We are looking for business owners who like to join the

Manningham Network Group and Community Paper.

• Accounting Services

• Acupuncture

• Architect

• Architectural Interior Design

• Attorney- Family

• Auctions- Real Estate

• Bookkeeper

• Bowen Therapy

• Builder- Commercial

• Business Coach

• Business Equipment Financing

• Business Insurance

• Cabinets

• Caterer

• Graphic Designer

• Plasterer

• Chinese Medicine

• Chiropractor

• Creative Director

• Commercial Mortgage

• Computer Repair

• Computer Web Design

• Concrete

• Copywriting/Copy Editing

• Counselor/ Psychotherapist

• Dentist

• Digital Media

• Electrical Operations

• Electrician

• Finance Bookeeper

• Financial Planner

• Fitness Trainer

• Flooring

• Pilates

• Garage Doors

• General Insurance

• Health & Wellness Coach

• Homeopathy

• Lactation Consultant

• Lawn Care

• Lawyer

• Life Coach

• Loans

• Marketing

• Massage Therapist

• Meditation/Yoga

• Mortgage Broker

• Naturopathic Medicine

• Nutrition

• Osteopathy

• Painter

• Personal Trainer

• Photographer

• Plumber

• Podiatrist

• Printer

• Project Management

• Psychologist

• Real Estate Rentals

• Real Estate Sales

• Reiki

• Residential Cleaning

• Residential Mortgage

• Security

• Signs

• Solar

• Solicitor

• Travel Agent

• Website Developer

• Wedding Planner

By Warren Strybosch

The Find Manningham is a community paper that aims to support all things Manningham. We want to provide a place where all Not-For-Profits (NFP), schools, sporting groups and other like organisations can share their news in one place. For instance, submitting up-andcoming events in the Find Manningham for Free.

We do not proclaim to be another newspaper and we will not be aiming to compete with other news outlets. You can obtain your news from other sources. We feel you get enough of this already. We will keep our news topics to a minimum and only provide what we feel is most relevant topics to you each month.

We invite local council and the current council members to participate by submitting information each month so as to keep us informed of any changes that may be of relevance to us, their local constituents.

EDITORIAL ENQUIRES: Warren Strybosch | 1300 88 38 30 warren@findnetwork.com.au

PUBLISHER: Issuu Pty Ltd

We will also try and showcase different organisations throughout the year so you, the reader, can learn more about what is on offer in your local area.

To help support the paper, we invite local business owners to sponsor the paper and in return we will provide exclusive advertising and opportunities to submit articles about their businesses. As a community we encourage you to support these businesses/columnists. Without their support, we would not be able to provide this community paper to you.

Lastly, we want to ask you, the local community, to support the fundraising initiatives that we will be developing

and rolling out over the coming years. Our aim is to help as many NFP and other like organisations to raise much needed funds to help them to keep operating. Our fundraising initiatives will never simply ask for money from you. We will also aim to provide something of worth to you before you part with your hard-earned money. The first initiative is the Find Cards and Find Coupons – similar to the Entertainment Book but cheaper and more localised. Any NFP and similar organisations e.g., schools, sporting clubs, can participate.

Follow us on facebook (https://www. facebook.com/findmanningham) so you keep up to date with what we are doing.

We value your support,

The Find Manningham Team.

POSTAL ADDRESS: 248 Wonga Road, Warranwood VIC 3134

ADVERTISING AND ACCOUNTS: editor@findmanningham.com.au

GENERAL ENQUIRIES: 1300 88 38 30

EMAIL SPORT: sport@manningham.com.au

WEBSITE: www.findmanningham.com.au

The Find Manningham was established in 2019 and is owned by the Find Foundation, a Not-For-Profit organisation with a core focus of helping other Not-ForProfits, schools, clubs and other similar organisations in the local community - to bring everyone together in one place and to support each other. We provide the above organisations FREE advertising in the community paper to promote themselves as well as to make the community more aware of the services these organisations can offer. The Find Manningham has a strong editorial focus and is supported via local grants and financed predominantly by local business owners.

The City of Manningham is a local government area in Victoria, Australia in the north-eastern suburbs of Melbourne. Manningham had a population of approximately 125,508 as at the 2018 Report which includes 27,500 business and close to 45,355 households. The Doncaster and Templestowe Council administered the area until December 15, 1994.

The Find Manningham acknowledge the Traditional Owners of the lands where Manningham now stands, the Wurundjeri people of the Kulin nation, and pays repect to their Elders - past, present and emerging - and acknowledges the important role Aboriginal and Torres Strait Islander people continue to play within our community.

Readers are advised that the Find Manningham accepts no responsibility for financial, health or other claims published in advertising or in articles written in this newspaper. All comments are of a general nature and do not take into account your personal financial situation, health and/or wellbeing. We recommend you seek professional advice before acting on anything written herein.

By Gen Alcampor

As the summer holidays come to an end, it’s time to pack the backpacks, sharpen the pencils, and get ready for another exciting year of learning, growth, and new adventures.

The first day of the school year is always exciting and rather chaotic. Friends have a chance to catch up who may not have seen each other for weeks, and even friends who have spent a lot of time together are still excited to see each other again. Everyone is clamouring to tell their class all about what they got up to, the adventures they had and even what they received for Christmas. I’m not sure how much schoolwork gets done on that first day as even the teachers seem happy to be back amongst the pandemonium of day one.

If your family is completely new to the school system with your little one starting Foundation, the nerves for both the parent and student can be that much higher with many tears shed. But by the end of the day for most people, this anxiety is removed, and everyone settles into a new normal.

Although starting a new school year can bring a mix of excitement and nerves for teachers and students alike – for parents, it can also bring some added costs. But don’t worry, there are programs designed to make it easier!

In Victoria there are a couple of programs to help families with the cost of school-related expenses: the Victorian School Saving Bonus and the Camps, Sports and Excursions Fund (CSEF).

The Victorian School Saving Bonus is a great initiative that aims to help families with the cost of school uniforms and other essential supplies. If you're a parent or guardian in Victoria, you might be eligible to receive a bonus to make things a little easier.

This bonus helps with essential items like uniforms, shoes, and school bags – things that every student needs to start the school year off right. Whether your child is heading into kindergarten, primary school, or high school, this bonus is designed to ease the financial load.

Who can access the Victorian School Saving Bonus? Eligibility can depend on factors like your family’s income or if you're receiving other forms of financial assistance. It’s worth checking in with your school or local council to see if

you can apply for this bonus. Even if you don’t think you qualify, it’s always a good idea to ask. Schools are there to support families, and they can guide you through the application process.

The Camps, Sports, and Excursions Fund (CSEF) is another great program that helps students participate in extracurricular activities like school camps, sporting events, and excursions. These activities can often come with an extra cost, but the CSEF is here to help ensure that all students have the opportunity to get involved, regardless of their financial situation.

This fund helps cover the costs of things like:

• School camp fees

• Sports programs and equipment

• Excursions and incursions

• Outdoor activities like swimming or team-building exercises

• Whether your child is looking forward to a school camp, an exciting excursion, or a new sport, the CSEF can help cover these costs, making sure that they don’t miss out on the fun because of financial barriers.

Who can apply for CSEF? If you hold a Health Care Card or Pensioner Concession Card, or if your family receives certain government assistance, you may be eligible to apply for the CSEF. The application process is simple, and you can check with your school to see if you're eligible and how to apply.

1. Victorian School Saving Bonus: Reach out to your child’s school or your local council to inquire about

eligibility and application details. Some schools will automatically inform families of how to apply, while others might require you to fill out an application form.

2. CSEF: You can apply for the CSEF through your child’s school. They’ll provide you with the necessary forms and guide you through the process. Be sure to apply as early as possible, as some schools have specific deadlines for applications.

The start of a new school year is an exciting time, but it can also be stressful for families who are worried about the costs. Programs like the Victorian School Saving Bonus and the CSEF are here to make sure that all students can start their school year with the resources and opportunities they need to succeed. These programs help families with essential school expenses, allowing them to focus on what really matters: education, growth, and making memories with friends. They also ensure that students have the chance to participate in important activities that promote teamwork, health, and personal development.

This school year is a fresh start filled with new possibilities. With the help of programs like the Victorian School Saving Bonus and the CSEF, you can rest easy knowing that there are resources available to help make school more affordable. So, take a deep breath, get ready for an exciting year ahead, and don’t forget to check out these programs to make the most of what’s available!

Here’s to a successful, fun, and fulfilling year of learning!

By Jodie Moore

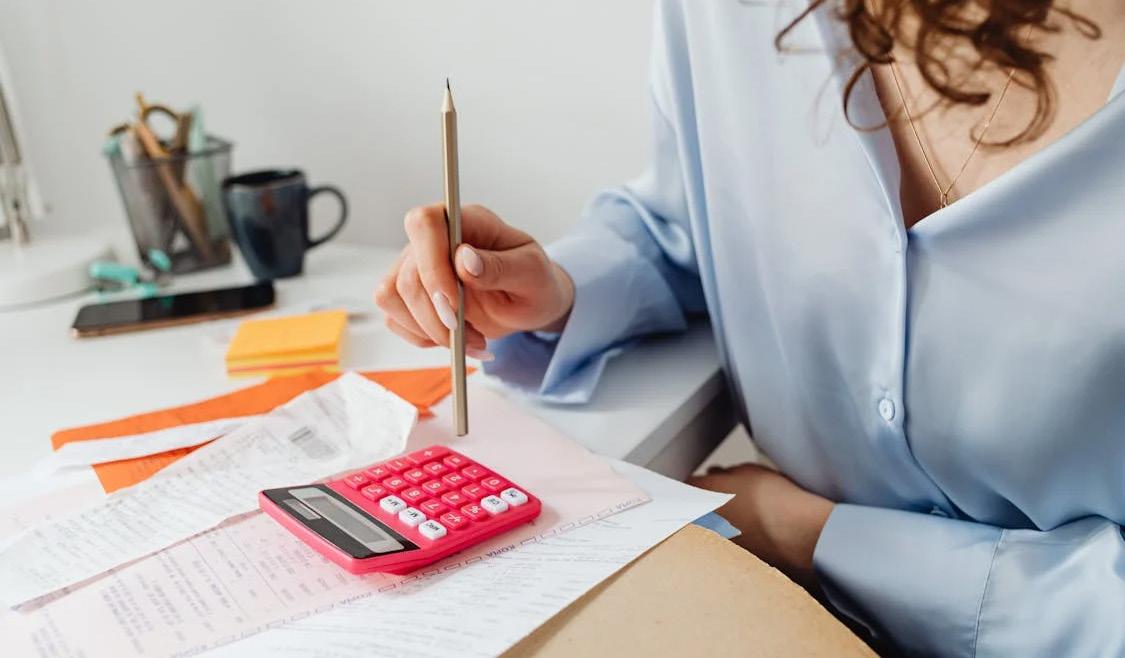

Pricing a product or service is one of the most critical decisions a business owner must make. Charge too much, and you risk scaring away potential customers. Charge too little, and you might not cover your costs or earn the profit you need to sustain and grow your business.

Here’s a step-by-step guide to help you understand how to determine the right price for your product or service using smart pricing strategies.

The first step in pricing is understanding all of the costs involved in delivering your product or service. These costs typically break down into two categories:

• Fixed Costs: These are costs that remain constant, regardless of how much you produce or sell. They include things like rent, utilities, software subscriptions, and salaried employees.

• Variable Costs: These fluctuate depending on how much you produce or sell. Materials, hourly wages, packaging, and shipping costs all fall under this category.

Once you’ve calculated both fixed and variable costs, you can figure out your break-even point—the minimum number of sales you need to cover both types of costs. This is crucial, as it ensures that your pricing will at least allow you to avoid losses.

Next, you’ll want to research the market. Understanding what your competitors charge is an essential part of the pricing strategy. However, just copying your competitors isn’t always the best approach. Look at:

• Direct Competitors: These are businesses offering similar products or services. What price range do they offer, and how does your product compare in terms of quality and features?

• Indirect Competitors: These may not be offering exactly what you do,

but they still capture your potential customers’ attention. For example, a local bakery might compete with a coffee shop that offers prepackaged pastries.

• Customer Expectations: What do your customers value most? Are they looking for premium quality, or are they more focused on affordability? This can help you position your price in a way that aligns with what your target market expects.

One of the biggest mistakes small business owners make is not accounting for the profit margin. After covering all your costs, you need to ensure that you’re making a profit. Profit margin is typically calculated as a percentage of the cost of goods sold (COGS). A common rule of thumb for small businesses is to target a profit margin between 10% and 20%, though this can vary depending on the industry. For instance, if your total cost per product is $50, and you want a 20% profit margin, you would add $10 to the cost (for a total price of $60). This ensures that your pricing strategy not only covers costs but also allows for sustainable growth.

Psychological pricing can have a powerful impact on your sales. For instance, pricing something at $99.99 instead of $100 can trigger a perception of a better deal, even though the difference is just one cent.

In addition to this “charm pricing,” consider tiered pricing strategies, bundling, or offering discounts for bulk purchases. Offering multiple price points or subscription-based pricing can also appeal to different customer segments and encourage repeat business.

Even with all the research and calculations in place, pricing is not a one-time decision. Over time, customer behaviour, market conditions, and your business costs can change. That’s why it’s important to test your pricing strategy. You might try offering a new product at a slightly higher price to see how customers respond or provide limitedtime discounts to see if they increase sales volume.

By tracking your sales data and monitoring customer feedback, you’ll be able to adjust your pricing strategy as needed, ensuring long-term profitability.

Pricing is both an art and a science. By carefully calculating costs,understanding market conditions, factoring in profit margins, and considering psychological pricing techniques, you can find a price point that supports your financial goals. In the end, the right price isn’t just about what customers are willing to pay—it’s about creating a balanced strategy that ensures your business can thrive in both the short and long term.

By Ethan Strybosch

The digital marketing trends every nonprofit business is jumping on this year

With the new year comes new resolutions, fresh goals, and the motivation to better ourselves and our businesses. As January gets well underway, the time to build stronger donor relationships, increase engagement and create a greater impact in your Not-For-Profit (NFP) is now. What can you do right now to start reaching your goals and growing your NFP?

Digital Marketing.

Here are four digital marketing trends shaping the NFP sector in 2025:

• AI in operations

• Short-form media

• Data-driven decision making

• Business-donor transparency

AI in operations

Chatbots and virtual assistants are evolving to be capable of more humanlike interactions, providing the capacity for the automation of routine tasks such as lead nurturing and email marketing, which in turn allows human teams more time and resources for strategic work and brainstorming.

Improving skills in, and familiarity with customer service tools that utilise AI — especially those with customer segmentation and content personalisation abilities — could improve customer and donor relations with your NFP. The skills these AI tools possess allow them to interpret sentiment in conversation, so they can provide customers or donors with a more personalised experience.

Short-form media

TikTok, Instagram, and YouTube are gaining popularity as effective ways to provide information and convey your nonprofit’s mission while catering to the population’s growing desire for simple, entertaining and interactive pieces of content.

With a little strategic planning, marketing teams can embrace the changes in these media platforms and use them for their benefit. Interactive features such as polls and quizzes, and short-form content such as YouTube shorts and Instagram reels can be utilised to boost engagement and target your niche audiences. Adapting to Live-streaming and Q&A’s

can open additional opportunities for real-time engagement.

Data analytic techniques have become standard practice to guide nonprofits in their decision-making.

By collecting and analysing donor data, and using analytic techniques, your business can assess campaign strategy success, donor giving patterns, and audience engagement quickly and easily.

By maximising the use of data analytics you can make more effective decisions for your NFP.

Research is suggesting that transparency in nonprofits improves volunteer engagement and donor contributions, which can contribute to the overall success of your business.

You can maximise transparency in your nonprofit in a number of areas including:

• Finances: Share detailed financial reports, revenue breakdowns, and spending allocations openly on your website.

• Funding: Explain clearly how donor contributions are used and the intended impact of different donation types.

• Annual Reports: Publish annual reports showcasing the financial health, accomplishments and program outcomes of your NFP.

• Policies: Make organisational policies including conflict of interest and whistleblower policies easily accessible and public.

• Partnerships: Clearly disclose partnerships in the non-profit and forprofit sectors and their contributions to the finance and mission of your business.

As digital marketing becomes integral to nonprofit businesses and trends in digital marketing continue to evolve, nonprofits that embrace these trends will be better equipped to connect with their communities, enhance their operations, and achieve their mission more effectively. By integrating AI, creating engaging short-form content, leveraging data-driven insights, and maintaining transparency, your organisation can reach those New Year’s goals and stay ahead in 2025.

Keeping your not-for-profit at the forefront of digital marketing in 2025 starts with staying informed

By Warren Strybosch

I thought it would be worth reminding everyone that it is important when seeking financial planning advice, to do some due diligence in relation to the person and/or company you are about to deal with before entrusting your money to them. Firstly, I want to tell you my story and why I got into financial planning.

It all began over 25 years ago. I was a secondary teacher and I wanted to go back and do some further studies. Prior to becoming a teacher and before joining the army, I was halfway through my accounting qualifications. I thought that would be a good place to start –to go and complete my accounting degree. However, someone mentioned that I should look at financial planning. It was an emerging profession that would bring together insurance agents, investment advisors, and the like. It sounded interesting so I decided to do an introductory subject in this area with the Securities Institute of Victoria and Deakin.

It did not take long before word got around that I was studying financial planning. I was approached by an older friend of mine who had trouble reading and understanding financial matters. He presented me with a piece of paper and asked me to explain what the share certificate meant. I had to point out to my friend that what I was holding was not a share certificate but in fact a letter confirming he had gifted over $150,000 to someone we both knew who called himself a financial planner.

There is a lot to this story, but the end result was that whilst my friend got hi s money back, many other people who also

got caught up in the scheme (we are talking about thousands of people in my community and around Australia), lost their money, their homes, ended up in divorce and some becoming so physically sick they could not get out of bed.

How did this happen?

Well, the person selling the scheme worked in a trusted position and told everyone he was a financial planner. Unfortunately, no one at the time did any due diligence to determine if he was really a financial planner. It was only later discovered that this person, whilst he was listed on the ASIC register as a financial planner, was licenced by a company that was in the process of being deregistered.

Also, the person was selling a scheme that was literally too good to be true. People were being told that their money would double or triple in only a couple of years’ time when the company they invested in listed on the stock exchange.

Unfortunately, many people believed his story…he was a good salesperson. He was raided by ASIC and the whole scheme fell apart.

It was because of this event that I decided to become a fully licensed financial planner. I made it my mission to try and protect as many people as possible; to educate them and help them with their financial needs. I have been working as a financial planner for over 20 years now and I see part of my role, for which I am unapologetic for, is to try and remove people from our profession that are, in my opinion, doing that wrong thing.

Even now, I find myself currently dealing with mortgage brokers and ex-financial planners who think it is ok to either provide advice when they are not qualified and/ or licenced to do so or they are setting

up schemes to either defraud the ATO or someone else. It never ends.

So, who can you trust and talk to when it comes to your money and needing advice?

In Australia, financial planning is governed by strict regulations designed to protect consumers. However, just like anywhere, there are still important steps to take to ensure you’re working with someone you can trust. Here’s how you can go about finding a trustworthy financial planner and making sure their advice is in your best interests.

1. Understand the Regulatory Framework in Australia

• Australian Securities and Investments Commission (ASIC): ASIC regulates financial planners in Australia and ensures that they adhere to the legal requirements of the industry. You can check the ASIC Financial Adviser Register to verify whether a financial advisor is licensed and check for any disciplinary action against them.

• Australian Financial Services (AFS) License: Anyone providing financial advice must hold an AFS license or be an authorized representative of an AFS license holder. This ensures they meet the standards for providing financial advice in Australia.

2. Check for Relevant Qualifications and Credentials

• Qualifications: Nearly all of the current financial planners have updated their qualifications in the past few years, For most, they will have a bachelor or post grad in financial planning.

• Financial Advice Association of Australia (FAAA) or Institute of Financial Professionals (IFPA): Look for advisors who are members of the FAAA or IFPA, as they adhere to the association's code of ethics and ongoing professional development requirements. Note: it is not a requirement to belong to an association anymore so whilst this was a requirement to practice financial planning in the past it is no longer a requirement.

• Registered Tax (Financial) Adviser or Accountant: If you’re dealing with tax and investment strategies, you might want to look for an adviser with this registration, ensuring they’re qualified to give advice on tax issues. As an example, I am both a financial planner and an accountant. There are not many people in Australia who are both.

• Best Interest Duty: Since 2013, Australian financial advisers have been legally required to act in their clients' best interests under the Corporations Act. This means they must prioritize your needs over their own financial interests. The “best interest duty” requires financial advisers to act with care, skill, and diligence.

• Fiduciary Duty: Some advisers might have a fiduciary duty (i.e., they must act in your best interest) while others may not. Financial planners who are fiduciaries are required to disclose any conflicts of interest and provide clear, unbiased advice. While the legal duty to act in your best interest is broad, it’s still important to ask upfront whether they have a fiduciary obligation and how they’re compensated.

• Fee-for-service (fee-only): Advisors who charge a fixed fee or an hourly rate are typically considered to be more transparent and less likely to have conflicts of interest. This means they don’t earn commissions from the financial products they recommend.

• Commission-based: Some advisers earn commissions from recommending specific products, such as insurance or investment products. It is important to understand why they receive commissions and how this might have an impact on the advice provided. For instance, we only receive commissions for personal insurance advice because people are reluctant to pay large fees to get advice in this area especially if they are unsure if they will obtain the insurance cover to begin with.

Important Tip: Since 2019, Australian financial advisers are required to disclose all fees upfront, which has helped reduce conflicts of interest. Still, always ask for a Statement of Advice (SOA), which outlines their recommendations and the cost of those services.

• ASIC Financial Adviser Register: You can verify if an adviser is properly licensed by checking the ASIC Financial Adviser Register. It provides details of advisers’ qualifications, history, and whether they've faced any disciplinary action.

• FAAA’s Adviser Search: The Financial Advice Association of Australia has an online Adviser Search tool, where

• you can find members who meet professional standards, including compliance with the FAAA's Code of Ethics.

• Google Reviews, Testimonials, and Word of Mouth: It can be helpful to search for reviews online or ask friends, family, or colleagues if they’ve worked with a particular adviser. Personal referrals can help you feel more confident in your choice.

• Awards. Some advisors have won awards. Whilst this is not a true indication of trustworthiness, it is good to know that they are contributing to their profession or are known by their peers.

Here are some key questions to ask when choosing a financial planner:

• Do you have a best interest duty?

• How are you compensated (fees, commissions, or both)?

• How much do you charge and are you on the higher or lower end when it comes to fees compared to other advisors?

• Can you explain the reasons behind your advice?

• What are your qualifications and experience?

• How often will we meet to review my financial plan?

• Can you provide a detailed Statement of Advice (SOA)?

7. Evaluate Their Communication and Transparency

• Clear Communication: A trustworthy financial planner should explain things in a way that is clear and understandable. If you don’t understand their recommendations or they use jargon, that’s a red flag.

• Transparency: Make sure the adviser is open about any potential conflicts of interest, fees, and commissions. They should be willing to provide a detailed breakdown of their costs and explain the reasons behind their recommendations.

If you’re ever unsure about an adviser’s recommendations, don’t hesitate to seek a second opinion from another licensed professional. This helps ensure that you’re not missing out on better options or falling victim to bad advice.

for

Financial planning is not a one-off task; it’s an ongoing relationship. Make sure that you feel comfortable with the

adviser and that they take the time to understand your unique financial goals. Choose someone who listens and gives you advice tailored to your situation, rather than offering generic solutions.

• High-pressure tactics: If an adviser is pushing you into a decision or pressuring you to sign something immediately, that’s a red flag.

• Unexplained fees or commissions: If they’re not transparent about how they earn money or can’t clearly explain the fees involved, walk away.

• Unclear advice or evasiveness: If the adviser is evasive when explaining how their advice benefits you or how their fees are structured, that’s a sign to be cautious.

Finding a trustworthy financial planner in Australia requires some effort, but it’s worth it for your financial peace of mind. By making sure they have the right qualifications, adhere to ethical standards, and are transparent about their fees, you can build a relationship based on trust. Don’t rush the process—take the time to find an adviser who aligns with your values, understands your goals, and has the skills to help you achieve them.

Do you have any specific questions about finding a financial planner in Australia, or are you navigating a particular financial situation you need advice on? If so, consider giving Find Wealth and Find Retirement a call on 1300 88 38 30

Warren Strybosch 1300 88 38 30 |warren@findwealth.com.au www.findwealth.com.au

Financial Planning is offered via Find Wealth Pty Ltd ACN 140 585 075 t/a Find Wealth & Find Retirement.

Wealth is a Corporate Authorised Representative (No 468091) of Alliance Wealth Pty Ltd ABN 93 161 647 007 (AFSL No. 449221).Part of the Centrepoint Alliancegroup https://www. centrepointalliance.com.au/

Warren Strybosch is Authorised representative (No.468091) of Alliance Wealth Pty Ltd. Services offered are superannuation, retirement planning and aged care advice.

This information has been provided as general advice. We have not considered your financial circumstances, needs or objectives. You should consider the appropriateness of the advice. You should obtain and consider the relevant Product Disclosure Statement (PDS) and seek the assistance of an authorised financial adviser before making any decision regarding any products or strategies mentioned in this communication.

Whilst all care has been taken in the preparation of this material, it is based on our understanding of current regulatory requirements and laws at the publication date. As these laws are subject to change you should talk to an authorised adviser for the most up-to-date information. No warranty is given in respect of the information provided and accordingly neither Alliance Wealth nor its related entities, employees or representatives accepts responsibility for any loss suffered by any person arising from reliance on this information.

By Warren Strybosch

In Australia, most people who earn an income need to submit a tax return, but the specifics depend on your income, situation, and other factors. Here’s an overview of who typically needs to file:

1. You Earn Above the Tax-Free Threshold

• The tax-free threshold in Australia is $18,200 (as of the 2023-24 financial year). If your income exceeds this amount, you'll need to file a tax return. This includes wages, salaries, business income, investments, etc.

• If you earn $18,200 or less, and you have no other taxable income, you may not need to file. However, in most cased, even if you do earn under the threshold the ATO requires you to submit a return even if you believe it is not necessary. Also, you might still want to, to claim any tax withheld or get a refund that might be owing to you.

2. Self-Employed or Business Owners

• If you’re self-employed, a freelancer, or run a business (whether full-time or part-time), you must submit a tax return, even if your income is below the threshold.

• You’ll need to report your income and expenses, and you might be subject to Goods and Services Tax (GST) if you earn over $75,000 per year.

• If you receive income from investments, such as interest, dividends, or rental income, you may need to file, regardless of whether you’re employed. This income is taxable, and you’ll need to report it.

• If you’re a resident for tax purposes and earn income from overseas, you must declare this income in your Australian tax return, even if tax has already been paid in another country.

• If your employer has withheld tax from your wages, you need to file a return to settle your final tax liability. Often, this will result in a refund if too much tax was withheld.

• Similarly, if you have had PAYG (Pay As You Go) withholding or other tax taken from government payments (like pensions or unemployment benefits), you might need to submit a return.

• If you want to claim deductions (e.g., work-related expenses, education costs, donations to charity), you need to file a tax return to do so.

• Similarly, to claim tax offsets like the Low Income Tax Offset (LITO), Senior Australians Tax Offset (SATO), or the Family Tax Benefit, a return is required.

• If you rent out property or receive income from renting assets (like a car or equipment), you need to file a return, even if your total income is below the threshold.

• If you have assets overseas or income from outside Australia, you need to declare these. Australia has strict rules on foreign income, and failing to declare it can lead to penalties.

• If you receive government payments from Centrelink (e.g., the JobSeeker Payment, Parenting Payment), you may need to lodge a tax return, especially if your total income exceeds the taxfree threshold or if your payments include taxable components.

• Students and Part-Time Workers: Even if you’re a student or working part-time, you may need to submit a tax return if your income exceeds $18,200, or if you’ve had tax withheld and are eligible for a refund.

• Retirees and Pensions: Retired individuals who receive a pension or income from superannuation may need to submit a return depending on their income level. Often retirees have the misconception that if they are in receipt of the Age Pension or are fully retired and over the age of 67 and do not earn more than the tax-free threshold that they are not required to submit a return. This may be incorrect and not doing so might require the estate to lodge several returns when you pass away causing unwanted issues for the executors.

• Even if your income is below the threshold, you might still want to file to claim any refunds or offsets. The Australian Tax Office (ATO) may also pre-fill some of your information, so filing can be easier than expected.

• The Australian financial year runs from July 1 to June 30, and tax returns are generally due by October 31. If you’re using a tax agent, you can file later, usually 15th of May the following calendar year, but you’ll need to sign up with one before the October deadline.

In short, it is better to simply submit your return and keep everything up to date.

By Kathryn Messenger

Your skin is not just the shell to your body, it’s actually an organ, and whilst topical creams, lotions and balms all have their place, if the issue is due to the relationship between your skin and other organs, the topical treatment will likely fall short.

Whilst hormones are usually the first place most people look, I actually find looking to the liver can be most helpful. The relationship between the liver and the skin is strong as the major role of the liver is in detoxification, and if the liver is unable to preform this task well, it’s often the skin that suffers as the body attempts to detoxify via the skin.

But detoxification is not the only role of the liver, it also metabolises hormones. This means that there are 2 pathways by which the liver is involved: detoxification and hormones. Usually minor liver dysfunction is evident before puberty, however the change in hormones brought about by the onset of puberty can make this more obvious through symptoms like headaches, fatigue and sluggish digestion. Since the liver is primarily a digestive organ, working closely with the bowels, if constipation or food allergies are present, the toxic load of the liver can increase.

As expected, hormones also play a large part in acne, as high androgens (oestrogen and testosterone) can cause the skin to become more oily which can block the skin pores.

Stress is also involved, due to increased production the hormone cortisol with high stress. This is helpful in the short-term, but long-term high cortisol leads to inflammation.

If acne is already a problem for you, stress will likely exacerbate it with increased inflammation of the skin.

Sugar also plays an important role in the inflammatory process, as the energy high, followed by the low will also increase cortisol and lead to inflammation, along with further inflammation when the sugar is metabolised by the liver.

So, as you can see, there are a lot of factors at play, but here are some recommendations to improve acne:

• Reduce sugar intake, and include whole foods (such as fruit and vegetables)

• Reduce alcohol and processed foods

• Increase water intake to assist your body in detoxification

• Eat bitter leafy greens (rocket, dandelion greens) and cruciferous vegetables

• (broccoli, cauliflower, brussels sprouts)

• Reduce life stressors that you are able to.

If you need further support, natural medicines can help with improving liver function, regulating the nervous system response to stress and balancing hormones.

Kathryn Messenger

BHSc (Naturopathy) kathryn@wholenaturopathy.com.au

By Warren Strybosch

At Find Retirement, we love helping people with their retirement needs. It is an exciting chapter in many people’s lives as they move from full-time work to spending more time with grandkids, travelling, playing a sport they love e.g., golf or lawn bowls, or simply having more time to work on that hobby or interest that has been sitting on the shelf for way to long.

Most often people decide to retire around the end of each financial year which is now only five months away. Can you believe January has already flown by? As such, we thought it would be timely to get those of you who are considering retirement this coming year to consider some important factors to ensure a smooth transition into your retirement years. Here’s a list of things to think about:

1. Retirement Goals & Lifestyle

• What kind of lifestyle do you want? Consider your desired activities, travel plans,hobbies,or where you want to live.

• Do you want to downsize? Many people opt to sell their homes and move to a smaller, more affordable place or relocate to a different area, perhaps even abroad.

• How will you spend your time? Having a plan for how to stay mentally and physically active can make a huge difference in post-retirement satisfaction.

2. Retirement Savings and Income Needs

• How much money do you need to live comfortably? Make sure you’ve estimated your monthly and annual living expenses in retirement, accounting for things like housing, healthcare, food, travel, and entertainment.

• Are your retirement savings enough? This includes superannuation, investment properties, shares, or other investments. Ensure they’re aligned with your estimated retirement income needs.

• Have you accounted for inflation? Over time, the cost of goods and services will likely rise. Your plan should factor in potential increases in prices over the next 20-30 years.

• When should you start claiming Social Security? For many people you will

pension when you reach age 67 and this is subject to the amount of assets you own (not including the house). For others, it may be years before you can claim the age pension, if at all, until your assets fall below the upper threshold asset test.

• Do you have an allocated pension (from your own superannuation monies)? If so, understand when you can start collecting and how much you’ll receive.

• Will your spouse's benefits impact yours? If married, coordinating Social Security and pension benefits with your spouse can increase your lifetime income.

4.

• What’s your plan for healthcare? Should you continue to pay for private health care? The costs can be quite prohibitive but for some people who have acute health care needs, cancelling this type of insurance may not be an option.

• How will you handle long-term care costs? Nursing homes, assisted living, or in-home care can be expensive. Plan ahead for how you'll cover these potential costs. Giving money to your children is not always the wisest move given you might need to pay a refundable accommodation deposit (RAD) in the future.

• Are you prepared for out-of-pocket costs? Even with Medicare, there are deductibles, premiums, and co-pays. Plan for these potential gaps.

• Should you continue to pay life insurance premiums? If you have no debt and a suitable amount of assets in retirement, you should consider whether to continue paying high premiums or use these funds to help cover future lifestyle expenses.

• How will taxes impact your retirement income? Understand how withdrawals from pension accounts will be taxed.

• Will you need to submit a tax return? If you earn $1 of income from nontax-free sources you may need to submit a tax return, even if no tax is payable. Don’t leave it up to your estate to have to prepare lots of returns on your behalf.

• Have you paid off high-interest debt? Ideally, you should try to pay off as much debt as possible before retirement, especially credit cards or other high-interest loans.

• Do you have a mortgage? Consider whether you want to pay off your mortgage before retiring or if you’re comfortable carrying it into retirement.

• Are there any other financial obligations? Things like student loans, personal loans, or family support might need to be factored into your retirement budget.

• How should you adjust your investment portfolio as you approach retirement? Consider shifting your portfolio from high-risk assets (like stocks) to more stable investments (like fixed interest ETFs) to reduce the risk of major losses.

• Understand your withdrawal obligations? Most people do not realise you have to withdrawal minimum amounts from your pension account. As you get older this amount increases over time.

• How much risk are you comfortable taking? Think about your tolerance for market volatility and whether you're okay with potential ups and downs in your investment value.

• Do you have an emergency fund? Ideally, this should be separate from your retirement savings. Having 3-6 months’ worth of living expenses set aside can give you peace of mind in case of unforeseen circumstances (medical emergencies, unexpected repairs, etc.).

• Do you have an updated will or trust? Make sure your will or trust is in place to specify how your assets should be distributed.

• Have you chosen a power of attorney and healthcare proxy? These documents ensure someone you trust can make medical or financial decisions on your behalf if you're incapacitated.

• What are your estate tax implications? Some estate planning may be necessary to minimize taxes for your heirs, particularly if you have a larger estate.

• Do you want to keep working parttime? Many retirees enjoy working part-time or consulting to stay active and generate income.

• Are you interested in volunteering? Giving back to the community can provide a sense of purpose and fulfillment post-retirement. If any of you love writing articles then talk to me

about the Find Foundation (yes, that was cheeky place that in here).

11. Mental and Emotional Readiness

• Are you emotionally prepared for retirement? Transitioning from a work identity to retirement can be challenging. Think about how you’ll stay socially engaged and mentally stimulated. Males find it harder to transition from work to retirement because work has been their whole life. Having a network of friends who are also moving into retirement or having specific goals can help with the transition.

• What will your daily routine look like? Having a structured daily routine can help avoid the potential feeling of boredom or loss of purpose.

12. Review and Adjust Your Plan

• Do you have a retirement plan in place? Regularly review your retirement plan to ensure it’s still on track, especially if you experience major life changes (e.g., health issues, job changes, or changes in the economy).

• Are you prepared to adjust your lifestyle if needed? Flexibility is key. Economic changes, healthcare costs, or other factors may require you to adjust your plans in retirement.

13. Legacy and Giving Back

• What kind of legacy do you want to leave? Think about charitable

1. Email to returns@findaccountant.com.au requesting your PAYG return to be completed. Provide us with your full name, D.O.B and address

2. A Tax engagement letter will be emailed to you for signing via your mobile (no printing or scanning required).

3. You will be then sent a tax checklist to complete online. Takes less than 5 minutes.

4. We will then require you to upload your documents to our secure portal.

5. Once we have received all your documentation, we will complete the return.

6. We will email you the completed return with our invoices. Once you sign the return and pay the invoice we will lodge the return on your behalf.

contributions, setting up college funds for grandchildren, or passing down values to your family.

• Do you want to leave something for your heirs? If so, make sure your estate plan reflects these wishes.

Taking the time to consider these factors well before retirement can lead to a smoother, more secure transition, and a more enjoyable retirement overall. Do any of these stand out to you as areas you’re still unsure about or need more info on?

At Find Retirement, we would love to help you on your retirement journey. Give us a call on 1300 88 38 30 or email warren@ findretirement.com.au and book in a time to discuss your retirement needs.

This information is current as at August 2022. This article is intended to provide general information only and has been prepared without taking into account any particular person’s objectives, financial situation or needs (‘circumstances’). Before acting on such information, you should consider its appropriateness, taking into account your circumstances and obtain your own independent financial, legal or tax advice. You should read the relevant Product Disclosure Statement (PDS) before making any decision about a product. While all care has been taken to ensure the information is accurate and reliable, to the maximum extent the law permits, Alliance Wealth and its related bodies corporate, or each of their directors,officers,employees,contractors or agents, will not assume liability to any person for any error or omission in this material however caused, nor be responsible for any loss or damage suffered, sustained or incurred by any person who either does, or omits to do, anything in reliance on the information contained herein.

Contact them on 1300 88 38 30 info@findretirement.com.au | www.findretirement.com.au

Manningham residents are invited to come together and celebrate Clean Up Australia Day on Sunday 2 March, with a clean up event at Koonung Creek Linear Park from 10.00am to 1.00pm.

Manningham Mayor, Councillor Deirdre Diamante encourages the local community to get involved.

“Clean Up Australia Day is coming up and a great way to take collective action to help our parks, waterways and wildlife.”

Manningham is home to a variety of parks and reserves as well as rivers and creeks that connect to larger water systems. Unfortunately, litter is being

found in many of these areas, which can endanger waterways and wildlife.

When our waste ends up on the ground, it doesn’t just stay there – it washes into local waterways, especially during rainy or windy weather.

This litter can disrupt water quality and create hazards for our aquatic life, making it harder for plants and animals to thrive. Wildlife can also mistake plastic bags, food wrappers or small debris for food.

Clean Up Australia Day is a chance to take positive, practical action.

“By keeping litter out of our natural environment, we can create a cleaner, healthier Manningham for all.”

Event details

• Sunday 2 March 2025

• 10.00am to 1.00pm

• Koonung Creek Linear Park, 105 Leeds Street, Doncaster East, enter via Boronia Reserve

Gloves, litter collection gear, and a barbecue lunch will be provided. Registration is required.

“It’s incredibly rewarding to get outside, connect with nature and work together to make a positive impact – plus, the free barbecue is always a bonus!” Cr Diamante said.

For more information about this event or to register, visit manningham.vic.gov.au/ events/clean-australia-day

Manningham’s highly anticipated International Women’s Day Breakfast event returns on Thursday 6 March, with tickets now available.

This year’s keynote speaker, Dr Emma Fulu, is a world-leading expert on gender equality and ending violence against women and girls. She has worked for the United Nations and other global programs.

Manningham Mayor, Councillor Deirdre Diamante said International Women’s Day was an opportunity to celebrate, connect and reflect.

“I’m so pleased to welcome Dr Emma Fulu to Manningham to speak on such an important issue that demands attention and action both globally and locally,” Cr Diamante said.

“Championing gender equality and respect in every aspect of our lives is at the heart of driving change.

“We all have a role to play in turning promises into progress. I encourage men and women to join us for what will be an insightful and inspiring morning,” the Mayor added.

International Women’s Day (IWD) is a global celebration of women’s achievements and raises awareness for women’s equality.

Dr Fulu will speak to this year’s UN Women Australia IWD theme, ‘March Forward: It’s time to turn promises into progress’.

The theme is in reference to the 30th anniversary of the United Nations Beijing Declaration and Platform for Action

(1995) – considered to be the most progressive blueprint for advancing women’s rights.

While women have broken many barriers since then, there’s still much to be done for millions of women around the world and it’s time to turn promises into progress.

Dr Fulu will be joined by a panel of guest speakers who will bring their lived experience and individual lens to this important discussion.

The event will be held on Thursday 6 March, 7.30am to 9.30am at the Manningham Function Centre. Tickets are $25 and include a plated breakfast.

For more information and to book your ticket, visit manningham.vic.gov.au/IWD.

The Manningham Community Panel has reached a significant milestone, charting a course for the future after delivering its final recommendations to Council.

Manningham Mayor Councillor Deirdre Diamante said the Panel’s insights will be invaluable in ensuring that the Council’s strategic plans are grounded in the community’s needs and aspirations.

“By listening to the voices of our community, we’re ensuring that our decisions and actions reflect and align with what matters most to our residents,” Cr Diamante said.

“The Panel has played a crucial role in this process, comprising members from diverse age groups, cultural backgrounds and geographic locations that represent the unique tapestry of our community.

“This collaborative approach will help enable us to create a more inclusive, resilient, sustainable and vibrant community for all.”

The Panel was established to identify Manningham’s key priorities, challenges and opportunities – to help guide the Council’s strategic plans. This includes the Community Vision 2040, the four-year Council Plan, and the 10-year Asset and Financial Plans.

Throughout the process, Panel members deliberated for approximately 1,680 collective hours and heard from over 50 speakers from Council and community.

They handed over their recommendations to Council at the final meeting on 1 February 2025. They span several themes including community safety, transport, open spaces and more.

“Over the coming weeks, we’ll prepare a response to each of the panel’s recommendations, including how they will be implemented or the reasons for not supporting any recommendation,” Cr Diamante said.

“We’re sincerely grateful to the panel members for their time and efforts during this dynamic process and committed to implementing the panel’s recommendations to the fullest extent possible.

We’ll ensure their insights are carefully considered in all our decision-making as we plan ahead for Manningham,” the Mayor added.

For further information and stay up to date, visit yoursay.manningham.vic.gov. au/help-shape-manninghams-future

An aquatic playgroup is a structured water-based program designed for young children (often infants and toddlers) and their parents or caregivers. These playgroups focus on providing a safe and supportive environment for early childhood development through fun, sensory, and skill-building activities in the water.

Engaging in water play activities during baby and toddler swim lessons can strengthen parent-child bonds and provide opportunities for social interaction. Such shared experiences contribute to a child’s confidence and comfort in aquatic settings.

Each session consists of water familiarisation for parents and babies, guided by a qualified swim teacher. All babies must be accompanied by an adult in the water. The Aquatic playgroup

is available for babies from three months to 11 months of age.

Water play promotes learning in various developmental areas, including

cognitive and physical skills. Activities like filling, pouring, and splashing help children understand concepts such as cause and effect, while also enhancing their coordination and motor skills.

The

Engaging in social and recreational activities is vital for seniors, as it enhances physical health, cognitive function, and

emotional well-being. Participating in dance classes, such as ballroom or line dancing, promotes physical fitness and social interaction. For instance, 101-yearold Ron Crutch attributes his longevity to his passion for dancing, which he believes keeps him mentally and physically active.

Participating in these activities not only enriches daily life but also contributes to overall happiness and longevity. It’s essential for seniors to choose activities that align with their interests and physical abilities to maintain motivation and enjoyment.