I ran my 20th annual marathon last month. While it wasn’t my fastest effort, it was by no means the slowest either. After you’ve run a few you become a little more stoic about the thing; you even at times feel invincible.

I have come to love the moments before the start when thirty thousand or so of us are amassed in various finishing time pens on the road alongside Arlington National Cemetery. You meet some interesting people at this time, and generally they are younger and a lot more worried than you. They talk about “if” they finish, not “when,” and you the older and maybe the wiser tell them this is your twentieth marathon, and yes, they, too, will finish.

It’s not about time as much as about finishing. The fact that

you can still get your aging, fat butt around a long day’s course is amazing, and if you’re really cunning like some of us, you print your name on the front of your shirt so that total strangers will cheer you on for 26.2. It’s good for me to have this annual goal, and it is no less humbling when some 80-something year old passes me mid race.

Thus leads me to the theme of this month’s issue - Upgrades.

I won’t compare an aging runner to upgrading a submarine cable system; that would be too cheeky. But somehow

the addition over the years of Kinesio tape or Zensah compression sleeves to my regimen is kind of like upgrading; adding new tools to the old system to buy some more life, maybe even make it faster and better.

Every year I’m asked how long I’ll keep doing this, and my answer is the same: as long as I

can. I am reminded of that last line from Blade Runner, and I suppose it’s true for anything: “I didn’t know how long we had together... Who does?”

I guess that still holds true.

Wayne Nielsen is the Founder and Publisher of Submarine Telecoms Forum, and previously in 1991, founded and published “Soundings”, a print magazine developed for then BT Marine. In 1998, he founded and published for SAIC the magazine, “Real Time”, the industry’s first electronic magazine. He has written a number of industry papers and articles over the years, and is the author of two published novels, Semblance of Balance (2002, 2014) and Snake Dancer’s Song (2004).

+1.703.444.2527

wnielsen@subtelforum.com

In This Issue...

90% Undersea Cables In Nigeria

Under-utilised

A Multinational Project To Build A New Underwater Cable Uniting Latin America And The U.S.

AAG submarine cable to restart full operation on 3 October

AAG Upgrades Trans-Pacific

Submarine Cable Network With Ciena

Alcatel-Lucent Loss Narrows As Cost Cuts Boost Margins

Alcatel-Lucent Reinforces Plan To Take Submarine Network Division Public

Alcatel-Lucent To Double Capacity Of Today’s Data Transport Networks By Being First To Deliver A Single-Carrier 200G DWDM Optical Line Card

APTelecom ‘State of Subsea’ Bangkok Receives Strong Reviews As Expert Event Series Makes Asian Debut

Brazil-to-Portugal Cable Shapes Up as Anti-NSA Case Study

Broadband Internet For Solomons In 2016

Cable & Wireless Broadens Horizons With Columbus Deal

Chunghwa Telecom To Jointly Build Cross-Pacific Cable Network

First Phase Of 100G Submarine Cable Upgrade With Ciena

Faster Internet Speeds By 2018 Under BIMP Project Seen

Fugro Commences The Cable Route Survey For AAE-1

Furukawa Electric Announces Commercial Production Of Micro ITLA For 400 Gb/s Optical Coherent Transmission

HC2 Announces Acquisition Of Global Marine Systems Limited And Completion Of Related Financing Transactions

Interent Service Providers Assure Service Will Not Be Affected By Submarine Cable Maintenance

Internet connectivity 100% restored in Vietnam as cable cut fixed 1 day early

Internet Service Remains Stable

Amid SAT-3 Facility Cut

Internet Service Remains Stable Amid SAT-3 Facility Cut

KT Vows To Build Global Internet Hub In Busan

MainOne Urges Submarine Cables Protection

MoEF Committee Clears Reliance,

Vodafone Marine Cable System

NEC Inks Supply Deal For AAE-1

Submarine Cable

NEC To Supply The World’s First Submarine Cable Across The South

Atlantic

New Cut Found On Submarine

Cable System Providing Internet

Connection To Vietnam

New LC Crimp And Cleave

Connector And Termination Kit

Expand Breadth Of OFS’ GiHCS®

Industrial Cabling Solution

New SEA-US Submarine Cable System To Link Indonesia, Philippines With US

Orascom Telecom Media And Technology Holding Announces The Launch Of Service Of Its

Submarine Cable (MENA)

Orascom Telecom Relinquishes

Submarine Cables Licensing

Repairs To Cable Break Disrupting

Vietnam’s Internet To Take Nearly 20 Days

Tampnet To Acquire CNSFTC From BPEOC

TE Aims To Expand Number Of Submarine Cables To 21 By End Of

2016

TE SubCom Optical Fiber Connects

Subsea Gear

U.N. Task Force Says New Ocean Telecom Cables Should Be ‘Green’

Vietnam Service Provider Blames

Poor Design For Submarine Internet

Cable Fractures

Xtera Demonstrates 150 x 100G

Transmission over Unrepeatered Distance of 410 km Using Wise Raman™ Solution

INTELLIGENCE, ANALYSIS, AND

THE INTERNATIONAL TELECOMMUNICATIONS INFRASTRUCTURE COMMUNITY

Terabit Consulting is a leading source of market intelligence, forecasting, and guidance for the international telecommunications infrastructure community. Its long history of accurate, innovative analysis and advisory services is in large part attributable to the trust and respect it has earned among industry leaders. Terabit Consulting has completed studies for dozens of leading telecom infrastructure projects worldwide and its analysts have traveled to research and deliver studies in more than 70 countries, giving it an unmatched level of experience in nearly every region of the globe.

Terabit’s primary clients include financial institutions, development agencies, government ministries, telecom carriers, project developers, suppliers, financiers, law offices, and industry associations, as well as other members of the international telecommunications infrastructure community.

Learn more at www.terabitconsulting.com or contact a Terabit Consulting representative today.

Terabit Consulting

245 First Street, 18th Floor

Cambridge, Massachusetts 02142 USA

Tel. +1 617 444 8605

info@terabitconsulting.com

Overview

System Upgrades An

Kieran Clark

Welcome to SubTel Forum’s annual Upgrades issue. This month, we’ll take a look at the impact upgrade technology has had on the industry, and discuss what it means for the future. The data used in this article is obtained from the public domain and is tracked by the ever evolving SubTel Forum database, where products like the Almanac and Cable Map find their roots.

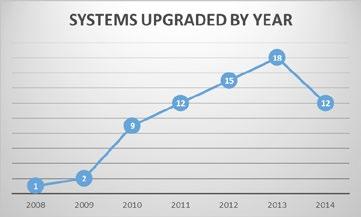

The first instance of a cable system being upgraded was in 2008. Since then, a total of 59 systems have been reported to be upgraded around the world. Several of these systems have been upgraded

multiple times, resulting in a total of 69 reported upgrades.

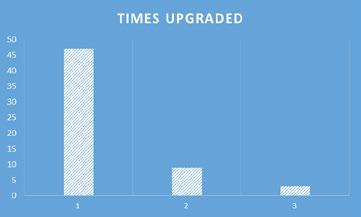

As illustrated by the chart below, upgrades became much more common after 2010. We saw an increase in the number of systems upgraded every year until 2014, which had a moderate decrease in upgrade activity.

With upgrades giving system owners a way to stay competitive at a fraction of the cost of entirely new systems, it’s no surprise that the upgrade market has been robust in recent years. Being able to upgrade capacity by simply swapping out easily accessible hardware has allowed many aging systems to stay competitive, and keep

up with capacity demands. The cost effectiveness of upgradeable capacity has even resulted in making brand new systems fiscally impractical, allowing owners to stay on top of their respective markets. In short, upgrades are a smart and effective way to keep a system relevant, even years after its saturation date.

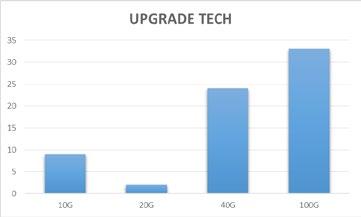

The chart above illustrates that 100G technology has been the most prevalent upgrade technology utilized to date, with 40G following at a short second. This is due to system upgrades not becoming popular until 2010, when 100G first hit the market. It’s very likely that the advent of

100G technology is actually responsible for the sudden surge in upgrades. For many systems still on 10G or earlier technology, it allowed for massive capacity increase for just a fraction of the cost a new system would entail. While 40G technology was available as early as 2008, it did not offer many system owners a cost effective capacity increase at the time. With 100G being available so soon after 40G, there is a good chance many owners simply chose to wait until they could upgrade their systems tenfold, if not more.

Looking ahead slightly, we can already see companies working on 200G and 400G. These technologies should be

available in the next year or two, giving system owners even more options. It’s likely that 400G will be the most popular, while 200G will likely be reserved for edge cases, similar to 40G and 20G technologies. With there being no currently known limit to just how much data can be packed on a single wavelength, the possibilities for upgrade technologies over the next decade could quite literally be limitless.

The vast majority of upgraded systems have only been upgraded a single time. The previous two charts have shown us that upgrades only started to be popular in 2010, with 100G being the most

popular upgrade technology. With 100G having been made available as early as 2010, it’s no surprise to see that most systems have only been upgraded once. The longest a system has been active before being upgraded was 18 years, while the shortest amount of time was a single year of service. Over 59 systems, the average age before being upgraded for the first time is 8 years. With 400G upgrade technology on the horizon, it will be interesting to see if more recent systems decide to upgrade and start to bring that average down.

With bandwidth demands projected to increase at a rather rapid pace across the

globe, expect the number of system upgrades to increase accordingly. Many aging systems will need to upgrade to stay relevant, while more recent systems will likely want to keep the demand for new systems low.

While nearly every region has seen at least some upgrade activity, the vast majority of upgraded systems have been in the Pacific and the Atlantic regions. This should come as little surprise, as these are by far the two most competitive regions in the industry. A capacity upgrade can allow more customers to be served, and potentially drive out new systems by meeting or exceeding current capacity

demands. As a result of owners trying to stay on top of the competition, 13 systems in the Atlantic have been upgraded, with 18 in the Pacific. Out of 59 total systems upgraded since 2008, these account for more than half.

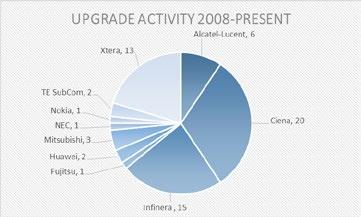

The chart above showcases all the players in the upgrade market since its inception. As you can see, three companies have managed to carve out their own niche in the submarine telecoms industry by focusing heavily on upgrades. In general, upgrades have given equipment suppliers a new way to generate revenue, rather than relying on

manufacturing entirely new systems. While the money brought in from performing an upgrade is much less than building an entirely new system, it is perhaps a more consistent form of income.

As upgrades continue to increase in popularity, we can expect these companies to increase their market activity.

Kieran Clark is an Analyst for Submarine Telecoms Forum. He joined the company in 2013 as a Broadcast Technician to provide support for live event video streaming. In 2014, Kieran was promoted

Forum publications. He has 4+ years of live production experience and has worked alongside some of the premier organizations in video web streaming. to Analyst and is currently responsible for the research and maintenance that supports the SubTel Forum International Submarine Cable Database; his analysis is featured in almost the entire array of SubTel

With so many systems in the world considering an upgrade, there may even be opportunities for new players to enter the market.

Gone are the days when owners needed to commission an entirely new system to keep up with capacity demands. Instead, they can simply purchase equipment to

improve their already existing cables. This saves money, and perhaps more importantly, time. Building a new cable system is a very lengthy process, while upgrading a system can be done relatively quickly and with hardly any interruption of service. Looking forward, expect the upgrade market to become

increasingly competitive, and perhaps lessen the demand for new systems in certain highly developed regions like the north Atlantic and north Pacific. In short, we can see that upgrades are very much a part of this industry’s future, and an increasingly important one at that.

Transport

Upgrades Are Evolving

According to industry representatives, upgrades are evolving at a fast pace and the market is only getting better.

“It’s actually very robust right now,” said Steve Grubb, Infinera’s director of optical systems. “Everyone’s [upgrading].”

The last few years has seen almost continual increase in the capacity and viability of upgrade technology. In fact, Grubb said, the continual improvement of the technology caused a lack of market demand for the 100 gigabyte upgrades when they initially became available.

“I think a lot of people were indecisive about what to do,” Grubb said.

Initially, no one wanted to be the first to try out the new upgrades, he said, but once they were proven the market exploded for the new product. Grubb said this is mainly because people are trying to get as much as possible from existing cables.

The secret of this consistent improvement in capacity in upgrades is Coherent technology.

“It was something that was developed for the terrestrial market,” Grubb said.

The new Submarine Line Terminal Equipment (SLTE) allows for coding in both

the phase and amplitude of light, creating a whole new dimension in which to encode information.

“That’s kind of the de facto standard now,” Grubb said.

Currently, there’s a tug-ofwar between the decision to upgrade and the decision to lay a whole new line. The choice tends to be made by the expiration date of the line.

The new Coherent technology also has the benefit of mitigating degradation of information like chromatic dispersion (CD), polarization mode dispersion (PMD) and more recently, nonlinear impairments, according to him.

Still, Grubb said, the use of the new 100 gig upgrades is a viable choice, even if interest is still growing.

This may, in fact, create a period that negatively affects producers of the upgrades, while the use of 100 gig upgrades takes greater hold.

“I think carriers will digest this new technology and drive down the price,” Grubb said.

Despite that, Grubb said that the 100 gig upgrades using Coherent technology are becoming a standard choice for companies looking to increase capacity without laying new cable.

In the near future, with implementation as soon as 2016, the use of Coherent technology will allow for 400 gig upgrades.

“I’d hesitate to say it’s more advanced,” Grubb said. “It’s built on the 100 gig, technology. It’s more of an evolution.”

There are apparently new limitations to an increase to 400 gig upgrades, however.

According to Colin Anderson, submarine networks marketing director of Ciena, there is an assumption that 400 gig technology will give 4 times the ultimate capacity of 100 gig upgrades.

“When we migrated from 16 x 2.5 gig to 16 x 10 gig, the ultimate capacity of the cable increased four times,” he said in an email. “And moving from 64 x 10 gig to 64 x 100 gig meant a 10 times increase in ultimate capacity.”

However in those 2.5G and 10G systems, the optical signals did not fully occupy the allocated bandwidth slots.

So, when increasing the linerate, the number of channels could remain constant, and the ultimate capacity increased according to the line-rate, according to Anderson.

While 100 gig upgrades can accommodate technologies like spectral shaping and flexible grid tuning to pack the waves closer together and occupy almost the entire spectrum, 400 gig single-wave solutions will only be able to

accommodate a fourth of the waves of a 100 gig upgrade.

“So for example 20 waves of 400 gig would be possible where before we had 80 waves of 100G, resulting in the same ultimate capacity,” Anderson said.

When upgrades to 400 gig becomes available, these solutions will be made only if they save infrastructure or operational costs, not because they offer increased ultimate capacity, according to Anderson.

“New technologies such as single-wave 400 gig or 1 terabyte line-side may come in the future, but client interfaces of up to 400 gig or 1 terabyte do not rely upon their deployment,” Anderson said, “and the existing coherent 100 gig / 200 gig / SuperChannel technologies have great potential to continue to effectively extract the maximum possible ultimate capacity and lowest cost per bit from the submerged plant of any submarine cable, existing or new.”

The technology is still progressing, though.

According to Grubb, Infinera plans to have 1.2 terabytes available.

“It’s defiantly an exciting time in the market,” he said.

Stephen Nielsen is staff journalist for Submarine Telecoms Forum. He is a graduate of the Virginia Commonweath University School of Mass Communications and was recognized as a finalist for the Society of Professional Journalism’s Mark of Excellence Award.

Paradigm Shifts

In Submarine Cable Upgrades

Dr. Stephen Grubb

The change in transport technologies for upgrading submarine cable systems has changed dramatically over the past 2-3 years, arguably in a more rapid and universal fashion than any other time in the history of submarine fiber cables. Prior to 3 years ago, the submarine carriers were largely agnostic to bit rate and transponder technology format, they were simply seeking an answer as to what gave them the highest capacity on their particular submarine cable and the lowest cost per bit of transport. The answers would vary depending on the carrier and the particular properties of the fiber wet plant. However since 2009 or so, we have witnessed an extremely rapid change from 10 Gb/s SLTE transponders (several different modulation formats) to 40 Gb/s (both coherent and non-coherent) to 100 Gb/s coherent SLTE transponders. Coherent 100 Gb/s technology adoption has been near universally accepted as the de-facto choice for all submarine system SLTE upgrades, both for existing

dispersion managed cables as well as new fiber builds, which are based purely on positive dispersion large area fiber, which accumulate such large values of dispersion that they are locked into coherent technology for SLTE transponders.

Why has there been such a rapid and universal acceptance of 100 Gb/s coherent transponders as the technology of choice for SLTE? Clearly the answer must be favorable with regards to the two most important factors

in SLTE upgrades: the chosen technology is required to lead to the highest capacity possible on a particular cable system as well as the lowest cost per bit of transport. 100 Gb/s coherent transponders can be selected to operate in a variety of modulation formats, and it has been consistently demonstrated that 100 Gb/s waves will lead to a higher total cable capacity than other bit rate and technology choices. 100 Gb/s transponders have also been shown to lead to the lowest

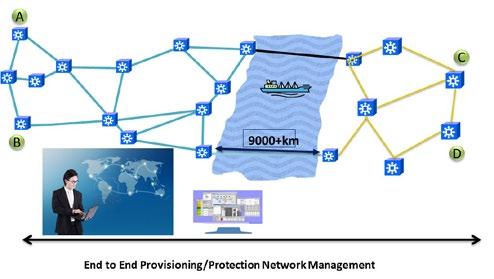

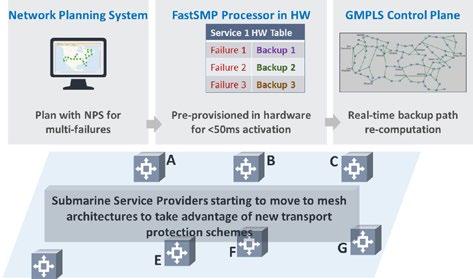

1: Integration of Submarine and Terrestrial networks into Global Networks enable carriers to provision and protect in increasingly faster time periods.

cost per bit for SLTE upgrades. One major reason for this significant economic benefit has been that, for the first time the submarine cable industry has been able to successfully leverage technology and transponders developed for terrestrial fiber applications. This allows the submarine market to leverage the large volumes and economies of scale of the terrestrial market, which is well over an order of magnitude larger than the SLTE upgrade market. Coherent technology was

Figure

Figure 2:

Fast mesh restoration for submarine networks via recently emerging standards such as fast SMP is now becoming a reality.

originally developed for the terrestrial market and flowed into the SLTE upgrade market primarily through equipment providers that are focused on the terrestrial long haul fiber market. This also leads to another phenomenon discussed below, that submarine and terrestrial networks are being merged into full global links that leverage common technologies, interface types and global protocol standards such as OTN.

100 Gb/s coherent technology also has other significant advantages over prior technologies. The mitigation of impairments, primarily chromatic dispersion (CD), polarization mode dispersion (PMD) and more recently, nonlinear impairments, are able to be compensated in the electronic domain.

Coherent technology effectively marries the power of electronics, the digital signal processors (DSPs) used in coherent transponders, with the power of photonics.

Coherent technology also naturally allows the use of flexible and dense channel grid spacing (Nyquist channel spacing) due to the fact it does not require traditional optical multiplexing and demultiplexing technologies required in previous technologies. This leads to higher spectral efficiency and hence higher capacities than with traditional channel plans. Flexible, non-standard channel plans are also being supported by the availability of new Flex WSS components,

which again have been developed for the terrestrial long haul market.

How do Carriers Differentiate Themselves in the Submarine Market ?

Now that submarine carriers have decided to use very similar 100 Gb/s coherent transponders in their SLTE upgrades, the natural question arises as to how these carriers can differentiate themselves in this highly competitive marketplace. There are several possible avenues that many of these carriers are pursuing to various degrees.

The first differentiating trend is the integration of submarine and terrestrial networks, as shown in Figure 1. The use of common technology base 100 Gb/s transponders between terrestrial and submarine networks facilitates this, but also the superior reach of 100 Gb/s transponders with SDFEC also allow the possibility of extending the network beyond the traditional cable landing stations (CLS) and enables POP to POP connectivity. This allows the

carriers to add and provision additional bandwidth much more rapidly on the combined global network, leading to revenue acceleration as well as the possibility of winning new business via the ability to turn up new services and bandwidth faster than their competitors. Submarineterrestrial integration also allows the elimination of a significant number of transponders and interfaces, thereby lowering the total network cost.

The ability to provision new bandwidth rapidly is becoming an important

differentiator with several submarine carriers. One method by which this can be achieved is by the ability to order and receive new client interface modules and install them only at POP locations.

In addition, if additional capacity is pre-planned and available in the system the additional bandwidth can be turned up entirely via software in principle in a matter of minutes. Indeed, these new possibilities have revolutionized the speed at which carriers can turn on and deliver new capacity and services. The reduced delivery and deployment

times associated with volume production also provides an advantage to submarine carriers who often have to respond to new capacity demands much more rapidly than has occurred in the past.

An additional differentiator is the ability of automated and shared mesh protection, one option is depicted in Figure 2. Submarine networks have shown their vulnerabilities over the past several years: the Taiwan earthquake of 2006, the 2011 Japanese Tsunami, numerous critical cable cuts, as well as a suspected terrorist attempt

on a submarine cable. Some carriers have augmented their submarine networks into new networks with an increased degree of mesh connectivity. Automated protection using protocols such as GMPLS are now possible, leading to restoration at much faster timescales that were previously possible. Even faster restoration schemes are possible such as the newly emerging standard of fastSMP, which allow restoration within a 50 msec timescale. Fast restoration within 50 msec in submarine networks is possible with some currently available 100 Gb/s transponders.

Elastic Bandwidth or Instant Bandwidth is an option for carriers to rapidly react to new and changing traffic volumes and flows.

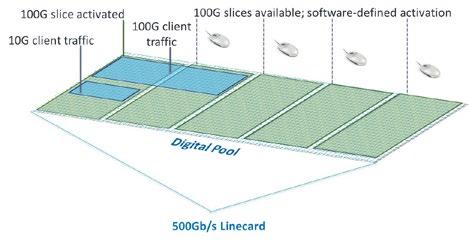

Some carriers are also currently deploying SLTE linecards that have a capacity several times the 100 Gb/s line rate, as high as 500 Gb. This gives the advantage of a larger “pool of bandwidth” within a single linecard, which can be more efficiently addressed with a variety of different client interface rates as well as allowing more flexible and efficient switching of this bandwidth. Also some

Figure 3:

of the additional bandwidth on this high capacity card can remain latent and ready to be rapidly activated via software. This can be enabled by the new concept of elastic or instant bandwidth. It is possible for the carrier to activate this additional capacity via software and pay for this additional bandwidth only as needed and after activation. This concept is shown in Figure 3. Activation of additional bandwidth can also be done on a limited time basis; examples include addressing peak capacity demands of their customers or to provide emergency capacity in response to a cable cut or fault in the network. This concept of elastic or instant bandwidth can give some carriers a highly differentiated position with respect to their competitors, as well as enable a new financial model impacting how they sell and add new bandwidth to address their customers changing requirements.

What’s Next ? Beyond 100 Gb/s

Now that we have experienced perhaps the most rapid technology disruption in the history of submarine cable upgrades, it begs the question: What is next, what is beyond 100 Gb/s? In peering into the future, it is good to consider a quote from Bill Gates: “We always overestimate the change that will occur in the next two years and underestimate the change that will occur in the next ten.“ Very few if any of the experts in this field could have predicted 5 years before first 100 Gb/s coherent installations the absolute disruption and dominance of this technology that we are experiencing today in submarine networks.

The rapid adoption cycle of 100G technology has caused such a sea change in submarine cable upgrades that there will most likely be an assimilation period and the technology shift may temporarily move away from hardware into areas that emphasize carrier network differentiation, as discussed in the previous section. Of course, there will always continue to be performance and cost driven improvements in submarine transponder technology and a drive towards achieving the maximum capacity on each submarine link. But the focus may temporarily shift towards software and features that allow carriers to provision, protect and use bandwidth in a nimble fashion

that separates them from their competitors in this highly competitive marketplace. Software defined networking (SDN) and Network Functions Virtualization (NFV) technologies will begin to take on an important role in submarine networks.

Based on the history of DWDM, one would expect the next step beyond 100Gb/s per wavelength to be an increase in data rate to 200Gb/s, 400Gb/s, or even 1 Tb/s. However, the industry is now dependent on coherent processing, which is driven by the performance of high speed ASICs, Analog to Digital Converters, and Digital to Analog Converters. Performance increases in serial electronic processing

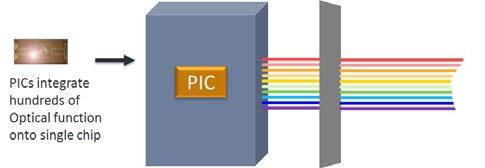

Figure 4: Photonic Integrated Circuits (PICs) enable high capacity superchannels by increasing the density/ capacity per single linecard.

rates have tended to plateau, and this has produced an alternative strategy for increasing units of line card capacity – the coherent superchannel. A super-channel is an evolution in DWDM in which multiple coherent optical carriers are implemented on a single line card, so that this capacity can be installed in a single operational cycle. Super-channels are already widely deployed in terrestrial networks, and we are continuing to see a similar trend of terrestrial technology migrating into submarine networks in order to benefit from the cost/volume drivers. Super-channels have the advantage of increasing the line capacity, enabling new higher speed services, and continuing to decrease the cost per bit of transport. To be effectively implemented, it is critical that the entire capacity of the super-channel should be contained within a single line card. A key technology that enables this is that of Photonic Integrated Circuits (PICs), as is shown in Figure 4. Similar to coherent technology, PIC technology

was originally developed for long haul terrestrial markets, but can be leveraged into adjacent markets including submarine, where they can benefit from the volume and cost drivers as well as the proven field reliability of PIC technology.

The next 3-5 years of submarine networks will continue to be as exciting as the previous time period. Coherent technology at 100 Gb/s now dominates all SLTE transponders, both for existing fiber upgrades as well as for new positive dispersion fiber plants. Submarine carriers will now strive to differentiate themselves in this competitive marketplace in the areas of provisioning, protection, and flexibility of adding new capacity and services purely via software. As is already beginning to happen in advanced terrestrial networks, coherent super-channels at 400 Gb/s and 1 Tb/s will undoubtedly play a role in next generation submarine networks. The simultaneous drivers of maximum capacity, flexible

optical networking and continually decreasing cost per bit will continue to drive submarine networks to adopt, modify and drive the best technologies of terrestrial transport technology into submarine.

Dr. Grubb is currently a Fellow at Infinera, responsible for next generation technologies and product directions in submarine networks. He has previously held positions at Corvis, SDL, and AT&T/Lucent Bell Laboratories. He led R&D that was responsible for the first commercial deployment of Raman amplification in a network, and developed several novel high power fiber lasers and amplifiers. He received his Ph.D. in Chemical Physics from Cornell University. He has held the position of IEEE Distinguished Lecturer. Dr. Grubb is an author on over 90 publications and conference presentations and is an inventor on over 70 issued U.S. patents.

18–21 January 2015 | Honolulu, Hawaii

Hilton Hawaiian Village ® Waikiki Beach Resort

Submarine Cable Workshop: Long Live Submarine Cables!

Moderated by Paul McCann, Managing Director, McCann Consulting International, Australia & Elaine Stafford, VP, The David Ross Group (DRG), USA

Executive Insight Roundtable 3: Putting the Bounce into Submarine Cable

Moderated by Michael Constable, CEO, Huawei Marine Networks, Peoples Republic of China

Topical Session 7: Submarine Cable - Developments in the Critical Peripheral Facets

Moderated by John Hibbard, CEO, Hibbard Consulting Pty Ltd, Australia

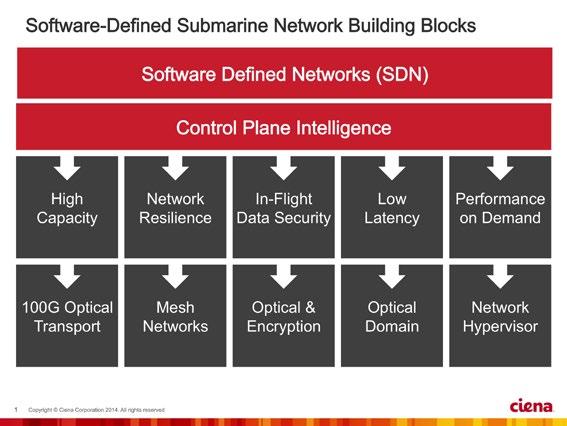

What SDN Can Bring to Submarine Networks

Colin Anderson

Five years ago, many of us had no real idea what “the cloud” was. Even though we already used Gmail and other types of web-based services, we probably didn’t recognize these services as “cloud applications,” and we almost certainly couldn’t have imagined that the cloud would impact our daily lives and our businesses as it does now. Today, we live in a cloud-centric and content-driven world, and the cloud is in our reach no matter where we are: at work, at home, and on the move.

The cloud will continue to transform industries and enable innovative processes, solutions, and ways of doing business. It has already proven to have a significant effect on the telecommunications industry, and is now presenting even more opportunities for industry change.

According to the 2014 UN Broadband Commission’s State of Broadband report, more than 40 percent of the world’s population are already online, and the number of Internet users will rise from 2.3 billion in 2013 to 2.9 billion by the end of 2014. Within three years, more than half of the world’s population will have Internet access. In

addition, the popularity of broadband-enabled social media applications continues to soar. 1.9 billion people are now active on social networks, and according to the 2014 report mobile broadband was designated as the fastest growing technology in human history. The report

estimates that more than 2.3 billion people worldwide will access mobile broadband by the end of 2014, and by 2019 global mobile broadband subscriptions could climb to approximately 7.6 billion—with 5.6 billion of these on smartphones.

This rapid growth of Internet users and the corresponding proliferation of broadbandconnected devices—many of them utilizing the cloud and accessing cloud-based, contentdriven applications—imply enormous demands on network capacity. These applications also

change bandwidth consumption patterns, requiring service providers to upgrade their connectivity services to enable increased speed, flexibility, and integration of the network with compute and storage in the cloud ecosystem. This applies to international networks as well as national networks —perhaps

even more so to international networks, where bandwidth prices are higher.

Service providers, including submarine network operators, play an important role in enabling the success of the cloud, as fulfilling its potential will require the right underlying

infrastructure to be in place, capable of evolving as cloud services evolve. In the cloud world, demands on capacity and connectivity are fluid, entirely dependent on users’ specific requirements, habits, and whims at a given time. Consequently, the underlying communications network infrastructure must be

able to grow with increasing demand, scale down when the resources are needed, and adapt to the different applications and varying traffic patterns required by the cloud.

Implications for Global Network Owners & Operators

Regardless of the sector, most businesses are now “informationpowered.” Innovative businesses leverage the power of modern information technology to grow their revenue, control costs, and innovate faster than their competitors. Informationpowered businesses leverage both expansive and real-time data; they analyze it with automated, powerful computebased processes; and they leverage the results directly and dynamically to both masscustomize and mass-optimize their offers, as well as support customer “self-service” delivery and respond more quickly to product innovation signals and opportunities.

Telecom network operators also understand the power of becoming truly informationpowered, but an “agility gap” is getting in the way and impacting their ability to quickly address the new challenges presented by the unpredictable nature

of the cloud. The hardware and software of past networks have not been flexible or programmable enough to enable on-demand networking. To date, network capacity has not been open, like other technology resources such as computing and storage. In the past, these resources were also “closed,” but their providers managed to develop new business models enabling them to offer on-demand experiences which meet users’ needs while providing revenue and margin growth for those providers.

In a fixed-capacity telecom industry, demand for capacity is high—yet capacity itself has become commoditized. Consequently, declining prices follow positive growth.

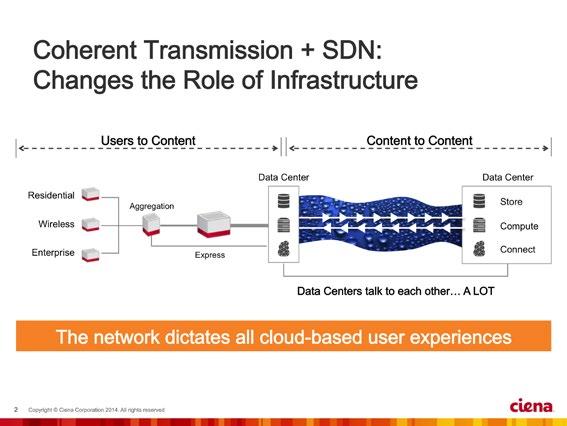

Some fundamental issues for submarine network operators remain. Chief among them is the need for networks to interconnect the points where the traffic originates and terminates. Subsea networks increasingly need to connect PoP to PoP, or data center to data center, rather than beach to beach, and need to be integrated with their terrestrial counterparts. Another important issue is the need to increase ultimate capacity to maximize the useful lifetime of

existing submerged plant assets while minimizing the overall cost-per-bit of traffic.

The industry has made great progress in these two areas in the past five years, with rapid advances in Submarine Line Terminating Equipment (SLTE) technologies, including coherent detection, softdecision FEC, 100Gb/s line rate, advanced modulation schemes, and flexible grid wavelength allocation. In fact, the advances in SLTE technology have enabled the submarine network industry to move from 10 Gb/s WDM to 100Gb/s WDM technology— with many consequent advantages—in approximately one third of the time that it took the same network industry to move from 2.5 Gb/s to 10 Gb/s.

In addition to strong growth in capacity demand and use, we’ve also seen steep price declines and increased commoditization of capacity. Service providers have at times struggled to differentiate themselves from their competitors.

Rethinking Network

Infrastructure as a Programmable Platform

For telecom service providers, including submarine network operators, the lack of agility prevents them from offering new services on-demand.

To combat the commoditization of capacity while at the same time satisfying user demands, providers must create virtualized, performance ondemand networks. This can be achieved if we have networks that are dynamic and open, compared to the fixed and closed networks of today. Such open and dynamic networks can be achieved with software defined networking (SDN).

Fortunately, the same hardware and software technologies which enable the applicationcentric world we live in —the smart phones, tablets, and advanced software applications of today—also enable us to re-think the way we design networks, whether terrestrial or submarine.

the scalability of networks through 100Gb/s coherent and converged packet-optical technologies. Second, networks are becoming more dynamic and programmable, equipped with flexible multi-purpose hardware to enable software defined networking (SDN). Third and finally, vendors and service providers alike are developing network-level software applications to support the network being a truly open resource.

Many of today’s existing telecom networks are rigid and siloed.

So what is being done to make submarine and terrestrial networks more open and programmable, to achieve performance on-demand for a better user experience? There are three main things being done to drive this change. First, service providers are increasing

The combination of these hardware and software technologies, together with the appropriate design philosophies and architectures, allows service providers to truly leverage open software control. That means that they can transform what was previously only “capacity” into “capability” and “revenue” through innovations in service creation and delivery as well as the optimisation of operations. But such performance ondemand requires massive scale, and requires a real convergence of optical and packet technologies.

Changing Network Behavior with SDN

Capacity on submarine networks still remains relatively scarce and

therefore a valuable resource compared to terrestrial capacity. Customers—enterprises, content providers, and others— who cannot afford a permanent high-capacity fixed international circuit are likely to seek either lower-capacity fixed circuits or use Over-the-Top (OTT) services to access the Internet. Although such international OTT services may seem attractive due to them being “free” at first, they often end up costing more as a result, leading to poor performance, high latency, and eventually dissatisfied end-customers.

If a medium-sized content provider needs to replicate or back up data between two data centers on different continents, using the Internet via an OTT service might be an acceptable solution some of the time. However, international OTT services are subject to variable capacity, latency, and reliability, creating more vulnerability for data backup failure than if the content provider were to use a reliable high-capacity, ondemand circuit for a limited time.

increased demand for scheduled transmission of high-definition, uncompressed video between stadia and video production houses or other facilities— sometimes on different continents. To enable maximum, cost-effective application performance, network bandwidth consumption has to match the consumption models for compute and storage, so connectivity services must be set up fast, with elastic bandwidth, between changing sites.

The ability to provide ondemand capacity services allows the service provider to access new and previously untapped customer bases. In addition, where there is a requirement for scheduled high-capacity transmission links for limited time periods, customers are often willing to pay a premium price.

of bandwidth resources between end-users and data centers, as well as interconnecting data centers.

On-Demand Services are the Right Answer, Even for International Services

be started by an upgrade of the SLTE alone.

On-demand services can benefit both the end-user and the service provider. For example, live sports, media, and entertainment events all create an

On-demand services are connections set up with a flexible number of end-points and flexible bandwidth, start time, and duration, through a self-service portal. The network solution for enablement of on-demand services is built on a packet-optical network augmented with control and programmability. On-demand services enable more efficient use

In the international submarine network environment as well as the domestic telecommunications sector, SDN solutions allow providers to deploy on-demand services that set up connections over any number of end-points with flexible bandwidth, start time, and duration through a self-service portal, or are controlled directly by data center applications. End-users can set up connections through the portal and keep track of the health of the connectivity service. Service providers can obtain revenue from excess equipped capacity on their networks, which would otherwise remain idle, increasing their overall revenue and profitability.

The combination of packetoptical technologies and solutions coupled with agile, software- programmable hardware and open ecosystems can enable agile on-demand cloud-based services from these networks, something that can

These new services allow service providers to offer differentiated services to meet their individual customers’ needs, rather than providing raw capacity, which is increasingly becoming a commodity product. There is no doubt that SDN will continue to reshape the networking industry—undersea, on land, and in the cloud.

Colin Anderson is marketing director for global submarine systems at Ciena. Colin has 25 years’ experience in sales & marketing, engineering, and business development roles in the subsea and terrestrial telecommunications markets.

Submarine Cables of the World

Recovering and Relaying Cables For Building New Subsea Systems

Why Cable Relay?

With the prevalence of submarine cable systems in international communications, two trends can be observed in the development of international subsea longhaul transmission infrastructure. The first one is the increase in capacity for existing busy routes, which can be achieved by either building new subsea cable systems or upgrading existing ones. The second trend is the building of new subsea routes in order to bring physical diversity to existing ones for increased resiliency, or to offer optical connectivity to small islands that do not have access to high-speed telecoms services.

In essence, the new subsea systems aiming to provide small communities with connectivity to the rest of the world do not require huge capacity but must offer a low price point to make the business case viable (keeping in mind the intrinsic small number of customers).

Two options are available: (i) building a new subsea cable system, using components carefully selected to minimize the cost, or (ii) recovering and redeploying a subsea system that has been decommissioned, most

often because of the unfavorable ratio between capacity and operational expenses on highly competitive submarine routes.

In Xtera’s experience, which includes the implementation of multiple cable redeployment projects, building regional lowcapacity systems on new routes represents the application where a cable relay makes the most sense. On cable system operators’ side, cable relay is a concept that is more and more accepted [1].

Lifetime of Recovered Cables

Both submarine cables and repeaters are designed, specified and manufactured to offer a

nominal life span of 25 years. Practically speaking, this lifetime can be much longer due to system overdesign to ensure the lifetime requirements are met and to the fact that materials used in cables have a significantly longer life than what was originally thought [2].

In a recently worked example, Xtera looked at an opportunity where the decommissioned cable had been in use for just under 10 years. Taking the pessimistic n value of 3 [See papers by Davies et al., Southampton University] and given the reliability being proportional to kV to power n, we showed that if the cable was originally operating at 7kV and,

subsequent to that, at 3kV in a shorter system, then the cable had in excess of 600 years left at these voltages.

For the wet plant, including repeaters, the major factor is that there are several elements which allow the status and expected lifetime to be assessed. These elements are: very few active optical elements in a repeater (in fact, only the semiconductor lasers), a well-documented fault history and, in general, access to the repeaters to indicate how well these were performing prior to decommissioning.

Taking the same system and knowing that the wear-out mechanism for lasers follows a

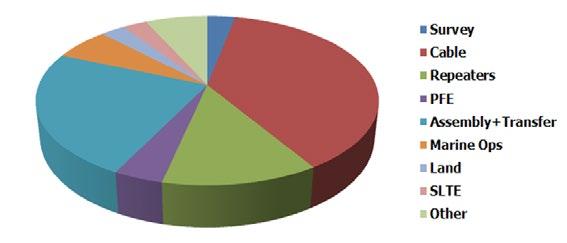

Figure 1: Typical cost structure of a new regional cable system.

lognormal distribution, the total laser (and associated electronics) failure rate increases from 85 FITs at 25 years to 128 FITs in a further 25 years. Xtera was able to show that this corresponded to 0.65 ship repairs over the next 25 years. As this rounds up to 1 then this is no different to a new build equivalent for the same link.

A further level of comfort can be gained from the understanding that, in general, most ageing occurs in the early life of a system. This means that, several years after commissioning, the subsea cable operators have a pretty good idea of the “physical shape” of their wet asset: either multiple, regular failures happened and a pattern can be deducted to predict degradation in the midterm, or no degradation happened after 1 or 2 years of commercial service and there is a high level of confidence that the subsea cable was properly designed, manufactured and installed, and that it will retain good characteristics and performances for the future.

Of course, there is an alternative scenario when there is some doubt. The solution is to reuse the cable and replace the

repeaters, and this too has been shown to be cost effective and offer a capacity boost.

Benefits from Cable Redeployment

Lower Project Cost

The typical cost structure of a new regional submarine cable system is depicted in Figure 1. The largest portions are cable, repeaters, transfer to the deployment location, and marine operations. These portions also represent the biggest opportunities for cost savings.

On the one hand, cost is saved on the cable (and repeaters if they are recovered and re-used as well). On the other hand, some extra marine operations are required for this wet plant recovery. The cost of extra marine operations is primarily driven by level of difficulty required to recover the cable from the sea bed, and is dependent on the original installation (surface laid or buried). But in the end, and when the transportation costs of new cable from the few cable factories dotted around the world are factored in, the cable relay approach can lead to significantly lower system prices compared to new builds

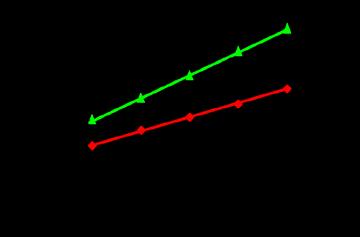

as represented in Figure 2.

The price comparison in Figure 2 assumes a two fiber pair system, a short distance between recovery and redeployment locations, a system in deep water with little burial, and some new cable purchased for the shore ends.

Shorter Lead Time

Another key benefit of the cable relay approach is the shorter lead time for project execution compared to new builds based on new cable. While manufacturing a long optical submarine cable can take several months (a typical figure is 9 to 12 months), recovering an

Figure 2: Comparison of system price as a function of system length between new build and redeployment approaches.

existing cable requires much less time (in general, Xtera targets the recovered cable to be in the region of the redeployed cable so general lag time is 3-4 months prior to redeployment).

Greener Approach

Manufacturing a new cable requires energy and multiple materials, some of them being scarce or costly to produce. On the other hand, recovering an existing cable requires minimal energy (namely cable ship fuel). A global comparative study about the potential environmental

impacts of submarine cable systems has shown, however, that the recovery and relay of an existing submarine cable correspond to about 5% of the environmental impact caused by the manufacturing and deployment of a new cable [3].

Cable Considerations

In order to make a redeployment project viable from both the economic and technical perspectives, there is more to consider than simply the physical status of the cable that is candidate for recovery and redeployment.

Where Is the Cable Coming From?

Cable redeployment is an appropriate approach if the cable is recovered from a less or similarly benign seabed than the destination seabed. Because recovery of extensively well buried armored cable can be a slow and risky process, the redeployment solution works best for a destination that needs a minimal amount of armored cable and a maximal quantity of deep water cable. When the existing cable is simply surface laid, cable recovery is fast and is very unlikely to degrade the cable characteristics.

Additional Technical Challenges

Optical Line Design

To optimize the optical line design, circulating loop and straight-line setups with the ability to use different types of line fibers and repeaters represent powerful test beds. These, coupled with accurate optical transmission modeling tools, enable the replication of the new subsea system and the maximization its performance.

Cable Recovery Process

The cable recovery process has to be well controlled in order to avoid applying mechanical tensions on the cable and repeaters which exceed the upper specified limits. Here, the challenge is to maximize the cable recovery yield, i.e. the amount of the existing wet plant that can be effectively re-used.

Landings

Where possible, existing landing should be re-used in order to avoid cost of permits, lead time to obtain them, and all the installation activities needed for the landing itself. Armored cable is required for shore ends and shallow water. In general, this will be a new build.

Figure 3: Three redeployment projects based on decommissioned Gemini cable.

Line Monitoring

If repeaters are re-used in the redeployed cable, they must be monitored in the new system. The line monitoring equipment is therefore required to generate and detect the test signals appropriate to the system and locate the fault to within one repeater section.

Project Management

Management of a redeployment project is quite different from a new cable project as many more boundary conditions need to be taken into account. As one does not start from scratch, with brand new, clearly specified wet components, cable redeployment project are typically more challenging projects to execute.

Redeployment Examples

Starting in as early as 2007, Xtera has been developing its expertise and has gained an unrivalled experience in cable relay projects. Below are three examples of cable relay projects based on the recovery of the Gemini cable. The Gemini system was a twoleg transatlantic cable system that was phased out only 6 years after its commissioning in 1998 due to its obsolete terminal

transmission technology. Pieces of the decommissioned Gemini cable were recovered and redeployed for the three relay projects depicted in Figure 4.

Conclusion

There are many compelling reasons to use recovered cables around the world. Compared with new builds, using a cable relay offers the following benefits:

• It can be significantly quicker to get the system up and running with funding in place;

• In some cases, we can see savings close to 50% when compared with new build;

• There are massive environmental savings upwards of 95%.

Recovering a phased out cable system with the objective of building a new system in another location is a challenging endeavor requiring additional skills with respect to standard new builds based on brand new wet plants from the factory. Also, the commercial benefit the purchasers can expect from the relay approach is strongly driven by multiple factors,

including original marine installation of the cable to be recovered, relative locations of existing and new systems, and project requirements. As such, relay project assessment shall be carried out on a per project basis, and requires a high level of expertise in order to correctly identity, quantify and optimize all the factors impacting the project cost and performance.

References

[1] “The Re-Deployment Route to Cost Effective Cable Systems”, Maja Summers and John Kincey (Cable & Wireless), SubOptic 2007 – We6.01.

[1] “Recovery and Reuse Of Underwater Optical Fibre Cables”, Dr. Frank Donaghy, Submarine Telecoms Forum, Issue 77, July 2014.

[2] “Twenty thousand leagues under the sea: A life cycle assessment of fibre optic submarine cable systems”, Craig Donovan – KTH, Stockholm, Sweden, October 2009.

Bertrand Clesca is Head of Global Marketing for Xtera and is based in Paris, France. Bertrand has over twenty five years of experience in the optical telecommunications industry, having held a number of research, engineering, marketing and sales positions in both small and large organizations.

Bertrand Clesca holds an MSC in Physics and Optical Engineering from Ecole Superieure d’Optique, Orsay (France), an MSC in Telecommunications from Ecole Nationale Superieure des Telecommunications, Paris (France), and an MBA from Sciences Politiques, Paris (France).

Magneto-hydrodynamic Corrosion of Submarine Telecommunication Cables

Liam P. Talbot

When a conductor and magnetic field move relative to each other a potential difference is induced across the conductor. This phenomenon also holds when expanded on a global scale; where perturbations in the Earth’s magnetic field induce currents on the Earth's surface.

Known as Geomagnetically Induced Currents they can flow in any conducting structure; and since saltwater is an electrical conductor GIC can act as a voltage source across the Earth’s oceans - making submarine cables particularly susceptible.

GIC in stationary conductors are limited to variations in the Earth’s magnetic field, which are infrequent and detectable. However, in areas of fast flowing saltwater, the conductor’s movement relative to the Earth’s magnetic field induces large currents.

susceptible.

GIC in stationary conductors are limited to variations in the Earth’s magnetic field, which are infrequent and detectable. However, in areas of fast flowing saltwater, the conductor’s movement relative to the Earth’s magnetic field induces large currents.

If a situation arose where the flow of seawater was transverse to the submarine cable thendue to Fleming’s left hand rulea current would be induced along the longitudinal axis of the cable.

Galvanised steel armour offers some protection; however, if this coating is damaged and the steel is exposed, it will present a path of least resistance to the GIC. An electric current flowing along the exposed cable will gradually corrode the steel due to electrolysis, weaken the armour and eventually lead to cable failure.

Galvanised steel armour offers some protection; however, if this coating is damaged and the steel is exposed, it will present a path of least resistance to the GIC. An electric current flowing along the exposed cable will gradually corrode the steel due to electrolysis, weaken the armour and eventually lead to cable failure.

Several cable breaks have been attributed to magnetohydrodynamic corrosion and each displays a characteristic conical corrosion of the armour wire. The steel corrodes to a sharp point; tapering over approximately 150mm.

moving water is flowing perpendicular to the cable, where GIC of tens to hundr eds of amperes can be generated across a volume of ocean.

The steel armour of submarine cables is protected by a corrosion resistant coating. However, if this is damaged and the steel is exposed to the conductive seawater, corrosion can occur due to electrolysis.

Electromagnetic Induction

If a situation arose where the flow of seawater was transverse to the submarine cable thendue to Fleming’s left hand rulea current would be induced

I suspect that the dimensions of this tapering relates to the electric current, and thus water speed. If this is the case, then this relationship can be used for forensic and predictive calculations.

Geomagnetically Induced Current

Several cable breaks have been attributed to magnetohydrodynamic corrosion and each displays a characteristic conical corrosion of the armour wire. The steel corrodes to a sharp point; tapering over approximately 150mm.

Geomagnetically Induced

Currents affect everything from transmission grids to oil platforms. However, it is submarine cables that are most at risk as the induced current is not dependent on variations in the Earth’s magnetic fi eld: since the cables are immersed in an

Electromagnetic induction can be explained using the Lorentz Force and the conservation of energy: the direction of induced current opposes the change in magnetic flux which induces the current. If a charge , moves with velocity , in a magnetic field of strength , making an angle , then the magnetic Lorentz force is, If and are perpendicular, , , and,

The direction of this force is perpendicular to both and and is given by Fleming’s Left Hand Rule.

Suppose a submarine cable lies perpendicular to both the Earth's magnetic field and the flow of the ocean. We know that the conducting steel rods contain free electrons, which are able to move within the metal. An electrons charge is defined as,

The direction of this force is perpendicular to both and and is given by Fleming’s Left Hand Rule.

Therefore, each electron is subjected to a Magnetic Lorentz force,

The direction of this forcefound using Fleming ’s left hand rule- will be along the steel rods and causes the electrons to collect at one end. The resulting polarity means a potential difference is produced between the ends of the steel conductor, known as the induced . This produces an electric field within the steel rod, the

Therefore the potential difference produced is, strength of which can be calculated,

If the cable is not perpendicular to the magnetic field, but makes an angle with it, then the component of the magnetic field perpendicular to the cable will be,

The induced across the ends of the steel rod will now be,

current passes through seawater; Hydrogen appears at the negatively charged Cathode and Oxygen appears at the positively charged Anode. The electrolyte present in seawaterprimarily Sodium Chloridewill disassociate into Cations and Anions; the Anions are attracted to the Anode where they neutralise the build-up of positively charged particles; similarly, the Cations are attracted to the Cathode where they neutralise the negatively charged particles. This allows for the continued flow of electricity.

Suppose a submarine cable lies perpendicular to both the Earth's magnetic field and the flow of the ocean. We know that the conducting steel rods contain free electrons, which are able to move within the metal. An electrons charge is defined as, Therefore, each electron is subjected to a Magnetic Lorentz force,

The direction of this forcefound using Fleming ’s left hand rule- will be along the steel rods and causes the electrons to collect at one end. The resulting polarity means a potential difference is produced between the ends of the steel conductor, known as the induced . This produces an electric field within the steel rod, the

The force on an electron due to this electric field is, which opposes the direction of the electric field.

The produced opposes the motion of electrons caused by the Lorentz Force: in accordance with Lenz ’ s law. As the number of electrons at one end increases, the magnitude of the electric force increases until it equals and opposes the magnetic force . The potential difference produced across the steel rod is now constant,

Electrolysis of Seawater

Faraday’s First and Second Laws of Electrolysis

The direction of this forcefound using Fleming ’s left hand

If the cable armour's corrosion resistant coating is damaged, and the steel is exposed, it will present a path of least resistance to the GIC. An electric current flowing along the exposed cable will gradually corrode the steel due to electrolysis -the decomposition of seawater into its constituent parts. When current passes through seawater; Hydrogen appears at the negatively charged Cathode and Oxygen appears at the

Faraday's First Law of Electrolysis: The mass of a substance altered at an electrode during electrolysis is directly proportional to the coulombs of electricity transferred to that electrode.

Faraday's Second Law of Electrolysis: For a given quantity of electric charge the mass of material altered at an electrode is directly proportional to the elements equivalent weight

where, is the mass of the substance liberated at an electrode, is the total electric charge passed through the substance, is the Faraday Constant: 96485 , is the molar mass of the substance and is the valency of the substance's Ions (electrons transferred per Ion). is known as the equivalent weight.

For Faraday's First Law; , and are constant. The larger the value of , the larger the value of .i.e. more current, more loss.

For Faraday's Second Law; , and are constant. The larger the equivalent weight, the larger the value of .

In the simple case of constantcurrent electrolysis, leading to,

A Forensic Calculation:

Estimating water speed from corroded cone dimensions

If a failed cable displays the characteristic signs of magnetohydrodynamic cable corrosion .i.e. one or more steel rods has corroded into a cone. Then the volume of this shape can be calculated from its height and radius . The volume of a cone is defined,

Assuming a homogenous shape, the volume of this section of cable before it was damaged would have been,

Equation 2

Therefore the volume lost is, Equation 2 minus Equation 1

Equation 3

Where is the radius of the cone at height , Therefore,

The density of the steel is known to us. Multiplying Equation 3 by this will give us the lost mass,

Equation 4

Once we have the lost mass we can use Faraday ’s law of electrolysis to calculate the charge that damaged the cable,

and inserting our value for Equation 4 gives us,

Equation 5

Rearranging the definition of charge to find current,

Equation 6

And inserting Equation 6 into the definition of Voltage, Gives us,

Equation 7

where is electrical resistance, defined by,

And the volume of the cone is,

Equation 1

Assuming a homogenous shape, the volume of this

Rearranging to,

where is Resistivity, is rod length and is rod crosssectional area, which for a cylinder is, making the resistance,

making the resistance,

Equation 8

Assuming resistance is constant we can insert Equation 8 into the voltage Equation 7, resulting in,

Assuming the Earth's magnetic field is constant at a chosen point we can insert the voltage Equation 9, resulting in an equation for water speed,

had failed after approximately one year ’s service life, or,

The previous method can also be used to estimate the lifetime of a cable if it is subjected to magneto-hydrodynamic corrosion. However, the equation has to be altered to remove the height of the cone

Inserting the charge Equation 5 gives,

Equation 10

The cable was lying perpendicular to the ocean current, and on inspection the steel rods displayed the characteristic effects of magneto-hydrodynamic corrosion; the ends had corroded into a cone of height,

Worked Example

A submarine cable's steel armour has the following properties;

Equation 9

Using Fleming's Left Hand rule,

Using these figures along with Faraday's constant,

, as this can only be measured once the cable has already failed. What can be estimated is the time taken for a given percentage of mass to be lost.

Previously we used,

Which is now altered to describe the entire mass of the cable,

Equation 11

the average water speed can be calculated using Equation 10 as,

Where is the Earth's magnetic field, is the length of the rod and is the angle of the cable with the water current.

Rearranging,

Assuming the Earth's magnetic field is constant at a chosen

The valency of the steel armour can be anything between 2 or 3 but experience appears to suggest the latter. (

A cable retrieved from an area of,

A Predictive Calculation: Estimating lifetime of a cable subjected to magneto-hydrodynamic corrosion

The previous method can also be used to estimate the lifetime

Where the parameter now reflects the length of cable in question. If we now replace the in the water-speed solution Equation 10 so that it reflects the mass of the entire cable we are left with,

Equation 12 and rearranging to find ,

adding a percentage variable to the equation - for example 0.1 denoting 10%, 0.9 denoting 90%- allows us to calculate the time taken for a given percentage of mass to corrode,

adding a percentage variable to the equation - for example 0.1 denoting 10%, 0.9 denoting 90%- allows us to calculate the time taken for a given percentage of mass to corrode,

Equation 14

Equation 14

Worked Example

Worked Example

A submarine cable's steel armour has the following properties;

A submarine cable's steel armour has the following properties;

Using these figures along with Faraday's constant, the time taken for the entire cable to decay, can be calculated using Equation 14 as,

Conclusion

A stretch of cable is to be laid in an area of, and perpendicular to the water current of,

However, if the Magnetohydrodynamic effect is concentrated on 1cm (10%) of the cable then the time taken to decay reduces to or approximately 40 days.

The initial hypothesis was that Magneto-hydrodynamic corrosion resulted in signature conical decay of submarine cable armour. The dimensions of the conical decay, along with the time till failure, could then be used to calculate water speed. Further to this, given water speed and cable parameters the lifetime of the cable can be estimated should it be subjected to magnetohydrodynamic corrosion. The predictive calculations yield reasonable results but untested I would estimate that the equations hold significant errors, maybe as high as 20%. The accuracy of these predictive equations could be improved through analytical experiment, as at the moment this study is purely theoretical.

Liam is currently an Engineer Officer in the Royal Navy. After graduating from the University of Liverpool in 2010 with a Bachelor’s Degree in Physics and Mathematics he went to work as a Telecommunications Rigger on the 4G rollout in Canada. On returning to England he was employed at Cable & Wireless where he worked as a Capacity Planning Engineer on the UK fibre optic network, before moving to the Submarine Systems Engineering department. Here he audited network installations and researched problems affecting the physical performance of submarine cables.

Subsea Cables UK position statement on post cable lay trawl sweeps

UK position statement on post cable lay trawl sweeps

It is the position of Subsea Cables UK that submarine cables, buried or otherwise, can present a potential entanglement risk or hazard to fishermen Fishing over cables is a lso a potential hazard to cables and can cause damage to cables . W e would strongly advise against any type of fishing, whatsoever, where there is a known and charted cable.

It is the position of Subsea Cables UK that submarine cables, buried or otherwise, can present a potential entanglement risk or hazard to fishermen. Fishing over cables is also a potential hazard to cables and can cause damage to cables. We would strongly advise against any type of fishing, whatsoever, where there is a known and charted cable.

for the fisherman or other person actually carrying out such action. In both cases it would be a defence to show that the cable owner had given its informed consent prior to such action being taken.

Trawl Sweeps

Information on submarine cables around the UK and Northern Europe can be downloaded for all types of fishing plotters free of charge at www.KIS-ORCA.eu Subsea Cables UK strongly advise that all fishermen should ensure that up to date cable data is installed on their fishing plotters. W e also urge all regulators and marine authorities to advise the same.

It is against UK, EU and international law to wilfully damage a submarine cable (Submarine Telegraph Act 1885, UNCLOS). The execution of such action, such as that outlined below, resulting in damage to a subm arine cable carries the risk of vicarious liability for the person requesting, approving or supervising such action, and direct liability for the fisherman or other person actually carrying out such action. In both cases it would be a defence to show that the cable owner had given its informed consent pr ior to such action being taken.

Trawl Sweeps

gas sector, this operation does not transpose to the cables sector.

Whilst Subsea Cables UK acknowledges that there may be a need for such operations the oil and gas sector, this operation does not transpose to the cables sector.

Trawl debris clearance, or trawl sweeping as it is more commonly referred to, is a method of making an area of sea bed that could potentially be hazardous to fishermen safer. It is commonly used within the oil and gas industry when decommissioning oil fields and their associated infrastructure, or after the installation of large diameter pipelines.

cable ship progresses forward and the cable plough buries the cable as described above. Depth of burial is controlled by varying the position of the hydraulically controlled skids.

It is the position of Subsea Cables UK that post cable lay trawl sweeps are not required there has been no clearly stated reason why trawl sweeps should be carried out over Consequently, a greement to undertake such an operation would suggest that it is safe over a cable and Subsea Cables UK would never condone such an action.

Trawl debris clearance, or trawl sweeping as it is more commonly referred to, is a method of making an area of sea bed that could potentially be hazardous to f ishermen safer. It is commonly used within the oil and gas industry when decommissioning oil fields and their associated infrastructure, or after the installation of large diameter pipelines

Items of debris that are commonly dropped on the seabed in oil and gas field areas generally consists of scaffold poles or small sections of grating displaced during storms. Large deposits of clay may be present after pipeline removal or installation.

These are cleared by undertaking a bottom trawl with apparatus s uch as in the picture below.

Information on submarine cables around the UK and Northern Europe can be downloaded for all types of fishing plotters free of charge at www.KIS-ORCA.eu. Subsea Cables UK strongly advise that all fishermen should ensure that up to date cable data is installed on their fishing plotters. We also urge all regulators and marine authorities to advise the same.

It is against UK, EU and interna tional law to wilfully damage a submarine cable (Submarine Tele graph Act 1885, UNCLOS). The ex ecution of such action, such as that outlined below, resulting in damage to a submarine cable carries the risk of vicarious liability for the person requesting, approving or supervising such action, and direct liability

Items of debris that are commonly dropped on the seabed in oil and gas field areas generally consists of scaffold poles or small sections of grating displaced during storms. Large deposits of clay may be present after pipeline removal or instal-

These are cleared by undertaking a bottom trawl with apparatus such

Whilst Subsea Cables UK acknowledges that there may be a need for such operations within the oil and

It is the position of Subsea Cables UK that post cable lay trawl sweeps are not required and there has been no clearly stated reason why trawl sweeps should be carried out over a cable. Consequently, agreement to undertake such an operation would suggest that it is safe to fish over a cable and Subsea Cables UK would never condone such an action.

Information on Cable Burial

The overwhelming majority of submarine cable installation is undertaken using a submarine cable plough. Various types of plough for various ground conditions exist, but they operate on the same principle. Towed from a cable ship the plough cuts a wedge of soil through the seabed. The cable is then fed through the plough and the wedge of soil replaced as cover over the cable. The simultaneous lay and burial of the cable is then achieved as the

The controlled operation by which cable ploughs work, “displacing” the sediment into which the cable is lowered, followed by the natural backfilling of the trench, ensures that soil disturbance is kept to a minimum.

An alternative to plough burial is the use of an ROV to bury the cable through water injection liquefaction of the seabed directly under a cable in suitable sediment conditions. Where the conditions allow, this method allows the cable to sink under its own weight when water is injected into the seabed sediment. Subsequently hydraulic pressure and normal seabed process allow the sediment to consolidate again over the cable, achieving burial dependent on the sediment type.

Whilst Subsea Cables UK acknowledges that there may be a need for such operations within the oil and gas sector, this operation does not transpose to the cables sector.

Cables

Telecoms consulting of submarine cable systems for regional and trans-oceanic applications

Back Reflection

Technology Convergence Part 2

The Battle for Combined Telephony and Telegraphy Services Across the Atlantic

In last month’s issue we described how just after WWII the structure of the telecommunications market was radically different in the UK and the USA and that the planning for TAT-1 was the catalyst for the GPO to promote “Technology Convergence” in the form of combined telegraphy and telephony services over a single cable. The possibility that AT&T would be able to offer public telegraphy services over TAT-1 was seen by ITT as a threat to its dominant position in the international telegraph market. To counter this threat they began to promote project

by Stewart Ash & Bill Burns

“Deep Freeze” which would have been the first repeatered trans-Atlantic telegraph cable. Promotion of this project required lobbying at the highest levels of government in the UK and USA which culminated in informal meetings taking place in Washington DC during May 1956, where the stances adopted by the British and USA delegations were poles apart and the chances of finding common ground appeared unlikely. The story continues!

The final outcome of the May 1956 discussions was an agreement that the US side would look at ways and means for proposals by American companies to the UK Government to be first cleared with the relevant government agencies and, so as to preclude over-investment, to look at whether the companies could

operate competitively while using circuits in a telegraph cable owned by them as a consortium and the UK Government. For their part the British agreed to review the landing licenses situation, to consider whether they would buy into existing cable facilities and to reconsider Deep Freeze.

The British delegation was extremely disappointed with the discussions that took place during these meetings, and came away with a clearer view of the power politics in Washington. It reported that no US Government agency was prepared to accept responsibility for future policy, so that replies were based on the existing situation and negative to proposals for change. They concluded that: “The communication operating companies are extremely powerful