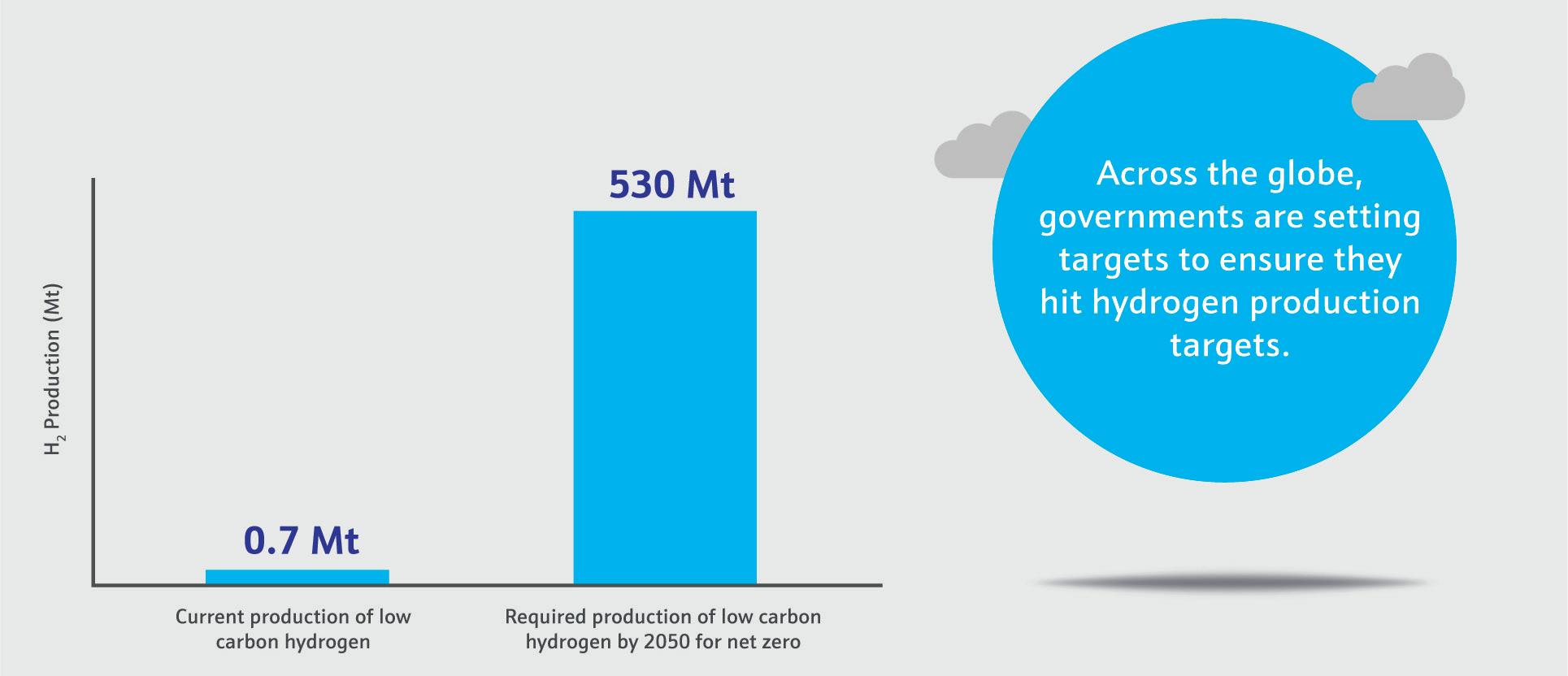

Baker Hughes is looking to the future of hydrogen applications

Any process that moves or stores hydrogen requires a valve.

Rest assured that when designing systems for hydrogen production, transportation or storage you’ve got the best and safest in control and pressure relief.

Face new challenges with confidence with Baker

Hughes Valves

03 Comment

04 Hydrogen industry outlook for the MENA region

Aliaksei Patonia and Martin Lambert, Oxford Institute for Energy Studies, UK, explore the MENA region’s hydrogen outlook and the latest developments and challenges that it faces.

10 Navigating complex pathways

Eugene McKenna, Johnson Matthey, Henrik Solgaard Andersen, Equinor, and Nilay Shah, Imperial College London, explore the intricate landscape of energy transition decarbonisation and the critical role of hydrogen.

13 Capturing value from renewable hydrogen megaprojects

Hydrogen developers can use digital twins to improve the economic viability of renewable projects and meet increasing demand. Nas Andriopoulos, Dominik Don, Joaquin Ubogui, and Maurits Waardenburg, McKinsey & Co., illustrate how, using renewable hydrogen as an example.

17 Unlocking plant performance in an uncertain world

Ben Laws and Nicolai Szeliga, Siemens Digital Industries, explore how Digital Twins and the process optimisation capabilities that they bring are becoming essential components of green hydrogen projects.

24 A newly rising energy vector

Antoine Ghorayeb, Ali Natour, and Yann-Olivier Placiard-Fleys, Saipem SA, present a case study for the implementation of large-scale ammonia (NH3) storage and cracking on board of a unique concrete hull by means of a gravity-based structure (GBS).

29 Ambition, matched with pragmatism, can unleash hydrogen’s power

Javier Cavada, Mitsubishi Power, outlines the approach required from governments and decision-makers worldwide to fulfil the potential of

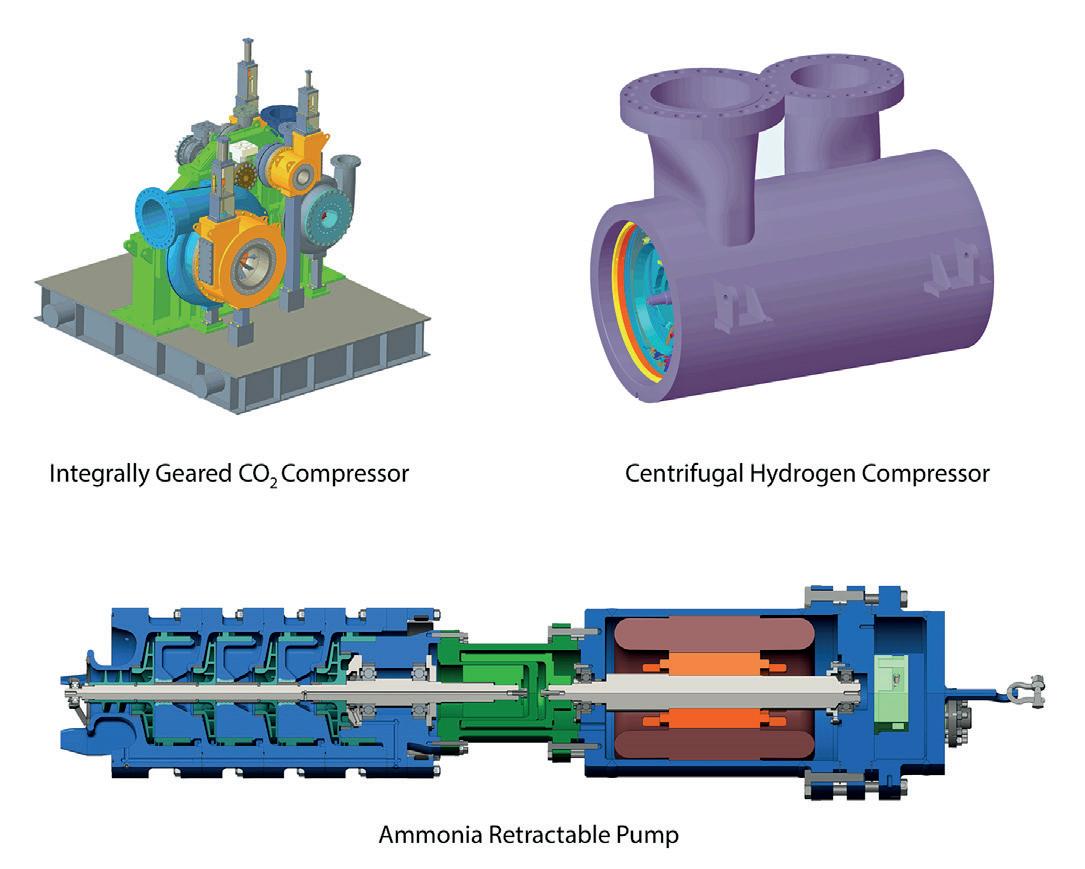

33 The sustainable energy turbomachinery infrastructure dilemma

Klaus Brun, Ebara Elliott Energy, USA, addresses the challenges associated with adapting turbomachinery in order to meet the demands of sustainable energy and hydrogen production.

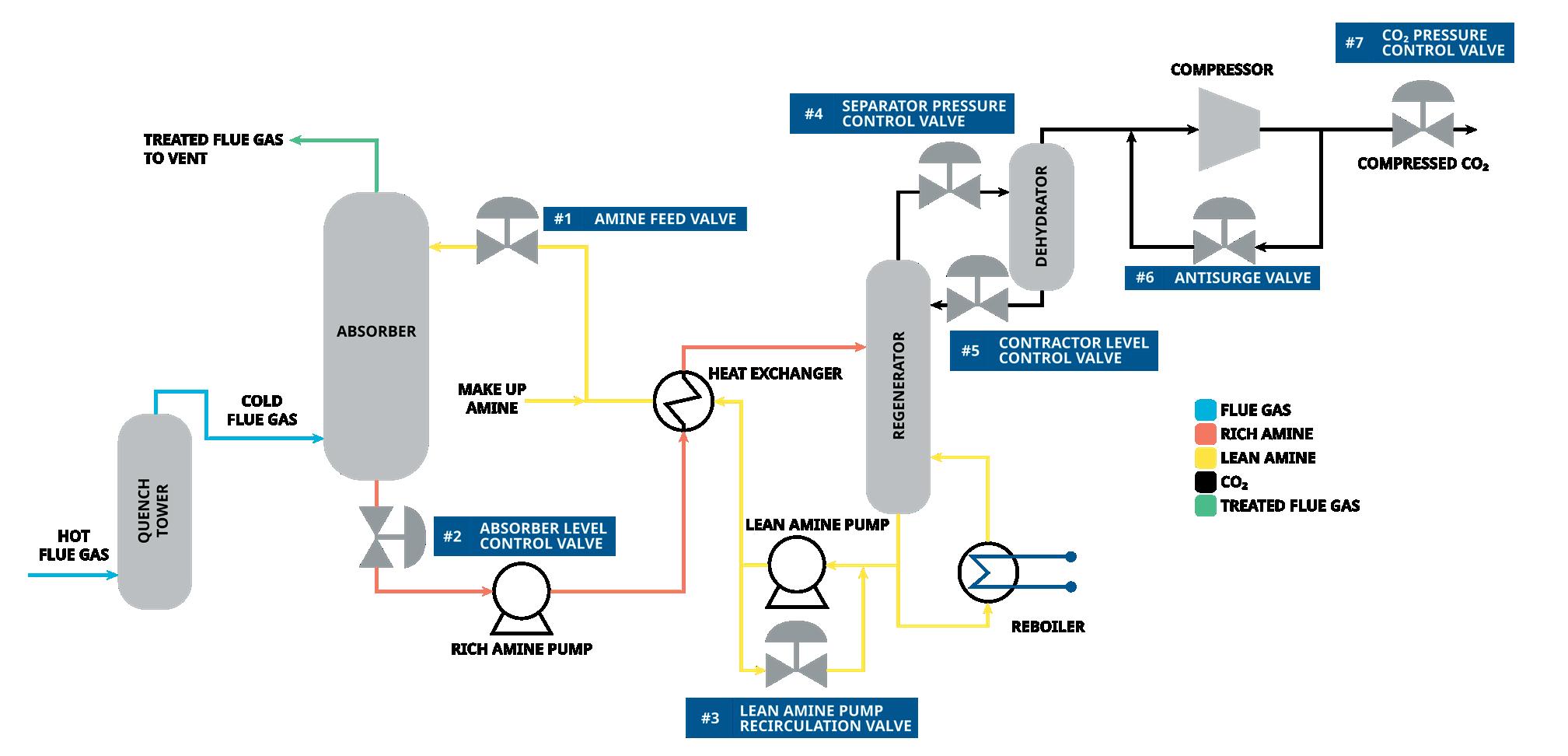

36 From grey to blue

Scot Bauder, Emerson, USA, explains how properly specified valves and related control equipment can ensure reliable operations when designing the systems required to convert grey hydrogen to blue hydrogen.

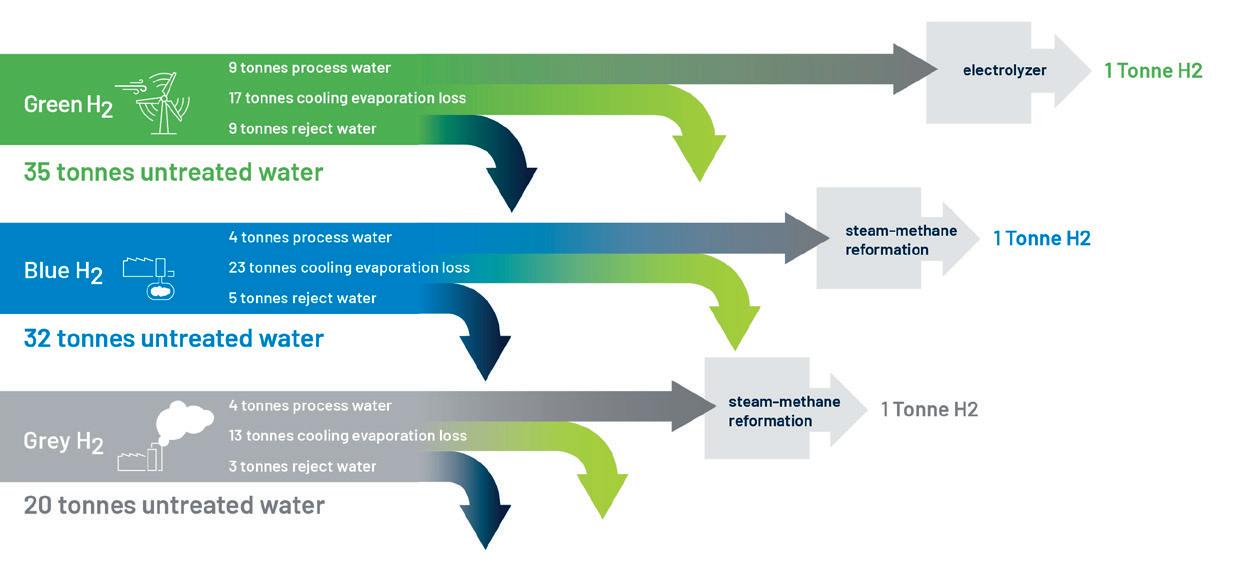

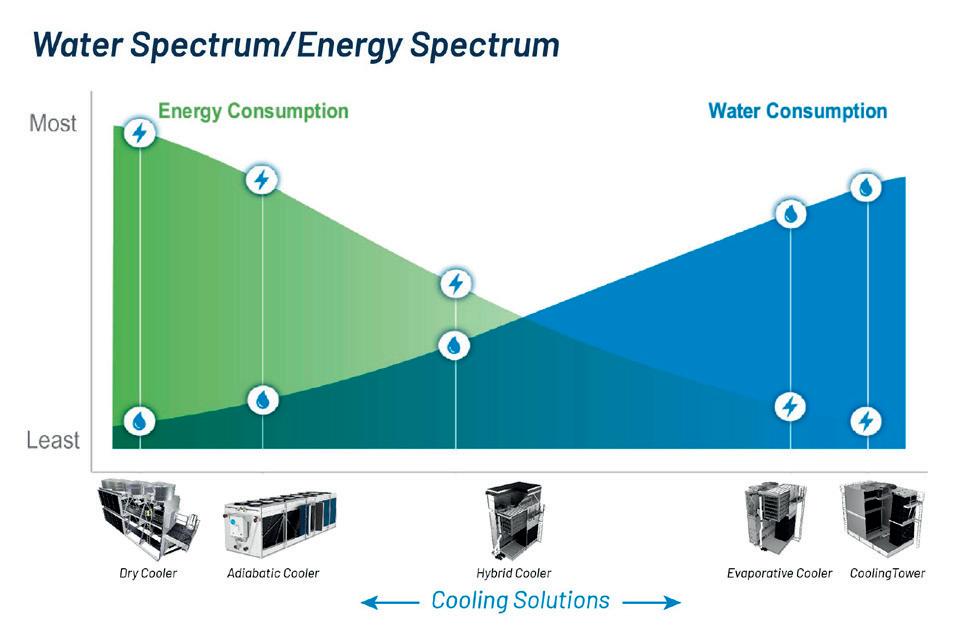

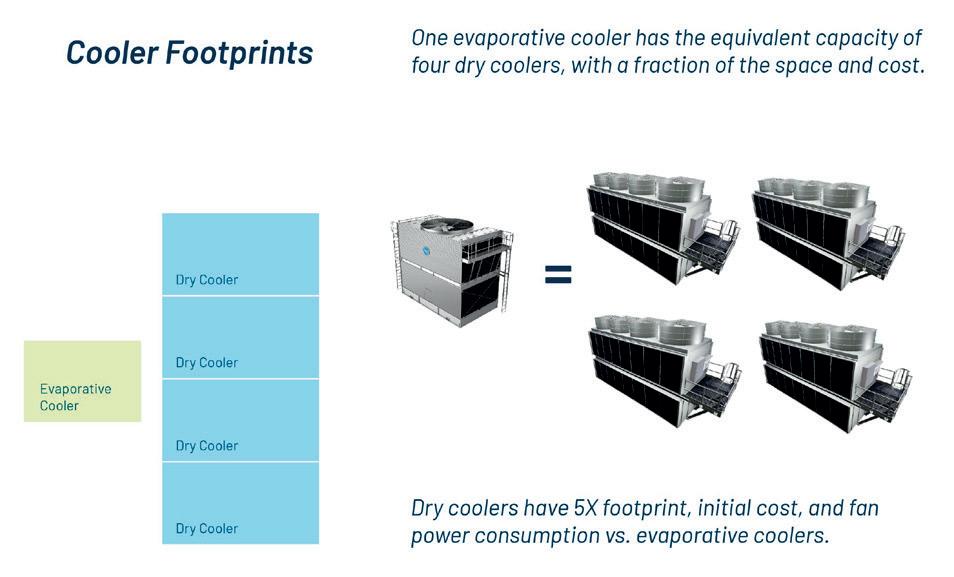

41 Water saving solutions

Blair Garrett, BAC, USA, explores options to solve the challenges of water management in hydrogen production.

45 PEM’s promise

Matt Behrns and Dr. Alex Papandrew, Mott Corp., USA, explore how scaling up efficient proton exchange membrane (PEM) solutions will be key for the future energy landscape.

49 Switch to green

Richard Koeken, Fluid Components International (FCI), the Netherlands, and Florian Stahl, Ekomat Gmbh & Co., Germany, discuss the role of accurate liquid/air flow monitoring switches in producing green hydrogen from renewables using PEM fuel cells.

53 Sensing safety

Michael Nofal, H2scan, USA, and Robert H. Shelton, H2C Safety Pipe, USA, look at ways to enhance the safety and efficiency of green hydrogen transport.

57 Handle with care

Rosanna Tumolo, Neohance, the Netherlands, and Andrea Manfredi, Sensitron, Italy, outline why advanced detection technologies are vital in mitigating the safety risks associated with hydrogen use across various sectors.

61 Sustainable steelmaking

Rhys Jenkins, Servomex, UK, explores how greater hydrogen use can support the decarbonisation of the steelmaking industry.

Hiperbaric is focused on the development, manufacture and commercialisation of hydrogen compression technology generating pressures of up to 500 and 1000 bar. Hiperbaric’s range of compressors offers a complete plug-and-play solution, adaptable to any level of production and demand. The hydraulically driven piston compressor units are safe, efficient and reliable. Hiperbaric is a global leader in the development of high pressure technologies for different sectors and applications, with installations in more than 50 countries.

Scaling the Hydrogen Ecosystem

Secure the project funding you need and advance to net zero

Ready to start your clean-hydrogen project? Yokogawa can help you qualify for investment, design profitable production, and ensure capturing critical government incentives, all while maintaining focus on safety and security. Our hands-on, solution-oriented approach will help you reduce risks, optimize processes, and enable faster, more informed decisions. Together, we can build a sustainable hydrogen economy, driving us toward a net-zero future. yokogawa.com

Poppy Clements Assistant Editor

Managing Editor James Little james.little@palladianpublications.com

Senior Editor Callum O'Reilly callum.oreilly@palladianpublications.com

Assistant Editor Poppy Clements poppy.clements@palladianpublications.com

Editorial Assistant Emilie Grant emilie.grant@palladianpublications.com

Sales Director Rod Hardy rod.hardy@palladianpublications.com

Sales Manager Chris Atkin chris.atkin@palladianpublications.com

Sales Executive Ella Hopwood ella.hopwood@palladianpublications.com

Production Manager Kyla Waller kyla.waller@palladianpublications.com

Head of Events Louise Cameron louise.cameron@palladianpublications.com

Digital Events Coordinator Merili Jurivete merili.jurivete@palladianpublications.com

Digital Content Coordinator Kristian Ilasko kristian.ilasko@palladianpublications.com

Digital Administrator Nicole Harman-Smith nicole.harman-smith@palladianpublications.com

Events Coordinator Chloe Lelliott chloe.lelliott@palladianpublications.com

Junior Video Assistant Amélie Meury-Cashman amelie.meury-cashman@palladianpublications.com

Admin Manager Laura White laura.white@palladianpublications.com

The British pop singer, Ed Sheeran, has been hitting the headlines in the UK for a couple of reasons in the last few weeks. It was not only his awkward interruption of a post-match interview with Manchester United’s new manager, Ruben Amorim, that has been criticised by the media, but also his objection to the 40 th anniversary edition of Band Aid’s charity Christmas song, ‘Do they know it’s Christmas?’

Sheeran’s vocals were used to create a new blended version of the single for Christmas this year, yet he has insisted that he would have declined participation if he had been asked for permission beforehand. The singer took to Instagram to cite his belief that the song projects dehumanising stereotypes of an Africa dependent on Western support and plagued by drought and poverty. Since making his opinion public, Sheeran has been praised in some quarters and criticised in others, with some perceiving his stance as a misinterpretation of the charity’s message. Over the years, the charity song has helped to raise nearly £150 million to support famine relief, an issue which threatens to become more widespread in the wake of climate change and extreme weather events.

The recent COP29 conference in Baku, Azerbaijan, shed light on the magnitude of the issue of water scarcity and the fact that nearly 50% of the world’s population live in water-stressed conditions. 1 In response to this stark reality, the COP29 Presidency introduced the COP29 Declaration on Water for Climate Action, an initiative focused on water-related climate action, including the improvement of water security, availability, quality and sanitation. Hydrogen was also in the spotlight at COP29, with the scale-up of clean hydrogen production being widely discussed, as well as a pledge being made to provide financial and technical support to facilitate the hydrogen industry in developing countries.

Considering the heavy hydrological footprint of hydrogen production and the intensified pressure on the world’s most critical resource, sensible water usage has never been more important in the hydrogen industry. As a critical component in hydrogen production, the industry must put responsible water management at the top of its list of priorities. Blair Garrett of Baltimore Aircoil (BAC) provides valuable insights into the different water consumption profiles of hydrogen production methods and outlines water saving techniques on page 41 of this issue of Global Hydrogen Review . This issue also features an interesting report by Aliaksei Patonia and Martin Lambert from the Oxford Institute for Energy Studies, focusing on the hydrogen industry’s outlook in the most water-scarce region of the world, the Middle East and North Africa.

Editorial/advertisement offices:

As outlined at COP29, the acceleration of decarbonised hydrogen production is set to continue through 2025 and with responsible growth, the industry should be hitting the headlines for all the right reasons.

1. https://cop29.az/en/pages/baku-dialogue-on-water-for-climate-action-backgroundinformation

Aliaksei Patonia and Martin Lambert, Oxford Institute for Energy Studies, UK, explore the MENA region’s hydrogen outlook and the latest developments and challenges that it faces.

Hydrogen production is currently still largely dependent on unabated fossil fuels in general and natural gas in particular. At the moment, the Middle East alone produces one-fifth of the entire world’s hydrogen from unabated natural gas. It is also the second-largest consumer of hydrogen in industrial applications after China. Given its hydrocarbon endowment and almost perfect suitability for renewable power generation, it should therefore be no surprise that the MENA region is actively attracting promoters of both low-carbon blue and renewable green hydrogen. It may serve not only as a potential strategic supplier but also as a consumer of this ‘fuel of the future’.

Despite most of the global attention in the hydrogen sector currently being paid to Europe and North America, the MENA region also appears to have a large number of clean hydrogen initiatives and is currently constructing the world’s largest green hydrogen generation facility. With 27 hydrogen production projects currently under negotiation and development in Egypt, 19 in Oman, 16 in the UAE, 8 in Morocco, and 2 in Saudi Arabia, the region is gaining momentum as one of the key global hubs for clean hydrogen development. Nevertheless, experience worldwide has demonstrated the challenge of moving projects from the development phase to Final Investment Decision (FID), and the MENA region is likely to face similar challenges.

Egypt

Currently, Egypt has the greatest number of clean hydrogen initiatives in the entire MENA region. It should not be surprising, as the country has a historical legacy in clean hydrogen production, being one of the first countries to produce green hydrogen through the KIMA plant, which began operations in 1960 using hydroelectric power from the Aswan Dam to create ammonia. However, this initiative was halted in 2019 when the plant switched to natural gas

due to economic viability concerns, marking a shift towards grey hydrogen generation that emits CO2 without abatement. At the same time, while currently Egypt is a net importer of natural gas, it is actively exploring various projects aimed at harnessing its renewable energy and green hydrogen potential, with a number of important documents signed between local and international firms.

Most notably, this year’s offtake agreement with Yara Clean Ammonia made Egypt a step closer towards the annual manufacturing of 150 000 t of green ammonia in the country. In addition to that, in mid-2024, a collaboration between the Norwegian solar power generator Scatec and Fertiglobe, a UAE-based fertilizer company, appeared to be a sole winner in the pilot H2Global auction. It is therefore expected that Fertiglobe will deliver up to 397 000 t of green ammonia by 2033 from Egypt to Europe at a contract price of €1000/t including transport costs.

At the same time, despite these advancements and the country’s impressive green hydrogen ambitions, just like most other countries in the MENA region, Egypt appears to be one of the world’s most water-scarce nations. This has a tremendous impact not only on the nation’s agriculture, health and sanitation sectors, but also on social and economic development overall. Since the production of green hydrogen via electrolysis requires substantial fresh water – between 9 and 21 l/kg of hydrogen – and no currently commercialised electrolyser technology is able to run on salt water, intensive development of large-scale green hydrogen projects in Egypt is likely to raise concerns about competing demands for this vital resource in agriculture and residential use.

Oman

The government of Oman has developed an ambitious green hydrogen strategy, creating a specific organisation, Hydrom, to structure and accelerate development of the sector. Recognising its more limited hydrocarbon resources compared to many of its neighbours, the strategy has multiple objectives, including ensuring energy security, diversifying the economy while decarbonising and supporting innovation and investment. There is a target to produce 1 million t of green hydrogen by 2030. Hydrom has already held two

auctions resulting in awards of land and infrastructure support for 8 projects, five in Duqm and three in Salalah.

So far, however, just one 300 MW project, being developed by the Indian company, ACME, is under construction, with production expected to start in 2027. In March 2024, the project signed a binding offtake agreement for 100 000 tpy of green ammonia with Yara Clean Ammonia, covering effectively all the output from the first phase of the project.

As in all countries, bringing a major project to FID is a significant challenge, but with abundant wind and solar potential and a supportive government, Oman appears well placed to move forward with green hydrogen and is attracting serious attention from international investors including Shell, BP, Posco, Engie and Fortescue to name just a few.

UAE

Overall, the UAE’s updated hydrogen strategy sets an ambitious target of producing 1.4 million tpy of low-carbon hydrogen by 2031, scaling up to 15 million tpy by 2050. This includes a mix of green, blue, and pink hydrogen, with domestic demand projected to reach 2.1 million tpy by 2031 and 10.1 million t by mid-century. In contrast to Egypt’s focus primarily on electrolytic green hydrogen, the UAE welcomes all shades of clean hydrogen, aiming to turn the country’s ambition of becoming a ‘top global producer of low-carbon hydrogen’ into reality.

While the UAE is strategically aiming for gas self-sufficiency by 2030 through increased natural gas production – meaning natural gas is likely to remain a significant part of the national energy mix – the country plans to ensure that renewables and nuclear energy together constitute 40% of its energy sources. The Barakah Nuclear Power Plant is a key component of this strategy, as it is being explored for hydrogen generation, particularly pink hydrogen, which is produced via electrolysis powered by nuclear energy.

However, just like in any other countries, the reliance on hydrogen production raises concerns regarding cost-effectiveness compared to direct electricity use. While hydrogen can decarbonise sectors such as heavy industry and transport, high production costs and challenges related to transportation and storage hinder scalability. Therefore, while the UAE’s plans are ambitious, they must carefully balance hydrogen production with direct energy utilisation to optimise resource allocation effectively.

Morocco

With eight planned clean hydrogen initiatives, Morocco is making significant strides towards establishing a green hydrogen economy, dedicating 1 million ha. of land for hydrogen projects. This initiative is part of the government’s broader strategy to transition to renewable energy sources and capitalise on the country’s abundant solar and

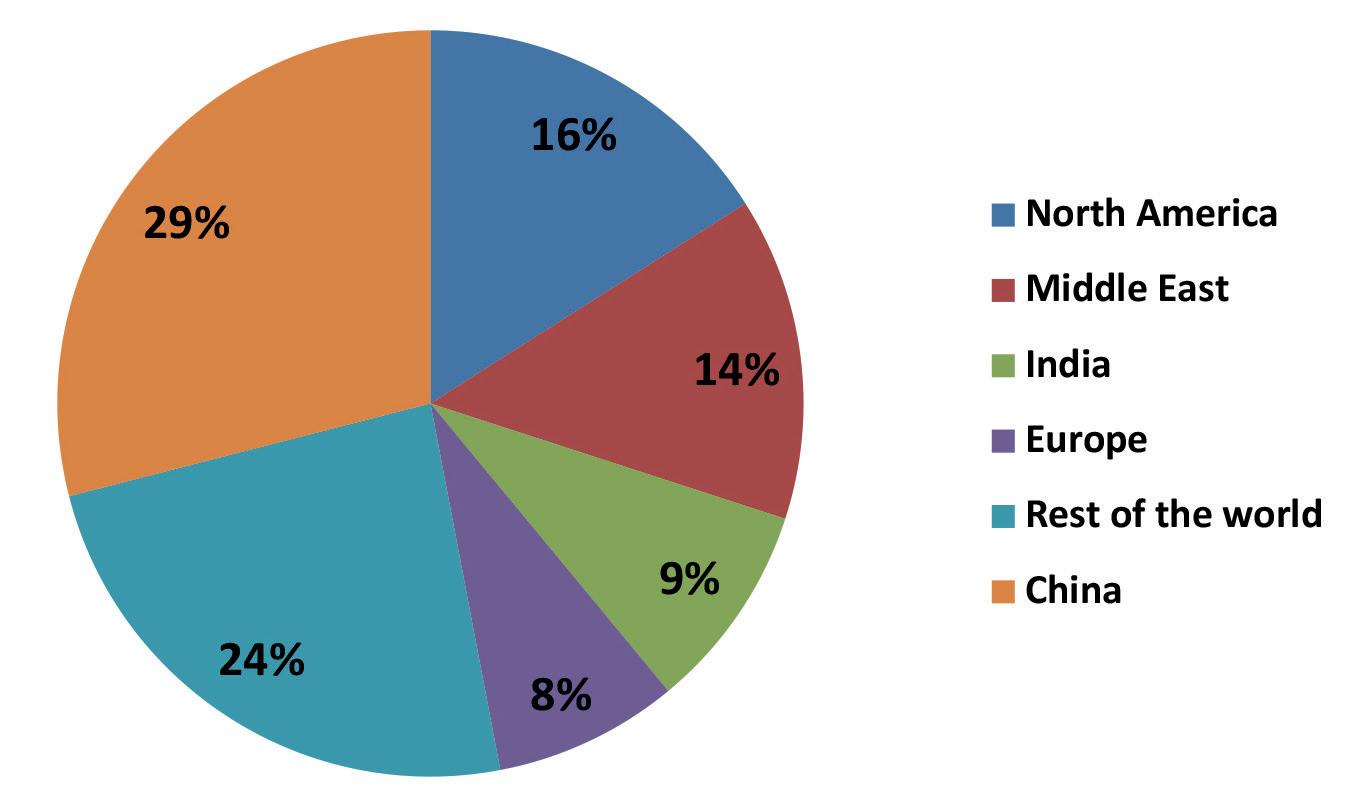

Figure 1. Hydrogen use by region, 2023. Source: IEA.

MARENÉ RAUTENBACH

Principal Scientist

Topsoe

KNOWING YOUR LOW-CARBON POTENTIAL

As decarbonization requirements go up, refining companies are looking for cost-efficient ways to bring their carbon intensity down. One way to go is low-carbon hydrogen. Using low-carbon hydrogen has the potential to support refining businesses and the energy transition by reducing the carbon intensity of fossil transportation fuels.

wind resources. Investments in green hydrogen are being supported by international financial institutions, and projects like the KfW Development Bank’s reference plant in Guelmim are set to showcase large-scale hydrogen production using renewable energy. The government’s strategy includes a phased approach to hydrogen development, focusing initially on local usage (around 121 000 tpy), and then expanding to export markets (around 303 000 tpy) by 2030.

While the Moroccan government aims to produce 52% of its energy from renewable sources by 2030, the current national energy mix remains heavily dependent on coal and natural gas. In fact, at present, nearly half of Morocco’s electricity is generated from coal, with an additional 10% sourced from natural gas, which is predominantly imported. Although this heavy reliance on fossil fuels clearly explains why the country is omitting other hydrogen ‘colours’ and focusing primarily on green hydrogen development, it raises questions about the feasibility of ramping up renewables for domestic power use before dedicating wind and solar energy to the production of green molecules. This is particularly relevant given that the conversion and inefficiency-related losses associated with manufacturing hydrogen from water using renewable power are likely to result in at least 30 - 40% energy losses. Therefore, given the current energy landscape, it may be more prudent for Morocco to prioritise increasing its renewable energy capacity for domestic consumption before fully committing to large-scale hydrogen production.

Saudi Arabia

Saudi Arabia has historically been very reliant on the oil and gas industry, which reportedly contributes 50% of GDP, 70% of government revenue and 90% of export earnings. In 2016 the government launched Vision 2030 aiming to diversify the economy away from oil and achieve a far reaching social and economic transformation. This has included pursuing various new industries such as renewable energy, tourism, entertainment and culture. Positioning the country as a major hydrogen exporter is also part of Vision 2030. Unlike some other MENA countries, the Saudi hydrogen strategy is ‘colour-blind’ with emphasis on both CCS-enabled blue hydrogen as well as renewable power driven electrolytic green hydrogen.

Saudi Arabia is home to the world’s largest green hydrogen project under construction with the

Neom Green Hydrogen project, a joint venture between NEOM, ACWA Power and Air Products to produce 1.2 million tpy of green ammonia. The US$8.4 billion project achieved financial close in mid-2023 and is expected to start production in 2026, with a renewable energy capacity of 4 GW supplying 2.2 GW of electrolysers, considerably larger than any other renewable hydrogen project under construction. It will be interesting to see whether such a first-of-a-kind large scale electrolyser and ammonia complex can be brought onstream smoothly or whether it will take time to move up the learning curve.

Meanwhile, the state oil company, Saudi Aramco is focusing on blue hydrogen and ammonia. In 2020 the company demonstrated the shipment of blue ammonia to Japan, and in July 2024 it acquired an equity interest in the Jubail-based Blue Hydrogen Industrial Gases company.

In addition, it has been reported that the Kingdom is planning to invest at least US$10 billion in clean hydrogen (presumably both blue and green) through a new vehicle, the Energy Solutions Company, owned by the Public Investment Fund, the country’s sovereign wealth fund.

Conclusion

From the above snapshot of hydrogen developments in a selection of key MENA countries, it becomes clear that there are both similarities and differences. Given the abundance of both hydrocarbon resources and renewable energy potential, it is no surprise that there is widespread interest across the region in both blue and green hydrogen. It also follows the pattern seen elsewhere in the world of a large number of potential projects of which only a few have already achieved, or are indeed likely to ever reach, FID. Many projects in the region, unlike those in Europe and the US, are largely focused on export markets rather than domestic use, and therefore ammonia is commonly considered, given it is much easier to transport than hydrogen itself. In terms of differences, however, it is notable that some countries, for example Egypt and Oman, are focusing on green hydrogen, while others like the UAE and Saudi Arabia are taking a more technology-neutral approach. We remain at an early stage of development of the global hydrogen economy, but despite the undoubted challenges including water scarcity and the need to decarbonise their own energy systems, the countries of the MENA region are clearly important players.

Table 1. Leading clean hydrogen developers in the MENA region

Turn to Ebara Elliott Energy for operational flexibility in hydrogen applications.

Ebara Elliott Energy’s solution for hydrogen compression features flexible, configurable, and economical options for hydrogen applications. Designed with proven Elliott® compressor technology, the Flex-Op’s™ compact arrangement of four compressors on a single gearbox maximizes compression capability with enough flexibility to run in series, in parallel, or both. Turn to the experts at Ebara Elliott Energy for a partnership you can trust.

Learn more about our clean energy initiatives at elliott-turbo.com.

Advanced energy technologies for a sustainable future.

Eugene McKenna, Johnson Matthey, Henrik Solgaard Andersen, Equinor, and Nilay Shah, Imperial College London, explore the intricate landscape of energy transition decarbonisation and the critical role of hydrogen.

As demand for hydrogen surges, driven by ambitious sustainability targets from industries and governments, the conversation focuses on overcoming critical challenges related to scalability and cost efficiency. Despite the clean hydrogen project pipeline expanding to US$570 billion, only 7% of hydrogen projects have secured Final Investment Decisions (FID).

Challenges in scaling the hydrogen economy

The rising demand for hydrogen driven by industries and governments aiming for ambitious sustainability goals necessitates a focus on overcoming critical challenges such as scalability and cost efficiency.

Challenges and delays in scaling up the hydrogen economy underscore the complexity of this endeavour. Over the next 30 years, the objective is to entirely restructure the energy infrastructure that has driven global growth since the Industrial Revolution.

Scaling up the hydrogen economy to match the vast infrastructure of the fossil fuel economy is a monumental task. This transformation requires developing both upstream and downstream components simultaneously. Successful projects are those where stakeholders collaborate vertically, from initial energy input to the end user.

Types of clean hydrogen

There are two primary types of clean hydrogen: electrolytic hydrogen and low-carbon hydrogen.

Electrolytic hydrogen is produced by splitting water using renewable energy to create green hydrogen. This is a fascinating and rapidly growing industry, but the production method faces significant industrialisation and scaling challenges across the supply chain.

Low-carbon hydrogen is produced from natural gas with carbon capture and sequestration. This approach is mature and currently deployed worldwide, providing a scalable solution for kick-starting the hydrogen economy.

Role of low-carbon hydrogen

For now, scalability is best achieved with the mature technology of low-carbon hydrogen. This involves producing hydrogen from natural gas and sequestering the resulting carbon dioxide. Developing large-scale plants that produce substantial amounts of clean hydrogen will serve as lighthouse projects around which the rest of the hydrogen economy can develop.

One challenge is that low-carbon hydrogen is not yet a fungible commodity. Developing robust value chains and building out entire ecosystems simultaneously is essential for scaling. Developing a hydrogen project requires more than considering the inputs and production volume. Developers must also consider partners for hydrogen storage, transportation, and most importantly, the end users. Coordination and collaboration across the entire value chain are essential. Policy support, procurement subsidies, and government actions must be ecosystem-oriented, benefitting the whole value chain rather than focusing on individual players. A narrow focus on single entities will hinder scaling and development.

The companies likely to succeed in the next five years will not necessarily be those inventing new technologies but those effectively utilising the best available components and demonstrating strong project competence.

Connecting production with offtake is crucial. At Saltend (UK), Equinor built the plant next to all off-takers, but pipelines are essential for scaling up and reaching larger markets. In some areas of Europe there is a dual system initially based on the Groningen gas field, which is now shutting down. Much of the hydrogen pipeline development in northern Europe involves repurposing these low-calorific value pipelines.

While some modifications are needed, this presents a smaller barrier to developing the necessary infrastructure and, generally, in Europe, the TSOs are very proactive and forward-thinking.

Accessing talent and expertise

Scaling hydrogen production presents challenges in accessing expertise in project development and technology. Many project developers possess a high-level understanding of hydrogen projects. However, especially for green and to a lesser extent blue hydrogen, significant practical integration assistance is often required. This includes managing the integration of variable renewable energy, deciding on battery storage needs, and accessing carbon capture and storage infrastructure.

In the UK alone, there are 300 000 people who know how to work with natural gas from upstream and offshore to home boilers. These individuals can make an important contribution to hydrogen development.

Future of blue and green hydrogen

The debate on the best path forward for hydrogen – blue or green – remains significant, with both expected to play crucial roles in the energy transition. The answer varies by region, but both types of hydrogen are essential. Blue hydrogen facilities are advantageous in regions with a significant focus on industries requiring baseload hydrogen, while green hydrogen will progress rapidly as more clean electrons become available.

The goal is to develop chemical feedstocks and energy carriers essential for decarbonising the energy and chemicals sectors without greenhouse gas emissions. Focusing on the carbon intensity of these processes is crucial for future-proofing the technologies people invest in.

Deploying the best possible technology is essential to ensure scalability and futureproofing. In advancing large-scale projects,

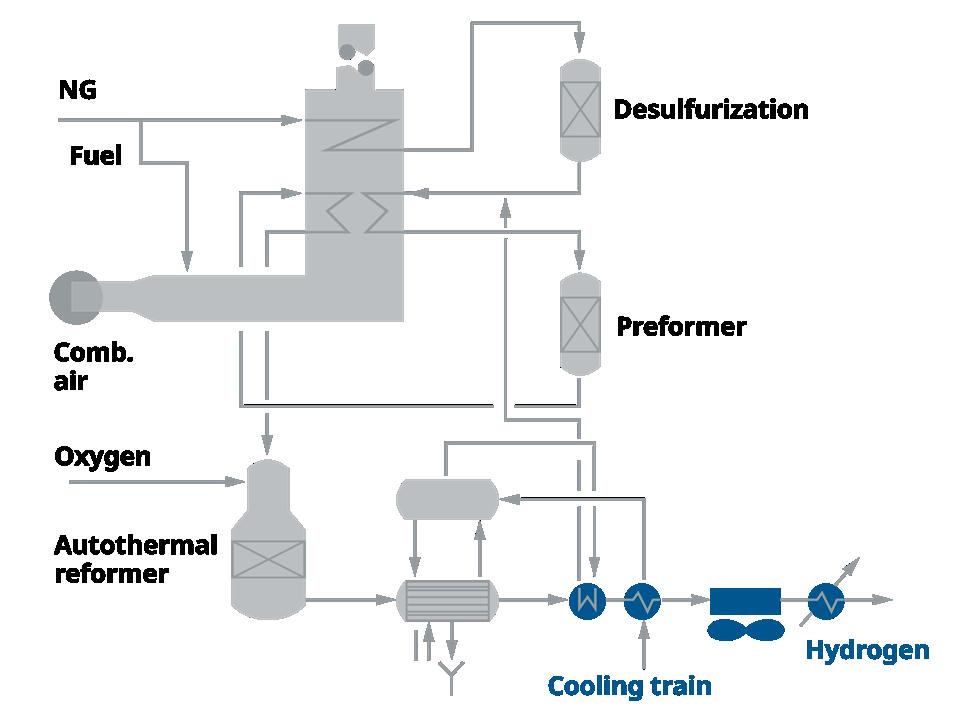

low-carbon hydrogen from natural gas plays a significant role in optimising hydrogen production from methane while capturing the maximum amount of carbon dioxide. This approach utilises proven components already deployed in the global methanol market and ensures the lowest costs from both a CAPEX and OPEX perspective, giving the project the best chance for a competitive levelised cost of hydrogen and overall success.

The industry still needs initial support through subsidies and a regulatory framework that allows it to compete fairly with polluting alternatives. Taxing high-carbon fuels is also necessary to create a level playing field for hydrogen. Geography will significantly influence each region’s choice and technology requirements. Over the next few decades, low-carbon blue hydrogen and green hydrogen will be competing head-to-head to decarbonise the world. That they go quickly is much more important than which technology is in front at any particular time. Currently, natural gas prices set the cost of electricity in countries like the UK. Green hydrogen might set the gas price in the future, flipping the current situation.

Regional opportunities

Electrolysers can run at maximum capacity in regions with consistent wind and solar energy, making these the cheapest places to produce green hydrogen. Regions like Australia have ideal conditions for producing green hydrogen, ammonia, and methanol, while the UK and Norway have excellent geology for carbon dioxide sequestration and natural gas resources, making them prime locations for low-carbon blue hydrogen production. In the North Sea region, this creates a certain circularity. This was the cradle of enormous fossil fuel sources and due to its geological advantages, it can foster both a low-carbon blue hydrogen ecosystem and a green hydrogen ecosystem. This synergy is promising for the future of hydrogen production.

Conclusion

Despite the opportunities, challenges remain for the hydrogen economy. The biggest factor that will slow down its uptake is the lack of policies incentivising and supporting hydrogen use and demand. Many potential projects worldwide are stalling at the FID stage due to the absence of secure offtake agreements. These projects aim to limit spot market exposure because a proper hydrogen commodity market does not yet exist. To feel secure, they need over 90% offtake agreements. While there is strong ambition to produce hydrogen, there is not yet matching demand or large-scale counterparty agreements to support it. Establishing a viable hydrogen economy necessitates overcoming substantial technological, policy, and infrastructure hurdles. With concerted efforts from industry leaders, governments, and stakeholders, the hydrogen economy holds significant potential to drive the global energy transition towards a more sustainable future.

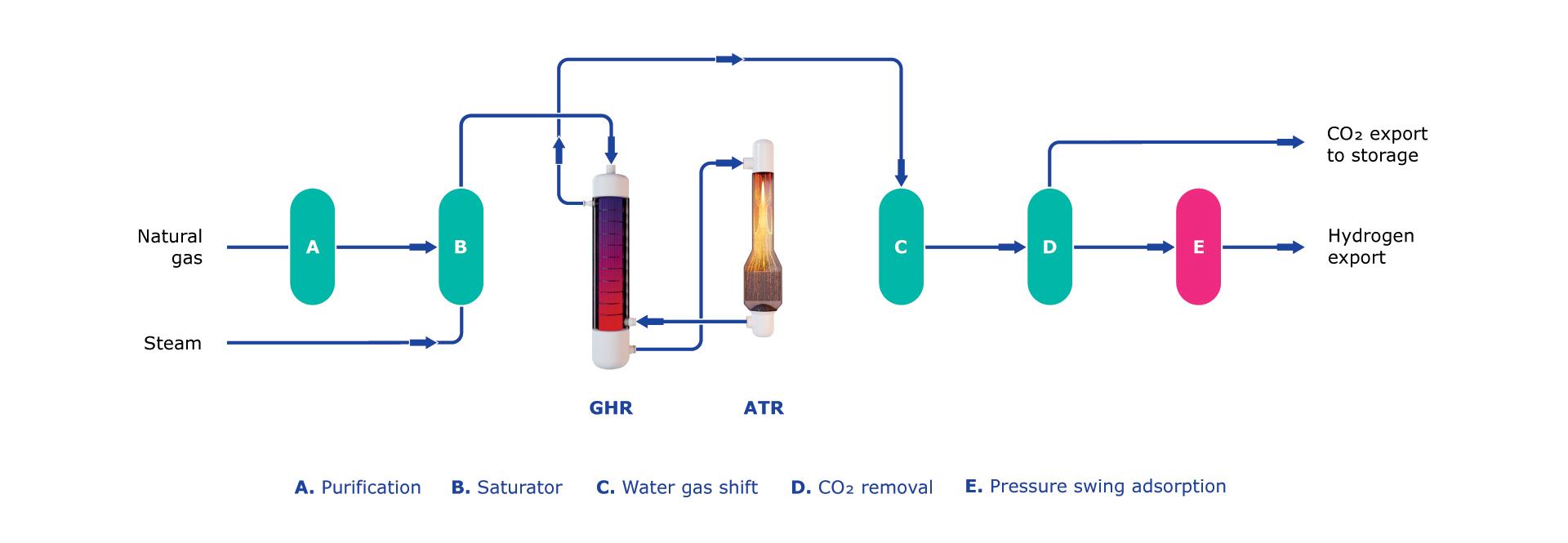

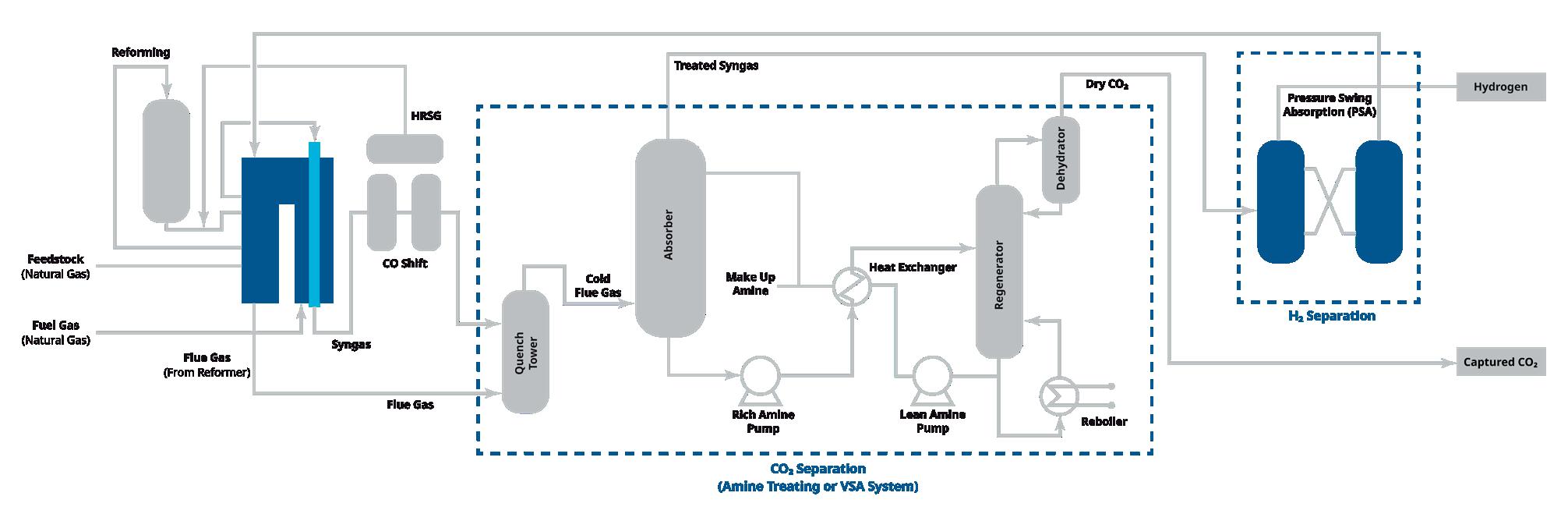

Figure 1. Process for low-carbon hydrogen production.

Figure 2. Global hydrogen supply overview.

Hydrogen developers can use digital twins to improve the economic viability of renewable projects and meet increasing demand. Nas Andriopoulos, Dominik Don, Joaquin Ubogui, and Maurits Waardenburg, McKinsey & Co., illustrate how, using renewable hydrogen as an example.

As the world accelerates its decarbonisation plans, renewable hydrogen and its derivatives offer a promising alternative to fossil fuels – but to date, there are still no gigascale renewable hydrogen production plants in operation.

The demand for clean hydrogen is expected to increase significantly. New plants could be scaled to meet this growing demand, which could require investments of US$700 billion to maintain the 2030 net zero trajectory.

Currently, hydrogen demand is driven largely by the fertilizer and refining industries. The majority of hydrogen produced is grey hydrogen and, to a lesser degree, blue. To support net zero ambitions, developers and investors could use a trusted technical and financial blueprint that quantifies risk and may accelerate the scale-up of green hydrogen plants. Digital twins – which can simulate a physical plant from the planning stage before it is built to the end of its lifetime – could help reduce the risks of investment, save costs, and speed up project timelines.

This article highlights the obstacles preventing the build-out of large-scale renewable hydrogen production plants and explores how developers could overcome – or at least help to address –these challenges by using digital twins.

Challenges facing renewable hydrogen production today

Renewable hydrogen is still an emerging industry, facing short-term headwinds to realise its long-term potential. Costly infrastructure and the necessary hydrogen storage – as well as the variable nature of renewable energy sources themselves –also put pressure on plant economics. Developers struggle to confirm final grant and investment approvals, across Europe and other regions.

Uncertainties surrounding the technology, interest rates, regulatory schema, offtake market, and electrolyser availability all act as hurdles to achieving large-scale production:

� Electrolysers are a core component of any renewable hydrogen project. Recently, the CAPEX required for electrolysers increased by around 70%, driven by financing costs, labour, and materials. Variations in availability, price, and performance across a suite of options increase the complexity of project planning.

� While there are lower-cost options available for electrolysers, cheaper does not always mean better. For example, some of the first large plants in operation are now underperforming

on their minimum loads. This means that if the power output falls below 50%, these plants have to turn off the electrolysers and remove them for maintenance to solve the problem. In the future, this may change, but developers face tough choices. They need to consider the trade-off between CAPEX and performance, as well as the size and sequencing of electrolysers used in the plant.

y Investors require a high level of confidence to reach a Final Investment Decision (FID) due to the risks associated with megascale projects. Developers stand to benefit if they can secure offtake early on in the process. Once there is guaranteed offtake – ideally a minimum of 50 - 70% of production – it becomes easier to secure finance and increase investors’ confidence. However, in an environment of increased interest rates, securing a sufficiently low cost of debt to enable attractive equity internal rate of returns (IRRs) has become more difficult. This has led to some developers seeking less debt and requiring a greater share of equity – which typically increases upfront equity commitment costs by 10 - 25%.

y While recent legislations create a favourable environment for boosting renewable hydrogen demand, understanding multiple regulatory frameworks can be challenging for developers. Definitions and requirements for production – for instance, regarding carbon intensity and where production facilities can be located, and how they match output and electricity consumption – differ across regions, which compels hydrogen producers to consider a wide range of designs and operational plans to have a compliant product for multiple markets. Legislation to boost clean hydrogen production includes the 2021 US Bipartisan Infrastructure Law and the US Inflation Reduction Act of 2022 (IRA), both of which could require closer integration between renewable energy sources and the plant. Meanwhile, the EU’s Renewable Energy Directive (RED III) mandates renewable fuel of non-biological origin (RFNBO) compliant hydrogen, which introduces its own set of requirements on additionality of renewable energy and matching of renewable energy used and hydrogen production.

For megaprojects to get the green light for development, projects could be designed to ensure the lowest possible production costs over the lifetime of the plant, within some of the constraints described above. A digital twin can help to achieve this as it can evaluate hundreds or thousands of options and combinations of components to optimise plant design and increase investor confidence. The bulk of lifetime plant operating costs are locked in during design, and a digital twin supports decision making early on in the process before the plant is built.

How digital twins unlock value

Despite the challenges, hydrogen megaproject momentum is building as early movers transition to pre-FID design and engineering. Global developers are now looking for ways to solidify their business cases – and digital twins can play a significant role in this regard.

Reducing production costs

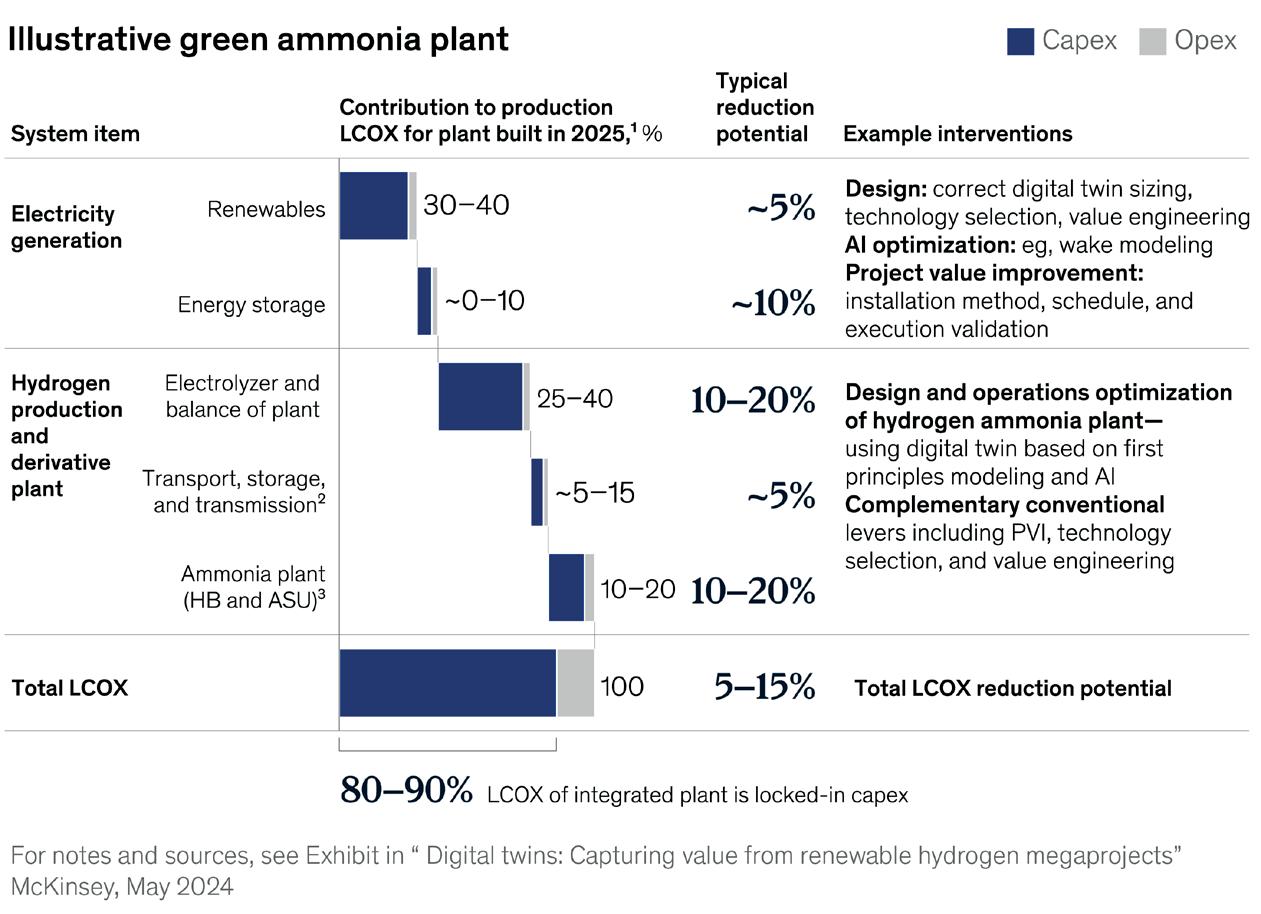

Leveraging probabilistic advanced analytics (AA) and generative-AI (gen AI) techniques, digital twins can help clarify project viability by quantifying the impact of external factors on the economic performance of a potential project design over its operating lifespan. By fully embracing digital twins, production costs (LCOx) could be reduced by 5 - 15% (Figure 1).

Some developers are already reining in production costs by using a digital twin to quantify risks and ensure that investments have the highest probability of delivering desired returns. For example, one global energy company with a series of megaprojects for renewable hydrogen and ammonia was able to identify US$500 million of NPV improvement potential (see sidebar ‘Case study: How a global energy company optimised the design of its renewable ammonia plant’).

Optimising plant design

The power of a digital twin lies in its ability to quickly evaluate plant complexities, identify optimised setups, and compare alternatives against a set of constraints (for example, regulatory requirements for green hydrogen). It can investigate all possible alternate design strategies, such as different storage sizes, multiple electrolysers and their yields, and balance of plant (BoP) setups, and can explore a broader solution space by using AI optimisation for process modelling. For instance, digital twins can simulate and compare the performance of multiple types of electrolysers under different conditions, which will increase the confidence in the planned design of the plant. For some projects, it might be beneficial to ‘oversize’ the electrolyser capacity while others may require more flexibility to balance electrolyser capacity with storage capacity.

Digital twins can improve design where traditional approaches often fall short and can help to solve complex trade-offs inherent in e-plant design and engineering,

Figure 1. Production costs can be reduced by an estimated 5 - 15% through digital twins and supporting interventions.

HIGH PRESSURE H₂ COMPRESSION TECHNOLOGY

Advanced Plug-&-Play Containerized Hydrogen Compression Solutions of up to 1,000 bar / 14,500 psi for sustainable and decarbonized mobility & industry storage

Reciprocating piston compression technlogy of up to 500 - 1,000 bar

Safe and reliable solution thanks to the venting system

Oil Free design compressors, with a complete turndown: 0% to 100%

Efficient cooling thanks to piston compressor innovative design

Some of our Hydrogen Customers

such as power firmness, load factor, or subcomponent selection. Some examples are provided in the following section.

Power firmness

Digital twins can help to solve complex trade-offs in power firmness by comparing the lowest-cost intermittent power sources with the need for energy storage or grid firming. This can achieve the balance of high-firmed output with an increased levelised cost of electricity (LCOE).

Load factor

Digital twins can help developers understand the electrolyser stack degradation impact on the levelised cost of hydrogen (LCOH) while defining an operative strategy. This includes defining the load factor of the different modules or arrays of the electrolysis plant. This can then be fed directly into the operating facility and planned maintenance strategy.

Process design integration

When operating a large-scale industrial process (such as direct reduction of iron, Fischer-Tropsch, Haber-Bosch, or Sabatier), high uptime and continuous process operation are critical for reactor stability and efficiency. However, renewables are inherently intermittent. Designing the end-to-end, power-to-molecules system that balances CAPEX on renewable energy sources, buffer stores, and reactor uptime is the largest driver of LCOx of the plant. Digital twins can rapidly assess and optimise the potential sizing of all elements of the system, even factoring in probabilistic elements, such as weather patterns, equipment failure, and evacuation schedules.

Sub-component selection

BoP selection is a major driver of system CAPEX and OPEX. Digital twins can help developers choose between equipment and component options. For example, modelling can show whether it is better for plant economics to pursue fewer, larger components (such as compressors or pumps) with concentrated failure points, or to install many modules of smaller components and embed additional redundancy in the process.

Product storage size

Hydrogen storage is expensive and different options can be explored. For example, a developer can invest in a smaller hydrogen or ammonia storage capacity with a great risk of stoppage, or they could choose a larger storage buffer and bear the related cost. This can be modelled to integrate with offtake schedules and contractual negotiations.

Maximising the value of a digital twin

Digital twins can deliver benefits far beyond initial design and development too. When properly set up during plant design, digital twins can form the basis of a variety of use cases throughout the plant’s life cycle.

Operations

Plant design and operations are initially considered and optimised together with a digital twin, providing greater clarity of the operation and maintenance needs of the plant to enhance planning. This technology can also provide greater cost certainty on the plant’s OPEX in advance.

Case study: how a global energy company optimised the design of its renewable ammonia plant

A global energy company with a series of megaprojects producing renewable hydrogen and ammonia faced challenges with project cost and establishing a repeatable development process across its projects. Its existing modelling approach had shortcomings in auditability and transferability between projects. The company was able to optimise its design using digital twin technology. The process included evaluating the existing design, validating key design components, and developing a probabilistic operating twin to suggest improvements. Alternative cases were analysed to optimise project design. Employees were core to developing the model and were trained on how to get the most use out of the digital twin, including how they could adapt and improve the twin after the initial study.

A US$500 million NPV improvement potential was identified, and risks were quantified and better understood. Furthermore, the number of employees who were able to use digital twin technology tripled, increasing transparency, usability, and auditability with one source of truth.

Financing and investment

Having a reliable and proven digital twin could make financing and investors’ decisions less risky, creating a better position to enhance financing rates and negotiate offtake contracts.

Serial project delivery

Having an established digital twin and embedded capability can allow faster, lower-cost development of all future projects, and enable developers to quickly test whether project concepts are viable. For example, when prioritising two projects, they can rapidly be virtually modelled and assessed. Developers can reuse their concepts for all future projects and can decide from very early on in the process which projects to drive forward and which ones to stop immediately.

Finance and management

A curated and customisable dashboard can be created to provide easy-to-access insights for a range of senior stakeholders, supporting negotiation and project stage gate reviews, as well as regular reporting once in operation.

Auditing

Digital twins can even be used as a basis for internal and external auditing, for example, by contrasting the real events on a plant’s unexpected cold stop with the model responses. They can also provide solid, future-looking economics for further operational choices.

Conclusion

Renewable hydrogen is a much-needed resource for helping the world achieve its decarbonisation goals. With the move toward hydrogen megaprojects, it is critical to make sure that plants are designed in the most economical fashion to help secure investments and reach FID. Digital twin technology can not only help to reduce initial CAPEX costs but also drive efficiency over the lifetime of the plant.

Ben Laws and Nicolai Szeliga, Siemens Digital Industries, explore how Digital Twins and the process optimisation capabilities that they bring are becoming essential components of green hydrogen projects.

The global energy landscape is transforming to mitigate climate change, with the International Energy Agency projecting that annual clean energy investment must triple to US$4.5 trillion by 2030 to reach net zero emissions by 2050.1 This shift to renewable energy sources like solar and wind faces challenges such as supply intermittency, grid instability, and the need for long duration energy storage.

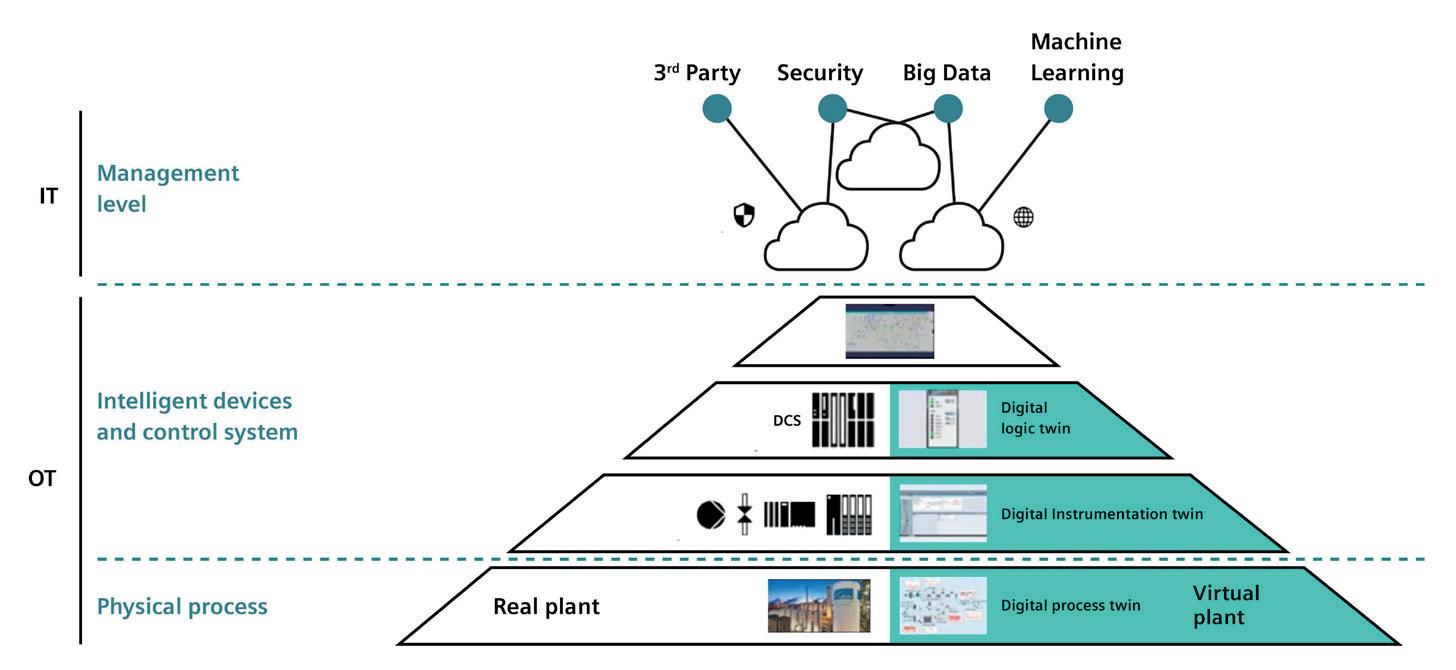

The Digital Twin: optimising plant operations

A Digital Twin (DT) is defined by the Digital Twin Consortium as an integrated data-driven virtual representation of real-world entities or processes.6 In the process industry, DTs typically contain three components: the Plant Twin, Process Twin, and Automation Twin. Each element delivers distinct capabilities to different project teams and across the project lifecycle. When combined, they form an Integrated Digital Twin of an asset.

Green hydrogen offers a solution by serving as a renewable energy vector, providing long-term storage and enabling sector coupling. Power-to-X (PtX) processes, which use green hydrogen to synthesise feedstocks such as ammonia or methanol, are key to decarbonising hard-to-abate sectors from shipping to fertilizer production.2 However, large-scale use of green hydrogen and PtX faces technical and economic hurdles. Advanced digital technologies can help to overcome these challenges and accelerate adoption.

Green hydrogen: a major opportunity for decarbonisation

Green hydrogen, produced via water electrolysis using renewable electricity, is the most sustainable form of hydrogen, offering CO2-free emissions and relying solely on sustainable inputs. The electrolysis process is more efficient than traditional steam methane reformation (SMR) and can more easily adjust production rates to match demand and supply fluctuations. However, production and distribution of green hydrogen is complex and dynamic, with significant uncertainty arising from the inherent intermittency – and often higher cost – of renewables. Producers must also contend with changing demand profiles, evolving regulations, and a lack of industry-wide economies of scale. To run a production process efficiently, operators are tasked with deciding when and how to produce hydrogen to balance multiple, often competing objectives related to output, efficiency, equipment degradation, and sustainability. Decisions include how to run electrolyser clusters, what electricity source to use, and whether to store or export produced hydrogen – all of which can be constrained by operational or environmental parameters. Critically, decisions must be made and re-made continuously to adapt to constantly changing circumstances. When combined with the limited operational experience in the industry, this proves a formidable challenge for project owners. The impact is that green hydrogen is often significantly more expensive to produce than grey hydrogen.3

While global demand for clean hydrogen is projected to lie between 125 and 585 million tpy by 20504, forecasted supply lags far behind under most scenarios. To address this supply gap, project developers must bring production costs down, improving the economic viability of their assets and reducing reliance on support schemes like the UK’s Low Carbon Hydrogen Agreement.5 Digital Twins can help project owners achieve these goals.

For operating dynamic process plants, the Process Twin is particularly vital and is this article’s focus. When calibrated, Process Twins combine real-time plant data with mechanistic models to provide a predictive simulation of plant behaviour. Simulation enables continuous performance monitoring and analysis, and powers true mathematical optimisation of the process. A Process Twin typically incorporates:

y High-fidelity models: based on first-principles physics, thermodynamics, and electrochemistry, these models accurately represent the core process units and associated systems, including non-linearities and dynamics.

y Real-time data integration: live data streams from plant sensors and control systems ensure the virtual model reflects the current plant state.

y Advanced analytics: solvers and optimisation algorithms incorporate historical and real-time data to identify patterns, estimate the system’s state, and optimise operational parameters.

y Visualisation tools: intuitive interfaces allow operators to make informed decisions.

y Scenario simulation: operators can test strategies and optimise processes virtually without risking the physical plant.

By integrating each of these elements, Process Twins can empower project teams whether they are in the control room or situated remotely.

To address operational challenges in a plant, DTs must be deployed in an online environment. Deployment ensures the DT can access live information and communicate with the plant’s automation hierarchy in near real-time. Online implementation involves several steps, many of which can in fact be initiated during a project’s design phase. A full lifecycle approach to building the DT means its capabilities can be used for performance validation, scenario analysis, operator training, and other vital tasks even before plant commissioning.

The implementation process typically includes:

y Design specification and data collection.

y Model development (physics-based and data-driven).

y Digital infrastructure setup and deployment.

y User interface and visualisation creation.

y Integration and testing.

When deployed, a DT sits above the traditional automation hierarchy (Figure 1) in the IT layer, interfacing with various plant

Figure 1. The digital hydrogen plant.

COMMITTED TO A BETTER FUTURE

Optimizing combustion for a greener tomorrow WE’RE

There has never been a greater need to decarbonize fired equipment, produce cleaner energy sources, and operate in a more environmentally responsible way.

Optimized combustion and enhanced predictive analytics are key to reducing plant emissions and ensuring equipment uptime. Designed for safety systems, our Thermox® WDG-V combustion analyzer leads the way, monitoring and controlling combustion with unparalleled precision.

Setting the industry standard for more than 50 years, AMETEK process analyzers are a solution you can rely on. Let’s decarbonize tomorrow together by ensuring tighter emission control, efficient operations, and enhanced process safety for a greener future.

systems in the OT layer for data exchange and control. DTs can be used in either an open loop advisory mode or a closed loop implementation mode. While conventionally digital applications have been deployed in open loop mode to advise operators, development of autonomous operations in the process industry is an area of rapid evolution and increasing priority. Integrated DTs are increasingly seen as offering a reliable foundation to project owners pursuing fully autonomous and remote operations.

A Digital Twin for green hydrogen plants

Green hydrogen plants, with their inherent operational complexity, are ideal candidates for DT technology. In this application, a high-fidelity process model describes key system units, from energy input to hydrogen production, purification, compression, storage, and export. The DT application seamlessly integrates real-time plant data from critical units and flows, as well as external data such as energy supplies, tariffs, and demand profiles.

Operators interact with the online DT through dashboards that provide performance monitoring to different stakeholders located anywhere in the world. Advanced state estimation algorithms provide ‘soft-sensing’ capabilities, while rigorous production optimisation features allow for dynamic production scheduling to meet hydrogen demand efficiently.

Combining a physics-based model with live data streams improves plant behaviour simulation, aiding operators in confident decision-making. Crucially, the model adapts to short-term dynamics (e.g. weather changes) and long-term trends (e.g. equipment degradation), ensuring it remains ‘evergreen’. Its modular framework and industry-standard connectors allow easy expansion for additional data-driven capabilities, further enhancing operations and asset maintenance with features like anomaly detection, maintenance scheduling, and fleet monitoring.

DTs are becoming essential components of projects targeting a successful Final Investment Decision (FID), as they provide confidence to operators, project owners, and investors alike –especially when considering what are often highly innovative designs.

Digital Twins in action

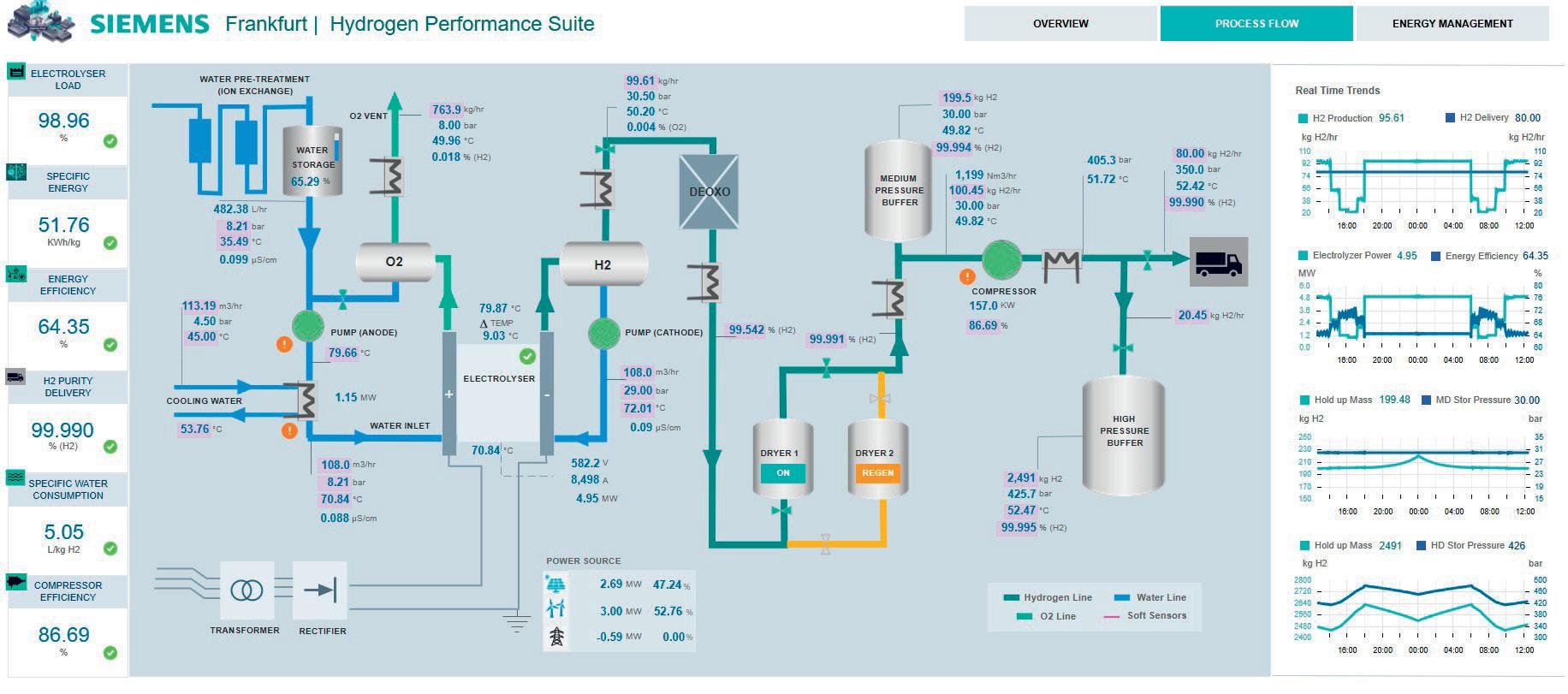

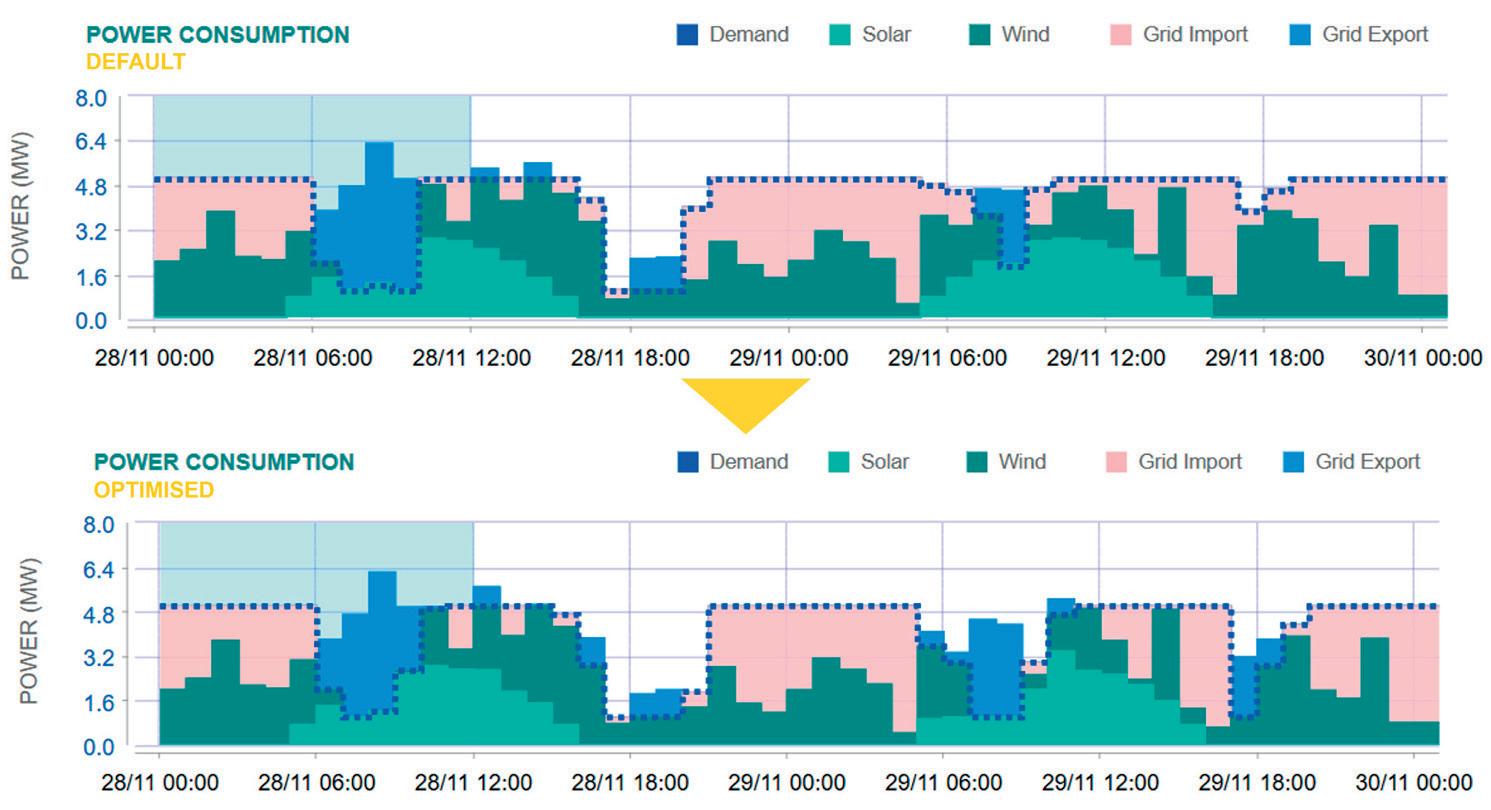

Consider a simplified demonstrator project with 5 MW proton exchange membrane (PEM) electrolyser capacity. This demonstrator uses wind, solar, and grid power to produce green hydrogen at a nominal rate of 80 kg/hr. The following case study represents capabilities that can be delivered by the Hydrogen Performance Suite, an an operational DT designed specifically for green hydrogen and PtX plants.

Dynamic real-time optimisation

Production optimisation is a task that operators face daily or even hourly. This involves scheduling the times to produce and store hydrogen – and deciding how to operate the process – to meet off-taker requirements while minimising levelised cost of production. Operators need the ability to prepare optimal production plans as well as the ability to re-optimise at short notice should the production environment change (e.g. through a sudden drop in demand or change in renewable energy supply).

Figure 2 presents a dashboard from the Hydrogen Performance Suite, including production management information and relevant data streams. An hour-by-hour production schedule is provided for an upcoming 48-hour period, while the time profiles summarise renewable data, grid tariffs, and the hydrogen demand. In this baseline, hydrogen demand is a constant 80 kg/hr. The dashboard also delivers live

Figure 2. Hydrogen Performance Suite, process management dashboard.

Figure 3. Hydrogen Performance Suite, production optimisation dashboard.

chartindustries.com howden.com

power monitoring across the asset for easy assessment of energy usage.

In Figure 3, a second day is represented, with different weather forecasts and a decrease in hydrogen demand for several hours. Under the baseline production schedule, 22.4 MWh grid power supply is needed to meet this demand profile. Figure 4 presents the same scenario with an optimised production plan. Hour-by-hour dynamic optimisation of electrolyser load, storage capacity, and production rate is used to minimise the use of grid energy, thereby reducing production costs and ensuring more certifiable green hydrogen is produced.

In this case, the optimiser suggests production of hydrogen at times when either renewable energy is plentiful or when the grid tariff is low. In some hours, sale of excess renewable energy to the grid is recommended to offset costs. Storage capacity is also used proactively: the stored quantity is adjusted to buffer differences between hydrogen production and demand.

Following dynamic optimisation, the total grid usage in the plan is 14.4 MWh, a 36% decrease. Realisable financial savings in this demonstrator were over 10%, indicating the significant economic potential of optimised production. Operators – or the application itself in a closed loop deployment – can implement production plans that maximise asset performance, while continuous data input and model simulation ensures every re-optimisation reflects the latest plant state.

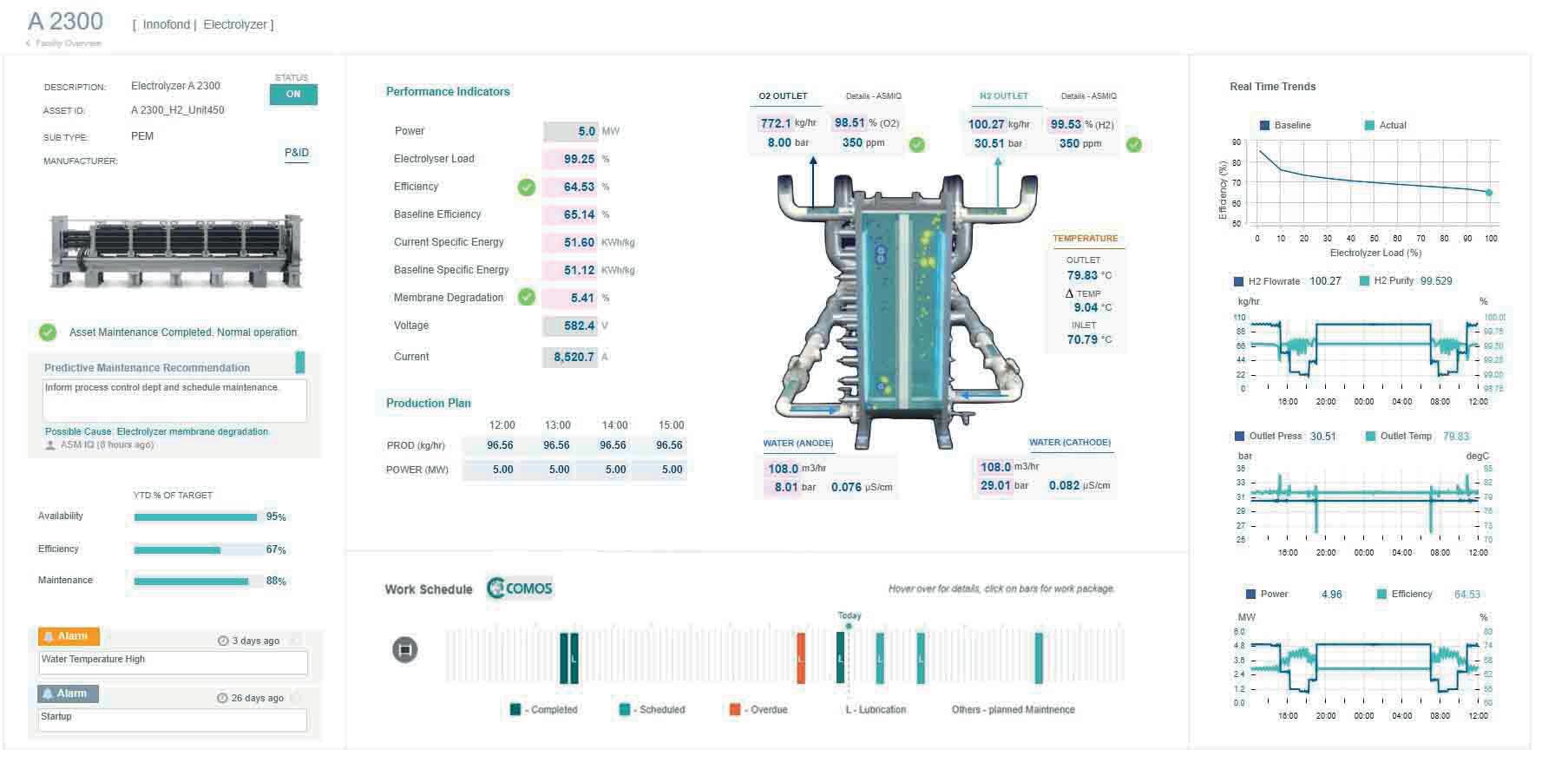

Soft-sensing electrolyser performance

Effective dynamic real-time optimisation is only possible when an optimiser can obtain an accurate reflection of the plant state in real-time. Without this, production schedules may be based on incorrect or outdated unit efficiencies or system behaviour, limiting their utility. Equally, operators must understand the performance of critical units like electrolyser stacks to determine production cost, calculate energy usage, and plan maintenance efficiently.

While these needs may be partially addressed through sensor placement, some data cannot be measured physically due to design limitations or a lack of suitable sensors. In this scenario, soft-sensing plays a vital role. Soft-sensing is the continual calculation of key process variables using the calibrated process

model with advanced state estimation algorithms. This enables live assessment of streams or units without the need for installed sensors – or provides cost-effective redundancy for safety-critical values that are being measured.

Figure 5 highlights an electrolyser monitoring page including soft-sensed variables such as efficiency, flow rates, and stream conditions. One graph compares soft-sensed efficiency to the performance information provided by the vendor. During long-term operation, efficiency may deviate from vendor-supplied expectations. With the soft-sensor installed, operators can pinpoint any deviation from the nominal performance and respond accordingly. The updated calculated values are subsequently used in the production optimisation to avoid reliance on incorrect data. Degradation models – either empirical or mechanistic – can also be incorporated and periodically re-calibrated to assess long-term performance decay.

The installation of soft-sensors leads to both superior process optimisation and a reduced need for redundant instrumentation throughout the asset. Collectively, these benefits result in significant cost savings in addition to the gains from optimised production scheduling.

Building holistic Digital Twins

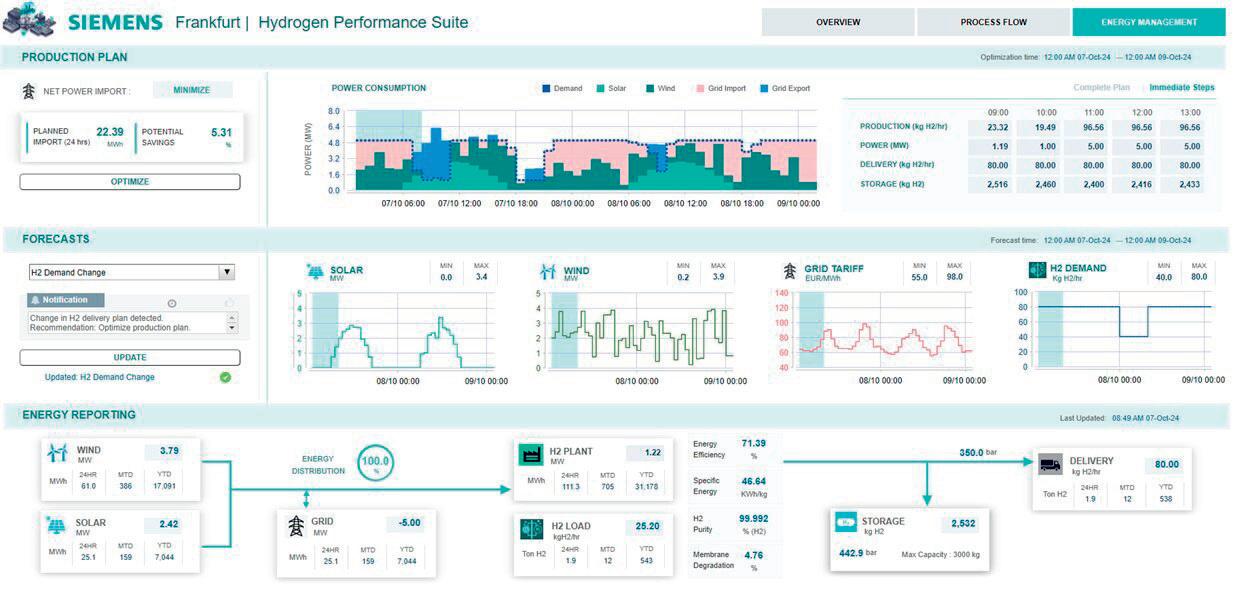

Whilst dynamic process optimisation is a key route to reducing hydrogen production costs, other opportunities exist. A significant parallel challenge is the effective management of the power ecosystem. Integrating an energy management solution (EMS) – which may handle power distribution, demand response, and trading decisions – with process optimisation can unlock further performance enhancements and cost reductions while providing a more seamless workflow for operators. For PtX plants in particular, this synergy, facilitated by open data exchange, is crucial for achieving true optimality across both process and power systems. The modularity and flexible data connectors of the previously described DT enable easy EMS integration.

The industry now targets ‘holistic Digital Twins’, which unify EMS, online Process Twins, and predictive data-driven features within a single interface and application. These comprehensive tools promise to deliver superior performance improvements in a streamlined and cost-effective manner, and will represent an evolution in digital plant management.

Outlook: plants of the future

Green hydrogen has immense decarbonisation potential, but this will not be realised unless the gap between demand and supply narrows. The vital reductions in production costs are achievable through rigorous process optimisation. Online DTs, combining physics-based simulation with real-time data, offer powerful monitoring, analysis, and optimisation directly to operators. Continuous simulation can ensure plants operate near

Figure 4. Comparison between default and optimised hydrogen production profiles.

optimal levels despite uncertainties, as shown in the Hydrogen Performance Suite case study.

DTs will continue to integrate an increasing array of capabilities, from power optimisation to predictive analytics and multi-asset remote management. These solutions are now deemed a necessary component of all major projects; owners and developers must leverage virtual replicas to navigate uncertainty, address critical production challenges, and increase the impact of their technology.

References

3. https://observatory.clean-hydrogen.europa.eu/index.php/ hydrogen-landscape/production-trade-and-cost/cost-hydrogenproduction#:~:text=Hydrogen%20production%20costs%20 via%20electrolysis,median%20of%206.20%20EUR%2Fkg.

4. https://www.mckinsey.com/industries/oil-and-gas/our-insights/ global-energy-perspective-2023-hydrogen-outlook

1. IEA Net Zero Roadmap, 2023 update, https://iea.blob.core. windows.net/assets/4d93d947-c78a-47a9-b223-603e6c3fc7d8/ NetZeroRoadmap_AGlobalPathwaytoKeepthe1.5CGoalinReach2023Update.pdf

2. World Economic Forum, November 2023, https://www.weforum.org/ agenda/2023/11/power-to-x-a-key-component-in-the-global-energytransition/

5. https://www.spglobal.com/commodityinsights/en/ market-insights/latest-news/natural-gas/081023-uksets-out-support-mechanism-for-low-carbon-hydrogenproduction#:~:text=Strike%20price%20and%20floor,gas%20 price%20setting%20a%20floor

6. https://www.digitaltwinconsortium.org/initiatives/thedefinition-of-a-digital-twin/

Figure 5. Hydrogen Performance Suite, electrolyser performance monitoring dashboard.

Antoine

and

Ghorayeb, Ali

Natour,

Yann-Olivier Placiard-Fleys,

Saipem SA, present a case study for the implementation of large-scale ammonia (NH3) storage and cracking on board of a unique concrete hull by means of a gravity-based structure (GBS).

The global demand for alternative clean fuels is gaining momentum at a constantly accelerating pace due to the pressing decarbonisation targets set at international and national levels for a multitude of industries. Low-carbon footprint, high volumetric energy density, safe storage, and easy transportation are the leading criteria for new potential commodities. In this race, one of the newly rising energy vectors that satisfies the enforced terms is ammonia (NH3), chiefly the clean ‘green’ and ‘blue’ NH3 for hydrogen (H2) applications, power generation, and propulsion.

Ammonia as a hydrogen carrier

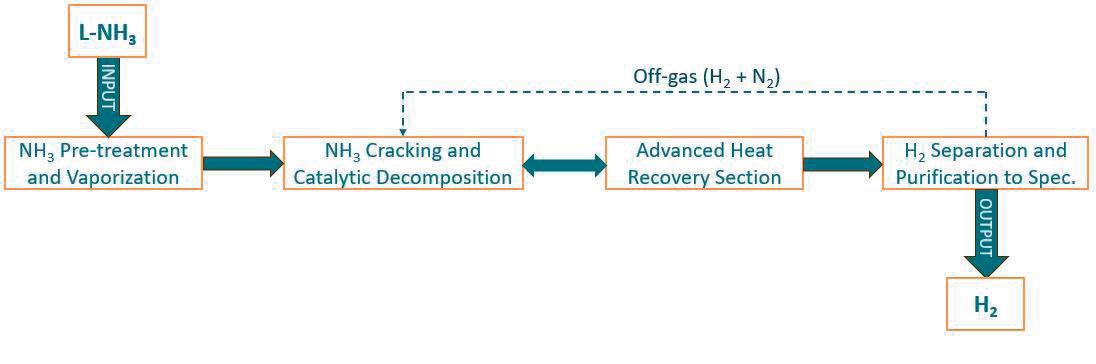

When observing NH3 as a hydrogen carrier that combines high hydrogen density in its molecule, hydrogen has been well demonstrated as a fuel in combustion engines, gas turbines, and fuel cells, that can be converted efficiently into heat and electricity. But compared to liquid hydrogen (LH2), the refrigerated storage of liquid ammonia (LNH3) is a more feasible practice due to its larger volumetric energy density (approximately 13MJ/l for NH3 vs 8.5MJ/l for H2) and its reasonable liquefaction temperature at atmospheric pressure (-33°C for NH3 vs -253°C for H2). In comparison, the storage of LH2 requires at least five times more volume when compared to most petroleum-based liquified gases, while LNH3 requires approximately 2.4 times more volume. Therefore, the volume of LNH3 storage tanks is significantly less than storage tanks for LH2 at a similar energy requirement, even more upon counting the thermal insulation scheme of tanks. NH3 has been industrially produced for more than five decades with an extensively-established infrastructure and offtake, as well as known regulations and norms for handling and storage. A vital process to unlock this energy-dense and low-carbon hydrogen carrier lies in NH3 cracking for H2 production purposes.

Ammonia cracking process

Ammonia cracking involves a central process that reconverts NH3 into H2 at scale. The heart of this technology is the NH3 cracker, which is a catalytic cracking furnace in

which the NH3 synthesis is reversed at elevated temperatures and in the presence of a high-performance catalyst by means of the following endothermic chemical reaction:

2NH3 + (heat and catalyst) N2 + 3H2

The cracking process scheme comprises several steps (Figure 1). First, LNH3 is fed from the tank for its pre-treatment and vaporisation, and then it is cracked at approximately 800°C in the furnace unit. After the efficient integration of the heat recovery section, the purified H2 can be obtained in compliance with the predefined customer’s specifications after being processed through the pressure swing adsorption (PSA) purification unit to separate the nitrogen gas (N2) and other residual by-products. The PSA off-gas containing all the remaining H2 and N2 residues can be used as fuel to fire back the NH3 cracker, therefore maximising the overall efficiency of this process.

Presently, some distinguished licensors for NH3 cracking technology are Casale, Topsoe, KBR, Air Liquide, Duiker, Thyssenkrupp and H2SITE.

LNH3 storage: why is it special?

Anhydrous NH3 is stored in its liquid state, being either under convenient pressure at atmospheric temperature, or fully refrigerated at atmospheric pressure near its boiling point of approximately -33°C. Industrial-scale LNH3 is typically stored in a fully-refrigerated state as this scenario costs less than that of pressurisation. Onshore LNH3 tanks of capacities up to 80 000 m³ (55 000 t) are not uncommon.

The toxicity of the gas, the ability of liquid NH3 to conduct electricity, and the susceptibility of steel in direct contact with

either the gaseous or liquid phases of NH3 to stress corrosion cracking (SCC), render LNH3 storage as specific. The toxic nature of NH3 and its severe health hazards has always called for certain measures to be taken within the design and operation of bulk LNH3 facilities.

The phenomenon of SCC specific to NH3 service can be defined as an anodic degradation process that occurs when susceptible material under tensile stress is exposed to conditions leading to successive localised breakdowns of the corrosion product film formed at its surface. It has been the major preoccupation for designers and operators of LNH3 tanks in the industry, which imposes designers to set efficient preventive measures to avoid SCC and propose advanced types of crack monitoring system for NH3 primary containers. This engages the operators to have special respects for the internal inspection intervals and maintenance scheme of such storage tanks.

Resistant materials to ammonia’s SCC

Based on an interpretation of the IGC code, the principal candidate steels for LNH3 primary containment are low-nickel steels (nickel < 5%), low-temperature carbon steels (LTCSs) (with contents of manganese < 5% and carbon ≤ 0.23%), and austenitic stainless-steels. Besides, high yield strength steels are more prone to SCC than lower yield strength steels, and particularly for LTCSs, upper limits on their yield and tensile strengths are usually specified if the post-weld stress relief heat treatments are not applied.

LNH3 storage inside GBS hull

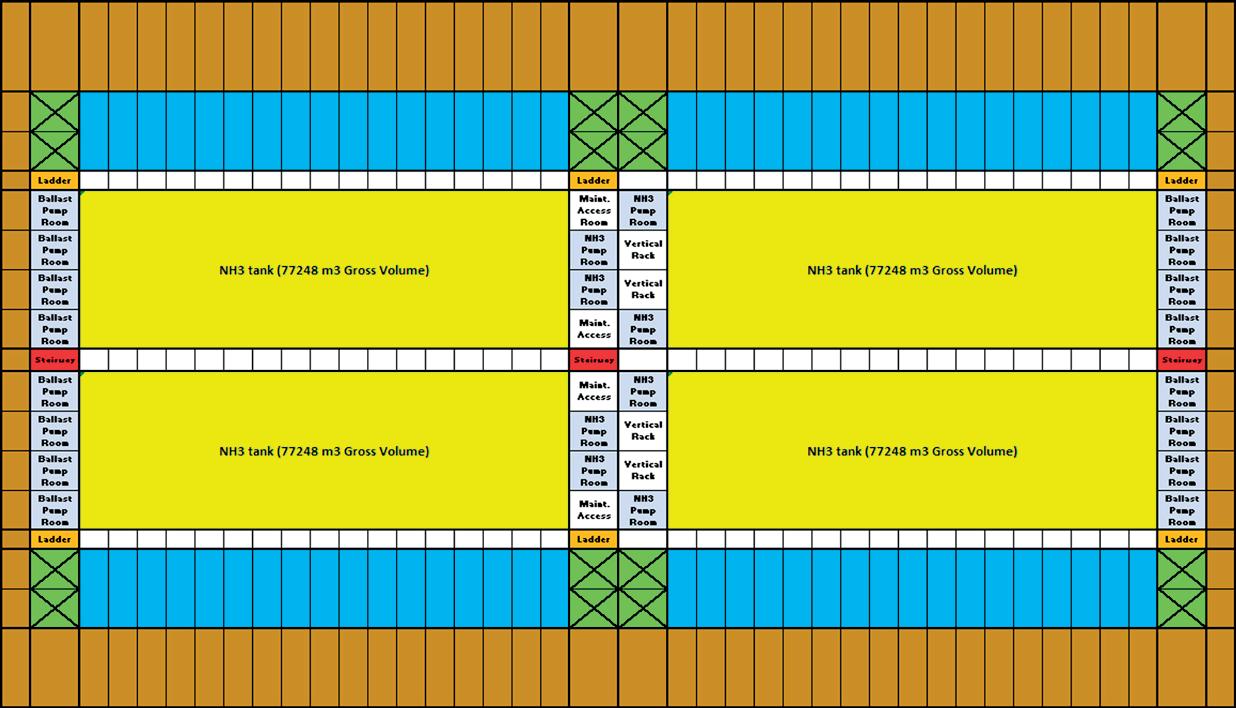

Saipem has conducted a development study to evaluate the business opportunity for a large-scale NH3 storage and cracking facility supported on a GBS. This facility comprises two identical NH3 cracking trains that are pre-sized to produce up to 150 000 Nm³/h of pure H2 product per train , in addition to trains’ associated utilities, technical buildings and rooms, auxiliary equipment, living quarters, unloading platform, and all interconnecting pipe racks that are strictly necessary to complete fully independently operable systems. Furthermore, the GBS is capable to contain inside its hull up to 300 000 m³ of LNH3 to be accommodated within a reliable technology of low-temperature storage tanks. The study was based on a plot plan of NH3 cracking technology provided by a well-recognised licensor, where the footprint envelope of each cracking train measures approximately 110 m x 80 m.

The GBS plot plan configuration adopted for the purpose of this study was fundamentally inspired from the return of experience and lessons-learnt during previous GBS projects that were designed and/or executed by Saipem. The GBS is made of monolithic concrete of 328 m long x 152 m wide at its base slab level. The GBS height was adjusted sufficiently to meet the floatability and in-place stability conditions, as well as to contain the required target gross storage volume of NH3

Figure 1. Typical ammonia cracking scheme.

Figure 2. GBS plan view at slab level of LNH3 tanks (Saipem).

WHEN WE GIVE IT A NEW LIFE

Our goal is to lead the transition towards a net zero economy.

Our FLEXIBLUE® low carbon technologies o er advanced solutions in hydrogen and ammonia, reducing carbon emissions up to 99% while optimizing e ciency.

We are improving sustainable solutions that ensure future generations can meet their needs while respecting the planet, fully believing in research and innovation, integrating technologies, engineering, contracting and construction solutions that reconcile industrial progress with environmental responsibility.

Trust Casale to provide the high-performance, reliable solutions needed to meet your decarbonization goals.

Join us in pioneering a cleaner, more sustainable future.

Figure 2 shows the plan view of the GBS at NH3 tanks level. The yellow rectangles represent the NH3 tanks, the brown areas are the wet-packed sand ballast tanks, and the blue areas are the seawater ballast tanks. The green compartments are reserved for utilities and storage of other products, and the remaining compartments are used for access ladders, stairways, ballast pumps, LNH3 transfer pumps, dry compartments, etc.

For the LNH3 primary containment system inside the GBS hull, a self-supported fully-refrigerated prismatic Type-A tank system was selected. It is a relatively thick-plated metallic tank made of 3.5% nickel steel with all required stiffeners inside. The tank insulation is made from closed-cell poly-urethane foam panels mounted directly on the outside of the tanks shell. The tanks prismatic shape offers wide flexibility for eventual integration into the caissons of GBS, regardless of any geometrical complexities. It also favours the optimisation of the quantities of construction materials. The GBS includes four metallic NH3 tanks of prismatic type satisfying a gross storage capacity of approximately 77 250 m³ each. The guaranteed daily boil-off rate for this configuration would be 0.03% - 0.04% by weight for each tank.

Around 225 000 m³ of concrete is estimated to construct the GBS hull structure. To allocate for sufficient GBS floatability during temporary and towing phases, the use of various concrete types of modified-density and light-weight aggregates should be considered. The overall GBS net dry weight is estimated to be about 690 000 t and the expected under keel draught during towing is projected not to surpass 14 m, closely depending on the prevailing metocean conditions from the GBS construction yard to its selected installation site, as well as on the general arrangement and actualised weights of the topside modules.

Why adopt the GBS concept?

Generally, GBS has demonstrated to be a robust, flexible, and adaptable solution that is suitable for the storage of various refrigerated liquified gases (RLGs), including LNG, LPG, and ethane. GBSs, in different forms, have been successfully deployed in the oil and gas industry for more than 30 years. Whilst its application set records with structures such as the Troll A platform in the late 1990s, the GBS technology is undergoing a strong comeback as the energy industries scramble to decarbonise on one side, and to meet the intensified global demand for LNG in the market on the other side.

Specifically, the GBS concept can allow the entire integration of all topside structures and modules necessary for NH3 cracking processes on a single concrete hull that contains the NH3 storage tanks itself. The performance of construction activities can be maximised in a safely protected and well-controlled

work environment, whether at the GBS construction yard or in the fabrication yards of topside modules, NH3 tanks, and other large mechanical outfitting elements. The GBS can be floated-out, towed, positioned, and sunk at its installation site with the strict minimum on-site works (ballasting, hook-up, commissioning, and ready-for-start-up). Additionally, the GBS design can be reproduced with limited customisation, and GBSs can even be relocated at any instance during their service lifecycle due to their ballast system at a minor maintenance cost.

Recently, to support natural gas pre-treatment and liquefaction, three GBS units (3 x 6.7 million tpy LNG trains) were designed for construction, with a storage capacity of 229 000 m³ of LNG contained inside each GBS. As part of this project, Saipem has carried out extensive FEED works including engineering and constructability studies, that was succeeded by key contribution to EPC phase.

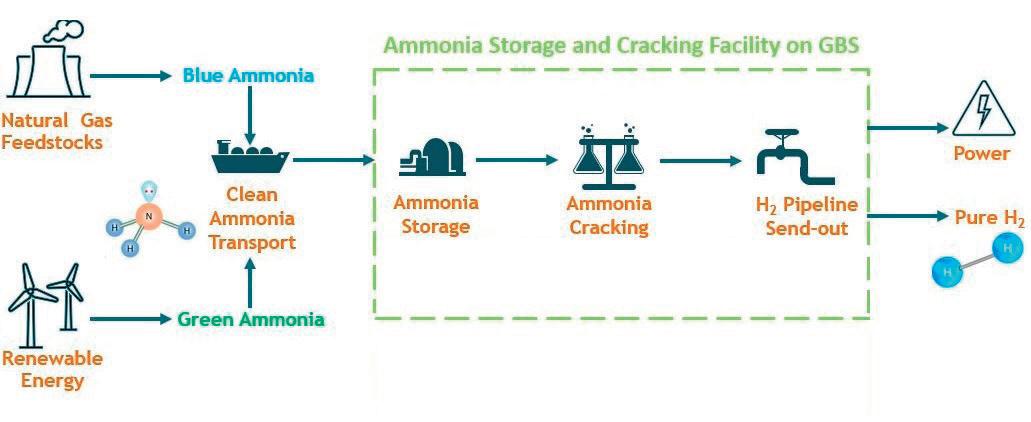

Indeed, amongst all the liquid hydrogen carriers, NH3 has attested itself as a carbon-free and sustainable product. In close similitude with LNG applications, GBS can significantly contribute to the NH3 value chain by supporting NH3 storage and cracking for hydrogen production (Figure 3). It can also be utilised for inland H2 distribution systems, or for the generation of thermal power, or for bunkering vessels at-scale with LNH3 or LH2 as fuels.

In this context, the general architecture of GBS is designed to provide a rigidly massive structure, which is a basic requirement for NH3 storage. The GBS benefits from very high resistance and adaptation to harsh environmental conditions. The safety risks are markedly mitigated since all the facility components are situated relatively far enough from populated areas. In the worst-case scenario of high-speed collision inducing very significant local damages to the GBS caisson, this would never result in the loss of the primary containment due to wide buffer compartment corridors that entirely enclose the NH3 tanks.

Conclusion and perspectives

Saipem has developed an objective assessment of the opportunity for the development of a NH3 cracking and storage facility situated on board of a GBS that can produce up to 300 000 Nm³/h of H2, with GBS hull accommodating up to 300 000 m³ of LNH3, being equivalent to more than three times the storage capacity for conventional very-large LNH3 carriers.

In the near future, the number of GBSs has an opporunity to increase worldwide since this solution has proven to be convenient for most RLGs applications, for all types of vessels, and could be tailored to attain large storage capacities with negligible onshore space. The modular concept that is consistently adopted for GBS topside structures and its storage tanks offers countless advantages in terms of eased logistics, enhanced safety and quality control, cost-effectiveness, overcoming the lack of local skilled labour, and severe weather conditions at site, as well as time-saving benefits. The main complexity that could be met in such projects is that the GBS technology, being a site-specific solution, demands the timely availability of a suitable construction yard.

Saipem aims to capitalise on its expertise to provide reliable solutions to its clients during such large-scale GBS projects.

Figure 3. Value chain of ammonia for hydrogen production.

The electrification of everything will create a doubling of global electricity demand by 2050 according to the International Energy Agency (IEA).1 The simple truth is that renewables cannot meet this demand alone. The world is betting on a 100% renewables future without enough determination to fast-track the supporting clean technologies, such as renewable hydrogen that will make this possible.

Innovation is the currency for solving the world’s big problems. Hydrogen has unparalleled potential to drive the energy transition – but it faces barriers to growth. Two things are required to

Javier Cavada, Mitsubishi Power, outlines the approach required from governments and decision-makers worldwide to fulfil the potential of hydrogen in the energy transition.

overcome such barriers: a pragmatic approach that identifies where hydrogen can directly fit into energy systems now; and a vision for its long-term potential to decarbonise a range of high emitting sectors.

Europe is well behind on delivering its hydrogen goals, with a recent report from the European Court of Auditors suggesting a ‘reality check’ on Europe’s Hydrogen Strategy.2 Among the barriers to growth are high financing costs, investor confidence and a lack of off-takers. To overcome these, the hydrogen industry in Europe needs stronger demand signals from government – moving from policies to targets and commitments to contracts.3

If hydrogen is to scale, bold decisions must be made. Policy and regulation must be used to create the conditions for private capital to follow – to create cross-border and global trading and unlock the socio-economic benefits of this clean molecule with vast potential. This requires hydrogen to be recognised through an international certification to drive investor confidence, get projects to Final Investment Decision (FID) and demonstrate its potential through real-world projects. After this, hydrogen can be utilised and confidence can be built in its ability as an agent of decarbonisation, particularly for heavy industry.

Where hydrogen fits into the energy transition

Renewables will be the mainstay power source in a low-carbon future, but it is not possible to leapfrog to a system wholly reliant on wind and solar power. Otherwise, a route would have already been found. Renewable power is intermittent, unreliable and not domesticated enough to be directly delivered to homes via existing grid systems – it requires back up.

Across the world, natural gas is used in gas peaker plants to provide dispatchable power at peak demand and ensure grid stability – a factor that is rising in importance as more wild renewable energy comes onto grids. But in a low-carbon scenario, hydrogen will blend with gas, and longer-term, could fully replace gas in turbines to generate electricity. This is an immediate route for hydrogen to be incorporated into existing power systems to deliver emission reductions.

COP28 in Dubai, UAE, was important in many respects, including witnessing many historic agreements. The parties committed to tripling renewable energy capacity by 2030, and according to experts, this goal is the single biggest action the world can take for the climate in this decade.4 While there is no single solution to the decarbonisation puzzle, the technologies that will be prioritised are those supporting and enabling renewables.