A slowdown in industrial real estate? Yes, but Twin Cities CRE pros say better times are on the way

By Dan Rafter, Editor

It’s long been one of the most consistent commercial real estate sectors. But the industrial market across the country is seeing a slowdown in leasing activity, investment sales and new construction.

Blame high interest rates and construction costs. But throughout the country – including in Minnesota –the industrial sector’s boom days appear over for now.

The good news? The fundamentals of this real estate sector remain strong. And commercial real estate professionals working the Twin Cities region predict that leases, sales and new development will again trend

up, especially now that the Federal Reserve Board has cut its benchmark interest rate and is poised to enact future cuts.

Peter Mork, founding partner with Edina-based Capital Partners, said that leasing activity has slowed, especially for industrial spaces with larger square footage. Those properties of 100,000 square feet or more? Owners are taking longer to fill them with tenants.

“The market has slowed,” Mork said. “My rationale for it is that we are in an indecisive time with interest rates, inflation and the presidential election. Those

three things make larger publicly held companies pause before making major decisions.”

As Mork says, it’s more difficult for larger companies, those that need more expansive industrial space, to ask for board approval today to expand their plant, shop or warehouse space. Doing so requires borrowing money at interest rates that are still high.

Many of these large companies? They are waiting until the next presidential administration takes office before making expansion plans, Mork said.

Slowdown to page 22

The big divide: Newer and renovated office properties still attracting clients in the Twin Cities

By Dan Rafter, Editor

Abit of a rebound? Yes. But plenty of remaining challenges, too. That’s the state of the Minneapolis-St. Paul office market entering the fourth quarter of the year.

Avison Young recently released its third-quarter Minneapolis-St. Paul office report. And the news from the report was decidedly mixed.

But in an interview with Minnesota Real Estate Journal, two CRE professionals with Avison Young said that not all office space in the Twin Cities is performing equally. Newer properties filled with amenities? They are doing well.

It’s why Tate Krosschell, principal and managing director with the Minneapolis office of Avison Young,

said that there are plenty of opportunities for developers willing to buck the trend and add new, high-quality Class-A office space to the Twin Cities market.

“The flight to quality is a long-term trend,” Krosschell said. “Companies are looking for ways to encourage their people to come back into the office. Giving them better office space is one strategy.”

Photo courtesy of Capital Partners.

1

A slowdown in industrial real estate? Yes, but Twin Cities CRE pros say better times are on the way: It’s long been one of the most consistent commercial real estate sectors. But...

1

4

6

8

The big divide: Newer and renovated office properties still attracting clients in the Twin Cities: A bit of a rebound? Yes. But plenty of remaining challenges, too.

As the healthcare real estate industry evolves, medical providers need to take care of their patients, too: The healthcare real estate industry is evolving to meet the needs of patients who prefer to receive care in outpatient facilities instead of being forced to travel to busy hospitals.

Saint Paul office vacancy rates are rising in all classes: Still challenging. That’s how the Greater Saint Paul Building Owners and Managers Association describes the Saint Paul, Minnesota, office market.

JLL research: Experiences still matter when it comes to retail success:

10

Multifamily operators turning to concessions to attract renters:

U.S. apartment owners and operators face increasing competition today from new multifamily properties and the lure of single-family housing. To attract renters?

12 Occupancy, rent growth and long-term demand on the rise in medical office space:

As the healthcare delivery system continues to shift toward outpatient care, a mid-year medical office review by The Laramar Group shows a positive outlook for occupancy, rent growth and long-term demand.

14 Counselors of Real Estate 2025 prediction? Plenty of uncertainty

16 Managing sustainability and cost amid increasingly complex environmental concerns

President | Publisher

Jeff Johnson jeff.johnson@rejournals.com

Managing Editor Dan Rafter drafter@rejournals.com

Senior Vice President Jay Kodytek jay.kodytek@rejournals.com

Chief Financial Officer

Todd Phillips todd.phillips@rejournals.com

Art Director | Graphic Designer Alan Davis alan.davis@rejournals.com

Managing Director

National Events & Marketing Kaitlyn LaCroix kaitlyn.lacroix@rejournals.com

7767 Elm Creek Boulevard, Suite 210 Maple Grove, MN 55369

As the healthcare real estate industry evolves, medical providers need to take care of their patients, too

By Dan Rafter, Editor

The healthcare real estate industry is evolving to meet the needs of patients who prefer to receive care in outpatient facilities instead of being forced to travel to busy hospitals. But what if healthcare providers struggle to find the employees they need to staff the new freestanding clinics and ambulatory care centers they are opening?

That’s a major topic of JLL’s first Employee Perspective on Healthcare Real Estate survey. The report, which collected responses from more than 1,000 healthcare employees, explores how healthcare companies can best attract and retain workers.

JLL’s report found that this is a challenging time for healthcare employers. According to the survey results, nearly a quarter of healthcare employees are considering leaving their jobs in the next 12 months. A total of 10% of survey respondents said that they plan to leave the healthcare industry.

JLL researchers said that employees are leaving their jobs or the industry not only because they are seeking higher pay -- though that certainly matters -- but because they are seeking less-stressful or exhausting positions. Others are looking for a shorter commute to work.

“Humans rely on healthcare at their most vulnerable moments, and the people who provide that care are essential. At its core, healthcare is humans taking care of humans,” said Cheryl Carron, chief operating officer for JLL Work Dynamics Americas, in a written statement.

“While pay and benefits remain top priorities, in today’s competitive labor market, employers need to look beyond compensation and recognize how the physical workplace plays a crucial role in employee experience and can significantly impact employee satisfaction,” Carron said.

More than 40% of respondents ranked location/proximity to their employer in their top three factors for choosing a new position.

Clinicians ranked the specific role they would take on in their top three factors over location more often than those working in operational positions. This is not surprising considering physicians, advanced practitioners and nurses are more specialized, JLL said.

Members of different generations are also looking for differing benefits from their work situations. A total of 31% of Gen Z respondents, a generation that has more entry-level workers, placed higher importance on workplace culture,

Photo by Cedric Fauntleroy.

The Vision To See Banking Differently

Discover Bridgewater Bank.

Greater Saint Paul Building Owners and Managers Association: Saint Paul office vacancy rates are rising in all classes

By Dan Rafter, Editor

Still challenging. That’s how the Greater Saint Paul Building Owners and Managers Association describes the Saint Paul, Minnesota, office market. In its 2024 Market Report, the Greater Saint Paul BOMA reported that the overall office occupancy rate in the Saint Paul CBD market stood at 85% as of October of this year.

That is a dip from last year at this time, when the local chapter of BOMA reported that the Saint Paul occupancy rate was 90% for downtown office space.

The Greater Saint Paul Boma’s report also lists how much office space is currently in the Saint Paul Central Business District. According to BOMA’s numbers, the Saint Paul CBD totals 1.43 million square feet of office space.

The CBD is made up of 46% competitive office space, 34% government space and 20% owner-occupied space.

The overall competitive office vacancy rate for the Saint Paul market jumped from 22% at this time last year to a far higher 32% as of October of 2024. The overall office occupancy vacancy rate for the Saint Paul CBD is lower because owner-occupied and government office space tend to have occupancy rates.

All classes saw a jump in vacancy rates, with Class-B office properties seeing the greatest year-over-year vacancy increase, 15.59 points. Class-B competitive office vacancy rates jumped from 26.98% last year to 42.57% now in Saint Paul’s CBD.

Class-C competitive office properties experienced an increase of 8.06 points, with vacancy rates increasing from 13.29% last year to 21.35% this year. Saint Paul CBD Class-A office properties saw a much smaller

increase in vacancy rates, a jump of 1.2 points from 18.5% last year to 19.7% this year.

This provides more evidence that the flight to quality is real in the office market, both across the country and in Saint Paul. Tenants continue to move to higher-quality Class-A office spaces, helping to explain the higher vacancy rates in Class-B and -C properties in the Saint Paul CBD market.

Photo courtesy of Pixabay

JLL research: Experiences still matter when it comes to retail success

By Dan Rafter, Editor

Consumers are increasingly seeking experiences from their living environments, which means a rising demand for mixed-use developments that offer a live/work/play environment.

That’s the key takeaway from JLL’s 2024 Global Consumer Experience Survey released this month.

JLL calls it the “experience economy,” commercial spaces that don’t just offer consumers products to buy or meals to eat. Instead, the top-performing retail spaces today offer consumers an experience.

What is the experience economy?

Think a home-goods retailer that offers cooking lessons or invites celebrity chefs to demonstrate their products. Or bowling alleys and arcades pitched to adults hoping to rewind after a long work week. Or high-end movie theaters that serve chef-quality food during showings of their films.

JLL’s report found that not only do consumers desire these experiences, they are willing to spend more to get them.

“It’s people we ultimately build places for, and understanding what they need first is imperative,” said Lee Daniels, JLL Global Growth and Innovation Lead, Work Dynamics. “By developing comprehensive experience strategies that encompass multiple dimensions, we recognize that it is people who transform places and spaces, while experiences and interactions ultimately shape people.”

JLL surveyed more than 3,200 respondents across the globe. A total of 41% of these respondents strongly agreed with the statement “I am willing to pay a premium for high-quality experiences.” An additional 27% said that they agreed with this statement. Only 10% disagreed while only 10% strongly disagreed. An additional 12% said that they were neutral on the statement.

A total of 49% of respondents strongly agreed with the statement “Cities need to provide new experi-

ences to stay relevant.” An additional 27% agreed, while 7% disagreed and 4% strongly disagreed. These responses indicate that a large number of consumers are eager for more opportunities to connect with others in meaningful ways, JLL says in its report.

“Forward-looking new development projects should consider how to enable greater social connectivity within individual buildings and throughout multi-building development campus locations,” said Peter Miscovich, JLL Global Future of Work Lead, Work Dynamics.

“For example, organizations can develop an integrated employee experience based upon leading consumer experience practices by treating their employees in the same manner as they would treat high-value customers.”

The most successful retailers will continue to focus on both their online and physical stores, JLL says.

According to the survey, 75% of consumers report feeling satisfied with online shopping experiences. But the survey also finds that people still enjoy

shopping in a physical store. A total of 64% of respondents said that they prefer shopping in-person versus online.

“Developers, investors and occupiers are seeing increased demand for ‘destination’ places and spaces, as consumers expect increased choice and quality in the places where they live, work and visit,” said Ruth Hynes, JLL’s EMEA Work Dynamics Research and Strategy Director.

“And this is where we are seeing increased demand for research and data in planning and development, to unlock insights into consumer expectations across real estate. In increasingly complex environments, research and data-driven strategies for human-centric developments are more important than ever.”

Berkadia report: Multifamily operators turning to concessions to attract renters

By Dan Rafter, Editor

U.S. apartment owners and operators face increasing competition today from new multifamily properties and the lure of single-family housing. To attract renters? Many of these owners and operators are turning to concessions.

That’s the takeaway from the latest research from Berkadia.

According to Berkadia’s apartment concessions report released in October, more than one out of every five professionally managed apartment units across the United States offered concessions in the second quarter of 2024.

While that figure represents an increase over recent concession activity, it remains lower than what the industry has seen in the past. Berkadia reported that from the third quarter of 2009 through the third quarter of 2019, an average of 28.1% of U.S. apartment units came with concessions.

And from the third quarter of 2022 through the third quarter of 2007, that figure averaged an even higher 41.3%.

From the third quarter of 2020 through now, though, an average of just 15.2% of all apartment units in the United States came with concessions.

What has increased is the value of these concessions when compared to asking apartment rents.

According to Berkadia, from the third quarter of 2020 through the second quarter of 2024, concessions averaged 5.2% of asking rent. That is up from an

average of 4.6% from the first quarter of 2010 through the fourth quarter of 2019.

It’s little surprise that the amount of concessions has increased as vacancy rates have also risen.

Berkadia said that the multifamily occupancy rate in the second quarter of 2024 stood at 94.2%. That is a dip of 50 basis points when compared to the same quarter a year earlier.

In good news for apartment operators, though, Berkadia predicts that the national multifamily occupancy rate will increase 20 basis points by the end of this year and continue to rise to 94.8% by the fourth quarter of 2025.

And that increase in occupancy should correlate to a dip in concessions.

Image by Michal Jarmoluk, Pixabay.

Laramar Group report: Occupancy, rent growth and long-term demand on the rise in medical office space

By Laramar Group

As the healthcare delivery system continues to shift toward outpatient care, a mid-year medical office review by The Laramar Group, a national real estate investment firm, shows a positive outlook for occupancy, rent growth and long-term demand.

These market conditions are generating positive momentum in several Midwest markets such as Chicago, Indianapolis and St. Louis.

An aging population and shifting healthcare delivery dynamics have pushed medical office properties to the forefront for many investors looking for stability and long-term growth. The number of people who are at least 80 years old is on track to increase by 50% during the next decade. This dynamic is expected to create rapid growth in outpatient volume and drive investor demand for medical office properties.

“The long-term outlook for medical office properties is favorable, given the continuing shift toward outpatient locations that provide proximity and convenience to support the aging population,” said Ben Slad, Senior Vice President of Investments for Laramar, which has corporate offices in Chicago and Denver. “We expect to see continued growth and demand in the medical office sector.”

In the Midwest, St. Louis ranked as the eighth top market for medical office construction, with nearly 1 million square feet delivered in 2023, according to research from Colliers and Revista. There was 10.8

million square feet of medical office space delivered across the country in 2023, up from 10.3 million square feet in 2022.

Madison, Wisconsin, had the highest share of medical office buildings under construction when compared with total inventory, reaching 16.2%. St. Louis had a 6.7% share of buildings under construction.

Nicole Haapala, Vice President, National Account

nhaapala@firstam.com | 612.816.8596

Yankee Doodle Medical Center, a 24,000-square-foot facility in Eagan, Minnesota, owned by Laramar Group.

(Photo courtesy of Laramar Group.)

Average net asking rents in this sector reached a record high of $24.37 per square foot in 2023 with the Chicago market ranking ninth with approximately $23 per square foot. Chicago also was the most active sales market in 2023, recording approximately $460 million in activity. The ninth market was another Midwest market, Indianapolis, which had approximately $220 million in sales.

Occupancy rates for medical properties have remained above 90% since the end of 2010, demonstrating the stability of this asset type.

The nature of most work done by healthcare professionals, including x-rays, blood draws, minor surgery and dental work, requires special equipment and facilities as well as patient in-person visits.

While more than 40% of information, tech, professional and business services employees now work from home, the vast majority of healthcare workers either work in a medical office or a hospital. According to the 2021 American Community Survey, just 10% of healthcare workers reported that they worked primarily from home. Medical office has not faced the structural change occurring in the traditional office sector.

An additional demand driver has been the increasing share of the insured U.S. population. The share of the U.S. population that has health insurance has increased from 81% to 90%. The increase in the insured population continues to elevate demand for physician

visits as uninsured persons typically do not visit doctors or seek medical care.

Rising construction costs and interest rates have contributed to muted supply. While deliveries in 2023 were on par with 2022, construction starts fell nearly 45% due to elevated borrowing and construction costs, according to Colliers’ research. In 2023, new starts declined from 16.2 million square feet to 8.9 million square feet. At the end of 2023, 31.9 million square feet were under construction.

Despite a multitude of demand factors, future medical office deliveries are projected to remain below the 17-year average. Because of the high cost to build out a medical office space and proximity to patients, medical office tenants tend to remain in the same space for longer, providing stable occupancy. Since 2009, medical tenant retention has averaged in the low 80% range and is currently 82.3%.

Lastly, on a national level, healthcare expenditures have been rising substantially since 1970. National healthcare expenditures as a percentage of GDP were 7.5% in 1970 and are projected to rise to 20% of GDP by 2030. The current share of healthcare spending is outsized for the 65+ age cohort, who comprise 18% of the population but account for 36% of medical expenditures annually.

supply and increased insurance coverage are driving long-term growth in medical office demand. These investments can offer strong returns, portfolio stability, and diversification across economic cycles, positioning this asset class as a strategic choice in the current real estate market.

Founded in 1989, Laramar Group is a national real estate investment corporation with a multi-billion-dollar portfolio. Laramar has a presence in more than 15 markets, with historical presence in 50+ markets, and maintains corporate offices in Chicago and Denver.

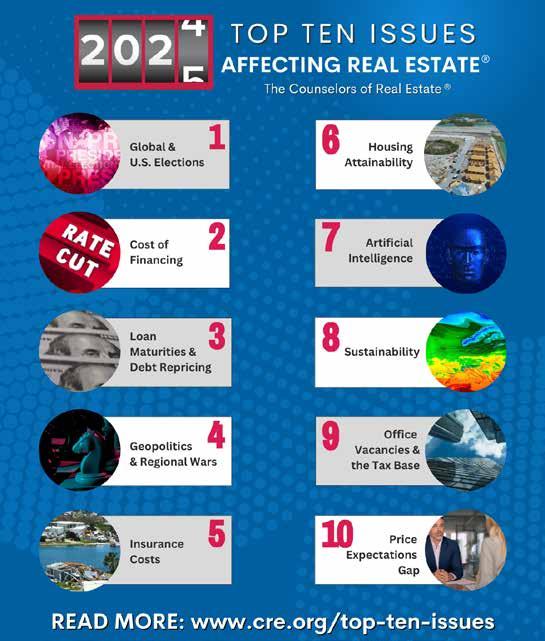

Counselors of Real Estate 2025 prediction? Plenty of uncertainty

by The Counselors of Real Estate

Political uncertainty is the leading concern for top commercial and multifamily real estate advisors as 2025 approaches—but it has a lot of competition, according to the Top Ten Issues Affecting Real Estate®, a just-released annual report from The Counselors of Real Estate®, a global organization comprised of leading property advisors. Each year, the report poses potential solutions to the industry’s most critical challenges.

In addition to political uncertainty, the real estate industry also faces $1.8 trillion in commercial real estate debt set to mature before 2026; $380 billion in economic losses in 2023 due to extreme weather; soaring insurance costs; and persistent, still-elevated interest rates. On the bright side, interest-rate induced bleeding has slowed as deal volume has begun to stabilize heading into 2025.

“This coming year, elections in more than 70 countries could shake up an already volatile geopolitical landscape, and the U.S. elections in particular will have a significant impact on regulation, trade, corporate taxes, immigration policy and sustainability,” said Anthony DellaPelle, global chair of the Counselors of Real Estate®, in the Top Ten Issues report.

“The urgency of prioritizing sustainability and climate resiliency in real estate strategies has never been more apparent, as we saw massive economic

losses last year due to extreme weather, which is also contributing to sky-high insurance costs.”

The Counselors of Real Estate® is approaching the disruptions caused by this pervasive uncertainty

YOUR PARTNER

for managing risk, making smart investments, and bringing projects to life.

• Phase I & Phase II ESAs

• Desktop Environmental Reports

• Asbestos, Lead, Radon, & Mold Services

• ESG+R Consulting

• Remedial Cost Estimates

• Environmental Remediation

• Valuation & Appraisal

• Property Condition Assessments

• Seismic Risk Assessments

• Construction Risk Management

• Compliance

• Distressed Asset Due Diligence

• Policy Consulting

with a focus on solutions, enhancing the industry’s understanding of how these issues will impact various asset classes within commercial real estate.

Top Ten Issues Affecting Real Estate in 2025

1. Political Uncertainty Pervades Every Corner – In 2025, the real estate sector is navigating uncertainty due to elections in more than 70 nations including the United States, Taiwan and the EU. In the U.S., notable real estate-related issues to watch include potential rent caps for corporate landlords and modifications to the 1031 like-kind exchange. Globally, elections could affect trade and military policies, with repercussions for the U.S. economy overall. This unpredictability complicates real estate transactions and real estate workouts for distressed assets, as investors seek clarity on economic growth, inflation, and interest rates.

2. Transactions Will Remain Tepid Amid High Financing Costs – While interest rates came down in September 2024, the financing markets remain challenged due to still-elevated rates. As a result, deal assessments and market valuations remain complex. While transaction volumes are stabilizing, uncertainty still persists. Many owners are hesitant to sell, and po-

Anthony DellaPell (Photo courtesy of The Counselors of Real Estate.)

Managing sustainability and cost amid increasingly complex environmental concerns

By Oliver Fox, Senior Director, MGAC

While owners, developers, and builders overall continue to adopt more environmentally sustainable practices, they still need to be proactive and vigilant about ever-increasing scrutiny from both investors and regulatory bodies. Sustainable and responsible practices are worthwhile in themselves, of course, but especially in an era of increased ESG mandates they are crucial for ensuring profitable and successful projects.

From conception, owners and developers can evaluate design, engineering, and construction options from a range of angles, such as building costs, scheduling projections, and difficulty of execution. This involves hard questions, including some fundamental ones.

It’s often said that the most sustainable building is the one you don’t build. However, is it better to build a new Net-Zero building and tear down a poorly performing building, considering its embodied carbon? Or is adaptive-reuse the answer? Or is it better simply to bring specific aspects of a building within local codes? Where a project lives will also impact priorities from cost and sustainability perspectives—which is to say nothing of individual organizational goals. Ultimately, owners need to make decisions based on increasingly complex sets of data—and often need to navigate mandates that may appear at first to cross

purposes, such as cost and sustainability. In other words, what is built and how it is built are one thing. How much it costs and how it can be done most ef-

ficiently are usually quite another. Long after owners, architects, and engineers determine the environmental impacts of a project, there continues to be project

PUTTING THE PIECES TOGETHER.

Getting projects built takes dedication, time – and money. Our attorneys work with clients to source and combine financing for real estate projects, and help you navigate the sometimes rocky path of real estate finance. We see roadblocks and detours as opportunities in disguise, and develop creative, practical alternatives to obstacles that arise.

Image by PIRO from Pixabay

risks and pricing concerns that are tied to decisions related to sustainability. A transparent, cost-effective, long-term project and cost management approach is crucial.

Each project presents a distinct set of environmental challenges, and while sustainability considerations are undeniably important, the financial feasibility of a project or property also remains of paramount importance. If a ground-up or renovation project doesn’t pencil out, its sustainability goals become moot because the project won’t move forward. At the very least, a building won’t maximize its utility across its lifecycle, which benefits neither the people who use it nor the owners and investors. Similarly, owners need to be intentional about upgrades to older buildings to meet increasingly stringent and punitive codes, as well as to ensure they’re future-proofed to the degree that’s possible.

Challenges include the financial burden on property owners, the need for innovative retrofitting solutions, and the pressure to maintain property value while complying with regulations. After the design and construction considerations are planned, there is still a significant effort needed to ensure that all sustainability goals are met, the project team is built to address them, and the schedule and budget can accommodate them.

A project needs to have clear benchmarks in mind and ensure that materials, building practices, and the

finished product are aligned to hit compliance goals or incentive targets. From a carbon perspective, one approach is to interrogate carbon quantities to look for potential changes at the design stage to reduce the impact. For example: How many times will an owner or occupier need to replace the material? What is the anticipated maintenance schedule and costs?

The focus isn’t just on minimizing costs; it’s about more involved cost-benefit analyses that assess the long-term financial implications of sustainable features. The approach should ensure sustainable options fit within the budget. This could involve evaluating construction methods that balance environmental benefits with cost-effectiveness, as well as lifecycle costing, which considers maintenance, repairs, and energy consumption.

Overall, resource and cost management are particularly important facets of managing projects compliantly and responsibly. This efficiency is crucial for property owners seeking to adopt sustainable practices without compromising the business side of a project. Ultimately, sustainability and project profitability are intertwined. By overseeing the alignment of the project’s environmental goals and diligently managing compliance, owners and developers can mitigate risks and enhance the outcome of a project.

Oliver Fox, is a Senior Director based in MGAC’s Washington, DC office and has more than 20 years of experience providing pre-construction and construction project control services for a variety of project types and sectors including vertical and horizontal construction.

Jen Nergard (Photo courtesy of Schafer Richardson.)

while 15% of Baby Boomers chose flexibility as their top factor in choosing a position.

The specific role was of higher importance to Gen X and Baby Boomers, with 45% and 46% placing it in their top three criteria, respectively, according to the survey. One-third of millennials chose pay and benefits as their top factor compared to 22% of Gen X and 21% of baby boomers.

“We’re seeing a clear shift in priorities across generations,” said Kari Beets, senior manager of Healthcare Research for JLL, in a statement. “Healthcare organizations need to take a nuanced approach to workplace strategy to meet the diverse needs of their multigenerational workforce.”

The research also shows the importance of location factors, including proximity to affordable housing, shopping and restaurants; safety; and convenience. For employees considering leaving their roles, 22% said that their jobs were too far from affordable housing, likely contributing to their desire to leave.

“If you can’t move your location, explore how to change your location,” said Jay Johnson, U.S. practice leader for Healthcare Markets at JLL, in a statement. “By making improvements that speak to the concerns

that lead to attrition, healthcare organizations can improve employee experience and satisfaction.”

How can healthcare employers make their workspaces more attractive to potential employees? According to JLL’s survey, addressing safety issues should be a priority. Employers can add lighting and boost security patrols.

Employees also enjoy working near restaurants, shopping and other amenities, according to JLL’s survey. Healthcare providers who also own facilities can attract restaurants and shopping nearby, JLL said in its report. Another option? Health systems can join with state and local programs to kickstart affordable and workforce housing developments or partner with private developers themselves.

Healthcare providers who want to retain employees need to give them a pleasant place at which to work. According to JLL’s survey, employees planning to stay in their current positions were more likely to report that their workplace enabled them to work productively (93%), provides technology to help with efficiency (90%), allowed them to care for patients effectively (88%) and supported their overall well-being (87%).

“There are numerous ways they can improve the employee experience through thoughtful workplace

Creating Spaces Realizing Goals

Enclave’s build-to-suit industrial platform harnesses the strength and expertise of our unified team.

Prioritizing your vision and investment results in a seamless project delivery, providing space to realize your goals.

Warehousing Build-To-Suit Solutions

Logistic Centers

Cold Storage

Showrooms

Data Centers

design and amenities,” said Andrew Quirk, Institutional Industries Lead for Project and Development Services at JLL, in a statement. “Providing well-maintained spaces for rest and recharging like breakrooms and outdoor areas with green space can have a significant positive impact. Just as important as creating and maintaining them is ensuring these spaces are accessible to all employees.”

Counselors from page 14

tential buyers are wary of high prices, still expecting a surge in distressed asset sales due to upcoming loan maturities. The Counselors’ report predicts that buyers will continue to adopt a cautious approach, focusing on higher cap rate deals, with a more aggressive market re-entry likely not materializing for another two years.

3. Commercial Real Estate Market on the Edge of a $1.8 Trillion Debt Cliff – The real estate sector faces a looming $1.8 trillion in commercial loan maturities by 2026. While lenders are increasingly extending these loans in hopes of better market conditions, this temporary relief may soon reach its limits as banks grapple with regulatory constraints and insufficient capital reserves. While forecasts suggest a decline in federal funds rates from 5.25–5.50% to around 3.5–4.0% by the end of 2025, borrowers who secured loans at sub-4% cap rates may encounter debt service payments that are 75% to 100% higher. This increase, combined with a reset in property values, complicates refinancing efforts for many owners. The resolution of these maturing loans will significantly impact market dynamics in 2025, potentially triggering a domino effect that could alter competition and tenant retention across properties.

4. Expect Higher Cap Rates as Investors Price in Geopolitical Risks and Market Volatility – Ongoing geopolitical turmoil, from conflicts in Ukraine and Gaza to supply chain disruptions, is reshaping the real estate landscape. This instability drives inflation,

affects labor and housing affordability, and complicates monetary policy, all of which impact real estate pricing and risk-adjusted returns. Expect higher cap rates as investors price in greater risk. The current environment of “higher-for-longer” interest rates means returns must expand beyond the Treasury rate. In this type of disrupted market, it’s key for investors to tailor strategies to specific market conditions, as they can no longer rely on historical cycles.

5. Insurance Costs Soar as Natural Disasters Cause Hundreds of Billions in Losses– Towering insurance premiums, driven by inflation, increased property values and extreme weather, are hitting real estate owners hard. In 2023, natural disasters caused $380 billion in losses, with only 31% covered by insurance. Residential, hospitality, and senior living properties are particularly impacted, with rising claims and “runaway juries” inflating awards. Government legislation, like California’s habitability lawsuits, adds further pressure. The old model of buying insurance is fading as owners focus on risk management, rightsizing coverage, and exploring alternative risk transfer solutions to control escalating expenses.

6. The Dream of Affordable Housing Slips Further Out of Reach – Housing affordability continues to worsen due to rising costs and a shortage of 4.4 million units. Multifamily rent growth has slowed, but rents have climbed 45% over the past 15 years. Despite increased construction, development is uneven, concentrated in major metros, and insufficient to meet de-

mand. Nearly 54% of renters are now cost-burdened, spending over 30% of their income on housing. Declining multifamily construction and growing demand from younger renters suggest affordability challenges will intensify in 2025. Solutions require both building new housing and preserving existing affordable units, with private sector involvement crucial.

7. Artificial Intelligence (AI) Impact Hinges on Data Accessibility and Accuracy – AI’s role in real estate is rapidly evolving, with focus shifting to the accuracy, granularity, and timeliness of data inputs that drive algorithms. While AI can optimize certain processes, commercial real estate still faces challenges with fragmented data and location-specific nuances. As AI algorithms demand significant computing power, data centers are booming, but advancements in algorithm efficiency could change their appeal as investment opportunities.

8. Extreme Weather Events Propel Need for Resilience and Regulation – Increased frequency of hurricanes, wildfires, and floods have caused billions in property damages. In Europe, new regulations like the EU’s Corporate Sustainability Reporting Directive and the U.K.’s Minimum Energy Efficiency Standards are setting strict sustainability rules, while U.S. regulations remain fragmented. As extreme weather and investor demands grow, the business case for resilient properties is stronger than ever, driving a need for investment in green technologies and AI.

9. Office Vacancies Will Drive Adaptive Reuse in Urban Cores – A generational shift is happening in cities, as how people use offices stabilizes into a new paradigm—leaving many office buildings poised for adaptive re-use into residential, healthcare and educational uses with the potential to revitalize urban cores. U.S. office vacancy rates are expected to peak at 19.7% by the end of 2024, leading to lower occupancy rates and declining property values, particularly in cities like New York and San Francisco. This structural shift impacts tax bases, city finances, and the broader real estate ecosystem; however, while converting offices is a potential solution, it’s costly and complex.

10. Buyer-Seller Price Gap Narrows – Some good news amongst uncertainty: the divide between buyers and sellers on asset prices persists but is no longer widening. Pricing declines, especially in sectors like core business district (CBD) office, are slowing, providing hope for stabilization. Industrial real estate has been less affected, showing an 8.6% annual price increase. As interest rates stabilize, the worst of the pricing shock appears to be over. However, loan maturities could force sellers to adjust expectations, pushing more deals as refinancing pressures build. More declines in interest rates or stronger rent growth would also help further bridge the gap.

Slowdown

from page 1

Tenants looking for smaller spaces of 20,000 to 40,000 square feet, though, are still active in the Minneapolis-St. Paul market, Mork said.

These companies are simply nimbler and able to make decisions faster, he said.

“It comes down to the company approval process,” Mork said. “The smaller companies are not publicly traded. If they have a need, they fill it. This might not be an ideal market, but if they need another 30,000 square feet, they’ll make the move. They can react faster than the bigger companies.”

Mork said that he doesn’t expect the demand from these smaller, often regional, companies to lessen any time soon. The fundamentals of the Twin Cities market remain strong, he said.

“The nice thing about the Twin Cities is that it’s not overbuilt,” Mork said. “There is not a ton of new industrial construction right now. It’s difficult to get financing for new developments. Land prices are not in line with the market. We are not seeing much new product being added to the market.”

Mork said that he expects industrial vacancies to fall. Demand for industrial space will rise, he said. And when it does, there won’t be enough space to meet it because of the current slowdown in new industrial construction.

“We will see a tighter market,” Mork said. “There will be fewer options for tenants. There will be a chance for landlords to push rents and annual escalations. I think we’ll see vacancies start coming down soon.”

This isn’t to say that the Twin Cities industrial market doesn’t face challenges. Mork pointed to the Minnesota legislature and the city councils in Minneapolis and

St. Paul. These government bodies continue to send large sums of money, Mork said. To help fund that? Mork predicts that they will fund it partly by increasing taxes on industrial real estate and residential homeowners.

“Values are only going to go up in industrial real estate,” he said. “Every other commercial segment is flat or going down. Industrial real estate has a target on its back. I’m worried that higher taxes will drive corporations out of Minnesota. That will be unfortunate.”

When will new industrial development begin rising again? No one knows for sure, but does predict that industrial construction activity will pick up soon, thanks in part to the lower interest rates resulting from the Fed’s decision to cut its benchmark interest rate.

At the same time, the cost of construction is also coming down, Mork said.

And when construction starts up again? Certain Twin Cities submarkets will likely see more activity than others. Mork said that the southeast submarket of the Twin Cities remains strong. The northwest quadrant has long been solid and will continue to be so, he added.

Mork also pointed to the Dayton and Rogers markets, which he said are strong today and will only grow stronger as sales and construction activity increase. Mork said that the Interstate-94 corridor in the Woodbury market is seeing a jump in industrial leasing activity, too.

At its heart, a business is about people. A group of people coming together to create something bigger than themselves. To create a solution or a product or an experience in the service of other people. At Huntington, it’s our belief that running a business is about more than making money, it’s about making people’s lives better. So let’s roll up our sleeves and get to work, together.

People are at the heart of what we do.

At its heart, a business is about people. A group of people coming together to create something bigger than themselves. To create a solution or a product or an experience in the service of other people. At Huntington, it’s our belief that running a business is about more than making money, it’s about making people’s

and get to work, together.

Peter Mork (Photo courtesy of Capital Partners.)

Paul Hyde (Photo courtesy of Hyde Development.)

Slowdown to page 24

Slowdown

from page 22

“Minnesota is a very conservative state when it comes to new development and pushing rents,” Mork said. “The market is not overbuilt. We have a great education system here with a highly educated workforce. We always attract new companies and talent. It’s a great place to live. The qualify of life is high. If our local and state government don’t tax people out of the state, this is a great place to do business.”

Ready for a brighter industrial future

Paul Hyde, chief executive officer of Minneapolis’ Hyde Development, said that the industrial sector in the Twin Cities region is now going through a correction.

Leasing demand for industrial space soared during the COVID pandemic.

“There was a sense that all commerce would be ecommerce,” Hyde said. “People were gobbling up space left and right, especially large users. Large industrial deals became common.”

To meet this demand, developers added larger industrial spaces to the Twin Cities market, including properties of 500,000 to 1 million square feet.

And when demand inevitably slowed after this boom period? It’s led to a slight increase in vacancies and far less industrial leasing activity today.

“Some of those larger industrial spaces were a result of that over-enthusiastic COVID reaction to demand,” Hyde said. “That led to a rise in construction costs and significant impacts on the supply chain for building materials. Your typical four months of lead time for precast panels or steel got pushed out to 12, 14 months or longer.”

The slowdown in leasing activity, spurred in large part by rising interest rates, has resulted an equally dramatic slowdown in new industrial construction, Hyde said.

This slowdown was necessary, correcting the oversupply of industrial product in the Minneapolis-St. Paul

Photo courtesy of Capital Partners.

The Northern Stacks Project by Hyde Development. (Photo courtesy of Hyde Development.)

market. It also slowed the acceleration of construction cost increases and normalized the lead times for building materials such as precast panels and steel, Hyde said.

Hyde says that this is setting the local industrial market up for its next growth cycle, one that this industry veteran says should start in 2025.

“Everything that needed to happen to correct the market has happened,” Hyde said. “This points toward a promising future for industrial during the next several years. As long as interest rates keep coming down, we’ll be in really good shape.”

Hyde said that as interest rates fall, construction activity in the industrial sector will begin to rise. That’s

largely because as tenants look for space in the Minneapolis-St. Paul market, they’ll see that there isn’t much available because of the recent slowdown in new deliveries.

As leasing demand increases, companies such as Hyde Development will begin building new industrial properties.

Hyde is predicting that new construction activity will begin in 2025 and only grow stronger in 2026.

“The last thing we are all hoping to see and are counting on is that interest rates will keep ticking down,” Hyde said. “With commercial real estate, 60% or sometimes more of the capital to build these buildings comes from loans. If interest rates are high, it is

more expensive to build. Then owners need to charge higher rents, and you run up against how much tenants are willing to pay. If interest rates come down, so will the cost of building and rents. That will spur new construction.”

Hyde Development is already seeing positive signs. Hyde completed construction on a 200,000-squarefoot industrial property in Fargo, North Dakota, in February. The company signed a lease in October that filled the last remaining vacant space in that property.

A tenant signed a million-square-foot lease to fill Hyde Development’s 76 Commerce Center development in Brighton, Colorado. And at Hyde’s The Waters in Eagan, Minnesota, occupancy has jumped from 80% leased to 96%.

Hyde said that tenants are smart to lease industrial space today. When new construction activity ramps up again, industrial rents will rise. Tenants today, though, can still land a solid deal when leasing industrial space.

“It takes a bit of courage, but companies that see what is coming are acting now,” Hyde said. “They are jumping in the water and leasing space now while they can get a better deal.”

What makes these Hyde developments so attractive to tenants? Hyde says that these buildings are Class-A quality and are either newly built or recently renovated. They are also located on infill sites close to urban cores. They are near quality labor and large customer bases.

“In a slower market, the best buildings get leased first,” Hyde said.

The Waters development from Hyde Development in Eagan, Minnesota. (Photo courtesy of Hyde Development.)

Divide from page 1

Many companies are also leasing a smaller amount of square feet but in higher-quality office properties, Krosschell said. This way, they can provide their workers with more attractive and comfortable office space while not spending much more than if they were renting more square feet in a less expensive property.

“As we mention in our report, there is a clear divide between which office properties are seeing activity and getting leased and which are not,” Krosschell said. “New or recently renovated space is performing better. There is a huge opportunity here for landlords to elevate their buildings to compete and be in contention for more tenants moving forward.”

A positive sign

Demand for office space in the Minneapolis-St. Paul office market rebounded in the third quarter after a weak second quarter, with leasing activity up more than 58% when compared to the second quarter of 2024, according to Avison Young’s report.

The problem? Leasing volume remains down 28% through the first three quarters of this year when compared to the same period in 2023.

Again, though, not all office properties are seeing the same struggles. An example? When comparing the first three quarters of 2024 to the first three of 2023,

BUILDINGS ARE COOL

should know. We design the behind-the-walls systems that bring them to life.

One Southwest Crossing in Eden Prairie is an example of a modern office property that is in demand by tenants today.

(Photo courtesy of Avison Young.)

office leases of under 10,000 square feet grew from 37.9% to 48.6% of sector transaction activity.

Larger offices are experiencing more leasing struggles today, according to Avison Young. Office leases of more than 100,000 square feet decreased from 22.8% to 11% of transaction activity during the first three quarters of this year when compared to the same period in 2023.

Newer office properties remain in higher demand, too, as Krosschell emphasized. Avison Young reported that Minneapolis-St. Paul office buildings built after 2010 experienced a 16.5% decrease in availability, falling from 37.9% in the first quarter of 2020 to 21.4% in the third quarter of 2024.

In contract, the availability of office properties built before 2010 has increased from 14.5% in the first quarter of 2020 to 22.11% in the third quarter of 2024.

That’s yet more evidence that that the flight-to-quality trend is not only very real but is still happening.

“In our report, it is clear that we are seeing the office sector perform in a segmented manner,” said Joseph Stockman, market intelligence analyst with Avison Young. “The high-quality and well-positioned assets are driving any increases in leasing activity.”

to page 28

Tate Krosschell (Photo courtesy of Avison Young.) Joseph Stockman (Photo courtesy of Avison Young.)

Slowdown

Stockman said that the Minneapolis-St. Paul market is far from a rarity. This trend is playing out across the country, he said.

“The segmentation of the market is becoming a prevalent theme,” Stockman said. “Companies want to move into higher-quality office space.”

Krosschell pointed to office properties such as North Loop Green, RBC Gateway and 10 West End, all of which are seeing high levels of leasing activity. All three properties are newer and highly amenitized. They are also located in busy areas that feature plenty of restaurants and retail.

“North Loop Green and RBC Gateway had a ton of pre-leasing,” Krosschell said. “By the time they delivered, they were at least half full. They are also getting higher rental rates. It points to that flight to quality. People want to be in the newest buildings.”

And for brokers looking for a bit of hope in the office sector? Avison Young reported that the number of office job postings is rising. Avison Young said that job postings in office-using industries increased in August of this year to 6.7% higher than January of 2023 levels.

What about the older office properties?

But what about those older office properties? What will happen with Class-C office space in the Minneapolis-St. Paul market?

“That is the million-dollar question,” Krosschell said. “What happens with the space that might become functionally obsolete? I believe that obsolete buildings will be taken off the market. There is always a need for true value space for tenants that don’t want to pay Class-B or -A rents. But I do think we will see properties taken off the market if they become obsolete.”

Some older office properties might be converted to other uses. But conversions don’t work for all buildings. That’s why Krosschell says that some older office properties might be razed. Developers can then start over with a new use, such as multifamily, on that now vacant land.

“The land becomes more valuable than the property at that point,” she said.

Krosschell said that while the Twin Cities office market does face challenges, it’s been largely resilient, too. Vacancy rates here could be even higher. Krosschell points to the high number of Fortune 500

companies with a presence in the market as one reason for the sector’s resiliency when compared to other large markets.

Minneapolis-St. Paul features a vibrant downtown, too, with plenty of entertainment, shopping and dining options. This is attractive for companies looking to locate in a metropolis that offers plenty to do for their employees.

“When people move here, they tend to want to stay here,” Krosschell said.

Avison Young has developed a tool to measure how busy CBDs across the country are today, its Busyness Index. Stockman says that this tool evaluates cellphone and GPS tracking technology to determine visitation levels in central business districts.

Stockman said that traffic in in the CBDs that Avison Young tracks stands ats about 60% of where it stood pre-pandemic. In Minneapolis-St. Paul, that figure stands at about 50%, above markets such as Seattle and Jacksonville, Florida, but below many others.

2024 Minnesota

COMMERICAL REAL ESTATE INVESTMENTsummit

UPCOMING EVENTS

November 6, 2024

26th Annual Minnesota

Industrial Summit

4 Hours CE APPROVED

November 14, 2024

20th Annual Minnesota

Commercial Real Estate Investment Summit

4 Hours CE APPLIED for

November 20, 2024

12th Annual Minnesota

Condo & Homeowners Association Summit

4 Hours CE and CAI APPLIED for

December 6, 2024 11th Annual Minnesota Affordable Housing Summit

4 Hours CE Will be APPLIED for

December 11, 2024 12th Annual Minnesota Office Summit

4 Hours CE Will be APPLIED for

January 9, 2025 20th Annual Minnesota Apartment Summit