10 minute read

The Myth And Reality Of The Mongolian Mining Industry

Ben Jones and Daan de Jonge, CRU Consulting, UK, provide an outlook for the Mongolian mining industry.

The mining industry is key to the health of the Mongolian economy: revenues from the export of coal, copper, gold and iron ore, for example, amounted to approximately US$6.3 billion in 2019. The potential for further growth is staggering: CRU Consulting’s analysis shows that many of Mongolia’s coal assets are among the lowest cost producers globally. The country is also substantially under-explored, and holds vast polymetallic resources.

However, while the mining industry has expanded significantly in the past decade – and further expansions are at various stages of development, including major ramp ups to operating assets at Tavan Tolgoi and Oyu Tolgoi – it has nonetheless generally failed to live up to some of the frothier growth expectations of the early 2010s. In fact, there has been an absolute decline in exploration licenses since 2011.

This reflects the practical barriers to successful investment in this frontier market. As investors such as Rio Tinto will no doubt attest, developing mining assets in Mongolia is not without its challenges. Developers are impacted by challenging technical conditions, including scarce water resources, fragile and under-developed infrastructure, and a deep scepticism among some sections of political and civil society about the merits of foreign investors in the industry.

This article explores the myths and realities that stand over the Mongolian industry. It reports some of the key

findings from a recent in-depth study by CRU Consulting into the prospects for, and barriers to, future expansion of the mining industry in Mongolia, and discusses some of the major policy and investment decisions shaping industry and broader economic outcomes in the coming years.

A complex web of policy, institutional, and infrastructure related barriers continue to hamper investment

The mining industry in Mongolia is likely to be shaped by a number of key barriers and impediments, which will be critical to address to ensure a secure future.

From an institutional perspective, investors must grapple with a high level of state participation in the industry. Key strategic assets, such as Oyu Tolgoi and Tavan Tolgoi, are owned partly by the state mining company, Erdenes Mongol. Levels of transparency in this institution and the quality of overall governance more generally are low, and a clear dividend policy is lacking. These issues undermine the eff ectiveness of this organisation in developing and unlocking resource value. Policy instability and weak property rights have also been prevailing issues. Weary investors will point to the state’s appropriation of the Dornod Uranium deposit from Canadian-based Khan Resources between 2009 – 2011, or even current discussions regarding the prospects for revision to the financial agreement on Oyu Tolgoi, as reasons to consider investments extra risky.

Inflation is an economy wide issue, but high transportation costs are a particular boon for exporters of bulk materials, such as iron ore and coal. An under-developed rail network and poor road surfaces mean that transporting ores over long distances to off takers in China, Russia, and beyond can be expensive. Many of the border points are particularly significant bottlenecks, with extensive traff ic blocks a common sight in Gashuun Sukhait and Shivee Khuren. CRU Consulting’s analysis finds that transportation costs account for over three-quarters and half of delivered costs of iron ore and metallurgical coal respectively (10 – 40% higher than leading international competitors in the case of the former). This implies substantial upside to value creation in key industry segments in the event of network expansions and upgrades – in particular for South Gobi bulk exporters, such as those of metallurgical coal.

Perhaps foremost among the productive constraints is the absence of suff icient water distribution infrastructure. With little rainfall, water scarcity is a nationwide issue: with an estimated 85 – 99% of water currently being extracted from non-renewable sources, this issue will only become worse over time if alternatives are not found. Such issues cannot be ignored by prospective mining investors and policy makers alike, and could represent a major constraint to future growth. Analysis by CRU Consulting suggests that the mining industry would ultimately exhaust local supply in some regions. As a result, without significant investment in a distribution network and more water eff icient extraction processes, the industry has the potential to ‘crowd out’ water access in regions such as the South Gobi.

200

150

100

50

0

Met Coal Copper Iron Ore

Strong growth is expected, but the upside to policy reform is huge

Figure 1. Production growth by commodity 2020 – 2025 (2020 = 100).

7,000

6,000

Business costs ($/tonne)

5,000

4,000

3,000

2,000

1,000 Central & South America Australia Mongolia China

0 North America

In spite of these barriers, CRU Consulting projects that continued macroeconomic development, population growth, and urbanisation in Mongolia (and internationally) will help foster the conditions for expanding production and mineral revenues, particularly in the short and medium terms, as expansions at Oyu Tolgoi and Tavan Tolgoi take place. For example, CRU Consulting projects in the region of 70 – 85% growth in copper and metallurgical coal production by 2025, respectively (compared to 2020 levels). There is further upside potential in the event that some of the key barriers and obstacles discussed are overcome. For example, CRU Consulting has explored the implications of constructing additional railways, both in the South Gobi and the northern corridor, on potential mine supply, investment, and profitability. In the case of Tavan Tolgoi, it found that such debottlenecking, as well as optimisation of trucking routes, could yield an approximate 15% uptick in Cumulative production, '000 tonnes Cu annual revenues, and an increase in sector margins more broadly approaching one-quarter.

Erdenet Africa CIS Oyu Tolgoi

0 5,000 10,000 15,000 Figure 2. Copper mining business costs, 2020 (US$/t copper).

Balancing politics and economics are key to success

Economic development in Mongolia is closely tied to key strategic assets, such as Oyu Tolgoi. The history of Oyu Tolgoi, with its landmark geology and drilling technologies, as well as its massive blow out in capital expenditures and acrimonious relationships among shareholders, is well known. However, as the equity partners prepare the next phase of investment in this asset, it will be critical to balance both the economic and political factors as part of eff orts to enhance the assets’ long-term commercial future.

In terms of economics, the scale of the resource clearly warrants further exploitation. Indeed, the future competitiveness of the asset critically depends on the development of a capital eff icient mine expansion plan, in order to deliver stronger economies of scale and bring down the cash costs. Nonetheless, a large scale mine expansion plan based significantly around block caving is inherently risky from a technical perspective, and the shareholders will be naturally wary of further possible cost inflation. However, these important economic and commercial issues also need to be understood and communicated in a way which reflects the politics of this strategically critical national resource.

There is a substantial weight of expectations from politicians, the Ministry of Finance and civil society that the asset makes a major contribution to the government’s coff ers. The absence of any dividend to date has proven challenging to justify to many such stakeholders, and has, perhaps unsurprisingly, contributed to a reignited debate surrounding the fiscal and broader financing terms upon which the equity partnership rests. While it is in the interests of all parties that satisfactory value sharing arrangements can be agreed, any renegotiation of framework agreements also has the potential to damage investor confidence, which is a particularly acute issue with long lived assets in frontier jurisdictions. Such issues are confounded by the lack of high-quality independent analysis into how value is currently being shared, how that diff ers from established practices in other relevant mining jurisdictions, and what the implications might be of alternative fiscal and financing terms.

Recent analysis undertaken by CRU Consulting, for example, finds that eff ective government take associated with the Mongolian fiscal regime is broadly in line with mainstream international practices: in a comparative analysis, it found that the eff ective tax burden on Oyu Tolgoi was ranked third out of the five countries studied. However, when exploring possible alternative tax policies and equity structures, it also found clear trade-off s between government revenue, in the form of tax income and dividends, which are at the heart of the policy choices facing the Mongolian government.

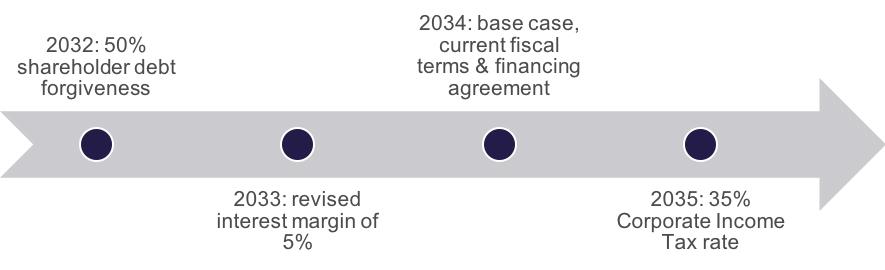

These trade-off s mean that the net eff ects of some potential changes to fiscal policy may be relatively limited. Using CRU Consulting’s detailed fiscal-mine model to explore the impacts of various potential alternative tax policy and financing terms for Oyu Tolgoi – the timing of the first dividend payment, for example, was found to be relatively insensitive to many of the potential reform options. While a combination of reforms to the tax and financing arrangements has the potential to influence cashflows further still, such deeper routed revisions have the potential to ensnare the negotiation processes and weaken long-term investment commitments.

These conclusions may be challenging for some domestic stakeholders to the mining industry within Mongolia. Fundamentally, the highly capital-intensive nature of large scale mining operations implies a tendency for equity owners to both receive substantially backloaded profits and incur a high degree of revenue risk associated with inflation (and compounded by market volatility). This means that, under current equity arrangements (even in the event of substantial shift in financing terms or debt forgiveness), or under a shift to a more traditional tax policy led regime (encompassing loss carry forward rules), the prospects for substantial fiscal revenues during and for an extended period aft er any ramp up phase are relatively limited.

2032: 50% shareholder debt forgiveness 2034: base case, current fiscal terms & financing agreement

The future is bright, but a healthy dose of realism by investors is required

2033: revised interest margin of 5%

Mongolia’s natural resource endowment is undoubtedly rich. Export revenues have grown strongly over the past decade or more, but the industry has generally failed to live up to its promise. This reflects the complex web of policy, institutional, and infrastructure related barriers which potential investors must grapple with. CRU Consulting expects strong growth to continue in the years ahead, driven by expansions at Tavan Tolgoi and Oyu Tolgoi, but that debottlenecking infrastructure and water related constraints could have an important bearing in unlocking additional value. Much of the upcoming focus will be on the negotiations between the recently elected government and the shareholders in Oyu Tolgoi. In this context, it will be critical to balance both economic and political factors in securing an agreement regarding the long-term commercial future of this strategically critical asset. CRU Consulting’s analysis highlights the potential challenges associated with meeting political demands for large scale, front-loaded revenue streams, given the capital intensive nature of the mine expansion plan and the scale and structure of state participation. Finding an acceptable 2035: 35% pathway forward could be Corporate Income Tax tremendously valuable for both shareholders in the long term, and signal a bright future for the industry Figure 3. Oyu Tolgoi first dividend date by fiscal and financing scenarios. at large.