Members of IEA’s Task 39 group recently discussed the SAF industry’s 2024 development and status.

BY KATIE SCHROEDER

18 FEEDSTOCK Feedstock State of Affairs

Surging biomass-based diesel feedstock demand has led to a boom in used cooking oil imports, adding to U.S. soybean oil’s struggles.

BY SUSANNE RETKA SCHILL

26

PROJECT

DEVELOPMENT Mapping the Buildout

Biodiesel Magazine reviews the recently completed 2025 Biodiesel, Renewable Diesel & SAF map, providing updates for industry development across the U.S. and Canada.

BY ANNA SIMET

Current barriers to higher biomass-based diesel blends have been identified, along with strategies to address them.

ROBERT MCCORMICK

Advertiser Index

2025

Carbis Solutions Group, LLC

Clariant Corp.

Clean

BiodieselMagazine.com

PUBLISHING & SALES

Joe Bryan

Tom Bryan

John Nelson

Anna Simet

Erin Voegele

Katie Schroeder

Chip Shereck

Bob Brown

Jessica Tiller

Marla DeFoe

CEO jbryan@bbiinternational.com

President tbryan@bbiinternational.com

Vice President of Operations/ Marketing & Sales jnelson@bbiinternational.com

Vice President, Production & Design jsatterlund@bbiinternational.com

Graphic Designer rboushee@bbiinternational.com

Subscriptions Subscriptions to Biodiesel Magazine are free of charge to everyone with the exception of a shipping and handling charge for any country outside the United States. To subscribe, visit www.biodieselmagazine.com or send a mailing address and payment (checks made out to BBI International) to: Biodiesel Magazine Subscriptions, 308 Second Ave. N., Suite 304, Grand Forks, ND 58203. Reprints and Back Issues Select back issues are available for $3.95 each, plus shipping. Article reprints are available for a fee. For more information, contact us at 701-746-8385 or service@bbiinternational.com. Advertising Biodiesel Magazine provides a specific topic delivered to a highly targeted audience. We are committed to editorial excellence and high-quality print production. To find out more about Biodiesel Magazine advertising opportunities, please contact us at 701-746-8385 or service@bbiinternational.com. Letters to the Editor We welcome letters to the editor. Please include a name, address and phone number. Letters may be edited for clarity and/or space. Send to Biodiesel Magazine Letters, 308 Second Ave. N., Suite 304, Grand Forks, ND 58203 or email asimet@bbiinternational.com.

2025 International Biomass Conference & Expo MARCH 18-20, 2025

Atlanta, GA (866) 746-8385 | www.biomassconference.com

Now in its 18th year, the International Biomass Conference & Expo is expected to bring together more than 900 attendees, 160 exhibitors and 65 speakers from more than 25 countries. It is the largest gathering of biomass professionals and academics in the world. Powered by Biomass Magazine, the conference provides relevant content and unparalleled networking opportunities in a dynamic business-to-business environment. In addition to abundant networking opportunities, the largest biomass conference in the world is renowned for its outstanding programming, maintaining a strong focus on commercial-scale biomass production, new technology, and near-term research and development. Join us at the International Biomass Conference & Expo as we enter this new and exciting era in biomass energy.

2025 International Fuel Ethanol Workshop & Expo

June 9-11, 2025

Omaha, NE

(866) 746-8385 | www.fuelethanolworkshop.com

Now in its 41st year, the FEW provides the ethanol industry with cutting-edge content and unparalleled networking opportunities in a dynamic business-to-business environment. As the largest, longest running ethanol conference in the world, the FEW is renowned for its superb programming—powered by Ethanol Producer Magazine—that maintains a strong focus on commercialscale ethanol production, new technology, and near-term research and development. The event draws more than 2,300 people from over 31 countries and from nearly every ethanol plant in the United States and Canada.

2025 Sustainable Fuels Summit June 9-11, 2025

Omaha, NE

(866) 746-8385 | www.sustainablefuelssummit.com

The Sustainable Fuels Summit: SAF, Renewable Diesel and Biodiesel is a premier forum designed for producers of biodiesel, renewable diesel, and sustainable aviation fuel (SAF) to learn about cuttingedge process technologies, innovative techniques, and equipment to optimize existing production. Attendees will discover efficiencies that save money while increasing throughput and fuel quality. Produced by Biodiesel Magazine and SAF Magazine, this worldclass event features premium content from technology providers, equipment vendors, consultants, engineers, and producers to advance discussions and foster an environment of collaboration and networking. Through engaging presentations, fruitful discussions, and compelling exhibitions, the summit aims to push the biomassbased diesel sector beyond its current limitations. Colocated with the International Fuel Ethanol Workshop & Expo, the Sustainable Fuels Summit conveniently harnesses the full potential of the integrated biofuels industries while providing a laser-like focus on processing methods that deliver tangible advantages to producers. Registration is free of charge for all employees of current biodiesel, renewable diesel, and SAF production facilities, from operators and maintenance personnel to board members and executives.

Please recycle this magazine and remove inserts or samples before recycling

It’s nearly a month post-election, and speculation is ongoing regarding the fate of Biden-enforced climate and clean energy policy, programs and funding under a Republican president and a Republican-controlled House and Senate. Though industry is always wise to brace for the worst, considering the Inflation Reduction Act alone, the vast majority of money spent has been in Republican-controlled districts. According to a recent report by E2, red states and Republican congressional districts are benefitting the most from the IRA. Despite the fact that no Republicans voted for it, to date, more than half of all projects have been in Republican districts, and 19 of the top 20 congressional districts for clean energy investments are held by Republicans. On top of that, according to the report, “Nearly 60% of the announced projects—representing 85% of the investments and 68% of the jobs—are in Republican congressional districts.”

It’s wait-and-see for now, but be sure to visit biodieselmagazine.com to listen to a recent podcast during which I chatted with Paul Winters, director of public affairs and federal communications at Clean Fuels Alliance America, about the road ahead. Winters will be a general session presenter at the International Biomass Conference & Expo in March, and by then, there will be much to discuss when it comes to the aforementioned.

As for the stories in this issue, in our page-18 feature, “A Feedstock State of Affairs,” freelance writer Susanne Retka Schill investigates the largely unforeseen surge in Chinese used cooking oil, and how those imports, massive feedstock appetites of renewable diesel facilities, and California’s Low Carbon Fuel Standard carbon-intensity scoring has impacted soybean oil’s share in biomass-based diesel production. Soybean oil use has been increasing, says Scott Gerlt, American Soybean Association chief economist, but not to the expected utilization levels. “We’ve been building out domestic crush plants to provide more soybean oil,” he tells Retka Schill, “and we have seen more use, but are concerned about underutilization of oncoming assets.”

Some of the renewable diesel facilities he references are featured in our page-26 article, “Mapping the Buildout,” on page 26. Much of the information for this story was drawn from our recently completed 2025 U.S. & Canada Biodiesel, Renewable Diesel & SAF Map. For example, in early November, Imperial Oil confirmed that its renewable diesel project under construction at the company’s Strathcona refinery near Edmonton, Alberta, continues to progress on schedule with startup expected during the first half of next year. The company completed a coprocessing project in the third quarter of 2024, which will allow the facility to coprocess plant-based feedstocks.

By the summer edition of Biodiesel Magazine, we’ll have a clearer view of what’s in store for the broader biofuel industry in terms of policy and support changes. We’ll be keeping our finger on the pulse of things, so be sure to follow our daily news stories, weekly newsletter and podcast, and attend the International Biomass Conference & Expo and Sustainable Fuels Summit to educate yourself on the events that impact our industry as they unfold.

News Roundup

Greasezilla, bp Enter Strategic and Financial Agreement

Downey Ridge Environmental Co. (Greasezilla) and bp announced an agreement that will enable the capture and extraction of brown grease waste as a feedstock for biofuel production. As part of the agreement, bp will finance the expansion of Greasezilla's production facilities to support the delivery of brown grease feedstock to the market, aimed at furthering the renewable diesel (RD) and sustainable aviation fuel (SAF) markets.

Clean Fuels Alliance Elects New Board Members

Clean Fuels Alliance America members announced the election of new leadership to reflect the interests of both large and small companies, biodiesel and renewable diesel producers, as well as soybean growers and renderers. Clean Fuels members voted to fill eight board seats for two-year terms: Greg Anderson, Nebraska Soybean Board; Bob Haselwood, Kansas Soybean Commission; Tim Keaveney, Hero BX; Courtney Lawrenson, Ag Processing Inc.; Peter Ostenfeld-Rosenthal, Seaboard Energy LLC; Tim Ostrem, United Soybean Board; Rob Shaffer, American Soybean Association; and Paul Teta, Kolmar Americas Inc.

Continuing to serve on the board for a second year are: Kent Engelbrecht, ADM; Neville Fernandes, Chevron Renewable Energy Group; Kerry Fogarty, Incobrasa Industries Ltd; Chris Hill, Minnesota Soybean Research & Promotion Council; Ryan Pederson, North Dakota Soybean Council; Harry Simpson, Crimson Renewable Energy; and Dave Walton, Iowa Soybean Association.

The agreement includes the funding of up to 40 new FOG receiving stations with up to $5 million per site, using proprietary Greasezilla technology. Any subsequent phases will focus on expanding production capacity and further developing the technology to maximize efficiency and environmental benefits, according to Downy Ridge Environmental.

The board appointed Kent Engelbrecht to serve as chair, Rob Shaffer as vice chair, Courtney Lawrenson as second vice chair, Ryan Pederson as treasurer, Paul Teta as secretary, and Mike Rath as immediate past chair.

New Projects to Help Create Great Lakes

Green Shipping Corridor

The Hamilton Oshawa Port Authority welcomed the announcement of two transformative projects supported by Transport Canada’s Green Shipping Corridors Fund, marking a significant step forward in sustainable marine transportation on the Great Lakes.

The Port Colborne Marine Biofuel Terminal is a new 12-acre, 8-million-liter (2.1-million-gallon) biofuel terminal in Port Colborne, Ontario. The $33 million project, supported by $13.8 million in federal funding, represents a partnership between HOPA Ports, Canada Clean Fuels and Canada Steamship Lines. At full capacity,

the facility will distribute up to 70 million liters of biodiesel annually, sufficient to fuel more than 100 vessels per year. The project is expected to reduce greenhouse gas emissions by approximately 144,000 metric tons by 2030 and 2.8 million metric tons over the facility’s lifetime.

HOPA Ports’ partner, Sterling Fuels, also received funding to modify existing infrastructure and construct additional vessel fueling facilities at the Port of Hamilton. The $4 million project, supported by $2 million from the Green Shipping Corridors Program, will add two tanks to Sterling Fuels’ existing Hamilton facility, as well as the associated pumps and piping to allow Sterling Fuels to receive, store and deliver biofuels. These strategic improvements, in conjunction with improved capabilities in Windsor, will allow Sterling Fuels to meet its customers’ future demand for biofuels

Iowa Celebrates Record Biodiesel Sales

The Iowa Biodiesel Board is celebrating a milestone in the adoption of biodiesel blends, with sales in 2023 reaching 486.5 million gallons. This is nearly triple from the 160.8 million gallons recorded in 2007, according to the IBB, which said the news comes from the state’s new Biofuel Tax Credits Program Evaluation Study, published by the Iowa Department of Revenue.

State incentives, including a producer’s credit, a fuel tax differential and a retailer’s credit for sales of 30% biodiesel and above (the nation’s first), played a critical role in this success, the IBB said. These incentives offer financial support to retailers who sell biodiesel blends, effectively making biodiesel more accessible across Iowa and helping drive a significant increase in biodiesel’s share of Iowa’s diesel market. In 2007, biodiesel blends accounted for 22.6% of total diesel sales in Iowa; today it represents 58.7%, according to the IBB.

Florida Man Pleads Guilty to Biodiesel Fraud Conspiracy

A Florida man pleaded guilty on Nov. 7 for his role in a scheme that generated over $7 million in fraudulent U.S. Environmental Protection Agency renewable fuels credits and sought over $6 million in fraudulent tax credits connected to the purported production of biodiesel, according to the U.S. Department of Justice.

According to court documents, Royce Gillham was the general manager of a biofuel company based in Fort Pierce, Florida, that produced and sold renewable fuel and fuel credits and claimed to turn various feedstocks into biodiesel. When reporting the number of gallons produced to the IRS and U.S. EPA, Gillham and his employer vastly overstated their production volume in an effort to generate more credits. When auditors sought more information from the company, Gillham and his coconspirators provided false information about their fuel production and customers.

Gillham pleaded guilty to conspiring to commit wire fraud and to filing false claims. A sentencing date has not yet been scheduled. He faces a maximum penalty of five years in prison and a $250,000 fine for the conspiracy count.

UK SAF Mandate Signed Into Law

The U.K.’s sustainable aviation fuel (SAF) mandate was signed into law on Nov. 18 and is set to come into force on Jan. 1. The government has also launched a new Jet Zero Taskforce.

The U.K. first announced plans to implement a SAF mandate in mid-2021. In 2023, the Department of Transport opened a public comment period on a proposed SAF mandate, and earlier this year, the government confirmed plans to move forward.

The finalized SAF Mandate will require 2% SAF beginning in 2025, ramping up to 22% by 2040. Hydroprocessed esters and fatty acids will be allowed to contribute up to 100% of SAF demand in 2025 and 2026, decreasing to 71% in 2030 and 35% in 2040. A requirement for SAF produced via power-to-liquid technology will be introduced starting in 2028 at 0.2% of total jet fuel demand, increasing to 2.5% of total jet fuel demand in 2040.

The Jet Zero Taskforce builds on the previous Jet Zero Council and aims to support the production and delivery of SAF and zero-emission fuels, as well as look at how to improve aviation systems to make them more efficient. It will include high-level government officials along with the CEOs of major airlines, such as easyJet and Virgin, airports like Heathrow and Manchester, as well as fuel producers, trade bodies and leading universities.

USDA Revises Forecast for Soybean Production, Yields

The USDA released its latest Crop Production report on Nov. 8, reporting reduced forecasts for 2024 soybean production and yields. However, both production and yields are up significantly when compared to last year.

According to the agency, soybean production for beans is forecast at 4.46 billion bushels, down 3% from last month but up 7% when compared to 2023. Based on conditions as of Nov. 1, yields are expected to average 51.7 bushels per acre, down 1.4 bushels from the previous forecast but up 1.1 bushels from last year. Area harvested for beans in the U.S. is forecast at 86.3 million acres, unchanged from the previous forecast but up 5% from 2023.

Aemetis India Completes $103 Million in Biodiesel Deliveries in 2024

Aemetis announced that its Universal Biofuels subsidiary in India successfully completed delivery of $103 million of biodiesel to the three government-owned Oil Marketing Companies under cost-plus supply agreements for the one-year marketing period ending Sept. 30, 2024.

Aemetis recently received an initial $58 million of new allocations from OMCs for biodiesel supply in the current marketing year ending September 30, 2025, and has been producing biodiesel for deliveries scheduled to begin this month. The first allocation of biodiesel deliveries for the current year was issued by the OMCs in late November 2024 and the pricing for the deliveries will be based on a cost-plus pricing formula. Multiple tenders were issued during the last supply year ending September 30, and multiple tenders are expected again in the current year, according to Aemetis.

TONSIL™

TONSIL™ your solution for oils, fats, and greases. Enhance your refining process with state-of-the-art purification and targeted impurity removal, while safeguarding your catalyst for advanced protection and optimal e ciency in your operations.

Energy Transloading Experts

PODCAST PREVIEW

WITH JOHN WORRELL, FILTRATION TECHNOLOGY CORPORATION

Season 2, Episode 1, of the SAF Magazine/Biodiesel Magazine podcast features John Worrell, vice president of sales at Filtration Technology Corporation, a leader in filtration and separation systems. During the podcast, Worrell discusses the design, features and application of the company’s Invicta liquid-solids filter cartridges.

Q: Tell us about Filtration Technology Corporation.

Worrell: FTC is a Houston-based filtration company, specializing in high-efficiency pleated medias in four primary categories—those being liquid-solids separation, gas-solids filtration, liquid-liquid separation and gas-liquid separation. The company was founded by John Hampton in 1987, specializing in the oil and gas industry, and subsequently has grown to more downstream processes, including gas treatment, refining and even food and beverage.

Q: FTC changed the shape of traditional cylinder filters. Why did the company do that?

Worrell: First of all, it’s important to understand that filter performance can be directly tied to usable surface area. All things being equal, the more usable surface that you have in a given system, the more dirt a filter will hold, and the higher efficiency a filter will have at removing a given contaminant size. This can be proven via Darcy’s Law, which we use to calculate flow through any porous media. We know according to Darcy’s Law, that dirt-holding capacity is indirectly proportional to flux rate, or flow per unit area. So, the more surface area that a cartridge has, the more contaminants a cartridge can hold. Over the years, many traditional cylinder cartridge designs have been modified to try to pack as much surface area as you can get into a given cylindrical cartridge. And that’s been done through increased pleat count, tighter pleat spacing, putting taller pleats in a cartridge, or even staggering the pleat heights, which we call W pleats, in diameters ... all in order to maximize the amount of surface area in a given cartridge ... So, there has been a

PLAY

lot of variations in cartridge diameters ... in the attempt to try to improve the amount of surface area in a given housing. Now, there is a problem with the cylindrical design, and it’s that all things being equal, your pleats will also be spaced tighter at the ID than they are at the OD. This can result in a partial use of the surface area at the ID, because the pleats get so close together that the dirt does not quite penetrate down into the ID of the cartridge—we call that tip loading. In other words, the contaminate doesn’t fully load throughout the surface area of the cartridge, so therefore, you pay for surface area that you don’t fully utilize ... subsequently, with cylindrical designs, you can only get so many cartridges in a given vessel design no matter what diameter you use, because you can only fit so many circles within a circle. Therefore, you have wasted space in the vessel. This is where the Invicta design comes in—we’ve solved two fundamental problems.

Listen to the full podcast by tuning in at www.biodieselmagazine.com/pages/podcasts

John Worrell

SAF FLYOVER

The IEA’s Task 39 group has new research regarding the development and status of the sustainable aviation fuel industry.

BY KATIE SCHROEDER

Considering the onslaught of sustainable aviation fuel (SAF) project and offtake agreement announcements, companies highlighting their unique conversion technologies, and varying assessments of where the industry is and must be to reach incremental goals, it can be difficult to assess what stage of development the industry has actually reached. To address this, researchers with the International Energy Agency’s (IEA) Task 39 released a report on the state of SAF production and availability in Q1 of 2024.

Jack Saddler, professor emeritus at the University of British Columbia, and Susan van Dyk, research associate with the University of British Columbia, shared the report’s findings during an October webinar.

Saddler discussed Canadian—and specifically, British Columbian—efforts to address climate change through programs such as the BC-Sustainable Marine, Aviation, Rail and Trucking Fuels Consortium (BC-SMART), while van Dyk explained the pros and cons of different SAF production pathways, vari-

ous technologies’ commercialization statuses, policy’s role in the industry’s buildout, and progress made thus far in displacing fossilbased jet fuel.

SAF has a key role to play in reducing aviation emissions, constituting 65% of the total emissions reductions needed to reach net zero by 2050, van Dyk explained. A volume of 400 billion liters (approx. 105.6 billion gallons) must be produced annually to reach net zero, but current production levels are still below 1% of the volume needed by 2050, she said.

It may seem that SAF is moving forward by leaps and bounds. As according to the International Civil Air Organization, there are 337 SAF production facilities that are announced, under construction or operational, and a total of 127 airports have distributed SAF and signed offtake agreements for 53 billion liters (approx. 14 billion gallons) of fuel. However, van Dyk cautioned against an overly optimistic view of these numbers, because many of the facilities may not be completed, and offtake agreements are essentially a memorandum of understanding with the purpose of help-

ing SAF production facilities obtain funding. Though hundreds of projects have been announced, data indicates that it is likely many of the projects will fail, with the success percentages ranging from 25% to 50%. “Not all these companies will succeed, that’s just the reality,” van Dyk said.

Understanding Timelines

A total of 11 technology pathways are approved for SAF production, including the hydrotreated esters and fatty acids process (HEFA), alcohol-to-jet process, FischerTropsch and others. “I think what people forget sometimes is that ASTM approval does not mean that the technology is commercial or that the fuel produced will be sustainable— ASTM is only concerned with the safety aspect,” van Dyk said.

These pathways do not all offer the same degree of sustainability benefits or possess the same level of commercial viability. “When we [anticipate] how fast technologies are going to become commercial, and how quickly we will see production and expansion, HEFA is

still the only fully commercial technology,” she said. “And it’s generally agreed that by 2030, the majority of SAF will come from HEFA.”

However, the limited volume of waste fats and oils requires other technologies to fill in the gap, and many of these technologies are not going to be able to scale up in time, according to van Dyk. She explained that people overestimate how quickly these technologies will move through technology readiness levels (TRL) and reach fully commercial stage. Moving through each of the nine TRL stages takes two to three years. “[If] a company is only at pilot scale, that should tell you that, realistically, it’s going to be years before they reach commercial scale—regardless of what they try to tell you, it will take time,” she said. For example, even after permitting, financing and construction are complete, it may take a company an entire year of commissioning before the plant runs at full capacity. Average construction times for SAF facilities using complex technologies like gasification stand at around five years.

Many investors are wary of new SAF technologies because they remain a high-cost, high-risk investment. At conferences, investors have communicated that they are waiting for the first project to prove itself and succeed before they jump onboard, van Dyk explained.

Overly optimistic scaling is another issue. Companies with novel SAF technologies may announce plans to jump from pilot plant up to a 200- to 400-liter facility, but that speed of scaling may be problematic. Van Dyk provided the example of Fulcrum BioEnergy, a plant that turned municipal solid waste into ethanol and then SAF, explaining that some within the industry believed that the 40-million-liter plant scaled up too soon. When looking at the data, it appears unlikely that the U.S. and European Union will be able to achieve 2030 goals. “We have to be realistic,” she said. “Things are going to [be] slower than we think. And the reality is that the targets are so ambitious that meeting these SAF targets will be extremely challenging.”

Sourcing Challenges

Supply chains for forest and agricultural residues are nonexistent, which is a problem, van Dyk explained. It is easy for feedstocks and supply chains to be a “forgotten critical issue” when understanding a technology’s potential. Many of the lowest-carbon-intensity feedstocks also have the lowest energy density and are the most spread out geographically, making an efficient, cost-effective supply chain crucial. Agricultural supply chains exist, but they are not designed for transporting lowenergy feedstocks such as crop residues, which also are not economical to transport over long distances, van Dyk explained. Because of this, the feedstock must be located near the biorefinery, which may cause difficulties when trying to position the fuel source near a large airport.

SAF Percentages

When hearing about a new SAF project, those interested in the progress of the SAF industry must keep in mind that 95% of technologies actually produce varying ratios

of SAF alongside other fuels, including renewable diesel and light ends such as naphtha (which can be converted into gasoline). “Some companies say that they’re going to produce SAF because this is sort of the buzzword,” van Dyk said. In reality, she explained, these facilities determine how much of which fuel they would like to produce depending on the economic advantage it provides. Choosing to produce a higher ratio of jet fuel requires them to add more processing equipment, making the process more expensive, thus lowering a plant’s incentive to produce SAF.

Misconceptions about the total capacity of a SAF plant can lead to an overestimation of the total volume of SAF being produced, van Dyk said. Several factors make HEFA a more attractive process for producing renewable diesel rather than SAF. A HEFA refinery initially produces 15% SAF, but that could be increased to 50% or more with extra investment. However, increasing a facility’s ratio of SAF to over 50% of total volume reduces overall yields of liquid fuels by 10% and requires the addition of second hydrocracker, van Dyk said. “Not only do you have a bigger investment and it’s more expensive, but you also have a lower yield of valuable liquid hydrocarbon products,” she said. “SAF production from HEFA biorefineries is not favorable economically unless there are additional policy drivers.” Currently, U.S. policy offers higher tax credits for renewable diesel, which may disin-

centivize SAF production. However, there are other pathways attracting attention from project developers, policymakers and investors.

Ethanol: Crop or Cellulosic?

The alcohol-to-jet (ATJ) pathway, frequently discussed with ethanol as the feedstock, is another production method that has garnered attention due to projects such as LanzaJet’s Freedom Pines facility in Soperton, Georgia. Usage of sugarcane ethanol as a feedstock for the ATJ process constitutes a “low-hanging fruit,” explains van Dyk. The United Kingdom and EU do not recognize crop-based ethanol’s potential, requiring ATJ SAF to be derived from cellulosic sources. “If you look at technoeconomic analyses for SAF from cellulosic ethanol, the minimum selling price is more than double that of corn ethanol-to-jet,” van Dyk said. Price is not the only problem; cellulosic ethanol has not attained widespread commercial production. Van Dyk explained that since the first cellulosic ethanol project started in 2013, most projects have failed or only attained limited success due to a variety of factors.

One of the challenges is the large-scale storage required for the massive amounts of residue required to operate throughout the year. Van Dyk referenced a technoeconomic analysis that stated a 200-million-liter facility would need a total of 2 million bales stored. When stored for long periods of time, crop

residue tends to degrade, impacting process yields. She highlighted the efforts of Idaho National Laboratory in seeking solutions for the degradation problem, explaining that their research is “substantial” in eliminating the challenges preventing widespread commercialization.

Crop-based ethanol does not face these feedstock problems and is already being widely produced. “With alcohol-to-jet, we have the potential opportunity to use crop-based ethanol to prove all these different technologies,” she said. “And the other benefit with ethanol is that because it’s a high-density intermediate ... it can be transported over long distances, which is already happening.”

Fischer-Tropsch Complications

The Fischer-Tropsch process begins with gasification of biomass into syngas, which then goes through Fischer-Tropsch synthesis, followed by hydrotreating/hydrocracking. The closure of the first commercial FischerTropsch refinery, Fulcrum BioEnergy, will have a negative impact on commercializing this technology because it highlights the challenges faced by this process, van Dyk explained. Feedstock complexity was the major problem for the defunct facility, with some reports citing buildup of a “cement-like substance meters deep in the gasifier” and formation of corrosive nitric acid, she said.

Feedstock challenges are a significant barrier to commercializing Fischer-Tropsch SAF. “You get the tar formation and contaminants, the syngas cleanup is expensive because of the oxygen in the biomass, and you get a very low hydrogen-to-carbon ratio,” van Dyk said. “You have very low feedstock density, so transportation costs are expensive, and you have to build the facility closer to the feedstock. There are all these project challenges because these feedstocks haven’t previously been used.”

The syngas conversion portion of the process is commercialized, but for biomassbased Fischer-Tropsch SAF projects, the challenge lies in the feedstock. Van Dyk explains that the process is proven commercially when natural gas is used as the feedstock, but biomass and waste sources present a challenge due to ash content and processing.

Power-to-Liquids

The power-to-liquids process utilizes carbon dioxide—collected through direct air capture or point source capture—and employs the water-gas shift reaction to make carbon monoxide (CO). After that CO is combined with hydrogen produced via electrolysis using water and renewable electricity, a syngas is created. The syngas can be upgraded to SAF through a Fischer-Tropsch synthesis or methanol synthesis. This pathway is a favorite in the

EU, which has a current mandate requiring 600 million liters of eSAF by 2030, but meeting this goal is unlikely, according to van Dyk. “While there’s been a lot of announcements of power-to-liquids companies, most are not at final investment decision stage and, ... if you look at that seven-year timeframe, it’s going to be very, very difficult to get that,” she said. Although elements of the process such as electrolysis and Fischer-Tropsch are commercial, CO2 capture is not widely proven and the water-gas shift reaction is still at a lower TRL.

Renewable electricity is in high demand, and supplies are strained as electricity usage for EV charging, heating, decarbonizing the grid and other applications increases. Van Dyk referenced a McKinsey study that found 36 megawatts per hour are needed to make one ton of efuel; that number increases to roughly 1.1 terawatts of electricity per 50,000 tons of efuels when direct air capture (an energy-intensive technology) is used to collect the CO2 needed.

The draw of this technology is its “theoretically unlimited potential,” according to van Dyk, and it could be a good solution if the price of renewable electricity drops significantly.

Flying Forward

With the current goals set by govern-

ments and organizations around the world, there is still a tremendous amount of work to be done before these goals will be achievable. Overcoming the cost differential is vital, according to van Dyk. Currently, HEFA-produced SAF costs over $2,000 per ton, while conventional jet fuel costs about $700 per ton. That significant gap must be addressed via long-term policies to push these production technologies toward commercialization by derisking investment.

“We’re going to see a higher cost of producing SAF for a long, long, time,” she said. “We have limited availability of feedstocks and there’s limited investment. I think companies will tell you there’s a lot of funding out there, but the problem is that it is still very high risk because these technologies have not been proven yet.”

Stable policy will help derisk investment to improve commercialization, but moving a technology from pilot to full commercialization will take time. “A country might say, ‘Okay, we want 10% by 2030,’” van Dyk said. “But that is just an ambition until there are policies put in place to actually achieve that.”

Surging biomass-based diesel feedstock demand has led to a boom in used cooking oil imports, and when combined with current policy mechanisms, U.S. soybean oil is at a disadvantage.

BY SUSANNE RETKA SCHILL

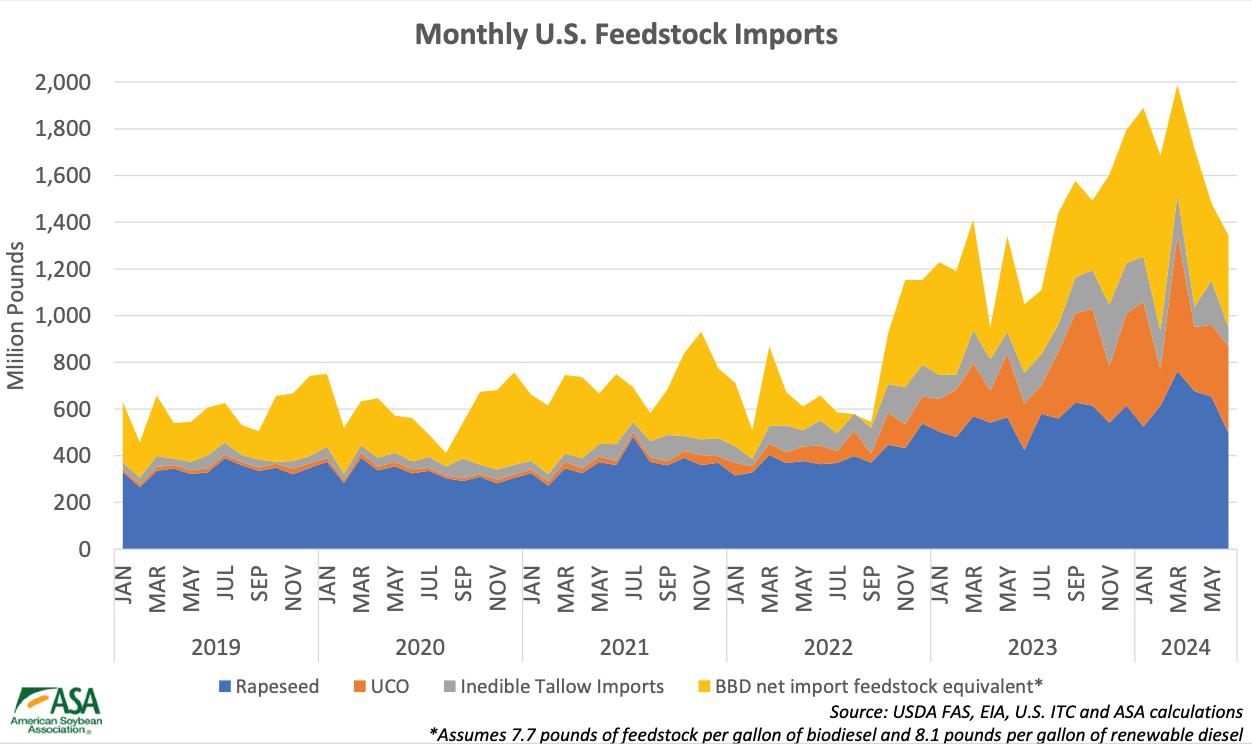

Imports of used cooking oil (UCO) and tallow have exploded, paralleling the rapid increase in renewable diesel (RD) capacity and production. Renewable diesel capacity grew from approximately 859 million gallons at the end of 2020 to 3.86 billion gallons in 2023, with production more than doubling, reports the USDA’s Economic Research Service in its analysis, “Oil Crops Outlook: July 2024.” Imports of animal fats (tallow and poultry fat) and greases (including used cooking oil) doubled in one year from 2.2 billion pounds in 2022 to 5 billion pounds in 2023, which accounted for just under half of the total 11.9 billion pounds of animal fats, waste oils and greases used for biofuel production in 2023. Imports from China in particular raised eyebrows, as they rose from zero in 2021 to 1.5 billion pounds in 2023, comprising over half of all imported fats, oils and grease (FOG).

Questions quickly arose to whether the Chinese UCO could be adulterated with

virgin palm oil. The jury is out on that claim, however. The issue first surfaced in Europe in early 2023. In its August 2024 annual “EU Biofuels” report, the USDA Foreign Agricultural Service says widespread concerns about mislabeling and fraud of UCO biodiesel from China “led to investigations, albeit so far without conclusive results.” The International Sustainability and Carbon Certification responded to the claims of potential fraud with unannounced audits, resulting in seven certificates being suspended or withdrawn. “However, the sanctions of these seven economic operators did not conclusively indicate criminal behavior,” the ISCC reports

on its website.

In the U.S., a June letter from a bipartisan group of six senators, led by Sen. Roger Marshall, R-Kansas, to multiple federal agencies expressed concern with the dramatic increases in UCO imports from China that may be a blend of UCO with virgin oil. They noted that domestic sources of UCO are held to rigorous verification and traceability requirements, but expressed concern with the lack of transparency surrounding U.S. efforts to verify imported UCO.

Replying to emailed questions, EPA says that contrary to some media reports, “the referenced investigations were routine Renewable Fuels Standard inspections

Post a Job Reach Workers

Donnell Rehagen, Clean Fuels Alliance America

Scott Gerlt, American Soybean Association

chemical analyses producers use to ensure compatibility with their process “are effective at identifying feedstocks like virgin vegetable oil, which are not used cooking oil.” Such analyses are not definitive, however, and testing techniques are still a developing field of analytical science.

Feedstock Challenge

Raising the question of imported UCO with industry spokesmen quickly shifts to a broader discussion of the feedstock challenge. It’s not just about UCO imports, but all the feedstocks that play in the mix for biomass-based diesel fuels (BBD), says Donnell Rehagen, CEO of the Clean Fuels Alliance America.

that evaluate all aspects of the companies’ compliance.” Declining to provide details on ongoing investigations, the agency’s spokesperson says direct oversight is largely supported by records that must be audited by independent third parties annually. EPA also inspects facilities and reviews the records of renewable fuel producers.

Asked about the challenge in verifying the authenticity of UCO, EPA says the

Biodiesel, renewable diesel and (eventually) sustainable aviation fuel production, all pull from the same pool fed by five feedstock supplies, he says, which just isn’t large enough. Using all the domestic feedstocks combined, he says, would produce between 3 billion and 3.8 billion gallons of BBD.

That’s figuring in about half the soybean oil crush (with the other half bound for food use) plus all of the domestic animal fats, distillers corn oil and canola oil—which, he adds, is unrealistic because those feedstocks have other uses as well. “We’re a 5 billion gallon industry—where does the rest come from?”

The growth in BBD capacity is virtually all renewable diesel, with the biodiesel industry’s capacity in the 2-billion- to 2.5-billion-gallon range. RD capacity is expected to continue to grow, Rehagen adds, to about 4 billion gallons next year. “These are massive plants—700 MMgy plants. We have very few biodiesel plants that are even 70 MMgy.

“One of the logistical challenges that RD producers have when they scale like that is they need a massive amount of feedstock every single day,” Rehagen continues. “We are the largest consumer of soybean oil in the U.S.; we use a little more than food. We use everything that’s available, but we have needs beyond that. And when you think about it, these RD plants are not ideally located to bring in soybean oil or canola oil.”

Most of the largest RD facilities are retrofitted oil refineries located on West Coast and Gulf ports, he points out, and thus, logistically situated to handle imports.These RD facilities are using as much feedstock in one day as some of our biodiesel plants use in a year, Rehagen says. “That’s not a knock on biodiesel at all, it’s just the reality of how those plants have come online. They are massive consumers of feedstocks, and they need to have it every day. That’s where the challenge has become trying to balance their needs to produce at the levels they need to, with the availability and logistics of all the domestic feedstocks. You throw on top of that LCFS [low carbon fuel standard] markets like the one in California, and that distorts everything.”

The LCFS has created impressive demand for renewable fuels, Rehagen adds. “It’s a 3 or 4 billion-gallon-a-year diesel market and almost three-fourths is now biodiesel and renewable diesel. It’s a massive amount flowing into California.”

Policy Distortions

The distortion Rehagen refers to comes from how various fuels earn valuable carbon credits under the California Low Carbon Fuel Standard. All transportation fuels are scored for carbon intensity (CI) based on the greenhouse gas emissions associated with producing, distributing and consuming the fuel, which includes feedstock data. Fuels scoring above the standard for the year must buy credits from fuels with lower CI scores. Averaging all the pathways scored in California’s LCFS, renewable diesel from soy scores around 57 gCO2g/MJ compared to 23.7 g for RD from UCO. “A renewable diesel or biodiesel producer wanting to access this California market has reason to buy the lowest-CI feedstock they can get their hands on because they can make more money,” Rehagen says. “The top of the heap in California is UCO, and works its way down through animal fats, distillers corn oil, soybean oil and canola oil. It has this distorting effect on feedstock. The largest supply is soy oil, but unfortunately under the California’s low CI program, it’s the least valuable feedstock for a fuel going into California.”

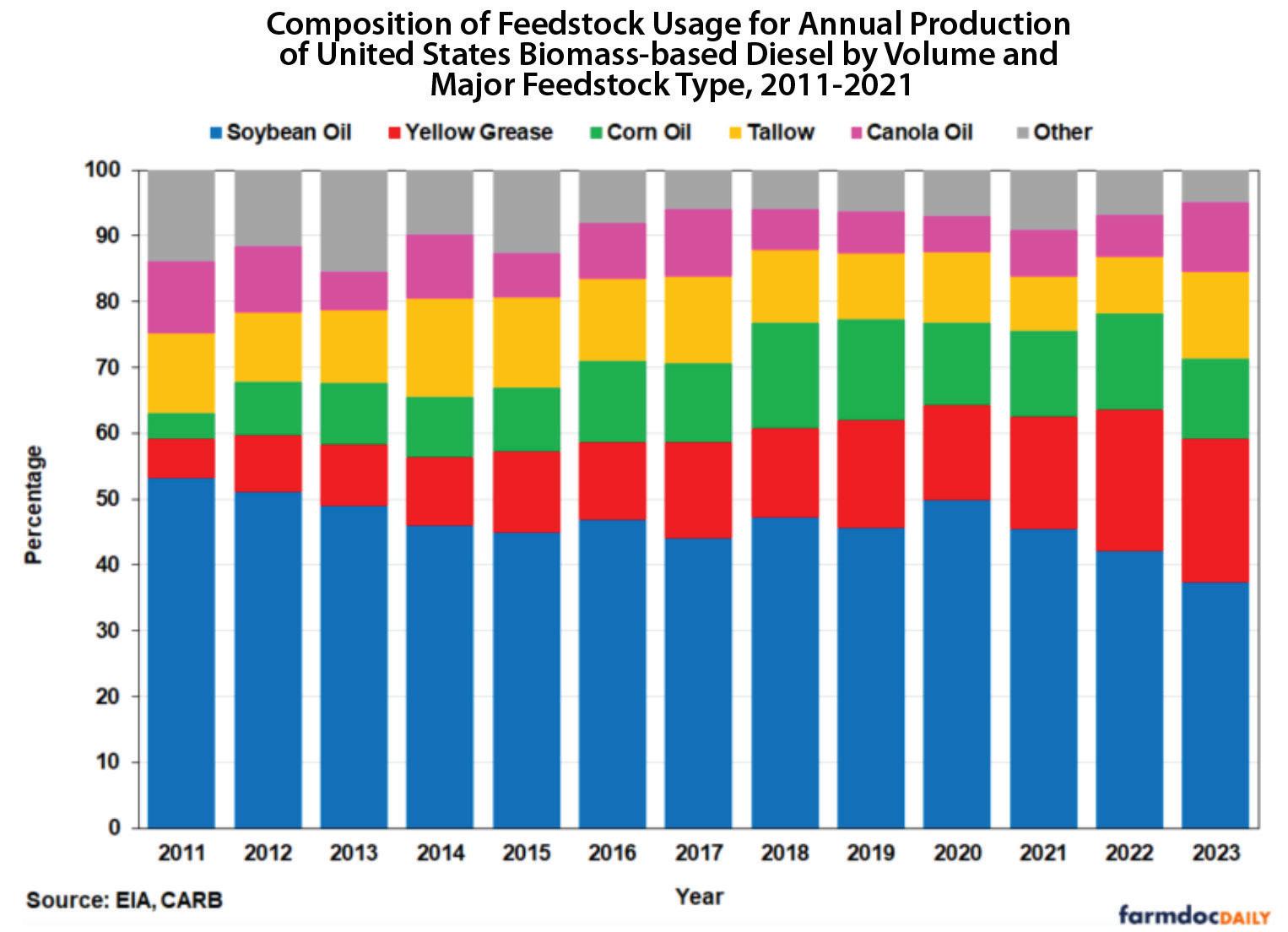

For the soybean industry, the surge in FOG imports adds to soybean oil’s struggle to maintain market share. Feedstock demand for both both RD and biodiesel grew by more than one-third from 19.2 billion pounds in 2021 to 32 billion pounds in 2023. The share of animal fats and processed oils (primarily UCO) increased from 32% to 37% while the share of vegetable oils (soy, canola, corn oil) declined from 68% to 63%. Between 2022 and 2023, soybean oil’s share of BBD feedstock declined from 44% to 40%, and in the first four months of 2024 declined to nearly 33%, the Oil Crops Outlook noted.

Soybean’s declining share in BBD production is illustrated in charts developed by University of Illinois ag economists. Through 2023, the volume of soybean oil used for BBD grew while its share declined, particularly since 2020 (See Figure 1). Soybean crushers who are planning expansions to meet expected RD growth look askance at soybean’s declining share and the burgeoning imports.

Soybean oil use has been increasing, says Scott Gerlt, American Soybean Association chief economist, but not to the ex-

Figure 2

SOURCE: “FAME BIODIESEL, RENEWABLE DIESEL, AND BIOMASS-BASED DIESEL FEEDSTOCK TRENDS OVER 2011-2023,” UNIVERSITY OF ILLINOIS, FARMDOCDAILY

pected utilization levels. “We’ve been building out domestic crush plants to provide more soybean oil,” he says, “and we have seen more use, but are concerned about underutilization of oncoming assets.”

He points to an analysis of what EPA expected for feedstock use when setting the renewable volume obligations (RVOs) for 2023-'25 under the Renewable Fuel Standard, compared to what has happened. The assumptions for 2023 were close to reality, Gerlt says, but in 2024, BBD production from FOG skyrocketed while production from soybean oil flatlined. (See Figure 2).

The impact on the domestic soybean oil industry is significant. The FOG BBD production of 580 million gallons in excess of EPA projections amounts to 4.7 billion pounds of soybean oil being displaced, Gerlt calculates, which would have come from 11 average crush plants processing soybeans from 7.5 million acres of soybeans. If you add to the 500 million gallons of finished renewable diesel imports that are assumed to be waste based, the total would displace the oil crushed at 20 plants processing soybeans from 14 million acres. “EPA was assuming a certain amount based on soybean oil production capacity,” Gerlt says, explaining the ASA had to show EPA how much crush expansion was coming online. In setting the blending levels for BBD, EPA assumed a certain amount coming from soybean oil, the typical usage of other sources and very little imported feedstock. “In fact, for 2025, they assumed imports at zero,” he says. The EPA got it wrong, but in fairness, he adds, few saw the surge in imports coming.

The RVOs, in essence, set a fixed blend rate, Gerlt argues. So, the growth in imports effectively pushes soybeans out of biofuel use at the margins. On top of that, the California LCFS puts soybean oil feedstocks at a disadvantage, and new rules will likely intensify that. The rules, adopted in November for the LCFS, add traceability requirements and call for capping vegetable oils (soybean and canola) at 20% of a facility’s production, with any excess receiving the conventional fuel score. “That’s going to make the situation even more extreme, because companies are going to have to switch away from soy/canola and look for waste feedstocks,” Gerlt says.

The new Clean Fuel Tax Credit (45Z in the Inflation Reduction Act) may offset some of the disadvantages for soybeans. The credit applies only to domestically produced fuels, and there’s a bipartisan effort in Congress to extend that domestic requirement to the feedstocks used for qualifying fuels. “If that were to go into effect, it would help the situation,” Gerlt says, “although considering some of the changes in California, I’m not sure it would completely shut off imports.” The playing field may also be leveled some, he adds, if the 45Z rules giving lower CI scores for feedstocks produced with conservation practices are easily implementable by farmers and biofuel producers.

Contact: Anna Simet Editor, Biodiesel Magazine asimet@bbiinternational.com

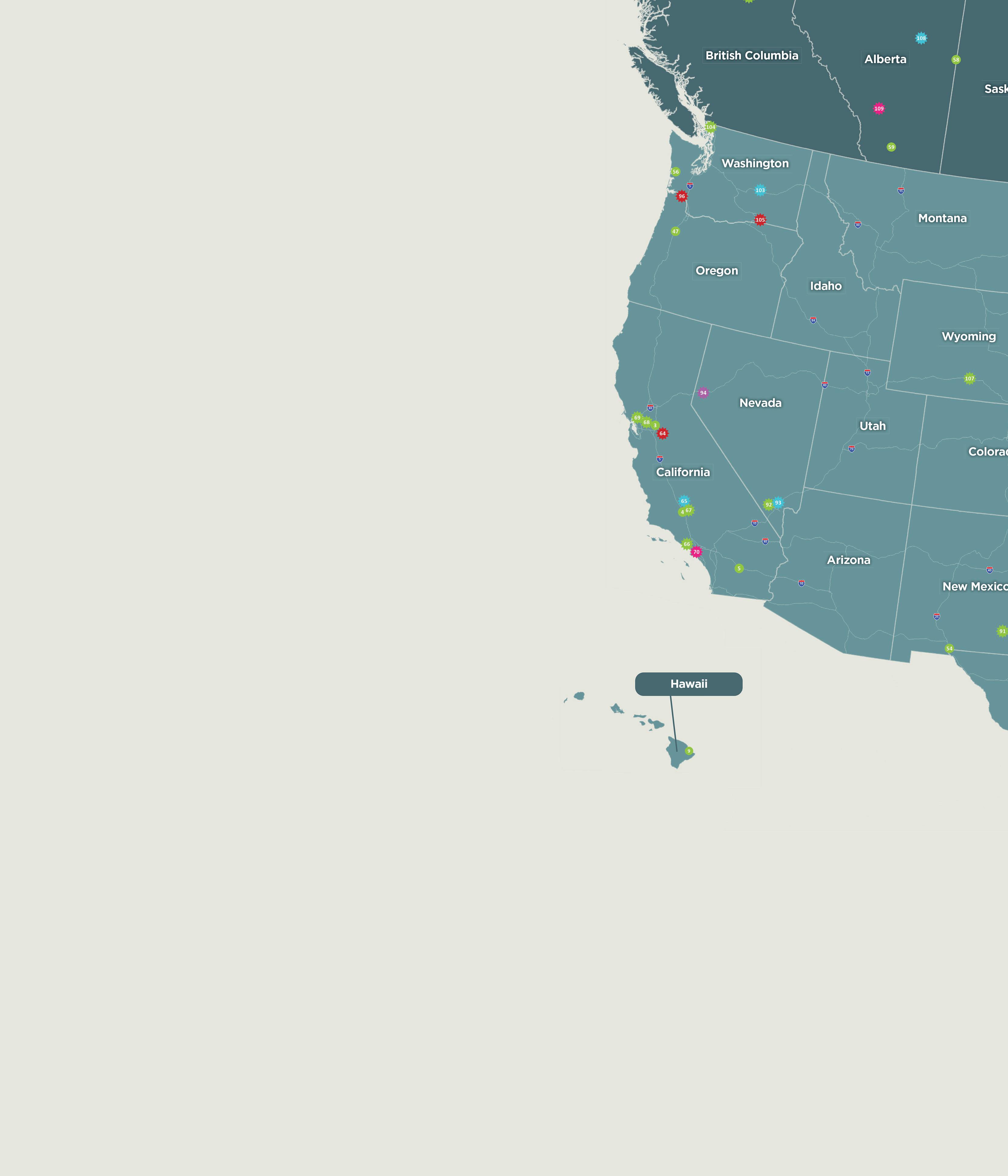

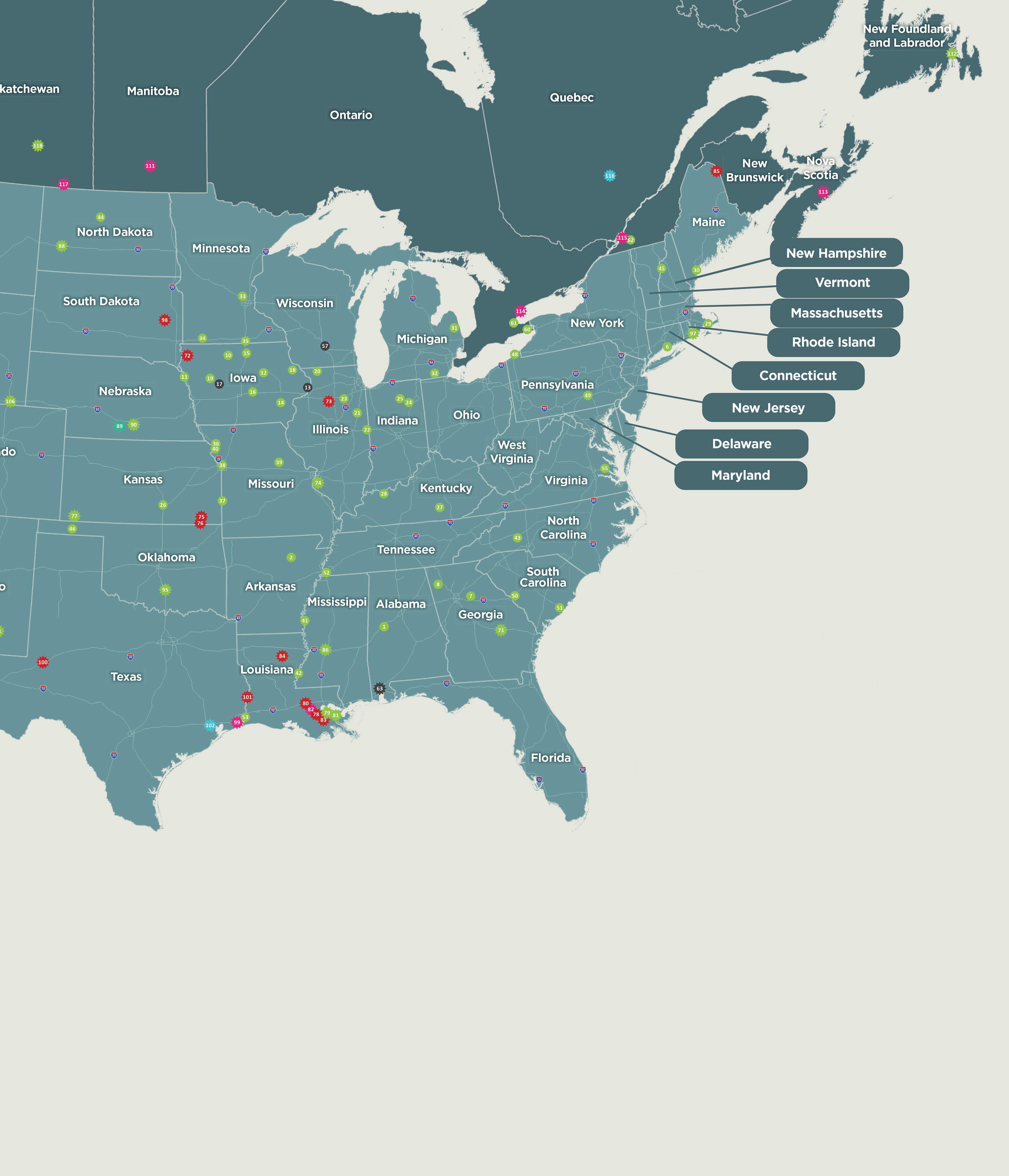

MAPPING

THE BUILDOUT

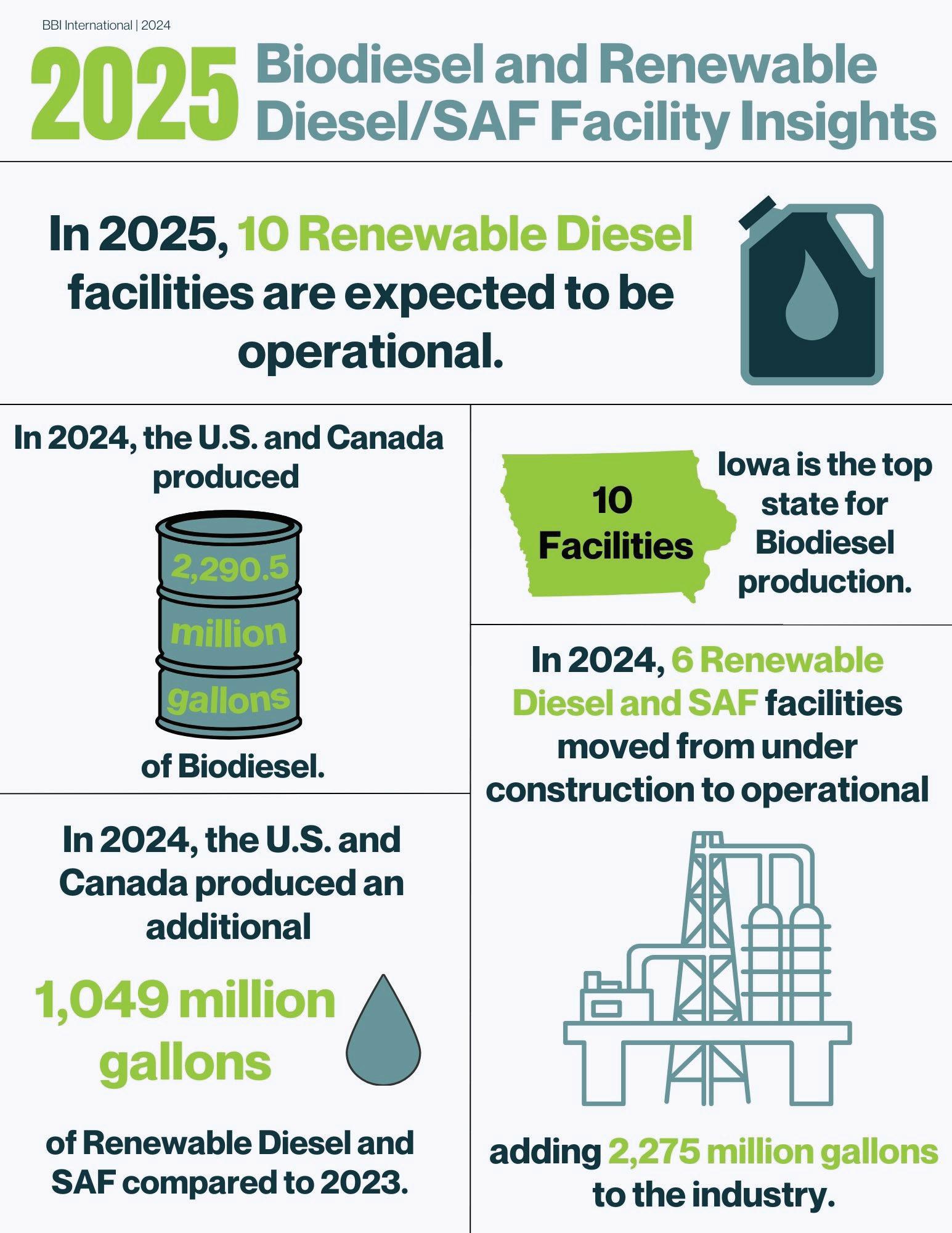

Biodiesel capacity in the U.S. and Canada dipped slightly stable in 2024, with several renewable diesel producers reporting headwinds and lower margins alongside a drove of SAF projects in various stages of development.

BY ANNA SIMET

As of October 27, there were 65 biodiesel plants in the United States and Canada, six of which are currently idle/not producing biodiesel. This includes Hero BX-Clinton in Clinton, Iowa (10 MMgy); REG Ralston in Ralston, Iowa (48 MMgy); REG Marison in DeForest, Wisconsin (28 MMgy), and Delek Renewables’ three plants in Cleburne, Texas; Crossett, Arkansas; and New Albany, Mississippi, which collectively remove another 40 MMgy from U.S. production capacity (at least temporarily).

As of early October, operating biodiesel capacity in the U.S. and Canada totaled approximately 2.23 MMgy.

As for renewable diesel and SAF facilities, Biodiesel Magazine’s data shows 56 projects in various stages of development (operational, under active construction/expansion and under development/proposed), with 22 operational facilities. Of those opera-

tional facilities, 16 are producing renewable diesel only (but may be producing coproducts such as naphtha, hydrogen, etc.), four are producing both renewable diesel and SAF, and four are producing SAF only. Total U.S./Canada renewable diesel and SAF operational capacity topped 5 billion gallons going into 2025.

Of the six facilities under construction, three report initial plans to produce renewable diesel only (558 MMgy of total under construction capacity). Two report plans for SAF only—World Energy’s Houston plant conversion, which is expected to be complete in 2027 and produce 250 MMgy, and Twelve’s Moses Lake, Washington, facility, which recent reports indicate has a target of 50,000 gallons of CO2-based SAF per year. One facility under construction will produce both SAF and RD—Edgewood Renewables’ 120 MMgy plant in Las Vegas, Nevada, which is expected to come online in 2025). Three facilities are currently under expansion.

For proposed projects, 21 facilities are included on this year’s map, totaling 5.1 billion gallons of capacity (facilities not yet sharing a project location are not included).

The following includes updates on projects in various stages of development, as reported by Biodiesel Magazine online news editor Erin Voegele, and BBI International Map and Data Coordinator Chloe Piekkola.

Under Construction/Expansion

Imperial Oil & ExxonMobile-Strathcona Refinery

In November, Imperial Oil confirmed that its renewable diesel project under construction at the company’s Strathcona refinery near Edmonton, Alberta, continues to progress on schedule with startup expected during the first half of 2025. During a third quarter earnings call, Imperial Oil President and CEO Brad Corson

said he is pleased with the construction progress on the renewable diesel unit at Strathcona. Corson noted that the company added feedstock coprocessing capabilities during the third quarter. He also expressed confidence regarding the underlying economics of the Strathcona renewable diesel project, noting that development of production capacity at an existing refinery allows Imperial to lower capital costs by leveraging existing utilities, rail infrastructure, staff and other elements. The facility will leverage locally produced feedstock oils, reducing feedstock transportation costs, and utilize technology provided by ExxonMobile that will allow it to produce a drop-in diesel product that is effective over a range of temperature conditions. Regulatory considerations are also much different in the U.S. than in Canada, he added, which provides additional economic support to the project.

Montana Renewables

On November 8, Calumet released third quarter financial results and outlined plans for the development of Montana Renewables’ MaxSAF initiative, which will be supported by a U.S. Department of Energy loan guarantee. The DOE has issued Montana Renewables a conditional commitment for a loan guarantee of up to $1.44 billion to fund the expansion of its biorefinery located in Great Falls, Montana.

According to Calumet, the expansion project would position Montana Renewables as one of the largest SAF producers in the world, with production capacity of approximately 300 MMgy of SAF and 330 MMgy of combined SAF and renewable diesel.

Todd Borgmann, CEO of Calumet, explained that the MaxSAF project is designed to be modular—a set of discrete projects developed in a series. The initial expansion project is expected to take approximately two years and will boost the facility’s SAF capacity to 150 MMgy. That capacity is currently expected to be operational by 2026. Further expansions will take longer to engineer and install, Borgmann added, noting they will include an expansion of renewable hydrogen production, expanded feedstock pretreatment capacity, a new wastewater system, renewable electricity and steam via cogeneration, enhanced SAF truck loading capabilities and other efficiency improvements.

Newly Operational/Ramping Up

Martinez Renewable Fuels

Marathon Petroleum Corp. confirmed in November that the Martinez Renewable Fuels biorefinery in California remains on track to be operating at full nameplate capacity by the end of the year. At full capacity, the facility can produce 730 MMgy.

Marathon officials briefly discussed operations at the Martinez biorefinery during the company’s third quarter earnings call. The facility, previously a Marathon oil refinery, was converted to a renewable diesel biorefinery via a 50/50 joint venture between Marathon and Neste Corp.

The Martinez Renewables facility began production in early 2023, but operations at the facility have been impacted by a fire that occurred late that year. During the earnings call, Marathon CEO Maryann Mannen said the company believes the Martinez biorefinery will be profitable once it is operating at capacity. John Quaid, chief financial officer at Marathon, discussed the upcoming expiration of the biobased diesel tax credit, noting the industry was still awaiting guidance on the 45Z clean fuels production credit, which is scheduled to take effect in 2025. Quaid said the company is preparing for all scenarios and believes that the market will balance out in the longer term.

Marathon also operates a 180 MMgy renewable diesel facility in Dickinson, North Dakota.

Rodeo Renewable Energy Complex

In October, Phillips 66 reported that its renewable fuels segment was impacted by lower margins during the third quarter of this year, but company officials expect margins to improve moving forward. The company also reported that it began producing SAF in September.

The company’s Rodeo Renewable Energy Complex has been under development since mid-2022 and reached full processing rates during the second quarter of 2024. Kevin Mitchell, chief financial officer at Phillips 66, reported that the Rodeo facility produced 44,000 barrels per day of renewable fuels during the third quarter. The biorefinery has a nameplate capacity of approximately 50,000 barrels per day (800 MMgy).

Brian Mandell, executive vice president of marketing and commercial, noted that the company is still in startup mode in terms of its renewable segment. He said the Rodeo facility is currently utilizing some higher-carbon-intensity feedstocks during the fourth quarter as the plant prepares for implementation of the 45Z clean fuels production credit net year.

Moving into the fourth quarter and beyond, Mandell said Phillips 66 expects to see margin improvements for renewables. He explained that feedstock prices remain depressed, and a number of renewable diesel plants are struggling. He also noted that some current renewable diesel capacity is going to be converted to SAF and cited lower imports, a tighter West Coast car diesel market, the tightening of credit markets and the disincentivizing of biodiesel production as factors that the company expects to drive stronger renewable diesel margins.

Mandell also cautioned that the Rodeo facility is not likely to produce SAF during the fourth quarter of 2024, but said the bio-

refinery is expected to be in steady-state operations by the first quarter of next year. SAF production should be underway at that time, he indicated.

CVR Energy Wynnewood

In late October, CVR Energy Inc. reported that the renewable diesel unit at its Wynnewood refinery in Oklahoma processed 19.6 million gallons of vegetable oil feedstock during the third quarter, down from 23.8 million gallons during the same period of 2023. The company said it ran the unit at lower utilization rates in an effort to optimize catalyst life.

David Lamp, CEO of CVR Energy, said the HOBO (heating oil to bean oil) spread for the third quarter was slightly weaker than the preceding three months due to lower diesel prices. He noted the decrease was offset by higher prices for D4 RINs and Low Carbon Fuel Standard credits, which helped drive a positive result for the quarter.

According to Lamp, the third quarter was the first full quarter of operations for the feedstock pretreatment unit. He said the company is pleased with the performance of the renewable diesel unit and pretreater for the three-month period. Lamp also pro-

vided an update on possible plans to produce SAF. He said CVR Energy’s discussions with counterparties related to the potential conversion of the Wynnewood renewable diesel unit to 100% SAF are ongoing. He stressed that that potential conversion won’t move forward without an offtake structure for SAF that would provide the company with downside protection and minimize its reliance on government credits.

Valero/Diamond Green Diesel

In October, Valero Energy Corp. reported increased production for both its ethanol and renewable diesel segments, and that its SAF project is expected to be fully operational before the end of 2024. Valero’s renewable diesel segment, which consists of the Diamond Green Diesel joint venture, reported $35 million of operating income for the quarter, down from $123 million during the same period of 2023. Sales volumes averaged 3.5 million gallons per day, up 552,000 per day when compared to the third quarter of 2023. According to Homer Bhullar, vice president of investor relations and finance at Valero, the company expects renewable diesel sales volumes for the full year 2024 to be approximately 1.2 billion gallons.

Lane Riggs, president and CEO of Valero, reported that the SAF product under development at the DGD Port Arthur plant in Texas reached mechanical completion in October and is now in the process of starting up. At press time, the project was expected to be fully operational by year-end, providing the plant with the option to upgrade approximately 50% of the facility’s current 470 MMgy production capacity to SAF.

Additional Updates

Other updates acquired by Biodiesel Magazine include Vertex Energy’s decision to idle its 200 MMgy renewable diesel plant in Mobile, Alabama, due to a lack of margin, and the closure of New Leaf Biofuel in December 2023. The company told Biodiesel Magazine that although it no longer produces biodiesel, the company has a renewables terminal in Fontana, California, that distributes biodiesel, and that the company still collects and sells feedstock.

Author: Anna Simet Editor, Biodiesel Magazine asimet@bbiinternational.com

SOURCE: NREL

Overcoming Limitations of Higher Biomass-Based Diesel Blends

Current barriers to higher biomass-based diesel blends have been identified along with strategies to address them.

BY ROBERT MCCORMICK

Commercial haulers, transit bus agencies and other heavy-duty applications can use United States-produced biodiesel blended with conventional diesel to reduce their environmental impact. But the amount of biodiesel used in fuel blends has been limited to up to 20% (B20), and there is not much information available on the properties of higher-level blends.

A large body of data supports B20 use, and the required properties of blends up to B20 are described in ASTM International’s standard D7467. But the use of higher blends, such as 50% (B50), 80% (B80) or even 100% biodiesel (B100), has not been widely explored in controlled engineering studies. The National Renewable Energy Laboratory, sponsored by the U.S. Depart-

ment of Energy Vehicle Technologies Office, conducted research to identify barriers preventing the use of blends over 20% along with strategies to overcome them.

Gauging Higher Blend Performance

Biodiesel is an oxygenate made from fats, oils and greases. Renewable diesel is made from the same feedstocks as biodiesel

CONTRIBUTION: The claims and statements made in this article belong exclusively to the author(s) and do not necessarily reflect the views of Biodiesel Magazine or its advertisers. All questions pertaining to this article should be directed to the author(s).

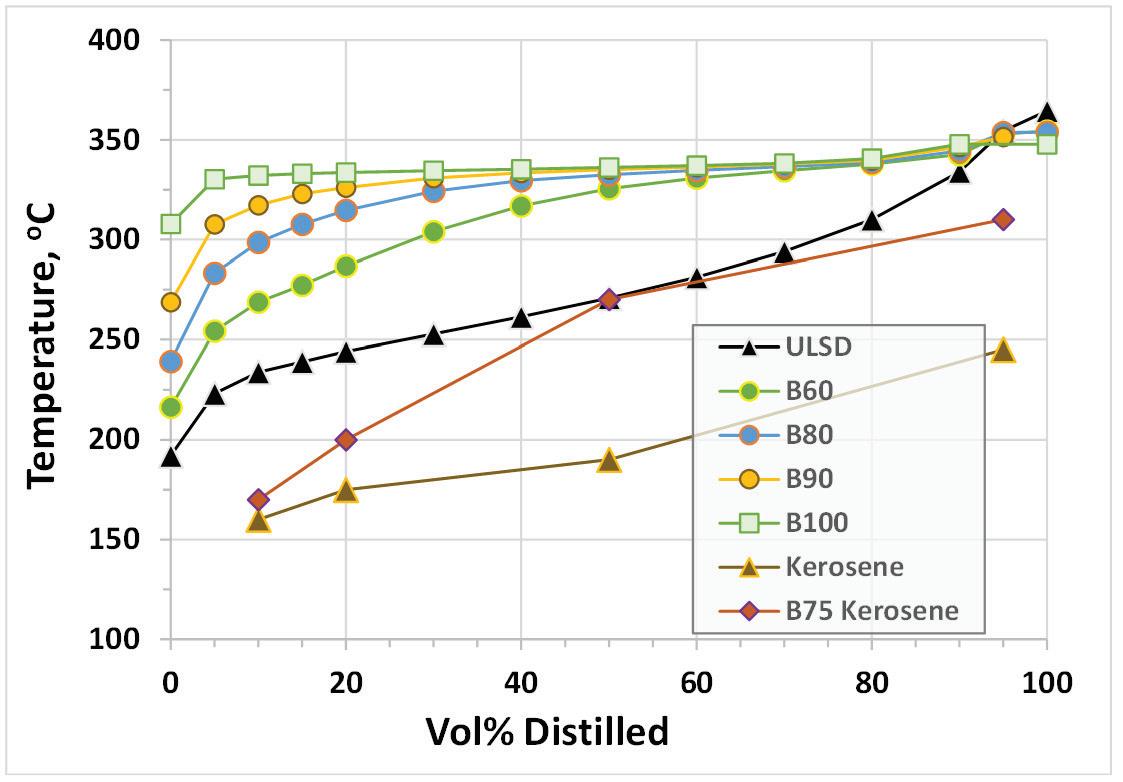

Figure 1: D86 distillation curves for ULSD and its biodiesel blends.

'Results showed that the most significant difference in fuel properties for biodiesel versus petroleum diesel or renewable diesel is boiling point or distillation curve.'

but processed into a hydrocarbon that is chemically more like petroleum diesel. The use of biodiesel and renewable diesel is forecast to reduce transportation-related greenhouse gas emissions from 40% to 86% compared to petroleum diesel, depending on the feedstock used. Biodiesel blends with renewable diesel are 100% renewable.

The National Renewable Energy Laboratory investigated the performance of 20%, 40%, 60%, 80% and in some cases, 90% blends of biodiesel into both renewable diesel and petroleum diesel. The research paper, “Properties That Potentially Limit High-Level Blends of BiomassBased Diesel Fuel,” in the journal Energy & Fuels, describes the results. The research addresses a major data gap about biodiesel blends, as it looks at high-level blends as well as blends with renewable diesel and petroleum diesel.

The results showed that the most significant difference in fuel properties for biodiesel versus petroleum diesel or renewable diesel is boiling point or distillation curve. Conventional diesel fuel and renewable diesel boil between 200 and 350 degrees Celsius (390 to 660 degrees Fahrenheit). The lower-boiling-point components in the fuel evaporate and ignite at lower temperatures, releasing heat and increasing temperature so that the higher-boiling components can also evaporate—a critical step in combustion. But biodiesel has a much narrower boiling range of 300 to 350 degrees C and boils at the high end of the diesel range. This means that as the blend level is in-

creased, there are fewer lower-boiling components, requiring higher temperatures to begin evaporating the fuel. Biodiesel’s high and narrow distillation curve can make fuel evaporation more difficult to achieve for high-level blends (over 50%) and B100.

The high boiling point of biodiesel can make engine cold starting more difficult. Additionally, if the fuel sprayed into the engine does not fully evaporate, the unevaporated fuel can accumulate in the engine lube oil, leading to less effective lubrication. Perhaps the most important problem caused by the high and narrow boiling point of B100 and high-level blends is that, in certain cases, it can cause the diesel oxidation catalyst (DOC) to fail to light off. In many diesel engine emission control systems, supplemental fuel is injected into the exhaust to be oxidized over the DOC, increasing the exhaust temperature for regeneration of the downstream diesel particle filter. A recent study of high-level blends found that B50 and higher blends were not being converted over the DOC at temperatures below about 350 C, likely because most of the fuel was not evaporating and simply passed through the catalyst as aerosol droplets. As a result, the particle filter did not achieve adequate temperature to burn off the accumulated soot.

Mitigating the Issues

An approach to mitigating the cold starting, cloud point, lube oil dilution and DOC light-off issues for high-level blends is to use a No. 1 diesel or kerosene as the hydrocarbon blending component. Fuel

blenders commonly use this approach to lower the cloud point of wintertime diesel, including biodiesel blends. Because No.1 diesel/kerosene has a larger number of lower-boiling components than conventional diesel (it boils between approximately 150 and 300 C), it produces a biodiesel blend that boils across a wider range of temperatures.

Another approach that vehicle owners have used successfully is retrofitting the engine with a heated fuel system, like the Optimus Vector System, that starts the engine on petroleum diesel and switches to B100 after both the B100 and engine are warmed up. Heated fuel systems work for B100 as well as high-level blends. This approach addresses cold starting, cloud point and lube oil dilution, but may not address DOC light-off.

For the DOC light-off issue with B100 and very high-level blends where kerosene blending may not be effective, it is possible that a B100-specific engine calibration will be required. Calibration is part of the programming of the computer that governs operation of the engine. A B100-specific calibration would change engine operating parameters, such as injection timing and exhaust gas recirculation, to heat the exhaust to over 350 C before commanding fuel injection for DOC light-off and particle filter regeneration.

Significant future research is needed to address the challenges of high-level biodiesel blends, particularly regarding how they impact diesel engine emission control systems. The aforementioned NREL paper is a research road map for addressing these challenges.