HANDBOOK Powering shipping’s emissions-cutting ambitions Propulsion stream | Alternative fuels stream | Technical visit Two days of conference streams exploring compliant technology & fuel solutions to meet IMO’s 2050 milestone and EU’s Fit for 55 proposed tandem regulation, specifically the journey to 2030 shore power. This year the programme will also feature sessions on eFuels & Bio Fuels, Ammonia, Methanol and Multifuel engines. While providing industry leaders a space to network and knowledge share. Chairmen: Lars Robert Pedersen, Deputy Secretary General, BIMCO Reinhard Lüken, Managing Director, VSM German Shipbuilding and Ocean Industries Association visit: propulsionconference.com contact: +44 1329 825335 email: conferences@propulsionconference.com #MotorshipPFF

Organised by: MOTORSHIP INSIGHT FOR MARINE TECHNOLOGY PROFESSIONALS THE 22 24 Hamburg Germany NOV 2022 2022 43RD Supported by: Sponsored by: Headline Sponsor Silver Sponsors

Le Meridien Hotel, Hamburg, Germany

Headline Sponsor :

What determines the maritime fuel mix of the future?

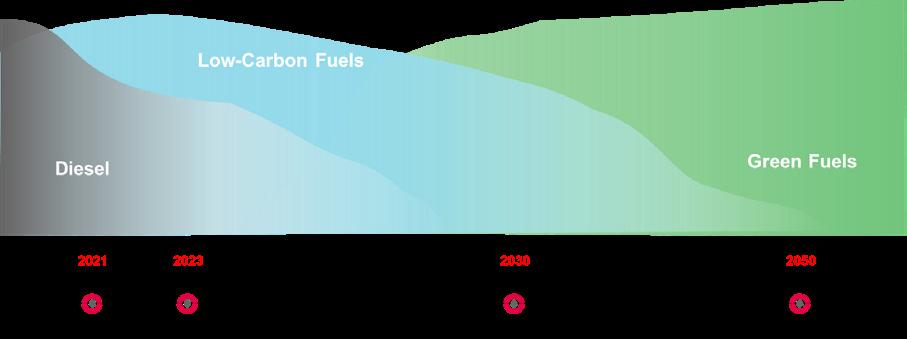

By 2030, 5% of the energy for shipping should come from carbon-neutral fuels. The new Maritime Forecast to 2050 report outlines under what conditions each new possible fuel type will proliferate and what production, distribution and bunkering infrastructure investments are required. Download your free copy. dnv.com/maritime-forecast

NICK EDSTROM Editor, The Motorship

NICK EDSTROM Editor, The Motorship

Dear delegates,

Welcome to the latest Motorship’s Propulsion & Future Fuels Conference. We are delighted to welcome our attendees back to Hamburg, after last year’s enforced sojourn in Copenhagen.

Our conference has covered innovations in the marine fuels and propulsive technologies field since 1979, and offers a unique opportunity for shipowners, OEMs and other interested parties to come and keep track of the regulatory, technical and market developments in the gaseous fuels market. We are excited to bring together a strong programme of leading industry experts, class society specialists and a number of ship owner sand ship operators. Our focus on gaseous and alternative liquid fuels, including ammonia and methanol, and the rapid pace of developments since our last conference means that regulatory and technical themes are more topical than ever.

Our conference opens with a topical High Level Panel discussion, which will cover the expected impact of requirements for shore-power infrastructure development under the Alternative Fuels Infrastructure Regulation (AFIR), as well as the FuelEU Maritime Regulation which will come into effect in 2025, imposing life cycle GHG footprint requirements on the energy used on board ships.

The major change in the years since our conference was last held in Hamburg is the amount of investment that is flowing into upstream developments for the production of biofuels, renewable hydrogen, ammonia and methanol.

The concurrent introduction of upstream fuel (or hydrogen vector) production with dualfuel vessels capable of operating on methanol (or ammonia from 2024) will lead to profound changes in the fuel mix used in the deep-sea shipping market. Similar changes are occurring in the LNG market, where bio-methane and subsequently synthetic LNG, are likely to reduce GHG emissions from the market.

It is fascinating to see how the order of methanol and ammonia-fuelled vessels by a number of progressive shipowners and cargo owners is creating demand for methanol and ammonia, which in turn is spurring investment in the production of fuels by others. Far from being part of the problem, shipping is acting as an enabler for the faster introduction of solutions.

3 Welcome Letter 2022 43RD

We include a number of technological case studies from shipowners and technology partners who have adopted innovative technologies. The shortlist for the editor’s award focuses on four innovative projects that have demonstrated the potential for GHG emission savings, including

Egil Ulvan Rederi’s zero-emission self-discharging hydrogen-fuelled bulk carrier design, With Orca; Hoegh Autoliners’ multi-fuel and zero carbon ready Aurora Class vessel; the Northern Lights’ liquid-CO2 carriers in carbon-transport-and-storage project; a series of hybrid DF PCTC vessels for NYK Line and Wärtsilä’s retrofit-optimised solution to convert existing 2-stroke electronically-controlled engines to run on either LNG, methanol or ammonia.

Once again, we are fortunate enough to be joined by a strong programme of leading industry experts, class society specialists and ship owners and ship operators.

Our thanks go to our dedicated and knowledgeable advisory committee members and our kind sponsors, including Gold Sponsor DNV and Silver Sponsors Accelleron and GTT, without whom this event could not have taken place.

It is our hope that our conference permits an exchange of ideas around the decarbonisation issue. I wish you a productive, illuminating and thought-provoking few days in Hamburg and I look forward to witnessing, as always, a generous exchange of ideas.

Yours sincerely, Nick Edstrom Editor, The Motorship

Welcome Letter 4

LARS ROBERT PEDERSEN Deputy Secretary General, BIMCO

Dear delegates,

Once again the time has come to welcome you all to Hamburg and the 43rd Propulsion and Future Fuels conference.

While I write this the world is gathering in Sharm El Sheikh, Egypt for the 27th conference of the parties to the UNFCCC to discuss how climate change can be tackled effectively. Climate change is the overarching challenge now and in the future for all sectors of society – and that includes shipping.

We will continue to explore options to fuel future ships in a carbon limited world.

This year we take a closer look at some of the regulatory initiatives which will likely affect shipping in the coming years. We will also explore deeper some of the new fuels. Energy transition is all about electrification. Green sustainable electrons deployed in the grid or to produce sustainable Hydrogen.

We will explore some of the electric applications in shipping such as shore power, hybrid propulsion, and generation onboard ships.

What role will digitalisation play in decarbonising shipping? We will dive into this aspect in a dedicated session on digital and other future technologies.

Decarbonisation also have to be good business. That is why we will explore the state of economic measures to close the price gap between old and new solutions.

Lastly, but not least the Motorship Award will be given to one of the five projects in the run-up.

As always I look forward to helping you manoeuvre the many different aspects presented in the 2-day packed program of 2022PFF.

Yours sincerely, Lars Robert Pedersen Deputy Secretary General, BIMCO

Chairman’s Welcome Letter

5

2022 43RD

REINHARD

LÜKEN

Managing Director, German Shipbuilding and Ocean Industries Association (VSM)

Dear delegate,

A warm welcome to you all attending to for the 43rd edition of the Propulsion & Future Fuels Conference here in Hamburg.

International shipping accounts for the lion’s share of the global transport volume - 90 per cent of world trade is carried by sea. Ships are by far the most efficient mode of transport, but with a total annual consumption of around 350 million tons of conventional fuels, they are also responsible for almost three per cent of global greenhouse gas emissions. This immense fuel demand predestines shipping to be a pioneer in exploiting the market potential of synthetic, climateneutral fuels and enabling their widespread use in other sectors of the economy as well.

Together with our Colleagues from VDMA VSM has tabled a PtX Roadmap for the maritime energy transition describing the technological and required regulatory levers to achieve the ambitious climate targets.

New fuel and propulsion solutions are a necessary requirement on our path to climate-neutral shipping. However, for the road to success efficiency and energy saving will be key. We need to reinvent the entire system ship. For innovative minds these are exciting times!

This conference will provide you with great opportunities to listen, to present your ideas, and to listen to others, to learn, to discuss and to exchange views on challenges and opportunities. I wish you fruitful days and a great time in the city of Hamburg.

Yours sincerely, Reinhard Lüken Managing Director, German Shipbuilding and Ocean Industries Association (VSM)

Chairman’s welcome letter

6

2022 43RD

Move further

Contents 8 Contents Welcome Letter............................................................................................................................................... 03 Welcome Address .......................................................................................................................................... 05 Lars Robert Pedersen, Deputy Secretary General, BIMCO Chairman’s Welcome 06 Reinhard Lüken, Managing Director, German Shipbuilding And Ocean Industries Association (VSM) Gold Sponsor Welcome ........................................................................................................................... 12 Rasmus Stute, Area Manager, DNV DAY 1 TUESDAY, 22 NOVEMBER 2022 Keynote Panel: ShorePower ................................................................................................. 14 Session 1 Electrification for big ships .................................................................. 22 Session 2 Digitalization, digital efficiency and the future technology of the maritime sector ............................ 44 Session 3 The Motorship Awards ............................................................................ 71 DAY 2 WEDNESDAY, 23 NOVEMBER 2022 Session 4 Carbon Levy Solutions ........................................................................... 90 Session 5 Market Based Measures ...................................................................... 112 Session 5.1 eFuels & Bio Fuels .................................................................................. 114 Session 5.2 Sustainability through alternative fuels ...................................... 142 Session 6 Alternative Fuels..................................................................................... 166 Session 6.1 Ammonia .................................................................................................... 168 Session 6.2 Methano ...................................................................................................... 187 Session 7.1 Multifuel Engines.................................................................................... 213 Session 7.2 Retrofit Solutions .................................................................................... 254

Passion for innovation and technological excellence serving a sustainable world

With almost 60 years of experience, GTT is the partner of choice to design cutting-edge technological solutions for an improved energy efficiency. We bring our passion for innovation and our technical excellence to the service of our customers, in order to meet their transformation challenges both for today and tomorrow.

Our expertise goes from LNG ships to LNG-fuelled ships. We support all your LNG related operations, train and assist your crews to optimise your vessel economics. As shipping is turning digital, GTT Digital proposes Shipping Solutions, combining our experiences and skills to offer a wide range of digital services to the maritime industry.

The GTT teams are at the heart of our mission. Committed and united, we are determined to contribute to building a sustainable world.

gtt.fr © Joseph Lynch

LARS ROBERT PEDERSEN Deputy Secretary General, BIMCO

BIOGRAPHY

Deputy Secretary General Lars Robert Pedersen is responsible for BIMCO’s technical and operational activities involving all technical and nautical issues within the area of marine environment, ship safety and maritime security.

Lars Robert is furthermore responsible BIMCO’s activity related to regulatory developments relevant for shipping at international, regional and national levels. He joined BIMCO In early 2010 after a long career at A.P. Moller-Maersk. For more than 25 years he was involved in regulatory affairs at IMO level, technical management of the Maersk fleet of container ships and prior to that as seagoing engineer officer. Lars Robert holds an unlimited Chief Engineers license.

Chairman 10

REINHARD LÜKEN

Managing Director, German Shipbuilding and Ocean Industries Association (VSM)

BIOGRAPHY

After five years at the executive office of the Treuhandanstalt in Berlin, the German privatisation agency, Mr. Lüken joined the Meyer Shipyard in Papenburg, Germany in 1998, taking charge of politics and strategy.

In 2000, the Community of European Shipyards Associations (CESA) appointed him first as Brussels Representative and half a year later as Secretary General.

As the first Secretary General of SEA Europe he managed in 2012 the formation of the new joint association for shipyards and marine equipment producers. He then returned to his home country to take the helm at the German association.

Mr. Lüken chairs the SEA Europe Market & Trade Committee since 2015, represents CESA as its Chairman, and was elected as President of the German Maritime Centre at its inauguration in 2017.

Mr. Lüken holds a PhD in political science, economics and sociology.

Chairman 11

RASMUS STUTE

Area Manager, DNV Maritime

BIOGRAPHY

A naval architect, Rasmus Stute has worked for DNV for the past 18 years in different management positions both in Asia and Europe. Before being appointed as Area Manager for Germany, he worked to develop the new Containership Excellence Centre in Hamburg and was its founding Director, before taking the lead of the German Business Development team in 2020. Mr Stute is also currently a member of BIMCO’s marine safety and environment committees.

Gold Sponsors Welcome

12

Engineering state-of-the-art Gas Systems for the Maritime Industry

TGE Marine Gas Engineering is the leading liquified gas systems‘ provider specialising in cargo handling systems for gas carriers (LPG, LEG, NH3, Ethane, CO2 & LNG), FSRUs and bunker vessels, including tanks.

Furthermore, TGE Marine is a pioneer in fuel gas systems for LNG, NH3 and other alternative fuels. The company has been contracted for more than 250 gas handling, fuel gas and storage systems globally.

Fuel Gas Systems

LNG, LPG, Ethane, NH3 and other alternative fuels, including storage

• LPG / Ethylene and other Gas Carriers

Gas handling and storage systems for LPG, LEG & CO2 carriers

• LNG / NH3 Shuttle Tankers & Bunker Vessels

Cargo handling and fuel supply systems as well as type C storage solutions

• Floating Storage Units

FS(R)Us & F(P)SOs

• CO2 Carriers

Shipping of and floating solutions for Carbon Capture & Storage

www.tge-marine.com

Fuel Gas Systems Floating Storage & Regasification Units LNG Tankers (Shuttle Tankers & Bunker Vessels) LPG / LEG / CO2 CO2 Carriers

Innovations for Greener Shipping The Gas Experts

The journey to 2030 with Shorepower

14

KEYNOTE PANEL

RICARDO BATISTA

Policy Officer, Directorate-General for Mobility and Transport European Commission

BIOGRAPHY

Naval Architect and Marine Engineer, specialized and working in sustainable energy systems for ships. Currently working at European Commission, Directorate-General for Mobility and Transport – Maritime Transport unit. In the Commission, Ricardo is engaged in the development, negotiation and preparatory work for implementation of the FuelEU regulation, under the Fit for 55 package. In addition, In DG-MOVE, Ricardo is also the chair of the European Sustainable Shipping Forum on Sustainable Alternative Fuels & Power Systems for ships (ESSF – SAPS), an expert group assisting the Commission with all different aspects related to the development, promotion, identification of barriers and scientific discussion related to alternative fuels and power systems. At international level, Ricardo is part of the IMO working group on development of the IGF Code and associated interim guidelines for the safe use of alternative fuels.

Before joining the European Commission, Ricardo worked in the European Maritime Safety Agency (EMSA) for seven years, responsible for technical and scientific support to the Commission on several topics of Ship Safety and Sustainability/Pollution Prevention.

In addition to the above, Ricardo has Classification Society experience, having worked in the American Bureau of Shipping (ABS), in London, integrating the Advanced Analysis team, as well as previous experience as a Marine Engineer onboard naval ships and Naval Architect responsible for shipyard/dockyard work.

Keynote Panel – Speaker 1

15

VALTER SELÉN

Senior Policy Advisor Sustainable Development, Cruise and Ferry Network, EcoPorts Coordinator, ESPO

BIOGRAPHY

Valter Selén joined ESPO as senior policy advisor for sustainable development in June 2020, having previously worked with drafting the first annual EU MRV Report during his time in the European Commission (DG CLIMA). Valter dedicates his career to EU climate policy and sustainable development, focusing his attention on the maritime sector.

Valter holds a double-degree Master in European Governance from the University of Utrecht, The Netherlands and Konstanz University, Germany. Valter wrote his thesis on how European business associations gain access to EU institutions in order to influence climate policy negotiations.

Keynote Panel – Speaker 2

16

MARTIN KRÖGER

Chief Executive Officer, VDR German Shipowners’ Association

BIOGRAPHY

Since 2012 Martin Kroeger is Managing Director of the German Shipowners’ Association, VDR, and a specialist in international shipping policy and related government affairs management. He has worked in the international maritime community for over a decade and serves as a leading industry representative to many international and intergovernmental organisations.

Martin also holds the position of Managing Director of the German Shipping Foundation, a facility founded to co-sponsor training and education of seafarers in Germany. Martin is delegated member to several European and international maritime related advisory committees and expert groups. As alternate member of the Board of Directors of the European Community Shipowners Association - ECSA in Brussels and acting Chairman of the ECSA Safety and Environmental Committee, he actively engages in EU policy making for the maritime sector.

Before joining VDR, Martin worked as Managing Director for the Association of German Seaports Operators and was actively involved in the work of the Federation of European Private Port Operators – FEPORT in Brussels. Martin was admitted to the bar of the State of Hamburg in Germany as attorney-at-law (Rechtsan-walt) in 2007. In the same year, his law and consultancy practice was founded, headquartered in Hamburg, Germany.

Martin was educated in Germany and Australia before he graduated in 2001 from the University of Hamburg in Germany with a degree in Law and Legal Studies. In 2003 he earned a Master of Laws degree in Shipping Law with honours at the University of Cape Town. Martin has been awarded with the Capt. Bob Deacon Shipping Law Prize of the University of Cape Town in 2004. In 2006 he was awarded with a Doctor of Laws (Dr. jur.) by the University of Hamburg in Germany.

Martin is an alumnus of the Harvard University’s John F. Kennedy School of Government executive education program on International Trade Policy, which he successfully concluded in 2016, and the programme on Climate Change and Energy, which he successfully concluded in 2019.

Keynote Panel – Speaker 3

17

DR. KAI-DIETER CLASSEN Deputy Director External Affairs, Hamburg Port Authority

BIOGRAPHY

Kai-Dieter Classen studied jurisprudence in Kiel, Stockholm, Ham-burg and Berkeley. He holds a PhD degree (Doctor iuris) from Hamburg University in European Law and a Master of Laws (LL.M.) degree from University of California at Berkeley in US and International Law. He worked as a graduate research assistant at the Universities of Hamburg and Berkeley, as a private lecturer and as a lawyer. Dr. Classen then became an official for the Ham-burg State Government. He served i.a. as a National Expert in the EU Commission’s Legal Service in the field of International Trade Law. In 2012, he joined the Hamburg Port Authority’s (HPA) In-ternational Affairs Division. There, he works as a senior strategic legal and policy advisor with a broad range of topics.

Dr. Classen is a member of the Legal Committee of the International Association of Ports and Harbors (IAPH) as well as of the Legal Advisory Committee and the Port Governance Committee of the European Seaport Organization (ESPO).

As an adjunct professor at Hamburg University’s Law School he teaches WTO-Law and European Seaports Law and is a Member of the Board of Examiners for European and International Law. He publishes frequently on port- and shipping-related topics.

Keynote Panel – Speaker 4

18

WOLFRAM GUNTERMANN Director Regulatory Affairs Fleet,

Hapag-Lloyd AG

BIOGRAPHY

Captain Wolfram Guntermann graduated with his Masters Licence at the Marine Polytechnic Elfleth/Germany in combination with a scholarship at the Plymouth Polytechnic of Marine Science. He also received his Engineers Licence at the Hamburg Polytechnic in order to serve as Ship Operation Officer holding a dual licence.

After having set his feet for the first time on deck a vessel in 1979 he went through the ranks receiving his first command as Master in 1996. He also took various assignments ashore as Trio Tonnage Center London and Director Marine Operations in the Hapag-Lloyd America Office in Piscataway/New Jersey for almost nine years.

After repatriation to the Hamburg based Headquarters the current function as Director Regulatory Affairs was taken with a lot of challenging opportunities emerging in light of new environmental legislation and initiatives.

Keynote Panel – Speaker 5

19

BIOGRAPHY

TORSTEN SCHRAMM

President Maritime, DNV

Torsten Schramm is the President of DNV Maritime.

Mr Schramm joined Germanischer Lloyd in 1989. He held a number of positions within the company including the role of Principal Surveyor for Japan, Area Manager for China, Region Manager for Europe, the Middle East and Africa as well as Chief Operating Officer.

A Marine Engineer by training, Mr Schramm served on board Gas Carriers before joining GL, rising to the rank of Chief Engineer.

Mr. Schramm also represents DNV on the Council of the International Association of Classification Societies (IACS).

Keynote Panel – Speaker 6

20

A smarter perspective

wingd.com

on a low carbon future

Electrification for Big Ships

22

SESSION 1

DR. TORSTEN BÜSSOW Managing Director, Electrical & Power Systems Business, Wärtsilä

BIOGRAPHY

Dr. Torsten Bussow manages Wärtsilä’s electric & power systems business which includes electric drive solutions such as diesel-electric, hybrid, zero emission,shaft generator and shore connection systems. He has been bringing newtechnologies, often around digital innovations, into shipping for over 13 years as businessunit director in DNV GL and Wartsila. Before that he ran digitalisation and strategytransformation projects in a global consultancy brand.

Speaker

23

STEFAN GORANOV General Manager, Sustainability Solutions, WinGD

BIOGRAPHY

In his current role, Stefan is responsible for sustainability advisory and creating value-based solutions that improve the environmental and financial performance of ships operations through electrification and digitalisation.

His career in the maritime industry has spanned over 20 years, where he has held various technical and managerial positions.

Today, Stefan’s team advises ship owners, operators, charterers, and financers in the field of sustainability in the maritime industry – from technical and economic assessments, to defining system features and user experience. They also develop and deliver turn-key energy efficiency solutions for new and existing ships, tailored to concrete requirements.

Speaker

24

SIMONE BERNASCONI

Head of Global Product Line Upgrades, Accelleron

BIOGRAPHY

Simone heads Global Product Line Upgrades, a cross-functional product line focusing on supporting owners and operators in achieving higher operational efficiency with lower fuel consumption while meeting environmental regulations.

Simone began his career at ABB Turbocharging in 2008 as an application engineer. He later led Engine & Turbocharging Systems in Technology, following which he joined the Service organization and held several positions before leading the Upgrades team, a position he has held since 2020.

Simone holds a master’s degree in mechanical engineering from the ETH Zurich and a Certificate of Advanced Studies in Corporate Finance from the University of Zürich.

Speaker

25

Turbocharging solutions to support the decarbonization journey

ABSTRACT

To support shipping’s journey towards decarbonization, easy-to-implement turbocharger technology can play an important role in reducing the CO2 footprint of existing installations. But to achieve any significant impact, wide market adoption is key. Combining greater efficiency with a sound business case will be vital to maintaining a competitive edge in a low carbon world.

INTRODUCTION

Maximizing the fuel efficiency of merchant vessels has always been a key goal of the shipping industry. Fuel costs are the major operating expense in marine transport [1] and have risen meanwhile to dramatic high values.

However, there is a new aspect that has joined the game: the decarbonization mega-trend is gaining momentum at fast pace and further enhances the need for improving transport efficiency.

Ambition loop and disruption of transport sector

The development of the long-term decarbonization ambition of virtually all players in the maritime industry has been showing unprecedented expansion in the last 5 years.

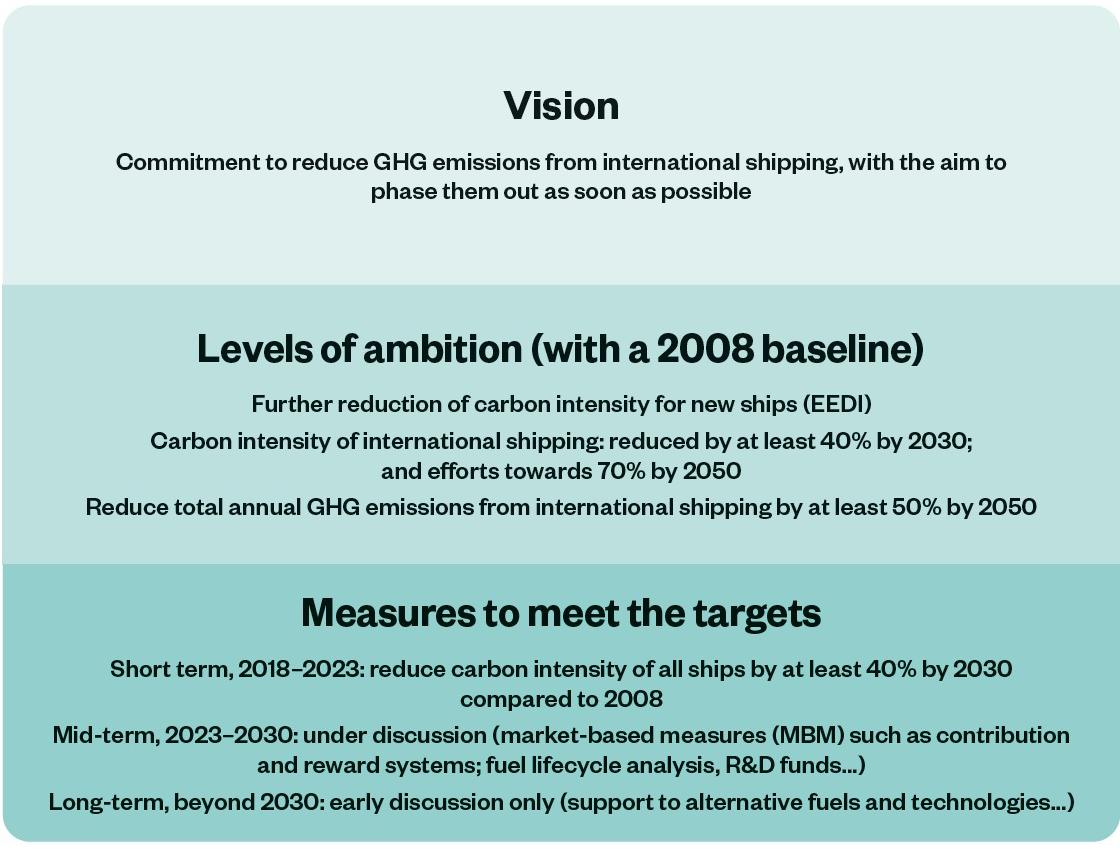

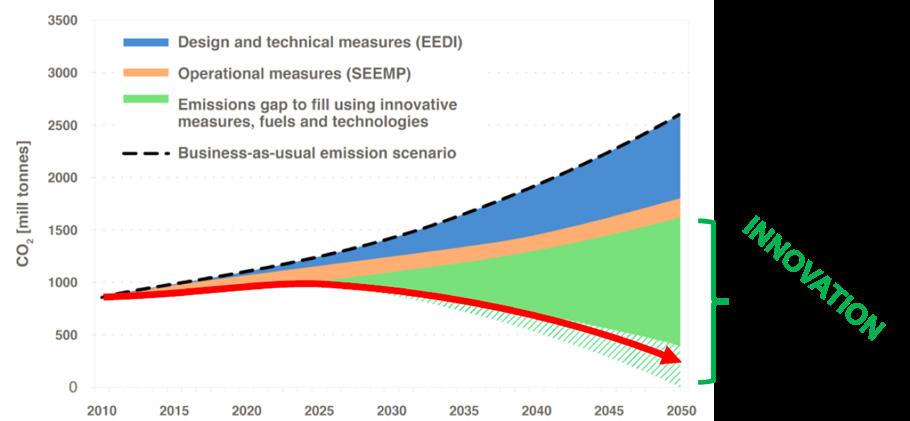

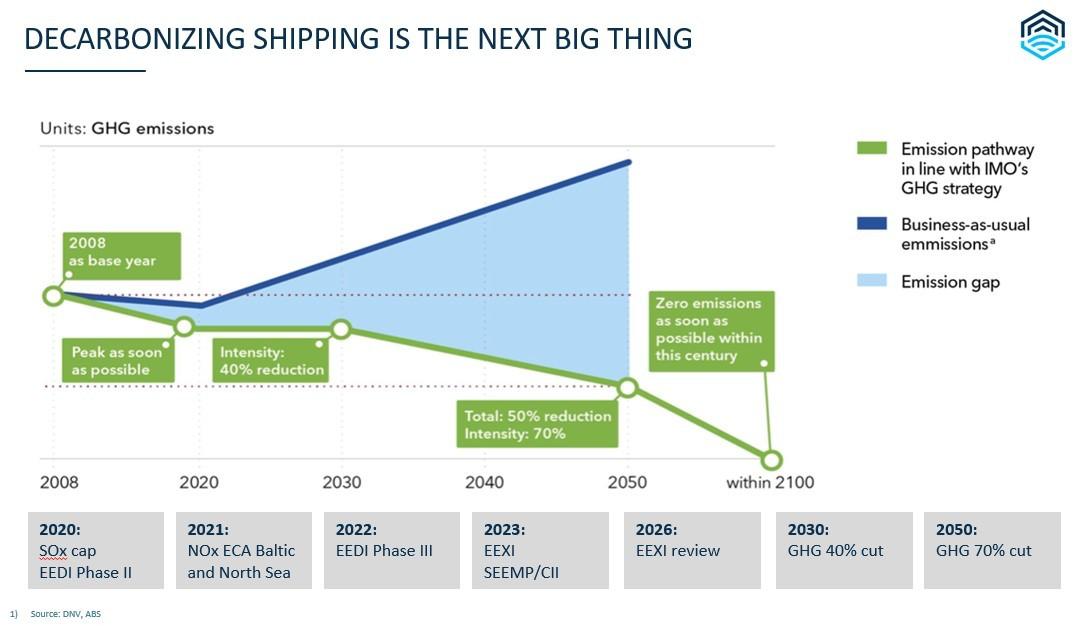

One of the first game changers was formulated by the IMO in 2018, targeting a reduction of CO2 per transport work of 40% by 2030 when compared to levels in 2008, and an absolute reduction of 50% by 2050 irrespective of the (increased) globally transported volume [2].

Figure 1: IMO decarbonization goals [3]

Back in 2018 those targets were perceived by many with skepticism: being too strict, costly and not realistic. Many players in the maritime industry were questioning why shipping should decarbonize at all.

Looking at the market nowadays, only 4 years later, we now observe a completely different picture. An ongoing, continuous ambition loop towards considerably stricter targets supported by key players across the industry. Meanwhile, decarbonization is not only accepted, but also expected.

Conference Paper 26

An increasing number of customers in marine transport (e.g. Nike [4] and IKEA [5]) are openly declaring commitment to improving their environmental impact and decarbonizing their supply chain. Financial institutions like bank and insurance companies are defining frameworks as e.g the Poseidon Principles for banks and insurances [6] to enforce the compliance of their financed / insured portfolio of ships with the 2050 IMO global GHG emission target. Local and regional regulation as well as taxonomy are being defined and we can expect them to enter into force in the next decade, e.g. the fuel GHG standard FuelEU Maritime [7] and the inclusion of shipping in the EU ETS [8]. Global efficiency standards will be tightened and enhanced in the coming years [9], e.g., IMO’s EEXI [10] and CII[11]. These regulatory developments will further accelerate the decarbonization of the maritime industry.

Overall, the commercial, political, and social pressure on the maritime industry to reduce the environmental impact is high and we expect it to grow exponentially. The disruptive innovation of the energy and transport sector has started.

[6]

DECARBONIZATION APPROACHES FOR THE MARITIME INDUSTRY

In spite of showing the lowest specific CO2 emission per weight of transported goods [12] and distance as well as of having achieved solid specific emission reductions in the last decades, the maritime industry doesn’t have the image of being clean. The global perception is rather negative, often seeing maritime transportation as dirty and from time to time even non-compliant.

The expectation on our industry is high, and we - as the maritime industry - are expected to make the difference in the future. Key to success are two main aspects that must be considered and can’t be ignored when it comes to decarbonization: a holistic approach and wide adoption.

1) Holistic approach

Decarbonization needs to be implemented throughout the whole value chain, considering the overall CO2 emissions and environmental impact. Drawing the system boundary on the vessel and focusing only on downstream emissions stemming from its chimney (tank-to-wake) is not sufficient [13]. The origin of the fuel and the grey energy involved (well-to-wake) need to be considered to avoid distortion and in the worst case, global increase of CO2 emission despite of clean shipping on paper. Such life-cycle considerations, although being highly complex, are paramount to a sound decarbonization journey.

2) Wide adoption

Unlike the local character of NOx emissions, CO2 and its effect on climate plays a global role. The decarbonization targets are ambitious and consequently, to achieve a perceptible global impact, solutions for decarbonization and efficiency improvements must be widely adopted. Flagship projects are required for showcasing new technology, but their direct global impact is marginal. It is pivotal to success that technology demonstrations become widely adopted

Conference Paper 27

Figure 2: Carbon intensity target and trajectories for the global fleet [gCO2/tnm]

standards within a reasonable timeframe. This may be achieved by considering global availability as well as affordability from the very early conception phase of the proposed technology.

Long term solutions (net zero transportation)

As a matter of fact, net zero maritime transportation is already possible nowadays. Fully electrified short range ferries and even medium range ferries may be possible, provided the electricity has a net zero carbon footprint. For short range ferries first installations have been already in operation for a few years [14].

For long range transportation the fully electrical approach by means of batteries is technically not applicable. A containership sailing from Asia to Europe with a 1-month travel time, would need as many as 100’000 tons of batteries on board, 60% of the freight capacity [15]. This approach is financially and environmentally not sustainable.

A Net zero carbon footprint can be actually achieved by the use of sustainable fuel like biofuels or fuels generated from renewable energy sources (e.g. solar, wind, hydro, ...). From a vessel and engine technological perspective a full transition to net zero emission vessels is actually possible in less than 10 years. The major engine OEM announced availability of Ammonia engines from 2025, pilot initiatives with sustainable fuel are multiplying (e.g. Maersk [16], AIDA [17]).

Yet the global transition will take several decades to be implemented. The reasons behind this huge difference can be named directly: fuel.

The biggest challenge to overcome is the global availability and distribution of net zero carbon fuels (e.g. even for a globally well available fuel as LNG, the distribution and local availability is still a challenge for many ports). This is going to be a long process that take decades to implement and is not directly in the hands of the shipping industry itself. There will be fierce competition for sustainable energy between industries at local and global level, onshore and offshore (electricity, heating, private transportation, aviation, construction, ...).

The only technical alternative to chemical energy carriers for long haul maritime transportation would be nuclear energy. However, this technology nowadays faces low acceptance.

Transition phase - short and medium term

Presently, we are at the beginning of the carbon transition journey. Whereas the target and ambition are known, the exact means of implementation are widely unknown, and there will be many paths towards the common target.

Existing fleet

For a large portion of the existing fleet investment / divestment decisions are required. Investment strives to improve the carbon footprint of the vessel to keep its competitiveness in the market and avoid divestment.

It is certain that during the decades of carbon transition a vast diversity of technologies will emerge which cater to incremental CO2 footprint improvements. There won’t be a one fits all solution and most likely a single solution will not do the job. A sound combination of multiple incremental improvements are the key to making the existing fleet fit for the decarbonization journey.

The IC engine is at the heart of emissions related to the maritime industry. During the conversion from chemical to mechanical energy, CO2 is released during the oxidation of hydrocarbon fuels. Future fuels, such as methanol, ammonia or hydrogen, once available, will enable a global netzero CO2 balance. Yet it is paramount to operate the engine as efficiently as possible: (1) in the

Conference Paper 28

case of traditional fuels to reduce the amount of released CO2 and (2) in the case of future carbon neutral fuels to improve the financial sustainability (renewable fuel prices are expected to be higher compared to today’s costs of Diesel & LNG).

The following section will shed light on one of the low-hanging fruit technologies already available today to decrease the CO2 emission of IC engines: turbocharger upgrades.

The turbocharging system is a key component of the marine engine. Through its direct interaction with the engine, an upgraded turbocharger with higher efficiency has a leverage on emissions: (1) directly lowering specific fuel consumption and hence CO2 emissions by improved overall system efficiency and (2) enabling new engine tuning and concepts for even higher reduction potential.

So how do we integrate the latest available turbocharging technology within existing installations while maintaining a wide global adoption through a positive business case?

MARINE EQUIPMENT & TURBOCHARGER UPGRADE STRATEGIES

Maritime assets have a lifetime spanning over several decades, from 15 to 30 and more years depending on the vessel type. During this long time span the marine equipment is required to be serviced to ensure acceptable reliability, operational safety, and energy efficiency.

There are two main service approaches described below when it comes to servicing marine equipment. In this paper a third one combining the benefits from both approaches is presented.

1) The standard approach: classical service

When components need to be repaired or replaced, the conventional service approach is to install new equipment (like-for-like) having the same design & technology that was available when the vessel was delivered (old technology).

This approach has certainly the advantage of being straight forward to implement, no adaptation to interfaces and automation is required and the service event can often be implemented during already scheduled port stay (in the best case, no impact on vessel schedule). The downside of this approach is that owner and operator do not profit from the technological developments achieved by our industry over the last decades. The maintenance budget is spent buying old technology, striving to achieve the original performance of the vessel during its maiden voyage.

This traditional service concept is no longer sufficient.

In view of the increasingly stringent decarbonization targets, regulatory developments, as well as high fuel prices, our industry needs to rethink the approach when it comes to marine service. Every investment in servicing or replacing marine equipment is also an opportunity to apply an upgrade instead and increase the competitiveness of the vessel.

2) The upgrade approach: exchange to newer equipment design

An alternative approach to the classical service is to apply an upgrade instead. Older equipment is removed from the vessel and replaced by newer components with a more recent design. The approach has the advantage of letting owners and operators profit from the latest technology developments in efficiency, ease of service and spare part availability.

Unfortunately, changing equipment to a newer version requires in many cases adaptations of the interfaces as well as to the automation of the vessel. This increases the technical complexity, project management effort and downtime required to complete the installation.

Conference Paper 29

In many cases the increased complexity, direct and opportunity costs of the upgrade have a negative impact on the business case, resulting in reduced adoption of the upgrade technology in the market.

To achieve wide adoption of upgrades globally, the financial sustainability needs to be further improved.

3) The new way: component upgrade (combine simplicity with benefits)

It becomes obvious that to open the door for a wide adoption of upgrades in the market it is required to combine the benefits of the previously described approaches:

1) The simplicity of the standard service. No adaptation of interfaces, implementation during an already scheduled port stay, technical complexity the same as for a standard service.

2) Implement the latest technology in terms of design and material achieving higher efficiency, same or higher reliability, same or higher spare part availability, reduced maintenance costs.

But how can this be achieved? How can we apply upgrades while keeping the complexity at a similar level to a standard service event?

Figure 3: Integration of latest technology into older turbocharger generation

The turbocharger component upgrade is the solution to this dilemma, and is based on a simple concept:

5 The latest know-how in design and materials for the newest turbocharger generation is modified to fit into older turbocharger equipment from a previous generation.

5 Only the turbocharger internal performance relevant components are replaced by new upgrades, while the turbocharger casings and all interfaces to the engine remain untouched.

Conference Paper 30

The component upgrade approach requires a dedicated development, qualification and verification effort by equipment OEM’s. Once available it provides a great alternative to the standard service for owner and operators. A great instrument to simultaneously improve the CO2 footprint and competitiveness of their vessels, without interfering with the already scheduled maintenance scheme.

PRACTICAL EXAMPLES

In line with the market requirements and targeting a wider industry adoption, Accelleron has developed several products that can support owners and operators to reduce CO2 emissions, fuel expenses and support the compliance with new regulations for the existing fleet.

4-stroke engines with TPL-A and TPL-C turbocharger

A wide portfolio of component upgrades covering the entire TPL-A and TPL-C turbocharger range has been developed. The product requirements have been strictly based on four main pillars:

1) The turbocharger upgrade shall enable a positive business case for the end customer to ensure wide adoptions globally;

2) The turbocharger efficiency shall be substantially increased to reduce the engine fuel consumption and engine thermal load;

3) The time required for implementation and technical complexity shall be similar to a standard turbo service event;

4) The recommended exchange interval of the turbocharger rotating component shall be extended by 50%.

The environmental benefits can be separated into two categories: 1) direct CO2 reduction by reduced engine fuel consumption; 2) indirect CO2 reduction by reducing the number of spare parts required (grey energy for production and transport) enabled by an increased recommended exchange interval of the rotor and reduced thermal wear & tear of the engine hot components exposed to the exhaust gases.

One more thing, how to multiply the benefits?

The component upgrades have been developed in close cooperation with engine OEM’s and for many engine platforms the increased turbo efficiency is unlocking new upgrades on the engine side. The combination of engine with turbo upgrade are generating great synergies that enable fuel consumption reductions to be multiplied up to a factor of four (4x more benefits).

Conference Paper 31

Figure 4: Turbocharger component upgrade, upgrade only the core turbo performance components

2-stroke engines with TPL-B and A100/200-L turbos

Many 2-stroke engines feature a fuel optimization in the power range above 75%-85% load but are operated for most of the time at lower engine power. Furthermore, in many cases EPL (Engine Power Limitation) must be applied to fulfill the EXXI limits, further reducing the service power. For those vessels there is a mismatch between the relevant engine operating range, and the actual optimal operating range of the engine. This mismatch leads to inefficiencies in terms of increased CO2 emission, increased fuel expenses and increased maintenance efforts due to higher thermal load and carbon deposits.

Figure 5. EPLO fuel reduction characteristics

Engine Part Load Optimization (EPLO) is a solution based on a turbocharger component upgrade to reduce the fuel consumption and improve the engine operation at part load (engine power <70%) for 2-stroke engines.

The basic concept is as simple as it is effective. The turbocharger specification is optimized for a specific engine power range provided by the customer (below 75% power). To maximize the benefits, the engine tuning, and optionally also key engine components, are optimized to leverage synergies in the engine-turbo interaction.

This opens the question of engine operation at higher loads after the EPLO implementation. Two different options are possible:

1) Keep 100% MCR capability by installing an exhaust gas wastegate. The resulting fuel consumption at high load will be slightly higher compared to the reference case, but is irrelevant for the overall yearly vessel performance.

2) Apply permanent engine derating, where the maximal engine power is permanently reduced. No wastegate is required.

Both of the set-ups above combine well with EPL (Engine Power Limitation) to fulfill the EEXI requirement.

4-stroke engines with older generation turbochargers

For older generation turbochargers (like the VTR generation) the best upgrade option is to switch to a newer turbo version, by replacing the complete turbocharger, see Figure 6.

As described above it needs to be considered that due to the change of the turbo footprint the interfaces between turbo and engine need to be adapted. The benefits in terms of efficiency gain and reduction in turbo maintenance costs overcome the drawbacks from increased complexity of the project.

Conference Paper 32

CONCLUSION

The maritime industry is going through a disruptive decarbonization journey. Even though the transition to net zero emission vessels on a global scale could be completed in less than 10 years (technology development), this process is in reality going to require several decades to complete. Whereas electrification may play a role for short range vessels, chemical fuel carriers will continue to play a key role in long range transportation. The major challenge we are facing is the global availability and local distribution capability of carbon neutral fuel.

In the transition phase it is pivotal to combine measures to progressively improve the energy efficiency of shipping and relentlessly reduce the carbon footprint. To make a significant difference in a global context efficiency measures need broad adoption. This is only possible if the technology is reliable, and the implementation is financially sustainable (positive business cases are enabled).

Internal combustion engines are at the core of emission generation for the shipping industry. Measures to reduce their environmental impact can’t be removed from the global sustainability equation and must be carefully evaluated.

The turbocharger component upgrade is a simple measure that can be integrated into the regular maintenance scheme of the turbocharger. It reduces the direct CO2 emission onboard the vessel through lower fuel consumption, and also the indirect CO2 emission (grey energy for production) by increasing the lifetime of key components (50% extended replacement intervals of rotor, reduced wear & tear of hot parts).

The key to enabling wider adoption globally relies on two main pillars: 5 Integration of the upgrades into the regular turbocharger maintenance plan, without additional engine downtime. This minimizes direct and opportunity costs of the upgrades.

5 Replace only the core performance components of the turbocharger whenever possible while keeping all interfaces untouched. This reduces the complexity of the upgrade to the level of a standard service.

Outlook

A further step towards CO2 reduction would be to leverage data to further optimize the turbo performance and maintenance pattern. This increases the productivity of the equipment, while reducing emissions directly by lowering engine fuel consumption and indirectly by optimizing the required maintenance reducing the grey energy required for its production, transport and installation.

Conference Paper 33

Figure 6: Upgrade by replacing the turbocharger with a new generation version

Data may play a key role in optimizing and giving enhanced flexibility to conventional maintenance schemes by considering individual equipment status and existing customer maintenance schedules.

The recently launched Turbo SmartCare product by Accelleron [18] is a good example of data enabled service targeting highest performance, reliability, and optimization of turbocharger maintenance based on data and health assessment.

REFERENCES

[1] https://www.morethanshipping.com/fuel-costs-ocean-shipping/ (accessed on September 26th, 2022)

[2] RESOLUTION MEPC.304(72). https://unfccc.int/sites/default/files/resource/250_ IMO%20submission_Talanoa%20Dialogue_April%202018.pdf (accessed on September 26th, 2022)

[3] DNV. Achieving the IMO decarbonization goals. https://www.dnv.com/expert-story/ maritime-impact/How-newbuilds-can-comply-with-IMOs-2030-CO2-reduction-targets. html (accessed on September 26th, 2022)

[4] https://about.nike.com/en/impact (accessed on September 26th, 2022)

[5] https://about.ikea.com/en/sustainability/value-chain-climate-footprint (accessed on September 26th, 2022)

[6] Poseidon Principles. Assessment of climate alignment. https://www.poseidonprinciples. org/finance/wp-content/uploads/2019/07/Poseidon_Principles_Assessment.pdf (accessed on September 26th, 2022)

[7] Regulation of the European Parliament and of the council on the use of renewable and low-carbon fuels in maritime transport and amending Directive 2009/16/EC https://ec.europa.eu/info/sites/default/files/fueleu_maritime_-_green_european_ maritime_space.pdf (accessed on September 26th, 2022)

[8] Directive (EU) 2018/410 of the European Parliament and of the Council of 14 March 2018 amending Directive 2003/87/EC to enhance cost-effective emission reductions and low-carbon investments, and Decision (EU) 2015/1814. EUR-Lex - 32018L0410 - EN - EUR-Lex (europa.eu)

[9] https://www.imo.org/en/MediaCentre/PressBriefings/pages/MEPC76.aspx (accessed on September 26th, 2022)

[10] Resolution MEPC334(76). 2021 Guidelines on survey and certification of the attained Energy Efficiency Existing Ship Index https://wwwcdn.imo.org/localresources/en/ OurWork/Environment/Documents/Air%20pollution/MEPC.334(76).pdf (accessed on September 26th, 2022)

[11] Resolution MEPC.339(76). 2021 guidelines on the operational carbon intensity rating of ships (CII rating guidelines, G4) https://wwwcdn.imo.org/localresources/en/OurWork/ Environment/Documents/Air%20pollution/MEPC.339(76).pdf (accessed on September 26th, 2022)

[12] Environmental Performance: Comparison of CO2 Emissions by Different Modes of Transport. https://www.ics-shipping.org/shipping-fact/environmental-performanceenvironmental-performance/ (accessed on September 26th, 2022)

[13] IMO, Cutting ships’ GHG emissions - working towards revised strategy. https://www.imo. org/en/MediaCentre/PressBriefings/pages/MEPC-78-.aspx (accessed on September 26th, 2022)

[14] Electric Ship Moves Closer to reality, Motorship Mai 6th, 2015

[15] NZZ Magazin, Die Giganten der Weltmeere müssen sauber werden, July 2nd, 2022

[16] https://www.maersk.com/news/articles/2021/08/24/maersk-accelerates-fleetdecarbonisation (accessed on September 26th, 2022)

[17] Press release, AIDA Cruises starts the use of biofuels, July 22, 2022

[18] Robban Assafina, Volume 14, Issue 81 – Sept/Oct 2022, page 83. http://magazine. assafinaonline.com/books/jnhf/#p=1 (accessed on October 3th, 2022)

Conference Paper 34

BIOGRAPHY

NATALIA ZUBENKO

Business Development Manager, Gaztransport & Technigaz (GTT)

Natalia joined the GTT engineering team in France in 2011 as a lead process engineer. Five years later, she was promoted to Business Development Manager with a key focus on EU area.

Previously she held positions in DNV as an approval engineer and also in Moss Maritime, as a process engineer. Natalia graduated in 2007 from Gubkin Russian State University of Oil and Gas in Moscow with a master degree in gas processing engineering.

Speaker

36

Motorship conference • November • 2022

Improving energy efficiency including electrical production for LNG fueled vessels.

Improving energy efficiency including electrical production for LNG fueled vessels

By Natalia Zubenko, Business Development Manager, GTT

Introduction

Introduction

The LNG as fuel revolution has taken off. To succeed in this transition, ship-owners need to modernize and adapt their fleets to comply with the new international regulations and environmental standards. How can we improve the fuel gas system in order to optimise the efficiency of a LNG fuelled vessel, in particular the electricity production on-board?

The LNG as fuel revolution has taken off. To succeed in this transition, ship-owners need to modernize and adapt their fleets to comply with the new international regulations and environmental standards. How can we improve the fuel gas system in order to optimise the efficiency of a LNG fuelled vessel, in particular the electricity production on-board?

LNG fuel system functions

LNG fuel system functions

First, let’s recall few key functions of LNG as fuel system: primary purpose to is fed engines to produce power to propel the vessel, then electrical power needs to be generated for hotel load. Boil-off has to be managed using consumers or, in exceptional cases, by the boiler or the vent mast.

First, let’s recall few key functions of LNG as fuel system: primary purpose to is fed engines to produce power to propel the vessel, then electrical power needs to be generated for hotel load. Boil-off has to be managed using consumers or, in exceptional cases, by the boiler or the vent mast.

Figure1: LNG fuel system functions

Figure1: LNG fuel system functions

More and more main engines (ME) are equipped with the Shaft Generator, also called Power Take Out (PTO). Shaft generator is driven by the main engine (slow or medium speed) and supply power to the main switchboard (instead of auxiliaries). This mode is called PTO or SG mode. The opposite is also possible and called Power Take In (PTI). PTI provides propulsion power to the shaft that boosts the ME with extra power. It can also be used as an emergency backup machinery to propel the ship to the nearest shore. PTO can improve ship Energy Efficiency Design Index (EEDI), while PTI can deteriorate the EEDI figures if used for increasing the ship’s speed.

More and more main engines (ME) are equipped with the Shaft Generator, also called Power Take Out (PTO). Shaft generator is driven by the main engine (slow or medium speed) and supply power to the main switchboard (instead of auxiliaries). This mode is called PTO or SG mode. The opposite is also possible and called Power Take In (PTI). PTI provides propulsion power to the shaft that boosts the ME with extra power. It can also be used as an emergency backup machinery to propel the ship to the nearest shore. PTO can improve ship Energy Efficiency Design Index (EEDI), while PTI can deteriorate the EEDI figures if used for increasing the ship’s speed.

This document is strictly confidential. Any unauthorised access to, appropriation of, copying, modification, use or disclosure thereof, in whole or in part, by any means, for any purpose, infringes GTT’s rights. This document is part of GTT’s proprietary know-how and may contain trade secrets protected worldwide by TRIPS and EU Directives against their unlawful acquisition, use and disclosure. It is also protected by Copyright law. The production, offering or placing on the market of, the importation, export or storage of goods or services using GTT’s trade secrets or know-how is subject to GTT’s prior written consent. Any violation of these obligations may give rise to civil or criminal liability. © GTT, 2010-2022

Conference Paper 37

Figure 2: Propulsion layout

Figure 2: Propulsion layout

Figure 2: Propulsion layout

Fuel Gas Handling System for MEGI engine

Fuel Gas Handling System for MEGI engine

Fuel Gas Handling System for MEGI engine

Here below is the basic FGHS for a vessel equipped with a MEGI engine.

Here below is the basic FGHS for a vessel equipped with a MEGI engine.

Here below is the basic FGHS for a vessel equipped with a MEGI engine.

Figure 3: FGHS for a vessel equipped with a MEGI engine

Figure 3: FGHS for a vessel equipped with a MEGI engine

Figure 3: FGHS for a vessel equipped with a MEGI engine

BOG is sent to gen-sets and boilers through the low pressure compressors. LNG is sent to the ME through PVU at approximately 300 bar and +45°C. It can be difficult to handle the BOG when you have low gen-set consumption. The very first solution is to select high performance insulation with very low BOR, as offer by GTT Mark III Flex membrane tanks. Then, one option is to add an HP compressor, but this comes with high CAPEX and OPEX. The simpler option is the recondenser, with low CAPEX and almost no OPEX. The principle of the re-condenser is to use the cold power from the LNG to recondense the BOG.

BOG is sent to gen-sets and boilers through the low pressure compressors. LNG is sent to the ME through PVU at approximately 300 bar and +45°C. It can be difficult to handle the BOG when you have low gen-set consumption. The very first solution is to select high performance insulation with very low BOR, as offer by GTT Mark III Flex membrane tanks. Then, one option is to add an HP compressor, but this comes with high CAPEX and OPEX. The simpler option is the recondenser, with low CAPEX and almost no OPEX. The principle of the re-condenser is to use the cold power from the LNG to recondense the BOG.

BOG is sent to gen-sets and boilers through the low pressure compressors. LNG is sent to the ME through PVU at approximately 300 bar and +45°C. It can be difficult to handle the BOG when you have low gen-set consumption. The very first solution is to select high performance insulation with very low BOR, as offer by GTT Mark III Flex membrane tanks. Then, one option is to add an HP compressor, but this comes with high CAPEX and OPEX. The simpler option is the recondenser, with low CAPEX and almost no OPEX. The principle of the re-condenser is to use the cold power from the LNG to recondense the BOG.

This document is strictly confidential. Any unauthorised access to, appropriation of, copying, modification, use or disclosure thereof, in whole or in part, by any means, for any purpose, infringes GTT’s rights. This document is part of GTT’s proprietary know-how and may contain trade secrets protected worldwide by TRIPS and EU Directives against their unlawful acquisition, use and disclosure. It is also protected by Copyright law. The production, offering or placing on the market of, the importation, export or storage of goods or services using GTT’s trade secrets or know-how is subject to GTT’s prior written consent. Any violation of these obligations may give rise to civil or criminal liability. © GTT, 2010-2022

This document is strictly confidential. Any unauthorised access to, appropriation of, copying, modification, use or disclosure thereof, in whole or in part, by any means, for any purpose, infringes GTT’s rights. This document is part of GTT’s proprietary know-how and may contain trade secrets protected worldwide by TRIPS and EU Directives against their unlawful acquisition, use and disclosure. It is also protected by Copyright law. The production, offering or placing on the market of, the importation, export or storage of goods or services using GTT’s trade secrets or know-how is subject to GTT’s prior written consent. Any violation of these obligations may give rise to civil or criminal liability. © GTT, 2010-2022

Conference Paper 38

Recondensor solution is pushing LNG as fuel efficiency to a higher level

Recondensor solution is pushing LNG as fuel efficiency to a higher level

On engines side, 2-stroke technology have emerged as widely adopted as propulsion of choice, mainly due to better efficiency and reduced methane slip. However, feeding those engines have raised 2 main questions, especially when they are of high pressure type:

On engines side, 2-stroke technology have emerged as widely adopted as propulsion of choice, mainly due to better efficiency and reduced methane slip. However, feeding those engines have raised 2 main questions, especially when they are of high pressure type:

5 How to simplify boil-off gas management system – in particular with alternatives to High pressure compressors?

5 How can the wasted cold power during LNG vaporization process towards engines be recovered?

-How to simplify boil-off gas management system – in particular with alternatives to High pressure compressors?

-How can the wasted cold power during LNG vaporization process towards engines be recovered?

With this in mind, GTT proposes a solution that manages to solve these 2 questions at once: a compact and easy to operate recovery system – called RECYCOOL that is:

With this in mind, GTT proposes a solution that manages to solve these 2 questions at once: a compact and easy to operate recovery system – called RECYCOOL that is:

5 Compact passive system, easily integrated to recover cold on way to main engine

5 Highly efficient & improves operability of existing supply system

Compact passive system, easily integrated to recover cold on way to main engines

5 CAPEX competitive

Highly efficient & improves operability of existing supply system

5 Reduces burden on auxilairy engines

CAPEX competitive Reduces burden on auxilairy engines

5 Reduces vessel carbon footprint

Reduces vessel carbon footprint

5 Significant fuel savings in particular when combined with Shaft Generator (PTO)

Significant fuel savings in particular when combined with Shaft Generator (PTO)

Figure 4: Simplified diagram of RECYCOOL

Figure 4: Simplified diagram of RECYCOOL

This document is strictly confidential. Any unauthorised access to, appropriation of, copying, modification, use or disclosure thereof, in whole or in part, by any means, for any purpose, infringes GTT’s rights. This document is part of GTT’s proprietary know-how and may contain trade secrets protected worldwide by TRIPS and EU Directives against their unlawful acquisition, use and disclosure. It is also protected by Copyright law. The production, offering or placing on the market of, the importation, export or storage of goods or services using GTT’s trade secrets or know-how is subject to GTT’s prior written consent. Any violation of these obligations may give rise to civil or criminal liability. © GTT, 2010-2022

Conference Paper 39

Figure 5: RECYCOOL integrated in the PVU unit

Figure 5: RECYCOOL integrated in the PVU unit

Figure 5: RECYCOOL integrated in the PVU unit

Concept : The otherwise wasted cold energy is stored inside LNG tank as a reserve for operating cost reduction, optimization of operation and safety.

Concept : The otherwise wasted cold energy is stored inside LNG tank as a reserve for operating cost reduction, optimization of operation and safety.

Concept : The otherwise wasted cold energy is stored inside LNG tank as a reserve for operating cost reduction, optimization of operation and safety.

Main system features

Main system features

Recondensor is like a reliquefaction plant of excess gas – which helps to reduce burden on auxiliary engines and boil-off management.

Main system features

Recondensor is like a reliquefaction plant of excess gas – which helps to reduce burden on auxiliary engines and boil-off management.

5 Static equipment only: heat exchangers, valves… to be connected downstream existing low pressure compressors

5 Small footprint / compact system / easy integration

5 No additional rotating machines

Static equipment only: heat exchangers, valves… to be connected downstream existing low pressure compressors

Recondensor is like a reliquefaction plant of excess gas – which helps to reduce burden on auxiliary engines and boil-off management.

5 System reactivity / cool-down time reduced

Small footprint / compact system / easy integration

5 Advanced control system for HP pump cavitation monitoring:

Static equipment only: heat exchangers, valves… to be connected downstream existing low pressure compressors

5 Compatibility with oil-injected screw compressors

No additional rotating machines System reactivity / cool-down time reduced

Small footprint / compact system / easy integration

No additional rotating machines

System reactivity / cool-down time reduced

Advanced control system for HP pump cavitation monitoring: Compatibility with oil-injected screw compressors Enhancement of ship performance using PTO systems:

o Fuel savings

Advanced control system for HP pump cavitation monitoring: Compatibility with oil-injected screw compressors

Enhancement of ship performance using PTO systems:

This document is strictly confidential. Any unauthorised access to, appropriation of, copying, modification, use or disclosure thereof, in whole or in part, by any means, for any purpose, infringes GTT’s rights. This document is part of GTT’s proprietary know-how and may contain trade secrets protected worldwide by TRIPS and EU Directives against their unlawful acquisition, use and disclosure. It is also protected by Copyright law. The production, offering or placing on the market of, the importation, export or storage of goods or services using GTT’s trade secrets or know-how is subject to GTT’s prior written consent. Any violation of these obligations may give rise to civil or criminal liability. © GTT, 2010-2022

Fuel savings

Conference Paper 40

5 Enhancement of ship performance using PTO systems:

o Fuel savings

o GHG emissions: methane slip reduced

o GHG emissions: methane slip reduced

o GHG emissions: methane slip reduced

o Fuel savings

o Fuel savings

o Fuel savings

o GHG emissions: methane slip reduced

o GHG emissions: methane slip reduced

o GHG emissions: methane slip reduced

o Aux. engines maintenance costs reduced

o Aux. engines maintenance costs reduced

o Aux. engines maintenance costs reduced

Recycool: performance overview

Recycool: performance overview

Recycool: performance overview

Figure 6: BOG management capacity with RECYCOOL for 7k TEU container vessel

Figure 6: BOG management capacity with RECYCOOL for 7k TEU container vessel

Figure 6: BOG management capacity with RECYCOOL for 7k TEU container vessel

What we see on the figure 6 is the consumption vs ship speed. The genset consumption is constant (in grey). The quantity of BOG we can recondense (in blue) will depend on the LNG flow consumed by the ME, which varies with the vessel speed. On this example for 7000 TEU vessel RECYCOOL is able to recondense half of the natural BOG at 15kts and 100% at 20kts.

What we see on the figure 6 is the consumption vs ship speed. The genset consumption is constant (in grey). The quantity of BOG we can recondense (in blue) will depend on the LNG flow consumed by the ME, which varies with the vessel speed. On this example for 7000 TEU vessel RECYCOOL is able to recondense half of the natural BOG at 15kts and 100% at 20kts.

What we see on the figure 6 is the consumption vs ship speed. The genset consumption is constant (in grey). The quantity of BOG we can recondense (in blue) will depend on the LNG flow consumed by the ME, which varies with the vessel speed. On this example for 7000 TEU vessel RECYCOOL is able to recondense half of the natural BOG at 15kts and 100% at 20kts.

Figure 7: Example: 15k TEU / trade Asia-Europe

Figure 7: Example: 15k TEU / trade Asia-Europe

Figure 7: Example: 15k TEU / trade Asia-Europe

What happen if we put the same graph in the real life, with varying speed and varying gen-sets load?

What happen if we put the same graph in the real life, with varying speed and varying gen-sets load?

What happen if we put the same graph in the real life, with varying speed and varying gen-sets load?

This document is strictly confidential. Any unauthorised access to, appropriation of, copying, modification, use or disclosure thereof, in whole or in part, by any means, for any purpose, infringes GTT’s rights. This document is part of GTT’s proprietary know-how and may contain trade secrets protected worldwide by TRIPS and EU Directives against their unlawful acquisition, use and disclosure. It is also protected by Copyright law. The production, offering or placing on the market of, the importation, export or storage of goods or services using GTT’s trade secrets or know-how is subject to GTT’s prior written consent. Any violation of these obligations may give rise to civil or criminal liability. © GTT, 2010-2022

This document is strictly confidential. Any unauthorised access to, appropriation of, copying, modification, use or disclosure thereof, in whole or in part, by any means, for any purpose, infringes GTT’s rights. This document is part of GTT’s proprietary know-how and may contain trade secrets protected worldwide by TRIPS and EU Directives against their unlawful acquisition, use and disclosure. It is also protected by Copyright law. The offering placing on the market of, the importation, export or storage of goods or services using GTT’s trade secrets or know-how is subject to GTT’s prior written consent. violation these obligations may give rise to civil or criminal liability. © GTT, 2010-2022

Conference Paper 41

The recondensing capacity varies with the speed. This is the area between the dotted line and the gen-sets consumption (in grey). The BOG has its own variation, as it depends on the tank filling, the external temperature, and is represented in light blue line.

We can see on the figure 7 that the RECYCOOL recondense a good part of the BOG (in dark blue). We also see the periods where the gen-sets are sufficient.

Let’s focus on periods where BOG is higher than gen-sets and RECYCOOL combined. This can be handled in 2 ways: if it is a short time, just let the pressure rise, and use more recondensing capacity afterwards. Otherwise anticipate this low consumption period and send more BOG to recondenser beforehand.

The recondensing capacity varies with the speed. This is the area between the dotted line and the gen-sets consumption (in grey). The BOG has its own variation, as it depends on the tank filling, the external temperature, and is represented in light blue line. We can see on the figure 7 that the RECYCOOL recondense a good part of the BOG (in dark blue). We also see the periods where the gen-sets are sufficient. Let’s focus on periods where BOG is higher than gen-sets and RECYCOOL combined. This can be handled in 2 ways: if it is a short time, just let the pressure rise, and use more recondensing capacity afterwards. Otherwise anticipate this low consumption period and send more BOG to recondenser beforehand. So, we are always able to handle the BOG.

So, we are always able to handle the BOG.

Figure 8: Example: Ship trade : 15k TEU - 53 days - LNG bunkering SING

Figure 8: Example: Ship trade : 15k TEU - 53 days - LNG bunkering SING

If we push the study a little bit further and see the potential benefit for OPEX and emissions (figure 8). ME consume less and has less methane slip than 4-stroke engines. This is why PTO solution is gaining momentum. The OPEX reduction with a PTO can be around 2%, because you still use gen-sets often as the main BOG management solution onboard. Combining with RECYCOOL, the use of PTO can be maximised to reach 5% OPEX reduction and dramatic cut of gen-sets emissions.

If we push the study a little bit further and see the potential benefit for OPEX and emissions (figure 8). ME consume less and has less methane slip than 4-stroke engines. This is why PTO solution is gaining momentum. The OPEX reduction with a PTO can be around 2%, because you still use gen-sets often as the main BOG management solution onboard. Combining with RECYCOOL, the use of PTO can be maximised to reach 5% OPEX reduction and dramatic cut of gen-sets emissions.

This document is strictly confidential. Any unauthorised access to, appropriation of, copying, modification, use or disclosure thereof, in whole or in part, by any means, for any purpose, infringes GTT’s rights. This document is part of GTT’s proprietary know-how and may contain trade secrets protected worldwide by TRIPS and EU Directives against their unlawful acquisition, use and disclosure. It is also protected by Copyright law. The production, offering or placing on the market of, the importation, export or storage of goods or services using GTT’s trade secrets or know-how is subject to GTT’s prior written consent. Any violation of these obligations may give rise to civil or criminal liability. © GTT, 2010-2022

Conference Paper 42

SESSION 2

Digitalization, Digital Efficiency and the Future Technology of the Maritime Sector 44

MIA ELG R&D Manager, Deltamarin

BIOGRAPHY

Mia has 15 years of experience with various ship energy efficiency and machinery design related tasks. Mia Elg’s current role as R&D manager is related to leading the development of Deltamarin’s products and services. Mias areas of expertise include: Thermal engineering, product development and productization of different energy- and environmental services, energy balance calculation, energy flow simulation and environmental impact assessment. In addition to this, she has led the development of zero emission ship machinery in several projects. Mia has a Master’s degree in Thermodynamics. At the side of the work at Deltamarin Mia is also committing doctoral studies at Aalto University in the field of energy efficiency in marine applications. As a “high level task” both at Deltamarin and in the studies, Mia develops an advanced energy efficiency analysis method, suitable for maritime and offshore domain.

Speaker

45

Shipping decarbonization and digital thread

Shipping decarbonisation can be technically divided into three main categories: operational optimization, design and equipment improvement and optimization and low-carbon fuel alternatives. In our earlier studies, such as in a joint industry project regarding tanker decarbonisation alternatives together with DNV, Total and Minerva Marine in 2020 we have evaluated the total cost of ownership of the case ships with various fuelling alternatives. In the study we estimated that over 90% decarbonisation of the ships on a well to wake perspective could easily double the total cost of ownership of the vessels, compared to the current fossil fuel operated modern designs. Therefore, focusing on energy saving is nowadays more important than ever. The development is also pushed from legislative perspective in form of ship carbon intensity index CII or energy efficiency index for existing ships, EEXI.

Improving ship energy efficiency with single actions, such as optimizing ship hull further in single specified conditions is not alone enough to provide substantial energy savings for ships. Rather, the still untapped potential of energy saving lies in optimizing the designs and selecting the ship equipment and energy saving devices considering the realistic operational patterns. The operational profile includes also estimating the magnitude of operative energy management and optimization, such as weather routing performed on route. This hybrid of operational- design and technology optimization is also at the heart of an ongoing EU-project CHEK, where Deltamarin is the ship design partner in the large consortium consisting of technology providers, research parties, classification society representation and ship charterer and owner. The enabler for the design optimization in the project is digital modelling, which works as a platform for the studied operational improvements and energy saving technologies integrated in the ship design.

Digital twins and Digital thread

Digital twins based on measured system data are often suggested as technical tool for shipping decarbonisation, at least in connection to energy savings and for maintaining good operational efficiency. A digital twin can be formed of a ship utilizing measurement data of the operating vessel. One clear benefit of digital twin is that it can function as a single point of contact to a highly complex system, such as a ship. However, if we want to make the largest possible impact for a ship regarding her overall performance, the key decisions are made long before the ship or her digital twin are born: during the early concept design phase. This is also the time for ensuring a necessary capacity onboard the ship for future sustainable fuels.

Therefore, creating a digital representation of the ship as early as possible during ship life cycle enables focusing on the cost efficient technical ship optimization, such as system dimensioning and machinery, hull and propulsion system optimization when it is still possible. Creating ship digital models in several “generations” is a pragmatic way to combine the ship environmental performance development in the traditional ship design phases form conceptual design to basic and detail design and ship building, followed by the operational phase.

Dimensions of ship digital model

For a ship designer a ship digital model should be rather a flexible combination of scalable tools and processes, which allow a holistic evaluation of the vessel energy and environmental efficiency, considering even the ship entire life cycle. The figure below illustrates Deltamarin’s in-house tools and processes for this.

Conference Paper 46

The first dimension includes the ship hull and volume model including the ship main structures and the cargo carrying capacity. This model including the main equipment is the basis for performing economical evaluations, in addition to the necessary naval architectural analysis.

The second dimension of the digital ship model is the virtual operation profile of the vessel including the external forces caused by wind and waves and other environmental factors. This part of the analysis introduces a realistic propulsion power profile for the vessel and together with the environmental conditions it is the input for the energy model of the ship.

The third dimension, the ship energy simulation “layer” combines the ship energy consumers, such as heat, electricity and mechanical power requirements to the machinery and other equipment onboard. Modelling the energy conversions onboard including the stored energy onboard in form of fuel or batteries and considering also renewable energy sources and shore power, for instance. The result of this dimension is simulation of ship fuel consumption and environmental performance on a typical route.

A digital representation of the ship enables studying a large number of variations regarding any single aspect of shipping decarbonisation. Most of all, the method is valuable in evaluating the impact of a combination of design, operational or technical improvements and the impact of alternative fuels. The digital model can also be utilized for performing various optimization routines with correct set-up. This optimization platform is in Deltamarin’s technical development focus in project CHEK.

Conference Paper 47

Digital thread in action