15 minute read

Roadblocks and obstacles for the land Down Under

Bruce Robertson, IEEFA, Australia, explains how climate risks, competition, falling demand, and legal challenges are strong headwinds for Australia’s LNG industry.

The Australian LNG industry faces headwinds in 2021 due to new climate commitments from major customers, falling demand, legal risks, and competition from Qatar.

In addition, the International Energy Agency (IEA) has adopted a new position on ‘natural’ gas which is far from its former place of gas as a transition fuel with demand increasing. It now sees gas as an industry in decline.

New climate commitments by major gas and LNG importing nations are, over time, likely to result in lower global demand for gas. The US is already seeing falling demand and Australia has experienced lower demand since 2014.

Coupled with increased climate risks, the Australian LNG industry faces significant legal risks highlighted by the recent Sharma vs Minister for the Environment judgement.

Australian LNG also faces competitive risks from Qatar, the global low-cost LNG supplier. Qatar is planning a 64% increase in production which will place pressure on prices.

Balanced against all of this is the substantial nature of Australian government subsidies. Australia’s gas industry cannot survive without large government investment and these subsidies are merely prolonging the inevitable decline of gas as a fuel in the energy system.

With demand now in decline and climate deadlines nearing, investors must be aware of the high likelihood of gas assets in Australia becoming stranded.

International Energy Agency foretells end of gas

The IEA has traditionally been captured by the fossil fuel industry and blind to the revolution that has occurred in the way people produce and consume energy. This

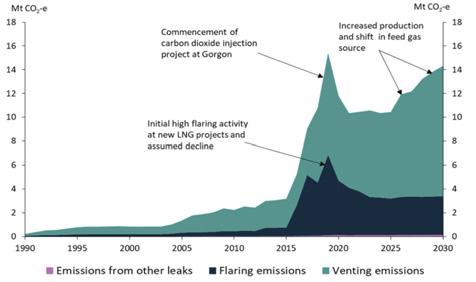

Figure 1. Official gas emissions. Source: Department of Industry, Science, Energy and Resources; Australia’s Emissions Projections 2020.

Figure 2. Total domestic consumption of gas in Australia has declined. Source: AEMO.

positioning recently changed with the release of its report ‘Net Zero by 2050 – A Roadmap for the Global Energy Sector’; a report peer reviewed by Shell and ENI with BP as a contributor.

IEA’s report came to the startling conclusion that the world has to get off gas. In summary the IEA stated that: Beyond projects already committed as of 2021, there are no new oil and gas fields approved for development in the major pathway. Many of the LNG liquefaction facilities currently under construction or at the planning stage are not needed. Between 2020 and 2050, gas traded as LNG will fall by 60%. During the 2030s, global gas demand will decline by more than 5% per year on average, meaning that some fields may be closed prematurely or shut temporarily.

The IEA concludes that the gas industry will decline by 5% per annum compound and stranded assets will abound. Essentially, the IEA is ringing the bell that gas is now a declining industry globally.

Climate change legal risks are rising following Sharma vs Minister for the Environment

Eight teenagers and an 86-year-old nun acting as their legal guardian recently sued Australia’s Federal Minister for the Environment claiming that the Minister owed them a “duty of care” to protect young children from the harms induced by climate change.

The Federal Court of Australia made a ruling that the country’s Environment Minister has an obligation to consider the harm caused by climate change in the approvals process of fossil fuel-related projects.

In closing, Justice Mordecai Bromberg said there is evidence of the “severe harm” climate change can cause future generations.

“It will largely be inflicted by the inaction of this generation of adults, in what might fairly be described as the greatest intergenerational injustice ever inflicted by one generation of humans upon the next,” Bromberg said.

Whilst the court refused an injunction of a forthcoming approval for a coal mine extension, the possibility of it granting one remains open.

The effect of this landmark judgement was neatly summed up by prominent environmental lawyer Elaine Johnson from Australia’s Environmental Defenders Office:

“When you start to contemplate the effect of the Sharma judgement on new fossil fuel projects in Australia, it’s fair to say that the future of all such projects is now in doubt. Fossil fuel projects are now highly vulnerable to legal challenge.”

Qatar plans large expansion of cheap LNG

Qatar, the world’s biggest LNG exporter until last year, has advised it will push ahead with a huge expansion of capacity, taking it from 77 million tpy to 110 million tpy by 2025, then potentially to 126 million tpy just two years later.

Qatar is looking to develop its North Field, a field shared with Iran who has already pushed ahead with development. This 64% expansion from the world’s lowest cost LNG producer will make development in higher cost fields more problematic.

Qatar has also cut prices by approximately 22% to secure new customers. A recent deal was struck with Sinopec at a ‘slope’ or index against crude oil of just 10.19%.

Qatar is a very low-cost producer and can comfortably afford to cut the price of LNG. According to Wood Mackenzie: “At a long-term breakeven price of just over US$4/million Btu, Qatar’s LNG production is at the bottom of the global LNG cost curve, alongside Arctic Russian projects.”

Qatar is not only looking to price to garner customers, it is also looking at producing lower emitting LNG via building facilities capable of capturing and storing 7 million tpy of emissions by 2030.

In November 2020, Qatar Petroleum signed the world’s first deal that details the carbon dioxide pollution of each cargo shipped to the buyer in Singapore. Qatar Petroleum plans to reduce the amount of greenhouse gases (GHG) it emits from its LNG plants by 25% and upstream operations by 75% by 2030 via cutting flaring and reducing methane leakages to 0.2%.

LNG emissions

LNG is a significantly higher emitting fuel than piped gas. In Australia, over 9% of gas is consumed at LNG facilities in order to ‘super cool’ the gas down to -160˚C.1 A further 2% - 6% of methane is lost or burnt in the shipping process. In sum, approximately 13% of the gas is lost or burnt prior to it being regasified in the importing nation (typically in Asia).

This higher emissions nature of LNG will make it a less preferred fuel as the world accelerates efforts to decarbonise.

Emissions intensity

In a recently released paper, the Institute for Energy Economics and Financial Analysis (IEEFA) estimates that between 2014

Figure 3. US natural gas consumption by sector, net change from previous year (2018 - 2022). Source: US Energy Information Administration.

Figure 4. Cost stack of select LNG projects (DES to Asia). Source: Wood Mackenzie; Australia Oil & Gas Industry Outlook Report.

and 2019, the emissions intensity of Australia’s gas production increased by approximately 30% as newer projects released higher rates of GHG emissions. The average amount of GHG associated with gas production increased from 0.54 t of CO2-e per t of LNG produced, to 0.7 t of CO2-e per t of LNG produced.

The original fields that supplied projects in the north of Western Australia (North Rankin and Goodwyn fields) have low reservoir CO2 (3 v%). However, a further, similar steep increase in emissions is likely to be repeated when the five original fields in the North West Shelf of Western Australia finally deplete their currently producing reservoirs and gas is piped (as foreshadowed by Woodside) from the Browse area 900 km away. Those fields are reported to contain 10 - 16 v% CO2 and in combination with compression for the long pipeline, make them far more emissions intensive than the original fields that supplied the project.

Emissions from venting and flaring are growing faster than production

The gas industry has expanded venting and flaring at a far faster rate than its expansion in production. Between 2014 and 2020, the gas industry expanded production from 691 PJ to 1916 PJ, an increase of 177%.2 Official venting and flaring emissions rose by 300% during this period, far in excess of the increase in production.3

Official figures from the Australian Government Department of Industry, Science, Energy, and Resources assume there are no other emission leaks apart from those occurring with the flaring and venting of gas. This is an assumption that does not stand up to scrutiny.

In Figure 1, the figures used for emissions from other leaks such as fugitive emissions and those in the supply chain (the faint pink line at the bottom of the graph) were sourced from several cherry-picked wells by the Gas Industry Social and Environmental Research Alliance (GISERA), which is the gas industry funded, gas industry controlled arm of Australia’s science agency, the CSIRO. They are not in line with the experience in other parts of the world.

Demand and capacity factor reduction

Both domestically and globally, there are signs showing that gas demand has peaked.

In Australia, total domestic consumption of gas is down 16% since 2014 (Figure 2). Declines have been more pronounced in the gas-fired electricity generation sector where gas usage has declined by 42% since 2014. The decline in gas-fired generation has occurred despite the rapid uptake of renewable energy. Renewables now account for 28% of generation in Australia’s National Electricity Market (NEM).

Australia’s federal government is doing everything in its power to reverse the declining usage of gas. It recently progressed the building of the 660 MW Kurri Kurri gas-fired peaking power plant based in New South Wales (NSW) by the government-owned company Snowy Hydro.

As well as the AUS$610 million to build the Kurri Kurri plant, the federal government gifted Chinese-owned EnergyAustralia AUS$83 million to build the 316 MW Tallawarra B gas plant near Wollongong in NSW, which is approximately 25% of the cost. The government also gifted Andrew ‘Twiggy’ Forrest, the well-known Australian billionaire, AUS$30 million to assist in the building of his 650 MW gas plant also in Wollongong. In total, the federal government is currently subsidising gas-fired powered generation in NSW to the tune of AUS$723 million to build a significant 1700 MW of gas plants that Australia simply does not need.

In addition to demand reduction, there is also massive latent capacity in Australia’s gas peaking power stations. Capacity utilisation of gas peaking plants has fallen from 15.5% in 2014 to just 6.5% in 2020. Snowy Hydro itself owns the Colongra gas peaking plant near Kurri Kurri. It had a capacity utilisation of just 0.9% in 2020.

US gas demand

Gas demand fell in the COVID-affected year of 2020. Interestingly, the US government’s Energy Information Administration (EIA) is forecasting a rebound in industrial and residential consumption offset by a large fall in gas powered generation. Overall, the US domestic market is expected to decline in the future as renewable energy eats into gas’ market share.

Global LNG demand

Globally, nations are coming to grips with their newfound climate commitments. As outlined in the IEA roadmap, there is no room for more gas in a carbon constrained world. Over time it is expected that this will translate into lower demand in important South-east Asian markets.

Key new gas field developments in Australia

The key new gas field developments in Australia include Barossa and the Beetaloo in the Northern Territory, the Scarborough gas field in Western Australia, and the Narrabri

gas project in NSW. They are by no means the only new gas field developments as there are also new onshore fields being developed in all states and territories of Australia, with the exception of the Australian Capital Territory and Tasmania.

The development of new gas fields is incompatible with any meaningful climate commitments.

Barossa, Northern Territory

In good news for the LNG industry in Australia, the Barossa gas field located offshore Northern Territory gained Final Investment Decision (FID) from Santos and SK E&S on 30 March 2021. The US$3.6 billion project extends the life of the 3.7 million tpy Darwin LNG facility which has been sourcing its gas from the Bayu-Undan field, a field that is running out of gas.

Barossa is the highest emitting gas and LNG project on the globe. Field emissions of CO2 are so high that John Robert, IEEFA guest contributor, quipped that: “The Barossa to Darwin LNG project looks more like a CO2 emissions factory with an LNG byproduct.”

Santos is exploring the potential of carbon-neutral LNG from Barossa. In the meantime, it will vent the CO2 from the field. Santos recently received a AUS$15 million grant from the federal government to build a carbon capture and storage facility at Moomba. The CO2 will be used for enhanced oil recovery, however Moomba is too far from Barossa to capture its emissions.

Scarborough, Western Australia

The remote Scarborough field off Western Australia was discovered in 1979. Woodside proposes to develop the Scarborough gas resource through new offshore facilities connected by a 430 km pipeline to an expansion of the existing Pluto LNG facility on the Burrup Peninsula (Pluto Train 2). The Pluto Train 2 LNG brownfields expansion would have a capacity of approximately 5 million tpy.

At an Australian Petroleum Production and Exploration Association (APPEA) conference in May 2013, in the days when ExxonMobil was a stakeholder in the Scarborough gas field, Exxon Executive Mark Nolan was reported as saying that the Scarborough project will be “very challenged from a cost point of view.” Scarborough contains very dry gas so there are no liquids to improve the economics of the project. The field is shallow and broad and will require expensive deepwater horizontal drilling – according to Exxon.

In a report by Wood Mackenzie dated 9 March 2020 (commissioned by APPEA), the Pluto expansion project, utilising gas from Scarborough, is the most expensive at over US$9/million Btu delivered to Asia. The increasing competition globally puts even greater pressure on the economics of the Scarborough gas field and Pluto LNG expansion.

Woodside has struggled to secure long-term contracts for its Scarborough gas expansion. In January 2021, Woodside announced an expansion of the binding 13-year Sales and Purchase Agreement (SPA) with Uniper of Germany. Initial supply commencing in 2021 is for a volume of up to 1 million tpy increasing to 2 million tpy from 2026.

The initial agreement with Uniper was struck over a year ago in late 2019. Woodside has been unable to attract any other customers. With the frosty relationship that currently exists between Australia and China – which is the fastest growing LNG market – Australian companies have more limited customer opportunities.

Given that the Pluto expansion is for 6.5 million tpy, only 31% of the project’s output is contracted. Typically for a project to proceed, greater than 80% of volumes need to have found long-term customers.

The Beetaloo, Northern Territory

The federal government is looking to the Northern Territory as one of its key areas of expansion under its gas-fired recovery.

In January 2021, the government announced it was pouring AUS$173 million into road infrastructure in the Beetaloo basin and a further AUS$50 million directly into subsidising gas exploration wells.

The drilling in the Beetaloo is recommencing this dry season after COVID and low prices halted development. Companies such as Tambouran Resources, Santos, Origin Energy, Empire Energy, and Falcon Oil and Gas are all vying for a share of the government’s largesse.

Subsidies for new projects are not uncommon in Australia, however direct subsidisation of high-risk exploration wells is rare.

Narrabri, New South Wales

Santos’ controversy-plagued Narrabri gas project appears to have stalled following its final approvals in November 2020. Pipeline access appears to have been the problem with APA not submitting its Environmental Impact Statement by 4 May 2021 for its Western Slopes Pipeline to connect Narrabri with the Eastern gas grid. There appears to be little progress by APA on this project.

The federal government is looking to subsidise the other gas pipeline that could connect Narrabri into the gas grid, which is the Queensland Hunter Gas pipeline (QHGP). The QHGP was first approved in 2009 but the company will need significant government support to get its pipeline built. It is likely that government support will be forthcoming to facilitate the Narrabri gas project.

Conclusion

The LNG industry in Australia faces an increasingly competitive global market placing pressure on profitability.

The government is looking at providing considerable support for the industry in the form of offtake agreements, subsidies for exploration and infrastructure, and legislative support. In the end, it is likely that the failing economics of gas will overwhelm government support. Investors need to understand the existential risks to their capital if they choose to employ it in the LNG industry.

References

1. Department of Industry, Science, Energy and Resources,

Australian Energy Update 2020, September 2020. 2. AEMO. Gas forecasting portal. 2021. 3. Department of Industry, Science, Energy and Resources,

Australia’s emissions projections 2020 Chart Data Spreadsheet, 2020.

Note

The views expressed herein are those of the author and not necessarily the views of IEEFA, its management, its subsidiaries, its affiliates, or its other professionals.