THE STATE OF UNHEALTHYSAVAGELYTHEHOUSINGMARKETSAVAGELYUNHEALTHY HousingWire Lead Analyst, Logan Mohtashami MAGAZINEHOUSINGWIRE ❱ 2022SEPTEMBER September 2022

Mortgage expert, meet CreditXpert. Maximize borrowingapplicantpotential. creditxpert.com One of the best ways to increase profitability is to ensure EVERY mortgage applicant has the highest credit score possible. In fact, 73% of applicants can move up 20 points in 30 days. Show the clear path to a higher score. We’ll help you compete for every loan when you show applicants their full credit potential. Offer more competitive rates Qualify more applicants Increase applicants’ purchasing power The home of credit potential. 631 +56 +35 +39 632 632PotentialCurrent XPN TU EFX

HOUSINGWIRE EDITOR-IN-CHIEF SARAH WHEELER MANAGING EDITOR JAMES KLEIMANN SENIOR MORTGAGE REPORTERS BILL CONROY, GEORGIA KROMREI REAL ESTATE & TITLE REPORTER BROOKLEE HAN MORTGAGE REPORTER FLÁVIA FURLAN NUNES REPORTER CONNIE KIM LEAD ANALYST LOGAN MOHTASHAMI CONTRIBUTORS RICK SHARGA, SCOTT OLSON CEO CLAYTON COLLINS COO DIEGO SANCHEZ DIRECTOR OF FINANCE ANDREW KEY DIRECTOR OF PEOPLE AND CULTURE AMY BEARD CHIEF OF STAFF ALEX BRIDGEMAN VICE PRESIDENT OF GROWTH CAREN KARRIS GROWTH MARKETING MANAGER GREG ROBERTS MAGAZINE EDITOR AUDREY LEE SENIOR GRAPHIC DESIGNER EMILY CARPENTER GRAPHIC DESIGNER BRANDON JOHNSON VICE PRESIDENT OF PRODUCT HOLDEN PAGE UX/UI MANAGER BO FRIZE WEB DIRECTOR BRENT DRIGGERS AD OPS COORDINATOR ELIZABETH LEDOUX DIRECTOR OF HW+ & EVENTS BRENA NATH SENIOR WEBINAR & EVENTS MANAGER ALLISON LAFORGIA MARKETING PROGRAM MANAGER LESLEY COLLINS MEMBERSHIP COORDINATOR SARAHI DE LA CUESTA PEOPLE OPERATIONS MANAGER JAMIE BRIDGES PRODUCT MANAGER MATTHEW STAFFORD MEMBERSHIP DEVELOPMENT SPECIALIST CAROLINE ABAD EMAIL MARKETING SPECIALIST ALI MORRISSEY GROWTH COORDINATOR SYDNEY SMITH SENIOR EVENTS MANAGER KATIE GALBRAITH EVENT SPECIALIST MAKENNA CLAY BUSINESS ANALYST WHITNI ROWE SOCIAL MEDIA STRATEGIST KENNEDY BENJAMIN SALES SVP SALES AND OPERATIONS JENNIFER WATSON LAWS VP SALES MICHAEL ORME WESTERN CHRISTI HUMPHRIES, LINDSLEY HARRIS, CASS HECKEL CENTRAL & NORTHEAST SAMANTHA STEIN SOUTHERN TAMARA WREN, AMINA JAHIC CLIENT STRATEGY MANAGER ADINA RITTER STRATEGIC ACCOUNT MANAGER BRIA SOYELE SALES MARKETING MANAGER TOD MOHNEY CONTENT SOLUTIONS MANAGING EDITOR MALEESA SMITH CONTENT EDITOR JESSICA DAVIS ASSOCIATE EDITOR MARNI DAVIMES MULTIMEDIA PROJECT MANAGER DALTON JOHNSON JUNIOR DIGITAL PRODUCER ELISSA BRANCH CONTENT SOLUTIONS COORDINATOR EUNICE GARCIA REALTRENDS VICE PRESIDENT OF REAL ESTATE MARK ADAMS EDITORIAL DIRECTOR TRACEY VELT DIRECTOR OF RANKINGS PROGRAMS LIZ SMITH EXECUTIVE MANAGER, CEO PROGRAMS JILL OLMSTED SENIOR DATA ANALYST KEERI TRAMM FINLEDGER EDITOR JOE BURNS REPORTER TANNISTHA SINHA HOW TO REACH US LETTERS TO THE EDITOR EDITOR@HOUSINGWIRE.COM TIPS AND STORIES EDITORIAL@HOUSINGWIRE.COM CURRENT MEMBERSHIP / SUBSCRIPTION HWPLUSMEMBER@HOUSINGWIRE.COM NEW MEMBERSHIP / SUBSCRIPTION HOUSINGWIRE.COM/MEMBERSHIP MARKETING & ADVERTISING JLAWS@HOUSINGWIRE.COM OR (469) 870-4572 ADVERTISING CLIENT SUCCESS CLIENTSUCCESS@HOUSINGWIRE.COM REVERSE MORTGAGE DAILY EDITOR CHRIS CLOW HW MEDIA CORPORATE 4 ❱ HOUSINGWIRE SEPTEMBER 2022

The housingunhealthysavagelymarket

#6you? #4 by @LoganMohtashami Brena Director,NathHW+ & Events @BrenaNath LETTER FROM THE EDITOR 5 ❱ HOUSINGWIRE SEPTEMBER 2022

Mohtashami, since writing that piece, has continued to expand on what this means, diving deeper and deeper into recession talks and even adding the word “nightmare” to the mix. Because of the timely September issue theme, retail and lending, we asked Mohtashami to update readers in a feature piece that focuses on the need-toknow information moving into the rest of 2022 and beyond. Starting on page 26, you’ll hear directly from him about the state of housing and the economy. And, for those who would love to see him in person, you can join us at HousingWire Annual for his Housing Super Session. Go to page 19 to learn more.

The information contained within should not be construed as a recommendation for any course of action regarding legal, financial or accounting matters. All written materials are disseminated with the understanding that the publisher is not engaged in rendering legal advice or other professional services. HW Media does not guarantee the accuracy of information provided, and is not liable for any damages, losses or other detriment that may result from the use of these materials.

Streets

Tweets From The

Back in March, HousingWire Lead Analyst Logan Mohtashami coined the phrase “savagely unhealthy” to describe the state of the housing market. As catchy and memorable as the saying is, it signifies a very volatile and discouraging time for industry professionals and people look ing to buy a home. Do you notice how I used a present-tense word there? Unfortunately, this phrase still rings true six months later. When Mohtashami first used the phrase in his commentaries back in March, he said, “I have lost my five-year home-price growth model of 23% in just two years, and inventory has wors ened in 2022. So now, I consider this not just an unhealthy housing market, but a savagely unhealthy housing market.”

Now that we are days from August, you feel my savagely unhealthy housing vibe, don’t

© 2022 by HW Media, LLC • All rights reserved

What’s your affordable homeownership strategy? Homeownership should be accessible and affordable to all Americans, yet disparities persist, especially for communities of color. Across the mortgage industry, the message is clear: We all have a role to play in bridging the racial equity gap in homeownership. MGIC’s ARCS framework can help you ask the right questions and build your affordable housing and racial equity plan in 4 key areas: • Awareness • Readiness • Community • Solutions

All Things Housing October 3-5, 2022 Fairmont Scottsdale,PrincessAZ HousingWire Annual Heads to Scottsdale Content Technology Community Register today! housingwireannual.com

8 ❱ HOUSINGWIRE SEPTEMBER 2022

12 New leadership was sworn in at HUD following a nom ination by President Joe Biden. Take 5 14 Get your next favorite book recommendation from Chuck Iverson, president at Mason-McDuffie Mortgage. Local Intel 16 Beachfront towns like Siesta Key in Florida have a lock on real estate for remote workers. Event Calendar 18 Kick off conference sea son in warmer climates with big events from AIME, NAMMBA, and HW Media. Inside Agent 21 Hidden vacation gem, Southaven, Michigan, is home to this $4.495 million home. Trade Desk 70 NAHB is encouraging stu dents to consider careers in the skilled trades during Build Across America Day. Real Estate 74 Chicago-based Realtor Stephanie LoVerde shares her experience working in the Windy City.

Reverse Mortgage 78 Christina Harmes Hika is coaching the next gener ation of reverse professionals.mortgage Mortgage 82 There are several mortgage companies who are hiring even in the changing hous ing market. Kudos 88 Learn how to get involved with the Mortgage Bankers Association Opens Doors Foundation. Parting Shot 90 The HW Media team can’t wait for all of you to join us at HousingWire Annual 2022. 2022

PeopleSeptemberMovers

The state of the savagely unhealthy housing market The current state of housing is a far cry from the great recession of 2008. So, what is coming next? 26fffeaturesCantechpointCompassintherightdirection? Compass has made a massive impact in the industry, but can the company maintain this technologically fueled momentum ? 48 2022 HousingWire Insiders HousingWire’s 2022 Insiders represent the unsung heroes of the top companies in the industry. Congrats to these 50 behind-thescenes rockstars. 32 What a difference a year makes By Rick Sharga 22 Is it time to bring Fannie and Freddie out of con servatorship? By Scott Olson 24 Special Reports These 12 companies showcase the newest fintech products and services that will amplify your business. 54 9 ❱ HOUSINGWIRE SEPTEMBER 2022

ServiceLink Congratulates Laura DiRienzo on being named a 2022 HousingWire Insider! Learn more at svclnk.com

Never one to expect the spotlight, Laura DiRienzo is the embodiment of an organizational Insider. Her work ethic, relentless pursuit of knowledge and passion for the mortgage industry inspires all those around her. Laura, thank you for all you do to move the industry forward! ServiceLink congratulates you on this well-deserved honor.

Laura DiRienzo Vice OriginationPresident,Title&Close

PEOPLE MOVERS

Karthik Kumar | LendArch | Chief Operating Officer and Executive Vice President Mortgage consulting firm LendArch named Karthik Kumar as the chief operating officer and executive vice president. Kumar most recently served as the global mortgage practice head at Tata Consultancy Services, where he spent 18 years focusing on solution architecture, operational delivery and entity transformation. Kumar will be responsible for fundamental changes in lending procedures, including areas like behavior, market dynamics and products.

Vinay Singh | Department of Housing and Urban Development | Chief Financial Officer

Wells Fargo named Kleber Santos as CEO of consumer lending. Santos joined the bank in November 2020 as head of diverse segments, representation and inclusion. Before Wells Fargo, he worked for Capital One for 15 years in various leadership positions, including as retail and direct banking president. Santos will continue to report to Wells Fargo CEO Charlie Scharf, who said Santos has “built the DSRI function over the past two years and driven significant outcomes in both representation and inclusion.”

Vinay Singh was appointed as the chief financial officer of the Department of Housing and Urban Develop ment following his nomination by President Joe Biden in April. Singh will oversee financial management at HUD and his priorities will range from grants management to improving the department’s budget process. Singh has more than 25 years of experience in finance-related positions. Singh served as a senior advisor at the U.S. Small Business Administration from September 2021 to July.

Andrew Weiss | BlackFin Group | Partner Management consulting firm BlackFin Group hired Andrew Weiss as a partner. Weiss, who has more than 25 years of experience, will work in the company’s technology practice. Recently, Weiss served as senior vice president of platform strategy at Origence. He also held leadership roles at Bank of America, Newbold Advisors and New Penn Financial. Weiss started his career in the mortgage industry in 1991, serving as senior vice president of advanced technology at Fannie Mae.

iEmergent appointed Megan Horn as its new chief marketing officer. In this role, Horn will expand the brand strategy of iEmergent, a forecasting and advisory company that works with real estate, financial services and mortgage industries. Horn moves into this role after working as a consultant for iEmergent through her own business, Megan Horn Digital. Prior to her time in the housing industry, Horn worked in the marketing departments for companies such as Far Reach and Innovate Energy.

Former FHFA director Mark Calabria has been appointed to Evolve Mortgage Service’s advisory board. The board is focused on promoting the company, the leadership, network expansion and audience expansion. Calabria currently serves as a senior advisor at Cato Institute. Before his appointment as FHFA director, he served as the chief economist to Vice President Mike Pence.

12 ❱ HOUSINGWIRE SEPTEMBER 2022

Sushil Sharma | Better.com | Chief Growth Officer Digital mortgage lender and real estate company Better.com hired Sushil Sharma as the chief growth officer. Sharma, who brings more than 20 years in product management and software engineering from other in dustries, will lead user acquisition efforts. He previously worked at LendingTree and Match, where he helped the company go public in 2015. Sharma also serves on the board of advisors for the University of Texas at Arlington.

Mark Calabria | Evolve Mortgage Services | Advisory Board Member

Kleber Santos | Wells Fargo | CEO of Consumer Lending

Megan Horn | iEmergent | Chief Marketing Officer

The competitive edge you need to stay ahead. Complimentary seat saved at HousingWire’s virtual events and access to on-demand librariesJointoday:housingwire.com/membership HW+ members get exclusive access to: Deeper dives into the stories impacting the housing industry and your bottom line Connect with other industry leaders and HW Editors in an exclusive membersonly experience Premium Content Virtual Events HW+ Slack Channel

TAKE 5 14 ❱ HOUSINGWIRE SEPTEMBER 2022

4. The book I can’t stop recommending is... “Relentless” by Tim Grover, who was Michael Jordan and Kobe Bryant’s trainer. a trip to Scotland and Amsterdam this year. 2022 has been a make-up year for the

Chuck Iverson not only serves as the current president of Mason-McDuffie Mortgage, but he also serves on the board of directors for the California Mortgage Bankers Association and was the recent chair of their breakout Mortgage Innovators Conference. Iverson has over 30 years of experience in the mortgage industry and has 1. I felt like a success at my job when... our team introduces a new product, solves a small problem or somehow improves some

2. My favorite thing to do with my employees is ... hang out and get to know them! This usually involves a meal and just getting to connect as If I had picked a different career path, I would a Scientist. I love the idea of being able to

Chuck Iverson, President, Mason-McDuffie Mortgage

The Minneapolis-Saint Paul metropolitan area, better known as the Twin Cities, is home to everything from professional sports teams to award-winning theater pro ductions, a vibrant craft beer scene, as well as the nation’s largest shopping mall. With all these attractions, it is easy to see why so many people want to call the Twin Cities home. “The Twin Cities is almost always in those ‘top ten places to live' lists," Ryan O’Neill, a local RE/MAX agent, said. “There is a strong employment base, four distinct seasons and big city amenities without the crowds of some other major cities.” Like just about everywhere else in the country, the Twin Cities has been dealing with an inventory issue. On the day O’Neill spoke with HW Media, he said there were rough ly 5,000 homes on the market in the area, and noted that a balanced market is closer to 18,000 homes. “Interest rates are rising, and we are seeing some cooling, but demand is still strong, just not as strong as it has been the last couple of years.”

By Brooklee Han Remote work flexibility opened up the possibilities of where people could live, so more and more homebuyers have decided to make the move to the beach. Just outside of Sarasota and right on the Gulf of Mexico, Siesta Key is one of the many beachfront locales these buyers have flocked to. “The beach has been a huge draw — it never snows here, you never have to worry about shoveling the driveway or scraping off your car,” Trystan Foglia, a local eXp agent, said. “And with the COVID-19 pandemic, things started opening up in Florida a lot earlier than other places, so some people moved here because of that.” But as interest rates have ris en, demand, which was once white hot, has started to cool. “Now we are starting to see houses sit on the market for more than a week when you used to be able to get five offers in under 24 hours,” Kayla Minck, who works with Foglia on The Kameli Team, said. Both Minck and Foglia said that while things are cooling down, it is not quite a buyers’ market, though it may turn that way in the future. “Buyers are active, but not as active as they once were. Prices are high and now rates are high and every time we have spoken to buyers recently, they say they are waiting for the rates to go back down, but at this point, I think they will be waiting a while,” Minck said.

LOCAL INTEL Siesta Key, Florida

16 ❱ HOUSINGWIRE SEPTEMBER 2022

Twin Cities, Minnesota

TexasAustin, Raleigh,NorthCarolina

Sioux Falls, South Dakota

17 ❱ HOUSINGWIRE SEPTEMBER 2022

Even before the onset of the COVID-19 pandemic, Raleigh was one of the fastest growing cities in the country. As more and more people flocked to the metro area, Raleigh’s housing market turned scorching hot according to Redfin. However, local agent Marti Hampton, of Marti Hampton Real Estate, said that rising interest rates have been putting a damper on the previously hot market. “It is still a very strong sellers’ market and there is not enough inventory for the buyers, however, I have seen a shift in the number of offers that we are receiving,” Hampton said. “A few months ago, we were receiving 30 or 40 offers on a single property and that has dropped down some. We have seen a slight seasonal increase in inventory like we normally would see this time of year, but it is still not enough.” Despite the downshift, Hampton is confident this big city’s small-town southern charm, along with other attractions like top universities and health care providers, will continue driving homebuyers to Raleigh.

Temperatures in Austin have been in the triple digits for months now, but the metro area's housing mar ket finally started to cool off. Austin’s housing market has generated plenty of headlines over the past two years, as major corporations, as well as individuals, have decided to call the capital of the Lone Star State their new home. But, as mortgage rates have risen and home prices in the metro have contin ued to rise, the market has calmed down. “Instead of seeing 10 plus offers on something, you are seeing more like five offers. Instead of going in three or four days, homes are now sitting a bit longer,” Jeremy Vandermause, a local Bramlet Residential Real Estate agent, said. Vandermause also noted how much pur chase power homebuyers have lost as interest rates have risen. “People are more hesitant,” he said. “I have a client right now whose price range was $400,000 to $420,000 and now it is more in the $360,000 to $390,000 range because her original budget was created when interest rates were at 3% or 4%.”

Sioux Falls, the largest city in South Dakota, accounts for roughly 30% of the state’s population and has become quite the destination. Its namesake, the Big Sioux River, runs just north of the downtown area providing lush landscapes and picturesque waterfalls for locals to enjoy. It is easy to see what is attracting homebuyers to Sioux Falls. As with so many metro areas, however, an increase in homebuyer demand has, of course, created some challenges for the lo cal housing markets. “We are still seeing fairly low inventory,” local agent Amy Stockberger, of Amy Stockberger Real Estate, said. “We have seen a little bit more inventory accumulate but it is nothing in the big picture.” As interest rates have risen, Stockberger said she has seen a slight drop off in demand, but conditions have more or less persisted at their current rate. “Anything under the $400,000 price point is still pretty aggressive and getting a lot of offers, then we also have an aggressive market for things above $900,000, which is really interesting,” she said. Stockberger attributes the high level of demand for pricier homes to the influx of out-of-state buyers the area has seen, and while the market may cool due to rising interest rates, she expects the area’s natural beauty and lack of a state income tax to continue attracting buyers in the coming months and years.

“During the Great Recession, it was like somebody turned the faucet off,” she said. “It was gangbusters, home sales like crazy, then all of a sudden it went down.”

LOCAL INTEL

Savage and Messerli discuss their ”halftime report” of 2022, some of the trends the industry is seeing this year, the challenges the industry has to overcome and more.

KM: I think big one, of course, was the rising rates, low inventory and affordability. And those were areas that we wanted to really expand on, like what are the dynamics there because people were sometimes saying different things or had different perspectives on it. Then there were trends around like the shift to non-depositories and also automation.Itends up being a lot of categories.different Scan the code to listen now! Sept. 15-17

EVENT CALENDAR

Cost to attend: Members: $499 | Non-members: $1,499

For this Housing News episode, HW Media CEO Clayton Collins is joined by Chief Savage,BoomerangCoachOfficerInnovationatMortgageandSalesDaveaswellas the Experience.com Vice President of Strategy Kristen Messerli. The three dive into a discussion on the current state of the mortgage industry.

Cost to attend: $395

Presented by the National Association of Minority Mortgage Bankers of America ORLANDO, FL CONNECT is a popular real estate and finance industry conference. At tendees are treated to three days of panels, round tables, keynote speak ers and fun networking events with like-minded professionals in the in dustry. Plus, there are unique events like the gala dinner, College Days and sector-specific speakers for attendees to get information that is relevant to their niche community. Take full advantage of everything Connect has to offer through sponsored luncheons, dinners and a three-day exhibition hall where you can try out the latest technology. Attendees will take a wealth of knowledge away from this year’s Connect conference and build a better industry moving forward.

Presented by the Association of Independent Mortgage Experts LAS VEGAS, NV

Sept. 29-Oct. 1

THE FIFTH ANNUAL Fuse National Conference is built for mortgage pro fessionals who are ready to grow their business, network with other pro fessionals and get the inside scoop on where the industry is headed. This conference features special sessions and panels on VA loans; diversity, equity and inclusion; working in a recession and women in the mortgage industry. Saturday’s keynote speaker, Mat Ishbia, president and CEO of UWM, will present and later that day attendees will enjoy a celebration of the top 100 producers in the industry.

NAMMBA Connect 2022 Oct. Cost3-5toattend: Members: $655 | Non-members: $1,295

SCOTTSDALE,

HousingWire Annual 2022

“Housing News” Dave Savage and Kristin Messerli discuss the current state of the mortgage industry

LISTEN NOW

AIME Fuse 2022

18 ❱ HOUSINGWIRE SEPTEMBER 2022

HOUSINGWIRE ANNUAL is the ultimate event for housing industry professionals to connect and learn. Featuring dozens of panels, speakers and networking opportunities, HW Annual is the place to be if you want to learn from industry leaders and experts, connect with like-minded profes sionals and explore the latest technology from conference sponsors. Don’t miss the Marketing Leaders Success Summit or the Women of Influence Forum taking place on Oct. 3 prior to the HW Annual. These individually ticketed, half-day events will feature housing industry leaders with specific marketing experience and powerful women in the industry who want to build a better industry moving forward.

Presented by HW Media AZ

HousingWire: What were the drivers and the data points that you chose to focus on to help build the thesis for this halftime report? Kristen Messerli: Well, what was really cool about this report is that we did get all of this initially from the experts and so we tran scribed all of the interviews and then went through and categorized where everyone was talking about different subjects. Then we did additional research. So it’s cool because I do feel like we aggregated the information, but it’s kind of written by the industry and industry experts. HW: When you did that categorization, what were the data areas that started to form that people were talking about?

Nominations close September 23rd Recognizing the most impactful and innovative technology leaders serving the economy.housing 19 ❱ HOUSINGWIRE SEPTEMBER 2022

EVERY STATE HAS A LUXURY SIDE to it, and the Wolverine State is no exception. On the west coast of Michigan lies South Haven, a mainly resort town of less than 4,000 permanent residents and a cavalcade of second-home dwellers That’s where Jackson Mattson comes in. Mattson has been a real estate agent in southwest Michigan for the last 20 years. His trade is selling homes along the pristine, though for months of the year, frozen, Lake Michigan waterfront. For the last 10 years, Mattson has hung his license with @properties, which makes some sense. The brokerage has the biggest market share in Chicago. And “85% to 95%” of people buying property in South Haven or neighboring St. Joseph are “from the Chicagoland area.”

jackson@atproperties.comal@propertiesMattsonJacksonChristie’sInternationRealEstate

INSIDE AGENT

21 ❱ HOUSINGWIRE SEPTEMBER 2022

“We’ve been coined the riviera of the Midwest,” Mattson said. “There are a lot of attractions, the lakefront sunsets, wineries. There is a lot of fruit. People come here just to pick blueberries.”Asforthe Monroe Boulevard abode, the home was con structed by Mike Schaap Builders, a luxury homebuilder in nearby Holland, Michigan. The 4,479-square-foot home stands along 100 feet of Michigan shoreline. It has floor-to-ceiling windows, and a saltwater swimming pool. The home, Mattson points out, is within walking dis tance to a downtown that has a distinctive vibe from the lake front.“There are usually graduation parties, sports gatherings around here,” he said, adding that he hopes the ebbing COVID-19 pandemic will spark a “wave of activity.” 906 Monroe Boulevard South Haven, Michigan 49090 $4.495 million 5 bedrooms, 4.5 bathrooms

“In fact, the MBA expects the number of refi loans to drop from 6.4 million in 2021 to under 2.2 million in 2022 and just over 1.6 million in 2023.”

22 ❱ HOUSINGWIRE COMMENTARY SEPTEMBER 2022

By Rick Sharga In 2021, it seemed like the biggest problems mortgage lenders faced were how to process the growing backlog of loan applications and how to hire enough people to handle the volume of business coming through the door. But as proof to be careful what you wish for, a simple 2.5% hike in mortgage rates solved those problems completely. In turn, it created a whole different, much more unpleasant set of challenges.Asrates for 30-year fixed-rate loans jumped from sub-3.0% to between 5.0-6.0%, the rate-based refi market unsurprisingly dried up, leading to massive layoffs, industry consolidation and some lenders simply going out of business. In the July mortgage market forecast, the Mortgage Bankers Association (MBA) said it anticipated refi volume would drop from $2.345 trillion in 2021 to $706 billion in 2022 and further to $540 billion in 2023. So this isn’t a short-term problem for the industry, and we’ll likely continue to see more layoffs, more consolidation and more lenders in distress. Will other mortgage loans help make up this deficit? While cash-out refi volume will probably increase, the size of these loans is typically much lower than rate-based refis. The number of borrowers taking out these loans is generally much lower too. In fact, the MBA expects the number of refi loans to drop from 6.4 million in 2021 to under 2.2 million in 2022 and just over 1.6 million in 2023. This enormous fall-off in refinance activity will take its greatest toll on independent mortgage banks (IMBs) and non-bank lenders, which have dominated the refi market over the past few years and relied heavily on fine-tuned and aggressive direct-toconsumer business models to drive their sales. Many of these lenders are ill-equipped to shift from refi to purchase loans.

What a difference a year makes The changes to the lending game from 2021 to 2022 and beyond

PURCHASE LOANS ARE NO PANACEA Lenders banking on a move from refinance loans to purchase loans may also be in for an unpleasant surprise. The MBA’s Purchase Loan Application Index hit its lowest levels in over 20 years in late July, and it has been running about 20% below both 2019 and 2021 levels. The MBA forecast calls for purchase loans to be virtually flat on a year-over-year basis between 2021 and 2022, from about $1.65 trillion last year to a little over $1.66 trillion this year. The forecast is only projecting a modest increase to $1.7 trillion in 2023. And the organization is actually forecasting a lower number of total purchase loans — from almost 4.9 million last year to 4.4 million this year and just over 4.3 million next year. So while the dollar volume of loans will edge up slightly due to increasing home prices, the actual number of loans originated will go down a bit. All told, the combination of fewer refi loans and fewer purchase loans will drop overall mortgage origination volume by 40% in 2022 according to the MBA, and the 2023 volume will dip slightly lower still. Profitability will also be challenged — purchase loans take longer and are more complicated to process than refi loans. That 2.5-point jump in mortgage rates has had an extraordinary impact — not just on refinance activity, but on home sales as well. Freddie Mac has pointed out that this increase in rates was the biggest this century, and probably the largest since the early 1980s. It also reversed a 20-year trend where higher home prices were offset by steadily decreasing mortgage interest rates to keep monthly payments relatively affordable. The combination of double-digit home price appreciation and higher interest rates means that prospective homebuyers will expect to pay between 40-50% more in monthly mortgage payments than they would have in 2021. Homes are simply unaffordable for many buyers — especially first-time buyers — and it is difficult for many others to even qualify for a loan.

CHANGE OFTEN LEADS TO OPPORTUNITY

Over the past few years, many mortgage lenders have done very well by offering a small selection of products. With buyers in a near frenzy and rate-based refi borrowers looking to take advantage of historically low rates, there was no reason to get creative. But the changing market may offer opportunities for those lenders who have a different and more varied product offering.Asimple example of this is adjustable-rate mortgages (ARMs), which fell out of favor during the Great Recession and accounted for less than 4% of purchase loans as recently as December 2021. As homebuyers look for ways to affordably purchase a property, 5/1 and 7/1 ARMs are likely going to become more and more popular among borrowers and a more important tool in lenders’ arsenals. And ARMs won’t be exclusively purchase loans, either; expect cash-out refinance borrowers to also explore ARMs as an option when they’re considering a refi. Lenders shouldn’t overlook opportunities with FHA and VA borrowers as the market shifts. Over the past two years, these borrowers were at an enormous disadvantage — trying to compete with cash buyers and pre-approved conventional loan borrowers who could close a transaction much more quickly than the process allowed with these government loans. An FHA or VA borrower simply had no chance to buy a home when it sold within a week of being listed, as was the case in many markets. But as sales volume has slowed down due to affordability issues, days on market are increasing and buyers aren’t as frequently bidding up and over-paying for properties. We’ll likely see both FHA and VA loan volume moving from unusually low numbers back up to normal levels over the next year or two. Lenders who issue those loans should see an uptick in business. The FHA has also announced plans to more aggressively promote its 203(k) loans, which allow borrowers to add repair costs to their loan amount if they’re buying “fixer-uppers.”

Lenders who survive — and thrive — during this downturn will probably be those with broader product offerings and those who are nimble enough to shift gears and move into other product areas to meet the shifting needs of this changing marketplace. Rick Sharga serves as the executive vice president of Market Intelligence at ATTOM. Prior to this, he was the executive vice president of RealtyTrac, an ATTOM company that publishes the country’s largest database of foreclosure information for real estate agents and investors.

“These reports show sales at 5.12 million existing homes and 590,000 new home sales in 2022.”

23 ❱ HOUSINGWIRE SEPTEMBER 2022 COMMENTARY

This is a product that hasn’t had much attention in recent years, but it might be a part of the FHA’s efforts to help buyers find more affordable housing.

The bottom line is that the next few years are going to be extraordinarily challenging for mortgage lenders, especially those lenders whose businesses were heavily reliant on refinance loans.Retail lenders, who tend to be less exclusively reliant on mortgages, may find themselves in a position of competitive advantage during this period, as will lenders who manage large mortgage servicing portfolios, where values often rise in concert with interest rates.

Another “back from the dead” product candidate is the home equity line of credit (HELOC). Homeowners today are sitting on a record amount of equity — over $27 trillion. Many of these homeowners have decided to stay where they are (with their comfortable 3.0% mortgages) and wait for market conditions to settle down a bit. These are exactly the kind of homeowners who may be interested in tapping into their bulging equity to make home improvements, pay down more expensive debt or use these funds for college, vacations or other needs. Our data at ATTOM showed an almost 28% increase in HELOC activity in the first quarter of 2022 compared to the prior year.

None of this paints an especially pretty picture for the industry, where many former high flyers are already struggling to right-size operations to meet the reduced loan volume. And the MBA’s July projections may be overly optimistic — they’re based on an economy that grows slowly but doesn’t enter a recession. Their purchase loan volume is based on a housing market where 5.6 million existing homes and 744,000 new homes are sold in 2022, both significantly higher than annualized sales based on June numbers from the National Association of Realtors (NAR) and the Census Bureau. These reports show sales at 5.12 million existing homes and 590,000 new home sales in 2022.

Baby Boomers are increasingly aging in place in much higher numbers than prior generations, and are strong candidates for HELOCs as well as for home equity conversion mortgages (HECMs), also known as reverse mortgages. Boomers, as a group, probably have the largest total amount of equity, just based on the size of the cohort, and how long they’ve been accruing equity in their properties. While not as widely offered as other mortgage products, reverse mortgages might just find themselves the new belle of the ball — the right product at just the right time in a shifting marketplace.

24 ❱ HOUSINGWIRE COMMENTARY SEPTEMBER 2022

By Scott Olson July 30 marked the 14-year anniversary of President George W. Bush, a Republican president, signing into law the Housing and Economic Recovery Act (HERA), developed under a Democratic-controlled Congress.

WITHSTANDING THE TEST OF TIME

A 2015 report by the New York Federal Reserve found that “conservatorship achieved its key short-run goals of stabilizing mortgage markets and promoting financial stability during a period of extreme stress.”

FANNIE AND FREDDIE FULFILLING THEIR HOUSING MISSION

At the same time, Fannie and Freddie have hit the sweet spot of both performing well financially and fulfilling their housing mission. Fannie and Freddie were an essential source of

I

Loan portfolios have been dramatically slashed, ending the significant pre-HERA Fannie/Freddie interest rate risk exposure. And, the GSEs have their own version of the Dodd-Frank Qualified Mortgage (QM), which generally outlaws no doc, no income loans, a major contributor to the GSEs’ conservatorship.

“Conservatorship achieved its key short-run goals of stabilizing mortgage markets and promoting financial stability during a period of extreme stress.” - New York Federal Reserve

HERA established a process for conservatorship of Fannie Mae and Freddie Mac, situated FHFA as a first-class regulator and codified GSE mission provisions like the Housing Trust Fund, Duty to Serve and Housing Goals.Many are disappointed that Fannie and Freddie are still in conservatorship 14 years later. From my perspective as a House Financial Services Committee housing staffer, who worked on the HERA legislation at that time, I think it is important to remind people how well-crafted HERA was and how well it has served taxpayers, homeowners and our nation’s housing markets.

Longer term, HERA and conservatorship reforms have addressed the major risk characteristics of the pre-2008 version of the GSEs credit risk transfers, which are still being used to transfer risk away from taxpayers and to provide market discipline — a kind of early warning sign if the GSEs are going off the rails.

The GSEs have been under conservatorship for 14 years

s it time to bring Fannie and Freddie out of conservatorship?

When HERA was signed into law, few people envisioned that its conservatorship authority would be invoked just 39 days later — but it was. Fortunately, HERA’s de novo conservatorship provisions have more than withstood the test of time.The immediate impact was to stabilize financial markets in turmoil. The conservatorship facilitated the Home Affordable Modification Program (HAMP) that enabled 645,000 GSE distressed borrowers to save their homes through loan modifications and the Home Affordable Refinance Program (HARP) that enabled 3.5 million underwater borrowers to lower their mortgage rates.

ADDRESSING MAJOR RISK CHARACTERISTICS

Finally, there are GSE housing goals. Housing goals have been criticized from all sides of the political spectrum. But no, though some have claimed, they did not cause the 2008 crisis; every major study has rejected this theory. And, housing goals don’t require the GSEs to buy bad loans or participate in social engineering. They rest on the simple premise that Fannie and Freddie should not use a taxpayer backstop to cherry-pick higher quality, higher income mortgage loans — but instead must predominately carry out their statutory mission requirement to serve low- and moderateincome homebuyers and renters.

25 ❱ HOUSINGWIRE SEPTEMBER 2022 COMMENTARY

In fact, it is not essential for Congress to enact legislation. HERA includes the tools for the conservator (FHFA) to take Fannie and Freddie out of conservatorship.

The best approach, in my personal opinion, is for Fannie and Freddie to exit conservatorship under a true utility model using the housing mission tools of HERA, a vigilant FHFA that makes sure the GSEs do not take on dangerous levels of risk to maximize shareholder profit and an explicit federal backstop to establish MBS investor confidence.

mortgage credit for the housing recovery after the 2008 subprime mortgage crisis. Under conservatorship, Fannie and Freddie paid back their Treasury advances and generated an additional $110 billion in profits for American taxpayers. A few years ago, FHFA restarted the process of letting the GSEs retain profits to build up their net worth and provide a buffer against future economic downturns.

So, in the absence of consensus and congressional guidance, it is understandable that no FHFA director over the last 14 years has taken Fannie and Freddie out of conservatorship.

Ideally, Congress would hold extensive hearings to develop a bi partisan consensus on how to move forward — and then have FHFA use its authority under HERA to act.

But there are good faith differences of opinion on many key issues, including how to resolve the government’s preferred stock holding.

The three Duty to Serve market areas are manufactured housing, affordable housing preservation and rural housing. As a result, Fannie and Freddie now pay particular attention to these critical areas — which were often ignored before the adoption of HERA.

Looking forward, the great parlor game in Washington is when, if ever, Fannie and Freddie will exit conservatorship. At the time when they were put in conservatorship, Treasury Secretary Paulson called it a “timeout.” That is one heck of a time-out! And one that apparently will not end soon. The reason is simple. We seem to be waiting on Congress — but Congress is plagued by legislative gridlock — and detailed legislation is not the best way to address the complexities of how Fannie and Freddie should operate and be regulated post-conservatorship.

WILL THE “TIMEOUT” END SOON?

Either way, 14 years later, HERA still provides a sound foundation for making this critical part of our housing finance system work effectively. It would be nice if all federal legislation were that successful. Scott Olson is executive director of the Community Home Lenders Association. Olson has over 20 years of experience on Capitol Hill – including 15 as a top housing staffer on the House Financial Services Committee, working on housing and mortgage finance issues.

An important HERA provision was the creation and funding of the Housing Trust Fund, the first significant affordable housing program since the housing tax credit program was created 22 years earlier. A small portion of GSE profits are allocated by the states for construction or substantial rehabilitation of affordable rental housing for the lowest income earners. Since the program began in 2016, $2.659 billion has been contributed by Fannie and Freddie for the Housing Trust Fund.

Or not. Many in Washington think the conservatorship is working well and believe there is no urgency for Fannie and Freddie to exit conservatorship.

GSE HOUSING GOALS

Another HERA provision was the creation of Duty to Serve. This is based on the reality that the GSEs were able to meet their housing goals while ignoring certain profitable and critically important segments of the market, simply because they are lower volume activities that require the GSEs to roll up their sleeves a bit.

How housing today is different than the Great Recession of 2008 and where it is headed next THE STATE OF MARKETHOUSINGUNHEALTHYSAVAGELYTHESAVAGELYUNHEALTHY 26 ❱ HOUSINGWIRE SEPTEMBER 2022

MohtashamiLoganBy 27 ❱ HOUSINGWIRE SEPTEMBER 2022

T he housing market in 2022 has been savagely unhealthy. It’s not unhealthy like the housing bubble crash of the great financial crisis, but it is frustrating none theless. In my economic work, the years 2020-2024 have always stood out as our most prominent housing demographic group reaches their home-buying years during this period.

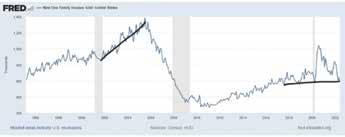

EXISTING HOME SALES

I am writing this article at the beginning of August, and with how data moves, a lot of things can change. With that said, we are basically at the halftime show for 2020-2024 and it’s time to assess all the sectors of the U.S. housing market and the general U.S. economy

As always, the marginal homebuyer always gets hit the worst in this situation. Whenever mortgage rates go below f%, housing demand grows. Then when rates get above 4% and head toward 4.5% to 5%, things tend to slow down. We saw this in the previousHowever,expansion.inthesummer of 2020, home prices started their massive acceleration. At this time, I started to raise my concerns about rising home prices, while others were pontificating about the threat of a forbearance home price crash.Even in February of 2021, I warned people that we needed higher rates to cool things down. Back then, people were still talking about a forbearance housing crash. In 2022, rates finally broke over 4%. Strangely, 4-5% mortgage rates weren’t cooling demand as much as I thought they would initially.

Once they rose above 5%, they finally had an effect. Housing followed the traditional trajectory of rising rates, which means a downward shift in the sales trend like we saw in the previous expansion. The rise of ARM loans also mitigated the damage to home sales.

Starting in 2020, I expected to see a solid five years of at least 6.2 million total home sales each year, with enough demand to keep housing construction moving since demographics equal demand. Everyone needs shelter and somewhere to live. Ever since inventory started falling in 2014, you could see a problem brewing for 2020-2024. The only thing that can ruin this house party is too much heat on the dance floor, meaning home prices get out of hand too quickly.

During the housing bubble years, we had more inventory and sales. We also had less price growth. From 2020-2022, we had fewer sales and listings, but the price growth was much hotter. Don’t get me wrong; the demand from the past two years is more than the demand from 2008-2019. However, the too-hot pricing velocity was a function of total inventory hitting all-time lows during this period that had good demographics and lower rates.

During the previous expansion, my token line was that we would have the weakest housing recovery from 2008-2019.

However, mortgage rates between 5-6% changed the housing dynamics too, and the demand decreased more noticeably. In the past, when mortgage rates fell, the market stabilized and sales increased. It will be interesting to see whether recent home price growth will limit that stabilizing factor this time around.

I will be very interested to see as mortgage rates fall, which they typically do going into a recession, how much of a stabilizing effect it will have on the housing market.

NEW HOME SALES

The icing on the cake was the market reaction to the invasion and the push-up in some of the inflationary data. All of this indicated that the Federal Reserve would be aggressive in its response. The 10-year yield and mortgage rates then made a historic rise together, resulting in a 2% increase in mortgage rates in a very short period.

Last but not least, you always want to keep an eye on the mortgage purchase application data on a year-over-year basis when thinking about the future of existing home sales. As long as this data is negative, sales have the ca pacity to fall.

Because of the long wait times on a new build, new home sales get impacted more by higher rates. For the same reason, the new home sales market is also more complex than the existing home sales market. The new home sales sector had to deal with lumber prices and delays in getting products. There are still some new homes that are waiting for their garage door to be delivered or their countertops installed.

T 28 ❱ HOUSINGWIRE SEPTEMBER 2022

Our demographics were too old or too young to get total sales over 6.2 million, meaning total housing starts would not begin a year over 1.5 million until 2020-2024.

So, I set a five-year home-price growth limit: As long as home prices only grew 23% in five years, we would be OK. Well, guess what? In just 2.5 years, home prices grew over 40%. This is genuinely savage. The one thing that I feared the most happened — inventory levels broke to all-time lows and we have not returned to 2019 inventory levels.

New home sales also suffered from massive price growth since 2020, so when rates went higher, demand should have cooled down noticeably. The writing was on the wall for a cool-down in this sector as soon as the business

So what does that mean now?

In the past, when rates fell, we never worked from a pe riod when home prices exploded higher as it has over the past 2.5 years.

The housing market changed the moment the 10-year yield broke over 1.94%. This occurred after Russia invaded Ukraine in March, an event that pushed mortgage rates over 4%. In my 2022 forecast, I discussed how mortgage rates could get above 4%, which required global yields to rise, particularly in Germany and Japan, which they did before the Russian invasion.

• 2.24 months of supply hasn’t even been started yet.

As we can see below, the monthly supply has taken off once again, currently at 9.3 months. The builder’s business model is at risk, of course. The builders are here to make money; this isn’t a charity. They don’t put their head in the sand and build, build and build, waiting for buyers to come around and buy a new home. So, naturally, when the monthly supply data breaks over 6.5 months, the builders pause their construction and make sure they can sell their products. This is how a business works: they create something, sell it and make money from it.

• 6.22 months of supply is under construction.

aggressively.Single-family

However, due to the inability to build homes promptly, most of the active supply is either under construction or not even started yet.

29 ❱ HOUSINGWIRE SEPTEMBER 2022

Housing starts and permits have had a good run since the lows in the previous expansion (from 2012-2022). With the rise in new home sales and the need for rent, hous ing permits kept that uptrend going. However, things have changed for the worse here as mortgage rates rose very

• When supply is 4.4 to 6.4 months, this is an OK mar ket for the builders. They will build as long as new home sales are growing.

My rule of thumb for anticipating builder behavior is based on the average monthly supply of new homes over three months: • When supply is 4.3 months and below, this is an excellent market for the builders.

HOUSING STARTS

• The builders will pull back on construction when the supply is 6.5 months and above.

construction is pretty much done until the builders can get rid of their backlog of homes that are in construction. Once that is taken care of, the builders need to feel comfortable building homes again. As we can see, the builder's confidence has collapsed with higher rates. This collapse in builders' confidence is one of my six recession red flags, and I raised it in June as it was evident that the cycle had ended. The builder's housing completion data has looked terrible for some time, so they will take their time now in building those homes.

model of the builders was at risk.

However, we must be mindful of one current reality that differs from the past: Only 0.83 months of supply is actually finished homes.

The builders also had to deal with delays in construction, which meant that people who had qualified for loans with rates around 3% were now being hit with the reality that by the time they were ready to move in, rates would jump onSo,them.naturally, the cancellation rates were going to rise.

The one big difference between now and the peak of the housing bubble years is that new home sales are currently already low on a historical basis. The peak of the housing bubble had roughly 1.4 million new home sales, which meant that production levels were matched to that sky-rocketing demand. Now, new home sales are at 590,000, so the builders are in a much better spot to manage this downturn.

This was the 2019 inventory level, and although that was a four-decade low in inventory, it was a sane marketplace back then. We want a dull and balanced marketplace.

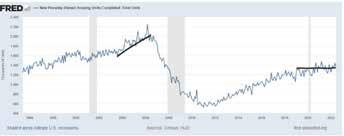

I will keep an eye out on this data line if mortgage rates fall with more intensity. As I make comp adjustments to this data, I can get a sense of when this line is turning for the positive. For now, this isn’t the case.

At some point, we will find a bottoming-out process with pending home sales. Keep an eye out for how the market reacts to lower mortgage rates. Housing data lags, but purchase application data is forward-looking. With that said, pending home sales and existing home sales have trended well together for many years. We might have a few reports here and there where we encounter a demand mismatch. That does occur from time to time, but keep it simple: As pending home sales rise or fall, existing home sales will follow.

With three different refinancing waves since 2012, the homeowner in America looks better than ever on paper.

PENDING HOME SALES

HOME PRICES

Once the 10-year yield broke over 1.94%, I had anticipated 18-22% year-over-year declines in the purchase application data on a four-week moving average. That didn’t happen with 4-5% mortgage rates, but when rates were between 5-6%, we had enough damage to the data to reach my target level.

The weekly data from Redfin and Realtor.com are still showing double-digit median sales listing prices from a year ago. Ouch! Or shall I say, savage! Savagely Unhealthy. This is because we started the year at all-time lows in inventory, and the housing market takes time to adjust prices versus demand.

Just imagine if mortgage rates didn’t rise — where would housing be this year?

This was the core premise of the savagely unhealthy market and why we needed to break out of the all-time low inventory status because nothing good happens when inventory levels are this low.

The National Association of Realtors claims the median sales price is still up double digits as of the last report.

Now that inventory levels are rising, the growth rate in pricing should cool. My rule of thumb during this period has always been that we want total inventory in America to get back into a range of 1.52-1.93 million and get four months of supply to get back to normal.

As I write this, the four-week moving average decline is at 18%; this looks about right to me, but it needed 5-6% mortgage rates to get there.

Below you can see the NAR total inventory data from 1982 to today. Currently, we are at 1,260,000.

PURCHASE APPLICATION DATA

It is also worth noting that homeowners are staying in

30 ❱ HOUSINGWIRE SEPTEMBER 2022

The number of pending home sales continues to fall these days, and as long as mortgage rates stay this high and forward-looking purchase application data is negative year over year, they have room to fall lower.

CREDIT PROFILE Household balance sheets look great for homeowners. Homeowners have enjoyed a fixed long-term debt product while their wages grew over the years.

They have homes they haven’t even started building, so don’t look for many actions on those sites until the homes under construction have more visibility and can be sold promptly.Thebuilders will finish their multifamily construction projects as rental demand will stay firm because the higher rates will convince more renters to stay in their homes and apartments longer than normal.

One thing about this data line is that the comps will be much harder starting in October, as that was when mortgage demand started to pick up last year.

The most savage aspect of housing is that prices are still up year over year, so not only do we get the hit from higher mortgage rates, we don’t get the benefit of prices falling this year to offset those rates. The S&P CoreLogic Case Shiller home price index, which lags the market, is still showing near 20% year-over-year growth in prices as of the end of July on transactions from earlier in the year.

We can see possible 25-35% year-over-year declines at that point just by using more challenging comps.

The halftime show is here, and it’s been a crazy first half for the housing market during this period. It would have been much better if home prices grew 3-4% every year during 2020, 2021 and 2022, but that hasn’t been the case.

Chart source in order of appearance: New York Fed, St. Louis Fed, St. Louis Fed, St, Louis Fed, Fred.

With such excellent cash flow, the FICO score looks impressive because we no longer have any exotic loan debt structures in the system. The most significant difference between the 2008 period versus the 2022 period, is that mortgage credit has looked outstanding for over a decade. Credit stress worsened in 2005, 2006, 2007 and 2008. Then the job loss recession happened, so don’t expect to see similar credit stress because the loans that created that kind of damage were banned post-2010.

their homes longer and longer. Not only have they built up a lot of nested equity, but their cash flow has gotten much better over time. Also, this type of cash flow data works well in a higher inflationary period as their shelter cost isn’t as impacted as a renter, and their fixed mortgage payment doesn’t change. This is why I have stressed time and time again that the homeowner's financial credit risk isn’t significant unless they lose their job. On paper, they have never looked better. Even if they lost their jobs, they’re in a much better spot than the credit risk profiles of American homeowners from 2002-2008. Have I mentioned how hot their cash flow looks?

The homebuilders also pushed it on pricing during this time because they had pricing power. When rates rose, home affordability faced tough issues. Now, we are in a different stage of economic expansion. My six recession red flags are up, which means that his torically, past 1982, bond yields and mortgage rates have fallen into a recession. My job is to not only track housing economic data but track all economic data. Just like what happened before and after the COVID-19 recession with the America’s Back recovery model, I will do my best to create models and a pathway for you to see what the economic data is saying.

31 ❱ HOUSINGWIRE SEPTEMBER 2022

In this day and age, we have a lot of financial noise, both bullish and bearish. This is why economics done right is spoken by Numbersnumbers.can’tlie; people can, but numbers are golden. The issue is always how the numbers are presented. If done correctly, economics is boring. However, when you do it this way, you become a detective.

2022 AWARDS PROGRAM 32 ❱ HOUSINGWIRE SEPTEMBER 2022

Gavin TheresaLeeAmyGeoffreyNicoleDaveHeikeHeatherChelseaLauraJacobTimLisaTammyJoeLauraBrianTanyaKyleRachelKristiJohnJoJoryAmyJohnMarliseAlesAlkhasAslanianAvery............................35BeechEllenBergstromCadyChristian....................36CunninghamDayDeLiaDevlin........................37DiRienzoDombrowskiFahmiFiondella.....................38FoleyGibbsGivnerGoyer......................39HanwackerHellwigHerbstHerold......................40HickmanHuchthausenJelenicKelems....................41 Sarina Kinder Joy HuruySuzieErickKatieAprilSumantAustinCJRobySharonCraigRishiAmandaCalebDebbieTitoAndrewJordanCarrieKarisKnochKoehnKoester....................42LichtLloydLopezMichel....................43MittelstetPriceRanjanRebmann..................44ReichhardtRobertsonRoseRoss........................45SridharanSteeleVinckWilliams....................46WoodwardYohannes.................47 33 ❱ HOUSINGWIRE SEPTEMBER 2022

The HW Insiders award spotlights the industry professionals who are essential to the performance and success of their organizations but may be lesser known to those on the outside. These industry pros are the engines that keep things running smoothly, the secret sauce to their teams’ success. Some other descriptions in this year’s submissions include “unsung hero,” “secret weapon,” “critical to success” and “visionary,” among a slew of other illustrations used to describe these oper ational all-stars. One honoree, CJ Rose, is senior director of strategic growth and acquisitions for OriginPoint, a new mortgage origination joint venture between Guaranteed Rate and Compass. Rose has acquired and recruited talent who have produced more than $3.6 billion in total loan volume for OriginPoint in less than a year. Under the leadership of Tammy Fahmi, the senior vice president of global ser vicing and strategy, the Sotheby’s International Realty brand launched eight new companies internationally and opened nearly 90 new offices around the world, including opening offices in five new territories, which contributed to an interna tional sales volume growth of nearly 60% year over year.

HomeLight chief operating officer Sumant Sridharan’s leadership has raised $645 million in funding, acquired three companies and currently sits at a $1.7 billion valuation. His contributions played a huge role in closing the company’s first $15 million Series A back in 2015, and the company’s most recent $478 million in Series D. It's clear that this year’s winners are driving big growth within their organiza tions and have the metrics to back their successes. Learn more about these and all the other 2022 honorees in the following pages. Congratulations to the 2022 class of HW Insiders.

34 ❱ HOUSINGWIRE SEPTEMBER 2022

Over the last year, Alkhas has led Project Edge. The goal is to ex pand and fortify eXp Realty’s infrastructure as the company has grown to more than 82,000 real estate agents in 21 countries. Throughout the complexities of Project Edge,Alkhas has kept projects organized and moving forward. Colleagues say that she has an innate ability to stay calm and reassure the team in the chaos.

Avery possesses a rare blend of compliance expertise and technical know-how that has allowed her to support Docutech’s operational compliance needs. Her work has enhanced the mortgage lending process for hundreds of lenders, enabling them to implement regulatory change in an accurate, efficient and timely manner. Her expertise in the intersection between regulation and technology runs deep. Early in her career, she wrote the original code to calculate the Annual Percentage Rate in Docutech’s product suite.

John Aslanian Chief Revenue Officer SimpleNexus

35 ❱ HOUSINGWIRE SEPTEMBER 2022

Leveraging his extensive sales leadership experience, he grew his team from six members to 70, designing it to help SimpleNexus expand while helping connect lenders with the tools they need to achieve their desired business results.

Amy Avery Director of Compliance Implementations Docutech, a First American Company

Gavin Ales Chief Compliance Officer DocMagic

Gavin Ales has spent his career in mortgage compliance, working for both lenders and technology vendors. His experience armed him with a unique understanding of the lending process and the compliance complexities buried within it. As chief compliance officer at DocMagic, his responsibilities include tackling the most arduous industry com pliance challenges, and he’s always at the forefront of effectively addressing ever-changing compliance rules, mandates and procedures. Ales’s rich knowledge of compliance adherence and unyielding passion serves as his internal driver to efficiently lead DocMagic’s compliance department and implement tough compliance projects that ultimately help lenders avoid issues. In the last year, he participated in multiple company- and indus try-based projects, including the development of DocMagic’s e-Eligibility Solution, the implementation of ADA capability to assist the blind, the implementation of the Affordable Housing Initiative and on going efforts to move lenders toward a fully digital mortgage process.

Marlise Alkhas

John Aslanian brings decades of experience building high-performing sales teams and leading mortgage technology firms through M&A transactions to the C-suite of SimpleNexus. As chief revenue officer at SimpleNexus, Aslanian has been central to helping the company earn the business of hundreds of enterprise lenders. In the process, Aslanian has expanded the company’s sales team by 1,067% and achieved revenue growth that has landed the company on the Inc. 5000 list of fastest growing companies each year of his tenure.

Senior Finance Project Director eXp Realty Marlise Alkhas joined eXp Realty as a senior finance project director in January 2021. She is an excellent finance technology leader who ex cels at managing business transformations that focus on innovation and automation. She brings 33 years of experience, most recently as a senior manager of global technology solutions for Verizon.

Amy Avery, director of compliance implementations at Docutech, a First American Company, has worked behind the scenes for 22 years to enable mortgage lenders to implement regulatory and industry changes using dynamic document technology. Avery inspires confi dence in Docutech’s internal teams by ensuring they understand the ‘why’ behind compliance changes and how they can be implemented in a way that best serves clients. As a result, her work has enhanced the lending process for hundreds of lenders.

Aslanian joined SimpleNexus three years ago as senior vice president of sales. After just two years in the role, SimpleNexus CEO Cathleen Schreiner-Gates promoted him to CRO, citing his success in expanding SimpleNexus’ user base and aggressive sales growth.

Alkhas is an inspiring and collaborative leader who has been rec ognized for reducing complexity and streamlining data and processes. In addition to overseeing 28 direct reports, she consolidates competing priorities for several departments, including accounting, brokerage operations and technology.

Kristi Christian VP, Legal and Compliance Sourcepoint

36 ❱ HOUSINGWIRE SEPTEMBER 2022

John Cady SVP, Retail Cardinal Financial John Cady has over 30 years of mortgage experience, serving as a leader and mentor to a nationwide team of branch managers. His wisdom and influence have empowered those under his leadership to achieve tremendous growth and offer clients the next-level service that carries forward Cardinal Financial’s record of success.

Jory Beech is a senior operations leader with LERETA, a leading national provider of real estate tax and flood services for mortgage servicers. In this role, Beech is responsible for overseeing LERETA’s tax data procurement and reporting. She oversees a team of 50+ tax specialists nationwide who are responsible for the tactical and strategic process engineering of the company’s principal standard tax products. LERETA’s Standard Tax Service manages escrow and non-escrow portfolios across 24,000 tax agencies. Since moving into her current role with LERETA, Beech has been instrumental in designing procedures, ensuring quality control and streamlining her teams’ workflows. She recently worked with leader ship to restructure the company’s operational teams, increasing the amount of time senior leaders could spend working one-on-one with their managers. This process change led to the team meeting more of their SLAs, better customer service and reduced claims. This year, LERETA has met 99.9% of all SLAs.

Cady joined Cardinal Financial in 2019 as senior vice president of retail. He saw “a challenge and an opportunity” to guide and support the next generation of lending professionals. There’s no doubting that it’s been a remarkable success, with sales teams under his leadership closing over $1.2 billion in loans in 2021. A passionate leader inside and outside the office, Cady is a treasured community volunteer, serving as a youth baseball coach and working with the Rescue Mission.

Jo Ellen Bergstrom VP, Data Acquisitions ATTOM

Kristi Christian, vice president of legal and compliance at Sourcepoint, is a people-centric leader who is focused on helping her team members learn and grow both personally and professionally. She has more than 30 years of experience in the mortgage industry, includ ing underwriting experience. Her compassionate and collaborative leadership style brings people together and helps the organization overcome challenges, achieve high-impact outcomes and thrive. During the past year, in addition to providing top-notch legal and compliance support for internal clients, she played an instrumental role in Sourcepoint’s acquisition of The StoneHill Group. In her role, Christian is tasked with heading contract and litigation management and ensuring regulatory compliance and licensing. Christian’s industry knowledge allows her to go beyond being a law yer and act as a true business partner to internal clients — understanding their challenges, building trust and creating solutions in a timely manner.

Bergstrom’s valuable contributions to ATTOM — now the parent company of RealtyTrac, Homefacts, Home Disclosure, Home Junction and GeoData Plus — have not only paved the way for the company to continue to deliver new data sets to the market to power innova tion but have helped ensure that the company continues to deliver on its mission of serving as a transformative information and data services organization that fuels innovation, growth and strategy for its customers.

As vice president of data acquisitions for ATTOM, Jo Ellen Bergstrom manages a critical resource team comprised of over 50 entities na tionwide that supply foreclosure, neighborhood and MLS data to the ATTOM data warehouse. With over 35 years of experience, and 18 of those years at ATTOM, Bergstrom’s experience in foreclosures has largely contributed to making ATTOM the go-to source for foreclosure data and her assistance on numerous data acquisitions has further solidified ATTOM as the one-stop shop for premium property data.

Cady has prepared his teams for the shift from refinance to pur chase and enoucraged creativity. Thanks to Cady, technology and innovation are at the forefront of these efforts and Cardinal Financial’s sales teams are prepared to take on the industry’s future challenges.

Jory Beech Senior Operations Leader LERETA

Cunningham’s team focuses their efforts to both grow and retain Sales Boomerang’s customer base. Cunningham is, directly and in directly, responsible for many of Sales Boomerang’s growth metrics. In 2021, Sales Boomerang saw a record 5.1% growth in its customer base while executing 56 customer renewals for millions in contract value. She also created a Planning for Partnership program, resulting in strategic conversations and significant growth of key clients.

Brian Devlin Managing Director, Capital Markets Finance of America Mortgage

Kyle Day VP, Customer Success OJO Labs

Rachel Cunningham Director of Customer Success Sales Boomerang

As vice president of customer success, Kyle Day is fundamentally improving the homeownership journey for consumers. Since joining OJO Labs, Day has developed and scaled four teams within the customer success organization that are responsible for supporting and bettering the performance of OJO’s network of more than 30,000 agents. From recruiting new agents to deploying successful training campaigns, and improving back-end lead processes, Day and his team are instrumental to the success of OJO’s agents and consumers. Since joining OJO, Day has launched and scaled four agent-support teams, ensuring each one works to deliver the best support to agents. To ensure that OJO partners with and matches consumers with the best of the best, Day worked to create a recruitment model focused on finding mission-aligned agents while still empathizing with consumers in today’s complex housing market. As a result, OJO’s exclusive referral network of agents, The OJO Select Network, has grown to more than 30,000 agents across the U.S. since it launched in 2020.

As director of customer success, Rachel Cunningham’s passion for ensuring the long-term success of Sales Boomerang and its customers is evident not only to her team and the company but to its clients as well. Her commitment to the Sales Boomerang ethos “No Borrower Left Behind” is clear as she works diligently day in and day out for the betterment of everyone around her. Cunningham’s influence can be felt by Sales Boomerang’s customers in their pipeline growth and increased customer retention as well as by Sales Boomerang itself in its customer and revenue growth.

37 ❱ HOUSINGWIRE SEPTEMBER 2022

Tanya DeLia Single-Family VP, Automated Underwriting Risk Assessment Freddie Mac Tanya DeLia, single-family vice president of automated underwrit ing risk assessment at Freddie Mac, is an impactful and innovative technology leader serving the housing industry. She leads efforts on a variety of groundbreaking technology solutions that directly benefit lenders by shortening cycle times and reducing costs. Lenders overwhelmingly provide positive feedback because they are success fully leveraging the Freddie Mac technology solutions that DeLia has championed.DeLiaplays an integral role in bringing innovative solutions to market and her tenacity is proving to the industry that Freddie Mac’s data-fueled solutions reduce lender costs and deliver a better borrower experience while effectively managing risk. She oversees the appraisal modernization efforts to create a spectrum of collateral valuation options. This work includes automated collateral evaluation appraisal waivers that help borrowers save money on their appraisals and help lenders save time on their loans.

In his 19 years in the mortgage industry, Brian Devlin has become one of the most connected capital markets leaders — if a person in the mortgage industry is buying or selling a loan, Devlin knows them well. As managing director of capital markets at Finance of America Mortgage (FAM), Devlin’s relationships with Wall Street traders and national and community banks allow him to keep his finger on the pulse of our industry’s recent volatility. His knowledge, expertise and foresight keep FAM ahead of the curve. He keeps its employees informed with total transparency during weekly all-organization town hall meetings. A lot of what Devlin does is behind the scenes, however, as he’s a large part of the rudder that turns the ship. Devlin has been responsible for changing FAM’s lending landscape and capabilities. He created strategic advantages that made FAM more flexible and able to operate independently by bringing all trading and hedging in-house. Devlin also established over 20 new trading counterparties for mortgage-backed securities and whole loans.

Tammy Fahmi is the senior vice president of global servicing and strat egy for the Sotheby’s International Realty brand. She is responsible for all matters related to U.S. and international affiliated companies. Fahmi also managed the brand’s growth internationally, opening offices in five new territories, which contributed to an international sales volume growth of nearly 60% year-over-year. The Sotheby’s International Realty brand launched eight new companies interna tionally and domestically in 2021 and opened nearly 90 new offices around the world.

Tammy Fahmi SVP, Global Servicing and Strategy Sotheby’s International Realty

Fahmi supported affiliated companies as they grew their business es, which achieved a record $204 billion in 2021 global sales volume. The brand’s U.S. sales volume grew by 33.8% year over year, significantly outpacing NAR’s national increase of 20.6% from the prior year. To further grow the brand, Fahmi worked on significant retention efforts of affiliate companies, securing more than $700 million in domestic renewals.

Laura DiRienzo, vice president of origination title and close at ServiceLink, has spent her 20-year career learning the ins and outs of the origination, title and close business. Since starting at ServiceLink, she has held just about every position that touches the life cycle of a loan within the origination group. DiRienzo isn’t comfortable doing the bare minimum of her job function and goes above and beyond gaining a knowledge of ServiceLink’s business. Never one to expect the spotlight, DiRienzo is one of the unsung heroes within the ServiceLink organization. She wears many hats, overseeing the work product of six divisions — operations (Texas location), policy, claims, escalations/risk, doc audit and QARR (quality assurance rejection resolution) — and 33 employees. Components of her role include risk mitigation, process improvement, developing and conducting employee and client training (digital and in-person) and ensuring back-end processes run smoothly for clients and that employees are providing a top-notch customer experience.

Joe Dombrowski

As Senior Director of Product Management at Sagent, Joe Dombrowski is responsible for powering trillions of dollars in loan balances for America’s top mortgage servicers. Dombrowski is highly technical and a translator who leads his team to build great experiences to serve not just homeowners, but lenders, banks, investors, GSEs, reg ulators and ecosystem partners. Dombroski is a key driver and secret weapon in Sagent’s journey to being the housing industry’s most modern, homeowner-first ser vicing fintech. His three decades in the servicing and tech trenches inspires and educates Sagent teams and customers. Thanks to the work of Dombroski and his team, 84% of servicers on Sagent said they can service more loans with Sagent than another platform, 82% of servicers believe Sagent’s real-time data has a material impact on their operations and customer service, and 90% of servicers on Sagent believe LoanServ saves time relative to similar options in the marketplace.

Upon joining ICE Mortgage Technology in 2021, Fiondella had an immediate impact. With over 25 years of leadership experience in B2B and B2C data and analytics, she brought a fresh perspective to the data and analytics business and has since grown its projected revenue by an astounding 50%. Her strategic thinking, combined with a deep knowledge of the consumer data market and data product development, has enabled her to tackle several large projects over the past year. Fiondella worked closely with the MERS team to enhance the quality assurance and risk management services that protect members by ensuring high data quality on the MERS system.

As vice president of product management for data and analytics at ICE Mortgage Technology, Lisa Fiondella is driving innovation with an impact that goes well beyond her product line. She is known for being a gracious and empowering leader by both her team and her peers. Fiondella fosters a culture across her organization that focuses on speed, agility and innovation, while never sacrificing quality.

Senior Director of Product Management Sagent

38 ❱ HOUSINGWIRE SEPTEMBER 2022

Lisa Fiondella VP, Product Management - Data & Analytics ICE Mortgage Technology

Laura DiRienzo VP, Origination Title and Close ServiceLink

Chelsea Goyer National Head of Brokerage Opendoor

Tim Foley EVP Anywhere Real Estate

Tim Foley serves as the executive vice president, brokerage and franchise operations, for Anywhere Real Estate. In his role, he oversees op erations, data insights and lead generation for the company’s owned brokerage and franchise brands. These comprise nearly 21,700 offices and approximately 388,000 independent sales associates around the world. Foley works to implement business strategies and strategic ini tiatives that drive growth and provide innovative services for agents that focus on tool adoption, commission analytics and business in telligence. Foley’s work is the backbone for agent productivity and quality of life throughout the organization. Agent satisfaction and exceptional agent experiences are high pri orities for Foley and have led to the creation of many cutting-edge services to reduce costs and improve productivity among agents.