Annual subscription: UK £270, all other countries £292. For two year subscription: UK £510, all other countries £527. Airmail prices on request. Single copies £50 Digital subscription: (6 issues). 1 year: £259. 2 years: £414. 3 years: £544. Single issue: £35

ALUMINIUM INTERNATIONAL TODAY is published six times a year by Quartz Business Media Ltd, Quartz House, 20 Clarendon Road, Redhill, Surrey, RH1 1QX, UK. Tel: +44 (0) 1737 855000 Fax: +44 (0) 1737 855034

Email: aluminium@quartzltd.com

Aluminium International Today (USO No; 022-344) is published bi-monthly by Quartz Business Ltd and distributed in the US by DSW, 75 Aberdeen Road, Emigsville, PA 17318-0437. Periodicals postage paid at Emigsville, PA. POSTMASTER: send address changes to Aluminium International c/o PO Box 437, Emigsville, PA 17318-0437.

10 Bauxite Boom: Responsible mining for People and the Planet

HEALTH & SAFETY

13 Quick to Forget

FOCUS ON CHINA

16 An insightful Keynote

DIGITALISATION

20 EGA: A Digital Future

22 The Unified Namespace for Digital Transformation in the Industry

AUTOMOTIVE

25 Alumobility: Further Lighthweighting the Porsche Taycan

HYDROGEN

27 Hydrogen in the Aluminium Industry

DECARBONISATION

34 European Aluminium Calls for a Real Industry Decarbonisation Deal

36 Aluminium Industry DecarbonisationA Turning Point?

Coming to a close

Welcome to this special digital highlights issue, which features a round-up of popular news, articles and interviews from the past year.

I look to the 2023 editors’ note for inspiration to write this; I’ll begin by quoting: “While the world remains an uncertain and turbulent place, the day-to-day duties and fastpace of innovations, technical advances and general developments across our industry have resulted in one of the busiest and most content-rich years I have seen in my time as an Editor.” – Nadine Bloxsome 2023. Looking back on 2024, this quote is still relevant.

The world has faced unprecedented challenges such as geopolitical tensions and numerous climate disasters. After reflecting upon 2023, the doomsday clock was once again set to 90 seconds to midnight (after moving to this position in 2022). I wonder how close to midnight we will be for 2024?

But despite the several challenges set in front of us, the industry has maintained its commitment to progressing forward.

The aluminium industry has announced new partnerships, investments, projects, and findings that continue to evolve and improve the industry, highlighting the industry ‘s commitment to innovation and sustainability.

This issue has, hopefully, captured the positives of 2024, despite the challenges.

I hope you have enjoyed all the issues brought to you over the past year. Wishing you and your loved ones a Happy New Year!

Ma’aden and Hexagon Partner

Ma’aden and Hexagon have announced their partnership to launch the Middle East’s very first digital mine.

Hexagon’s life-of-mine technology solutions are being successfully deployed at Mansoura Massarah mine, combining sensor, software, and autonomous technologies to enhance efficiency, productivity, quality and safety across the mine’s operations.

Duncan Bradford, Executive Vice President Base Metals and

New Metals, Ma’aden, said: “This partnership strongly aligns with our digitisation strategy, as we work to use the vast amounts of data that we mine to make our mine safer and more efficient. We look forward to working closely with Hexagon to implement and utilise the region’s first digital mine to elevate Mansourah Massara’s operations.”

Nick Hare, President of Hexagon’s Mining division, said: “We are excited to help bring to life

this important shift toward digitisation of the mine, one that holistically leverages intelligent data and automation across workflows to minimise the impacts of mining while simultaneously improving safety, productivity and operational efficiency. This is about co-authoring the next chapter of mining in this region with a partner who shares in our drive toward a sustainable future.”

Novelis Doubles Capacity in UK

Novelis Inc. has announced it is investing approximately $90 million to increase recycling capacity for used beverage cans (UBCs) at its plant in Latchford, UK. The project will increase the facility’s recycling capacity for UBCs by 85 kilotonnes per year, equaling a growth of more than 100%.

“Of all the recycling players in the European market, Novelis has the highest ambition to maximise its recycled content across our product range,” said Emilio Braghi, executive vice president of Novelis and president, Novelis Europe. “Globally, Novelis had an average of 63% recycled content in our products in fiscal year 2024. This investment marks a

major milestone in our ambitious program to further expand our recycling capacity. It underscores

our strong commitment to sustainability as we continue to drive

the transformation of the aluminium industry towards full circularity and lead the market with innovative, high-recycled and low-carbon aluminium solutions.”

The investment includes the construction of a new dross house, three new bag houses, and the installation of state-of-the-art shredding, sorting, de-coating, and melting technologies. The expansion of recycling capacity, as well as the implementation of advanced technologies, will result in an annual CO2e reduction of more than 350,000 tonnes for Novelis Europe.

The project is expected to begin commissioning in December 2026.

Industry Reports Decline in Emissions

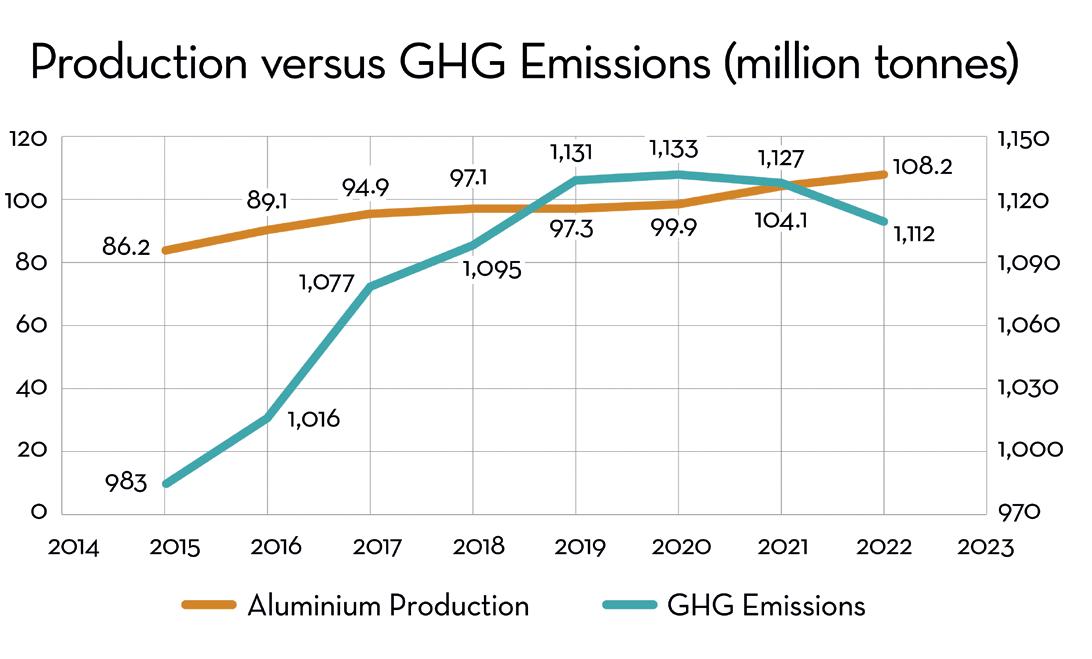

New data from the International Aluminium Institute (IAI) reveals that, for the first time, total greenhouse gas emissions from the global aluminium sector did not grow, even though aluminium production grew.

The 2022 data shows aluminium production grew by 3.9% from 104.1 million tonnes to 108.2 million tonnes. However, greenhouse gas emissions from the industry showed a slight decline from 1.13 giga-tonnes CO2e to 1.11 giga-tonnes CO2e, and the GHG emissions intensity of primary aluminium production

(the average quantity of emissions from the production of a tonne of primary aluminium) has been declining since 2019. In 2022, intensity declined by 4.4% from 15.8 tonnes CO2e per tonne to 15.1 tonnes CO2e per tonne.

IAI Secretary General Miles Prosser said: “Our challenge is to reduce emissions while growing production.”

He continued: “The 2022 data shows the effectiveness of work by the aluminium industry to reduce the emissions intensity of production. While much remains to be done, 2022 was the first year that

these intensity reductions offset production growth.

“The transformation needed in the industry to meet global climate targets is much bigger than the early changes we are witnessing. Emissions reductions must be deeper, faster and more widespread, but for the first time, we can talk about heading in the right direction. If we continue to see investment and implementation of low-carbon energy sources and GHG reduction technologies, 2021 could be the year that GHG emissions from the aluminium industry peaked.”

Industrial- scale Demo of ELYSIS™

Alcoa Corporation has announced further progress on ELYSIS™ technology with Rio Tinto’s plans to launch the first industrial-scale demonstration of the breakthrough technology, which eliminates all greenhouse gas (GHG) emissions from the traditional smelting process and produces oxygen as a byproduct.

William F. (Bill) Oplinger, President and Chief Executive Officer of Alcoa Corporation commented, “we are proud to progress the technology initially developed at our technical center to its next phase within the ELYSIS™ partnership. Aluminum plays a critical

role in the world’s energy transition and decarbonisation efforts; with the ELYSIS™ technology, the smelting of this important metal

can also be done without direct carbon emissions.”

To support the industrial demonstration, Alcoa will man-

ufacture the proprietary ELYSIS™ anodes and cathodes at ATC, which will include installing and operating new equipment. Alcoa anticipates benefitting from the learnings of this phase of the demonstration and expects to apply them to future phases in ELYSIS™’s development. Metal produced through the ELYSIS™ process will further improve upon Alcoa’s lower carbon products already on the market, such as the Sustana™ product line.

Rio Tinto has announced it will be installing carbon free aluminium smelting cells using first ELYSIS™ technology licence.

Transforming to a Circular Economy

Speira is investing 40 million euros for additional recycling capacity to drive the transformation of Rheinwerk and achieve a total saving of up to 1.5 million tonnes of CO2 per year at the site.

Boris Kurth, Head of the can business at Speira as well as the recycling and foundry operations at the Rheinwerk stated, ‘over

the past 20 years, we have already built furnaces with leading recycling capacity in Europe and Europe’s most modern sorting plant for UBC scrap, substituting the highly energy-intensive primary production of aluminium. We are consistently pursuing this path and emphasising our commitment to the circular economy with the fourth recycling furnace at Rheinwerk.’

The furnace will be built in 2025. Production is scheduled to start at the beginning of 2026. Speira is also converting the third of four existing casting centres to be optimised for recycling alloys. This will enable Rheinwerk to further reduce its ecological

footprint. Overall, Rheinwerk will then have a recycling capacity that will save up to 1.5 million tonnes of CO2 compared to primary production of the same quantity of aluminum.

The new furnace and the remodelling of the casting plant are step one that will be followed by others.

One third of the phased-out smelter will be home to the new scrap warehouse. This will provide storage space and facilities for sampling incoming scrap and preparing it for melting.

The new recycling furnace will be used to melt aluminium alloys that are processed into beverage cans after rolling.

Alba and EGA Sign Agreement

Aluminium Bahrain B.S.C. (Alba) and Emirates Global Aluminium (EGA) announced the signage of a Technology Services Agreement for Alba’s Reduction Line 6. The agreement encompasses both onsite and remote assistance wherein EGA will provide Alba with technical support services, monitoring services as well as operational consultation. The agree-

ment also covers operational and process audits, technical training workshops, as well as hands-on operation support among others.

Alba’s CEO Ali Al Baqali stated:

“We are excited to build on our partnership with EGA through this technical services agreement as it will enable our human talent to continuously benefit from EGA’s DX+ Ultra advancements and

achieve our sustainability objectives.”

Abdulnasser Bin Kalban, Chief Executive Officer of Emirates Global Aluminium, stated: “EGA’s longstanding partnership with Alba reflects the vision of our wise leadership to deepen the dynamic relations between our two countries.”

Constellium to deploy low to zero carbon technology

Constellium have announced that its facility located in Ravenswood, West Virginia, was selected by the U.S. Department of Energy Office of Clean Energy Demonstrations to begin award negotiations for up to $75 million as part of the Industrial Demonstrations Program (IDP). This investment will support the installation of low-emissions SmartMelt furnaces that can operate using a range of fuels, including clean hydrogen.

Century Aluminum to Build New Smelter

Century Aluminum Company was selected by the U.S. Department of Energy Office of Clean Energy Demonstrations to begin award negotiations for up to $500 million to build a new aluminum smelter. With the help of this funding, Century plans to build the first new U.S. primary aluminum smelter in 45 years. The smelter would double the size of the current U.S. primary aluminum industry.

Constellium receives grant to increase casting capacity

Constellium announced that its facility in Muscle Shoals, Alabama has been selected by the U.S. Department of Defense for an investment of $23 million to rebuild its Direct Chill aluminium casting centre. Constellium will use the funds to install state-of-the-art casting equipment on the site of a dismantled casting center intended to add up to 300 million pounds of annual casting capacity.

Aluminium Duffel: New Milling Installation

Aluminium Duffel announced the start-up of their new milling installation, an investment worth €26 million. The milling installation has a capacity of no less than 400,000 tonnes of aluminium per year.

A milling installation provides the top and bottom of an aluminium rolling block with a cleaner surface by removing or milling a layer. This is necessary to continue the rolling process. Until now, an amount of the slabs were

milled in the former sister company in Koblenz.

“Our widest slabs, which are essential for our customers in the automotive sector, are now milled in-house, which gives us more independence. Thanks to the high-tech properties of the installation, we can make the milling process more sustainable, an important step towards our environmental goals. In short, in this way we continue to invest in a sustainable future for our company, for our people and for our environment,” says Koen Libbrecht, General Manager at Aluminium Duffel.

The new logo, which is shaped into a heraldic shield, aims to reflect the company’s core values: Change & Courage, People & Power, and Excellence & Teamwork.

“The new brand identity and logo are a promise to our customers and stakeholders and a tribute to our strong team. Every employee is a hero who contributes to our success and future every day. In recent years, we have experienced several acquisitions and defied the energy crisis. Thanks to our team, we got through this period well. There is no better way to honour this than with a strong symbol,” says Koen Libbrecht.

Alcoa to Supply Nexans

Alcoa have announced that it will supply global cable producer Nexans with aluminium produced from ELYSIS™.

Nexans will be the first cable manufacturer to use metal from the ELYSIS™ process.

Several Nexans facilities in Western Europe and Scandinavia will use aluminium produced from the ELYSIS™ process to start qualifications for the metal’s use in various types of cables, from low, medium to high voltage.

This latest announcement further builds on the two companies’ historic long-term relationship.

Since the launch of ELYSIS™ in 2018, the technology company has produced R&D quantities of the metal. Alcoa is marketing and selling its share of the ELYSIS™ metal, which has also been used for the wheels on the Audi eTron GT. Apple is also an investor in the technology and has used ELYSIS metal for some of its products.

Renato Bacchi – Executive Vice President and Chief Commercial Officer at Alcoa stated, “Alcoa is well positioned to supply low carbon aluminium for the world’s transition to renewable energy, as we know that the true impact of decarbonisation will also include the choice of materials used to build the infrastructure for generation, transmission and distribution networks. While we are developing ELYSIS™for the future, we are also supplying low-carbon aluminium today with our EcoLum™metal, which can help customers meet their own sustainability goals and lower their carbon footprints.”

Vincent Dessale – Nexans Chief Operating Officer Senior Executive VP commented, “In the fight against climate change, solutions that support the world’s energy transition make a real difference. By increasing our use of low-carbon aluminium, we want to lead the way toward a sustainable electrification of the world: the rod produced with this breakthrough technology could eliminate a significant portion of carbon dioxide emissions in the future. We are proud to be the world’s first cable manufacturer to use metal from the breakthrough technology ELYSIS™.”

Alunorte Production Using Natural Gas

Hydro Alunorte alumina refinery has started using natural gas in alumina production, replacing fuel oil. When fully completed, six steam generation boilers and all the refinery’s calciners will operate on natural gas.

The R$1.3 billion investment to replace fuel oil with natural gas at Hydro Alunorte alumina refinery will reduce the refinery’s carbon emissions by 30 percent. The fuel switch project is a key step in Hydro’s climate strategy and global commitment to reduce Hydro’s greenhouse gas emissions by 30 percent by 2030.

Alunorte has an expected annual natural gas consumption of 29.5 Tbtu. When the transition from fuel oil to natural gas is completed, the change in the energy matrix at Alunorte will reduce the refinery’s annual CO2 emissions by 700,000 tonnes.

Significant changes have been made to the refinery’s operation to make this transition possible, with focus on automation and process safety.

“We have implemented the most modern technologies available for using natural gas in

our alumina production. We are proud of our contribution to fulfilling Hydro’s decarbonization commitment,” says John Thuestad, Executive Vice President for Hydro’s Bauxite & Alumina business area.

The natural gas used in the process is delivered to Alunorte via a floating storage and regasification unit (FSRU) and import terminal operated by New Fortress Energy. The project replacing fuel oil with natural gas at Alunorte has been an enabler bringing natural gas to Pará and to other projects in the region.

Event Review: Future Aluminium Forum

The Future Aluminium Forum took place between the 22nd – 23rd May in Istanbul, Turkey. The event saw key players and experts come together to discuss innovative technologies pushing the industry forward to a developed future.

“Future aluminium is all about sustainability”- Erol Metin, Advisor to the Board of Directors, Talsad

Commenting on the event, Nadine Bloxsome, Former Editor, Aluminium International Today said:

“I am pleased that we were finally able to host the Future Aluminium Forum in Istanbul, after having planned this before the COVID pandemic. In collaboration with the Turkish Aluminium Industrialists Association (TALSAD) and various stakeholders, the event showcased the latest advancements in digital manufacturing and Industry 4.0 technologies, promising to revolutionise production processes and elevate quality and sustainability standards within the industry.

“We are delighted to report that the Future Aluminium Forum was exceptionally well-received by all delegates and sponsors alike. Their enthusiastic participation

and positive feedback underscore the importance and relevance of the topics discussed at the event.

The Turkish Aluminium Industry “Turkey’s strategic geographic location and thriving aluminium industry provide the perfect backdrop for this regional event. With its steady growth and significant contributions to the global aluminium market, Turkey serves as a hub for both regional and global players, offering a dynamic environment ripe for exploration and collaboration.” – Nadine Bloxsome

Erol Metin, Advisor to the Board of Directors, Talsad, kickstarted the event with his keynote presentation. Breaking down the Turkish aluminium market, he discussed its position in the global market.

Turkey has:

� 1 smelter

� 18 Wrought aluminium producers

� 22 rollers, plate manufacturers

� 122 extruders

� 14 wire and cable manufacturers

� 28 packaging manufacturers

Commenting on the industry growth in turkey, he reported that Turkey’s imports and exports of aluminium have

doubled over the last 10 years. Despite a 14% reduction in exports in 2023, Metin remained positive with regards to the Turkish aluminium’s future. He observed that the reduction was “mainly due to slow down in main export markets such as the EU and US.”

Moving onto decarbonising the Turkish aluminium industry, he said that “total CO2e emissions from Global Aluminium Industry must come down from 1.1 GT/ year to 250 Mt/year; i.e 80% reduction.” In face of this challenge, he came forward to present the audience with an industry roadmap designed for the Turkish industry. The roadmap focused on decarbonisation of electricity with renewables; shifting to electric furnaces; and carbon reductions in the supply chain. He also noted the importance of National Initiatives, and utilising these to the industries advantage.

“The total carbon footprint of Turkish aluminium industry is estimated to be in the range of 22-28 million tons per year,” said Mr Metin.

Looking further into decarbonising the industry he homed in on the key issue, that “86% of total Carbon budget of Turkish aluminium is due to footprint of primary aluminium imports 18-19 Mt CO2 embedded (scope 3) emissions.”

Metin went onto state the importance of assessing each part of the production chain and finding personalised solution for decarbonising each aspect.

Metin concluded his overview saying, “Overall significant shifts yet to evolve in global demand and supply cycle. Türkiye’s position as global semi and finished products manufacturing industry need to maintain the balance between decarbonisation and global supply / demand flows.”

Future of Aluminium: Technology and Data

“The Future Aluminium Forum was conceived with a singular purpose: to explore the transformative potential of digital technologies in the aluminium industry.” – Nadine Bloxsome Technology, like living things, naturally goes through evolutionary processes. Without evolution technology’s purpose would soon be void in the name of industry. Industry 4.0 signifies the latest industrialisation, but it does not represent the possible futures that could be our reality.

Technologies and developments present the industry with exciting possibilities. Hope is often associated with these possibilities; yet, while beneficial, hope can be misleading. Ron Knapp, Adviser, China Hongqiao Group Limited (HK), addressed the industry stating, “sometimes we have to wait for the research to catch up with the technology.” This statement lingered throughout the forum; there is, somewhat, a unanimous understanding that the industry needs innovation, but at a practical industry scale.

Ron Knapp went onto provide insight into the China Hongqiao Group which has seen 100% production growth in the last 20 years. The company currently has a primary aluminium capacity of 6.46 Mt under China’s 45 Mt Cap. Once again, EU and US production decline was mentioned.

Emirates Global Aluminium (EGA), Chief Digital Officer, Carlo Khalil Nizam

heeded this statement and presented real life examples of AI application in the EGA plants. Providing recordings of digital transformation, digitalisation and digitisation, he defined each term while giving examples of “walk[ing] the talk.” Examples included outlining 10 digital capabilities, as well as implementing AI in the use of industrial cranes.

“The main objective of Industry 4.0, at EGA, is to lead the transformation [of EGA] into a smarter organisation. Using the elements of Industrial 4.0 such as, big data, artificial intelligence, internet of things, and many more.” - Abdulla Karmustaji, Product Owner Industry 4.0, Emirates Global Aluminium (EGA).

Industry 4.0 signifies the next steps of industrial revolution. Rather than it being the next natural step, it could be considered to be the next necessary step. Reviewing the global climate, perhaps the unexpected is the only thing we know for certain. Carlo K. Nizam also discussed EGA’s position and its vision for an advanced sustainable future, quoting Darwin for inspiration on the future: “It is not the strongest nor the most intelligent that survives, it is the ones that are the most adaptable to change.”

Adaptability to change is a natural requirement of evolution. So how can technology assist in ensuring we are as

flexible as we can be?

Amadou Ndiaye, Industry Executive Advisor for Energy and Natural Resources, SAP EMEA, discussed “Forging a Sustainable Aluminium Business with Integrated Data and Next Generation Business Processes.” He presented optimisation strategies that can be put in place with the assistance data collection and business technology platforms. With the aid of platforms, one can combine and embed any technology under the umbrella of development, automation, integration, data & analytics, and AI. With this systematic organisation, technology and data can seamlessly work together to develop a better future.

Pernelle Nunez, Deputy Secretary General, International Aluminium Institute (IAI), noted the IAI’s position towards data, emphasising its importance as a way to communicate with both the industry and stakeholders.

“We are on track, but we need to work together to ensure everyone is on the same track,” said Siri Sande, Marketing Manager, Storvik.

To assist one another by aligning the industry on the same path may be one of the ways that help push the industry forward when looking at both decarbonisation and the adoption of new technologies. Looking at technology, Sande explained that to make sure the industry is progressing, “we need to make sure the numbers are real numbers and not just estimates.” She called for a new era of sustainability that is supported by in-depth data. She provided examples of application enhancement with the assistance of data, as well as data collection methods.

But is this a part of the problem? “We talk about pilot projects, but we are stuck at pilots. We need to scale these projects; this is why digital projects fail.” – Denis Gontcharov, Data Engineer. The issue that Gontcharov raises is that that we have this data, but we don’t know how to utilise it. Not only this but data is often

Gontcharov, Data Engineer. The issue that have this data, but we don’t know how to utilise it. Not only this but data is often

spread everywhere. He presents a solution to organise, understand, and use data to progress the industry.

“Introduction of automation is difficult, but necessary” – Marcus Quantillion It seems that for the industry to develop and evolve technological advancement is necessary. For efficiency, economics, and production benefits, progression to industry 4.0 and beyond is almost a no brainer. But what about in the name of sustainability?

Greener Aluminium: Sustainability

“Aluminium’s properties make it essential for a sustainable future,” said Pernelle Nunez.

It has long been known that the decarbonising is an immoveable part of the aluminium future. But the decarbonising roadmap also understand that innovation and new technologies are essential to bringing a decarbonised future into fruition. Amadou Ndiaye declared that the industry must “embed sustainability into its DNA.” But how?

Ron Knapp presented the decarbonisation roadmap of China Hongqiao Group: “We will strive to peak carbon emissions before 2025 and to achieve net-zero emissions in Scope 1 and 2 before 2055,” said Chairman Zhang Bo, China Hongqiao Group. Decarbonisation is on the global agenda. But this does not mean that the method to decarbonise is one size fits all. New energy is one such way for a company to decarbonise, Ron Knapp elaborated on the company’s

new energy projects: Hongtai & Honghe Facilities. Thes projects aim at utilising wind and solar energy, replacing coal. He also noted that solar and wind electricity generation, in China, is cheaper than coalbased electricity. He demonstrated that the call for decarbonising the industry has been heard and is being acted upon.

Pernelle Nunez discussed the IAI global roadmap which aims to unify the industry and direct it toward a greener future. She also encouraged the industry saying that “sustainability issues are complex, evolving and interconnected,” but with the challenges, opportunities arise. But realism must also come into play here. There is surely a point where challenges present barriers that cannot be broken down?

“Costs are also an important factor” –Marcus Oberhofer, HAI

A reality check when it comes to implementing new technology has already been mentioned, but this is also the case for sustainability goals. Understanding the limits when it comes to adopting technology and making changes is important when it comes to making sustainable aspirations a reality.

Oberhofer noted the importance of creating realistic goals within realistic guidelines by discussing HAI’s opposition to recycled content requirements. In certain circumstances, creating limits can restrict development, but also divert attention from the real issue at hand. Oberhofer analysed that the industry is having the “wrong discussion” when it

comes to recycled content requirements. Rather than assist the scrap market, he claims this will result in further issues. He also called for the industry to be careful of greenwashing, which could also hinder the progress of the industry.

“Biggest global threat of today is global warming” - Asís Quecedo, Sales Engineer, GHI Smart Furnaces

So there is a balance that needs to be found for the industry to successfully decarbonise. It seems apparent that technology and data will have a profound influence on the development of the industry, referring to both economic and sustainable goals. But it is down to the industry to utilise the technology to our advantage.

Conclusion

With the warm Turkish sun heating the evening and the light catching the blue sea, the aluminium industry was given a beautiful setting to network by TALSAD. Hopefully the tranquil view reflected the future of the industry. But perhaps more realistically, the sea represented the unpredictable nature of the industry as rain and a grey sea was reported the following week.

“Moving forward, the Aluminium International Today team is committed to sharing the key discussion topics and relevant announcements with our readers across future issues. We look forward to continuing the dialogue and driving further innovation and progress within the aluminium industry.” - Nadine Bloxsome �

• Ultra-Low NOx up to 80% Reduction

• Highest Melting Rate up to 35% Increase

• CO² Reduction up to 60%

• Energy Savings up to 60%

• Short ROI ∼ 12 Months

IPCU (Furnace Pressure Control)

• Long Lifetime Design

• Hands-off operation

• Ultra-low maintenance

• Tailor-made fit

Bauxite Boom: Responsible Mining for People and the Planet

By Matthew Groch*

The rapid shift towards electric vehicles (EVs) is a cornerstone of the global strategy to reduce carbon emissions. However, the surge in demand for aluminium, a key material for electric vehicles, is causing significant environmental and social impacts. This presents a critical challenge in the race towards a greener future with electric vehicles: how can the urgent need for sustainable transportation be balanced with the urgent need to protect communities and ecosystems?

The need for effective ethical aluminium sourcing

The world’s leading automakers are heavily promoting their electric vehicles as a greener alternative given zero tailpipe emissions; however, green motoring means more than just going electric. A critical consideration is the sourcing and sustainability of materials used in these vehicles.

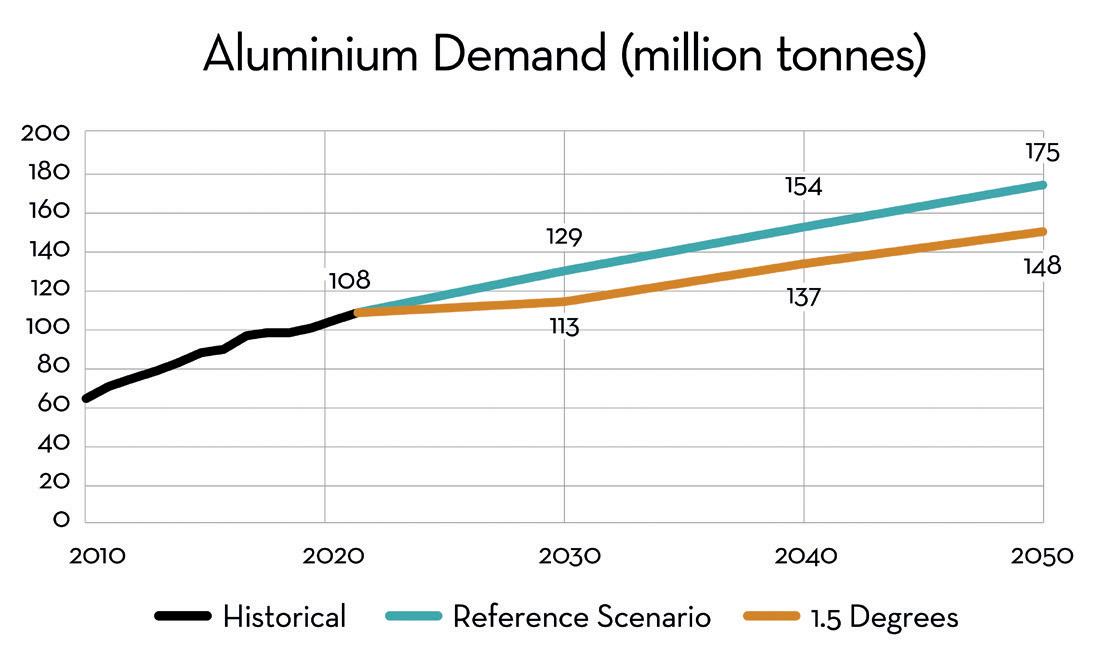

Aluminium is pivotal in electric vehicles production due to its lightweight and durable properties that enhance fuel efficiency and extend driving ranges. As a result, electric vehicles use significantly more aluminium than gas-powered vehicles, with battery electric vehicles using about 85% more aluminium.[1] Currently, car manufacturers account for approximately 18% of the world’s

aluminium production, and this demand is expected to double by 2050.[2]

The demand for electric vehicles is still high

Quarterly electric car sales tend to decrease from Q4 to Q1 each year, leading some to

incorrectly conclude that the demand for electric vehicles is slowing. This, however, is the wrong comparison as it does not control for seasonality. A more appropriate comparison would be to analyse the first quarter of 2024 to the first quarter of 2023. Using this methodology, sales of

Director for

*Senior

Heavy Industry Decarbonisation at Mighty Earth

Aerial view of Hydro Alunorte, a world-renowned alumina refinery. Alumina is the raw material for aluminium and is produced from bauxite ore Credit to: Tarcisio Schnaider

Former bauxite mine in West Kalimantan, Indonesia Credit to: Rdt Radihan

electric vehicles grew by 25%. In absolute numbers, this means that more than 3 million electric cars were sold in the first quarter of 2024, continuing its year-toyear growth trend from 2023, according to the International Energy Agency, an autonomous intergovernmental organisation.[3]

Assuming this growth trend, it’s imperative to plan for a future with high demand for EVs. The challenges associated with aluminium sourcing will not only persist but will also intensify, leading to greater environmental and community impacts. The unrelenting quest for more aluminium derived from mined bauxite has led to real consequences for the communities and environment surrounding the mines. Bauxite is found in the ground, largely under the forest floor. Miners generally use heavy machinery to strip large surface areas to access the bauxite, which can cause significant deforestation if the bauxite is in biodiverse or forested areas, and the runoff from this open cast mining can lead to the pollution of rivers, streams, and other bodies of water.

In addition, the aluminium sector is responsible for 1.1 billion tons of carbon dioxide pollution per year, about 2% of global emissions. More than 60% of the aluminium sector’s emissions are from the electricity, most derived from coal power, used during the smelting process. As a result of turning bauxite into aluminium, current mining practices have uprooted the lives of those living near the mines and the forest floors surrounding the mines.

A review of bauxite mining’s impact on people & planet Mighty Earth’s recently released report, “The Impact of the Bauxite Boom on People and Planet” [4] is the first report to take a global look at the bauxite and aluminium industry by reviewing and combining all available literature on the industry and its impact on people and the environment for four specific countries: Australia, Brazil, Guinea, and Indonesia. Each of these countries have substantial reserves of bauxite, and each country has incorporated their vast reserves of bauxite into its pursuit of economic development. The people living closest to the mines in Australia, Brazil, Guinea, and Indonesia have protested, filed lawsuits, and advocated for better treatment and healthier environments. This report helps amplify the plights of these individuals. In Indonesia, the government passed laws restricting public criticism and protests against mining companies. One such law states that “anyone who hinders or disturbs mining activities by permit holders who have met the requirements …

may be punished with a maximum prison term of one year and maximum fines of 100 million rupiah [$7,000].” [5] Initially seen as a warning, it has been used in practice to silence criticism. In 2021, 10 people were charged with violating this specific provision, out of 53 total people accused of opposing mining companies.[6]

A Bloomberg report found that much of the aluminium used in the Ford F-150 sold in the United States originated from northern Brazil, where a large mining company dominates aluminium production. This company has been accused of toxic metals pollution in surrounding rivers and streams, which provide water and food for locals. According to one estimate, waterways

mining on their communities:

“Complainants state they have witnessed an unprecedented decline of wildlife and even the total extinction of some species in the region. They believe that water pollution as well as the impacts of mining infrastructure, notably mining roads and the railway lines crossing fields and forests, are probably the main causes. The decline of animals and fish has also significantly contributed to the degradation of livelihoods since communities largely depended on fishing and hunting, in addition to agriculture.”[10] Similar destruction is also taking place in Australia, where the Western Australian Government recently approved a mining company’s plan to clear 800

were “at levels 57 times greater than what health experts consider safe.”[7] Byproducts of the mine are so prevalent that medical staff found at least one woman had “175 times the amount of aluminium considered safe in her hair.”[8] Although the company was faced with monetary penalties in the past by the Brazilian government, local residents remain dissatisfied and have filed a lawsuit in the Netherlands.

In West Africa, residents from 13 Guinean villages in 2019 filed an official complaint alleging that a large bauxite miner had violated their rights and did not provide adequate compensation to locals. The complaint was filed against the International Finance Corporation, a division of the World Bank, which provided a $200 million loan to a mining company. [9] Three nonprofit organisations filed the complaint on behalf of the villages, vividly expressing the negative impact of bauxite

hectares a year for mining.[11] This land is widely recognised as the world’s most biodiverse temperate forest, housing 800 plant species and 10 endangered animal species.[12] A new study found that, “The primary cause of deforestation in Western Australia’s Southwest forests is bauxite mining...Bauxite mining has cleared at least 32,130 hectares of publicly owned forest...and fragmented 92,000 to 120,000 hectares of the Northern Jarrah Forest up to December 2019, and the rate is accelerating.”[13]

The impact of bauxite mining and aluminium production in each of these countries – Australia, Brazil, Guinea, and Indonesia are significant but can be mitigated. Automakers purchasing aluminium and government regulatory bodies have the power to drive this change. The demand for minerals such as bauxite and aluminium will continue to increase as they become more important

Red mud - toxic residue of aluminium production polluting the soil on huge area. Guinea, Africa. Credit to: Igor Grochev

in the transition to a decarbonised world. With the rapid increase in electric vehicle production globally, it’s more important than ever to ensure aluminium is sourced responsibly from bauxite mines.

Mighty Earth and other groups are challenging the world’s leading automakers to adopt ethical practices throughout their EV supply chains. Global campaigns around the world have been pressuring the world’s leading industry to invest in environmental sustainability and

take social responsibility in their operations. They are also urging manufacturers to ensure that the sourcing of materials does not come at the cost of human rights or environmental degradation.

There is a path forward for responsible mining of bauxite and the production of aluminium. Electric vehicle manufacturers and other downstream manufacturers can play a significant role in raising the standards for their supply chains, and national and local governments should

strive to ensure their local constituencies are protected from the negative effects of bauxite mining. The transition from traditional vehicles to electric vehicles should reduce emissions and pollution and make the world a cleaner place. It is the responsibility of governments and automakers to make sure that local and Indigenous communities are not made worse off in the transition, and responsible mining means precious forests, peatlands, and the environment are protected. �

Mighty Earth and local climate organisers perform a dance at the NYC International Auto Show, urging Hyundai to clean up their auto supply chains as the industry transitions to EVs Credit to Jeremy Varner

Quick to Forget

By Alex Lowery*

Many in our industry assume large explosions occur rarely and, for the most part, have been prevented from occurring. This mindset unintentionally downplays the seriousness of the hazard in their workplace(s). It exposes their workers and surrounding community to a deadly hazard. This false safety belief is farthest from the truth. Because for the past 23 years our industry has continued to suffer through one or more catastrophic molten metal explosions annually. An explosion killed six workers and destroyed a casthouse in April, 2022. 2023 seemed to be anomaly with no explosion until an explosion occurred in September killing four and injuring thirty workers. Another explosion occured killing two workers two weeks later.

The hazards associated with molten metal are universal and exist in every workplace that processes molten metal. Still some workplaces downplay the severity of this hazard. No other hazard in our industry caused more financial losses than molten metal explosions. Insurance claims over the past 13 years have been filed for over $400,000,000 in the USA because of molten metal explosions. Why is our industry so quick to forget ?

Workplaces fail to acknowledge this

hazard because of a lack of education and awareness. Understanding how molten metal explosions occur can provide a workplace with the knowledge to inspect and identify machinery, tasks or procedures where an explosion could generate.

Industry knowledge of this hazard progressed through the decades of research by scientists around the globe. These research studies formed the foundation for our industry’s best practice toward safety when handling molten aluminium.

Scientists proved explosions occur when molten aluminum reacts with water in either a physical or a chemical reaction. Physical reactions are the most common. They occur when molten aluminum covers

*Author & General Manager, Wise Chem LLC

China 2020

China 2020

China 2022

water or moisture on a bare substrate (e.g., concrete, steel, stainless steel). The moisture expands rapidly propelling the molten metal covering it away. A common example is during transfer of a crucible and some of the contents spill onto a wet floor. When this occurs the temperature of the water rises instantaneously propelling or throwing off molten metal. The flying molten metal creates other hazards when it lands. If it lands on a combustible (e.g., wood, cardboard, etc.), the combustible will ignite. These explosions damage equipment and workers can be injured or killed.

Chemical reactions occur when aluminium bonds with oxygen (forming aluminium oxide) releasing hydrogen (in the form of energy) on a molecular level. Scientists have calculated that the force generated from one kilogramme of molten aluminium is equivalent to three kilogrammes of Trinitrotoluene (aka TnT) exploding. Furnaces in aluminum plants contain 300,000 to 1,000,000 kilogrammes of metal. The explosions can be very large, destroying workplaces, injuring and killing workers and even create shockwaves detectable by seismic earthquakes stations. It should also be noted that in physical reactions the molten metal that reacts with water is unchanged with regards to its mass. If 1000 kg of molten aluminium physically reacts with water, the result is 1000 kg of solidified aluminium. Thi is not the case with chemical reactions. If the same 1000 kg chemically reacts with water, the 1000 kg instantly transforms to aluminum oxide. This is why after chemical reaction explosions a large mushroom cloud of aluminium oxide generating from the workplace occurs. The aftermath of the site will also look like it is covered in snow because of the aluminium oxide.

In 1980, the Aluminum Association started the Molten Metal Incident Reporting Program. It arose from a request within the industry to develop

a programme where companies could learn from one another on an anonymous basis about molten metal explosions that were occuring. For the past 42 years, this programme has been a valuable safety tool for companies around the globe. There are currently 200 reporting plants worldwide that forward a detailed report when they experience an explosion in their workplace. The Aluminum Association states that the MMIR might catch less than 10% of all incidents. Regardless, this programme is a great resource for educating plants on trends in our industry. All reporting companies receive a detailed annual report listing where in a workplace the explosions occurred (e.g., melting, transfer, and casting).

During the melting phase explosions have been recorded that included scrap, sows, alloy addition, ingot/t-bar, others. Scrap is a growing source for raw material throughout our industry. Scrap can be divided into two categories, internal or

external. Internal scrap is material that was generated internally within the workplace and kept undercover. External scrap is either material received from outside the workplace or internally generated scrap that was stored outside and exposed to the elements. “Careful scrap inspection, storage and, where appropriate preparation, are vital to prevent molten metal explosions and other mishaps. A concern with scrap shipments is that hazards may be hidden or buried and difficult to discover.” states the Guidelines for Aluminum Scrap Receiving and Inspection Based on Safety and Health Considerations. This document is a useful resource on identifying the variety of hazards involved in scrap.

In addition to scrap causing explosions, sows, ingots, t-bars and RSI (remelt secondary ingot) can cause explosions too. For sows and RSI, the process of molten metal cooling in mould can result in a shrinkage cavity. Shrinkage cavities

Norway 2017

Brazil, September 2023

form during the cooling process when the outermost surfaces of the metal solidifies while the center remains molten. Overtime a shrinkage cavity can collect moisture. If a sow or a RSI is charged into a furnace without properly drying moisture in the shrinkage cavity an explosion can result. One workplace reported a sow’s shrinkage cavity with a volume of 19 Liters.

The Molten Metal Incident Reports recorded over 1000 explosions during the casting phase of the direct chill (dc) process and during casting sows. These explosions have been reported at the beginning of cast, steady state and at the end of the cast. Hand tools and tools used by vehicles have been reported to be a source of an explosion. If a tool is “wet” an explosion will result. The MMIR has reported more than 116 reported explosions from “wet tools” over the past 45 years. Tools can become wet either through exposure to moisture (e.g., stored outside, or near an open door) or when the tool comes into contact with chemical salts. All tools, no matter their size, should be preheated prior to use to prevent explosions.

Over 850 molten metal explosions were reported during the transfer phase. These explosions occurred in drain pans, troughs, crucibles, and on floors. The causes varied from wet floor/spill, wet refractory or tools, and wet/rusty drain pans. Drain pans are an overlooked area that have generated a considerable number of explosions. The MMIR lists 357 reports of explosions from drain pans over its history.

There has been one or more force 3 explosions annually in our industry over the past 22 years. The root causes for these explosions vary but many share a common characteristic of molten metal escaping from its holding spot. Molten metal flowing uncontrollably from a furnace leak, trough overflow, bleed out on a casting table, etc. is a workplaces worst nightmare. An explosion may result when molten metal comes into contact with a surface not coated with an approved safety coating. Workplaces need to properly maintain the safety coatings that are applied on steel substrate (e.g. casting table), concrete (e.g, casting pit, adjacent maintenance pit, under furnaces, etc.), and stainless steel (e.g., casting pit and tooling). The history of our industry changed when the Aluminum Association (USA) spearheaded an industry wide effort to research molten metal explosions in 1968. It was through that initial research study and subsequent studies of specific coatings to prevent molten metal explosions in our workplaces was developed. The Aluminum Association’s “Guidelines for Handling Molten Aluminum” lists four coatings that were tested and “found to be effective in preventive molten metal

water explosions where molten metal comes into contact with water with steel, concrete (or stainless steel) following bleedouts and spills during bleedouts and spills during dc casting”. These approved coatings are Wise Chem E-212-F, Wise

USA, 2016

Chem E-115, Carboline Multi Gard 955CP, and Courtaulds Intertuf 132HS products. This hopefully clarifies that other coatings currently in the marketplace, such as Chemglaze and Lord’s E212, as far as I know, have never been tested by the industry and should not be recommended to for use anywhere near molten metal in our industry. If it has been tested and approved, I welcome correcting my statement. In addition, it was noted in the Rustoleum Red coating, that it “did not prevent explosions”. The elimination of untested coatings in our industry will make casthouses safer, as well as protect workers from injuries and fatalities.

The maintenance and reapplication of the approved safety coatings is required because the coatings wear away after repeated molten metal contact. The bare substrate beneath the coating eventually becomes exposed. Scientific studies proved that the minimum bare area to generate an explosion on a steel substrate is 5 cm x 5cm, on concrete it is twice as large. Periodic maintenance of the safety coatings should be completed and recoat of the casting pits every 16-20 months, and tooling every 12-16 months.

Each and every molten metal explosion that destroys an aluminium plant may result in the injury and death of workers and nearby residents. Through the Molten Metal Incident Reporting Program past incidents can be used to prevent future recurrences when workplaces use MMIR’s annual report and inspect their plant for similar hazards. It is hoped that the current record of 23 years of catastrophic explosions will finally be broken. �

Records are made to be broken. Historical forgetting is rarely accidental.

India, September 2023

South Korea, February 2023

An Insightful Keynote

Following an insightful Keynote presentation at the recent Future Aluminium Forum (FAF), Nadine Bloxsome* spoke with Ron Knapp** from China Hongqiao Group, a leading global aluminium producer based in China, to find out more about the company’s long-term goals and how this aligns with a focus on sustainability.

The environmental and commercial challenges for aluminium producers are growing as the consumer – and the global community – expect higher standards of responsibility throughout the production cycle.

Some aluminium producers have had the benefit of being in countries/regions with access to low-carbon sources of electricity, providing a strong foundation for a low carbon emissions production profile. Other producers have been developing in countries/regions where

1.

the electricity and energy supply has been dominated by fossil fuel sources, resulting in a carbon emissions footprint as much as four to five times higher. An obvious example is that of China, where historically coal has been the backbone of the energy supply for industry – India and Australia have similar coal-energy legacies to address in the modern era of cutting carbon emissions as a key element in the fight to address climate change.

In the case of China, now the leading producer in the aluminium industry,

the focus often points to the energy component and the sheer size of the industry with more than 50% of global primary aluminium production. But there’s more to the China aluminium story than just energy. At the recent Future Aluminium Forum 2024 in Istanbul, Turkey, I caught up with Ron Knapp from China Hongqiao Group and asked him about the approach being taken by the company in addressing the challenges facing a major Chinese aluminium producer.

Nadine Bloxsome (NB): Ron, welcome to Istanbul and the 2024 edition of the Future Aluminium Forum! The China Hongqiao Group is one of the largest aluminium producers, not just in China but globally with over six million tonnes of annual production of primary aluminium and 19 million tonnes of alumina. Your FAF presentation showed a commitment to achieving both peak carbon and net zero carbon goals – how will China Hongqiao meet these goals . . . is this achievable by an aluminium producer based in a country traditionally sourcing its energy for aluminium production from coal-fired electricity?

Ron Knapp (RK): Good question, Nadine! From our size and our main production base in Shandong Province, there should be no surprise that we have the biggest carbon footprint in the whole global aluminium industry, but not the most carbon intensive – and let me comeback to that in a minute.

China Hongqiao has several advantages to help us to offset our obvious disadvantages – these advantages will enable us to address the first steps in our carbon abatement challenge and set us on the pathway to the attacking the harder parts of the task. We can’t achieve it all with the wave of a magic wand – it will take time and it will require more research success to give more solutions and

opportunities in fixing the future steps… the Future Aluminium Forum in action!

Looking at our China Hongqiao advantages, the first simple advantage but a key to delivering outcomes is a combination of our ownership, management and workforce. We are spin-off from Shandong Weiqiao Pioneering Group following Weiqiao’s entry into the aluminium industry in 2001; China Hongqiao is listed on the HKEX (Stock Code #1378). People use Weiqiao or Hongqiao in conversation, given our heritage and because Weiqiao is the majority shareholder of China Hongqiao with over 60% shareholding.

Our ownership, with Weiqiao holding a majority of the shares provides a strong

leadership and management structure for the company; Chairman and CEO Zhang Bo is also the chairman of Weiqiao. The workforce is highly committed to delivering positive results for the company and the local communities where the majority of our workforce reside. Zouping/ Binzhou (Shandong Province) takes on an aluminium family characteristic, with a large number of big and small enterprises associated with the aluminium cluster business model that has been a central feature of the Hongqiao organisation from the very beginning. More than 150 enterprises are involved in the cluster, including suppliers and customers as well as a wide range of service providers.

Ron Knapp

2.

NB: You talk about aluminium industry clusters – what is the role or purpose of the clusters?

RK: Here is one of the simplest of concepts and one of the highly valuable parts of the China Hongqiao business model. The most obvious element or contribution comes from the high percentage of aluminium metal delivery to our customers as hot molten metal. Both the producer and consumer receive an advantage. Over 90% of all our aluminium metal is delivered as hot molten metal, reduced cast-house requirement on our side and reduced energy requirements for the customer to remelt their aluminium metal supply. Multiply the per tonne saving by, say, five million tonnes for example – and there is a great saving in energy and another small contribution to lowering carbon emissions.

3.

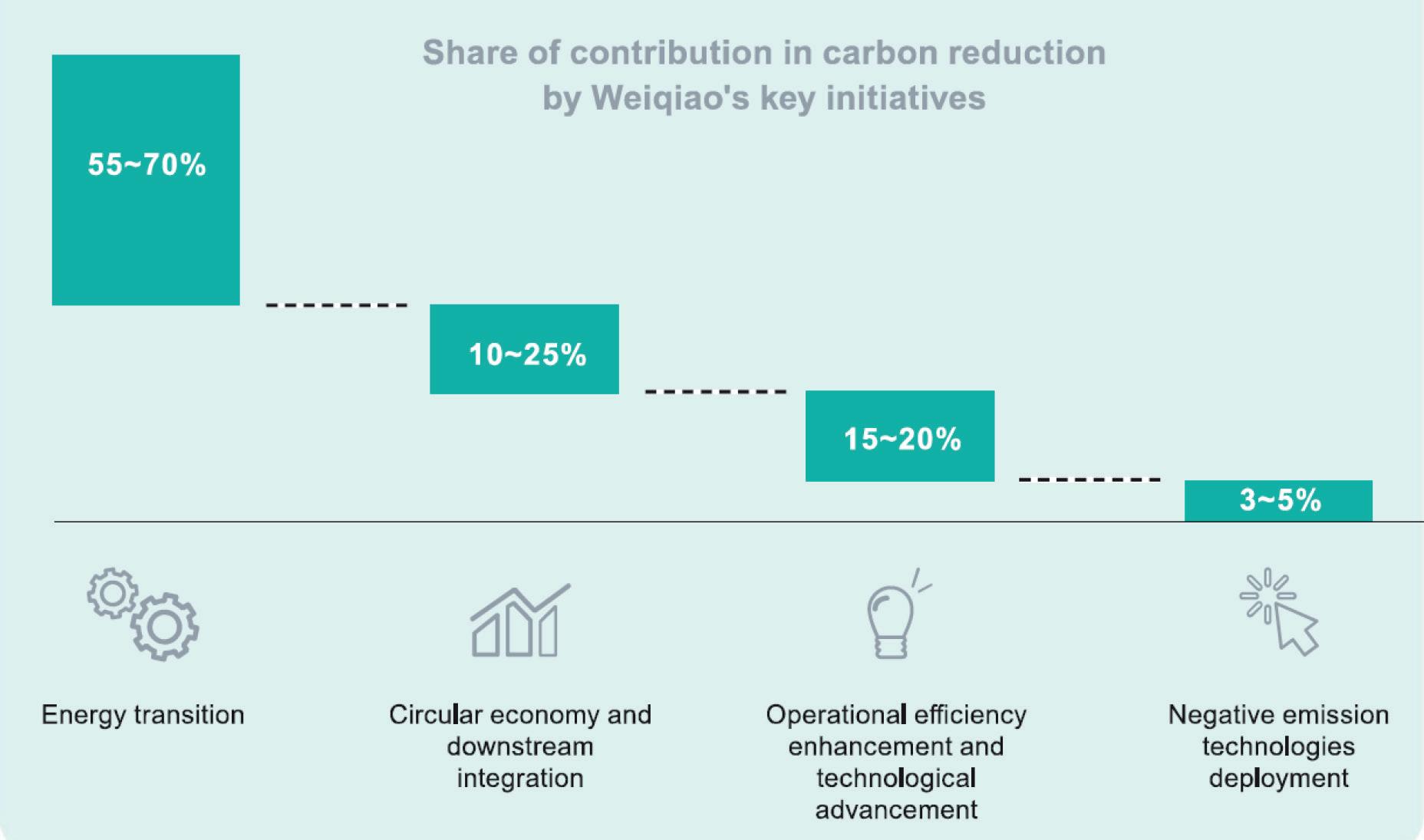

NB: The Weiqiao carbon reduction roadmap covers a full swathe of actions to be applied to the China Hongqiao operations – how do you see these actions evolving and in what order will they be introduced?

RK: Our Chairman, Zhang Bo, has publicly committed to meeting our responsibilities under China’s dual carbon goals and we will strive to peak carbon emissions before 2025 and to achieve net-zero emissions in

Yunnan Province – this is an energy and environmental game-changer, from coal to clean energy. The Yunnan Hongtai & Yunnan Honghe projects are in line with government objectives to optimise the

Scope 1 and 2 before 2055.

This is a very serious commitment and obligation for our company… we have this very big (total) and heavy (intensity) carbon emissions challenge to deal with across our operations, from upstream through midstream to downstream. Our programme of carbon reduction across our production activities and new aluminium alloys and products will also help the carbon balance of others because we see these actions will be helping consumers face lower Scope 3 emissions. It’s about increased aluminium use and new applications, combined with lower carbon emissions in the aluminium we produce.

Looking at the Weiqiao Carbon reduction roadmap, you will see one of our first priorities is the task of changing the energy structure of our business, particularly the fuel source for the huge electricity consumption required to produce our six million tonnes of primary aluminium metal.

The most dramatic shift in the Hongqiao story is the project currently underway of relocating 60% of our primary aluminium capacity from Shandong to

aluminium industry through supply side management, and to promote green development.

2023 brought a new achievement with production from our Yunnan Hongtai complex achieving one million tonnes. That’s a great boost in moving our energy transition towards our long-term goals.

But we know these are first steps in our journey. By 2026, we will have four million tonnes of capacity located in Yunnan. To complement these moves, Weiqiao has a renewable energy work programme for the development of 13 GW of wind and solar PV across Yunnan Province and Shandong Province. We’re not standing still and waiting to see how things happen – our Chairman Zhang Bo is driving forward to ensure success.

Several of the elements of our net carbon emissions are being progressed concurrently. While it is easy to see why energy is often spotlighted on centre stage, given the size of its contribution to our carbon footprint, we are very active in enhancing operational efficiency and technological advancements. Our lightweighting centre is a major growth segment in the company – and the circular economy is very much in focus with our new recycling facility with capacity to disassemble 100,000 vehicles per annum as the opportunities for such activities grow with the NEVs and higher volume of aluminium scrap available from the vehicle fleet reflecting increased aluminium content.

4.

NB: Where are the yellow warning flags – or even red flags – that need more work before solutions can be found and introduced?

RK: The aluminium industry must keep working on more solutions; we do not have all the answers yet. I immediately think of the carbon anode in the electrolysis segment of the operations –it’s not the “big ticket” item for the whole global aluminium GHG emissions budget, that honour remains with energy but for some producers who already have low- or

introduce the most technically advanced processes in our smelter pot rooms and throughout the production process. This provides us with first class energy efficiency, with the latest 600kA potlines down at sub-12,400 kWh per tonne of aluminium. With this comes a huge energy saving…for example, the average energy efficiency for the North America

zero-carbon energy available, the anode has more GHG emissions prominence in their total GHG emissions. As we pull down the energy emissions number which currently accounts for some 75% of the total aluminium cradle-to-gate GHG emissions identified by the IAI, the 13-14% share attributed to the anode production/consumption segment will increase in significance in the race to net zero. The answer is a new technology breakthrough that can be commercialised, or an additional burden will be placed on negative emission technologies, such as Carbon Capture, Utilisation, and Storage (CCUS).

While the research continues into the alternatives, we are continuing to

and European regions is around 14,000 kWh – that gives us a 1,500 kWh per tonne advantage and a saving to be able to continue R & D investment and further upgrading of production units.

Our smelter fleet is less than 10 years old – and with daily output of around 4.5 tonne of aluminium metal per pot from our 600 kA smelter potlines, this brings further operational efficiencies.

These factors help us to have a per tonne carbon emission lower than the average for aluminium production where coal-fired electricity is the energy input.

Often, aluminium is characterised as one of the sectors that is hard-to-abate, due to the production process involving carbon and the energy input required.

NB: Ron, look into the crystal ball and tell what you see for aluminium and China Hongqiao

RK: An easy one to finish with! A very positive future for global aluminium, with ongoing growth in supply coming from primary and recycled sources – and demand coming from traditional and new innovative applications. China Hongqiao will accelerate sustainability and efficiency outcomes, with the commitment of ownership, management and workforce. We will continue to strive to be the best – and always continue to improve our environmental performance, hand-in-hand with our commitment to the delivery of globally competitive aluminium metal and products. Efficiency, industrial clusters and innovation remain critical elements for the delivery of our vision for the future – and this is reflected in Chairman Zhang Bo’s approach in building a platform for the integration of science, education, innovation, and production - and to promote industry-education integration and industrial innovation to accelerate high-quality development…linking technological and commercial worlds for better outcomes.

5.

NB: What’s next for the Group?

RK: Next is already with us and is being developed and rolled-out …it’s the aluminium lightweighting developments and NEVs, - the next evolution of the Weiqiao Pioneering Group. First it was textiles and the start of the journey, then in 2001 the birth of the aluminium leg of the family.

Twenty years later and with very different commercial and environmental opportunities, a new industrial evolution is emerging and quickly taking shape, drawing several key strands or elements together into a new pillar of activity of the Weiqiao Group.

Recognising the pull of a changing market, Weiqiao has been building an aluminium lightweighting centre, combining vehicle component production and new growth areas created by intense research and development activities. The new pillar, or third leg, of activities also includes recycling facilities to strengthen our march into the circular economy –the Sino-German Hongshun Technology Industrial Park including the China Hongqiao-Scholz JV vehicle dismantling and recycling aluminium production technology facility is all part of the development now underway.

The next step was the acquiring of a majority shareholding by Weiqiao in the vehicle production plant known as BAW or Beijing Auto Works.

With these different elements, we now have the start of the next cluster of industries being combined to build efficiency through co-location of different activities and economies of scale enabling a wider net production across the industry.

In May 2024, Weiqiao-Hongqiao Chairman Zhang Bo joined with his peers in celebrating the delivery of the first batch of REACH NEV aluminium vans, part of the commercial vehicle plan which will include heavy trucks, commercial vans and passenger buses.

The Weiqiao lightweight strategy runs through the entire vehicle development process – and supported by vehicle development standards system, automotive grade aluminium alloy technology development standards and technology patents.

Weiqiao New Energy Vehicles will become a key element in our drive towards sustainability. Primary and recycled aluminium will be partners in these developments.

A modern 600kA smelting pot room part of the China Hongqiao aluminium cluster in Binzhou, Shandong Province

EGA: A Digital Future

Aluminium International Today spoke with Carlo Nizam* following his attendance at the Future Aluminium Forum. Carlo disused digital technologies and their application at Emirates Global Aluminium (EGA).

1. The video presented to delegates at the Future Aluminium Forum was very well-received. For those who were not in attendance, can you provide an overview of Emirates Global Aluminium’s new digital strategy and its objectives?

We are executing our digital transformation strategy with a dual track approach that simultaneously delivers tangible business impact through quarterly waves of uses cases and lays the digital foundations to enable sustainable digital transformation at scale. Our strategy will not only make us more operationally and financially competitive but also more agile, efficient and adaptable in an exponential age of technology that is accelerating at breakneck speeds. This is not something reserved for tech start-ups, it’s something that we as large industrial companies need to embrace whole heartedly to future-proof our businesses.

2. What specific digital technologies are being implemented as part of this strategy, and how are they expected to enhance operations within the aluminium industry?

We have identified ten digital capabilities to support a broad spectrum of use cases across both our physical operations and corporate activities globally and that collectively enable smarter, more agile, and data-driven decision-making processes. While these may evolve over time, they currently include cloud computing, data analytics and AI, Internet of Things, digital

3. You have shared information about EGA’s dual track approach within the digital factory. Can you share more detail around how Emirates Global Aluminium plans to leverage digitalisation to improve efficiency, productivity, and sustainability across its operations?

While the digital factory is delivering strong impact and change through waves of more than 200 use cases, this alone is not enough to sustain digital at scale across EGA. So far, we have executed more than 80 of 200 use cases identified, That is why we are simultaneously laying structural foundations to prepare EGA to scale digitally and go beyond just use cases. For example, we are defining top-down digital ambitions and value roadmaps for each of our business areas across EGA. These value roadmaps are used to identify priority use cases in line

process automation, to name a few, and many more.

We believe these capabilities will enable sector-wide digital transformation for the aluminium industry and drive operational excellence, improve sustainability, and create a more connected and resilient value chain.

with business priorities before they are executed by the digital factory.

Separately, our goal is to fully integrate industry 4.0 digital capabilities into the business. This requires upskilling our people, who have the real business domain expertise, with new digital skills so they can be more autonomous and productive. To achieve this, we have set up a digital academy that has so far upskilled more than 2,000 of our employees on effective use of analytics, AI applications and agile ways of working. Our employees are not only learning about the different digital capabilities but also how to leverage them using our digital technology platforms. This is crucial if we want to achieve a digital critical mass across the company.

The next foundation is all about technology but before we look at that, let’s take a moment to reflect on our metal value chain. In our industry, raw materials are refined to create an end product. Now

*Chief Digital Officer at Emirates Global Aluminium

at each step of the value chain, there is a digital footprint of data for everything that happens. This can also be refined as a resource to create additional value and herein lies a very big untapped opportunity.

To leverage this opportunity, we need a data refinery which we call a data platform, that ingests and structures data to make it easily accessible for our employees to analyse. We introduced our EGA data platform in early 2023 and it made a significant impact for our business, both commercially and technically.

But we also have other platforms that sit on top of the data platform for each of our 10 digital capabilities. These selfservice digital platforms are designed to be used by our upskilled employees without IT involvement. Simplifying the use, providing access and training to such platforms is key to scaling digital transformation across EGA.

4. Could you elaborate on any challenges or obstacles faced during the implementation of the digital technology strategy, and how were they addressed? Is there any advice you would offer to the rest of the sector?

Digital transformation is not just about leveraging new technology capabilities, but also about transforming ways of working, mindsets and ultimately culture. As the old saying goes, “culture eats strategy for breakfast”. It is crucial to understand the driving forces behind workplace culture and build a strong foundation of trust with a coalition of the willing.

Start with small initiatives and achieve quick wins is essential build momentum, confidence and trust, while also working on laying solid foundations that will support lasting impact and value. Technology is exciting but it is only a small part of the bigger picture – people are what drive meaningful change.

6. You mentioned at FAF 24 that “the speed of innovation is growing exponentially.”

How does Emirates Global Aluminium ensure the security and integrity of its digital infrastructure and data in the face of increasing cyber threats?

Ensuring the security and integrity of our digital infrastructure is paramount. We adhere to the highest standards of cybersecurity, continuously improving our defenses and making considerable investments to maintain robust cyber security measures. We are also leveraging our 10 digital capabilities particularly AI and advanced analytics, to foresee and counter cyber threats proactively.

7. Can you discuss any partnerships or collaborations that Emirates Global Aluminium has formed to support the implementation of its digital technology strategy?

We rely on an ecosystem of strong partners to support our digital transformation. This includes consulting services, software, hardware as well as private and government research institutions.

9. What measures are being taken to ensure that employees are adequately trained and equipped to effectively utilise the new digital technologies?

As I mentioned, we established a digital academy to strengthen enhance our employees’ digital literacy and capabilities. So far, we have upskilled more than 2,000 of our employees across multiple areas such as analytics, AI and agile ways of working. Our employees not only learn about the different digital capabilities but also how to leverage them using our digital technology platforms so they can contribute pro-actively to our ongoing and future digital transformation projects.

5.You stated that “As a digital lighthouse for our region, we democratise digital capabilities to ‘change the game’ and create inspiring experiences for ourselves, our customers, and our partners” - EGA’s digital ambition. In what ways do you anticipate that the new digital technology strategy will impact the company’s competitiveness within the global aluminium market?

It is already creating a tangible impact on our productivity and efficiency. So far, we have delivered over $100m of impact through over 80 use cases. Our agile way of working is helping emphasise a sense of urgency to accelerate how we work, which in turn reinforces a relentless focus on our customers.

8. How is Emirates Global Aluminium utilising data analytics and artificial intelligence to optimise decision-making processes and drive innovation?

EGA is utilising data analytics and AI in many ways. For example, our smart cranes employ machine vision technology and neural networks to ensure adherence to operational standards. This system automates compliance checks through visual inspections, enhancing process accuracy while reducing the need for manual interventions. AI-powered compliance monitoring ensures consistent quality control and safety performance across operations.

Another example is we use machine learning models to forecast potential pot failures. These predictive models analyse historical and real-time data to identify early warning signs of equipment issues. These capabilities minimise unplanned downtimes, enhance asset reliability, and extend the lifecycle of critical production equipment.

EGA is optimising its sales planning strategies through advanced analytics and predictive algorithms to optimise sales planning. This approach allows for dynamic demand forecasting, smarter inventory management, and improved supply chain visibility, which ultimately enable more accurate and profitable business decisions.

By embedding these AI-driven solutions into our core business functions, EGA is not only optimising current processes but also paving the way for new innovations that redefine industry standards. This data-centric approach empowers us to remain agile, improve our competitive edge, and create long-term value in a dynamically evolving market landscape.

10. Looking ahead, what are the future plans and aspirations for Emirates Global Aluminium’s digital technology strategy, and how do you envision it evolving in the coming years?

We will continue to push the boundaries of what is possible to achieve ambition of becoming a digital lighthouse for our region and industry. We see enormous potential to unlock additional value for our business through Industry 4.0, not only to fulfil our purpose of innovating aluminium to make modern life possible but also to leverage digital capabilities, products and services as potential new revenue streams.

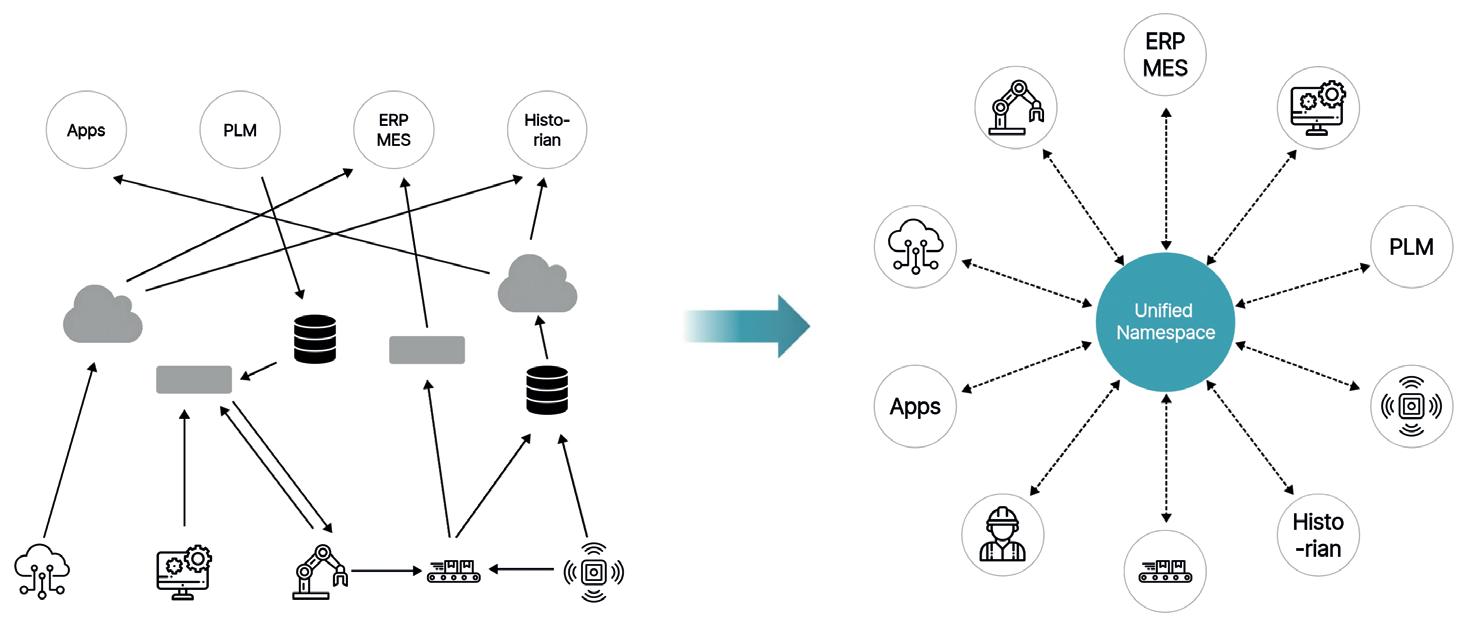

The Unified Namespace for Digital Transformation in the Industry

This article presents the author’s learnings from five years of performing digital transformation in the aluminium industry. The focus lies on highlighting the common pitfalls encountered. Subsequently, the concept of the unified namespace is introduced as a solution to common data-problems in aluminium manufacturing. Finally, a concrete approach of how to build a unified namespace at your plant is presented. The goal is to have a running system that solves a common manufacturing use case within three months. By

Denis Gontcharov*

Why Becoming Digital Matters

The aluminium industry is conservative and therefore slow to adopt modern digital technologies. Nevertheless, by now there’s a consensus that the industry has to digitally transform in order to stay competitive in the future. Various challenges such as artificial intelligence, automation and sustainability and decarbonisation demand a more rigorous use of the vast quantities of available data. However, processing vast quantities of data is easier said than done.

“Saying aluminium+++ manufacturers have an abundance of data is like saying the earth’s crust has an abundance of aluminium.”

Most Data Projects Fail

Many manufacturing companies have already started their digital transformation journey. The focus was often on implementing various industrial use cases, for example preventive maintenance or image analysis. Unfortunately, the results of many of these use cases were unsatisfactory. In fact, according to a 2021 study by the McKinsey consulting company, 69 percent of digital transformation projects fail. According to the author’s experience, the two most

common reasons are exceeding the project’s budget and being stuck in “pilot purgatory”.

Projects Exceeding the Budget

Most digital projects that go over budget do so because the time to complete the project turns out to be much longer than initially planned. Nearly always, the reason is that the part of “getting the data” takes much longer than expected. Data is often assumed to “just be there” and little regard is given to the often messy state in which this data is stored.

Projects Stuck in Pilot Purgatory

The second way in which a technically successful digital use case fails to deliver on its promises is by not being scalable. Often, there’s a wish to roll out successful solutions of one plant across the other plants. Assuming the new solution is merely a copy, this challenge appears trivial.

However, the data infrastructure always differs slightly between two plants. This means that each roll out requires some modifications to the way data is fed. In practice, these modifications most of the time turn out to be substantial. In that case, the roll is often abandoned.

The Two Underlying Data Problems

Why do unsuccessful projects fail because they go over budget, and successful projects are stuck in pilot purgatory? The devil is always in the details: there are two main problems plaguing your data.

First, the various required data sources are never found in one place. After all, a manufacturing plant consists of many individual software systems that only communicate with each other through laboriously constructed point-to-point connections. Combining disparate data sources into one collection suitable for data analysis therefore requires a connection to each individual source system.

Second, technically having all data in one place does not yet solve the challenge of finding this data, if the data was already hard to find in the source system.

The company you work for may have a data lake or data warehouse that contains data from various source systems. But how do you navigate this large data repository to find a particular variable? More often than not, the data model (i.e. the structure under which the data is saved) is an exact copy of the data model in the original source system. This requires the person looking for the variable to have an intimate knowledge of the original

*Denis is a data consultant who helps aluminium manufacturers break down data silos.