Annual subscription: UK £270, all other countries £292. For two year subscription: UK £510, all other countries £527. Airmail prices on request. Single copies £50

ALUMINIUM INTERNATIONAL TODAY is published six times a year by Quartz Business Media Ltd, Quartz House, 20 Clarendon Road, Redhill, Surrey, RH1 1QX, UK. Tel: +44 (0) 1737 855000 Fax: +44 (0) 1737 855034

Email: aluminium@quartzltd.com

Aluminium International Today (USO No; 022-344) is published bi-monthly by Quartz Business Ltd and distributed in the US by DSW, 75 Aberdeen Road, Emigsville, PA 17318-0437. Periodicals postage paid at Emigsville, PA. POSTMASTER: send address changes to Aluminium International c/o PO Box 437, Emigsville, PA 17318-0437.

Printed in the UK by: Stephens and George Ltd, Goat Mill Road, Dowlais, Merthyr Tydfil, CF48 3TD. Tel: +44 (0)1685 352063 www.stephensandgeorge.co.uk

STRATEGY

Stopping the aluminium drain

Driving due diligence practices through supply chains

Event Review: FAF 2024

DIGITAL

TRANSFORMATION

The unified namespace for digital transformation in the industry

FOCUS ON CHINA

An insightful keynote

Aluminium industry in Egypt

DECARBONISATION

Major challenges for 1.5°C-aligned aluminium procurement strategies

Shell Energy: Decarbonising aluminium

Further lightweighting the Porsche Taycan EXTRUSION

Alumex PLC: More than extrusion

Advanced measurements and furnace monitoring MELTING

The timing of the most recent ELYSISTM announcement couldn’t have been better, as I had just sat down to write this note and was searching for inspiration when the press release dropped into my inbox.

It is great to be able to see that this JV has has achieved a significant milestone with its carbon-free smelting technology, which represents a monumental leap towards sustainable aluminium production.

As you will be able to read on these news pages, the first commercial-scale demonstration of this new technology is now underway at Rio Tinto’s Alma smelter, with plans to make it commercially available later this year.

As we continue to monitor and report on the advancements within the industry, we remain committed to providing you with the most comprehensive and insightful coverage. Our upcoming issues will look at delving deeper into the technical intricacies of the ELYSIS process and explore its potential impacts on global supply chains.

For now, this issue is packed with extra content from the recent Future Aluminium Forum, which not only offers a look into the growth in the Chinese aluminium market, following an insightful Keynote presentation from the one and only, Ron Knapp.

We also explore the concept of the unified namespace as a solution to common data-problems in aluminium manufacturing, something that was touched upon by speaker Denis Gontcharov.

You can also find a review of other recent events such as the CRU World Aluminium Conference and a reminder of why you should visit the next UK Metals Expo! nadinebloxsome@quartzltd.com

Industrial-Scale Demonstration of ELYSISTM Carbon-Free Smelting Technology

Alcoa Corporation have announced further progress on ELYSIS technology with Rio Tinto’s plans to launch the first industrial-scale demonstration of the breakthrough technology, which eliminates all greenhouse gas (GHG) emissions from the traditional smelting process and produces oxygen as a byproduct.

Established in 2018, ELYSIS is a technology partnership between Alcoa and Rio Tinto to advance technology first developed at the Alcoa Technical Center (ATC) outside of Pittsburgh. Rio Tinto’s demonstration project will occur at Arvida in Quebec, Canada, and includes 10 ELYSIS smelting pots operating at 100 kiloamperes (kA), a size similar to those operating at smaller-scale commercial smelters.

Alcoa has the right to purchase up to 40 percent of the metal produced from the demonstration at Arvida, allowing for Alcoa customers to benefit from ELYSIS’s carbon-free electrolytic process early in the technology development cycle. The target for first production is by 2027.

“Since inventing the aluminum smelting process in 1886,

which is still in use today, Alcoa has continued to create transformational technologies to improve our industry,” said William F. (Bill) Oplinger, President and Chief Executive Officer of Alcoa Corporation. “We are proud to progress the technology initially developed at our technical center to its next phase within the ELYSIS partnership. Aluminum plays a critical role in the world’s energy transition and decarbonization efforts; with the ELYSIS technology, the smelting of this important metal can also be done without direct

carbon emissions.”

To support the industrial demonstration, Alcoa will manufacture the proprietary ELYSIS anodes and cathodes at ATC, which will include installing and operating new equipment. Alcoa anticipates benefitting from the learnings of this phase of the demonstration and expects to apply them to future phases in ELYSIS’s development. Metal produced through the ELYSIS process will further improve upon Alcoa’s lower carbon products already on the market, such as the Sustana™ product line.

Hydro pursuing zero-carbon aluminium by testing green hydrogen technology

Green hydrogen can replace fossil energy in the recycling of aluminium, enabling zero-carbon aluminium products. In a three year industrial scale pilot, Hydro will test green hydrogen technology in the new recycling unit at Hydro Høyanger, Norway.

Replacing liquid natural gas with green hydrogen in the recycling of 100 percent post-consumer scrap is one of the fastest routes to zero-carbon aluminium. However, the remelting of aluminium requires high heat, an energy intensive process which is hard to achieve without fossil energy such as natural gas. Hydro will be testing technology with global poten-

tial in this pilot, which is building on Hydro’s ‘world first’ industrial scale test of green hydrogen in aluminium recycling in June 2023.

“Hydro is pursuing multiple paths to decarbonize our operations. With this pilot we take another step on our path to zero-carbon aluminium. Green hydrogen is an exciting potential option to decarbonize aluminium and other hard to abate industries,” says Hanne Simensen, Executive Vice President of Hydro Aluminium Metal.

During the pilot, green hydrogen will power one remelting furnace at the Høyanger recycling unit. This is key to unlock this re-

newable fuel’s decarbonization potential in aluminium, and will provide insight into fuel switch technology, metal quality, and necessary infrastructure for green hydrogen projects.

This project is enabled by Hydro’s competence in both energy and aluminium. Hydro Havrand, Hydro’s green hydrogen unit, has been granted soft funding from the Norwegian Government (Enova) up to NOK 83.3 million to enable this pilot. The aluminium produced in the recycler will be used to further lower the CO2 footprint of aluminium products from Hydro’s Norwegian smelters.

Rio Tinto will invest US$165 million (CA$226 million) in its Grande-Baie smelter to refurbish two anode baking furnaces that have reached the end of their useful life. The company will also carry out feasibility studies for the eventual replacement of the scrubbers and overhead bridge cranes at the anode production centre.

The work to rebuild the concrete shell and refractory lining of the anode baking furnaces will be carried out over two years, in 2025 and 2026. The new equipment will ensure a competitive supply of anodes to the GrandeBaie and Laterrière plants for decades to come.

Rio Tinto will offset the carbon emissions related to the construction project through various initiatives like planting trees near the aluminium smelter.

Grande-Baie and Laterrière Op-

Rio Tinto invests to maintain anode production at Grande-Baie smelter

erations Director Martin Lavoie said: ‘‘The refurbishment of the Grande-Baie smelter’s anode baking furnaces is a major investment that will ensure the sustainability and competitiveness of responsible aluminium production in the region for decades to come and will generate significant economic

Further transforming to circular economy

Speira is investing 40 million euros for additional recycling capacity to drive the transformation of Rheinwerk and achieve a total saving of up to 1.5 million tonnes of CO2 per year at the site.

The direction has been set for a long time: “We want to become the number 1 in aluminium recycling in Europe,” explains Boris Kurth, Head of the can business at Speira as well as the recycling and foundry operations at the Rheinwerk. “Over the past 20 years, we have already built furnaces with leading recycling capacity in Europe and Europe’s most modern

sorting plant for UBC scrap, substituting the highly energy-intensive primary production of aluminium. We are consistently pursuing this path and emphasising our commitment to the circular economy with the fourth recycling furnace at Rheinwerk.”

The furnace will be built in 2025. Production is scheduled to start at the beginning of 2026. Speira is also converting the third of four existing casting centres to be optimised for recycling alloys. This will enable Rheinwerk to further reduce its ecological footprint. Overall, Rheinwerk will

benefits. We are very happy to be completing this project over the next years in collaboration with our employees and local business partners.”

Rio Tinto completed the replacement of its anode baking furnaces at the Alma aluminium smelter in 2021.

then have a recycling capacity that will save up to 1.5 million tonnes of CO2 compared to primary production of the same quantity of aluminum.

The new recycling furnace will be used to melt aluminium alloys that are processed into beverage cans after rolling.

EGA’s GAC signs term sheet with Government of Guinea for development

Emirates Global Aluminium’s (EGA) subsidiary Guinea Alumina Corporation has signed a term sheet with the Government of Guinea for the development of an alumina refinery. The signing of this preliminary agreement is a decisive step forward in the development of the project.

GAC’s delegation was led by EGA’s Chief Executive Officer Abdulnasser Bin Kalban.

The alumina refinery project is expected to be built on GAC’s concession near Tinguilinta in

Boké province, with an initial production capacity of one million tonnes of alumina per year.

Hydro and Brompton pedal toward net-zero with world’s first bicycle wheel rim made from fully recycled aluminium

In June 2023, aluminium and renewable energy company Hydro and London based bicycle company Brompton, entered into a partnership with the aim to introduce Hydro’s low-carbon aluminium in Brompton’s range of bikes. The collaboration has now resulted in bicycle rims made from Hydro CIRCAL 100R, a product that not only reduces weight, but also guarantees batch-by-batch transparency and a near-zero CO2 footprint.

ALFED Launches UK Aluminium Manifesto

Following the announcement that the UK will now face a General Election on Thursday 4th July, the Aluminium Federation (ALFED) is launching the UK Aluminium Manifesto; a comprehensive document outlining key stipulations for the next UK Government to prioritise and support the vital role of the aluminium manufacturing and processing sector in driving economic growth, sustainability, and energy security.

Pomini Tenova secures Roll Grinder contract for Hindalco’s Renukoot aluminium plant in India The contract concerns a new Roll Grinder that will be supplied by Pomini Tenova. The roll grinder will grind work rolls, backup, and auxiliary rolls for the existing hot and cold rolling mills in the Renukoot aluminium plant, in Uttar Pradesh, India.

Ground-breaking ceremony for joint venture in South Korea

Hammerer Aluminium Industries (HAI) is relying on strong partnerships to drive forward the strategic development of the HAI Group. Together with LS Cable & System, HAI is investing in a company in South Korea. The official ground-breaking ceremony for the construction of the new production hall took place on 17 April 2024.

In his speech, CEO Rob van Gils emphasised the importance of the joint venture for the strategic development of the HAI Group. The new company will enable the HAI Group to strengthen its focus on the production of highly complex aluminium components for electromobility and at the same time serve the important South Korean market locally.

With an investment volume of around 46 million euros, a 13,800 m² production hall including a 60 MN press for the production of aluminium components will be created. From 2025, the HAI Group and LS Cable & System will produce aluminium components for electric vehicles for the South Korean market at the Gumi site.

GNA alutech inc. is now fully owned by EBNER GROUP

The acquisition marks the culmination of a five-year partnership between EBNER and Ted Phenix, which began with EBNER Group acquiring a majority stake in GNA in 2019.

“We are excited to announce the full acquisition of GNA alutech inc. and would like to thank GNA’s founder, Ted Phenix, for his vision and leadership in building GNA into a successful company over 41 years. Over the last 5 years I was always impressed by the deep understanding and knowledge Ted was able to share with customers. Our strong professional developed to a strong personal friendship. says Robert Ebner, CEO of EBNER Group.

The leadership of GNA has been placed in the hands of Kaleb Wright, President of Business De-

velopment, and Chantal Coupal, President of Operations. Kaleb Wright brings extensive experience in business development and sales to the role, while Chantal Coupal has a deep understanding of GNA’s operations and technology.

Based on GNA´s 41 years success story the company is committed to continuing its focus on green technology and cost efficiency. As part of a strong EBNER GROUP, GNA provides a full range of technologies and services to their customers including newest and upcoming technologies such as rotary furnace, EMS pump, own regenerative burners, CO2 free burner, etc.

Mighty Earth urges producers to commit to responsible mining

A new Mighty Earth report, “The Impact of the Bauxite Boom on People and the Planet” examines the environmental and social impacts of bauxite mining for aluminum used in electric vehicle (EV) production in four key producing countries: Indonesia, Brazil, Guinea, and Australia.

In the first global analysis of the bauxite boom across four continents, the report analyses the adverse effects of bauxite mining –

the principal ore of aluminum for electric vehicles – and the resultant environmental degradation and health repercussions faced by local and Indigenous communities.

Drawing on new satellite data, the report highlights extensive

www.aluminiumtoday.com

SEPTEMBER

10th - 12th

Fastmarkets International Aluminium

Join the aluminium industry at the heart of contract season, to connect, negotiate and agree new deals. Hear from the end users driving demand, and remain on top of all the new technologies, processes and opportunities that green aluminium is bringing. Held in Athens, Greece www.fastmarkets.com

11th - 12th

UK Metals Expo

This event brings together professionals from primary metal manufacturing to supply chain management, processing metals, fabrication, machinery, engineering, surface coatings, and recycling. Held in Birmingham, UK www.ukmetalsexpo.com

25th - 27th

IBAAS

The 12th International Bauxite, Alumina & Aluminium Conference & Exhibition, in collaboration with The Indian Institute of Metals (IIM). Stay updated on the latest industry trends, challenges, and opportunities through engaging discussions and presentations. Held in Goa, India www.ibaas.info/

OCTOBER

8th - 10th

ALUMINIUM 2024

deforestation driven by bauxite mining in the four country case studies.

With the demand for aluminum expected to double by 2050, the report calls on the world’s biggest bauxite producers to commit to responsible mining and for global EV manufacturers to ensure their global supply chains are not driving human rights abuses, deforestation and environmental harm.

ALUMINUM is the world’s leading trade fair and B2B platform for the aluminum industry and its main user industries. The focus of the trade fair is on solutions for automotive engineering, mechanical engineering, building and construction, aerospace, electronics, packaging and transport. Held in Düsseldorf, Germany www.aluminium-exhibition. com

For a full listing visit www.aluminiumtoday.com/ events

TOGETHER TOWARDS PERFORMANCE

THE TIME TO ACT IS NOW

REEL is on a journey to contribute towards a net-zero aluminium industry.

REEL Aluminium is a major solution provider dedicated to the reduction of the Aluminium industry‘s carbon footprint. This is achieved through both internal and external collaborations and partnerships, new ways of understanding the problem, and the development of innovative technological advancements to achieve net-zero solutions within the Aluminium industry. These efforts assist in REEL‘s goals on its path to decarbonization and a greener Aluminium future.

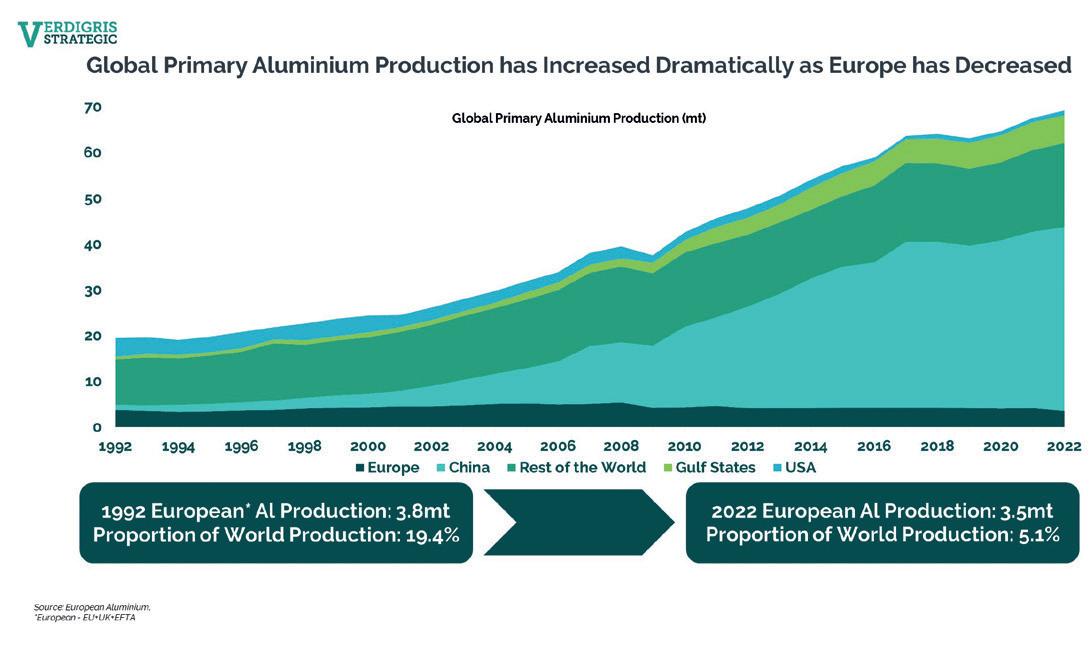

In May, Jay Hambro, CEO of Verdigris Strategic Ltd (pictured right) spoke at the CRU Aluminium Conference in London on the topic of “Stopping the Aluminium Drain”. Verdigris Strategic is an advisory and investment group focussed on metals, mining, industrials businesses, green energy and associated infrastructure. The group has extensive experience in aluminium where the team has been active for many years in operations, finance, marketing and leadership.

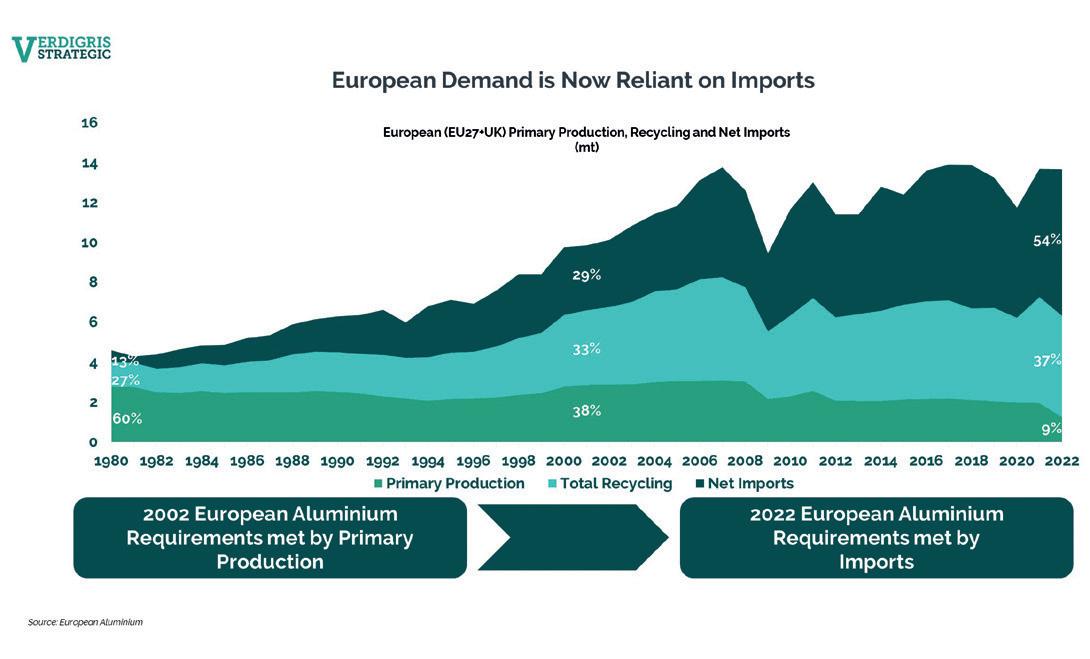

In recent years Europe has seen demand for Aluminium increase consistently year on year, a trend set to continue as the green transition dramatically escalates requirements. At the same time, Europe has seen production of primary aluminium decrease continuously as smelters have shut down or become idled. Moreover, the capacity to remelt scrap has not seen sufficient investment and therefore exports of scrap in all forms have increased year on year.

Worse still is that whilst Brussels promotes policies on Critical Metals, Europe’s requirements for aluminium are now increasingly supplied via imports from countries producing aluminium at a much higher CO2 burden than producing in Europe or recycling scrap. Additionally, an increase in reliance on international aluminium providers will only lead to localised vulnerability as critical metals increase in demand and value. The fragility of supply chains continue to be exposed as has been seen numerous times in recent years. Europe’s governing bodies are slowly waking up to the issues but not quickly enough and more must be done.

Verdigris believe that Europe should become a closed circular economy for scrap aiding the drive for net zero by 2050 whilst assisting with the green transition.

How have we reached this situation?

Over the last 30 years Europe’s position as a global producer of primary aluminium has diminished to a point of almost global insignificance. In 1992 Europe was producing 3.8mt of aluminium annually which was 19% of global total requirements of 19mt1. In 2022, annual global requirements have increased 3x to 68mt whilst production in Europe has decreased to 3.5mt equating to just 5% of global requirements1. No one is forecasting for primary production in Europe to return as smelters are closing with no new plants expected to be built. In 2002, Europe had 23 active smelters but in 2023 this number had reduced to nine, with further closures expected over the coming decade1

The decrease in primary production

Stopping the Aluminium Drain Stopping the Aluminium Drain

By Will Savage*

and increase in demand has meant that requirements have had to be met elsewhere, predominantly through imports but also through recycling. In 1980, Europe was able to supply 60% of its requirements through its own primary production with recycling making up 27% of demand and imports just 13%¹. In the last 40 years these figures have changed dramatically. Europe is now predominantly reliant on imports which meets 54% of requirements. In recent years recycled aluminium has increased in Europe, now making up 37% of annual usage. However, requirements are continuing to outpace the ability to recycle - resulting in an increased need for imports year on year with no sign of this slowing down.

When Aluminium is imported into Europe it is highly likely that the CO2 burden is much greater than if the aluminium had been produced in Europe and even greater still than if it was recycled in Europe. On average, producing primary aluminium in Europe releases 6.7kg of CO2 per kg of Aluminium produced². If primary aluminium is produced in China, this figure increases to 20kg (CO2 eq/kg), a 200% increase, in the Middle East 11kg (CO2 eq/kg), a 64% increase and compared to the World Average 17kg (CO2 eq/kg), an increase of 154%. In comparison, when recycling aluminium the figure reduces to just 0.5kg (CO2 eq/kg).

Whilst the European demand or requirement for scrap aluminium is there it is now continually being exported in unnecessarily large quantities. In 2021,

*Adviser, Verdigris Strategies

more than 1.5mt of scrap aluminium (HS 7606)1 was exported out of Europe which will be bought back to the continent at a later date, at a higher cost and at greater environmental expense. Figures for exports of all aluminium are poorly recorded and the actual figure of all types of aluminium being exported will be far greater than the 1.5mt given.

Why is it important to stop the aluminium drain?

The increased demand for aluminium in Europe shows no sign of slowing down, with forecasts suggesting an increase of 40%³ over the next decade. The green transition will see dramatic increases in requirements for aluminium in the following areas: Aerospace, Energy Efficient Buildings, Recycled Packaging, Battery Storage, Solar Modules, Wind Turbines, Electrical Cabling and Vehicle Light Weighting. It is predicted that part of the increased requirements (over 2.8mt³) will be met by recycling however Verdigris, as an adviser and investor, is struggling to see if there is a melt margin that would entice the investment community into the market. CRU data also predicts a marginal increase in the production of European primary aluminium, however again Verdigris’ research and recent data would suggest this forecast is optimistic. Forecasted data suggests an increase of over 1mt of imported aluminium resulting from levels of recycled aluminium usage failing to keep up with demand. The result is a net increase in CO2 emissions at the

same time as Europe aims for Net Zero by 2050. Reduction in the production of primary aluminium is not reducing greenhouse gas emissions, it is merely offshoring them as a higher environmental cost. Verdigris believes that an increase of just 1mt of imported primary aluminium is a modest estimate compared to the likely requirements.

The other issue with an ever-increasing reliance on imports is the increased vulnerability this causes. In just the last 36 months, the Suez Canal was blocked for 6 days which pushed benchmark aluminium prices near their highest for 3 years and threatened to intensify a rare shortage of aluminium. The Panama Canal has seen water levels at their lowest in decades forcing a reduction in the numbers and total weight of vessels through the canal with its longevity in question. Houthi attacks in the Red Sea led to major shipping companies suspending freight through the region and most recently, the closure of the Baltimore Port, saw issues as 12%4 of all US primary Aluminium passes under this now collapsed bridge.

What is being done to stop the aluminium drain?

European governments are waking up to the continent’s aluminium exposure however what they are proposing has been slow to implement and both focus and financial support is lacking. The long-term plan for Critical Raw Materials (CRM), of which Aluminium is one, is laid out in the Critical Raw Materials Act (CRMA)5. The aim is to have 10% of each raw material extracted in Europe, 40% of processing and 15% of recycling with Europe not relying on one single nation to supply more than 65% of one particular CRM. Given where bauxite can be mined and the recent and continued reduction in the processing of alumina in Europe,

the Extraction and Processing targets will never be met. Europe must therefore focus on the use of recycled aluminium as it is abundant, infinitely recyclable and requires little energy to reproduce.

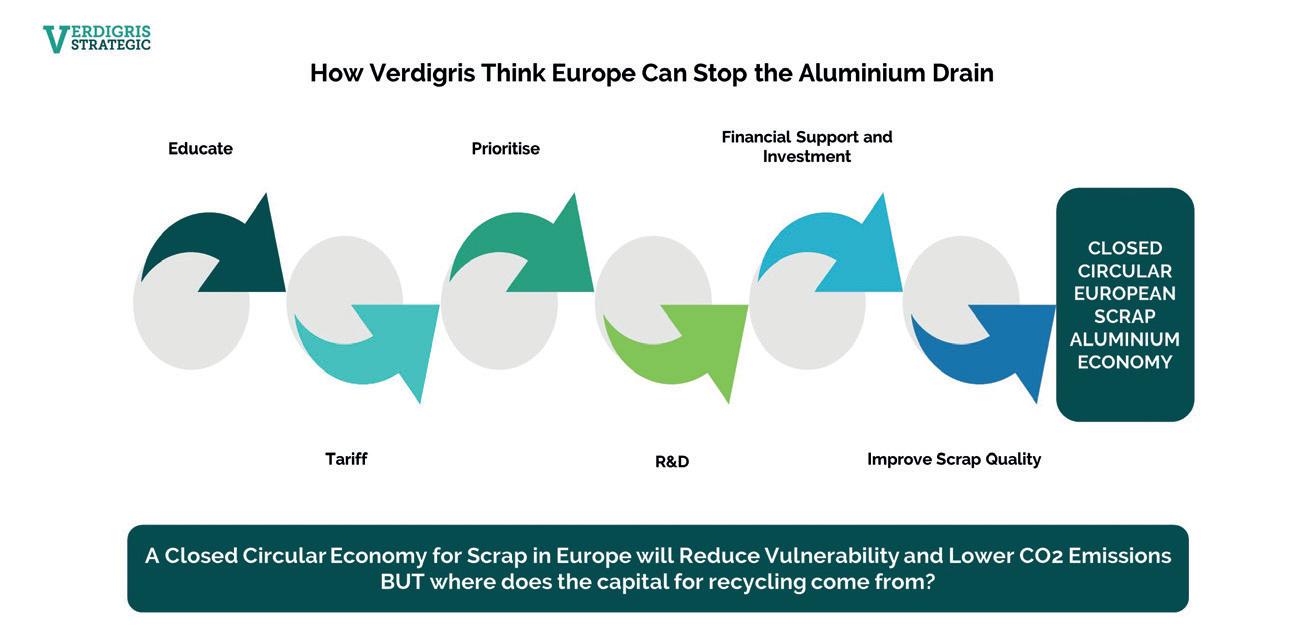

At present there is not enough support to prevent the Aluminium Drain or to increase localised European recycling. However, Verdigris has devised 6 key drivers, that if done simultaneously, could stimulate a localised, closed scrap aluminium recycling sector within Europe:

1) Educate – Private investors should be educated in the lucrative opportunity that secondary aluminium provides

2) Tariffs – It may be possible to implement export tariffs, add quotas, or limit the export of scrap aluminium, as seen in Saudi and the UAE with Oman currently discussing the idea

3) Prioritisation – If scrap aluminium is prioritised, Europe will see the opportunity created by forming a closed circular economy whilst achieving Net Zero

4) R&D – Europe wide research and development should be conducted into potential new scrap sorting and processing sites and to “up-grade” current sites to increase scrap quality and value output

5) Financial Support and Investment – Funding for European projects will be

pivotal in stopping the aluminium drain. Investment from The EU Horizon Fund and more locally from entities like UKIB should encourage and support private recycling initiatives

6) Improve Scrap Quality – Through the introduction of Deposit Return Schemes which have been successfully implemented across Scandinavia and expected to be rolled out in the UK in 2027 we will see an increase in the quality of scrap which will become increasingly appealing

Despite the inevitable, limited future of the primary aluminium sector within Europe, there is a lucrative opportunity for Europe to become the global leader in creating a closed circular economy for the recycling of scrap aluminium. This will become invaluable as the green transition intensifies in the coming years, especially as the world looks beyond globalisation as has been seen through the CRMA, export tariffs and other agendas worldwide. The demand for aluminium will only increase and Europe must be cautious of becoming held to ransom if the reliance on imports continues and supply chains are disrupted as we have seen at various points in recent years. �

Driving due diligence practices through supply chains

By Laura Dombi and Rachel Lock*

At the CRU World Aluminium Conference in May this year, one of the prominent points of discussion was on how the aluminium sector can realise competitive advantage, being “the least hard” to abate of the hard-to-abate sectors.

Some of the classic ESG claims, such as “aluminium is endlessly recyclable”, “it is a light-weight and flexible material” seem to have less gravitas in the market, as competitor sectors, such as steel are making strides in bringing to market reduced, low and zero-carbon products verified against Chain of Custody standards and assured carbon savings.

In parallel, there is increasing scrutiny over aluminium companies’ raw material supply chains, from both a climate decarbonisation and Scope 3 emissions reduction point of view (1.5 degrees pathway, CBAM, CSRD/ESRS), but also from a social and human rights perspective, with the proliferation of regulations enforcing measures to address

these issues (CSDDD, NTA, LkSG, EU Forced Labour Act etc) where they were previously addressed through voluntary initiatives.

Yet aluminium plays a crucial role in current and future global supply chains across various industries. Total aluminium consumption is expected to grow by 33.3 Mt in the following decade, going from 86.2 Mt in 2020 to 119.5 Mt in 2030.

Around 37% of this growth is expected to come from China, followed by 26% from Asia ex. China, 15% from North America and 14% from Europe.1

The aluminium demand for EVs alone is expected to grow over 900% by 2030 compared to 2015.

In addition to increasing customer

*Principal Consultants at DNV

expectations, banking institutions and investors are paying closer attention to supply chain due diligence practices particularly where there are close links to complex supply chains, such as aluminium and critical minerals. Whilst the investments may be in large-scale solar/wind or EV vehicle infrastructure projects, due diligence of the project alone is no longer an accepted practice, and investors are now cascading due diligence expectations across the whole supply chain with the responsibility sitting at the investee / project level. This has a significant influence and impact on the supply chain dynamics and presents both challenges and opportunities for the sector at large.

There is increasing stakeholder and regulatory pressure to hold companies accountable for how and where their products are manufactured and by whom. Emerging regulatory and industry standard requirements place renewed responsibility on aluminium producers and their customers/investors to integrate social performance into the financial evaluation of the company. As independent assessors, we bring insights into understanding stakeholder relationships, priorities and expectations and help companies bring the “outside perspective in” and integrate into better decision-making.

Whilst integrated aluminium producers and product semi-fabricators/material conversion producers are already subject to legislative requirements, such as the Modern Slavery Act in many jurisdictions where they operate, thus expected to release an annual modern slavery statement, detailing their salient human rights impacts, risks and opportunities in their direct operations or through their business relationships (typically screening tier 1 – direct suppliers), the introduction of CSDDD, and the EU Forced Labour Act means that aluminium producers are now expected to provide transparency across the entire supply chain, including upstream actors such as smelters, refineries and bauxite mines.

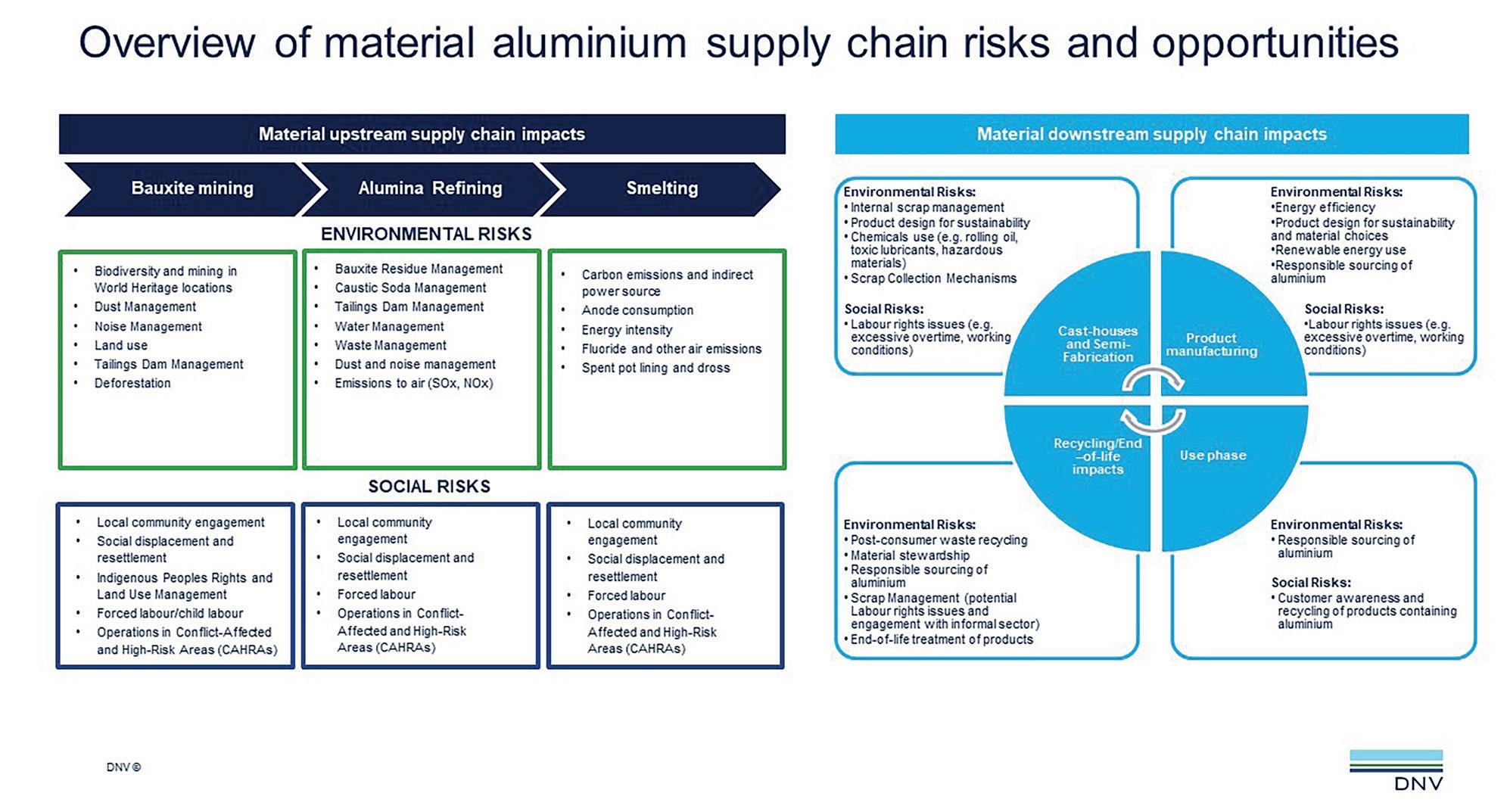

Currently relationships with upstream actors are typically weaker - these supply chain actors could be 3-4 tiers removed from downstream customers, as often metals are traded through intermediaries, traders and through spot-buying arrangements. This makes supply chain visibility harder and more complex, especially when considering non-metal strategic supplies, such as alloying elements, carbon anodes and other input materials to smelting

and cast-houses. Cast-house operations are the typical traceability choke points in the aluminium value chain, where primary metal, secondary (recycled) metal and alloying elements are mixed, and visibility of aluminium flows and sourcing arrangements between key players is lost in public data.

See Fig 1. for an overview of material upstream and downstream supply chain impacts

So what does this mean for the aluminium sector?

Aluminium companies must equip themselves to tackle the complexity of their supply chains and demonstrate compliance towards emerging regulations, whilst delivering value and performance through their supply chains. This can be achieved by:

� Assessing material supply chain risks through a double materiality lens: Companies must analyse and assess their material impacts with an explicit focus on environmental and social risks in the supply chain. This can be achieved through sharing ESG questionnaires with suppliers, EcoVadis assessments and other

survey-based tools. Historically, companies request such information purely for sustainability reporting purposes and the process to obtain such data is time consuming and resource intensive. The new era of regulation means that companies must now go beyond simply obtaining such data, and start to act on the identified risks ensuring ongoing monitoring and strategic review of the data gathered and of their suppliers. Understanding the commercial benefits of doing this is also imperative and will help internal teams gain the buy-in and resource support.

� Internal collaborations to navigate the unchartered landscape of financial materiality. Engaging with procurement and finance teams within companies on salient risks will become increasingly critical in understanding the financial materiality. Questions relating to environmental and social risks and impacts will need to be considered both at the initial onboarding and procurement stage as well as through ongoing supplier account reviews. Procurement teams, in parallel to finance teams, could also be pivotal in helping understand and analyse

Laura Dombi Principal Consultant, DNV Supply Chain and Product Assurance UK

the commercial value that can be derived from this approach and identify where further investments could create further efficiencies and cost savings. The role of sustainability teams is to demonstrate the business case for action and the potential negative impacts of doing nothing. Key considerations could include the potential impact of buying metal from a supplier with local community health and safety concerns, environmental spills, or potential human rights violations, the security of supply risks, and the resiliency of the supply chain.

� Going beyond box-ticking exercises when it comes to supply chain due diligence – engaging in conversations with suppliers on material risks and identifying cross-industry collaboration opportunities that could drive technological innovations and / or reduce risks and impacts and generate cost savings. There is a general survey fatigue across suppliers, and companies are getting increasingly frustrated by filling out the same due diligence questionnaires, often with no follow-up. This one-way transactional relationship misses a key opportunity for companies to use these types of supplier engagement to strengthen relationships, and better utilise leverage and incentives in a way that benefits all supply chain actors and society at large.

� Engaging with suppliers on corrective action plans and improvement opportunities: where possible, companies should actively engage with suppliers to build capacity on the emerging ESG expectations, and work with them to provide more transparency on the corrective actions they will take to mitigate any potential or actual human rights and environmental impacts. Companies should also seek to identify where there are common risks and issues where they can leverage efficiencies through a common or collaborative approach. This approach helps to deliver continuous improvement at scale and with greater efficiencies for all stakeholders.

� Identify and invest in circular economy opportunities: Some producers

spend millions of dollars shipping their spent pot lining (SPL), dross or dross residues to approved landfills, often outside of the country of production, or deposit them in a way that may risk leakage of refractory materials into the environment. As locally, they often lack a circular ecosystem where these byproducts can be recycled and aluminium recovered. More needs to be done to effectively engage with local stakeholders, the cement and other industries to create ecosystems for a circular design.

What’s next?

� Digitalisation of the human rights and environmental DD process and assurance / verification will lead to efficiencies, so procurement professionals have more time to focus on analysing the outcomes of the DD process, and link it back to their strategy.

� Increasing customer demand for verified low carbon aluminium products: increasingly, customers are asking for a Chain of Custody (CoC) verified (often ISO 22095) low-carbon product claims through contractual relationships. Creating CoC boundaries and obtaining assurance of Product Carbon Footprint (PCFs) will become an increasing expectation, and the aluminium industry is encouraged

References

to collaborate on common frameworks and definitions. Sourcing from smelters with hydropower/renewable energy and providing clear traceability assurance will become an advantage in the market.

� Digital product passports: emerging regulations will mandate verified ESG claims and properties of aluminium products, bringing together assured claims and data points (see the EU Digital Product Passport (DPP) under the EU Ecodesign for Sustainable Products Regulation).

Why DNV?

We are independent experts, specialising in assurance and risk management, driven by a purpose to safeguard life, property, and the environment. Our mission is to provide reliable insights and information to empower our customers and their stakeholders to make critical decisions confidently. Based on our extensive supply chain and ESG expertise, we are well positioned to help companies get ready for CSDDD, create Chain of Custody and assured PCF claims and increased supply chain due diligence expectations. For more information, please get in touch with our experts at sustainability.uk@dnv. com �

The Future Aluminium Forum took place between the 22nd – 23rd May in Istanbul, Turkey. The event saw key players and experts come together to discuss innovative technologies pushing the industry forward to a developed future.

“Future aluminium is all about sustainability”- Erol Metin, Advisor to the Board of Directors, Talsad

Commenting on the event, Nadine Bloxsome, Editor, Aluminium International Today said:

“I am pleased that we were finally able to host the Future Aluminium Forum in Istanbul, after having planned this before the COVID pandemic. In collaboration with the Turkish Aluminium Industrialists Association (TALSAD) and various stakeholders, the event showcased the latest advancements in digital manufacturing and Industry 4.0 technologies, promising to revolutionise production processes and elevate quality and sustainability standards within the industry.

“We are delighted to report that the Future Aluminium Forum was exceptionally well-received by all delegates and sponsors alike. Their enthusiastic participation

and positive feedback underscore the importance and relevance of the topics discussed at the event.

The Turkish Aluminium Industry “Turkey’s strategic geographic location and thriving aluminium industry provide the perfect backdrop for this regional event. With its steady growth and significant contributions to the global aluminium market, Turkey serves as a hub for both regional and global players, offering a dynamic environment ripe for exploration and collaboration.” – Nadine Bloxsome

The Erol Metin, Advisor to the Board of Directors, Talsad, kickstarted the event with his keynote presentation. Breaking down the Turkish aluminium market, he discussed its position in the global market. Turkey has:

� 1 smelter

� 18 Wrought aluminium producers

� 22 rollers, plate manufacturers

� 122 extruders

� 14 wire and cable manufacturers

� 28 packaging manufacturers

Commenting on the industry growth in turkey, he reported that turkey’s imports and exports of aluminium have doubled

over the last 10 years. Despite a 14% reduction in exports in 2023, Metin remained positive with regards to the Turkish aluminium’s future. He observed that the reduction was “mainly due to slow down in main export markets such as the EU and US.”

Moving onto decarbonising the Turkish aluminium industry, he said that “total CO2e emissions from Global Aluminium Industry must come down from 1.1 GT/ year to 250 Mt/year; i.e 80% reduction.” In face of this challenge, he came forward to present the audience with an industry roadmap designed for the Turkish industry. The roadmap focused on decarbonisation of electricity with renewables; shifting to electric furnaces; and carbon reductions in the supply chain. He also noted the importance of National Initiatives, and utilising these to the industries advantage.

“The total carbon footprint of Turkish aluminium industry is estimated to be in the range of 22-28 million tons per year.”

Erol Metin

Looking further into decarbonising the industry he homed in on the key issue, that “86% of total Carbon budget of Turkish aluminium is due to footprint of primary aluminium imports 18-19 Mt CO2 embedded (scope 3) emissions.”

Metin went onto state the importance of assessing each part of the production chain and finding personalised solution for decarbonising each aspect.

Metin concluded his overview saying, “Overall significant shifts yet to evolve in global demand and supply cycle. Türkiye’s position as global semi and finished products manufacturing industry need to maintain the balance between decarbonisation and global supply / demand flows.”

Future of Aluminium: Technology and Data

“The Future Aluminium Forum was conceived with a singular purpose: to explore the transformative potential of digital technologies in the aluminium industry.” – Nadine Bloxsome Technology, like living things, naturally goes through evolutionary processes. Without evolution technology’s purpose would soon be void in the name of industry. Industry 4.0 signifies the latest industrialisation, but it does not represent the possible futures that could be our reality.

Technologies and developments present the industry with exciting possibilities. Hope is often associated with these possibilities; yet, while beneficial, hope can be misleading. Ron Knapp, Adviser, China Hongqiao Group Limited (HK), addressed the industry stating, “sometimes we have to wait for the research to catch up with the technology.” This statement lingered throughout the forum; there is, somewhat, a unanimous understanding that the industry needs innovation, but at a practical industry scale.

Ron Knapp went onto provide insight into the China Hongqiao Group which has seen 100% production growth in the last 20 years. The company currently has a primary aluminium capacity of 6.46 Mt under China’s 45 Mt Cap. Once again, EU and US production decline was mentioned.

Emirates Global Aluminium (EGA), Chief Digital Officer, Carlo Khalil Nizam

heeded this statement and presented real life examples of AI application in the EGA plants. Providing recordings of digital transformation, digitalisation and digitisation, he defined each term while giving examples of “walk[ing] the talk.” Examples included outlining 10 digital capabilities, as well as implementing AI in the use of industrial cranes.

“The main objective of Industry 4.0, at EGA, is to lead the transformation [of EGA] into a smarter organisation. Using the elements of Industrial 4.0 such as, big data, artificial intelligence, internet of things, and many more.” - Abdulla Karmustaji, Product Owner Industry 4.0, Emirates Global Aluminium (EGA)

Industry 4.0 signifies the next steps of industrial revolution. Rather than it being the next natural step, it could be considered to be the next necessary step. Reviewing the global climate, perhaps the unexpected is the only thing we know for certain. Carlo K. Nizam also discussed EGA’s position and its vision for an advanced sustainable future, quoting Darwin for inspiration on the future: “It is not the strongest nor the most intelligent that survives, it is the ones that are the most adaptable to change.”

Adaptability to change is a natural requirement of evolution. So how can technology assist in ensuring we are as

flexible as we can be?

Amadou Ndiaye, Industry Executive Advisor for Energy and Natural Resources, SAP EMEA, contemplated “Forging a Sustainable Aluminium Business with Integrated Data and Next Generation Business Processes.” He presented optimisation strategies that can be put in place with the assistance data collection and business technology platforms. With the aid of platforms, one can combine and embed any technology under the umbrella of development, automation, integration, data & analytics, and AI. With this systematic organisation, technology and data can seamlessly work together to develop a better future.

Pernelle Nunez noted the IAI’s position towards data, emphasising its importance as a way to communicate with both the industry and stakeholders.

“We are on track, but we need to work together to ensure everyone is on the same track”. – Siri Sande

To assist one another by aligning the industry on the same path may be one of the ways that help push the industry forward when looking at both decarbonisation and the adoption of new technologies. Looking at technology, Sande explained that to make sure the industry is progressing, “we need to make sure the numbers are real numbers and not just estimates.” She called for a new era of sustainability that is supported by in-depth data. She provided examples of application enhancement with the assistance of data, as well as data collection methods.

it. Not only this but data is often spread to organise, understand, and use data to progress the

But is this a part of the problem? “We talk about pilot projects, but we are stuck at pilots. We need to scale these projects; this is why digital projects fail.” – Denis Gontcharov, Data Engineer. The issue that Gontcharov raises is that that we have this data, but we don’t know how to utilise it. Not only this but data is often spread everywhere. He presents a solution to organise, understand, and use data to progress the industry.

“Introduction of automation is difficult, but necessary” – Marcus Quantillion It seems that for the industry to develop and evolve technological advancement is necessary. For efficiency, economics, and production benefits, progression to industry 4.0 and beyond is almost a no brainer. But what about in the name of sustainability?

Greener Aluminium: Sustainability “Aluminium’s properties make it essential for a sustainable future” - Pernelle Nunez, secetary general, International Aluminium Institute.

It has long been known that the decarbonising is an immoveable part of the aluminium future. But the decarbonising roadmap also understand that innovation and new technologies are essential to bringing a decarbonised future into fruition. Amadou Ndiaye declared that the industry must “embed sustainability into its DNA.” But how?

Ron Knapp presented the decarbonisation roadmap of China Hongqiao Group: “We will strive to peak carbon emissions before 2025 and to achieve net-zero emissions in Scope 1 and 2 before 2055,” said Chairman Zhang Bo, China Hongqiao Group. Decarbonisation is on the global agenda. But this does not mean that the method to decarbonise is one size fits all. New energy is one such way for a company to decarbonise, Ron Knapp elaborated on the company’s new energy projects: Hongtai & Honghe Facilities. Thes projects aim at utilising

wind and solar energy, replacing coal. He also noted tat solar and wind electricity generation, in China, is cheaper than coalbased electricity. He demonstrated that the call for decarbonising the industry has been heard and is being acted upon.

Pernelle Nunez discussed the IAI global roadmap which aims to unify the industry and direct it toward a greener future. She also encouraged the industry saying that “sustainability issues are complex, evolving and interconnected,” but with the challenges, opportunities arise. But realism must also come into play here. There is surely a point where challenges present barriers that cannot be broken down?

“Costs are also an important factor” –Marcus Oberhofer, HAI

A reality check when it comes to implementing new technology has already been mentioned, but this is also the case for sustainability goals. Understanding the limits when it comes to adopting technology and making changes is important when it comes to making sustainable aspirations a reality. Oberhofer Noted the importance of creating realistic goals within realistic guidelines by discussing HAI’s opposition to recycled content requirements. In certain circumstances, creating limits can restrict development, but also divert attention from the real issue at hand. Oberhofer analysed that the industry is having the “wrong discussion” when it comes to recycled content requirements. Rather than assist the scrap market, he

claims this will result in further issues. He also called for the industry to be careful of greenwashing, which could also hinder the progress of the industry.

“Biggest global threat of today is global warming” - Asís Quecedo, Sales Engineer, GHI Smart Furnaces

So there is a balance that needs to be found for the industry to successfully decarbonise. It seems apparent that technology and data will have a profound influence on the development of the industry, referring to both economic and sustainable goals. But it is down to the industry to utilise the technology too our advantage.

Conclusion

With the warm Turkish sun heating the evening and the light catching the blue sea, the aluminium industry was given a beautiful setting to network by TALSAD. Hopefully the tranquil view reflected the future of the industry. But perhaps more realistically, the sea represented the unpredictable nature of the industry as rain and a grey sea was reported the following week.

“Moving forward, the Aluminium International Today team is committed to sharing the key discussion topics and relevant announcements with our readers across future issues. We look forward to continuing the dialogue and driving further innovation and progress within the aluminium industry.” - Nadine Bloxsome, Editor, Aluminium International Today �

✓SINGLE CHAMBER / MULTI CHAMBER FURNACES

✓SCRAP DECOATING SYSTEMS

✓TILTING ROTARY MELTING FURNACES

✓SCRAP CHARGING MACHINES

✓LAUNDER SYSTEMS

✓CASTING / HOLDING FURNACES

✓HOMOGENIZING OVENS

✓COOLERS

✓SOW PRE-HEATERS

✓REPAIR & ALTERATIONS

The unified namespace for digital transformation in the al Industry

This article presents the author’s learnings from five years of performing digital transformation in the aluminium industry. The focus lies on highlighting the common pitfalls encountered. Subsequently, the concept of the unified namespace is introduced as a solution to common data-problems in aluminium manufacturing. Finally, a concrete approach of how to build a unified namespace at your plant is presented. The goal is to have a running system that solves a common manufacturing use case within three months. By

Denis Gontcharov*

Why becoming digital matters

The aluminium industry is conservative and therefore slow to adopt modern digital technologies. Nevertheless, by now there’s a consensus that the industry has to digitally transform in order to stay competitive in the future. Various challenges such as artificial intelligence, automation and sustainability and decarbonisation demand a more rigorous use of the vast quantities of available data. However, processing vast quantities of data is easier said than done.

“Saying aluminium manufacturers have an abundance of data is like saying the earth’s crust has an abundance of aluminium.”

Most data projects fail

Many manufacturing companies have already started their digital transformation journey. The focus was often on implementing various industrial use cases, for example preventive maintenance or image analysis. Unfortunately, the results of many of these use cases were unsatisfactory. In fact, according to a 2021 study by the McKinsey consulting company, 69 percent of digital transformation projects fail. According to the author’s experience, the two most

common reasons are exceeding the project’s budget and being stuck in “pilot purgatory”.

Projects exceeding the budget

Most digital projects that go over budget do so because the time to complete the project turns out to be much longer than initially planned. Nearly always, the reason is that the part of “getting the data” takes much longer than expected. Data is often assumed to “just be there” and little regard is given to the often messy state in which this data is stored.

Projects stuck in pilot purgatory

The second way in which a technically successful digital use case fails to deliver on its promises is by not being scalable. Often, there’s a wish to roll out successful solutions of one plant across the other plants. Assuming the new solution is merely a copy, this challenge appears trivial.

However, the data infrastructure always differs slightly between two plants. This means that each roll out requires some modifications to the way data is fed. In practice, these modifications most of the time turn out to be substantial. In that case, the roll is often abandoned.

The two underlying data problems Why do unsuccessful projects fail because they go over budget, and successful projects are stuck in pilot purgatory? The devil is always in the details: there are two main problems plaguing your data.

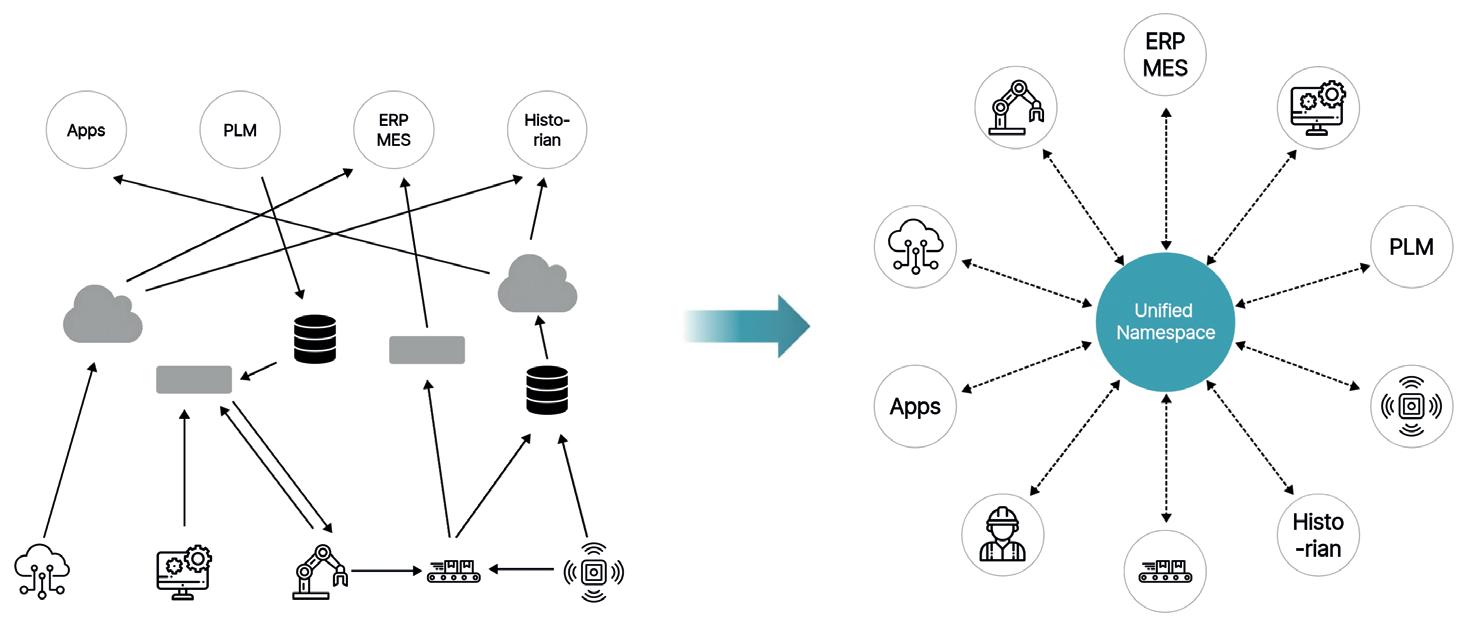

First, the various required data sources are never found in one place. After all, a manufacturing plant consists of many individual software systems that only communicate with each other through laboriously constructed point-to-point connections. Combining disparate data sources into one collection suitable for data analysis therefore requires a connection to each individual source system.

Second, technically having all data in one place does not yet solve the challenge of finding this data, if the data was already hard to find in the source system.

The company you work for may have a data lake or data warehouse that contains data from various source systems. But how do you navigate this large data repository to find a particular variable? More often than not, the data model (i.e. the structure under which the data is saved) is an exact copy of the data model in the original source system. This requires the person looking for the variable to have an intimate knowledge of the original

*Denis is a data consultant who helps aluminium manufacturers break down data silos.

Image source: United Manufacturing Hub, Unified Namespace, https://www.umh.app/

source system’s data model, which is unlikely if the person has no experience working with this system in the first place. In consequence, the data lake or data warehouse are difficult to work with: people are simply getting lost in there.

The Unified Namespace

The unified namespace is a software architecture that addresses the two data problems raised in the previous chapter. Before delving into how the unified namespace solves both problems, the concept is illustrated on a high level in Fig 1

The philosophy of the unified namespace entails collecting all data of the entire company in one place, and making it available to anyone who needs it in an easy-to-understand way. In technical terms, this means building a single source of truth where data is organised in a semantic hierarchy. Both concepts are further detailed below.

A central idea in the philosophy of the unified namespace is the separation of process control and data analytics. The former is already handled by the various layers of the so-called “automation pyramid”. The unified namespace strives to be a parallel system to support the latter. This separation is important because it allows a plant to implement a unified namespace without risking interrupting production. In addition, the original control systems of the automation pyramid don’t need to be upgraded.

Single Source of Truth

By connecting all data sources of the enterprise with the unified namespace, it becomes the single source of truth for all real-time information of the business. This way, any use case (e.g. a new software application) that requires data will only have to implement one connection: from the application to the unified namespace. In the case that the application produces new data on its own (by processing data coming from the unified namespace), the application will write this data back

to the unified namespace. This way, the unified namespace can supply this data to any future application requiring such data. This approach guarantees that each new application requires only one new additional connection (to the unified namespace).

Semantic Hierarchy

Up to this point, the unified namespace may not look much different from the data lake and data warehouse mentioned earlier: both strive to be the single source of truth. The crucial difference lies in the way data is stored in the unified namespace, i.e. the data model. Where the latter solutions simply replicate the original data model of the source system, the unified namespace organises its data in a semantic hierarchy.

Simply put, this means that all data in the unified namespace is organised according to a hierarchy of subsequent levels that reflect the actual structure of the enterprise. This hierarchy is not arbitrary, but instead derived from the ISA-95 Part 2 specification, acting as a standard across the globe. Any data analyst with a basic understanding of manufacturing will be able to find a variable by navigating down the hierarchy.

The following example illustrates how a particular value belonging to a certain machine can be found within the semantic hierarchy:

Imagine a fictive primary aluminium smelting enterprise “Aluminium Smelting Co” with a smelter located in Iceland. An engineer is interested in the “pot voltage” of pot number 124 on potline 1 of the electrolysis area of the plant. The pot voltage will be found under:

• Aluminium Smelting Co

• Iceland smelter

� Electrolysis area

� potline 1

� pot number 124

� pot voltage

The “raw data” tag contains all the raw process values coming from the machine, in this case electrolysis pot 124.

Getting Started with a Unified Namespace

Let’s say you want to try out the unified namespace at your plant. How do you get started? The approach suggested below is straightforward to implement. It does not require any financial budget if completed fully in-house, and can be completed within three months with one dedicated engineer and support from the in-house IT department.

A common use case in manufacturing is the calculation of the Overall Equipment Effectiveness (OEE) of a given machine, e.g. a rolling mill. Calculating the OEE requires data from only two source systems: the process data coming from the machine (most often found in the process historian) and the Manufacturing Execution System (MES). The project consists of 1) deploying a unified namespace 2) connecting the machine and the MES to the unified namespace and 3) calculating the OEE.

Instead of building a unified namespace from scratch, it’s recommended to deploy the open-source solution provided by the [United Manufacturing Hub](https://www.umh.app/product). Their product is free to use for commercial purposes and already implements the OEE calculation for a given machine. This way, a use case demonstrating the merits of a unified namespace can be developed in minimal time and risk

Conclusion

This article highlighted that most digital transformation use cases fail because of two data problems: the data not being in one place, and data being hard to find. The unified namespace offers a solution to both problems via its single source of truth and semantic hierarchy, respectively. It’s important to note that the unified namespace does not require changing the existing systems at the plant. Rather, the automation pyramid is extended by the unified namespace, who becomes the single interface for all data in the enterprise. This greatly facilitates data analytics without jeopardising process control. The presented use case to calculate the OEE of one given machine presents a quick-win to implement a unified namespace and convince the plant’s leadership of the merits of this approach.

If you would like to know more about the unified namespace, have a look at the [website of Denis Gontcharov](https:// gontcharov.eu).

�

Title

An Insightful Keynote

Following an insightful Keynote presentation at the recent Future Aluminium Forum (FAF), Nadine Bloxsome* spoke with Ron Knapp** from China Hongqiao Group, a leading global aluminium producer based in China, to find out more about the company’s long-term goals and how this aligns with a focus on sustainability.

The environmental and commercial challenges for aluminium producers are growing as the consumer – and the global community – expect higher standards of responsibility throughout the production cycle.

Some aluminium producers have had the benefit of being in countries/regions with access to low-carbon sources of electricity, providing a strong foundation for a low carbon emissions production profile. Other producers have been developing in countries/regions where

1.

the electricity and energy supply has been dominated by fossil fuel sources, resulting in a carbon emissions footprint as much as four to five times higher. An obvious example is that of China, where historically coal has been the backbone of the energy supply for industry – India and Australia have similar coal-energy legacies to address in the modern era of cutting carbon emissions as a key element in the fight to address climate change.

In the case of China, now the leading producer in the aluminium industry,

the focus often points to the energy component and the sheer size of the industry with more than 50% of global primary aluminium production. But there’s more to the China aluminium story than just energy. At the recent Future Aluminium Forum 2024 in Istanbul, Turkey, I caught up with Ron Knapp from China Hongqiao Group and asked him about the approach being taken by the company in addressing the challenges facing a major Chinese aluminium producer.

Nadine Bloxsome (NB): Ron, welcome to Istanbul and the 2024 edition of the Future Aluminium Forum! The China Hongqiao Group is one of the largest aluminium producers, not just in China but globally with over six million tonnes of annual production of primary aluminium and 19 million tonnes of alumina. Your FAF presentation showed a commitment to achieving both peak carbon and net zero carbon goals – how will China Hongqiao meet these goals . . . is this achievable by an aluminium producer based in a country traditionally sourcing its energy for aluminium production from coal-fired electricity?

Ron Knapp (RK): Good question, Nadine! From our size and our main production base in Shandong Province, there should be no surprise that we have the biggest carbon footprint in the whole global aluminium industry, but not the most carbon intensive – and let me comeback to that in a minute.

China Hongqiao has several advantages to help us to offset our obvious disadvantages – these advantages will enable us to address the first steps in our carbon abatement challenge and set us on the pathway to the attacking the harder parts of the task. We can’t achieve it all with the wave of a magic wand – it will take time and it will require more research success to give more solutions and

opportunities in fixing the future steps… the Future Aluminium Forum in action!

Looking at our China Hongqiao advantages, the first simple advantage but a key to delivering outcomes is a combination of our ownership, management and workforce. We are spin-off from Shandong Weiqiao Pioneering Group following Weiqiao’s entry into the aluminium industry in 2001; China Hongqiao is listed on the HKEX (Stock Code #1378). People use Weiqiao or Hongqiao in conversation, given our heritage and because Weiqiao is the majority shareholder of China Hongqiao with over 60% shareholding.

Our ownership, with Weiqiao holding a majority of the shares provides a strong

leadership and management structure for the company; Chairman and CEO Zhang Bo is also the chairman of Weiqiao. The workforce is highly committed to delivering positive results for the company and the local communities where the majority of our workforce reside. Zouping/ Binzhou (Shandong Province) takes on an aluminium family characteristic, with a large number of big and small enterprises associated with the aluminium cluster business model that has been a central feature of the Hongqiao organisation from the very beginning. More than 150 enterprises are involved in the cluster, including suppliers and customers as well as a wide range of service providers.

*Editor, Aluminium International Today **China Hongqiao Group, a leading global aluminium producer based in China.

Ron Knapp

2.

NB: You talk about aluminium industry clusters – what is the role or purpose of the clusters?

RK: Here is one of the simplest of concepts and one of the highly valuable parts of the China Hongqiao business model. The most obvious element or contribution comes from the high percentage of aluminium metal delivery to our customers as hot molten metal. Both the producer and consumer receive an advantage. Over 90% of all our aluminium metal is delivered as hot molten metal, reduced cast-house requirement on our side and reduced energy requirements for the customer to remelt their aluminium metal supply. Multiply the per tonne saving by, say, five million tonnes for example – and there is a great saving in energy and another small contribution to lowering carbon emissions.

3.

NB: The Weiqiao carbon reduction roadmap covers a full swathe of actions to be applied to the China Hongqiao operations – how do you see these actions evolving and in what order will they be introduced?

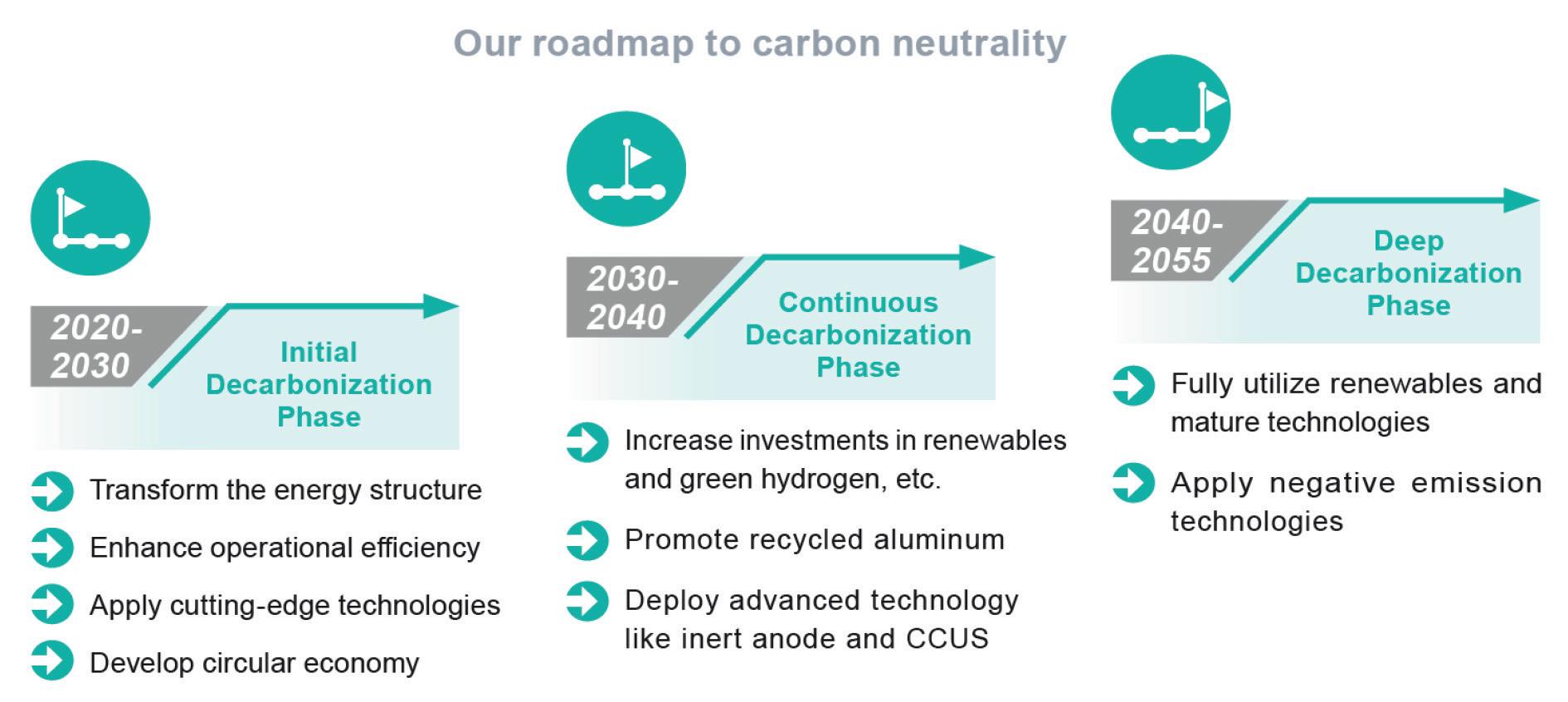

RK: Our Chairman, Zhang Bo, has publicly committed to meeting our responsibilities under China’s dual carbon goals and we will strive to peak carbon emissions before 2025 and to achieve net-zero emissions in Scope 1 and 2 before 2055.

environmental game-changer, from coal to clean energy. The Yunnan Hongtai & Yunnan Honghe projects are in line with government objectives to optimize the aluminium industry through supply side management, and to promote green

This is a very serious commitment and obligation for our company… we have this very big (total) and heavy (intensity) carbon emissions challenge to deal with across our operations, from upstream through midstream to downstream. Our program of carbon reduction across our production activities and new aluminium alloys and products will also help the carbon balance of others because we see these actions will be helping consumers face lower Scope 3 emissions. It’s about increased aluminium use and new applications, combined with lower carbon emissions in the aluminium we produce.

Looking at the Weiqiao Carbon reduction roadmap, you will see one of our first priorities is the task of changing the energy structure of our business, particularly the fuel source for the huge electricity consumption required to produce our six million tonnes of primary aluminium metal.

The most dramatic shift in the Hongqiao story is the project currently underway of relocating 60% of our primary aluminium capacity from Shandong to Yunnan Province – this is an energy and

development.

2023 brought a new achievement with production from our Yunnan Hongtai complex achieving one million tonnes. That’s a great boost in moving our energy transition towards our long-term goals.

But we know these are first steps in our journey. By 2026, we will have four million tonnes of capacity located in Yunnan. To complement these moves, Weiqiao has a renewable energy work program for the development of 13 GW of wind and solar PV across Yunnan Province and Shandong Province. We’re not standing still and waiting to see how things happen – our Chairman Zhang Bo is driving forward to ensure success.

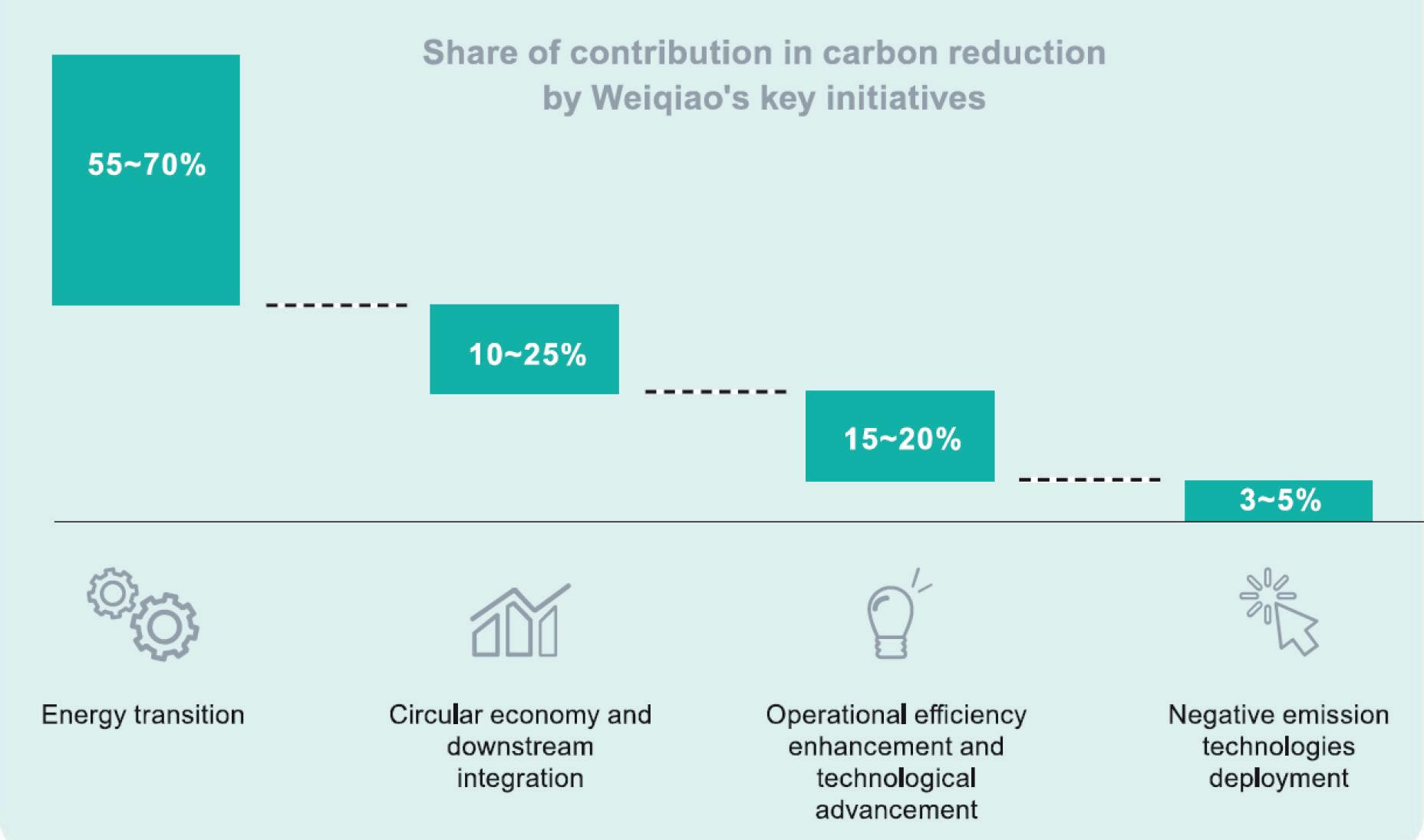

Several of the elements of our net carbon emissions are being progressed concurrently. While it is easy to see why energy is often spotlighted on centre stage, given the size of its contribution to our carbon footprint, we are very active in enhancing operational efficiency and technological advancements. Our lightweighting centre is a major growth segment in the company – and the circular economy is very much in focus with our new recycling facility with capacity to disassemble 100,000 vehicles per annum as the opportunities for such activities grow with the NEVs and higher volume of aluminium scrap available from the vehicle fleet reflecting increased aluminium content.

NB: Where are the yellow warning flags – or even red flags – that need more work before solutions can be found and introduced?

RK: The aluminium industry must keep working on more solutions; we do not have all the answers yet. I immediately think of the carbon anode in the electrolysis segment of the operations –it’s not the “big ticket” item for the whole global aluminium GHG emissions budget, that honour remains with energy but for

processes in our smelter pot rooms and throughout the production process. This provides us with first class energy efficiency, with the latest 600kA potlines down at sub-12,400 kWh per tonne of aluminium. With this comes a huge energy saving…for example, the average energy efficiency for the North America

some producers who already have low- or zero-carbon energy available, the anode has more GHG emissions prominence in their total GHG emissions. As we pull down the energy emissions number which currently accounts for some 75% of the total aluminium cradle-to-gate GHG emissions identified by the IAI, the 13-14% share attributed to the anode production/consumption segment will increase in significance in the race to net zero. The answer is a new technology breakthrough that can be commercialised, or an additional burden will be placed on negative emission technologies, such as CCUS.

While the research continues into the alternatives, we are continuing to introduce the most technically advanced

and European regions is around 14,000 kWh – that gives us a 1,500 kWh per tonne advantage and a saving to be able to continue R & D investment and further upgrading of production units.

Our smelter fleet is less than 10 years old – and with daily output of around 4.5 tonne of aluminium metal per pot from our 600 kA smelter potlines, this brings further operational efficiencies.

These factors help us to have a per tonne carbon emission lower than the average for aluminium production where coal-fired electricity is the energy input.

Often, aluminium is characterised as one of the sectors that is hard-to-abate, due to the production process involving carbon and the energy input required.

5.

NB: What’s next for the Group?

RK: Next is already with us and is being developed and rolled-out …it’s the aluminium lightweighting developments and NEVs, - the next evolution of the Weiqiao Pioneering Group. First it was textiles and the start of the journey, then in 2001 the birth of the aluminium leg of the family.

Twenty years later and with very different commercial and environmental opportunities, a new industrial evolution is emerging and quickly taking shape, drawing several key strands or elements together into a new pillar of activity of the Weiqiao Group.

Recognising the pull of a changing market, Weiqiao has been building an aluminium lightweighting centre, combining vehicle component production and new growth areas created by intense research and development activities. The new pillar, or third leg, of activities also includes recycling facilities to strengthen our march into the circular economy –the Sino-German Hongshun Technology Industrial Park including the China Hongqiao-Scholz JV vehicle dismantling and recycling aluminium production technology facility is all part of the development now underway.

The next step was the acquiring of a majority shareholding by Weiqiao in the vehicle production plant known as BAW or Beijing Auto Works.

With these different elements, we now have the start of the next cluster of industries being combined to build efficiency through co-location of different activities and economies of scale enabling a wider net production across the industry.

In May 2024, Weiqiao-Hongqiao Chairman Zhang Bo joined with his peers in celebrating the delivery of the first batch of REACH NEV aluminium vans, part of the commercial vehicle plan which will include heavy trucks, commercial vans and passenger buses.

NB: Ron, look into the crystal ball and tell what you see for aluminium and China Hongqiao

RK: An easy one to finish with! A very positive future for global aluminium, with ongoing growth in supply coming from primary and recycled sources – and demand coming from traditional and new innovative applications. China Hongqiao will accelerate sustainability and efficiency outcomes, with the commitment of ownership, management and workforce. We will continue to strive to be the best – and always continue to improve our environmental performance, hand-in-hand with our commitment to the delivery of globally competitive aluminium metal and products. Efficiency, industrial clusters and innovation remain critical elements for the delivery of our vision for the future – and this is reflected in Chairman Zhang Bo’s approach in building a platform for the integration of science, education, innovation, and production - and to promote industry-education integration and industrial innovation to accelerate high-quality development…linking technological and commercial worlds for better outcomes.

The Weiqiao lightweight strategy runs through the entire vehicle development process – and supported by vehicle development standards system, automotive grade aluminium alloy technology development standards and technology patents.

Weiqiao New Energy Vehicles will become a key element in our drive towards sustainability. Primary and recycled aluminium will be partners in these developments.

A modern 600kA smelting pot room part of the China Hongqiao aluminium cluster in Binzhou, Shandong Province

DUOMELT INDUCTION FURNACE

STRIP FLOTATION FURNACE

Aluminium Industry In Egypt

By Richard McDonough*

The Arab Republic of Egypt (Egypt) has one of the 35 largest economies in the world. The country has the largest economy in North Africa and is the most populous nation in this region. According to the World Bank, the Gross Domestic Product (GDP) of Egypt was estimated to be approximately (US) $476,747,720,000 in 2022.

In a report issued by the International Monetary Fund (IMF) in April of 2024, the Real GDP of Egypt is projected to grow 3% in 2024.

According to that same report, the IMF projected Consumer Prices in Egypt will increase 32.5% in 2024.

The country has one of the 15 largest populations among all nations. According to the World Bank, the most recent population stats indicated that there were 110,990,103 people living in Egypt in 2022. This population level ranks Egypt as the third largest in Africa; both Nigeria and Ethiopia have larger populations. In terms of geography, Egypt is one of the 30 largest countries globally. Egypt includes land in both Africa and Asia

totalling approximately 1,001,450 km2 of territory.

Trade

Egypt was the 47th largest importer of aluminium and related products worldwide in 2023. The nation’s ranking placed it between Finland and South Africa. In 2019, Egypt was ranked as the 40th largest importer of these products globally, with the country being ranked between Portugal and Israel. The country was ranked number 41 in 2020, number 43 in 2021, and number 44 in 2022.

The amount of aluminium and related products imported into Egypt in 2023 represented less than 1% of all global imports of these products.

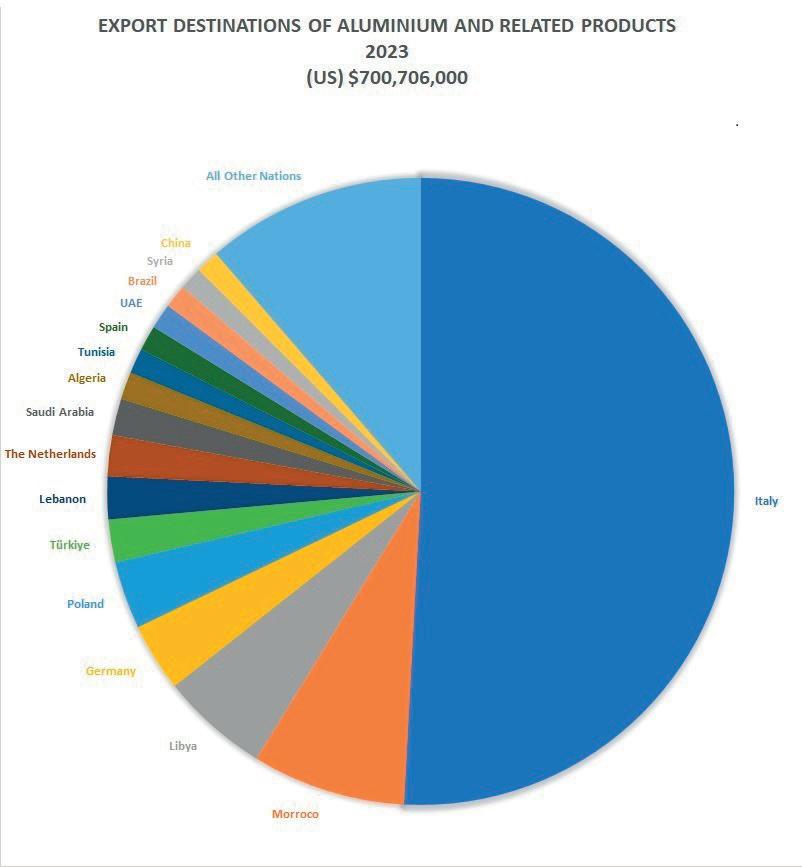

In 2023, Egypt was ranked as the 50th largest country globally in exports of aluminium and articles thereof. This ranking placed Egypt between Croatia and Bulgaria in that year. It was ranked at number 49 in 2019; Egypt was ranked between Croatia and Indonesia in that year. The country was ranked number 47 in 2020 and in 2021; number 55 in 2022.

The amount of aluminium and related products exported from Egypt in 2023 represented less than 1% of all global imports of these products.

This information is according to the International Trade Centre (ITC). Unless otherwise stated, statistics detailing imports and exports of aluminium and articles thereof (hereafter noted as “aluminium and related products”) to and from Egypt are approximate and are from the most recent reports issued by the ITC. This information also includes the statistics detailing individual segments of the aluminium industry.

Please note that the rankings among nations listed in this news column combine the statistics for China and Hong Kong.

Imports

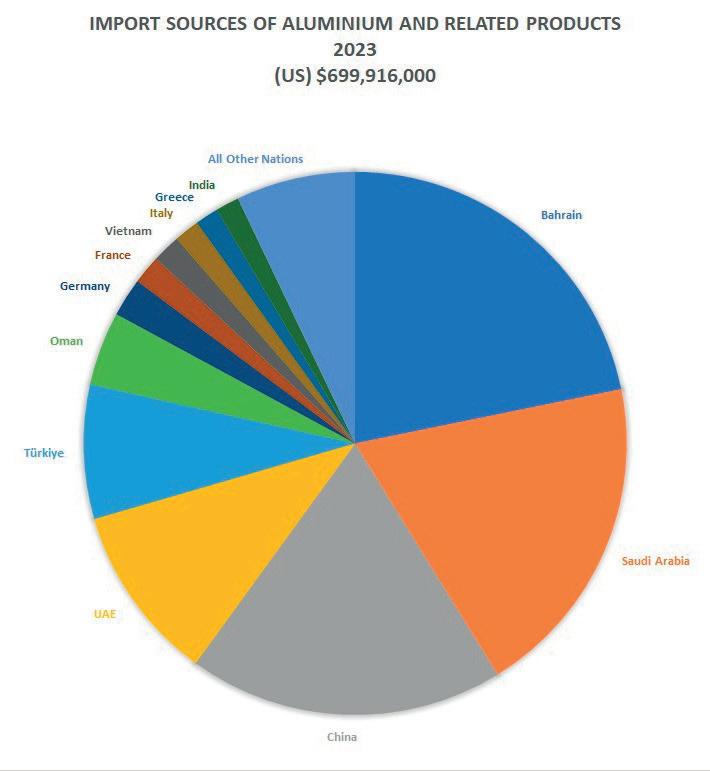

Fig 1

The value of the imports of aluminium and related products into Egypt in 2023 was similar to the value of these products imported in 2019, increasing less than 0.1% from 2019 to 2023. The amounts increased in both 2021 and in 2022, but

(The photograph was provided courtesy of United States Department of State.)

decreased in 2023. The decrease from 2022 to 2023 was 23.9%.

In 2019, imports of these products amounted to (US) $693,784,000; in 2020, (US) $672,813,000; in 2021, (US) $808,221,000; in 2022, (US) $919,216,000; and in 2023, imports of aluminium and related products were valued at (US) $699,916,000.

Major sources of aluminium and related products imported into Egypt included countries in Asia and Europe. Five of the top six sources of these products were nations in the Middle East.

With one year as an exception, Bahrain, Saudi Arabia, and China were the three largest sources of aluminium and related products imported into Egypt in each year from 2019 to 2023. The one exception was in 2020. In that year, Türkiye was a larger source of imported aluminium and related products than Saudi Arabia.

Imports of aluminium and related products into Egypt from Bahrain increased from (US) $132,764,000 in 2019 to (US) $152,499,000 in 2023; from Saudi Arabia, imports increased from (US) $106,625,000 in 2019 to (US) $135,799,000 in 2023; and from China, imports increased from (US) $117,635,000 in 2019 to (US) $131,754,000 in 2023.

The actual increases in the importation of these products into Egypt also resulted