Submarine Telecoms Forum is published bi-monthly by WFN Strategies, L.L.C. The publication may not be reproduced or transmitted in any form, in whole or in part, without the permission of the publishers.

Submarine Telecoms Forum is an independent commercial publication, serving as a freely accessible forum for professionals in industries connected with submarine optical fibre technologies and techniques.

Liability: while every care is taken in preparation of this publication, the publishers cannot be held responsible for the accuracy of the information herein, or any errors which may occur in advertising or editorial content, or any consequence arising from any errors or omissions.

The publisher cannot be held responsible for any views expressed by contributors, and the editor reserves the right to edit any advertising or editorial material submitted for publication.

Contributions are welcomed. Please forward to the Managing Editor: Wayne F. Nielsen, WFN Strategies, 19471 Youngs Cliff Road, Suite 100, Potomac Falls, Virginia 20165, USA.

Tel: +[1] 703 444-2527, Fax:+[1] 703 444-3047.

Email: WNielsen@SubTelForum.com

General Advertising

Tel: +[1] 703 444 2527

Email: Advertising@SubTelForum.com

Designed and produced by Ted Breeze

Exordium

Ode to Ted

The reasons escape me today, but I went to work as Marketing Department Manager of BT Marine – Southampton in 1991 with the original intent of firing Ted Breeze’s ass. Instead, he took me to a pub on our second day where we talked and drank for several hours, and began both a professional and personal friendship that spanned our generational and cultural differences, and some 14 years.

Ted was from the old school, the print media, and everything he created, whether electronic or paper, had the look and feel of a glossy pin-up. He applied his earlier skills of photographing scantily clad models to that day’s cableships and trenchers and ploughs. And together we created “Soundings” and “Real Time,” and more recently, “Submarine Telecoms Forum,” as well as a plethora of high class brochures and tear sheets and ties and handkerchiefs and diaries and corporate images.

I had the pleasure of traveling to a dozen or more countries with Ted for various exhibitions over the years. I think my favorite was PTC in the early 1990s when our exhibition team wore matching orange and black BTM Hawaiian shirts, and by the end of the show, all of our customers and even our major competitor, CWM, wore Ted’s design. And every January, we held court together at the Royal Hawaiian’s Mai Tai Bar, and in several cases, way into the wee hours.

I know our losing of Ted on Christmas Eve in no way compares to the natural disaster not two days later, but he will nonetheless be sorely missed in our industry, as he was the only one of his ilk who could best depict an idea; he was truly a one-of-a-kind kind of guy.

So, Peg and Jack and I toasted you, Ted, in my Danish familial way, with a bottle of ice-cold Aquavit and a beer chaser on the night of news of your departing, and we told lots of funny reminiscences and “Breeze” anecdotes, and shed none too few tears as well. Your passing left a hole in my family; but as always, we’ll leave that stool open for you next week at the Mai Tai Bar.

Auf Wiedersehen, Wayne Nielsen

Globacom Planning Nigeria-UK Cable

Nigeria’s second national carrier, Globacom, is moving forward with its plans to build a submarine cable from Nigeria to the United Kingdom at a cost of US$170 million within the next year.

ARCOS Restoring Services After Two Cable Cuts

New World Network Ltd. has begun restoring international communications services to seven Latin American countries after the ARCOS fiber optic ring suffered two separate undersea fiber cuts within days of each other.

www.subtelforum.com/NewsNow/ 12_december_2004

AT&T Unveils New Internet Data Center in Singapore

AT&T has announced that it has opened a new Internet Data Center in Singapore and expanded its ability to offer businesses in the South East Asia region globally consistent managed hosting services. This latest center is AT&T’s sixth in the

Asia Pacific region and brings the company’s total to 26 worldwide.

www.subtelforum.com/NewsNow/ 2_january_2004

Contract for New Caribbean System Awarded

Alcatel has announced that it has signed a turnkey contract valued at 21 million Euros with Global Caribbean Network (GCN), a subsidiary of the Group Loret, to deploy a submarine cable network for the Regional Council of Guadeloupe.

www.subtelforum.com/NewsNow/ 29_november_2004

Global Marine Exits Administration with Approval of CVA Proposals

Peter Ford, CEO of Global Marine Systems Limited and his Leadership Team have announced the successful outcome of the recent process, which has enabled Global Marine to restructure its business to meet the needs of the marketplace.

www.subtelforum.com/NewsNow/ 21_november_2004

www.subtelforum.com/NewsNow/ 29_november_2004

EXECUTIVE FORUM

John Hibbard

Since 2001, John Hibbard has been a consultant with his own company, Hibbard Consulting Pty Limited, focusing primarily on the many facets of international telecommunications. John spent most of his career with Telstra and OTC. In the 7 years prior to his departure, John was Managing Director, Telstra Global Wholesale responsible for a team maintaining and growing Telstra’s international carrier business around the globe. John was also the Chairman of the Australia Japan Cable from its formation, having conceived the project and oversighted its execution. He was also elected by the industry to the Executive Board of the prestigious Pacific Telecommunications Council and is currently a member of its Advisory Council.

Are business conditions improving or getting worse, and are you optimistic or pessimistic about the future?

2005 looks like being a much improved year for the submarine cable industry. Clearly it won’t be the bonanza that was 1999 and 2000 but it looks like being a whole lot better than 2002 and 2003, and modestly better than 2004.

The rollout of broadband internet connections is reason for the positive tone. The emergence of cost effective offerings affording increased speeds at near to the same price as 56Kbps dial-up is causing a mass migration to the higher speed connections, whether effected through cable modems or ADSL. Measurements indicate that the average monthly download by a broadband customer is between 8 and 15 times that of a dialup customer. But more significantly, measurements suggest that the number is increasing when intuitively it should decrease as “less interested” users migrate.

me very optimistic about the future as its power should swamp the negative aspects, such as oversupply, still pervading the industry.

What do you see as the short term and long term health of the international telecoms industry?

“With internet connectivity being the prime driver, then the ISPs and those carriers who provide the interface to the submarine system operators will be the key customers in the submarine cable market.”

The Australian experience, of which I am familiar, is that in the year 2004, international capacity activation has exceeded 100% growth. The signals are that this could be at least a further 80% in 2005, which on the larger base means an increased quantum of activation over 2004. Heavy activation means that currently spare capacity is being put to use. In many cases, it is utilisation of already owned capacity but in some cases, it involves

the purchase of new capacity. In both cases, there are O&M payments so more money flows into the coffers of the submarine cable system owners.

As much of the download can result from accessing foreign websites, the demand for submarine cable capacity is being fuelled. It is magnitude of this tsunami of demand that makes

But most significantly it consumes the spare lit capacity, bringing forward the day when more capacity will need to be lit. This is a positive sign for the manufacturers. However with so much unlit capacity in existing cables, it seems still a

long time before there will be great need for many new cables.

In the South Pacific, the heavy activation has seen the cessation of sales of discounted capacity. Some holders of surplus capacity in cables such as Southern Cross had been leasing off excess holdings on one, two and three year terms at substantial discounts to the cable company’s price. However that has now stopped and in fact the message has gone out that when the leases expire, they may not be renewed as the capacity will be required by the original owners. Lease holders will have to go the cable company for either IRUs or leases. As a consequence, the price of capacity for some looks likely to rise temporarily. As volumes increase, there will be unit cost reductions but overall, precipitous declines will be a thing of the past. The combination of increased demand and stabilised pricing suggests the aggregate expenditure on international connectivity (primarily payments to cable system operators) will rise in 2005, making for a very positive outlook for the coming year.

This may not yet be occurring in other locations but it is only a matter of timing. This bodes well for the industry in the nearer term. However with the movement towards fibre-to-the-home, the trend towards greater downloads will continue. With caching technologies being challenged to meet the new dimensions, international internet traffic should continue to surge for the longer term.

Who do you see as the customers, and how do their past requirements compare to those in the future?

With internet connectivity being the prime driver, then the ISPs and those carriers who provide the interface to the submarine system operators will be the key customers in the submarine cable market. Assuming that a sane business model evolves for the broadband delivery of internet to the home and business, then these entities, in combination with the content providers will be the most important customers during the period of recovery.

As a senior member of the Pacific Telecommunications Council (PTC), I see a return to the era when ISPs and associated carriers saw value in participating in such organizations for the development of mutually cooperative commercial arrangements.

From

your perspective, what is the state of the market, and how will your company cope with the change?

The availability of much more cost effective advanced techniques for upgrading cables coupled with the shorter delivery times will enable additional wavelengths to be readily established on existing cables. As such existing cable owners may now be able to harvest the potential of their asset. Those who upgrade systems have a promising near-term future. However suppliers of

new cable systems may have to wait several years before new orders emerge. In very approximate terms, it seems that across the globe, less than 20% of potential cable capacity is lit and less than 10% is activated so there is a still a lot left in the existing systems.

The Tata –VSNL acquisition of the Tyco Global Network is yet another positive sign. In a similar vein to the Reliance acquisition of FLAG, we are seeing carriers acquiring the systems from non-carrier owners. This has the benefit of having owners who actually generate the traffic affording increased motivation to utilise the systems. Additionally these carrier owners have a diversity of revenue streams and are not solely dependant on the cable system for their returns (of course Tyco, although not a carrier had a range of revenue streams). I believe that we will see more restructuring along these lines where the ownership of cable systems migrates more to carriers (or should I say, back to carriers because the original systems were carrier consortium cables).

As a consultant, the rewards in the past came from new cables and there will be few of these. The number of rationalisations will be modest but will offer some work. However it is clear that there have been some departures of some long term participants and as such I see an ongoing demand for experience to provide the insight into past practices and to help avoid a repeat of a disaster. With the move to greater carrier involvement in

The Jakarta Post

Telecom: Not to be taken for granted

Zatni Arbi, Contributor, the Jakarta Post

All of us are still reeling from the impact of the "Black Sunday" tsunamis. The death toll keeps rising by the hour, and the pictures broadcast by local TV stations, CNN and others continue to haunt us.

The people who live in the affected areas are totally devastated. No less miserable are people elsewhere who have been trying frantically to contact family members and friends in the affected areas to see if they survived.

In normal times, calling someone across the archipelago or across the globe is not a big deal. We have come to take basic telecommunications for granted. However, when a disaster of this magnitude strikes and all lines of communications are cut off, total confusion reigns.

A Red Cross article in the Dec. 28 issue of starbulletin.com tells the story of two East-West Center students from Aceh left helpless because they have been unable to contact loved ones back home. We read about similar desperate searches for those in isolated areas in newspapers, including The Jakarta Post. Some TV and radio stations have even gone out of their way to put people in touch with one another.

What has all this catastrophe taught us?

Telecommunication is as indispensable now as public utilities and roads. We have become used to being in constant communication with each other, and once that

communication is broken we are paralyzed. Therefore, it is the responsibility of each country to make sure that telecommunication is available to all communities, especially during crises.

Telecommunication is also needed to coordinate emergency responses. That is why Telecoms sans Frontieres (TSF) has been established as an NGO under the United Nations Working Group on Emergency Telecommunications (WGET). Its main task is to provide telecommunications in emergency situations anywhere in the world.

The last time I checked www.tsfi.org, TSF teams were in Sri Lanka just one day after the disaster. They set up satellite-based telecommunication centers there to help coordinate rescue efforts and to provide a GSM network to the area.

Using the most up-to-date telecommunications equipment, TSF partners with a number of operators and vendors, including Alcatel, AT&T, Cable & Wireless, Ericsson, France Telecom and Vodafone. Alcatel contributes by supplying the necessary equipment and it has also made donations.

In relation to Aceh, TSF has reported that emergency telecommunication is an extreme need. Responding to this call, Alcatel Indonesia just submitted a proposal of cooperation to PT Telkom and has pledged 100,000 euro to rebuild the telecommunications infrastructure in stricken areas.

Focus on developing countries

It is not surprising that Alcatel was one of the first global telecom vendors to respond to this tragedy. First, it has all the required equipment and expertise, including satellite, terrestrial -- both wired and wireless -- and submarine infrastructure.

Second, for many years it has focused its R&D on bringing telecom to developing areas, realizing very well that operators in developing countries have a different context than those in developed markets.

Alcatel sees several important trends in emerging markets, where investment resources are often severely limited. Chief among these trends are the optimization of the Public Switched Telephone Network (PSTN), Internet Protocol (IP) network evolution, long distance and international Voice over IP (VoIP) traffic.

PSTN optimization can be achieved by reducing operating and maintenance costs by replacing old equipment and parts with newer ones that are ready for the next generation network. IP can be provided to rural areas through the proliferation of broadband networks, which will also serve as a conduit for VoIP traffic.

The results of Alcatel's focus on the needs of emerging markets are quite encouraging. Today, the company has accumulated experience in narrowing the digital gap in very difficult mountainous terrain such as Bhutan in the Himalayas. Due to the highly challenging topography, Bhutan Telecom has chosen Alcatel's solution consisting of microwave radio and VoIP to provide rural areas with voice and data communications.

Broadband, as Alcatel has asserted, should no longer be considered a luxury that only rich urban people can enjoy. The range of technology that the company has -- ASDL, Next Generation Network, Broadband in-the-sky -- can be used to bring affordable Internet and VoIP to far-flung towns such as Banda Aceh and Meulaboh.

"For a long time operators have actually been able to offer different levels of service to their customers," said Jan Glinski, president director of Alcatel Indonesia, when I met with him in his office one afternoon several weeks ago. "Whoever cannot afford to pay for high bandwidth or who has no use for it can opt for the bandwidth level that suits their needs and budget."

The ability to offer services that meet the individual requirements of subscribers can help bring broadband to rural areas. As to economic restoration and redevelopment, there is no doubt what data and voice communications can do to expedite the process.

Telecom should be included

No technology could have prepared us for the type of disaster that occurred that Sunday morning a week ago. No fiber-optic network could withstand the destruction caused by the crushing water, and there is no use to have the telecom infrastructure intact if all the people and everything else has been swept into the sea.

Still, as Indonesia begins to reconstruct the devastated areas, it would be in the best interest of the affected areas -- and it would be the best time -- to include a more up-todate telecom infrastructure as an integral part of the reconstruction plan, along with the infrastructure for clean water, roads and electricity. Once again, experience has shown that telecommunication is now a basic necessity.

In addition to his regular job as a research staff at the Indonesian Institute of Sciences, Zatni Arbi is an IT observer and writer. For almost 14 years he has been contributing IT articles to The Jakarta Post, the leading English daily in Indonesia. His articles appear in this newspaper every Monday. In addition, he regularly contributes articles to PCMedia, a monthly computer magazine. Once in a while his articles also appear in regional publications such as Asia Computer Weekly. He has also volunteered to teach a course on the development of communication technology in the Department of Communication, University of Indonesia.

The International Committee of the Red Cross is coordinating the Red Cross/Red Crescent Movement’s relief operations in the stricken regions of northern and north-eastern Sri Lanka and in Indonesia’s Aceh province as well as in Somalia, areas where it already had a strong operational presence before the disaster. Make an online donation to the ICRC at www.icrc.org.

PTC’05 - Broadband and Content: From Wires to Wireless

Hilton Hawaiian Village Beach Resort & Spa, Honolulu, Hawaii, USA,16-19

January 2005

PTC’05 will be a milestone conference to address key shifts in telecommunications as the issue of broadband availability gives way to content, access and use. The PTC’05 conference will focus on the value of content in broadband networks, the market forces that drive demand for content, the players positioning for new revenue opportunities and the rising importance of content delivery over mobile networks. Interact with the top executives from ICT carriers, suppliers, broadcasters, user organizations; content providers, technologists and international consultants. Mark your calendar and maximize your participation in PTC’05:

l Register early and save

l Exhibit, sponsor & advertise

l Full-time volunteer

For more information, please contact Claudine Naruse at: +1.808.941.3789 ext.124 or claudine@ptc.org or visit www.ptc05.org.

“Their Time Has Come”

Asian Pacific Overview

Asi Overview

“Sleeping

Giants Awaken in Asia”

By Julian Rawle

China & India begin to make an impact but each giant is treading a different path

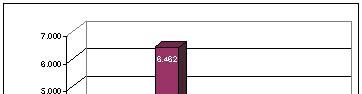

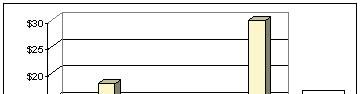

Ever since the submarine fibre optic cable industry went into its latest slump, the wise money has been on the Asia Pacific region providing the demand growth required for a revival. While other regions, such as the Caribbean and the Persian Gulf, are spawning small-scale opportunities, the Asian population multiplier is impossible to ignore. Little wonder then, that the first increase in annual capital investment in the industry for four years consists almost entirely of projects located in Asia.

Investment in Transpacific & Asia Pacific Submarine

Fiber Optic Systems 1999-2005

The shift in market dynamics has been remarkably rapid. In 2002, the Chinese government split China Telecom in two and created a government-owned second operator, China Netcom, whose first major initiative was to acquire the assets of Asia Global Crossing, which included the pan-Asian submarine cable system, “EAC”, and to form an international arm, known as Asia Netcom.

Source : Pioneer Consulting, LLC

But there is a new dynamic in the Asia Pacific submarine fibre optic cable industry. Gone are the days of the entrepreneur with deep pockets and no pedigree in the industry. The collapse in bandwidth prices brought about by over-capacity and hyper-competition has more or less cleared the field for incumbent telco’s to re-assert their dominance.

China Netcom’s next step was to approach PCCW with a view to acquiring the latter’s Hong Kong assets. This deal is still in the balance but it reveals that China Netcom will not be content with simply developing its existing market. For its part, there are strong rumours that Asia Netcom intends to activate the branching unit from EAC into the Chinese mainland: something which Asia Global Crossing could never get permission to do.

Moreover, the traditional global operators, such as MCI, AT&T, BT, and Cable & Wireless, no longer have the appetite for sinking millions of dollars into the World’s oceans. Instead, regional incumbents are coming to the fore, taking advantage of ongoing industry consolidation and distressed assets, and the leaders among this group are companies from China and India.

In November 2004, China Netcom made an initial public offering of its shares in Hong Kong and New York. Much to the surprise of many analysts, the offering was many times oversubscribed and the company netted over US$1.1 billion in fresh funds to continue to develop its network in mainland China and elsewhere.

Meanwhile, at the other end of the region, the Indian government has unleashed a frenzied programme of telecom de-regulation

which saw the liberalisation of both domestic and international telecom markets in short order. This provided opportunities for cashrich Indian industrial conglomerates, such as Bharti, Tata, and Reliance to quickly develop strong footholds in these markets and then to begin international expansion on the back of increased demand for international connectivity driven by the outsourcing phenomenon.

Source : Pioneer Consulting, LLC

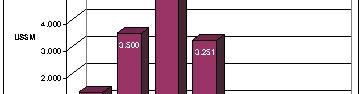

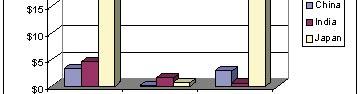

Exhibit 2 : Total Chinese, Indian, & Japanese ICT Investment in 2004

Indian operators’ desire to move into the Asia Pacific region is reflected in the 2003 bilateral interconnection agreement between VSNL and Asia Netcom which provides reasonably robust and seamless connectivity from Europe to the West Coast of the United States via India over the SEA-ME-WE-3, EAC, and Tyco Transpacific (now owned by VSNL) cable systems. In 2004, this arrangement was enhanced with the announcement of a “strategic partnership” between VSNL and Asia Netcom which will allow the new Tata Indicom Chennai-Singapore Cable System (TCSCS) to land at Asia Netcom’s shore station in Singapore. VSNL has also recently announced a partnership with Japanese incumbent, NTT, to offer international IP-VPN to their respective corporate customers.

Paradigm Shift or Flash In The Pan ?

Outward investment by Chinese and Japanese companies was muted this year and was completely eclipsed by the massive capital outflow from India. However, interest from foreign investors in 2004 was focused mainly on China and Japan with a relatively low capital inflow to India.

By themselves, however, these figures only tell half the story. Exhibit 3 shows a slightly different picture when investment is compared to population size :

First, Bharti Group, in co-operation with Singapore Telecom, built the “i2i” submarine cable system between India and Singapore. Then, Tata Industries acquired a controlling interest in the incumbent Indian international operator, VSNL, and gave the company a new aggressive international development mandate. This resulted in VSNL’s recent acquisition of the “Tyco Global Network” of submarine cable systems at around 10 cents on the dollar. Reliance Infocomm’s purchase of recently restructured FLAG Telecom at a heavily discounted price was equally startling. In the last two years, a substantial amount of the World’s existing and planned global submarine fibre optic capacity between Europe, Asia, and the United States has fallen into Indian hands.

A Perfect Fit

So do the recent activities of Chinese and Indian operators represent a fundamental alteration to the balance of power in the Asia Pacific region or will these initiatives come to nought ? To answer this question, Pioneer Consulting looked at ICT investment in these two countries in the last twelve months and compared it with investment in the traditional regional powerhouse of Japan.

The complementary nature of Chinese operators’ desire to expand their sphere of influence outside the domestic market and the

In terms of investment by domestic companies in their own ICT markets, both China and India invested about twice the amount committed by Japan in 2004 (see Exhibit 2).

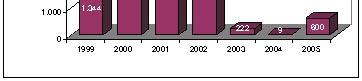

Exhibit 3 : Total ICT Investment per Head of Population in China, India, & Japan 2004

This exhibit provides a much clearer view of investors’ risk perception in each country. Japan with its developed ICT infrastruc-

ing demand for submarine fibre optic capacity more so than simple increases in Internet user population. In other words, it is not so much how many subscribers you have, but ture attracts significantly more investment per head of population from both domestic and foreign investors, than does either China or India. Interestingly, while domestic investment per head is more or less on a par in China and India there is more

how much bandwidth they will be using.

Julian Rawle

Pioneer Consulting’s recent report, “New Business Models for the Transpacific & Asia Pacific Submarine Cable Industry 2005 Update”, in at at inward investment in China than in India. This reflects the perception of a better risk-reward equation in China.

Looking more closely at the deals done in 2004 l diff b t

in this market and concludes that developed economies, such as Japan, South Korea, Singapore, Hong Kong, and Taiwan will continue to drive growth in the Asia Pacific bandwidth market.

India and China on the one hand, and Japan on the other. While investment in India and China has been focused almost exclusively on infrastructure projects, investment in Japan has been equally skewed towards value-

However, broadband growth in China is reaching phenomenal rates and is likely to underpin further investment activity by Chinese operators in the next few years. India, on the other hand, appears to be banking th t i h C tl adding services because the infrastructure is already in place.

how many potential subscribers you have, but looks in detail at the demand drivers at work on the outsourcing phenomenon. Currently,

So what does this mean for the Asia Pacific

Pioneer is skeptical as to the real long-term significance of this dynamic, unless the recent increase in available international connectivity is matched by an equally dramatic improvement in Indian access speeds. Upgrading

Since joining Pioneer Consulting, Julian has brought his broad international industry experience and his knowledge of the market to bear on issues facing the submarine fibre optic industry today. He has completed a number of ground-breaking market reports, most recently focusing on Asia Pacific, the Caribbean, Latin America, Eastern Mediterranean, Indian Ocean, and Persian Gulf regions. He has also led numerous projects for major corporate clients.

Julian has a first degree from Manchester University, U.K. in Russian Studies and a MBA from Cranfield, one of Britain’s top three business schools.

terrestrial networks across the sub-continent may not prove to be as attractive to those Indian companies which have made such a big splash in the international market in the last three years.

submarine fibre optic cable industry ? While ownership and control of capacity has shifted back towards consortia of regional incumbent telco’s, with China and India assuming leadership of the pack, the markets which this capacity is serving have not altered so much.

Japan, with its fully developed ICT infrastrucChina and India, there is significantly more 2004, a clear difference emerges between capacity is serving have not altered so much.

Surplus capacity is now being steadily eroded by broadband subscriber growth which is driv-

After initially pursuing a 10-year career in the oil industry, Julian spent 4 years as Cable & Wireless Representative Director in Moscow, building up a large and profitable business, based on aggregation of international PSTN traffic and provision of managed data services to multi-nationals. He then accepted a post with Cable & Wireless Global Marine as International Marketing Director, Japan. Based in Tokyo for two years, he assisted Global Marine’s Japanese joint venture partner, NTTWEM, to develop and implement a new international marketing strategy.

“The Path More Traveled By”

Fiber Optic Cables Vs. Fixed Satellite Services

A Framework for Analyzing Their Relative Merits for Serving the Pacific Region

by Nikos Nikolopoulos & Travis Kassay

Since the 1980s, operators have been migrating their point-to-point communications requirements from fixed satellite services (“FSS”) to fiber optic cables as a result of the cost, reliability and performance advantages fiber optic transmission has over satellite technology. By the late 1990s, the introduction of new performance expanding optical technologies such as optical amplification, higher bit rates and DWDM accelerated this process.

In the major economic and telecom hubs of the world this process was virtually completed with the massive fiber optic

construction build out during the telecom boom of 1996-2001. However, today there are still a great number of regions of the world – particularly the South Pacific and Southeast Asia – that depend exclusively on FSS for their point-to-point communications.

Satellite and undersea cable systems have a broad range of difference from the type of coverage and amount of capacity available to the cost of solution deployment.

The common denominator among these regions is that they are characterized by low traffic volumes (“thin routes”) and remoteness from international telecom hubs (“remote hubs”); two factors which have made fi ber optic cable solutions expensive in the past but which have begun to disappear recently.

There are six key reasons/trends that explain this change. First, the development of cellular networks in “thin route” countries has led to increased demand for international connectivity. Secondly, many governments are using telecommunications as a way to stimulate

economic growth by developing call center and telemarketing infrastructures. Furthermore, the massive build-out of the 1990s means that dozens more cities have emerged as gateway cities thus pushing the gateways much closer to remote locations. This build-out has also resulted in drastic price declines (8095% since 1998 on many of the major routes) thus making onward connectivity considerably cheaper. Many of the design improvements originally developed to improve performance and reduce costs of longhaul systems have found their way to short-haul networks. And finally, many thin route countries are nearing the STM-1 level in total demand – a point at which fiber satellite often becomes cost prohibitive.

As a result, thin route regions are now in a position to analyze the merits of migrating to fiber-based solutions by building: (1) small “feeder” submarine systems that connect to a global fiber grid;

Coverage

Deployment

SATELLITE UNDERSEA CABLE

Ubiquitous – A single geostationary Satellite covers 42.4% of the world’s surface.

Rapid deployment of terrestrial equipment and nearly instant adjustment to the satellite itself.

Last Mile

Broadcast / Point-toPoint

Satellite can broadcast directly to service providers and end users thus eliminating last mile issues.

Direct – systems are designed between specific points.

A typical system can be constructed 12-18 months after contract signature.

Terminates at either a cable station or designated PoP and then relies on terrestrial networks for last mile.

or (2) standalone systems such as domestic festoons.

Satellite and undersea cable systems have a broad range of difference from the type of coverage and amount of capacity available to the cost of solution deployment. Table 1 on the left gives a side-by-side comparison of satellite and undersea cable systems.

Capacity

Cost/bit

Latency

Offer point-multipoint. Beneficial for television, video streaming and caching.

Limited – A single undersea cable has more capacity than the entire fleet of 220 GEO satellites.

High – due to limited capacity, cost/bit is extremely high.

High – Transmission from ground to Satellite exceeds ½ a second. Negatively impacts applications like voice, video conferencing.

Mostly for point-to-point but with increasing broadband deployment to the premises, cable systems are increasing able to offer point to multi-point/broadcast type services.

High – Current technology allows up to 10.24 Tb/s in a single repeatered cable.

Low – because of the significant bandwidth available, the cost per bit is extremely low.

Low – Latency averages 1/50 second. Suitable for all communications needs including live video.

Any economic rationale for replacing existing FSS with an undersea fiber optic cable system must pass several tests: financial, ownership, development value, performance and quality.

Financial Test: Analysis based on return on investment (ROI), the internal rate of return (IRR) and net present value (NPV) calculations, a payback period determination, an evaluation of the market size and its potential, debt financing, equity financing, and other traditional sources of funding.

Life

Satellites have a life cycle of 12-15 years, FSS transponder leases are typically offered for less than 10 years. 25 year life cycle.

The cost of undersea systems and satellite solutions can vary greatly based on region and weather for satellites, and need for burial, distance from major hub, and capacity requirements. Additionally, the ongoing cost of operation must be considered before deciding on satellite or undersea system; the NPV analysis incorporates all of these costs and normalizes them based on today’s dollars, thus giving an easy method for comparing the two solutions. In addition to an economic justification, one must also consider the value

of ownership; the impact or furtherance of public policy and performance requirements. The tests below include questions that each customer must consider before purchasing a solution.

Ownership versus Leasing Value Test:

While satellite capacity is normally leased, fiber optic networks can be owned and expensed over a longer period of time. Of course, fiber optic networks can also be financed and essentially be structured as a leased asset provided the underlying business model (and off-take contracts) are present. Operators need to decide whether ownership vs. leasing is more appropriate for their financial situation.

Development/Public Policy Value Test:

Does high bandwidth connectivity have a spillover effect on the economic development of the country/region?

Can the country provide additional high-tech services such as call-centers, computer programming, etc.?

Will submarine cable infrastructure support/attract foreign direct investment?

Will submarine cable infrastructure enhance education, and tele-medicine applications?

Will submarine cable infrastructure support/ enhance homeland security?

Performance and Quality Value Test:

Does the operator require real time, latency free communications capabilities?

Is the region subject to heavy rain or other environmental/climactic disturbances that can affect wireless communications such as FSS and intra-island microwave links?

Is traffic growth expected to grow steadily, and/or significantly over the coming years?

Is the region characterized by a large, in-land dispersed population? Or is most of the population near coastal areas?

Conclusion

Recent price and network engineering improvements on undersea fiber optic systems together with increasing traffic demand and government initiatives are prompting many regional operators in the Pacific Rim to migrate their point-to-point communications requirements from geostationary satellite links to undersea fiber-based cable systems. Looking forward over the next 3-5 years, we see an accelerating trend of regional customers replacing or augmenting satellites links with undersea cable solutions - initially for pointto-point communications, but with increasing broadband deployment even for point-tomultipoint communications.

Nikos Nikolopoulos.

Nikos Nikolopoulos is Director of Business Development for Tyco Telecommunications, a position that he has held for the past 3 years. Nikos has more than 14 years of telecommunications experience including 6 months as contractor for the European Commission, and 3 years performing legal and regulatory consulting. Nikos joined Tyco Telecommunications in 2001 as Director of Business Development for Europe where he had responsibility for regional development. Currently Nikos is responsible for project development support including assistance in securing financing. Nikos holds a BSEE from the University of New Hampshire and a JD from the Chicago Kent Law School.

Travis

Kassay

Travis Kassay is Senior Manager of Business Development for Tyco Telecommunications. Travis has, over the past five years, held various positions at Tyco Telecommunications including positions in Marketing, Business Development and Global Sales operations. From 2000-2002, Travis had responsibility for the global procurement of terrestrial fiber for the Tyco Global Network. Currently, Travis supports project opportunities through assistance in securing financing and developing business models. Travis holds a BS in Finance and English from Boston College and is currently pursuing his MBA from the Stern School at NYU.

S. B. Submarine Systems Co. Ltd. (SBSS) is a key player in the submarine cable industry in Asia. The Company was established in January 1995 as a joint venture between China Telecom and Cable & Wireless, and is located in Shanghai, China.

When SBSS was set up 10 years ago, the Company had only one main cable ship Fu Lai and a total of 95 staff. The company installation capability was very limited at that time. After 10 years strong development in terms of both technology and working experience, SBSS has now grown up as an active player in the international submarine telecoms cable construction market, especially in Asia.

By end of 2004, SBSS had completed more than 25,500 kilometers of telecoms cable installation and participated in many international projects such as China-US, SMW3, APCN2 and C2C. In the difficult years of 2003 and 2004, the Company won the Thailand – Indonesia – Singapore installation contract and the TATA installation contract. SBSS has also been selected as one of the long-term operators for the Yokohama Zone Maintenance Agreement since 1997, responsible for maintaining the regions cables for six months every year.

S. B. Submarine Systems

and adapting to the changing market.

Adopting New Technology

Along the Chinese coast, a new development in fishing technology “stow net fishing”, threatened the integrity of the cable systems. The technology involved nets being anchored to the seabed and allowed to drag with the tide. This recent change in fishing technology negated previous standard burial techniques. One meter burial was no longer adequate to protect cables so new methods had to be developed to ensure the best protection to cables. Realizing this market requirement, SBSS started a series of investments in deep burial technology.

As General Manager Ian Douglas explains, the key to success for SBSS is adopting new technology

An Overview

By Vivian Hua

Deep cable burial technology requires a plough with the capability to use either jet assisted ploughing or water injection technology. A HiPlough meeting this technical requirement was brought into SBSS in year 2000 and subsequently modified with injector technology .This enabled the company to bury cable consistently to three meters in the sediments found along the East

coast of China, well below the current threat levels imposed by “stow net fishing” The Dragon Sledge was designed to easily and cheaply deploy deep burial three-meter technology in shallow water. Dragon Sledge was conceived as a diver less system deployable from either a shallow water vessel or the more traditional cable vessel and has successfully completed a number of shallow water projects. Upgrades can allow Dragon Sledge to operate up to the 200-meter contour and complete burial as deep as five meters.

Besides owning and operating burial equipment, SBSS also operates two DP vessels the Fu Hai and the Fu Lai and a shallow water DP cable barge the Fu Xing.

Fu Hai is specifically designed for cable installation and repair with a gross tonnage of 6292. Fu Hai is able to deploy SBSS subsea equipment Hi-Plough and SBSS ROV Sea Lion. Since her delivery to SBSS in year 2000, Fu Hai together with Hi-Plough have completed in total 1,250 km 3m burial in projects such as APCN2 and China-US rerouting. Fu Hai recently carried out extensive

operations in Indonesian and Thai waters.

. Fu Lai was until recently heavily involved in the telecoms cable market. However she has been adapted to the oil and gas offshore industry and has carried out extensive dive support operations (DSV). The Fu Lai also successfully completed a 33 km power cable installation in between offshore platforms after modifications in a Hong Kong shipyard. The operations represented a complex engineering solution along with a combined diving and operations and cable installation.

Fu Xing was specially designed for the challenges of shallow water installation in the region. She is able to deploy burial equipment Dragon Sledge and SBSS ROV Sea Lion. Fu Xing has carried out a number of shore end installations where cable was buried to three meters depth. In 2004, Fu Xing carried out a repair to the China-US cable network

segment N1. The water depth was just 3.9 meters and the damaged cable was buried deeper than expected at 3.3 meters. The operating window was small due to the presence of a high tidal range. Fu Xing together with Dragon Sledge recovered the cable and completed the repair successfully in only a few days. In another domestic cable installation project on the east coast of Fu Jian Province in 2004, Fu Xing with Dragon Sledge worked at an impressive 1 kilometer per hour for 3-meter burial over the entire 46-kilometer route.

Adapting to the Changing Market

As it became clear that the cable industry faced a significant downtime, SBSS started implementing its strategy of applying its skills and expertise in the offshore oil and gas industry when it undertook the Dong Fang Offshore 1-1 Gas Project in South China in 2003. Though the Dong Fang project was a relatively small project, it was an important step for SBSS to enter into another market.

To adapt to the offshore market, SBSS modified her previous cable ship Fu Lai into a diving support vessel (DSV), made it suitable for various offshore support work such as pipeline trenching support, pipeline inspection support, offshore diving support etc. With the company’s 10-year experience in cable laying, Fu Lai is also able to install power cable in oil field.

CABLE PROTECTOR – A SPECIALIZED DEEP SEABED BURIAL

BARGE

by

Siew Ying Oak

Protection Requirements for Submarine Cables

For protection of submarine cable against fishing activities, burial of cable up to 1 meter in the seabed is normally considered adequate in South East Asia region. In Singapore and Hong Kong where protection of cable against ship anchors is necessary, cable is usually buried to a depth of 6 to 8 meters in the seabed where it is soft and 4 meters where it is hard.

For some specific reasons in certain areas e.g. where special fishing technique is employed or where there is sand movement, cable burial of depth greater than 1 meter may be required for protection against fishing.

Cable Burial Machine

Various types of cable burying machines, including plowing and water jetting machines have been developed for burying of cables up to a depth of 3 meters.

For burial of cable up to 10 meters, a special purpose built barge equipped with deep cable burial injector and rock-cutting machine will be required.

The barge “Cable Protector” is built for the purpose of burial of cable up to 10 meters.

Cable Protector is a “dynamically positioned” state-of-the-art deep burial-laying barge. This sophisticated barge is also equipped with 6 points mooring system, 2 supplemented

CABLE PROTECTOR

Cable Laying Barge “Cable Protector”

spuds and fitted with a 6 tonnes main pulling anchor.

A special-purpose trenching injection system is used for cable burial into the seabed to a depth up to 10 meters. The Injector is capable of supplying high pressure water through its nozzles from the leading edge and base of the injection assembly, creating a trench in the ground into which cables are laid beneath the seabed.

Cable Protector is also equipped with a RockSaw trenching system capable of trenching 0.4 meter wide, 4.5 meters deep into hard seabed.

Cable Projects

In 2003, Cable Protector successfully carried out the cable deep burial project in Singapore. She was used in various shore-end cable landings in the Philippines and Thailand in the years 2002 and 2003. During the same period, because of the requirement of position accuracy, she was used to lay an

optical fiber cable of about 100 km beside the oil pipeline.

A few months ago, Cable Protector successfully laid 135 km of submarine optical cable across Malacca Straits. The cable was buried up to 3 meters.

Asia and Indian Ocean Cable Maintenance Agreement (SEAIOCMA).

ACPL operates two cable ships, namely ASEAN EXPLORER and ASEAN RESTORER. These two ships are suitable for submarine cable installation and maintenance in both shallow water and deep sea.

About ASEAN Cableship PTE LTD

ASEAN Cableship Private Limited (ACPL) is incorporated in Singapore in 1986. ACPL has been providing the repair and maintenance of submarine cables in the South-East Asian and Indian Ocean regions under the South East

In addition, ACPL operates a cable-laying barge named Cable Protector, specially designed for submarine power/telecommunication cable installation and in particular suitable for shore end with deep burial installation requirements.

ACPL Responds to Tsunami

There was an earthquake of magnitude 9 in the area off the north of Sumatra Island in the morning of 26 Dec 2004.

A cable was failed. The fault was located in water depth of about 2000m near Sumatra. It is believed that the fault was caused by underwater landslide at the time of the earthquake. The cableship ASEAN Restorer of ASEAN Cableship PTE Ltd was mobilized to carry out the repair. Though there was a severe tsunami that damaged some of the beaches and the low land areas of the various countries in the region, the shore-end cables landing in Colombo of Sri Lanka, Chennai of India, Satun of Thailand, Penang of Malaysia, Medan of Indonesia and Yangon of Myanmar did not suffer any damage.

SECRETS AND LIES IN REGIONAL SYSTEMS

By Marc Fullenbaum

I. INTRODUCTION

Expectations have firmed up over the last 18 months in the field of Regional Systems. These stems from the current situation in the trans-oceanic systems, which can be described by the word, overbuild. The main transoceanic routes now have several cable systems, each with a tremendous upgrade potential. While large transoceanic systems are not disappearing, the market pull may end up with one large system being built every two years. Therefore the industry ought to prepare to better face the challenges of Regional Systems, generally of lower capacity, and with reduced CAPEX and OPEX than the major trans-oceanic systems.

II. THE MARKET

There is no doubt that the Regional Systems market demand has picked up over the past two years in all the parts of the world (e.g. Farice, CamRing, TIS, Med Cable). The driving demand is regional connectivity in areas that aren’t connected to the large transoceanic systems. For the sake of clarity, the upper boundary of Regional Systems is considered as 2000 - 3000 km in length. Our analysis has shown

that the market for such Regional Systems will be around 1/3 of the total submarine system market over the next few years. Thus a deeper understanding of this market is warranted.

Regional Systems will generally link under-served countries/areas to high capacity international hub nodes. They may be targeted at relieving a regional capacity bottleneck, or to serve the needs of new carriers wanting to gain international access in a deregulated market. These systems will be located in regions such as South East Asia, the Mediterranean basin, Pacific Islands, East Africa, West Africa and in the Caribbean.

In light of the recent dramatic events in South East Asia, it is worth keeping in mind that Regional Systems should ideally be environment independent telecommunication solutions boasting flexible reach, high reliability and flexibility over time in order to offer secure connectivity in a multi customer configuration. To our knowledge, only one submarine system stopped carrying traffic due to a cable cut, following the Tsunami attack. All the other ones (about 90 % of the submarine systems operating in the region) have kept on

operating as planned.

By and large, most of the purchasers will be “new comers” to the submarine world. The rationale for turning to a submarine solution will be twofold.

Firstly the submarine cable is considered a simple and reliable medium to provide connectivity with a large enough capacity. Secondly, the supply industry has demonstrated a willingness to help operators build their business cases with cost optimized solutions and also guide them throughout the typical phases of building and operating a submarine cable system.

The low cost expectation for regional systems stems from their “low” capacity requirements: the ball park is 300 Gbit/s to be compared to the 6 Tbit/s of transoceanic systems, so it’s only natural that the customers will expect a lower cost base. In essence, the endof-life capacity will not be the main customer priority since the two drivers are optical fiber connectivity and low cost.

The low cost aspect is crucial in order to make viable business cases, so Regional Systems will require shrewd solutions to satisfy the investors.

But what are the main cost drivers for regional systems? They are shown in the following diagram for the sub-sea plant current generation (terminal and services cost not displayed because they represent only a small percentage of the total initial investment).

Clearly, the solution must optimize the cable costs and repeater count. This begs two questions:

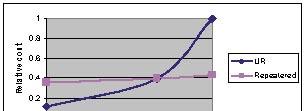

• How to choose between an UR and a repeatered solution for the shortest span;

• How to cost optimize the repeatered solution. These questions will be addressed in turn.

Cost percentage versus distance (2fp)

III. THE UR LIMITS TODAY AND

TOMORROW

For Unrepeatered Systems, system optimization results from smart anagement of the optical power, defined by the delicate balance in between the fiber effective area, the pumping scheme and the fiber characteristics (attenuation and nonlinear characteristics). The current ‘best in class’ solution uses large core 110 µm2 fiber exhibiting 0.172 dB/ km attenuation in an industrially produced cable structure, and single fiber pumping ROPA (Remote Optically Pumped Amplifier).

Current ‘best in class’ Unrepeatered Solution with ROPA

This scheme has been used on the longest 10 Gb/s WDM UR link operating today (350 km Italy-Greece GWEN system) with the previous generation of terminal equipment. Alcatel has successfully deployed 6 systems with this simple configuration

with another two under construction. Only two ROPA pumps are needed per fiber pair carrying traffic, and no additional ‘pumping fibers’ are needed. Today, the UR system reliability comes close to that of repeatered systems with only an extra 10 % outage time. Further UR system improvement can be implemented with a Raman copropagating scheme on top of the ROPA.

Next step for UR with Raman co-propagating

This scheme relies upon the use of the same ROPA, of new generation of terminal equipment (8.5 dB FEC) and of Raman co-propagating pumping. This will yield 10 Gb/s WDM systems up to 450 km to be operated in the 2006-2007 time frame.

Our tradeoff analysis shows that complicated UR schemes don’t make sense today to attain a 500 + km span. Such solutions could potentially be implemented but the pre-requisites are numerous:

• New exotic ROPAs would have to be developed;

• Each traffic carrying fiber pair requires at least 1 fiber pair plus 1 fiber for pumping purposes only (not carrying traffic);

• Each traffic carrying fiber pair requires 8 pumps onshore;

• < 0.165 dB/km fiber, in an industrially cabled structure.

The outage time will be 3 times and the cost 1.5 times those of a repeatered solution, not taking into account the solution development costs. Although high performance fibers can be delivered by fiber suppliers for lab experiments or for manufacturing experiments with short lengths of cables, a cabled fiber with < 0.165 dB/ km attenuation over all cores is not yet attainable in industrial lengths of cables (0.172 dB/km being the current benchmark for real cable delivery).

For spans over 450 km the optical power management is more reliable and more economic today with repeaters. We do not anticipate economically sound 500 km unrepeatered solution before 4 years, when the technology is ripe: 150 µm2 fiber with attenuation < 0.165 dB/km; improved FEC (~10 dB);

PFE measurements while C-OTDR measurements would locate a failed repeater.

Regarding optical channel protection, the use of unprotected terminals with N+1 SDH protection at STM-64 level provides a 3.6 mn/year outage using current generation equipment. Addition of a second layer of protection in the terminal itself at channel level provides no significant improvement (3.5 mn/year outage) while adding significant cost and complexity. These can be avoided by avoiding such double protection schemes. Therefore removing supervision, channel protection and simplifying dispersion compensation is an economic approach with a potential savings of approximately 25 %.

The Marine Operations costs are split into “Services” and “Installation”, typically 40 % to 60 %. Moving towards a “bare bone” scope of work is feasible on the service side (e.g reduced corridor survey, no pre-lay grapnel run, etc..)

The O&M costs throughout the System life are important to bear in mind. Common practice is to join one of the traditional zone agreements or private

maintenance agreements where there is "guarantee" for service availability. Customized service level could be set up. Another approach would be to rent a cable ship only upon fault occurrence when either the cost of or the transit time to the nearest agreement is significant or lengthy.

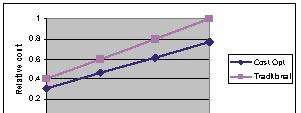

V. CONCLUSION

Seeking a WDM unrepeatered solution implementation over 450 km in 2006-2007 is a false economy since a repeatered solution is the best value for money.

Unrepeatered and Repeatered solution cost versus distance

As for the repeatered solution cost optimization, the preliminary work points to a 30 % cost break with respect to a traditional repeatered solution. This

solution will make use of optimized cable, repeaters and terminals.

Cost optimized versus traditional cost comparison.

Marc Fullenbaum Marc has worked 14 years in the optics field. since graduated from “Ecole Superieure d’Optique” in 1991. He worked two years at the IBM T.J Watson Research Center then spent three years with the French Delegation for Armaments. Marc also worked three years with the Com Dev Space Group prior to joining Alcatel Submarine Networks where he is currently in charge of Product Marketing.

has entered into an arrangement with

Lloyd’s Register

Fairplay

making available, complimentary to subscribers, comprehensive databases of commercial vessels (www.sea-web.org/), ports and companies (www.portguide.com).

Call for Papers

FROM: Mr. Graham Marle ICPC Secretary FAX: +44 870 432 7761

TEL: +44 1590 681 673

DATE: 15 November 2004 E-mail: secretary@iscpc.org

Web-site: www.iscpc.org

The International Cable Protection Committee (ICPC) is organising its next Plenary meeting in Sydney, Australia during the period 15 17 March 2005 inclusive.

All of the World’s major telecommunications companies are represented within the ICPC whose principal purpose is to promote the safeguarding of submarine cables against manmade and natural hazards. This unique and prestigious organisation also serves as a forum for the exchange of technical, environmental and legal information concerning the marine aspects of both telecommunications and power submarine cable systems.

Recent feedback from ICPC membership revealed that the following topics would be of most interest to them:

• Cable owners’ experience/problems of cable protection

• Legal issues associated with cable retirement and cable protection

• Cable repair experience and techniques

• Topical fishing issues - e.g: deep water fishing, stow nets etc.

• Submarine power cable issues.

The Executive Committee (EC) therefore seeks presentations by interested parties that would primarily address the above topics.

Papers which address other relevant areas of the submarine cable industry (e.g. environmental issues and scientific use of retired cable systems) may also be considered.

***NB: Recognising the location of this Plenary, papers with content that is relevant to the Asia-Pacific region will be especially welcome.

Prospective presenters are respectfully advised that papers which are overtly marketing a product or service will not be accepted.

In order to qualify for a free trial of these services, contact LRFTrialOffer@SubTelForum.com.

Presentations should be 25 minutes long including time for questions. The EC will evaluate all submissions based on content and quality.

NB: Commercial exhibits may be displayed near the ICPC meeting room by special arrangement. Please contact the Secretary for further details.

Abstracts should be sent via email to secretary@iscpc.org no later than 28 January 2005.