Submarine Telecoms Forum is published bimonthly by WFN Strategies. The publication may not be reproduced or transmitted in any form, in whole or in part, without the permission of the publishers.

Submarine Telecoms Forum is an independent com mercial publication, serving as a freely accessible forum for professionals in industries connected with submarine optical fibre technologies and techniques.

Liability: while every care is taken in preparation of this publication, the publishers cannot be held responsible for the accuracy of the information herein, or any errors which may occur in advertising or editorial content, or any consequence arising from any errors or omissions.

The publisher cannot be held responsible for any views expressed by contributors, and the editor reserves the right to edit any advertising or editorial material submitted for publication.

Contributions are welcomed. Please forward to the Managing Editor:

This month marks the beginning of SubTel Forum’s 10th year in circulation. The annual calendar is out; the submarine cable map is presently winging its way to walls around the globe; we are packed and ready to escape the snow in Virginia for leave at PTC in Honolulu.

We start 2011 with a renewed sense of direction and purpose. We have honed the magazine themes to better reflect where we

are in the industry today. We are adapting this year the magazine and RSS Feed for the executive on the go, adding some truly digital advances. We are improving and adding to the utility of our industry tools. In the coming months, we hope you will enjoy the roll-out of some rather interesting SubTel Forum enhancements, many of which the boys in the backroom say will simply work!

Should you be attending PTC, please come by our booth to say hello; and as always, save me a seat at the Mai Tai Bar.

Cable Firms Accused of Paying Bribes

Columbus Networks Builds On Metaswitch

Deep in the ocean, internet networks hang by a thread

EASSy to double capacity

EPOCH Launched by OMM

Gulf Bridge International (GBI) And Subcom Commence Marine Operations For The GBI Cable System

Hibernia Atlantic Achieves An Important Milestone For Project Express

IMEWE submarine cable launched for commercial use

News Now

Liberia Hosts International Broadband Connectivity Workshop

LIME-US$35M submerged cable to link Dominican Republic, the Caribbean

Mada signs Regional Cable Network agreement to transform Telecom in the Middle East

Main One and Galaxy Backbone set to deliver Broadband services to the Public Sector at a lower cost.

MTN Rwanda Expects to Land EASSy Cable Early Next Year

Palapa Ring to be completed by 2012

Southern Cross labelled vital in Wikileaks cable

Superonline Collaborates on Regional Cable Network Project

Telkom Kenya to Invest 5 Billion Shillings in Network

Undersea cables: Still waiting for price crash

Verizon Marks Another Year of Expanded Network Reach, Increased Capacity and Enhanced Performance

WFN Strategies Headed to the South Pole

WFN Strategies to host a workshop at PTC 2011

The Connected World 2010 Development in Review & 2011 Outlook

Stephen Jarvis

Each year, one of the major marks of growth in the Telecoms Industry is also one of its most tangible: the laying and activation of new cable. In difficult economic times, the industry has managed a notable expansion, with a number of cables successfully launched for business. In 2010, eleven new cables were activated, creating a combined increase of over twenty terabits per second of bandwidth in the Middle-east, Africa, and other regions.

Historically, new development happens in bundles and regions. Occasionally, this is due to power shifts, an area’s international importance, but mainly it is just a matter of timing. Connections spread, the world moves on, and it is time for another region to step into the limelight. If 2010 is any indication, this time belongs to the Middle East and Africa.

Of the nine newly activated cables, five of them go to the Middle East: EASSy, EIG, I-ME-WE, MENA, and TE North. These cables bring an average of 3.6 terabits per second to the region. The highest bandwidth among them is MENA, a $400 million system, 8,000 km long, and providing 5.7 Tbps. It connects Italy and Greece to a number of countries including Egypt, Saudi Arabia, and India. However, the largest

of the new cables is EIG. Costing $700 million and 15,000 km in length, it adds 3.84 Tbps and connects the UK, France, Monaco, Portugal, Gibraltar, Portugal, Libya, Egypt, Saudi Arabia, Djibouti, Oman, the United Arab Emirates, and India.

Three cables have been launched in the regions of Africa and South Africa. Main One, Lion, and EASSy average 2.1 Tbps and connect many African countries both to the west and to the east. The largest cable, also with the greatest bandwidth, is EASSy. It is 10,000 km long and connects South Africa to Sudan via landing points in Mozambique, Madagascar, the Comoros, Tanzania, Kenya, Somalia, and Djibouti. Main One currently has operating landing points in Nigeria, Ghana, and Portugal and plans are underway to open a second stage extending to South Africa. The remaining new cables provide improved bandwidth

to various parts of the world. The Honotua cable, for example, has created new, and in a few cases, the first, links to several Pacific islands such as Bora Bora, Huahine, Moorea, and Tahiti; all of which are now connected by Honotua to Hawaii.

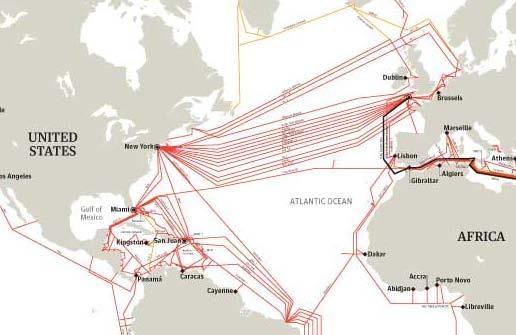

For 2011 and beyond, there are already no less than twenty-two new cables planned. Of them, two particularly innovative cables were announced in 2010: the Arctic Link and Project Express cable systems. The Arctic Link is a planned cable connecting Asia with Europe, routed through the Arctic. The cable will be 16,093.5 km and pass through Japan, the United States, Canada, Greenland, the Arctic region, and the United Kingdom, a daunting undertaking.

Project Express, on the other hand, will serve a very different purpose. It will be the first new cable since 2003 to cross the Atlantic. Given its planned activation for 2012, this will be nearly ten years since any new cables have been laid in this region. However, it differs greatly from previous trans-Atlantic cables following the same route due to its primary usage by the financial sector. Project Express is planned link the banking hubs in New York, Chicago, Toronto, Frankfurt, and London, and all with extremely low latency.

While the economic climate has not been a friendly one in 2010, the telecoms industry is still growing. With the continued business in the Middle East and Africa the prospect for sustained improvement is hopeful. Last year’s additions are nearly dwarfed by the six new planned

systems for both regions. These include cables off the both the eastern and western coasts of Africa (WACS, ACE, Main One, e-five, and LION-2) and again in the Middle East (GBICS, Flag HAWK). As these areas continue to step out into the global spotlight, the future of world communications looks bright.

Stephen Jarvis is a freelance writer in the Washington D.C. area. He has published articles and done editorial work with several publications including Submarine Telecoms Forum. Also, he has been a speaker for the Popular Culture Association / American Culture Association National Conference.

A LOOK AHEAD

TO TRANSATLANTIC SUBSEA GROWTH & OPPORTUNITIES IN 2011

Jaymie Cutaia

Source: The Guardian

See full map here

& SUB SEA CABLES

The financial trading marketplace has changed significantly in the past few years, in large part due to distinct advancements in technology, networks, equipment and in the delivery of critical information. By shaving micro and milliseconds off of the routes that the financial data travels, from broker firms, hedge funds, and market data providers to financial Exchanges, millions of dollars can be gained or lost. Each component of a specific low latency route - from the software the trader is using to the computer systems to the fiber connectivity to the optical and transport systems connecting the fiber – can make significant differences in how fast the overall trade can be conducted and the dollars/Euros involved.

It’s no wonder that in a recent study by Ovum, as reported by Bob’s guide recently, illustrated that technology investments by financial services industry will grow by 4.5% in 2011. Many financial houses and exchanges are clamoring to keep up with the technology to ensure its used optimally within their IT infrastructures.

So how can the financial arena keep up and stay competitive? What’s needed on a global scale to support this growth and the fast-pace of technological advancements? At the very foundation of trades and transactions is the infrastructure the

world’s financial networks are built upon—it all starts with subsea fiber optic cable systems that support the massive amounts of data that speeds back and forth across the globe every second. As the majority of financial trades are made between New York and London, let’s explore this region a bit further. Subsea transAtlantic fiber optic cable systems have been in place for years – from the first one, TAT-8, which went into operation in 1988 to others that followed, including TAT-9-14, CANTAT 3, PTAT-1, Apollo, AC1, AC-2/Yellow, Flag, VSNL, and Hibernia Atlantic (utilizing the 360 Networks

subsea cable which was completed in 2001). Whether these cables were built by a consortium of telecommunications companies like TAT-14, or owned by private companies such as Hibernia Atlantic, these high-speed systems are relied upon to deliver information that drives global business, financial markets, and everyday consumers. In essence, if there is information that needs to cross the Atlantic Ocean, it does so on one of these cables.

THE COMPETITIVE LANDSCAPE

But are all subsea cables created equally? In general, the more modern the cable line, the safer the communication flow. Other competitive advantages include available capacity (as today’s consumer, financial and streaming media needs, to name a few, require large amounts of bandwidth). Additionally, location is imperative. The fastest distance between Point A and B is a direct line—so the most direct path between two cities, New York to London for example, takes the least amount of time to transport data. But also location is key as too many cables in the same congested areas, such as around the NYC and London waterways, cause vulnerabilities. For example, a fishing ship drops its anchor along the sea floor when casting its nets. A common cable outage is caused by these anchor trawlings, and as there are many fishing boats in these London and New York seaports, and as there are many subsea cable landings within a 50-mile radius as well, cable security is at a high

risk. Therefore, having diverse subsea paths, as well as direct, low-latency crossings, are critical for any network operator.

As initially discussed, financial firms need to continuously boost performance and reduce the latencies on their network paths. The most lucrative trade is the one that is conducted faster than the others, which can capitalize on small changes in the market, and therefore, gains can be huge. You can see why achieving the lowest latency possible across key financial routes is highly sought after. Carriers and service providers buy routes/paths on these transAtlantic cable systems to form their own networks and infrastructure and ultimately sell capacity to enterprises, multinational corporations, and financial firms. The newer subsea cable systems were built with increased redundancy and diversity to ensure data transmissions have maximum uptime and availability. If an outage occurs on one part of the cable system the data traffic can be automatically re-routed to another path –ensuring network availability.

NEW SUBSEA BUILDS ON THE RADAR

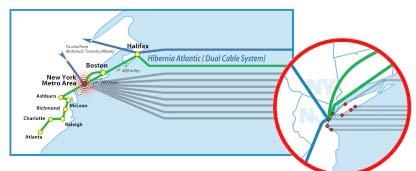

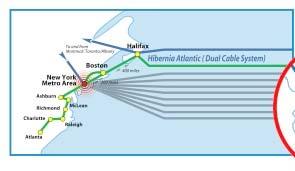

There hasn’t been a transAtlantic build for the past ten years or so, until now – with Hibernia Atlantic’s newest plans for its

cable system, Project Express. A state-ofthe-art submarine network build designed specifically for financial community stretching from North America to Europe. This subsea build will be completed Summer 2012, and will offer the lowest latency route from New York to London with just 60 milliseconds round trip delay and will also connect Toronto to London at sub 70 milliseconds. This historic build strengthens Hibernia Atlantic’s existing Global Financial Network, which already connects hundreds of banks, financial exchanges, data centers and key carrier hotels across major financial cities including Amsterdam, Chicago, Dublin, Frankfurt, London, New York, and Toronto.

Initially deployed with 40 Gigabit technology, Project Express will be a boon to financial community who can capitalize on some of the lowest latency routes in the world – further ensuring they make the fastest possible trades. Some would argue that there is a glut of fiber connecting North America to Europe with all of the existing subsea systems; however with today’s ever-increasing consumption of bandwidth and the need for secure, fast routes, there are only a few, modern cables that can adequately support this growing demand. Hibernia Atlantic is banking on the aggressive quest for the lowest latency to fill up its cable system with financial firms, market data providers and

Exchanges. The first phase of the build will be a new cable from the County of Somerset in the United Kingdom, to Halifax in Canada then connect to Hibernia’s current low latency cable from Halifax to New York City. The future brings increased capabilities as Project Express is upgraded to 100 Gigabit technology further driving competitive advantages to the financial arena.

LOOKING AHEAD

Deep under the ocean, transAtlantic subsea cable systems play a pivotal role to what is happening above within the Internet and global data networks. Technology will continue to drive advancements that can be used to secure competitive advantages. The savvier financial market firms will adopt these new capabilities

and continue to push the technological envelope to achieve the lowest latency and in ultimately making bigger bucks.

“In 2011, we will see a further push towards technology, both by the consumers and by the network operators,” states Bjarni Thorvardarson, CEO of Hibernia Atlantic.

“Consumers are driving the need for bandwidth, with smartphones, tablet and mobile applications, content uploads, streaming video and more. Additionally, the average user is spending more time online and as networks continue to light new communities, there are more users coming ‘on-net’ every day. Network operators, which today includes the traditional carriers and service providers as well as the financial, medical, media and other professional, private networks, are looking for cutting-edge technologies that can increase their speed and performance.

New York to London, and considering the natural arc of the Earth, this allows our new cable to pass through New England and Canada before connecting to the UK. So in one calculated plan, we are removing unnecessary latencies, deploying the latest modern cable technologies and including future growth strategies, such as including branching units for future latency enhancements to the US and Continental Europe. We are planning today for tomorrow’s bandwidth demands.

“It is our belief here at Hibernia that 2011 and beyond will be filled with innovative subsea and terrestrial cable innovations, where network operators are constantly trying to optimize both new and existing cable lines, in preparation for tomorrow’s bandwidth, security and latency demands. The market is driving this; we need to ensure we have the necessary infrastructure in place to support this demand. So these next months ahead will be focused on network deployment and enhancements.”

“Our Project Express initiative is an example of this need for fast bandwidth driving innovation. We are building the most direct and therefore fastest route from

Jaymie A. Scotto Cutaia is the Founder, CEO and Principal of Jaymie Scotto & Associates (JS&A), a premier Marketing and PR firm dedicated to advancing the technology community, and CEO and Founder of DealCenter, LLC, an online meeting system for event planners and associations.

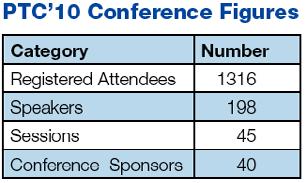

This is a special insert into SubTel Forum, designed as a preview for the upcoming PTC Conference in Hawaii. As President of the Pacific Telecommunications Council, I want to thank the SubTel Forum team for this opportunity to contribute to this issue.

Notwithstanding all of the financial strictures as a consequence of the global financial crisis and the slow recovery, particularly in North America and Europe, registrations for the conference so far suggest it will be again strongly attended. The theme is Connecting Life 24/7, which well captures the ever-increasing customer demands of the telecom industry.

Of course a key ingredient of the conference is that of submarine cables, which this year is given expanded coverage with three dedicated sessions and numerous other peripheral sessions. The articles in this section will give you a taste of some of the topics that will be debated from 16th to 19th January. As usual, there will be opportunities to blend serious content sessions with the convivial networking that PTC in Hawaii is so well known for.

On behalf of PTC members and secretariat, I invite you to the PTC Conference and look forward to seeing you there.

John Hibbard

In less than a week, we will embark on our 33rd annual conference, PTC’11: Connecting

Life 24/7. If the response to and interest in PTC’11 is any indication, the event is sure to be a memorable and successful one.

PTC’11 will unite leaders from all sectors of the telecommunications industry. The program theme, which explores the various ways in which people’s lives are becoming increasingly connected, also highlights the interconnectedness of each of the telecom sectors.

As you attend the numerous program sessions, exhibits, and social events, you will likely notice that PTC’11 reflects the hard work and support of many different groups of people. PTC’s leadership—the Board of Governors and the Advisory Council—has directed the PTC’s overall work and progress. The PTC’11 Program Committee, led by co-chairs

Stephan Beckert, Gary Kim, and Richard Taylor, has guided the program planning process to ensure an impressive and first-rate conference program. PTC’11 sponsors have provided their generous support, which will significantly contribute to the success of our annual conference. I am extremely grateful to the members of each of these groups for their ongoing support and contributions.

I would like to extend a special word of thanks to PTC’s members. Throughout the year, many of PTC’s members offer their support, feedback, and encouragement, each of which strengthens the organization and the value of membership.

On behalf of the entire PTC Secretariat, I wish you an enjoyable and productive conference experience. May you also have the opportunity to delight in the many sights, sounds, and food that Hawaii has to offer.

Warmest alohas, Sharon Nakama

PTC'11: Overview

Vision

The Pacific Telecommunications Council (PTC) is the leading professional organization promoting the advancement and commercial use of information and communication technologies, services, policies, and knowledge, to benefit its members and the people of the Pacific Hemisphere.

Mission Statement

To realize its Vision, the Pacific Telecommunications Council (PTC) motivates and enables its members to conduct trade in equipment, technologies, and services and to use the power of information and communication technologies (ICT) to improve the quality of life in the Pacific Hemisphere.

Specifically, we will:

• Organize conferences, exhibitions, and other forums to promote the open exchange of information, ideas and views in the context of the commercial, social, economic, and other development needs in the Pacific Hemisphere.

• Bring together influential leaders from diverse backgrounds and locations to informally debate contemporary and controversial issues affecting the development and use of ICT.

• Encourage the research, development, and application of technologies, services and policies through our constituency of educators, governments, commercial organizations, non-profit entities and user communities, especially to overcome uneven development and competency divides.

• Grow an active diverse membership of

experts and influential professionals committed to achieving our Vision.

• Monitor and address members’ needs and continuously create value for them.

• Develop the resources and capabilities needed to achieve our Vision in a sustainable manner.

• Promote widely the views, role and activities of the Pacific Telecommunications Council.

Preview of workshops, round tables, sessions

Sunday, 16 January 2011

0900 – 1230 SUBMARINE CABLE

WORKSHOP: “It Takes a Village” –Parenting the Development of a Submarine Cable System

Organized by WFN Strategies

The workshop will consider three phases of a new submarine cable project (Development, Implementation, Service Provision, one session per phase) using speakers representing differing interests and disciplines followed by brief interactive question and answer sessions including speakers and the audience.

The objective is to have a set of instructional sessions allowing debate and questions between speakers and plenty of time for audience questions.

Workshop introduction by Wayne Nielsen, Managing Director, WFN Strategies.

Moderator:

GUY ARNOS, Director, Projects, WFN Strategies, LLC, USA

Panelists:

DOUGLAS BURNETT, Partner, Squire Sanders & Dempsey L.L.P., USA

SIMON COOPER, VP, Global Submarine Cables Strategy & Projects, Tata Communications, Singapore Networks, France

TONY FRISCH, SVP, NXT Product Line, Xtera Communications, USA

DREW KELTON, President, Enterprise Services, Bharti Airtel Ltd, India

ANDREW LIPMAN, Partner, Bingham McCutchen, USA

MICHAEL RIEGER, VP, Tyco Electronics SubSea Communications LLC, USA

ROBIN RUSSEL, CEO, Australia Japan Cable, Australia

IHAB TERAZI, VP, Global Network Planning, Verizon, USA.

INTERNATIONAL TELECOM TRENDS

WORKSHOP

Organized by TeleGeography

TeleGeography’s annual workshop on international market trends, has become one of PTC’s most popular sessions. TeleGeography’s senior research team will present their latest findings on global voice and data traffic, network supply and demand, and trends in IP VPN and Ethernet service pricing. Specific topics will include: wholesale hot spots, Internet traffic, voice, wholesale prices and enterprise services.

Panelists:

STEPHAN BECKERT, VP, Strategy, TeleGeography, USA

BRIANNA CHARPENTIER, Research Analyst, TeleGeography, USA

TIM STRONGE, VP, Research, TeleGeography, USA

Tuesday, 18 January 2011

1400 – 1530 FEATURED SESSION 4 –

Undersea/Submarine Cable Developments in the Pacific

The last 12 months have seen an array of initiatives across the Pacific. While most have been very good, some have raised concerns. Others have raised challenges. The session will cover a few of these. There is the first new private cable initiative for some time in the form of Pacific Fibre which will test the current appetite for funding. The development of the new OADM BU appears to have real application for the Pacific. New regulations and changing interpretation of existing rules give cause for concern and need to be understood. And for something different, the novel idea of using communications cables to measure deep-sea currents will test conventional thinking. The speakers will engage you on these developments.

Moderator:

JOHN HIBBARD, CEO, Hibbard Consulting Pyt, Ltd, Australia

Panelists:

MARK RUSHWORTH, CEO, Pacific Fibre, New Zealand

MICHAEL RIEGER, VP, Tyco Electronics SubSea Communications LLC, USA

KENT BRESSIE, Partner, Wiltshire & Grannis LLP, USA

BRUCE HOWE, Professor, University of Hawai’I, USA

1545 – 1715 BREAKOUT SESSION T4: Subcable Vendor Smack Down

Are we upgrading or building, and who got the best “pick in mix” this time? A panel discussion where we put the spotlight on suppliers. Suppliers need to get creative with larger systems, smarter systems, ones capable of dealing with the challenges of meshing and cloud computing.

As operators we want big fat reliable pipes, we want seamless transition from our old

technology to the new stuff, with maximum flexibility at a price we can afford and grow into. Moreover, models are changing and in some cases there are multiple owners now of different fibers in the same cable– what if they want different suppliers for their upgrades at different times, can it all work together? How can the technology interface seamlessly with terrestrial networks to have structured simplicity? The business models and the customer requirements are changing and how are suppliers responding to this new wave.

Moderator:

FIONA BECK, President and CEO, Southern Cross Cable Network, New Zealand

Panelists:

NIGEL BAYLIFF, CEO, Huawei Marine Networks Co. Ltd., people’s Republic of China

HERVE FEVRIER, EVP and COO, Xtera Communications, USA

DAVID WELCH, Founder, EVP and CSO, Infinera, USA

THOMAS MOCK, SVP, Strategic Planning, Ciena, USA

The Industry Needs Its Champion

John Hibbard

As the telecoms industry will again gather at PTC in Hawaii, the question again arises as to the means of getting a credible voice for the submarine cable industry. The industry needs a champion who will be listened to by those external parties who shape our industry through either pro-active action, reactivity or passivity. Submarine cables are effectively the pinnacle of optical fibre technology yet they are not understood nor appreciated even though they are a necessary (but not sufficient) requirement for the penetration of the internet and the economic benefits that it can bring.

The World Bank findings, which have been replicated by Booz and Company (and reinforced by McKinsey) indicate that every 10% of penetration of broadband increases a country’s GDP by around 1.3%. This is substantial economic growth which will not occur without high bandwidth, low latency international connectivity. For many countries, that means submarine cables.

So why do so many countries seem to go out of their way to frustrate the provision, protection, operation and maintenance of submarine cables. At the SubOptic conference back in May, Kent Bressie provided an illuminating and persuasive argument that the lack of consideration for cables was a direct consequence of a series of myths held by our national and political leaders. Unless such myths are de-bunked, our industry will continue to be frustrated, and economies damaged, unknowingly by those aiming to stimulate economic growth. So how should we go about educating the politicians and the public of the importance of submarine cables and so encourage not

just the removal of roadblocks, but rather create an expressway which will accelerate the processes within our industry.

SubOptic is arguably our best known industry body. It holds the premier industry event every 3 years when the top thinkers and the leading content combine for our engagement. Comprised primarily of the vendors and the cable owners, SubOptic has a limited role between events. In the last triennium, SubOptic took the initiative to develop a supply contract template as a way to increase its value to the sub cable industry. Is this the first step to raising its profile so as to be the industry spokesman? Is the current structure of modest funding from vendors sufficient to enable such a transition, or is a more dramatic recasting of its organisational arrangements necessary for it to have the requisite clout?

The International Cable Protection Committee is another potential champion for our industry. The ICPC has been involved in lobbying in the past such as with the United Nations

Convention on the Law of the Sea. It has done much with the fishing industry to encourage harmony between competing forces. Historically only submarine cable owners could be members and hence much of the banter at their meetings involved preaching to the converted. The message was not getting out. At their most recent meeting, the decision was taken to widen their membership to allow governments to have representation with the aim of education, hopefully leading to better understanding and in due course supportive legislation. Very few countries have legislation to simplify the permitting for the provision of submarine cable while at the same time creating legally enforceable protection of a nation’s sub-sea umbilical cord(s). The ICPC move is clearly a step in the right direction but is it enough. The current ICPC charter is pitched towards cable protection and so can it be focussed on the simplification of permitting and provisioning. Should the charter of ICPC be extended to cover these aspects? Its funding from members has allowed active lobbying in the past so it may have the structure to expand and take on a broader role.

PTC is another body which has the possibility of being the industry spokesperson. It has the breadth of membership and a high degree of recognition, albeit mainly in Asia-Pacific and mainly for its annual conference. It has the capacity to extend its role but while it has always actively entertained the sub cable industry, its focus is much broader, and so its clout in presenting a case for our industry may be lessened. But with its breadth and

involvement with the broader aspects of telecommunications, it could well take a role in supporting the industry champion should one emerge.

ITU represents another potential spokesman, particularly as it is an arm of the United Nations and central body for telecommunications. However historically it has been hesitant at championing causes, and the operating logistics has made the generation of recommendations quite tortuous.

The industry needs its spokesperson to get out its message. It needs to educate those that matter on the merits of sub cables and to correct the myths that handicap the efficient operation of our business and the growth in the wealth of nations.

So what are those myths that pervade the minds of public, government officials and politicians. Clearly the greatest one is the belief that most international communications are carried on satellite. Even those in the communications areas of government believe that, when in fact 98% of non-TV intercontinental transmissions travel via submarine cables. Why is it so? One of our biggest handicaps is that we are out of sight. Hidden away on the sea-bed, it is not something that the average person

will ever encounter. We try to keep our cable station unobtrusive to avoid attention. The media, through the news gathering process is primarily focused on satellite. How often do we hear that news reader crosses via cable to an on-the-scene reporter? Never!! Yet such media material only represents a miniscule amount of what is downloaded daily on submarine cable from You Tube.

It is the squeaky wheel which gets the most oil. So assuming that we have a mouthpiece, how might we squeak loudly to get the desired attention. Maybe we could do so through extolling our technology. The gee-whiz factor is an important ingredient in why space travel or medical engineering get great recognition. People use the term “rocket scientists” as a synonym for engineering wizard. I doubt that many around the globe appreciate that submarine fibre optics is one of the highest tech pieces of science and engineering. By now everyone has heard of fibre optics. But how many comprehend the awesome nature of the technology which will transport billions of internet accesses across thousands of miles of ocean in a pipe the size of a garden hose which should remain faultless for 25 years. This is a story of supreme engineering which needs to be told.

I am not even sure that we ourselves don’t take such an achievement for granted. This message came home to me many years ago when I was hauled onto radio to explain a cable break. I recalled the time when the original SEACOM cable failed crossing the Marianas trench at 26,000 feet (8000+ metres).. We take as a matter of course that we can fish up the cable, repair it and return it to the sea. But the recovery and repair of cable is truly a major engineering feat.

To put it context for the listeners I portrayed the picture of flying in a jumbo, throwing out a rope to hook a garden hose – and doing it blind-folded. It was quite overwhelming the discussion and commentary that subsequently occurred highlighting that we have a story to tell.

So how do we tell this story of our business? Whether it is one of technology and one of economic importance, we need to get the message out there. But we can only do that with an industry champion. We need at least one body with an array of credible spokespersons to do this to cover the various facets of our business. We need a media campaign to ensure every opportunity is taken to maximize our exposure. Yes raising the profile of our industry could heighten the risks to our infrastructure but hiding our light under a bushel will see more and more adverse regulations introduced which will hamper our efficiency and raise the cost of cables. The industry needs a champion, at least one but several would be even better.

John Hibbard is a leading consultant in international telecommunications, particularly in the development of submarine cable projects. He has over 40 years experience in the telecommunications industry, mostly in international activities and submarine cables. Prior to becoming a consultant, John was Managing Director Global Wholesale at Telstra Australia, where he managed Telstra’s international business, and was founding Chairman of the Australia Japan Cable. He is now President of the Pacific Telecommunications Council and Chairman of its Board of Governors.

Embracing Subsea Cable Leadership

Dean Veverka

What is the ICPC?

The International Cable Protection Committee (ICPC) was formed in 1958 and its primary goal is to promote the safeguarding of submarine cables against man-made and natural hazards. It also provides a forum for the exchange of technical, legal and environmental information about submarine cables.

I wonder if those 10 founding organisations of ICPC had a vision of what the submarine cable landscape would look like 52 years later. After all, they were still in the coaxial cable era, TAT-1 the first transatlantic telephone cable had only been launched in 1956 and the first transatlantic fibre-optic cable was still 30 years away, with TAT-8 going into service in 1988!! One thing they did realise is the significance of providing utmost protection to submarine cables and that is even more vital these days due to the strategic importance of submarine telecommunications cables as Critical Infrastructure.

submarine fibre optic cable. The ICPC currently has over 100 members from 58 countries, and those members are responsible for almost 100% of international submarine telecommunications cables and a significant proportion of submarine power cables, thus making the ICPC the World’s premier submarine cable industry association.

Challenges for the Industry

The humble telecommunications submarine cable no longer just carries “telephone calls”. TAT-1 had a capacity of just 36 simultaneous telephone calls, today’s multi Terabit systems carry voice, data, the Internet, financial and social networks to such an extent that they are critical infrastructure to the economy of many nations.

following is the relevant extract from his report:

71. Submarine cables.

A need has been expressed by some States, including in recent workshops, to consider gaps in the existing legal regime regarding submarine cables at the international and national levels, in particular in the implementation of article 113 of the United Nations Convention on the Law of the Sea. Views have been expressed that the current legal regime is not adequate with respect to the operation of, and threats to, submarine cables. In particular, a need for a code of best practices with regard to the laying and repair of submarine cables and the conduct of cable-routing surveys was mentioned, among other things. In that context, a need for capacity-building activities facilitating the review of the legal regime and possible gaps therein could be considered.

There is still a widely held misconception that satellites carry the majority of international telecommunications capacity. However the reality is that almost all transoceanic communications is carried by

Following the disruptions to the internet caused by an earthquake in Taiwan/2006 and other events in Egypt/2008 and Sicily/2009, there is much greater awareness among Governments, the financial sector and other influential groups that submarine cables are part of the World’s critical infrastructure.

This message has spread even to the United Nations, where on 29 March 2010, the UN Secretary-General expressed concerns about the status of the world’s submarine cable network to the 65th Session of the General Assembly. The

The rapid evolution of submarine power cables is also gaining much attention as the world looks to offshore renewable energy sources. Submarine power cables suffer many of the same problems as telecommunications cables in terms of permitting, repair and environmental considerations.

So the new challenges for our industry are education and awareness of the importance of submarine cables to national governments and the end users. As well

as encouraging Governments to enact legislations that mirror the intentions of the United Nations Convention on Law of the Sea (UNCLOS) in terms of the protections and freedoms for submarine cables prescribed within the treaty.

ICPC way forward

The ICPC recently announced that it has changed its rules to allow Governments and companies that are key players in the submarine cable industry to be represented within its membership. The ICPC’s objective in making this change is to foster improved cooperation between Government and Industry, which is deemed essential to enhance the security of submarine cables.

A key factor that has emerged is that Governments are often in the critical path for installation and remedial work. It is therefore anticipated that having these represented within the ICPC will facilitate improved education and awareness, strengthening of legislative protections and rights in accordance with UNCLOS and the creation of single points of contact. The latter is deemed essential to help eliminate permitting delays and to facilitate the provision of urgent assistance in the event that the security of a submarine cable is threatened by illegal action.

the seabed with other users and to the understanding and protection of the marine environment.

Subject to certain criteria, membership of the ICPC is now also available to submarine cable system manufacturers, cable ship operators and submarine cable route survey companies in addition to submarine cable owners and maintenance authorities. It is anticipated that broadening the ICPC’s membership in this manner will improve the sharing of technical expertise within the submarine cable industry.

Recognition of ICPC on the World Stage

ICPC’s profile on the world stage has risen significantly in recent years. We are regularly invited, as the industries expert representative, to many workshops and conventions dedicated to submarine cable issues.

Presentations in the past two years given to:

• APEC-TEL Cable Protection Workshop in Singapore (At the invitation of the Australian government)

• Oceans Conference on Legal Challenges in Maritime Security, Heidelberg.

• Rhodes Academy on subject of submarine cables and UNCLOS.

• China Regional Workshop on Submarine Cables, Beijing. (ICPC cosponsor)

• ROGUCCI Summit, Dubai

• Submarine Cable Workshop, Centre for International Law, Singapore (ICPC co-sponsor)

• Cyber Security Summit, Dallas

• SubOptic 2010, Yokohama

In May and December 2009 the ICPC co-sponsored workshops in Beijing and Singapore with leading international law centres solely focused on submarine cables. The workshops brought together the top experts on international law of the sea, industry, and foreign Governments to study issues regarding protection of cables from terrorists, pirates, anchoring, and problems arising from requirements to obtain repair permits outside of territorial seas. Reports from the two workshops have been widely reviewed by Governments and are specifically referenced in the above quote from the UN Secretary-General. Diplomats are engaged to follow through on the various recommendations from the workshops in close liaison with the ICPC.

ICPC will continue its strong commitment to cooperative initiatives aimed at sharing

• Strategic Planning workshop on Global Oceans Issues in Marine Areas beyond National Jurisdiction, Nice.

The cooperation between Governments and the ICPC reflects the comfort the former has in dealing with a global body that broadly represents the cable industry

as opposed to dealing with individual companies. As the activities for ocean use intensify, Governments such as Australia and Singapore, international organizations such as the ISA, IMO, and ITU, as well as regional organizations such as APEC and ASEAN, will increasingly look to the ICPC as a global voice for the submarine cable industry. The ICPC’s success in pursuing partnership approaches with these Governments and organizations has been a unique success story in the history of submarine cables.

Recent Achievements

ICPC has also been the catalyst for independent research into submarine cables and the marine environment. This has led to peer-reviewed scientific papers as well as non-technical reports such as that prepared with the United Nations Environmental Programme (UNEP).

Entitled “Submarine cables and the oceans: connecting the world”, the UNEP-ICPC review was undertaken by a range of specialists in submarine communications. It deals with a suite of topics beginning with the history of submarine cables, their characteristics, cable deployment and maintenance, the status of cables in international law, environmental effects, human and natural hazards, and finally, a tentative look into the future. The 64 page booklet can be found at http://www. iscpc.org/ or http://www.unep-wcmc. org/pdfs/ICPC-UNEP_Cables.pdf .

Presently ICPC is involved with studies of (i) chemical leaching from cables, (ii) the submarine sediment flows that periodically damage the network off Taiwan and (iii) seabed response to sediment ploughing.

Much of this work forms part of a highly successful ICPC public information initiative. Reports, papers and PowerPoint presentations are readily accessible on the ICPC website where the presentation, “About Submarine Telecommunications Cables”, is attracting over 44,000 downloads annually.

Plenary announcement and call for papers

The ICPC holds an annual plenary meeting which provides updates to our members and a range of presentations. The 2011 plenary will take place in Singapore during the period 12-14 April 2011 inclusive and its theme is: Government & Industry working together: Enhancing the security of submarine cables

The Call For Papers is available from www.iscpc.org and the closing date for submissions is 31 January.

ICPC is Ready for the Leadership challenge

representing the submarine cable industry. We have evolved our membership criteria and look forward to working more closely with Governments and other industry participants to enhance the security of submarine cables and the vitally important traffic they carry.

Many of the ICPC members attend PTC and we look forward to another successful PTC event and continuing this debate.

Dean Veverka is the Director of Networks and Vice President of Operations for the Southern Cross Cable Network.

The ICPC has a broad membership base and a level of expertise that makes us the leading international association

PTC 2011: It Takes A Village

Guy Arnos

This year in Honolulu, WFN Strategies is proud to moderate a new workshop for all PTC attendees. Called “It Takes a Village”, this workshop consists of three panels composed of system owners, legal specialists, and system suppliers who are providing a primer on parenting the development of a submarine cable system. Broken down into three sessions, the workshop covers all aspects of a system’s life and growth, including infancy to adolescence and adulthood, corresponding with the system phases of development, implementation, and service provision.

Throughout the sessions, topical and important industry information will be candidly discussed. In the three hourlong sessions, topics of discussion will include, but are not limited to:

• The process of conceptualizing the project and assessing the market

• The process of financing a project

• Regulatory and permitting hurdles

• Supplier involvement in marketing, financing, logistics, and project management

• Project implementation issues and challenges

• Current and emerging markets and technologies, including what is frequently requested by customers, what is currently available and what new developments are required to provide nascent and emerging services

The panel of experts will provide not only their own insights and experience but will participate in an interactive question and answer period at the end of each session.

The panel of experts:

Infancy: Developing the Connection

Simon Cooper

Andrew Lipman

for company strategy development and execution for global network investment and partnership. He also leads pre-sales engineering and commercial discussions for Global Carrier Solutions. Previously, Mr. Cooper held various management roles at Level 3 Communications. He began his career at Cable and Wireless. Mr. Cooper held a Bachelors degree in Electronic Engineering from University of Nottingham.

Simon Cooper, Senior Vice President of Global Carrier Solutions at Tata Communications,

responsible

is

Andrew Lipman has spent more than 30 years developing Bingham’s Telecommunications, Media and Technology Group into one of the largest practices of its kind in the nation. He practices in virtually every aspect of communications law and related fields, including regulatory, transactional, litigation, legislative and land use. The TMT Group is international in scope, representing clients in the U.S., Central and South America, Europe, Asia and other parts of the world. Andy represents clients in both the private and public sectors, including those in the areas of local, long distance and international telephone common carriage; Internet services and technologies; conventional and emerging wireless services; satellite services; broadcasting; competitive video services; telecommunications equipment manufacturing; and other high technology applications.

Mike Rieger

Mr. Michael Rieger is Vice President of Sales at TE SubCom. He has been with Tyco Electronics since early 2000. In his current position, Mr. Rieger manages all sales activities on a global basis. Prior roles at TE SubCom include VP Sales for the TGN global network and Managing Director of Technology for TGN Operation Systems. Prior to his current assignment, Mr. Rieger held the position of Solutions Executive at IBM. Mr. Rieger has also held the positions of Senior Software Engineer for Bellcore and Systems Analyst for Merrill Lynch. Mr. Rieger has a Bachelors degree in Computer Science from Rutgers University in New Brunswick, New Jersey USA.

Adolescence: Making the Connection

Doug Burnett

Doug Burnett is a maritime partner in the New York City office of Squire, Sanders & Dempsey L.L.P, an international law firm with 32 offices in 15 nations. Mr. Burnett is a 1972 graduate of the U.S. Naval Academy and a 1980 graduate of the University of Denver Law School. He is a retired captain in the U.S. Navy and has worked on submarine cable cases for over 25 years. He has served as the International Law Adviser of the International Cable Protection Committee since 1999.

Motoyoshi Tokioa

Motoyoshi Tokioka has over twenty five years of experience in the international telecommunications system supply market, always working closely with world-class telecommunications operators, public and private organizations. Highly skilled at working across diverse cultural boundaries, Mr. Tokioka has successfully been satisfying a variety of customers’ needs. He served as Vice Chairman for the SubOptic 2007 Program Committee and now is a part of the Executive Committee for SubOptic 2013. Based in Tokyo, Mr. Tokioka is currently responsible for Global Sales and Marketing of NEC’s Submarine Networks business. He holds an MBA from the Graduate School of International Management, Aoyama Gakuin University in Tokyo.

Binod Sriwastav

Binod Sriwastav is the Business Head & VP for Global Connectivity Business at Bharti Airtel. He has been working in the telecom industry in India for more than 14 years. Prior to joining Bharti Airtel last year, he worked for a long stint at VSNL and TATA Communications. He has held several positions in product management, partnerships developments, sales, business development and international expansion.

Adulthood: Applying the Connection

Tony Frisch

Tony started in R&D, working at BT’s Martlesham labs on the first generation of submarine optical systems. He moved to Alcatel Australia and become involved in the practicalities of testing submarine systems during production, laying and final acceptance. A later move to Bell Labs (US) gave him experience in terminal design and troubleshooting, after which he went back to Alcatel, starting a gradual move towards the commercial world. In Alcatel France he worked initially in Sales and then moved to head Product Marketing for Submarine Networks. He is now SVP for repeatered solutions for Xtera Communications.

Per Hansen

Per Hansen is currently Senior Director, Submarine Solutions at Ciena, where he is focused on the networking needs of submarine cable operators. Per joined Ciena in September 2008 from ADVA Optical Networking, Prior to joining ADVA in 2004, Per was one of five founding professionals who established Photuris Inc., an early innovator of dynamic optical networking solutions. Earlier, he was with Bell Labs, where he worked on high-capacity, ultra-long haul transmission technologies for submarine applications. Per holds a doctorate in electrical engineering from

the Technical University of Denmark and Master of Business Administration from the Wharton School of Business at the University of Pennsylvania.

Robin Russell

Robin Russell has over thirty years experience in the telecommunications industry.

For the last seven years he has been CEO of Australia Japan Cable (AJC), an economical and ultra reliable submarine fibre optic network enabling links between Asia or North America and Australia. He holds a Master of Commerce degree from the University of New South Wales.

Ihab Tarazi

As vice president of Verizon’s Global Network Planning organization, Ihab Tarazi oversees one of the largest facilities-based communications networks in the world. Tarazi is responsible for the development and expansion of the FiOS, VoIP, IP and Ethernet network capabilities globally. He is driving the implementation of 100G Optical and Ethernet backbone to support the explosion of IP demand, and the implementation of Video product enhancement including Over The Top applications. Tarazi is the Chairman of the Board for Southern Cross Cable System and a Board Member of the Australia Japan Cable System. He is a graduate of the University of Maryland and has a Masters Degree in Telecom

Management from Southern Methodist University (SMU) in Dallas, Texas.

Moderator

Guy Arnos

Mr. Arnos has over 25 years experience in submarine and terrestrial networks, and has been responsible for the planning, engineering and implementation of transoceanic, transcontinental and metropolitan telecom systems. With WFN Strategies he has supported efforts in a number of submarine and terrestrial telecom projects, including the provision and installation of inter-platform submarine cable systems in the North Sea, Gulf of Mexico and Australia; engineering, provision and installation of fiber optic, RF, microwave and cellular telecom systems in Alaska, Antarctica and Colorado; and the engineering and provision of worldwide broadband services and trans-Pacific submarine cable systems. He joined WFN Strategies in 2001 as Director of Projects, and has been responsible for accomplishment of telecoms engineering projects in Angola (ADONES), Australia (NW Shelf), Antarctica, Trans-Pacific cables (MPC, Unity North), UAE (Multi-use Submarine Cable System), Colorado/Oklahoma/Wyoming (Broadband Wireless), and the Gulf of Mexico.

2011:

THE YEAR OF THE INVESTEMENT INTO NEUTRAL, DARK FIBER NETWORK INFRASTRUCTURE

Hunter Newby

It can be expected that 2011 will bring significant change to the network landscape in all aspects. In this New Year, many necessary steps will be taken to build both American and global infrastructure so that it can support the digital world and its present and future demands. The investment in physical layer assets ranging from dark fiber in the metro, regional and long-haul portions will enable more access points for fiber laterals to data centers, wireless towers and rural networks. With that access a more efficient use of fiber and transport will stimulate new designs for data center development and utility power delivery and consumption as well as fiber backhaul for wireless towers, community, government

and educational networks. It is and will be an exciting, challenging and rewarding time for everyone actively involved in the evolution of the industry. The recognition and awareness of the need for new dark fiber in every aspect of global networks is vital. From subsea to FTTH and everything in between, new dark fiber investments are being made globally. It is actually not a trend, but a necessity for every nation that wishes to be globally competitive on multiple levels. Investments are being made in fiber to towers and data centers, new diverse routes, better fiber for the 100G wavelengths and more. For those that invest and do so wisely, the returns will be significant in the years to come.

NETWORKS DRIVING NEW TRENDS

A new network system will drive the trends of 2011 and beyond. When network operators use services provided by neutral, colocation fiber-optic cable service providers, they reap the benefit of immediate access and avoid the problems of acquiring routes for fiber and constructing and maintaining the fiber systems. Neutral fiber providers are landlords to the network operators, providing them with access to the space, power and fiber they need to run their businesses.

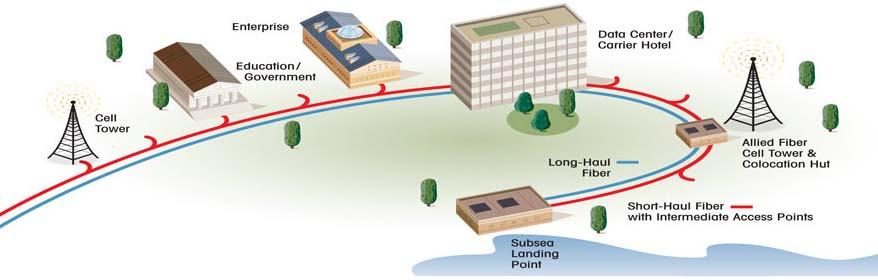

Allied Fiber, for example, is not a carrier itself. It is in the physical layer, dark fiber, neutral colocation and interconnection

business. The company uses a multi-duct fiber system design that deploys longhaul duct-and-fiber cable with a separate, parallel, short-haul duct-and-fiber cable. The short-haul duct-and-fiber cable (the red line in the above diagram) is built with hand holes usually placed every 3,000 feet, but hand holes can be placed wherever required. Hand holes provide intermediate access to fiber for physical routing to the closest colocation facility providing access to the long-haul fiber. The hand holes are placed wherever there is a point of interest for fiber, such as an existing regional, rural or metro fiber network, a data center, an office park, a university or a wireless telecommunications tower. It is left to those who have local knowledge to build lateral fiber ducts or subtending dark fiber rings off of the route to reach these points of interest. The multi-duct business model and design provides for access to any and all network operators that need an environment in which they can openly and freely interconnect with other networks.

FIBER-TO-THE-TOWER

A revolutionary aspect of the multi-duct new design is its focus on fiber-to-the-tower overlaid on a long-haul fiber network. This approach to dark fiber connectivity to towers along the route for microwave backhaul to support mobile wireless traffic is unique. Without the interplay between

fiber and microwave transport, wireless carriers’ backhaul needs will never be met. Using the multi-duct system, transport providers to the mobile operators can more easily and cost-effectively design and build their networks over dark fiber that they light themselves. The multi-duct system’s long-haul dark fiber provides direct access back into the major carrier hotels and data centers where the mobile operators can easily exchange data traffic with other network operators, making the entire process more seamless and scalable.

OPEN MARKET FOR TELECOM

The multi-duct system ensures that more communities will have a chance to be onnet and share in the benefits that many other on-net communities have. This open market for telecommunications was once just a carrier secret in the largest cities. The concept for the new plan is to offer a neutral

connectivity environment to more and more communities to increase broadband access and improve the economy, health care and the overall standard of living. The multi-duct system begins at what is called the point of origin, essentially the location where international cables come up from the ocean, also known as subsea landing points.

SUBSEA LANDING POINTS

Subsea landing points represent the aggregated amount of global fiber-optic cable capacity flowing around the world. The multi-duct system begins and ends at these locations, harnessing the power of the networking demand of the earth’s continents and the countries, people and machines within them. In a network sense, the United States is geographically

located on planet Earth right in the middle of Asia, Europe and Latin America. The major subsea networks of the world travel across the Atlantic Ocean from Europe to New Jersey and Long Island, N.Y., from South America through the Caribbean Sea to Florida and from Asia across the Pacific Ocean to Washington, Oregon and California.

MOBILE BACKHAUL

Mobile backhaul is playing an increasingly dramatic role in the growth of all network transport requirements. In truth, there is not enough backhaul capacity to suffice and more intelligent routing and switching architectures must be deployed to keep mobile traffic as local as possible. This is not as much of an issue in submarine systems, but it is critically important from an inter-nation peering perspective particularly in Southeast Asia. The mobile network operators cannot expect to establish reliable, high-speed connections to content providers of video being served nations, or oceans away and have any meaningful level of quality of service or user experience. If the video content is local by nature then it is less of an issue, if any at all. If the video content is coming from a neighboring country, but via a connection on the Any2 Exchange at 1 Wilshire Blvd in Los Angeles, there will be throughput issues to contend with for sure. This will

necessarily dictate video peering to be established closer to home, or deal with a provider, perhaps only one, or two, that have a network robust enough to support the capacity and latency requirements. Verizon is once such provider, but their rate structure is quite different than lowcost to free peering on Any 2.

LOOKING AHEAD

As user demand increases, network systems must increase to meet the demands of consumers. Technologies, from standards in DWDM, Ethernet, IP, Wimax and LTE to smart phones and tablet computers, are strongly influencing and driving bandwidth growth. Broadband bandwidth cannot meet current demands (consider the rate at which smart phones and tablet computers, such as the iPads, are being sold). Certain mobile service providers have been forced to change their bandwidth plans to metered packages because unlimited bandwidth is not a realistic option. Backhaul and the backbone to support these networks will need to increase over the next year and in the future because the rate of which consumers are buying these types of products will only continue to increase. In order to be globally competitive, a national infrastructure that supports rapid growth must be present. Fueled by the subsea cable system, a new multi-duct system

can provide the needed backhaul for the technologies of the future.

Hunter Newby, a 15year veteran of the telecom networking industry, is the Founder and CEO of Allied Fiber. Mr. Newby possesses an extensive breadth of experience within the industry. In addition to physical layer interconnection, Mr. Newby is a recognized authority on Internet and Ethernet exchanges and VoIP Peering.

CONNECTING THE MIDDLE EAST REGION WITH

SUB SEA CABLES AND COMMUNICATION SERVICES

Ilissa Miller

The growth of the submarine cable industry is exploding in the Middle East – a land that tends to receive far too much attention on its political, religious and social issues, and not enough on its rapidly expanding economy, particularly in the area of telecommunications.

According to a 2008 study commissioned by the Telecommunications Industry Association (TIA), the Middle East ranked second in terms of growth within the telecom sector for global regions with a projected 11.1% growth rate for the years 2008 through 2011. In recent years, profound developments in telecommunications, computer and IT sectors have occurred, largely due to the opening of large and previously unreachable markets, high state investments, lessening of restrictions on foreign entry, increased market liberalization, and actions taken against piracy. Throughout the region, telecommunications infrastructures are advancing as more and more governments realize the critical role they have in sound economic development.

Although the ratio of telephone lines to population is still comparatively low while considering other global regions, such as Europe, the numbers are rising. Progression on networks based on fiber optic lines, wireless telephony, satellite transmission and submarine cable technology results with the bypassing of the existing communications infrastructure in the region, thus providing businesses and

affluent societies with alternative, superior grade telecom solutions. The modernizing telecommunications infrastructure is supported chiefly by the substantial growth of the Internet in the Middle East. Although the initial introduction of the Internet was perceived as a threat by local governments to the region’s traditional values and political systems, according to Info-Prod Research, now nearly all Middle Eastern countries permit public access to the World Wide Web, and experience a steady 10% usage growth per month. More than 100 companies in the Middle East now provide Internet connectivity, thereby causing an increased demand for both regular telephone and broadband infrastructure.

The 2010 Cisco Visual Networking Index (VNI) Forecast for 2009-2014 predicts that IP traffic in the Middle East will reach one Exabyte per month by 2014, at a growth rate of 45 percent. Internet traffic will generate 182 million DVDs worth of traffic, or 727 terabytes on a monthly basis. The VNI also concludes that the Middle East will possess the strongest mobile data traffic growth of any region.

Addressing this growth is submarine cable infrastructures, as modern cables utilize optical fiber technology to carry digital payloads, which in turn are used to then carry telephone, Internet and private data traffic. Submarine cables

As stated by the Global Technology Forum, from 2000 to 2010, the Middle East experienced a tremendous growth in Internet usage with a staggering 1,825% increase, and states within the region were also responsible for some of the highest growth rates in the use of DSL technology (presently the dominant form of broadband technology in the region).

link all of the world’s continents together, with the exception of Antarctica currently. In addition to linking countries together, today’s modern submarine cable systems are designed to deliver faultless Ethernet and mobile connectivity.

Today’s modern fiber optic submarine cable systems are considerably superior as compared to early generation cable, satellite and microwave networks to carry voice and data traffic. Additionally, they are capable of high speed data transfers, able to support the shorter latency demand, and ensure error-free communications. Global expansion of cable systems, in combination with evolving technology, offers a higher bandwidth that greatly reduce costs and improve quality.

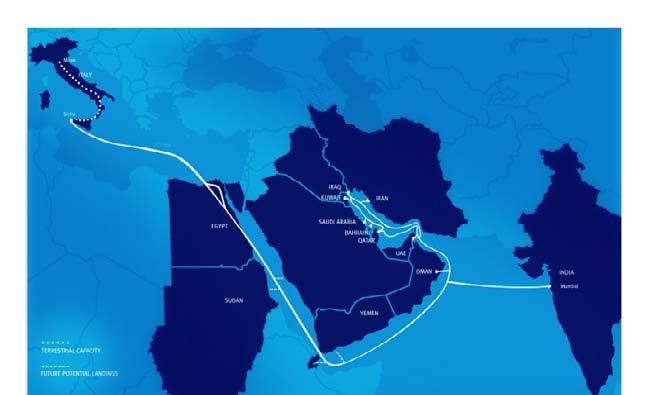

Further bridging the connection to the Middle East via submarine cable is Gulf Bridge International, the Middle East’s first privately-owned, submarine cable operator, posed to positively transform the face of international connectivity within the area. Thanks to lucrative partnerships with companies like Tinet, a global carrier exclusively committed to the IP and Ethernet wholesale markets, GBI will not only expand within its own region, but will be able to offer services throughout Europe as well. Earlier this year, GBI also partnered with Asia’s leading independent telecommunications service provider, Pacnet, allowing the company to increase its connectivity to

Asia as a whole, while providing new and cost effective solutions for customers.

With a scheduled 2011 launch, the GBI cable system will connect all of the countries in the Gulf via a core ring, which will reroute traffic, thus increasing resilience. The cable system, designed to operate for up to 25 years, has a design capacity of up to 5 terabits per second on select cable sections, and possesses the capability to address the

rapid growth of traffic originating and terminating in the Gulf. Providing greater capacity, reach, resilience, diversity and choice via its innovative cable system, GBI will notably become the region’s most advanced network providing broadband carrier services to telecoms operators from around the Gulf and beyond.

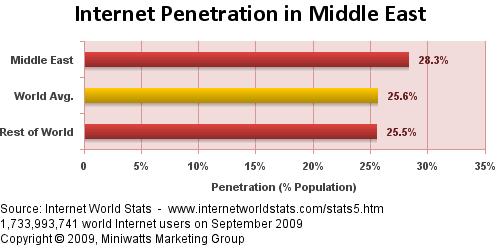

With Asymmetric Digital Subscriber Line (ADSL) as the prevailing broadband

Internet technology in the region with a 28.3% broadband penetration rate among its population (compared to 25.6% world average), the GBI cable system will undoubtedly serve as the chief method for sending and receiving global voice and data. GBI is particularly distinctive for its highly anticipated cable system as it will be developed and owned directly by GCC investors, who are building the infrastructure to best serve the entire region. Considering that laying these cables costs amounts upwards of one billion dollars and more, most of the systems are owned by consortiums comprised of several telecom companies, each of which shares the cost, ownership and bandwidth fractionally. GBI stands out as the first and only privatelyowned submarine cable operator in this region.

With partners like Tinet, GBI largely benefits by having its network interconnected in Europe, and having its services, such as Global IP Transit, Ethernet, and VPLS connectivity offered via Tinet’s global footprint. Moreover, GBI will provide highly desired capacity to Tinet in countries and cities in which the GBI Cable System is present.

“This agreement with Tinet will strengthen our position in the European market,” comments Mr. Ahmed Mekky, Board Member and CEO of GBI. “We are pleased to be working with Tinet to facilitate a more resilient communications infrastructure

between the Middle East and Europe. Traffic between the Middle East and Europe is growing at an unprecedented rate and through agreements such as this, GBI will be able to provide comprehensive coverage across Europe to our customers.”

Tinet also commented on the rapidly expanding Gulf Region market. Tinet’s Chief Executive Officer Paolo Susnik states, “Our partnership with GBI will allow Tinet to extend our reach into fast growing markets, such as the Middle East, and further offer industry-leading connectivity services to customers.”

In addition to submarine cable operators such as GBI and IP Transit and Ethernet providers such as Tinet, there are several

other companies who have quickly responded to the rapidly advancing technology developments in the Middle East, and have since opened several regional offices in the Middle East. Microsoft, Intel, and Acer are just a few of the companies who are expanding in the area.

Specifically for submarine cable systems, companies like Tata Communications have partnered with major telecommunications operators in the Middle East to construct the TGN Gulf cable system, which will directly connect the region to the world’s top business hubs and city centers. In July, it was announced that six of the region’s leading telecom operators signed an agreement to build and maintain a multiterabit terrestrial cable system designed to connect the UAE, Saudi Arabia, Jordan, and Syria to Europe – known as the Regional Cable Network (RCN).

The positive developments taking place in the Middle East, particularly those related to telecommunications and innovative global submarine cable systems that will

further connect the region with the rest of the world, are crucial components to achieving and sustaining peace, stability and prosperity. Emerging technologies and freedom of the press ultimately have a helpful impact on the region’s youth, and will also reduce red tape and bureaucratic obstacles, thereby supporting participation in defining future strategies at both regional and national levels, and boosting investment opportunities in the area.

In the end, a possible key to achieving peace in this region could come from the establishment of reliable communications and interconnecting with the world. Global submarine cable systems are a feasible solution to furthering these efforts in the region, and enabling governments and citizens to feel empowered with technology.

Ilissa Miller brings over 10 years of experience in Sales and Marketing to JS&A. Mrs. Miller brings a wealth of experience and knowledge in sales and marketing for emerging global telecommunications and technology companies where she implemented and spearheaded many global product and marketing campaigns that included international private line and networks, IP transit, peering, IPVPN, hosted PBX, managed services and colocation products and solutions.

Capacity Just Waiting

Connecting Australia’s NBN Future To The Globe

Ross Pfeffer

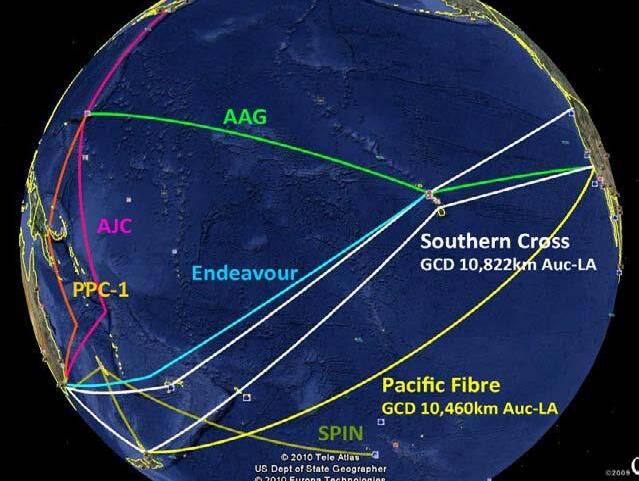

Five high capacity fibre-optic submarine cables with a total lit capacity of 2 Tbps leave the eastern seaboard of Australia. Three cables take the shortest path, some 28,000 kilometres across the Pacific to the US West Coast, and two terminate in S.E Asia to interconnect with the trans-oceanic superhighway.

But is this enough? Is there sufficient capacity, market competition and network resilience, is the cost of capacity too high, and will the current excess supply and upgrade capability be adequate to support Australia’s rapid move to high speed broadband and in particular the Government’s A$43 billion National Broadband Network that is now under construction.

Australia is approaching saturation in broadband penetration. Fixed line broadband subscriber growth fuelled the rapid growth in international capacity from 2005 until about two years ago, but capacity growth is now dominated by the combined effects of higher access speeds, larger data entitlements, lower data costs and the dominance of video based applications.

Data download costs fall dramatically

As a recent analysis by Market Clarity1 shows the cost of broadband subscriptions has remained about the same for a number

1 Market Clarity Report: “Broadband Download behaviour in Australia”, January 2011

• AU has 5 direct cables

• NZ has 2 direct and 3 indirect cables

• Replacement cost: >USD 2.7B

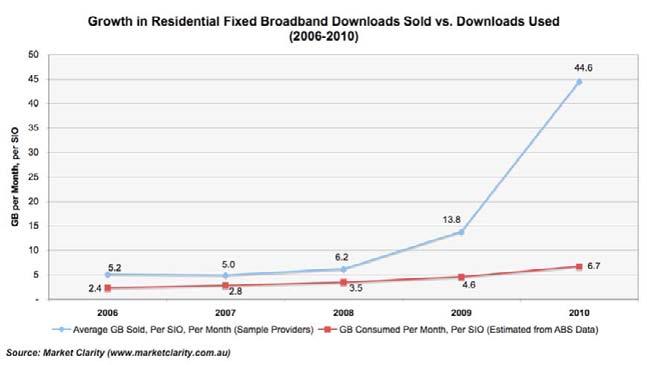

of years. At the same time data download costs have dropped dramatically, data entitlements have increased and, not surprisingly, downloads per subscriber have increased. Analysis of all the available data by Market Clarity indicates that the average data entitlement of fixed line residential subscribers was 44 Gigabytes as at June 2010 six times more than the average download per broadband subscriber (fixed + wireless) 6.7 Gigabytes.

Growth of Wireless

There has been an impressive shift in speed and entitlement in just a few years. We know broadband will continue to change at a rapid pace and the NBN will be a major platform for delivery. But it won’t be the only one. In recent years the move to wireless broadband enabled devices has been extremely rapid with the July 2010 IAS showing 39% of broadband connections had wireless access, growing

at 22% in 6 months compared to a fixed line increase of only 2%. At the same time average monthly downloads from wireless actually decreased slightly to around 600MB.

The wireless implication for international capacity demand is that an increasing proportion of internet experience is becoming wireless based where access speed and download quotas are much lower. Despite this as some suggest wireless may be substituting for additional retail spending on fixed network based services.

International Capacity

It’s all happening on the demand side, so can international capacity supply cope. For the five installed routes currently out of Australia I estimate total activated capacity to all destinations (excluding any provision for restoration or protection) at about 0.5Tbps. After making a provision for ISPs acquiring above base demand for factors such as protection then gross active capacity is estimated to be around 0.7 Tbps. At the same time total lit capacity is estimated to be around 2.0 Tbps.

For the near term, there appears to be plenty of capacity to support demand. In fact, over the last few years the industry has been in a state of excess supply having invested too much in cable deployment and subsequent equipping (with a

replacement cost of some US$3 Billion) relative to the current level of demand. At the present rate of growth in demand, and with no further investment, the excess supply may exist for another 5-6 years.

But that’s based on historical rapid demand growth as we know it, not the demand that could be. This raises the two key questions about the role of the submarine cable industry in Australia.

1. Is the cost of capacity too high to realise current latent demand;and

2. Are we on the cusp of an NBN induced demand change that is so big and rapid that the current excess supply and upgrade capability will not be adequate?

Cost of Capacity

It has often been said that the cost of international capacity for both Australia and its close neighbour New Zealand (which is solely supported by the two diverse cables of Southern Cross) is too high and this causes expensive retail broadband pricing and inadequate data download entitlements.

To be fair, international capacity prices (which are the same out of Australia and New Zealand) are still high by TransAtlantic and Trans North-Pacific standards. Despite higher capital cost (estimated at US$128 per Australasian User compared to US$14 per user on these Super-highway routes), ANZ to US capacity prices have

declined by an average of around 25% annually for over 10 years. Price has fallen under the combined influence of healthy competition, rising demand and falling upgrade costs, but is price still acting as a demand throttle?

A valid way to determine this may be to compare actual data downloads with download entitlements. Over the last few years there has been a steady and dramatic improvement in the volume of data entitlement for broadband subscribers in Australia. In Market Clarity’s recent report average monthly download entitlements are estimated to have grown from 5 Gigabytes per month in June 2006 to nearly 45 Gbytes by June 2010. At the same time data downloads for fixed plus wireless broadband subscribers increased from just 2.4 Gigabytes to nearly 7 Gigabytes.

Leaving aside the growth over the last six months in terabyte plans, the implication of the ABS data to June 2010 must be that Australian broadband subscribers effectively pay much more for their data than they need to (compared to buying a cheaper plan with a lower entitlement). Alternately, if they could, or wanted to, as at June 2010 they could on average download another 38 Gigabytes per user for the same average cost. So it looks like the cost of international data is unlikely to be throttling broadband downloads.

Access Speeds

There must be other reasons why capacity demand is not higher so we will now consider access speed. Based on ABS reports, the weighted average access speed increased from 300kbps to about 7Mbps (or 2300% increase) over the period 2007 to 2010. As the percentage of subscribers with 8 Mbps access or higher continues to grow from the current 40% the likelihood of access facilitating greater download volumes will strengthen. More importantly as the NBN is rolled out with the objective of providing around 90% of the population with access at 100Mbps there can be little doubt about the complete removal of access speed as a potential constraint right across Australia.

600% paradigm shift in access speed and the 900% shift in data entitlements. On the basis of past experience the likelihood of further huge increases in average access speed, of the magnitude planned for the NBN, resulting in commensurate increases in downloads in the future seems very low.

Not everyone wants or needs to download large volumes of data. If the internet was actually faster users can do a lot more in the same amount of time they spend now.

Contention