Ross McGavin and James Reid, Wood Mackenzie, UK, consider the importance of government support in the effort to reduce the upstream sector’s import dependency in Europe.

12 A Window Into The Future

David Barnett, Wild Well Control, USA, discusses the evolution of relief wells, and the benefits of intervention wells in increasing safety and enhancing P&A operations.

Front cover

Relief Wells are no longer just for resolving blowouts. The experience gained through years of relief well execution combined with advances in directional drilling and proximity ranging have created opportunities for relief wells to be used for other important purposes. Intervention wells are now used to enhance P&A isolation and to de-risk wells requiring complex surface intervention.

17 Navigating The Depths Of Oil And Gas Safety

Danny Constaninis, EM&I, Malta, explains how incorporating emerging technology with a desire to mitigate safety risk, reduce impact on operations, drive efficiencies and save costs will maintain the integrity of offshore hulls.

21 Leak Remediation Without The Usual Drawbacks

Alex Nicodimou, Welltec, Denmark, outlines an effective option for maintaining well integrity and optimising remediation operations.

24 Elevating Performance

Brandon Rosler and John Alvarado, Nabors Drilling Solutions, USA, explain how integrating automation in daily operations is allowing drilling contractors of all sizes to realise greater efficiencies.

28 Building an understanding

Mike Aughenbaugh, Swagelok, explores the distinctions between pitting corrosion and crevice corrosion.

32 UK and Norway Exploration and Production Outlook 2024

Graeme Bagley, Westwood Insight, UK, provides an outlook for the UK’s and Norways’ exploration and production in 2024.

Our priority is the safe on-time delivery of your global energy projects. CRC Evans utilises market-leading welding and coating services, technologies and advanced data solutions, combined with a right first time approach.

Comment

Jack Roscoe, Editorial Assistant jack.roscoe@palladianpublications.com

This summer, the eyes of the world have been drawn towards the French capital, as Paris became only the second city to host the Summer Olympic Games three times. The 30th edition of these Games featured 48 different sports, welcomed 206 participating countries, and is expected to have cost around €9 billion.

It marked a century since the City of Light last hosted the Olympics, and although the 1924 event was vastly different to this summer’s spectacle – both Parisian Games have shown the ever-evolving nature of the Olympics.

The 1924 Paris Olympics were a landmark Games for a number of reasons: these were the first Games to have an Olympic village, use a swimming pool with marked out lanes, and the first to use the famous motto “citius, altius, fortius” (faster, higher, stronger).1 It embraced change and looked towards the future – for example, the number of participating committees jumped from 29 to 44. Furthermore, it was the first ever Olympics to be broadcast live – welcoming over 1000 journalists. The 1924 Olympics was the first time the Games were a truly global event and welcomed change, which laid the foundations of the Olympics we know today. Finding the balance of honouring the past whilst also embracing the future is at the centre of the Olympics’ identity – and 100 years after Paris hosted their second Games, the balance was still present this summer. There was an Olympic debut for breakdancing, and the dramatic boat-parade along the river Seine was the first time in Olympic history that the opening ceremony has been held outside a stadium. However, the Paris 2024 Olympics’ commitment to sustainability is where a focus on the future and embracing change really shone through. Perhaps one of the most talked about features of this summer’s Olympics was Paris’s ambitious project to clean up the River Seine. An estimated US$1.5 billion was spent to achieve this, which meant it marked the first time that an urban river has been used for swimming events at the Games since they were revived in 1896. It is hoped that the cleaning of the Seine will cement Paris’s brand as a new capital of sustainability – a place where cars and tarmac are ceding space to bikes, pedestrians and trees.2 It was also the first set of Games to fully embrace the IOC’s strategic roadmap, set out in the 2020 Olympic Agenda –while schemes such as cardboard beds in the Olympic village have also been put in place to reduce carbon emissions.3

It is not just the Olympics that has embraced change, as the oil and gas industry is also evolving to become a more sustainable sector. There has been significant investment into technology to reduce carbon emissions – for example Chevron has set aside US$10 billion from 2021 – 2028, expanding Carbon Capture and Storage hubs in the USA.4 ExxonMobil have also embraced CCS, and since 2008 they have stored around 8 million tons of CO2 in Norway, setting aside US$100 million annually for these projects. 5

The Olympics showed us this summer that tradition can still be respected whilst welcoming change, and as the oil and gas industry has come under more pressure, it too is embracing the future as it moves towards more sustainable practices.

Production: Kyla Waller kyla.waller@palladianpublications.com

Sales

Sales Director: Rod Hardy rod.hardy@palladianpublications.com

Sales Manager: Chris Lethbridge chris.lethbridge@palladianpublications.com

Sales Executive: Daniel Farr daniel.farr@palladianpublications.com

Website

Digital Content Assistant: Kristian Ilasko kristian.ilasko@palladianpublications.com

Digital Administration: Nicole Harman-Smith nicole.harman-smith@palladianpublications.com

Events

Head of Events: Louise Cameron louise.cameron@palladianpublications.com

Digital Events Coordinator: Merili Jurivete merili.jurivete@palladianpublications.com

Marketing

Administration Manager: Laura White laura.white@palladianpublications.com

Reprints: reprints@palladianpublications.com

Palladian Publications Ltd, 15 South Street, Farnham, Surrey GU9 7QU, UK Tel: +44 (0) 1252 718 999 Website: www.oilfieldtechnology.com

Email:

emily.thomas@oilfieldtechnology.com

World news

Chevron starts production at anchor with deepwater technology

Chevron has announced that it started oil and natural gas production from the Anchor project in the deepwater U.S. Gulf of Mexico.

Anchor production marks the successful delivery of high-pressure technology that is rated to safely operate at up to 20 000 psi, with reservoir depths reaching 34 000 ft below sea level.

“The Anchor project represents a breakthrough for the energy industry,” said Nigel Hearne, Executive Vice President, Chevron Oil, Products & Gas. “Application of this industry-first deepwater technology allows us to unlock previously difficult-to-access resources and will enable similar deepwater high-pressure developments for the industry.”

The Anchor semi-submersible floating production unit (FPU) has a design capacity of 75 000 gross bpd and 28 million ft3 of natural gas per day. The Anchor development will consist of seven subsea wells tied into the Anchor FPU, located in the Green Canyon area, approximately 140 miles (225 km) off the coast of Louisiana, in water depths of approximately 5000 ft (1524 m). Total potentially recoverable resources from the Anchor field are estimated to be up to 440 million boe.

“This Anchor milestone demonstrates Chevron’s ability to safely deliver projects within budget in the Gulf of Mexico,” said Bruce Niemeyer, president, Chevron Americas Exploration & Production. “The Anchor project provides affordable, reliable, lower carbon intensity oil and natural gas to help meet energy demand, while boosting economic activity for Gulf Coast communities.”

The Anchor FPU is Chevron’s sixth operated facility currently producing in the U.S. Gulf of Mexico, one of the lowest carbon intensity oil and gas basins in the world. Chevron’s operated and non-operated facilities in the Gulf of Mexico are expected to produce a combined 300 000 boe/d by 2026.

To reduce carbon emissions, the Anchor FPU was designed as an all-electric facility with electric motors and electronic controls. Additionally, the FPU utilises waste heat and vapour recovery units as well as existing pipeline infrastructure to transport oil and natural gas directly to U.S. Gulf Coast markets.

bp gives go-ahead for sixth operated hub, Kaskida, in the US Gulf of Mexico

bp has taken a final investment decision on the Kaskida project in the US Gulf of Mexico. This demonstrates bp’s long-term commitment to deliver secure, affordable and reliable energy.

Kaskida will be bp’s sixth hub in the Gulf of Mexico, featuring a new floating production platform with the capacity to produce 80 000 bpd of crude oil from six wells in the first phase. Production is expected to start in 2029.

“Developing Kaskida will unlock the potential of the Paleogene in the Gulf of Mexico for bp, building on our decades of experience in the region,” said Gordon Birrell, bp’s Executive Vice President of production and operations.

Owned 100% by bp, the Kaskida field has discovered recoverable resources currently estimated at around 275 million boe from the initial phase. Additional wells could be drilled in future phases, subject to further evaluation.

The project is fully accommodated within bp’s disciplined financial framework, reflecting bp’s drive to focus on value and returns.

Located in the Keathley Canyon area about 250 miles southwest off the coast of New Orleans, the Kaskida project unlocks the potential future development of 10 billion bbl of discovered resources in place across the Kaskida and Tiber catchment areas.

bp plans to leverage existing platform and subsea equipment designs that can be replicated in future projects to drive cost efficiencies across Kaskida’s construction, commissioning and operations.

July/August

2024

South Africa

Impact Oil & Gas Ltd has announced that its wholly-owned subsidiary, Impact Africa Ltd, has entered into an agreement with Silver Wave Energy to acquire its entire interest (10%) in Area 2, offshore South Africa.

Norway

Miros has successfully supported the laying of a 109 km pipeline for the Northern Lights CO2 transport and storage (CCS) project.

Indonesia

TGS has completed the reprocessing of a 2D seismic survey in Indonesia’s Sumatra basin, tying key discoveries in the region to open acreage.

North Sea

Viaro Energy signs agreement to take over Shell and ExxonMobil’s UK Southern North Sea assets.

Brazil

Strohm wins TCP Flowline contract with TotalEnergies EP Brasil. The deal marks the largest commercial award for pipe supply in the company’s 16-year history and a first project in the Brazilian pre-salt.

Singapore

Seatrium has announced the successful delivery of its fourth jackup rig, named ‘Vali’, to Borr Drilling, about a year ahead of its planned delivery next year.

World news

Diary dates

17 – 20 September 2024

Gastech 2024

Texas, USA www.gastechevent.com

28 – 30 October 2024

YNOW2024

Texas, USA www.yokogawa.com

04 – 07 November 2024

ADIPEC 2024

Abu Dhabi, United Arab Emirates www.adipec.com

19 – 23 May 2025

29th World Gas Conference (WGC2025) Beijing, China www.wgc2025.com

Web news highlights

Ì Shell invests in Phase 2 of Surat gas project in Australia

Ì Petrobras confirms gas discovery in Colombia

Ì QatarEnergy increases participation in Suriname’s offshore exploration

Ì Salunda ‘Red Zone’ safety technology adopted by BP for North Sea assets

Ì Deltic Energy announce rig mobilisation in the North Sea

July/August 2024

Pantheon secures rig for Megrez-1 well and award of new leases

Pantheon Resources has announced that it has executed a rig contract to secure the use of the Nabors 105AC rig to drill the Megrez-1 well in Q424.

Pantheon has also announced that the leases which it successfully bid for in December 2023 have been awarded and are expected to be issued within the coming weeks.

Pantheon has formally contracted to use the Nabors 105AC drill rig, a rig the company is familiar with having used it in previous drilling campaigns, to drill the Megrez-1 exploration well which will target the Ahpun East topset play. Siteworks for construction of a gravel pad along the west side of the Dalton Highway are expected to commence in September and upon completion of these siteworks the drill rig will be mobilised.

The Megrez-1 well is estimated to have a 69% geological chance of success and will target the topset sands in the Ahpun East project area which the company estimates to contain 609 million barrels of marketable liquids and 3.3 ft3 of natural gas. The Ahpun East topsets are significantly shallower than the Ahpun western topsets drilled previously.

The company has also paid the remaining portion of the fees for the 46 new oil and gas leases acquired in the state of Alaska’s 2023W Areawide oil and gas lease sale held in December 2023 as announced on 14 December 2023. Based on the official title work done by the State prior to awarding the leases, the 46 new leases consist of an aggregate of 65 691.5 acres, 30 of which are located on the western boundary of the Kodiak Field and 16 of which cover the Ahpun East topset play. The State of Alaska will execute and issue the leases in the next few weeks.

Jay Cheatham, Pantheon’s Chief Executive, commented: “With a management best estimate for the eastern topsets in Ahpun at over 1 billion boe to be tested by the Megrez-1 well, located immediately adjacent to pipeline and road infrastructure and in reservoirs expected to be orders of magnitudes better than western topsets, we believe this to be one of the most impactful onshore exploration well being drilled anywhere in the world during 2024. Success here would further advance our Ahpun development models and plans.”

SBM Offshore awarded FSO contract for Woodside’s Trion development

SBM Offshore has announced that it has signed a contract with Woodside Petróleo Operaciones de México, S. de R.L. de C.V. (Woodside), operator of the Trion deepwater oil field development located in the Perdido Belt of the western Gulf of Mexico. Under this contract, SBM Offshore will construct and thereafter lease to Woodside a Floating Storage and Offloading (FSO) unit for a period of 20 years. This award complements the Transportation & Installation contract for the FSO and the FPU awarded to SBM Offshore in 2023.

The new build FSO, based on a Suezmax-type hull, will be equipped with a disconnectable turret mooring (DTM) system designed by SBM Offshore. The FSO will be moored in water depth of about 2500 m and will be able to store around 950 000 bbl.

The Trion field is located 180 km off the Mexican coastline and 30 km south of the US/Mexico maritime border. The Trion project is an alliance between Woodside (60%, Operator) and PEMEX Exploración y Producción (40%, non-Operator).

To read more about these articles and for more event listings go to: www.oilfieldtechnology.com *News continued on p31

Unconventional Intervention:

Wild Well is the beacon of expertise in well intervention and remediation, where conventional methods falter. Our comprehensive services exceed the ordinary, enabling us to tackle projects on land and at any operational water depth with unparalleled precision and efficiency.

Our commitment to excellence is evident in our array of specialized services:

Hot Tapping: Safely determining the presence of pressure in oilfield equipment, when conventional methods fail, minimizing downtime, and maximizing efficiency.

Gate Valve Milling: Precision machining solutions to address valve obstruction and restore optimal flow up to 15,000psi.

Freeze Services: Create temporary pressure barriers in oil and gas wells by freezing existing fluids at ultra-low temperatures.

Cutting Services: Various cutting tools mechanical and abrasive can address different needs, from well bore tubulars to complete rig infrastructure.

Discover the power of unconventional intervention with Wild Well. Your challenges are our opportunities for transformation.

Ross McGavin and

James Reid, Wood Mackenzie,

UK, consider the importance of government support in the effort to reduce the upstream sector’s import dependency in Europe.

Europe’s reliance on Russian gas has reduced, but import dependence remains high. Although concerns about energy security and affordability have subsided, the issue is never far away. Some governments have been forced to accept the importance of their own domestic supply and look to grow it.

However, Europe’s policymakers do not speak with one voice, especially as they grapple with both the promise of energy security and a commitment to the energy transition. Upstream investors will favour investment in countries where government support is strong.

Europe has successfully diversified supply in the aftermath of Russia’s invasion of Ukraine with increased LNG imports.

But indigenous production – dominated by Norway – makes up less than half of total European gas supply. Governments have a choice to make; support their home upstream industries or increasingly rely on imports in a volatile world.

Fiscal

policy changes across Europe’s upstream industry

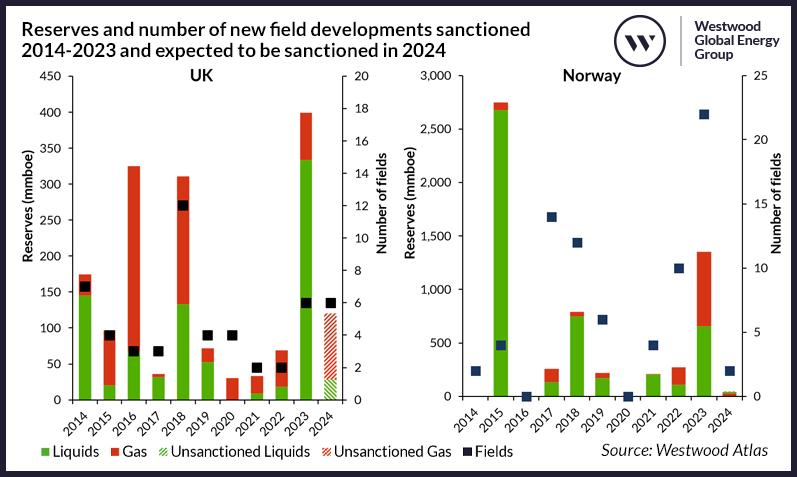

The North Sea exemplifies this contrast in government upstream policy. In Norway, support has been strong. Tax packages and the state’s backing of Equinor has allowed Norway to supply gas to Europe at record levels. However, the UK’s recent raft of fiscal changes has brought significant investor uncertainty.

The UK government introduced the Energy Profits Levy (EPL) in May 2022, in response to rising commodity prices and record upstream profits. The marginal tax rate was increased from 40 – 65% until December 2025. But in November 2022, the EPL was further increased, taking the marginal rate to 75%, with the windfall tax period extended to March 2028. This was followed by a third change in March 2024, where the EPL was extended to March 2029.

The main issue with the EPL is not so much the tax rate, but the constant change and instability it brings. This seriously harms investors’ confidence and their ability to plan long term, particularly for long-lead projects.

After winning the General Election, the newly elected Labour party has continued in the same vein as the previous Conservative administration. The government is proposing to increase the EPL by 3% (taking the EPL to 38% and the headline rate to 78%), extend the sunset clause to 31 March 2030, remove the 29% investment allowance, and reduce the capital allowances. The industry will now wait with bated breath ahead of the budget on 30 October to see what the ambiguous ‘reduction in capital allowances’ equates to. In the short-term, investor confidence will be dampened, and activity could slow to a crawl.

Norway has levied a 78% effective tax rate on oil and gas profits for over three decades. But headline tax rates are only one part of the fiscal system. There are generous capital allowances and refunds on losses for non-taxpaying companies. The Norwegian government also introduced a temporary tax package between 2020 – 2022 which incentivised US$35 billion of investment in over 30 projects. This will help Norway maintain production of around 4 million boe/d until the end of this decade. In comparison to the UK, Norway is a bastion of fiscal stability.

Government support for key projects is vital for progress

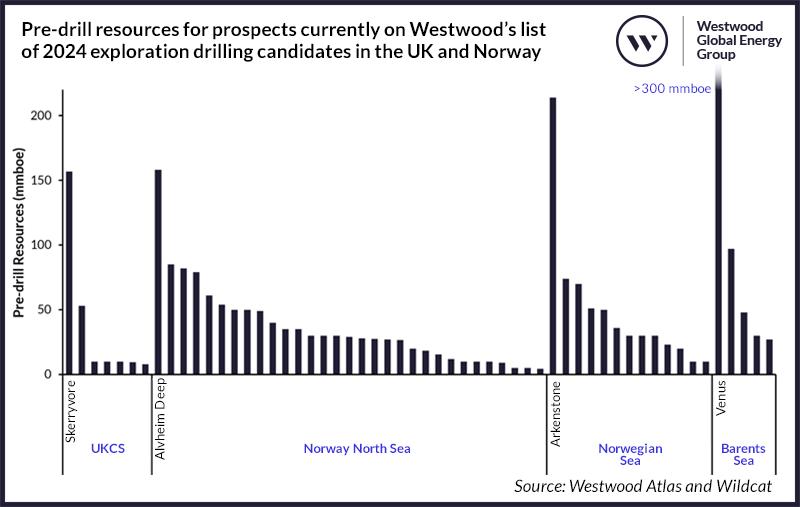

Elsewhere in Europe, government support for gas megaprojects in the Black Sea is transforming the region. Romania’s government has approved vital investor-friendly reforms to the controversial Offshore Law. This has unlocked progress at the 3.5 trillion ft3 Neptun Deep field and, in principle, stabilised the tax terms for Black Sea projects. However, there is no guarantee that regulatory volatility will be avoided in future, as shown by Romania’s current producer gas price cap.

The Neptun Deep project took FID last year, and once onstream in the late-2020s, it will transform Romania into the EU’s largest gas producer, allowing it to export 4 billion m3 of gas throughout Europe.

In Turkey, national oil company TPAO’s 17.5 trillion ft3 Sakarya gas project was brought online in 2023. The three years from discovery to start-up was impressive for an operator with minimal deepwater experience.

The project is of national importance, helping Turkey reduce its US$100 billion energy import bill by meeting up to 30% of domestic demand by the early 2030s. Success hinges on the ramp up, which to date has been slower than TPAO promised. An additional phase took FID in 2023, and contracts for another larger phase could be awarded this year.

In the East Mediterranean, the Cypriot government is pushing to develop its discovered gas resources, but it is yet to agree a development concept with operators. 12 trillion ft3 of gas has been discovered in the ultra-deepwater of the Mediterranean Sea, but none has been commercialised.

The government would prefer that the volumes were delivered to Cyprus, but Chevron wants a lower cost tie-back to Egypt’s under-utilised LNG facilities, a high-level concept that the Cypriot

Figure 1. UK oil and gas marginal tax rate changes since 2000.

Figure 2. Offshore production in Romania and Turkey.

Figure 3. European gas balance.

Figure 4. Emissions intensity of delivered gas to UK.

government has reluctantly agreed to. However, the operator’s development plan for Aphrodite has been rejected twice. The first time was due to the lack of a floating facility in Cypriot waters and the second was over the timing of FEED.

In Italy, the controversial PiTESAI legislation, restricting the development of natural resources, was cancelled by a court in Rome. The law was introduced by the previous government, but the incumbent Meloni government is not expected to challenge the ruling as it favours growing domestic production. The ruling was welcomed by UK-listed player, Energean, saying it re-establishes a more secure and equitable regulatory framework. Despite the cancellation, Italian operators will still have to navigate the notoriously complex and multi-layered regulatory environment. Bureaucratic challenges, including delays to environmental approvals at the regional level, will still be there at Italy’s onshore gas fields.

Although the UK Energy Profits Levy undoubtedly impacted investor confidence it does at least provide an incentive to invest. 29% of capital expenditure is, currently, allowed as an extra deduction for EPL. For those in a taxpaying position, this has helped boost project economics. Indeed, 2023 saw the most UK FIDs for five years. This included the 325 million boe Rosebank field West of Shetland, despite strong environmental and political pressures. However, removal of the 29% investment allowance could cause investors to re-think any upcoming UK FIDs. The temporary tax package in Norway between 2020 and 2022 successfully incentivised billions of dollars of investment into the upstream sector, which is expected to unlock over 2.5 billion boe of reserves from over 30 projects.

However, with most projects operated by a handful of companies, capital and resource allocation is a challenge. The strong demands on the service sector have inflated costs and caused delays in project execution.

Norwegian gas production will however increase in 2024 following extensive maintenance in 2023. Gas production set a record in Q124 of

348.7 million m3/d, which is forecast to meet 20 – 25% of European demand through this decade.

Energy Minister, Terje Aasland, stated that Norway “will not lose sight of the need for energy security, both at home and abroad,” before adding, “this is why the government will continue to develop the Norwegian petroleum sector”. As investment and government support for upstream in the UK stutters, Norway continues to power ahead.

How have changes impacted progress towards the energy transition?

Despite the increased focus on energy security, several European countries are limiting their upstream sectors, or at least considering doing so, to combat climate change. Countries which have very little of Europe’s remaining resources or have not been dependent on Russian gas, tend to be most likely to phase it out. Denmark has put a 2050 end date on its upstream sector, although it will likely have ceased by then anyway. France, Ireland, Portugal and Spain have also stopped issuing new exploration licences.

By limiting the production of domestic resources, Europe’s reliance on gas imports from elsewhere increases.

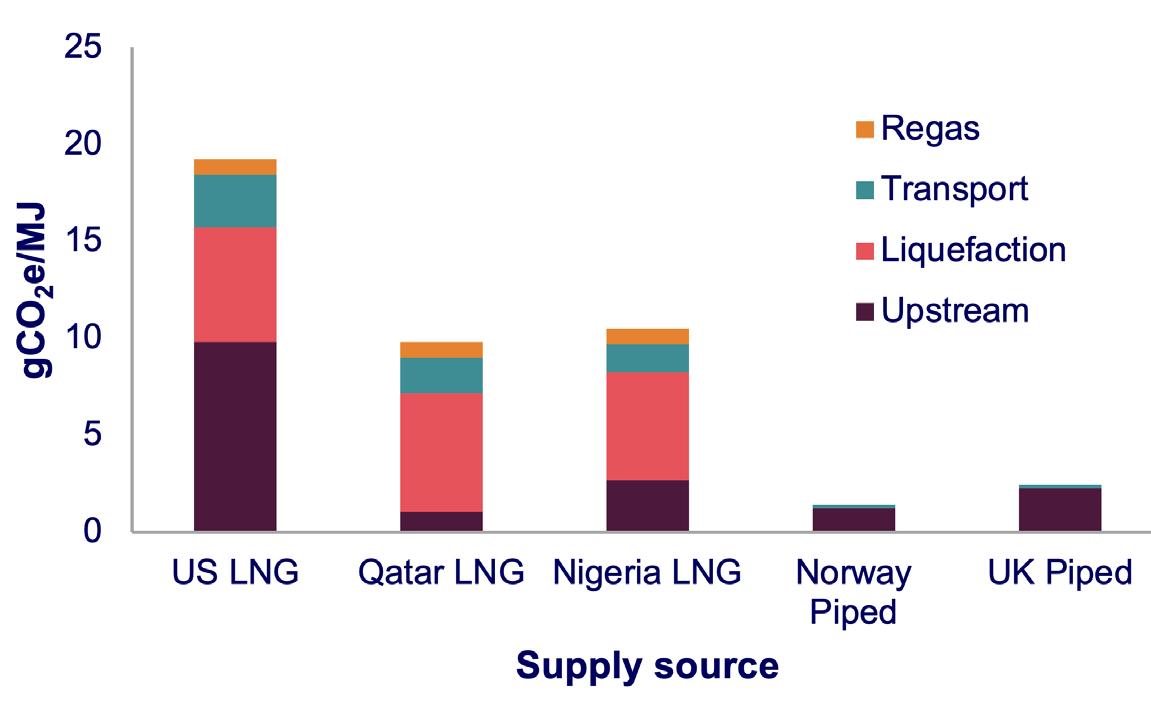

LNG’s share of European supply will increase from around 20% to 40% by the end of this decade as it displaces Russian volumes to Europe.

The trouble is, imported volumes are far more emissions intensive than domestic piped gas. Data from Wood Mackenzie’s emissions benchmarking tool shows that when liquefaction and transportation is accounted for, LNG imports have up to 7.5 times more total emissions than gas imported from Norway and five times more emissions than UK-produced gas.

There is no doubt that domestic gas production is less emissions intensive than LNG imports. It just remains to be seen whether European governments support it.

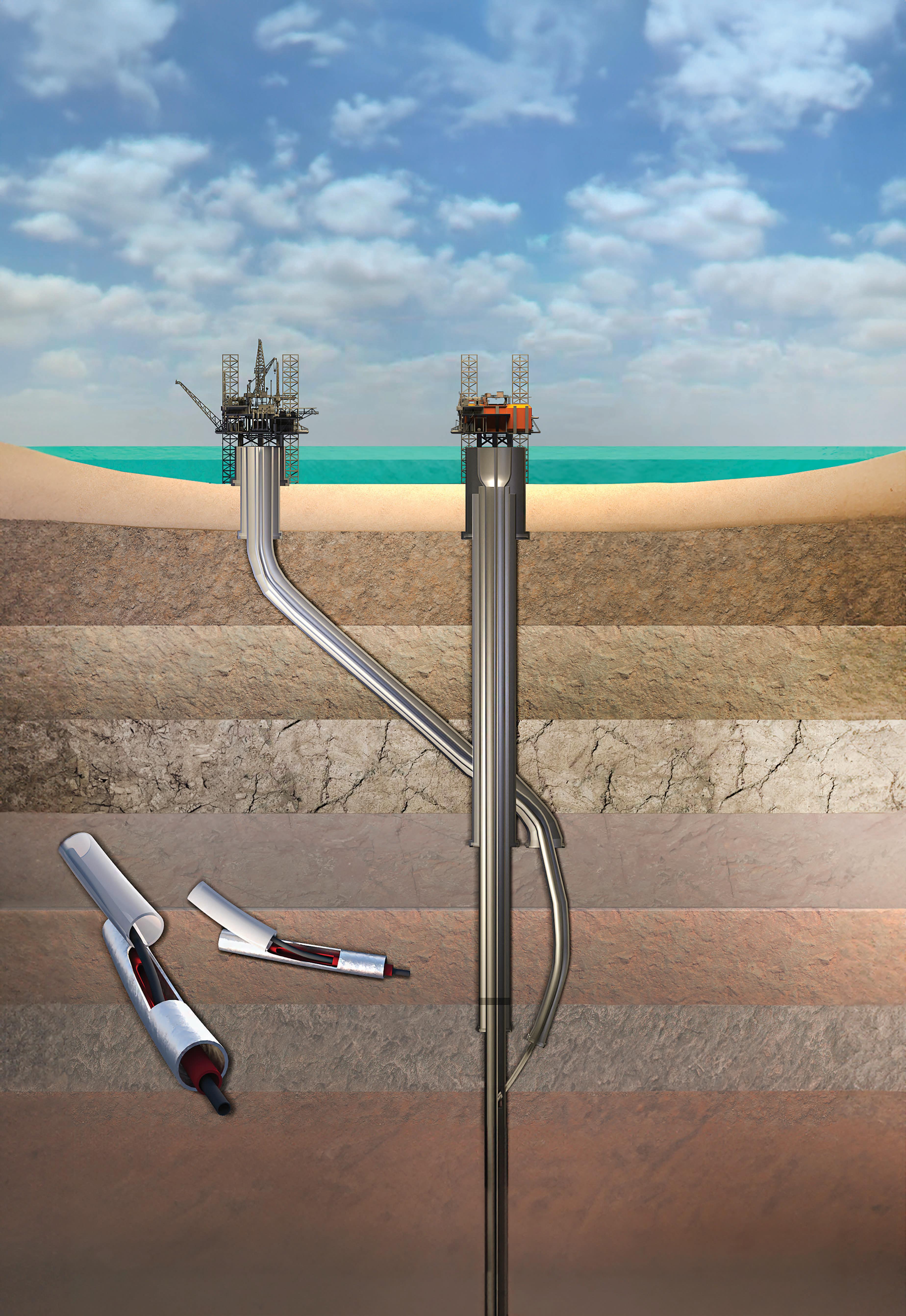

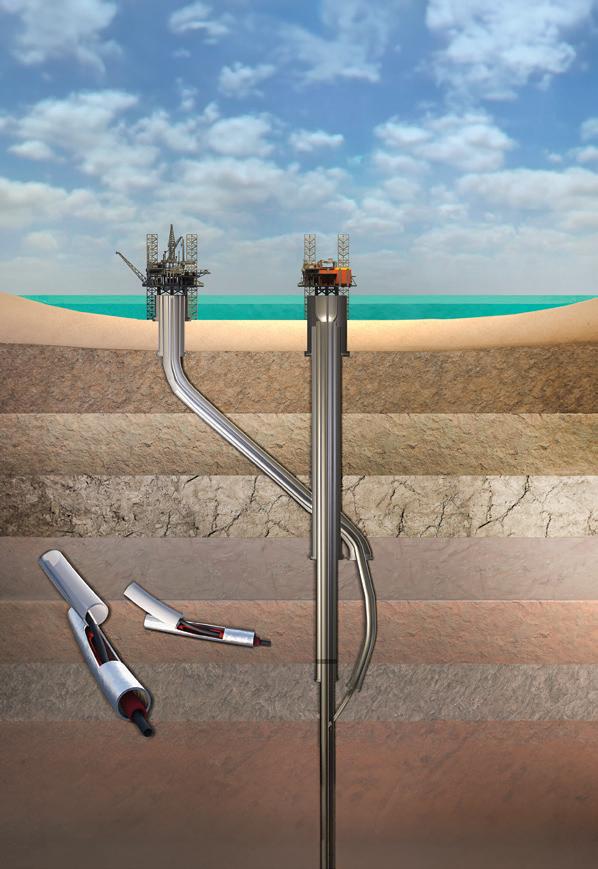

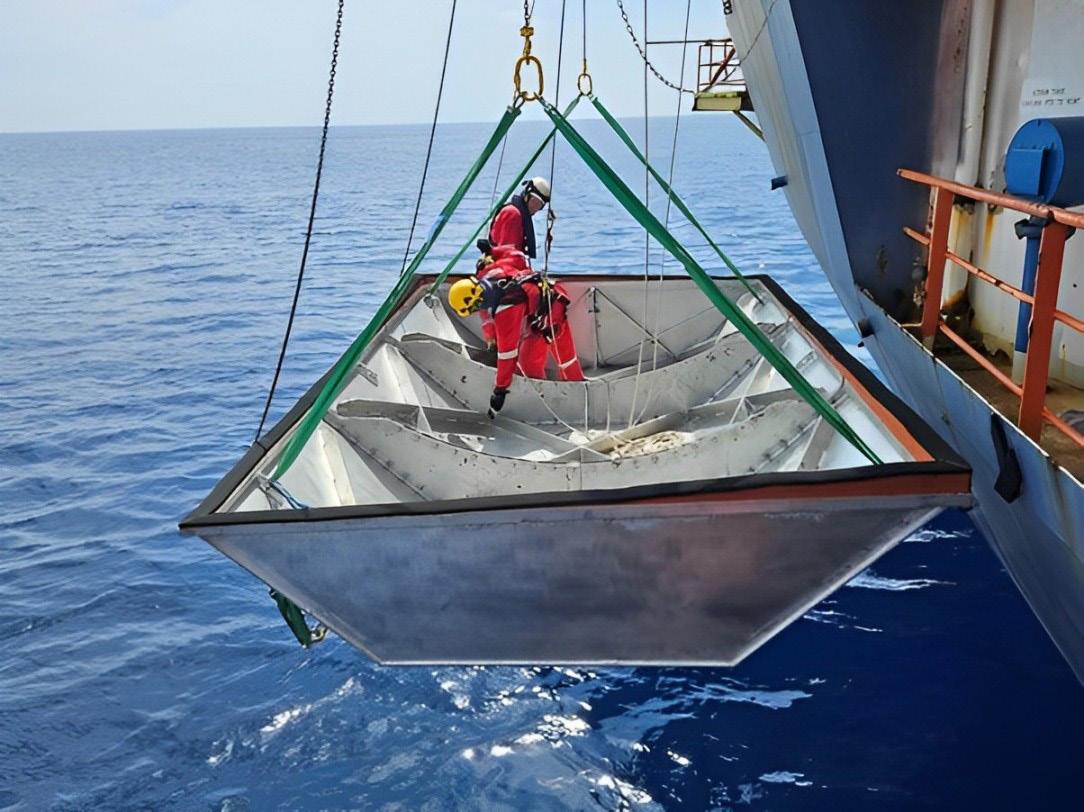

A window the future

David Barnett, Wild Well Control, USA, discusses the evolution of relief wells, and the benefits of intervention wells in increasing safety and enhancing P&A operations.

For many years, relief wells were seen as a last resort solution, only to be used when all other strategies failed or were clearly unsuitable. However, as directional drilling capabilities evolved, and ‘ranging’ techniques improved, relief wells gained more acceptance as a dependable solution. This perception of dependability transformed the relief well from a solution of last resort to a primary solution in many cases.

window into future

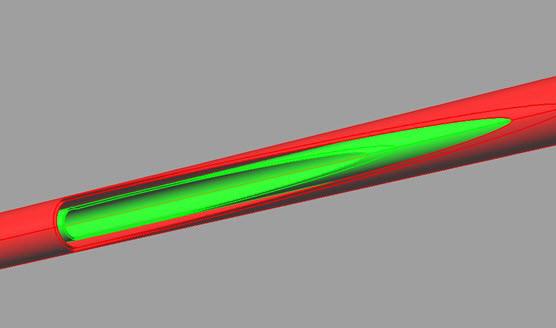

Most people’s concept of a relief well operation involves drilling a new well into an existing well that is blowing out – often accompanied by high rate dynamic kill operations. These operations still take place, but the techniques that evolved from years of relief well drilling gave rise to another use for high-precision intercept wells – the intervention well (IW). IWs use similar technology in terms of magnetic ranging and well placement, but their purpose is to align with and typically penetrate a well that is not blowing out, usually for the purpose of isolating potential flow sources. This enables the de-risking of planned surface operations and enhancement of previous plug and abandonment (P&A) efforts where well access is not possible or practical.

The ability to use an IW to enhance poorly implemented or questionable P&A operations has become increasingly valuable

as operators move towards using old producing oilfields for carbon capture and sequestration (CCS).

Evolution of relief wells

Relief wells have been employed for decades to resolve well control events. Prior to the advent of borehole surveying instruments, wells were drilled vertically near a blowing well and then used to ‘relieve’ the reservoir pressure by flowing the relief well at high rates. Most people generally agree that the first modern relief well was drilled near Conroe, Texas in 1933. This well initiated a period where relief wells would be directionally drilled into the reservoir much closer to the blowout. Water and kill mud would then be pumped into the blowout reservoir to actually kill the blowout. This type of relief well strategy remained standard practice until the 1970s. By 1970, wireline conveyed instruments were used to detect the blowout well tubulars and guide the relief well to the first direct intercept (perforation between wells).1 By the mid-1970s, methods were developed to guide relief wells using passive magnetic ranging (PMR). This approach measured the perturbations in the Earth’s magnetic field caused by the remnant magnetic poles on the blowout casing or drillstring. The predecessor of modern relief well guidance technology was developed around 1980. This system is called active magnetic ranging (AMR) and works by analysing a magnetic field that is induced by injecting an AC current through the sediment from the relief well onto the target well. AMR, often used in conjunction with improved PMR methods, is used to guide modern relief wells. These tools, along with improvement in measurement while drilling (MWD) and wellbore surveying lead to direct intercept relief wells where the relief well actually makes controlled contact with the blowout well and a hole is milled into the blowout well casing. This greatly improved the implementation of dynamic kill operations since the flow path for kill fluids was no longer through the producing formation or perforations.

The latest milestone in relief well drilling is the ability to align the relief well with sufficient precision that a window can be milled in the target well casing that allows re-entry with small tubing strings. This version of the relief well can be used to implement zonal isolation through placement of additional cement plugs.

Work is ongoing to broaden the use of these high precision wells by devising ways to conduct operations below the intercept window (milling, fishing, running downhole tools, etc.) and milling entire sections of casing to facilitate placing a rock to rock isolation plug.

Reducing safety risks

The industry is plagued with old wellbores and wellheads that are in poor condition. Sometimes these wellbores and/or wellheads pose serious safety risks that make it difficult for even specialised intervention. Many of these wells have a single barrier that may be of questionable integrity and disturbing it may lead

Figure 1. Diverter on damaged well (left) and on newly drilled well (right).

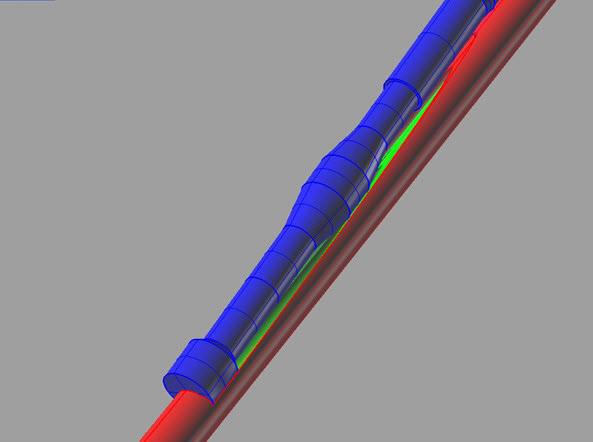

Figure 2. Depiction of milling assembly penetrating casing and tubing.

to an uncontrollable situation. It is most often the lack of shallow wellbore pressure integrity that drives the solution towards isolating the pressure source(s) at the bottom of the well –or at least deep enough to re-establish caprock integrity. The goal of the IW in this instance is to reduce the safety risk from an uncontrolled blowout down to managing trapped pressure below the existing barrier.

Reducing operational risk

As the number of P&A wells increase, there is a corresponding number of instances where previous P&As are coming under escalated scrutiny. Some of these are due to minor leaks or soil disturbances observed around previous wellbores; others may be a result of due diligence associated with acquisitions. One recent development is the review of previous P&As related to carbon capture and sequestration (CCS).

Logically, the best candidates for CCS are often older, depleted reservoirs. However, almost all of these reservoirs were exploited using numerous wellbores. Once the productive zones were depleted, the wells were permanently abandoned. Unfortunately, some of the permanent P&As were not done in accordance with best practices or there were no records to confirm that adequate, long term isolation was established and verified. Many wells were left with wellheads removed and shallow cement plugs set. In cases where wellhead access is either impossible or cost prohibitive, an IW may be an ideal choice to verify or enhance zonal isolation.

If the need to confirm or enhance zonal isolation is identified, the decision process is relatively simple, given that the well is easily accessible. A direct intervention can be done, even if a tie-back and new wellhead installation is required. However, if the well is not easily accessible (for instance, it is offshore with the wellhead removed below the mud line, a land well with casings removed, or it is damaged below a depth where excavation is practical) then the decision process should include an IW as a solution.

Numerous successful excavations have been carried out both on land and in the offshore environment. However, these operations involve substantial operational risk that can sometimes be avoided with an IW. Costly and time-consuming excavations followed by well tie-backs almost always pose the risk of operational difficulties during the actual re-entry. Years of corrosion, unknown blockages and unforeseen downhole damage could make the P&A intervention unsuccessful. A thorough operational risk assessment should be carried out anytime there is a distinct

Figure 4. Re-entry window after milling operations.

Figure 3. IW diagram: passby, alignment and intercept.

possibility of any downhole problems. The risks identified with direct re-entry should be assessed relative to those involved with using an IW to establish the required isolation.

It should be noted that the ability to conduct P&A operations will almost always be better with a conventional well re-entry than it will be with an IW. Direct re-entry allows the use of conventional tools for diagnostics, cement placement, utilisation of full bore plugs and packers and the ability to confirm plug placement through application of weight and pressure testing.

Case study 1

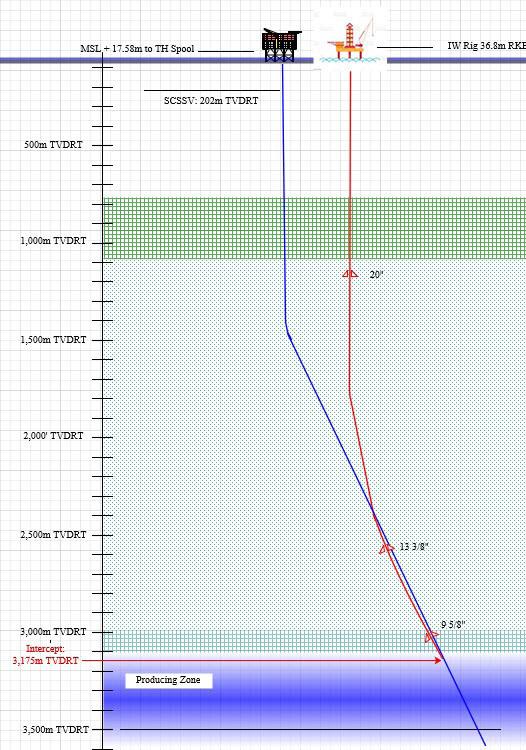

A new well was drilled on an offshore platform that already contained numerous other wellbores. There was an obstruction encountered immediately upon drilling below the 30 in. conductor. It was believed at the time that the obstruction was caused by a deformation near the bottom of the conductor. Under that belief, the solution was to use a mill to clear the conductor. After extensive milling, it was discovered that the obstruction was actually an adjacent well. Milling operations had penetrated into the adjacent well and severed the 4 ½ in. production tubing just above the surface controlled subsurface safety valve (SCSSV). The adjacent (damaged) well could produce several hundred barrels of oil per day with significant volumes of gas containing high concentrations of H2S.

Once the real situation was discovered, options for securing the damaged well were investigated. Once the extent of the damage was fully known, it became obvious that intervening directly on the well involved intolerable risks. If the SCSSV or the tubing below it was disturbed, there would be no chance of containing the surface pressure and a blowout would surely result.

The chosen solution was to install a very large diverter assembly with four overboard lines made up of 13 3/8 in. casing, then drill an IW to isolate the reservoir (Figure 1). The IW was successfully drilled using a semisubmersible rig that was positioned nearby but had to overcome serious collision avoidance issues in the crowded well environment. Penetration of the damaged well was made at approximately 8000 TVD. A window was milled in the 7 5/8 in. production casing and 4 ½ in. production liner which allowed a 2 3/8 in. cementing string to be introduced into the well (Figures 2 and 3). A 1200 cement plug was placed across the perforated section which was later tested using a well test arrangement that allowed an underbalance to be created above the plug. Surface intervention operations were then initiated to fully abandon the damaged well.

Case study 2

In another instance, an offshore well was scheduled to be P&A’d. At the beginning of the rig operations, it was discovered that the production tubing was parted at a very shallow depth and that there was no wellbore pressure integrity. Fluid pumped into the tubing from the top of the production tree was seen exiting from the conductor x surface casing annulus. Meanwhile, the SCSSV was thought to contain reservoir pressure at values approaching 7000 psi. Several direct intervention options were discussed including the removal of the parted tubing and tie back using high pressure pack off overshot. Ultimately the decision was made that the direct intervention was too risky without first isolating the reservoir.

A diverter assembly was installed on the target well and the IW drilling commenced from a JU rig. The IW, though challenging, was drilled without significant problems and an intercept was made above the production packer (Figure 3). As soon as the

production casing was penetrated, flow was observed at the target well platform as seawater was displaced to drilling mud. The well was stabilised and then the production tubing was penetrated. The lack of additional flow at the target well confirmed the integrity of the target well tubing.

Since the well had a downhole tubing hanger near the surface, the parted tubing did not drop into the well. This made it possible to create a window through the production casing and the 4 ½ in. tubing, and then introduce a 2 3/8 in. tubing string. A cement plug was placed across the perforations and into the tubing above the packer. The production tubing was then perforated, and an annular cement plug was circulated into place to enhance isolation (Figure 4).

Planning and implementation

Recognition of the growing importance of IWs is encouraging an increase in suppliers providing support for such operations. However, it is important when developing a plan for an effective intervention well to consider engaging with an experienced well control provider. An IW cannot be regarded merely as just another high-precision directional well. In many instances, there are underlying well control risks associated with an ageing well that require a fully-rounded plan from a well control company. Failing to recognise the different requirements of an IW from a standard high-precision directional well can exacerbate existing on-site problems.

Engineering, management, and design services are often required to ensure proper and comprehensive planning and oversight for the safe and successful execution of the intervention well plan.

Project planning will involve the supervision of drilling, testing, and completion operations. This will include the management of operator and service company non-routine technical support personnel. It will also involve the coordinated management of personnel and equipment for directional drilling and MWD, borehole surveying, homing in (electromagnetic ranging) and wireline, and milling and perforating.

Effective and accurate intersection management planning is also critical. This should include:

Ì Well trajectory planning and well construction.

Ì Well surface location selection.

Ì Target well and intervention well position uncertainty derivation.

Ì Ranging strategy (active, passive, and other methods).

Ì Intersection strategy.

Ì Hydraulic communication and kill strategy.

Ì P&A execution and verification.

A window into the future

An evolution from relief wells, intervention wells are increasingly becoming recognised as an effective solution in reducing the operational and safety risks associated with intervening on ageing wells. Intervention wells can be deployed to effectively de-risk planned surface operations and enhance P&A where direct well access is no longer possible. Alongside the benefits of new or improved P&A, intervention wells allow the verification of zonal isolation and can be an active enabler in the development of sites for carbon capture and sequestration.

References

1. WRIGHT, LW., and FLAK, L., Advancements in technology and application engineering make the relief well a more practical blowout control option.

Navigating the Depths of Oil and Gas Safety

Danny Constaninis, EM&I, Malta, explains how incorporating emerging technology with a desire to mitigate safety risk, reduce impact on operations, drive efficiencies and save costs will maintain the integrity of offshore hulls.

Maintaining the integrity of offshore hulls is playing a critical role in the energy business. Hulls age and get damaged, needing maintenance and repair for their planned life on station, often over 25 years. Below the waterline, inspection and repairs once meant dry dock, extensive and expensive out of service (OOS) time. More recently, diving operations reduced the need for dry dock, at the expense of safety, unwanted extra people on board and costly DSVs (dive support vessels).

But there are better, safer and proven alternatives that minimise OOS time and expense. The industry is conservative, and while these new methods are being adopted, faster take-up will bring the safety, OOS and economic benefits more quickly.

A progressive mindset

When operators, regulators and innovators work together, the identification of commonly agreed challenges and solutions progresses faster.

One industry group, made up of representatives of all of these elements, is the Hull Inspection Techniques and Strategy Joint Industry Project (HITS JIP) which celebrates its tenth anniversary, and looks back with pride on the outcomes of such collaboration. HITS is one of the longest operating such projects, initially part of the Global FPSO Research Forum, which is now re-focused and re-named as the Floating Energy Research (FER) Forum.

The collaboration has benefited from leadership and engagement from Energy Majors, owners and operators, the major Classification societies, innovative services providers, and representatives from academia and technical research.

At the outset, the JIP members agreed a series of objectives which would benefit the sector, mainly to mitigate the safety risk to humans. The first of these was to reduce the requirement for diver intervention, noting the inherent risk, and the significant financial impact of diving operations to inspect and repair FPSOs, particularly in hostile metocean conditions around the world.

The benefits of that collaboration, and the resulting technology and techniques have now expanded into asset integrity management of mobile offshore drilling units (MODU), floating gas production units including FLNG and FSRUs, and early engagement with floating renewable energy production stakeholders, particularly in floating offshore wind (FOW).

But do we really need to replace diving as a capability for asset integrity management in the floating energy production sector?

Understanding the risk

Professor Andy Woods, of the Institute of Energy and Environmental Flows at Cambridge University, in his 2022 work, ‘A Report on Fatalities in Commercial Diving’, presented sobering statistics, not just on the frequency of such fatalities, but also the human and commercial cost.

The outcome of that work must be that as alternative, diverless options for asset integrity management are available, owners and operators of floating energy production assets have an obligation, both moral and commercial, to their employees, subcontractors, shareholders and the public, to implement safer alternatives.

Complex problems with simple solutions

Maintaining hull integrity below the waterline, with minimal diving intervention, presents a number of challenges. For example, carrying out hull and critical sea valve and sea chest inspections that satisfy Class and regulatory requirements is no mean feat. Maintaining coatings and corrosion protection systems underwater is a further challenge, and that is without mentioning repair and replacement of essential equipment.

One challenge has been to provide an answer to ‘so what?’ from owners and operators who pointed out that a diverless inspection solution still needed diver intervention if repair or maintenance was required. This point meant that industry had to come up with diverless solutions for inspection, repair and maintenance. ODIN® diverless technology has been developed over the last decade as a means of reducing diver intervention, much of the innovations being in response to the direction of the HITS JIP.

Diverless UWILDs

UWILDs (underwater inspection in lieu of dry dock) have traditionally been carried out by divers, mostly in sheltered waters. There has been an unacceptable level of injury and fatalities particularly when these methods have been used on assets located offshore. Furthermore, weather related downtime

Figure 1. The HITS JIP.

Figure 2. A report on fatalities in commercial diving.

Figure 3. Launch of the integrity class ROV.

and failure to complete workscope is an inevitable feature of diver-based solutions in areas of high currents, swell and strong winds.

Replacing divers with ‘integrity class’ ROVs that can operate from the deck of the asset with a 3-person team, is proven and efficient. These ROVs are capable of ‘cavi cleaning’ surfaces for inspection and indeed maintenance, and carry NDT tools for thickness measurement, mooring chain measurement and cathodic protection readings.

Sea valves and sea chests are inspected from inside the hull using an ODIN Port. This device allows cameras and other tools to be inserted through a pipe so that the valve can be inspected during operation, with no OOS time; a more reliable inspection than a diver or ROV poking a camera through a grating some distance away from the valve or using a small diameter borescope through a strainer. A safer, more productive and lower cost solution that can operate in conditions that divers cannot.

Diverless sea valve and sea chest, inspection and repairs

The early diverless inspection benefit left operators hungry for more. Inspection and repair were just two elements of an underwater campaign, and if more of the underwater scope could be fulfilled, the safety, operational and commercial benefits increased.

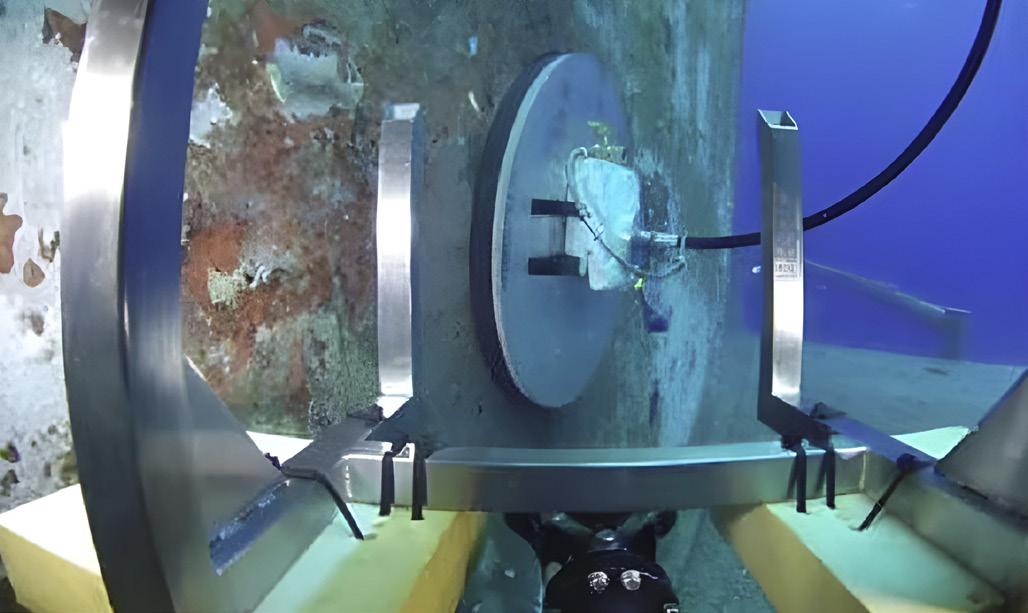

With this feedback and encouragement, ODIN diverless services were expanded to include blanking of the hull discharge lines (PLUGTM) and sea chests to enable diverless repair or replacement of sea valves (LIMPETTM).

PLUG technology is based on a double block seal created by an inflatable plug pushed inside the discharge line, backed up a secondary seal comprising a metal plate with a rubber faced seal.

LIMPET blanks are sealing plates, designed to fit and seal sea chest intakes. An integrity class ROV cleans the sealing surfaces of the sea chest and surrounds, then attaches lines to the LIMPET blank which is fitted with ‘intelligent’ remotely operated, proprietary winches, designed to draw the blank into place, and reinforce the hydrostatic pressure once the sea chest is internally drained. Once sealed by either PLUG or LIMPET, the lines are available for the safe removal and repair or replacement of the sea valves.

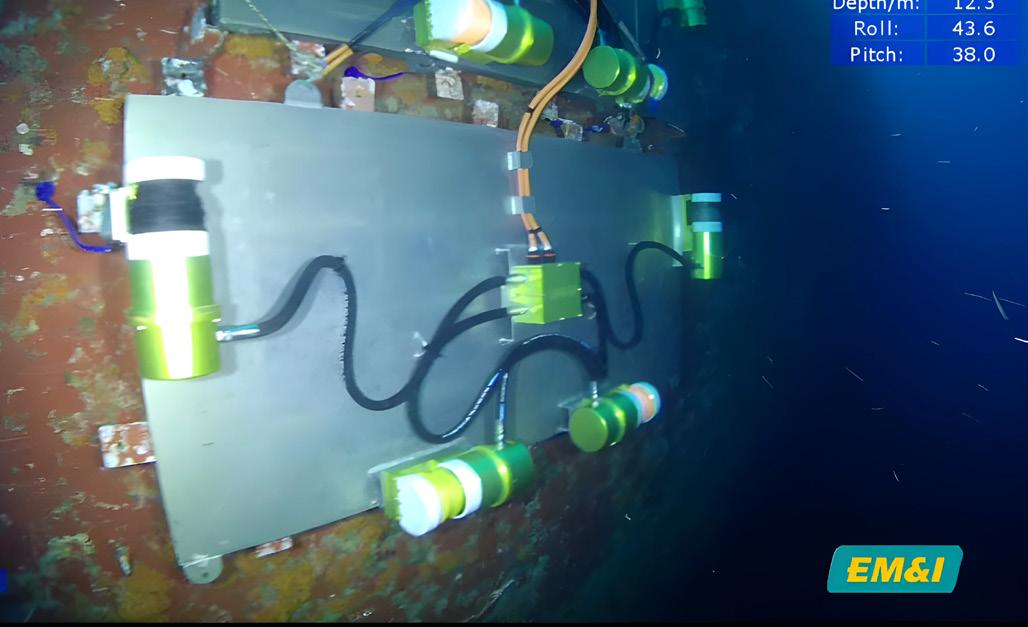

CLAMTM are custom made cofferdams, remotely attached and sealed to the hull to enable replacement of corroded, cracked or otherwise damaged steel hull plating. The design and installation of CLAMs (which can be as large as 5 m x 3 m to date), requires a new and higher level of engineering to ensure safe and effective deployment.

The hydrostatic and operating loads are significant and depth and swell dependent. Full finite element modelling is used to ensure adequate strength with a good safety margin, whilst keeping the weight of the cofferdam low.

Hull surfaces are far from flat, so laser scans are used to ensure the CLAM sealing face is a perfect match to the hull. Lowering a CLAM over the side and through the splash zone involves numerical modelling to define the weather and hull movement limitations.

All these things have to be taken into account for a successful project but the rewards are huge: no dry dock, continued production and safety.

Malaysian CLAMs

The operator of an FPSO offshore Malaysia faced a significant challenge with leaks in the hull, in locations that were below

the water line during normal operations, and therefore critical to the asset’s integrity. Several temporary repairs had been implemented, using cement boxes to stem the leak – these had been proven ineffective.

In addition to these temporary repairs, more permanent options were sought, and the traditional route of diver repair was explored. This led to unsuccessful campaigns and tragically, the death of another diver.

Following a series of mandatory surveys, a condition of class was imposed, and a permanent solution was urgently sought. For a sister vessel, this meant coming off-station, moving to a drydock to repair similar damage, and with that came significant financial penalties.

The owner was far sighted and searched for new options, including the CLAM diverless repair technology.

Figure 4. An ODIN access port.

Figure 5. PLUG overboard discharge isolation.

Figure 6. LIMPET blank in place.

This led to detailed discussions, review of previous projects and a contract to do the first of a number of repairs. A strong bond and technical understanding were developed between the client, the service provider, and critically, the Classification Society which had imposed the requirement for the repair. This collaboration and understanding included:

Ì An early site survey, including the laser scanning of the hull around the repair site to ensure the precise design of the cofferdam for optimal seal.

Ì Engineering liaison for the finite element analysis and numerical modelling.

Ì Design of the cofferdam (at 5 x 3 m, one of the largest deployed for such work on an FPSO globally).

Ì Approval of the engineering plan.

Ì Fabrication in South Africa, where the client visited once for progress, and secondly to witness the factory acceptance test, before approving the work plan for submission to Class.

Ì Both the service provider and the client liaising with Class for approval of that work plan.

Despite it being cyclone season, the repair team deployed to complete the repair within the deadline for condition of class. CLAM specialists, supported by local Malaysian technicians worked with the FPSO’s operator and attending class surveyor.

The first task was the removal of the temporary concrete repairs, followed by the installation of internal ODIN winches through ODIN ports for the cables to draw the cofferdam in to place, giving the double assurance of hydrostatic pressure to create the seal.

With the cofferdam travelling in two parts due to the size, first task on board was to assemble the CLAM cofferdam. With work continuing inboard, the cofferdam was deployed from the deck above the repair site which had been previously cavi cleaned by the ROV. Meanwhile, cables deployed through the ODIN access ports were attached to the cofferdam on the deck.

The team were able to monitor and guide the cofferdam installation using the integrity class ROV deployed for that purpose. The cofferdam was lowered into the area of repair, winched into place, drained and tested to confirm a complete seal.

Once the seal was assured the cropping and replacing of damaged plating was completed to the satisfaction of both the FPSO’s operator and the attending surveyor.

On completion of the steel renewal, the process was reversed, and the external face of the repair coated later, by rope access, when offloading brought the repair site above the water line.

The outcome of the successful project resulted in these comments from the vessel operator: “The crop and renew steel repairs were conducted behind the largest cofferdam ever built using marine grade Aluminium material, secured by ODIN technology, efficiently, effectively, and safely throughout. This was a first for underwater repairs in Malaysian waters, which was carried out based on precise engineering design, delivered on schedule, during rough weather in monsoon season…. As the operator, we understood the progress every step of the way; there was no impact to operations and production; and the integrity of the hull has been regained.”

Critically, all of the project on board was completed while the FPSO was conducting normal operations, therefore saving the significant cost and production implication of coming off station to go to drydock.

Where to now?

Building on the direction of the members of the HITS JIP, feedback from the market and a parallel exploration of technology available in neighbouring sectors, the scope of diverless services is expanding beyond the initial inspection, through CLAM, PLUG, and LIMPET.

New opportunities being explored include deeper inspection and cleaning of mooring systems with integrity class (as opposed to work class) ROVs; the replacement of depleted anodes on floating production units; and larger scale hull cleaning for asset integrity, all under the ODIN diverless technology ‘umbrella’.

So far, we have discussed diverless methodologies and their benefits. HITS however also mandates methods to be developed to avoid manned entry into confined spaces for inspection because traditional strategies create risks of confined space and working at height, a double jeopardy also the subject of a safety study by Professor Andy Woods of Cambridge University.

NoMan® methods combine remotely operated cameras, laser imaging, remotely operated UAV, to provide integrity data on the condition of tanks and other confined spaces.

Conclusion

Incorporating emerging technology with a desire to mitigate safety risk, reduce impact on operations, drive efficiencies and save costs will improve outcomes all round.

In the current context of the energy transition equation, reducing team size and improving that efficiency will reduce carbon emissions and play a noticeable part in the route to Net Zero.

Will the moral and commercial obligations be approached in a realistic, honest and effective way? The technology is available to support.

Figure 7. CLAM cofferdam preparation.

Figure 8. CLAM cofferdam attachment.

Leak remediation without the usual drawbacks

Alex Nicodimou, Welltec, Denmark, outlines an effective option for maintaining well integrity and optimising remediation operations.

Water shut-off and leak remediation typically involves the use of straddles or other wireline-set patches. The problem with these traditional methods is that they often result in a significant reduction in the tubing’s inner diameter (ID), and this reduction restricts the flow of oil and gas, leading to lower production rates and increased

pressure drops, which in turn necessitate higher pumping pressures and energy consumption. Additionally, the decreased ID can limit the access of downhole tools, complicating future well intervention operations. These traditional patches are also not straight forward to install, often leading to complex and time-consuming operations.

Furthermore, they may lack long-term durability, necessitating frequent and costly interventions. Overall, these limitations lead to higher operational costs, reduced production, and increased maintenance exposure and expenses.

But what if there was a more efficient way to fix the problem without significantly affecting the tubing’s ID, therefore avoiding all the usual knock-on effects of the repair?

Welltec® and Isealate AS have provided a downhole remediation solution with negligible impact on tubing ID, called the Isealate Springblade Patch.

How does it work?

The solution is e-line deployed for maximum efficiency, beginning its journey downhole as a pre-rolled laminate steel-sheet held under tension by shear clamps. This technique also allows for high expansion ratio patches and brings

the advantage of allowing subsequent patch-thru-patch deployments, i.e., patches already deployed do not interfere with future interventions. Once at the desired location and positioned across the damaged or leaking section of the tubing, a setting tool is activated, causing the laminate steel sheet to spring open and unravel, breaking the shear clamps and conforming to the tubing ID. Sealing is supported by a heat-activated resin, and each sheet deployed has only a 3 –5 mm effect on the ID.

The first commercial application

The Isealate Springblade Patch was first commercially utilised by an IOC operating in Northern European in October 2023.

The intervention involved a gas producer well with a 3 ½ in., 9.3 pounds per foot (ppf) tubing. A shallow leak had been detected just below the tubing-retrievable surface valve (TRSV) at the depth where the velocity string compression packer was set. This leak posed a threat to the well’s integrity, necessitating a robust and reliable solution to restore functionality and safety.

Specifications included the need for an ability to:

Ì Be set in a 2.992 in. diameter.

Ì Fit within a TRSV inner diameter (ID) of 2.75 in.

Ì Achieve a minimum ID reduction to 2.75 in.

Ì Withstand a collapse pressure of 100 bar.

Ì Endure a burst pressure of 180 bar.

The setting tool used for the operation had an outer diameter (OD) of 2.68 in., ensuring compatibility with the existing well infrastructure.

After running the patch and executing the setting procedure according to predefined protocols, a differential pressure of 180 bar was endured to confirm the structural integrity of the patch and tubing.

Furthermore, a multi-finger caliper (MFC) log confirmed that a minimal reduction in the tubing’s ID had been achieved, changing from 2.992 in. to 2.81 in., which translates to a loss of only 0.182 in.(4.62 mm), maintaining the well’s production capabilities and ease of future intervention – the client expressed satisfaction with the outcome.

The successful deployment not only resolved the immediate issue but also demonstrated the technology’s effectiveness and reliability. While production was halted to carry out the operation on this occasion, the well was brought back online within 24 hours of setting the patch. The communication

Figure 1. Deployment across damaged tubing – the new solution is e-line deployed for maximum efficiency.

issue between the tubing and ‘A’ annulus was fully resolved, eliminating the leak, and restoring the well to its optimal operational state.

Technical and economic benefits

The Isealate Springblade Patch has demonstrated capability to comprehensively avoid all the usual drawbacks and knock-on effects of traditional leak remediation, effectively ensuring well integrity.

Ì Production: minimal effect on ID means that flow is almost unaffected, maintaining production rates established prior to intervention.

Ì Pressure: with minimal effect on the tubing ID, flow efficiency and production pressure can be maintained.

Ì Future intervention: downhole access is maintained for future interventions, including patch-thru-patch deployments, i.e., repairs through and beyond previously set patches.

Ì Time and cost: fast and efficient e-line deployment, giving operators the opportunity to perform workovers and interventions without pulling the production tubing.

Ì HSE: regulatory compliance, avoiding potential environmental harm, cost-saving, and improvement to safety by reducing the need for extensive equipment handling and potential exposure to hazardous conditions.

A ‘minor’ but widespread problem

Due to various factors such as geological conditions, operational conditions, materials, design, and old age, the reality is that ‘minor’ leaks in production tubing are a common problem,

where corrosion or other damage leads to unwanted issues like water production/ingress, or loss of integrity.

As a ‘minor’ but widespread problem, a fast and efficient solution with a minimal footprint is ideal, and this can be achieved via lightweight e-line deployment of the Isealate Springblade Patch.

Well integrity management

Since the first successful application in Northern Europe, field trials have been ongoing, with multiple Isealate Springblade Patches set in a range of different scenarios in Alaska. These have included:

Ì Remediation of a tubing connection leak in a gas producer.

Ì Remediation of a connection leak in an oil well.

Ì A novel use of a set patch acting as a TRSV hold-open sleeve inside the flow tube, holding the TRSV flapper open while running another patch through the area to remedy the leak below.

Conclusion

The solution represents an advancement in leak remediation technology for the oil and gas industry. By minimising the reduction in tubing ID, it helps ensure that production rates and pressure efficiency are maintained while allowing for future interventions without complications. Its e-line deployment method is both time-efficient and cost-effective, reducing the need for extensive equipment handling and enhancing safety. The successful application of this technology in Northern Europe and ongoing field trials in diverse scenarios underscore its reliability and versatility, making it an effective option for maintaining well integrity and optimising remediation operations.

Brandon Rosler and John Alvarado, Nabors Drilling Solutions, USA, explain how integrating automation in daily operations is allowing drilling contractors of all sizes to realise greater efficiencies.

As energy companies continue to raise the bar on well cycle times, they are now approaching both the rig equipment and human factor technical limits. In this current landscape, drilling contractors are responding by developing and integrating advanced automation technologies that are positioning them to meet the most formidable challenges head on.

The winds of change

A decade or so ago, drilling contractors were able to achieve significant efficiencies by capitalising on the skills of a seasoned workforce with intimate knowledge of the rigs they crewed. As these more experienced personnel reached retirement age and began exiting the workforce, it became more difficult to attract new workers. Part of the reason was the misperception that the oil and gas industry is antiquated in terms of technology and disinterested in environmental issues. Another contributing factor is the inherent difficulty of the work and the perception that drilling operations take place in relatively inhospitable, isolating environments.

In the face of these challenges, drilling contractors are trying to answer the question of how to maintain and improve drilling performance with less-experienced personnel in a more transient work environment. In the absence of experienced workers passing on their expertise to the next generation, drillers have to figure out not only how to achieve the same level of performance, but also how

to extend proficiency and consistency across an entire fleet of rigs irrespective of the experience and skill level of the crew. The answer is automation.

Tapping into advanced technology

The long-term viability of drilling projects depends on the ability to safely operate efficiently and consistently. With this goal top of mind, drillers took a step back to reassess the drilling process, and instead of focusing solely on workforce issues, they began examining drilling processes to identify ways to streamline them through automation with the goal of reducing the well cycle time, achieving fleet consistency, and improving adherence to procedures. It became evident that integrating process and machine automation could resolve challenges they were facing while also improving drilling performance.

For Nabors, that journey began nearly 15 years ago. Focusing initially on the Nabors fleet, engineers began looking for ways to improve rig efficiency and execution. Realising automation could deliver a higher level of efficiency and performance and also reduce exposure to higher risk activities for workers, the company concentrated on technologies that would enable the transition to automated drilling.

The first step was to evaluate the existing rig operating systems (ROS). Finding none that was appropriate for full automation, engineering designed a system with a machine layer and a flexible sequencing engine that would allow the drilling process to be tailored to specific field requirements and accommodate different equipment components. With this capability, the system could deliver consistent performance without being restricted to a rigid process or workflow, and by designing it as an agnostic system, engineers ensured that it would have the broadest range of applications. This laid the groundwork for the intelligent SmartROS® rig operating system which contributed to a fully automated robotic land rig that became operational in 2021.

The company continued to develop additional automation technology to further enhance their portfolio, including an automated directional guidance and execution system that incorporates anticollision software and automated rotary steerable downlinking achieving consistent directional decisions. This automation technology adjusts to unexpected changes in the formation and improves performance by reducing overall cycle time. The result of this technology development has been transformational.

Technology at work

Applying advanced drilling automation software creates execution consistency to reduce connection times and unplanned trips by following automated workflows/recipes and implementing best practices.

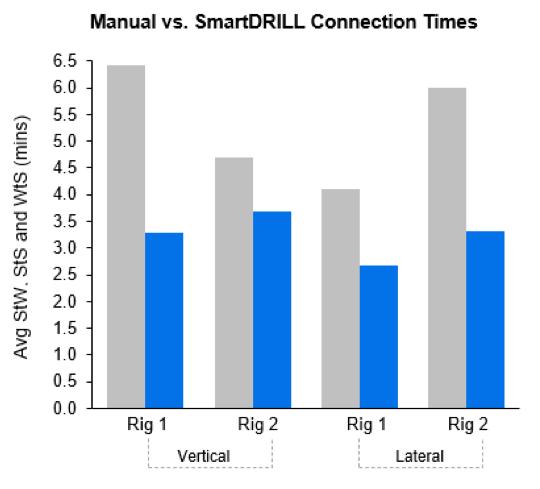

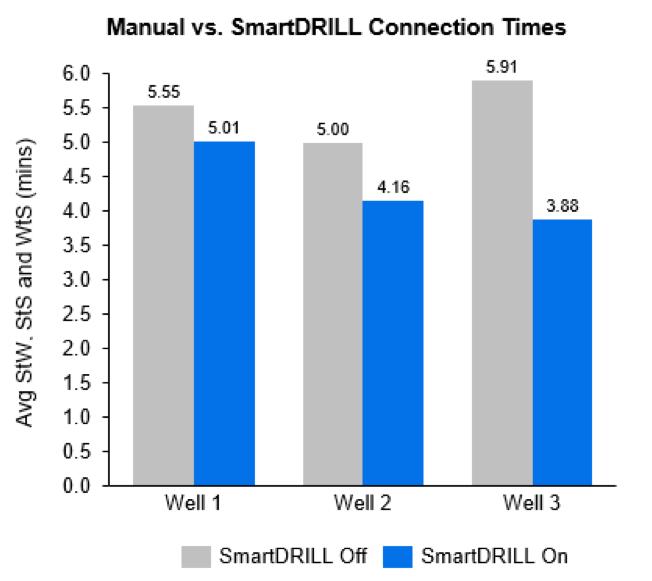

Recently, this technology was deployed on two rigs and delivered well-over-well connection performance improvements that cut weight-to-weight connection by 2.09 mins with an average utilisation of 93%.

Another automation solution was designed to mitigate torsional vibration that causes stick-slip and can damage cutters on bits, slow the rate of penetration (ROP), damage motors and downhole equipment, and cause drill pipe fatigue and failure. This technology automatically changes boundary conditions to expand the efficient drilling window enabling better bit engagement resulting in a higher overall average ROP with minimal stick-slip. Live data tracking illustrates how the technology senses and responds to downhole conditions to optimise performance.

Figure 1. Illustrates the average weight-to-weight connection times the two rigs saw when using manual operations vs SmartDRILL® automation technology.

Figure 2. Shows an independence contract drilling (ICD) Rig 304 operating in West Texas.

A more recently introduced technology is rig floor automation, known as redzone robotics (RZR), so named because it delivers consistent performance without requiring workers in the red zone. The RZR rig floor automation module integrates with the SmartROS® rig operating system to enable complete control of the rig floor from the drillers cabin. The technology includes a fully autonomous triple racking tubular handling system with electric axes and a hydraulic gripper that execute completely hands-free pipe handling. The tubular handling system automatically builds stands of pipe online and offline, and its modular and scalable design makes it suitable for installation on any AC rig and enables connection to advanced rig controls through the ROS.

This technology was deployed and continues to work in West Texas to determine how well drilling operations can be executed with no one on the rig floor to carry out normal connection, tripping and racking procedures.

The system proved its viability as the rig was put through its paces, tripping pipe and racking it and flawlessly making and breaking connections. The results showed a significant improvement in flat time as well as increased productivity from workers, who otherwise would have been actively executing drill floor functions. At the same time that the RZR technology improved safety, it also contributed to improved margins and days vs depth for more cost-effective operations.

3. Illustrates the average weight-to-weight connection times across three wells when using manual operations vs SmartDRILL® automation technology.

Furthermore, this programme made it clear that instead of eliminating jobs, automation is actually allowing people to be put to better use, carrying out functions that require different skills and using their time to conduct maintenance work or prepare for the next operation on the rig.

The hope is that automating onerous tasks will not just streamline operations but also lead to higher employee retention by allowing equipment to perform exhausting, labour-intensive work instead of requiring workers to put in demanding 12-hour shifts on the drill floor. It is even possible that this advancement in technology could open the door to a broader group of potential employees who do not have the physical capacity to perform arduous work in the traditional way.

Partnering for success

A look at the US land rig count illustrates how the fleet and the industry are changing. In December of 2003, there were 1022 active rigs. In April of 2024, there were 619. Despite the dramatic decline in the number of rigs, production increased. According to the U.S. Energy Information Administration, onshore daily oil production in the United States averaged 5650 barrels in 2003. At the end of 2023, when there were 403 fewer active rigs, average production was around 12 928 bpd. Some of this increase can be attributed to human factor efficiency gains, but much more of the increase is the result of technology advances that are streamlining the drilling process and enabling automation technologies.

As technology evolves and alters the face of drilling operations, it also is inexorably changing the culture and the character of the industry. The historically competitive landscape is giving way to a more cooperative environment in which efficiency gains can be realised on a much larger scale.

One of the drivers behind this shift is the understanding that access to cutting-edge technologies can elevate performance across the industry, enabling all companies to achieve more exacting environmental and operational performance standards. This is particularly advantageous to smaller drilling contractors that have neither the expertise nor the financial ambition to develop advanced technology on their own.

Independence contract drilling (ICD) recently made the move to incorporate automation technology and worked directly with Nabors to install advanced systems on its rigs in executing a programme it calls ‘ICD Impact.’ The goal of the programme is to take advantage of automation technologies that can be installed without a large up-front cost and without significant disruption to operations.

ICD elected to work with Nabors in part because of their efficiency and outcomes. Another driver for this decision was the fact that the installation could be done during a rig move, which meant not only that there would be no disruption to operations, but that the new technology could be put to work immediately on the designated drilling programme. Furthermore, if ICD were unhappy with the results, removing the equipment would be equally straightforward due to the minimal footprint and no major control system modifications.

Installing the SmartROS® platform along with the SmartDRILL® application to reduce vibrations achieving measurable improvement, including 34% reduction in weight-to-weight connection time, 24% savings in overall average connection time, and 91% utilisation by the time ICD drilled its third well in this drilling programme.

These successes led the drilling contractor to install REVit® advanced top drive automation technology later in the year on an East Texas rig, where the company achieved immediate performance improvements. In this drilling programme, stick-slip was reduced by 62%, overall ROP increased by 9%, and the total number of days was reduced by 42%.

These results illustrate the value of automation and perhaps more significantly, prove that partnerships that were inconceivable within the drilling contractor community in the past could become commonplace in the future.

Looking down the road

Advanced technologies are delivering drilling efficiencies and decreasing well cycle times, and ongoing investment in R&D will continue introduce solutions that increase production while reducing the carbon footprint of operations.

Figure

Mike Aughenbaugh, Swagelok, explores the distinctions between pitting corrosion and crevice corrosion.

Stainless steel components may degrade over time when they are exposed to internal and external factors that cause corrosion, which can cost facilities significant time and money. Deteriorated parts may require repairs or replacement, either of which can result in unplanned downtime for the system involved (Figure 1).

According to the National Association of Corrosion Engineers (NACE), corrosion can cost offshore and nearshore facilities more than US$1 billion each year. Fortunately, several simple solutions exist that can mitigate or eliminate the problems before they become insurmountable for oil and gas companies.

Before specific identifications are made, teams must understand what causes corrosion and what steps they can take to prevent it from worsening and putting the fluid system at risk

of failure. Then maintenance teams should identify which kind of corrosion is harming their fluid systems by learning and understanding what sets the different types apart. Once a complete understanding of which corrosion is affecting a system is reached, then teams can take action.

Why stainless steel corrodes

Almost every metal in the world can corrode under certain conditions, but the harsh conditions of oil and gas applications present specific challenges especially for offshore installations.

Corrosion results from electrochemical reactions and oxidation (loss of electrons) at an anode, or reduction (gaining of electrons) at a cathode (Figure 2). A common example is iron tubing, which may oxidise and release two electrons. Water introduced to the system can cause the iron to dissolve into Fe 2 positive ions. At the same time, the electrons may cause a reduction reaction, changing dissolved O 2 into OH-, a negatively charged hydroxide ion.

Susceptible metal tubing can be found in analytical and process instrumentation, hydraulic lines, and control and utility applications in the oil and gas industries. To avoid initial corrosion damage, most systems are designed with stainless steel that has a minimum of 10% chromium in its composition. Sufficient chromium levels induce the creation of an oxide layer that helps slow or even prevent corrosion. Even the strongest stainless steels can succumb to corrosion if environmental conditions destroy that oxide layer. Without that layer, corrosion reactions may proliferate quickly.

The two most common corrosion types facing the oil and gas industry are pitting corrosion and crevice corrosion.

The differences between pitting and crevice corrosion

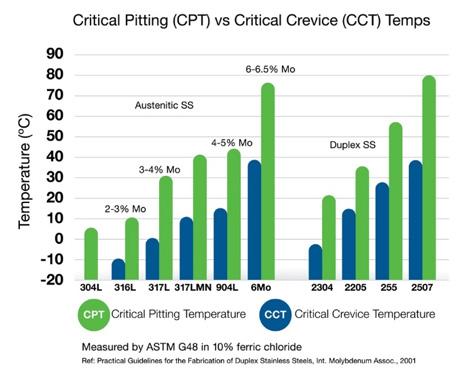

At many oil and gas facilities, several corrosion types may happen simultaneously and destroy entire fluid systems in the process because of the operation environment, materials used, and process fluids. The two most common forms of stainless steel corrosion are pitting corrosion and crevice corrosion (Figure 3).

Pitting corrosion

Pitting occurs when the chromium layer is destroyed over time, leaving the bare metal underneath unprotected. When the bare metal is exposed to corrosive solutions, damage will occur. Typically, the damage takes the form of small cavities, commonly known as pits.

Visual inspection may reveal the beginnings of pitting corrosion, but the amount of lost material underneath the surface can silently undermine a pipe’s performance. In the worst-case scenarios, pitting corrosion can perforate tube walls and result in costly leaks. Left unaddressed, pitting corrosion can lead to cracks in components under tensile loads. If the environment contains high levels of chloride (CI-), such as seawater hitting offshore drilling platforms, pitting corrosion is even more likely, especially if high temperatures are involved.

A clear signal that pitting corrosion is occurring is reddish-brown iron oxide deposits on the surface as well as the beginnings of actual pits. If CI-bearing water like seawater pools and evaporates, the remaining solution will become even more corrosive. Keep upward-facing surfaces clear of

Figure 1. Facilities can consider components in their fluid systems made from 316 stainless steel, whose chromium levels provide extra protection against the damage corrosion can inflict.

Figure 2. Both pitting and crevice corrosion begin when the oxide layer on the outside of the metal surface breaks down and creates space for corrosive materials to do damage.

Figure 3. Pitting corrosion (left) and crevice corrosion (right) represent significant risks to offshore oil and gas fluid systems. Facilities should make sure their teams are equipped with the knowledge to identify, repair, and prevent either type of corrosion.

standing water to prevent CI-induced pitting corrosion.

Crevice corrosion

The cause of crevice corrosion is similar to pitting corrosion, meaning that the oxide layer has broken down. What makes crevice corrosion more insidious is that it rarely happens in plain sight. Instead, as the name implies, it occurs in crevices, making it more challenging to find and prevent. Additionally, the wide and relatively shallow pits that occur in crevice corrosion only grow once the process has begun. In most fluid systems, crevices are created between tubing and tube supports or clamps, between adjacent tubing runs, and under dirt and deposits that have collected on the surface.

No matter how clever the design, crevices will inevitably happen. The tightest crevices pose the single greatest danger to the integrity of the system’s stainless steel components. Crevices are particularly problematic in offshore applications because seawater can diffuse into the crevice without access to an outlet. The resulting chemically aggressive environment does not allow corrosion-causing ions to come back out, leaving the entire surface susceptible to rapid corrosion.

4. Critical pitting temperatures (CPT) and critical crevice temperature (CCT) are important values used to determine which materials will best resist corrosion in harsh operating environments.

Additionally, crevice corrosion often stays hidden until a tubing clamp is removed, leaving it potentially undetected for long periods of time. Unlike pitting corrosion, crevice corrosion occurs at lower temperatures because it is easier to create a pit beneath a tube clamp or other such device.

Keeping corrosion from occurring