz (2010) and discussed in Chapter 4. They consider two borrowing variables: (i) total debt of households and (ii) debt-to-income ratio. The first measure is a gross increase in borrowing. In the second measure, debt is normalized by income to capture the sustainability of the debt or the leverage of the household. They document that during this period mortgage debt amounts to 88% of total debt. Therefore, most of the changes in household debt will be driven by changes in mortgage debt. Mian and Sufi show that, for the two measures, households living in housing supply inelastic (bubbly) municipalities borrowed more than households living in housing supply inelastic (non-bubbly) municipalities. To be specific, they report that between 2002 and 2006 the increase in total debt was 20% higher in housing supply inelastic (bubbly) municipalities. Similarly, the change in the debt-to-income ratio was .6 higher in housing supply inelastic (bubbly) municipalities. Then, they formally