In Loving Memory of Our Precious Daughter, and Sister, Sammi Kane Kraft

In Loving Memory of Our Precious Daughter, and Sister, Sammi Kane Kraft

Follow us: @StockNewsNow

Published Since 2006

SNN Inc. 4055 Redwood Ave. Suite 133 Los Angeles, CA 90066 www.SNN.network

Follow us: @StockNewsNow

SNN inc. 4055 Redwood Ave. Suite 133 Los Angeles, CA 90066 www.SNN.network

Robert K. Kraft, MBA SNN Chief Executive Officer, Executive Editor & Director rkraft@snnwire.com

Robert K. Kraft, MBA

SNN Chief Executive Officer, Executive Editor & Director rkraft@snnwire.com

Shelly Kraft SNN Founder, Publisher Emeritus skraft@snnwire.com

Shelly Kraft

prices are higher across the board except for one important category: stock prices! The post pandemic correction is upon us. Inflation is the all-time equalizer driving food, clothing and shelter prices higher. Interest rates are soaring, car prices are surging, and travel and entertainment are climbing. Even gold a hedge against inflation is in reverse as the US dollar trades higher against foreign currencies worldwide. And the “R” word is on the lips of the market pundits! So where are the opportunities? How do investors with cash buying power take advantage of this special situation of high dollar versus low stock prices? Buy, Buy, Buy! Buy with cash, not on margin.

Lynda Lou “Lulu” Kraft SNN President & Director lkkraft@snnwire.com

SNN Founder, Publisher Emeritus skraft@snnwire.com

As we get bombarded with market information and intel in the news, social media, newsletters, TV ads, YouTube etc. we have to keep our own perspective in mind, which is, how does what’s happening in the stock market affect microcap stocks? How do we manage the holdings in our portfolio? How do we make our decisions of whether we should buy, sell or hold? As investors we do need to decipher pertinent details from the noise of those trying to sell us their ideas. Picking up morsels of truth is still relevant to our decision making which brings me to the point of staying in our lane, picking sources we trust with a history of accuracy, doing this will do more to protect our self-made directives while resisting a constant repetitive barrage of attempted paid influences.

ASIAN PACIFIC CORRESPONDENT

Leslie Richardson

Lynda Lou “Lulu” Kraft SNN President & Director lkkraft@snnwire.com

aSiaN paciFic corrESpoNDENT

SNN COmPLIANCE AND DUE DILIgENCE ADmINISTRATION

Leslie Richardson

Jack Leslie

SNN coMpLiaNcE aND

As microcap investors we now have the opportunity that wealthy investors enjoy, buying low. Most fortunes are made during financial crisis’ when equities sell off as investors run for the doors raising cash to cover margin calls, have more essential financial needs other than their portfolio’s or simply want to stop the bleeding in their portfolio holdings. Regardless of their reasons this rare opportunity presents itself in broad daylight. It’s a smorgasbord of choice; what do we want to own?

CHAIRmAN OF SNN ADvISORy BOARD Dr. Leonard Makowka

DUE DiLigENcE aDMiNiSTraTioN

Jack Leslie

Pundits in the microcap world often preach doing your homework, believe in your own methods, stick to your plan, learn from your mistakes, and build your sensibility to maintain focus. I believe for the most part they are correct. How ever, it’s quite difficult to locate non-biased information during our searching for it and even harder to interpret incoming information when it finds you.

cHairMaN oF SNN aDviSory BoarD Dr. Leonard Makowka

ADvERTISINg and SALES info@snnwire.com

aDvErTiSiNg and SaLES info@snnwire.com

Unitron Media Corp info@unitronmedia.com

SNN CONFERENCES info@snnwire.com

grapHic proDUcTioN Unitron Media Corp info@unitronmedia.com

SNN coNFErENcES info@snnwire.com

©Copyright 2022 by Planet Microcap Review Magazine Inc. All Rights Reserved. Reproduction without permission of the Publisher is prohibited. The publishers and editors are not responsible for unsolicited materials. Every effort has been made to assure that all Information presented in this issue is accurate and neither Planet Mi crocap Review Magazine or any of its staff or authors is responsible for omissions or information that is inaccurate or misrepresented to the magazine. Planet Microcap Review Magazine is owned and operated by SNN Inc.

This publication and its contents are not to be construed, under any circumstances, as an offer to sell or a solicitation to buy or effect transactions in any securities. No investment advice is provided or should be construed to be provided herein. Planet Microcap Review Magazine and its owners, employees and affiliates are not, nor do any of them claim to be, registered broker-dealers or registered investment advisors. This publication may contain “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. All statements other than statements of historical fact are “forward-looking state ments” for purposes of federal and state securities laws, including, but not limited to, any projections of earnings, revenue or other fi nancial items; any statements of the plans, strategies and objectives of management for future operations; any statements concerning proposed new services or developments; any statements regarding future economic conditions or performance; any statements of belief; and any statements of assumptions underlying any of the foregoing. Such forward-looking statements of or concerning the companies mentioned herein are subject to numerous uncertainties and risk factors, including uncertainties and risk factors that may not be set forth herein, which could cause actual results to differ materially from those stated herein. Accordingly, readers are cautioned not to place undue reliance on such forward-looking statements. This publication undertakes no obligation to update any forward-looking statements that may be contained herein. Planet Microcap Review Magazine, its owners, employees, affiliates and their families may have investments in companies featured in this publication, may purchase securities of companies featured in this publication and may sell securities of com panies featured in this publication, at any time and from time to time. However, it is the general policy of this publication that such persons will refrain from engaging in any pre-publication transactions in secu rities of companies featured in this publication until two trading days following the publication date. This publication may contain company advertisements/advertorials indicated as such. Information about a company contained in an advertisement/advertorial has been fur nished by the company, the publisher has not made any indepen dent investigation of the accuracy of any such information and no warranty of the accuracy of any such information is provided by this publication, its owners, employees and affiliates. Pursuant to Section 17(b) of the Securities Act of 1933, as amended, in situations where the publisher has received consideration for the advertisement/ad vertorial of a company or security, the amount and nature of such consideration will be disclosed in print. Readers should always con duct their own due diligence before making any investment decision regarding the companies and securities mentioned in this publication. Investment in securities generally, and many of the companies and securities mentioned in this publication from time to time, are specu lative and carry a high degree of risk. The disclaimers set forth at Planetmicropcap.com or SNN.Network - disclaimer are incorporated herein by this reference.

©Copyright 2022 by MicroCap Review Magazine Inc. All Rights Re served. Reproduction without permission of the Publisher is prohib ited. The publishers and editors are not responsible for unsolicited materials. Every effort has been made to assure that all Information presented in this issue is accurate and neither MicroCap Review Magazine or any of its staff or authors is responsible for omissions or information that is inaccurate or misrepresented to the magazine. MicroCap Review Magazine is owned and operated by SNN Inc. This publication and its contents are not to be construed, under any circumstances, as an offer to sell or a solicitation to buy or effect transactions in any securities. No investment advice is provided or should be construed to be provided herein. MicroCap Review Magazine and its owners, employees and affiliates are not, nor do any of them claim to be, registered broker-dealers or registered investment advisors. This publication may contain “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. All statements other than statements of historical fact are “forward-looking state ments” for purposes of federal and state securities laws, including, but not limited to, any projections of earnings, revenue or other fi nancial items; any statements of the plans, strategies and objectives of management for future operations; any statements concerning proposed new services or developments; any statements regarding future economic conditions or performance; any statements of belief; and any statements of assumptions underlying any of the foregoing. Such forward-looking statements of or concerning the companies mentioned herein are subject to numerous uncertainties and risk factors, including uncertainties and risk factors that may not be set forth herein, which could cause actual results to differ materially from those stated herein. Accordingly, readers are cautioned not to place undue reliance on such forward-looking statements. This publication undertakes no obligation to update any forward-looking statements that may be contained herein. MicroCap Review Magazine, its own ers, employees, affiliates and their families may have investments in companies featured in this publication, may purchase securities of companies featured in this publication and may sell securities of companies featured in this publication, at any time and from time to time. However, it is the general policy of this publication that such persons will refrain from engaging in any pre-publication transactions in securities of companies featured in this publication until two trad ing days following the publication date. This publication may contain company advertisements/advertorials indicated as such. Information about a company contained in an advertisement/advertorial has been furnished by the company, the publisher has not made any independent investigation of the accuracy of any such information and no warranty of the accuracy of any such information is provided by this publication, its owners, employees and affiliates. Pursuant to Section 17(b) of the Securities Act of 1933, as amended, in situations where the publisher has received consideration for the advertise ment/advertorial of a company or security, the amount and nature of such consideration will be disclosed in print. Readers should al ways conduct their own due diligence before making any investment decision regarding the companies and securities mentioned in this publication. Investment in securities generally, and many of the com panies and securities mentioned in this publication from time to time, are speculative and carry a high degree of risk. The disclaimers set forth at http://www.microcapreview.com/disclaimer/ - disclaimer are incorporated herein by this reference.

This editorial is not meant to be a lesson in picking tops and bottoms nor the recommending to blindly throw money at perceived bargains it is rather to suggest you follow your tried-and-true methods of due diligence and stock picking since you have been tracking stocks to buy in your perceived great companies but were overpriced, overvalued or out of your reach. How do they look today? It doesn’t matter if you look at any tier of the market but especially small and microcap which have taken massive hits to their

Although I am a market traditionalist and since I historically lean on using my own common sense, this method may be costly since it also embeds learning from one’s own mistakes. For example, for generations investors relied on their stockbroker or wealth advisor to “trust” their advice, timing, ideas, guidance and performance. For better or for worse this marriage could have been a very successful marriage, oh by the way, the Internet, social media, relentless advertising, and regulatory intervention changed everything. The advent of dis count brokering, and millennial DIY activity gave investors the power of making decisions but added the need for discipline, research, and trial & error. As far as

WaiTiNg oN EDiToriaLMicroCaps, but overall markets, is when I’m reflecting on how I want to deploy cash that will set me up for financial independence in the next 10-15-20 years. We don’t have all the answers, however, by reading this issue of the magazine, I hope that you’re able to walk away with a few nuggets that can help you on your path to financial independence.

price and market cap. Even the brightest stars have fallen. Additionally, stock price drops suffering the usual 3rd quarter doldrums of poor earnings expec tations which will add to poor stock performance. Okay it might not be throwing the dart time but dust off the dart board and get your focus on because it just might be around the corner! —Shelly Kraft

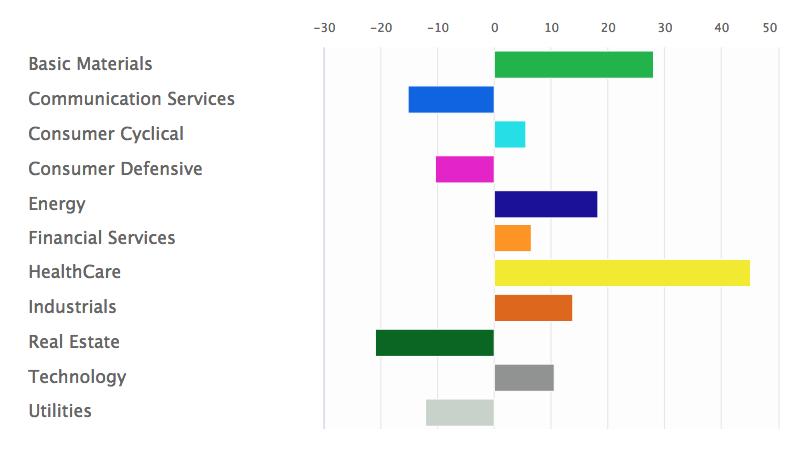

some good news: 29% of constituents had positive quarterly stock performance in Q3 2022 vs. 18% positive quarterly stock performance for Q2 2022. Healthcare was up 7.22% for the quarter lead by having four (4) companies in the top 10 performers, including Catalyst Biosciences, Inc., which was up 296.51%.

we get bombarded with market information and intel in the news, social media, newsletters, TV ads, YouTube etc. we have to keep our own perspective in mind, which is, how does what’s happening in the stock market affect microcap stocks? How do we manage the holdings in our portfolio? How do we make our decisions of whether we should buy, sell or hold? As investors we do need to decipher pertinent details from the noise of those trying to sell us their ideas. Picking up morsels of truth is still relevant to our decision making which brings me to the point of staying in our lane, picking sources we trust with a history of accuracy, doing this will do more protect our self-made directives while resisting a constant repetitive barrage attempted paid influences.

beat around the bush, for Q3 2022 (and all of 2022), it’s been tough being a MicroCap investor. The stats tell it all: The Planet MicroCap index was down 10.53%, which far outpaces the next biggest loser for the quarter (DJIA was down 6.25%). Year to date, MicroCaps are down 34.74% (according to the Planet MicroCap index). Looking at these numbers, it’s pretty clear, from a macro perspective, we’ve been a risk-off environment. When you dive deeper into individual sectors, sentiment has been negative across the board (Mining and Cannabis in particular) and capital has dried up. I’ve done a number of interviews with CEOs that are very VERY thankful they raised capital earlier this year because things now are much more difficult. Every sector in the index was hit hard, meaning down >3% (except Healthcare, more on that in a second), but there is

Pundits in the microcap world often preach doing your homework, believe in your own methods, stick to your plan, learn from your mistakes, and build your sensibility to maintain focus. I believe for the most part they are correct. How ever, it’s quite difficult to locate non-biased information during our searching for and even harder to interpret incoming information when it finds you.

This is not our first go round, markets are cyclical history verifies this. However, I always go back to insights that a friend of Planet MicroCap, Rick Rule, would always remind me: Bear Markets are authors of Bull Markets. I think about this (and the inverse) quite a bit. Specifically, what areas of the market are people disliking and avoiding and WHY? It’s abundantly clear looking at every statistic out there that MicroCap stocks are the unchosen right now. If you’re reading this editorial and this issue of the magazine, you prob ably already know this. That’s why the main theme for this issue is about “Fallen Angels” - many stocks that were once loved are now calling MicroCap their new home. There were already a ton of companies to look at, and now, there are even more. Do your homework, you’re in the right place to get started. —Bobby Kraft

Although I am a market traditionalist and since I historically lean on using my own common sense, this method may be costly since it also embeds learning from one’s own mistakes. For example, for generations investors relied on their stockbroker or wealth advisor to “trust” their advice, timing, ideas, guidance and performance. For better or for worse this marriage could have been a very successful marriage, oh by the way, the Internet, social media, relentless advertising, and regulatory intervention changed everything. The advent of dis count brokering, and millennial DIY activity gave investors the power of making decisions but added the need for discipline, research, and trial & error. As far as concerned and in my opinion, I would rather fail or succeed because of my own decisions rather than being led to slaughter and placing blame elsewhere.

Like everything in the Stock Market, MicroCaps are down. As of EOD on June 2022, the MicroCap Review (MCRI), our proprietary MicroCap index tracking MicroCap performance, is down 26.73% YTD; the only index we track that is doing worse is NASDAQ, which is down 31.36% YTD. I don’t want to spend time this editorial discussing why; I highly recommend tuning into Planet MicroCap Podcast to hear what my guests have to say about the matter. The real ques tion is, well, now what? The summer is an opportune time to start reflecting on what your financial goals are for the near and long term using some of the data enclosed in this issue of the magazine, as well as macro data/indicators. Few things we are certain of right now: liquidity has dried up, interest rates have gone up (and probably will continue to) in order to rein in inflation, high flying growth names have taken it on the chin. There’s actually a bunch of things that we’re now certain of, but at the end of the day, despite rising inflation, this

WaiTiNg oN EDiToriaL

F EATURESFallen Angels: Devoting Time to Companies that May Not Be Buyable at the Moment by Ben Claremon, Cove Street Capital

Fallen Angels: Pay Attention to Changes in Sector Money Flows by Fadi Diab, @TheGladiatorHC

The Utility of the Future by Peter Londa, CEO, Tantalus (TSX: GRID)

The Case for Bridging the Gap Between TradFi and DeFi by Caitlin Cook, Host, The DeadCaitBounce Experience

Is Gold Losing Its Lustre? Or Are We Just Short-sighted? by Gavin Wendt, MineLife

Incorporating EOS® into Succession Planning by Jackie Kibler

Understanding Blue Sky Laws by Andy Kyzyk, OTC Markets Group

ESG for MicroCaps by Dr. Tim Siegenbeek van Heukelom, Socialsuite

Market Maker Corner: Market Making Explained by Eric Flesche, Glendale Securities

On-demand Accounting and Finance by Aaron Spool and Neil Reithinger, Eventus Advisory Group

Door Half Open by Drew Bernstein, CPA, Marcum, Bernstein & Pinchuk

32 Fallen Angels: Can Beaten-Down E-commerce and Software Stocks See a “Resurrection?” by William Duberstein, Stone Oak Capital

44 Fallen Angels: When Optimistic Projections and Growth Don’t Add Up by Tim Travis, T&T Capital Management

“An Exercise in Clear Thinking” by Richard Revelins, Peregrine Corporate

Ask Mr. Wallstreet: Shorts by Shelly Kraft 100 Imaging Biometrics, LLC, a subsidiary of IQ-AI Limited (OTCQB: IQAIF) (LSE: IQAI) by Dr. Kathleen Schmainda, PhD 102 Bear Market Blues? by Roger Pondel, PondelWilkinson 106 Investor Relations for Bear Markets by Mike Porter, Porter, LeVay & Rose 108 Inflation, Inflation, Inflation. But What’s Going on With Gold & Silver? by David Morgan and Jon Little, The Morgan Report

The Micro-Cap IPO

by Lucosky Brookman LLP

Uplisting

Post-Pandemic

As long as children with rheumatic and congenital heart disease around the world continue to suffer without access to care, we will treat children, train medical professionals and raise the level of pediatric heart care worldwide, from our heart in Israel. From the children and parents with the courage to trust, to the doctors with courage to heal, we are SAVE A CHILD’S HEART.

For the past 25 years Save a Child’s Heart has treated over 6,000 Children from 64 different countries. Children are treated regardless of race, religion, gender, nationality or financial status. 50% of the children are from the Palestinian Authority and Gaza, Iraq, and Morocco, more than 40% are from Africa, and the remainder are from Asia, Eastern Europe, and the Americas. It only costs $15,000 USD to save a child in need.

Norah - Zambia“Join us and together let us make the network to help children with heart disease globally big enough to be equal to the task. There is work for everybody. There are no dollars and cents in it, but it is worth a fortune."

-Dr. Ami Cohen Founder of Save a Child’s Heart

-Dr. Ami Cohen Founder of Save a Child’s Heart

Itoccurs to me that just about every investor will have a different definition of what he or she considers a fallen angel. To me, a simple definition would be a high return, growing company that previously was held in high regard by the stock market, but whose price has fallen from previously lofty levels. Markets vacillate between greed and fear and during times when people are fearful, there is the opportunity to buy really good businesses at much more reasonable valuations. Now, all of that makes for some nice bullet points within an investor presentation but the important question is: how does an investor position himself or herself to be able to benefit from temporary to slightly longer lasting dislocations? We were reminded in March and April of 2020 that in times when markets are falling quickly, it is very hard to perform a deep diligence process on a brand new company. During such times, investors invariably have to engage in triage within their existing portfolios and prioritize businesses they have researched in the past when deciding what to add to the portfolio. Ideally, what I want during a market downturn is to have a list of wide moat businesses within secular tailwinds that I have done a fair amount of diligence on. If I have done the work and established prices at which I would be excited to own such companies, it is much easier to perform a small amount of additional diligence and then act swiftly.

Again, all of that sounds great in theory. But, with thousands of publicly traded securities within my investment universe, how do you I decide to devote my limited time to a company that may not be buy able at the moment? It is always a tough decision and I know I don’t always get this right. However, my strategy is to spend time on companies that trade at

valuations just outside of what I consider reasonable, given the returns and growth profile of the company. These can be companies that have gone from being insanely valued to merely expensive or cult-like stocks that are always a little expensive. Build an intellectual history with these companies, set a reasonable price at which to buy them and then wait for the vicissitudes of the market to hand you opportunities when the whole market goes down or when a stock has its own mini-recession.

I have long admired Trimble (Ticker: TRMB). The company has very solid margins and has shown impressive growth over the last 20 years. Trimble’s mission is to fundamentally change—via technology— some industries that have been quite slow to adopt new technology: engineering and construction, agriculture and transportation. These are verticals with huge TAMs so there is no reason to believe that Trimble won’t be able to grow consistently for the foreseeable future. The problem for someone with a value-bias is that the stock, which does have some end market cyclicality risk, is always “expensive.” Based on our standard deviation adjusted multiples, over the last 15 years the stock has traded at aver age EV/EBITDA and P/E multiples of 17.8x and 36.4x, respectively.

The stock has gone from being very rich to just ex pensive and that has made it a priority for me. I bring up Trimble because I think the stock is emblematic of the type of situations I look for, as described above.

In your opinion, is now the time to consider looking at companies considered by your definition to be “Fallen Angels”?

I think investors need to be careful. To me, compar ing a stock’s current price to the 52-week high it hit in late 2021, for example, is potentially quite misleading and dangerous. In our office, I have recently heard the question “what in the world was the market thinking when the stock was $X eight months ago?” quite often. Anchoring to previous stock prices as if they represented anything but noise is a good way to lose a lot of money. Also, there are plenty of COVID beneficiaries that were clearly over-earnings but the market—in my opin ion—did not do a great job at recognizing that until recently. So, determining the core earnings power or

true growth profile can be quite challenging.

So, the short answer is yes, there are more interest ing companies showing up on our screens than in early 2022. But, like during most of recent history outside of early 2020, it is prudent to be highly selective.

Ben Claremon joined Cove Street in 2011 as a research analyst. He also serves as a Co-Portfolio Manager for our Classic Value | Small Cap Plus strategy. Previously he worked as an equity analyst on both the long and the short side for hedge funds Blue Ram Capital and Right Wall Capital in New York. Prior to that, he spent four years with a family commercial real estate finance and management business. Mr. Claremon was also the proprietor of the value investing blog, The Inoculated Investor. He is now the host of the Compounders podcast. His background includes an MBA from the UCLA Anderson School of Management and a BS in Economics from the University of Pennsylvania’s Wharton School.

Disclosure: Ben Claremon does not own any shares in Trimble.

DISCLAImER AND FORWARD-LOOKINg STATEmENTS NOTICE: This article is provided as a service of SNN inc. or an affiliate thereof (collectively “SNN”), and all information presented is for commercial and informational purposes only, is not investment advice, and should not be relied upon for any investment decisions. We are not recommending any securities, nor is this an offer or sale of any security. Neither SNN nor its representatives are licensed brokers, broker-dealers, market makers, investment bankers, investment advisers, analysts, or underwriters registered with the Securities and Exchange Commission (“SEC”) or with any state securities regulatory authority

SNN provides no assurances as to the accuracy or completeness of the information presented, including information regarding any specific company’s plans, or its ability to effectuate any plan, and possess no actual knowledge of any specific company’s operations, capabilities, intent, resources, or experience. any opinions expressed in this article are solely attributed to each individual asserting the same and do not reflect the opinion of SNN. information contained in this presentation may contain “forward-looking statements” as defined under Section 27a of the Securities act of 1933 and Section 21B of the Securities Exchange act of 1934. Forward-looking statements are based upon expectations, estimates, and projections at the time the statements are made and involve risks and uncertainties that could cause actual events to differ materially from those anticipated. Therefore, readers are cautioned against placing any undue reliance upon any forwardlooking statement that may be found in this article.

SNN does not receive compensation for, nor engage in, providing advice, making recommendations, issuing reports, or furnishing analyses on any of the companies, securities, strategies, or information presented in this article. SNN recommends you consult a licensed investment adviser, broker, or legal counsel before purchasing or selling any securities referenced in this article. Furthermore, it is encouraged that you invest carefully and consult investment related information available on the websites of the SEC at http://www.sec. gov and the Financial industry Regulatory authority (FiNRa) at http://finra.org.

Note: This article is not an attempt to provide investment advice. The content is purely the author’s personal opinions and should not be considered advice of any kind. Investors are advised to conduct their own research or seek the advice of a registered investment professional.

EB: Reliance Global Group, Inc. (NASDAQ: RELI, RELIW) is an insurtech company combining advanced technologies, with the personalized experience of a traditional insurance agency model. Reliance Global Group’s growth strategy includes both an organic expansion, through its InsurTech platforms, 5Minu teInsure.com , its business-toconsumer platform, and RELI Exchange , its business-tobusiness platform for agency partners, as well as acquiring well managed, undervalued and cash flow positive insurance agencies.

• Successful track record of acquiring cash flow positive ‘offline’ home and auto agencies, and utilizing technology to more cost effectively service the acquired policies and enhance profit ability

• Capitalizing on consumer shift to ‘online’: more and more customers search for insurance online, but consumers prefer the personal touch of an agent

o 5minuteInsure.com is Reliance Global Group’s online business-to-consumer plat form and utilizes artificial intelligence and data mining, to provide competitive insur ance quotes within 5 minutes, with minimal data input.

o RELI Exchange is Reliance Global Group’s B2B InsurTech platform and agency partner network for insurance agents and agencies, leveraging the 5 Minute Insure quoting plat

form alongside a custom white label website. RELI Exchange is designed to give independent agents an entire suite of business development tools, allowing them to effectively compete and win against national agencies.

• By implementing artificial intelligence and robotic process automation (RPA) and, Reliance can:

o Dramatically reduce cost to write new business and maintain clients.

o Allow agents to focus on selling new policies

o Create a digitally empowered and scalable insurance agency model

• Ability to rapidly expand Reliance’s agency net work nationwide, driving margin expansion

RK: HOW WOULD yOU DESCRIBE THE COmPANy’S PERFORmANCE TO THIS POINT (BEgINNINg OF SEPTEmBER 2022) IN THE yEAR? HAvE yOU REACHED THE mILESTONES AND gOALS THAT yOU SET FOR THE COmPANy?

EB: In the second quarter of 2022, we achieved a 92% year-over-year increase in revenue compared to the last year’s second quarter. This growth has been driven by our proven acquisition strategy and the increasing successes of our recent acquisitions, JP Kush & Associates, Medigap Health Insurance Company and most recently, Barra & Associates, which was subsequently relaunched as the highly successful, RELI Exchange.

We were enthusiastic when we acquired Barra & Associates in April of this year. We viewed Barra as a highly strategic acquisition, one that was extreme ly complementary to our existing offerings and, more importantly, the perfect vehicle with which to support our nationwide expansion plans. This was exactly the type of transaction we had been searching for, as it added more than sixty agents and agency partners to our existing agency partner network, and we believed we could scale the busi ness both rapidly and cost-effectively. More impor tantly, Barra brought an advanced technology infra structure that was well-aligned with our acquisition strategy. By combining 5MinuteInsure.com, with the Barra technology infrastructure, we saw this acquisition as an opportunity to create synergies for growth, including the affiliated-agent business model.

Barra was relaunched as RELI Exchange, a first in class, business-to-business InsurTech platform and agency partner network that builds on the artificial intelligence and data mining backbone of 5MinuteInsure.com, a platform that was designed to target the direct-to-consumer market. We are proud to report that in just three short months, we have aggressively grown our agency and partner network by more 30% illustrating both the strength of the platform as well as its popularity with our agency partners. The platform is designed to pro vide instant and competitive insurance quotes from more than thirty insurance carriers nationwide in just a few minutes. In addition, it reduces an agent’s back-office burden and expenses by eliminating paperwork, thus providing the agent with more time to focus on their clients, selling policies, and building their businesses.

Unlike a franchise model, RELI Exchange was designed with both a low barrier to entry as well as a compelling value proposition that we believe has contributed to the accelerated growth of our agency partner network we are currently experienc ing. The response from agents using the platform, whether our in-house agents now transitioning to RELI Exchange, or our new, outside agency part ners that have embraced the platform, has been overwhelmingly positive. They are reporting to us that they are experiencing a positive impact on their business since moving onto the RELI Exchange plat form.

• The U.S. insurance broker and agency industry gen erated revenue of $182 billion in 2020. The market has grown steadily over the past 5 years due to macroeconomic growth, beneficial legislation, and positive trends within the insurance sector.

• The InsurTech industry is poised to disrupt the insurance industry, in much the same way the fin tech market has disrupted the financial services industry. InsurTech refers to the use of technol ogy innovations designed to squeeze out savings and efficiency from the current insurance industry model.

• The industry itself is projected to grow to a $11.2 billion global industry by the year 2027, as per AllTheResearch. InsurTech is disrupting an industry once known for having to call individual agents with little price transparency, and much like its FinTech forefathers, streamlines the trans action processes and provides significant eco nomic value for consumers.

• Reliance Global brings its thirty plus years of insurance industry experience to 5MinuteInsure. com and RELI Exchange. Reliance Global backs 5MinuteInsure.com and RELI Exchange with a combined blend of technology and insurance expertise, through advanced innovation, a net work of independent agents, and solid relation ships with top-rated insurance companies. As a result, 5MinuteInsure.com literally brings its cus tomers success in minutes, and RELI Exchange helps lead agents to similar success.

RK: 2022 HAS BEEN A vOLATILE yEAR FOR mICROCAPS AND A NUmBER OF mACRO TRENDS THAT yOU HAvE TO PAy ATTENTION TO AS WELL (WAR IN UKRAINE, SUPPLy CHAIN, INFLATION, ETC…). WHAT HAS BEEN yOUR STRATEgy TO NAvIgATE THROUgH THESE CHALLENgES?

EB: On the business-to-business side of the busi ness, while these macro trends do not have a direct impact on Reliance, the uncertainty they cre ate may cause people to try and find new ways to secure their financial futures and this may actu ally lead more people towards entrepreneurship. In turn, this may result in an uptick in the number of people looking to open up their own insurance business and become a part of the RELI Exchange network, which immediately provides them a plugand-play solution, with the look and feel of a sig nificant agency.

Looking at it from the consumers point of view, dur ing difficult economic times, people look to save money where they can, and both 5MinuteInsure. com and the RELI Exchange platforms can help consumers do that as they are designed to provide instant and competitive insurance quotes from more than thirty insurance carriers nationwide. In addition, historically, in this type of macro environment, the insurance industry has typically been very strong.

RK: WHAT ARE SOmE OF THE COmPANy’S vALUE CATALySTS FOR THE REST OF 2022, gOINg INTO 2023?

EB: We believe we have a best-in-class platform and are not aware of any other offering in the insur

ance industry with the speed, or versatility of RELI Exchange. We look forward to continuing to aggres sively add new agency partners to our network and believe this will have a multiplier effect on the growth of our business. Using the proprietary soft ware which we developed, the agency network we have built is highly scalable, and we believe it will provide us with the ability to grow our business line significantly with little additional costs. Our goal is to build RELI Exchange into the largest agency partner network in the country and we believe the results we have already experienced demonstrate that we are, indeed, on the right path.

For more information about Reliance Global Group, please visit: www.relianceglobalgroup.com

regulatory authority

SNN provides no assurances as to the accuracy or completeness of the information presented, including information regarding any specific company’s plans, or its ability to effectuate any plan, and possess no actual knowledge of any specific company’s operations, capabilities, intent, resources, or experience. any opinions expressed in this article are solely attributed to each individual asserting the same and do not reflect the opinion of SNN.

information contained in this presentation may contain “forward-looking statements” as defined under Section 27a of the Securities act of 1933 and Section 21B of the Securities Exchange act of 1934. Forward-looking statements are based upon expectations, estimates, and projections at the time the statements are made and involve risks and uncertainties that could cause actual events to differ materially from those anticipated. Therefore, readers are cautioned against placing any undue reliance upon any forwardlooking statement that may be found in this article.

The company profiled has paid consideration to SNN or its affiliates for this article. SNN does not engage in providing advice, making recommendations, issuing reports, or furnishing analyses on any of the companies, securities, strategies, or information presented in this article. SNN recommends you consult a licensed investment adviser, broker, or legal counsel before purchasing or selling any securities referenced in this article. Furthermore, it is encouraged that you invest carefully and consult investment related informa tion available on the websites of the SEC at http://www.sec.gov and the Financial industry Regulatory authority (FiNRa) at http://finra.org.

Children provides a lifetime of healing for those whose lives have been forever changed by terrorism, military conflict or mass violence.

Will you help a child who is coping with the aftermath of a

Make a

For more

clothing donation, become a youth

simply call and tell us how you'd like to get involved. Our families need your support.

please call

visit

with

The utility of the future will face a perfect storm of operational and environmental challenges.

Itis a future in which demand for power threatens to exceed supply, electric vehicles (“EVs”) and distributed energy resources (“DERs”) threaten to destabilize the grid with power generated at the grid edge, and extreme weather events threaten to make power outages the new norm. It’s a future in which utilities need more visibility, flexibility and control at the edge than ever before. The only way to thrive in this future is for electricity and data to flow together, in parallel, all the way from SCADA to the edge.

In short, the utility of the future needs to make every kilowatt and kilobyte count. It’s the only way for utilities to achieve true sustainability across all core functions—finances, operations, environmental impact, regulatory compliance, and serving their communities.

It’s plain to see wherever we look—EV adoption, online shopping, cloud computing and server farms, computer chips embedded in every device and appliance across all industries—virtually every aspect of daily life is becoming electrified and connected.

With the continued acceleration of this trend, the United States EIA expects global energy demand to increase 47% in the next 30 years.

The bottom line is, we need as much reliable electric ity as possible. Because of electric vehicle adoption alone, it is estimated that U.S. power production will need to double by 2050.

Because of government policy, increasing regula tions and consumer demand, people everywhere are investing more in renewable energy and trying to move away from fossil fuels and coal. Renewables are becoming a greater share of total energy output while traditional sources of power production are declining.

In addition, consumer adoption of technologies such as rooftop solar, home battery storage and EVs is putting an even greater strain on a grid that is already outdated and in dire need of modernization. The traditional distribution grid was never designed to absorb consumer-generated electricity at this

level. Without additional visibility at the edge and the ability to safeguard transformers, utilities face major safety issues and operational risks.

Wildfires, hurricanes, heatwaves, winter storms and other extreme weather events are impacting the electric grid on a global scale, resulting in increasingly frequent outages that threaten lives and livelihoods. With an 83% increase in extreme weather disasters from 2000 to 2020, grid resilience has never been more important, nor has the need for more visibility, command and control at the edge. This is yet another reason we need kilowatts of electricity and kilobytes of data flowing seamlessly together from headquarters to the edge and back in near real time.

Increased demand for power. New consumption pat terns and consumer-generated power at the edge. A reduced ability to scale. A world that is becoming more volatile with each passing year. These are just a few examples of what we are dealing with today, and it’s only getting more intense.

That is why the utility of the future will need more visibility, which will enable more command and con

trol at the edge than ever before. It is the only way to safeguard the communities who rely on public power. There is no room for waste. There will be no surplus ... and there is less room for error in the face of an emergency. At the same time, transformative new data-driven technologies are emerging, making it possible for utilities to deliver innovative services to the community.

Fortunately, there is a way for utilities to not only become truly sustainable in the face of all this change, but to become innovative change agents, themselves. There are ways to improve reliability and resilience, offer valuable new services and power the next generation of connected devices. But the only way to get there is with a direct line of sight into what is unfolding at every point along the distribution grid—from headquarters, to the substation, to the meter and into the premise—and that takes a truly interoperable and secure smart grid.

The utility of the future needs to achieve true sus tainability along five critical vectors:

But to create inherent sustainability for a utility’s operations, finances, environmental impact, regula tory compliance and community empowerment, it is critical to first reimagine the smart grid as an intrinsically interoperable platform. It is a platform that operates less like a one-way, analog delivery grid and much more like a neural-network comput ing grid. It is a platform in which each kilowatt of electricity is paired with contextual data about the electricity itself. It is a platform in which granular data can be accessed, transported and analyzed in real time along any point of the grid, including behind the meter, no matter the device or protocol.

What was once a one-way flow of power ...

and micro-grids are all now contributing to the flow of power through EV and DER adoption.

With so much happening behind the meter, utilities need visibility, command and control from headquar ters to the substation and straight into the home or business. In short, utilities need SCADA all the way to the edge.

… has become a multi-directional, decentralized network of connected devices. Homes, businesses

This is a bold vision, yes—but it’s one Tantalus is already making a reality. This is a vision we must continue to work towards if utilities are to continue powering the next decade of prosperity for their cities. Because managing electricity with up-to-themoment data is the only way utilities can achieve the visibility that enables the command and control they need to adapt to an increasingly unpredictable future.

Now, as with any data-driven platform, cybersecurity is of paramount importance. Data interoperability helps make the entire grid more resilient through bet ter supply-and-demand forecasts and responsiveness to extreme weather events. But that kind of interoper ability comes with risks. One industry expert observed that between 2018 and 2020, 10% of ransomware attacks on industrial assets targeted utilities.

As the grid becomes increasingly digitized, we should expect it to become more susceptible to attacks from hackers. Still, there are many paths to hardening the grid against cyberattacks, including virtual private networks. Blockchain is another technology that promises to offer unprecedented levels of security against such threats. The point is, with every new opportunity comes a new threat— and vice versa.

To make every kilowatt count, every kilowatt must be counted, and that requires robust and up-to-themoment data. Utilities everywhere must become as proficient in the flow of data as they are in managing the flow of electrons. But to make the most of this data, utilities need real-time awareness of their entire grid—from HQ through the substation to the meter and into the premise. This is the only way to boost reliability, enhance resilience, and innovate new services.

Some utilities are already starting to leverage real-time data and interoperability to increase efficiencies, reduce costs, increase security, get ahead of regulation, and harness new revenues and technologies. Here are just a few examples of what is possible for the data-driven utility of the future:

• Increase efficiencies: Power generation at the edge can be more easily managed through AIdriven substation automation, reducing all the functions of a substation to the software level.

• Reduce costs: Automation enabled by real-time data extends the life of substation transformers, while utilizing high- capacity battery storage to backup older equipment.

• Increase security: Virtual Private Networks with advanced cybersecurity methodologies create a secure environment to access, transport, and deliver all real-time and near real-time data for the utilities of the future; and future blockchain applications hold even more promise for security.

•

Anticipate regulation: Utilities can no longer think like monopolies, and the best way for utilities to get ahead of new regulations and requirements is to embrace the data and innovate.

• Harness new revenues: Fiber-to-the-Home creates a direct pipe into residences, making it possible to deliver new value-added services. The digitized grid and behind-the-meter capa bilities allow utilities to deliver more power—not less—to those incorporating EV chargers and other elements of the Electrification of Every thing.

• Leverage blockchain: A digitized grid empow ers the use of blockchain to connect and track the transactional aspects of the system, including the use of cryptocurrency to prevent the waste of unused green energy. Blockchain also promises to transform grid security in the future. In fact, many industry experts consider blockchain to be one of the most disruptive new technologies on the horizon for utilities, second only to artificial intelligence.

•

Embrace other disruptive technologies: A digitized grid powered by multi-directional real-time data lets utilities not only power increasingly energy-intensive applications and devices; it also allows utilities to incorporate transformative data-driven technologies into their own operations, providing a platform for continuous innovation.

Tantalus is the ideal partner to give utilities the visibility, command and control of their grids so they can thrive in any future scenario. Our technology platform— which includes hardware, software and interoperable data-driven services— provides the ideal foundation for continuous adaptation, evolu tion and innovation.

For the nation’s utilities, the time is now to move beyond the one-directional, siloed mentality that permeated electricity providers in the 20th Century. No utility can simply buy power from generators and then sell it to homes and businesses. Those that continue down that path will find their operations sputtering as their communities suffer from a lack of investment and growth.

Increasing demand for energy, the rise in EVs and DERs, extreme weather events, and the ongoing demand for innovative, data-driven services—these trends are not solved by the mere delivery of energy.

These trends are answered by a reliable, robust, smart and truly interoperable smart grid network.

To proactively manage that kind of grid, every counted kilowatt needs a corresponding kilo byte—traveling in tandem and being made fluid and flexible by a smart grid platform that covers the enterprise to the edge, and from operations to the consumer. When every kilowatt counts, utilities achieve an operational efficiency that enables them to adjust to our shifting world.

For more information about Tantalus and our solu tions, visit, www.tantalus.com

DISCLAImER AND FORWARD-LOOKINg STATEmENTS NOTICE: This article is provided as a service of SNN inc. or an affiliate thereof (collectively “SNN”), and all information presented is for commercial and informational purposes only, is not investment advice, and should not be relied upon for any investment decisions. We are not recommending any securities, nor is this an offer or sale of any security. Neither SNN nor its representatives are licensed brokers, broker-dealers, market makers, investment bankers, investment advisers, analysts, or underwriters registered with the Securities and Exchange Commission (“SEC”) or with any state securities regulatory authority

SNN provides no assurances as to the accuracy or completeness of the information presented, including information regarding any specific company’s plans, or its ability to effectuate any plan, and possess no actual knowledge of any specific company’s operations, capabilities, intent, resources, or experience. any opinions expressed in this article are solely attributed to each individual asserting the same and do not reflect the opinion of SNN. information contained in this presentation may contain “forward-looking statements” as defined under Section 27a of the Securities act of 1933 and Section 21B of the Securities Exchange act of 1934. Forward-looking statements are based upon expectations, estimates, and projections at the time the statements are made and involve risks and uncertain ties that could cause actual events to differ materially from those anticipated. Therefore, readers are cautioned against placing any undue reliance upon any forward-looking statement that may be found in this article.

The company profiled has paid consideration to SNN or its affiliates for this article. SNN does not engage in providing advice, making recommendations, issuing reports, or furnish ing analyses on any of the companies, securities, strategies, or information presented in this article. SNN recommends you consult a licensed investment adviser, broker, or legal counsel before purchasing or selling any securities referenced in this article. Furthermore, it is encouraged that you invest carefully and consult investment related information available on the websites of the SEC at http://www.sec.gov and the Financial industry Regulatory authority (FiNRa) at http://finra.org.

For a micro-cap company to see significant share price appreciation, it needs two main things to go its way. Firstly you obviously need the management and board of directors to work together to achieve the specific objectives they set out to achieve. With each milestone being met the company theoretically should see an increase in its valuation and share price. Secondly the sector itself

needs some tailwinds to bring in broader market support and money flow. As macro factors benefit a specific industry or natural resource, money starts flowing down into the smaller end of town, i.e. micro-cap stocks, as their propensity to achieve substantial percentage gains are much higher than large cap stocks. A fallen angel, in my opinion, is a stock that benefited from these two factors and as

How would you define a company that is labelled a “Fallen Angel”?

consequence enjoyed the share price increasing by many multiples which then had to deal with the removal of one or both of these factors. Most of the time the factor that changes is the money flow into that sector drying up which drags the share price and valuations of these stocks down, regardless of how much the management team have achieved.

I recently conducted an exercise of reviewing 600+ micro-cap stocks with the intent of trying to find hidden gems. The vast majority of these stocks were trading at a 50-80% discount to their highs prior to the stock market correction starting at the end of 2021. Each of these companies suffered greatly with the liquidity drying up in the micro-cap space as institutions and retail investors took a risk off mental ity. To give an example I’ll use a company called ADN or Andromeda Metals Ltd which is listed on the ASX. For transparency sake, I have never owned this stock nor do I intent on buying it in the future. ADN

is a natural resource explorer focussed specifically on Kaolin assets. This sector had a magnificent run in 2019-2020 and subsequently with ADN discovering a very good asset, its share price rose from 0.5c to over 40c during that period. Since that high in March 2021 it has substantially decreased to a current share price of about 5c. So you can see how easily a sector moving out of favour with the market can affect its share price.

From my perspective, my strategy is focussed on finding unloved stocks, trading at a very small enter prise value which the market has yet to pick up on. So I personally very rarely buy stocks that are con sidered to be ‘fallen angels’. This doesn’t mean that considering fallen angels isn’t a viable strategy, rather my own strategy concentrates on looking forward to a sector that hasn’t been re-rated yet because the trigger for that hasn’t happened yet. For example in 2018/19 I was very bullish on the short-medium term future of rare earths and as such I purchased a stock in my $50k challenge at 0.5c which met most of the criteria in my strategy. Off the back of the US/China trade wars the whole sector took off and my stock, as well as many others in this industry, substantially re-rated. So using this strategy, if you can time the sector money inflows and outflows, you can purchase a stock before the market is aware of it and sell it before it becomes a fallen angel.

Fadi Diab is a MicroCap investor and educator with a predominantly Aus tralian (ASX) focus. From an education perspective I created two courses that discuss in detail my end to end investment strategy developed over a 10 year period. I also am the owner of my website www.thespecinvestor. com.au and a Non-Executive Director of CarbonXT Group Limited. The author is not a shareholder of ADN.

DISCLAImER AND FORWARD-LOOKINg STATEmENTS NOTICE: This article is provided as a service of SNN inc. or an affiliate thereof (collectively “SNN”), and all information presented is for commercial and informational purposes only, is not investment advice, and should not be relied upon for any investment decisions. We are not recommending any securities, nor is this an offer or sale of any security. Neither SNN nor its representatives are licensed brokers, broker-dealers, market makers, investment bankers, investment advisers, analysts, or underwriters registered with the Securities and Exchange Commission (“SEC”) or with any state securities regulatory authority

SNN provides no assurances as to the accuracy or completeness of the information presented, including information regarding any specific company’s plans, or its ability to effectuate any plan, and possess no actual knowledge of any specific company’s operations, capabilities, intent, resources, or experience. any opinions expressed in this article are solely attributed to each individual asserting the same and do not reflect the opinion of SNN. information contained in this presentation may contain “forward-looking statements” as defined under Section 27a of the Securities act of 1933 and Section 21B of the Securities Exchange act of 1934. Forward-looking statements are based upon expectations, estimates, and projections at the time the statements are made and involve risks and uncertainties that could cause actual events to differ materially from those anticipated. Therefore, readers are cautioned against placing any undue reliance upon any forwardlooking statement that may be found in this article.

SNN does not receive compensation for, nor engage in, providing advice, making recommendations, issuing reports, or furnishing analyses on any of the companies, securities, strategies, or information presented in this article. SNN recommends you consult a licensed investment adviser, broker, or legal counsel before purchasing or selling any securities referenced in this article. Furthermore, it is encouraged that you invest carefully and consult investment related information available on the websites of the SEC at http://www.sec. gov and the Financial industry Regulatory authority (FiNRa) at http://finra.org.

Note: This article is not an attempt to provide investment advice. The content is purely the author’s personal opinions and should not be considered advice of any kind. Investors are advised to conduct their own research or seek the advice of a registered investment professional.

From my perspective, my strategy is focussed on finding unloved stocks, trading at a very small enterprise value which the market has yet to pick up on. So I personally very rarely buy stocks that are considered to be ‘fallen angels’.

Dg: Crexendo (NASDAQ:CXDO) is an award-winning premier provider of Unified Communications as a Service (UCaaS), Call Center as a Service (CCaaS), communication platform software solutions, and collabora tion services with video designed to provide enterprise-class cloud communication solutions to any size business through our business part ners, software licensees, agents, and direct channels. Our solutions currently support over 2.5 million end users globally and was recently recognized as the fastest growing UCaaS platform in the United States. We provide our ser vices through two divisions, our Telecommunications Division, and our Software Solutions Division.

Dg: We are very pleased with Crexendo’s strong performance for the first half of 2022. Coming off of fiscal year 2021 where we saw a 71% increase in revenue and strong Non-GAAP earnings of $1.7M on total revenues of $28.1M, we have continued that strong momentum into the first half of 2022. YTD 2022 revenue is up 65% year over year to $17M with Non-GAAP income of $917K and Adjusted EBITDA of $928K YTD.

In addition, we increased our contractual backlog by 54% to $42.2M compared to Q2 of 2021. This

number represents all of the con tracted revenue that we have yet to recognize and will benefit from as it converts to revenue monthly over the next 60 months.

With strong revenue growth, strong cost management, improving gross margins that are close to 70% and a very strong balance sheet with virtually no debt, we are positioned well for the future.

As we started 2022, we highlighted to our shareholders that we would recognize cost synergies from our acquisition of NetSapiens in 2021 which we have successfully accomplished. We also committed to improving our gross margins and Non-GAAP income which we have done as well. We are committed to continuing our strong organic growth and continue to aggres sively explore inorganic growth through acquisitions within our existing licensee community.

Dg: Yes, the adoption of the Cloud for business communications continues at a very rapid pace. In the US market, approximate 55% of businesses have yet to migrate to the Cloud for their communications. It is not a matter of “if” but rather “when” these businesses will convert their older, legacy telephone systems to the Cloud. Covid hastened the migration of businesses to cloud communications due to the benefits like mobility, work from anywhere, and video collaboration that our solutions provide. Since businesses need more flexibility in their communica

tion solutions, Crexendo’s solutions are the prefect fit for them. Our solutions make businesses more efficient, improves internal and external communica tions, and in most instances saves businesses money over their less effective premise-based telephone systems.

Since approximately 55% of businesses in the US still need to migrate to the Cloud for their com munications, this is the tailwind that will drive these businesses to companies like Crexendo and ensure our strong and continual growth.

RK: 2022 HAS BEEN A vOLATILE yEAR FOR mICROCAPS AND A NUmBER OF mACRO TRENDS THAT yOU HAvE TO PAy ATTENTION TO AS WELL (WAR IN UKRAINE, SUPPLy CHAIN, INFLATION, ETC…). WHAT HAS BEEN yOUR STRATEgy TO NAvIgATE THROUgH THESE CHALLENgES?

Dg: Crexendo has had and always will have an inherent focus on fundamentals which we believe helps us weather any stormy challenges that arise. With a focus on top line growth, cost management, and non-gaap income while maintaining a pristine balance sheet, we feel we are well positioned in good times and bad. Our solutions, although not recession proof, are very suited for businesses regardless of economic headwinds as all businesses need to communicate effectively and our solutions make businesses more productive and efficient and typically saves businesses between 20-50% on older legacy telecom solutions. This is a very appealing message to businesses regardless on the state of the economy. In addition, we have been able to

navigate well through all of the supply chain issues with proper planning and product management that have allowed us to not be affected in this area at all. We continue to execute on our game plans as is evident by our continued growth and top and bottom line performance.

Dg: We believe our company is significantly undervalued and is a diamond in the rough in a very challenging equities market. With strong revenue growth of 65% YTD and strong non-gaap earnings of $917K YTD, we are positioned nicely for continued growth. Our gross margins have improved signifi cantly in 2022 and we expect those trends to con tinue. We have over $42M in contracted revenues that will be recognized over the next 60 months which should be viewed very favorably. With a very strong balance sheet with virtually no debt, we are not impacted by raising interest rates that has crippled many of our competitors. On top of all of these positives is a very strong pipeline for possible acquisitions that will help our inorganic growth for years to come as we look accretive acquisitions from within our existing base of over 200 UCaaS licensees that use our platform today.

For more information about Crexendo, Inc., please visit: www.crexendo.com

DISCLAImER AND FORWARD-LOOKINg STATEmENTS NOTICE: This article is provided as a service of SNN inc. or an affiliate thereof (collectively “SNN”), and all information presented is for commercial and informational purposes only, is not investment advice, and should not be relied upon for any investment decisions. We are not recommending any securities, nor is this an offer or sale of any security. Neither SNN nor its representatives are licensed brokers, broker-dealers, market makers, investment bankers, investment advisers, analysts, or underwriters registered with the Securities and Exchange Commission (“SEC”) or with any state securities regulatory authority

SNN provides no assurances as to the accuracy or completeness of the information presented, including information regarding any specific company’s plans, or its ability to effectuate any plan, and possess no actual knowledge of any specific company’s operations, capabilities, intent, resources, or experience. any opinions expressed in this article are solely attributed to each individual asserting the same and do not reflect the opinion of SNN. information contained in this presentation may contain “forward-looking statements” as defined under Section 27a of the Securities act of 1933 and Section 21B of the Securities Exchange act of 1934. Forward-looking statements are based upon expectations, estimates, and projections at the time the statements are made and involve risks and uncertain ties that could cause actual events to differ materially from those anticipated. Therefore, readers are cautioned against placing any undue reliance upon any forward-looking statement that may be found in this article.

SNN does not engage in providing advice, making recommendations, issuing reports, or furnishing analyses on any of the companies, securities, strategies, or information presented in this article. SNN recommends you consult a licensed investment adviser, broker, or legal counsel before purchasing or selling any securities referenced in this article. Furthermore, it is encouraged that you invest carefully and consult investment related information available on the websites of the SEC at http://www.sec.gov and the Financial industry Regulatory authority (FiNRa) at http://finra.org.

Republican or Democrat? Still or sparkling? Cats or Dogs? No matter how serious or insignificant the topic, society at large has historically fallen prey to the simplicity of polarization. It’s a tale as old as time that repeats itself over… and over… and over again.

many issues with viewing the world strictly through a lens of binary choice, but the biggest one of all is the loss of much needed nuance.

Polarizing takes are nothing more than first order thinking. It’s easy; the path of least resistance. Pick a camp, and stick around people who will reinforce what you’ve taught yourself to be true. It’s easier to stubbornly pick a side than it is to take a thoughtful and well researched approach. Polarizing takes are often the ones that get air time. They can be thoroughly entertaining. But that doesn’t make them accurate. In fact, the truth rarely lies in the extremes.

Given the current state of the world, we see this play out in nearly every aspect of life: people fight over the extremes when, in reality, the answer lies some where in the middle. Within financial services, the topic du jour is Crypto, and the crux of most argu ments can be boiled down to one simple question: are you willing to embrace change and the inherent messiness that comes with it?

The history of the world is filled with countless examples of innovations put into place to make our lives easier. Faster. Cheaper. More efficient. Block chain technology is, at its core, nothing more than the latest in a long line of technological advances brought about to improve the systems we use every

day. BUT, what many people get wrong on the topic of crypto is that we can blaze a new path forward and leave legacy systems behind in the process.

The path forward cannot be paved without the cooperation of legacy incumbents. Change is uncomfortable, but market innovation doesn’t happen in a bubble, it happens for a reason: we’ve already started to see collaboration and targeted efforts by some of the largest firms in the financial

world. This was not done in haste. The Blackrocks and Fidelitys of the world see what I see: traditional and decentralized finance weren’t designed to be mutually exclusive; the best of each system will come together to build a better future. Progress requires collaboration from both sides.

For traditional finance (TradFi) participants, collabo ration means the following (and much more):

• Ensuring regulatory bodies get educated and have open dialogue with top builders in the space to blaze a path forward that encourages responsible innovation rather than stifles it (this is already happening!)

• Looking at the financial system as it stands today, acknowledging its many flaws (inefficien cies, inequities, costs, and more), and thinking about how to solve or mitigate them.

• Keeping an open mind and acknowledging the fact that innovation is always messy. There will be scams, things will break, and it won’t all last, but out of the chaos will come progress. Traditional finance participants who truly care about the long term growth and prosperity of the financial services industry should root for innovations that are intended to improve the space.

For decentralized finance (DeFi) builders and lead ers, collaboration means the following (and much more):

• Embracing the inevitable role of regulation in ensuring proper investor protections and implementation of guardrails put in place for the common good of all market participants

• Not abusing the information asymmetries inher ent with any up-and-coming technology for personal gain, and rather creating new solutions with long-term viability.

• Willingness to learn from legacy financial partici pants - how can you improve a system without intimate knowledge of how the system works to begin with?

• Chilling out on the over exuberant, maximalist attitude that so often deters newcomers from the space; patience, understanding, and educa tion are necessary for onboarding the masses, and leaders in the space should wield the power they have for good. Crypto builders who truly care about the long term growth and prosperity

of this nascent industry should take it upon themselves to help legacy firms cross the chasm.

TradFi participants who truly care about the long term growth and prosperity of the financial services industry should root for innovations that are intended to improve the space. It won’t be smooth sailing; we are in the early days of innovation and it will take many iterations to test and work out the kinks. DeFi builders who truly care about the long term growth and prosperity of this nascent industry should take it upon themselves to help legacy firms cross the chasm.

When it comes to onboarding the lion’s share of legacy financial participants, the most important component today is education. High quality content, from well versed crypto participants, written in a way that relates back to what traditional participants are familiar with (engineering jargon is intimidating and a huge barrier to entry - cut through it). TradFi participants need to be willing to listen with an open mind, and DeFi leaders need to be willing to put in the time and effort to teach. We can all learn from each other.

All of this is to say: there are choices, and the one you can make is to be progressive, innovate, and learn. Stagnation is death - sharks die if they stop swimming, why would you? As someone with a background in traditional asset management who has since made the transition to DeFi, I’ve made my choice and want to help others make educated choices as well.

My new podcast, the DeadCaitBounce Experience, was created with the sole purpose of helping TradFi onboard to DeFi. Listen in as I explore the relation ships I’ve cultivated both in TradFi and DeFi, and how they can better compliment each other to come up with something bigger than the sum of their parts. At the end of the day, you don’t have to change your mind… just open it.

Caitlin Cook is Head of Communications and Marketing at Hxro Labs and Host of the The DeadCaitBounce Experience Podcast. After starting her career in traditional asset management at Deutsche Bank, Caitlin transitioned to crypto in 2020 to spearhead the creation and develop ment of crypto education platform Onramp Academy. At Onramp, Caitlin oversaw content creation and presentation development for RIAs, family offices and other institutional allocators to help bridge the educational gap between traditional and decentralized finance. In June 2022, Caitlin became Head of Communications and Marketing for Hxro Labs - a Bermuda-based web3 development company and a core contributor to Hxro.

Note: This article is not an attempt to provide investment advice. The content is purely the author’s personal opinions and should not be considered advice of any kind. Investors are advised to conduct their own research or seek the advice of a registered investment professional.

MMuch is being made of gold’s recent price performance, with many questioning whether the yellow metal can still fulfill its traditional role as a safe-haven asset in turbulent times, as well as a hedge against skyrocketing inflation. After all, shouldn’t developments over the past couple of years – a global pandemic, unprecedented govern ment spending, European war, global uncertainty, and rampaging inflation - provide the perfect spring board for gold to thrive?

uch is being made of gold’s recent price performance, with many questioning whether the yellow metal can still fulfill its traditional role as a safe-haven asset in turbulent times, as well as a hedge against skyrocketing inflation. After all, shouldn’t developments over the past couple of years – a global pandemic, unprecedented govern ment spending, European war, global uncertainty, and rampaging inflation - provide the perfect spring board for gold to thrive?

The fact that questions are being asked about gold’s relevance is not at all a new phenomenon. Indeed, over recent decades with the advent of newfangled financial instruments and the emergence of cryptocurrencies, some speculators have become captivated by these shiny new financial market trinkets - to the detriment of gold.

The fact that questions are being asked about gold’s relevance is not at all a new phenomenon. Indeed, over recent decades with the advent of newfangled financial instruments and the emergence of cryptocurrencies, some speculators have become captivated by these shiny new financial market trinkets - to the detriment of gold.

But does this necessarily mean that gold is losing out in terms of performance? Gold’s relevance is typically measured and interpreted on the basis of its US dollar price performance - but this should not be viewed in perfect isolation - as gold’s perfor mance must also be viewed in the context of how it has performed in terms of other currencies, and also against other asset classes.

But does this necessarily mean that gold is losing out in terms of performance? Gold’s relevance is typically measured and interpreted on the basis of its US dollar price performance - but this should not be viewed in perfect isolation - as gold’s perfor mance must also be viewed in the context of how it has performed in terms of other currencies, and also against other asset classes.

Let’s begin with an examination of how gold has performed so far in 2022. Although gold is down for

Let’s begin with an examination of how gold has performed so far in 2022. Although gold is down for

the year in US$ terms below $1700, it is nevertheless outperforming most major asset classes - including Treasury bonds, U.S. corporate bonds, the S&P 500 and tech stocks. Gold has therefore effectively fulfilled its role as an insurance policy, by helping investors mitigate losses in other areas of their portfolio.

the year in US$ terms below $1700, it is nevertheless outperforming most major asset classes - including Treasury bonds, U.S. corporate bonds, the S&P 500 and tech stocks. Gold has therefore effectively fulfilled its role as an insurance policy, by helping investors mitigate losses in other areas of their portfolio.

Furthermore, the latest report by the World Gold Council (WGC) also makes the case that gold can typically be a powerful investment in the face of a potential economic recession. The London-based group has compared the performance of a number of asset classes during the course of the past seven U.S. recessions going back to 1971, and it has found that gold performed the best on average aside from government and corporate bonds.

The bottom-line therefore is that gold’s performance must not be viewed simply in terms of its US$ price performance in isolation, but it must also be viewed within the context of how well it has stacked up against other asset classes. On this basis, gold’s performance stacks up very well indeed.

Figure 1: gold versus other major asset classes over a 2-year period.

Furthermore, the latest report by the World Gold Council (WGC) also makes the case that gold can typically be a powerful investment in the face of a potential economic recession. The London-based group has compared the performance of a number of asset classes during the course of the past seven

What we know about gold so far in 2022 is that it has struggled in US$ price terms since April, due to the combined strength of a rampaging US dollar that is at fresh 20-year highs, along with the relent less march of the US Federal Reserve’s rate hike

“You have to choose between trusting to the natural stability of gold and the natural stability of the honesty and intelligence of the members of the government. And, with due respect to these gentlemen, I advise you, as long as the capitalist system lasts, to vote for gold.” —George Bernard Shaw