BY STEVE ADAMS BANKER & TRADESMAN STAFF

riple-decker construction may have a place in spurring housing production, but recent experiments in Boston and Somerville indicate only market-rate projects are financially feasible.

Somerville has seen an uptick in building permits for three-family dwellings in the past year after eliminating an

income-restricted requirement. The city now allows three-family construction in the vast majority of its residential areas.

“It allows a historical structure to be built and allows it to continue to exist,” said Ward 1 City Councilor Matt McLaughlin, who represents East Somerville. “This is something pretty small for Somerville, but if every city and town in the state did this, it would go a long way to addressing the housing crisis.”

In late 2023, Somerville updated zoning to allow three-family structures including triple-deckers to be built as-of right in its Neighborhood Residential 2 zoning district, which includes side

streets. It also removed a requirement that one of the three units in such projects be income-restricted.

Since then, the city has received 12 applications for new construction of detached or semi-detached three-family dwellings, according to data provided by the Somerville Inspectional Services Department. Another 11 applications were submitted for conversions from two- to three-family dwellings.

The elimination of the special permit requirement for three-family buildings has provided more certainty to developers to pursue projects, McLaughlin said.

Continued on Page 10

Timothy

ESTABLISHED

Associate Publisher: Cassidy Norton

Managing Editor: James Sanna

Associate

Finance

Contributing Writer: Scott Van Voorhis

Senior

Advertising

Graphic

Communications

Executive

Senior

Director

Data

Data

Data

Key

Parcel

Software

Senior

Systems

Controller: Janeen Silvestri

Assistant Controller: Olga Khalaydovsky

Accounts Recievable Specialist: Valarie Wickey

Human Resources Generalist: Nesima Bartlett

BANKER & TRADESMAN (ISSN 0005-5409) Volume 206, Number 03 Published each Monday.

The Warren Group LLC, 2 Corporation Way, Suite 250, Peabody, MA 01960. All rights reserved. No part of this publication may be reproduced without the written consent of the publisher. Banker & Tradesman and The Warren Group are trademarks of The Warren Group LLC.

Subscriptions to Banker &

28-STORY FURNISHED HOUSING TOWER APPROVED IN FENWAY

• The 400-unit, 299,000-square-foot building by Morro USA and Scape at Ipswich Street and Charlesgate West was originally proposed in 2021 under Boston’s compact living policy, which was suspended in 2023 after approving projects such as the 525 Linc complex which opened last year in Allston.

• The Charlesgate project required nine variances from the ZBA. The proposed 280-foot height exceeds the 135-foot maximum under zoning. The project also won’t include on-site parking, while 300 spaces are required. Incomerestricted compact studio units will rent for as little as $1,196 per month.

• The redevelopment plan at 4000 Mystic Valley Parkway in Medford was paused while state officials weighed and eventually rejected local officials’ argument that the city was exempt from Chapter 40B, the affordable housing zoning law.

• Mill Creek Residential’s project would replace a vacant 66,000-square-foot commercial building with a pair of 8-story residential buildings totaling 430,000 square feet, including 88 income-restricted units.

• Carvalho has been at the bank since 2022, holding roles as president, chief operating officer and treasurer. She will retain these titles after becoming the CEO. She joined the bank after stints as president, CEO and board chair at Cobblestone Management, president and CEO of Milford National Bank & Trust.

• She replaces Mark Haranas as CEO. Haranas was legal counsel to MutualOne beginning in 1989. He began his tenure with the bank as CEO in 2008 when it was then Framingham Co-operative Bank and guided it through a merger with Natick Federal Savings Bank in 2012.

part of the Fenway Triangle project.

• The transaction follows MEAG’s acquisition of apartment complexes in Texas, North Carolina and Washington, D.C. worth approximately $400 million in the past two years.

WU REFILES TAX SHIFT BILL, TAPPING INTO BUDGET SURPLUS

• Boston Mayor Michelle Wu has renewed her push to temporarily change the city’s property tax structure to cushion increases in residential values by raising tax rates for commercial properties for three years.

• The latest version adds the option of using surplus funds from the city’s budget as a fallback measure to reduce residential property taxes in case the mayor’s latest home rule petition fails on Beacon Hill, as her last one did in December.

HUMAN REMAINS FOUND AT MEDFORD SQUARE DEVELOPMENT

• Approximately 10 graves were discovered at a Medford Square property that the city is preparing to sell for a multifamily housing project.

• The property includes portions of the former Cross Street Cemetery, which lay in the path of Interstate 93. Remains interred there were relocated to Oak Grove Cemetery in 1958.

• But Medford Historical Commission members suspected that some remains from the Cross Street Cemetery might have been overlooked, and the city hired the archaeologist as part of its due diligence, Mayor Breanna Lungo-Koehn said.

Skanska Pulls Permit for 380 Stuart St.

BY SAM MINTON BANKER & TRADESMAN STAFF

Residential lenders will have to continue to navigate elevated interest rates in 2025 but competition for customers will not be as fierce, some of the state’s top mortgage professionals predict.

The average interest rate on a 30-year home loan rose past 7 percent las week according to mortgage-buyer Freddie Mac, as bond investors sweat concerns about Trump administration policies reigniting inflation.

And after interest rate cuts at the end of 2024, the Federal Reserve has projected only two reductions in its benchmark rate this year, a more cautious outlook than experts expected as recently as the fall of 2024.

reasons but as far as the interest rates just being probably one to 2 percent lower than they’d ever been in history,” Cross Country Mortgage loan officer Andrew Marquis said. “A big swath of people kind of got tricked into those lower rates and thinking these are the new rates and this is what it’s going to be. After that, when the rates shot up to 5, 6, 7 percent, it really halted the market for a year to two years.”

Rates close to 5 percent or 6 percent are the historical norm for well-qualified buyers, Marquis said, despite the low rates of the 2010s and the ultra-low rates of the pandemic years.

“Any time interest rates go down, it creates excitement, and it creates affordability.” – Shant Banosian, Guaranteed

But while top economists say it’s not looking likely that the average mortgage interest rate could drop below 6 percent anymore, many top mortgage professionals in Massachusetts say that may not matter as much anymore to homeowners who felt locked into low mortgage rates.

“Everything in the world is psychological and I think that people’s minds got really screwed up with COVID, for a million different

“I think there’s still people out there that will say, ‘Hey, I’m not doing this until rates go lower.’ Rates may never go lower,” he said. “But I think there’s still a bigger percentage of people that are realizing this is what interest rates are.”

Rate

Only around 75 percent American home mortgages had interest rates below 5 percent before a small refinance boom in the fall, according to real estate data firm ICE. That’s, down from 90 percent in 2022. Guaranteed Rate’s Shant Banosian acknowledged the psychological aspect of rate cuts but on the opposite side of the spectrum. He believes that no matter how high rates get, even the most minuscule of cuts can create a positive outlook on the market.

BY SAM DRYSDALE STATE HOUSE NEWS SERVICE

The Healey administration filed emergency regulations late Tuesday afternoon to implement the controversial law meant to spur greater housing production, after the state’s highest court struck down the last pass at drafting those rules.

The Supreme Judicial Court upheld the MBTA Communities Act as a constitutional law last week, but said it was “ineffective” until the governor’s Executive Office of Housing and Livable Communities promulgated new guidelines. The court said EOHLC did not follow state law when creating the regulations the first time around, rendering them “presently unenforceable.”

The emergency regulations filed Jan. 14 are in effect for 90 days. Over the next three months, EOHLC intends to adopt permanent guidelines following a public comment period, before the expiration of the temporary proce-

dures, a release from the office said.

“The emergency regulations do not substantively change the law’s zoning requirements and do not affect any determinations of compliance that have been already issued by EOHLC. The regulations do provide additional time for MBTA communities that failed to meet prior deadlines to come into compliance with the law,” the press release said.

The MBTA Communities Act requires 177 municipalities that host or are adjacent to MBTA service to zone for multifamily housing by right in at least one district.

Cities and towns are classified in one of four categories, and there were different compliance deadlines in the original regulations promulgated by EOHLC: host to rapid transit service (deadline of Dec. 31, 2023), host to commuter rail service (deadline of Dec. 31, 2024), adjacent community (deadline of Dec. 31, 2024) and adjacent small town (deadline of Dec. 31, 2025).

on Page 11

“I found that in my career that any time interest rates go down, it creates excitement, and it creates affordability, and it creates a little bit of fear missing out too, which all ultimately have people rushing back into the market,” Banosian said. “In fact, we saw it happen over the summer this year, when rates came down all the way from July through September.”

While interest rates receive a lot of headlines, BankFive Senior Vice President Patrick Deady noted that the availability of homes on the market is the real factor that affects buyers – many of whom are also the sellers the Massachusetts housing market relies on for inventory. And high interest rates, he said, are causing fewer homes to hit the market.

“The greatest issue for our buyers now is still inventory,” he said. I think as time goes on that should maybe loosen up a little bit in [20]25 but we’re not putting new housing out there in New England.”

Only significant life events like new jobs, divorces and deaths will motivate homeowners to enter the market, Deady said.

“I do think as time goes on, folks who’ve been married to their lower interest rate mortgages and maybe holding on and not making a move, their particular situation, whether they’re heading towards retirement, downsizing, upsizing, they’re going to have to make those decisions. They can’t put them off forever, regardless of what the rate is,” he said.

A Toxic Reputation, Too Much Compliance in Name Only Demands Rethink

BY SCOTT VAN VOORHIS BANKER & TRADESMAN COLUMNIST

Another day and yet another defeat for the MBTA Communities law.

This time it was voters in Needham who went to the polls to reject their town’s plan to comply with the state housing law, which requires cities and towns across Greater Boston to open their doors to a limited number of new apartments and condominiums.

Tuesday’s vote wasn’t even close. Nearly 60 percent of the roughly 11,000 residents who turned out rejected a previously-approved town plan that went above and beyond what MBTA Communities asked, according to results posted online by the town clerk’s office.

waged an ultimately unsuccessful legal battle against it.

The Healey administration and leading housing advocates love to tout all the communities that have passed zoning that complies with the MBTA Communities law, which requires, among other things, a sizeable multifamily zoning district near the local T station, albeit at a density that more resembles a neighborhood of triple-deckers instead of downtown Boston.

By now, 116 of the 177 communities covered under the law have complied, giving a green light to new zoning districts for apartment and condo projects.

Enlist the help of some of the state’s top marketing execs and PR gurus.

On top of the dozen or so that outright rejected the law, a number of others are slated to take up the measure in the spring town meeting cycle.

And governor, if you’re reading, here are four things you can do right away.

It’s Time for a Makeover

First, enlist the help of some of the state’s top marketing execs and PR gurus: The MBTA Communities law has a serious image problem.

And Needham is just the latest town to rebel against the 2021 measure, with more than a dozen towns having rejected plans to comply with the law either in referendums or at town meeting. Milton has infamously

But there has been a widely reported undercurrent of “paper compliance,” with some suburbs placing their new multifamily districts in industrial areas or in neighborhoods already packed with apartment buildings.

The debacle in Neeham should be a wakeup call for the Healey administration, which needs to reconsider its whole approach.

It’s gotten a reputation among some voters as a big-government plan to urbanize small towns and suburbs with massive apartment projects.

There is significant confusion over what the new zoning law actually does. The number of new units that theoretically could be built under the new zoning is routinely confused

Massive, often insurmountable amounts of student debt have prevented millions of otherwise qualified borrowers from obtaining financing to buy a house.

Of the 43 million Americans with education loans, roughly 17 million are in their prime homebuying years, according to the Education Data Initiative. But 51 percent of renters say those loans have kept them from becoming homeowners.

There are programs on the books to make your student debt go away, though – or at least to rein it in, so it no longer stands between you and homeownership.

There are several federal education loan relief programs: One plan is income-driven, another is for public servants and a third is for people with medical impairments. And according to a recent Consumer Financial Protection Bureau survey, 1 in 10 people who applied for relief with these programs were successful in having the debt discharged, canceled or forgiven.

You can access information and apply for relief on your own at studentaid.gov. But the applications are so full of legalese that you might want to enlist some experts who work with would-be homebuyers every day: people like Cat Kaiyoorawongs of LoanSense and Sara Parrish of CampusDoor.

Kaiyoorawongs works with those who have government-backed student loans, while Parrish works with folks with private education loans. (About 93 percent of all student loans are federal; the rest are private.)

Don’t

For starters, they said, you shouldn’t give up on owning a house. About 37 percent of all first-time buyers have student debt, the Education Data Initiative reports, so there is a way. But because of the all-important debt-to-income ratio, those with student debt have an average of 39 percent less buying power on their first houses than those without.

LoanSense tries to help buck that trend, working directly with consumers as well as mortgage lenders. Customers who are successful in reworking their student loans have lowered their payments from $650 to $350 a month, said Kaiyoorawongs, and raised their homebuying budgets by an average of $50,000 to $80,000 in the process.

One way to accomplish that is to consolidate your loans. While the average balance of student debt is $29,400, Parrish said that the borrowers CampusDoor sees typically have three separate loans with a total average balance of $64,000. And some have more than that.

By combining all your loans into one, you could trim your overall interest rate, at least temporarily, and increase your loan’s term. The monthly payment on the consolidated loans could be low enough that you will be able to qualify for a mortgage.

Beware, though: Refinancing or consolidating federal loans through a private lender results in the loss of important federal protections.

(sub)Payments Based on Income

with the number that would realistically get built, which is far lower.

Also, if you already own a home, the housing crisis may not seem like a crisis at all.

How about giving people like Joe Baerlein or Geri Denterlein a call?

Honey Works Better than Vinegar

Even in blue-state Massachusetts, state government doesn’t have enough staff and resources to effectively enforce the law if local officials are determined to cheat.

It’s time to consider legal forms of bribery, such as lots of additional money for schools, sewers, roads – you name it.

To qualify, borrowers need to first consolidate all their student loans and then certify their earnings and family sizes. You’ll have to recertify annually, but the payment plan could be low enough that you qualify for a mortgage. Better yet, after 25 years, Uncle Sam will forgive whatever balance is left, which is most people’s objective, said Kaiyoorawongs.

For debt owners who are public servants – anyone who works for local, state or federal government; works for a nonprofit organization; or serves in the Peace Corps, AmeriCorps or the military – you may be eligible to have your loan balance forgiven if you have worked full-time for 10 or more years.

To qualify, you must have made a total of 120 qualifying monthly payments under a federal incomedriven repayment plan. The payments need not be consecutive, though, and neither does the time worked as a public servant.

Two more options: extended and graduated repayment plans. An extended plan pushes your payments out to 25 years, thereby decreasing your monthly payment. But your balance will not be forgiven. With a graduated plan, your monthly payment starts low and then increases every two years. If you consolidate several loans under such a plan, you can have up to 30 years to pay off your debt, making it a good choice if you expect your income to keep growing.

People with total and permanent disabilities who are unable to work are eligible to have their student loans discharged. Moreover, the forgiven amount is tax-free –at least for now. That provision is up for renewal soon. Finally, if you believe your school misrepresented or made false promises about your degree or certification program, you may be able to have your loan balance discharged under the Borrower Defense program. Currently, though, the program’s rules are tied up in court. For those with private education loans, the options are far greater and more varied. Parrish said CampusDoor, which works through lenders and not directly with consumers, supports more than 1,600 unique programs offered by dozens of lenders, who have assisted more than 2.2 million borrowers along the way.

Lew Sichelman has been covering real estate for more than 50 years. He is a regular contributor to numerous shelter magazines and housing and housing-finance industry publications. Readers can contact him at lsichelman@aol.com. Banker & Tradesman

Another possibility is the Income-Based Repayment Plan, which expressly allows for federal loan forgiveness after 20 or 25 years of regular on-time payments. Sometimes called the Income-Contingent Repayment Plan, it bases your payment on your income and the size of your family.

REALTOR REMARKS

They Can Help Fix Mass. Housing Shortage If We Let Them

BY SARAH GUSTAFSON SPECIAL TO BANKER & TRADESMAN

The Commonwealth of Massachusetts took a leading step forward in 2024 with the passage of the Affordable Homes Act. The legislation authorizes a record amount of spending on housing over the next five years, $5.16 billion, and many major policy initiatives to counter rising housing costs. One of the most significant policies established by the law will begin Feb. 2, and enables property owners to build accessory dwelling units (ADUs) byright in all single-family zoning districts statewide.

The Massachusetts Association of Realtors supported this policy throughout the legislative process and stood alongside Gov. Maura Healey to celebrate when it was signed into law. Now, MAR is directing its advocacy efforts towards ensuring that the clearest and least restrictive regulations governing ADUs are adopted by the state. MAR is committed to helping address the housing crisis and the widespread adoption of ADUs will be a crucial tool to deploy to increase housing supply.

What’s an ADU?

ADUs, sometime referred to as in-law apartments, are secondary housing units created by homeowners on their property. As noted by the state, “ADUs can be within an existing primary residence, like converting a basement into an apartment, attached to a primary residence as a new construction addition, or completely detached, like a cottage or converted detached garage in a backyard.”

Under current state law, in towns where ADUs are permitted, they have generally been built by families looking to house relatives. This is largely because the regulatory burdens placed upon homeowners increase development costs for ADUs that far outpace any po-

tential rent return. By allowing them by-right, ADUs will be built more easily and may become an opportunity for homeowners to generate additional income.

The adoption of the Affordable Homes Act, along with the MBTA Communities Law, makes Massachusetts a national leader in essential housing reform.

Allowing ADUs by-right in single-family zoning statewide is expected to generate 8,000 to 10,000 new units of housing, according to the Healey administration. With an estimated need for 20,000 to 25,000 new units of housing a year through 2030 to balance and stabilize pricing, this adoption allows Massachusetts to take a real step towards meeting these goals.

By-right permission for ADUs under this law is essential to their success as a housing option.

This permitting will make ADUs easier to build by reducing red tape for homeowners. This is the most significant way to support ADUs as a viable housing type. If residents are required to work through special permitting processes it would add unnecessary time and money to the building process and create additional liability.

The other key element to success: Maximizing occupancy opportunities.

This will help increase ADU utility for homeowners. ADUs are already a compelling housing type for seniors or multigenerational housing. By allowing homeowners to also rent units to members of the public, ADUs have the potential to serve as another option in the housing market, allowing homeowners to use their homes most efficiently while addressing one of the state’s greatest needs: more housing.

Additionally, dimensional flexibility through a maximum size of 900 square feet and limited scaling require-

BY ANDREW MIKULA SPECIAL TO BANKER & TRADESMAN

In recent years, a widespread surge in home prices, rents and mortgage interest rates has made housing affordability a national political issue. Both major party candidates in the 2024 presidential election addressed housing costs during campaign speeches and proposed solutions, from down payment assistance programs to large-scale deportation operations. Federal solutions to the housing crisis are limited by the fact that most laws and procedures that guide housing development are controlled at the state and local levels. Still, there’s one idea supported by both Republicans and Democrats that may contribute substantially to housing production and affordability, albeit modified from its original form: facilitating housing development on federal lands.

At campaign rallies last fall in Nevada and Arizona, President-elect Donald Trump said his administration will “open up new tracts of federal land for large-scale housing construction,” an idea he dubbed “freedom cities.”

But instead of focusing on sprawling Bureau of Land Management (BLM) properties in the rural Southwest, the federal government should redevelop some of its properties in expensive urban areas with existing infrastructure. After all, land costs and availability are probably more likely to impede the construction of modestlypriced homes in urban enclaves, and large urban areas tend to have the most extreme housing shortages.

What’s Available to Build On?

With nearly 95 percent of federal lands managed by the BLM, National Park Service, Fish and Wildlife Service or Forest Service, there is not much low-hanging fruit for urban redevelopment at first glance.

But one agency stands out as a large urban landowner: the United States Postal Service. The USPS owns 179

properties in Massachusetts, including 14 in Springfield and 35 within Route 128. Many of these properties have underutilized parking lots and large strips of grass or dirt.

Others are located in prime downtown locations where housing or mixed-use development is clearly a better way to maximize the property’s value. USPS-owned properties constitute more than 15.3 acres in Downtown Boston alone, including the Dorchester Ave facility sandwiched between South Station and Fort Point Channel, which currently has an assessed value of $294 million.

The federal government is not subject to local zoning or discretionary reviews.

Redeveloping some USPS properties wouldn’t necessarily displace post offices or distribution centers, and service interruptions can often be minimized by building on existing parking lots. For example, there’s a 3-acre carrier annex property on Ward Street in Revere whose employee parking lot has suitable dimensions for housing. During construction, employees could take advantage of the fact that Ward Street has on-street parking on both sides.

Constructing this housing would require the USPS to partner with a private developer, perhaps under a ground lease arrangement, allowing the agency to keep the land costs low for the developer in exchange for stricter affordability protections on the units. Some observers have even suggested that redeveloping post offices to add housing could help stabilize the USPS’s finances, as the agency had total net losses of $9.5 billion in fiscal year 2024.

An aggressive and holistic approach to redeveloping Postal Service properties alone may result in thousands of additional housing units in Massachusetts. In and of itself, this is not very many considering that the time-

ments related to the size of the single-family home will help more homeowners access ADUs and give them the ability to right-size the structure to their needs. This outcome can be improved by including a provision in the final regulations that allows homeowners whose singlefamily home or lot that does not conform with current zoning to still benefit from by-right ADU approvals.

The implementation of this law is at a critical stage.

The Executive Office of Housing and Livable Communities (EOHLC) intends to issue final regulations by the effective date of the ADU law, Feb. 2. EOHLC initiated the regulatory development process on Dec. 6, 2024, by releasing draft ADU regulations.

MAR is watching this process closely and is an active participant on behalf of our members. The public comment period was open from Dec. 20, 2024, through Jan.10, 2025. A public hearing was also held on Jan. 10.

The implementation of this law is at a critical stage.

With a history of community opposition to housing in mind, MAR is extremely concerned about the ways in which municipalities may attempt to subvert the intent of this law. Massachusetts has one of the most expensive housing markets in the country because, quite simply, our housing demand far outpaces our supply. That asymmetry was created by decades of abuse of state-granted zoning powers. In its comments, MAR sought to highlight the critical importance of limiting the restrictions that can be placed on homeowners seeking to build ADUs.

As the state seeks to address the unprecedented crisis in housing availability and affordability, MAR will continue to press state leaders to establish innovative and thoughtful solutions, like allowing ADUs by-right in single-family zoning statewide.

Sarah Gustafson is the 2025 president of the Massachusetts Association of Realtors and a Realtor with KW Pinnacle Central in Worcester.

line and administrative process for this development would likely be very long and complicated.

However, one major benefit of building housing on federal lands is that the federal government is not subject to local zoning or discretionary reviews that often derail private developments in Massachusetts.

The Key Factor: Replicability

Further, there is potential for greater impact if the federal land redevelopments serve as a catalyst for state and local governments to redevelop similarly underutilized land that they own.

A 2024 study by the Lincoln Institute of Land Policy found that Massachusetts has the most buildable government-owned land in transit-accessible urban areas of any state, with 89 percent of it owned by local governments. If all these government-owned properties were redeveloped into housing at 15 units per acre, the same density prescribed by the MBTA Communities law, the state would add 387,000 housing units, enough to solve our housing shortage nearly two times over.

Lastly, it should be noted that federal government disposition of property to facilitate housing and mixed-use development has several recent precedents in Massachusetts, notably the Volpe Transportation Center redevelopment in Cambridge. The General Services Administration (GSA) is currently in the process of selling or transferring a Coast Guard building in Boston and an administrative building in New Bedford. Many more federally owned office and administrative buildings have been rendered obsolete by the post-COVID move to remote work and the recent expansion of online government services.

What’s missing is an effort to facilitate Volpe-like redevelopments at scale across agencies. This higher-level coordination is something the Trump administration could take on; indeed, Congress has already set the stage with legislation reforming the GSA and requiring more transparency over how federal office space is utilized.

While post offices may be disproportionately located in adaptable and village-like locations, they’re just the tip of the iceberg for redevelopment of government-owned properties. The incoming administration has already recognized this potential - here’s hoping they act on it.

Andrew Mikula is the senior housing fellow at the Pioneer Institute in Boston.

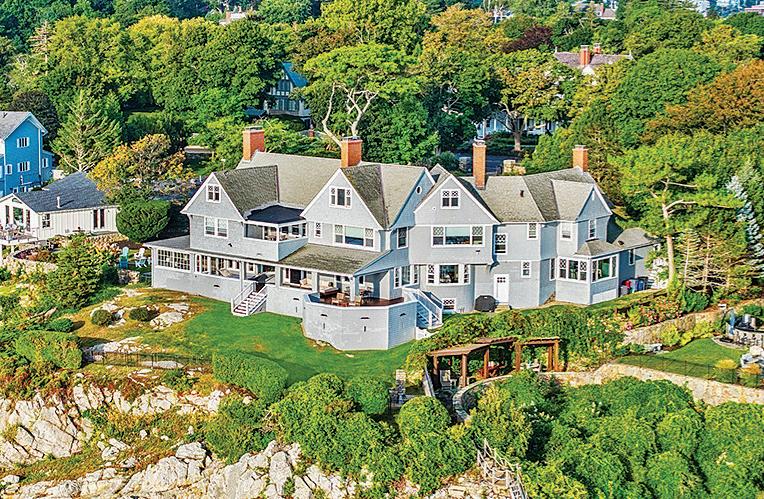

Address: 430 Stuart St. #35D, Boston

Price: $10,400,000

Buyer: Jennifer C. Paul

Seller: TS Residences Holdings LLC

Agent: Manuel Davis, The Collaborative Companies

Size: 2,297 square feet

Sold: 12/31/2024

Units high in the sky dominate this week’s Gossip Report. And no matter which one you pick they all have great views. The first looks east across Bay Village and the Seaport District in the distance. From the dinner table in the second, you can gaze almost due south towards Roxbury and the Blue Hills. The third gives great views of Boston Harbor and construction at the South Station Tower.

1,4,5 2

Address: 3 Dunes Road, Edgartown

Price: $10,000,000

Buyer: Dunes Road PCAC3 LLC

Seller: Stephanie D’Angelo

Agent: Courtney Marek and Leslie Heidt, Sandpiper Realty Size: 5,593 sq. ft. on 1.5 acres

Sold: 12/30/2024 2

Address: 363 Ocean Ave., Marblehead

Price: $7,250,000

Buyer: Heather B Rosenbaum RET

Seller: Cathe A. Chiaramonte

Agent: Jodi Gildea and Sean Jodi Gildea, Sagan Harborside Sotheby’s Size: 7,396 sq. ft. on 1.44 acres Sold: 1/2/2025

Address: 1 Dalton St. #4305, Boston

Price: $6,350,000

Buyer: Belairave LLC

Seller: Clarendon Bb2020 RT

Agent: Tracy Campion, Campion & Co.

Size: 2,188 square feet

Sold: 12/30/2024 4

Address: 240 Devonshire St #6008, Boston

Price: $5,725,000

Buyer: Marcella Behman

Seller: MCAF Winthrop LLC

Agent: Elise Bain, Patrick Cutter and R. Wayne Lopez, MP Boston Size: 2,484 square feet Sold: 12/30/2024 3

■ Showcase your listings alongside The Gossip Report, reaching high-net-worth individuals eager for the latest in luxury real estate.

■ Get noticed with exclusive online banner placements on bankerandtradesman.com, ensuring your name and listings shine bright in the digital sphere.

■ Stand out in Banker & Tradesman’s Weekly Newsletter with native ad property links and images, captivating engaged subscribers.

Contact Suzanne at 617-896-5307 or sprovencher@thewarrengroup.com for more details!

Title: President and CEO, Massachusetts Housing Investment Corp. Age: 48 years

Industry experience: 24 years

BY STEVE ADAMS BANKER & TRADESMAN STAFF

Anew fund managed by Massachusetts Housing Investment Corp. will offer financing to preserve private but moderately-priced housing, adding to the Boston-based nonprofit’s growing role in the housing market. Deep-pocketed institutions and the city of Boston contributed seed money to the revolving Boston Acquisition Fund. As administrator, MHIC will work with developers that commit to keeping rents affordable after acquiring properties. CEO Moddie Turay, MHIC’s CEO since 2022, previously worked in community development roles as an assistant to Washington, D.C. Mayor Anthony Williams in Washington, D.C. and an executive for the Detroit Economic Growth Corp.

We could start deploying any day now. We’re not waiting to have the entire fund funded.

Q: How does MHIC fit into the housing ecosystem?

A: We’ve invested over $3.5 billion over our now-35-year history, and $500 million of that is in Roxbury alone. We are the largest nonprofit [low-income tax credits] syndicator in Massachusetts. We also invest in Rhode Island and Connecticut and we’re looking to expand into upstate New York in 2025. Over the years, we’ve really been a partner with the state and the city with both private and nonprofit developers and small business owners. It literally says in our mission statement “to finance projects that others will not.” We go into neighborhoods well before and work with developers on projects before some of them are bankable by your traditional banks. So we are that entrepreneurial community finance partner for projects like that.

Q: What is the strategy of the new Boston Acquisition Fund?

A: It’s anti-displacement with a focus also on keeping units that have the potential to remain affordable, even if it’s a vacant building that’s going on the market, or a building that is on the market that is currently affordable, that could change hands and go to a developer who would raise rents. If we’re not focusing on preserving what we actually have, then that’s the hole in the bucket. You have to concern yourself with building new, and preserving what you have. The fund, and the partnership with the city, allows that to happen. There has to be flexibility and there has to be speed. These are private transactions that are happening. We’re trying to equip like-minded developers or apartment owners to be incentivized and be competitive in the marketplace, to go out and grab these properties and keep them affordable. To do that, they need low-cost capital, and they need speed to compete with the private marketplace.

Q: Has the fund exhausted most of the major institutional donor pool?

A: I think there is a lot of opportunity to raise. I wouldn’t say all the low-hanging fruit has been tapped. There are a lot of partners we are in conversations with that will invest in the fund. We are in constant contact with a lot of the other potential investors and donors. We’re already looking at deals. We could start deploying any day now. We’re not waiting to have the entire fund funded.

Q: How does the $50 million Developers Impact Fund work and when will it begin selecting projects?

A: We approved our first round of projects before the end of the year. That is funded by $50 million from the state, and we are going to raise additional funds. But right now, we are focused on the deployment of the first $50 million and we are making loans and will make an announcement shortly. The fund will offer predevelopment and growth capital through lines of credit and other financial assistance

Q: Has Boston’s emphasis on fast-track approval of affordable housing proposals made an impact?

A: We have to be doing everything everywhere at once. The ARPA money is starting to run out. People are having to get really creative to get these projects across the finish line. We at MHIC also invest in market-rate, which is also important to affordable housing. I get almost as excited about market-rate housing being built in Boston and other communities, because it takes the pressure off affordable housing. For Massachusetts, what used to be considered a starter home is no longer a starter home. If you have what used to be a starter home competing with someone who has a higher spending limit than you do, you’re going to lose every time. The only way we work our way out of that is to solve for all of these segments in our market.

Q: What are MHIC’s top priorities for 2025?

A:

We have spent all of our Healthy Neighborhoods II fund, which was about $42 million, so we’ll be focused on fundraising for Fund III, a $50 million fund. We actually score projects based upon health outcomes: communities that embrace healthy outcomes, walkability and proximity to healthy food and hospitals and health services. And we are hyper-focused on working with the city on their programs and MassHousing on the Equitable Developers Fund, and looking at how we can expand our [low-income tax credit] platform in Massachusetts.

BY STEVE ADAMS AND JAMES SANNA BANKER & TRADESMAN STAFF

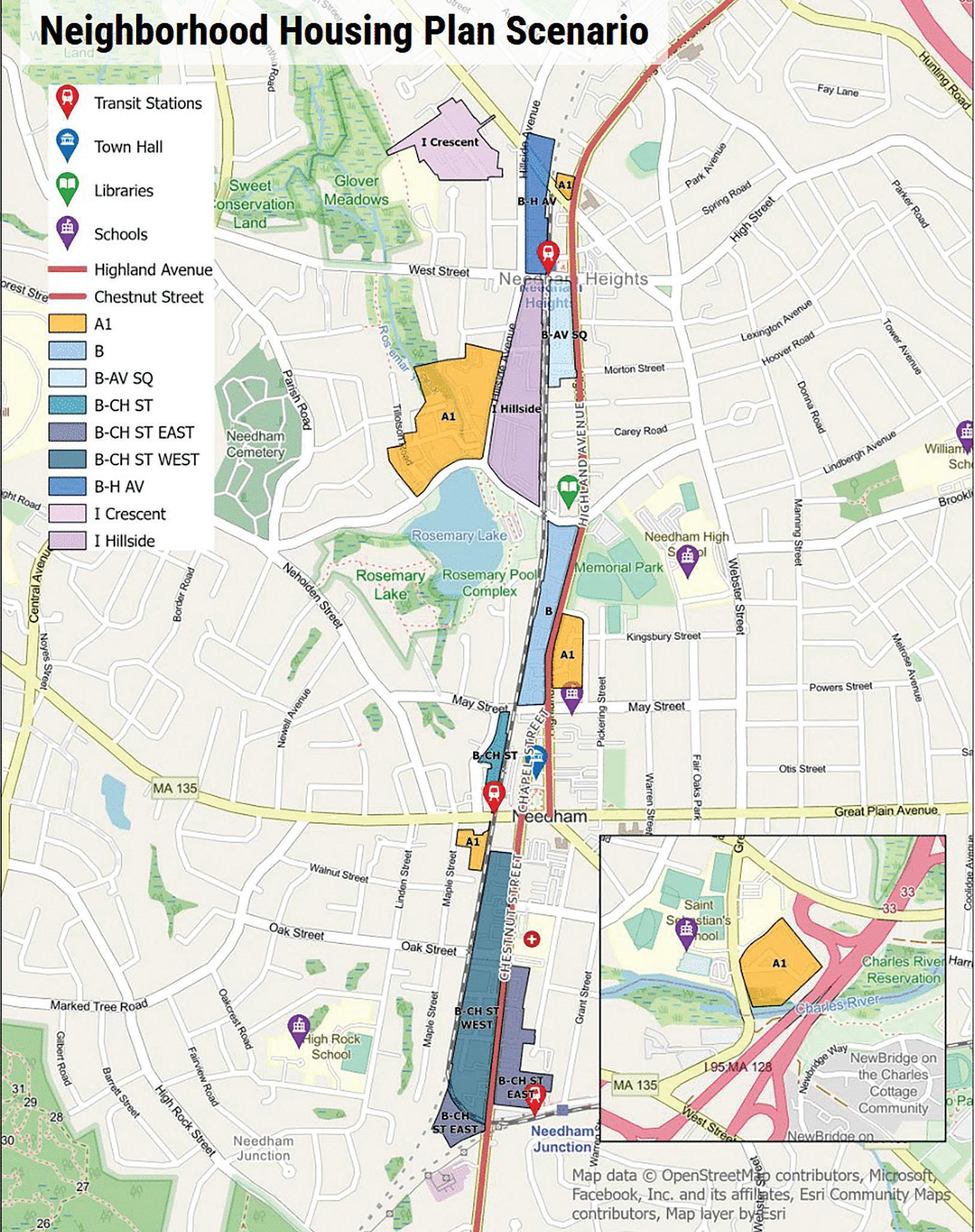

In another blow to advocates and state officials hoping for another Boston suburb that would welcome new zoning, Needham voters resoundingly rejected a plan last week to add thousands of new apartments in the town’s commercial districts.

The upzoning plan passed by Needham Town Meeting by a 118-90 vote in October to comply with the MBTA Communities law. It would have likely allowed up to 2,500 new homes to be built over the coming decades on top of the roughly 775 multifamily units that exist in the districts now, officials estimated.

But opponents used town bylaws to force a referendum on the plan. That referendum, held Jan. 14, saw Needham voters resoundingly reject the plan, 6,866 to 4,882 – a nearly 60-40 split against.

Yes for Needham, the coalition of businesses and residents supporting the zoning plan, fought back with data showing the new housing would benefit local businesses and would have minimal impact on the school district, particularly on its existing building plans.

“The voters have spoken, and while YES for Needham is disappointed with the outcome, we look forward to seeing the vision that the Planning Board and Select Board lay out over the coming weeks and months regarding the future of multi-family housing in Needham,” the group wrote in a Facebook post after the results were announced. “We stand with the town and are committed to ensuring a future where Needham seniors, workforce, and young people have access to flexible housing.”

The town could also face a lawsuit from Attorney General Andrea Campbell, a possibility confirmed by the state’s highest court last week.

Town officials supporting the larger rezoning project said they backed the state’s strategy of tackling Massachusetts’ housing affordability crisis through expanded multifamily development of multifamily in the suburbs.

Under new guidelines issued the same day by state housing officials, Needham has six months to come up with a new zoning plan that has room for 1,784 existing or new multifamily units near its commuter rail line stations before it loses access to a litany of state grant programs. The town could also face a lawsuit from Attorney General Andrea Campbell, a possibility confirmed by the state’s highest court last week.

Needham Residents for Thoughtful Zoning, the opposition group, had attacked the zoning plan using familiar avenues. The group’s website argues it would “destabilize” property values, lead to “uncontrollable growth” in the school-age population, bring congestion and damage what they described as Needham’s “small town” character.

The plan would have applied to sections of Chestnut Street, Highland Avenue, Crescent Road and Hillside Avenue, which include commercial properties and multifamily housing.

Last week, the Supreme Judicial Court upheld the state’s authority to enforce provisions of the law, but overturned regulations on its implementation because of a procedural error by the state Executive Office of Housing and Livable Communities. Gov. Maura Healey announced emergency regulations requiring communities to comply by July 14.

The new timetable gives additional time to suburbs that had been subject to a Dec. 31 deadline which applied to communities with commuter rail stations and adjacent communities.

Although at least 116 communities in the category submitted compliance plans, town meetings in Duxbury, Halifax, Hanover, Han-

son, Marshfield, Winthrop and Wrentham all rejected multifamily zoning districts late in the year. Many others have opted for so-called “paper compliance” by designing zoning districts that are unlikely to result in much new development due to dimensional limits, infrastructure limitations or existing land uses. Officials and voters in a limited number of other communities like Lexington and Watertown have moved to welcome dramatically more

THE WARREN GROUP | LOAN ORIGINATOR MODULE

housing units than they were required under the MBTA Communities law.

“As disappointing as the vote in Needham is, the overwhelming trend in Massachusetts is unchanged: cities and towns are consistently giving the green light to more housing because voters know that the future of our commonwealth depends on investing in housing,” Rachel Heller, CEO of Citizens’ Housing and Planning Association (CHAPA), said in a statement.

Identify top loan originators with The Warren Group’s Loan Originator Module. Analyze the local mortgage lending market with custom reports that highlight rankings, competitors, and individual loan officers. View data across various time periods, geographies, and so much more.

Visit www.thewarrengroup.com to view a sample report. Contact 617.896.5367 or email customerservice@thewarrengroup.com for more information.

Popularized during the late 19th century in Eastern and Central Massachusetts, triple-deckers’ construction declined sharply following the passage of the Massachusetts Tenement House law in 1912. Many jurisdictions also enacted zoning outlawing the building style amid an anti-immigrant backlash in subsequent years.

Seeing an opportunity for triple-deckers to fill hundreds of surplus building lots scattered throughout the city, the Boston Mayor’s Office of Housing last year sought innovative proposals for “Future Deckers” and offered a pair of parcels in Dorchester and Roxbury as proving grounds.

Despite the potential to acquire parcels at 379 Geneva Ave. and 569 River St. for a nominal price, none of the six proposals were able to make the finances work.

“Construction costs are a big challenge,” said Wandy Pascoal, manager of housing innovation and awards for the Boston Society of Architecture, which partnered with the city on the design competition. “And as we’ve seen over the last couple of years, the price points have been difficult for folks to grapple with.”

The request for proposals listed acquisition prices as low as $100 per parcel. But to qualify for additional city subsidies, developers were required to offer units at prices affordable to households earning a maximum of 100 percent of area median income. And at least half of units would be reserved for households earning a maximum 80 percent of AMI, with a maximum sales price of $297,200 per three-bedroom home.

Developers submitted a range of 21st century variations on the triple-decker.

Boston-based Athena Real Estate Development, in partnership with Kaplan Construction and Hacin + Associates, proposed a “Triple Quadra-Decker” including 12 units on the 569 River St. site.

The project incorporated modular construction techniques to reduce costs and construction timelines, but still fell approximately $300,000 per unit short of feasibility, Athena Real Estate Development President Lisa Serafin said. Construction costs were estimated at $600,000 per unit, approximately twice the maximum purchase price allowed under the competition’s guidelines.

“When the city is providing their land at no cost, they have expectations [for affordability],” Serafin said. “Part of it is where we are in

WHAT: WEST VILLAGE G STUDENT RESIDENCE HALL

WHERE: 450 PARKER ST., BOSTON

OWNER: NORTHEASTERN UNIVERSITY

BUILT: 2024

• Northeastern University selected Kripper Studio to redesign 109,000 square feet of interiors at the West Village G student residences in Boston, seeking to enhance quality of life and a sense of community.

• The six-story building includes four tiered classrooms along with apartment-style student residences.

• Led by general contractor Turner Construction, the project upgraded shared amenity spaces, classrooms and the building entrance while improving energy efficiency.

• Nearly 1,200 light fixtures including ground-floor pendants were updated with energy-saving LED bulbs. Flooring was replaced with a durable and low-VOC vinyl tile with a wood-like finish.

THEY SAID IT:

“Starting with the

THINK YOUR PROPERTY IS HOT?

Drop Steve a line at sadams@thewarrengroup.com

Studio

the construction market and labor costs. A lot of projects are not working, even in the best locations.”

The results of the competition point to the need for additional subsidies if projects include an affordable component, Serafin said.

One such program was announced in June, when the city of Boston and MassHousing’s CommonWealth Builder program awarded a combined $20.7 million to three developers that are constructing 55 affordable condominiums on vacant city-owned parcels. The projects will be built by DVM Housing Partners in Mattapan, DREAM Development in Roxbury and Urbanica in Dorchester. Some developers finding sites on the private market have had success reviving the next generation of market-rate triple-deckers, and could find expanded opportunities as Boston rezones residential neighborhoods.

After working at Boston-based developer Haycon Inc. in construction, Sean George founded his own firm to pursue infill housing developments. Scouring assessors’ data, he looks for vacant parcels of at least 2,000 square feet and tracks down owners to make offers.

None of the six ‘Future Deckers’ proposals were able to make the finances work.

In Boston, three-family dwellings currently are allowed in neighborhood zoning subdistricts in Allston-Brighton, Jamaica Plain, Roslindale, Roxbury and West Roxbury. Three-family zoning as-of-right was added in portions of East Boston and Mattapan in 2024.

A typical project was completed last May in Dorchester, where George and business partner Darren Maguire completed a triple-decker at 16 Church St. The developers acquired the property for $295,000 and received just over $1 million in construction financing from Needham Bank in May 2023. The completed product blends classic triple-decker features such as bay windows and front porches with modern touches such as open floor plans and pendant lighting, with rents listed at $4,200. Built with traditional techniques including central gas heating systems, such projects can be completed in under a year, George said.

George said the biggest hurdle to projects is time spent acquiring all of the necessary approvals, ranging from variances to fire and plumbing permits, which has taken as long as 260 days.

“Honestly, the city just has to fix the permit process,” he said. “Builders will build, and they’ll do it as quickly as they can to make it work.”

Email: sadams@thewarrengroup.com

Continued from Page 3

Nevertheless, Marquis, Banosian and many others interviewed for this story said they were optimistic 2025 could see an uptick in home sales – and thus mortgage demand –over last year.

And when it comes to converting those potential seller-buyers into mortgage customers, Leader Bank head of residential lending Sean Valiton believes that having loan originators that customers can trust is key to helping them navigating the mental hurdle of the interest rate environment.

“With our retail model and our highly seasoned loan officers – very high-performing loan officers – it’s about building trust,” he said. “It’s about the consultative approach of sitting down with a client, finding out what their needs are, and then being real with what the market looks like and what they should be expecting out there – and then building trust around the fact that they will have options with you in whatever scenario that they run into while they’re out there shopping and that we understand.”

If predictions of more home sales in 2025 come through, it appears that competition across the industry is still poised for a reduction.

In recent years, on both the buyer and lender side competition has been high due to a lack of inventory.

“Generally, I find that competition from the lending standpoint, gets more fierce when rates go up, because everybody’s scrapping and clawing through the same loans, because there’s less of them,” Banosian said. “When rates come down, it’s generally not as fierce because people tend to be doing okay as rates improve because application volume goes up, lock volume goes up, and on top of that, they have refinance volume they can also handle as well.”

Some financial institutions are also scaling back their mortgage lending as they try to reshape their balance sheets for the new interest rate environment. And some loan originators and mortgage companies have been driven out of business.

“You’ve also seen a lot of the kind of flyby-night originators, the part-timers, a lot of those people have not renewed their NMLS licenses,” Marquis said. “So, if there’s less folks in the business, they’re just going to have to be less competition and I think as we see more transaction and less lenders and originators to fulfill that that business, the less the competition would be.”

Email: sminton@thewarrengroup.com

BY JENNIFER SMITH COMMONWEALTH BEACON

Even as proponents of the MBTA Communities Act cheer its high court green light and await forthcoming emergency regulations, they’d like everyone to keep their feet planted solidly in reality about the possible impacts of the sweeping housing law.

“This is a good moment to reflect back on the last couple of years of debating the law,” Luc Schuster, executive director of Boston Indicators at the Boston Foundation, said on The Codcast, CommonWealth Beacon’s podcast. “With that in mind, I’ve been worried that both sides of the debate have been overstating the promise of MBTA Communities for a while now. And I come at that from the perspective of thinking this is directionally exactly the sort of thing we need to do as a state. We need to act collectively across municipal boundaries to build more housing.”

But the controversial zoning act, which requires cities and towns served by or near the MBTA system to zone for a multifamily district, is not about to open the housing floodgates.

“Forty thousand seems small compared to that,” Schuster said. “On the other hand, any new home we build is another family that can live in our communities, contribute to our local economy. And if we pass a few laws like MBTA Communities over the next several years – 40,000 here, 10,000 here, the governor’s legalization of accessory dwelling units is a few tens of thousands of units – that starts to really add up. So I think, big picture, this is exactly what we need to do. It’s just not a single silver bullet. And I think both sides have sometimes confused that piece of it.”

Needham voters rejected a zoning plan Jan. 14 approved by Town Meeting after two years of planning.

Schuster thinks language and estimates around “zoned capacity” – best guesses of how many units could legally be built under the new zoning rules – has led to confusion and strife in the rezoning process.

While the total upzoning promises hundreds of thousands of possible units, “I think many just very sincerely confuse that zoned capacity number with what would actually get built,” he said. Boston Indicators research into similar upzoning across the country found that only about 5 to 10 percent of those units actually change ownership – and therefore could be built with more units on the same lot – in a decade.

His back of the napkin math of “a positive optimistic scenario” for MBTA Communities estimates that the law might yield 40,000 new housing units in 10 years. It’s more housing in the pipeline, but falls far short of the roughly 200,000 units the Healey administration estimates the state will need in the coming years to meet demand.

Some municipalities have taken a more cynical swing at the rezoning, opting for “paper compliance.” Greg Reibman, president of the Charles River Regional Chamber, pointed out last year that an 850unit apartment project underway before the rezoning began was being counted as about 60 percent of the “new” units in Wellesley’s proposed multifamily district. The final approved rezoning plan would allow a total of 1,727 multifamily units, including the 850 already zoned for at Wellesley Park.

The Charles River Regional Chamber represents Newton, Needham, Wellesley and Watertown.

Needham voters rejected a zoning plan Jan. 14 approved by Town Meeting after two years of planning, Reibman noted. The town was torn – in a stark echo of Milton just a year ago – over the proposal’s top-line potential unit number.

The zoning unit counts and the name of the law go to the heart of the years-long debate, with about 28 communities opting to blow past their compliance deadlines while the high court deliberated.

“If I could roll back the hands of time, go in the way back machine, I would say please don’t call this the MBTA Communities Act,” Reibman said. “It’s just caused so much confusion about it.”

He and Schuster noted that housing policy is tethered to climate goals, local and regional economics, education access, and, yes, transportation.

Past efforts to sweeten the pot have failed, relying on highly targeted initiatives that involved a little sprinkle of money for every unit permitted near a train station.

This is a job that calls for hundreds of millions in potential grants and aid to help ease local concerns, not just a few million here and there.

Third, remember that towns like Milton and Winthrop probably aren’t worth making a stink over.

I don’t see developers lining up to build in Milton, whatever the zoning, while Winthrop is a 1.6-square-mile peninsula in Boston Harbor.

Every attempt by state officials to crack the whip against recalcitrant communities simply riles up potential opponents in other towns, while doing little to advance the cause of actually getting more housing built.

More Ways to Comply

Lastly, start promoting a broader array of housing, including starter homes.

Making MBTA Communities the centerpiece of the state’s efforts to rev up housing production was a real mistake.

The whole program feels like it was crafted to assuage the concerns of transit activists and

“The reality is that transportation is a huge impediment here,” Reibman said. “You can have debates on the floors of city councils and town halls, and when an opponent gets up and says, ‘But our schools; it’ll overcrowd our schools,’ say, ‘Well actually school enrollment has declined. Statewide school crowding is not really an issue.’ And they can say, ‘But water and sewer,’ and you say, ‘Well actually our water and sewer systems have been upgraded, or there’s a way to upgrade it, so that’s not a problem.’ And so on and so forth until they say, ‘but transportation’ and you go, ‘got me.’ Our transportation is not adequate to meet the needs for our housing.”

The MBTA Communities language was never designed to take the quality of transit service into account, which critics seized upon during the years of slow zones, long headways, burning trains, derailments, shuttles, and staffing shortages. After years of shutdowns for track work, the system quality has improved, with MBTA leadership celebrating a slow zone-free system this year.

The long-term well-being of the transportation system is still something of an open

question, as a fiscal cliff looms this summer, and Universal Hub diligently reports on the regular travails of passengers dealing with cracked rails and signal switch issues.

“I’d say there’s no way to fully separate the transit conversation from the housing one,” Schuster said. “So I think they’re going to have to be related to some meaningful degree no matter what. One challenge with MBTA communities is that I think it’s been a bit of a Rorschach test for people wanting to address different pressing challenges we face as a region.”

Organizations across the political spectrum have been pushing for implementation of the MBTA Communities Act, from the discrimination-focused Lawyers for Civil Rights, to the pro-housing Abundant Housing Massachusetts, to the free-market think tank Pioneer Institute. The blend of housing advocates, environmentalists, business groups, and even clergy working toward the rezoning goal, Reibman said, “should change the dialogue for years.”

This article first appeared on CommonWealth Beacon and is republished here under a Creative Commons license.

Continued from Page 3

Under the emergency regulations, communities that did not meet prior deadlines must submit a new action plan to the state with a plan to comply with the law by 11:59 p.m. on Feb. 13, 2025. These communities will then have until July 14, 2025, to submit a district compliance application to the state.

Communities designated as adjacent small towns still face the Dec. 31, 2025 deadline to adopt compliant zoning.

environmentalists, with creating new housing that people will actually want to live in a secondary concern, if that.

Not everyone wants to live near a train station. There should be an equal effort to revive starter homes, create pocket neighborhoods of single-family homes on small lots and other types of new housing.

And it shouldn’t all be tied to proximity to mass transit, which has some serious limitations in the Boston suburbs as it exists right now.

Give communities more options for building new housing, rather than having to buy into a relatively one-size-fits-all program.

MBTA Communities is not the solution to the state’s housing production woes, and it never will be.

It’s time for the Healey administration and housing advocates to put the initiative on the back burner and head back to the drawing board.

And a good starting point might be asking what types of housing Massachusetts residents want, rather than informing them that there is only one choice, take it or leave it.

Scott Van Voorhis is Banker & Tradesman’s columnist and publisher of the Contrarian Boston newsletter; opinions expressed are his own. He may be reached at sbvanvoorhis @hotmail.com.

Like the old version of the guidelines, the new emergency regulations gives EOHLC the right to determine whether a city or town’s zoning provisions to allow for multi-family housing as of right are consistent with certain affordability requirements, and to determine what is a “reasonable size” for the multi-family zoning district.

The filing of emergency regulations comes six days after the SJC decision — though later than the governor’s office originally projected. Healey originally said her team would move to craft new regulations by the end of last week to plug the gap opened up by the ruling.

“These regulations will allow us to continue moving forward with implementation of the MBTA Communities Law, which will increase housing production and lower costs across the state,” Healey said in a statement. “These regulations allow communities more time to come into compliance with the law, and we are committed to working with them to advance zoning plans that fit their unique needs.”

A total of 116 communities out of the 177 subject to the law have already adopted multifamily zoning districts to comply with the MBTA Communities Act, according to EOHLC.

Law firm (Apostolica Donovan & Donovan) has a modest amount of additional space for 1-2 professionals in a cost effective, low commitment format. The space is ideal for legal practitioners or real estate brokers seeking a credible Back Bay address for principles or clients, and within easy and immediate access to both the Mass Pike and Storrow Drive. Convenient parking and base administrative services (support) also available.

For more info contact Bill Apostolica, Esq. wpa@apostolica.com | 617-424-6500

Monthly Transfer Directory (COMP) Reports are a comprehensive property valuation andmarket resource containing sales transactions for all properties and their related assessment information, in an easy–to–read and portable report.

Each report lists every real estate transaction over $1,000, by market, including FSBOs, estate sales and foreclosure deeds for MA, NH, CT and RI.

• Perform comparable sales analysis

• Verify appraisals

• Identify sales trends

• Locate new homeowners for marketing campaigns

• Gives you easy access to comparable sales and their assessment details in the areas you care about most.

• A year-end compendium you can file away for future reference and research.

• Available in easy to read PDF format or in print for an additional cost.

• Includes all sales, including foreclosure deeds and fsbos, so you won’t miss a thing!

• Order an individual town, county, or state of your choice (MA, NH, CT, RI). County level includes all towns within that county.

Sale: $2,370,000 (10/17)

COMMERCIAL ST U:301 $605,000

B: Audrey K Yu S: Allen Karp & Danielle Karp

70954/270, Date: 12/30/24

Fairway Ind Mtg $544,500

Term: 2054

Use: 1 Bdrm Condo, Lot: 599sf Prior Sale: $574,500 (06/19)

50 COMMONWEALTH AVE U:905 $1,290,000

B: Christa C Bryant & Evan A Bryant

S: Sean Gilden

Book/Page: 70958/330, Date: 12/30/24

Mtg: LoanDepot Com $790,000 Term: 2054

Use: 1 Bdrm Condo, Lot: 860sf Prior Sale: $1,275,000 (06/23)

390 COMMONWEALTH AVE U:211 $1,275,000

B: Patriot Management LLC

S: William J Grubbs, Tr for Gb Holdings T

Book/Page: 70960/167, Date: 12/30/24

Use: 2 Bdrm Condo, Lot: 1346sf Prior Sale: $1,187,500 (09/19)

1 DALTON ST U:4305 $6,350,000

B: Belairave LLC

S: Caroline Rando, Tr for Clarendon Bb2020 Rt

Book/Page: 70957/203, Date: 12/30/24

Use: 2 Bdrm Condo

Prior Sale: $6,250,000 (06/22)

240 DEVONSHIRE ST U:4311 $1,575,000

B: David F Slayton & Tracey Slayton

S: Mcaf Winthrop LLC

Book/Page: 70954/81, Date: 12/30/24

Mtg: M&T Bank NA $1,121,976

Term: 2054 Rate: 4 1% Type: Adj Use: Condo

240 DEVONSHIRE ST U:4703 $2,600,000

B: Svatoslav Outulna & Katerina Outulna

S: Mcaf Winthrop LLC Book/Page: 70967/73, Date: 12/31/24 Use: Condo

240 DEVONSHIRE ST U:4814 $2,475,000

B: Rong Yang

S: Mcaf Winthrop LLC

Book/Page: 70958/1, Date: 12/30/24

Use: Condo

240 DEVONSHIRE ST U:5003 $2,825,000

B: Matthew J Peters, Tr for Matthew Peters RET

S: Mcaf Winthrop LLC

Book/Page: 70967/28, Date: 12/31/24

Mtg: M&T Bank NA $1,976,700 Term: 2054 Rate: 5 9% Type: Adj Use: Condo

240 DEVONSHIRE ST U:5009 $2,892,320

B: Ellen Chae & Paul Chae

S: Mcaf Winthrop LLC

Book/Page: 70965/169, Date: 12/31/24

Mtg: M&T Bank NA $2,169,240

Term: 2054 Rate: 5 3% Type: Adj

Use: Condo

240 DEVONSHIRE ST U:6008 $5,725,000

B: Marcella Behman

S: Mcaf Winthrop LLC

Book/Page: 70958/319, Date: 12/30/24

Use: Condo

65 E INDIAN ROW U:36C $891,000

B: Glenn Desouza & Qi Tan

S: Marjorie Schechner & Jacon G Shurt

Book/Page: 70970/311, Date: 01/03/25

Use: Condo

85 E INDIAN ROW U:16H $729,500

B: Dipali Sawhney

S: Harbor 10A LLC

Book/Page: 70971/318, Date: 01/03/25

Use: Condo

163 ENDICOTT ST U:3

B: Laverty Ford

S: Kelly Hudak

Doc#: 000000000957904, Date: 12/31/24

$665,000

Mtg: M&T Bank NA $465,500

Term: 2054 Rate: 6 8% Type: Adj

Use: 2 Bdrm Condo, Lot: 714sf Prior Sale: $343,000 (05/06)

1 FRANKLIN ST U:1808

B: John M Ferrara & Kathleen A Ferrara

S: Liyu Yang

Book/Page: 70970/302, Date: 01/03/25

$1,875,000

Use: 2 Bdrm Condo

700 HARRISON AVE U:401 $750,000

B: Mark J Doherty

S: James P Edasery & Beppy J Edasery

Book/Page: 66645/191, Date: 11/10/21

Use: 2 Bdrm Condo, Lot: 1084sf Prior Sale: $524,000 (03/10)

700 HARRISON AVE U:610 $808,500

B: Mark J Doherty

S: Rui Wang

Book/Page: 70918/203, Date: 12/18/24

Use: 2 Bdrm Condo, Lot: 1028sf Prior Sale: $870,000 (07/15)

700 HARRISON AVE U:610 $610,000

B: Andrew Bond & Christine Liang

S: Thomas Johnson

Book/Page: 48023/254, Date: 06/15/11

Mtg: Charles Schwab Bk NA $457,500

Rate: 4 0% Type: Adj

Use: 2 Bdrm Condo, Lot: 1028sf

107 JERSEY ST U:3-7 $435,000

B: Shannon Nornhold

S: Ross J Ozer & Scott D Gortikov

Book/Page: 70971/228, Date: 01/03/25

Use: Condo, Lot: 431sf Prior Sale: $60,000 (08/99)

3 JOHNNY CT $1,050,000

B: Row House Investments Inc

S: Robert Chin, Tr for Chin FT

Book/Page: 70962/278, Date: 12/31/24

Mtg: Life Ins Cmnty Inv $3,000,000

Term: 2025 Use: 4 Bdrm Row-Middle, Lot: 975sf

214 MARKET ST U:407 $760,000

B: Shu Chen S: Juhyung Park & Taeyeon Oh Book/Page: 70967/83, Date: 12/31/24

Mtg: Rocket Mortgage LLC $608,000

Term: 2054 Use: 2 Bdrm Condo 2 MARLBOROUGH ST U:1 $685,000

B: Annette Brien

S: Stephen Buchanan Book/Page: 70970/338, Date: 01/03/25 Use: 1 Bdrm Condo, Lot: 660sf Prior Sale: $486,000 (06/14)

51 N MARGIN ST $2,000,000

B: Bogart & Zoie Hldg LLC

S: Susan Cincotti, Tr for 51 N Margin St Rt Book/Page: 70971/179, Date: 01/03/25

Mtg: First Boston Cnst Hld $5,635,000 Use: Retail-Service, Lot: 2717sf

38 P ST U:2 $924,900

B: Nicole B Maher & Liam Maher

S: Christopher B Harding & Caroline F Foz Book/Page: 70971/87, Date: 01/03/25

Mtg: Cross Country Mtg Inc $174,900 Term: 2055 Use: 2 Bdrm Condo Prior Sale: $885,000 (11/22)

452 PARK DR U:A $1,160,000

B: 151 Highland LLC S: Mark Zamir & Leah Zamir Book/Page: 70970/237, Date: 01/03/25

Mtg: Middlesex Svgs Bk $800,000 Use: 2 Bdrm Condo, Lot: 777sf

133 SEAPORT BLVD U:1108 $2,480,000

B: Patricia A Lewis, Tr for Patricia Anne Lewis Ft S: Matthew M Fields & Antoinette A Campbell Book/Page: 70972/41, Date: 01/03/25 Use: 2 Bdrm Condo Prior Sale: $2,480,000 (12/24) 100 SHAWMUT AVE U:1101 $938,000

B: Michael Gillespie S: Astharasa Graha LLC Book/Page: 70961/30, Date: 12/31/24

Cross Country Mtg

The information appearing in this newspaper is taken from deed and mortgage documents filed at each of the twenty-one registries of deeds in the state. All property transfers with a sales price of at least $100 and all term-mortgage documents are collected.

Whenever possible, we combine the separate deed and mortgage documents so that we can present one complete record of the street address, purchase price, lender and mortgage amount. When we cannot link a deed with a mortgage (and vice versa) each transaction appears individually.

Real estate records are organized alphabetically by registry, then town, then by street name within a subhead (Real Estate Sales, Foreclosure Deeds, or Mortgages.) The exception is Suffolk Registry and the City of Boston which appear first.

n The statistics at the beginning of each town are for all single-family home sales with a purchase price of $100 and above from January through the most recent complete calendar month.

n The amount appearing on the same line as the street address is the purchase price from the deed. We print “No Amt Given” when the amount did not appear on the document we review. “No Street Given” appears in place of the street address when it was not available. The volume, page of the deed and filing date appear for all sales.

The mortgage lender and the amount of the mortgage used to purchase the property are shown. Any second mortgage (Mtg2) filed at the same time as the deed will also appear here.

n In communities where we have a file of all properties from the assessor’s office, we provide additional property details when available. This is done by exactly matching the address and seller name from the new sales record with the address and owner name found in the property file. No descriptive data appears whenever there is any doubt that the two records are the same property.

The “Use” is based on the code the assessor assigns to each building on a parcel. Whenever there is more than one use code or more than one building on a parcel, we flag these as “Multi-use” and “Multibldg” respectively.

n These deeds transfer title to the lender after the mortgage is foreclosed (unless there is a higher bidder at the auction.) The amount in these transactions is usually the amount of the outstanding mortgage that was foreclosed.

••Year-to-Date (YTD) statistics for all singlefamily home transactions within our price range criteria.

▶ REAL ESTATE SALES 315 MAIN ST U:15. $98,000 Pleasant Towers Condo B:John Doe & Mary Smith S:Jane Jones & Thomas Jones Mtg:Main Street Bank $70,000 Mtg2:Seller $8,400 Prior Sale:$93,000 (11/90)

• The first two buyer (B) names and seller (S) names listed on the deed are shown.

• Prior sale data (back to 1982) appears only when the address of the new sale matches exactly with the address of the older sale in our database.

(08/91)

of 1-Fam Sales 23 24

35-37 CLARK AVE $905,000

B: Rico Tayag S: Deborah Lochiatto

70968/247, Date: 01/02/25 Mtg: Guaranteed Rate Affin $724,000 Term: 2055 Use: 3-Family Family Flat, Lot: 2000sf Prior Sale:

Mtg: MSA Mortgage LLC $1,016,500

2054

3-Family Family Flat, Lot: 2848sf Prior Sale: $1,000 (09/15)

PALMER ST $310,000 B: Jose Cora

S: Beau Development Corp Doc#:

▶ REAL ESTATE SALES

32 ELM ST $175,000

B:John Doe & Mary Smith

S:Jane Jones & Thomas Jones

Mtg:Main Street Mtg Co $140,000

Use:3 Bdrm Colonial, Lot:6459sf Prior Sale:$170,000 (9/89)

• “Use” distinguishes residential homes from land sales and commercial sales.

• For residential homes, the number of bedrooms and house style appear when available.

• The lot size (Lot) is shown in square feet.

▶ FORECLOSURE DEEDS

43 MAIN ST $142,200

B:Main St Bank

S:John Smith & Main St Bank Prior Sale:$190,000 (11/85)

• The prior sale shows the original price paid for the property.

Please note: The information contained in this newspaper is taken from public records. While every precaution is taken, no responsibility is assumed for errors or omissions. Readers should confirm any information before taking action.

Date: 12/30/24

Mtg: Unitas Funding Llc $850,000

Use: Accessory Land Improved, Lot: 4794sf Prior Sale: $310,000 (12/24) Dorchester

MARKET STATISTICS THROUGH NOVEMBER YTD 2023 YTD 2024 Number of 1-Fam Sales 99 96 Median Price $716,000 $722,500

▶ REAL ESTATE SALES

648 ADAMS ST $1,550,000

B: Thuylinh Doan

S: Adams St Prop Mgmt LLC

Book/Page: 70969/270, Date: 01/03/25

Mtg: Fidelity Lending Solu $1,007,500 Term: 2055 Use: 3-Family Decker, Lot: 5657sf Prior Sale: $600,000 (03/15)

65 AUCKLAND ST U:2 $675,000

B: Charles J Horvath 3rd & Daniel G Horvath

S: Gregory M Shirmpton & Meghan E Mcpartlin

Book/Page: 70971/281, Date: 01/03/25

Mtg: Middlesex Svgs Bk $375,000

Term: 2055

Use: 2 Bdrm Condo, Lot: 1250sf Prior Sale: $572,000 (06/19)

56 BAKERSFIELD ST $816,000

B: Eilsabeth Ashforth

S: Miroslaw A Grochal, Tr for Miroslaw A Grochal Ft Book/Page: 70963/330, Date: 12/31/24

Mtg: LoanDepot Com $612,000 Term: 2054

Use: 2-Family Conventional, Lot: 2730sf

805 BLUE HILL AVE $545,000

B: 805 Blue Hill LLC

S: Gerald B Hall & Joyce D Hall

Book/Page: 70963/260, Date: 12/31/24

Mtg: RFLF 4 LLC $710,250 Use: 2-Family Conventional, Lot: 3252sf

60 BOWDOIN AVE $905,000

B: Linh T Tran, Tr for Kevin H Pham

S: Chinenye Udenna & Adedayo Adesogan

Book/Page: 70970/22, Date: 01/03/25

Mtg: Flexpoint Inc $678,750 Term: 2055 Use: 2-Family Conventional, Lot: 5932sf Prior Sale: $750,000 (12/22)

335 EAST ST $1,362,500

B: Jay S Milkiewicz & Hannah Burgress

S: Adam D Burns

Book/Page: 70972/268, Date: 01/03/25

Mtg: JPMorgan Chase Bank $953,750 Term: 2055

34 FAYSTON ST $150,000

B: Family & Developments LLC

S: Ronethia S Williams, Tr for 34 Fayston Street Rt

Book/Page: 70968/128, Date: 01/02/25

Mtg: Onyx Ventures Llc $160,000 Use: 2-Family Conventional, Lot: 3061sf

33 GREENBRIER ST $1,215,000

B: Tu N Vu, Tr for Michael D Tran

S: Marc Abou-Ezzi, Tr for 33 Greenbrier St Rt

Book/Page: 70972/213, Date: 01/03/25

Mtg: Pennymac Loan Service $850,500

Term: 2055

53 LINDEN ST $1,050,000

B: Thuhuong Nguyen & Tuan Nguyen

S: Thanh V Nguyen Book/Page: 70960/88, Date: 12/30/24

Mtg: Champions Funding Llc $840,000

Use: 3-Family Decker, Lot: 1982sf Prior Sale: $69,000 (11/92) 26 MARDEN AVE U:26 $243,539

B: Andy M Perez-Andujar

S: Shasha Baroza-Wade Book/Page: 70959/199, Date: 12/30/24

Mtg: Cooperative Bank $226,904

Term: 2054

Use: 3 Bdrm Condo, Lot: 1623sf Prior Sale: $192,000 (01/17)

41 MELVILLE AVE U:B $675,000

B: Amine Nasr

S: Timothy W Leahy Book/Page: 70953/191, Date: 12/30/24

Mtg: Total Mtg Svcs $472,500

Term: 2054 Use: 3 Bdrm Condo, Lot: 1331sf Prior Sale: $260,000 (07/02)

69 MYRTLEBANK AVE $1,020,000

B: Denis Harrington & Declan Harrington

S: Vlastos George Est & Diane J Capozzoli

Book/Page: 70960/327, Date: 12/31/24

Mtg: Leader Bank NA $867,000 Term: 2054 Use: 2-Family Conventional, Lot: 3600sf

36 NAHANT AVE U:9 $389,900

B: John B Mccarthy

S: Halley Mary M Est & Kathleen Finn Book/Page: 70958/81, Date: 12/30/24

Mtg: OneLocal Bank $311,920

Term: 2054

Use: 2 Bdrm Condo, Lot: 715sf 25 PEVERELL ST U:1 $690,000

B: Thomas Scanlon & Sabrina Brown

S: Philip Anderson & Morgan Callahari

70965/88, Date: 12/31/24

Sale: $505,000 (06/24)

Condo

106 WEBSTER ST U:301 $945,000

B: Carolyn Nevins S: Bcif Trs LLC Book/Page: 70959/133, Date: 12/30/24 Use: Condo

MARKET STATISTICS THROUGH NOVEMBER YTD 2023 YTD 2024 Number of 1-Fam Sales 117 104 Median Price $600,000 $657,500 ▶ REAL ESTATE SALES 113 BELNEL RD $520,000

B: Mildred Arce & Steven Sanchez S: James E Israel & Cynthia D Israel Doc#: 000000000957854, Date: 12/30/24

Mtg: Leader Bank NA $487,215 Term: 2054

Use: 3 Bdrm Cape Cod, Lot: 4601sf

Prior Sale: $40,000 (01/95)

54 OAK ST $875,000

B: Carla Mallqui & Cesar A Rojas S: Jeffrey E Roche, Tr for Julianne E Roche RET Book/Page: 70965/218, Date: 12/31/24

Mtg: Guild Mortgage Co $1,183,708 Term: 2054 Use: 3-Family Conventional, Lot: 16518sf

Prior Sale: $165,000 (10/98)

MARKET STATISTICS THROUGH NOVEMBER YTD 2023 YTD 2024

Number of 1-Fam Sales 54 56

Median Price $1,047,500 $1,186,938

▶ REAL ESTATE SALES

778 BOYLSTON ST U:W4A $1,800,000

B: Jey J Amalraj & Priscilla Amalraj

S: Cwb Apartments L P Book/Page: 70963/12, Date: 12/31/24

Use: Condo

778 BOYLSTON ST U:W5C $1,842,000

B: D&d Reside Boston LLC

S: Cwb Apartments L P Book/Page: 70965/53, Date: 12/31/24

Mtg: Cross Country Mtg Inc $1,381,500 Term: 2054 Use: Condo

8 JESS ST $770,000

B: Katherine E Slyman & Anthony L George

S: Jeremy Phillips Book/Page: 70955/104, Date: 12/30/24

Mtg:

Richard C Henderson & Audrey D Henderson Book/Page: 70964/49, Date: 12/31/24

L

Use: 3-Family Conventional, Lot: 3292sf Prior Sale: $926,100 (11/19) 4-6 HARLEM ST $600,000

Lot: 5456sf