Annual subscription: UK £270, all other countries £292. For two year subscription: UK £510, all other countries £527. Airmail prices on request. Single copies £50

ALUMINIUM INTERNATIONAL TODAY is published six times a year by Quartz Business Media Ltd, Quartz House, 20 Clarendon Road, Redhill, Surrey, RH1 1QX, UK. Tel: +44 (0) 1737 855000 Fax: +44 (0) 1737 855034

Email: aluminium@quartzltd.com

Aluminium International Today (USO No; 022-344) is published bi-monthly by Quartz Business Ltd and distributed in the US by DSW, 75 Aberdeen Road, Emigsville, PA 17318-0437. Periodicals postage paid at Emigsville, PA. POSTMASTER: send address changes to Aluminium International c/o PO Box 437, Emigsville, PA 17318-0437.

Printed in the UK by: Stephens and George Ltd, Goat Mill Road, Dowlais, Merthyr Tydfil, CF48 3TD. Tel: +44 (0)1685 352063 www.stephensandgeorge.co.uk

BAUXITE

7 Mixed forturnes for bauxite production

11 Responsible mining for people and planet

DECARBONISATION

17 Is the industry on track with decarbonisation?

22 Key to aluminium industry decarbonisation

27 The energy transition and decarbonisation

HYDROGEN

35 Zero-carbon using green hydrogen

THE ALUMINA CHRONICLES

41 Aluminium industry in Germany

PACKAGING

53 Decarbonising together

56 The UK Deposit Return Scheme SUSTAINABILITY

61 Investing in sustainable aluminium

65 Ensuring net-zero for the metal

DIGITAL TECHNOLOGIES

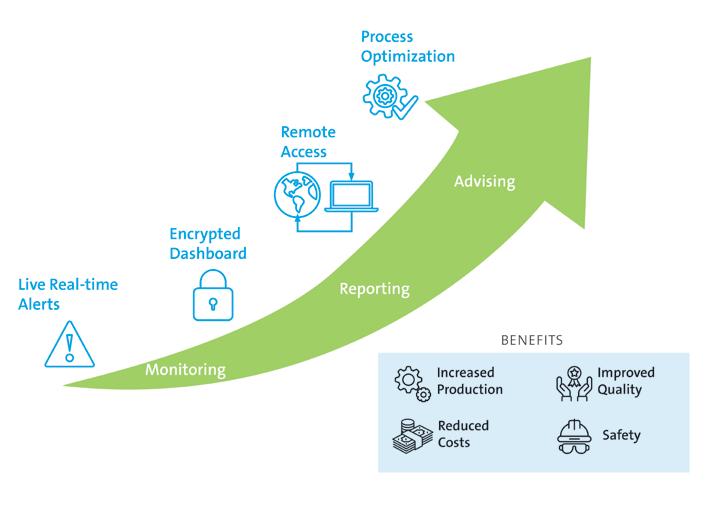

71 Real-time molten metal analysis of the future

74 The strategic role of technology

77 Q&A: Digitalising aluminium

CASTHOUSE

83 Enhancing casthouse operations

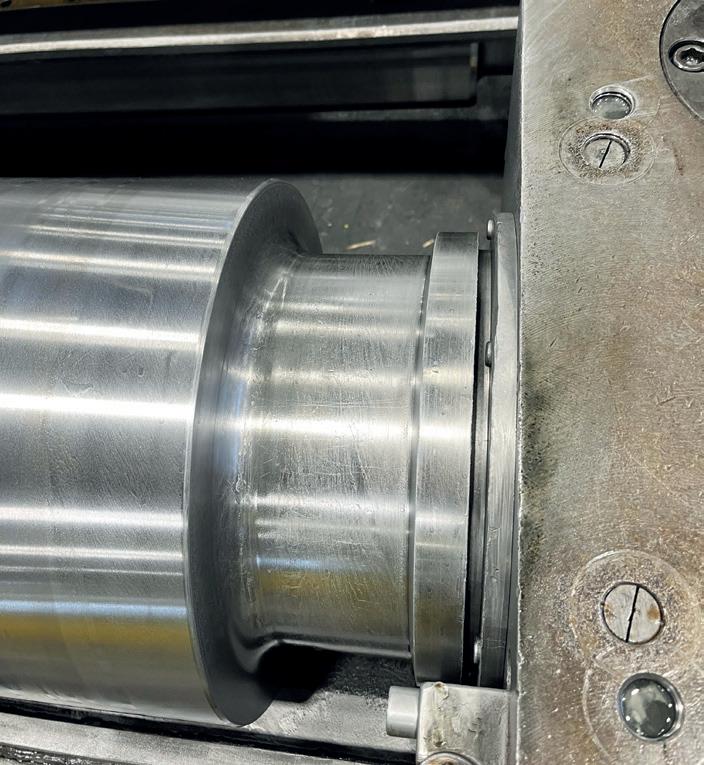

ROLLING

87 New technology for superior cleanliness

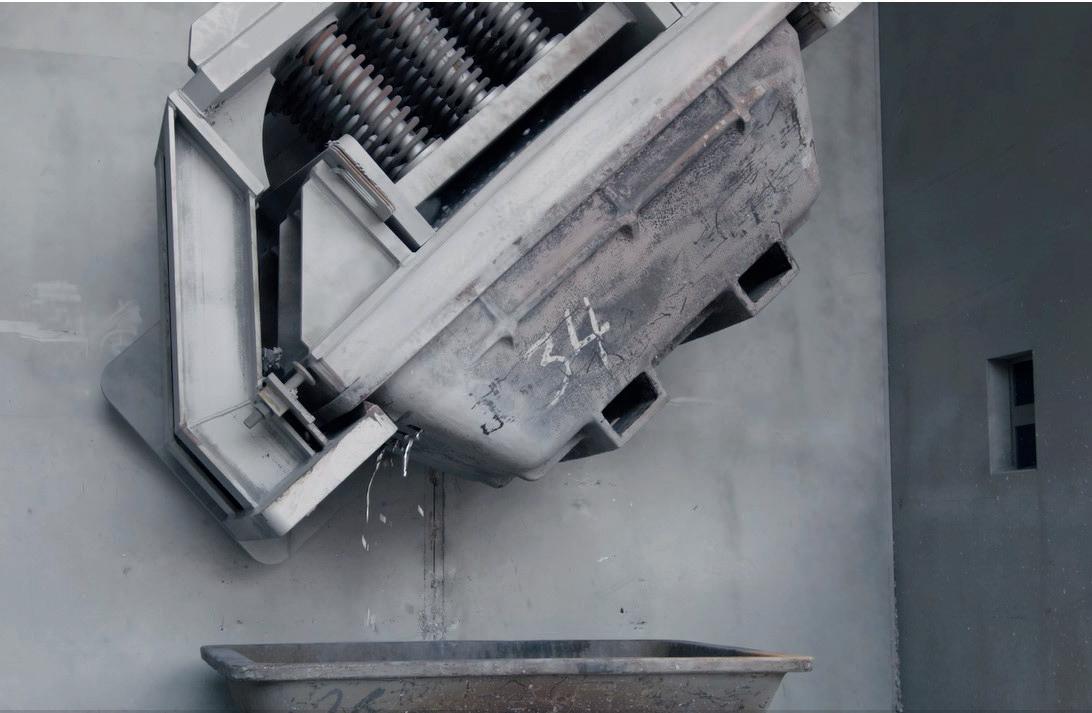

DROSS PROCESSING

91 New Benchmark in dross processing

REFRACTORIES

95 Calderys exhibits refractory solutions

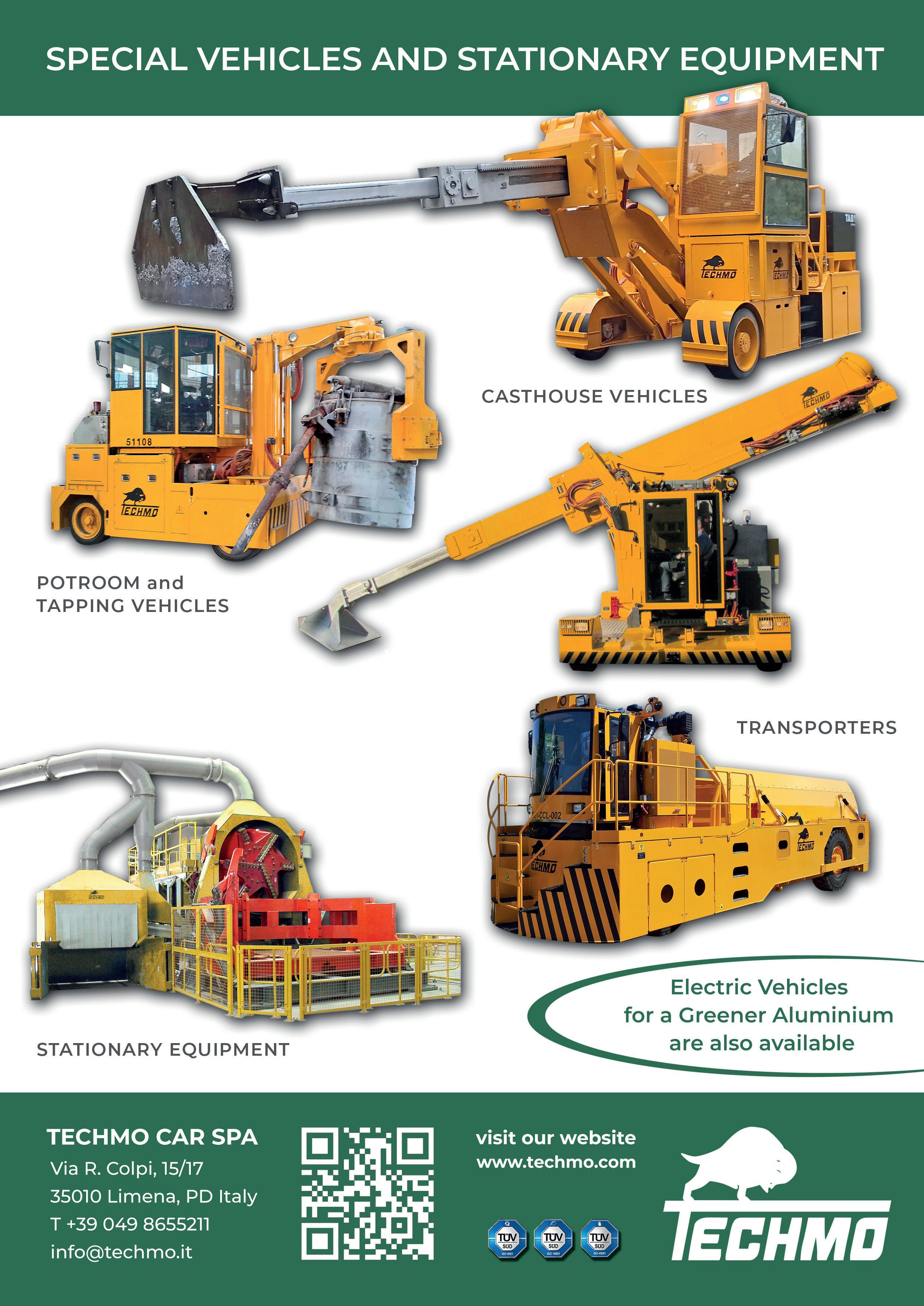

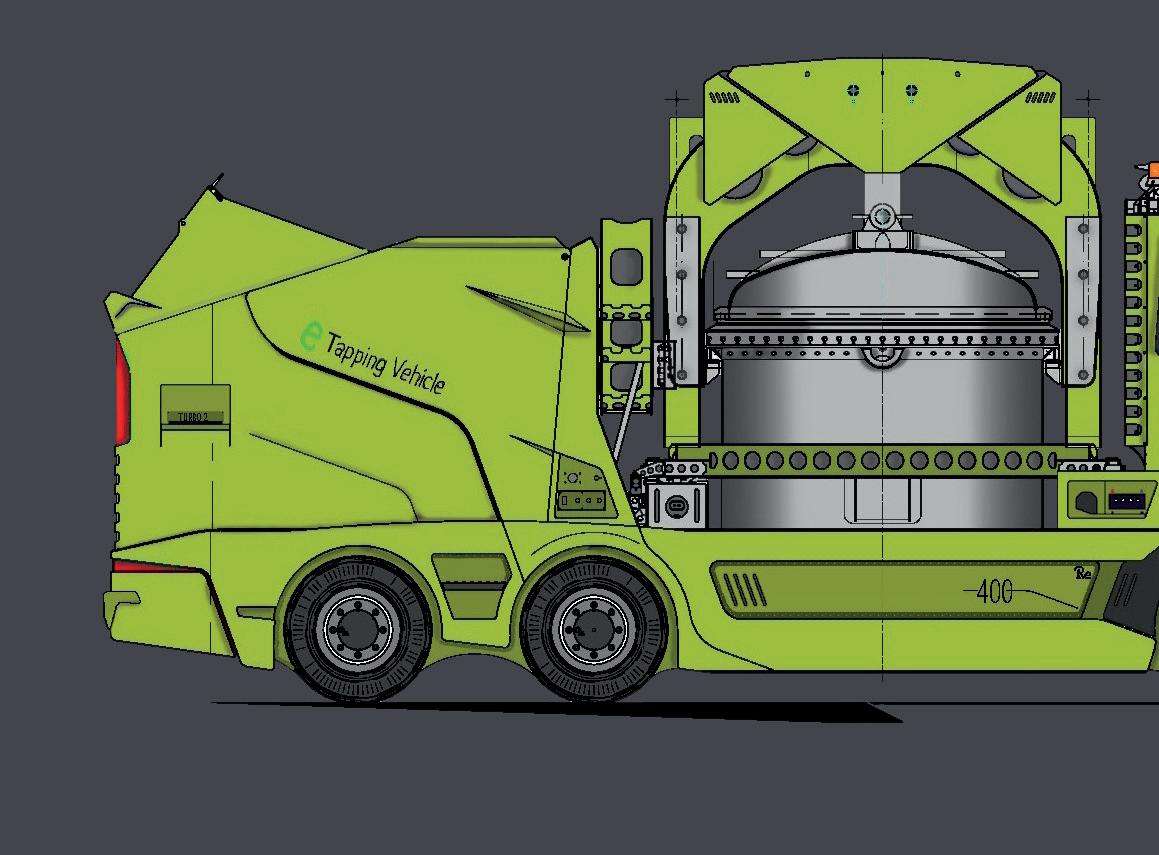

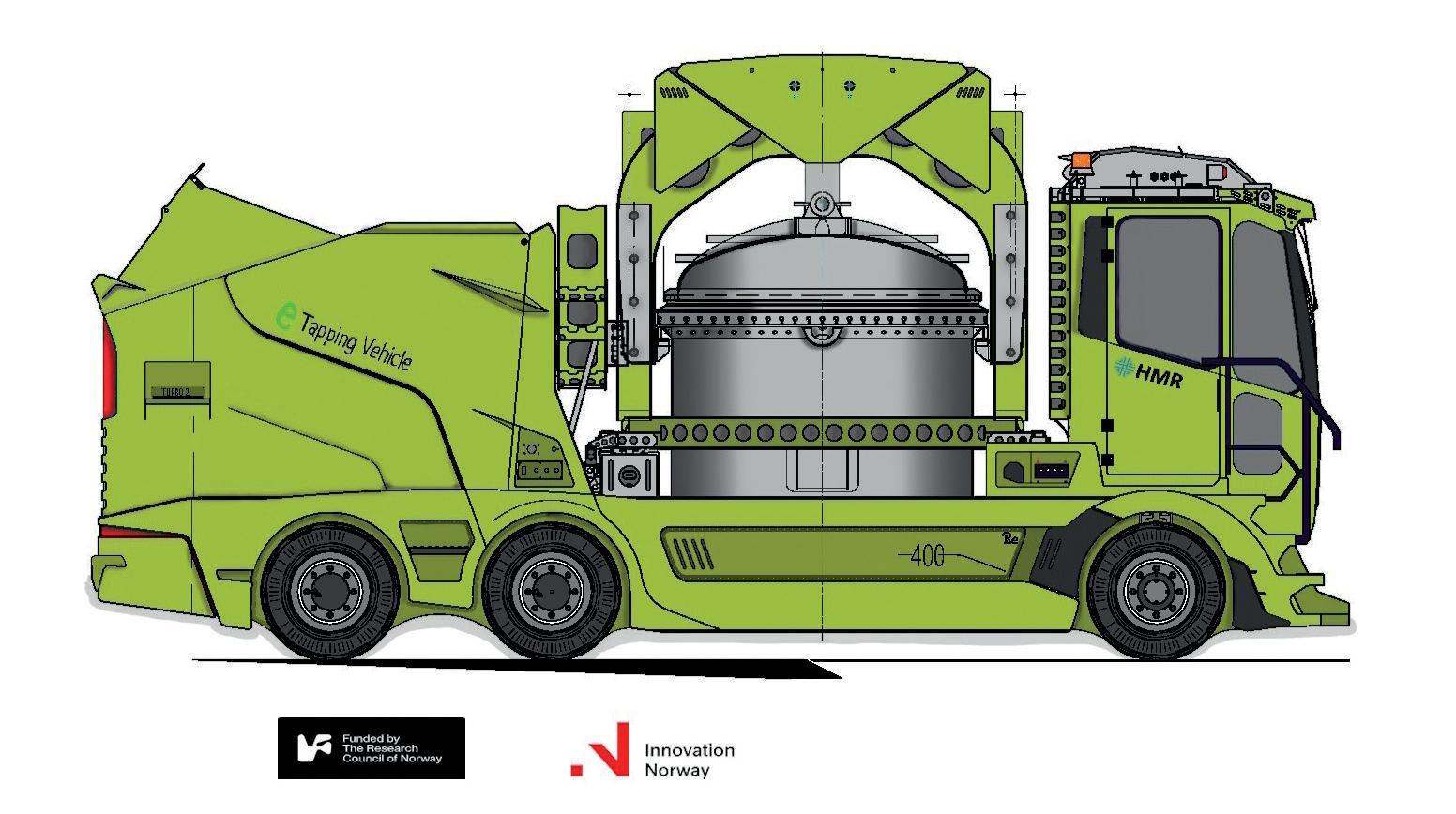

101 Electric tapping vehicles 102 Electric driven vehicles

COMPANY FOCUS 103 New automotive sector press line ASSOCIATION SPOTLIGHT 99 TALSAD: Turkish Aluminium

picture courtesy of Gillespie & Powers, Inc.

After more than a decade at the helm of Aluminium International Today, it is with a mix of excitement and nostalgia that I write this final editorial comment.

Over the past 10 years, this role has taken me to the far corners of the world, allowing me to witness firsthand the incredible innovations and production processes that define our industry. I’ve had the privilege of touring state-ofthe-art facilities, learning from the best in the business, and, most importantly, meeting wonderful people who have become much more than colleagues - they have become friends.

As I embark on a new chapter as the Chief Executive Officer of the Aluminium Federation, I find myself reflecting. My time as Editor has been incredibly rewarding, not only professionally but personally. The aluminium

industry is unique in its sense of community, and I am grateful to have been a part of it.

I am thrilled to be handing over the reins to our current Assistant Editor, Zahra Awan. Zahra has been an integral part of the team, bringing fresh ideas and a deep passion for the industry. I have no doubt that she will continue to drive AIT forward with the same dedication and enthusiasm that has always been at the core of our publication.

While I am stepping away from my editorial duties, I am pleased to say that I will not be disappearing entirely. I will continue to contribute articles and opinion pieces, particularly focusing on the UK market and the broader aluminium industry. It’s a way for me to keep a hand in the world that has given me so much and to continue sharing my perspectives with you, our valued readers.

I want to take this opportunity to thank each and every one of you for your support, interest, and engagement over the years. It has been an honour to serve as your Editor, and I look forward to continuing our conversations in a different capacity.

The aluminium industry is dynamic, resilient, and full of potential, and I am excited to see where we go from here, together.

Launch of the Alutrends Report 2024

Aluminium International Today proudly unveils the Alutrends Report 2024, a comprehensive exploration of the aluminium industry’s journey towards sustainability and innovation.

The report delves into the latest trends, technological advancements, and key sustainability initiatives shaping the aluminium sector. Featuring insights from industry leaders, its purpose is to delineate the crucial trends that will steer and transform the aluminium industry in the year ahead.

The report is poised to deliver indepth insights into the forces that will shape our industry’s trajectory in 2024 and focuses on pivotal areas such as challenges in recruit-

ment and resources, technological advancements, and the imperative shift towards sustainability, and will spotlight the strategies businesses need to adopt to navigate these evolving landscapes successfully.

“Aluminium’s role in the green energy transition takes centre stage,” says Nadine Bloxsome, Editor of Aluminium International Today. “From wind turbines to electric vehicle chassis, aluminium’s properties are driving the shift towards a sustainable future.”

The Alutrends Report 2024 is an essential resource for industry professionals seeking to stay ahead of the curve in sustainability and innovation.

Aluminium Bahrain B.S.C. (Alba) marks a significant milestone in sustainable aluminium production with Capral Aluminium becoming the first customer for its revolutionary EternAlTM low-carbon aluminium primary billet.

Launched in May 2024, EternAlTM is offered in two initial variants: EternAl-30 and EternAl-15 boasting a 30% and 15% recycled content respectively, reducing the product’s carbon footprint. Furthermore, EternAlTM has received independent verification by DNV, a globally renowned leader in verification assurance, cementing its sustainability credentials.

Capral Aluminium recently completed successful trials of both EternAl-15 and EternAl-30, enabling it to supply lower-carbon aluminium to a wide range of Australian manufacturing sectors, including marine, defence, transport, construction, signage, and general fabrication.

Ali Al Baqali, Alba’s Chief Execu-

EGA completes design phase of next generation smelting technology Alba secures customer for EternAlTM Aluminium

Emirates Global Aluminium have announced the completion of the design phase of the company’s next generation smelting technology, EX.

EX reduction cells are larger than EGA’s most recently industrialised technology DX+ Ultra, enabling higher amperage and improved current efficiency, increasing production capacity by up to 22 per cent.

EX has been designed with two variants – one to maximise productivity, and the other to further minimise greenhouse gas emissions. Reduced electricity consumption along with lower net carbon consumption and the reduced incidence of anode effects is expected to reduce greenhouse gas emissions per tonne of aluminium produced by around five per cent for the more productive variant and around 12 per cent for the lower energy variant.

tive Officer, expressed his enthusiasm about the partnership:

“At Alba, driving sustainable aluminium production is not just a goal, it’s our mission. The successful trials of EternAl-15 and EternAl-30 with Capral represent a significant leap forward in achieving that mission.

We’re proud to partner with a forward-thinking company like Capral, allowing us to deliver these high-quality, recycled content products to the Australian market.

DX+ Ultra is already one of the most efficient smelting technologies in the global aluminium industry.

EGA now intends to construct 10 pilot EX reduction cells at the company’s aluminium smelter in Al Taweelah to test and validate performance. The target is that EX is ready for full industrialisation by 2028.

Abdulnasser Bin Kalban, Chief Executive Officer of Emirates Global Aluminium, said: “Technology development has been a foundation of our global competitiveness for decades. EX technology will enable the production of more aluminium with less energy and lower emissions, unlocking opportunities for EGA’s growth and helping us to meet the increasing global demand for the low carbon primary aluminium required to reach net zero by 2050.”

Nadine Bloxsome

Novelis doubles capacity to recycle used beverage cans in UK

Novelis Inc. have announced it is investing approximately $90 million to increase recycling capacity for used beverage cans (UBCs) at its plant in Latchford, UK. The project will increase the facility’s recycling capacity for UBCs by 85 kilotonnes per year, equaling a growth of more than 100%.

The investment at Novelis Latchford supports a significant expansion of recycling capacity to substantially increase the recycled content and reduce carbon emissions in Novelis aluminium sheet.

“Of all the recycling players in the European market, Novelis has the highest ambition to maximize its recycled content across our product range,” said Emilio

Braghi, executive vice president of Novelis and president, Novelis Europe.

The investment includes the construction of a new dross house, three new bag houses, and the installation of state-of-the-art shredding, sorting, de-coating,

and melting technologies – enabling the plant to recycle a larger volume and new types of aluminium scrap, and to increase operational efficiency. The expansion of recycling capacity, as well as the implementation of advanced technologies, will result in an annual CO2e reduction of more than 350,000 tonnes for Novelis Europe.

The project is expected to begin commissioning in December 2026. Once complete, the facility will be able to recycle 100% of UBCs to be collected under the future UK deposit return scheme. This will create a local, fully circular system that will avoid the need to export scrap from the UK.

First industrial-scale aluminium slab using hydrogen combustion

Constellium announced the successful completion of its first industrial-scale hydrogen casting at C-TEC, Constellium’s primary R&D center. This casting was performed in a 12-ton furnace following strict internal procedures. Quality monitoring, including the use of Batscan™ technology, an inclusion detection tool for molten aluminium, was conducted and no quality impact from hydrogen combustion on metal was observed.

“We are thrilled to announce the successful completion of our first industrial-scale hydrogen casting. This achievement marks

Alcoa

Introducing the Rhodax® Club: Advancing Green Anode Plant

In the dynamic landscape of aluminum production, innovation and collaboration are essential, Fives has taken a significant step forward by launching the Rhodax® Club. This exclusive club brings together experts and end users to address critical challenges and drive advancements in the Rhodax® process technology.

Queensland Government and Rio Tinto partnership to support Gladstone’s Boyne Smelters

a pivotal step in Constellium’s journey towards decarbonising our industrial activities. Utilising hydrogen as a substitute for natural gas not only demonstrates our commitment to sustainability

but also paves the way for future innovations in green technologies,” said Ludovic Piquier, Senior VP, Manufacturing Excellence and Chief Technical Officer of Constellium.

The 12-ton aluminium slab produced using hydrogen will be further processed at our Neuf-Brisach site in France for use in electric vehicles. This milestone is significant in our roadmap towards decarbonising our industrial activities, as we have begun exploring the performance of hydrogen as a substitute for natural gas at an industrial scale.

completes acquisition of Alumina Ltd

Alcoa Corporation have announced the successful completion of its acquisition of Alumina Limited (“Alumina”). This strategic move positions Alcoa to further strengthen its market leadership as a pure play, upstream aluminum company.

“Alcoa is proud to announce the completion of our first major acquisition. The acquisition of Alumina Limited strengthens Alcoa’s position as one of the world’s larg-

est bauxite and alumina producers and is expected to result in longterm value creation from greater financial and operational flexibility,” said William F. Oplinger, Alcoa’s President and CEO.

With Alcoa’s acquisition of Alumina, the Alcoa World Alumina

and Chemicals (AWAC) joint venture is now fully owned and controlled by Alcoa. Alcoa previously held a 60 percent ownership interest in AWAC. AWAC consists of a number of affiliated entities that own, operate or have an interest in bauxite mines and alumina refineries in Australia, Brazil, Spain, Saudi Arabia and Guinea. AWAC also has a 55 percent interest in an aluminum smelter in Victoria, Australia.

The Queensland Government and Rio Tinto will work together to safeguard a pillar of the State’s heavy industrial manufacturing base around Gladstone under a partnership to support investment in renewable energy projects. The agreement announced represents an important step towards securing a long-term future for Australia’s secondlargest aluminium smelter, Boyne Smelters Limited (BSL) and thousands of jobs in central Queensland supported by the operations.

First

LME

brand producer

builds enhanced digital link to LMEpassport

The London Metal Exchange (LME) have announced that Emirates Global Aluminium (EGA) has become the first LME primary aluminium brand producer to build a digital certificate of analysis (CoA) connection directly from its smelters to the LMEpassport platform – removing the requirement for paper documentation and further innovating the future of aluminium production.

European aluminium foil rollers see continuing weak demand in Q1 2024

Figures for European aluminium foil deliveries in the first three months of 2024 indicate that weak demand continue to have a negative impact on volumes.

Total shipments reached 217.800 tonnes, a decline of 6,2% compared with the same period in 2023, according to the figures just released by the European Aluminium Foil Association (EAFA).

European demand fell 3% in the first period of 2024, while

exports plunged 26,6%, continuing the difficult overseas market conditions seen throughout 2023, where sales were down 22% year on year.

While overall inflation is now under control, continuing high interest rates and the ongoing effect of higher prices for consumers has led to very fragile demand in some sectors where foil is used. In addition, supply chain issues, particularly for raw materials, has led

to a slowdown in deliveries to traditional markets such as construction and automotive.

Thinner gauges, used mainly for flexible packaging and household foils, which is generally seen as a more resilient sector, saw sales down by 7,7% compared with Q1 2023. Inside Europe the decrease was 4,1% and overseas markets saw demand drop by more than 30%.

Suez and Alupro announce partnership to increase aerosol recycling

SUEZ recycling and recovery UK has entered into a two-year partnership with Alupro as part of a roadmap to increasing UK aerosol recycling rates.

An estimated 650 million metal aerosols are used in the UK each year, with over 80% of these used in the home. Upcoming reforms to packaging recycling in the UK, including a deposit return scheme for drinks containers, Simpler Recycling in England and Extended Producer Responsibility (EPR), present an opportunity for the metal packaging sector to redouble their efforts to push metal recycling rates even higher than they are today (the aluminium packaging recycling rate for 2023 was 68%.)

The project aims to provide

data and case studies on how to increase the capture, sorting and treatment of aerosols. The first phase, over the coming 12 months, will see SUEZ recruit three local authorities in different areas across the UK to monitor and analyse aerosol capture rates, ready for the next phase of the trial to start in 2025. The next

phase of the trial will see a yearlong sampling exercise measuring the quantities of aerosols collected through both the residual and recycling kerbside streams, as well as looking into the challenges of sorting and analysing aerosols collected through the kerbside system. Further, the year will see the trialling of a brand new communications campaign to consumers to boost aerosol recycling.

Through this partnership, SUEZ and Alupro will work together towards their goal of consumers recycling all their empty aerosols responsibly in their household collection service, with confidence that this will result in their packaging waste being collected, sorted, recycled and transformed into something new.

Constellium Muscle Shoals receives Department of Defense grant

Constellium announced that its facility in Muscle Shoals, Alabama has been selected by the U.S. Department of Defense (DoD) for an investment of $23 million under Title III, Defense Production Act to rebuild its Direct Chill aluminium casting center.

The funding was awarded via the Defense Production Act Investments (DPAI) Program. DPAI is overseen by the Manufacturing Capability Expansion and Invest-

ment Program (MCEIP) in the Office of the Assistant Secretary of Defense for Industrial Base Policy. Constellium will use the funds to install state-of-the-art casting equipment on the site of a dismantled casting center intended

2024 DIARY

SEPTEMBER

25th - 27th

IBAAS

The 12th International Bauxite, Alumina & Aluminium Conference & Exhibition, in collaboration with The Indian Institute of Metals (IIM). Stay updated on the latest industry trends, challenges, and opportunities through engaging discussions and presentations. Held in Goa, India www.ibaas.info/

OCTOBER

8th - 10th

ALUMINIUM 2024

ALUMINUM is the world’s leading trade fair and B2B platform for the aluminum industry and its main user industries. The focus of the trade fair is on solutions for automotive engineering, mechanical engineering, building and construction, aerospace, electronics, packaging and transport.

Held in Düsseldorf, Germany www.aluminium-exhibition. com

27th - 31st

ICSOBA 2024

The 42nd International Conference and Exhibition of ICSOBA is returning to the home turf Paul Héroult and the place of one of the first plants where Karl Josef Bayer implemented his patented process of alumina extraction from bauxite.

Held in Lyon, France www.icsoba.org/2024/

29th October

Women With Metal Conference

to add up to 300 million pounds of annual casting capacity.

“This investment under the Defense Production Act will enable our industry to meet the rapidly increasing demand for the aluminium products needed not only for our national security, but also necessary for the overall U.S. manufacturing sector and a healthy economy,” commented Buddy Stemple, President of Constellium Muscle Shoals.

Women With Metal is dedicated to creating connection between all women and allies working within the metal sectors. The annual conference provides knowledge to help you flourish in your career and aims to give you the confidence to shine. Held in Birmingham, UK www.womenwithmetal.com

For a full listing visit www.aluminiumtoday.com/ events

VISIT US AT ALUMINIUM 2024

Meet our Coil Coating Specialists Jakob Søndergaard and Ronnie Skov at Aluminium 2024 in Düsseldorf October 8 –10. You’ll find them in Hall 4, Stand 4F40.

Metalcolour proudly presents products from its Technical Coating area. Metalcolour Technical Coating is a highly specialized division offering customized solutions in coil coating of numerous metal substrates with own developed or customer specified primers, binders and coating. The solutions developed typically have

several purposes in a combination of technical requirements and high volume production. Main part of our clients utilizes Metalcolour to industrialize processes in order to take advantage of economies of scale in decreasing cost per unit. Great savings has been generated by solutions from Metalcolour Technical Coating.

Do you want to set up a personal meeting? Scan

SOLUTIONS SINCE 1913

Mixed fortunes for bauxite production

Michael Schwartz* looks at the US bauxite sector and analyses recent events in Brazilian bauxite.

Figures for last year’s global bauxite production have been released by the United States Geological Survey (USGS) although figures for bauxite production in the USA were withheld for reasons of commercial confidentiality. The USGS compiles crucial statistics and it is this organisation’s National Minerals Information Center (NMIC) that has answered Materials World’s US-oriented questions.

The USGS figures not only show that US domestic consumption of bauxite in 2023 continued a decline in production - which has led to a halving of domestic consumption since 2019 - but also a decline of 17% over 2022 to 1.8 Mt. While such a decline cannot be confined to one single factor, downstream uses in automotives and manufacturing in more general terms are negatively influencing output. Again, taking USGS figures, over the last five years, US bauxite consumption has been over 75% reliant on imports, Jamaica supplying 64%; US bauxite exports are minimal.

In the US, NMIC pointed out to Materials World, bauxite is mined from small deposits generally comprising a mixture of bauxite and bauxitic clays. One perhaps surprising aspect is that, “domestically mined bauxite is used for non-metallurgical uses, such as abrasives, cement, chemicals, proppants and refractories. All metallurgical-grade bauxite consumed in the US is imported.”

The NMIC was asked whether the USA had taken any steps to lower or remove altogether bauxite imports: “There are no policies designed to remove or lower imports of bauxite. Bauxite imports from countries with normal trade relations are not subject to tariffs.” In fact, the USGS

the US’s bauxite needs are met domestically.

Alternatives to bauxite…

In the USA bauxite is the only raw material used to produce alumina (that is, the oxide of aluminum that occurs both naturally as corundum and also within bauxite and which is used as a source of aluminum.) Kaolinite and other aluminacontaining clays are technically feasible as sources of alumina but are not currently economical; other potential but to date little-exploited sources of alumina include alunite, anorthosite, coal wastes and oil shales. The aluminum industry continues to study this issue and is making progress towards a solution.

…and import challenges

Materials World asked NIC whether bauxite importing is a stable process or if there are supply and logistics problems: “Currently, metallurgical-grade bauxite imported to the USA is largely sourced from Jamaica and shipped through the Port of New Orleans. In the past, hurricane activity has caused the ports in New Orleans and in Jamaica to temporarily shut down, leading to shipping delays. The alumina refinery owned by the Atlantic Aluminum Company LLC (Atalco) at Gramercy, Louisiana, briefly shut down during hurricane Ida in 2021, although it was done as a precaution and not because of shipping disruptions. Atalco’s bauxite source is a bauxite mine located in Jamaica, which it owns along with the Jamaican government. According to the company’s website, the mine has a 5.2 Mt/y capacity, which exceeds the 1.2 Mt/y capacity of its alumina plant.

3In April last year, mining giant Glencore

*Correspondent

acquired a 30% stake in Alunorte, the world’s largest alumina plant outside China, along with a 45% share in Brazilian bauxite producer Mineracão Rio de Norte (MRN.) Under the new acquisition Alunorte will be 62% owned by Norsk Hydro and 30% by Glencore with the remaining 8% owned by four minority shareholders; MRN itself is now a JV owned 45% by Glencore, 33% by South32 and 22% by Rio Tinto.)

One key change is that bauxite purchased by Glencore from MRN will be supplied to Alunorte, the latter reducing its intake from the Paragominas bauxite mine, which is wholly owned by Norsk Hydro. Materials World took this opportunity to ask MRN’s chief executive Guido Germani about recent changes, notably technological innovations, at the mine. He replied: “MRN has followed the path of modernisation by improving processes and adopting technologies for more sustainable and safe mining. One of our most recent innovations is the Dry Waste Disposal Method in Pits. In the conventional process, wastewhich comprises water and soil without the addition of chemical additives - is deposited in dams. In dry disposal, the material is filtered and the liquid is drained. The water is then reused or treated and returned to the environment, while the waste is used to fill pits.

“The land that houses the tailings is stable, safe and reintegrated into the environment and native landscape. The technique, also known as Tailing Dry Backfill, avoids the need for dams and vegetation suppression, reinforcing operational safety for workers and communities, in addition to environmental

estimates that less than 5% of

Additional information from USGS shows that mining of metallurgical grade bauxite largely ceased in the 1980s due to depleted bauxite reserves. Known deposits of bauxite in the US are not considered to be of high enough grade or large enough size to sustain commercial production of metallurgical bauxite. Generally, crude bauxite is beneficiated to meet required specifications for the manufacturing of alumina. The US aluminium industry has researched beneficiation requirements of domestic bauxite, although NMIC is not aware of any such research conducted by the US government.

sustainability. The dry waste process in pits is one of the distinguishing features of the Novas Minas Project (PNM) through which MRN intends to extend its activities for 15 years.

“We also highlight our participation in Mining Hub, the first open innovation hub for the mining sector in the world, where we even have a representative in the presidency of the Board. This has been essential to align actions that support increasingly modern and sustainable mining. The company started structuring an innovation area a few years ago due to the need to integrate this ecosystem and to learn different methodologies that encourage the energy transition with innovative solutions.”

Transportation and exports

Guido Germani outlined to Materials World the mining process at MRN, stressing its complexity and the need for careful management, from ore extraction to processing. Bauxite, he explained, is extracted from plateaus using techniques that seek to reduce the impact on the environment as much as possible, followed by transportation of the ore to processing and shipping facilities (involving the implementation of advanced systems to ensure that waste is treated and disposed of responsibly) while minimising environmental risks and promoting sustainability. Conveyor belts and wagons are used within the operations. Ship transport is used to access customers.

Germani continued: “MRN plays a significant role in Brazil’s bauxite industry. According to data from the National Mining Agency (ANM) of the Ministry of Mines and Energy (MME) and the USGS, Brazil has the fourth largest bauxite reserves on the planet, with around 2,700 Mt mapped until 2023. MRN is the largest

Brazilian producer, responsible for more than 90% of Brazilian gross production. The company supplies 64% of the Brazilian market. The remainder is exported to North America (19%), Europe (7%) and Asia (10%).”

Decarbonisation a priority…

For Germani, “The challenge of mining with sustainable practices in the Amazon is ongoing and MRN continues with initiatives to reduce the carbon footprint of its operations. The change in the use of the energy source of its plants to electrical energy is one example. The installation of the Transmission Line (a key MRN project for future operations) is one of the main projects to carry out an energy matrix transition, contributing to reducing the socio-environmental impact of global warming.”

With the project coming into operation in 2027, the company estimates a reduction in CO2 emissions of around 19% of all emissions, in line with the Paris Treaty and highlighting MRN’s ESG agenda. Additionally, MRN has joined the decarbonisation project for the mineral sector, with the purpose of identifying opportunities to reduce greenhouse gases in industrial processes and encourage the energy transition.

…as is training local personnel MRN stressed to Materials World its commitment to the communities near its operations, with MRN and its suppliers working to develop sustainability projects that can benefit the region. Initiatives include those in qualifications, training, education and alternatives for increasing income generation. The aim is to connect the needs of the population with the demands of local employability. Currently, MRN offers development opportunities

such as:

� Open Doors, its programme with affirmative vacancies for local communities. It offers various employment opportunities within its administrative area and is aimed at quilombolas (descendants of rebel slaves) and riverside dwellers. Courses include finance, HR, commerce, operations, maintenance and sustainability;

� scholarships for higher education courses in administration, accounting and related areas for those who do not yet have relevant degrees;

� Young Apprentice, whereby MRN offers first professional experience for people over 17;

� Basic Education Support Program, which allows access to basic private education. In addition to the monthly fee, students receive logistics (boats and buses), food, uniform, teaching and school materials and after-school support. It benefits the Boa Vista quilombolas territory and two riverside communities, costing just over US$1 million in 2023; and

� Program for Education in the Amazon, whereby MRN also offers education and professional qualifications in other locations. Since 2022, 368 students have already benefited from over 4,700 hours of coursework.

Conclusions

It is clear that changes are well underway in the Brazilian bauxite sector. Changes in US bauxite production are tending towards major reductions in output; it is unclear when this decline will stop. �

Bauxite boom: Responsible mining for people and planet

By Matthew Groch*

The rapid shift towards electric vehicles (EVs) is a cornerstone of the global strategy to reduce carbon emissions. However, the surge in demand for aluminium, a key material for electric vehicles, is causing significant environmental and social impacts. This presents a critical challenge in the race towards a greener future with electric vehicles: how can the urgent need for sustainable transportation be balanced with the urgent need to protect communities and ecosystems?

The need for effective ethical aluminium sourcing

The world’s leading automakers are heavily promoting their electric vehicles as a greener alternative given zero tailpipe emissions; however, green motoring means more than just going electric. A critical consideration is the sourcing and sustainability of materials used in these vehicles.

Aluminium is pivotal in electric vehicles production due to its lightweight and durable properties that enhance fuel efficiency and extend driving ranges. As a result, electric vehicles use significantly more aluminium than gas-powered vehicles, with battery electric vehicles using about 85% more aluminium.[1] Currently, car manufacturers account for approximately 18% of the world’s aluminium production, and this demand is expected to double by 2050.[2]

The demand for electric vehicles is still high

Quarterly electric car sales tend to decrease from Q4 to Q1 each year, leading some to incorrectly conclude that the demand for electric vehicles is slowing. This, however, is the wrong comparison as it does not control for seasonality. A more appropriate comparison would be to analyse the first quarter of 2024 to the first quarter of 2023. Using this methodology, sales of electric vehicles grew by 25%. In absolute numbers, this means that more than 3 million electric cars were sold in the first quarter of 2024, continuing its year-toyear growth trend from 2023, according to the International Energy Agency,

an autonomous intergovernmental organisation.[3]

Assuming this growth trend, it’s imperative to plan for a future with high demand for EVs. The challenges associated with aluminium sourcing will not only persist but will also intensify, leading to greater environmental and community impacts. The unrelenting quest for more aluminium derived from mined bauxite has led to real consequences for the communities and environment surrounding the mines. Bauxite is found in the ground, largely under the forest floor. Miners generally use heavy machinery to strip large surface areas to access the bauxite, which can cause significant

Director for Heavy Industry Decarbonisation

*Senior

at Mighty Earth

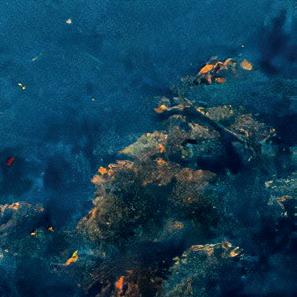

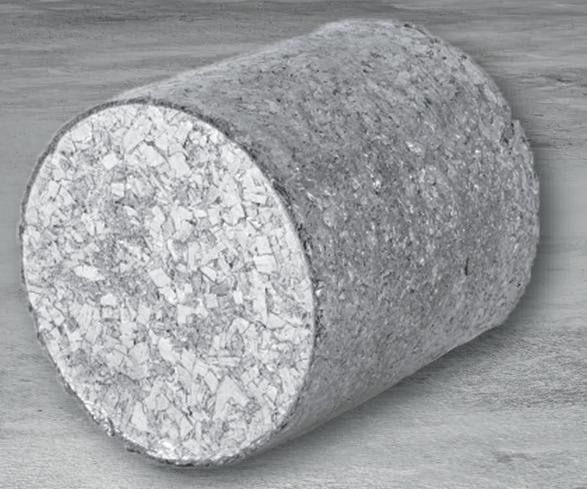

Aerial view of Hydro Alunorte, a world-renowned alumina refinery. Alumina is the raw material for aluminium and is produced from bauxite ore Credit to: Tarcisio Schnaider

Former bauxite mine in West Kalimantan, Indonesia Credit to: Rdt Radihan

deforestation if the bauxite is in biodiverse or forested areas, and the runoff from this open cast mining can lead to the pollution of rivers, streams, and other bodies of water.

In addition, the aluminium sector is responsible for 1.1 billion tons of carbon dioxide pollution per year, about 2% of global emissions. More than 60% of the aluminium sector’s emissions are from the electricity, most derived from coal power, used during the smelting process. As a result of turning bauxite into aluminium, current mining practices have uprooted the lives of those living near the mines and the forest floors surrounding the mines.

A review of bauxite mining’s impact on people & planet

Mighty Earth’s recently released report, “The Impact of the Bauxite Boom on People and Planet” [4] is the first report to take a global look at the bauxite and aluminium industry by reviewing and combining all available literature on the industry and its impact on people and the environment for four specific countries: Australia, Brazil, Guinea, and Indonesia. Each of these countries have substantial reserves of bauxite, and each country has incorporated their vast reserves of bauxite into its pursuit of economic development. The people living closest to the mines in Australia, Brazil, Guinea, and Indonesia have protested, filed lawsuits, and advocated for better treatment and healthier environments. This report helps amplify the plights of these individuals. In Indonesia, the government passed laws restricting public criticism and protests against mining companies. One such law states that “anyone who hinders or disturbs mining activities by permit holders who have met the requirements … may be punished with a maximum prison term of one year and maximum fines of 100 million rupiah [$7,000].” [5] Initially seen as a warning, it has been used in

practice to silence criticism. In 2021, 10 people were charged with violating this specific provision, out of 53 total people accused of opposing mining companies.[6]

A Bloomberg report found that much of the aluminium used in the Ford F-150 sold in the United States originated from northern Brazil, where a large mining company dominates aluminium production. This company has been accused of toxic metals pollution in surrounding rivers and streams, which provide water and food for locals. According to one estimate, waterways were “at levels 57 times greater than what health experts consider safe.”[7] Byproducts of the mine are so prevalent that medical staff found at least one woman had “175 times the amount of aluminium considered safe in her hair.”[8] Although the company was faced with monetary penalties in the past by the Brazilian government, local residents remain dissatisfied and have filed a lawsuit in the Netherlands.

In West Africa, residents from 13 Guinean villages in 2019 filed an official complaint alleging that a large bauxite miner had violated their rights and did not provide adequate compensation to locals. The complaint was filed against the International Finance Corporation, a division of the World Bank, which provided a $200 million loan to a mining company. [9] Three nonprofit organisations filed the complaint on behalf of the villages, vividly expressing the negative impact of bauxite mining on their communities:

“Complainants state they have witnessed an unprecedented decline of wildlife and even the total extinction of some species in the region. They believe that water pollution as well as the impacts of mining infrastructure, notably mining roads and the railway lines crossing fields and forests, are probably the main causes. The decline of animals and fish has also significantly contributed to the degradation of livelihoods since communities largely depended on fishing and hunting, in addition to agriculture.”[10]

Similar destruction is also taking place in Australia, where the Western Australian Government recently approved a mining company’s plan to clear 800 hectares a year for mining.[11] This land is widely recognised as the world’s most biodiverse temperate forest, housing 800 plant species and 10 endangered animal species.[12] A new study found that, “The primary cause of deforestation in Western Australia’s Southwest forests is bauxite mining...Bauxite mining has cleared at least 32,130 hectares of publicly owned forest...and fragmented 92,000 to 120,000 hectares of the Northern Jarrah Forest up to December 2019, and the rate is accelerating.”[13]

The impact of bauxite mining and

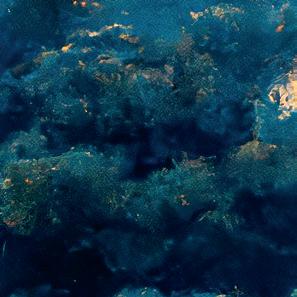

Red mud - toxic residue of aluminium production polluting the soil on huge area. Guinea, Africa. Credit to: Igor Grochev

Mighty Earth and local climate organisers perform a dance at the NYC International Auto Show, urging Hyundai to clean up their auto supply chains as the industry transitions to EVs Credit to Jeremy Varner

aluminium production in each of these countries – Australia, Brazil, Guinea, and Indonesia are significant but can be mitigated. Automakers purchasing aluminium and government regulatory bodies have the power to drive this change. The demand for minerals such as bauxite and aluminium will continue to increase as they become more important in the transition to a decarbonised world. With the rapid increase in electric vehicle production globally, it’s more important than ever to ensure aluminium is sourced responsibly from bauxite mines.

are challenging the world’s leading automakers to adopt ethical practices throughout their EV supply chains. Global campaigns around the world have been pressuring the world’s leading industry to invest in environmental sustainability and take social responsibility in their operations. They are also urging manufacturers to ensure that the sourcing of materials does not come at the cost of human rights or environmental degradation.

There is a path forward for responsible mining of bauxite and the production of aluminium. Electric vehicle manufacturers and other downstream manufacturers

can play a significant role in raising the standards for their supply chains, and national and local governments should strive to ensure their local constituencies are protected from the negative effects of bauxite mining. The transition from traditional vehicles to electric vehicles should reduce emissions and pollution and make the world a cleaner place. It is the responsibility of governments and automakers to make sure that local and Indigenous communities are not made worse off in the transition, and responsible mining means precious forests, peatlands, and the environment are protected. �

Take speed and stability to the next level

The Thermo Scientific™ ARL iSpark™ Plus Series OES Metal Analyzer uses single-spark acquisition to provide rapid elemental analysis—up to 15% faster than previous models. The increased speed and reliability minimize tap to tap times, save energy, reduce carbon footprints, and realize a faster return on investment.

Capable of providing ultra-fast, on-line analysis of nonmetallic inclusions, the ARL iSpark Plus adds to the versatility, dependability, and productivity of metal processing operations.

A Richards Consulting Ltd (ARC) awarded contract by Hulamin

� Increase maximum strip width capability of the mill to 1875 mm

� Higher material temperature capability from faster, back-to-back rolling

� Improved strip quality including: � New flatness sensor incorporating load cells � New strip scanner heads

� New spray system � New enhanced ARC strip dryness system � An upgraded optical centre guide system

� A new, ARC designed compact 3-roll entry bridle with colouring roll

� A new oil-air lubrication system for the mill

� Upgraded spool handling to cater for dual spool lengths

In September 2023, HULAMIN awarded the contract for the widening of their S5 aluminium cold rolling mill to A Richards Consulting Ltd (ARC). This followed one of several engineering studies carried out by ARC and resulted in the S5 widening project being awarded against a tight deadline to complete Phase 1 by December 2023 ready for board approval. This was immediately followed by Phase 2 which will see the widening project designed, manufactured and implemented by the second quarter of 2025.

Wider Strip Processing

Increasing the maximum strip width will open new markets to HULAMIN and allow the S5 mill to focus on processing wider, 14out high quality can stock material. In addition, this will enable better distribution of product across all areas of the plant thereby increasing the overall plant utilisation. The main component of this upgrade being a new entry bridle with colouring roll designed and supplied by ARC, which not only allows the wider material to be processed but also includes features to ensure accurate roll positioning, stable tension control and ease of maintenance.

Also included are new, longer work rolls and back up rolls with new bearing arrangements and the associated chock modifications to accommodate the increased width and higher operating temperatures.

The ARC design caters for increased strip temperatures and speeds but also meets the challenges of accommodating the new surface inspection cameras, strip scanners, strip dryness equipment and flatness measurement system in an already congested area of the mill.

Mill Upgrades

Upgrading a rolling mill is often necessary when introducing a new product and provides an alternative to investing in completely new equipment. Upgrading is also a cost-ffective solution to updating old or obsolete technology and can also minimise the loss of production associated with replacing equipment with new. However, this is a very specific area of expertise and one which requires the highest level of know-how.

Such is the case with the HULAMIN upgrade, where ARC has designed the new and upgraded equipment and planned the implementation to minimise the loss of production and disruption to the plant. The ARC team has many years of experience in modernisations and upgrades of rolling mills and processing equipment for the steel, aluminium and other nonferrous industries.

Working closely with HULAMIN over the past year or so, ARC has been able to provide insight into the process aspects of this upgrade, analysis and evaluation of different solutions. ARC also provided CAPEX estimates for the design, supply and implementation and now the full design, supply and supervision of installation & commissioning of the new upgraded S5 cold mill.

Aluminium Supplier to Africa and the World

HULAMIN is not only the largest aluminium rolling operation in Sub-Saharan Africa, but is one of the largest exporters, which represents more than 60% of sales. Aluminium semi-fabrication in the form of plate, sheet & foil is supplied to customers across South Africa, Africa and the world focusing on specific product and end-use markets such as automotive, packaging, transportation, building and electrical applications. �

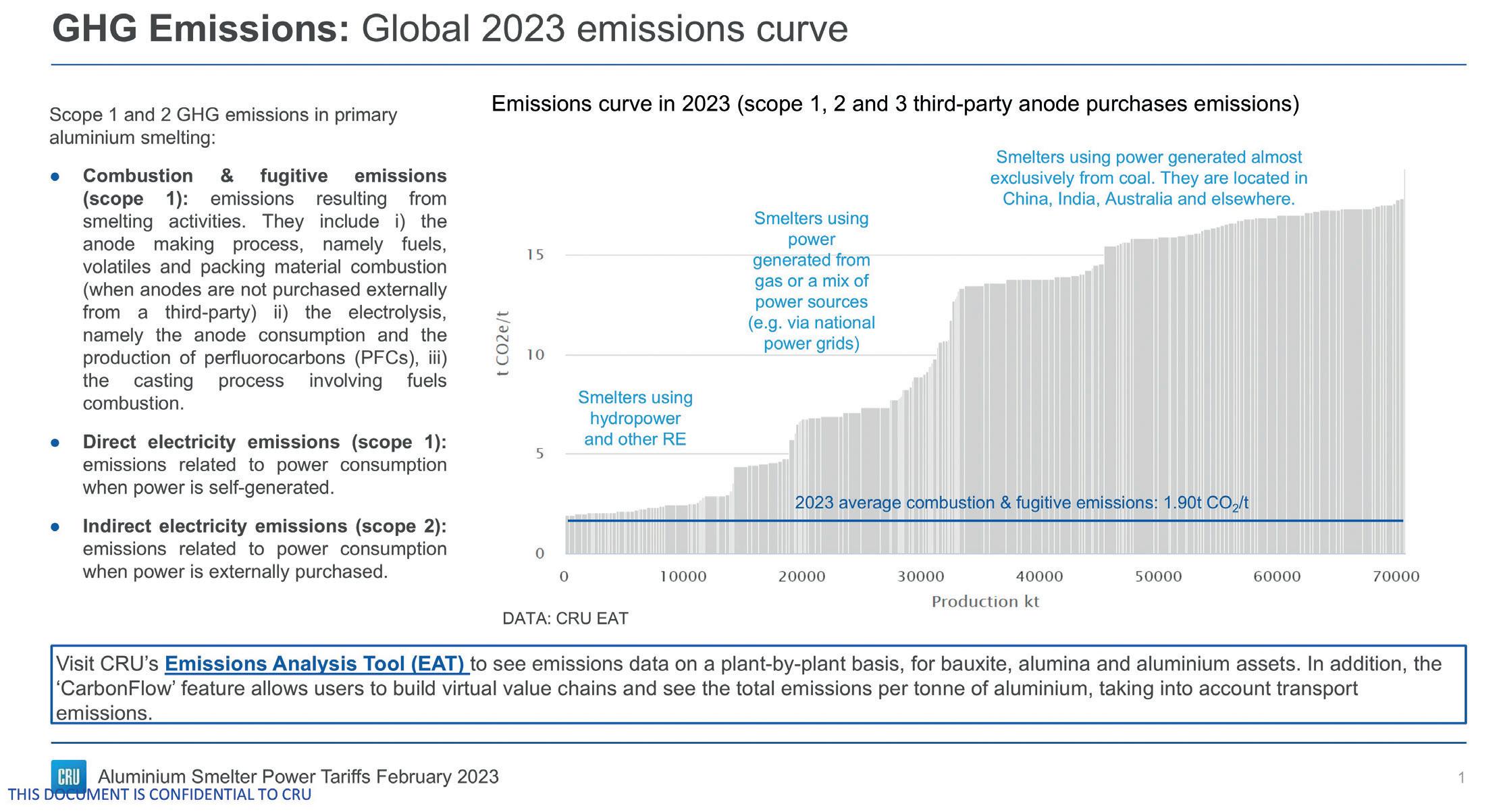

Is the industry on track with decarbonisation?

Is the industry on track with decarbonisation?

By Paul Williams*

The aluminium industry has begun a path towards decarbonisation, although there is still a long way to go.

Aluminium emissions across the value chain reflect bauxite mining, alumina refining, aluminium smelting, and downstream processing. Across the upstream value chain, CRU calculates that the industry’s average emission intensity in 2023 was 13.13t of CO2/t of aluminium produced, down from 14.31t in 2018. This includes emissions in the production processes, known as Scope 1 emissions, as well as the power used in the smelting process, known as Scope 2 emissions. These emissions in the power source have the greatest variation depending on whether the fuel is a renewable source of fossil fuel source, particularly coal. CRU estimates that China produced 72% of all emissions in the primary aluminium sector in 2023, followed by India with approximately 9% of all emissions, due to their reliance on coal.

To achieve further significant reduction in the average intensity we will not only need to move as much as feasible to renewable power, but increasingly apply innovative technologies and embrace continuous increases in the use of recycled metal.

Net zero now needed by 2034 to meet 1.5°C target

The stark need for industrial decarbonisation is evident in CRU’s Sustainability Division’s determination that the world now needs net zero by 2034 to meet the 1.5°C target. And at

current rates, commodities are currently on a 2.5°C temperature pathway at best out to 2050, which is a level deemed not to be within safe limits.

The aluminium industry only represents about 3% of global carbon emissions yet has an extremely important part to play in limiting the scale of climate change, as a lightweight material.

As noted, this can come from power source shifts and technological change in the primary metal production process, together with greater use of recycled metal. A key driver will be end-user market requirements, which will increasingly demand low carbon aluminium metal.

This raises the question of what is considered low carbon primary aluminium and what will incentivise its increased supply? There is no recognised definition, but one that CRU uses, and which forms the basis of our low carbon aluminium premiums assessments, is that of primary metal aluminium produced under 4.0t of CO2/t for Scope 1 and 2 emissions together with Scope 3 emissions for purchased third party anodes.

The accompanying chart, produced from CRU’s propriety emissions analysis tool (EAT), shows our primary aluminium emissions curve for 2023 and shows the production and typical location of smelters of 4.0 tonnes of CO2 and below (low carbon), that capacity which is considered mid-level carbon (in the second part of the chart) and smelters that are high carbon. On an average smelter basis, as shown in CRU’s EAT curve below, 14.26Mt of smelters are low carbon.

*Head of Aluminium at CRU

However, if you assess low carbon as based on % share of different power sources, then 23.8Mt of production can be identified as low carbon (renewables plus nuclear) incorporating smelters in Canada, Russia, Europe, America, and in Asia, which in recent years has increasingly come from China. Outside of China low carbon production reached 14.6Mt.

Indeed, the total low carbon production has increased with the continuing shift in power from coal based in China towards hydro power, especially in provinces such as Yunnan. In 2018, China’s power sources were 87% coal, 11% hydro, 2% other renewables and 0% nuclear. As of 2023, it was 78% coal, 15% hydro, 7% other renewables and 0.5% nuclear, and we expect renewable share to rise to 37% by 2033 in China.

To meet growing requirements in the future, it appears inevitable that production based on fossil fuels will continue to thrive, not least as availability of stranded low carbon power will simply not be sufficient. Indeed, in many regions and countries the competition for available renewable power will intensify between industries.

Demand for low carbon metal to rise – but by how much?

Increasingly key end-users across automotive, packaging and electronics will demand low carbon aluminium (whether that is from primary based metal, or from recycled aluminium) and we expect the fastest growth to come from these sectors. However, demand

for low carbon aluminium will rise across all sectors including construction and consumer goods.

In the case of primary metal while we do not see demand for low carbon material exceeding supply now, the market is likely to get tighter as demand grows. Europe is the region that will see demand rising the fastest and where a low carbon premium will be established first. Indeed, our latest assessments indicate that low carbon ingot premiums are around $15/t, but some value-added shapes command a higher premium, for example PFA at $30/t.

CRU has looked at what is a likely pace of growth in low carbon aluminium demand over the next decade for our long-term market report. And as a base view we see consumption for low carbon aluminium outside of China rising from 2 million tonnes to over 12.8 million tonnes by 2032 – about 35% share of demand.

As we have shown from our emission curve above, the availability of low CO2 aluminium exceeds current demand levels in the world ex. China. But this surplus will shrink significantly over time as growth in renewable capacity is going to be slower in our view. Of course, even that assumes Russian metal is available in the market. Current sanctions and industry self-sanctioning means that for now this metal is unavailable or increasingly unavailable in North America and Europe. The unavailability of Russian metal will tighten the market for low carbon metal far faster and yield a significant rise in the low carbon premium.

How fast can the industry continue to decarbonise?

One of the other reasons why the balance for low carbon aluminium will tighten is that its supply is not growing that fast.

Aluminium smelting capacity can only grow where availability of power is abundant, and low carbon capacity can only grow where renewable power is available. Capacity sourced from fossil fuels will continue to grow while capacity from renewable power (outside of China) appears only likely in South America, Russia, and North America at present. In China smelters in Western China, such as in Inner Mongolia, Xinjiang, Qinghai plan to invest in more renewable power in the next few years.

However, significant new capacity powered by renewables is not yet in sight, while potential Russian expansion projects are less likely in the current geopolitical environment.

So, with the potential to decarbonise more through significant growth in new capacity fuelled by renewables limited, how will the industry decarbonise? Below we discuss several of the pathways the industry is taking, some quicker than others.

� Increased use of renewable energy at existing smelters: Existing smelters will increasingly use more renewables in their mix. Over the last few years, we have seen producers shifting to low carbon power sources, which was unseen before. EGA, for example, is now using solar power in its mix with plans

to increase consumption depending on demand for low carbon aluminium.

Wind has also become competitive in places. In Norway, both Alcoa and Hydro have secured long-term PPAs (purchase power agreements), even if the country benefits from abundant hydropower resources. At the same time battery storage for large scale electricity will become a feature.

At casthouse and carbon bake furnaces and in alumina refineries the use of hydrogen is likely to be adopted.

� Innovative technologies will (need to) be adopted to lower emissions:

� Inert anodes

The inert anode technology can reduce emissions because in this process the carbon anode would not be consumed during the main reaction and therefore CO2 would not be created, instead oxygen would be emitted.

It is still not yet commercially available however, despite decades of research. When commercial production is achieved it will first be implemented in green field projects rather than being retrofitted because of design differences. This means opportunities are likely to be limited and progress towards reducing worldwide emissions slow.

� Carbon capture use and storage (CCUS)

Where emissions cannot be eliminated the industry will look at carbon capture and storage technologies.

� While waste heat capture and use

Integrated Lifecycle Partnership

To be the leading partner for our customers in this transformation, SMS group bundles all competencies from electrics/automation, digitalization, and technical service. Our goal is to maintain and expand the performance of our customers' plants throughout their entire lifecycle. Together with our customers, we develop integrated solutions speci cally geared to the customer's use case. In doing so, we focus on crucial KPIs such as plant availability, product quality, productivity, or delivery reliability but also on increasingly relevant topics such as sustainability and safety.

will also be developed.

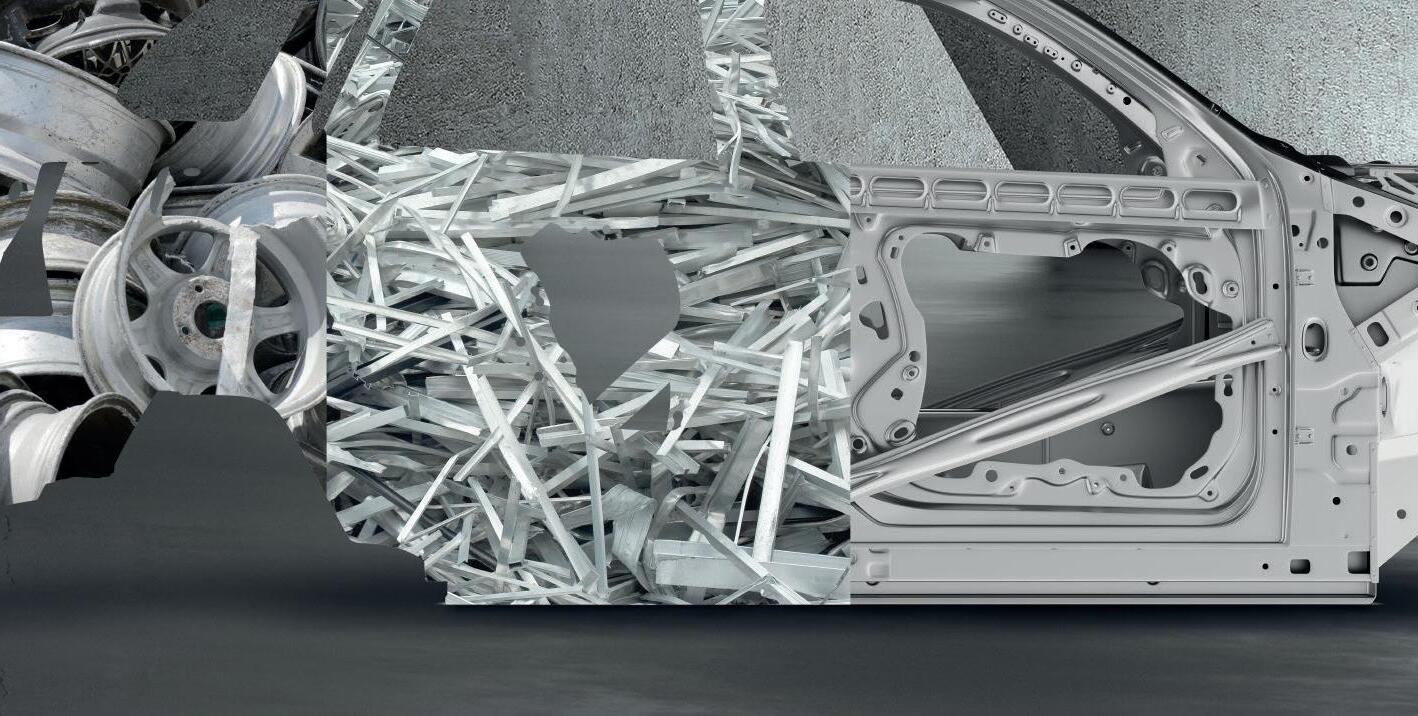

Is greater use of recycled metal the ultimate answer?

We are all aware that recycled metal uses 5% of the energy for primary smelting. Many end-users are demanding not just low carbon metal but also specifically asking for the recycled content in the metal they are receiving.

Very few emissions are emitted in the melting of scrap although debate still rages as to whether pre-consumer scrap should be given zero carbon status alongside that of post-consumer scrap, or whether it should have the same carbon content as the metal that produced it.

Assuming all scrap has zero carbon content, it is clear the greater the recycled metal content the better in terms of the carbon footprint. For recycled metal content to increase significantly, collection rates of post-consumer scrap will need to rise while improved sorting technologies need to develop to fully commercialise the use of the scrap. CRU’s detailed scrap analysis has shown that the use of post-consumer scrap remains low in downstream production (outside of beverage can sheet).

There is enough potential scrap that is available post consumption, but collection rates will need to rise, either through legislation or greater consumer environmental awareness. The main and most challenging bottleneck has historically been and will remain sorting and alloy segregation. Alloy sorting processes remain inefficient, expensive, and inadequate to upgrade lower-quality mixed scrap grades to higher-quality wrought alloy grades in meaningful volumes. If this challenge is overcome the use of post-consumer scrap in metal mixes will be able to rise significantly and support significant reductions in the average emission intensity of aluminium.

What will the future bring?

The start of this paper posed the question whether industry decarbonisation plans are on track, and relative to what we believe the target needs to be for all industries to meet to limit the temperature rise to 1.5°C - which is net zero by 2034then the answer is no.

The industry is continuing to decarbonise primary production through shifts in power mix and will begin to embrace innovative technologies to further lower

process emissions. The extent to which it will lower average intensity will be constrained by availability of renewable power, and by 2033 we expect average intensity to have fallen to ~11.6t of CO2 per tonne of aluminium.

Low carbon premiums will be established and rise which will support efforts to decarbonise although again access to affordable renewable power will constrain. The carbon border adjustment mechanism (CBAM) is still coming in the EU but as of now still only includes Scope 1 emissions. If it were to include Scope 2 emissions that would be a game changer that would raise the price to incentivise more investment in capacity linked to renewable power (although at the same time likely to cause demand destruction).

What we will see is the continued increase of the use of post-consumer scrap. We expect post-consumer scrap collection rates to rise; reaching 74% in 2033 in the world compared to the current estimate of 63%. In 10 years, the share of recycled metal mix in the metal requirement will have risen to 45% outside of China, compared to 40% currently, and globally to 39%, up ten percentage points from the current level. �

At Air Products we’re helping customers transition to low-carbon fuels such as hydrogen, generating a cleaner future for us all.

We’re also reducing emissions by improving the efficiency of existing aluminium production plants.

Our Smart Process Advisor system is playing a key role in decarbonising the industry, ensuring furnaces are operating at peak performance. Visit us at Aluminium 2024, Hall 6, Stand M70 to find out more.

Or contact us to see how these innovative new technologies can help you achieve your most critical KPIs.

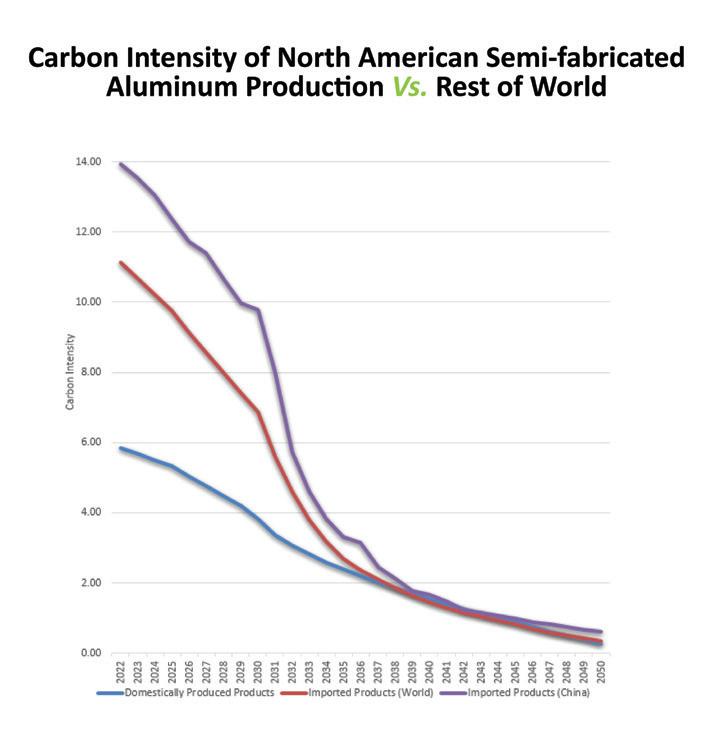

A new report from environmental consulting firm ICF and the Aluminium Association: Pathways to Decarbonization: A North American Aluminium Roadmap, highlights potential strategies to dramatically reduce carbon emissions in the North American (United States and Canada) aluminium industry by midcentury. The roadmap lays out theoretical pathways to achieve industrywide carbon emission reductions consistent with the International Energy Agency’s (IEA) Net Zero by 2050 goals. [1]

North American aluminium: Key to aluminium industry decarbonisation

Chuck Johnson* spoke with Aluminium International Today providing insights into the North American aluminium industry as well as details on the new roadmap.

1. “The report finds that the North American region has a significant first mover advantage in terms of its aluminium product carbon footprint –which is about 50% lower than global averages.” [1]

Could you give us a brief overview on the current position of North America when it comes to sustainable aluminium?

Chuck Johnson (CJ): The North American aluminium industry is healthy and growing, and decarbonisation of finished products that our metal is used in is helping to drive that growth. On the sustainability front, the aluminium industry is decarbonising our processes and our metal, and our major markets are using more aluminium to reach their own decarbonisation targets.

High value and infinitely recyclable aluminium is a material tailor-made for a more circular and sustainable economy. The energy and carbon impact of aluminium production in North America has dropped to its lowest point in history, declining by more than half over the last 30 years.

Secondary production (recycled aluminium) is already responsible for about 40% of North American automotive aluminium supply today (Source: ATG [2]). In fact, about 80% of all U.S.-based aluminium production today is using recycled aluminium. We are recycling more aluminium than ever here at home.

Aluminium helps transportation, packaging, construction and other sectors meet their sustainability objectives. So, it behoves us as an industry to stay at the forefront of making aluminium and aluminium products in the cleanest way possible – because it’s what our customers are demanding.

2. Why is the North American aluminium industry’s carbon footprint 50% lower than global averages? What insights can you give to the global audience?

CJ: It’s simple – North America uses more recycled metal than other global regions, and the primary metal that we do use is sourced almost exclusively from our partners in Canada, where it is made with hydroelectric power and is some of the lowest carbon aluminium on earth. Those two factors together, plus some other aggressive moves to source low and no carbon energy, add up to a regional carbon advantage.

Our investments over the past 30 years have set us up well for the next 30 years. Thanks to

3a. You announced the ‘Pathways to Decarbonisation: A North American Aluminium Roadmap’, could you explain why there was a need for this roadmap and what the roadmap aims to achieve.

CJ: Associations are the vehicle through which the industry comes together and works on collective issues—the Decarbonisation Roadmap is the perfect example of an issue that can’t be solved by any one organisation. This roadmap sets out plausible pathways that the industry can follow to reach Net Zero carbon emissions by 2050.

Both the International Aluminium Institute (IAI) and the Mission Possible Partnership (MPP) have done work to map the global industry’s pathways to netzero emissions that are in alignment with a 1.5 degrees Celsius pathway by 2050. The Aluminium Stewardship Initiative (ASI) has published ASI entity-level GHG pathways method and tool documents. At the regional level, European Aluminium (EA) has published a ScienceBased Decarbonisation Pathways for the European aluminium industry.

However, regionality matters here. The industry in North America has already done a lot of work to decarbonise in the past several decades, so the path forward for us looks different than much of the rest of the world.

The industry here is already well ahead of the game on carbon emissions compared to the rest of the world, largely due to our

heavy reliance on renewable hydropower, our well-established recycling system and the focus of decarbonisation by both the public and private sector. We thought it very important to have a Roadmap specific to our region that reflects this reality. Many of the strategies that global aluminium producers will need to take on are ones that the North American industry has already implemented or begun to implement, so we’re in a different starting place. A lot of the low hanging fruit has already been picked.

3b.What does 2050 look like and how do we get there?

CJ: A combination of technology development and policy interventions will be required to move us from here to there on the road to meet 2050 Net Zero emissions targets for North American aluminium production.

voluntary industry improvements and innovation like zero-direct carbon smelting technologies [3], access to clean energy and increased recycling, the average carbon emissions to produce a pound of aluminium in North America have declined by more than half since the 1990s.

Assuming the global aluminium industry commits to dramatic emission reductions efforts, it would still take 8 to 10 years for the rest of the world to produce semi-fabricated aluminium at the same carbon intensity as North America does today, and in that time, we will have raced ahead.

We must work together across borders and industries to continue these improvements. We’ve laid out some possible pathways in our recently released decarbonisation roadmap.

The International Energy Agency’s (IEA) aluminium data is considered as the net-zero aligned carbon “budget” for the global aluminium industry. Under the IEA’s Net Zero by 2050 scenario, global heavy industries are “budgeted” to have a total direct emission of 0.5 gigatons CO2e in 2050.

The industry is working toward the deployment of new primary aluminium production technologies that will eliminate all direct carbon emissions in the coming decades. Some of this work is already planned and underway. These technologies use various methods to eliminate all direct process emissions in making primary aluminium. The industry is working on new alumina refining technologies to reduce emissions in the production of alumina, the chemical building block of aluminium.

Aluminium producers are exploring new fuel sources including green hydrogen to power operations. The model assumes that up to 30% of aluminium industry furnaces will be electrified and 50% will transition to green hydrogen by 2050.

It is also fair to say that we can’t do this alone. Two thirds of the reductions in carbon intensity by 2050 that we need will come from reduction in our fuel sources – electricity and natural gas. We are partnering with these sectors and using the market power we have to push for investment in decarbonisation. We want to take responsibility for the energy we use, but many of these issues are ultimately outside our control.

Per the roadmap, carbon capture and sequestration (CCS) technologies will be used to capture emissions from existing primary aluminium plants and remaining gas-powered furnaces.

The scale and scope of this shift will depend heavily on availability and affordability of these new fuel sources and technologies in the coming decades, as well as public and private sector investments.

“provided

4. Investment is necessary for decarbonisation. A $6 billion federal investment in decarbonisation was recently announced. How do you think this investment will assist the industry.

CJ: We applaud Congress and the Biden administration for the passage of the Bipartisan Infrastructure Act, which provides significant investment in industrial decarbonisation. Facilitating more access to this kind of capital will be crucial, particularly for manufacturers deploying industrial decarbonisation technologies at facilities across the United States.

Already, we’ve seen this investment awarded to a variety of aluminium-specific projects including the potential construction of the first new U.S. primary aluminium smelter in 45 years; deployment of a first-of-a-kind zero carbon aluminium casting plant; construction of the first zero waste salt slag recycling facility in the U.S.; and technologies to reduce natural gas consumption, improve process efficiency and recycle 15% more mixed-grade aluminium scrap.

The government can also provide research and development incentives for clean aluminium production technologies in primary aluminium smelting, alumina refining, scrap melting, and semi-fabrication.

These investments will assist the industry’s progress, but we’d be remiss not to acknowledge the importance of the U.S. decarbonisation of the energy sector. Decarbonisation is not only the right thing to do for the planet and future generations, but also the right thing to do for our industry’s longevity. Fully two-thirds of the emissions reductions required to bring the industry to Net Zero will come from the energy sector. We think North America can help lead the way in moving the global industry forward.

5. “With North American primary aluminium accounting for about 6% of global production, a conservative estimate of approximately $60 billion in public and private investment for the region is needed to meet global netzero climate targets in the primary production segment alone.” The federal investment covers only 10% of the “conservative estimate,” how will the aluminium industry overcome this challenge. Do you have any advice regarding this, or alternatives that the industry can look to.

CJ: In total, only about one-third of the required emissions reductions by 2050 can come from improvements over which the industry itself has the most control. The other twothirds must come from a combination of newly developed, affordable manufacturing technologies; deployment of state and federal research and infrastructure investment; and a national policy that supports the clean energy transition.

To achieve these ambitious goals by mid-century, federal and state policymakers and regulators must do several things. First, the availability of abundant and affordable clean energy is paramount to industry’s decarbonisation success.

Regulators and policymakers must be serious about enforcing fair international trade practices. Further, by implementing monitoring that provides transparency about the carbon emissions embedded in international trade flows, we can more accurately track progress across the supply chain and ensure that the cleanest producers are not unfairly boxed out of the market.

Finally, we need state, local and federal actors to support policies and technologies that drive increased aluminium recycling. Recycling more aluminium more efficiently can dramatically speed up industry emissions reductions. In the roadmap, the Optimal Scrap Utilisation scenario eliminates an additional 160 million metric tons of CO2e emissions by 2050 for a total reduction of 287 million metric tons – the equivalent of taking more than 68 million cars off the road for a year.

Despite looking into alternative routes to overcome lack of funding, funding is essential to decarbonising:

6a. Addressing investors, what would you like to say to encourage funding.

CJ: One of the key steps to reducing emissions begins in reducing the carbon-intensive process of primary aluminium production. In order to produce aluminium, facilities use a carbon anode, which releases CO2 directly in the process. Several aluminium companies are examining alternatives to these anode technologies that would release only oxygen as a byproduct, not CO2. Commitment to innovations such as these should be encouraging to the overall industry, and investors alike. An investment in research and technologies like these is an investment on the road to a cleaner future.

6b.How can the aluminium industry encourage investments.

CJ: Progress begets progress. Overall, if we’re going to invest in decarbonisation, we should be decarbonising where the industry has already invested and already taken the first steps to reduce emissions. Our member companies are pioneering new technologies and processes to help us to make ever cleaner aluminium in North America. Together, our research, innovation and commitment to partnerships across the globe are a key element to the clean energy transition.

7.Anything else you would like to add.

CJ: Aluminium is one of the most recycled – and recyclable – materials in use today. Domestic aluminium demand is rebounding so far this year amidst continued interest from our customers and end consumers in alternative material solutions. Our monthly Aluminium Situation statistical report [4] shows demand for the aluminium industry in North America increased 4.3% year-overyear through the first quarter of 2024.

The aluminium industry is a significant driver in the American economy, generating nearly $230 billion in total economic output—nearly 1% of the U.S. GDP. The U.S. aluminium industry directly employs more than 164,000; when direct, indirect and induced jobs are included that number grows to 700,000 workers, who earn more than $54 billion in total wages. (Source: 2024 Economic Impact Report [5]). The bottom line is: aluminium is a growing industry with a bright future supporting a modern, clean energy economy in the United States and globally.

SPOT+ AL

ALUMINIUM PRODUCTION AND PROCESSING APPLICATION PYROMETER

ADVANCED NON-CONTACT INFRARED SPOT PYROMETER

SPECIFICALLY DESIGNED FOR ALUMINIUM PRODUCTION AND PROCESSING INDUSTRIES

SPOT+ AL uses AMETEK Land’s cutting-edge SPOT technology and unique, advanced data-processing algorithms to measure aluminium temperature in extrusion (E), quench (Q), strip (S), forming/forging (F), forming/forging of higher magnesium alloys (F Mg) and liquid (L) applications.

Dedicated pre-set algorithms provide the most accurate digital temperature readings of low and variable emissivity aluminium. This ensures optimised press speed and high-quality products with minimal scrap.

The SPOT+ AL integrates easily with control systems to enable optimisation of the press or mill with data also made immediately available via the rear display on the instrument or via a web server. A video camera within the pyrometer, the focus distance and other features can be accessed and configured locally or remotely.

GET THE BENEFITS:

ACCURATE AND FAST MEASUREMENTTemperature readings accurate to 0.25 % (K) output every 15 ms

AUTO ALIGNMENT AND TRACKING - SPOT Actuator automatically tracks and aligns to the tapping stream

Combining Ethernet, Modbus TCP, video, analogue, and alarm outputs in a single device, the SPOT+ AL is designed specifically to measure the temperature of aluminium in a range of processing applications.

REMOTE ACCESS AND INTEGRATED CAMERAFull process control through digital interfacing and live video view

MULTIPLE INTERFACES - Analogue and digital inputs and outputs, Modbus ethernet protocol

Petr Tlamicha* talks about the energy transition and alternatives to decarbonise the aluminium industry.

1. What is currently being done to support the decarbonisation of aluminium production?

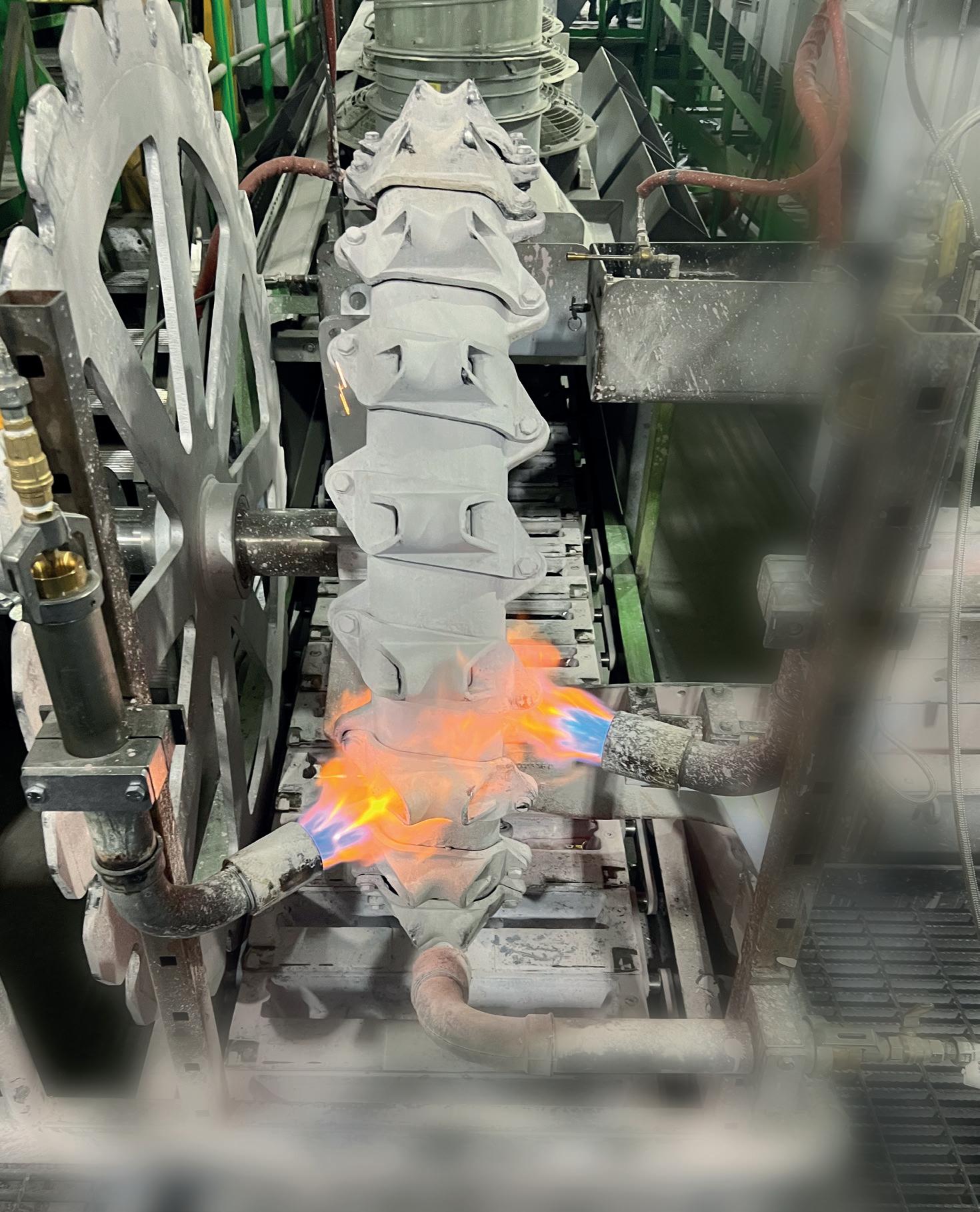

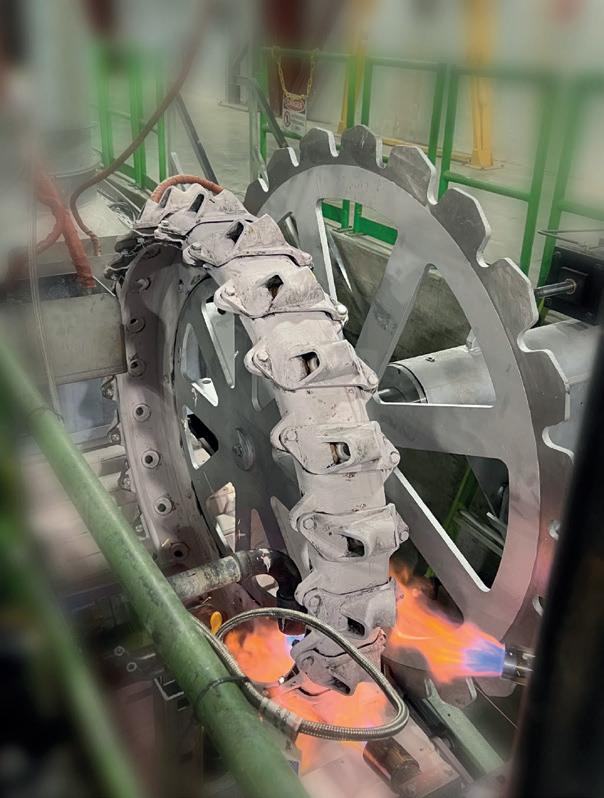

Decarbonisation is an important concern for aluminium smelters and recyclers. Although the carbon footprint of recycled aluminium production is 95 percent lower than primary production, there is still scope for improving sustainability in both. For example, oxyfuel has been used for decades for scrap melting and is a proven technology. It reduces CO2 emissions by up to 50 percent so it can play a major role in meeting the EU’s 2030 decarbonisation milestone. But while oxyfuel is used in most rotary furnaces, it is still only used in around 10 percent of reverb furnaces. There’s also scope for the industry to reduce energy consumption through smart technologies that optimise performance and remove human error, as well as new, more efficient burner designs.

2. What steps are industrial gases suppliers taking to make aluminium production more sustainable?

Producers are considering clean fuel, such as renewable or low carbon electricity, as part of their roadmaps. But full decarbonisation is a long journey. Air Products is investing in its hydrogen supply network, including building the world’s largest renewable hydrogenbased production facility in Saudi Arabia. Once on stream it will produce 600 tonnes per day of carbon-free hydrogen for heavy-duty transportation and industrial applications around the world. We are also developing hydrogen burners in preparation for a switchover to low carbon hydrogen in the industry.

5. How realistic is a green aluminium in your view?

Aluminium has already been produced using renewable hydrogen, and widespread production of low-carbon aluminium is only a matter of time. Major customers, in particular in the automotive industry, have their own sustainability targets, so are looking to aluminium suppliers to support those goals. The challenge for primary and secondary melters is ensuring these targets go hand in hand with business sustainability and competitiveness.

3.

How can aluminium producers work with gas suppliers to decarbonise their production?

Using smart technology to monitor furnace performance and efficiency is a first step. The Air Products Smart Process Adviser system can help maintain furnaces’ operation to ensure they are working at peak performance. Looking ahead, we are analysing the use of hydrogen on aluminium alloys in our large combustion laboratory and are working with some of our bigger aluminium customers to test hydrogen burner technology. We use turnkey solutions to examine the impact of different charge materials and furnace operation on yields and production rates, looking at everything from furnace design, material melting to final product casting. It’s all about partnership and sharing experiences to get the best results.

* Combustion Segment Manager at Air Products

4. What are the implications of energy transition for aluminium producers?

Energy transition inevitably has an impact on costs and competitiveness. New technologies, materials, and fuels are needed to become sustainable. The aluminium industry also needs to stay competitive outside Europe. The EU’s Carbon Border Adjustment Mechanism (CBAM) will have an impact and we are watching closely to see how quickly and effectively it is implemented.

6. When can we expect energy transition to hydrogen?

The sooner, the better! The first decarbonisation milestones in 2030 can be achieved using low-carbon electricity, effective oxyfuel solution, and smart process control, without a switch to alternative fuels. As we transition to hydrogen, we will be working with the aluminium industry on test site installations to gain a better knowledge and understanding of its use in their process.

We are working with customers to support the energy transition to lowcarbon fuels such as hydrogen to reduce emissions, while improving the efficiency of aluminium production plants, generating a cleaner future for us all.

Petr Tlamicha

TOGETHER TOWARDS PERFORMANCE

Experience our global network of Support and Technology Centres.

Our Global Support and Technology Centres, are dedicated to the development, support and promotion of efficiency, technology and innovation within the Aluminium industry. Our Technology Centres serve as focal points for research, development and customer service, bringing our support structures closer to our customers worldwide. REEL Aluminium is also committed to green innovation and sustainability which translates into REEL’s commitment to contribute towards a net-zero aluminium industry.

VISIT THE CALDERYS BOOTH AT ALUMESSE

Our aluminum experts are delighted to welcome you on booth n°6F11. Discover the group’s refractory solutions that deliver energy savings, increased campaign life, and efficiency.

• Monolithic refractories

• Bricks

• Precast shapes

• A full set of services

www.calderys.com

Innovation and sustainability: the pillars of FLUORSID in the aluminium industry